Embed Size (px)

Citation preview

Stockselect Performance Review 1 July 2011

We know that our quarterly review of past recommendations is one of the most eagerly awaitedupdates amongst our subscribers. Every quarter we therefore make it a point to review our estimateskeeping the long term picture in mind. This quarter, as is the case with the first quarter of every fiscal,we carried out the most in depth reviews after going through the management discussions in recentlypublished annual reports. Also the review this quarter carries our views from the perspective ofestimated financials for the financial year 2013-14 (FY14) as against FY13 estimates taken over thepast 3 quarters.

To give you a head up on the variables that govern our long term projections - the lingering inflation,stickiness of high commodity prices, high interest rates and global economic instability - have thebiggest influence. However, we have taken a cautious note of companies that can tide over the marginand growth pressures. Whether or not India heads into a period of temporary recession, we believethat some companies will continue to create value for shareholders.

Going forward we see the consumption story (especially cars and homes) taking a backseat for thetime being. Companies may also delay their capex plans in light of higher borrowing costs. This coulddampen the GDP growth prospects for the near term. However, we agree with the RBI that it isnecessary to sacrifice short term growth in order to tackle the inflationary monster effectively. Despitethe fact that most of the negatives for Indian companies are for the near term, the Sensex has beenone of the worst performers among major emerging markets in 2011.

But, the worst is still not behind us. While a strong monsoon should help ease food inflation, the recentdiesel hike will increase the costs of transporting agricultural produce. This is expected to further stokethe price rises, and may cause RBI to step in once again. Reduced duties on crude oil and petrolproducts are expected to result in a revenue loss for the government. Plus with the volatile stockmarket, it looks like the government's divestment target will not be met for this fiscal. Its ambitiousplans for reducing the country's fiscal deficit may once again remain on paper. Globally the debt crisisin the US and Greece remain the biggest dampeners on market sentiments.

At over 18,000 levels the benchmark BSE-Sensex is currently slightly higher than the level it was at theend of FY10. But, this level is nearly double the close of FY09. While markets may continue to remainvolatile for most part of the coming fiscal, it is the ebbs that can help us to pick up stocks atreasonable valuations. We are optimistic about the long term prospects of the Indian economy.However, we wouldn't be surprised to see some negative surprises in terms of corporate earnings,and inflation. Therefore we advise investors to buy into only those companies which have stable

http://www.equitymaster.com/qr/detail_sq.asp?story=3&date=07/01/201...

1 of 3 12/15/11 11:38 AM

managements, pricing power, and ability to tide over margin pressures, at attractive bargains.

With that we present you a review of our Stock Select recommendations. This time onwards, we willbe reviewing all our 'unique' (we will not be repeating the companies) StockSelect recommendationsthat still have open positions. By open positions we mean recommendations that have yet to completethe tenure of 2.5 years or have yet to meet the target price.

In 2010, a good portion of our recommendations were Sells. The main reason why we asked you toavoid adding or holding them in your portfolio was because these stocks were trading at unsustainablevaluations. Advising caution, we thus asked you to book profits at those high levels. More than threefourth of our Sell recommendations made in 2010 managed to correct by over 10% so far. Some ofour 'Sell' recommendations last year, which turned out to be very successful were on stocks likeBHEL, Voltas, Ashok Leyland, SBI etc, which saw a correction of around 15% or more.

Worth mentioning that the correction in 2011 offered us the opportunity to recommend 'Buys' on someof these where 'valuation' was the only issue. Rest assured, we will continue to advise you once theprices of other stocks under our coverage are trading at more reasonable valuations.

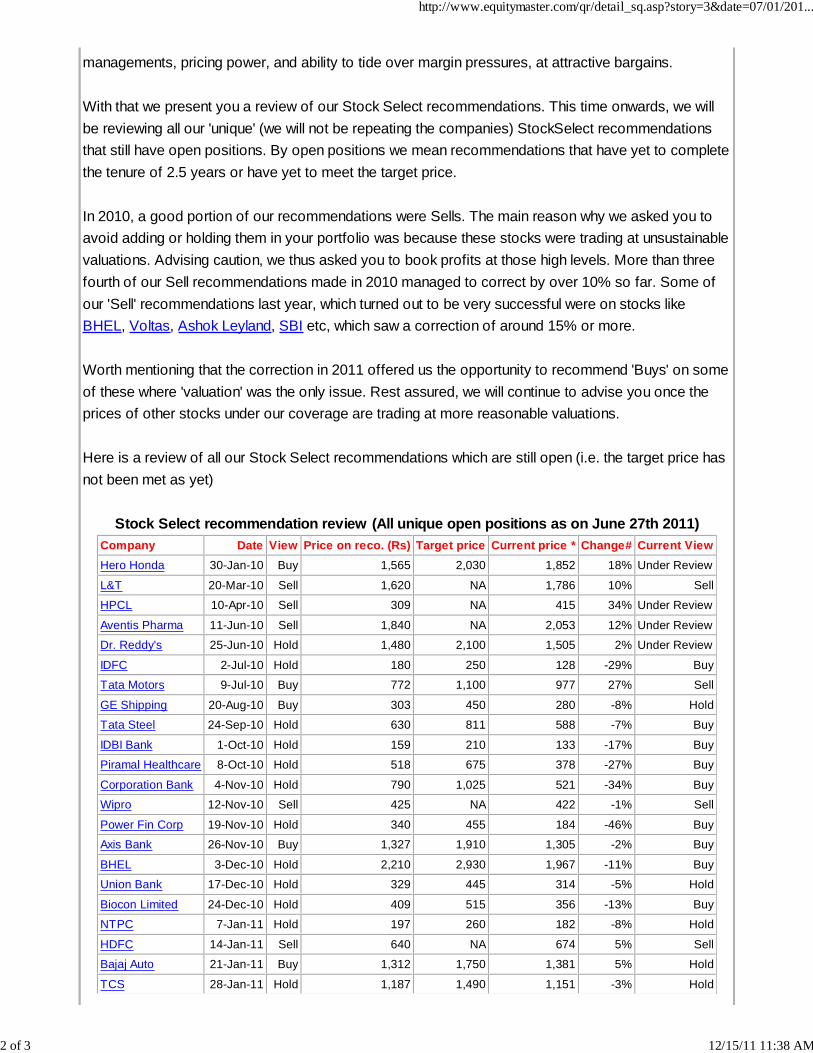

Here is a review of all our Stock Select recommendations which are still open (i.e. the target price hasnot been met as yet)

Stock Select recommendation review (All unique open positions as on June 27th 2011)Company Date View Price on reco. (Rs) Target price Current price * Change# Current ViewHero Honda 30-Jan-10 Buy 1,565 2,030 1,852 18% Under Review

L&T 20-Mar-10 Sell 1,620 NA 1,786 10% Sell

HPCL 10-Apr-10 Sell 309 NA 415 34% Under Review

Aventis Pharma 11-Jun-10 Sell 1,840 NA 2,053 12% Under Review

Dr. Reddy's 25-Jun-10 Hold 1,480 2,100 1,505 2% Under Review

IDFC 2-Jul-10 Hold 180 250 128 -29% Buy

Tata Motors 9-Jul-10 Buy 772 1,100 977 27% Sell

GE Shipping 20-Aug-10 Buy 303 450 280 -8% Hold

Tata Steel 24-Sep-10 Hold 630 811 588 -7% Buy

IDBI Bank 1-Oct-10 Hold 159 210 133 -17% Buy

Piramal Healthcare 8-Oct-10 Hold 518 675 378 -27% Buy

Corporation Bank 4-Nov-10 Hold 790 1,025 521 -34% Buy

Wipro 12-Nov-10 Sell 425 NA 422 -1% Sell

Power Fin Corp 19-Nov-10 Hold 340 455 184 -46% Buy

Axis Bank 26-Nov-10 Buy 1,327 1,910 1,305 -2% Buy

BHEL 3-Dec-10 Hold 2,210 2,930 1,967 -11% Buy

Union Bank 17-Dec-10 Hold 329 445 314 -5% Hold

Biocon Limited 24-Dec-10 Hold 409 515 356 -13% Buy

NTPC 7-Jan-11 Hold 197 260 182 -8% Hold

HDFC 14-Jan-11 Sell 640 NA 674 5% Sell

Bajaj Auto 21-Jan-11 Buy 1,312 1,750 1,381 5% Hold

TCS 28-Jan-11 Hold 1,187 1,490 1,151 -3% Hold

http://www.equitymaster.com/qr/detail_sq.asp?story=3&date=07/01/201...

2 of 3 12/15/11 11:38 AM

PNB 4-Feb-11 Buy 1,063 1,560 1,064 0% Buy

Glenmark Pharma 11-Feb-11 Buy 284 380 317 12% Hold

Oriental Bank 18-Feb-11 Buy 330 545 335 2% Buy

Voltas 18-Feb-11 Buy 158 225 159 1% Buy

ING Vysya 4-Mar-11 Buy 316 465 337 7% Buy

Ashok Leyland 11-Mar-11 Hold 52 65 49 -6% Buy

Essel Propack 18-Mar-11 Buy 43 69 47 9% Buy

Maruti Suzuki 25-Mar-11 Buy 1,183 1,535 1,153 -3% Buy

Infosys 1-Apr-11 Buy 3,218 4,150 2,868 -11% Buy

Gail 8-Apr-11 Hold 470 577 457 -3% Hold

Power Grid Corp. 15-Apr-11 Hold 105 135 109 4% Hold

Indraprastha Gas 21-Apr-11 Buy 321 415 373 16% Hold

Bank of Baroda 6-May-11 Buy 874 1,290 885 1% Buy

Bharti Airtel 13-May-11 Buy 367 600 396 8% Buy

Crompton Greaves 20-May-11 Buy 248 355 258 4% Buy

Cipla Limited 27-May-11 Hold 318 416 331 4% Hold

Tata Power 3-Jun-11 Hold 1,250 1,775 1,288 3% Hold

Gujarat Gas 10-Jun-11 Sell 380 NA 393 3% Sell

UltraTech Cement 17-Jun-11 Sell 967 NA 959 -1% Sell

HDFC Bank 24-Jun-11 Hold 2,381 3,060 2,416 1% Hold

* Current price as on June 27, 2011 NA - Not applicable # Calculated by dividing current price by recommended price

Note: Click on the company name to view its latest update

Also, our recommendations that met their target prices during 1QFY12 (April - June 2011) are asfollows:

Company Reco Date View Price on record date Target price (Rs) % Gain/ Loss# Target met onNovartis 22-May-10 Hold 594 810 36.4% 13-Jun-11

Grasim 4-Jun-10 Buy 1,780 2,557 43.7% 4-Apr-11

# Calculated by dividing current price as on 27th June 2011 by recommended price

If you have any questions or queries about your subscription, please write to us.

Now, Latest Recommendations Delivered to Your Desktop. Subscribe to RSS for StockSelect

PLEASE NOTE: This report is for your personal use only. We request you, our subscriber, NOT tocirculate this report or share any information contained therein with any person or group. Please note that ourTerms of Use policy, which you have accepted at the time of signing up for our services, prohibits you fromsharing our research. If you have any queries or wish to report any misuse of our research, please write in tous. Thank you.

http://www.equitymaster.com/qr/detail_sq.asp?story=3&date=07/01/201...

3 of 3 12/15/11 11:38 AM