Embed Size (px)

Citation preview

©2009 McGraw-Hill Ryerson Limited1 of 23

1818Dividend Policy and Retained

Earnings

Dividend Policy and Retained

Earnings

Prepared by:

Michel PaquetSAIT Polytechnic

©2009 McGraw-Hill Ryerson Limited

©2009 McGraw-Hill Ryerson Limited2 of 23

Chapter 18 - Outline

• Dividends vs. Retained Earnings

• Theories of Dividend Policy

• Dividend Policy in Practice

• Other Factors Influencing Dividend Policy

• Alternatives to Cash Dividend

• Summary and Conclusions

©2009 McGraw-Hill Ryerson Limited3 of 23

Learning Objectives

1. Discuss management’s decision criteria as to whether internally generated funds should be re-invested or paid out as dividends. (LO1)

2. Describe a dividend payment as a passive or active decision based on investor preference and the informational content of dividends. Calculate dividend payout ratios and dividend yields. (LO2)

©2009 McGraw-Hill Ryerson Limited4 of 23

Learning Objectives

3. Outline the factors to be considered in dividend policy. Calculate aftertax income from dividends and calculate share prices based on earnings multiples. (LO3)

4. Outline dividend payment procedures. (LO4)

5. Describe the effect of stock splits and stock dividends on the position of the shareholders. Calculate the changes in the balance sheet that result. (LO5)

©2009 McGraw-Hill Ryerson Limited5 of 23

Learning Objectives

6. Discuss the reasons for a share repurchase. (LO6)

7. Explain a dividend reinvestment plan. (LO7)

©2009 McGraw-Hill Ryerson Limited6 of 23

Dividends vs. Retained Earnings• A company has a choice or decision regarding what to

do with its profits:– Pay them out to shareholders as

OR– Retain the earnings in the business

• There is disagreement as to whether investors prefer dividends or reinvestment

LO1

©2009 McGraw-Hill Ryerson Limited7 of 23

Theories of Dividend Policy

1. Irrelevance of Dividend Policy

• Proposition: under ideal conditions, dividend policy is irrelevant and doesn’t affect share price.

• Logic: shareholders can create dividends on their own – – homemade dividends.

LO1

©2009 McGraw-Hill Ryerson Limited8 of 23

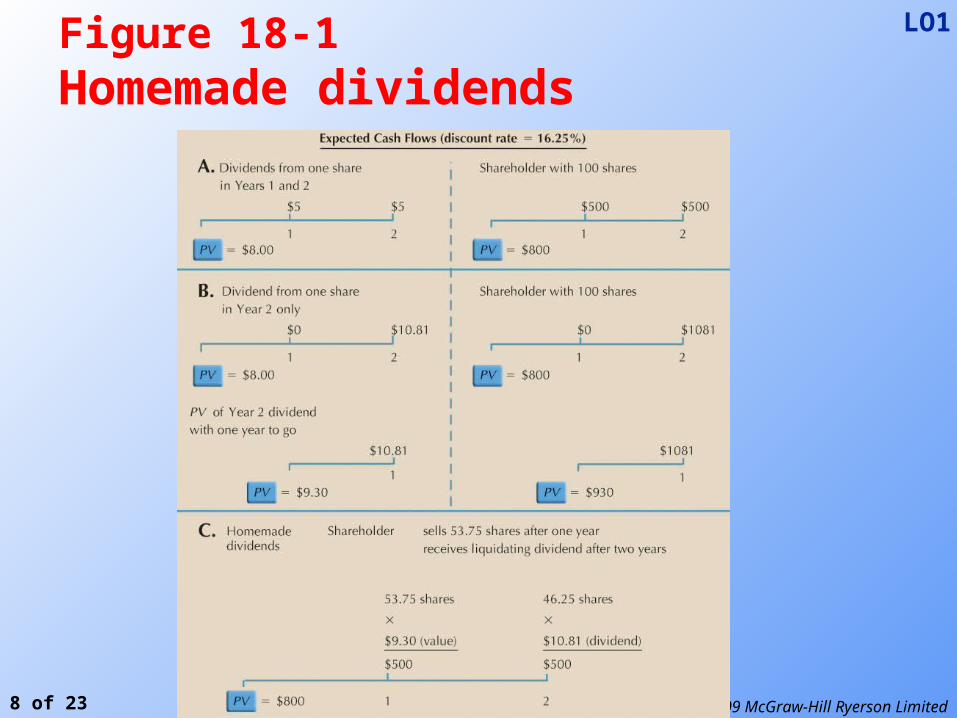

Figure 18-1Homemade dividends

LO1

©2009 McGraw-Hill Ryerson Limited9 of 23

Theories of Dividend Policy

2. Relevance of Dividend PolicyProposition: dividend policy is relevant and a positive relationship exists between dividends and share price because

a) dividends resolve uncertainty andb) dividends have information content – The corporate

is saying it had a good year.

As the real world is not perfect, dividend policy seems to be relevant.

LO1

©2009 McGraw-Hill Ryerson Limited10 of 23

Dividend Policy in Practice

• Cash dividends are usually paid quarterly, but annual dividend is used to calculate

• Payout Ratio =

Dividend per Share/Earnings per Share

• Dividend Yield =

Dividend per Share/Current Stock Price

LO2

©2009 McGraw-Hill Ryerson Limited11 of 23

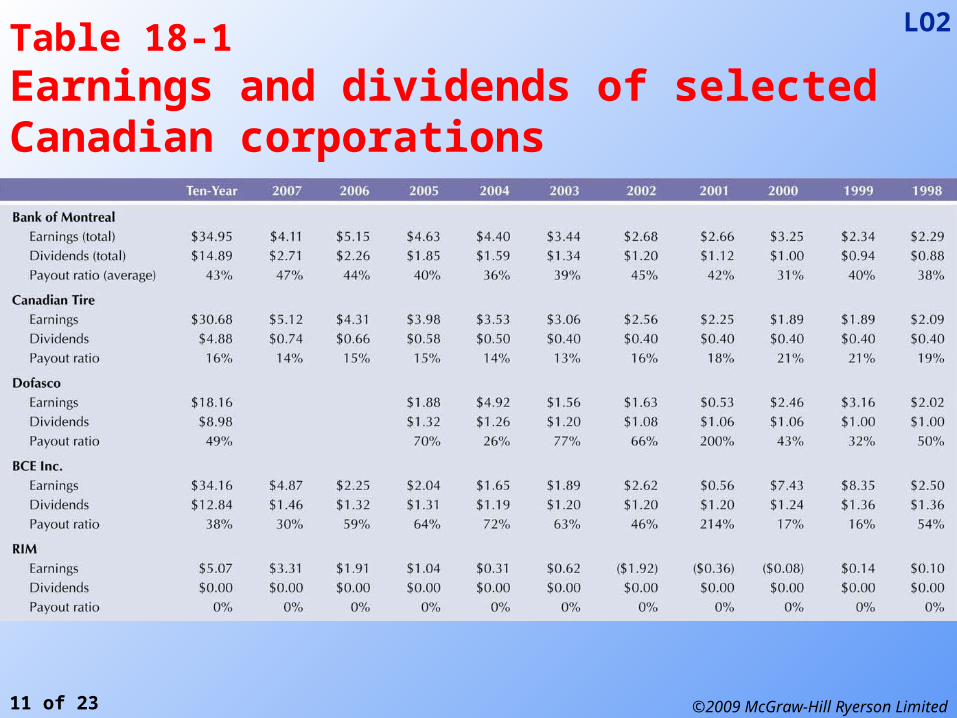

LO2Table 18-1Earnings and dividends of selected Canadian corporations

©2009 McGraw-Hill Ryerson Limited12 of 23

Dividend Policy in Practice1. Dividend Stability

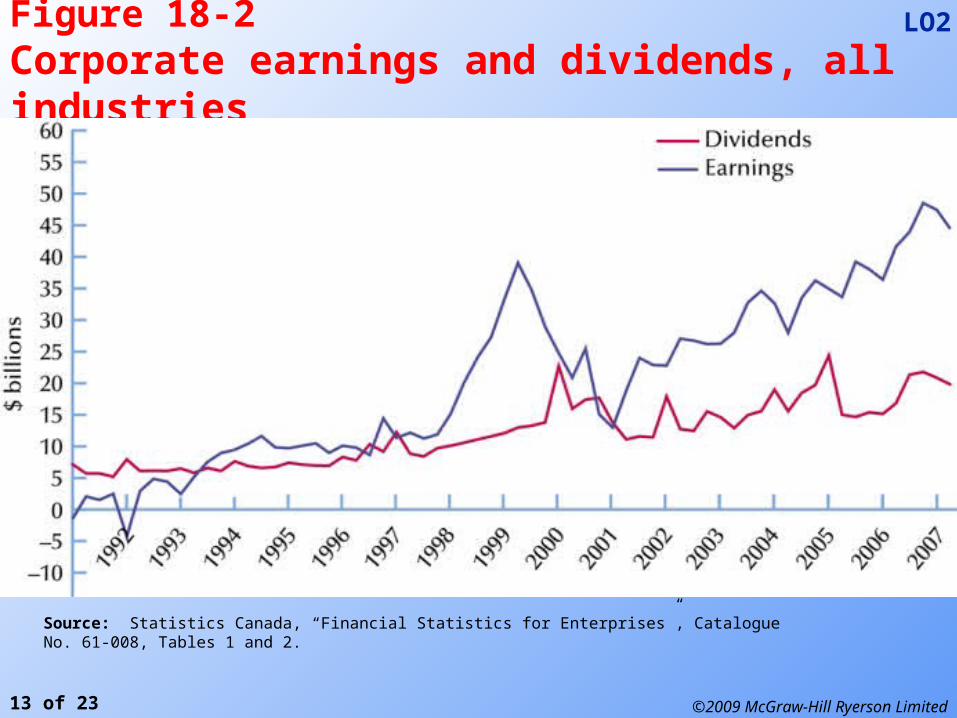

• Compared with volatile earnings, dividends are much more stable and predictable (Figure 18-2).

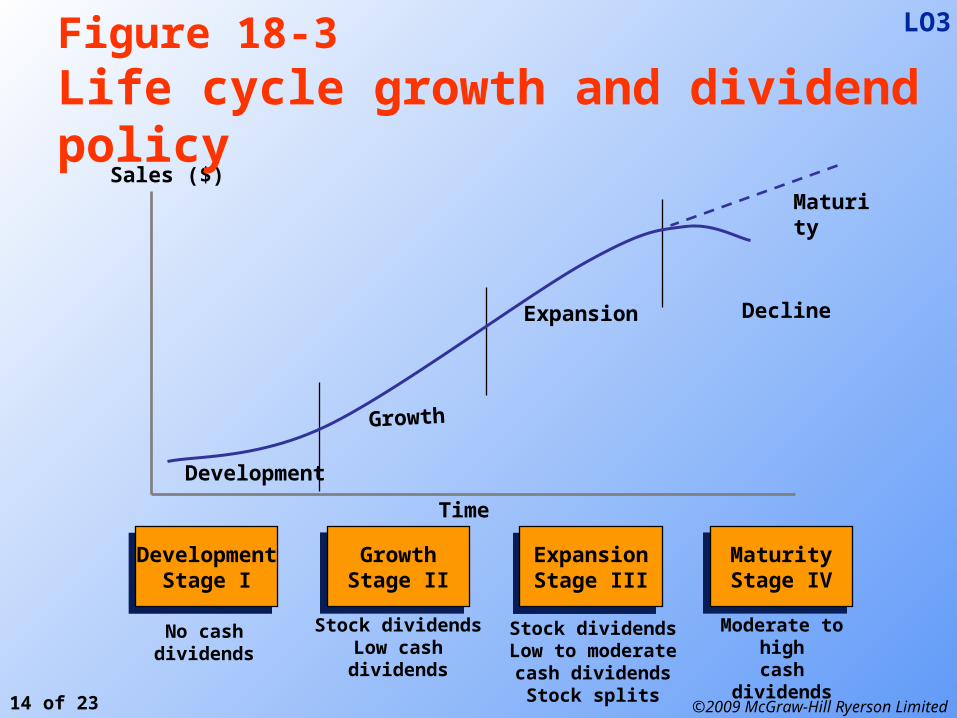

2. Life Cycle Growth and Dividends• Dividend policy is reflected in 4 stages (Figure 18-3):

Stage I - Development– no cash dividends

Stage II - Growth– stock dividends, low cash dividends

Stage III - Expansion– stock dividends, moderate cash dividends, stock splits

Stage IV - Maturity– moderate to high cash dividends

LO2

©2009 McGraw-Hill Ryerson Limited13 of 23

Figure 18-2Corporate earnings and dividends, all industries

LO2

Source: Statistics Canada, “Financial Statistics for Enterprises”, Catalogue No. 61-008, Tables 1 and 2.

©2009 McGraw-Hill Ryerson Limited14 of 23

DevelopmentStage I

DevelopmentStage I

GrowthStage II

GrowthStage II

ExpansionStage III

ExpansionStage III

MaturityStage IV

MaturityStage IV

No cash dividends Stock dividendsLow cash dividends

Stock dividendsLow to moderate

cash dividendsStock splits

Moderate to highcash dividends

Sales ($)

Development

Expansion

Maturity

Decline

Time

Growth

Figure 18-3Life cycle growth and dividend policy

LO3

©2009 McGraw-Hill Ryerson Limited15 of 23

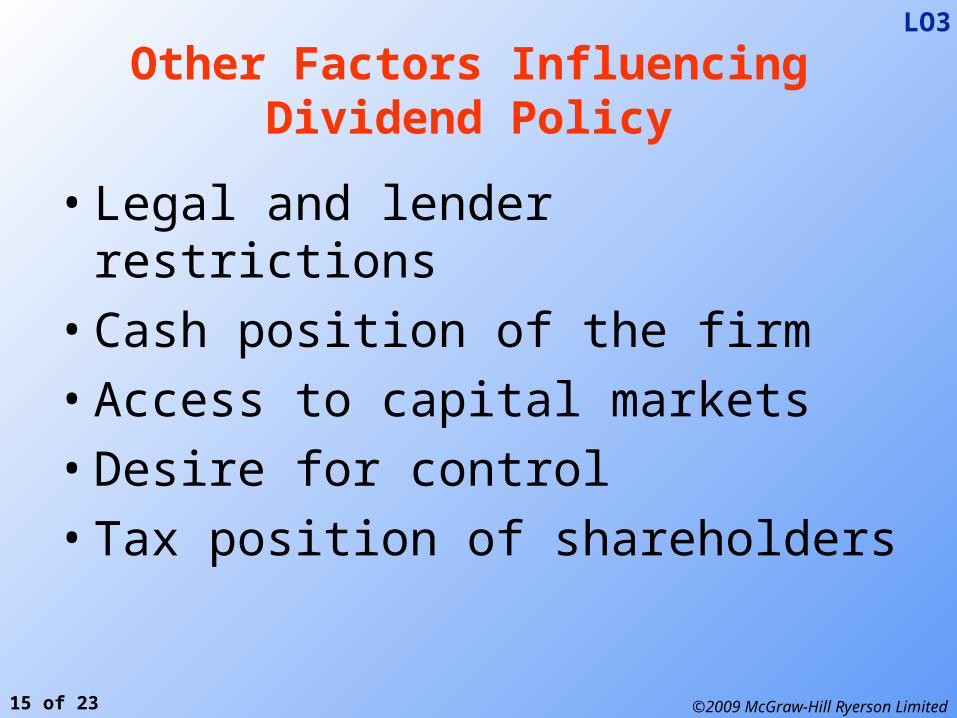

Other Factors Influencing Dividend Policy

• Legal and lender restrictions

• Cash position of the firm

• Access to capital markets

• Desire for control

• Tax position of shareholders

LO3

©2009 McGraw-Hill Ryerson Limited16 of 23

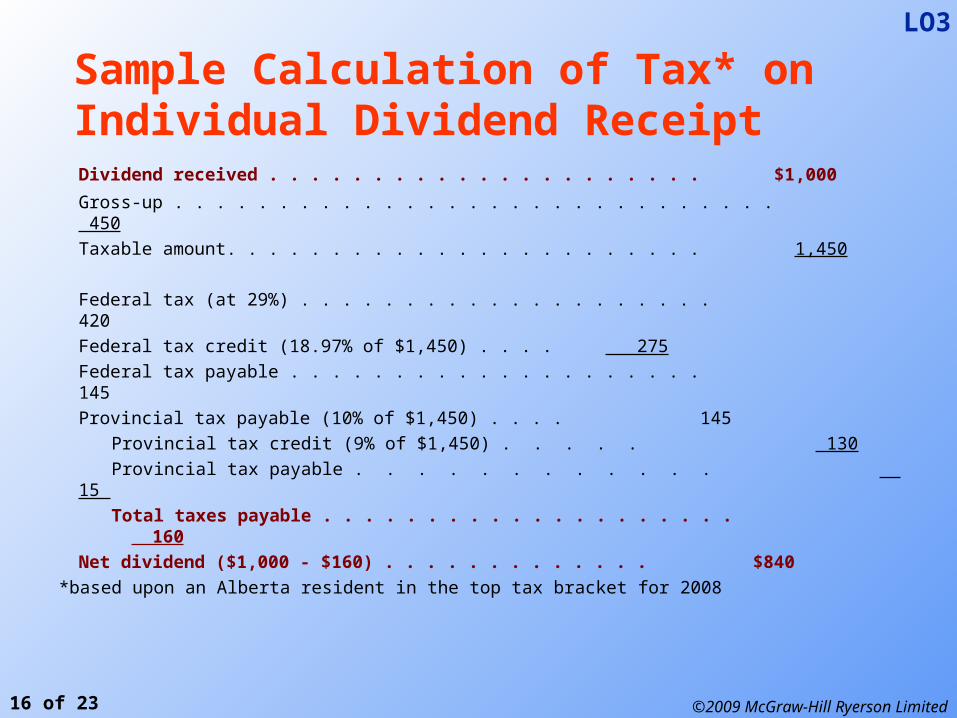

Sample Calculation of Tax* on Individual Dividend Receipt

Dividend received . . . . . . . . . . . . . . . . . . . . . $1,000

Gross-up . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 450

Taxable amount. . . . . . . . . . . . . . . . . . . . . . . 1,450

Federal tax (at 29%) . . . . . . . . . . . . . . . . . . . . 420

Federal tax credit (18.97% of $1,450) . . . . 275

Federal tax payable . . . . . . . . . . . . . . . . . . . . 145

Provincial tax payable (10% of $1,450) . . . . 145

Provincial tax credit (9% of $1,450) . . . . . 130

Provincial tax payable . . . . . . . . . . . . 15

Total taxes payable . . . . . . . . . . . . . . . . . . . . 160

Net dividend ($1,000 - $160) . . . . . . . . . . . . . $840

*based upon an Alberta resident in the top tax bracket for 2008

LO3

©2009 McGraw-Hill Ryerson Limited17 of 23

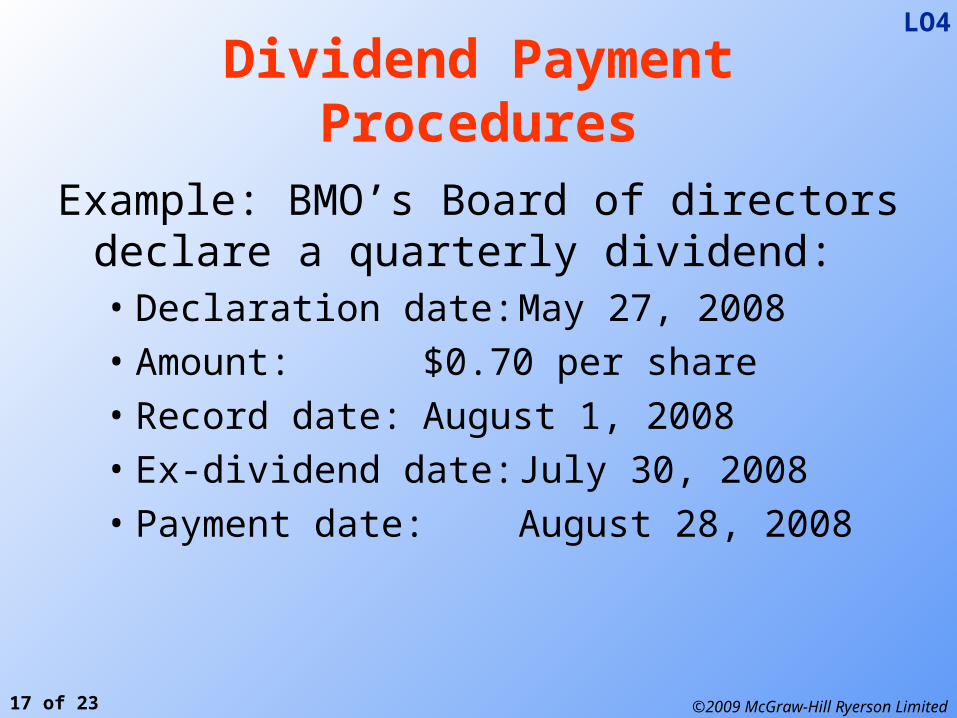

Dividend Payment Procedures

Example: BMO’s Board of directors declare a quarterly dividend:• Declaration date: May 27, 2008• Amount: $0.70 per share• Record date: August 1, 2008• Ex-dividend date: July 30, 2008• Payment date: August 28, 2008

LO4

©2009 McGraw-Hill Ryerson Limited18 of 23

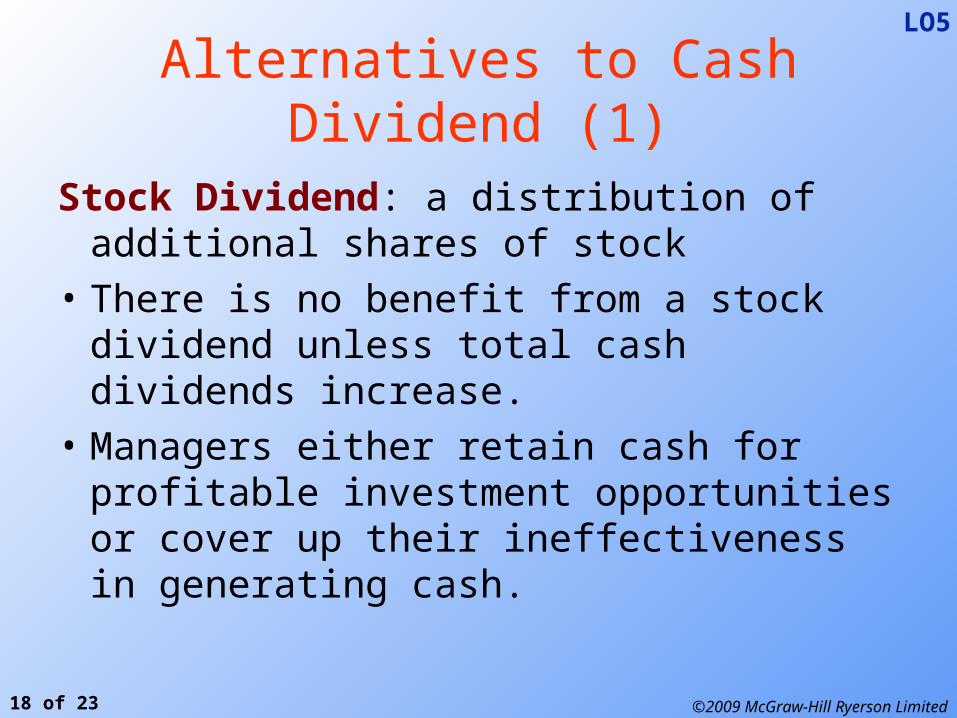

Alternatives to Cash Dividend (1)

Stock Dividend: a distribution of additional shares of stock

• There is no benefit from a stock dividend unless total cash dividends increase.

• Managers either retain cash for profitable investment opportunities or cover up their ineffectiveness in generating cash.

LO5

©2009 McGraw-Hill Ryerson Limited19 of 23

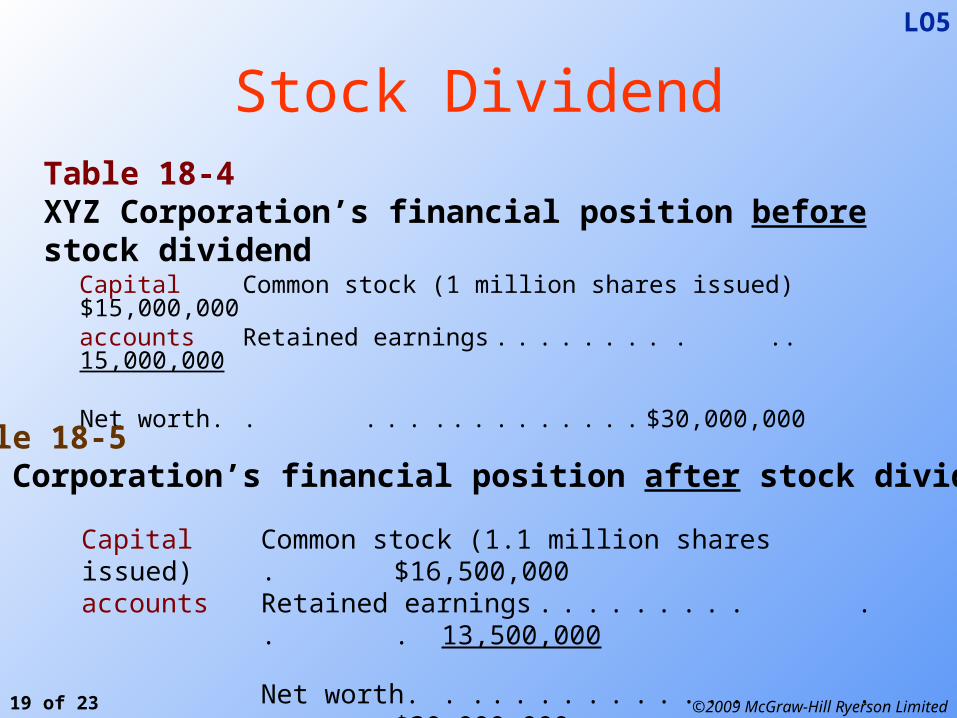

Stock DividendTable 18-4XYZ Corporation’s financial position before stock dividend

Capital Common stock (1 million shares issued) $15,000,000accounts Retained earnings . . . . . . . . . . . 15,000,000

Net worth. . . . . . . . . . . . . . . $30,000,000

Table 18-5XYZ Corporation’s financial position after stock dividend

Capital Common stock (1.1 million shares issued) . $16,500,000accounts Retained earnings . . . . . . . . . . . . 13,500,000

Net worth. . . . . . . . . . . . . . . .$30,000,000

LO5

©2009 McGraw-Hill Ryerson Limited20 of 23

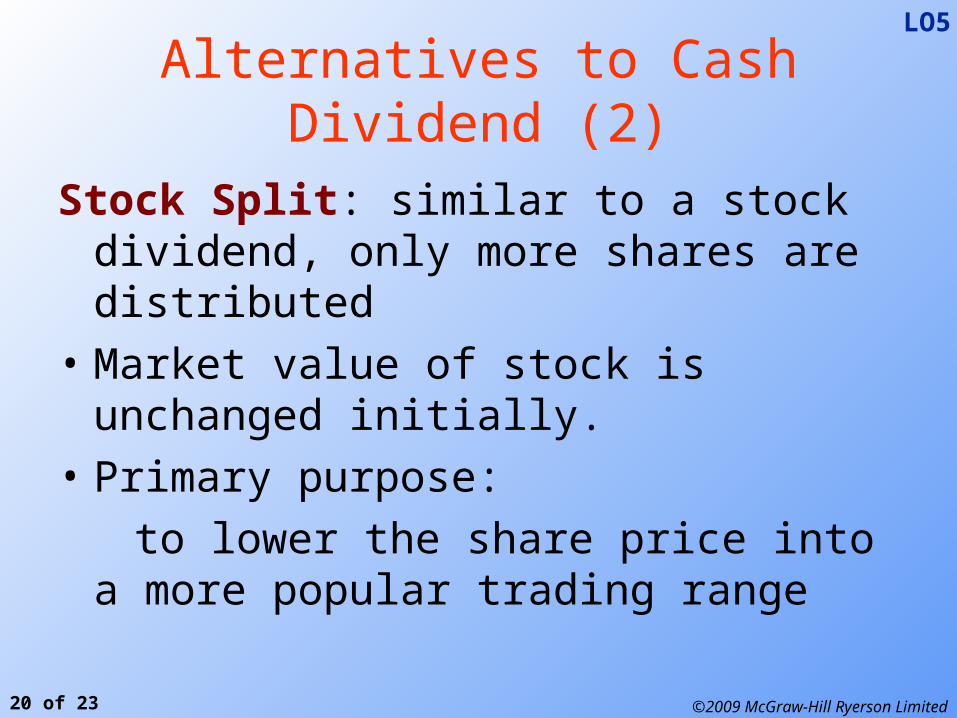

Alternatives to Cash Dividend (2)

Stock Split: similar to a stock dividend, only more shares are distributed

• Market value of stock is unchanged initially.

• Primary purpose:

to lower the share price into a more popular trading range

LO5

©2009 McGraw-Hill Ryerson Limited21 of 23

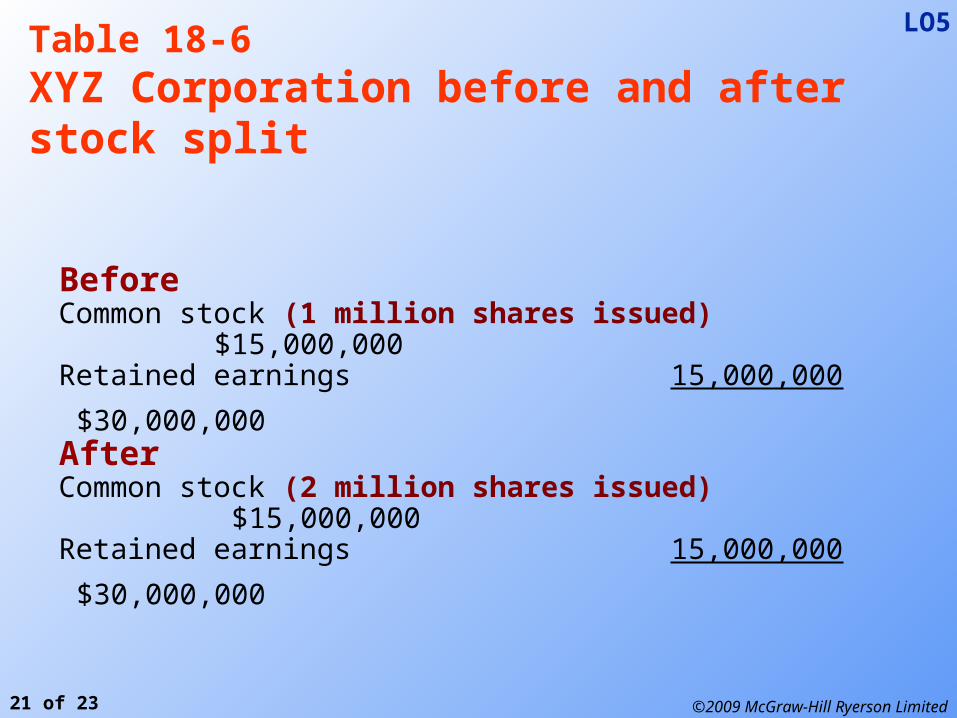

BeforeCommon stock (1 million shares issued) $15,000,000Retained earnings 15,000,000

$30,000,000AfterCommon stock (2 million shares issued) $15,000,000Retained earnings 15,000,000

$30,000,000

Table 18-6XYZ Corporation before and after stock split

LO5

©2009 McGraw-Hill Ryerson Limited22 of 23

Alternatives to Cash Dividend (3)

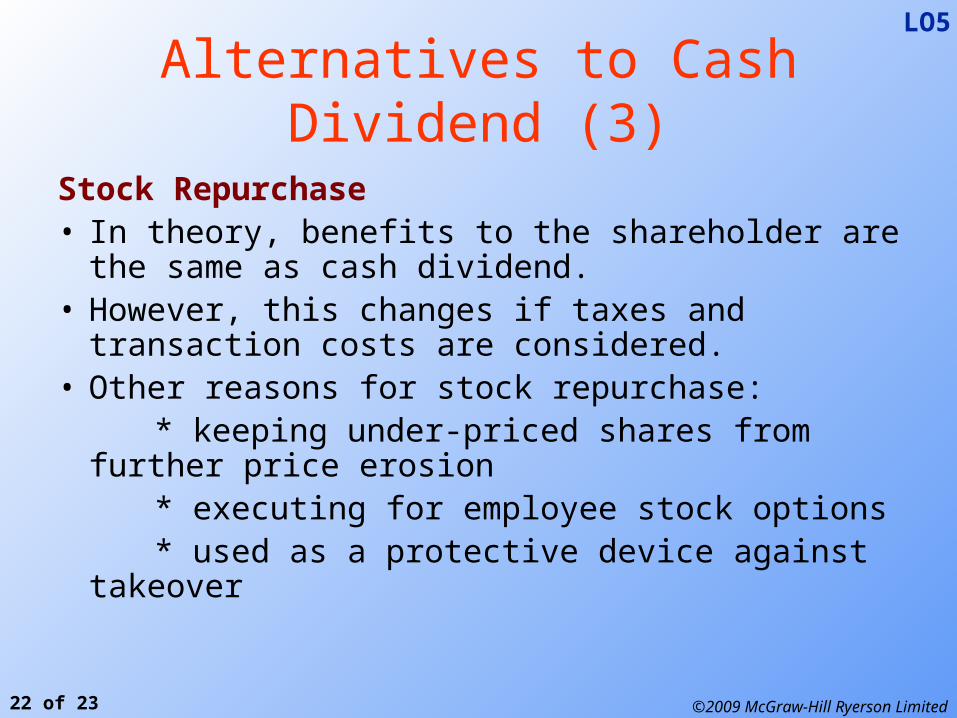

Stock Repurchase• In theory, benefits to the shareholder are the same as

cash dividend.• However, this changes if taxes and transaction costs

are considered.• Other reasons for stock repurchase: * keeping under-priced shares from further price erosion * executing for employee stock options * used as a protective device against takeover

LO5

©2009 McGraw-Hill Ryerson Limited23 of 23

Summary and Conclusions

• A profitable company must decide whether to retain (reinvest) earnings or to pay a cash dividend.

• Dividend policy relevance theory seems to be valid in our imperfect world.

• Two measures of dividend policy are payout ratio and dividend yield.

• Dividend stability is related to information content of dividend.

• Dividend policy changes as a firm goes through life cycle.• Shareholders’ preferences and other factors also influence

dividend policy.• Firms also use stock dividend, split and repurchase as

alternatives to cash dividend.