Embed Size (px)

Citation preview

2010 HEALTH CARE REFORMPATIENT PROTECTION AND AFFORDABLE CARE

HEALTH CARE RECONCILIATION

By: Brandon A. Lagarde, CPA, JD

Overview• Patient Protection and Affordable Care Act

• Health Care and Education Reconciliation Act of 2010

HEALTH CARE REFORM

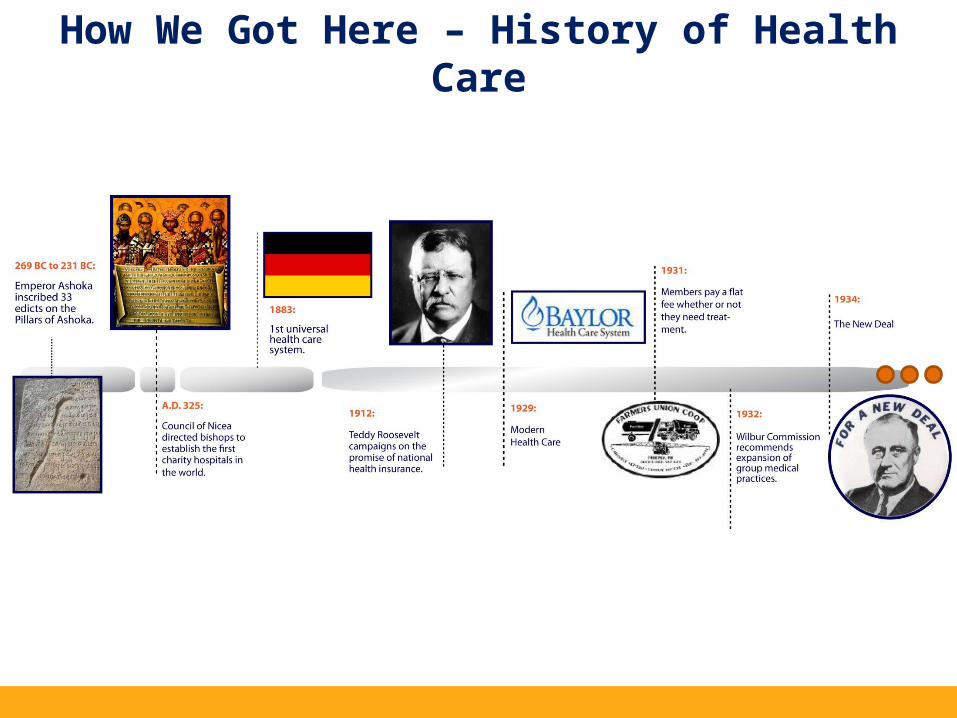

How We Got Here – History of Health Care

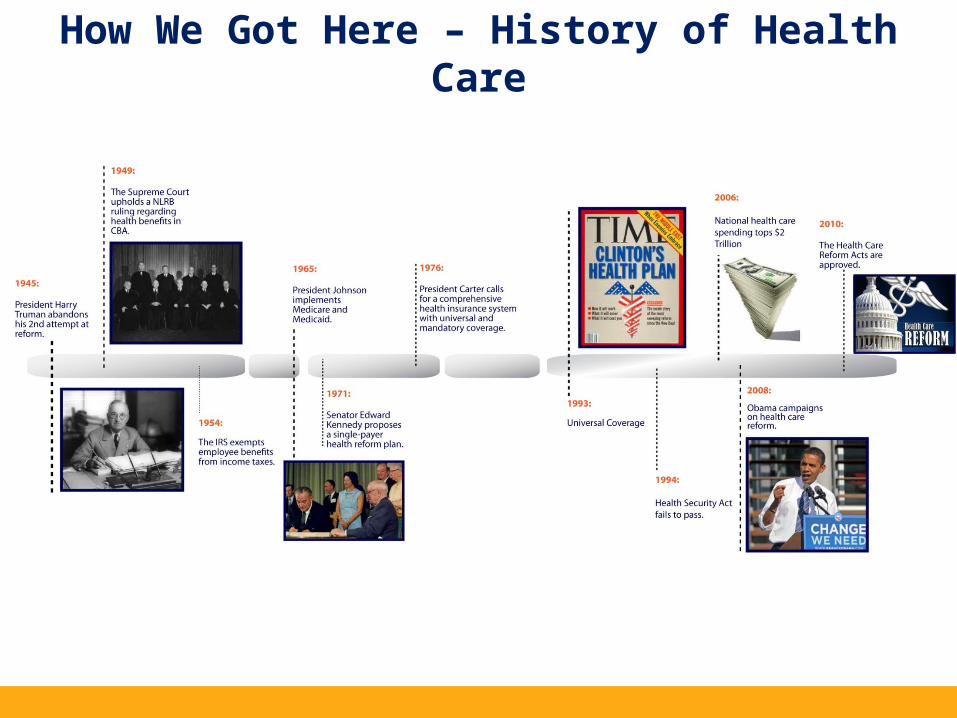

How We Got Here – History of Health Care

How Bill Was Enacted – What Does it Say Again?

Two Acts – A Framework

2000 pagesTotals to 3 million pages of regulations

Portion of Bill Already Repealed

• Expanded 1099 Reporting – Corporate Payees and “Property”

• Free Choice Vouchers• House Repealed Health Care Reform

o 245-189 vote to approve bill entitled “Repealing the Job-Killing Health Care Law Act” in 2011.

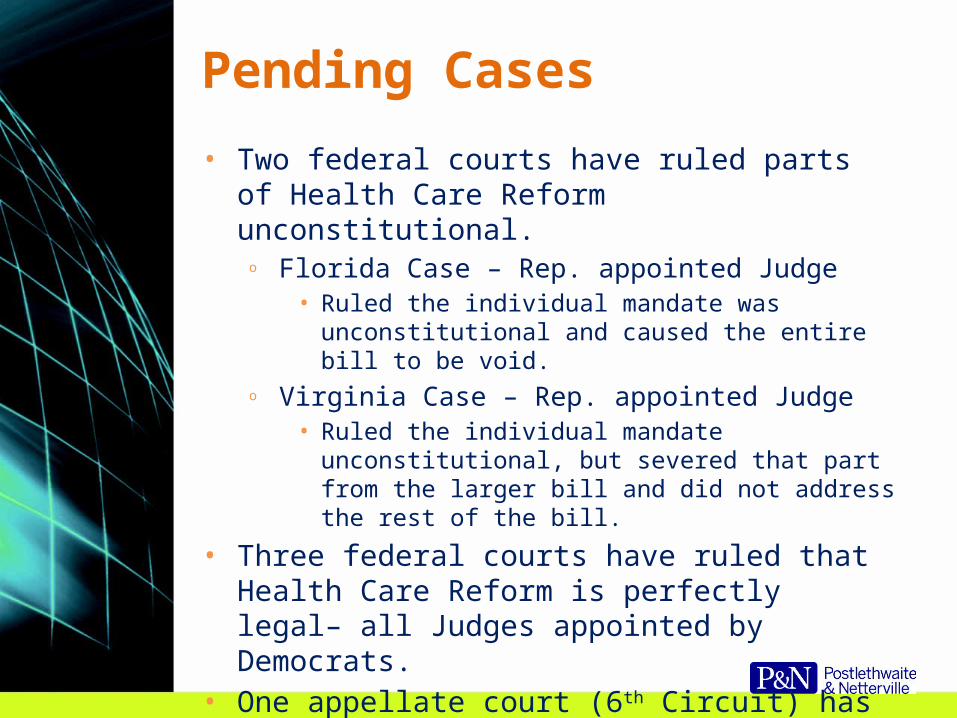

Pending Cases

• Two federal courts have ruled parts of Health Care Reform unconstitutional.o Florida Case – Rep. appointed Judge

• Ruled the individual mandate was unconstitutional and caused the entire bill to be void.

o Virginia Case – Rep. appointed Judge• Ruled the individual mandate unconstitutional, but severed

that part from the larger bill and did not address the rest of the bill.

• Three federal courts have ruled that Health Care Reform is perfectly legal– all Judges appointed by Democrats.

• One appellate court (6th Circuit) has upheld the law as constitutional. One dissenting Judge (Reagan appointee).

The Devil Is In the Details

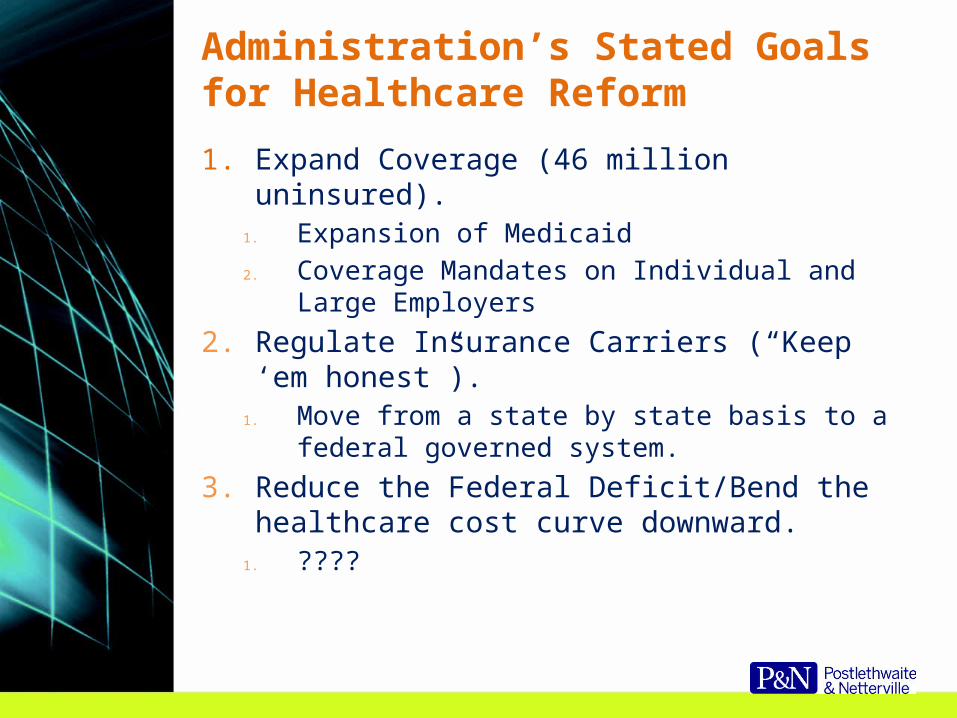

Administration’s Stated Goals for Healthcare Reform1. Expand Coverage (46 million uninsured).

1. Expansion of Medicaid2. Coverage Mandates on Individual and Large Employers

2. Regulate Insurance Carriers (“Keep ‘em honest”).1. Move from a state by state basis to a federal governed

system.3. Reduce the Federal Deficit/Bend the healthcare cost

curve downward.1. ????

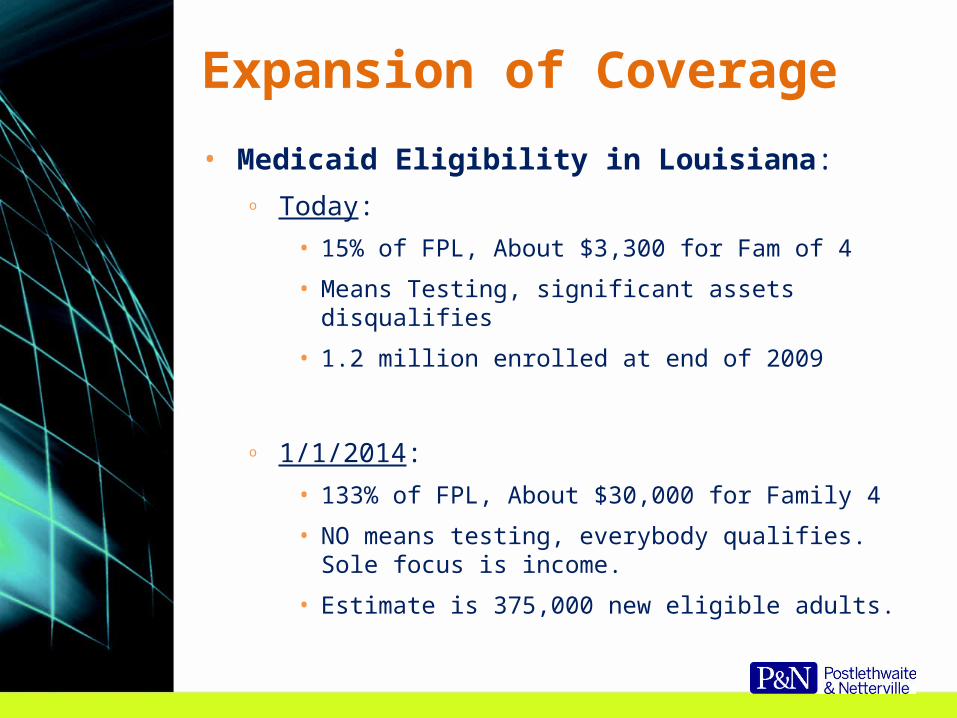

Expansion of Coverage

• Medicaid Eligibility in Louisiana:o Today:

• 15% of FPL, About $3,300 for Fam of 4

• Means Testing, significant assets disqualifies

• 1.2 million enrolled at end of 2009

o 1/1/2014: • 133% of FPL, About $30,000 for Family 4

• NO means testing, everybody qualifies. Sole focus is income.

• Estimate is 375,000 new eligible adults.

Expansion of Coverage

• Medicaid expansion will be funded by the federal government as follows:o 2014-2016: 100% FMAPo 2017: 95% FMAPo 2018: 94% FMAPo 2019: 93% FMAPo 2020 and beyond: 90% FMAP

• State is responsible for the rest.• For 2011 (Q1), the FMAP for Louisiana is

approximately 81% with ARRA. Set to drop to 63%.

Expansion of Coverage

• State based Exchanges operational by January 1, 2014.o Web portal to compare insurance choices

• For 2014-2016, Exchanges available to individuals and small groups (less than 100 employees, with State given authority to reduce to 50 employees).

• States authorized to open Exchange to Large Employers in 2017.

• Not all insurers are required to offer insurance through Exchange and Exchange is not required to offer all carriers and all products.

Expansion of Coverage

• Standardization of benefits (essential health benefits package)o Bronze, Silver, Gold and Platinum

• Insurers must offer at least one silver and one gold

o Catastrophic Plan – maximum cost sharing limits (except for 3 primary care visits); only available if under 30

o All plans offered in Exchange must be certified as “qualified health plans”

“Qualified Health Plans”

• Will be offered on state-operated exchanges beginning in 2014

• Requirements:o Offer the “essential benefits package”o Uniformity in premiums for each level of plan coverageo Limits on cost-sharing (5,900 individual and 11,900 family

and deductibles (2,000 for single and 4,000 for family). Deductible limits only applicable for small group plans.

o Underwriting requirements – Modified Community Rating

• State-based Exchanges available to individuals and small businesses (100 or fewer employees)

Exchanges

• Employers participating in the Exchanges specify level of support (e.g. Silver) and employee can select among qualified health plans that offer that level of coverage.o Potential for employees to be enrolled in

multiple insurance plans.

• Participating employers must make Exchange coverage available to ALL full time employees.

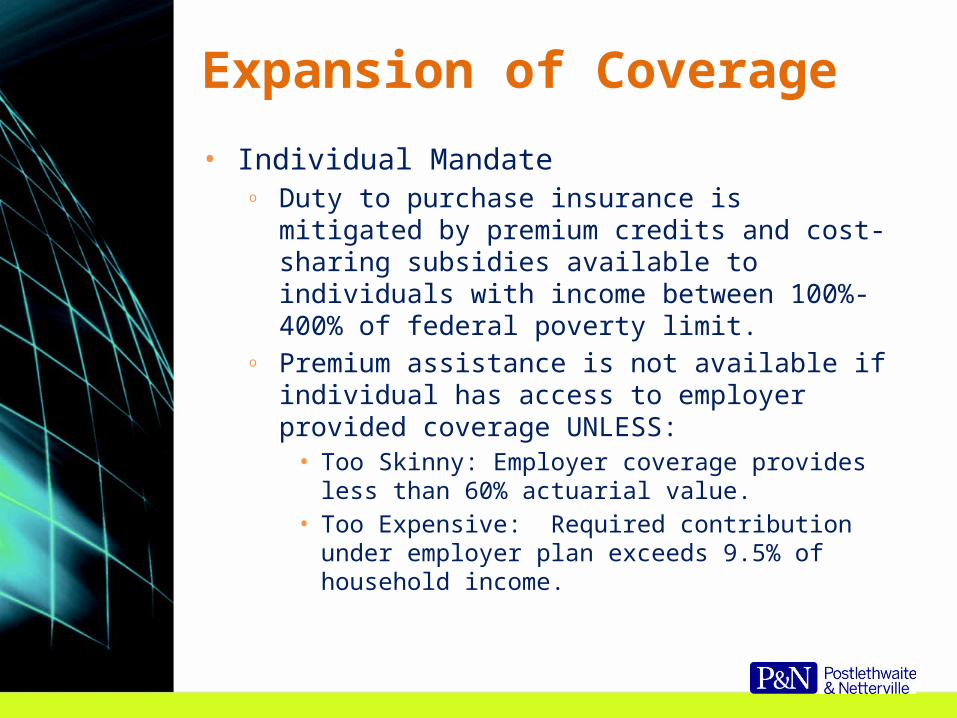

Expansion of Coverage• Individual Mandate

o With limited exceptions, ALL individuals must maintain “minimum essential coverage” or pay a penalty.

• Government provided coverage• Employer sponsored coverage• Exchange coverage.

• Exemption from mandate if required contribution to purchase insurance exceeds 8% of household income.

• Penalty amount is the lesser of a flat dollar amount of percentage of income.o 2014: $95 or 1% of household incomeo 2015: $325 or 2% of household incomeo 2016 and later: $695 or 2.5% of household income

Expansion of Coverage

• Individual Mandateo Duty to purchase insurance is mitigated by

premium credits and cost-sharing subsidies available to individuals with income between 100%-400% of federal poverty limit.

o Premium assistance is not available if individual has access to employer provided coverage UNLESS:

• Too Skinny: Employer coverage provides less than 60% actuarial value.

• Too Expensive: Required contribution under employer plan exceeds 9.5% of household income.

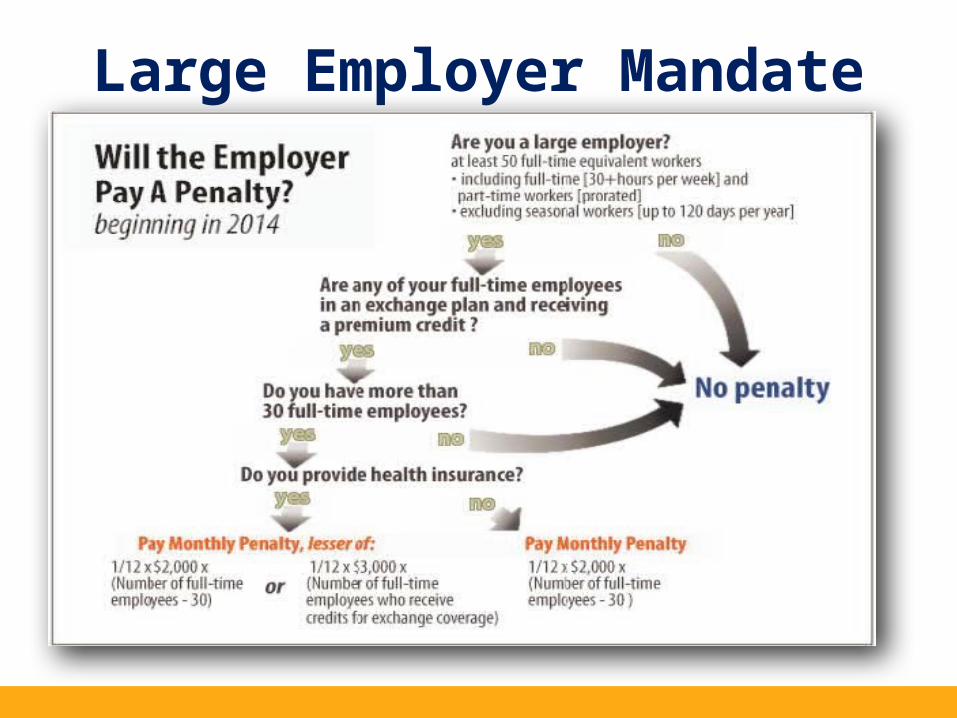

Large Employer Mandate

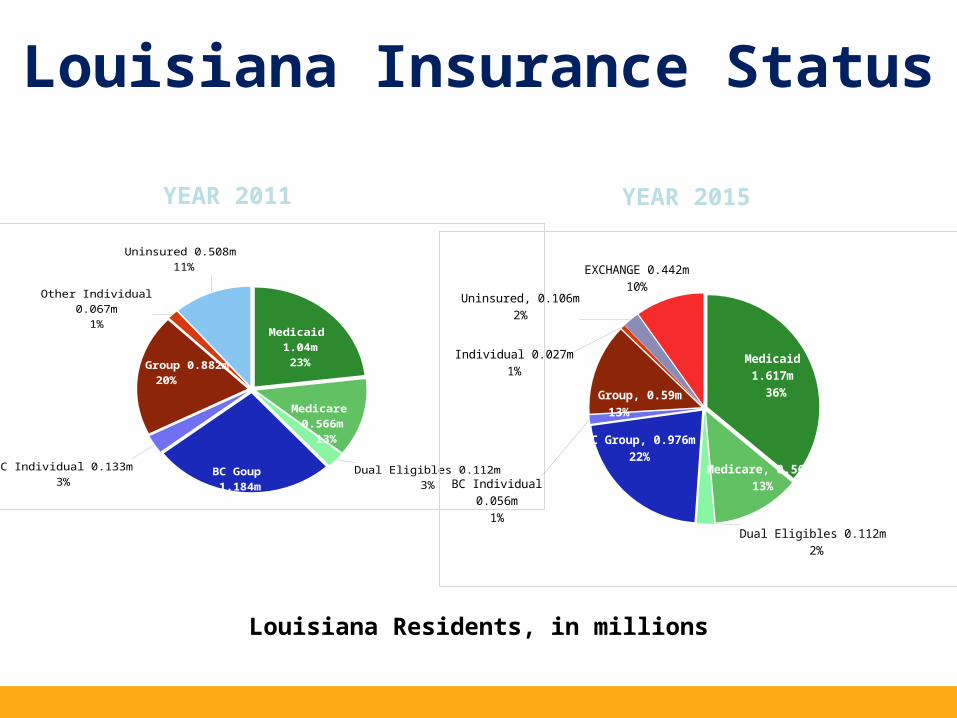

Louisiana Insurance Status

Medicaid 1.04m 23%

Medicare 0.566m

13%

Dual Eligibles 0.112m3%

BC Goup 1.184m

26%

BC Individual 0.133m3%

Other Group 0.882m20%

Other Individual 0.067m1%

Uninsured 0.508m 11%

Medicaid 1.617m

36%

Medicare, 0.566m13%

Dual Eligibles 0.112m 2%

BC Group, 0.976m22%

BC Individual 0.056m1%

Comm. Group, 0.59m13%

Individual 0.027m1%

Uninsured, 0.106m2%

EXCHANGE 0.442m10%

Louisiana Residents, in millions

YEAR 2011 YEAR 2015

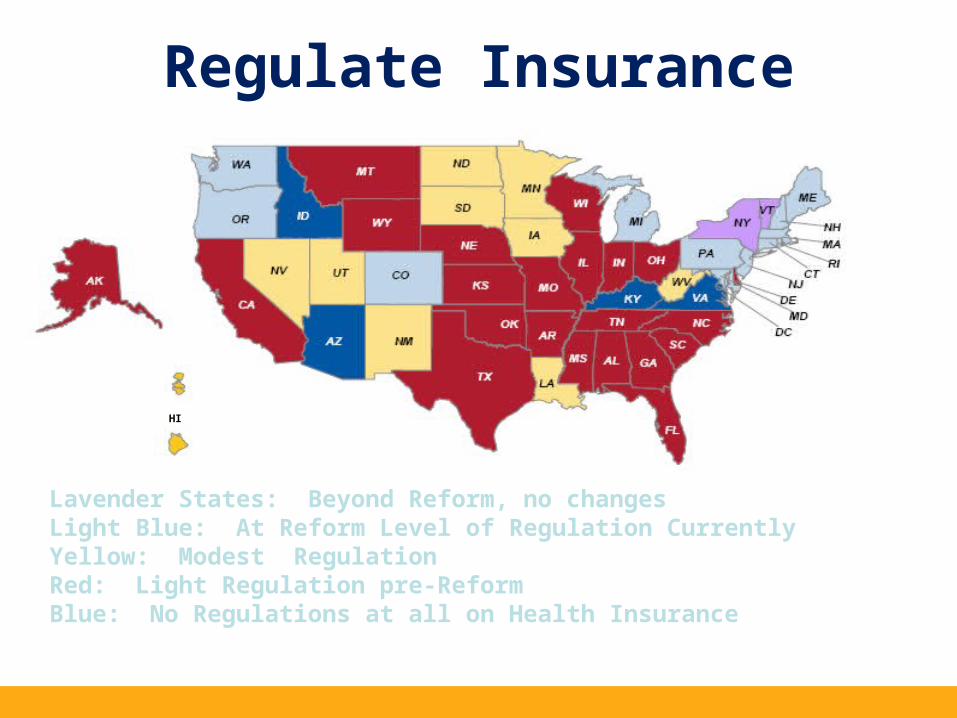

Lavender States: Beyond Reform, no changesLight Blue: At Reform Level of Regulation CurrentlyYellow: Modest Regulation Red: Light Regulation pre-ReformBlue: No Regulations at all on Health Insurance

Regulate Insurance

HI

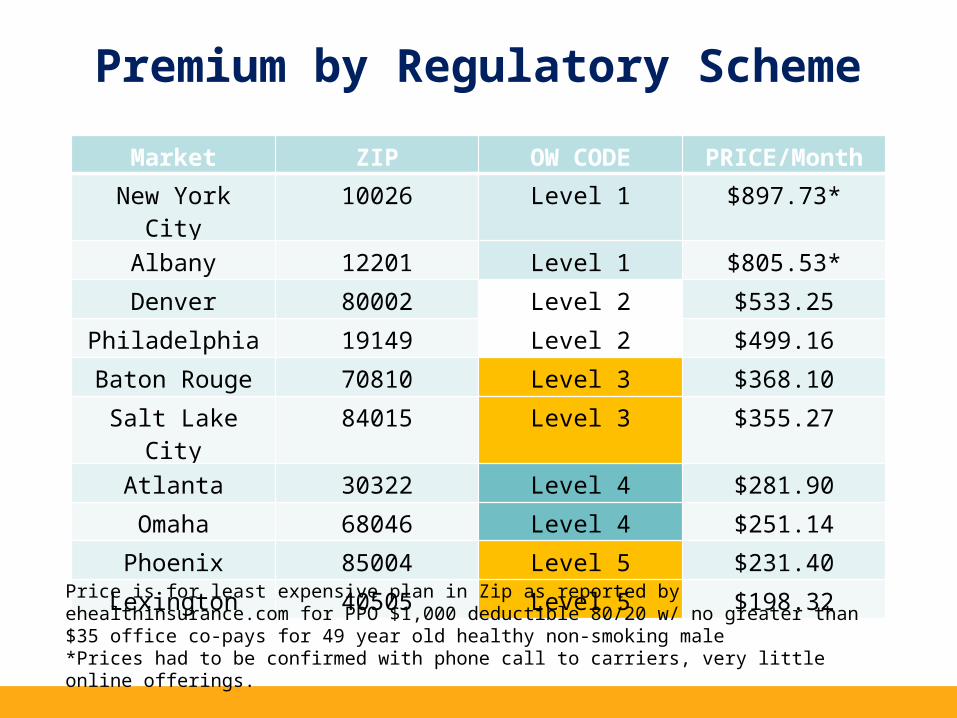

Premium by Regulatory Scheme

Markt

Market ZIP OW CODE PRICE/Month

New York City 10026 Level 1 $897.73*

Albany 12201 Level 1 $805.53*

Denver 80002 Level 2 $533.25

Philadelphia 19149 Level 2 $499.16

Baton Rouge 70810 Level 3 $368.10

Salt Lake City 84015 Level 3 $355.27

Atlanta 30322 Level 4 $281.90

Omaha 68046 Level 4 $251.14

Phoenix 85004 Level 5 $231.40

Lexington 40505 Level 5 $198.32

Price is for least expensive plan in Zip as reported by ehealthinsurance.com for PPO $1,000 deductible 80/20 w/ no greater than $35 office co-pays for 49 year old healthy non-smoking male*Prices had to be confirmed with phone call to carriers, very little online offerings.

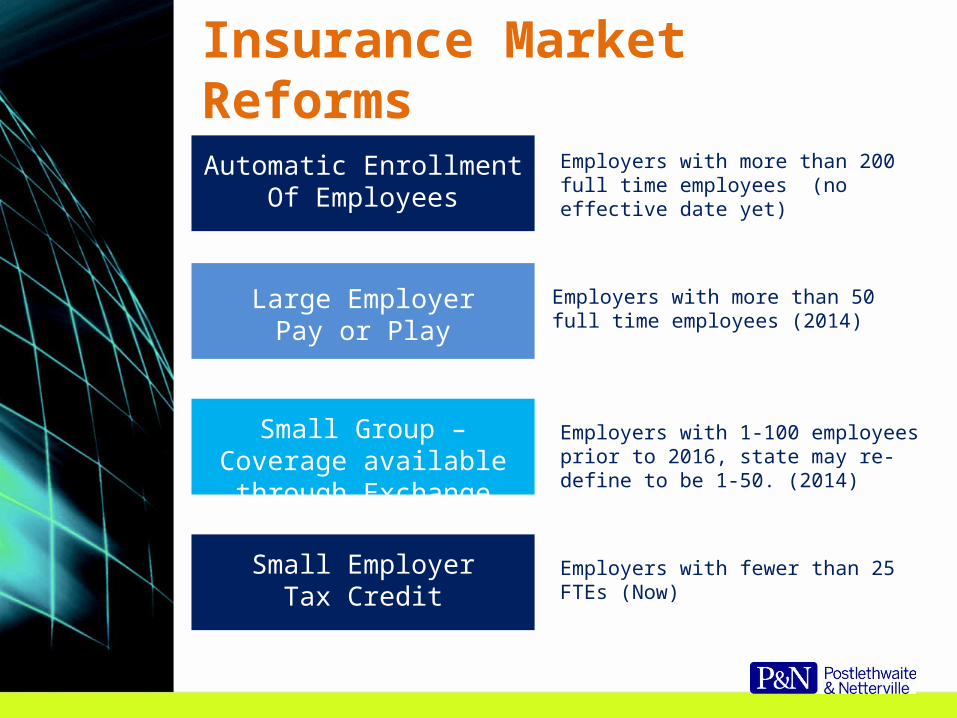

Insurance Market Reforms

Automatic EnrollmentOf Employees

Large EmployerPay or Play

Small Group – Coverage available through Exchange

Small EmployerTax Credit

Employers with more than 200 full time employees (no effective date yet)

Employers with more than 50 full time employees (2014)

Employers with 1-100 employees prior to 2016, state may re-define to be 1-50. (2014)

Employers with fewer than 25 FTEs (Now)

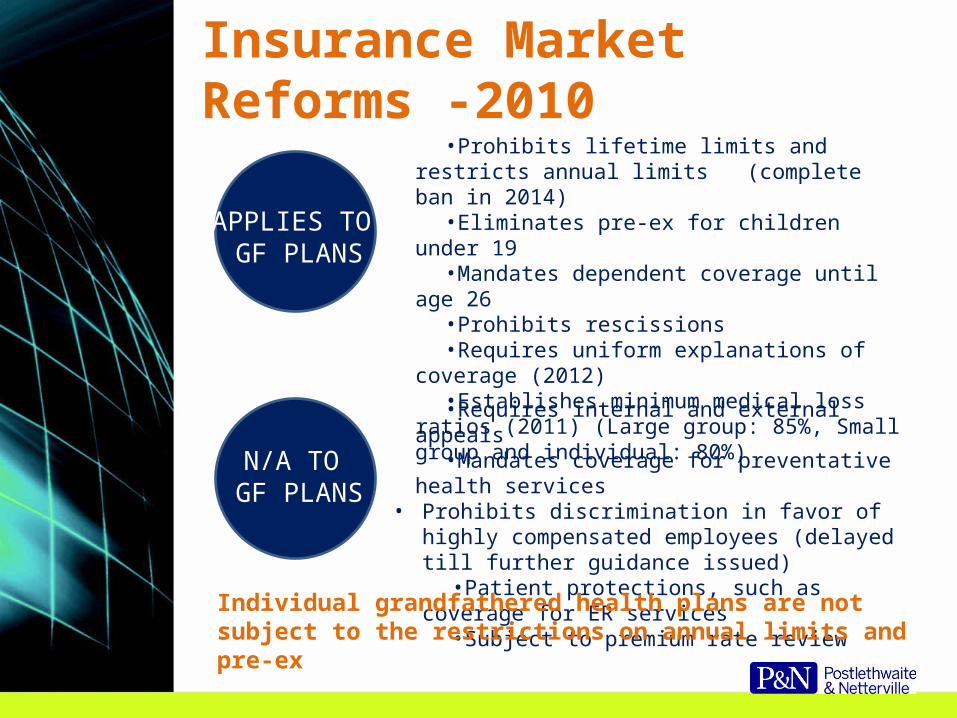

Insurance Market Reforms -2010•Prohibits lifetime limits and restricts annual limits

(complete ban in 2014)•Eliminates pre-ex for children under 19•Mandates dependent coverage until age 26•Prohibits rescissions•Requires uniform explanations of coverage (2012)•Establishes minimum medical loss ratios (2011)

(Large group: 85%, Small group and individual: 80%)

APPLIES TO GF PLANS

N/A TO GF PLANS

•Requires internal and external appeals•Mandates coverage for preventative health services

• Prohibits discrimination in favor of highly compensated employees (delayed till further guidance issued)

•Patient protections, such as coverage for ER services•Subject to premium rate review

Individual grandfathered health plans are not subject to the restrictions on annual limits and pre-ex

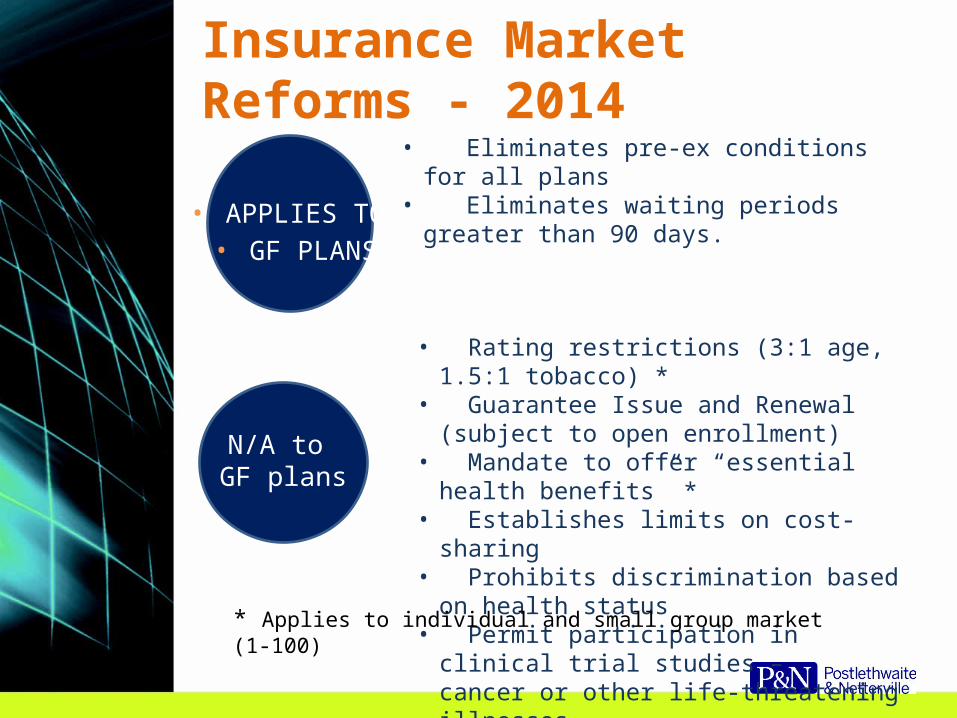

Insurance Market Reforms - 2014

• APPLIES TO • GF PLANS

• Eliminates pre-ex conditions for all plans• Eliminates waiting periods greater than 90

days.

N/A to GF plans

• Rating restrictions (3:1 age, 1.5:1 tobacco) *• Guarantee Issue and Renewal (subject to

open enrollment)• Mandate to offer “essential health benefits” *• Establishes limits on cost-sharing• Prohibits discrimination based on health

status• Permit participation in clinical trial studies –

cancer or other life-threatening illnesses

* Applies to individual and small group market (1-100)

How To Lose Grandfathered Status

• Have no other choice• Significantly reduce or cut benefits• Raise co-insurance charge• Significantly raise fixed dollar copayment charges• Significantly raise fixed amount deductibles• Significantly lower employer contributions• Add an annual limit, or decrease an existing annual limit• Change of insurance company between June 14

through November 14, 2010 will also result in loss of grandfather status for group plans

Dependent Coverage Expanded - 2011

• Plan years beginning on or after 9/23/2010.• Plans that provide dependent coverage of children

must make coverage available to a child until the child attain age 26, even if married and not a student.

• Plan cannot condition coverage on child being a “dependent” for tax purposes.

• Plan cannot charge extra for the child.• No more imputed income concerns through age 27• Grandfathered plans until 2014 – only if child is not

eligible for other coverage.• Estimated to add 1,250,000 young adults.• Children can be a son, daughter, adopted child,

stepchild or eligible foster child.

Unintended Consequences of Extension of Insurance to Children

Reduce Federal Deficit/BendCost of Health Care DownwardKeep in mind

If reform does not reduce the cost or volume (or both) of medical goods and services, then these costs/services continue to be performed and the health care providers must still be paid.

Who pays the cost may change – but the amount that must be paid will not change.

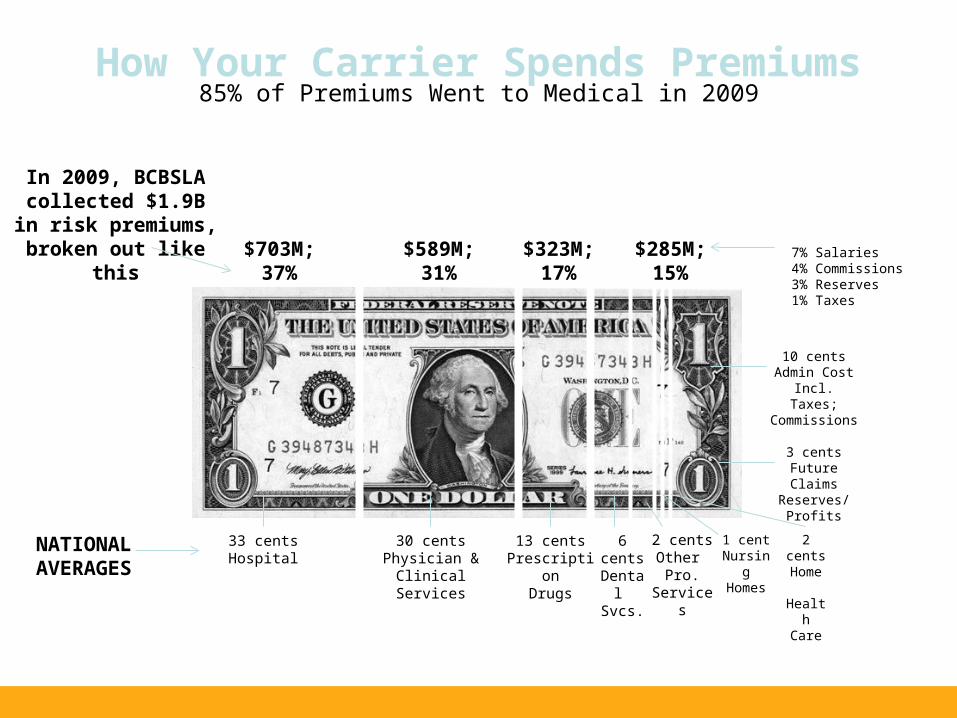

How Your Carrier Spends Premiums85% of Premiums Went to Medical in 2009

$703M;37%

$589M;31%

$285M;15%

$323M;17%

In 2009, BCBSLA collected $1.9B in risk premiums,

broken out like this

NATIONALAVERAGES

33 centsHospital

30 centsPhysician & Clinical

Services

13 centsPrescription

Drugs

6 centsDental

Svcs.

2 centsOther

Pro. Services

1 centNursingHomes

2 centsHome

HealthCare

3 centsFuture Claims

Reserves/Profits

10 centsAdmin Cost Incl.

Taxes; Commissions

7% Salaries4% Commissions3% Reserves1% Taxes

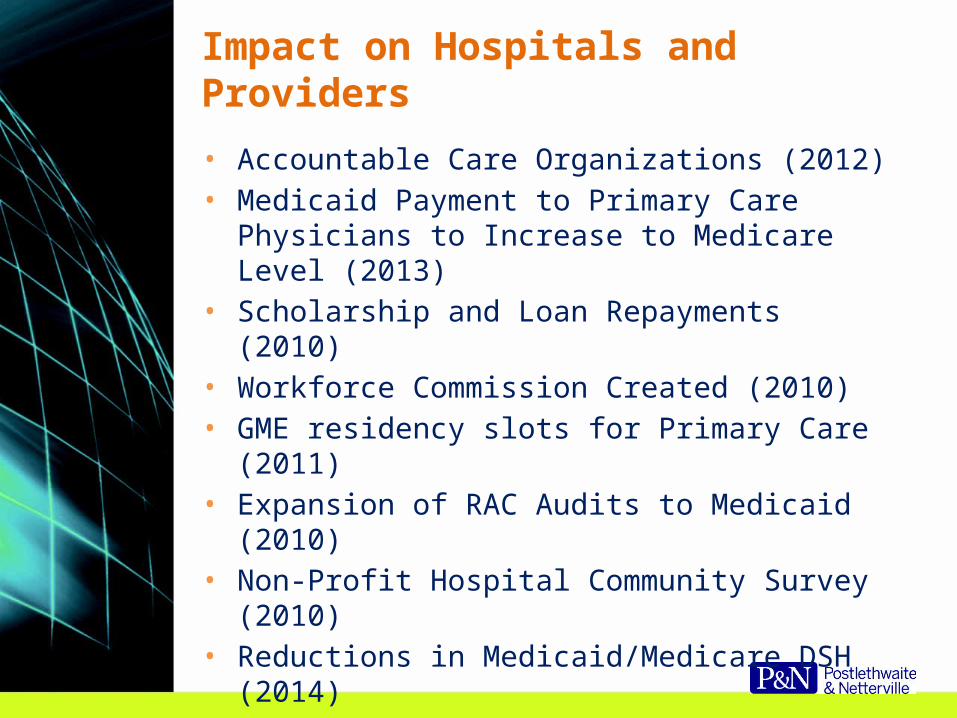

Impact on Hospitals and Providers

• Accountable Care Organizations (2012)• Medicaid Payment to Primary Care

Physicians to Increase to Medicare Level (2013)

• Scholarship and Loan Repayments (2010)• Workforce Commission Created (2010)• GME residency slots for Primary Care (2011)• Expansion of RAC Audits to Medicaid (2010)• Non-Profit Hospital Community Survey

(2010)• Reductions in Medicaid/Medicare DSH (2014)• Readmission Payment Adjustments (2012)• Physician Quality Reporting (2012)

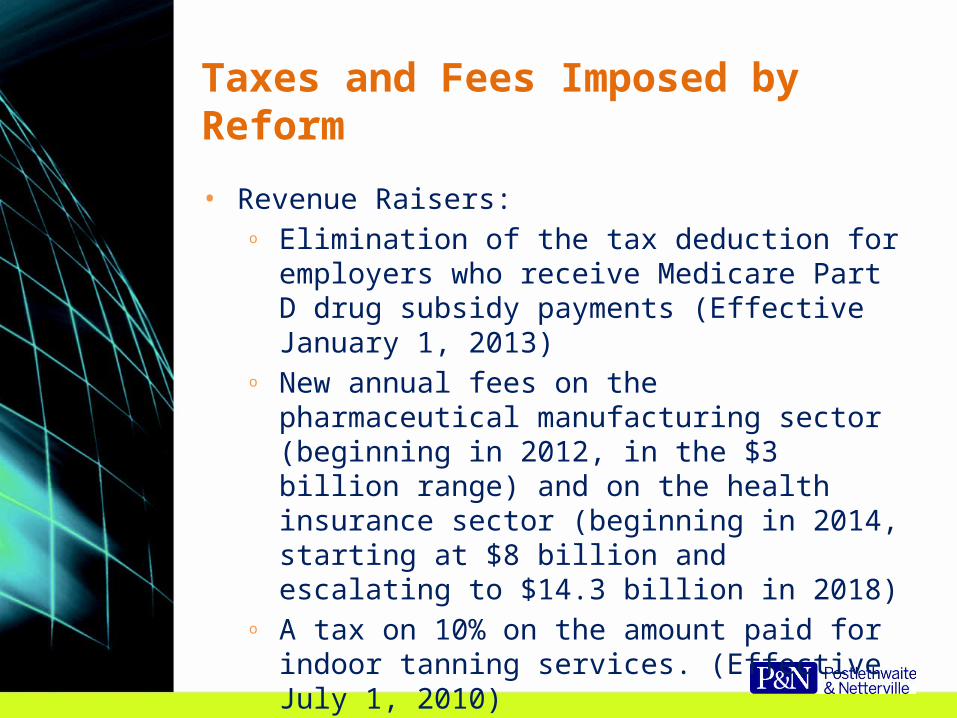

Taxes and Fees Imposed by Reform

• Revenue Raisers:o Elimination of the tax deduction for employers who

receive Medicare Part D drug subsidy payments (Effective January 1, 2013)

o New annual fees on the pharmaceutical manufacturing sector (beginning in 2012, in the $3 billion range) and on the health insurance sector (beginning in 2014, starting at $8 billion and escalating to $14.3 billion in 2018)

o A tax on 10% on the amount paid for indoor tanning services. (Effective July 1, 2010)

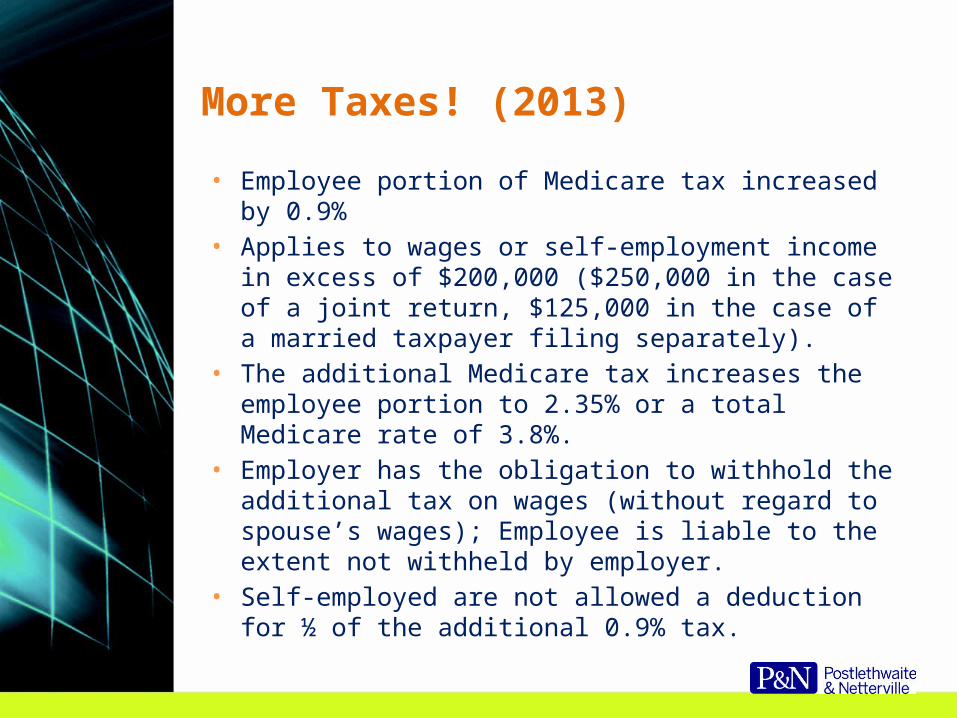

More Taxes! (2013)

• Employee portion of Medicare tax increased by 0.9%• Applies to wages or self-employment income in excess

of $200,000 ($250,000 in the case of a joint return, $125,000 in the case of a married taxpayer filing separately).

• The additional Medicare tax increases the employee portion to 2.35% or a total Medicare rate of 3.8%.

• Employer has the obligation to withhold the additional tax on wages (without regard to spouse’s wages); Employee is liable to the extent not withheld by employer.

• Self-employed are not allowed a deduction for ½ of the additional 0.9% tax.

The Taxes Keep Piling On! (2013)

• Individuals, estates and trusts required to pay 3.8% tax on net investment income such as interest, dividends, annuities, royalties, rents, capital gains and income from passive activities.

• Applies to the income in excess of $250,000 for joint returns, $125,000 for married filing separate and $200,000 for all others

More Taxes!!! I’m not kidding!

• Cadillac Tax (2018)o 40% excise tax imposed on insurance

company offering high cost Cadillac plans.o What is this evil “high-cost” plan?

• Employee-only coverage of $10,200 or more• Family coverage of $27,500 or more• Amounts indexed for inflation thereafter.

Other Provisions of Health Care Reform

• Small Employer Tax Credits• Over the Counter Drugs• Increase Penalty on Non-Qualified Expenses from HSA,

MSA• $2,500 Limitation on Health FSA under Cafeteria Plans

Small Employer Health Insurance CreditEffective 2010

• Allows eligible small employers to claim a 35% credit (25% in the case of tax-exempt employers) for premiums paid toward health coverage for its employees in tax years beginning 2010 through 2013. These percents increase to 50% and 35%, respectively, in 2014.

• An eligible small employer is an employer that has no more than 25 full-time employees and the average annual compensation of these employees is not greater than $50,000.

• The credit is reduced by 6.6667% for each full-time employee in excess of 10 employees and by 4% for each $1,000 that average annual compensation paid to the employee exceeds $25,000.

• After 2013, employer must participate in an insurance exchange to be eligible for credit.

Small Employer Health Credit (Cont.)Effective 2010• Must pay at least 50% of premium for all

employees and the percentage must be uniform among all employees, except for during the year 2010

• Steps in determining credito Determine number of employeeso Determine number of hours of service by those

employeeso Calculate number of employer’s FTEso Determine average annual wages paid per FTEo Determine premium taken into account

• Effective for tax year 2010; See Notice 2010-44

Credit Phaseout

• Example: For the 2010 taxable year, a taxable small employer has 12 FTEs and average annual wages of $30,000. The employer pays $96,000 in health insurance premiums for its employees and meets all other requirements for the credit.

• The amount of the credit is calculated as follows:

o The initial amount of the credit determined before any reduction: (35% x $96,000) = $33,600.

o Credit reduction for FTEs in excess of 10: ($33,600 x 2/15) = $4,480.

o Credit reduction for wages in excess of $25,000: ($33,600 x $5,000/$25,000) = $6,270.

o Total credit reduction: ($4,480 + $6,720) = $11,200.o Total 2010 tax credit equals $22,400.

No More OTC Medications - 2011

• Over-The-Counter medications, except insulin, items no longer reimbursable without a prescription

• Bandages and supplies may still be reimbursed• Impact on FSA, HRA and HSA• Most cafeteria plans will need to be amended – look for

a reference to 213(d)• Failure to amend from 213(d) would make all benefits

taxable to all employees

HSA, MSA Excise Tax - 2011

• The excise tax for paying nonqualified costs is increased to 20%

W-2 Reporting - 2013

• Postponed till calendar year 2012 – W-2s issued in 2013.

• Employer with less than 250 W-2s from previous year is exempt.

• Employers are not required to report aggregate cost of applicable employer-sponsored coverage prior to January, 2013.

• Cost reported is aggregate cost including both employer and employee portion.

• Notice 2011-28 discusses methods used to determine aggregate cost.

FSA Cap - 2013

• Limited to $2,500 each year• Indexed for inflation• Previously no cap• Family typically participated in just one plan