Embed Size (px)

Citation preview

2010 Legislative HighlightsFor Redevelopment

(Community Development and Urban Renewal)

J. Craig SmithKyle C. Fielding

Smith | Hartvigsen, PLLC

215 South State Street, Suite 600Salt Lake City, UT 84111www.smithhartvigsen.com

801.413.1600

Text © 2010 Smith|Hartvigsen, PLLCSlide 1

2010 Legislative Highlights for Redevelopment

(Community Development and Urban Renewal)

Text © 2010 Smith|Hartvigsen, PLLCSlide 2

•S.B. 197 becomes effective as of May 11, 2010

•New notice requirements

•Attorney certification for TEC approval

•Inter-project-area loans

•Enhanced protection against challenges

•Earlier collection of tax increment in certain circumstances

•Statutory relief from housing fund obligations

Summary of Significant Changes

2010 Legislative Highlights for Redevelopment

Text © 2010 Smith|Hartvigsen, PLLCSlide 3

•Technical and grammatical improvements

•Expressly authorizes environmental remediation activities within an economic development project area (previously was only expressly authorized under urban renewal)

•If the agency disposes of property then the agency must provide a summary on the Utah Public Notice Website (new requirement) and by newspaper publication (old requirement, still effective)

•“Successor Taxing Entities” bound under a CDA interlocal agreement or resolution

Summary of Other Changes

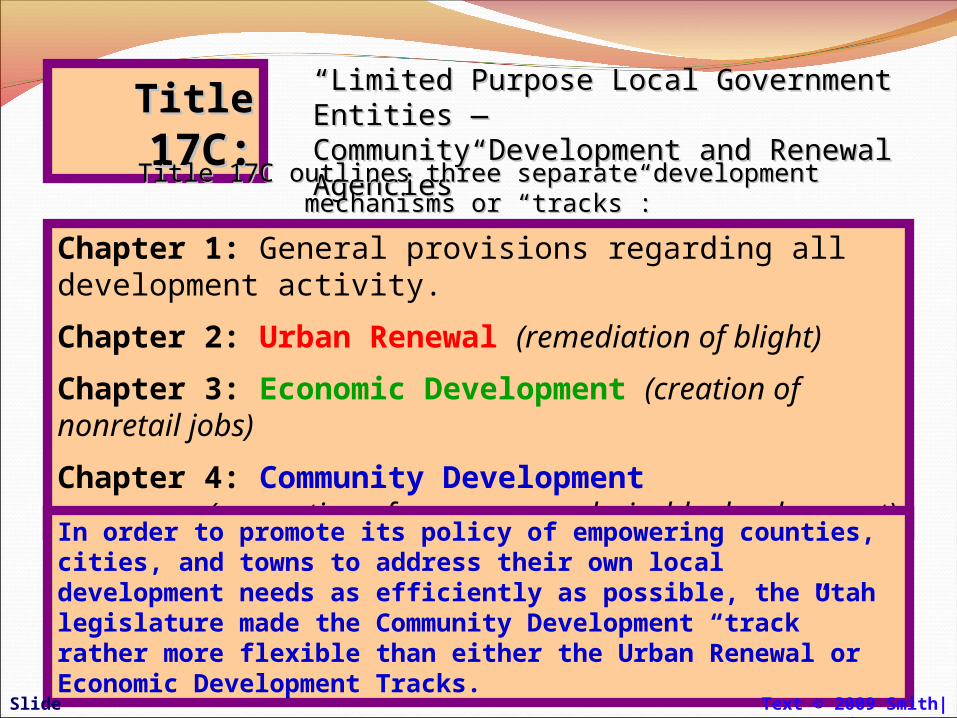

““Limited Purpose Local Government Entities ― Limited Purpose Local Government Entities ― Community Development and Renewal Agencies”Community Development and Renewal Agencies”TitleTitle 17C: 17C:

Chapter 1: General provisions regarding all development activity.

Chapter 2: Urban Renewal (remediation of blight)

Chapter 3: Economic Development (creation of nonretail jobs)

Chapter 4: Community Development(promotion of necessary or desirable development)

In order to promote its policy of empowering counties, cities, and towns to address their own local development needs as efficiently as possible, the Utah legislature made the Community Development “track” rather more flexible than either the Urban Renewal or Economic Development Tracks.

Title 17C outlines three separate development mechanisms or “tracks”:Title 17C outlines three separate development mechanisms or “tracks”:

Text © 2009 Smith|Hartvigsen, PLLCSlide 4

1. The Agency Designates a Survey Area

2. Parcel-by-parcel Blight Study

4. Blight Hearing

5. Agency Finding of Blight & Project Area selection

The TEC must approve the blight finding or demonstrate the absence of blight.

7a. Preparation of the Draft Project Area Plan

3. Mailed and published notice of public Blight Hearing

7b. Preparation of the Draft Project Area Budget

Inactive Superfund, Industrial, & Airport sites blighted de jure

6. Preparation of Plan and Budget

The TEC must approve the Budget, setting the Project Area Base Value; attorney must Certify

8a. Public review of Draft Plan

8b. Public review of Draft Budget

9a. Mailed & published notice of Draft Plan Hearing

10. Public Hearings on DRAFT PLAN & DRAFT BUDGET.

11. Agency adoption of Plan & Budget. 12. Community

Legislative adoption of the Plan by Ordinance.

13. Transmission of post-adoption notice to county officials and taxing entities.

9b. Mailed & published notice of Budget Hearing

Urban RenewalUrban Renewal

1. Agency selection of Project Area & authorization for preparation of Plan and Budget

2a. Preparation of Draft Plan

3a. Public plan review 3b. Public budget review

4a. Notice of Plan Hearing

2b. Preparation of Draft Budget

The TEC must approve the Budget; attorney must Certify TEC approval process

5. Public Hearings on the Draft Plan and Budget

7. Community legislative adoption of Plan by ordinance.

8. Transmission of post-adoption notice to county officials and taxing entities.

6. Agency adoption of Plan & Budget

Economic DevelopmentEconomic Development

Text © 2009 Smith|Hartvigsen, PLLCSlide Slide 55

4b. Notice of Budget Hearing

Compare the complexity of Compare the complexity of Urban Renewal Urban Renewal

& Economic Development …& Economic Development …

Community DevelopmentCommunity Development

Text © 2009 Smith|Hartvigsen, Text © 2009 Smith|Hartvigsen, PLLCPLLC

1. The Agency Selects a Project Area and authorizes preparation of the Project Area Plan and Negotiations with relevant Taxing Entities.

2b. Preparation of the Draft Project Area Plan

3b. Public review of Plan3a. Tax increment Agreements with willing Taxing Entities: Adopted by Resolution or Interlocal Agreement 4b. Notice of Plan Hearing

5. Public Hearing: Draft Plan.

2a. Consultation with various Taxing Entities.

6. Agency adoption of Plan.

7. Community Ordinance adopting the Plan by.

8. Transmission of post-adoption notice to county & taxing entities.

NOTES:

Budget Adoption is optional; no hearing is required.

Community Development doesn’t require TEC approval either: The Agency deals directly with each taxing entity.

Slide Slide 66

… … with the with the straightforward straightforward simplicity of simplicity of Community Community Development.Development.

Public Notice RequirementsPublic Notice Requirements

Text © 2010 Smith|Hartvigsen, PLLCSlide 7

Quiz:Currently, what public notice is required for a public hearing regarding a draft Project Area Plan or draft Project Area Budget?

Answer:1)One newspaper publication (14 days)2)Mailed notice to property owners and taxing entities (30 days)

Public Notice of Plan and/or Budget HearingPublic Notice of Plan and/or Budget Hearing

Text © 2010 Smith|Hartvigsen, PLLCSlide 8

S.B. 197:

1)30-day mailed notice to property owners and taxing entities, and

2)14-day notice by either*:

i. publishing in the newspaper, ORii. posting on both the Utah Public Notice Website and the

community website

*You can always post and publish, if you want to, but you are only required to do either one or the other

When to Begin Tax Increment Collection?When to Begin Tax Increment Collection?

Text © 2010 Smith|Hartvigsen, PLLCSlide 9

Before: “Tax increment may not be paid to an agency for a tax year prior to the tax year following: (i) for an urban renewal or economic development project area plan, the effective date of the of the project area plan; and (ii) for a community development project area plan, the effective date of the interlocal agreement that establishes the agency’s right to receive tax increment.”

S.B. 197: Allows the taxing entity committee, or the taxing entity under a CDA interlocal agreement, to waive this requirement, thus allowing immediate tax increment collection

Inter-Project-Area LoansInter-Project-Area Loans

Text © 2010 Smith|Hartvigsen, PLLCSlide 10

Quiz:Currently, can you take tax increment generated from Project Area “A” and provide a development incentive for property within a different Project Area “B”?

Answer:Only for infrastructure, and only after determining that Project Area “A” will benefit from the expenditure in Project Area “B”

Inter-Project-Area LoansInter-Project-Area Loans

Text © 2010 Smith|Hartvigsen, PLLCSlide 11

S.B. 197:

oAllows loans from one project area fund to another

oRequires approval by the Agency Board and the Community Legislative Body (Commission, Council)

oProjections for future tax increment in the borrowing project area must be sufficient to repay the loan for timely use in the loaning project area

oIf the borrowing project area is unable to repay the loan then the authorizing community must repay the loan to the project area fund

Attorney Certification RequirementsAttorney Certification Requirements

Text © 2010 Smith|Hartvigsen, PLLCSlide 12

S.B. 197 requires “attorney certification” of:

•Taxing Entity Committee Approval of a Project Area Budget (Urban Renewal or Economic Development), and

•Taxing Entity consent to tax increment under an interlocal agreement or resolution for a Community Development Project

*An agency cannot adopt a Project Area Budget requiring TEC approval before obtaining attorney certification

Attorney Certification RequirementsAttorney Certification Requirements

Text © 2010 Smith|Hartvigsen, PLLCSlide 13

Why require attorney certification?

•Justifies a 30-day contestability period. After 30 days, nobody can contest TEC approval

•Protects the community and agency

•Protects property owners by providing a safeguard over the rather unusual TEC approval process

Attorney Certification RequirementsAttorney Certification Requirements

Text © 2010 Smith|Hartvigsen, PLLCSlide 14

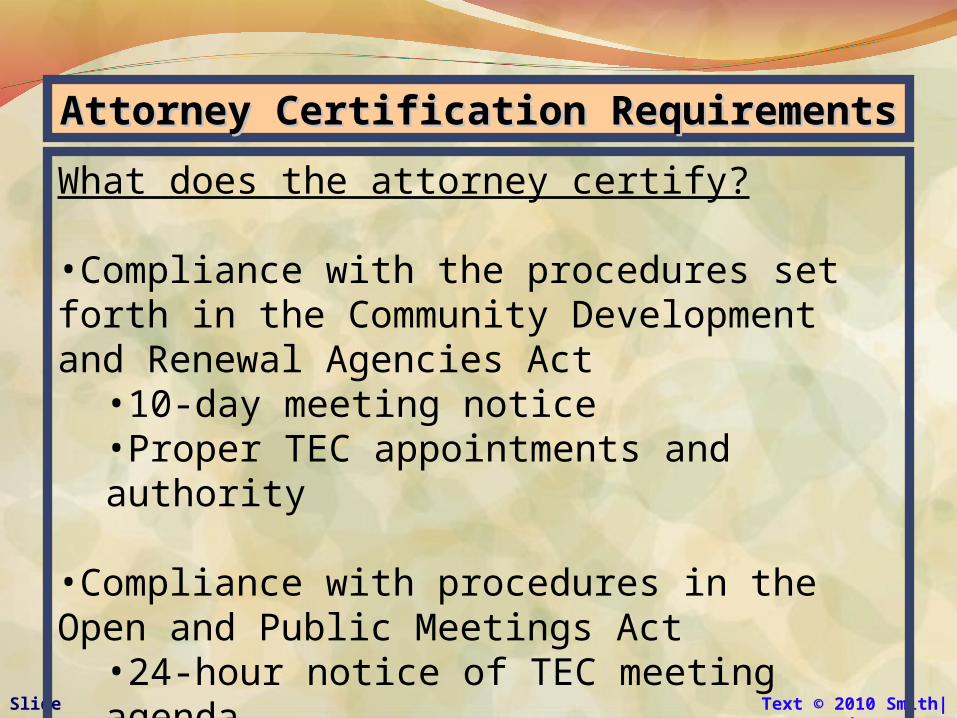

What does the attorney certify?

•Compliance with the procedures set forth in the Community Development and Renewal Agencies Act•10-day meeting notice•Proper TEC appointments and authority

•Compliance with procedures in the Open and Public Meetings Act•24-hour notice of TEC meeting agenda•Other procedural requirements

Attorney Certification of TEC ApprovalAttorney Certification of TEC Approval

Text © 2010 Smith|Hartvigsen, PLLCSlide 15

Practical Pointers:

•Involve an attorney before scheduling a TEC meeting, or anytime before executing a resolution or interlocal agreement for a CDA

•Involve the attorney in reviewing and/or drafting timelines, notices, agendas, and resolutions before they go out

•If any statutory procedures are not fully complied with, the attorney will not be able to provide a certification and the TEC will need to meet again

•Attorney certification of TEC approval is required before the Agency may adopt a Project Area Budget, or before an Agency may use funds under a CDA interlocal agreement or resolution

Housing RequirementsHousing Requirements

Text © 2010 Smith|Hartvigsen, PLLCSlide 16

2 Changes in S.B. 197:

(1) Expressly requires annual housing allocations in the Project Area Budget (no backloading)

BUT, IF YOU ALREADY BACKLOADED:

(2) Provides relief from making housing allocations to the extent tax increment is insufficient in the final years of the project

Questions?Redevelopment Attorneys

J. Craig [email protected]

Kyle C. [email protected]

Smith | Hartvigsen, PLLC

215 South State Street, Suite 600Salt Lake City, UT 84111www.smithhartvigsen.com

801.413.1600

Text © 2010 Smith|Hartvigsen, PLLCSlide 17