Embed Size (px)

Citation preview

©2010 Lifetime Brands, Inc.

LUS

SO

IN

TER

IOR

S

TOP TRENDS for 2011

EEMBRACINGMBRACING GGENERATIONAL ENERATIONAL DDIVERSITYIVERSITY

EEMBRACINGMBRACING GGENERATIONAL ENERATIONAL DDIVERSITYIVERSITY

©2010 Lifetime Brands, Inc.

1

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY

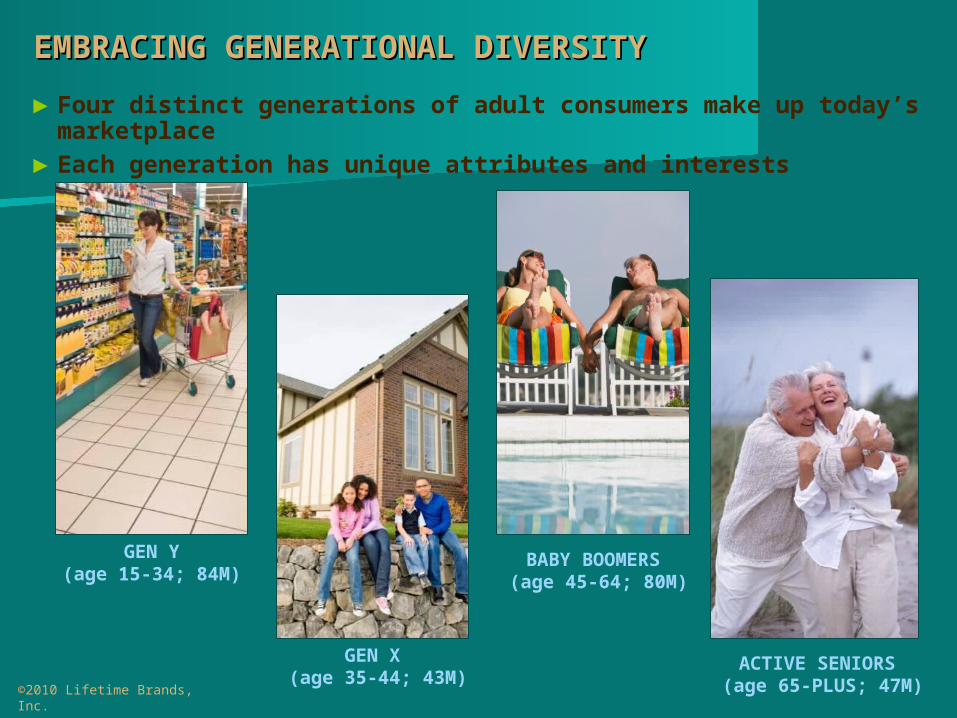

► Four distinct generations of adult consumers make up today’s marketplace

► Each generation has unique attributes and interests

BABY BOOMERS (age 45-64; 80M)

GEN X (age 35-44; 43M)

GEN Y(age 15-34; 84M)

ACTIVE SENIORS (age 65-PLUS; 47M)

©2010 Lifetime Brands, Inc.

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY

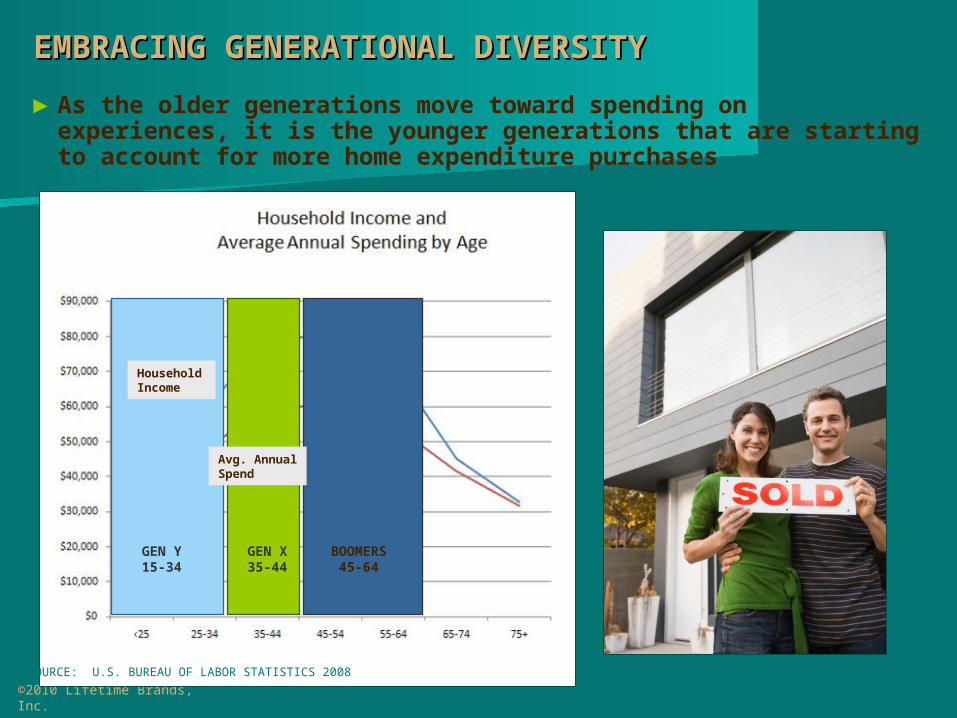

► As the older generations move toward spending on experiences, it is the younger generations that are starting to account for more home expenditure purchases

©2010 Lifetime Brands, Inc.

SOURCE: U.S. BUREAU OF LABOR STATISTICS 2008

BOOMERS45-64

GEN Y15-34

GEN X35-44

HouseholdIncome

Avg. AnnualSpend

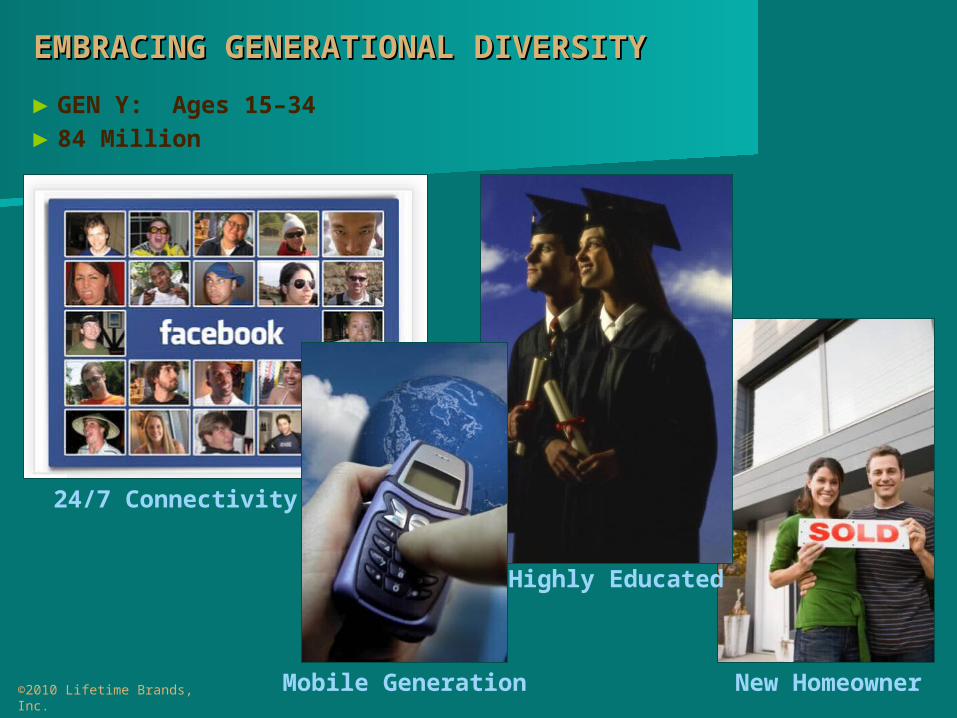

New Homeowner

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY

► GEN Y: Ages 15–34► 84 Million

©2010 Lifetime Brands, Inc.

24/7 Connectivity

Mobile Generation

Highly Educated

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY

► Gen Y (ages 15–34; 84 million; 22% of households) Earning power effected by later marriage

and more job hopping “Reverse mentoring”—tech savvy Gen Y is

influencing every preceding generation’s behavior and expectations;

66% of Gen X women choose Gen Y women as the most influential age group when it comes to defining trends in popular culture (PopSugar Media)

This young adult consumer is our most ethnically diverse generation: Targeting price points that understand limited

discretionary income yet a desire for unique product

Must understand the importance of technology for this new consumer

Love to entertain at home where everyone congregates in the kitchen

©2010 Lifetime Brands, Inc.

LIFETIM

E B

RA

ND

S

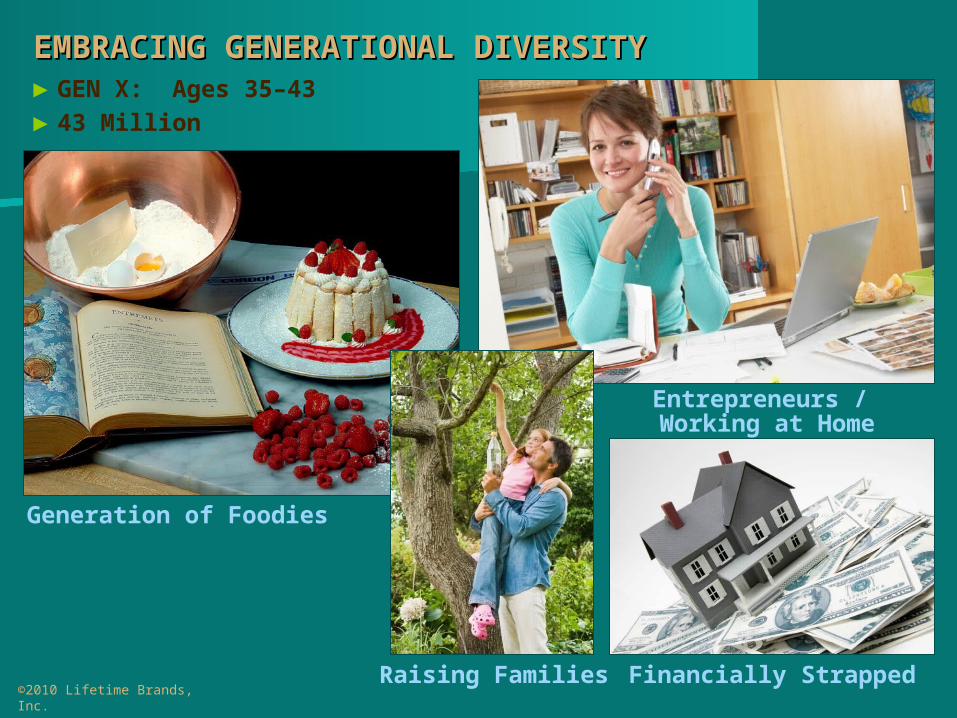

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY► GEN X: Ages 35–43 ► 43 Million

©2010 Lifetime Brands, Inc.

Generation of Foodies

Raising Families

Entrepreneurs / Working at Home

Financially Strapped

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY

► Gen X (ages 35–44; 43 million; 19% of households) Entering peak earning years as they turn 40 Stuck in starter homes due to the housing crisis Embracing domesticity; best skill set for the new economy At the forefront of bringing design into new places within the home:

Know how to market and merchandise to the Gen X’er ready to trade-up

They crave products which multi-task and help them save space Appeal to their design-savvy expectations – this generation sees

style as an important value alongside function Looking for solutions ; anything that can help them save time,

space or money

©2010 Lifetime Brands, Inc.

MA

E B

RU

NK

IN D

ES

IGN

LIFE

TIM

E BR

ANDS

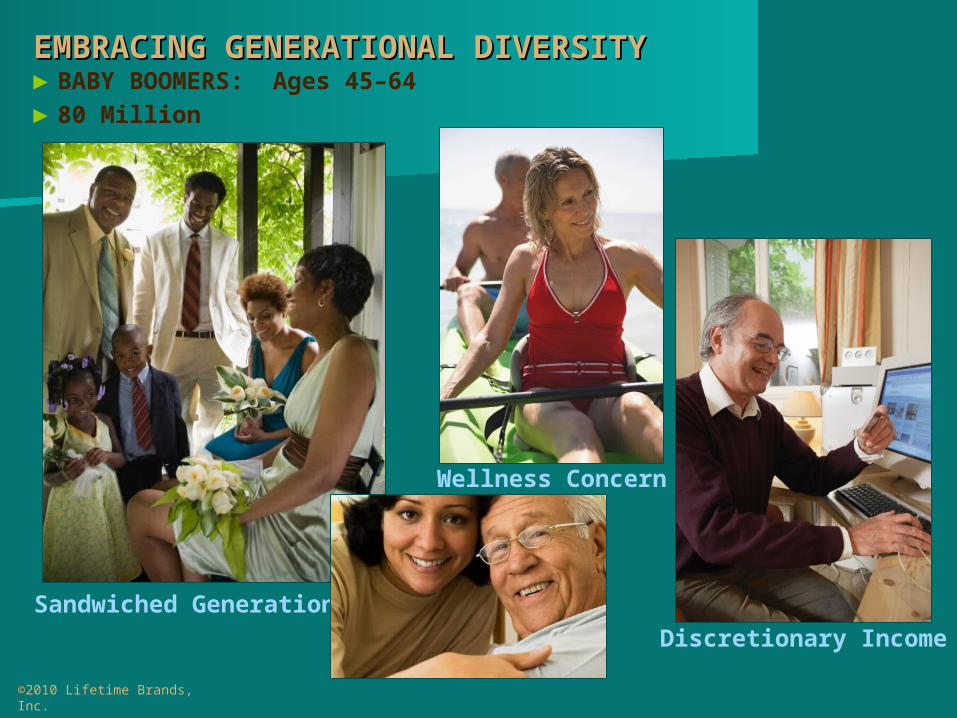

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY► BABY BOOMERS: Ages 45–64► 80 Million

©2010 Lifetime Brands, Inc.

Discretionary IncomeSandwiched Generation

Wellness Concern

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY► Baby Boomers (ages 45–64; 80 million; 38% of households)

Account for 40% of total consumer demand Entering a “second middle age” as they become active empty

nesters Started to spend more on experiences, such as travel and

entertaining: Businesses will need to reinvent solutions for Baby Boomers as they

reinvent themselves: Boomers do not call themselves “seniors” Most pursue an active lifestyle, staying engaged, vital and

empowered ‘A House that is a Home’: returning to family or a form of family

is part of the future plan, including living closer to children/grandchildren

Ergonomics in product are relevant to these consumers Intuitive design with strong visual cues

©2010 Lifetime Brands, Inc.

DES

IGN

FO

R L

IVIN

G

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY► ACTIVE SENIORS: Ages 65+► 47 Million

©2010 Lifetime Brands, Inc.

Grandchildren Connection

Reinventing Retirement

Wellness-Minded

Physically Active

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY

► Active Seniors (ages 65+; 47 million; 21% of households) 95% of those age 65–74 and 90% of those age 75–84 live in their own

home or apartment (Pew Research Center) Account for a rising share of single households Mental fitness—sales of ‘brain software’ are expected to jump from

$265 million to up to $5 billion by 2015 (SharpBrains) In-store lighting, counter reach, aisle width, signage size all key

variables Promote product solutions within the home which address safety,

strength and dexterity issues of this generation The OXO example—universal design that is a better product for all

©2010 Lifetime Brands, Inc.

©2010 Lifetime Brands, Inc.

EMBRACING GENERATIONAL DIVERSITYEMBRACING GENERATIONAL DIVERSITY

►Recovery strategies: Be prepared to capitalize on the recovery by addressing relevant

consumer touchpoints by generation: Gen Y’s starter apartment or home Gen X’s family raising lifestage Baby Boomers making choices for adult children as well as aging

parents Active Seniors needs both in-home and in-store

Experience economy = experience retail: how to make the shopping experience better, more interesting, more interactive for all generations: It goes beyond assortment to include visual presentation and

solution experiences Tailoring assortments to your core customer in order to make

more meaningful displays

RRECALCULATINGECALCULATING THE THE VVALUE ALUE EEQUATIONQUATION

RRECALCULATINGECALCULATING THE THE VVALUE ALUE EEQUATIONQUATION

©2010 Lifetime Brands, Inc.

2

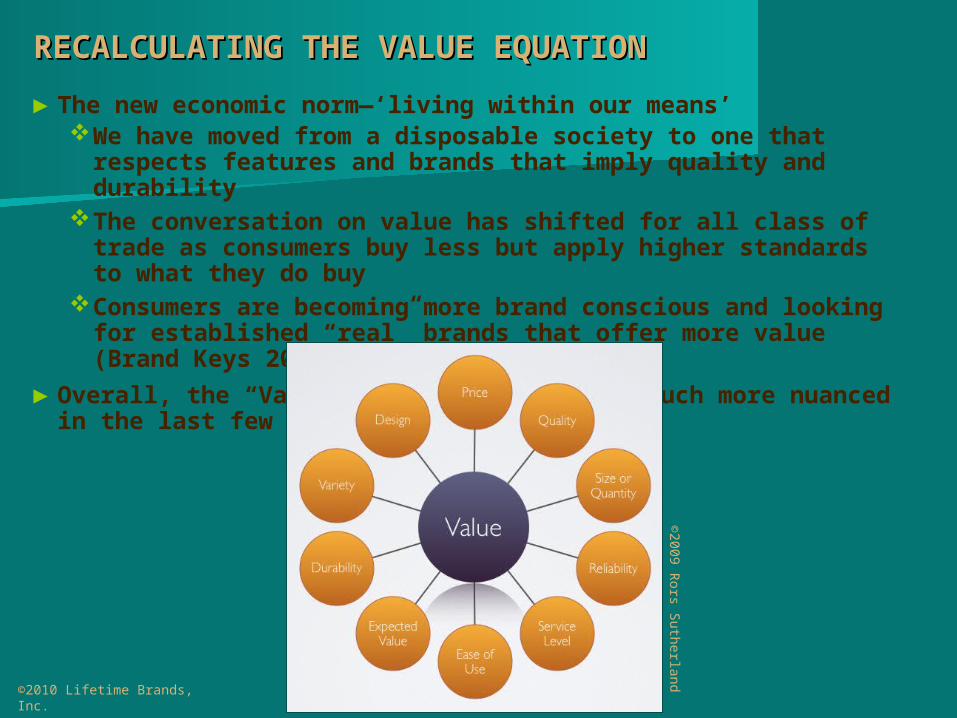

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION

► The new economic norm—‘living within our means’We have moved from a disposable society to one that

respects features and brands that imply quality and durability

The conversation on value has shifted for all class of trade as consumers buy less but apply higher standards to what they do buy

Consumers are becoming more brand conscious and looking for established “real” brands that offer more value (Brand Keys 2010)

► Overall, the “Value Equation” has become much more nuanced in the last few years

©2010 Lifetime Brands, Inc.

©2

00

9 R

ors S

uth

erla

nd

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION

► We have rediscovered price shopping (coupons, research and bargain-hunting), home entertainment (board games) and, the comfort and accomplishment of home made foods Consumers cutting coupons, buying more private label groceries,

only using credit cards for essentials, shopping at discounters and online and utilizing online price comparison web sites all in an effort to stretch incomes: We must excite consumers with ‘must-have’ product selection as

well as experiential shopping environments with interesting displays and events

Innovation comes from supplying creative consumer solutions Emotional connection—are you relevant to me? Role as educator (and even entertainer) as well as

supplier/manufacturer

©2010 Lifetime Brands, Inc.

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION

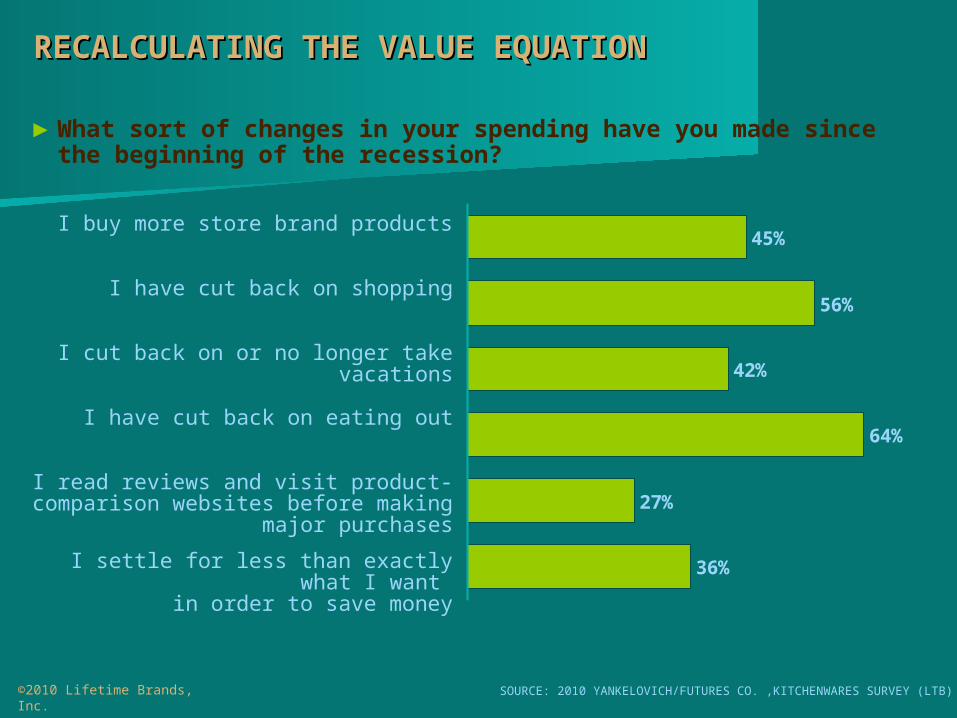

► What sort of changes in your spending have you made since the beginning of the recession?

©2010 Lifetime Brands, Inc.

45%

56%

42%

64%

27%

36%

I buy more store brand products

I have cut back on shopping

I cut back on or no longer take vacations

I have cut back on eating out

I read reviews and visit product-comparison websites before making

major purchases

I settle for less than exactly what I want

in order to save money

SOURCE: 2010 YANKELOVICH/FUTURES CO. ,KITCHENWARES SURVEY (LTB)

46%

48%

7%

32%

42%

26%

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION

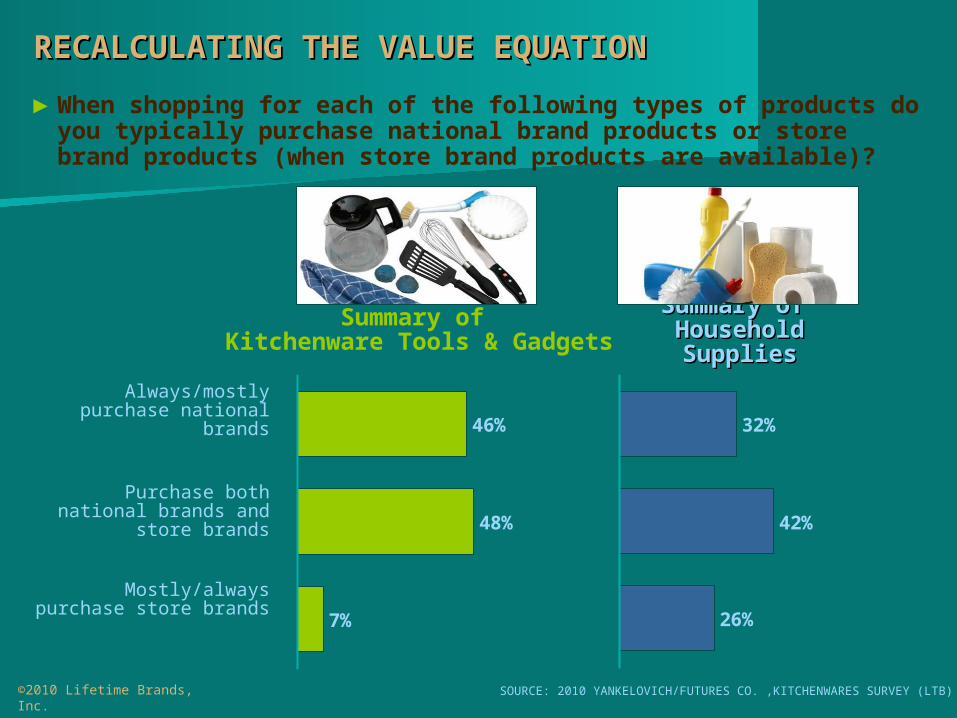

► When shopping for each of the following types of products do you typically purchase national brand products or store brand products (when store brand products are available)?

©2010 Lifetime Brands, Inc.

Summary of Kitchenware Tools & Gadgets

Summary of Summary of Household Household SuppliesSupplies

Always/mostly purchase national brands

Purchase both national brands and store brands

Mostly/always purchase store brands

SOURCE: 2010 YANKELOVICH/FUTURES CO. ,KITCHENWARES SURVEY (LTB)

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION

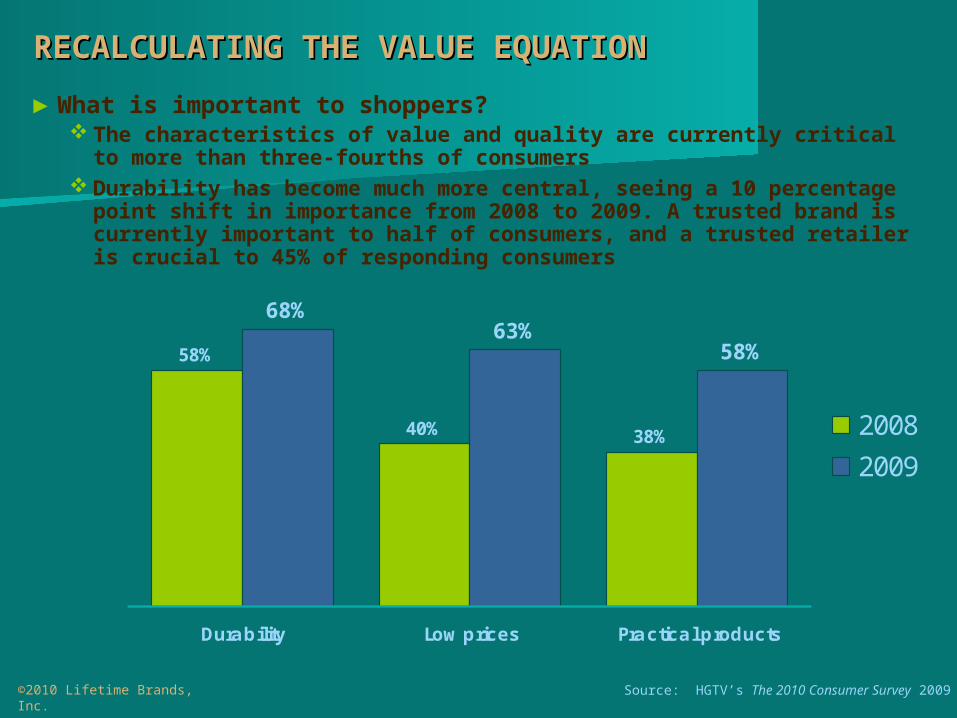

► What is important to shoppers? The characteristics of value and quality are currently critical to more

than three-fourths of consumers Durability has become much more central, seeing a 10 percentage

point shift in importance from 2008 to 2009. A trusted brand is currently important to half of consumers, and a trusted retailer is crucial to 45% of responding consumers

©2010 Lifetime Brands, Inc.

58%

40% 38%

68%

58%63%

Durability Low prices Practical products

2008

2009

Source: HGTV’s The 2010 Consumer Survey 2009

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION

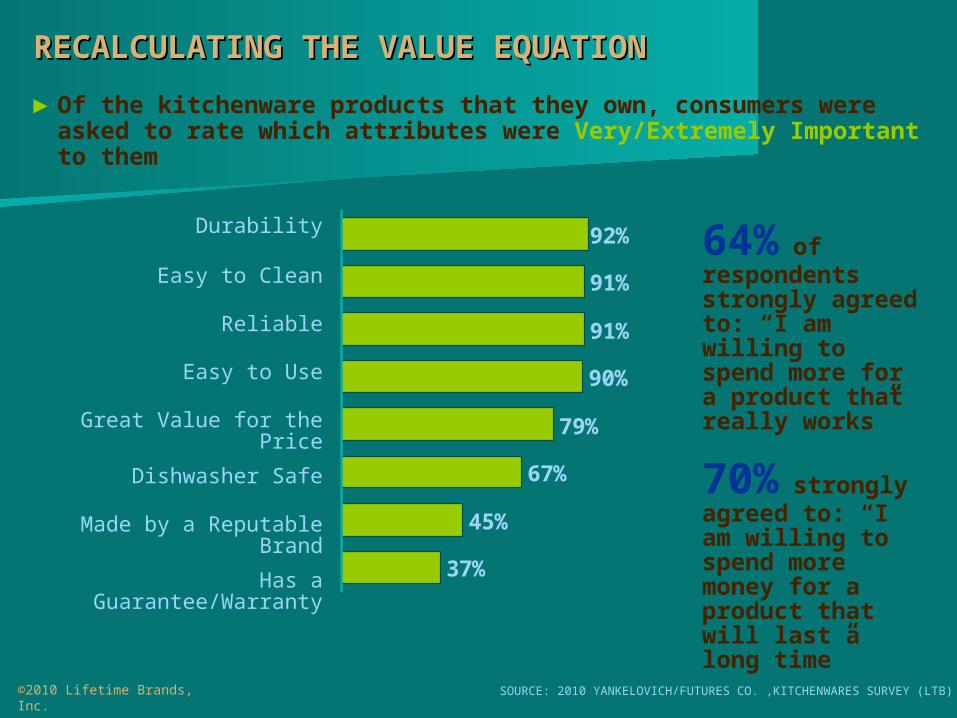

► Of the kitchenware products that they own, consumers were asked to rate which attributes were Very/Extremely Important to them

©2010 Lifetime Brands, Inc.

92%

91%

91%

90%

79%

67%

45%

37%

64% of respondents strongly agreed to: “I am willing to spend more for a product that really works”

70% strongly agreed to: “I am willing to spend more money for a product that will last a long time”

Durability

Easy to Clean

Reliable

Easy to Use

Great Value for the Price

Dishwasher Safe

Made by a Reputable Brand

Has a Guarantee/Warranty

SOURCE: 2010 YANKELOVICH/FUTURES CO. ,KITCHENWARES SURVEY (LTB)

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION

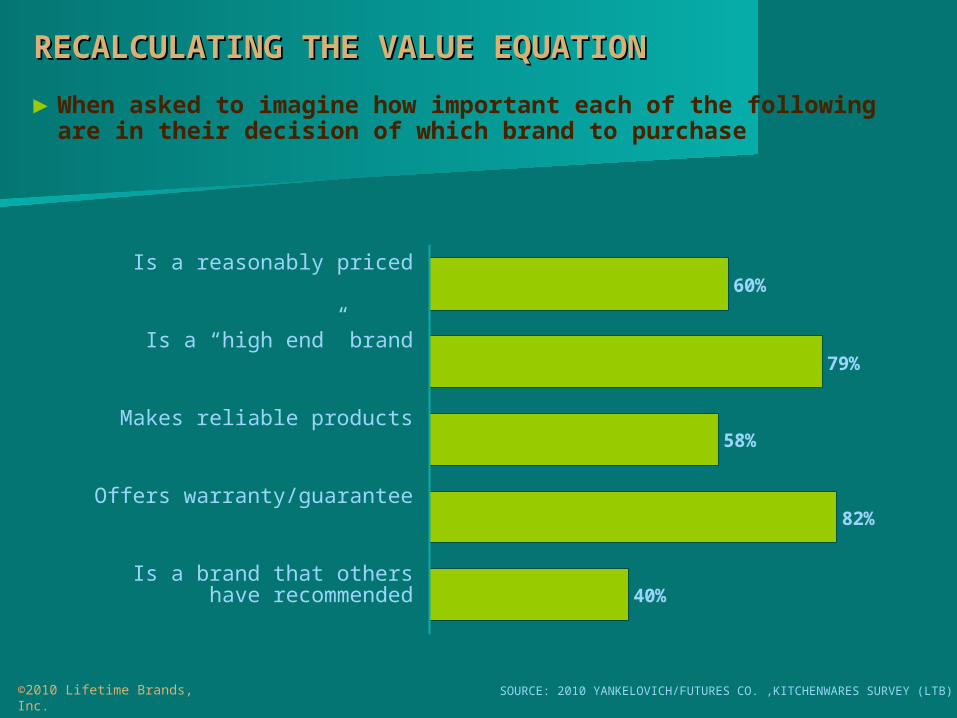

► When asked to imagine how important each of the following are in their decision of which brand to purchase

©2010 Lifetime Brands, Inc.

60%

79%

58%

82%

40%

Is a reasonably priced

Is a “high end” brand

Makes reliable products

Offers warranty/guarantee

Is a brand that others have recommended

SOURCE: 2010 YANKELOVICH/FUTURES CO. ,KITCHENWARES SURVEY (LTB)

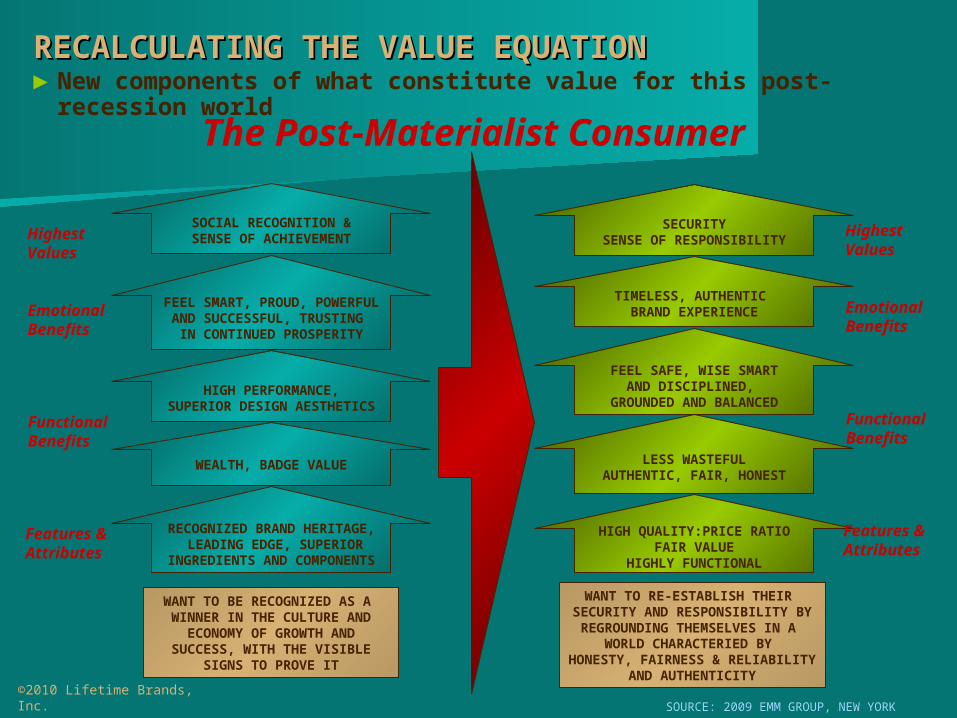

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION► New components of what constitute value for this post-

recession world

©2010 Lifetime Brands, Inc.

RECOGNIZED BRAND HERITAGE, LEADING EDGE, SUPERIOR

INGREDIENTS AND COMPONENTS

HIGH PERFORMANCE,SUPERIOR DESIGN AESTHETICS

WEALTH, BADGE VALUE

FEEL SMART, PROUD, POWERFULAND SUCCESSFUL, TRUSTING IN CONTINUED PROSPERITY

SOCIAL RECOGNITION &SENSE OF ACHIEVEMENT

HIGH QUALITY:PRICE RATIOFAIR VALUE

HIGHLY FUNCTIONAL

LESS WASTEFULAUTHENTIC, FAIR, HONEST

TIMELESS, AUTHENTIC BRAND EXPERIENCE

FEEL SAFE, WISE SMARTAND DISCIPLINED,

GROUNDED AND BALANCED

SECURITYSENSE OF RESPONSIBILITY

WANT TO BE RECOGNIZED AS A WINNER IN THE CULTURE ANDECONOMY OF GROWTH ANDSUCCESS, WITH THE VISIBLE

SIGNS TO PROVE IT

WANT TO RE-ESTABLISH THEIR SECURITY AND RESPONSIBILITY BYREGROUNDING THEMSELVES IN A

WORLD CHARACTERIED BY HONESTY, FAIRNESS & RELIABILITY

AND AUTHENTICITY

HighestValues

Emotional Benefits

Functional Benefits

Features &Attributes

The Post-Materialist Consumer

HighestValues

Emotional Benefits

Functional Benefits

Features &Attributes

SOURCE: 2009 EMM GROUP, NEW YORK

©2010 Lifetime Brands, Inc.

RECALCULATING THE VALUE EQUATIONRECALCULATING THE VALUE EQUATION

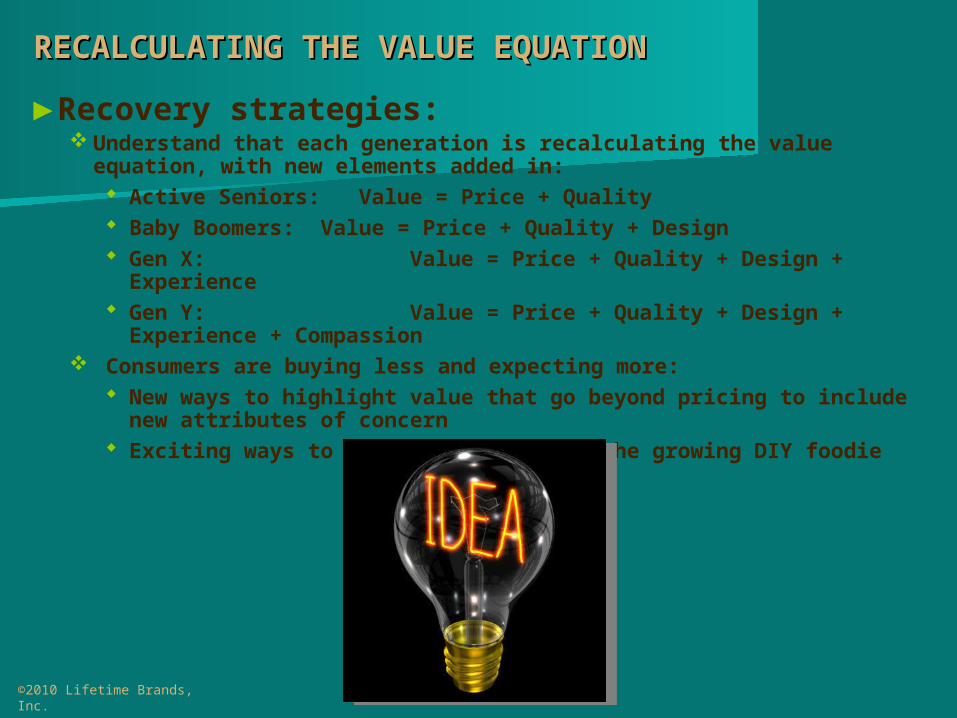

►Recovery strategies: Understand that each generation is recalculating the value equation,

with new elements added in: Active Seniors: Value = Price + Quality Baby Boomers: Value = Price + Quality + Design Gen X: Value = Price + Quality + Design + Experience Gen Y: Value = Price + Quality + Design + Experience +

Compassion Consumers are buying less and expecting more:

New ways to highlight value that go beyond pricing to include new attributes of concern

Exciting ways to educate and inspire the growing DIY foodie

MMULTI-ULTI-TTASKING IN THEASKING IN THE ““HHEART OF THE EART OF THE HHOMEOME””MMULTI-ULTI-TTASKING IN THEASKING IN THE ““HHEART OF THE EART OF THE HHOMEOME””

©2010 Lifetime Brands, Inc.

3

MULTI-TASKING IN THE “HEART OF THE HOME”MULTI-TASKING IN THE “HEART OF THE HOME”

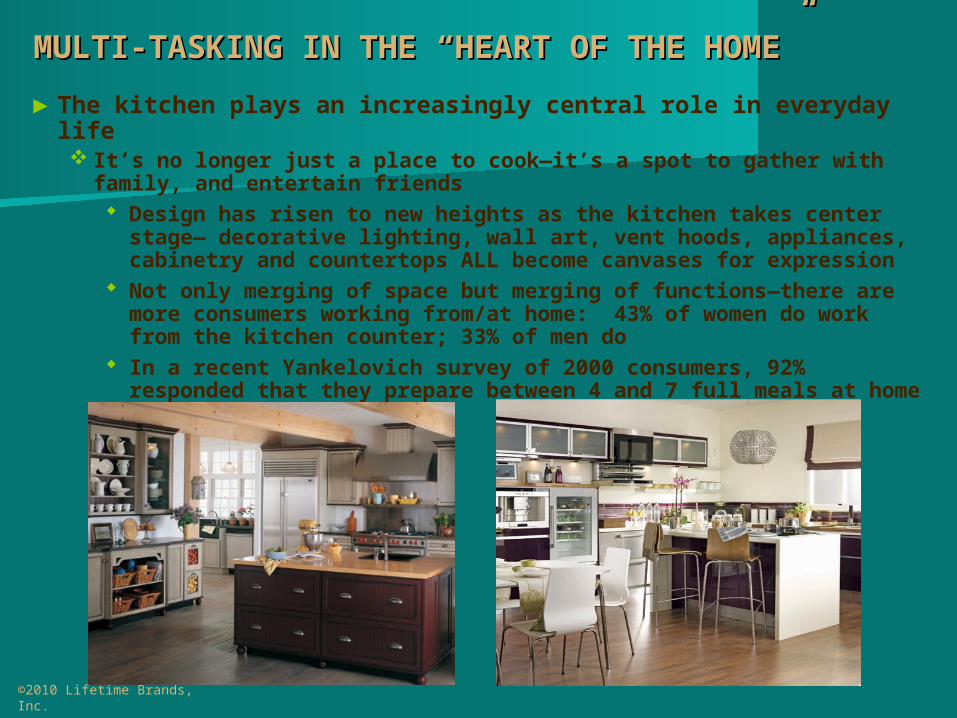

► The kitchen plays an increasingly central role in everyday life It’s no longer just a place to cook—it’s a spot to gather with family,

and entertain friends Design has risen to new heights as the kitchen takes center stage

— decorative lighting, wall art, vent hoods, appliances, cabinetry and countertops ALL become canvases for expression

Not only merging of space but merging of functions—there are more consumers working from/at home: 43% of women do work from the kitchen counter; 33% of men do

In a recent Yankelovich survey of 2000 consumers, 92% responded that they prepare between 4 and 7 full meals at home per week

©2010 Lifetime Brands, Inc.

42%

38%

10%

35%

38%

12%All buyers55+ buyers

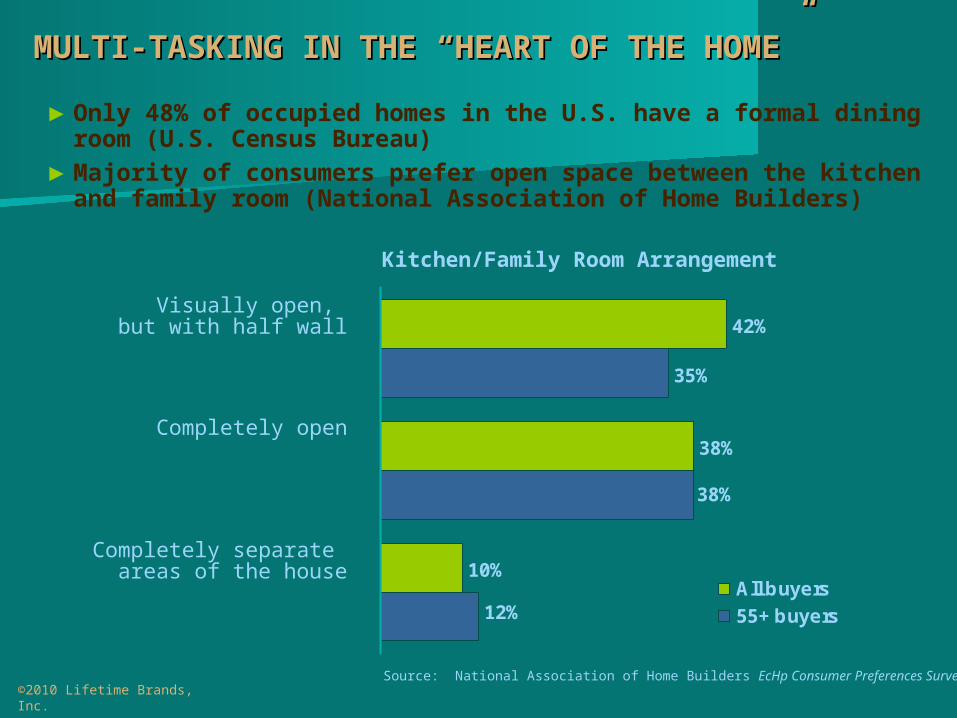

Source: National Association of Home Builders EcHp Consumer Preferences Survey

Kitchen/Family Room Arrangement

©2010 Lifetime Brands, Inc.

MULTI-TASKING IN THE “HEART OF THE HOME”MULTI-TASKING IN THE “HEART OF THE HOME”

► Only 48% of occupied homes in the U.S. have a formal dining room (U.S. Census Bureau)

► Majority of consumers prefer open space between the kitchen and family room (National Association of Home Builders)

Visually open, but with half wall

Completely open

Completely separate areas of the house

MULTI-TASKING IN THE “HEART OF THE HOME”MULTI-TASKING IN THE “HEART OF THE HOME”

► Today’s kitchen space is more egalitarian, with men and kids hanging out It is becoming a high-tech hub, with music and electronic media Nearly nine in 10 Americans (86%) are involved in some sort of

activity in their kitchen besides cooking such as paying bills, doing work or homework, doing a hobby or craft, reading or playing a game (Electrolux)

More multi-generational households: for example, 55% of men and 48% of women ages 18 to 24 live with their parents: Creating “me” and “we” space within the kitchen environment Multi-generational households bring a new set of expectations for

space and storage: adult children moving back home and/or older parents moving in, complete with possessions from prior living spaces

©2010 Lifetime Brands, Inc.

MULTI-TASKING IN THE “HEART OF THE HOME”MULTI-TASKING IN THE “HEART OF THE HOME”

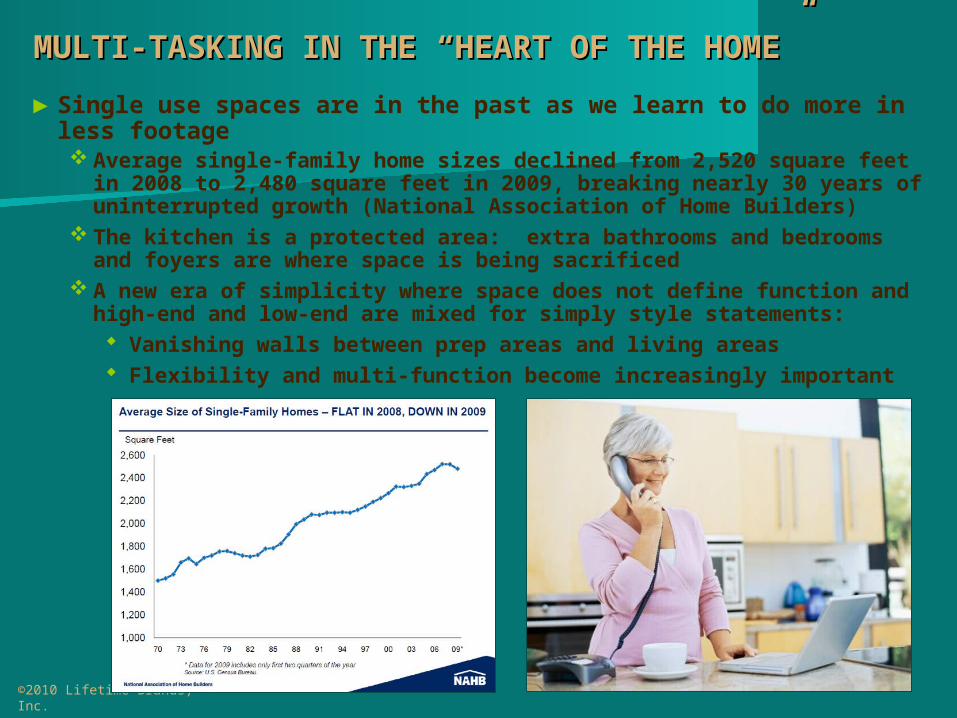

► Single use spaces are in the past as we learn to do more in less footage Average single-family home sizes declined from 2,520 square feet in

2008 to 2,480 square feet in 2009, breaking nearly 30 years of uninterrupted growth (National Association of Home Builders)

The kitchen is a protected area: extra bathrooms and bedrooms and foyers are where space is being sacrificed

A new era of simplicity where space does not define function and high-end and low-end are mixed for simply style statements: Vanishing walls between prep areas and living areas Flexibility and multi-function become increasingly important

©2010 Lifetime Brands, Inc.

MULTI-TASKING IN THE “HEART OF THE HOME”MULTI-TASKING IN THE “HEART OF THE HOME”

► The kitchen has become the upstairs rec room—67% of adults use their kitchen to socialize and entertain guests (Merillat) It is where we begin the day, and spend the most time: in fact,

according to research by kitchen cabinetry maker Merillat, 33% of adults spend three to four hours in their kitchen in a typical day while 20% say they spend more than five hours there every day

Food prep in many ways is entertainment many consumers who consider the process of the meal part of the experience to share with guests

©2010 Lifetime Brands, Inc.

LIFETIM

E B

RA

ND

S

©2010 Lifetime Brands, Inc.

MULTI-TASKING IN THE “HEART OF THE HOME”MULTI-TASKING IN THE “HEART OF THE HOME”

►Recovery strategies: Focus on products and merchandising that speak to new functions of

working, connecting and entertaining in the kitchen environment Address the growing desire for design and style for countertop

pieces and kitchen accessories. Function alone will not engage the consumer

Whether designing or selling product, consider the emerging need (and expectation) for products which: Save space (collapsible, de-constructible) Multifunction Save Time in preparation, execution or clean-up

MMAXIMIZINGAXIMIZINGEENTERTAINING NTERTAINING

OOPPORTUNITIESPPORTUNITIES

MMAXIMIZINGAXIMIZINGEENTERTAINING NTERTAINING

OOPPORTUNITIESPPORTUNITIES

©2010 Lifetime Brands, Inc.

4

MAXIMIZING ENTERTAINING OPPORTUNITIESMAXIMIZING ENTERTAINING OPPORTUNITIES

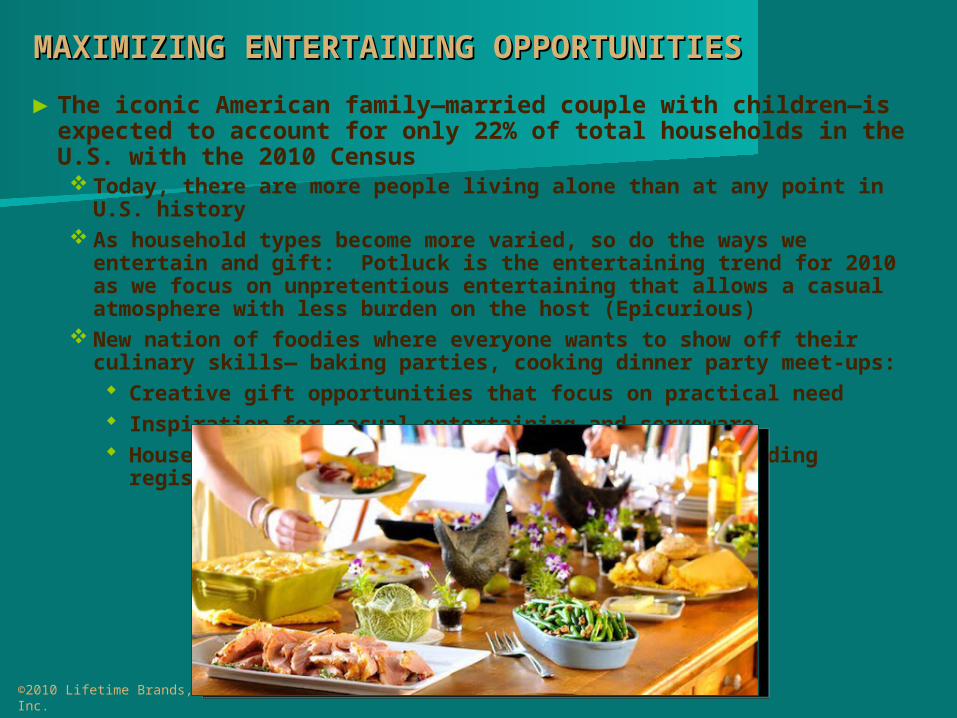

► The iconic American family—married couple with children—is expected to account for only 22% of total households in the U.S. with the 2010 Census Today, there are more people living alone than at any point in U.S.

history As household types become more varied, so do the ways we

entertain and gift: Potluck is the entertaining trend for 2010 as we focus on unpretentious entertaining that allows a casual atmosphere with less burden on the host (Epicurious)

New nation of foodies where everyone wants to show off their culinary skills— baking parties, cooking dinner party meet-ups: Creative gift opportunities that focus on practical need Inspiration for casual entertaining and serveware Housewares have even secured their position on wedding

registries

©2010 Lifetime Brands, Inc.

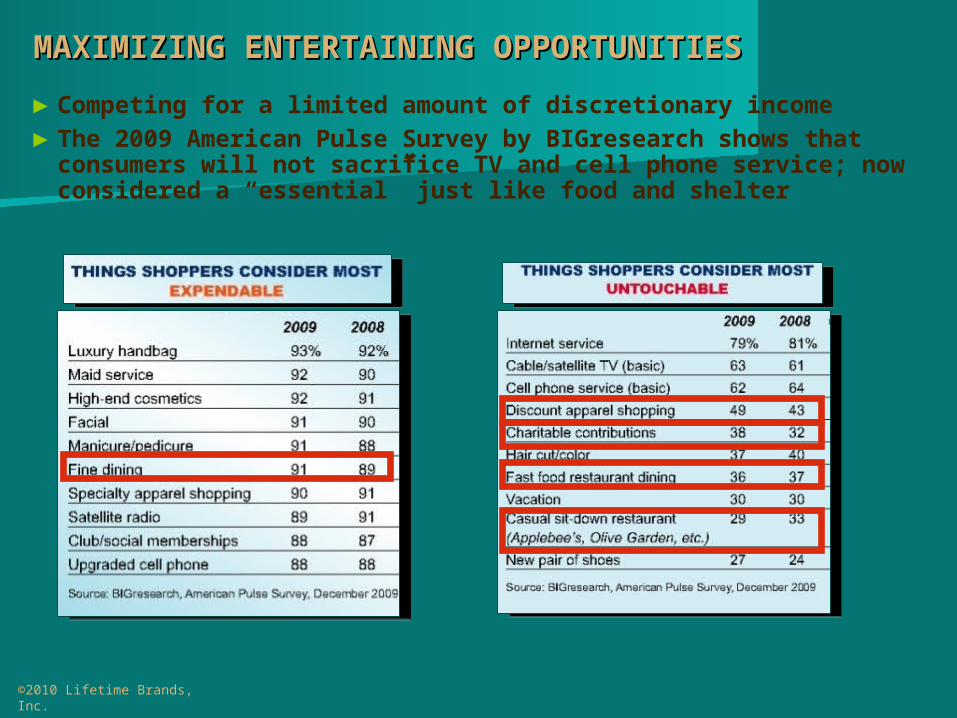

► Competing for a limited amount of discretionary income► The 2009 American Pulse Survey by BIGresearch shows that

consumers will not sacrifice TV and cell phone service; now considered a “essential” just like food and shelter

©2010 Lifetime Brands, Inc.

MAXIMIZING ENTERTAINING OPPORTUNITIESMAXIMIZING ENTERTAINING OPPORTUNITIES

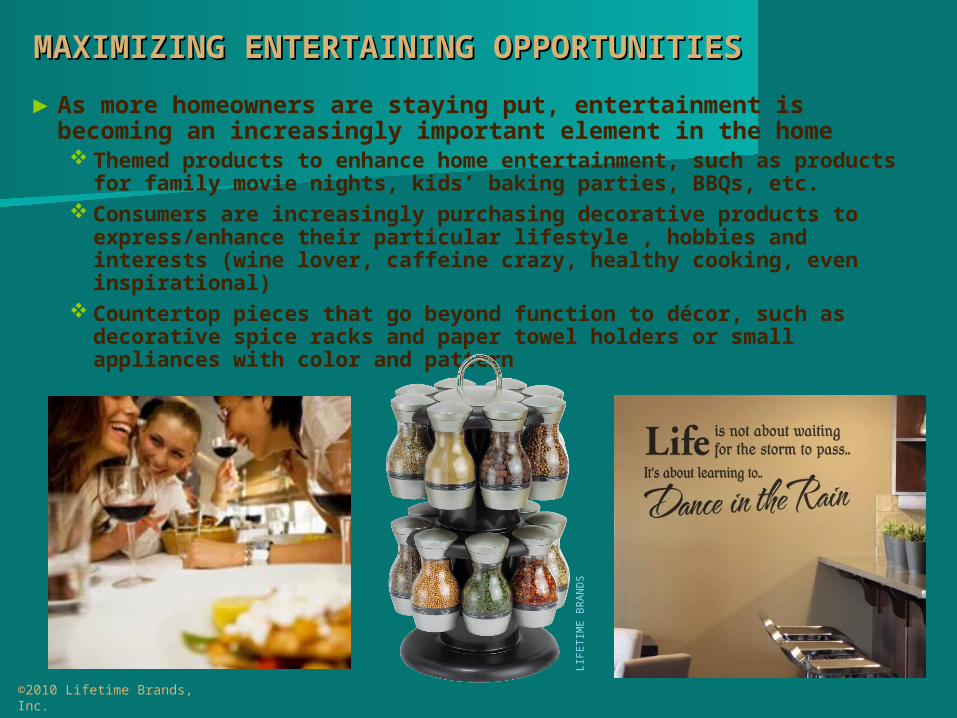

► As more homeowners are staying put, entertainment is becoming an increasingly important element in the home Themed products to enhance home entertainment, such as products

for family movie nights, kids’ baking parties, BBQs, etc. Consumers are increasingly purchasing decorative products to

express/enhance their particular lifestyle , hobbies and interests (wine lover, caffeine crazy, healthy cooking, even inspirational)

Countertop pieces that go beyond function to décor, such as decorative spice racks and paper towel holders or small appliances with color and pattern

©2010 Lifetime Brands, Inc.

MAXIMIZING ENTERTAINING OPPORTUNITIESMAXIMIZING ENTERTAINING OPPORTUNITIES

LIFETIM

E B

RA

ND

S

► The home moves from a showplace to a personal style statement Today’s consumer is a ‘mix master’—taking into account

performance function, aesthetic and giftability : From Tabletop to Countertop, they strive to create looks which

are unique expressions of their personal style Color has exploded across all home categories as consumers

search for self-expression in their most important environment Consumers do not want to look like the Joneses… or EAT like them

They will trade down where they can to trade up where it matters to them… but trade-ups are often justified at the expense of another expenditure E.g. trading off eating out as often to buy a superior set of cutlery

©2010 Lifetime Brands, Inc.

MAXIMIZING ENTERTAINING OPPORTUNITIESMAXIMIZING ENTERTAINING OPPORTUNITIES

LIFETIM

E B

RA

ND

S

BO

DU

M

► Today’s parents are craving more family time 78% say that spending time at home with my family has become

more important to me (2009 Hanley-Wood Survey) The act of preparing and sharing meals is a family bonding

opportunity… with 69% of consumers in families considering cooking inspired meals to be important (Research and Markets)

©2010 Lifetime Brands, Inc.

MAXIMIZING ENTERTAINING OPPORTUNITIESMAXIMIZING ENTERTAINING OPPORTUNITIES

©2010 Lifetime Brands, Inc.

►Recovery strategies: Create products and assortments that inspire/provide new

experiences in cooking and entertaining. Move beyond object-oriented selling and start delivering a better experience

Cooking has evolved from a chore to a fun activity for many consumers; make sure your products/assortments: Educate/Deliver new skills Provide opportunities for family involvement/interactivity Address the FUN in FUNction. to try new things, either for entertaining or to do with family

activities

MAXIMIZING ENTERTAINING OPPORTUNITIESMAXIMIZING ENTERTAINING OPPORTUNITIES

CCOMMITING TOOMMITING TO

SSUSTAINABLE USTAINABLE BBEHAVIOREHAVIORCCOMMITING TOOMMITING TO

SSUSTAINABLE USTAINABLE BBEHAVIOREHAVIOR

©2010 Lifetime Brands, Inc.

5

COMMITING TO SUSTAINABLE BEHAVIORCOMMITING TO SUSTAINABLE BEHAVIOR

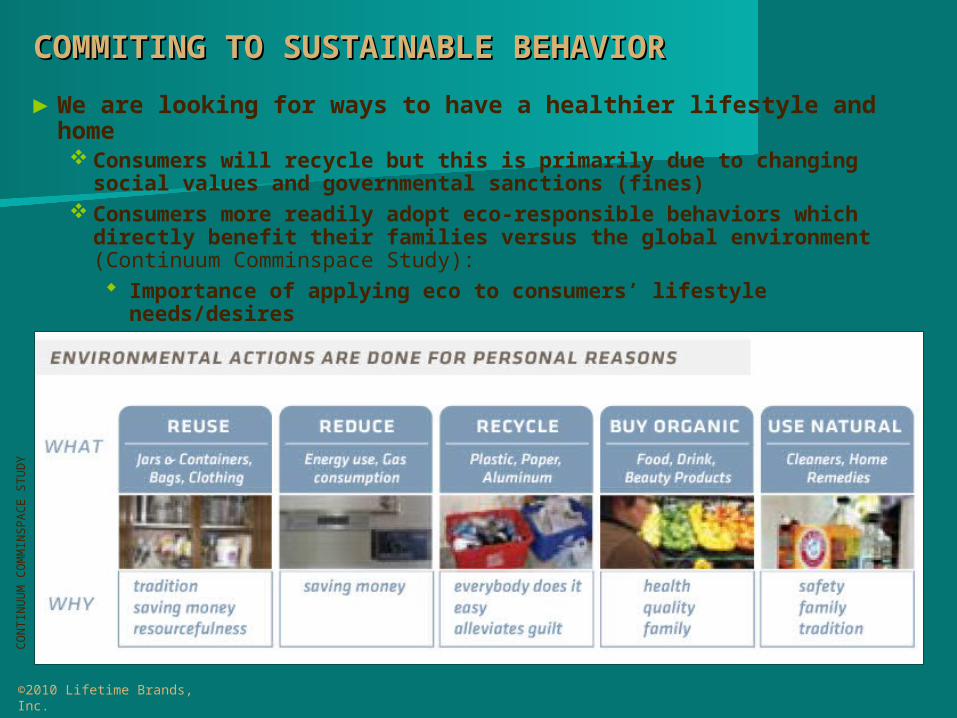

► We are looking for ways to have a healthier lifestyle and home Consumers will recycle but this is primarily due to changing social

values and governmental sanctions (fines) Consumers more readily adopt eco-responsible behaviors which

directly benefit their families versus the global environment (Continuum Comminspace Study): Importance of applying eco to consumers’ lifestyle needs/desires Searching out products that offer innovative solutions

©2010 Lifetime Brands, Inc.

CO

NTIN

UU

M C

OM

MIN

SPA

CE S

TU

DY

COMMITING TO SUSTAINABLE BEHAVIORCOMMITING TO SUSTAINABLE BEHAVIOR

► Reframing shopping behavior via sustainable strategies that also fit economic needs 15% of consumers have started buying secondhand goods just within

the last year (Brandweek): Competition not only includes traditional rivals but now second-

hand goods Studies show that consumers will spend for energy efficiency

products and services; next of concern is safety on what goes in and around their bodies (The Hartman Group): Go beyond greenwashing to practical alternatives

©2010 Lifetime Brands, Inc.

TH

E H

AR

TM

AN

N G

RO

UP

COMMITING TO SUSTAINABLE BEHAVIORCOMMITING TO SUSTAINABLE BEHAVIOR

► We are looking for ways to have a healthier and more responsible lifestyle and home ‘Freshness’ Food storage and refrigeration systems that can keep

fruit and vegetables fresher longer while consuming using less energy

Waste-reducing products like water bottles and thermal beverage products

Educating consumers about kitchen tools and gadgets that provide solutions for healthy eating, such as salad shakers, vegetable choppers choppers, oil sprayers, etc.

Consumers will pay for products that offer quality, multi-tiered solutions

©2010 Lifetime Brands, Inc.

LIFETIME HOAN RESEARCH

CU

ISIN

AR

T

FIT & FRESH

MIS

TO

DES

IGN

FO

R L

IVIN

G

COMMITING TO SUSTAINABLE BEHAVIORCOMMITING TO SUSTAINABLE BEHAVIOR► Consumer confusion is the biggest roadblock

Largest obstacles to consumer adoption of green alternatives: Lack of awareness on benefit Poor appearance Higher prices than eco-unfriendly alternatives Perceived sub-par performance

Yet, when all elements are equal, consumers will gravitate toward the more sustainable product

Most popular non-food categories for green products are Cleaning, Paper and Lighting

©2010 Lifetime Brands, Inc.

©2010 Lifetime Brands, Inc.

COMMITING TO SUSTAINABLE BEHAVIORCOMMITING TO SUSTAINABLE BEHAVIOR

►Recovery strategies: Food safety is a key touchpoint for consumers—bring solutions Consumers will recycle—how can you make it easier/cleaner/faster

for them Clearly highlight via in-store materials eco-friendly products and the

“why” behind these products focus on: Emphasize direct family health/safety benefits State clear economic benefits Focus on high frequency behaviors

Be clear about the benefits, and never overstate them—avoid greenwashing

Be authentic in your efforts and involvement; promote local and/or global causes that bring an emotional connection to the consumer

CCO-O-CCREATING THEREATING THE

FFUTURE UTURE KKITCHENITCHENCCO-O-CCREATING THEREATING THE

FFUTURE UTURE KKITCHENITCHEN

©2010 Lifetime Brands, Inc.

6

CO-CREATING THE FUTURE KITCHENCO-CREATING THE FUTURE KITCHEN

► Today’s consumer is looking for retailers, brands and products and that listen to them and understand the way they live Avoid being a commodity resource that can only compete on price;

consumers are looking for innovation and solutions that inspire them to buy

The median number of leisure hours available per week in 2008 was 16, a drop of 20% from 20 hours in 2007 (Harris Poll, 2008)—involve your consumer in ways to save both time and money in the kitchen, especially when they are increasing their cooking at home

Consumers are looking for tools and shortcuts that ease their day-to-day lives; our society is overextending and pressed for time

The replacement cycle for kitchen products is accelerating as consumers cook at home more often

©2010 Lifetime Brands, Inc.

KA

MEN

STEIN

FA

RB

ER

WA

RE

KAMENSTEIN

CO-CREATING THE FUTURE KITCHENCO-CREATING THE FUTURE KITCHEN

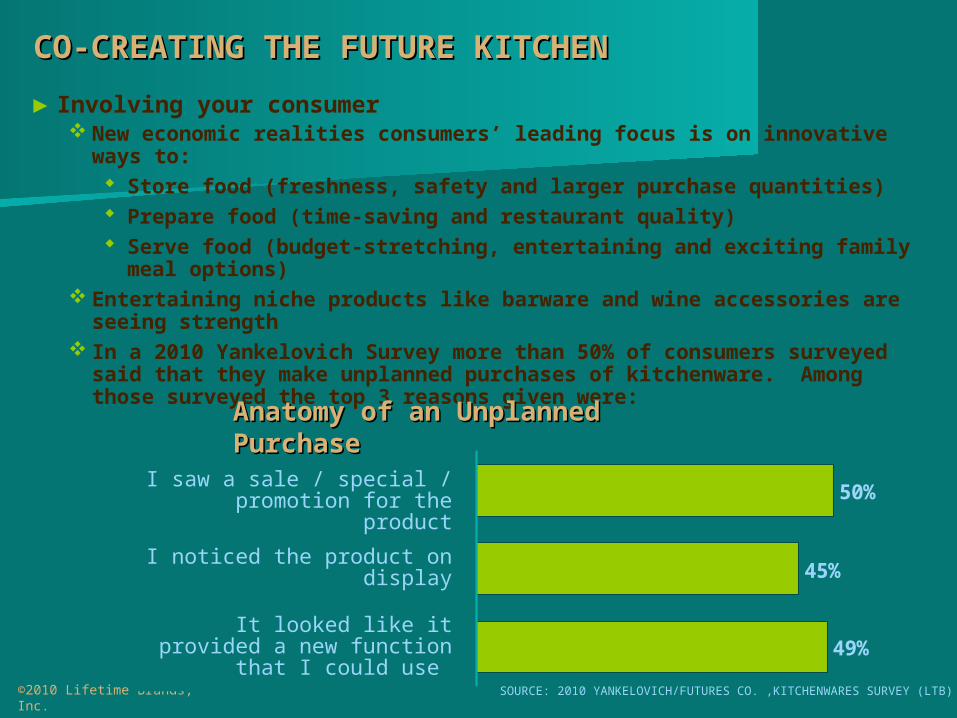

► Involving your consumer New economic realities consumers’ leading focus is on innovative

ways to: Store food (freshness, safety and larger purchase quantities) Prepare food (time-saving and restaurant quality) Serve food (budget-stretching, entertaining and exciting family

meal options) Entertaining niche products like barware and wine accessories are

seeing strength In a 2010 Yankelovich Survey more than 50% of consumers surveyed

said that they make unplanned purchases of kitchenware. Among those surveyed the top 3 reasons given were:

©2010 Lifetime Brands, Inc.

50%

45%

49%

I saw a sale / special / promotion for the product

I noticed the product on display

It looked like it provided a new function that I could

use

Anatomy of an Unplanned Anatomy of an Unplanned PurchasePurchase

SOURCE: 2010 YANKELOVICH/FUTURES CO. ,KITCHENWARES SURVEY (LTB)

CO-CREATING THE FUTURE KITCHENCO-CREATING THE FUTURE KITCHEN

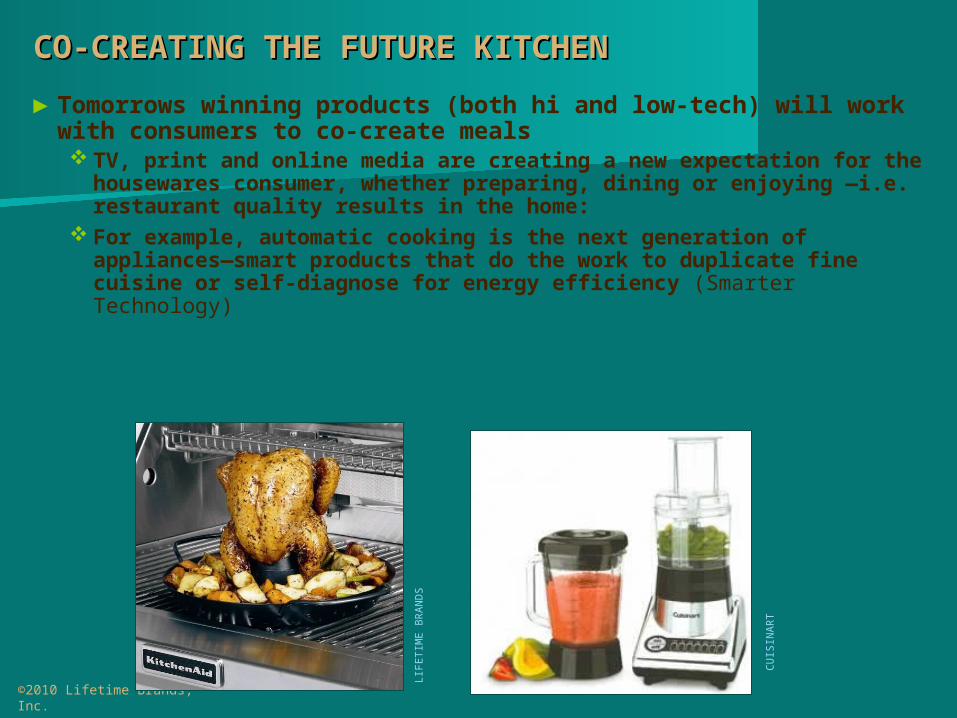

► Tomorrows winning products (both hi and low-tech) will work with consumers to co-create meals TV, print and online media are creating a new expectation for the

housewares consumer, whether preparing, dining or enjoying —i.e. restaurant quality results in the home:

For example, automatic cooking is the next generation of appliances—smart products that do the work to duplicate fine cuisine or self-diagnose for energy efficiency (Smarter Technology)

©2010 Lifetime Brands, Inc.

CU

ISIN

AR

T

LIFETIM

E B

RA

ND

S

CO-CREATING THE FUTURE KITCHENCO-CREATING THE FUTURE KITCHEN

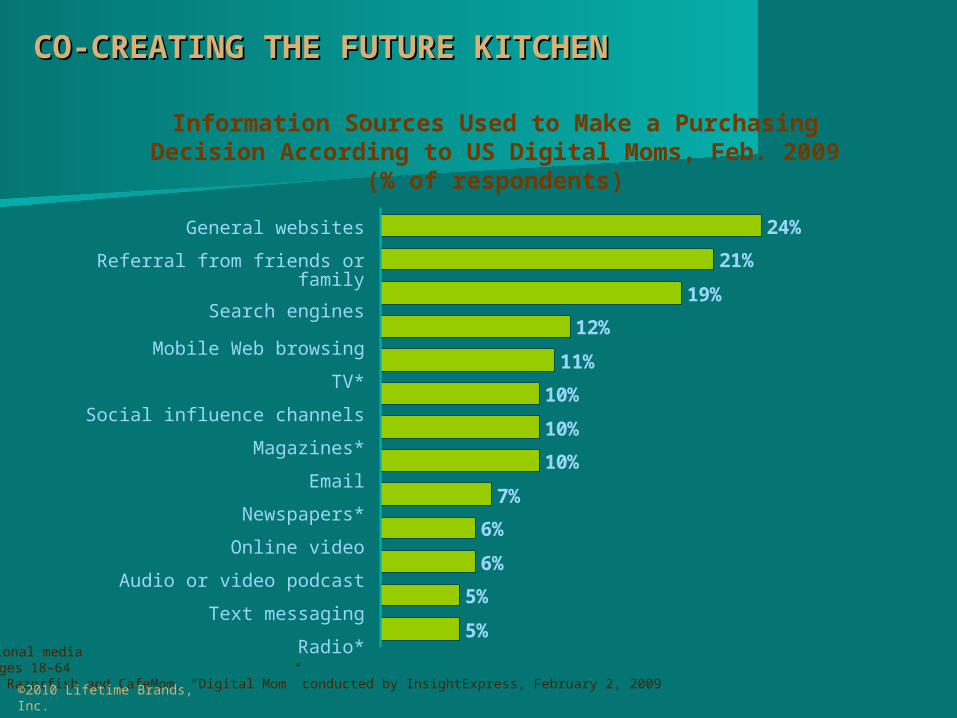

► Increasing role technology plays in co-creating our lives Affecting how we shop (mobile commerce), why we shop

(innovation), when we shop (24/7), where we shop (web research) and what we buy (new lifestyle needs)

Not only have technologies and their applications been accelerating, but so has consumer adoption of these applications: Social marketing strategies as a key part

of your marketing plan Understand the double-edged sword of a

24/7 world—the good and the bad can be spread to a wide community in matter of minutes

Constant change and inspiration are the mainreason to go to a brick-and-mortar location versus buying online

©2010 Lifetime Brands, Inc.

* Traditional mediaNote: Ages 18–64Source: Razorfish and CafeMom, “Digital Mom” conducted by InsightExpress, February 2, 2009

Information Sources Used to Make a Purchasing Decision According to US Digital Moms, Feb. 2009

(% of respondents)

©2010 Lifetime Brands, Inc.

CO-CREATING THE FUTURE KITCHENCO-CREATING THE FUTURE KITCHEN

General websites

Referral from friends or family

Search engines

Mobile Web browsing

TV*

Social influence channels

Magazines*

Newspapers*

Online video

Audio or video podcast

Text messaging

Radio*

24%

21%

19%

12%

11%

10%

10%

10%

7%

6%

6%

5%

5%

©2010 Lifetime Brands, Inc.

CO-CREATING THE FUTURE KITCHENCO-CREATING THE FUTURE KITCHEN

►Recovery strategies:

Become your own ‘Food Network’ by utilizing multi-channel strategies for inspiration and communication… Facebook, Yelp.com, etc.

Be the expert and “live” with your customers by using a website, in store events or other means to give them advice, tips, recipes, etc.

Remember that you don’t have to have your own website to be helped or hurt by the internet

Know the good and the bad of what consumers are saying about your business and act on it

©2010 Lifetime Brands, Inc.

TOP TRENDS for TOP TRENDS for 20112011

Embracing Generational Diversity

Recalculating the Value Equation

Multi-tasking in the “Heart of the Home”

Celebrating Entertaining Opportunities

Committing to Sustainable Behavior

Co-Creating the Future Kitchen

If you have any questions regarding this presentation, please contact:

©2010 Lifetime Brands, Inc. All rights reserved.©2010 Lifetime Brands, Inc. All rights reserved.

The information contained in this document is the exclusive property of Lifetime Brands, Inc., and is provided for internal research purposes only, and to give dimension and meaning to

current consumer and industry trends.

Any reproduction of this information is a direct violation of the Federal Copyright Law. This includes, but is not limited to, color copying, color printing, photocopying or faxing, as well as

email distribution of all content, photographs & images, or posting on the Internet.

Please be careful to not copy the designs, trademarks or intellectual properties of others reported within these pages, as this may result in your being sued or prosecuted by the owner

of that content.

Tom MirabileTom MirabileSVP, Global Trend and DesignSVP, Global Trend and Design

Lifetime Brands, Inc.Lifetime Brands, Inc.E: [email protected]

P: 516.740.6973