Embed Size (px)

Citation preview

| 1 |

| 2 |

Fedele ConfalonieriChairman

| 3 |

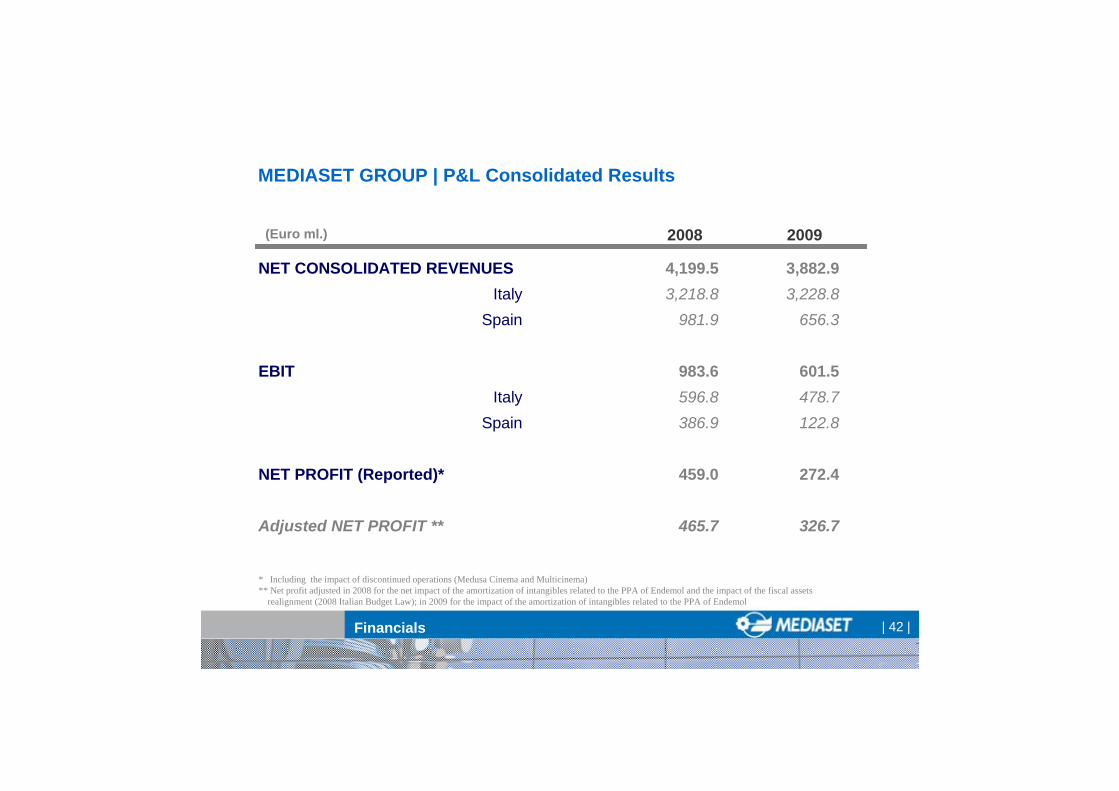

4,199.5

983.6

459.0

0.38

94%

MEDIASET GROUP | P&L Consolidated Results

Net Consolidated Revenues

Operating Profit

Net Profit

Dividend per Share (Euro)

Payout

3,882.9

601.5

272.4

0.22

92%

2008 2009(Euro ml.)

| 4 |

3,218.8

596.8

378.1

MEDIASET ITALIAN BUSINESS | P&L Results

Net Consolidated Revenues

Operating Profit

Net Profit

3,228.8

478.7

269.0

2008 2009(Euro ml.)

| 5 |

981.9

386.9

211.3

TELECINCO | P&L Results

Net Consolidated Revenues

Operating Profit

Net Profit

656.3

122.8

48.4

2008 2009(Euro ml.)

| 6 |

Pier Silvio BerlusconiExecutive Vice Chairman

| 7 |

CHALLENGES FOR BROADCASTERS

1. Few generalist channels

2. Revenues mainly from advertising

3. Broadcasting (no content)

4. Linear offer only

5. Analogue transmission only

1. Audience fragmentation

2. Advertising market maturity

3. Dependence on content providers

4. Technology enabling non-linear offers

5. Digital platforms multiplication

Traditional FTA Challenges

| 8 |

1. Audience fragmentation

2. Advertising market maturity

3. Dependence on content providers

4. Technology enabling non-linear offers

5. Digital platforms development

Challenges

1. Generalist + thematic channels

2. Advertising + Pay TV revenues

3. Broadcasting + vertical integration in content

4. Linear + non linear offer (“On Demand”)

5. Presence on all digital platforms + analogue

MEDIASET STRATEGIC REACTION

Mediaset way to broadcasting

| 9 |

GENERALIST FTA TV

| 10 |

Source: Auditel, 24h, (% audience share)

*2006: Spring 29/1-3/6 excluding 26/2-4/3+Autumn 3/9-2/12 2007: Spring 14/1-2/6 excluding 25/2-3/3+Autumn 9/9-1/12 2008: Spring 13/1-31/5 excluding 24/2-1/3+Autumn 7/9-29/11 2009: Spring 11/1-30/5 excluding 15/2-21/2+Autumn 6/9-5/12 2010 Spring 10/1-13/3 excluding 14-20/2

C5+I1+R4 R1+R2+R3

43.1 43.5 42.9 42.1

39.6

37.636.6

34.9

2006 2007 2008 2009

AUDIENCE SHARE | 2006-2009 Evolution15-64 years, audience guarantee*

| 11 |

MULTICHANNEL FTA TV

| 12 |

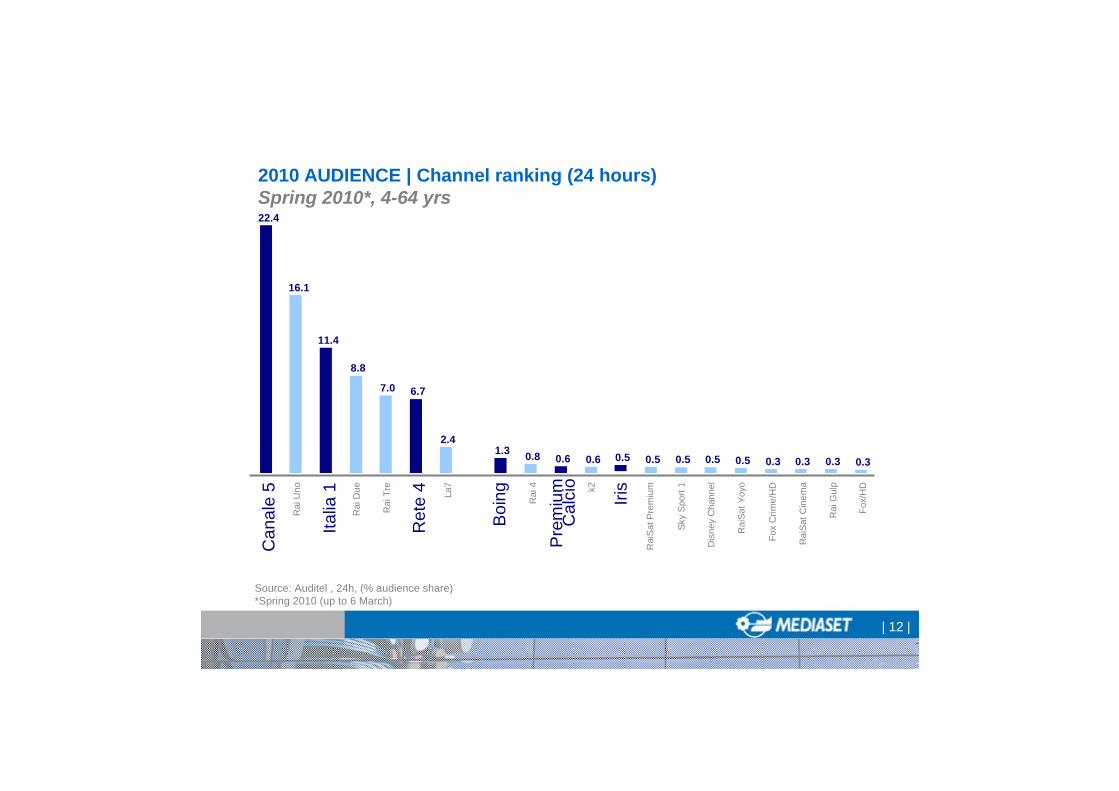

2010 AUDIENCE | Channel ranking (24 hours)Spring 2010*, 4-64 yrs

k2

22.4

16.1

11.4

8.8

7.0 6.7

2.41.3 0.8 0.6 0.6 0.5 0.5 0.5 0.5 0.5 0.3 0.3 0.3 0.3

Can

ale

5R

ai U

no

Italia

1R

ai D

ue

Rai

Tre

Ret

e 4 La7

Boi

ng Rai

4

Iris

Sky

Spo

rt 1

Dis

ney

Cha

nnel

Rai

SatY

oyo

Rai

Sat

Pre

miu

m

Fox

Crim

e/H

D

Rai

Sat

Cin

ema

Rai

Gul

p

Fox/

HD

Source: Auditel , 24h, (% audience share)*Spring 2010 (up to 6 March)

Pre

miu

mC

alci

o

| 13 |

+10.5%

+1.8%

-1.1%

-0.7%

13.1%

83.4%

8.4%

8.2%

Multichannel (RAI+MS)

Total (RAI+MS)

Satellite

Other

-8.7%Generalist (RAI+MS) 70.3%

Spring 2010* Δ vs. 2009*

2010 AUDIENCE | Switch-off impact in “All Digital” areas

“All Digital” Areas: Sardegna, Piemonte, Lazio, Campania, Trentino Alto Adige, Valle D’Aosta*Spring 2010 (up to 6 March)

Spring 2010*, Individuals

| 14 |

1.4%

2.2%

InflationMEDIASET

2001-2009 CAGR

-1.8%

0%

Initial Guidance

MEDIASET

2009

+1%

MEDIASET

2010

Guidance

FTA TV Costs = Personnel costs+operating costs+TV rights amortisations+other D&A+intra-company itemsSource: Istat

FTA TV COSTS | 2001-2009 evolution and 2010 budget

| 15 |

PAY TV

| 16 |

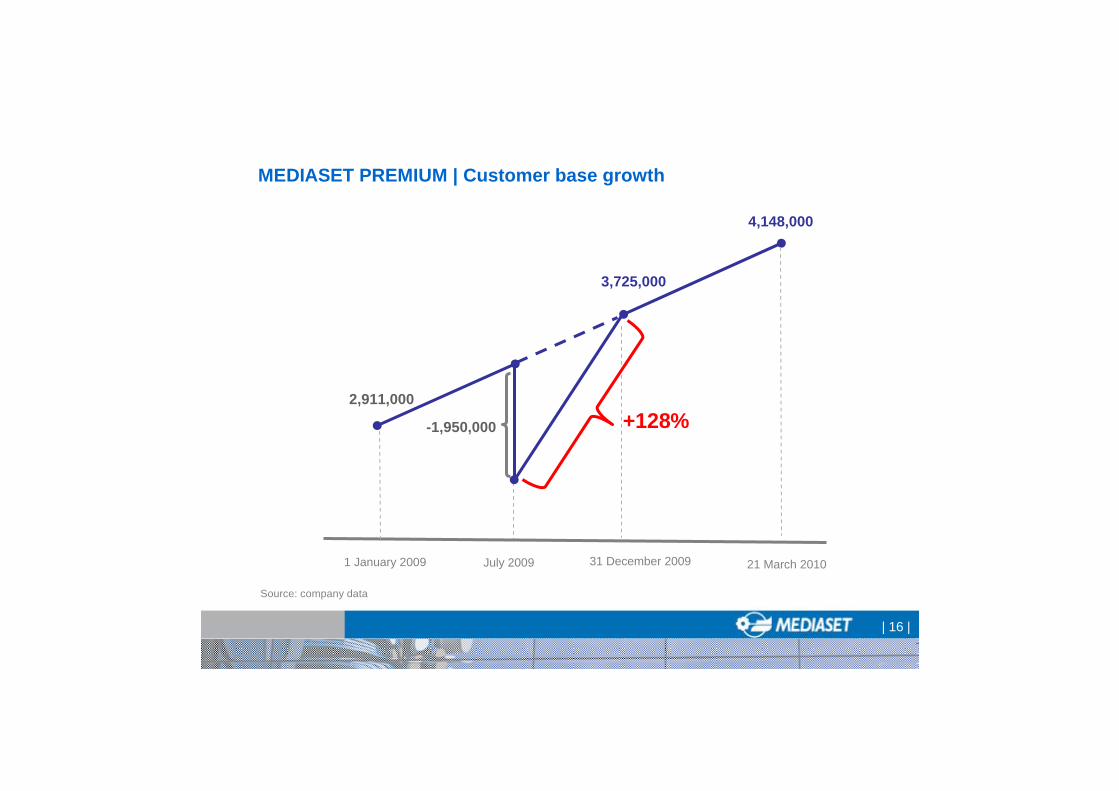

1 January 2009

MEDIASET PREMIUM | Customer base growth

3,725,000

Source: company data

31 December 2009 21 March 2010

4,148,000

July 2009

-1,950,000 +128%2,911,000

| 17 |

2007

MEDIASET PREMIUM | Commercial offer and revenues developmentMio Euro

226 ml €

2008 2009

404 ml €

561 ml €

ARPU 60€ ARPU 80€ ARPU 94€

+38.9%vs. 2008

Pay TV revenues+56.5% vs. 2008

| 18 |

Total Revenues: 3,228.8 ml Euro

Advertising Revenues

97%

2004 - 2009 | Mediaset Italian business revenues evolution

2004

Other Revenues3%

2009

Advertising Revenues

70.5%

OtherRevenues

29.5%

* Source: AC Nielsen

200832.9%

200934.7%

951.4 ml Euro

Publitalia Adv. market share

| 19 |

SPAIN

| 20 |

Telecinco in Spain faced a difficult market situation, characterized by several factors:

• Launch of 2 new generalist FTA channels • Unusual inventory exploitation for TVE• Severe macroeconomic downturn

SPAIN | Market environment called for reaction

We decided to react promptly in order to achieve the best deal available

1. Best fit between Telecinco and Cuatro (editorial + advertising)2. Opportunity to replicate the Italian strategy (free + pay)

| 21 |

Reinforce the leadership in the Spanish FTA market

45.1% of TV advertising market

28.1% audience in the commercial target (24 hours)

Development of significant revenues synergies

Achieve relevant cost synergies

Reinforce the multichannel strategy on DTT

Benefit from the coming advertising market upturn, in a leading market position

The right deal at the right time

SPAIN | Strategic rationale

| 22 |

Pay TV

Non linear TV

NUOVICANALI

Con

tenu

ti

Multichannel

Generalist FTA

Multichannel

Pay TV(*) minority

stake of 22%

Cuatro.com

(*)

NUOVICANALI

Non linear TV

Content

TV Generalista

MEDIASET WAY TO BROADCASTING

| 23 |

Giuliano AdreaniCEO

| 24 |

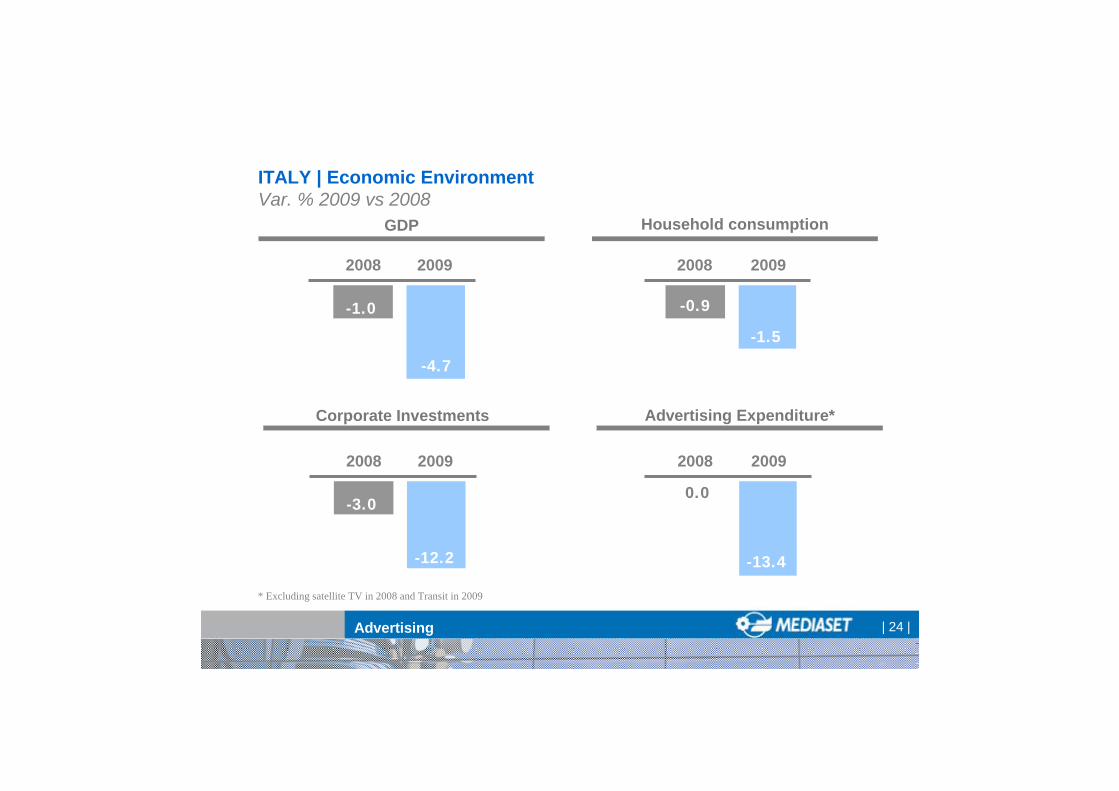

-4.7

2008

-1.5

-0.9

2009

GDP Household consumption

Corporate Investments Advertising Expenditure*

2008 2009

-1.0

ITALY | Economic EnvironmentVar. % 2009 vs 2008

-12.2

2008

-13.4

2009 2008 2009

-3.00.0

* Excluding satellite TV in 2008 and Transit in 2009

Advertising

| 25 | Advertising

-13.4% Italy

UK

France -13.3%

-8.9%

Spain-20.9%

EUROPE | Advertising market trendVar % 2009 vs. 2008

| 26 |

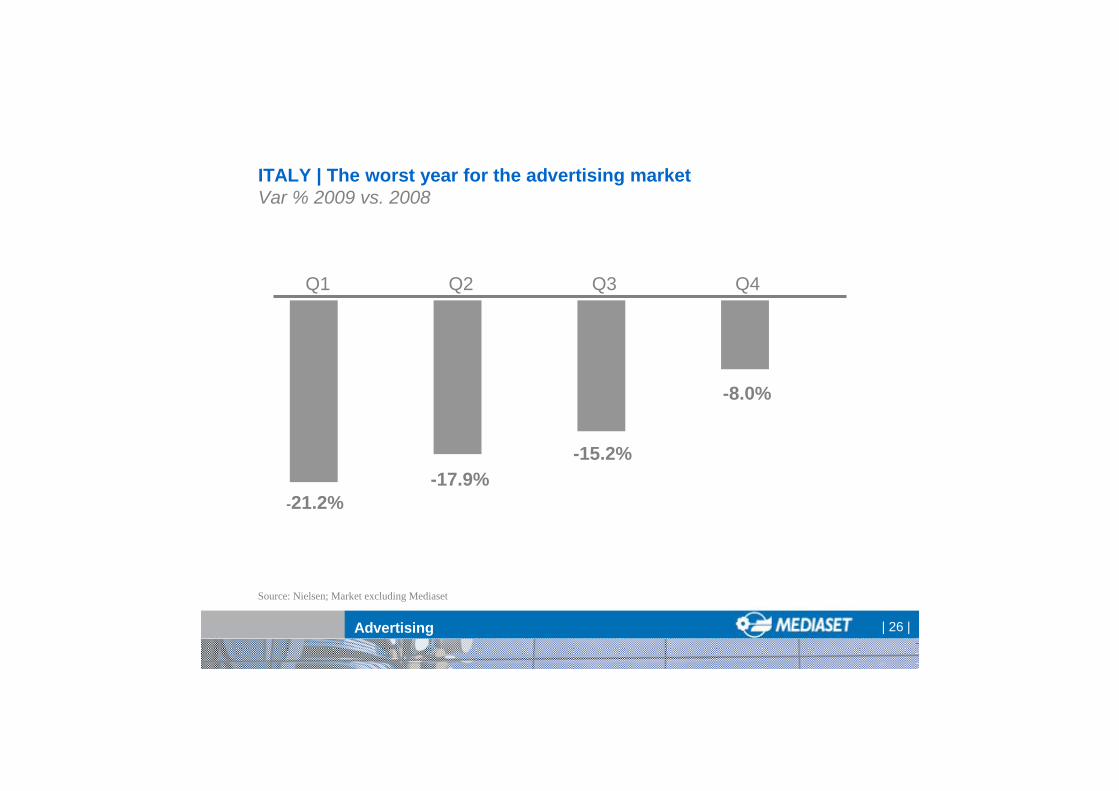

Source: Nielsen; Market excluding Mediaset

Q1 Q2 Q3 Q4

Advertising

ITALY | The worst year for the advertising marketVar % 2009 vs. 2008

-21.2%-17.9%

-15.2%

-8.0%

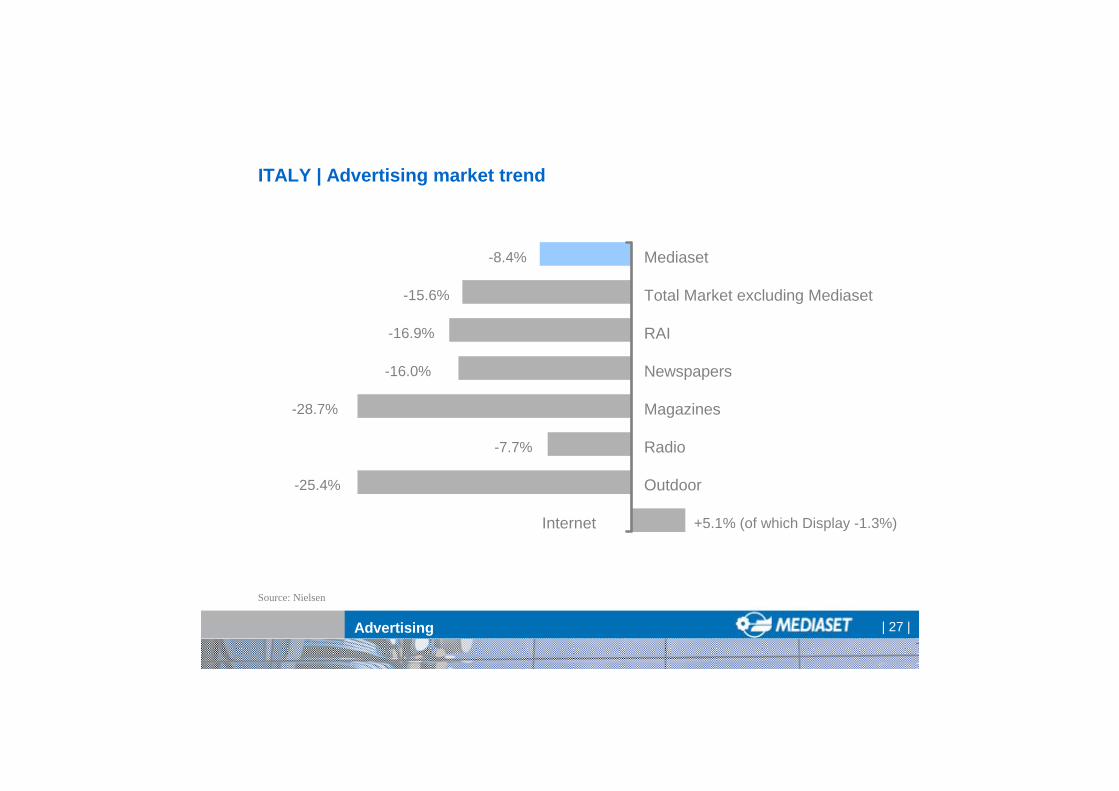

| 27 | Advertising

-8.4% Mediaset

RAI

Total Market excluding Mediaset -15.6%

-16.0% Newspapers

-28.7% Magazines

+5.1% (of which Display -1.3%)

ITALY | Advertising market trend

Radio

Outdoor

Internet

-16.9%

-7.7%

-25.4%

Source: Nielsen

| 28 | Advertising

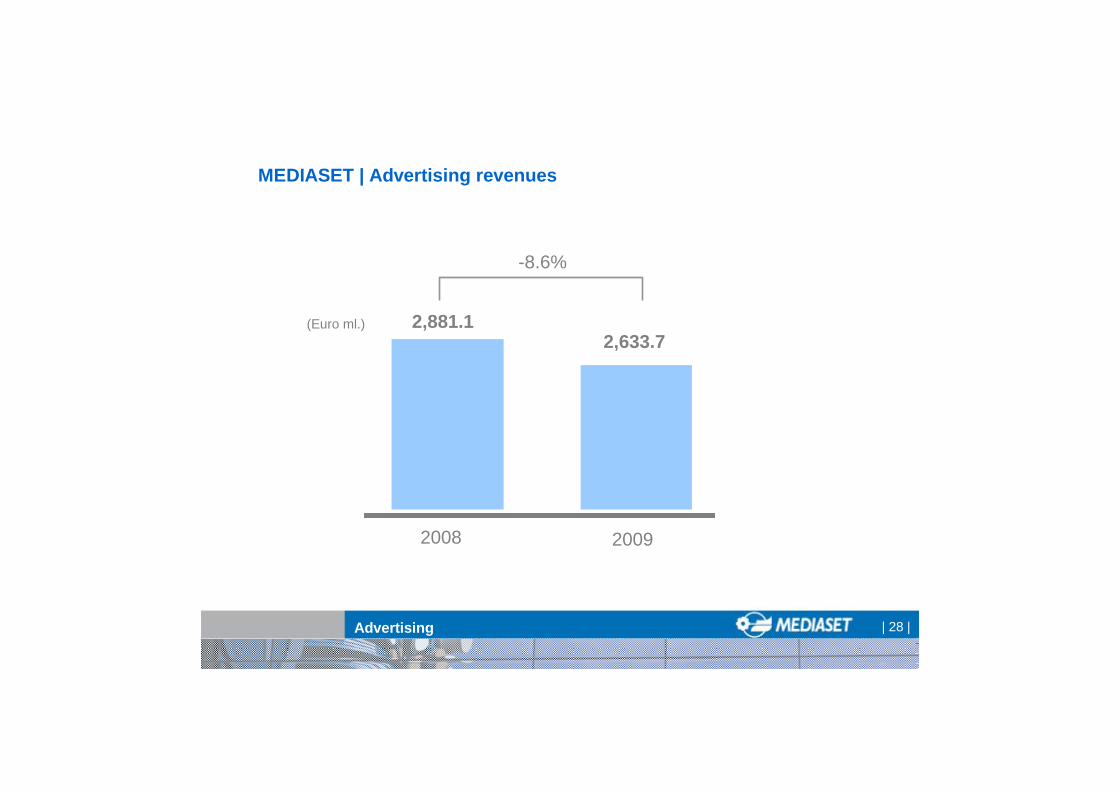

MEDIASET | Advertising revenues

(Euro ml.)

2008 2009

2,881.12,633.7

-8.6%

| 29 | Advertising

(Euro ml.)

2008 2009

2,937.5

2,704.9

-8.0% (including Digitalia)

MEDIASET | Advertising revenues

| 30 | Advertising

Q1 Q2 Q3 Q4

-21.2%

-12.8%

-17.9%

-11.1%

-15.2%

-6.2%-8.0%

-2.7%

Market excluding Mediaset Mediaset

ITALY | Publitalia outperforming the marketVar % 2009 vs. 2008

Source: Nielsen (excluding Direct Mail and Transit)

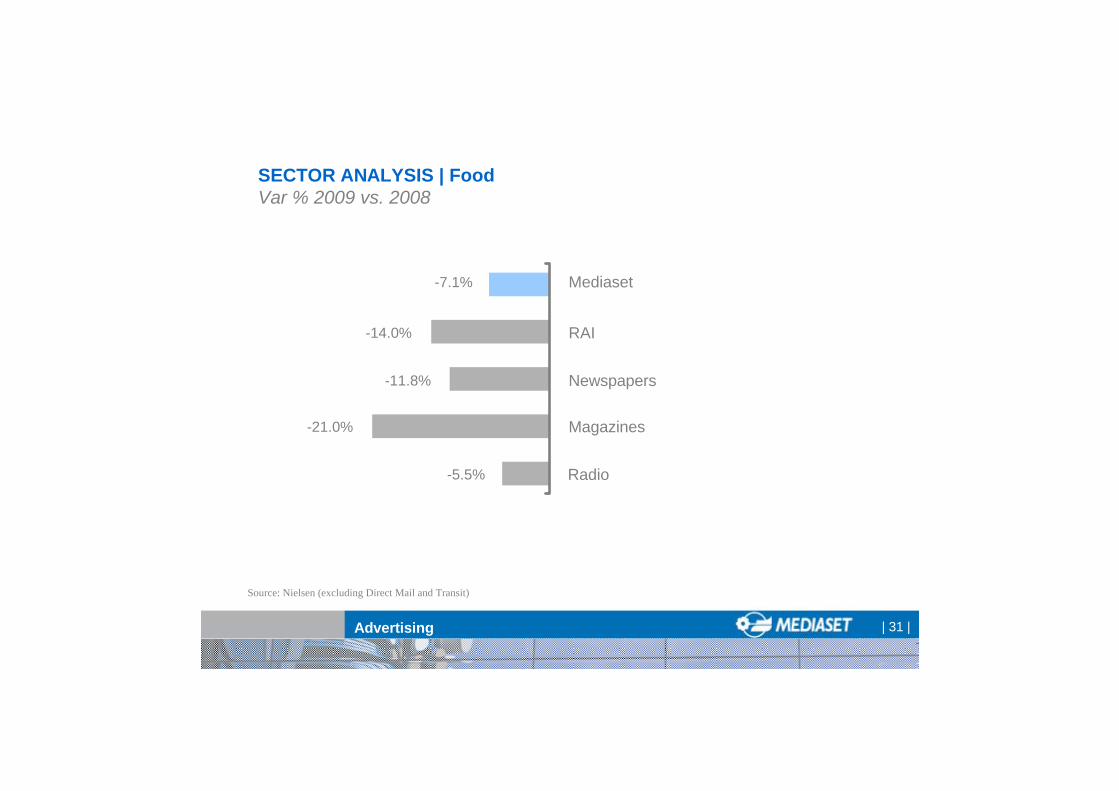

| 31 | Advertising

SECTOR ANALYSIS | FoodVar % 2009 vs. 2008

Source: Nielsen (excluding Direct Mail and Transit)

-7.1% Mediaset

Newspapers

RAI -14.0%

-11.8%

Magazines-21.0%

Radio-5.5%

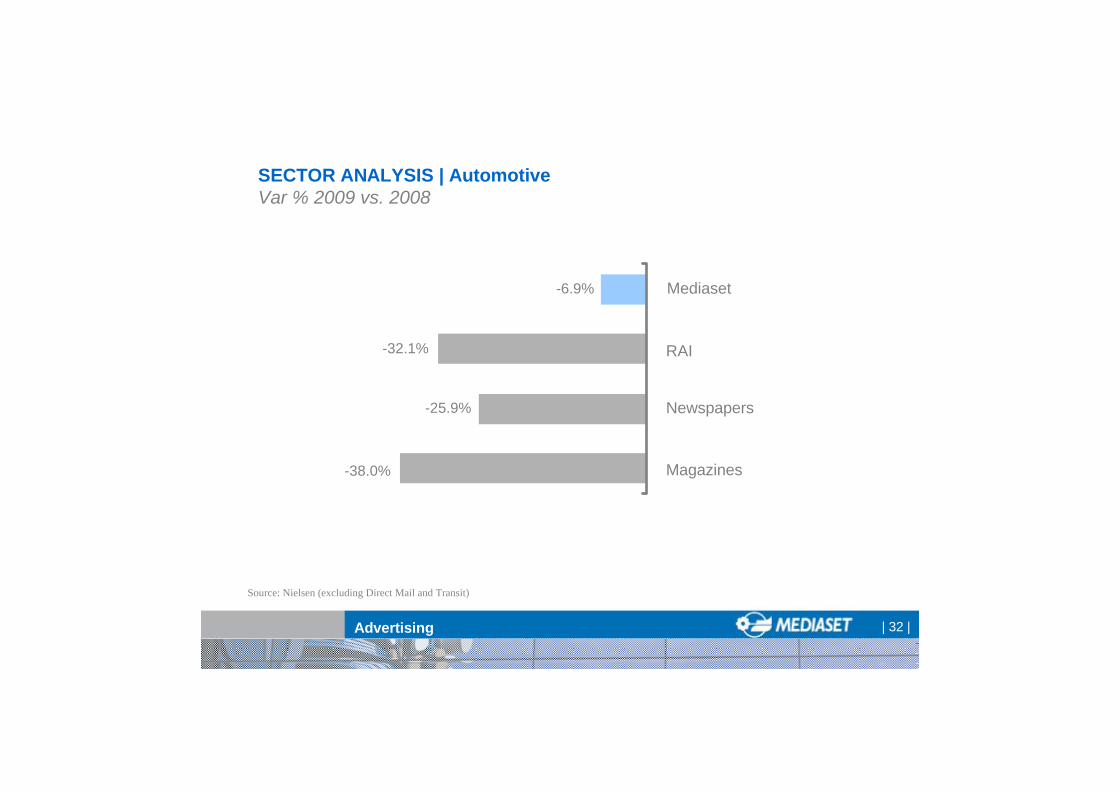

| 32 | Advertising

Mediaset

Newspapers

RAI -32.1%

-25.9%

Magazines-38.0%

-6.9%

SECTOR ANALYSIS | AutomotiveVar % 2009 vs. 2008

Source: Nielsen (excluding Direct Mail and Transit)

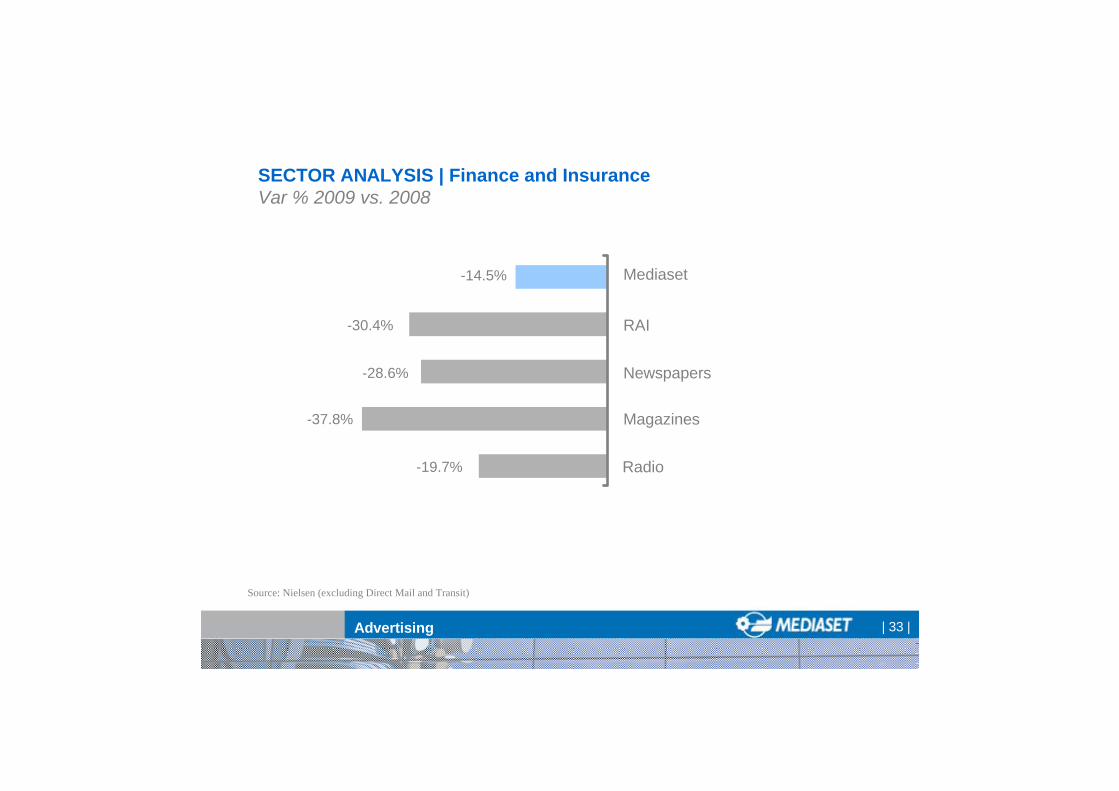

| 33 | Advertising

-14.5% Mediaset

Newspapers

RAI -30.4%

-28.6%

Magazines-37.8%

Radio-19.7%

SECTOR ANALYSIS | Finance and InsuranceVar % 2009 vs. 2008

Source: Nielsen (excluding Direct Mail and Transit)

| 34 | Advertising

+2.3%Mediaset

Newspapers

RAI -14.0%

-21.4%

Magazines-46.1%

-27.4%

Radio

Internet

+1.6%

SECTOR ANALYSIS | TelecomVar % 2009 vs. 2008

Source: Nielsen (excluding Direct Mail and Transit)

| 35 |

Why Mediaset outperformed the Market?

- Focus on core business and top clients

- Acquisition of new clients even in a difficult year

- Ability to maintain the same level of prices

| 36 | Advertising

Top 10 clients

Top 20 clients

Clients >101

2009 vs. 2008

-1.4%

-3.9%

-1.4%

MEDIASET | Focus on top clients*

(*) Holding clients – 2008 client ranking

| 37 | Advertising

1,018

254

Active clients

New clients

79.5 Euro ml.Revenues from new clients

MEDIASET | New business activity

| 38 |

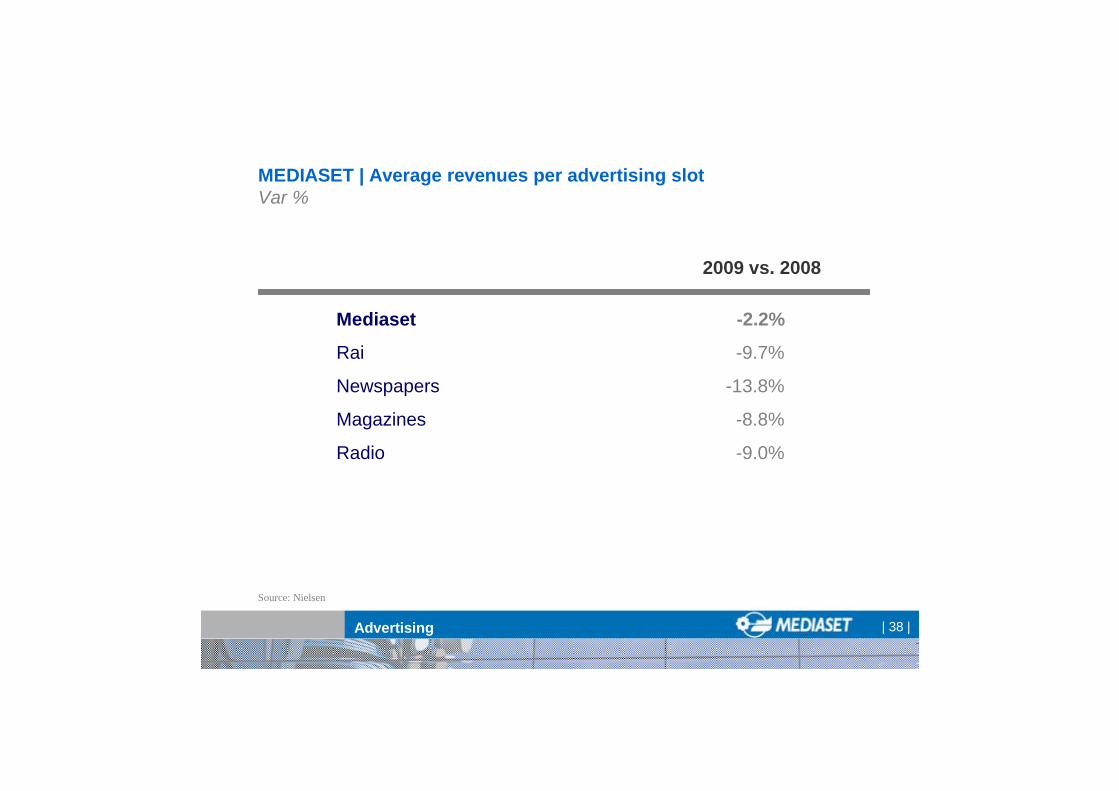

Mediaset

Rai

Newspapers

Magazines

Radio

Advertising

-2.2%

-9.7%

-13.8%

-8.8%

-9.0%

Source: Nielsen

2009 vs. 2008

MEDIASET | Average revenues per advertising slotVar %

| 39 |

First hints on 2010

| 40 |

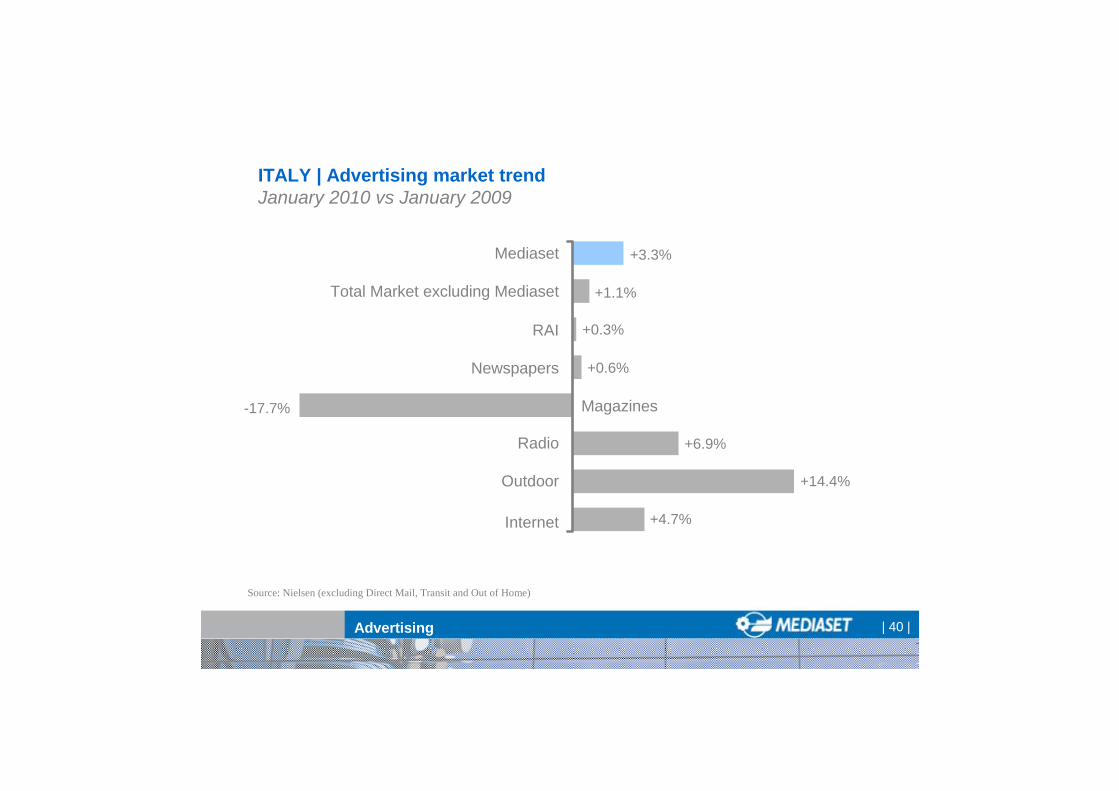

ITALY | Advertising market trendJanuary 2010 vs January 2009

Advertising

+3.3%Mediaset

RAI

Total Market excluding Mediaset +1.1%

+0.6%Newspapers

-17.7% Magazines

+4.7%

Radio

Outdoor

Internet

+0.3%

+6.9%

+14.4%

Source: Nielsen (excluding Direct Mail, Transit and Out of Home)

| 41 |

Marco GiordaniCFO

| 42 |

MEDIASET GROUP | P&L Consolidated Results

NET CONSOLIDATED REVENUESItaly

Spain

EBITItaly

Spain

NET PROFIT (Reported)*

Adjusted NET PROFIT **

2008 2009(Euro ml.)

Financials

* Including the impact of discontinued operations (Medusa Cinema and Multicinema)** Net profit adjusted in 2008 for the net impact of the amortization of intangibles related to the PPA of Endemol and the impact of the fiscal assets

realignment (2008 Italian Budget Law); in 2009 for the impact of the amortization of intangibles related to the PPA of Endemol

4,199.53,218.8

981.9

983.6596.8386.9

459.0

465.7

3,882.93,228.8

656.3

601.5478.7122.8

272.4

326.7

| 43 |

2009 RESULTS | Italian Business

| 44 |

3,218.8(418.7)

(1,234.9)

1,565.2(803.7)

(164.7)

596.8(77.0)

(33.3)

486.6(108.9)

22.4%

378.1

3,228.8(426.7)

(1,311.9)

1,490.2(865.3)

(146.2)

478.7(32.0)

(1.2)

445.5(166.7)

37.4%

269.0

Net Consolidated RevenuesPersonnel Costs

Other Operating Costs

EBITDARights Amortisation

Other Amortisation & Depreciation

Operating ProfitFinancial Income (Losses)

Associates

Pre-Tax ProfitTaxes

Tax rate

NET PROFIT

2008 2009(Euro ml.)

Financials

MEDIASET ITALIAN BUSINESS | P&L Results

+0.3%

(4.8%)

(19.8%)

(8.4%)

(28.9%)

% Var

| 45 |

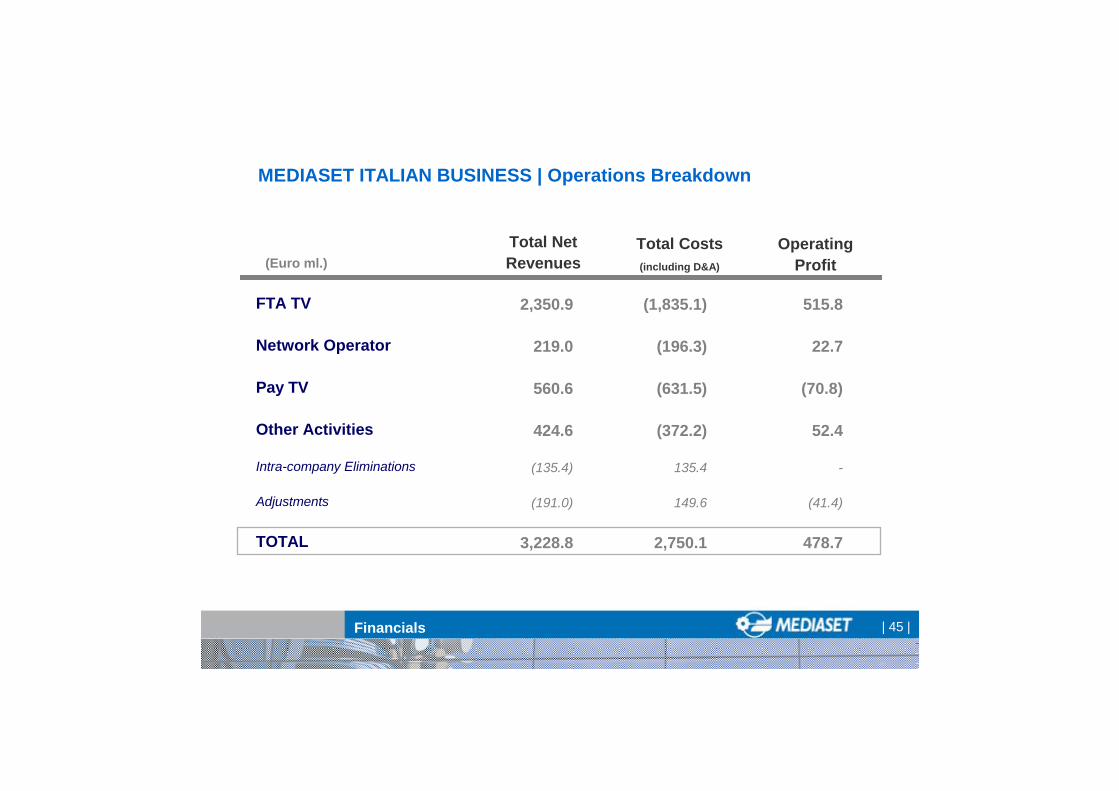

FTA TV

Network Operator

Pay TV

Other Activities

Intra-company Eliminations

Adjustments

TOTAL

Total NetRevenues

2,350.9

219.0

560.6

424.6

(135.4)

(191.0)

3,228.8

OperatingProfit

515.8

22.7

(70.8)

52.4

-

(41.4)

478.7

(Euro ml.)

Financials

Total Costs(including D&A)

(1,835.1)

(196.3)

(631.5)

(372.2)

135.4

149.6

2,750.1

MEDIASET ITALIAN BUSINESS | Operations Breakdown

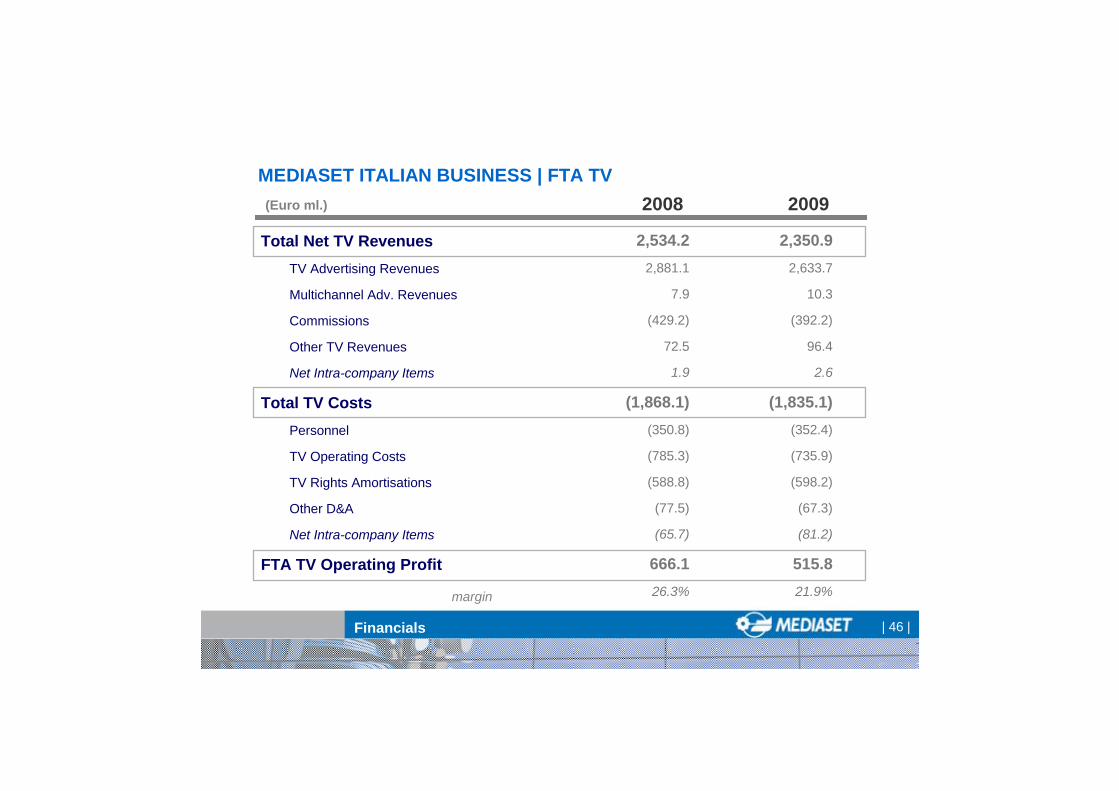

| 46 |

2,534.22,881.1

7.9

(429.2)

72.5

1.9

(1,868.1)(350.8)

(785.3)

(588.8)

(77.5)

(65.7)

666.126.3%

(Euro ml.)

Total Net TV RevenuesTV Advertising Revenues

Multichannel Adv. Revenues

Commissions

Other TV Revenues

Net Intra-company Items

Total TV CostsPersonnel

TV Operating Costs

TV Rights Amortisations

Other D&A

Net Intra-company Items

FTA TV Operating Profit

margin

20092008

2,350.92,633.7

10.3

(392.2)

96.4

2.6

(1,835.1)(352.4)

(735.9)

(598.2)

(67.3)

(81.2)

515.821.9%

Financials

MEDIASET ITALIAN BUSINESS | FTA TV

| 47 |

190.874.4

5.3

111.1

(180.1)(34.8)

(94.2)

(51.1)

10.85.7%

Total Net Revenues3° Party Revenues

Other Revenues

Net intra-company Items

Total CostsPersonnel

Other Operating Costs

Other Amortisation & Depreciation

Network Operator Operating Profit

margin

20092008(Euro ml.)

219.087.4

6.2

125.4

(196.3)(35.9)

(102.2)

(58.3)

22.710.4%

Financials

MEDIASET ITALIAN BUSINESS | Network Operator

| 48 |

403.7

199.1

13.1

192.9

(1.5)

(464.6)(8.8)

(196.7)

(217.3)

(41.7)

(60.9)

Total Net Pay TV Revenues

Pay TV Revenues

Advertising Revenues

Other Revenues

Commissions

Total Pay TV CostsPersonnel

Other Operating Costs

Rights Amortisations and Other D&A

Net intra-company items

Pay TV Operating Profit

20092008(Euro ml.)

560.6

311.5

29.8

223.5

(4.2)

(631.5)(14.6)

(302.6)

(267.0)

(47.3)

(70.8)

Financials

MEDIASET ITALIAN BUSINESS | Pay TV

| 49 |

371.5106.4

167.8

21.0

35.7

41.6

2.5

(355.6)(24.4)

(199.3)

(96.1)

(27.7)

(8.1)

15.94.3%

Total Net RevenuesMedusa/Taodue 3° Party revenues

Medusa/Taodue intra-company revenues

Multimedia

Mediashopping

Other Non-TV Revenues

Net Intra-company Items

Total CostsPersonnel

Other Operating Cost

Right Amortisations

Other Amortisations & Depreciations

Intra-company Items

Other Activities Operating Profitmargin

20092008(Euro ml.)

424.6104.6

191.0

20.5

61.2

39.8

7.4

(372.2)(24.0)

(212.3)

(120.9)

(8.1)

(6.9)

52.412.3%

Financials

MEDIASET ITALIAN BUSINESS | Other Activities

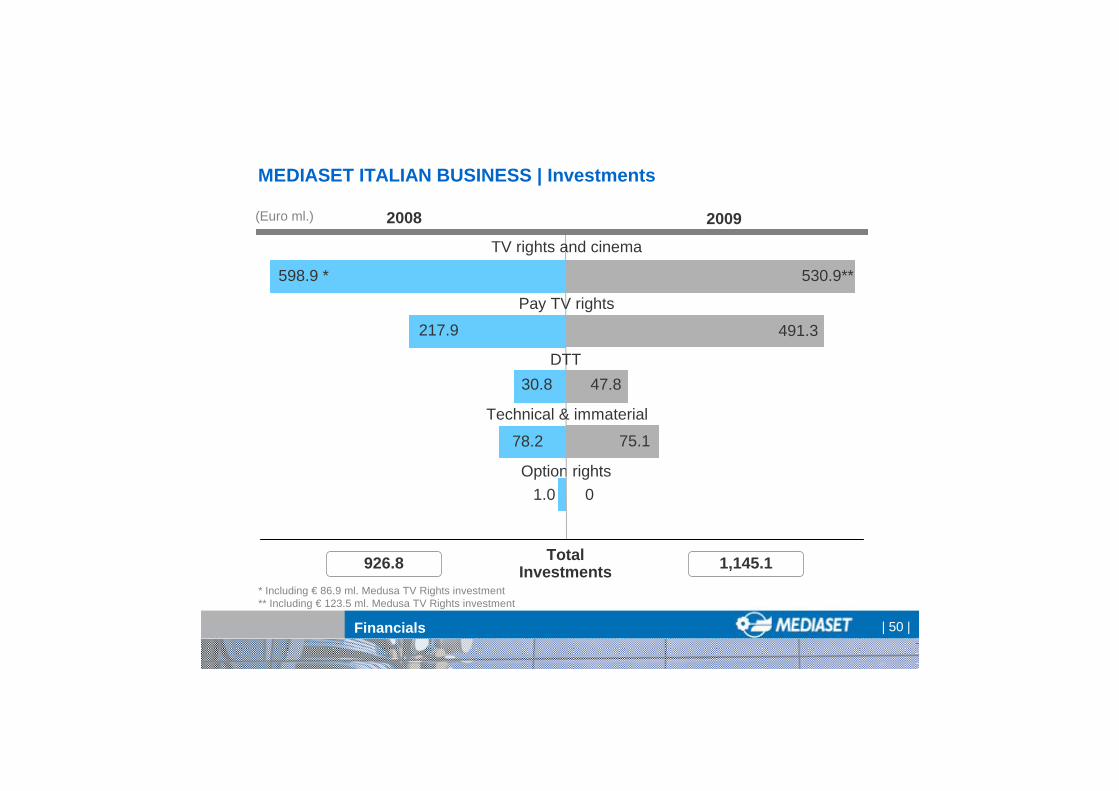

| 50 |

Option rights

20092008

78.2 75.1

217.9 491.3

30.8 47.8

530.9**598.9 *

1.0 0

926.8 1,145.1

(Euro ml.)

TV rights and cinema

Pay TV rights

DTT

Technical & immaterial

Total Investments

* Including € 86.9 ml. Medusa TV Rights investment** Including € 123.5 ml. Medusa TV Rights investment

Financials

MEDIASET ITALIAN BUSINESS | Investments

| 51 |

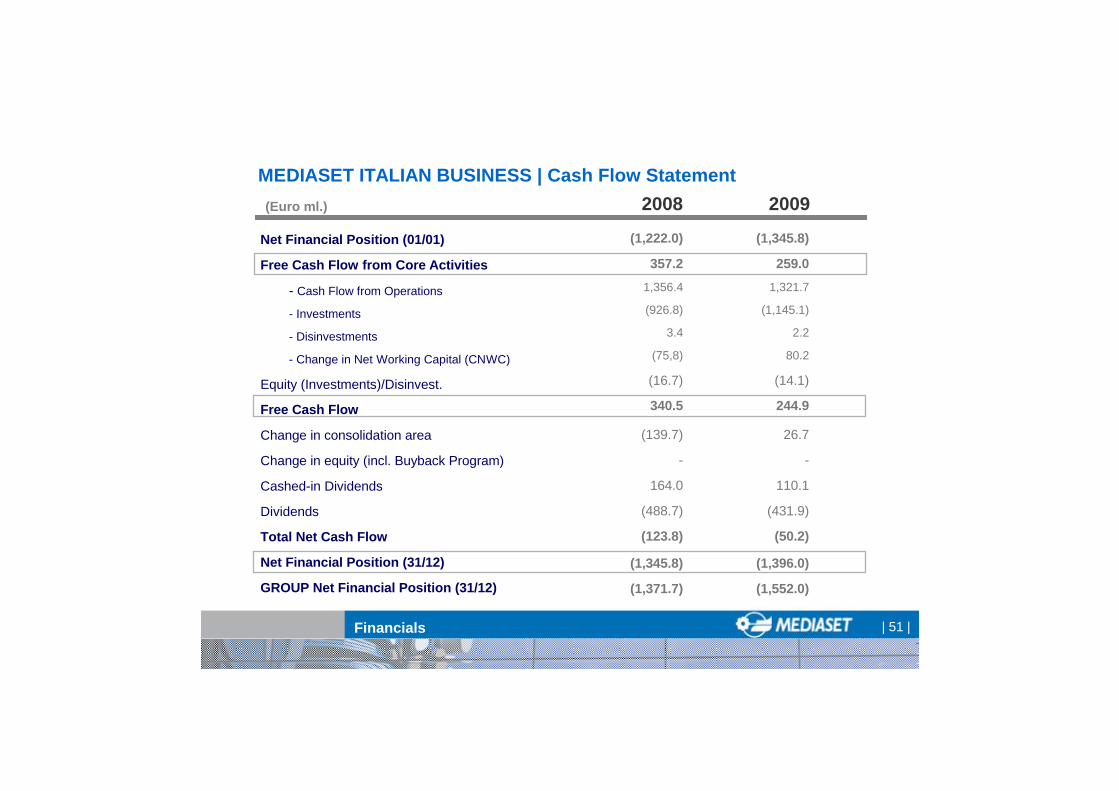

(1,222.0)

357.21,356.4

(926.8)

3.4

(75,8)

(16.7)

340.5

(139.7)

-

164.0

(488.7)

(123.8)

(1,345.8)

(1,371.7)

Net Financial Position (01/01)

Free Cash Flow from Core Activities

- Cash Flow from Operations

- Investments

- Disinvestments

- Change in Net Working Capital (CNWC)

Equity (Investments)/Disinvest.

Free Cash Flow

Change in consolidation area

Change in equity (incl. Buyback Program)

Cashed-in Dividends

Dividends

Total Net Cash Flow

Net Financial Position (31/12)

GROUP Net Financial Position (31/12)

20092008(Euro ml.)

(1,345.8)

259.01,321.7

(1,145.1)

2.2

80.2

(14.1)

244.9

26.7

-

110.1

(431.9)

(50.2)

(1,396.0)

(1,552.0)

Financials

MEDIASET ITALIAN BUSINESS | Cash Flow Statement

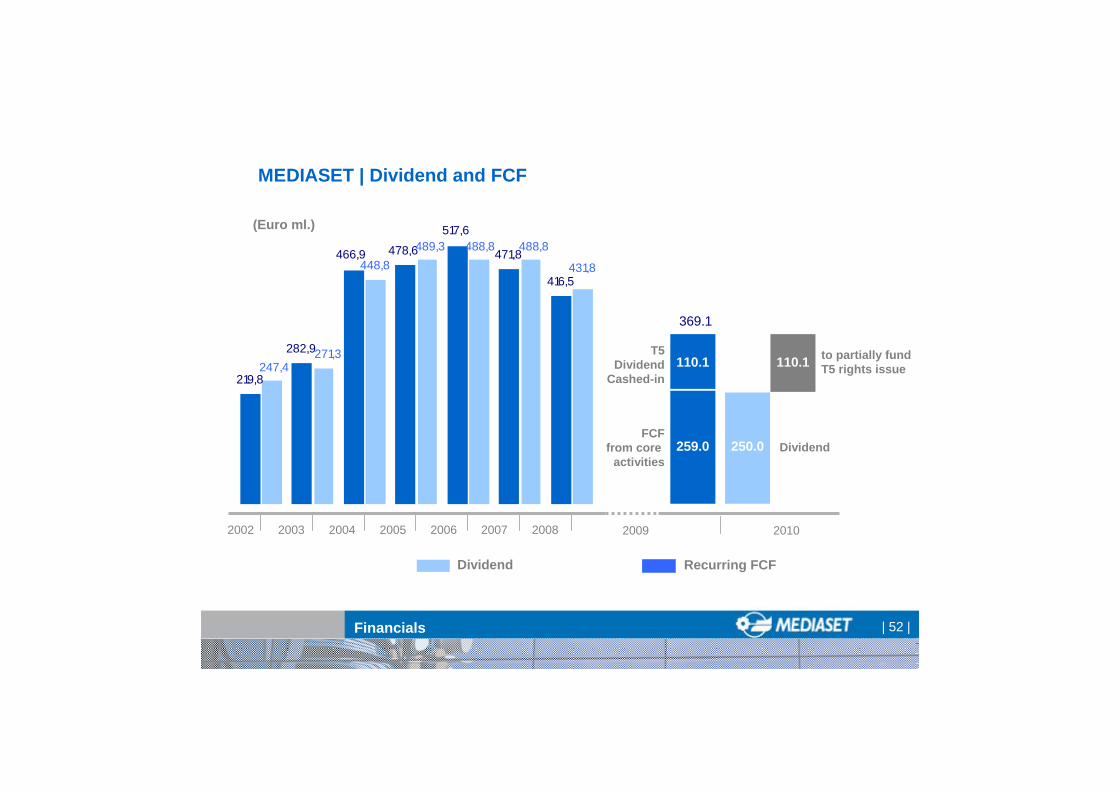

| 52 |

219,8

282,9

471,8

416,5448,8

466,9 478,6

517,6

431,8

488,8

271,3247,4

489,3 488,8

200420032002 2005

(Euro ml.)

Dividend Recurring FCF

2006 2007 2008

Financials

MEDIASET | Dividend and FCF

2009

369.1

2010

259.0

110.1T5

DividendCashed-in

FCFfrom core

activities250.0

110.1

Dividend

to partially fundT5 rights issue

| 53 |

* To be approved by AGM, 20th/21st April 2010; treasury shares are not eligible to receive dividends

Financials

MEDIASET GROUP | Dividend policy

2003 2004 2005 2006 2007 2008

Net Profit (Euro ml.) 369.7 549.6 603.4 505.5 506.8 459.0

Earnings per Share (Euro) 0.31 0.47 0.53 0.44 0.45 0.40

Recurring FCF (Euro ml.) 282.9 466.9 478.6 517.6 471.8 416.5

Dividends 271.3 448.8 489.3 488.8 489.5 431.8

Dividend per Share (Euro) 0.23 0.38 0.43 0.43 0.43 0.38

Dividend/Recurring FCF 96% 96% 102% 94% 104% 104%

Pay-out Ratio 73% 82% 81% 97% 97% 94%

(Euro ml.)

2009

272.4

0.24

259.0 (1)

*250.0

0.22

97%

92%

*

(1) Excluding 2009 Tele5 dividend cashed-in

| 54 |

MEDIASET GROUP | Back up Slides

| 55 |

(1,208.8)

672.2

1,865.0

(1,122.6)

4.5

(74.7)

(1.3)

(53.6)

(640.7)

(139.5)

(162.9)

(1,371.7)

Net Financial Position (01/01)

Free Cash Flow

- Cash Flow from Operations

- Investments

- Disinvestments

- Change in Net Working Capital (CNWC)

Change in equity (incl. Buyback Program)

Equity (Investments)/Disinvest.

Dividends (paid and received)

Change in consolidation area

Total Net Cash Flow

Net Financial Position (31/12)

20092008(Euro ml.)

(1,371.7)

354.1

1,627.2

(1,319.4)

6.5

39.8

(2.9)

(28.0)

(538.9)

26.7

(180.3)

(1,552.0)

Financials

MEDIASET GROUP | Consolidated Cash Flow

| 56 |

2,396,1

513.4

1,051.9

361.6

(195.5)

4,127.5

2,482.4

273.4

2,755.8

(1,371.7)

Television Rights

Goodwill and consolidation differences

Other tangible and intangible assets

Financial assets

Net working capital & other assets/liabilities

Net Invested Capital

Group shareholders’ equity

Minority interests

Net assets

Net financial position

2008(Euro ml.)

Financials

MEDIASET GROUP | Consolidated Balance Sheet

2,598.0

512.1

957.1

233.8

(210.7)

4,090.3

2,331.8

206.5

2,538.3

(1,552.0)

2009

| 57 |

2,266.6

150.2

931.6

746.5

(168.5)

3,926.4

2,527.2

53.4

2,580.6

(1,345.8)

Television Rights

Goodwill and consolidation differences

Other tangible and intangible assets

Financial assets

Net working capital & other assets/liabilities

Net Invested Capital

Group shareholders’ equity

Minority interests

Net assets

Net financial position

2008(Euro ml.)

Financials

MEDIASET ITALIAN BUSINESS | Balance Sheet

2,419.1

149.3

888.6

714.6

(242.6)

3,929.0

2,471.2

61.8

2,533.0

(1,396.0)

2009

| 58 |

MEDIASET GROUP | Net Profit Adjustment

NET PROFIT (Reported)

Edam Adjustments from Telecinco

Telecinco Minorities

Net Edam PPA Adjustment

Net Edam Goodwill Adjustment

Fiscal Assets realignment

Adjusted NET PROFIT

272.4

64.2

(31.3)

5.5

15.9

-

326.7

(Euro ml.)

Financials

2009

459.0

71.3

(34.8)

6.1

17.7

(53.5)

465.7

2008

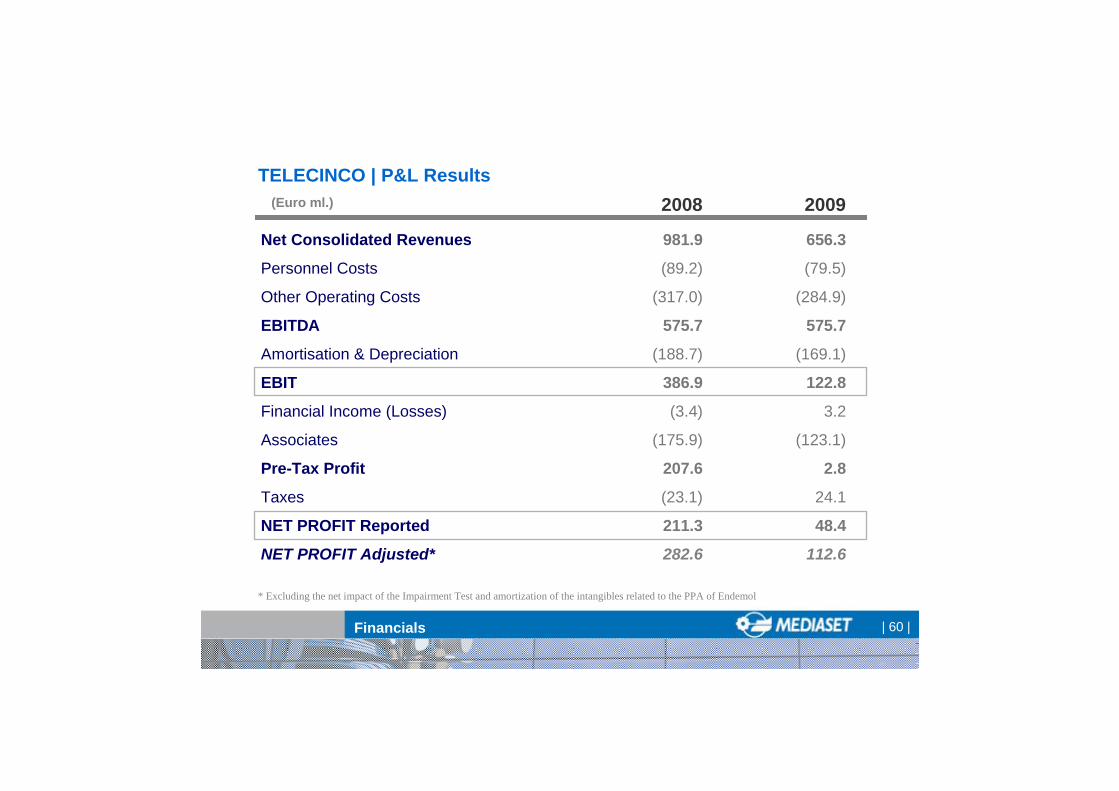

| 59 |

MEDIASET SPANISH BUSINESS | Back up Slides

| 60 |

981.9

(89.2)

(317.0)

575.7

(188.7)

386.9

(3.4)

(175.9)

207.6

(23.1)

211.3

282.6

656.3

(79.5)

(284.9)

575.7

(169.1)

122.8

3.2

(123.1)

2.8

24.1

48.4

112.6

TELECINCO | P&L Results

Net Consolidated Revenues

Personnel Costs

Other Operating Costs

EBITDA

Amortisation & Depreciation

EBIT

Financial Income (Losses)

Associates

Pre-Tax Profit

Taxes

NET PROFIT Reported

NET PROFIT Adjusted*

2008 2009(Euro ml.)

Financials

* Excluding the net impact of the Impairment Test and amortization of the intangibles related to the PPA of Endemol

| 61 |

20092008

148.1 159.3

9.0 5.2

TV rights

Tangible & Intangible Fixed Assets

Total Investments

TELECINCO | Investments

Financials

195.8 174.2

(Euro ml.)

38.7 9.8Co-production & Distribution

| 62 |

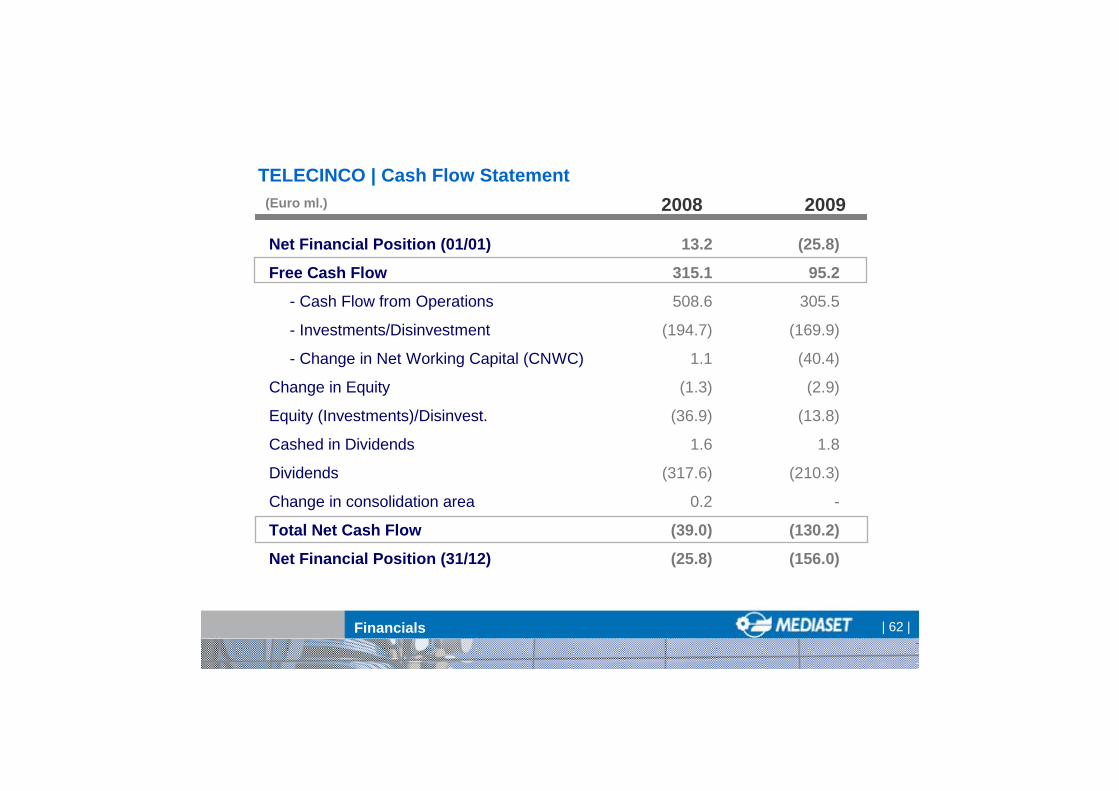

13.2

315.1

508.6

(194.7)

1.1

(1.3)

(36.9)

1.6

(317.6)

0.2

(39.0)

(25.8)

TELECINCO | Cash Flow Statement

Net Financial Position (01/01)

Free Cash Flow

- Cash Flow from Operations

- Investments/Disinvestment

- Change in Net Working Capital (CNWC)

Change in Equity

Equity (Investments)/Disinvest.

Cashed in Dividends

Dividends

Change in consolidation area

Total Net Cash Flow

Net Financial Position (31/12)

(25.8)

95.2

305.5

(169.9)

(40.4)

(2.9)

(13.8)

1.8

(210.3)

-

(130.2)

(156.0)

(Euro ml.)

Financials

2008 2009

| 63 |

Forward-looking StatementsStatements contained in this document, particularly the ones regarding any Mediaset Group possible or assumed future performance, are or may be forward looking statements and in thisrespect they involve some risks and uncertainties.

Mediaset Group actual results and developments may differ materially from the onesexpressed or implied by the above statements depending on a variety of factors.

Any reference to past performance of Mediaset Group shall not be taken as an indication of future performance.

This announcement does not constitute an offer to sell or the solicitation of an offer to buy the securities discussed herein.

The executive responsible for the preparation of the Mediaset S.p.A. accounts, Andrea Goretti, declares that, as per para. 2 art. 154-bis, of the “Testo Unico della Finanza”, that the accounting information contained in this document corresponds to that contained in the company’s books.

Investor Relations Department:

Tel: +39 02 2514.7008Fax: +39 02 2514.6719Email: [email protected]: www.mediaset.it/investor/