Embed Size (px)

Citation preview

TVK a

nnual

reporT

20

09

annual report 2009economic, social and environmental performance

20

09

20

09

member of the mol group

content

TVK at a Glance 4 TVK at a Glance 7 Key financial and operating data 8 letter from the Chairman 10 overview of the environment

our Businesses 14 Major Strategic Goals 18 Consolidated Companies 20 our production 26 our Sales

Financial and operational performance 30 Management Discussion and analysis on the results 42 Independent auditor’s report 47 Consolidated Financial Statements 48 Supplement to the consolidated financial statement 106 Key Corporate Data

Sustainability report 112 Main results and goals 118 protecting the environment 122 Human Focus 129 our Quality Management 130 our Social Commitment 132 performance indicators

Corporate governance 138 Corporate Governance 146 Structure of organization of T VK plc. 147 Board of Directors 150 Top Management 152 Supervisory Board 154 report by the Supervisory Board 155 Corporate Information

158 Glossary of Terms 161 Shareholder Information 162 Statement of responsibility 163 questionnaire

TVK annual report 20092

Enhancing our competitive power, we can increasingly lean on the MOL Group integration synergies: the secured feedstock supply, the robust financial background and strong position in the regional markets, together with the competitive products from the optimized production capacities. We pay particular attention to the continuous improvement of our product quality and customer portfolio, which - along with the cost cutting actions - can guarantee the efficient operation for the forthcoming years.

In our sales and marketing activity we intend to strengthen our position in Central-Eastern Europe that is core region for MOL as well. Along the rapid growth potential anticipated in regional polyolefin demand, the attractiveness of proximate markets can be derived from the outstanding knowledge of specific economic and infrastructural characteristics in the region, from logistic advantages and the potential to build strategic customer relationships. Beyond the production of high quality products, our most relevant competitive advantages are sales and marketing services, customer care and support as well as production facilities that provide permanent supply.We lay particular emphasis on better understanding of customer requirements and building stable business relations in order to improve a sustainable business model and to mitigate commercial risks in addition.

The performance of well prepared and committed professional staff can guarantee the sustainability of business development. We continue development in the fields of environmental protection, social responsibility and attitude of business ethics, which can provide firm basis to our business operation. We take an active part in chemical industry associations and in professional preparatory works of regulations in the European Union.

Mission

Our company offers petrochemical products of excellent quality and high level services to its customers. Our products are fundamental for a wide range of industrial applications and for production of a vast number of consumer goods that are essential to everyday life and provide more comfort and plenitude in people life. Continuous improvement and quality management in the widest sense are the essential parts of our business philosophy.

In Hungary TVK plays important role in health promotion, talent management and education development. Our aim is to build long term relationship with organizations achieving outstanding result in culture development.As member of the MOL Group, we conduce to enhance competitiveness and profitability in the refining sector and as well we can mutually mitigate each other risk profile.

Core values

In the course of completing our mission we coherently apply our core values:• We committed to responsibly stand up for health,

safety and our natural environment protection.• Our operation is competitive and value creating.

Our business moves are based on mutually beneficial, long term and fair business relations, where we consistently keep our ethical norms.

• Quality consciousness, endeavor to operational excellence and the innovative approach are immersing our day-to-day operation. Accordingly our highly qualified, creative and motivated employees can participate in shaping the future of our company. This active contribution comes from open and cooperative atmosphere and corporate culture that respects for personal, local and national characteristics.

Our corporate vision, which also reflects the outlines of our core values, takes shape in an awareness of our business environment, resources and capabilities.

Vision

We are to retain our leadership in the regional petrochemical industry by continuously developing our operating efficiency and the competitiveness of our assets. As the leading regional polyolefin producer, we are committed to pursue our activities according to the business philosophies of continuous development and operational excellence. Optimized in line with customer requirements, our high quality portfolio of products provide a firm basis for exploiting the opportunities arising from the surge of demand for polyolefins in Central Europe, which we couple with building on the advantages, emanating from strategic partnerships based on mutual benefits. Our corporate social responsibility guarantees that we are creating value for all stakeholders of our operation.

our core lines of business

We supply mainly European plastic converter companies with polyolefin products. Beyond our main profile, we sell olefins and other petrochemical co-products to regional chemical and oil companies, so to MOL as well. Our core activity includes two major production lines:

• Olefin production: the production and wholesale distribution of ethylene, propylene and other co-products from olefin production. Our petrochemical feedstock is supplied by MOL Refining and we sell olefin co-products to MOL refineries to the amounts of approximately one third of feedstock.

• Polyolefin production: includes the production and wholesale distribution of low and high density polyethylenes (LDPE, unimodal and bimodal HDPE) and polypropylenes (PP copolymer and homogeneous polymer).

We supply our partners with polyolefin products via proprietary sales network. TVK operates 100% owned sales subsidiaries in five countries – Germany, Poland, Italy, France and Ukraine. Above all our sales activity is also conducted through MOL subsidiaries in Austria and Romania. Sales as well as customer support in technical issues to the key accounts and on other markets are managed from TVK and SPC. We supply feedstock especially to European small and medium sized plastic converters, although our sales are active in more than 50 countries of the World.

our major goals – competitiveness, efficiency, profitability

Our prime objective is the retention of our petrochemical leadership in the Central European polyolefin markets where we see demand growth perspectives are to exceed the European average.

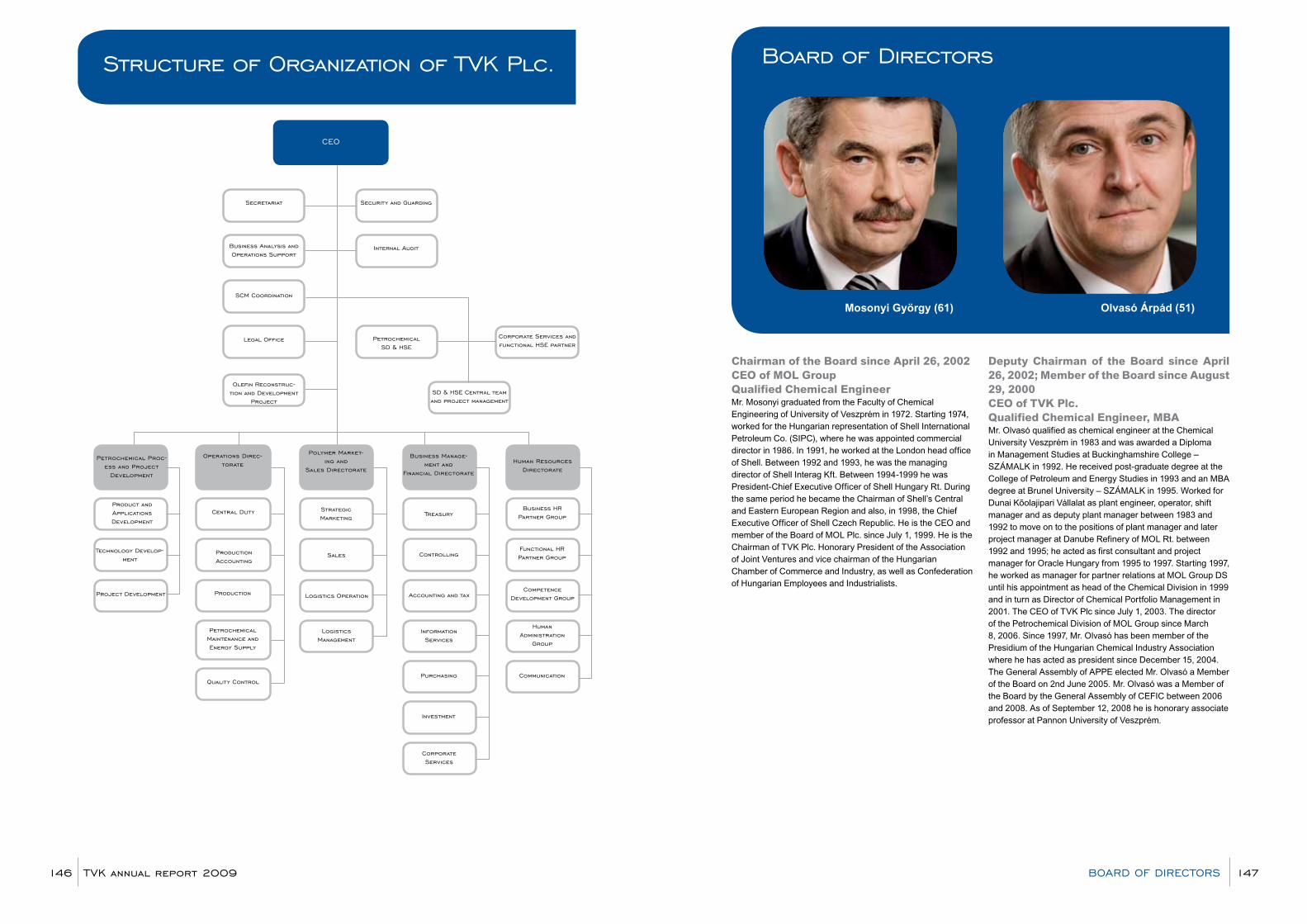

TVK at a Glance

Tisza Chemical Group Public Limited Company (hereinafter TVK Plc. or TVK), located in Tiszaújváros - is the largest chemical company in Hungary and by sales revenue it is the 18th largest Hungarian enterprise.

Along with Slovnaft Petrochemicals, s.r.o. (hereinafter SPC) - fully owned by Slovnaft, a.s. in Bratislava - TVK is composing the Petrochemical Division in the MOL Group, which holds leading position in petrochemical sector in the Central-Eastern Europe and one of the ten largest polyolefin producers in Europe. TVK and its Slovakian partner, SPC are operated in integrated manner, benefiting from joint optimization of production and integrated polyolefin sales. TVK has more than four decade experience in producing commodity polyolefins in competitive quality for the plastics processing industry, which products are fundamental for a wide range of industrial application and for the production of a huge number of consumer goods that are essential to our everyday lives.

TVK shares are listed and traded on the Budapest Stock Exchange and on the International Order Book of the London Stock Exchange.

TVK annual report 20094 5TVK aT a GlanCe

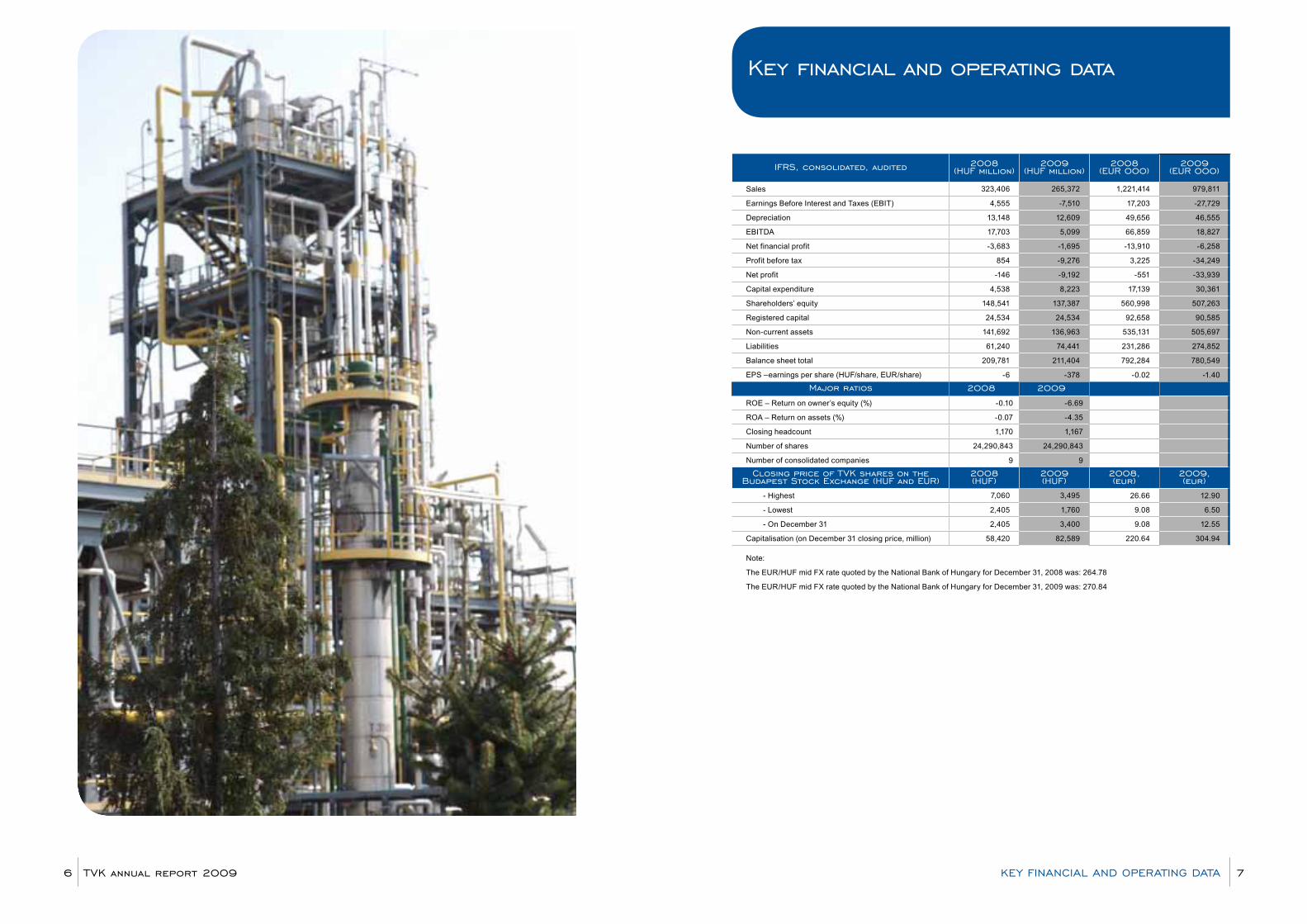

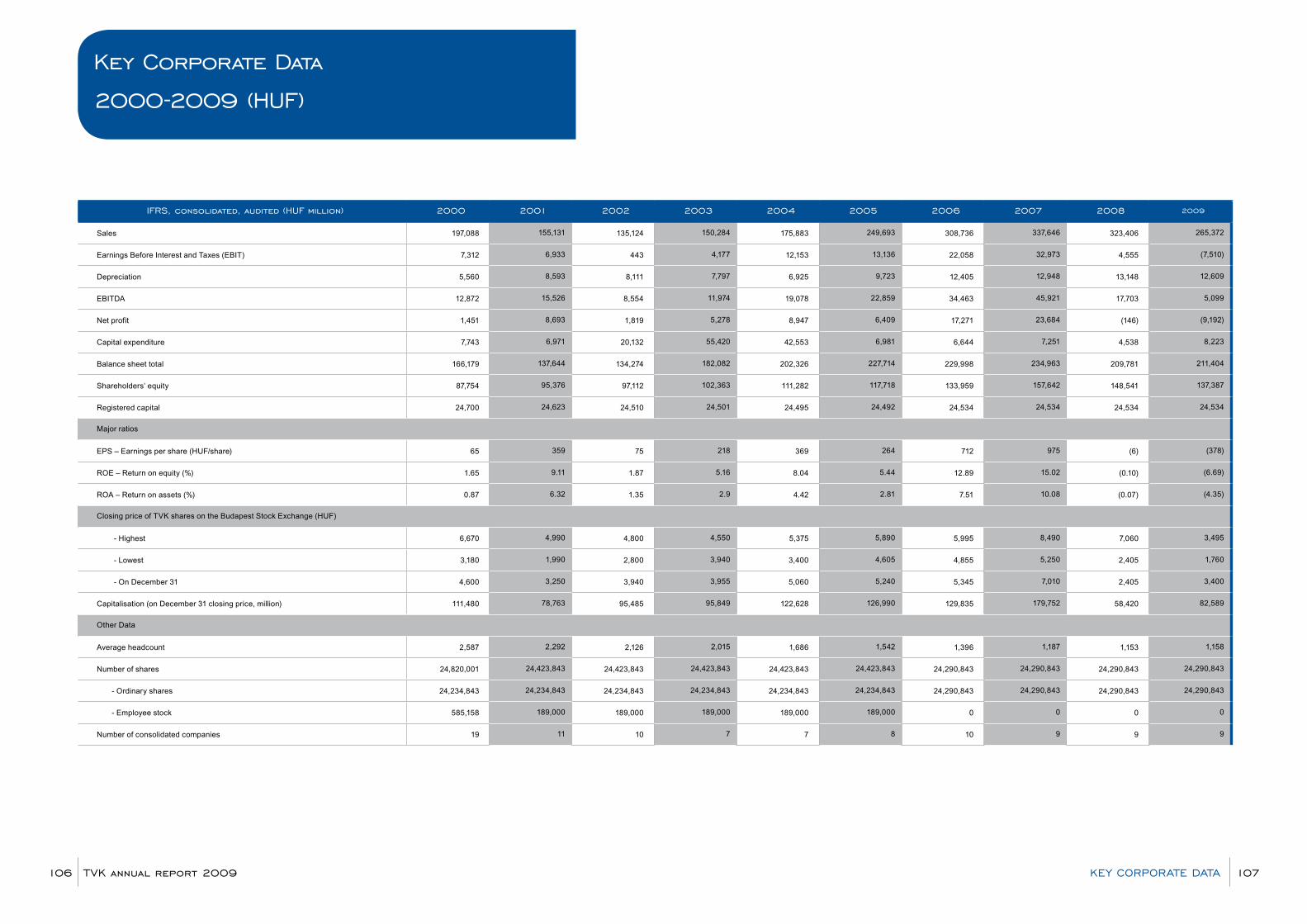

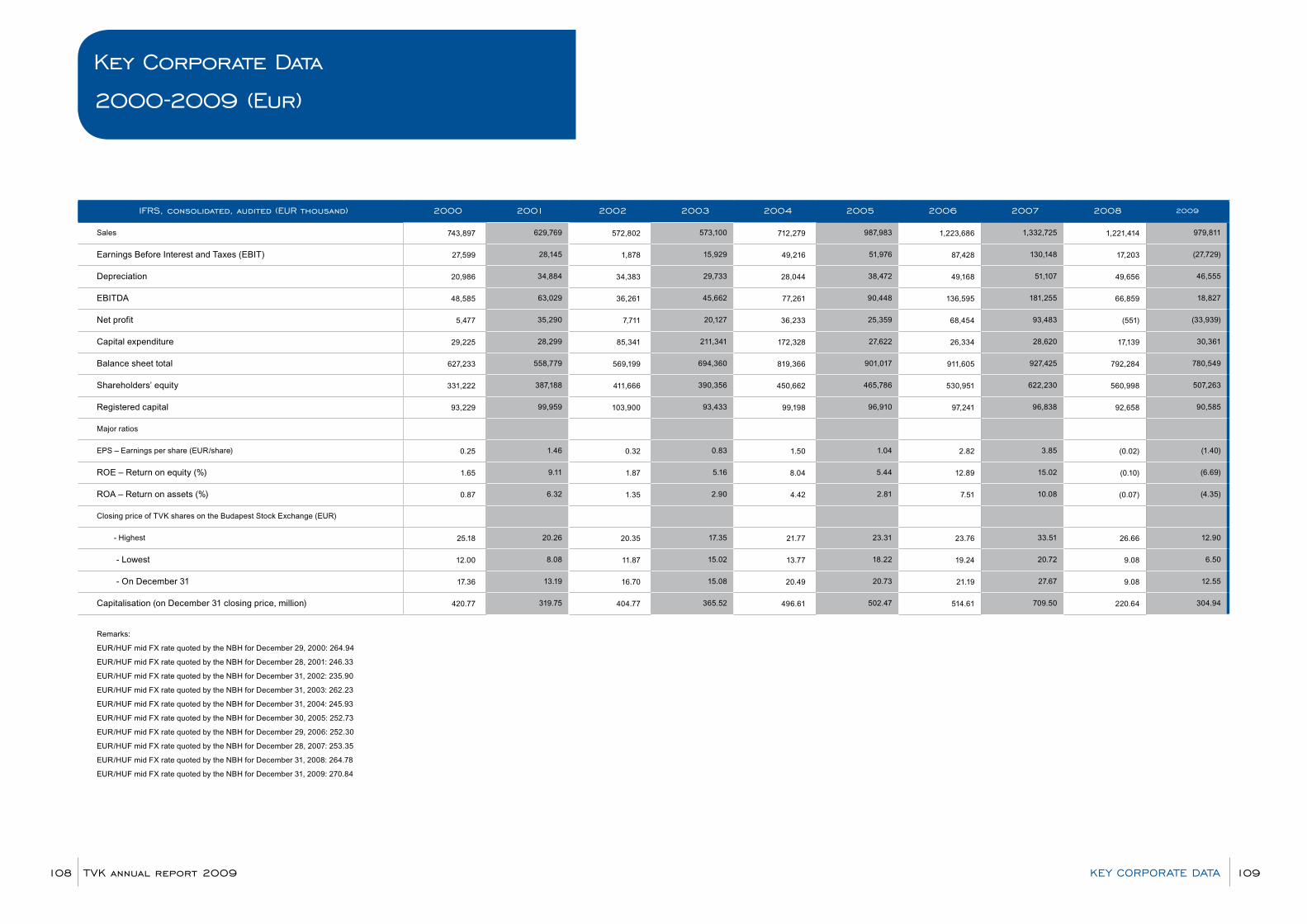

Key financial and operating data

IFrS, consolidated, audited 2008 (HuF million)

2009 (HuF million)

2008 (eur 000)

2009 (eur 000)

Sales 323,406 265,372 1,221,414 979,811

Earnings Before Interest and Taxes (EBIT) 4,555 -7,510 17,203 -27,729

Depreciation 13,148 12,609 49,656 46,555

EBITDA 17,703 5,099 66,859 18,827

Net financial profit -3,683 -1,695 -13,910 -6,258

Profit before tax 854 -9,276 3,225 -34,249

Net profit -146 -9,192 -551 -33,939

Capital expenditure 4,538 8,223 17,139 30,361

Shareholders’ equity 148,541 137,387 560,998 507,263

Registered capital 24,534 24,534 92,658 90,585

Non-current assets 141,692 136,963 535,131 505,697

Liabilities 61,240 74,441 231,286 274,852

Balance sheet total 209,781 211,404 792,284 780,549

EPS –earnings per share (HUF/share, EUR/share) -6 -378 -0.02 -1.40

Major ratios 2008 2009

ROE – Return on owner’s equity (%) -0.10 -6.69

ROA – Return on assets (%) -0.07 -4.35

Closing headcount 1,170 1,167

Number of shares 24,290,843 24,290,843

Number of consolidated companies 9 9

Closing price of TVK shares on the Budapest Stock exchange (HuF and eur)

2008 (HuF)

2009 (HuF)

2008,(eur)

2009,(eur)

- Highest 7,060 3,495 26.66 12.90

- Lowest 2,405 1,760 9.08 6.50

- On December 31 2,405 3,400 9.08 12.55

Capitalisation (on December 31 closing price, million) 58,420 82,589 220.64 304.94

Note:

The EUR/HUF mid FX rate quoted by the National Bank of Hungary for December 31, 2008 was: 264.78

The EUR/HUF mid FX rate quoted by the National Bank of Hungary for December 31, 2009 was: 270.84

TVK annual report 20096 7Key FInanCIal anD operaTInG DaTa

Chairman’s letter

To all Stakeholders,

The long-lasting double effect of the financial crisis stemming from 2008 affected the European polyolefin market also in 2009. Similarly to 2008, polymer producers faced not only a major decrease in polymer demand, their customers also struggled with gaining access to credit. In 2009 European polyolefin demand continued to drop in comparison to 2008, although at the year-end the market began to show some signs of recovery and in Q4 demand was higher than in the same period of 2008.

The crisis that hit the real sector during 2009 led to the worst results in our industry in the last two decades. The profitability of our polymer products dropped dramatically and, consequently, we recorded the lowest operating profits ever in the history of TVK. Despite the operating profit achieved in Q3, in 2009 the Group generated an operating loss of HUF 7.5 billion, which was more than HUF 12 billion lower than the preceding year’s overall result. The main drivers of this decrease included a lower integrated petrochemical margin, higher annual average energy costs, as well as lower production and sales volumes of the olefin plants.

Despite the considerable loss, we consider 2009 a success because we managed to maintain our cash generating ability and, owing to our integrated operation, we also remained a sound and reliable part-ner to our polymer customers, who were supplied and retained without any reduction in our polymer capacities. A continuous presence on the polymer market is a robust foundation for the improvement of our market position, competitive edge and liquidity. The operating cash flow reached HUF 4,855 million, mainly because of the positive EBITDA and working capital optimisation.

With the help of a cost-cutting and efficiency improvement programme, our company retained its liquidity without any bank loans. In addition to the successfully implemented maintenance overhaul activities, we were able to finance the scheduled tasks of the Olefin-1 Plant reconstruction programme as well as the debt service of our loans, therefore our gearing ratio also decreased in 2009.

We achieved this performance in spite of significantly worse capacity utilisation in our olefin production triggered by the fall in ethylene sales. In order to partially compensate this, in Q4 2009 we concluded a contract with Synthos, one of the largest chemical companies in Poland, for the supply of raw C4 fraction in 2010-2012, which helps us to improve the capacity utilisation of the olefin plants.

Exploiting our competitive advantage in the region, we modified our sales strategy in the field of logistics, product development and close costumer relations, focusing more intensively on Central and Eastern Europe. Consequently, we closed our commercial subsidiary in the United Kingdom and withdrew our sales staff from Russia. We are able to maintain our market presence in the above-mentioned countries however, through other, more effective sales channels. In order to boost sales towards Hungarian small and medium-sized enterprises, we opened two new sales sites in addition to the two existing points of sale in 2009.

Despite the difficult circumstances, our company continued acting as a responsible corporate citizen. TVK responsibly continued its practice of playing a leading role in promoting the achievement of, and

György MosonyiChairman of the Board of Directors

creating the opportunities for, outstanding results in the field of education and training, culture, arts, science and sports in the South Borsod region. We launched a successful project in the region called “One Day around TVK” within the framework of which we presented our activities and efforts for sustainable development to students forming the potential basis of our future workforce.

As a result of our actions aimed at improving the efficiency of energy, steam and water consumption, we reduced both our operating expenditure and our ecological footprint. With the help of technical development in SC-1 and SC-2 plants, steam consumption was reduced considerably. Steam is supplied by TVK Power Plant which now uses less gas and has thus reduced its CO2 emissions and costs.

The economic crisis and the recession force the petrochemical sector to face unprecedented challenges and severe competition in the future. We implemented numerous measures in order to offset the unfavourable changes. In addition to efficiency increase and strict cost control, we are also focusing on sharpening our competitive edge in our markets, continuing to develop our business and managing our product and customer portfolio pro-actively. As the markets of central Europe have greater growth potential than the European average, our sales strategy continues to concentrate on exploiting our favourable geographic location. In addition, we intend to strengthen our positions on the key western European markets. The 2009 sales volume has also proved that there is further growth potential in our main activity and markets.

Let me take this opportunity to thank all our colleagues for their responsible and committed work, which significantly contributed to our 2009 results and sustained stability. At the same time, I also ask them to maintain the same commitment and dedication in 2010 as well.

TVK annual report 20098 9CHaIrMan’S leTTer

A rollercoaster year for the world economyAs far as the global economy is concerned, 2009 was a rollercoaster year. At the beginning of it, the risk of an imminent financial and economic collapse seemed very real. Economic activity, trade and investment were declining steeply. Asset prices were volatile and still on a downward trend. Policymakers globally reacted by an extreme loosening of fiscal and monetary policies and in many countries by de facto guaranteeing the financial system. The result was a turnaround in economic activity after the first quarter, and a spectacular recovery in asset prices. Emerging markets in general led the economic recovery, while (mostly rich) countries burdened with high debt were lagging. Despite the economic upturn, unemployment continued to increase throughout the year in OECD countries, and there is a broad consensus among analysts that the recovery remains fragile as many of the factors behind it are temporary. The extreme monetary loosening has increased inflation risks and may have contributed to incipient new asset price bubbles in some areas. The unprecedented fiscal deficits raised concerns regarding the long-term sovereign solvency of some economies.

Driven by the improving economic climate and receding fears of a double-dip recession, oil prices nearly doubled throughout 2009 surging from around USD 40/bbl in January to just below USD 80/bbl by the year-end.

CEE economies hit hard, but recovery underwayMost CEE countries, particularly small export oriented economies were hit hard by the global recession and suffered a sharp drop of GDP during 2009. Real sectors, especially industrial production, construction and domestic demand recorded significant losses throughout the CEE. After hitting the bottom in Q2 2009, most CEE economies started to show signs of recovery thanks to the slow return of growth in the region’s main Western export markets. Investor’s confidence have since stabilized and the conditions of refinancing public debt eased sufficiently as credit default swap (CDS) spreads returned to comfortable levels. At the same time, domestic demand continue to remain weak and massive stimulus spending of governments increased budget deficits dramatically, although it still remains well below the EU15 average in CEE economies.

overview of the environment

Hungary: Export-driven rebound expectedThe Hungarian economy experienced a significant GDP drop in 2009 expected at around 6.3%. The large drop in private consumption played a considerable role in the downturn. Fiscal austerity measures reined in government spending and helped to bring the 2009 budget deficit figure to around 3.8% of GDP. The economic contraction likely bottomed out in Q3 only, later than in most CEE economies indicating that the massive debt reduction had a negative effect on growth. Weak household demand and high unemployment rate further constrains Hungary’s growth prospects, and thus the economic recovery will be fuelled by external rather than domestic demand. Annual GDP growth will likely remain slightly negative in 2010, and return to firm growth in 2011 only.

Petrochemical TrendsRegarding the European polyolefin demand, the year of 2009 was characterized by the long lasting effect of financial crisis started in 2008 which had double effect on polyolefin markets. Similarly to 2008 the polymer producers faced significant decrease in polymer demand and the credit limitations of their customers as

a result of financial crisis. On yearly basis the European polyolefin demand decreased further compared to 2008, however in Q4 2009, the demand slightly recovered compared to previous quarter and it was higher than in the same period of 2008. The negative impact of recession on sales was most significant in case of automotive and construction segments while the sales in consumer goods and consumer packaging segments showed slight increase in second half of the year. At the end of the year, the demand was supported by the change in price expectations and the some converters increased their purchases depending on their financing constraints.

In 2009 the average quoted (FOB med) price of naphtha (514 USD/t) showed a year on year decrease of 32% whilst the average quoted (CIF med) price of atmospheric gas oil (518 USD/t) was 44% lower than in 2008. The prices quoted in the European markets for the polymer products produced by TVK (ICIS’ fd nwe low spot, EUR/t) was on the lowest level in December 2008, because due to the economic crisis, the prices dropped significantly in the second half of the year. The average quoted prices of the polymers increased in the first quarter of the year, while the prices remained stable in the second quarter. In the second half of the year the prices increased further, while in the last months the market was characterised by decreasing prices. The annual averages of the quoted prices of polyethylene and of polypropylene – despite the almost continuous increase during the year - were lower by 27-28% and 26% y-o-y. For the year as a whole, the average quoted price of LDPE was 841 EUR/t, that of blown HDPE grade was 834 EUR/t, whilst PP homopolymer raffia and copolymer grades were 781 and 838 EUR/t.

The HUF strengthened by 12% against the EUR and by 18% against the USD, while the EUR weakened by 5% against the USD in 2009.

As a consequence of the changes in the feedstock prices, quoted polymer prices and exchange rates (especially EUR/USD), the integrated petrochemical margin declined significantly by 17% in HUF-terms to 85000 HUF/t and by 25% in EUR-terms to EUR 304/t in 2009 year-on-year.

TVK annual report 200910 11oVerVIew oF THe enVIronMenT

“we could permanently supply our cus-tomers without relevant capacity cut and generating profit for the Group, while our european competitors cut capacities and shut down plants, due to poor prof-itability and weak demand”

our businesses TVK annual report 200912

TVK member of the MOL Group - the advantages of integration The MOL Petrochemical Division, consists of TVK and SPC and operate in integrated manner with MOL Refining and Marketing Division. We process 2.0 – 2.5 million tons of petrochemical feedstock annually. Vast majority of this naphtha feedstock is produced by MOL refineries. This captive market of naphtha allows higher utilization rates for refining and provides better unit costs. Other important benefits from the integration are the joint and optimized energy and steam supply systems. Our petrochemical co-product sales to Refining amounts to the 30% of the total petrochemical feedstock purchased. These olefin plant products are important components in fuel and aromatic production. These connections with

petrochemicals plants provide higher operational flexibility to MOL Refining.

MOL Group Refining and Marketing Division secures the feedstock to the MOL Group Petrochemicals Division. The Group can also provide strong financial background to the cyclical petrochemical business.MOL Group supply-chain management system optimized along our ‘crude to plastic’ philosophy allowed us to keep operation up in 2009, against the unfavorable business environment and we could permanently supply our customers without relevant capacity cut and generating profit for the Group, while our European competitors cut capacities and shut down plants, due to poor profitability and weak demand.

Production, feedstock supply, maintenance shutdowns, investment in technology are the major synergic benefits deriving from the integration between TVK and SPC. The total polyolefin production capacity exceeds 1,2 million tones in the two sites that provides leader position in polyolefin production in Central Europe and represents considerable market share in Europe. Sales, marketing and logistics operation that we perform under integrated management and develop according to a coherent strategic approach, are generating further important benefits for MOL Petrochemicals.

2009 main resultsThe annual average of integrated petrochemical margin hit the lowest level in 2009 and dropped by 25 percent from its 2008 level. The petrochemical sector profitability touched its historical bottom resulting capacity cuts and tight supply in Europe. Only the third quarter brought some recovery and reasonable prices in the global market of polyolefin.

Profit generation potential in petrochemicals was hit by the coincidence of more unfavorable effects:• Beyond the peak of petrochemical cycle in 2007,

polyolefin prices have decreased,• The global financial and economic crisis resulted

significant setback in key customer segments, as the automotive and the construction industries,

• Crude oil prices kept growing and made a shift in petrochemical feedstock price to high level,

• Modern and competitive scale capacities came on stream in China and in the Middle East.

our main strategic goals and results

Our strategy focuses on competitiveness and value creation. The continuous improvement of competitiveness enables our company to permanently exploit business opportunities and reveal new ones. Keep tracking this strategic pattern, our operation creates added value for our shareholders and for all the stakeholders of our business.

We are committed to sustainable development as our actions show. We continued to study and minimize the environmental impact of our activities, as well as the use of energy, and pollutant emissions implementing many projects. We conduct researches to produce biodegradable polymers. Considering our present competitive position and our expectations for the business environment, our main strategic objectives are as follows:

• Maintain our leadership on the regional petrochemical market by continuously improving our operating efficiency and the competitiveness of our assets, by consequently implementing the planned development programs;

• Focus in the sales - By strengthening our polyolefin market positions in Central Europe by product developments

tailored to customer requirements - Improve our sales services and optimize our customer portfolio.• Utilize the largest possible extent the synergies emanating from cooperation with other MOL Group

companies to achieve a common business optimum.

TVK annual report 200914 15our MaIn STraTeGIC GoalS anD reSulTS

We managed to keep MOL Group petrochemical product sales volume in line with the preceding year’s figures, against the negative effects of the global economic setback, triggered by the crisis in the financial sector and hit the overall profitability in the petrochemical industry. Automotive and construction segments have reported the largest decline in sales. Sold volume in the industrial segments dropped considerably. Sales to other customer segments as consumer goods, packaging industry and to the agricultural segment had counteracted the negative effects.We were quick to respond the unfavorable market trends: despite we permanently closed the oldest and undersize LDPE-1 plant in March 2009, polyolefin production increased slightly in 2009, due to the high availability and utilization rate of polyolefin plants.We carried out maintenance and reconstruction works in the first quarter at TVK Steam Cracker-1 plant. With regards the maintenance shut downs planned in the third quarter at our competitors in Europe, we reschedule the general overhaul at TVK Steam Cracker-2 from the third to the second quarter, so our polyolefin plants were running at full stream, when prices started to increase because of the tight supply in the third quarter.

In line with our strategic aims of focusing on the regional markets - moreover to meet cost saving

targets, our sales offices have been closed in Russia and in the United Kingdom.

The experiences of 2009 have proven the decisive impact of external factors on the petrochemical business yet again and highlighted that our capabilities and business measures taken in due course can be sufficient to avoid losses and to cope with and overcome even extremely difficult periods.

Facing future challengesWhen our markets will get through the unfavorable effects of the recession, the economies in Central Europe will continue to converge to the level of development of Western Europe, which is expected to be swift and to bring major qualitative and quantitative shifts in the growing demand for polyolefin. Accordingly we revised our sales and marketing strategy and revalued the importance of our core-region - Central Europe, where we gain explicit benefit from the advantageous geographical position, the favorable logistics costs and from the better understanding of customer needs.

Integration benefits, the excellent location and the well balanced product and customer portfolios are the key momentums that can determine our competitive power.We are working to shape our business portfolio in a coherent system that evaluates every material

factor with a view to our strategic objectives. Although circumstances influencing the market are in constant change, our portfolio development relies on opportunities that promise to ensure that our company can sustain its value creation in the longer run. We are further improving our operational and organizational efficiency and continuously developing the quality of our products and customer services, to ensure that we can withstand strong competitive forces in long term. Our company has been traditionally excelled in these areas and performing at a high level of quality therefore we have every reason to face future challenges with confidence and to seize every opportunity that the future may present for a leading Central European petrochemical enterprise

Our development strategy seeks to shape and improve a balanced product portfolio. We attach equally high importance to develop our polyethylene and polypropylene product lines, but we are also examining additional diversification options to complement our polyolefin business lines on the basis of mutual benefits - either with the involvement of external partners. Cooperation with our strategic partners - such as MOL Group companies and BorsodChem, which look back on decade-long history - will remain a key element of our operations and will continue to improve the value of our business portfolio. In order to develop our business and improve our capacity utilization

rates at our olefin plants, in December 2009 we have signed a three years supply contract of selling butadiene rich C4 fraction to the polish polystyrene producer Synthos.

As regards sales, we further develop our successful method of active product and customer portfolio management, which is supported by a system designed to optimize the whole supply chain (Supply Chain Management).

We give high priority for protecting our environment. In this regard, we wish to live up to our corporate social responsibility by keeping our plants at a high technical level and by doing so reducing security and environmental risks as well as by operating environmental protection system that outperforms regulatory requirements. Moreover, we are also engaged in developing a new polyolefin product. In cooperation with two universities and a research company, our product development staff is working on the development of a special additive that enables us to produce biodegradable polyolefin products.

As regards the long term future, we are confident that polyolefins and other petrochemical products can play an important role in making people’s lives more perfect. Our mission is to make this opportunity real.

TVK annual report 200916 17our MaIn STraTeGIC GoalS anD reSulTS

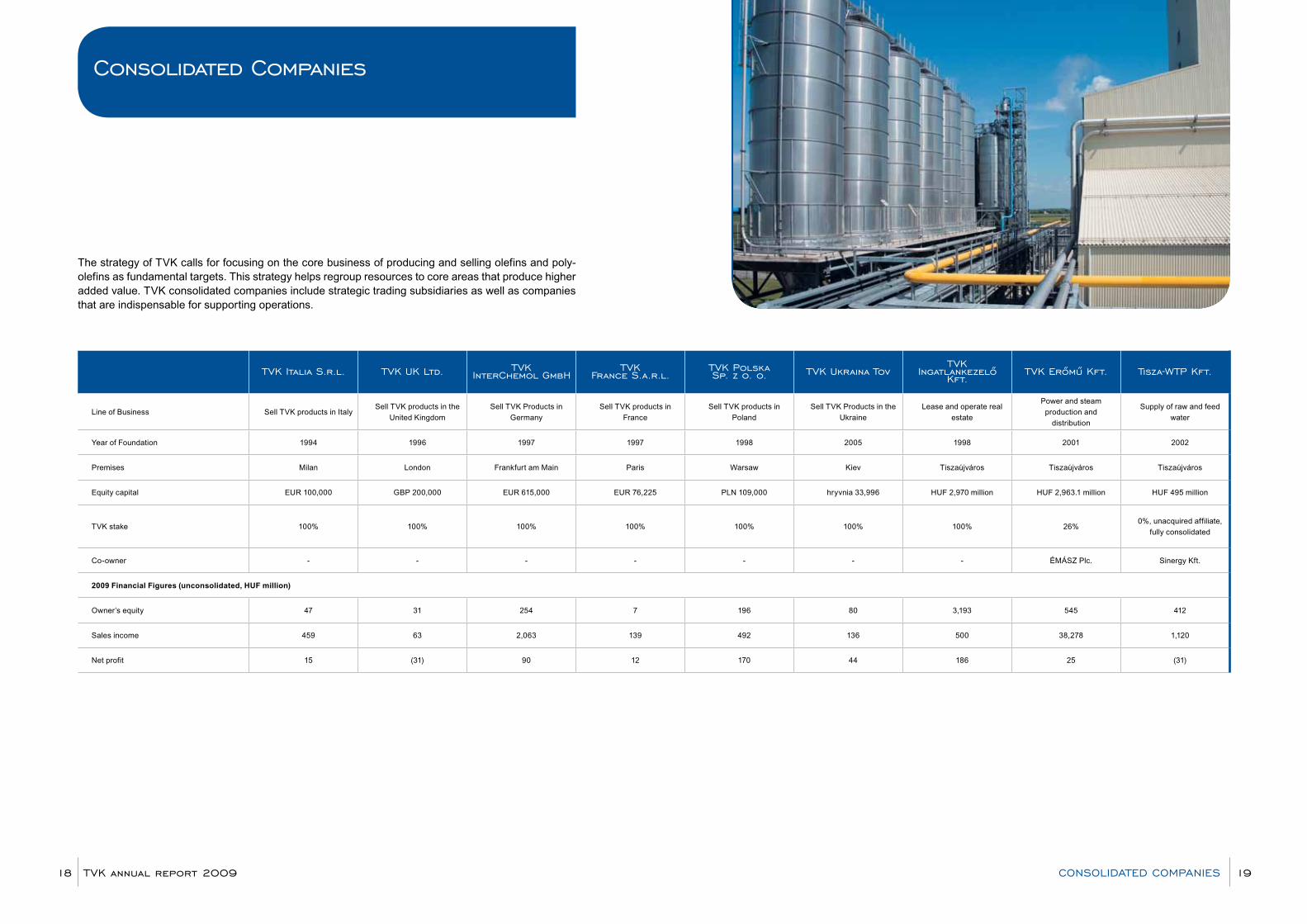

The strategy of TVK calls for focusing on the core business of producing and selling olefins and poly-olefins as fundamental targets. This strategy helps regroup resources to core areas that produce higher added value. TVK consolidated companies include strategic trading subsidiaries as well as companies that are indispensable for supporting operations.

Consolidated Companies

TVK Italia S.r.l. TVK uK ltd. TVK InterChemol GmbH

TVK France S.a.r.l.

TVK polska Sp. z o. o. TVK ukraina Tov

TVK Ingatlankezelő

Kft.TVK erőmű Kft. Tisza-wTp Kft.

Line of Business Sell TVK products in Italy Sell TVK products in the

United Kingdom

Sell TVK Products in

Germany

Sell TVK products in

France

Sell TVK products in

Poland

Sell TVK Products in the

Ukraine

Lease and operate real

estate

Power and steam

production and

distribution

Supply of raw and feed

water

Year of Foundation 1994 1996 1997 1997 1998 2005 1998 2001 2002

Premises Milan London Frankfurt am Main Paris Warsaw Kiev Tiszaújváros Tiszaújváros Tiszaújváros

Equity capital EUR 100,000 GBP 200,000 EUR 615,000 EUR 76,225 PLN 109,000 hryvnia 33,996 HUF 2,970 million HUF 2,963.1 million HUF 495 million

TVK stake 100% 100% 100% 100% 100% 100% 100% 26%0%, unacquired affiliate,

fully consolidated

Co-owner - - - - - - - ÉMÁSZ Plc. Sinergy Kft.

2009 Financial Figures (unconsolidated, HUF million)

Owner’s equity 47 31 254 7 196 80 3,193 545 412

Sales income 459 63 2,063 139 492 136 500 38,278 1,120

Net profit 15 (31) 90 12 170 44 186 25 (31)

TVK annual report 200918 19ConSolIDaTeD CoMpanIeS

TVK annual report 200920 21

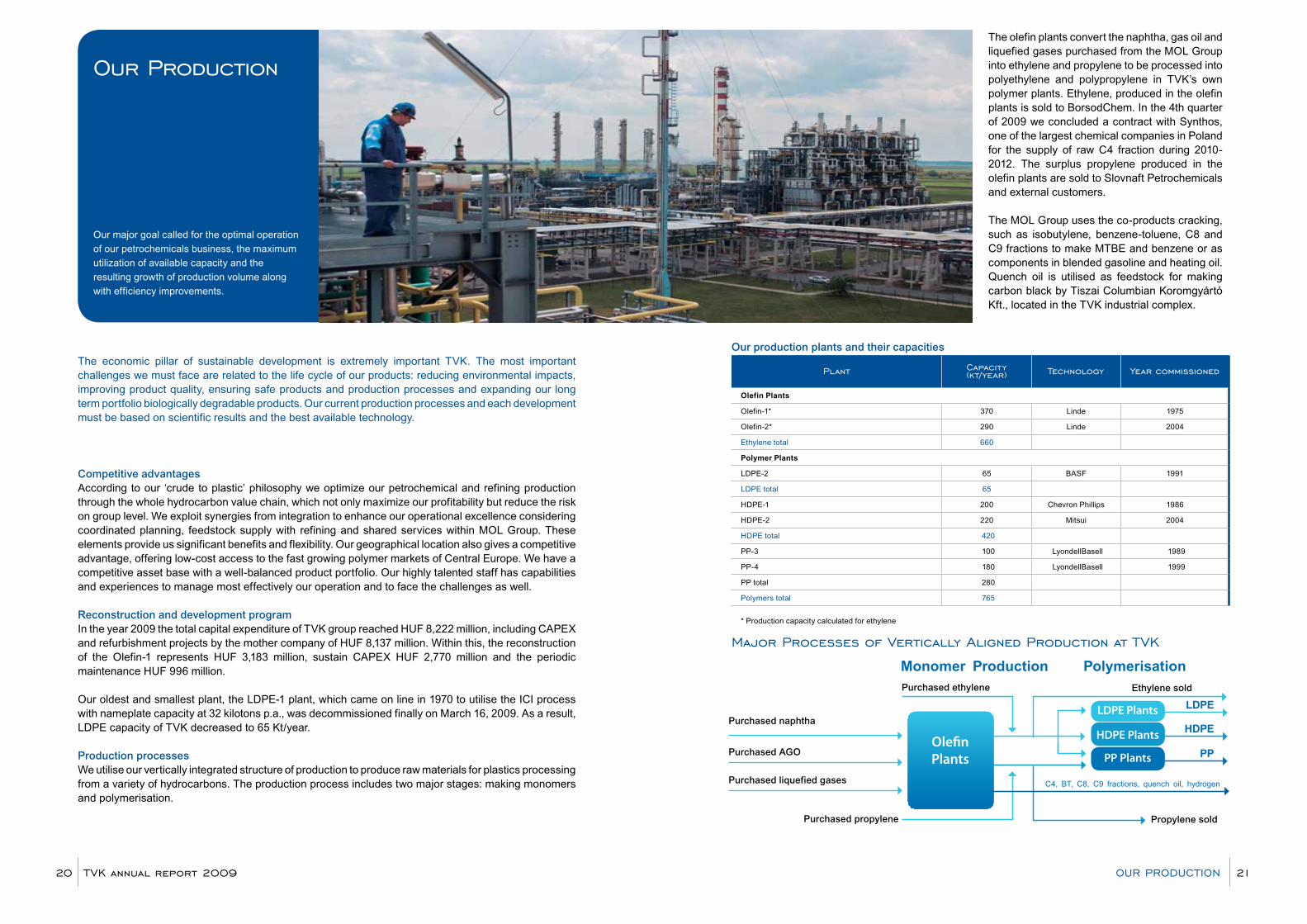

our production

Our major goal called for the optimal operation

of our petrochemicals business, the maximum

utilization of available capacity and the

resulting growth of production volume along

with efficiency improvements.

The economic pillar of sustainable development is extremely important TVK. The most important challenges we must face are related to the life cycle of our products: reducing environmental impacts, improving product quality, ensuring safe products and production processes and expanding our long term portfolio biologically degradable products. Our current production processes and each development must be based on scientific results and the best available technology.

Competitive advantages According to our ‘crude to plastic’ philosophy we optimize our petrochemical and refining production through the whole hydrocarbon value chain, which not only maximize our profitability but reduce the risk on group level. We exploit synergies from integration to enhance our operational excellence considering coordinated planning, feedstock supply with refining and shared services within MOL Group. These elements provide us significant benefits and flexibility. Our geographical location also gives a competitive advantage, offering low-cost access to the fast growing polymer markets of Central Europe. We have a competitive asset base with a well-balanced product portfolio. Our highly talented staff has capabilities and experiences to manage most effectively our operation and to face the challenges as well.

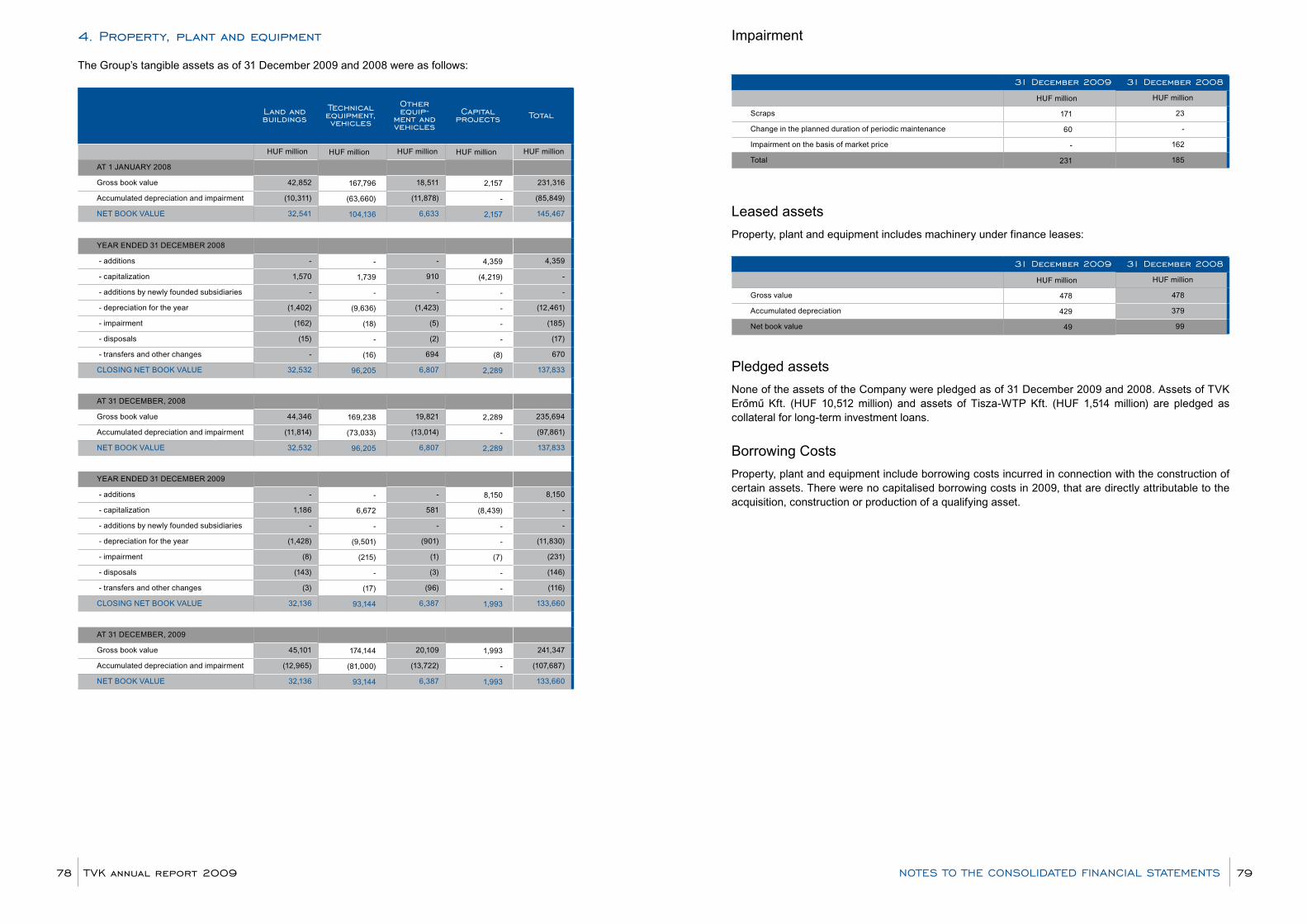

Reconstruction and development program In the year 2009 the total capital expenditure of TVK group reached HUF 8,222 million, including CAPEX and refurbishment projects by the mother company of HUF 8,137 million. Within this, the reconstruction of the Olefin-1 represents HUF 3,183 million, sustain CAPEX HUF 2,770 million and the periodic maintenance HUF 996 million.

Our oldest and smallest plant, the LDPE-1 plant, which came on line in 1970 to utilise the ICI process with nameplate capacity at 32 kilotons p.a., was decommissioned finally on March 16, 2009. As a result, LDPE capacity of TVK decreased to 65 Kt/year.

Production processesWe utilise our vertically integrated structure of production to produce raw materials for plastics processing from a variety of hydrocarbons. The production process includes two major stages: making monomers and polymerisation.

our proDuCTIon

Our production plants and their capacities

plant Capacity (kt/year) Technology year commissioned

Olefin Plants

Olefin-1* 370 Linde 1975

Olefin-2* 290 Linde 2004

Ethylene total 660

Polymer Plants

LDPE-2 65 BASF 1991

LDPE total 65

HDPE-1 200 Chevron Phillips 1986

HDPE-2 220 Mitsui 2004

HDPE total 420

PP-3 100 LyondellBasell 1989

PP-4 180 LyondellBasell 1999

PP total 280

Polymers total 765

* Production capacity calculated for ethylene

Major processes of Vertically aligned production at TVK

Monomer Production PolymerisationPurchased ethylene Ethylene sold

Purchased propylene

Purchased naphtha

Purchased AGO

Purchased liquefied gases C4, BT, C8, C9 fractions, quench oil, hydrogen

Propylene sold

Olefin Plants PP Plants

HDPE Plants

LDPE Plants LDPE

HDPE

PP

The olefin plants convert the naphtha, gas oil and liquefied gases purchased from the MOL Group into ethylene and propylene to be processed into polyethylene and polypropylene in TVK’s own polymer plants. Ethylene, produced in the olefin plants is sold to BorsodChem. In the 4th quarter of 2009 we concluded a contract with Synthos, one of the largest chemical companies in Poland for the supply of raw C4 fraction during 2010-2012. The surplus propylene produced in the olefin plants are sold to Slovnaft Petrochemicals and external customers.

The MOL Group uses the co-products cracking, such as isobutylene, benzene-toluene, C8 and C9 fractions to make MTBE and benzene or as components in blended gasoline and heating oil. Quench oil is utilised as feedstock for making carbon black by Tiszai Columbian Koromgyártó Kft., located in the TVK industrial complex.

TVK annual report 200922 23

Polymer Production In 2009, total polymer production reached 724 kt, decreased by 9 kt y-o-y. Production contracted in LDPE and PP segment, while there was increasing produced volume of HDPE products. The net income from polymer sales was down by 18% and it reached HUF 169 billion. 73% of the sales were realized in export markets.

Low-Density Polyethylene (LDPE) Product GroupUsing ICI technology, the LDPE-1 Plant of TVK came on in 1970 and was complemented by the LDPE-2 Plant of BASF technology in 1991. The LDPE-1 Plant was eventually shut down on 16 March, decreasing the annual LDPE capacity of TVK unit to 65 kt.

The sales income of the LDPE Product Group was HUF 19 billion in 2009, down by 27% compared to 2008. The sales volume was 80 kt. The production volume of LDPE product was 66 kt in 2009, down by 25% compared to 2008, as a consequence of the closure of the LDPE1 Plant. The capacity utilisation was 93%.

Sales Income and Volume Sold by the LDPE Product Group

0 200 400 600 800

20052006200720082009

0 30 60 90 120 150

20052006200720082009

VoluMe SolD (KIloTonS)

our proDuCTIon

olefin production

Olefin Production The Olefin-1 Plant started up in 1975 and Olefin-2 came on line at TVK site in 2004. Both utilise Linde technology. Calculated for ethylene, the annual capacity of the two plants from 2008 increased from 620 kt to 660 kt as a result of the efficiency improvement modifications made in 2007.

In 2009, ethylene production of Olefin-1 Plant was only 4% lower, compared to 2008, despite maintenance shut downs during the year, because the production volume was lower in 2008 caused by the unfavourable pyrolysis feedstock supply and the shut downs. The production of Olefin-2 Plant decreased by 10% compared to 2008, when ethylene production was equivalent to the name capacity of 290 kt

In 2009, the sales income of olefin production decreased by 34 %, ethylene output was down by 7% compared to 2008. The capacity utilisation of both plants calculated for ethylene decreased from 92% to 86% as a consequence of the lower ethylene sales to BorsodChem.

Sales Income and Volume Sold by the Olefin Business Unit

oleFIn SaleS InCoMe (HuF BIllIon)0 30 60 90 120

20052006200720082009

SaleS InCoMe (HuF BIllIon)0 10 20 30 40

20052006200720082009

0 200 400 600 800

20052006200720082009

eTHylene proDuCTIon (KT)

CapaCITy uTIlISaTIon (%)0 20 40 60 80 100

20052006200720082009

* Capacity utilisation calculated for ethylene

CapaCITy uTIlISaTIon (%)0 20 40 60 80 100

20052006200720082009

TVK annual report 200924 25our proDuCTIon

Polypropylene (PP) Product GroupThe PP-3 Plant has operated since 1989 with Spheripol (Himont, currently LyondellBasell) technology, and has been complemented by the PP-4 Plant, which uses Spheripol (Montell, currently LyondellBasell) technology since 2000. The total annual capacity of the two plants is 280 kt.

The PP product sales income was HUF 59 billion, down only by 23%. The total 270 kt production volume was lower in 2009 y-o-y, while the capacity utilization was 96%.

Outlook The planned turnaround will determine the production in 2010. The Olefin-2 plant was designed with 5 years turnaround period. The first turnaround will be carried out during 2010, resulting one month production break. The turnarounds of the HDPE-2 and PP-4 plants with 3 years turnaround period will be harmonised to this determinative event with three and two weeks production break, respectively. The external economic environment compels us to maintain austerity in cost management while focusing first of all on the continuous improvement of operating efficiency, maintaining and ensuring secure operations, enhancing the energy efficiency of our systems of process technology in view of the substantial rise of energy prices and on identifying and immediately implementing any remaining opportunities presented by our technological systems besides considering the environmental aspects in full.

Sales Income and Volume Sold by the PP Product Group

SaleS InCoMe (HuF BIllIon)0 20 40 60 80

20052006200720082009

0 100 200 300 400

20052006200720082009

VoluMe SolD (KIloTonS)

CapaCITy uTIlISaTIon (%)0 20 40 60 80 100

20052006200720082009

0 200 400 600 800

20052006200720082009

0 100 200 300 400 500

20052006200720082009

VoluMe SolD (KIloTonS)CapaCITy uTIlISaTIon (%)

0 20 40 60 80 100

20052006200720082009

SaleS InCoMe (HuF BIllIon)0 30 60 90 120

20052006200720082009

High-Density Polyethylene (HDPE) Product GroupUtilising Chevron Phillips process technology, the HDPE-1 Plant was constructed in 1986. The HDPE-2 plant utilising the Mitsui Chemicals so-called CX-process came on line in 2004. The joint annual capacity of the two plants is 420 kt.

Sales income of the HDPE Product Group decreased by 12% and reached HUF 91 billion. The total production volume was 387 kt, up by 7 % compared to 2008, increasing the capacity utilization to 92%.

Sales Income and Volume Sold by the HDPE Product Group

Total polymer production amounted to 724 kt in 2009, representing a year-on-year downturn of 9 kt. Altogether 749 kt of polymer products were sold, which is 15.9 kt higher than in the previous year. Sales contracted in LDPE and PP segment, while there was increasing volume of sales for HDPE products. As a consequence of the shut-down of LDPE-1 plant the LDPE sales decreased, which was partly offset by the domestic sales of SPC-LDPE product.

The net income from polymer sales amounted to HUF 169 billion in 2009, which is HUF 37 billion below the sales income of the previous year, since the positive effect of the higher sales volume was offset by the reduction of quoted polymer prices.

Export destinations represent 73% (546.5 kt) of total polymer sales, whilst the share of the domestic market was 27% (202.5 kt). In 2009, polymer sales continued to focus on Central- and Eastern European markets (54%), while 44 % of revenues were realised in other European countries, and only 2% were originating outside of Europe. Our proprietary distribution network, which we have been operating successfully for several years covering several European countries, has been instrumental in achieving

these results. We have offices in Austria, France, Poland, Germany, Italy, the Ukraine and Romania. Our foreign trading subsidiaries are engaged in selling the products of both TVK and the MOL Group member Slovnaft Petrochemicals.

We continued to implement the tactical elements of our strategy successfully despite the hardships: we enhanced our market analyses methodology, we have developed a new portfolio of services to strengthen customer loyalty, we have revamped our sales concept with a view to improving the efficiency of our sales channels and we continued to modify our product portfolio flexible in response to the outcome of continuous analyses.

Direct customer communications were strengthened as part of our new services portfolio. In November, 2008 we launched a customer magazine called PROGRESS, strengthening the loyalty of our costumers through this new channel. Our magazine offers useful information to clients about product development projects, our production and business activities and can get an inside view of the life of TVK.

OutlookThe economic crisis and the recession force the petrochemical sector to face unprecedented future challenges and severe competition. We have made numerous arrangements in order to offset the unfavourable changes. In addition to increasing efficiencies and strict cost control, we are focusing to sharpen our competitive edge on our markets, continuing to develop our business and managing proactively our product and customer portfolio.

As the markets of Central Europe have greater growth potential than the European average, our sales strategy continues to focus on exploiting our favourable geographic location. Besides, we intend to strengthen our key Western European penetration. In 2009 the sales volume also proved, that there are further growth prospect regarding our main activity and markets.

Our future goals- Maintain regional leadership- Maintain the reliable and stable customer

base, serving new customers and further improve customer loyalty

- Manage customer portfolio actively- Maintain secure relation with our partners- Manage product portfolio according market

requirements

We develop our products by continuously examining customer requirements. We do our best to deliver high quality services and product information related to our products in order to satisfy customer needs completely by keeping product liability in mind, which we interpret to mean that it is our duty to manage, improve and communicate the health, safety and environmental (HSE) effects during the life cycle of our products and production processes. Tailor made products were launched and we are working on further product developments with higher added value. It is our aspiration to integrate product liability into each section of the life cycle, including sales.

The international financial crisis and the ensuing economic recession left their marks on our performance in 2009 as well. Quoted prices and currency rates, which have a particularly high impact on the petrochemical business, hit our profitability significantly. However the margins mended during the third quarter of the year, they were moving in an unfavourable lane at major part of the year. TVK has proved to be a reliable partner, at the time of the crisis, for its costumers, as we were able to continuously serve them during the year, further deepening our relationship.

Exploiting our favourable geographic location we have amended our sales strategic, at the field of logistics product development and tight costumer relations, giving bigger focus to the Central- and Eastern European region. Therefore we have closed our sales office in the United Kingdom and Russia. We are able to maintain our market presence in the above-mentioned countries however, through other sales channel. In order to enhance the selling towards middle- and smaller size companies we opened two new selling points, besides the already existing two, in 2009.

We concluded a contract with Synthos, one of the largest chemical companies in Poland for the supply of raw C4 fraction during 2010-2012. In this way we are in position to increase the sales of the by-products of the olefin plant and to improve the capacity utilisation of the olefin plants at the same time, which is a significant risk mitigating factor at the time of the financial crisis and hide further market opportunities in itself.

our Sales

Due to our integrated operation and actively

managed product- and customer portfolio we

were able to maintain our market presence and

reputation both in Hungary and in the countries

of Central and Eastern Europe despite

extremely adverse market circumstances went

on in 2009, following the year 2008.

TVK annual report 200926 27our SaleS

“Despite of the significant losses we consider the year a success, because we preserved our cash producing ability and due to our integrated operation we were in position to supply and keep our polymer customers without reducing our polymer capacities.”

Financial and operational performanceTVK annual report 200928

TVK annual report 200930 31ManaGeMenT DISCuSSIon anD analySIS oF THe reSulTS

Management Discussion and analysis of the results

eFFICIenT operaTIon DeSpITe unFaVouraBle MarKeT enVIronMenT

The crisis starting from the financial sector in the year 2008 that became fully-fledged in the real sector during 2009 produced the worst results of the last two decades in our industry. The profitability of our polymer products dropped dramatically and consequently we had the lowest operating profits ever in the history of TVK. Despite of the significant losses we consider the year a success, because we preserved our cash producing ability and due to our integrated operation we were in position to supply and keep our polymer customers without reducing our polymer capacities. We achieved all this in spite of the significant worsening of the capacity utilisation of our olefin production resulting from the ethylene sales decrease. In order to partially compensate this, in the 4th quarter of 2009 we concluded a contract with Synthos, one of the largest chemical companies in Poland for the supply of raw C4 fraction during 2010-2012. In this way we are in position to increase the sales of the by-products of the olefin plant and to improve the capacity utilisation of the olefin plants at the same time. Continuous presence on the polymer market is a stable foundation for the improvement of our market position and of our competitive edge. Resulting from the implementation of our program mitigating the impact of recession we maintained the liquidity of our Company. Consequently we were in position to finance, in addition to the successfully implemented maintenance and turnaround activities, the actual tasks of the reconstruction program of our Olefin-1 plant and also the repayment of our credits therefore our gearing index have been decreased during 2009.

The figures presented in the 2009 Annual Report of the business year of Tisza Chemical Group Public Limited Company are audited and final. For the purposes of the Annual Report, the term “TVK Group level data” refers to the data of TVK Plc. and the entities under its control consolidated in line with international financial reporting standards (IFRS). 7 subsidiaries, 1 affiliated business and 1 non-participating business were fully consolidated while 2 businesses were consolidated by the equity method. As required under law, the annual report presents true and fair figures and statements, and does not withhold any facts that the issuer – to its best knowledge – considers to be of material importance in terms of evaluating the issuer’s position. The issuer is liable for the

contents of this flash report. The issuer is also liable for damages arising from a failure to make regular and extraordinary disclosures and any misleading representation in its disclosures.

TVK annual report 200932 33ManaGeMenT DISCuSSIon anD analySIS oF THe reSulTS

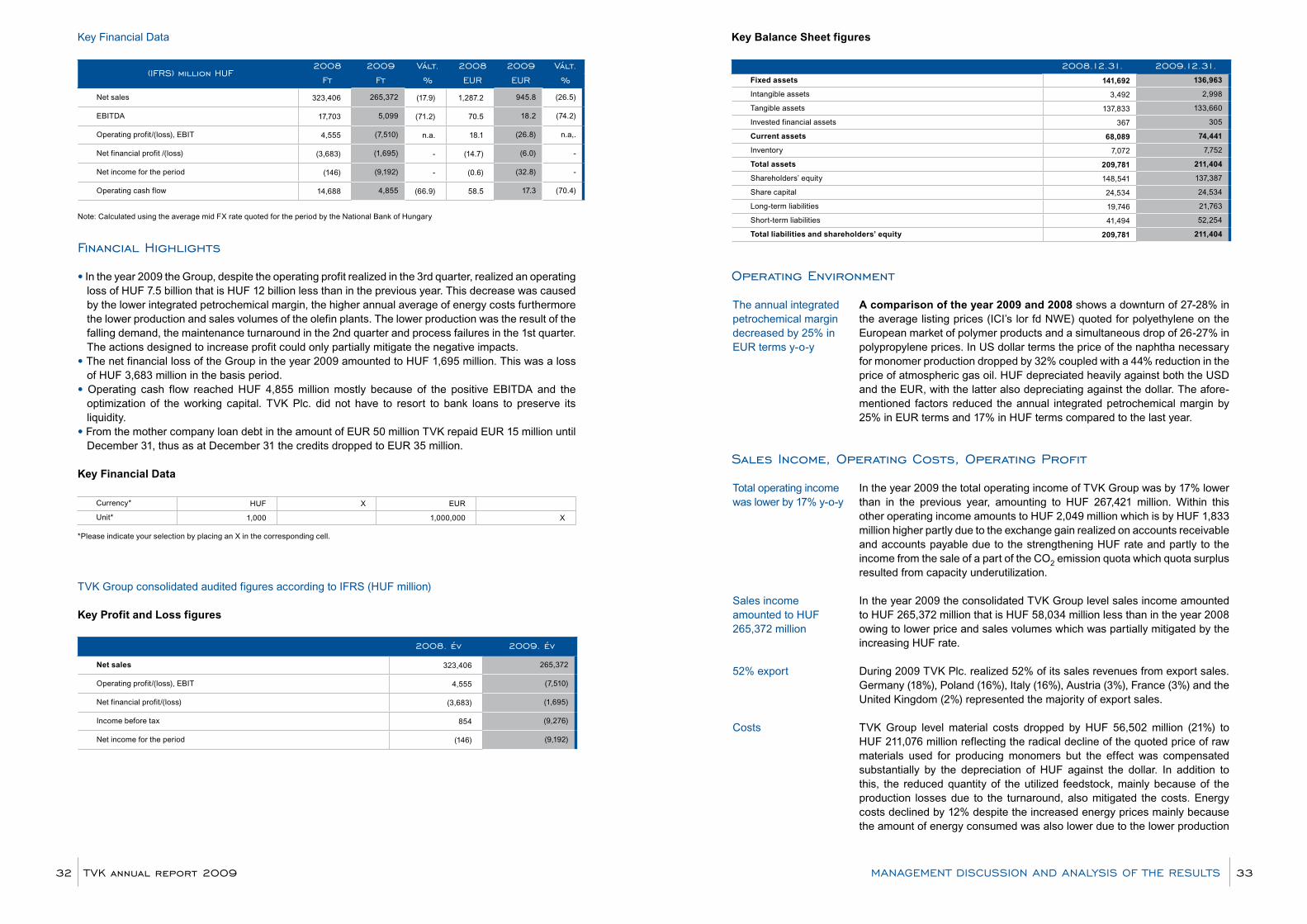

Key Financial Data

(IFrS) million HuF2008 2009 Vált. 2008 2009 Vált.

Ft Ft % eur eur %

Net sales 323,406 265,372 (17.9) 1,287.2 945.8 (26.5)

EBITDA 17,703 5,099 (71.2) 70.5 18.2 (74.2)

Operating profit/(loss), EBIT 4,555 (7,510) n.a. 18.1 (26.8) n.a,.

Net financial profit /(loss) (3,683) (1,695) - (14.7) (6.0) -

Net income for the period (146) (9,192) - (0.6) (32.8) -

Operating cash flow 14,688 4,855 (66.9) 58.5 17.3 (70.4)

Note: Calculated using the average mid FX rate quoted for the period by the National Bank of Hungary

Financial Highlights

• In the year 2009 the Group, despite the operating profit realized in the 3rd quarter, realized an operating loss of HUF 7.5 billion that is HUF 12 billion less than in the previous year. This decrease was caused by the lower integrated petrochemical margin, the higher annual average of energy costs furthermore the lower production and sales volumes of the olefin plants. The lower production was the result of the falling demand, the maintenance turnaround in the 2nd quarter and process failures in the 1st quarter. The actions designed to increase profit could only partially mitigate the negative impacts.

• The net financial loss of the Group in the year 2009 amounted to HUF 1,695 million. This was a loss of HUF 3,683 million in the basis period.

• Operating cash flow reached HUF 4,855 million mostly because of the positive EBITDA and the optimization of the working capital. TVK Plc. did not have to resort to bank loans to preserve its liquidity.

• From the mother company loan debt in the amount of EUR 50 million TVK repaid EUR 15 million until December 31, thus as at December 31 the credits dropped to EUR 35 million.

Key Financial Data

Currency* HUF X EUR

Unit* 1,000 1,000,000 X

*Please indicate your selection by placing an X in the corresponding cell.

TVK Group consolidated audited figures according to IFRS (HUF million)

Key Profit and Loss figures

2008. év 2009. év

Net sales 323,406 265,372

Operating profit/(loss), EBIT 4,555 (7,510)

Net financial profit/(loss) (3,683) (1,695)

Income before tax 854 (9,276)

Net income for the period (146) (9,192)

Key Balance Sheet figures

2008.12.31. 2009.12.31.Fixed assets 141,692 136,963

Intangible assets 3,492 2,998

Tangible assets 137,833 133,660

Invested financial assets 367 305

Current assets 68,089 74,441

Inventory 7,072 7,752

Total assets 209,781 211,404

Shareholders’ equity 148,541 137,387

Share capital 24,534 24,534

Long-term liabilities 19,746 21,763

Short-term liabilities 41,494 52,254

Total liabilities and shareholders’ equity 209,781 211,404

operating environment

A comparison of the year 2009 and 2008 shows a downturn of 27-28% in the average listing prices (ICI’s lor fd NWE) quoted for polyethylene on the European market of polymer products and a simultaneous drop of 26-27% in polypropylene prices. In US dollar terms the price of the naphtha necessary for monomer production dropped by 32% coupled with a 44% reduction in the price of atmospheric gas oil. HUF depreciated heavily against both the USD and the EUR, with the latter also depreciating against the dollar. The afore-mentioned factors reduced the annual integrated petrochemical margin by 25% in EUR terms and 17% in HUF terms compared to the last year.

Sales Income, operating Costs, operating profit

In the year 2009 the total operating income of TVK Group was by 17% lower than in the previous year, amounting to HUF 267,421 million. Within this other operating income amounts to HUF 2,049 million which is by HUF 1,833 million higher partly due to the exchange gain realized on accounts receivable and accounts payable due to the strengthening HUF rate and partly to the income from the sale of a part of the CO2 emission quota which quota surplus resulted from capacity underutilization.

In the year 2009 the consolidated TVK Group level sales income amounted to HUF 265,372 million that is HUF 58,034 million less than in the year 2008 owing to lower price and sales volumes which was partially mitigated by the increasing HUF rate.

During 2009 TVK Plc. realized 52% of its sales revenues from export sales. Germany (18%), Poland (16%), Italy (16%), Austria (3%), France (3%) and the United Kingdom (2%) represented the majority of export sales.

TVK Group level material costs dropped by HUF 56,502 million (21%) to HUF 211,076 million reflecting the radical decline of the quoted price of raw materials used for producing monomers but the effect was compensated substantially by the depreciation of HUF against the dollar. In addition to this, the reduced quantity of the utilized feedstock, mainly because of the production losses due to the turnaround, also mitigated the costs. Energy costs declined by 12% despite the increased energy prices mainly because the amount of energy consumed was also lower due to the lower production

Total operating income was lower by 17% y-o-y

Sales income amounted to HUF 265,372 million

52% export

Costs

The annual integrated petrochemical margin decreased by 25% in EUR terms y-o-y

TVK annual report 200934 35ManaGeMenT DISCuSSIon anD analySIS oF THe reSulTS

and energy optimization. The reconstruction and refurbishing work performed during the turnaround period incurred raw materials of HUF 1,073 million - this was offset in the self-manufactured assets line and was transferred to the investments

Material type services used dropped by HUF 626 million (-4%), and within this the amount of accounted agency fees dropped by HUF 175 million, of repair and maintenance costs by HUF 171 million, of the costs of recruiting workforce through temporary work agencies by HUF 127 million and of traveling and accommodation costs dropped by HUF 54 million. Transportation and warehousing costs are by HUF 86 million lower because of the lower sales volume and the modified tendering procedure of carriers.

The cost of the goods sold (COGS) is by HUF 1,521 million higher (25%) reflecting our cooperation with Slovnaft Petrochemicals s.r.o., where polymer products produced by Slovnaft Petrochemicals s.r.o. are sold by TVK. The purchasing costs of tar dropped by 21%. The positions appearing in the COGS are offset by sales.

Intermediated services increased significantly by the purchase of electricity for MOL Group through TVK Power Plant (TVK Erőmű Ltd.) in order to be able to optimize electricity purchase price. This cost was covered by revenue.TVK Group level Personnel type expenses are HUF 415 million (4%) higher mainly because of the changes in the value of raised and utilized provisions, implemented wage increase and accruals.

Other operating costs dropped by HUF 263 (6%). Within this it causes a reduction of HUF 632 million that the exchange loss on receivables and liabilities was reported among the costs in the basis period while it was included as profit among the other incomes in the reporting period. The expense of HUF 471 million booked when accounting the 2008 emission quota increases the costs incurred in the year 2009.

The change of self manufactured inventories in the reporting period shows a decrease of HUF 60 million, mainly because the quantity of self manufactured inventories has significantly dropped compared to the opening balance at the beginning of the year, at the same time this effect was significantly mitigated by the surging prime costs as the feedstock was more expensive than naphtha in December 2008 entailing the appreciation of inventories.

Capitalized own performances totaled at HUF 1,073 million in the year 2009 as the costs incurred because of the reconstruction and refurbishing works during the turnaround period were transferred to the investments.

The TVK Group level operating losses (EBIT) amounted to HUF 7,510 million in the year 2009, whereas in the same period of 2008 profits amounted to HUF 4,555 million.

profit/loss on Financial operations

The net financial loss of the Group in the year 2009 amounted to HUF 1,695 million. This was a loss of HUF 3,683 million in the basis period. Exchange loss of HUF 305 million was accounted on FX loans received and other assets denominated in foreign exchange, compared to the exchange loss in the amount of HUF 1,566 million in 2008. HUF 485 million less interest and HUF 97 million less discount was paid and interest income increased by HUF 158 million.

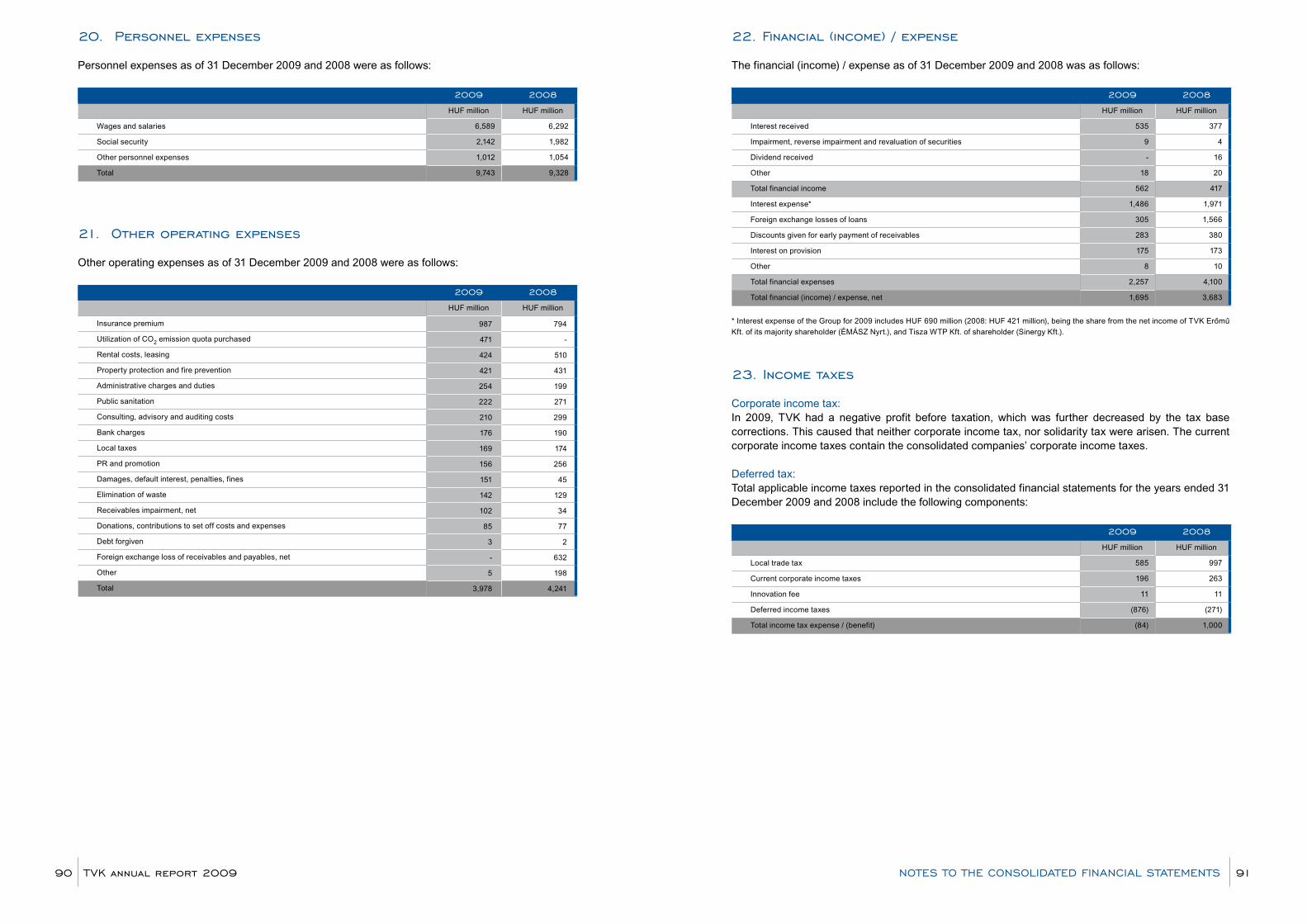

Taxation

In the year 2009 TVK Group income before taxes amounted to a loss of HUF 9,276 million with a tax liability of HUF 792 million. Deferred tax amounted to the negative figure of HUF 876 million and includes mainly the accrual of the negative tax base.

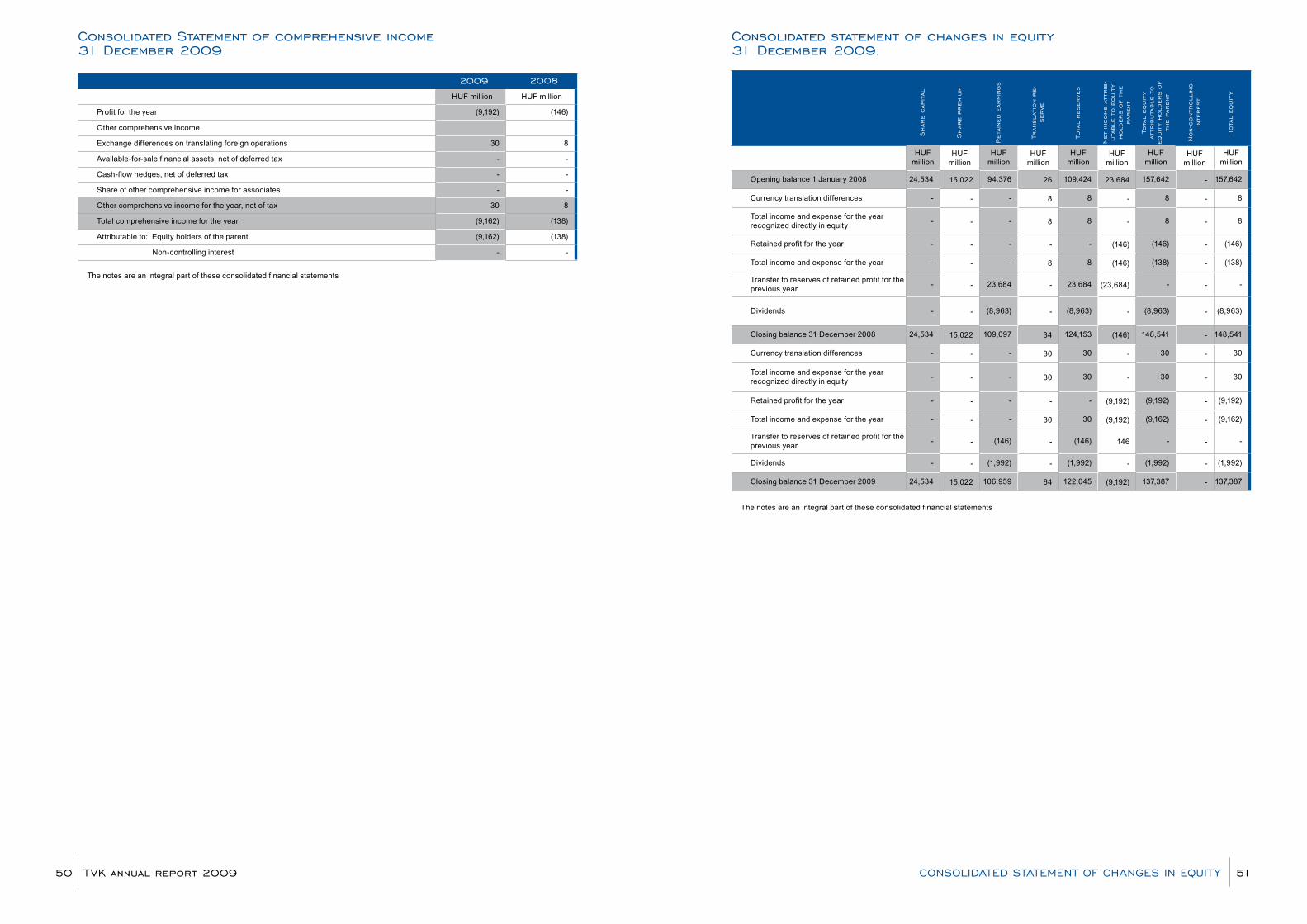

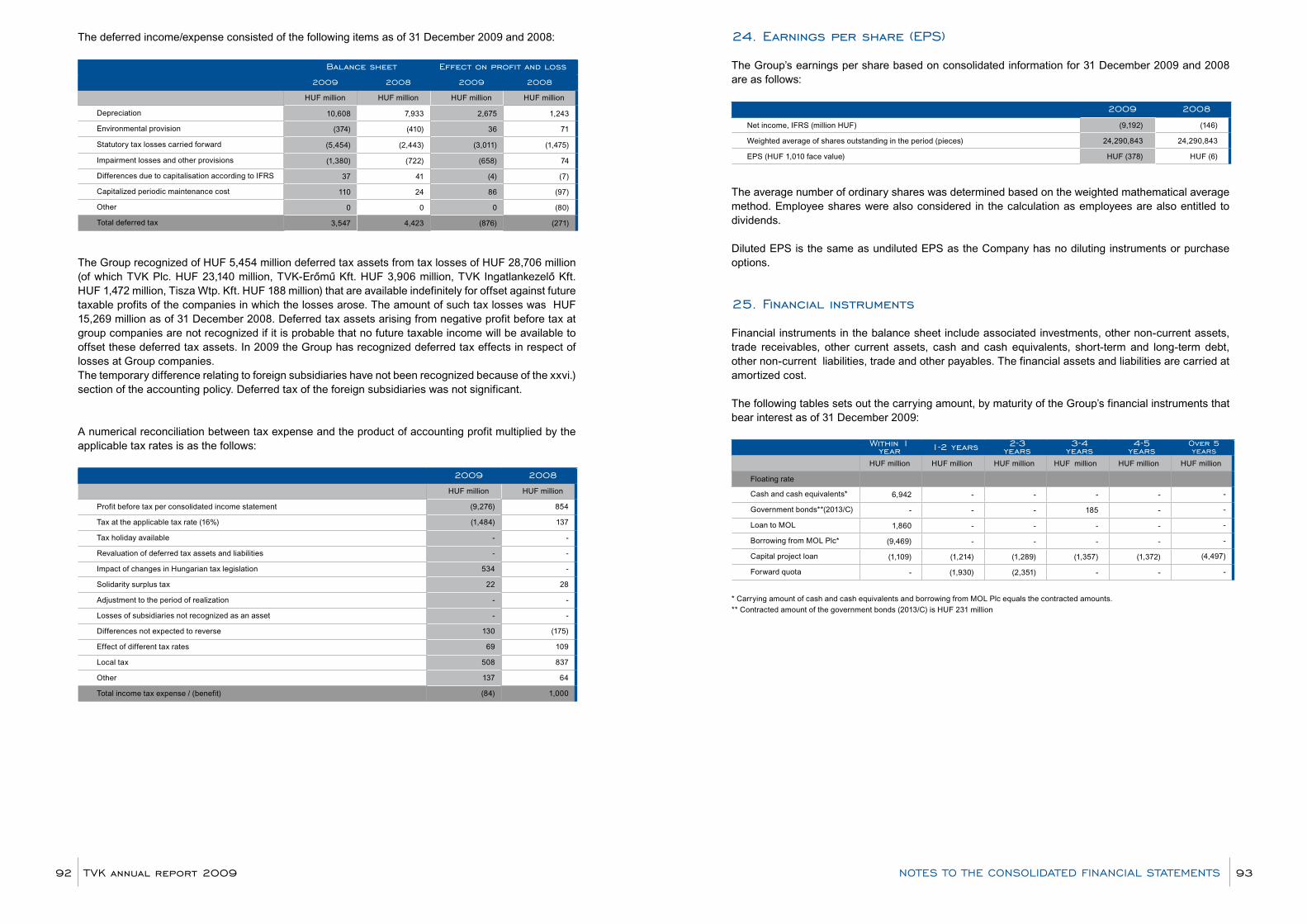

net profit

Consolidated net income (loss) for the period in totaled at HUF 9,192 million. Earnings per share (EPS) decreased to a HUF -378, compared to HUF -6 last year value.

net asset position

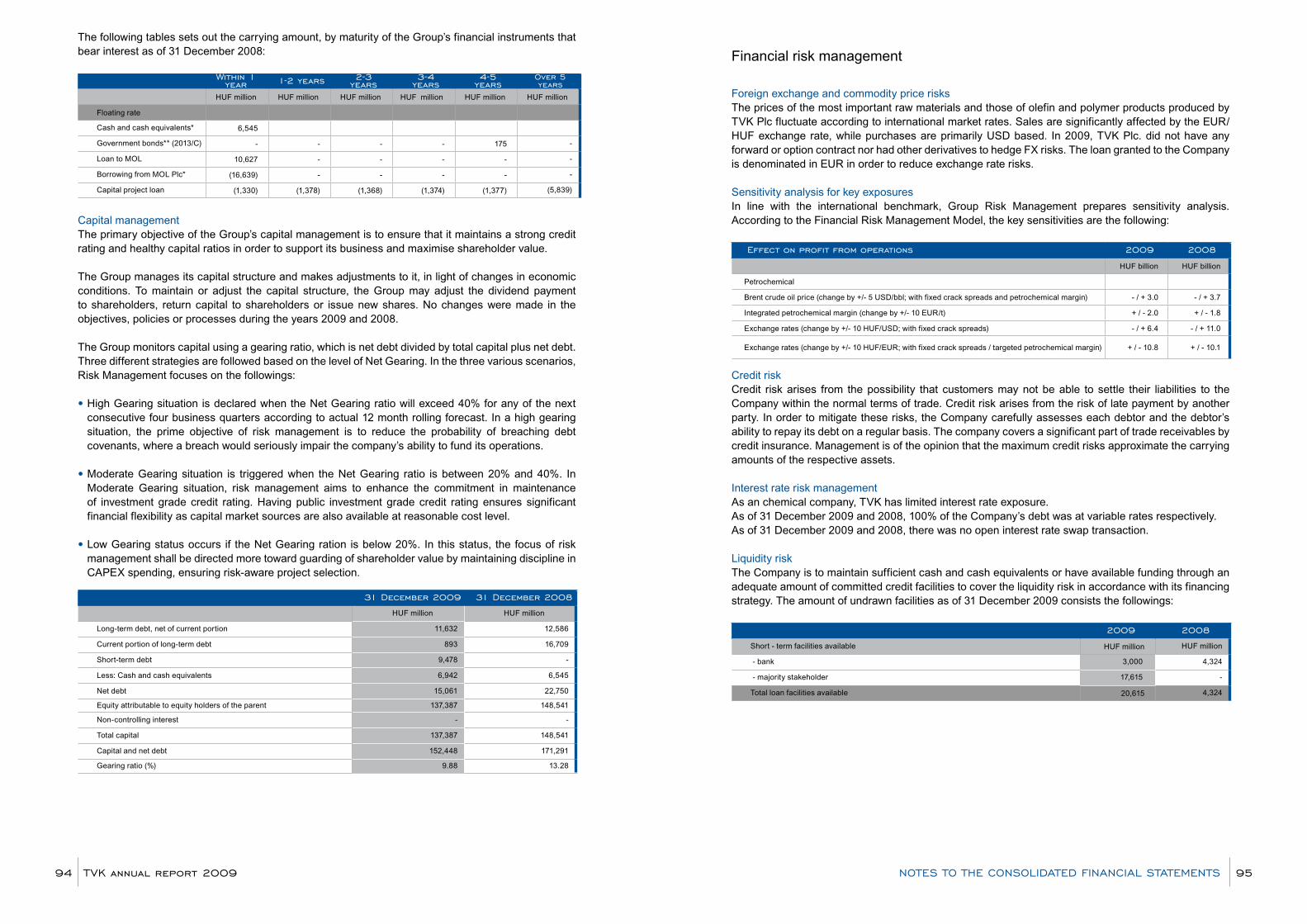

The value of the total assets of TVK Group stood at HUF 211,404 million as at December 31, 2009.

The consolidated value of non-current assets amounted to HUF 136,963 million as at December 31, 2009, 3% lower than on December 31, 2008 mainly due to the lower value - attributable to recognized depreciation - of tangible and intangible assets.

Current assets increased by 9% to HUF 74,441 million. Within the current assets inventories rose by 10% compared to the previous year. Self-manufactured inventories appreciated because of the purchase costs resulting from high feedstock prices, despite of the significant reduction of polymer finished product inventory, whereas olefin feedstock quantity increased slightly. The value of accounts receivable increased by 17% compared to the previous year due to the significant increase of polymer selling prices and of the polymer quantities sold, taking into consideration the last two months affecting the changes in the accounts receivable. The amount of other current assets dropped by 14% due to the reduction of the revolving loan extended to the mother company, which was slightly mitigated by the increase of VAT receivable.

Financial position

The portfolio of long term debts on December 31, 2009 was by about 8% lower than on December 31, 2008 and amounted to HUF 11,632 million and includes only the long term loans recorded in the books of the subsidiaries. The other long term liabilities at December 31, 2009 were HUF 4,288 million coming from forward transactions.

The value of short term liabilities rose by 26% to HUF 52,254 million between December 31, 2008 and December 31, 2009. The reason of the increase is the revolving credit concluded with the mother company and the higher accounts payable due to the increase of the price and quantity of the feedstock purchased for the olefin plant in December, compared to the lower price and quantity purchased in December of the previous year.

EBIT

Net financial loss was HUF 1,695 million

Tax liability

Earnings per share

Total assets

Non-current assets

Current assets

Long term debts on December 31, 2009 was lower by 8% y-o-y

Short term liabilities rose by 26% between December 31, 2008 and December 31, 2009

TVK annual report 200936 37ManaGeMenT DISCuSSIon anD analySIS oF THe reSulTS

A reducing element was that last December the installments of the long-term credits were not yet transferred within the year, which was terminated at the end of this year. From the mother company loan debt in the amount of EUR 50 million TVK repaid EUR 15 million until December 31, thus as at December 31 the credits dropped to EUR 35 million.

owner’s equity, registered Capital, Capital reserves and retained earnings

Shareholder’s equity amounted to HUF 137,387 million on December 31, 2009, by about 8% lower than on December 31, 2008. The decrease is attributable to the variance in the value of the profit/loss after taxation and the paid dividend. Share capital did not change, amounted to HUF 24,534 million.

Cash flow

Based on the group level cash flow statement of TVK dated December 31, 2009 liquid assets have increased by HUF 383 million since the beginning of the year.

The operating cash flow amounted to HUF 4,855 million increased by EBITDA by HUF 5,099 million, and changes in working capital (inventories, trade accounts receivable and payable, other receivables and short term liabilities altogether) increased it by HUF 3,489 million. Within the variance of the working capital, the cash flow deteriorating effect of the changes in the inventory originate from the substantial growth of the olefin plant feedstock prices - which determine the inventory prime cost - since December 2008 leading to inventory appreciation. The fact that the volume of polymer own produced inventories decreased considerably while olefin product inventories decreased modestly, could only mitigate this in part. The reason of the increase of accounts receivable was that during the year 2009 the sales prices and sales volumes in the last two months of the 4th quarter of 2009 were higher than in the last two months of the 4th quarter of 2008 (which determine the year-end accounts receivable). It led to the growth of accounts payable that the purchase price and the purchased quantity of olefin feedstock were both higher in December 2009 than in December 2008. As regards other receivables, mainly the increased amount of the refundable VAT, corporate tax and other taxes decreased the cash flow. Other short term liabilities decreased the operating cash flow due to the drop of the balance of accrued costs. The adjustment due to the non-cash effects included in the EBIT decreased the operating cash flow by HUF 2,023 million: within this the revaluation of inventories in January decreased the cash flow by HUF 394 million, the cancellation of the sale of CO2 quota from the operating cash flow decreased it by HUF 962 million, the changes in provisions decreased it by HUF 692 million and the non-realized loss on revaluation of accounts payable/accounts receivable decreased it by HUF 84 million. Taxes paid against the profit/loss further reduced the cash flow by HUF 1,710 million.

Investment activity increased the cash flow by HUF 7,074 million. An amount of HUF 8,639 million was used for the purchase of tangible and intangible assets, an income of HUF 1,582 million was realized on the sale of tangible assets and the interest received improved the cash position by HUF 584 million. The loan repaid by the mother company and the exchange rate

difference thereof increased the cash flow by HUF 9,262 million. Forward transactions generated HUF 4,283 million.

Net cash from financial operations decreased cash flow by HUF 11,546 million in the examined period reflecting the cash flow decreasing effect of the repayment of loans reclassified as short term loans, of the paid interests and financial expenses furthermore of the paid dividend.

Capital expenditure

In the year 2009 the total capital expenditure of TVK group reached HUF 8,223 million, including CAPEX and refurbishment projects by the mother company of HUF 8,137 million. Within this, the reconstruction of the Olefin-1 represents HUF 3,184 million, sustain CAPEX HUF 3,029 million and the periodic maintenance HUF 996 million.

The strict cost reduction program launched to compensate the negative impact of the general economic downturn protracting to the year of 2009 has basically determined the nature and content of our annual project development and project implementation activities.

Instead of a low number but high-value technology and production development projects (like the processing of olefin by-products) we deliberately concentrated on projects aimed at the efficiency improvement of petrochemical production, at the diversification of our product portfolio, at the management of operational safety and of the risks jeopardizing health and environment.

organizational and personnel Changes, employees

There was no major change occurring in the company structure in 2009.

During 2009 there was the following change in the senior management: from October 1, 2009 Krisztina Petrényi Szabó is the Polymer Marketing and Sales director, deputy CEO of TVK Plc. Mr László Piry has worked as Polymer Marketing and Sales director between 7 June 2004 and 30 September 2009. Mrs. Petrényi does not hold any TVK shares.

As at December 31, 2009 the total consolidated headcount of TVK-group included 1,167 full time employees, 3 persons less than the closing headcount on December 31, 2008. Within this, the headcount of the TVK-parent company did not change, while the number of employees at the subsidiaries decreased by 3 because TVK-UK Ltd. discontinued its activity as of the end of June.

Headcount

Full Time employees December 31, 2008 December 31, 2009Corporate level 1,139 1,139

Group level 1,170 1,167

Operating cash flow

TVK repaid EUR 15 million from the mother company loan until the year end

Total CAPEX reached to HUF 8,223 million

Strict cost reduction program

Projects aimed efficiency improvement, diversification of product portfolio and safety operation

Organization

Employment

Investment activity

Financial cash flow

TVK annual report 200938 39ManaGeMenT DISCuSSIon anD analySIS oF THe reSulTS

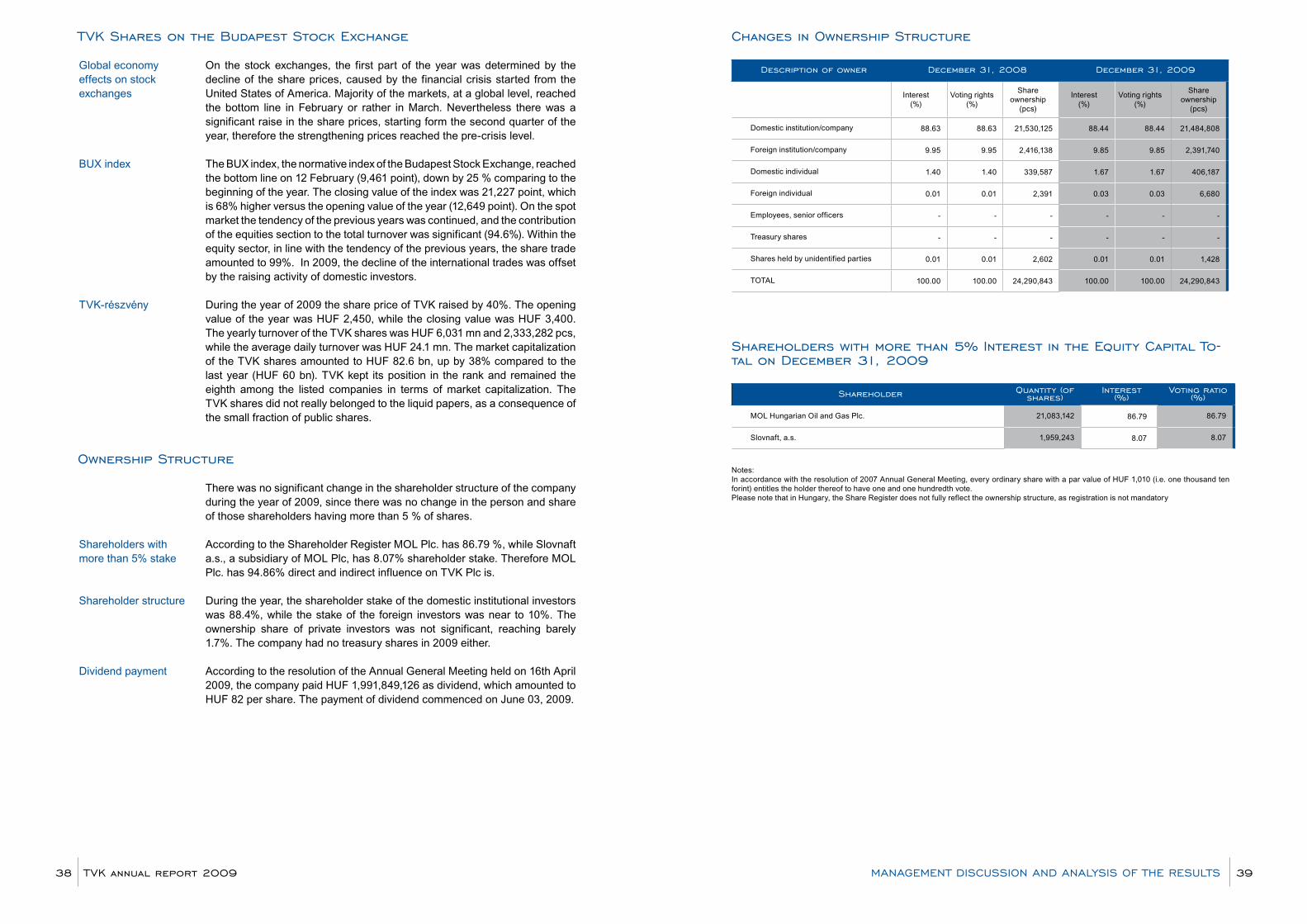

TVK Shares on the Budapest Stock exchange

On the stock exchanges, the first part of the year was determined by the decline of the share prices, caused by the financial crisis started from the United States of America. Majority of the markets, at a global level, reached the bottom line in February or rather in March. Nevertheless there was a significant raise in the share prices, starting form the second quarter of the year, therefore the strengthening prices reached the pre-crisis level.

The BUX index, the normative index of the Budapest Stock Exchange, reached the bottom line on 12 February (9,461 point), down by 25 % comparing to the beginning of the year. The closing value of the index was 21,227 point, which is 68% higher versus the opening value of the year (12,649 point). On the spot market the tendency of the previous years was continued, and the contribution of the equities section to the total turnover was significant (94.6%). Within the equity sector, in line with the tendency of the previous years, the share trade amounted to 99%. In 2009, the decline of the international trades was offset by the raising activity of domestic investors.

During the year of 2009 the share price of TVK raised by 40%. The opening value of the year was HUF 2,450, while the closing value was HUF 3,400. The yearly turnover of the TVK shares was HUF 6,031 mn and 2,333,282 pcs, while the average daily turnover was HUF 24.1 mn. The market capitalization of the TVK shares amounted to HUF 82.6 bn, up by 38% compared to the last year (HUF 60 bn). TVK kept its position in the rank and remained the eighth among the listed companies in terms of market capitalization. The TVK shares did not really belonged to the liquid papers, as a consequence of the small fraction of public shares.

ownership Structure

There was no significant change in the shareholder structure of the company during the year of 2009, since there was no change in the person and share of those shareholders having more than 5 % of shares.

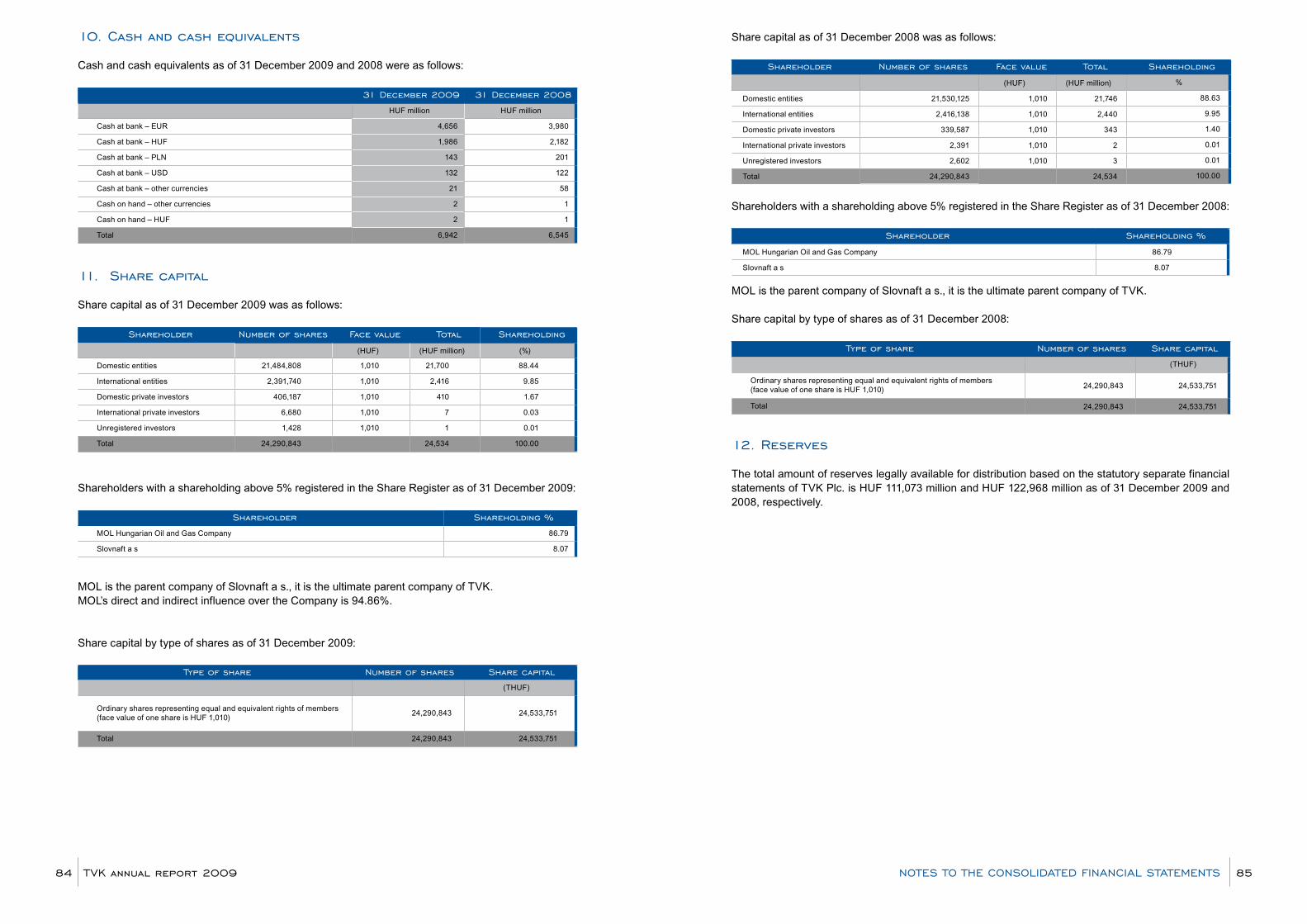

According to the Shareholder Register MOL Plc. has 86.79 %, while Slovnaft a.s., a subsidiary of MOL Plc, has 8.07% shareholder stake. Therefore MOL Plc. has 94.86% direct and indirect influence on TVK Plc is.

During the year, the shareholder stake of the domestic institutional investors was 88.4%, while the stake of the foreign investors was near to 10%. The ownership share of private investors was not significant, reaching barely 1.7%. The company had no treasury shares in 2009 either.

According to the resolution of the Annual General Meeting held on 16th April 2009, the company paid HUF 1,991,849,126 as dividend, which amounted to HUF 82 per share. The payment of dividend commenced on June 03, 2009.

TVK-részvény

Shareholders with more than 5% stake

Shareholder structure

Dividend payment

BUX index

Global economy effects on stock exchanges

Changes in ownership Structure

Description of owner December 31, 2008 December 31, 2009

Interest (%)

Voting rights (%)

Share ownership

(pcs)

Interest (%)

Voting rights (%)

Share ownership

(pcs)

Domestic institution/company 88.63 88.63 21,530,125 88.44 88.44 21,484,808

Foreign institution/company 9.95 9.95 2,416,138 9.85 9.85 2,391,740

Domestic individual 1.40 1.40 339,587 1.67 1.67 406,187

Foreign individual 0.01 0.01 2,391 0.03 0.03 6,680

Employees, senior officers - - - - - -

Treasury shares - - - - - -

Shares held by unidentified parties 0.01 0.01 2,602 0.01 0.01 1,428

TOTAL 100.00 100.00 24,290,843 100.00 100.00 24,290,843

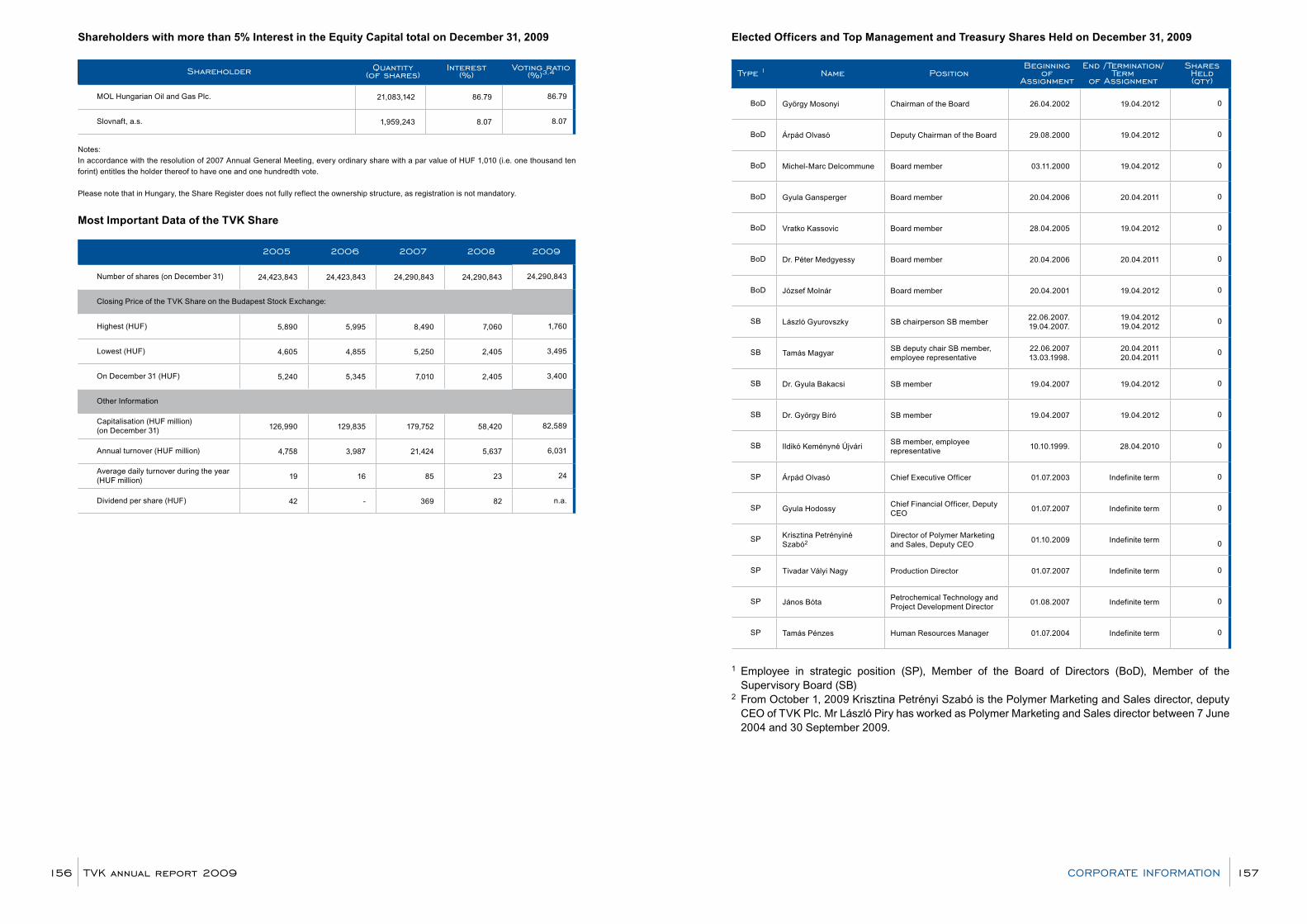

Shareholders with more than 5% Interest in the equity Capital To-tal on December 31, 2009

Shareholder Quantity (of shares)

Interest (%)

Voting ratio (%)

MOL Hungarian Oil and Gas Plc. 21,083,142 86.79 86.79

Slovnaft, a.s. 1,959,243 8.07 8.07

Notes: In accordance with the resolution of 2007 Annual General Meeting, every ordinary share with a par value of HUF 1,010 (i.e. one thousand ten forint) entitles the holder thereof to have one and one hundredth vote.Please note that in Hungary, the Share Register does not fully reflect the ownership structure, as registration is not mandatory

Tisza Chemical Group public limited Company and Subsidiaries

Consolidated financial statements pre-pared in accordance with International Financial reporting Standards together with the independent auditors’ report

31 december 2009

TVK annual report 200940 41ConSolIDaTeD FInanCIal STaTeMenTS

Opinion7.) We have audited the elements of and disclosures in the consolidated annual financial statements, along with underlying records and supporting documentation, of Tiszai Vegyi Kombinát Nyilvánosan Működő Részvénytársaság in accordance with Hungarian National Auditing Standards and have gained sufficient and appropriate evidence that the consolidated annual financial statements have been prepared in accordance with the International Financial Reporting Standards as adopted by EU. In our opinion the consolidated annual financial statements give a true and fair view of the equity and financial position of Tiszai Vegyi Kombinát Nyilvánosan Működő Részvénytársaság as at 31 December 2009 and of the results of its operations for the year then ended. The consolidated business report corresponds to the disclosures in the consolidated financial statements.

8.) Without qualifying our opinion we draw the attention to Note 26 to the consolidated financial statements that describe the environmental aspects of the Company’s operations and highlights the risk of additional significant decontamination expenses that might incur over the current amount of the provision in relation to past environmental damage as may be identified by future environmental surveys.

Budapest, 11 March 2010

Szilágyi JuditErnst & Young Kft. Registered AuditorRegistration No. 001165 Chamber membership No.: 001368

TVK annual report 200942 43

Független Könyvvizsgálói Jelentés

InDepenDenT auDITorS’ reporT

To the Shareholders of Tiszai Vegyi Kombinát Nyilvánosan Működő Részvénytársaság1.) We have audited the accompanying 2009 consolidated annual financial statements of Tiszai Vegyi Kombinát Nyilvánosan Működő Részvénytársaság (“the Company”), which comprises the consolidated balance sheet as at 31 December 2009 - showing a balance sheet total of HUF 211,404 million and a loss for the year of HUF 9,192 million -, the related consolidated income statement, consolidated statement of comprehensive income, consolidated statement of changes in equity, consolidated cash flows for the year then ended and the summary of significant accounting policies and other explanatory notes.

2.) We issued an unqualified opinion on the Company’s consolidated annual financial statements prepared in accordance with the International Financial Reporting Standards as adopted by EU as at 31 December 2008 on 20 March 2009.

Management’s Responsibility for the Consolidated Financial Statements3.) Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with the International Financial Reporting Standards as adopted by EU. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s Responsibility4.) Our responsibility is to express an opinion on these consolidated financial statements based on the audit and to assess whether the consolidated business report is consistent with the consolidated financial statements. We conducted our audit in accordance with Hungarian National Auditing Standards and with applicable laws and regulations in Hungary. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the consolidated financial statements are free from material misstatement.

5.) An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. Our work regarding the consolidated business report is restricted to assessing whether the consolidated business report is consistent with the consolidated financial statements and does not include reviewing other information originated from non-audited financial records.

6.) We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Independent auditors’ report