Embed Size (px)

DESCRIPTION

The release of the CW Group’s “2012 Middle East and Africa Cement Business Sentiment Survey” marks the third year the survey has been undertaken. The report shares a synopsis of current and emerging trends in the African and Middle Eastern region. Survey data was collected from key industry contributors throughout North Africa, Sub-Saharan Africa (SSA), the GCC States, other Middle East countries, and Turkey.

Citation preview

CemWeekCemWeekCemWeekCemWeekBMWeekBMWeekBMWeekCW GroupCW GroupCW Group

GLOBAL CEMENT INDUSTRY. KNOWLEDGE. DECEMBER 2012

2012BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

CemWeek’s middle east & afriCa Cement seCtor sentiment survey

KHD PROVIDES FULL RANGE OF

PLANT SERVICES:

• Spare parts

• Plant audits

• Training

• Operations and maintenance

Get more out of your cement plantthrough our full range of plant services.

Professional maintenance of process machinery and equipment is very critical

and helps maintain trouble-free production. At KHD, we not only provide

innovative, cost-efficient and environmentally friendly technologies, we offer

solutions to our customers that help increase their cement plants’ efficiency,

reduce operational downtime, ensure quality and thus, save money!

Our experience of over 150 years in creating innovative technologies allows

us to better understand the needs and requirements of our customers. We

carry out a complete spectrum of plant inspections, reconditioning, annual

maintenance contracts for particular machines, kiln alignment (hot/cold), and

plant and equipment upgrades. Such a wide range of services along with our

onsite audit and expert review ensure that our customers get more out of

their cement plants.

To get more out of your cement plant, visit www.khd.com

FOREWORD

emWeek’s third annual “2012 Middle East and Africa Cement Business Sentiment Survey” provides a snapshot of emerging and developing trends that have dominated the African and Middle Eastern cement sectors in recent months, along with those themes likely to be important in the short-term. Using quantitative data and

qualitative observations, the survey highlights the sentiments and experiences of individuals working within the African and Middle Eastern cement sectors.

The survey reveals changing business strategies, operations, sales and marketing activities and other attitudes that are influencing the cement sector, from cost to capacity concerns and employment projections. Data was obtained from survey respondents hailing from key industry contributors, including major corporations such as Lafarge, Holcim, Dangote and Asec to name just a few.

This document is meant as a summary of the themes reported by respondents, and the full data of tabulated responses provides insights that are more detailed. The CW Group is happy to assist you with a custom deep-dive review to help your organization uncover and understand trends and market dynamics in your country or region to help improve your competitive positioning.

To further understand the micro-trends and obtain more detail on the answers uncovered in this survey, please contact us at [email protected].

diana Heeb bivonaCW Publication [email protected]

KHD PROVIDES FULL RANGE OF

PLANT SERVICES:

• Spare parts

• Plant audits

• Training

• Operations and maintenance

Get more out of your cement plantthrough our full range of plant services.

Professional maintenance of process machinery and equipment is very critical

and helps maintain trouble-free production. At KHD, we not only provide

innovative, cost-efficient and environmentally friendly technologies, we offer

solutions to our customers that help increase their cement plants’ efficiency,

reduce operational downtime, ensure quality and thus, save money!

Our experience of over 150 years in creating innovative technologies allows

us to better understand the needs and requirements of our customers. We

carry out a complete spectrum of plant inspections, reconditioning, annual

maintenance contracts for particular machines, kiln alignment (hot/cold), and

plant and equipment upgrades. Such a wide range of services along with our

onsite audit and expert review ensure that our customers get more out of

their cement plants.

To get more out of your cement plant, visit www.khd.com cemweek 2012 middle east & africa cement sector surveycemweek.com 1BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

This year’s survey respondents hailed from North Africa, Sub-Saharan Africa (SSA), the GCC States, other Middle East countries and Turkey.

The survey analyzed a series of principal sentiments and trends across the region. General findings in this survey include:

■ Sixty percent of respondents indicated the cement industry had met their expectations, performing “ok” over the past six months.

■ Roughly 90 percent expressed optimism that the industry would perform “about the same,” “somewhat better” or “much better” over the next 12 months.

■ Emphasis on controlling costs, improving domestic sales, finding new export opportunities and reconstruction ranked as the most important themes in the months ahead for respondents.

■ In terms of employment projects, respondents did not express any concern that their careers were “at risk.” In fact, 60 percent were either fairly or highly confident that their careers would receive a boost in the next 12 months.

■ Fifty-five percent indicated their company’s workforce numbers would remain the same. Another 44 percent indicated they would be hiring a “bit more” to “a lot more” in the near future.

■ Regarding capital expenditure, 66 percent anticipated budgets would remain the same, with 11 percent suggesting an increase.

■ Seventy-seven percent of respondents considered compliance with U.S. or European environmental regulation to be “important.”

SURVEY INTRODUCTION

2012 Middle east and africa ceMent Business sentiMent survey

cemweek 2012 middle east & africa cement sector survey cemweek.com2BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

OF A REGIONSNAPSHOT

SNAPSHOT OF A REGION

AFRICAThe changes in the landscape of the African cement market in just a short period are astounding. It was not too long ago that Africa was often referenced as the world’s last cement frontier, running a significant supply deficit. Strong economic growth throughout the region and an intense focus by regional and global producers, however, have helped to narrow that once substantial deficit throughout much of the continent.

The political and economic backgrounds of each region, while sharing many similarities (strong infrastructure spending, solid economic growth, logistical challenges, etc.), do have their own unique challenges as well.

NORTH AFRICAThe political protests and revolution witnessed by Libya, Egypt and Tunisia have left an indelible mark on the development of these nations. Instability and ongoing uncertainty have hampered short- and mid-term construction projects to varying extents. Like most industries, cement has scrambled to adapt to changing demand levels and input costs due to unreliability and/or shortages.

CW Group analysts estimate that the North African cement market capacity for 2012 is roughly 122 mtpa, with demand sitting around 102 mtpa. With actual production trending at 98 mtpa, imported cement is still a necessity. As Libya and Tunisia strengthen their recovery, growth rates of 15 percent and 9.5 percent, respectively, are expected for 2013, but the continued political and social unrest plaguing Egypt places a gray cloud over the industry.

WEST AFRICAWhen speaking about cement growth in West Africa, there is one country leading the pack. Nigeria has been at the forefront of rapid expansion and growth, witnessing a breakneck pace in the increase of production capacity. Local maximum output for the Nigerian cement industry jumped from around 15 mtpa in 2011 to more than 22 mtpa in 2011, with the prospect of exceeding 31 mtpa by the end of 2014. Such an increase assists in explaining why Nigeria’s cement industry accounts for close to 64 percent of the region’s cement output, and the motivation behind investors pouring in even more money to further boost production capacities.

That investment may be on target and justified if the government moves forward with plans to upgrade and build new public infrastructure and to address the current housing deficit. The massive capacity increase in Nigerian cement has transformed in a matter of a few years one of the region's major importers into a fierce exporting force. However, in a sign that capacity is outstripping demand, units recently for the first time in a long time started idling and complaining cheaper imports.

Dangote Cement is the uncontested leader in the region with regard to spearheading capacity expansion growth. Over the last six years, the company has invested well over US$6.5 billion in ramping up production capacity and building market share. Through its aggressive expansion strategy, it has not only established a presence in 14 other African countries, but has become the

Dangote is the uncontested leader in the region with regard to spearheading capacity expansion growth.

cemweek 2012 middle east & africa cement sector surveycemweek.com 3BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

dominant force in many of them. The company already controls around 61 percent of the 2012 estimated Nigerian nameplate cement capacity. Therefore, suggestions that Dangote may well reach a production capacity of 50 mtpa by 2020 are plausible.

EAST AFRICA The cement industry in East Africa is expected to attract Sh320 billion in investments over the next two years, with regional cement consumption projected to hit 17 mtpa by 2014. Increases in infrastructure spending and the housing sector are expected to serve as the catalyst for the growth. Currently, the eastern region produces an estimated 11 mtpa, while consuming only eight mtpa — a gap that is expected to widen in the near term. Kenya is the largest market for cement, producing 53 percent of the region’s total capacity. Tanzania contributes 30 percent and Uganda another 15 percent.

Consumption of cement in the region has grown at a swift clip in the last decade, averaging 13.5 percent. Industry watchers project this rate to moderate somewhat to 7.8 percent, hitting 14.4 mtpa by 2017. Cement production capacity is expected to keep pace, hitting 17 mtpa.

High fuel prices, logistical challenges (treacherous roads and poor railway facilities) and rising costs of electricity and raw materials are in special focus for many of the industry players in this region.

SOuTHERN AFRICAThe Southern African cement region is dominated by South Africa, which has experienced a slumping sales and volume streak for the past few years. While the run-up to the World Cup games did much for the industry, that ship has sailed. Stalled government infrastructure projects and uncertainty now dominate the economic landscape of this country. The picture is markedly different for the rest of the region. Recovery in Zambia’s mining sector, economic stabilization in Zimbabwe and strong infrastructure demand in Botswana and Mozambique have fueled the cement sectors in these countries.

0

125

2009 2010 2011 2012 2013 2014

250

AFRICA MIDDLE EAST

CONSUMPTION IN MM TONS

SNAPSHOT OF A REGION

Consumption of cement in [East Africa]

has grown at a swift clip

in the last decade...

cemweek 2012 middle east & africa cement sector survey cemweek.com4BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

RQ 21517 ©2012 by SAP AG. All rights reserved. SAP and the SAP logo are registered trademarks of SAP AG in Germany and other countries. Business Objects and the Business Objects logo are trademarks or registered trademarks of Business Objects Software Ltd. Business Objects is an SAP company. Sybase and the Sybase logo are registered trademarks of Sybase Inc. Sybase is an SAP company. Crossgate is a registered trademark of Crossgate AG in Germany and other countries. Crossgate is an SAP company.

Mobile Technology Discover an Array of Unprecedented Opportunities

Mobility is a must-have strategy in the cement and building materials industry. Some employees are already mobile, like those in sales and transportation, while others are mobilizing rapidly, especially in manufacturing and asset management.

And executives are demanding instant insight into operations, anytime, anywhere. The technology exists – from really smart smartphones to Wi-Fi access – to support true mobility in building materials organizations. But how can you make sure that mobile technology brings the greatest value to your company?

Better customer service and expedited sales cycles can be achieved through instant access to customer, product, and pricing information or any other type of critical business data when and where needed. Moreover, safety and efficiency on the plant floor can be enhanced by delivering instant, paperless information about assets, operations, and risks, ultimately supporting continuity and performance in manu-facturing operations. Mobility promotes fast decision making by providing up-to-date financial and operational key perfor-mance indicators (KPIs) and data visualizations, as well as interactive drill-down functionality to support real-time data access.

Mobility is no longer a “nice to have” feature. It’s now con-sidered a strategic necessity that can boost productivity and drive competitive advantage. Read MoRe on how to maximize the value of mobile technology in your company.

Lead your company into the mobile future

Please visit: www.sap.com/industries/mill-products

MIDDLE EAST CEMENT SECTOROngoing government spending in several key Gulf countries is forecasted to fuel the growth in the region’s cement sector. Talk of another Saudi Arabian construction boom grows louder as an aggressive public spending campaign fuels the demand for cement both locally and regionally in one of the world’s largest economies. In 2012 alone, it is estimated that ongoing construction projects in Saudi Arabia’s pipeline are valued at more than US$159 billion. Construction spending is also on the rise again in the UAE, and whispers of a market rebound are growing in both the UAE and Oman, where the country is beginning to reap the benefits from the diversification policies implemented under the Vision 2020 plan. Qatar is also investing heavily in its infrastructure development with well over US $150 billion worth of projects in some varying degree of completion.

Iran’s production capacity showed strong growth throughout 2012. Cement capacity, estimated at around 74 million tons, is projected to rise to 110 million tons by 2015 as the government continues to implement new cement projects. Meanwhile, several regional players, keen on establishing operations, are eyeing the Iraqi market. Increased capacity also will be needed in Iraq as the government plans to spend US$60 billion on improving and building roads, bridges and housing through 2016. Estimates suggest Iraq will need around 2.5 million new homes in the next five years to meet housing demand.

Turkey’s cement sector exhibited continued growth in 2012. Ranking fourth in the world with regard to cement production, its cement capacity exceeds 105 mtpa. Additionally, an ongoing trend for investment and expansion is expected, which will likely fuel a moderate increase in the country’s cement output. Infrastructure development has assisted in fueling domestic demand, and the quest for a greater share of the global export market remains a priority.

SNAPSHOT OF A REGION

Iran’s production

capacity showed

strong growth throughout

2012.

cemweek 2012 middle east & africa cement sector survey cemweek.com6BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

the best talent an engineer can have is the will to learn something new every day

There’s always something new to learn in India. For further information please call +91 120 4018500, write an E-mail to [email protected] or visit www.loesche.com

AZ_Letter_2011_india_RZ.indd 1 24.06.2011 12:18:17 Uhr

Equipment vendor

Cement trader

Industry analyst, consultant

Cement

TYPE OF COMPANY

9%

9%

36%

45%

Other

Professional Staff

Management

Senior Management

LEVEL

1%

18%

36%

45%

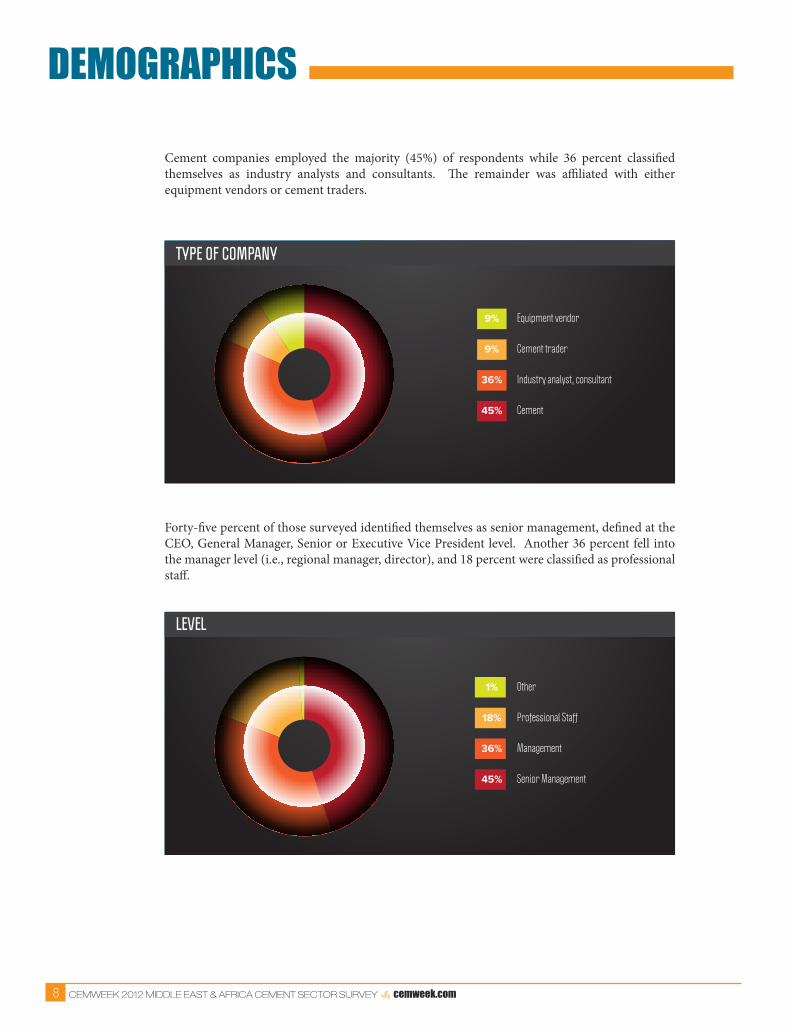

DEMOGRAPHICS

Cement companies employed the majority (45%) of respondents while 36 percent classified themselves as industry analysts and consultants. The remainder was affiliated with either equipment vendors or cement traders.

Forty-five percent of those surveyed identified themselves as senior management, defined at the CEO, General Manager, Senior or Executive Vice President level. Another 36 percent fell into the manager level (i.e., regional manager, director), and 18 percent were classified as professional staff.

cemweek 2012 middle east & africa cement sector survey cemweek.com8BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

Register for attendance directly on www.gmiforum.com/cbi-africa-2013-registration, or contact [email protected]. You may also call us in the USA at +1-203-516-7424

cement business & industry

JOHANNESBURG ♦ MARCH 27-28, 2013

CONfERENCE:

Organized by GMI GlobAl llC and supported by CeMWeek www.gmiforum.com

Backed by:

GMI GLOBAL

For attendance, speaking opportunities or general questions about the conference please contact the CBI Client Service team at [email protected] or via phone at +1-203-516-7424.

The Cement Business & Industry (CBI) Africa Conference, which will be hosted in Joahannesburg, South Africa on March 27 and 28, 2013, will create a new platform connecting the cement industry, analysts, technologists and other stakeholders from Africa and all parts of the world.

Africa has been experiencing strong growth in the majority of its cement markets for the past 15 years. This has led to quite a dramatic evolution of the industry on the continent resulting in new entrants coming into the market as well as increasing interest from multinationals and great development opportunities for existing players.

The program will take a dual-track business and technical approach to issues around:

■ Opportunities and challenges in North and Sub-Saharan Africa

■ Investments, finance and expansion programs

■ Environmental performance and alternative fuels

■ Cement trading, logistics and handling

■ Cement fuels: coal, petcoke and energy improvements

■ Manufacturing optimization, new technologies & automation

BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

cbi

AFricA

Cimentas-Izmir Cimento, in Turkey, wanted to upgrade and expand its existing

line but faced severe space limitations. Collaboration with FLSmidth resulted

in innovative technical solutions, and effective site management held kiln stop-

page to less than the 83-day limit. Final result: a maximum 33% output upgrade

within minimum space. We’ve been helping cement plants implement innovative

upgrades since 1882 – we’d be happy to do the same for you.

For more information about how FLSmidth can help make your

plant more competitive, visit www.fl smidth.com/upgrades

maximum outputmaximum outputmaximum outputmaximum outputmaximum output

Teamwork transforms minimum space for

SCAN HERE SCAN TO READ MORE ABOUT HOW UPGRADES CAN BOOST PLANT CAPACITY

Teaming up with FLSmidth turned into a valuable, long-lasting cooperation for CIMENTAS GROUP ERGUN OLGUNTechnical Affairs CoordinatorCimentas Group

FUNCTIONAL AREA

Other

Consulting & Research

Trading & Logistics

Production, Operations & Engineering

Sales & Marketing27%

9%

9%

36%

18%

LOCATION

Turkey

Other Middle East

GCC states

Sub-Saharan Africa

North Africa

9%

36%

9%

36%

9%

Those completing the survey, and who identified an affiliation, represented a wide mix of companies in the cement industry or serving it. Representatives from Lafarge, Holcim, Dangote, ASEC, Vicat and many others took part in the survey.

With regard to regional representation, 54 percent of respondents were from Middle Eastern countries, while 45 percent hailed from Africa. Roughly 36 percent of Middle Eastern respondents were from non-GCC states, and in Africa, 36 percent of those surveyed were located in Sub-Sahara Africa.

Participants represented a wide range of functions within the industry from consulting to production. More than 63 percent worked in consulting and research (36%) and in sales and marketing (27%).

Cimentas-Izmir Cimento, in Turkey, wanted to upgrade and expand its existing

line but faced severe space limitations. Collaboration with FLSmidth resulted

in innovative technical solutions, and effective site management held kiln stop-

page to less than the 83-day limit. Final result: a maximum 33% output upgrade

within minimum space. We’ve been helping cement plants implement innovative

upgrades since 1882 – we’d be happy to do the same for you.

For more information about how FLSmidth can help make your

plant more competitive, visit www.fl smidth.com/upgrades

maximum outputmaximum outputmaximum outputmaximum outputmaximum output

Teamwork transforms minimum space for

SCAN HERE SCAN TO READ MORE ABOUT HOW UPGRADES CAN BOOST PLANT CAPACITY

Teaming up with FLSmidth turned into a valuable, long-lasting cooperation for CIMENTAS GROUP ERGUN OLGUNTechnical Affairs CoordinatorCimentas Group

cemweek 2012 middle east & africa cement sector surveycemweek.com 11BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

HOW HAS THE CEMENT INDUSTRY PERFORMED IN THE PAST 6 MONTHS?

Poorly

Ok

Well

10%

60%

30%

LOOKING BACK AT THE PAST 6 MONTHS, HOW DID IT MEET YOUR EXPECTATIONS?

Below

Met

Exceeded10%

60%

30%

REFLECTIONRespondents were asked to reflect on the prior six-month period, to rank the performance of the cement industry as a whole and to answer whether it had met their expectations. Around 60 percent felt the cement industry had performed “ok.” The same percentage of respondents also indicated that it had met their expectations. On the other end of the spectrum, ten percent felt the industry had performed poorly, with 30 percent suggesting performance was “below expectations.”

cemweek 2012 middle east & africa cement sector survey cemweek.com12BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

LOOKING FORWARDCautious optimism appeared to be the theme when respondents were asked how performance would measure up over the next 12 months. Fifty percent of respondents answered “about the same.” Last year, about 60 percent of survey respondents had expected performance would be “much better” or “somewhat better.” This year, the percentage of those responding similarly was down to 40 percent.

HOW WILL THE NEXT 12 MONTHS PERFORM COMPARED TO THE LAST 6 MONTHS?

Somewhat worse

About the same

Somewhat better

Much better10%

30%

50%

10%

ARE YOU CONFIDENT YOUR CAREER WILL SEE A BOOST IN THE NEXT 12 MONTHS?

Probably the same

Fairly confident

Highly confident

40%

50%

10%

However, respondents appeared to be more confident in their careers in the coming 12 months. While 40 percent felt their careers would remain the same, around 60 percent expressed that they were either “fairly confident” or “high confident” that their careers would receive a boost in the months ahead.

cemweek 2012 middle east & africa cement sector surveycemweek.com 13BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

HOW WILL YOUR COMPANY BUDGET CHANGE?

Decrease

Stay the same

Increase11%

66%

22%

PRIORITIES

When asked what the most important themes would be for companies over the next 12 months, controlling costs remained the top priority. Around 55 percent ranked it as their top priority, up 26 percent from the previous year. This year, improving domestic sales (22%) ranked second among respondents, up from fourth place last year. Finding new export opportunities and reconstruction tied for third with 11 percent of the votes each in this year’s survey. The focus on operational improvement, which ranked third in terms of priorities in last year’s survey, did not rank as a top theme among respondents now.

Respondents were asked what they perceived to be the biggest challenge facing the cement sector over the next few years. Profitability moved to the number one position this year along with energy prices. Last year, 27 percent ranked energy costs as the most challenging for the industry, and only nine percent of respondents ranked profitability as the biggest challenge. This year, profitability and energy prices tied as the biggest challenge, with each receiving 33 percent of the vote. Excess capacity, which had held the number one position last year, slipped to third place.

While environmental issues were not ranked among the most important company themes by respondents, 55 percent did hold the belief that their country’s cement industry should sacrifice profitability to improve emissions and reduce CO2 emissions over the new few years. Additionally, 77 percent supported the premise that their cement industry should strive to be on par with U.S. and European emission standards.

With regard to company capital budgets, the majority (66%) of respondents expected budgets to remain the same. Last year, 43 percent of participants anticipated budget growth while only 11 percent did this year.

cemweek 2012 middle east & africa cement sector survey cemweek.com14BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

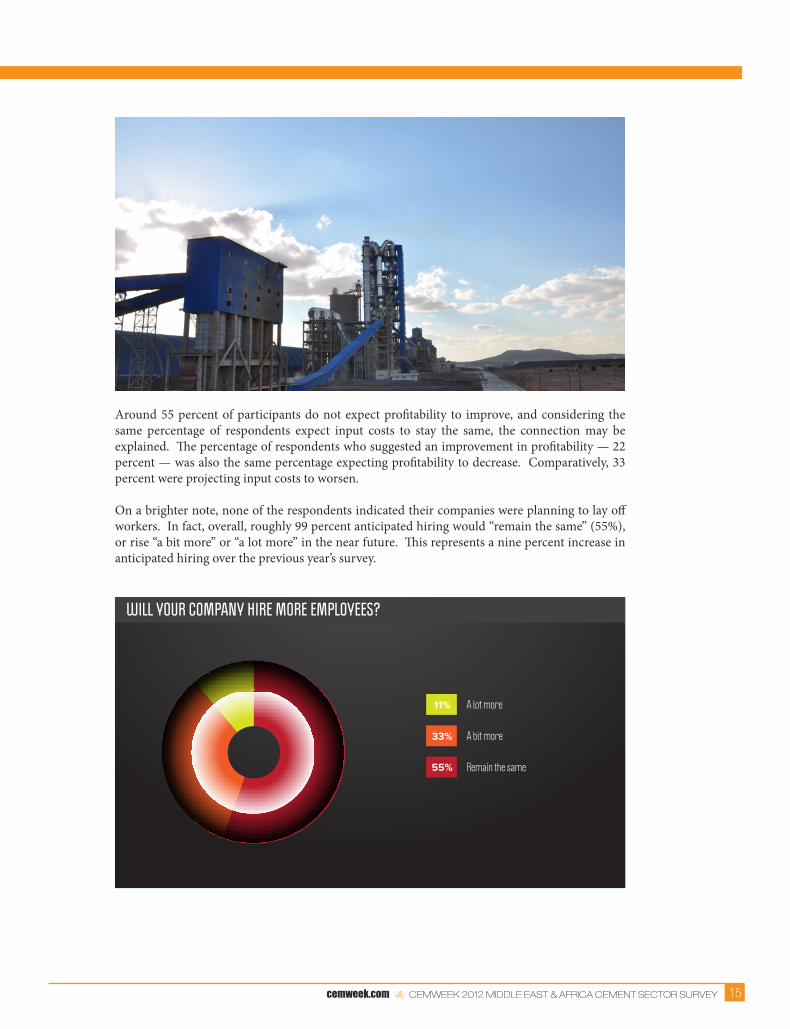

WILL YOUR COMPANY HIRE MORE EMPLOYEES?

A lot more

A bit more

Remain the same55%

33%

11%

Around 55 percent of participants do not expect profitability to improve, and considering the same percentage of respondents expect input costs to stay the same, the connection may be explained. The percentage of respondents who suggested an improvement in profitability — 22 percent — was also the same percentage expecting profitability to decrease. Comparatively, 33 percent were projecting input costs to worsen.

On a brighter note, none of the respondents indicated their companies were planning to lay off workers. In fact, overall, roughly 99 percent anticipated hiring would “remain the same” (55%), or rise “a bit more” or “a lot more” in the near future. This represents a nine percent increase in anticipated hiring over the previous year’s survey.

cemweek 2012 middle east & africa cement sector surveycemweek.com 15BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

EQUIPMENT SUPPLIERS

Respondents were asked to share their opinions of the various equipment manufacturers serving the cement industry. FLSmidth, KHD Wedag, IKN and Magotteau shared the top “best” rating. However, when combining those “best” and “good” results, FLSmidth leads with 24 percent of the votes.

cemweek 2012 middle east & africa cement sector survey cemweek.com16BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

CONCLUSIONS

Optimism appears to be the underlying sentiment expressed by this year’s respondents — optimism that may not be unfounded given the strong growth in infrastructure spending and consistent economic growth seen throughout most of this region. While unrest has once again reared its head in Egypt, and Syria struggles with ongoing civil war, much of the region continues to enjoy heightened public infrastructure spending and solid economic growth. These are facts that will strengthen the demand for cement.

Controlling costs, improving domestic sales and exploring new export opportunities will remain the focus for many in the industry, and concerns regarding profitability, energy prices and excess capacity will likely continue as key agenda items in boardrooms across the region. While these are not new conversations for most, the idea that performance may finally be on a road to recovery, allows for greater optimism.

cemweek 2012 middle east & africa cement sector surveycemweek.com 17BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal Week

cwgrp.com18

CW Group Research provides high-quality and data-centric custom and published market research. Our research and report services help companies conduct and leverage research to provide clear direction for business decision-making.

ӹ Market and country research ӹ Forecast services ӹ Due diligence research ӹ Competitive benchmarking ӹ Opportunity assessments ӹ Customized surveys ӹ Business intelligence

Contact us at [email protected] to discuss further how we can support your market intelligence needs.

www.cwgrp.com/research

Market analysisCompetitive benchmarking

Business intelligenceLet us guide you

T: +1-702-430-1748 F: +1-928-832-4762

848 N. Rainbow Blvd. Box #1658 Las Vegas NV 89107 USA

BMWeekBMWeek

BMWeekCemWeekCemWeek

CemWeekCW Group Coal WeekCW Group Coal Week

CW Group Coal WeekRESEARCH