Embed Size (px)

Citation preview

2012 Annual Report

1

Contents2 Executive Summary4 Operational Review24 Financial Review28 Corporate Social Responsibility 32 The Executive Team33 Directors & Advisors 34 Directors’ Report 36 Corporate Governance 41 Directors’ Responsibilities Statement 42 Independent Auditor’s Report 44 Consolidated Profit & Loss Account 45 Consolidated Balance Sheet 46 Company Balance Sheet47 Consolidated Statement of Total Recognised Gains & Losses 47 Reconciliation of Movements in Consolidated Shareholders’ Funds48 Consolidated Cash Flow Statement 49 Notes to the Consolidated Cash Flow Statement51 Notes to the Accounts80 Group Five Year Summary 81 Contact Details

2

Executive SummaryThe board remains confident that our businesses are well positioned to deliver another year of growth for the Group. South Staffordshire Plc is an integrated services group that operates two regulated UK water supply companies and provides a range of specialist services, predominantly in the UK water sector but also increasingly to other infrastructure owners.

The Group has experienced another positive year with successful operational delivery in the regulated water supply businesses of South Staffs Water and Cambridge Water (which was acquired in October 2011). In addition, the year has also seen the continuing successful development of opportunities arising in our non-regulated service divisions, SSI Services and Echo, which have experienced sales and profit growth despite the continuing difficulties in the UK economy.

South Staffs WaterDomestic water charges remain 25% below the industry average with the business continuing to offer high levels of service to its customers.

Despite the very dry weather conditions experienced during the year, which resulted in a drought in much of the country including the Midlands, the business’s water resource position remained healthy with no water use restrictions being imposed. A relatively wet spring and start to the 2012 summer have also increased resources further. However, continual close management of the resource position remains a priority for the business.

South Staffs Water has successfully delivered capital investment (net of contributions) of £26.3m in the year including the replacement of 63km of mains that are susceptible to bursts and leaks.

Cambridge WaterIn October 2011 the Group acquired Cambridge Water, a water only company supplying approximately 310,000 people in the city of Cambridge and the surrounding area. The business has many similarities with South Staffs Water in that both businesses have low charges to customers, supply high quality drinking water and offer excellent service, whilst having an efficient operation.

As the Group already owned one water company there was an automatic referral of the acquisition to the Competition Commission which, on 31 May 2012, cleared the acquisition without the need for remedies. The Competition Commission recognised the potential for positive benefits from the sharing of best practice and increased resilience to improve further the performance of both businesses.

3

SSI ServicesSSI Services, the Group’s specialist infrastructure contracting division, provides a broad range of specialist added value services working in regulated environments serving the public and private sectors, including water utilities, government agencies, as well as major contractors and facility management companies serving these sectors.

The division has operated in a challenging environment, with a reduction in public sector budgets impacting demand for our specialist services. However, despite these challenges, the division has continued to grow and improve the levels of operational efficiency. A number of businesses have performed very well, with the water industry entering the second year of AMP5 and demand in this sector increasing with further growth expected in the current year.

EchoEcho is a leading provider of customer process management services focusing on regulated markets. The business remains committed to developments that continue to support its clients with the major challenges they face including, in the UK water sector, their focus on further improving their levels of customer satisfaction. This support has included further development of Echo’s RapidXtra system, resulting in innovations in business process management, meter data management and web self-service.

The business remains committed to building on its position in Northern Ireland where it is already established as one of the leading public sector service providers. Inter-Credit, Echo’s debt collection business, has performed well during the year securing new clients in the water industry.

Management and EmployeesThe success of the Group could not be achieved without the hard work, dedication and innovation of our main asset, our management and employees. The Group continues to encourage our people to develop their skills and knowledge to the benefit of both themselves and our businesses.

OutlookDespite continuing uncertainty over the prospects for growth in the UK economy and the challenges this uncertainty brings, the Board remains confident that our businesses are efficient and are well positioned to deliver another successful year of growth for the Group.

4

Despite being one of the smaller companies in the UK water sector, South Staffs Water is recognised as being a leading company. Drivers for the water industry are demands for a constant supply of safe and clean water, excellent value and high customer service and the business has a proven track record of meeting these demands.

The Long Term Strategic Direction Statement, which guides company policy and decision making, continues to be based upon:

• Providing excellent service to customers;

• Maximising business efficiency through controlling costs; and

• Reducing the carbon footprint by further enhancing energy efficiency.

The challenge to square these key drivers is increasingly being put to the test, especially as the carbon agenda continues to increase in significance. Nevertheless, South Staffs Water’s household customers continue to pay the third lowest water bills in England and Wales, with the average figure of £130 being 25% lower than the industry average.

The business is also recognised for being one of the most efficient in the sector and is ranked in the highest band for efficiency by Ofwat. For operating costs, South Staffs Water attained upper Band A efficiency status in the last Periodic Review

(2009) and the business is committed to maintaining this position going forward. While costs continue to be very carefully controlled and further savings achieved, the cost base is continually being influenced by factors outside of the business’s control, such as power and fuel costs, new and increased government charges, bad debts, a volatile inflation rate and unpredictable weather conditions.

Historically water companies’ service performance has been assessed using the Overall Performance Assessment (OPA) and, for more than ten consecutive years, South Staffs Water has been represented in the top five in the industry, an achievement of which the business is incredibly proud. In the spirit of

Operational Review:South Staffs WaterSouth Staffs Water is recognised for being one of the most efficient companies in the sector by Ofwat.

5

Our average household customer bill is 25% below the

industry average

6

continually incentivising performance of companies, Ofwat has introduced the Service Incentive Mechanism (SIM), essentially to replace the OPA.

The SIM measure is dominated by assessing levels of customer satisfaction and has a very different emphasis to the OPA. It became fully effective in 2011/12 and there has been much work done by the business during the year to review and improve processes and systems in order to enhance the experience and satisfaction of customers when they have contact with the business on billing or operational matters. Over the year the establishment of the Customer Voice team has been

pivotal to these improvements and ensuring that all employees understand the vital role they play in delivering good customer service. South Staffs Water has significantly improved performance in the year and comparison to the rest of the industry will be available in mid 2012.

In recent years severe winter weather saw significant peaks in burst main and leakage levels. This past winter has been exceptionally mild but extreme variability in weather conditions makes it even more important to plan effectively and have flexibility in managing resources. Despite the business entering the spring of 2011 in a

healthy water resource position, the lack of rainfall over the last summer, autumn and winter has highlighted the vulnerability of water resources to unusual weather patterns.

Following two very dry winters, areas of the country, including the Midlands, were officially declared in drought by the Environment Agency. As a consequence a number of water companies imposed water use restrictions on their customers, although the situation has been helped by an unusually wet spring and start to the summer. As a result of moving significant volumes of water around its supply area to meet customer needs and to protect reservoir levels, South Staffs Water’s resource position remains healthy and there are no water use restrictions foreseen. However, to ensure this position is maintained, there will be continual close management of resources.

The management of resources is also impacted upon by leakage levels, and the mild winter and

(left) Much work has been done to enhance customer satisfaction.

7

continued investment has helped in achieving the leakage target for the year coupled with a low number of prolonged supply interruptions.

During the period, the business complied with 99.97% of all tests carried out on drinking water supplies. The result continues the trend of high compliance rates achieved over a number of years.

With increasing energy prices, the drive to improve efficiency in the production of water and electricity procurement continues to be important. A full review of production costs has been undertaken to ensure the efficient use of energy continues and is further enhanced. Such activities are becoming increasingly important as 2012/13 sees the introduction of the Carbon Reduction Commitment. South Staffs Water will continue to work very hard to maintain its recognised position as one of the most energy efficient companies in the sector.

Much work has been undertaken on further improvements to procurement, contracting and AMP5 capital investment delivery strategies. By using these strategies, the business has made good progress in delivering its capital programme to ensure its assets remain in good condition, maintain stable asset serviceability and ensure good quality, reliable water supplies to customers. Capital expenditure net of

contributions for the year of £26.3m is in line with the 2009 Ofwat Final Determination before accounting for a change in the COPI index reported during the year.

Good progress has been made in replacing mains that are susceptible to bursts and leakage with the renewal of 63km of mains and associated services in the year. With an enhanced programme of meter

The business has significantly improved

its SIM performance in the year

8

Whilst the third year of the current AMP5 period has just started, preparations are already in progress for the 2014 Periodic Review. This will require even greater customer support for the Business Plan and South Staffs Water is in the process of implementing an enhanced Customer Engagement strategy to ensure key stakeholder endorsement of our future plans.

With the publication of the Water White Paper and Ofwat’s Future Price Limits consultation, there is a drive to promote competition, significantly enhance customer engagement and reduce the industry’s impact on the environment. These key documents will have a significant impact on the industry and its regulatory environment. Currently, the plans are at an early stage and work will progress over the coming months to understand the practicalities of the proposed regime. The sentiments of the high level principles are already being factored into the business’s operational activities and future plans.

• Improve the business’s capabilities to schedule jobs for customers directly;

• Improve response times to operational activities; and

• Sustain high operational efficiency.

The first phase of the improvements, being the replacement of systems used in the area of water production and the introduction of devices for staff out in the field to communicate more effectively with Head Office and customers, is well established. The implementation is now being undertaken in the areas of customer operations and network management activities and will continue over the current year.

installations approved as part of the 2009 Periodic Review, good progress is being made which will continue to increase the business’s level of meter penetration.

A comprehensive review of current and future IT capabilities was undertaken in recent years to ensure the business can continue to be efficient in its operations and meet customers’ rising service expectations now and into the future. This review determined a need for significant further investment in systems and IT over a number of years to:

• Allow customers to have improved response times after contacting us;

• Gain better information for customers regarding operational job activities;

South Staffs Water has a culture of

strong employee engagement

9

South Staffs Water has a culture of strong employee engagement, astute financial awareness and planning and a desire to work hard to provide an excellent service to all customers. Over the year a programme has been undertaken to improve the staff appraisal framework with a system which utilises Key Performance Indicators to evaluate staff and management performance.

South Staffs Water is proud of its achievements and is determined to remain one of the best performing companies in the industry, which will only be possible through the continued hard work and support of its employees, suppliers and contractors.

Blithfield Reservoir – the resource position remains

healthy and will continue to be managed closely.

10

Cambridge Water provides drinking water and associated customer services to around 130,000 households and businesses in and around Cambridge, of whom nearly 70% have meters installed. Its area of supply is located in the driest part of the country with average annual rainfall of less than 600mm. It has an excellent record for service and quality while customers’ bills are the second lowest of all water suppliers.

Cambridge Water measures its success against three separate, but mutually supportive, objectives:

• To achieve high levels of performance;

• To comply with its legal and regulatory obligations; and

• To maximise the returns from its regulated assets.

The results of the second year of the current AMP5 regulatory period demonstrate significant success in achieving the business’s objectives. The business outperformed the operating cost targets set for this regulatory period while service performance improved in a number of areas.

The challenge of a second very dry winter in such a water stressed area was met by increased leakage detection and repair, demonstrating to customers and regulators alike a commitment to water efficiency and the environment. Leakage levels per customer and kilometre of the network are now at an

all time low and amongst the lowest in the industry. Control of leakage, combined with high meter penetration and investment in resources following the 1991/93 drought, has resulted in a significant balance of supply over demand. As a consequence Cambridge Water was one of only three suppliers in the East of England able to avoid announcing water use restrictions at the end of the financial year in the face of an unprecedented lack of rain. The unusually wet spring and start to the summer has also helped to mitigate the previously dry conditions.

Water quality remains the business’s highest priority and, while fortunate in drawing all its supplies from chalk aquifers, only six samples out of around 25,000 failed to meet the

Operational Review:Cambridge WaterCambridge Water is respected locally and nationally for its customer service, low prices and innovative approach.

11

Water quality remains the business’s

highest priority

12

prescribed level. This has resulted in a Mean Zonal Compliance of 99.93% for the financial year.

Ofwat’s indicator of customer service is the Service Incentive Mechanism (SIM). The indicator measures both quantitative (by numbers of unwanted calls and complaints) and qualitative (by independent customer survey) service performance. In 2011/12 Cambridge Water improved its score by five percentage points and one of the challenges for 2012/13 is to review our systems and processes to make further advances.

The business has always taken great pride in its approach to finding innovative solutions to its challenges. One such challenge was to reduce the costs of its network repair and maintenance activities. Having identified that difficulties in providing information to repair teams was reducing their efficiency, a pilot project to provide information for repair works on handheld mobile devices was launched. This has proved a success, reducing not only standing and travelling time, but also paper usage as all documents are visible on screen. This system will now be rolled out to all teams.

Major projects progressed well and the business met all of its obligations under its undertaking to deal with rising nitrate levels in its raw water. Although water from the chalk aquifer is generally of very high quality, the rural nature of the catchments and agricultural practice has resulted in rising nitrate levels.

Our first nitrate treatment plant was commissioned at Babraham, East of Cambridge, and the second at Eustom is anticipated to be completed in the current year to continue the business’s record of compliance.

Also completed in the year was the scheme to safeguard supplies to the west and north of Cambridge at peak demands. The Grantchester Road boosters were installed to budget and the planned programme.

The challenge for the coming year may be in the form of a third dry winter and the business is already planning for that possibility.

Cambridge Water has always taken great pride in its approach to finding

innovative solutions to its challenges

13

Cambridge Water is rightly respected locally and nationally for its customer service, low prices and innovative approach. This is made possible by our employees, partners and suppliers, all of whom adopt the following values of the business:

• A personal approach – to customers and employees;

• A local service provided by local people to local people;

• Employees empowered to help; and• One team dedicated to delivering for both shareholders

and customers.

Installation of control building at the Grantchester Road boosters.

14

restriction on public spending being undertaken by Government departments, local authorities and other related bodies, all of whom have been a core source of business for the division.

Despite this, the division performed broadly in line with expectations, whilst ensuring the division further enhances its operating efficiency and remained aligned to its markets and customers. This positive performance is a testament to the strength in depth of the management team and its ability to generate success in a competitive and challenging environment.

During the year, the division acquired Data Contracts, which is a specialist in maintaining and refurbishing

SSI Services is made up of four business streams:

• Clean Water, comprising Hydrosave and Integrated Water Services (IWS);

• Water Hygiene, where IWS also operates;

• Wastewater made up of OnSite Utility Services and Pipe Lining; and

• Industrial Services, including Data Contracts and Perco.

2011/12 was a challenging year for the division due in large part to factors outside of its control. These included the impact on the market caused by the generally weak economic climate which saw the majority of construction markets remaining quiet and the continued

SSI Services, the Group’s specialist infrastructure contracting division, provides a range of added value services from design to installation, and from testing and repair to long-term maintenance capabilities. The division’s businesses work in regulated environments, managing client risk and serving both public and private sectors. Clients range from water utilities to the Environment Agency, major contractors and facilities management companies in the water, wastewater, water hygiene, rail, power generation, construction markets and the public sector. Building and maintaining long-term relationships with clients remains a key focus for the division as does the provision of a quality based service.

Operational Review:SSI ServicesSSI Services is the Group’s specialist infrastructure contracting division, providing a range of added value services.

15

Building and maintaining long-term relationships

with clients is a key focus for the division

16

without sacrificing the quality of service, through effective recruitment and extensive multi-skilling training programmes.

The business has continued to build its presence across the water utility sector including adding South West Water to its water utility framework contracts. Its range of specialist technology based services has been further developed during the year, including the ability to offer customers a valve maintenance service, further advances in undertaking pipe condition assessment works using the likes of “smart ball” technology and advanced camera techniques as well as the provision of “floran” water treatment plant filter cleaning capabilities.

In Scotland, our activities have been consolidated giving clients a complete service offering.

Going forward, Hydrosave is focused on its two core capabilities with the creation of a dedicated leakage framework business unit targeting

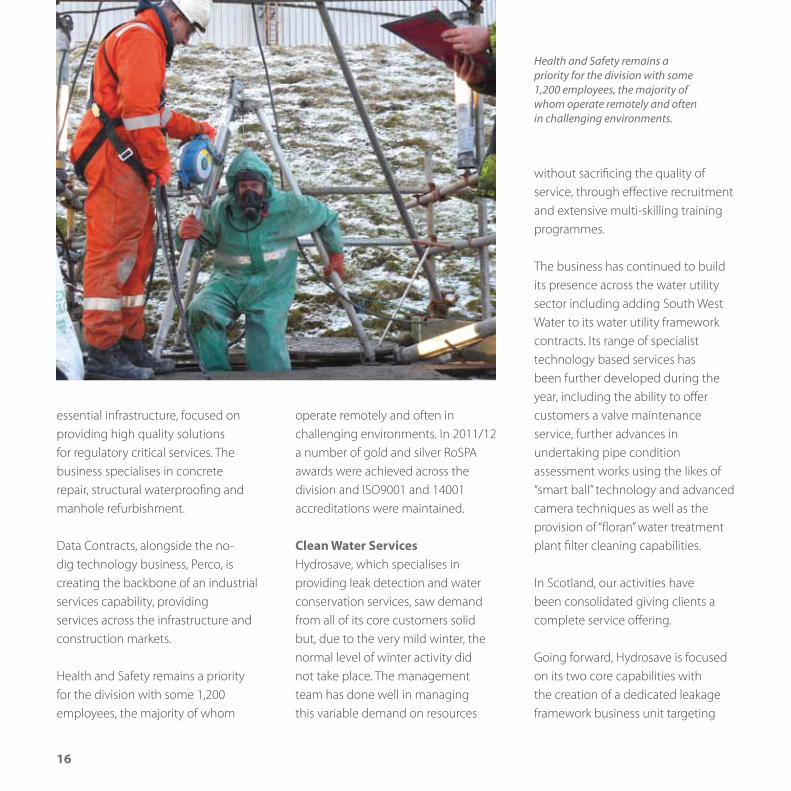

operate remotely and often in challenging environments. In 2011/12 a number of gold and silver RoSPA awards were achieved across the division and ISO9001 and 14001 accreditations were maintained.

Clean Water ServicesHydrosave, which specialises in providing leak detection and water conservation services, saw demand from all of its core customers solid but, due to the very mild winter, the normal level of winter activity did not take place. The management team has done well in managing this variable demand on resources

essential infrastructure, focused on providing high quality solutions for regulatory critical services. The business specialises in concrete repair, structural waterproofing and manhole refurbishment.

Data Contracts, alongside the no-dig technology business, Perco, is creating the backbone of an industrial services capability, providing services across the infrastructure and construction markets.

Health and Safety remains a priority for the division with some 1,200 employees, the majority of whom

Health and Safety remains a priority for the division with some 1,200 employees, the majority of whom operate remotely and often in challenging environments.

17

also had a successful year and has recently undertaken a project laying pipes to a major new water bottling plant in the Midlands. The business has continued to develop strong working relationships with key clients, becoming a valued partner in managing their networks.

scope outside of its traditional Midlands base. The Coal Authority remains an important client for the business which demonstrates the breadth and depth of capabilities and services available in managing and maintaining critical infrastructure.

The Pipeline Services business, which was integrated with IWS at the beginning of 2011/12, has

water utilities as well as a technical services unit which is working closely with water utilities and a wider range of commercial and industrial clients, promoting the use of technology in maintaining clean water networks.

IWS offers Mechanical and Electrical (M&E) services to the clean water market. The business also offers pipeline services, including new lay, repairs, maintenance and replacement of clean water pipes including those provided to South Staffs Water under their AMP5 framework contract. IWS had another excellent year with all parts of the business expanding their areas of operation, geographic scope and customer base.

The M&E business has undertaken further significant projects over the year, including working on a number of projects for South Staffs Water. The division was successful in winning a multi-year contract with Northumbrian Water as well as a new contract with Anglian Water, thereby extending its geographic

The division continues to build its presence across

the water utility and other infrastructure and

regulated sectors

18

a second tier contractor, as well as direct for its traditional water utility customer base.

The management team has continued to invest in business development and resource flexibility to enable it to satisfy its expanding client base. This has included increased amounts of work for the Environment Agency, British Waterways, Local Authorities and the Highways Agency.

Our Swindon office has provided a regional capability to support this wider client base.

The OS8000 Flow Monitoring system has become a recognised market leader in the UK due to its capability to not just record data reliably but also through the development of related software to interpret the information in support of clients’ needs to understand their network capabilities and performance. The system is now being increasingly used for long-term monitoring of key elements of wastewater networks.

local authorities, housing associations and other Government bodies.

Wastewater ServicesOnSite, which offers specialist wastewater services including flow monitoring, sewer rehabilitation, CCTV surveys and a 24/7 reactive sewer maintenance capability, mobilised a number of new contracts including those for Severn Trent Water and Yorkshire Water. The business went through a restructuring process during the year as it re-aligned itself to a new, broader customer base and has looked to enhance its capabilities to work as

Water HygieneIWS has continued to grow its capabilities and geographic presence in the water hygiene market. The business is now working nationally including the facility in Crayford, East London, opened at the beginning of 2011, thereby enabling IWS to better serve the London and south-east markets.

The business is now a market leading provider of legionella control services, water hygiene risk assessment, maintenance and remedial works to a wide range of clients from major facilities management companies to

Looking ahead, the division has the ability to offer its clients more

integrated specialist solutions

19

As a result, growth is anticipated to continue through improved operating efficiencies and new technology which leaves the division well placed to deliver its strategic objectives for 2012/13.

integrated approach to providing specialist infrastructure solutions. 2012/13 should see an increase in AMP5 workloads and, despite the general construction market remaining weak, some growth is anticipated in specialist markets.

In addition, OnSite’s pipe lining business, which provides leading edge sewer lining services, had an excellent year with strong demand in the market and the addition of UV lining to its portfolio (transferred from Perco) has enabled an enhanced product offering for its client base.

Industrial ServicesPerco, the no-dig technology specialist, is recognised as a market leader in undertaking specialist projects where augerboring, directional drilling, pipe-bursting and micro tunnelling is required. Perco is able to serve a broad range of clients from major contractors through to house builders and developers. Together with Data Contracts, which has had a very strong first year in the division, under a single management team, SSI Services has taken the first step in creating an industrial services business unit.

OutlookLooking ahead, the division has the ability to offer its clients, across a broader range of sectors, a more

The division’s businesses work in both the public and private sectors for a

range of infrastructure owners.

20

more accountable by requiring them to focus on meeting their customers’ expectations. As a wide variety of water company activities and service performance issues are captured through the principal forms of customer/company interaction covered by SIM, it provides an effective barometer of a company’s performance as rated by their customers. SIM has brought about a much greater focus on resolving calls on the first contact and managing the customer’s contact as a “case”, which can help to reduce repeat contacts. Echo’s UK water clients are looking to invest in services and tools that support this approach.

As part of its objective to develop and invest in its products, Echo has invested in further research

The water industry is facing a key period of change, with subjects such as the SIM measure, increasing customer debt and the possibility of expanded competition on the agenda. The publication of the Water White Paper has provided the water industry with more guidance on the likely direction the industry will take in the coming years. In this environment, Echo is dedicated to ensuring all of its UK water clients are able to drive change rather than be driven by it.

During 2011/12, Echo has supported its UK water clients as they strive to further improve their levels of customer satisfaction following the introduction of SIM, Ofwat’s customer satisfaction measurement. SIM aims to make water companies

Echo is a leading provider of customer process management services focused on regulated markets. Its services include customer contact management, resolving customer queries and issues, as well as a billing and revenue management service, including its proprietary RapidXtra billing and customer care software.

A fundamentally strong, stable and focused business strategy has enabled Echo to achieve continued growth, despite persistent challenging economic conditions. At the heart of Echo’s strategy is the ability to understand thoroughly the challenges faced by its clients and a commitment to working in partnership to develop solutions to address them.

Operational Review:EchoEcho is a leading provider of customer process management services focused on regulated markets.

21

Echo remains focused on further business growth

though new opportunities

22

In line with the objective to grow the business, Echo secured a further extension to the NI Direct contract and has continued to work closely with the client as they shape the future of the service. A highlight of the year was achieving the recommendation for continued certification of the Customer Contact Association Standard. This is the fourth consecutive year this recommendation has been made. It is expected that the award of the longer term strategic partnership procurement project will be made during 2012.

During the year a Director of Business and Product Development was appointed. This is an important executive appointment which reflects Echo’s continued commitment to growing the business and continuing to win new clients.

In line with the business’s objective to develop and invest in its people, Echo was successfully reassessed for the Investors in People accreditation. The

of businesses able to switch their water supplier from 2,200 to 26,000. This change could potentially impact the billing and customer service functions of UK water companies and Echo is currently working with its clients to help meet their individual requirements.

Echo’s London based debt collection agency, Inter-Credit International, has performed and grown as planned, despite challenging economic conditions. Inter-Credit has maintained its relationships with its public sector clients and has increased its penetration into the UK water industry by securing two new clients.

and development for RapidXtra, which has resulted in innovations in the areas of business process management, meter data management and web self-service. The business is focused on ensuring that its roadmap of future developments continues to support the key challenges facing its water industry clients. For example, in 2011 the Water White Paper outlined the potential for increased competition for commercial customers. Ofwat subsequently lowered the threshold for large water users in England from 50 megalitres to five megalitres per annum. This increases the number

Echo Northern Ireland was highly commended in the ‘Right Place to Work’ category of Northern Ireland’s most prestigious business awards.

23

public sector service providers. Echo will also continue to support its clients through the implications of SIM and the impact of the Water White Paper.

for Echo with a number of potential growth opportunities already identified. We expect the outcome of these to be realised in the course of the year. Echo remains fully committed to building on its position in Northern Ireland, where it is already established as one of the leading

assessment, which measures how the performance of an organisation is improved through the management and development of its people, included Echo India (where IT development activities take place) for the first time. A further highlight for the year was Echo Northern Ireland being highly commended by the Irish News at their annual Workplace and Employment Awards in the Right Place to Work category. The awards, the most prestigious business awards in Northern Ireland, recognise excellence in the workplace, with the Right Place to Work award honouring socially responsible organisations that can demonstrate close links to community or charitable initiatives and which have a genuine commitment to environmental issues.

Looking to the future, Echo remains focused on further business growth through new opportunities currently being worked on, including existing client relationships. The 2012/13 financial year will be a pivotal year

Echo is supporting its UK water clients as

they strive to further improve their levels of customer satisfaction

24

Financial ReviewThe Group has once again exceeded its financial targets for the year.Despite the continuing lack of growth in the UK economy and the challenging commercial environment, the Group has once again exceeded its financial targets for the year to 31 March 2012, through a combination of making the most of its opportunities and by continuing with tight cost and cash flow control. The Board is confident that the Group remains well positioned for further growth in 2012/13.

Turnover and ProfitGroup turnover increased by £29.3m (18.4%) to £188.8m (2011: £159.5m). After adjusting for the acquisitions made in the year and the full year effect of acquisitions made in the previous year this represents like-for-like growth of £7.6m (4.6%), representing an encouraging performance in a difficult economic environment.

Total turnover from regulated companies amounted to £102.1m (2011: £87.8m). South Staffs Water’s turnover increased from £87.8m to £91.1m, primarily due to the inflationary price increase allowed by Ofwat of 4.7%. The turnover of Cambridge Water, since its acquisition by the Group in October 2011, amounted to £11.0m.

Turnover from the Group’s non-regulated service companies increased by £15.1m to £86.7m (2011: £71.6m), with the increase being partly the result of acquisitions made during the year (£4.3m), the full year effect of those made last year (£6.4m) and further organic growth (£4.4m) in the majority of businesses as demand from our main customer base increased. This was due partly to 2011/12 being the second year of the AMP5 capital investment period in the water sector but also due to

a number of new contracts being awarded and further growth from our existing client base.

The Group’s operating profit (before goodwill amortisation) of £38.3m was ahead of our expectations and £8.7m ahead of last year with increased profits arising from the acquisitions made in the year (£5.5m), the full year effect of those made last year (£1.1m) and encouraging organic growth (£2.1m). High levels of inflation experienced throughout most of the year have put pressure on our cost base and profit margins, although tight control of costs where possible have mitigated the impact.

Operating profit in respect of our regulated companies increased by £4.0m to £25.6m. After adjusting for the impact of the acquisition of Cambridge Water, this represents like-for-like growth of £2.3m in respect

25

of South Staffs Water on last year with higher water charges of 4.7%, as allowed by Ofwat, partly offset by higher costs representing the effect of the expected inflationary pressures, additional power costs required to respond to the very dry weather conditions in the year, additional resources to ensure challenging service targets are achieved net of further operational efficiencies that have been generated. The operating profit of Cambridge Water, since its acquisition, amounted to £3.7m, being ahead of expectations set at acquisition, due principally to lower than expected operating costs.

Operating profit from our non-regulated service companies increased by £3.3m to £9.7m reflecting increased trading activity in the majority of the businesses, profits arising from acquisitions made in the year and the full year effect of acquisitions made last year. Total Group operating profit (after goodwill amortisation) was £35.3m (2011: £28.1m).

Finance charges (net of interest receivable) increased to £12.2m (2011: £8.7m) in the year principally due to the interest payable on increased borrowings (see below - including the borrowings of Cambridge Water which was acquired in October 2011). Overall, profit before tax increased from £20.8m to £23.1m.

TaxThe Group’s tax charge increased to £0.9m (2011: £0.3m) mainly representing the increase in Group profits as explained above.

DividendsTotal dividends paid and proposed in the year were £21.4m (2011: £28.8m). This includes £5.9m in respect of 2010/11 which was paid and proposed in the year but reflected

Tight cost control has helped to

mitigate the impact of high inflation

26

Staffs Water’s total expenditure (net of contributions) for the first two years of the AMP5 investment period of £54.3m is marginally behind Ofwat’s Final Determination after adjusting for an unexpected adjustment to the COPI index used to inflate the Determination. It is expected that the total shortfall to date of £3.3m will be recovered in 2012/13.

Tax payments amounted to £2.7m, an increase of £2.8m on last year, mainly representing the increased profits as detailed above.

Overall, free cash flow reduced to £18.0m from £24.3m with the reduction of £6.3m being better than expected and representing the Group’s continuing commitment to achieving strong cash flow performance.

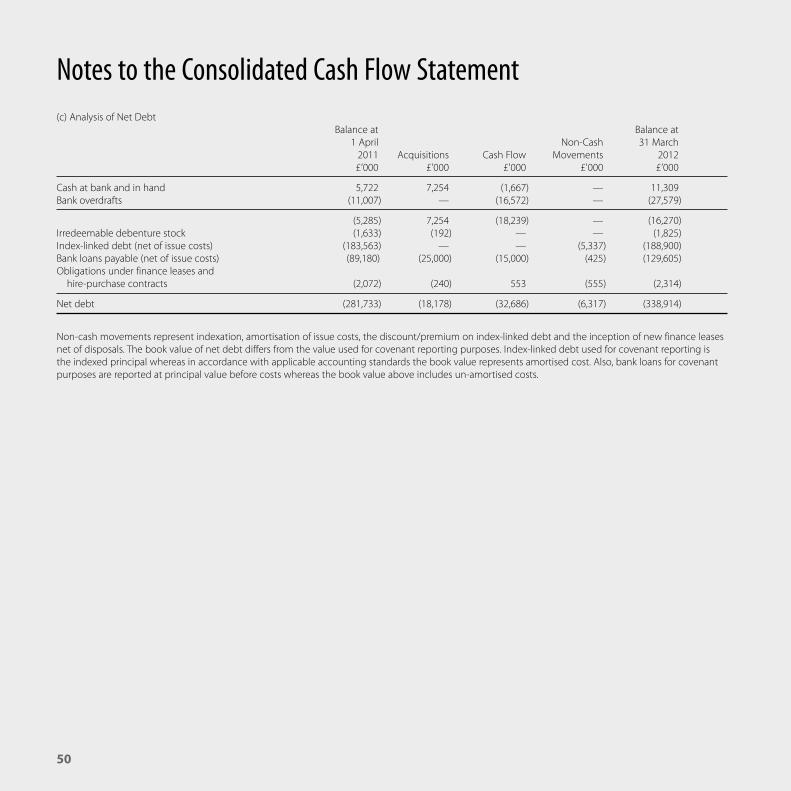

Group net book debt at 31 March 2012 amounted to £338.9m (2011: £281.7m). This differs from the value used for covenant reporting purposes of £325.8m (2011: £266.5m) which excludes unamortised

environment and reflects the Group’s ongoing commitment to keep working capital at efficient levels.

The Group’s net cash interest payments increased by £4.2m to £7.7m (2011: £3.5m) mainly due to higher interest paid on increased levels of borrowings, although the amounts paid were lower than expected due in part to strong cash flow performance and partly due to lower than expected interest rates.

Capital expenditure (net of capital contributions) increased to £34.5m compared to £29.9m last year, mainly reflecting the half year impact of Cambridge Water which was acquired in October 2011. South

better than expected cash flows and levels of debt achieved in 2010/11. Dividends of £15.5m were paid or proposed in respect of 2011/12, including a final dividend of £0.6m paid in April 2012. Dividends paid in cash in the year amounted to £23.3m (2011: £27.4m).

Cash Flow & DebtCash flow from operating activities was better than expected at the start of the year and increased to £61.0m from £56.4m mainly as a result of higher operating profits, as explained above, partly offset by lower working capital reductions than last year due to growth in trading activities, although this was better than expected in a very challenging

During the year, the Group invested £34.5m in capital

assets

27

Water, Cambridge Water and the Group has maintained significant headroom in respect of all borrowing covenants.

Standard and Poors continues to rate South Staffs Water as BBB+, well within investment grade, and South Staffordshire Plc as BBB-.

PensionsAs at 31 March 2012 the actuarial valuation of the Group’s existing final salary pension scheme (prepared in accordance with FRS 17) showed a post tax surplus of £9.2m (2011: £11.8m), with the year-on-year movement principally reflecting an increase in the value of the scheme assets with improvements in world-wide equity values offset by an increase in the present value of scheme liabilities due mainly to lower discount rates.

premium and issue costs and uses actual inflation at the relevant dates as opposed to the long-term inflation assumption used in the book value of index-linked debt. The increase in the covenant value from March 2011 of £59.3m mainly reflects the impact of acquisitions made during the year and higher values for index-linked debt of £7.9m, due to high levels of inflation experienced during the year.

South Staffs Water’s net debt for covenant reporting purposes was £182.8m (2011: £174.6m) being 72.4% (2011: 73.2%) of its Regulated Asset Value (RAV) of £252.5m (2011: £238.5m) being the Final Determination RAV uplifted for inflation. This ratio reflects inflation (RPI) at March 2012 of 3.6%, which is used to inflate RAV, whereas the majority of index-linked debt was inflated using inflation at July 2011 of 5.0%. South Staffs Water’s dividend policy is to pay dividends up to 77% of net debt/RAV although over the AMP5 period this ratio is expected to be at or below 77%. South Staffs

28

Corporate Social ResponsibilityCorporate Social Responsibility remained a focus during the year.

Corporate Social Responsibility (CSR) remained a focus for many activities during 2011/12. The environment and community in particular have benefited from a considered approach with various projects related to Sites of Special Scientific Interest, water efficiency and support for local and national charities.

During the year, Echo Northern Ireland was highly commended in the Irish News Workplace and Employment Awards in the ‘Right Place to Work’ category. The most prestigious business awards in Northern Ireland recognise excellence in the workplace, honouring social responsibility.

Health & SafetyThe Group recognises its employees’ contribution to the continued success of its businesses and is committed to safeguarding their occupational health, safety and welfare by providing, as far as

reasonably practical, a safe and healthy environment in which to work.

The Group believes that health and safety management should remain firmly at a local level within each business, ensuring individual Boards of Directors accept responsibility to protect the health and safety of their staff. To monitor this, and ensure consistent standards and governance, a Group Health and Safety Strategy Forum exists, led by the Group Finance Director which includes the Managing Directors of all the Group divisions.

All businesses operate under a comprehensive occupational health and safety management system, the majority of which have gained or retained certification to the internationally recognised OHSAS 18001:2007 standard. Systems continue to be reviewed to ensure they remain suitable and effective

and are aligned with the evolving needs of each business and external accreditation requirements. In addition, individual businesses continue to be externally recognised for excellence in safety performance, gaining awards from RoSPA and the British Safety Council.

During 2011/12 most businesses have been subjected to an external health and safety audit undertaken by RoSPA. The audit scores confirmed that, as a minimum, good levels of health and safety practice are being achieved, with the majority of businesses demonstrating high performance. The remaining businesses will be audited in 2012/13.

Although employee numbers across the Group continue to rise, the focus remains on targetting an incident and injury free environment for all. As such, monthly reporting to the Board now includes all accident frequency rates (accidents per

29

for renewable energy schemes according to current subsidy regimes.

At Blithfield, surveys have been carried out to explore the possibilities of creating a sustainable woodland management plan and the clearance of intrusive rhododendrons in order to revitalise approximately 38 hectares of dense woodland. Land drainage channels have been dredged to assist tenant farmers in reducing the extent of waterlogged areas of arable land with the added benefits of releasing more ground water run-off into the reservoir and creating new wildlife habitat.

to 1.2 million customers per annum. 96% of the electricity supplied now comes from good quality combined heat and power sources so has a lower carbon footprint than power from most other sources.

South Staffs Water’s strategy is to reduce carbon emissions in three main areas: firstly, continuing with a successful energy management programme and maintaining pumps to the highest efficiency levels in the water industry; secondly, reducing the volumes of water treated and pumped on a daily basis by further managing leakage and encouraging water efficiency; and thirdly, continuing to assess opportunities

100,000 hours worked) and severity rates (days absent per 100,000 hours worked) rather than simply capturing reportable accident totals. For the most part, businesses are making good progress; however, the number of reportable accidents, taking into account new business acquisitions, has increased from 22 incidents last year to 25. All accidents continue to be investigated appropriately in order to learn any lessons that can be implemented to improve health and safety standards.

EnvironmentClimate change is recognised as the greatest environmental challenge facing the world today. South Staffordshire Plc recognises the commitment of the UK government to tackle climate change and reduce carbon emissions by 34% from 1990 levels by the year 2020 and 80% by 2050.

At present, the vast majority of the electricity supplied to South Staffs Water is used to treat and pump over 124 million tonnes of drinking water

At Blithfield, land drainage channels have been dredged to help tenant

farmers reduce the extent of water-logged arable land.

30

Stakeholders- EmployeesThe Group, which strives to maintain its position as a highly regarded employer, has approximately 2,200 employees who all contribute to its success.

The Group runs many campaigns promoting personal health and well-being as well as screening programmes and full Occupational Health support. Much importance is placed on promoting personal health, a healthy workplace and working environment.

The Group’s commitment to development and training continues, resulting in a strengthening of the training team, helping drive excellence in Customer Service. Furthermore, at South Staffs Water, an implementation project was launched with the aim of introducing employee KPIs for all roles in April 2012. Based on a phased approach, role profiles and KPIs have been developed and agreed for more than 150 roles, including the Executive Team. Work is continuing on a scoring mechanism to be introduced at half year appraisals, following trials of internally developed options earlier in the year.

Employees are offered membership of a Group pension scheme, most employees have access to discounted private medical insurance schemes and an Employee Assistance Programme. Employees have access to an on-site nursery at Head Office, run by Busy Bees, which was rated as Good by Ofsted at its last inspection and takes part in a wide variety of activities.

The Group ensures that its equal opportunities policies are effectively operated, making every reasonable effort to ensure that all people have equal opportunities for employment, training and promotion, and strives for continued employment under normal terms and conditions where possible if an employee becomes disabled.

- CustomersRelationships with customers form a key element of the Group’s continued success and stability. The Group continues to strive for customer satisfaction in all areas, from domestic, public and commercial customers, through continued

Echo’s Community Scheme saw employees from the Midlands team extend their support to West Midlands based Acorn Children’s Hospice.

31

provision of high quality customer service, innovation and delivery of excellent service.

- CommunityEducation-based initiatives continued to benefit both the community and the Group alike. Emphasis was placed on partnerships with local schools to deliver water efficiency assemblies, outreach key stage 2 and 3 learning programmes and support for engineering road shows organised by Enterprise Business Partnerships.

The Group contributed £128,000 in the year to charities and sponsorship of youth teams and organisations linked to employees.

In addition, events ranging from a Gala Dinner, running half marathons, climbing mountains and sponsored bike rides raised in excess of £20,000 for WaterAid during the year. Echo employees raised over £5,000 for causes including Macmillan, Simon Community, Comic Relief, Make a Wish Foundation, PIPS and Mencap.

Echo’s Community Scheme, which allows employees to carry out charitable work in their local communities, saw employees support Habitat for Humanity and participate in Business in the Community events in Northern Ireland. In addition, the Midlands team extended their support to West Midlands based Acorns Children’s Hospice.

South Staffs Water’s Employee Volunteer Scheme continued to attract support for a wide range of community and environmentally based activities. Employees were involved in local projects including reading for the blind, habitat conservation, building restoration projects and fund raising events for charities.

Education-based initiatives continued to benefit both the Community and the

Group alike

32

and has previously been the Midlands area President of the Institute of Water Officers.

3. Stephen Kay, BSc (Eng), CdipAF, MICE, MCIWEMAppointed as Managing Director of Cambridge Water in April 2000, after a long career in the water industry – firstly in South Africa and Mauritius before commencing 36 years in the English water industry with Lee Valley Water, Thames Water and Cambridge Water. Stephen is Chairman of both the Water UK Standards Board and The Water Regulations Advisory Scheme Ltd. Stephen is a Board member for the Water Companies Pension Scheme trustee company.

4. Andrew Garcia, MBA, BA (Hons)Appointed as Managing Director of SSI Services in September 2010.

1. Adrian Page, BSc (Hons) ACAExecutive Director of South Staffordshire Plc. Appointed as Group Finance Director in April 2004. Previously Group Finance Director of South Staffordshire Group Plc from 1998 to 2002. Prior to this appointment Adrian worked for ACT Group Plc and KPMG. Adrian is a Board member for the Water Companies Pension Scheme trustee company.

2. Liz Swarbrick, PhD, BScAppointed as Managing Director of South Staffs Water in February 2011, having previously worked with the business as Quality and Planning Director and Regulation and Asset Management Director. A chemist by profession, she has over 20 years’ experience in the water industry. Liz has represented South Staffs Water in a number of strategic Water UK groups

The Executive Team

Prior to his appointment, Andrew spent 28 years in industry in the UK and in Europe having worked with Veolia ES, SIG Plc and Pilkington Glass in a variety of operational and commercial senior management roles. Andrew also led an Energy and Environment team as part of a major US consultancy specialising in public sector procurement, including working as Commercial Director for the Welsh Assembly Government’s Environment Department.

5. Phillip Newland, BA (Hons)Appointed Managing Director of Echo in April 2006, having previously worked with the business as Project Director and as Business Development Director. Prior to joining Echo, Phil was a Management Consultant with Automatic Data Processing (ADP) and Terence Chapman Associates.

1. 2. 3. 4. 5.

33

Directors Adrian Page

Simon Riggall

Alex Black

Secretary Jason Goodwin

Registered Office Green Lane, Walsall, West Midlands, WS2 7PD

Telephone: 01922 638282 Registered in England, Number 4295398

Auditor Deloitte LLP

Four Brindleyplace, Birmingham, B1 2HZ

Directors & Advisors

34

The Directors have pleasure in presenting their Annual Report for the year ended 31 March 2012.

Principal Activities and Review of BusinessThe Group is engaged in regulated water supply to domestic, industrial and commercial customers and non-regulated services in the water and wider infrastructure sectors. A detailed review of the Group’s businesses and the future development of the Group is presented in the Executive Summary, the Operational Review and the Financial Review on pages 2 to 27.

Major Corporate TransactionsThe Group has made two acquisitions during the financial year to 31 March 2012, as follows:• Cambridge Water PLC – a

regulated supplier of clean water in Cambridge and the surrounding area; and

• Data Contracts Specialist Maintenance Limited – a specialist infrastructure maintenance business, based in Nottingham.

As the Group owns two regulated water supply companies, the acquisition of Cambridge Water was referred to the Competition Commission for its review. On 31 May 2012, the Competition Commission cleared the acquisition without the need for remedies.

Except for any matters referred to elsewhere in this Annual Report, there have been no other significant events affecting the Company or any of its subsidiary undertakings since the end of the financial year.

Financial ResultsThe Group’s turnover increased to £188.8m (2011: £159.5m) with total operating profit of £35.3m (2011: £28.1m) and profit before tax of £23.1m (2011: £20.8m). The Group’s results are explained in more detail in the Financial Review on pages 24 to 27 and shown in the consolidated profit and loss account and the consolidated cash flow statement on pages 44 and 48.

Financial And Treasury RiskDetails of the Group’s policy in respect of financial and treasury risk are provided in note 28 to the accounts.

Fixed AssetsCapital expenditure before contributions towards tangible fixed assets, including infrastructure renewals, amounted to £40.7m (2011: £34.9m) during the year.

DirectorsNo Director had any material interest in any contract of significance with the Company or the Group during the year under review.

Indemnities have been given to all of the Directors to the extent permitted by the Companies Act 2006. Directors’ and Officers’ insurance has been established for all Directors and senior management to provide cover against any actions brought against them as Officers of the South Staffordshire Plc group of companies.

Directors’ Report

35

Details of the Directors who held office at the date of this report are as detailed in the table below.

Retirement & Re-Election Of DirectorsIn accordance with the Companies Act 2006 and the Articles of Association, Mr Black will retire by rotation and being eligible will offer himself for re-election.

Corporate Social ResponsibilitySouth Staffordshire Plc regards compliance with relevant environmental laws, the adoption of responsible social and ethical standards and the well-being and development of its employees, including disabled persons, as integral to its businesses. A summary of the Group’s practices is provided on pages 28 to 31.

Corporate Governance & RiskA report on corporate governance including the Group’s approach to risk management and the Directors’ assumptions in respect of preparing the accounts on a going concern basis is set out on pages 36 to 40.

DonationsCharitable donations and sponsorship of £128,000 were made during the year (2011: £117,000). There were no political contributions in the year (2011: nil).

Payment of CreditorsThe Group’s policy is to pay suppliers in line with the terms of payment agreed with each of them when contracting for their products or services. Group trade creditors at 31 March 2012 represent 57 days of purchases during the year (2011: 59 days).

AuditorIn Accordance with the Companies Act 2006, the Directors confirm that as far as they are aware, there is no relevant audit information of which the Company’s auditor is unaware, and that the Board has taken all reasonable steps to make itself aware of any relevant audit information and to establish that the Company’s auditor is aware of that information.

A resolution proposing the reappointment of Deloitte LLP as auditor will be put to the Annual General Meeting.

By Order of the Board

J GoodwinCompany Secretary29 June 2012Directors who held office during the year

First Appointed

Mr A Page 4 December 2003

Mr S Riggall* 14 November 2007

Mr A Black* 26 March 2010* Denotes a Non-Executive Director

36

South Staffordshire Plc and its subsidiary undertakings (the “Group”) continues to apply the spirit of the Combined Code where considered applicable to the Group.

The Board of DirectorsThe Group Board comprises of one Executive Director and two Non-Executive Directors.

Directors may be appointed by the Company by Ordinary Resolution or by the Board. As set out in the Company’s Articles of Association, a Director appointed by the Board will hold office until the next Annual General Meeting (AGM). At each AGM one third of the Directors will retire by rotation and will submit themselves for re-election at least once every three years.

All Directors and senior management are covered by Directors’ & Officers’ insurance against any actions taken against them as Officers of the Group.

Functions of the BoardCompany Law requires that a company has an effective Board, with duties aligned to the success and interests of the Company, setting strategic goals and ensuring that Company strategy is fulfilled.

The Board sets standards of conduct to promote the success of the Company, provides leadership, reviews the Group’s internal controls, risk management policies and governance structure. It approves major financial and investment decisions over senior management thresholds and evaluates the performance of the individual businesses and the Group as a whole by monitoring reports received directly from the subsidiary businesses and those prepared at a Group level. The Non–Executive Directors have a duty to oversee this work, and to scrutinise management performance.

In addition to the Audit Committee and guidance from the Turnbull recommendations, the Board is also

responsible for the Group’s systems of internal control, evaluating and managing significant risks to the Company and the Group.

In compliance with the Combined Code, all Board members are provided with sufficient information prior to any Board meeting to allow preparation time to ensure that they can properly discharge their duties. The Board undertakes site visits to maintain familiarity with the Group’s operations.

The Board also keeps up to date with legal and regulatory changes by receiving written briefings where appropriate from both internal and external advisors.

A schedule of matters specifically reserved for the Board’s decision has been adopted. The terms include, but are not limited to:

• Approval of capital and operating budgets;

• Reviewing and approving the Group’s strategy;

Corporate Governance

37

management, including the Executive Team. Non-Executive Directors do not receive any remuneration or fee.

The total remuneration package of the Executive Director and senior management includes basic salary, benefits, an annual bonus and a long-term incentive bonus that is linked to individual business targets and performance related incentives. Performance related incentives are designed to encourage and reward continuing improvement in the Group’s performance over the longer term.

Board Committees– Remuneration CommitteeThe Remuneration Committee is responsible for the remuneration policy of the Board and senior management, including the Executive Team, and meets at least once a year. No Director is involved in determining his own remuneration.

policies and procedures and other matters that are not reserved for the Board. There are written procedures containing a regime of authorisation levels for key decision-making.

The Board undertakes an informal evaluation of its performance, the performance of the individual Directors and various Committees. These appraisals do not take a written form as it is felt that more formal procedures would not add to the effectiveness of the Board.

All Directors are aware of the procedure for those wishing to seek independent legal and other professional advice. The Board also has access to the advice and services of the Company Secretary.

RemunerationThe remuneration packages are designed to attract, retain and motivate high-calibre Directors. The Remuneration Committee has overall responsibility for determining the Executive Director’s remuneration package and level and those of senior

• Reviewing and approving any changes to the Group’s capital structure;

• Review and approval of financial reports;

• Review and approval of major contracts; and

• Powers to delegate authority.

The Board maintains a flexible approach to Board matters with the delegation of power to a Committee, with precise terms of reference, being used for specific routine purposes. Both the terms of reference and composition of the Committees are regularly reviewed to ensure their ongoing effectiveness.

The Directors are supported by a team of senior managers, including the Executive Team, who have responsibility for assisting them in the development and achievement of the Group’s strategy and reviewing the financial and operational performance of the Group and its individual businesses. This team of senior managers is responsible, along with the Board, for monitoring

38

The key terms of reference for the Committee in this respect are to:

• Review and appraise the work of the external auditor;

• Monitor, review and challenge when necessary the integrity of the financial statements of the Company and other Group companies, including its Annual Report and any other formal announcement relating to its financial performance, and reviewing significant financial reporting issues and judgements which they contain; and

• Keep under review the effectiveness of the Company’s and the Group’s internal controls and risk management practices and policies.

There are also separate independent Audit Committees for both of the regulated companies in the Group, South Staffordshire Water PLC and Cambridge Water PLC.

– Audit CommitteeThe Audit Committee meets twice each financial year. Deloitte LLP, the Group’s external auditor, the Company Secretary and the Group Internal Audit Manager are also invited to the meetings.

The Committee is responsible for reviewing and monitoring the Group’s internal controls and systems for mitigating the risk of financial and non-financial loss. This includes assessing the integrity of financial statements, including changes to accounting policies, reviewing financial reporting procedures and risk management systems.

The Committee is responsible for recommending to the Board the appointment of the external auditor and monitoring the auditor’s independence, performance and effectiveness and approving the nature and scope of external audits and approving the auditor’s remuneration.

The key terms of reference for the Committee are to:

• Agree remuneration that will ensure that the Executive Director and senior management are provided with appropriate incentives to achieve high standards of performance and reward them for their individual contributions to the success of the Group;

• Determine such packages and arrangements with regard to any relevant legal requirements and associated guidance and to obtain reliable, up-to-date information about remuneration in other companies;

• Approve the design of, and determine targets for, any performance related pay schemes operated within the Group;

• Ensure that contractual terms on termination are fair and that failure is not rewarded; and

• Oversee any major changes in employee benefits structures throughout the Group.

39

into account the nature of the Group’s operations and risks. This process includes the identification, evaluation and management of the significant risks faced by the Group. The Board considers the internal audit arrangements in operation are appropriate to the size and complexity of the business but will continue to review these arrangements on a regular basis.

The Audit Committee will normally meet to review the annual accounts, to monitor the adequacy and effectiveness of internal controls and to review external and internal audit activity and strategy.

– Organisational StructureA defined organisational structure for the Group exists with clear lines of accountability and appropriate division of duties.

The Board sets overall policy and strategy and has delegated the necessary authority to departments in order to fulfil these. This is communicated to employees by way

prepared on a regular basis, as is the Group’s level of borrowing facilities, their maturity dates and liquidity.

The responsibilities of the external auditor in the area of financial reporting are set in their report in each year’s Annual Report.

– Internal ControlThe Board attaches considerable importance to its system of internal control and for reviewing its effectiveness, including its responsibility for taking reasonable steps for the safeguarding of the assets of the Company and the Group and for preventing and detecting fraud and other irregularities. Such a system is designed to manage rather than eliminate the risk and can nonetheless provide only reasonable, and not absolute assurance, against misstatement or loss. The Board has delegated some responsibility for such reviews to the Audit Committee.

There is an established internal control framework that is continually reviewed and updated taking

Accountability and Audit– Financial Reporting and

SystemsThe Board of Directors recognises the need to present a balanced and clearly defined assessment of the Group’s operational and financial performance and position including its future prospects. This is provided by a review of the Group’s performance as set out in the Executive Summary, Operational Review and Financial Review of each year’s Annual Report.

Three-year business plans, annual budgets and investment proposals for each business and for the Group have been formally prepared, reviewed and approved by the Board. These include three-year profit and loss and cash flow forecasts. Financial results and cash flows, including a comparison with budgets and forecasts, are reported to the Board monthly with variances being identified and used to initiate any action deemed appropriate. Forecasts of the Group’s compliance with its borrowing covenants are also

40

– External AuditorThe Board, assisted by the Audit Committee, reviews each year the external auditor’s performance, effectiveness and fees including the level of non-audit services and fees.

– Going ConcernThe Directors consider each year the appropriateness of the assumption of preparing the accounts on a going concern basis. This is based upon a review of the Company’s and the Group’s budget, the three-year operating plan, financial forecasts, the investment programme, and forecast compliance with borrowing covenants and with the committed borrowing facilities available to the Group.

of published policies and procedures and regular management briefings. The Group’s extensive financial regulations specify authorisation limits for individual managers, with all material transactions being approved by a member of the Board. In addition, formal treasury policies are in place. Where appropriate, commercial and financial responsibility is clearly delegated to local business units and supported by the Board.

– Risk ManagementRisk management is discussed at Board level both in terms of the Group and its businesses on a regular basis. The Group’s individual businesses are required to monitor risk and its management with any significant changes in business risk and any subsequent actions or controls to mitigate the risk being reported to the Board and the Audit Committee.

41

The following statement, which should be read in conjunction with the auditor’s statement of its responsibilities set out on the following pages, is made with a view to distinguishing for shareholders the respective responsibilities of the Directors and of the auditor in relation to the accounts.

Company Law requires the Directors to prepare accounts for each financial year which give a true and fair view of the state of affairs of the Company and the Group as at the end of the financial year. Under that law the Directors have elected to prepare the accounts in accordance with United Kingdom Generally Accepted Accounting Practice (United Kingdom Accounting Standards and applicable law).

In preparing these accounts, the Directors are required to:

• Select suitable accounting policies and then apply them consistently;

• Make judgments and accounting estimates that are reasonable and prudent;

• State whether applicable UK Accounting Standards have been followed, subject to any material departures disclosed and explained in the accounts; and

• Prepare the accounts on the going concern basis unless it is inappropriate to presume that the Company will continue in business, in which case there should be supporting assumptions or qualifications as necessary.

The Directors confirm that they have complied with the above requirements in preparing the accounts.

The Directors are responsible for keeping adequate accounting records that are sufficient to show and explain the Company’s and the Group’s transactions and disclose with reasonable accuracyat any time the financial position of the Company and the Group and

enable them to ensure that the accounts comply with the Companies Act 2006. They are also responsible for safeguarding the assets of the Company and the Group and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

The Directors, having prepared the accounts, are required to provide the auditor with such information and explanation as the auditor thinks necessary for the performance of its duty.

The Directors have responsibility for the maintenance and integrity of the Company’s website. Information published on the internet is accessible in many countries with different legal requirements. Legislation in the United Kingdom governing the preparation and dissemination of accounts may differ from legislation in other jurisdictions.

Directors’ Responsibilities Statement

42

We have audited the financial statements of South Staffordshire Plc for the year ended 31 March 2012 which comprise the consolidated profit and loss account, the consolidated and individual Company balance sheets, the consolidated statement of total recognised gains and losses, the reconciliation of movements in consolidated shareholders’ funds, the consolidated cash flow statement, notes to the consolidated cash flow statement, and the related notes 1 to 31. The financial reporting framework that has been applied in their preparation is applicable law and United Kingdom Accounting Standards (United Kingdom Generally Accepted Accounting Practice).

This report is made solely to the Company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the Company’s members those matters we are required to state to them in an auditor’s report and for no

other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of Directors and auditorAs explained more fully in the Directors’ Responsibilities Statement, the Directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s Ethical Standards for Auditors.

Scope of the audit of the financial statementsAn audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Group’s and the parent Company’s circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the Directors; and the overall presentation of the financial statements. In addition, we read all the financial and non-financial information in the annual report to identify material inconsistencies with the audited financial statements. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report.

Independent Auditor’s Report

43

report to you if, in our opinion:• adequate accounting records

have not been kept by the parent Company, or returns adequate for our audit have not been received from branches not visited by us; or

• the parent Company financial statements are not in agreement with the accounting records and returns; or

• certain disclosures of Directors’ remuneration specified by law are not made; or

• we have not received all the information and explanations we require for our audit.

David Hall FCA(Senior Statutory Auditor)for and on behalf of Deloitte LLPChartered Accountants and Statutory AuditorBirmingham, UK29 June 2012

Opinion on financial statementsIn our opinion the financial statements:• give a true and fair view of the

state of the Group’s and of the parent Company’s affairs as at 31 March 2012 and of the Group’s profit for the year then ended;

• have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice; and

• have been prepared in accordance with the requirements of the Companies Act 2006.

Opinion on other matter prescribed by the Companies Act 2006In our opinion the information given in the Directors’ Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

Matters on which we are required to report by exceptionWe have nothing to report in respect of the following matters where the Companies Act 2006 requires us to

Independent Auditor’s Report

44

Consolidated Profit & Loss AccountFor the year ended 31 March 2012

2012 2011 Note £’000 £’000

Turnover 2 188,796 159,452Less share of joint ventures’ turnover (245) (815)

Group turnover 188,551 158,637

Operating costs before goodwill amortisation (net) 3 (150,200) (128,892)

Group operating profit before goodwill amortisation 38,351 29,745

Share of joint ventures’ operating loss (64) (96)

Total operating profit before goodwill amortisation 38,287 29,649

Goodwill amortisation 11 (2,982) (1,567)

Total operating profit after goodwill amortisation 2 35,305 28,082

Exceptional profit on sale of tangible fixed assets — 1,465

Profit on ordinary activities before finance charges (net) 35,305 29,547

Finance charges (net) 7 (12,209) (8,744)

Profit on ordinary activities before taxation 23,096 20,803

Taxation on profit on ordinary activities 8 (875) (296)

Profit on ordinary activities after taxation 22,221 20,507

Less profit after tax of minority interests 26 (5) (1)

Profit for the financial year 22,216 20,506

Earnings per share Basic and diluted 10 173.3p 160.0p

A statement of movements in reserves is given in note 24 to the accounts.

The results above are all derived from continuing operations. The results of the businesses acquired during the year are disclosed seperately in note 2 to the accounts.

The accompanying notes are an integral part of these accounts.

4545

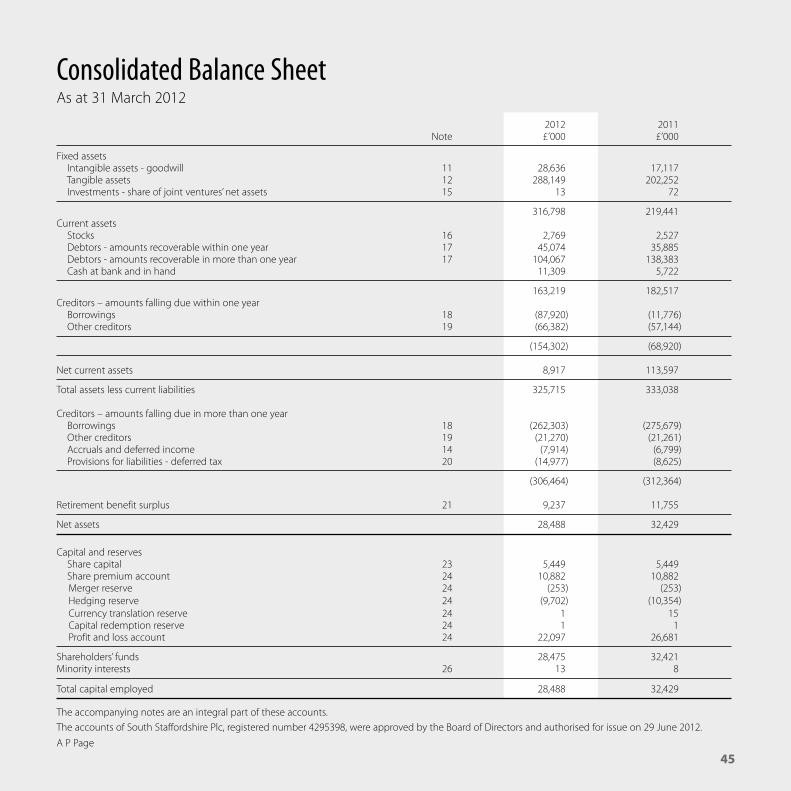

Consolidated Balance SheetAs at 31 March 2012

2012 2011 Note £’000 £’000