Embed Size (px)

Citation preview

20th Annual CAA Conference

Hilton Barbados

December 1-3, 2010

2010 Conference: “Riding the Waves of Change”

Insurance Accounting Proposals of the IASB and FASB –

Property/Casualty issues

Ralph Blanchard, FCAS, MAAA

CAS President

December 3, 2010

3

Caveat

The following represents the views and analysis

of the presenter, and does not necessarily

represent the official analysis, opinions or

interpretation of any of the organizations that he

is affiliated with.

4

Ins. Accounting Proposals – Presentation Outline

� Current situation (U.S., Canada, U.K.)

� Standard Setting process

� General approach

� Insurance project – current status

� IASB

� FASB

� Proposals – details� IASB� FASB

� Issues

� Next Steps

5

Current situation – Accounting Rules

International • IASB sets international standards (IFRS)

• No authority to implement

United States

• FASB sets US GAAP – overlayed by SEC

• FASB working on convergence with IASB

• SEC evaluating whether to accept IFRS (or adopt IFRS as US GAAP) – no decision yet.

Canada - Adopts IFRS on 1/1/2011 (cold turkey)

U.K. – EU “adopted” IFRS 1/1/2005

G20 – Pressuring everyone to adopt IFRS

6

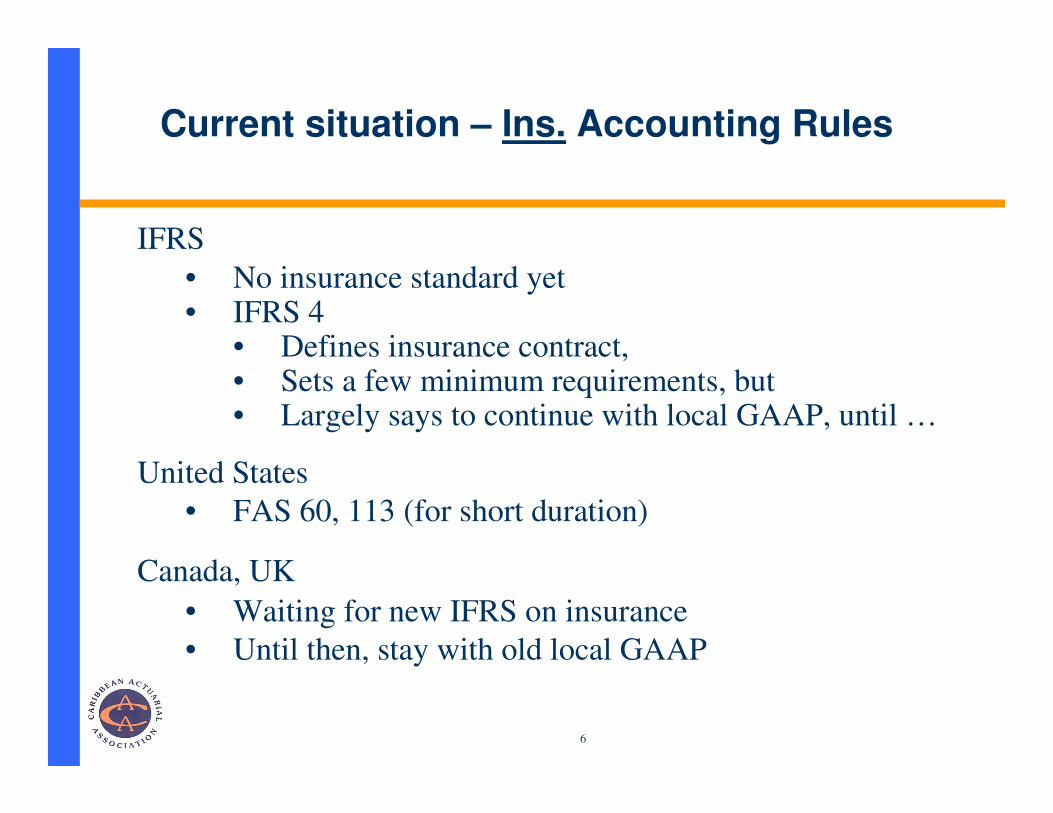

Current situation – Ins. Accounting Rules

IFRS

• No insurance standard yet• IFRS 4

• Defines insurance contract,• Sets a few minimum requirements, but• Largely says to continue with local GAAP, until …

United States

• FAS 60, 113 (for short duration)

Canada, UK

• Waiting for new IFRS on insurance

• Until then, stay with old local GAAP

7

Standard Setting Process

In sequential order

1. Discussion Paper • Preliminary Views, if any

• Issues

• Still in investigation phase

• Looking for comments, direction

2. Exposure Draft

• All issues decided (supposedly)

• Looking for problems with decisions

3. Final Standard

4. Effective Date

8

Standard Setting Process – current status

IASB/FASB:

• Joint project on Insurance Contracts

• Working together since Oct. 2008

IASB • Issued an Exposure Draft (ED) on Insurance – July 30, 2010

• Comments due Nov 30, 2010

• Final Standard – June 2011

• Effective 1/1/2014 ???

FASB

• Issued their views on IASB ED as Discussion Paper (Sept 17)

• Comments due Dec 15

9

Current Proposals – IASB ED outline

• Scope

• Definition of insurance

• Key Concepts

• Short duration vs. Long duration

• Recognition

• Measurement – short duration

• Presentation – short duration

• Disclosure – short duration

• Long Duration differences

• Ceded reinsurance

10

IASB ED - Scope

• Insurance contracts, whether or not written by insurers

• Includes Surety Bonds, Financial Guarantee

• Includes Insurance, Reinsurance (ceded & assumed)

• Excludes Policyholder accounting

11

IASB ED – Definition of Insurance

“a contract under which one party (the insurer) accepts significant

insurance risk from another party (the policyholder) by agreeing to

compensate the policyholder if a specified uncertain future event (the

insured event) adversely affects the policyholder.”

• Would allow for amount and/or timing risk

• US GAAP requires amount and timing risk under FAS 113

• No need for retroactive vs. prospective distinction

12

IASB ED – Key Concepts

• No gain at issue

• Approach to achieve this varies (short vs. long duration)

• Fulfillment Value (and NOT Fair Value)

• Three Building Block Approach

13

IASB ED – Fulfillment Value

Three Building Blocks

• Expected future cashflows

• Time value of money discount

• Risk adjustment

14

Building Block 1 – expected future cash flows

“unbiased … probability-weighted estimate (i.e. expected value”

• Reportedly, intent was not to require stochastic, but words may imply otherwise – differing views

• Reflect full range of all possible outcomes – impossible standard

“future cash flows”

• Incremental flows (to the portfolio) – including L&LAE, commissions, etc.

• Don’t include overhead

• Net of inflows and outflows within contract boundary

Unit of account – portfolio of insurance contracts

• “Insurance contracts that are subject to broadly similar risks and

managed together as a single pool”

15

Building Block 2 – time value of money

What discount rate should be used?

• Yield curve with no or negligible credit risk, adjusted for differences

in liquidity.

• Don’t reflect own credit risk

• Don’t base the rate on actual asset portfolio

• Approach consistent with a “benchmark portfolio” approach – i.e.,

based on hypothetical portfolio that matches expected payouts.

(based partly on a KPMG presentation material)

16

Building Block 3 – risk adjustment

“The maximum amount that the insurer would rationally pay to be relieved of the risk that the ultimate fulfillment cash flows

may exceed those expected."

• Must use one of the following techniques: • Confidence level• Conditional Tail Expectation (CTE = TVaR)• Cost of Capital (CoC)

• Does not specify the confidence level, TVaR or CoC to use.

• Requires Capital in CoC to be based on VaR.

• Estimated at a portfolio basis - reflect diversification within a portfolio but not between different portfolios

• Re-measured each reporting period

(based partly on KPMG presentation material)

17

IASB ED – Short vs. Long Duration

Short Duration

• Contract coverage period – approx. 1 yr or less

Short Duration contacts treated differently for:

• Pre-claims liability (aka UPR)

• Income statement

18

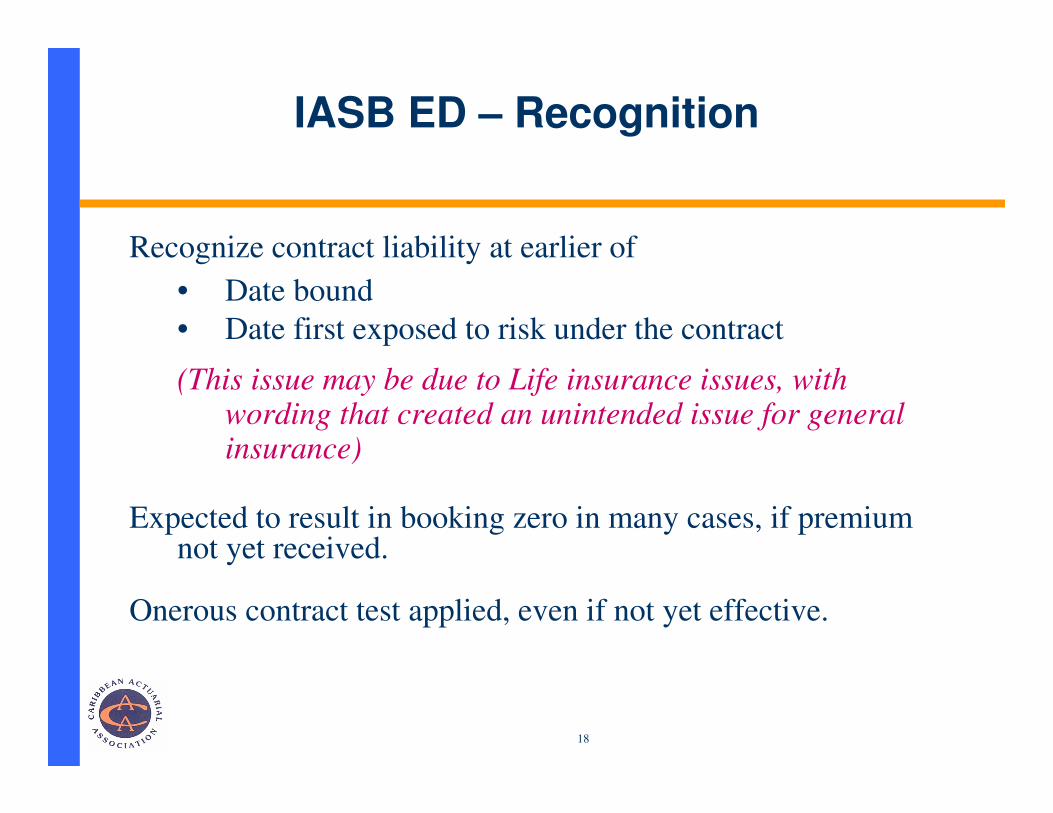

IASB ED – Recognition

Recognize contract liability at earlier of

• Date bound

• Date first exposed to risk under the contract

(This issue may be due to Life insurance issues, with wording that created an unintended issue for general insurance)

Expected to result in booking zero in many cases, if premium not yet received.

Onerous contract test applied, even if not yet effective.

19

IASB ED – Measurement – Short Dur.

Pre-claims obligation

Initially

• Premium received, plus

• Expected present value of future premiums, less

• Incremental acquisition costs

Subsequently

• Reduce over coverage period “in a systematic way that best reflects exposure from providing … coverage”• Basically US GAAP – typically pro rata

• Accrete interest on the pre-claims liability balance

Could be viewed as Unearned Premium Reserve, made complicated

20

IASB ED – Measurement – Short Dur.

Pre-claims liability =

Pre-claims obligation

MINUS

Expected present value of future premiums

Similar to netting the Unearned Premium Liability and the

Agents Balances Asset into a single liability item

NOTE: Current wording has omissions, confusions (not operational). IT WILL CHANGE

21

IASB ED – Measurement – Short Dur.

Pre-claims liability - Onerous Contract test

Based on fulfillment value (building blocks)

• Probability-weighted (i.e., expected value) of future incremental

cash flows (in and out)

• Discounted

• Risk adjustment

Unit of account – by portfolio (and by similar inception date)

Cushion created by exclusion of overhead costs in cash flows

Essentially a Premium Deficiency Test with a risk margin

22

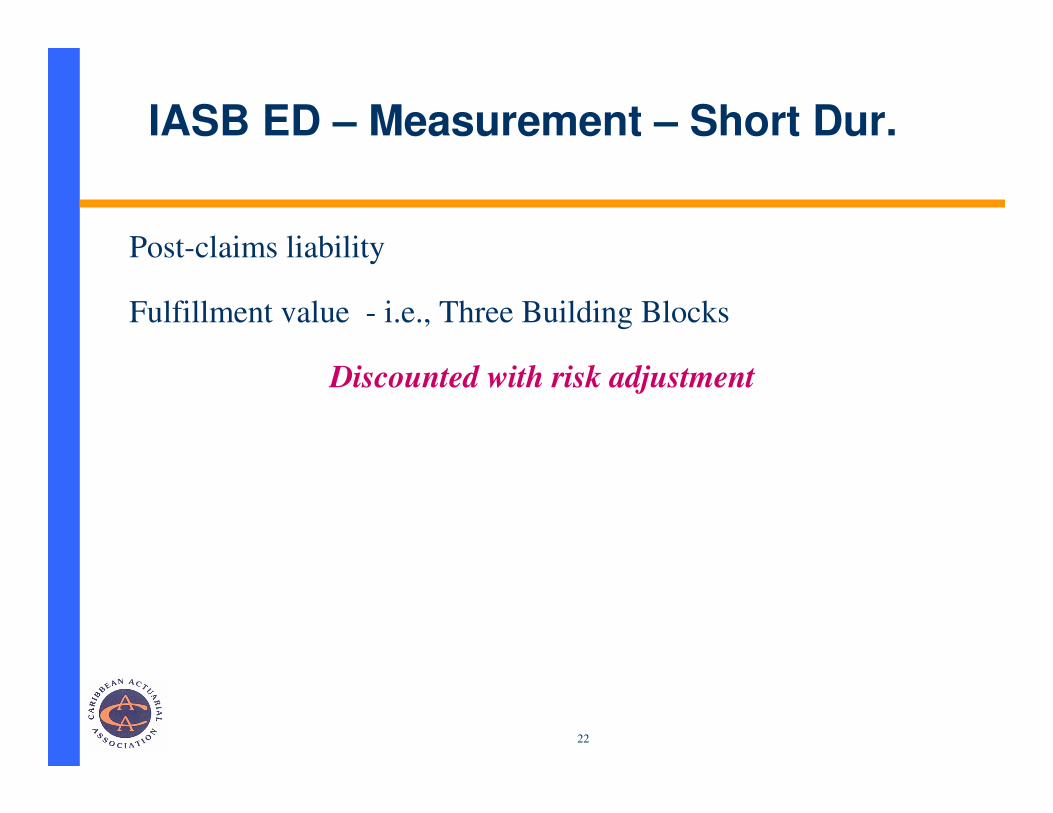

IASB ED – Measurement – Short Dur.

Post-claims liability

Fulfillment value - i.e., Three Building Blocks

Discounted with risk adjustment

23

IASB ED – Presentation – Short Dur.

Very similar to status quo for underwriting income portion

• Premiums (gross of incremental acquisition)

• Incurred Claims

• Expenses Incurred

• Amortization of incremental acquisition in “pre-claims liability”

Balance sheet

• US GAAP approach to Reinsurance

• Break out balances by portfolio (reporting segment??)

24

IASB ED – Disclosures – Short Dur.

Extensive disclosures required.

“An insurer shall consider the level of detail necessary to satisfy

the disclosure requirements and how much emphasis to

place on each of the various requirements. An insurer shall

aggregate or disaggregate information so that useful

information is not obscured by either the inclusion of a

large amount of insignificant detail or the aggregation of

items that have difference characteristics.”

In the end, it’s not clear whether the end result is any different

from requirements of the US SEC.

• (May be the same, may be more)

25

IASB ED – Long duration differences

1. Pre-claims

Initial measurement:

• Fulfillment value (3 building blocks)

• If initial gain would result, set up residual margin so that no initial gain

Subsequent measurement:

• Remeasured fulfillment value, plus

• Runoff of initial residual margin over the coverage period• Runoff pattern based on expected incurred loss timing

• Accrete interest on residual margin at initial discount rate

• Residual margin runoff done by portfolio by inception date

26

IASB ED – Long duration differences

2. Presentation

Essentially all long duration policies would be treated as deposits

• “Premiums” are deposits, not revenue:

• “Losses/Claims” are returns of deposits, not expenses

Revenue comes from margin releases

• Both residual margin and risk adjustment

Expense comes from amounts different from expected, and non-

incremental expenses

27

IASB ED – Ceded Reinsurance

Premiums shown net of commissions

Not clear if all ceded reinsurance follows long duration model,

or model of the ceded contracts

Confusion led to follow-up call by IASB staff (Oct 25th)

Problem of “policies attaching” reinsurance

1. All the underlying policies may be short duration, but resulting reinsurance policy may be “long duration”

(fix may be forthcoming)

2. Risk adjustment may span multiple underlying direct insurance “portfolios”

28

FASB Discussion Paper

1. Overall

FASB is asking if the IASB ED is an improvement over current

US GAAP.

Last FASB question asks which approach to follow from a

continuum, from adopting IASB ED to US GAAP status quo

with targeted improvements.

29

FASB Discussion Paper

2. Overall structure of FASB Discussion Paper

• Describes or summarizes IASB ED

• Describes preliminary FASB position on each IASB ED

item

• Asks for comments on selected items

• In the IASB ED, and

• Concerning their preliminary views

30

FASB Discussion Paper

3. Short Duration

• “Several” FASB Board members preliminarily would

accept the IASB short duration approach

• But the FASB DP takes no preliminary position

• They are asking whether there should be separate short

and long duration approaches or one approach, AND

• If two approaches, how might short duration be

defined

31

FASB Discussion Paper

4. Long Duration

• FASB disagrees with the “two margin” approach of

• Residual margin run off over coverage period, and

• Risk adjustment run off over coverage plus payment period

• FASB approach is a single composite margin

• Added to building blocks 1 and 2, so no gain at issue

• Run off over coverage + payment period

• No accrual for interest

• Very skeptical about reliability of risk adjustment calcs.

32

FASB Discussion Paper

5. Presentation

• Preliminary agreement with IASB ED proposals here.

• Not sure which contracts should be under the long duration

vs. short duration approaches

• Concerned about the use of two different presentation

approaches for insurance contracts.

• Wants feedback about the usefulness of the two approaches,

and which contracts would use each approach

33

Issues (General Ins. perspective)

• Definition of short duration

• Complicated approach for short duration pre-claims

• “probability-weighted cash flows”

• Restrictions on risk adjustment techniques

• Ceded reinsurance not following same model as underlying

• Are risk adjustment complications worth it?

• Portfolio definition uncertainty

Is this an improvement over current short duration accounting

(which is generally consistent throughout the world)?

34

Next Steps

• Comments due November 30 (IASB ED) and December 15

(FASB)

• IASB/FASB Roundtables to be held in US, UK, Japan

• IASB Final Standard in June 2011? (Effective ?)

• FASB yet to decide if changes will result from this.

35

Questions?