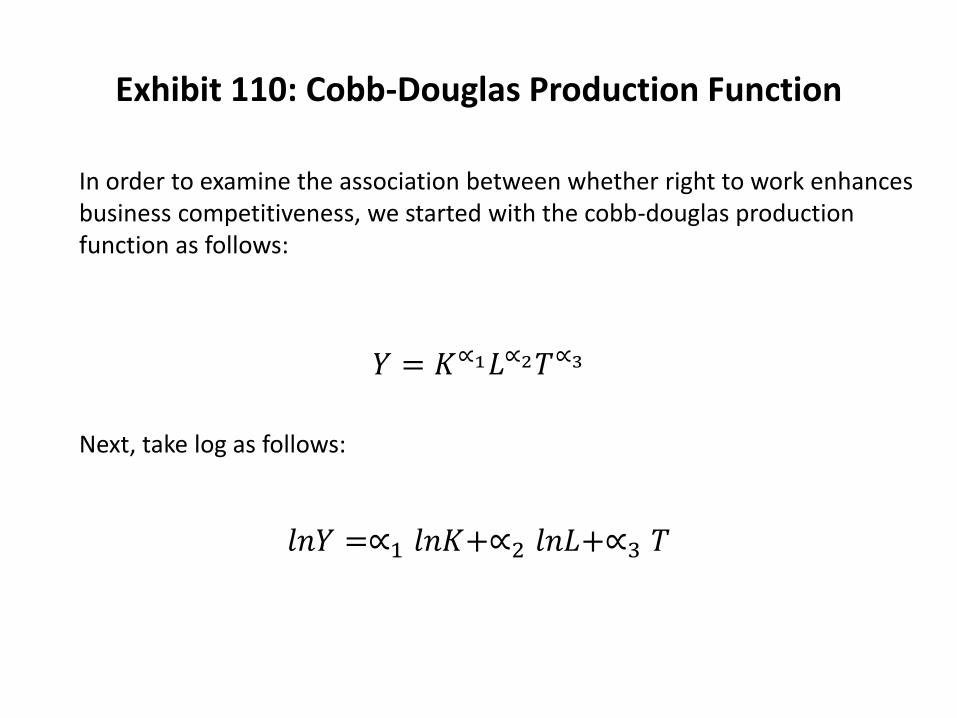

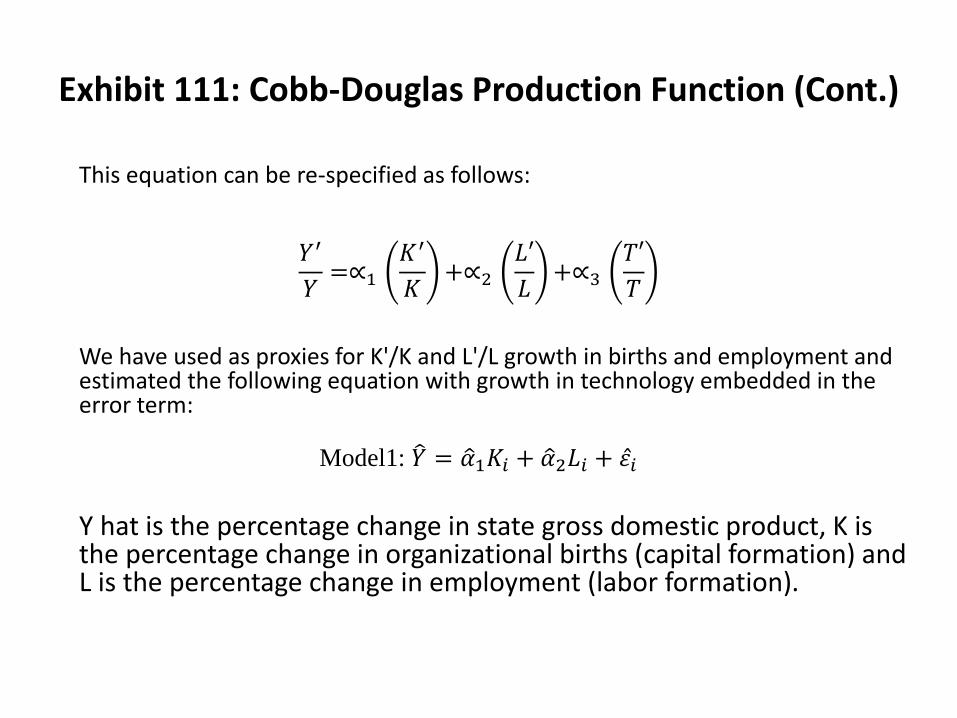

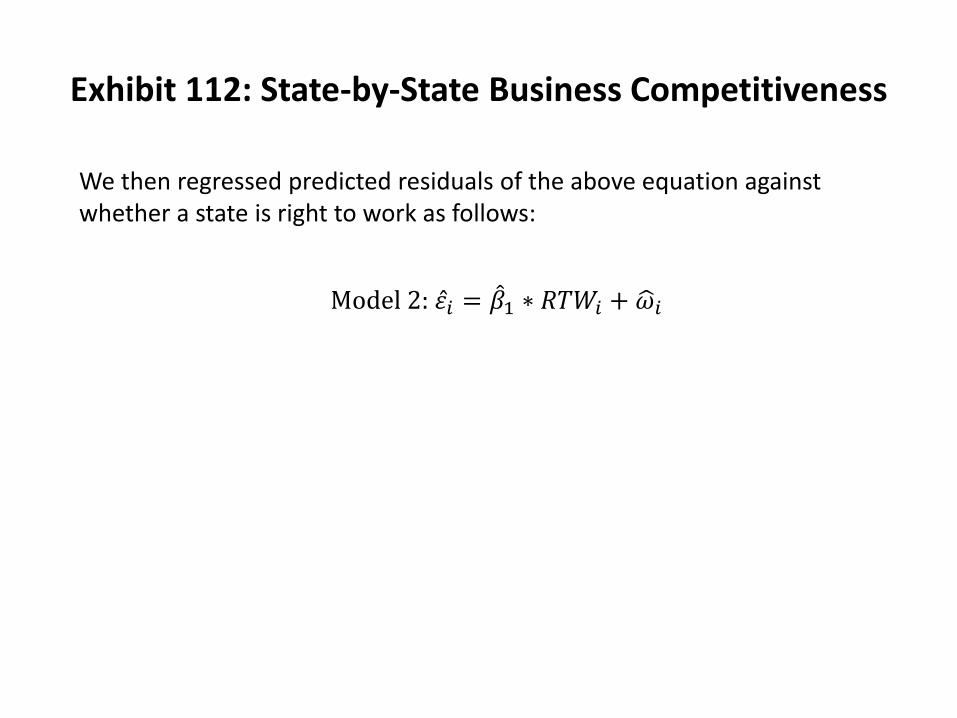

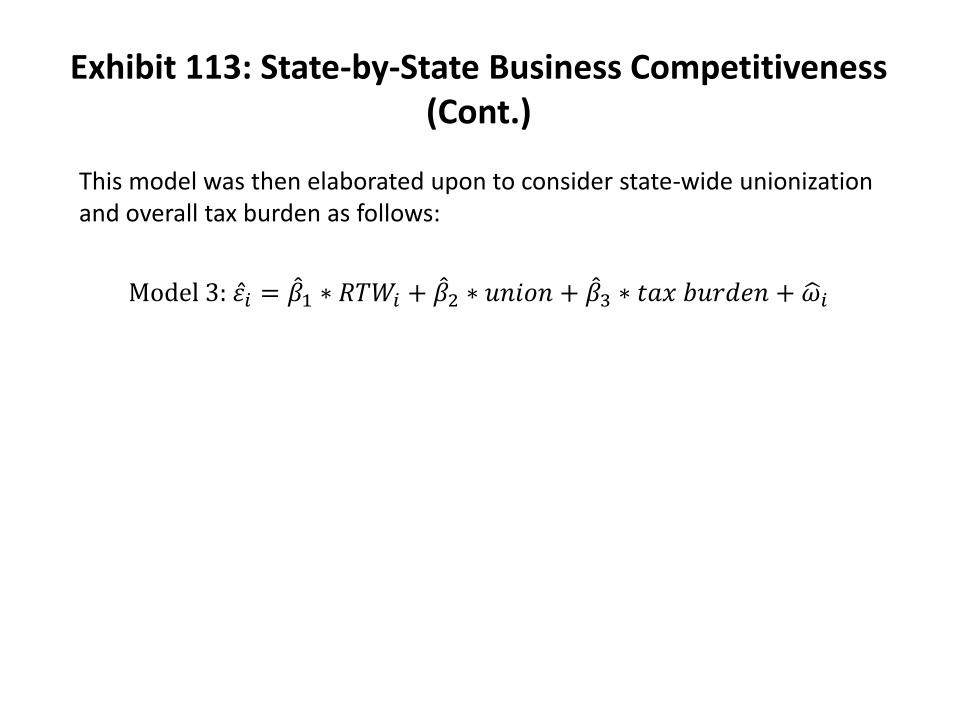

Embed Size (px)

Citation preview

2012 Michigan Economic

COMPETITIVENESS STUDY

An analysis of issues to advance Michigan in a complex global economy

2012 Michigan Economic Competitiveness Study:

An analysis of issues to advance Michigan in a complex

global economy

Executive Brief

2012 Michigan Economic Competitiveness Study Executive Brief

Page 2 of 12

About the Michigan Chamber Foundation

The Michigan Chamber Foundation was established as a non-profit supporting organization to the Michigan Chamber of Commerce in 1985 for the following purposes:

• To plan and conduct nonpartisan public education programs regarding free enterprise, productivity and basic economic issues affecting the state of Michigan;

• To establish and operate a leadership institute designed to provide promising future leaders assessment of Michigan’s assets, challenges and opportunities to give participants the background and network of contacts necessary to make a positive impact on Michigan’s future;

• To conduct nonpartisan research and distribute policy studies on issues facing Michigan including, but not limited to taxation, government regulation, government spending, health care and transportation.

Michigan Chamber Foundation Board of Directors

Chair: Kelly Rossman-McKinney, Truscott Rossman

Vice Chair: John Schreuder, First National Bank of Michigan

President: Rich Studley, Michigan Chamber of Commerce

At-Large: Gordon Kummer, Lloyd & Mabel Johnson Foundation

Steve Mitchell, Mitchell Research & Communications

Dan Ponder, Franco Public Relations Group

Jon Sorber, TWO MEN AND A TRUCK/INTERNATIONAL, Inc.

Bill Woodbury, Auto-Owners Insurance

Executive Director: Bob Thomas

2012 Michigan Economic Competitiveness Study Executive Brief

Page 3 of 12

Acknowledgements

The Michigan Chamber Foundation (MCF) would like to thank Northwood University for agreeing to conduct this study and assembling a first class team of researchers to bring it to fruition. In particular, the MCF like to thank Northwood University President and CEO Dr. Keith A. Pretty; Study Director, Dr. Timothy G. Nash, Vice President for Strategic and Corporate Alliances and the David E. Fry Endowed Chair in Free Market Economics for shepherding the project from inception to completion. The chamber would also like to thank the research team led by Dr. Nash, which is a diverse and talented group of economists and public policy thinkers from across Michigan and nationally. Dr. Debasish Chakraborty, Professor of Economics, Central Michigan University; Dr. Richard Ebeling, Professor of Economics, Northwood University; Dr. Adam Guerrero, Associate Professor of Economics, Northwood University; Dr. John Grether, Professor of Economics, Northwood University; Dr. Adam Okulicz-Kozaryn, Associate Professor of Public Policy, Rutgers University; Adam N. Matzke, Economics and Finance graduate, Northwood University; Adam Pretty, Law student, University of Notre Dame; and Charles Ruger, graduate student in Economics, University of Detroit-Mercy.

Finally, we would like to thank Joseph T. Nash, Rita G. Nash, Jeffrey G. Phillips, Susan Woodcock, John Young and Rochelle Zimmerman for their assistance with the chart construction, editing, typing and researching of this project.

2012 Michigan Economic Competitiveness Study Executive Brief

Page 4 of 12

Introduction

The purpose of the study was to conduct a comprehensive analysis of the Michigan economy

and evaluate its rank and performance across a number of metrics including, but not limited to,

Gross State Product (GSP) growth, tax policy, regulatory policy, and cost of doing business.

Accordingly, the focus was primarily on the Michigan economy and its outlook for the future. It

accomplishes that objective by focusing on different aspects of the Michigan economy and

compares it with all other states within the United States. The study briefly outlines the current

state of U.S. competitiveness in the global economy and then focuses on Michigan’s economic

performance relative to national averages and the other 49 U.S. states. It is important to note

that the Michigan economy moved in tandem with the U.S. economy in the sense that both

experienced a decline in competitiveness relative to its competitors. In order to find answers

for what contributed to this decline, the study’s authors conducted a comprehensive survey of

the literature regarding sources of economic growth to determine what was absent from or

hindering the Michigan economy. The authors focused on productivity in Michigan and the

factors that impact productivity. Specifically, the study focused on tax structures, the

regulatory framework governing businesses, education and other components reflected of the

general business environment. With a focus on productivity, this study also analyzed the issue

of Right To Work legislation both at a theoretical and an empirical level. The results are

interesting to say the least. Although the topic is controversial in some quarters, the results

deserve serious attention and discussion at all levels of the public policy decision making

process in Michigan.

To begin, there is fundamental agreement among economists as to the sources that drive

economic growth. There are definite reasons why some nations grow and others don't. Robert

Barro (1991) in his seminal paper, “Economic Growth in a Cross Section of Countries,” tried to

answer that question. He studied the key economic and political factors that determined 98

countries’ competitiveness that led to economic growth and standards of living. It is clear from

his study and others that economic growth is helped by investments in human capital, lower tax

2012 Michigan Economic Competitiveness Study Executive Brief

Page 5 of 12

rates, a lower regulatory burden on businesses and emphasis on the overall human

development matrix. It is also clear that the U.S. has been steadily falling behind in these

critical investment areas, or at least unable to keep up with the investments vis-à-vis its

competitors. Also, government is becoming increasingly more important in the overall scheme

of things as compared to the private sector. In addition, the federal government budget deficit

and national debt is growing alarmingly high and the financing of the deficit has been

instrumental in increasing the cost of capital, making it difficult for private businesses to invest

in critical areas. Many economists would argue that this unprecedented increase in government

spending has been the primary reason behind the relative decline in American competitiveness.

In the appendix of the study, numerous tables and charts are provided that highlight this

decline in U.S. competitiveness.

The 20th century clearly was the “American Century.” The 1900’s saw the United States

become the world’s largest, most productive and most competitive economy while also

becoming the world leader in invention and innovation. However, towards the end of the 20th

century, grave concerns began to be voiced as to whether or not the U.S. could maintain its

standing in the global economy. Income growth and job growth began to slow toward the end

of the 20th century and has continued to slow into the 21st century. While this was happening,

it is also true that government was becoming more and more significant in the U.S. economy.

According to the Congressional Budget Office and the Heritage Foundation, government at all

levels in the United States consumed less than eight percent of GDP by expenditures in 1902

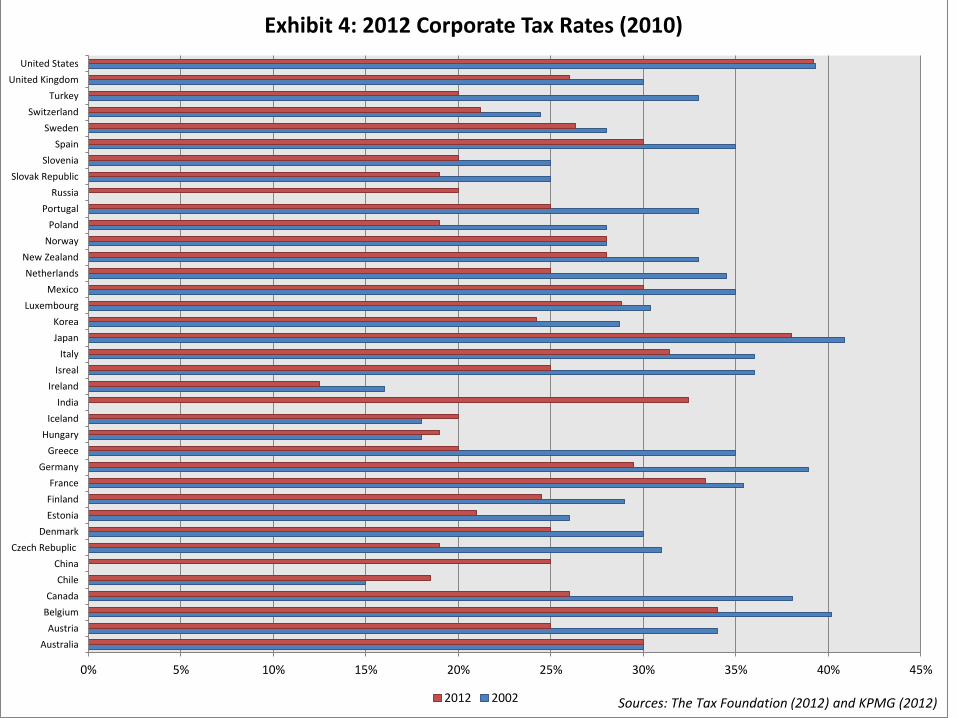

and today consumes more than 42 percent. The U.S. now has the highest corporate income tax

rate in the industrialized world at 39.2% (the industrialized world average is 24%) according to

the Tax Foundation, not because the U.S. has raised taxes, but rather because many of its

competitors have lowered their rates over the last decade. Based on 2010 data, the U.S. also

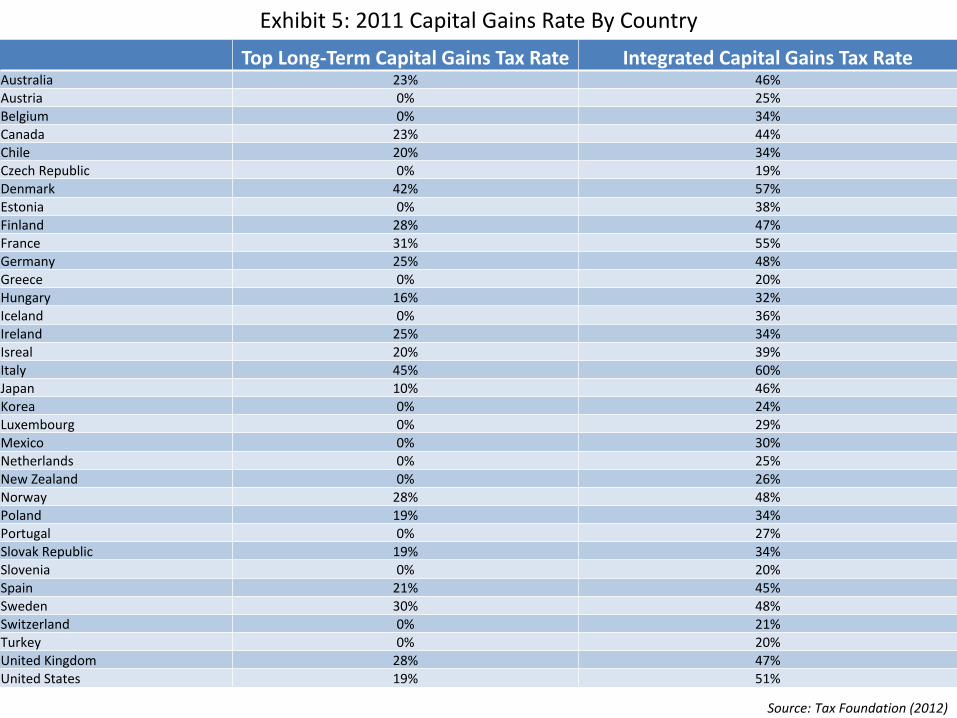

has among the highest long-term and integrated capital gains tax rates in the industrialized

world at 19% and 51.5% respectively. The U.S. tax system has become more and more

burdensome and has contributed to decline in U.S. competitiveness.

2012 Michigan Economic Competitiveness Study Executive Brief

Page 6 of 12

The 2012 Heritage Foundation/Wall Street Journal’s Index of Economic Freedom measures

political freedom, prosperity, and economic freedom across 10 metrics to gauge the economic

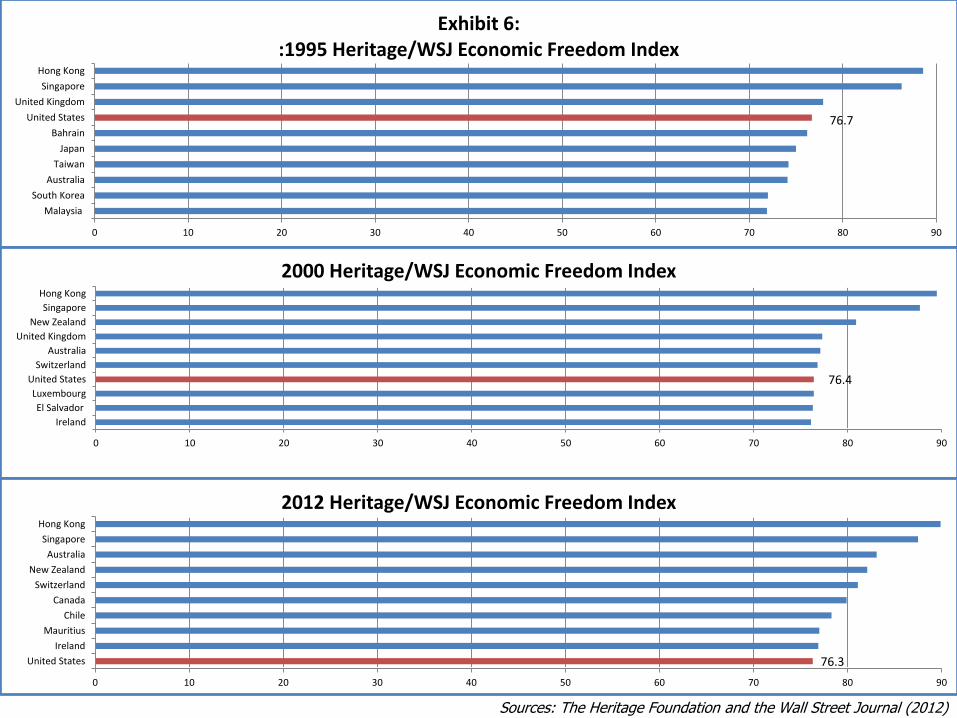

success of 184 countries around the world. In 1995, the U.S. was ranked fourth in the world on

the index and in 2012 the U.S. has dropped to tenth.

Over the last one hundred years, the United States as a country lost sight of what made it great.

The case is similar for Michigan. The U.S. economy’s pace for invention, innovation and new

business formation was staggering in the 1900’s, with Michigan at the epicenter of much of that

growth. Michigan-based companies like Amway, Chrysler, The Dow Chemical Company, The

Ford Motor Company, General Motors, Kellogg, Upjohn and Whirlpool were complemented and

supplemented by thousands of small and medium-sized entrepreneurial organizations making

Michigan a center for business excellence for much of the 20th century (U.S. Department of

Commerce Report, 2012). However, Michigan began to lose its competitive edge to lower-cost

U.S. states and foreign countries starting in the 1970’s and continuing into the twenty-first

century. Today, the Michigan economy is heavily dominated by the automobile industry and

has not attracted sufficient new businesses or developed home-grown entrepreneurs to ensure

strong economic growth and wide scale economic diversification.

The following are examples of the many factors used in this study to evaluate the

competitiveness of the Michigan economy relative to the U.S. as a whole, as well as Right To

Work (RTW) states and Non-Right-To-Work (NRTW) states:

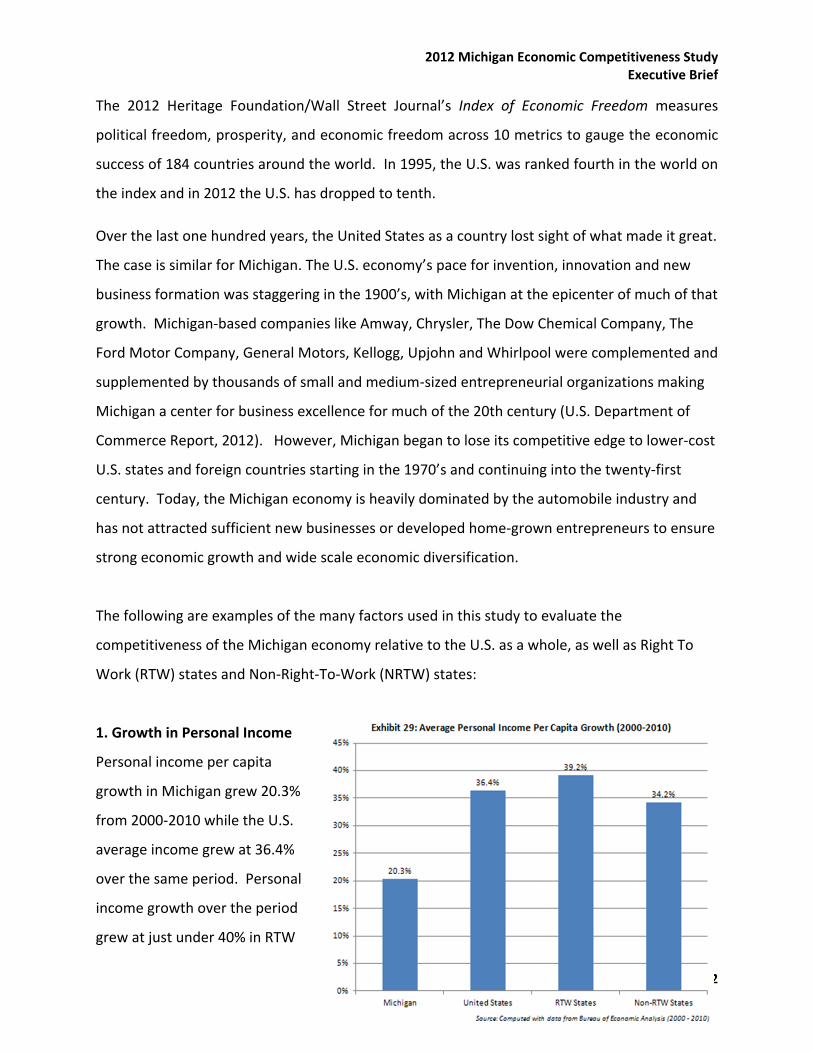

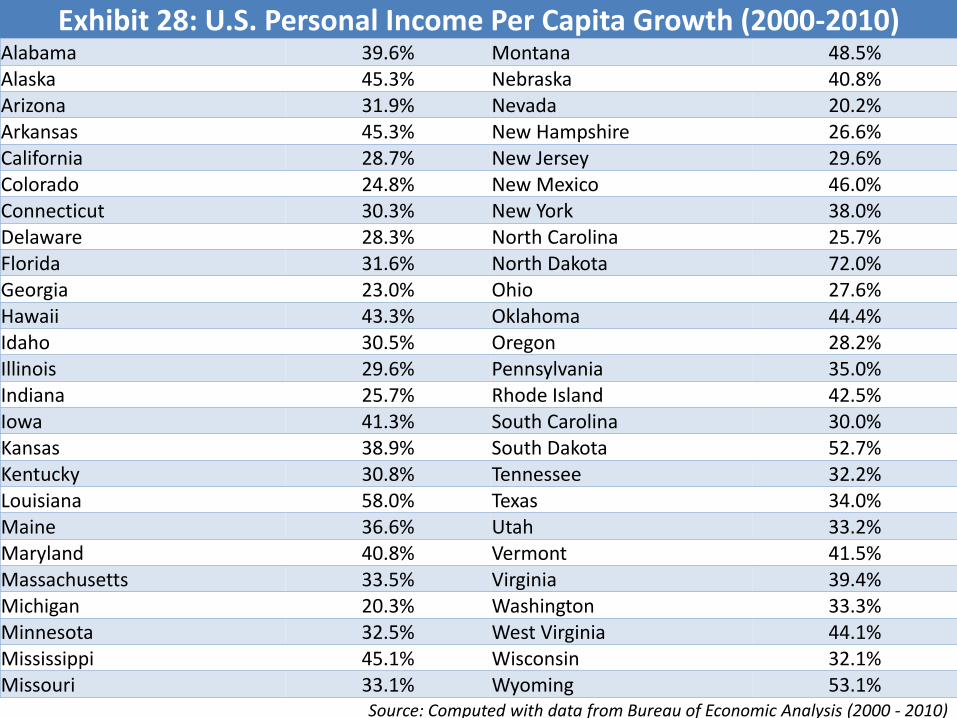

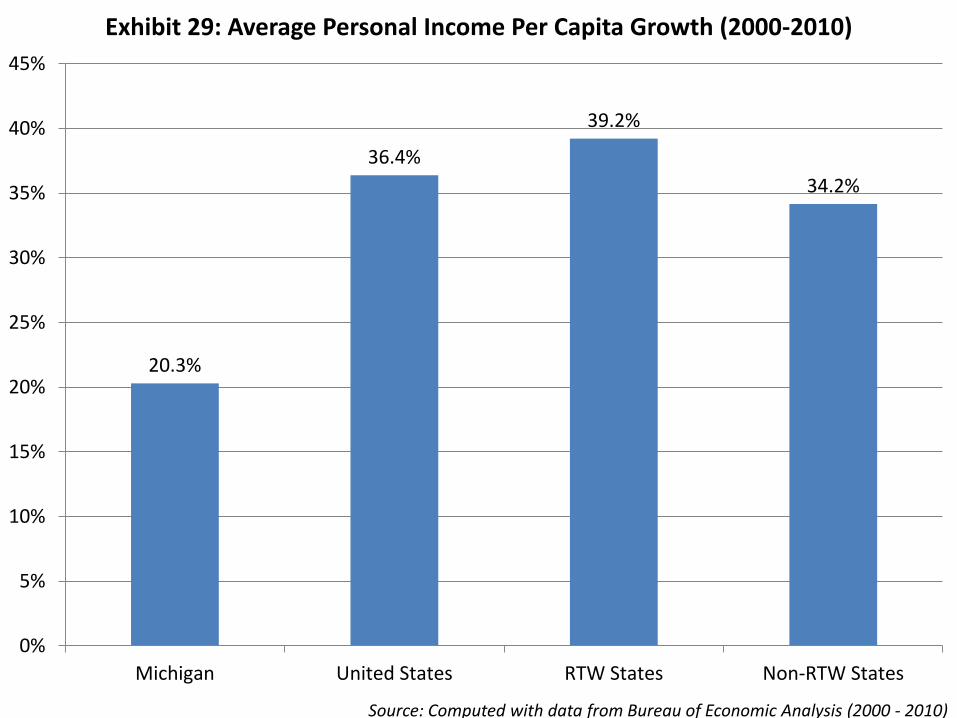

1. Growth in Personal Income

Personal income per capita

growth in Michigan grew 20.3%

from 2000-2010 while the U.S.

average income grew at 36.4%

over the same period. Personal

income growth over the period

grew at just under 40% in RTW

2012 Michigan Economic Competitiveness Study Executive Brief

Page 7 of 12

states and at 34.2% in NRTW states (see Exhibit 29).

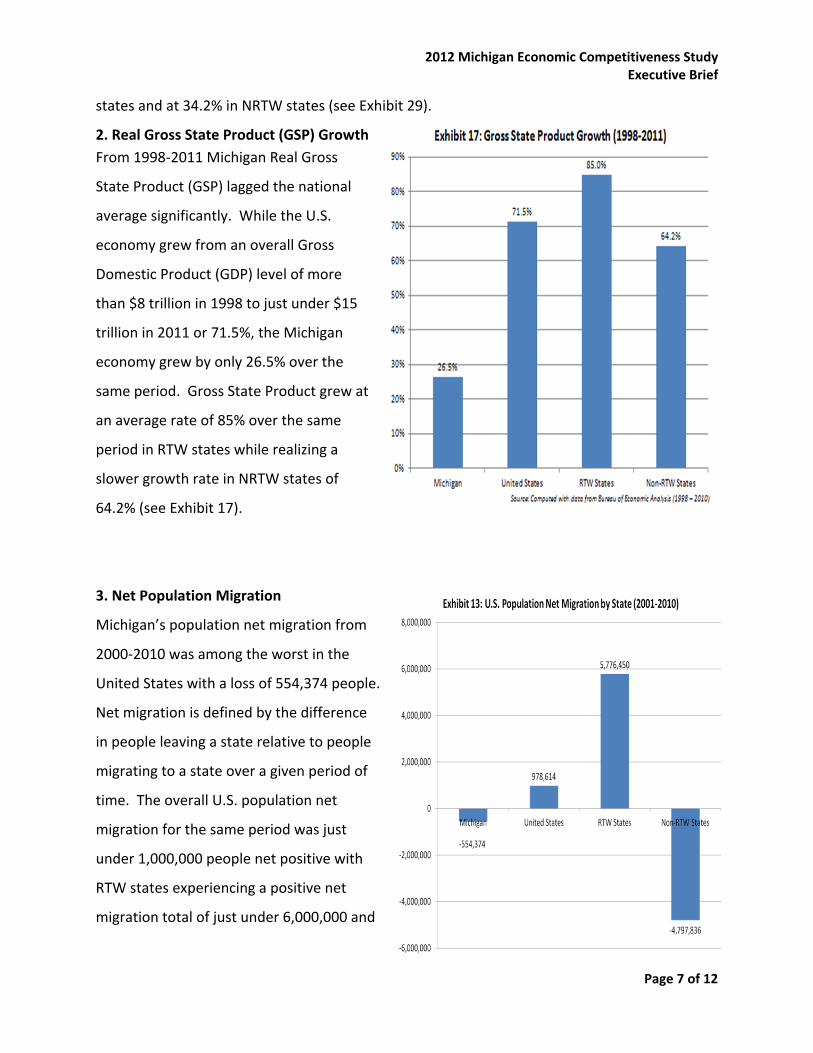

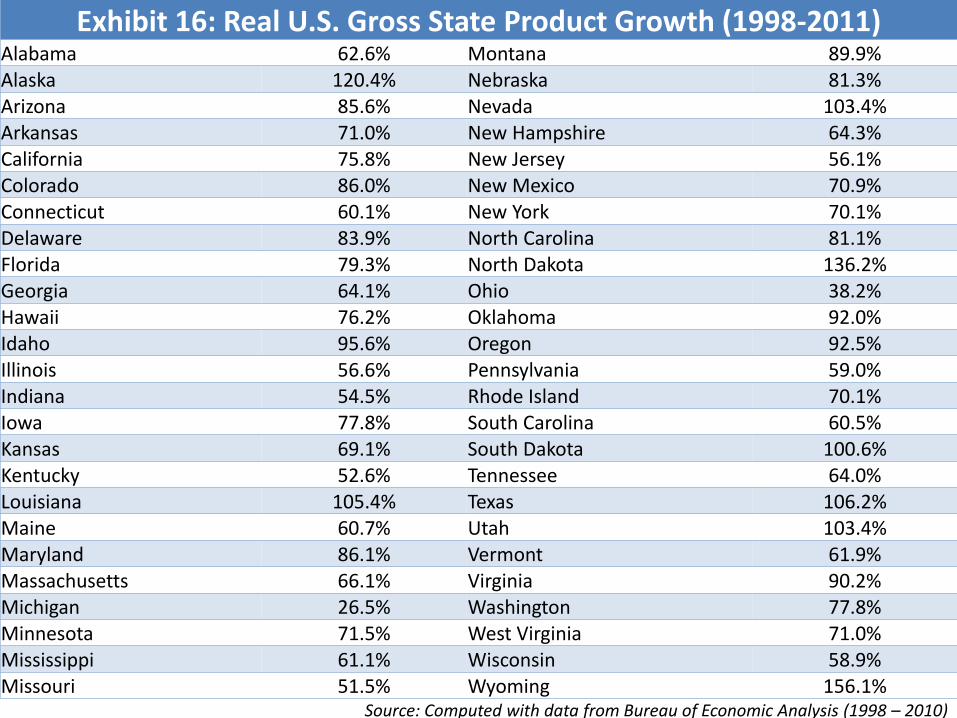

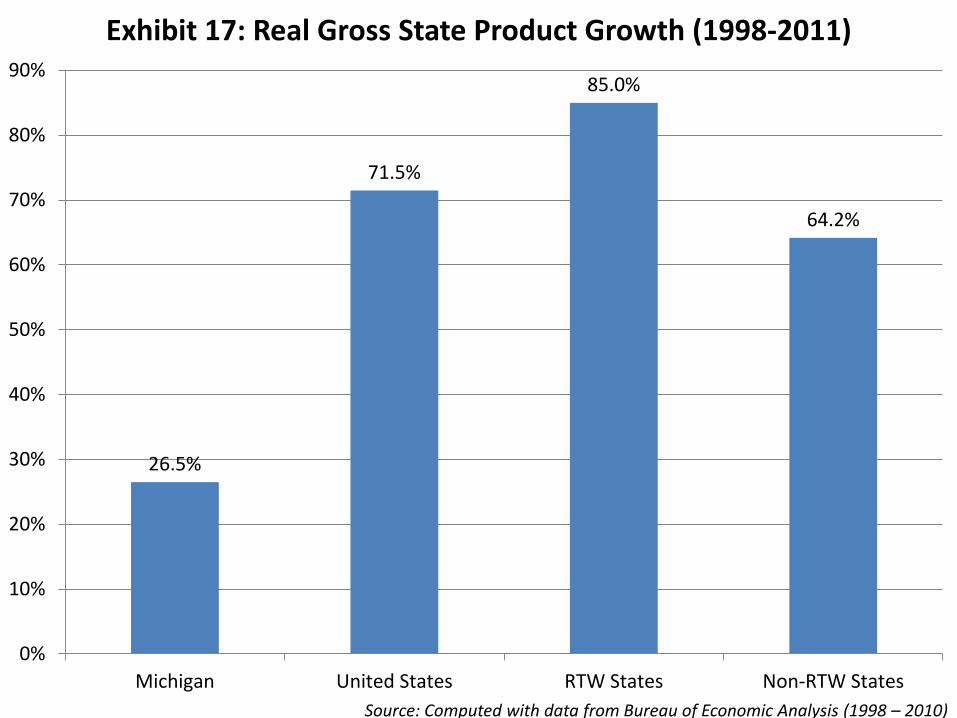

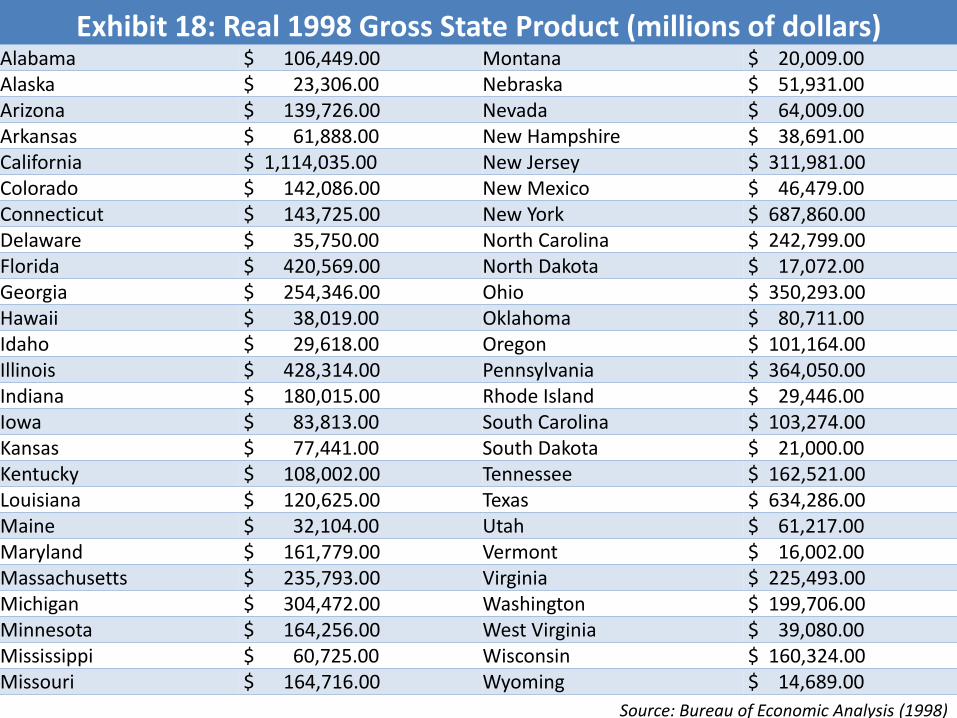

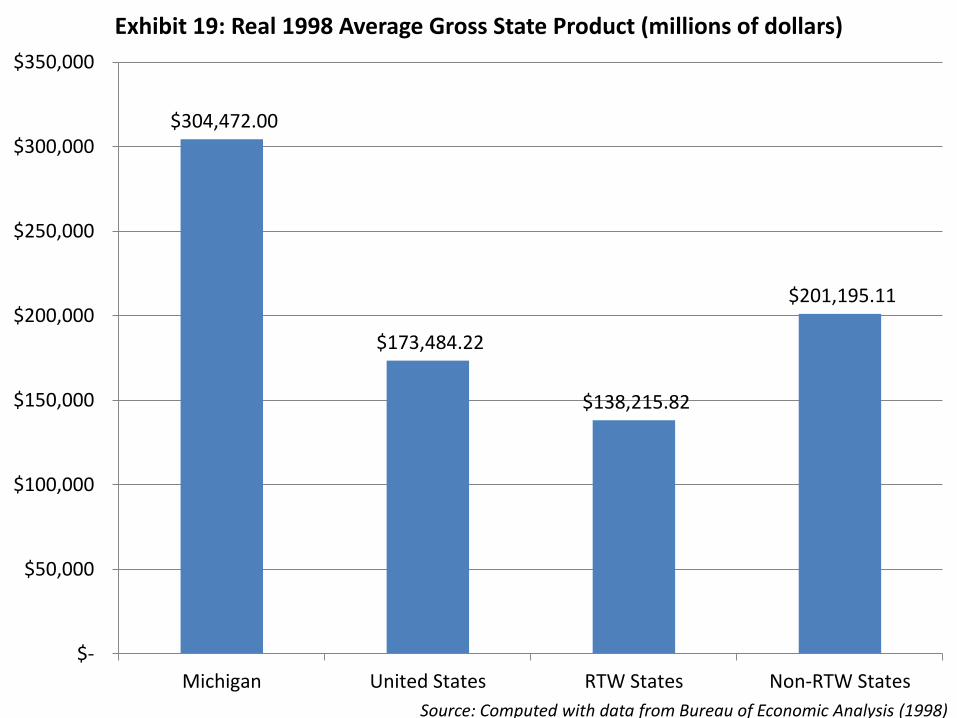

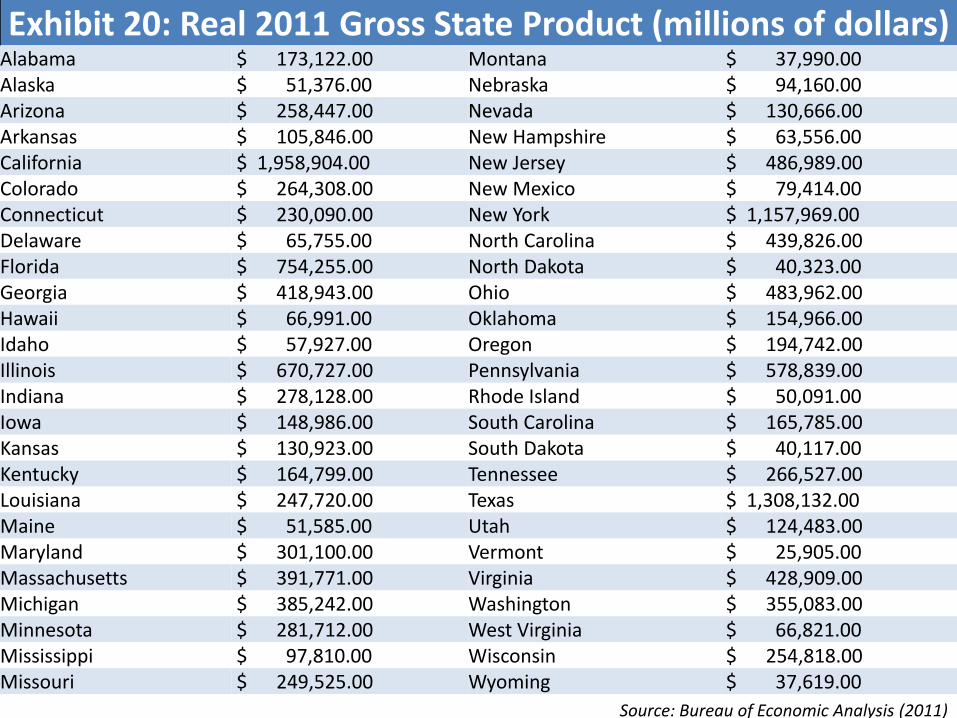

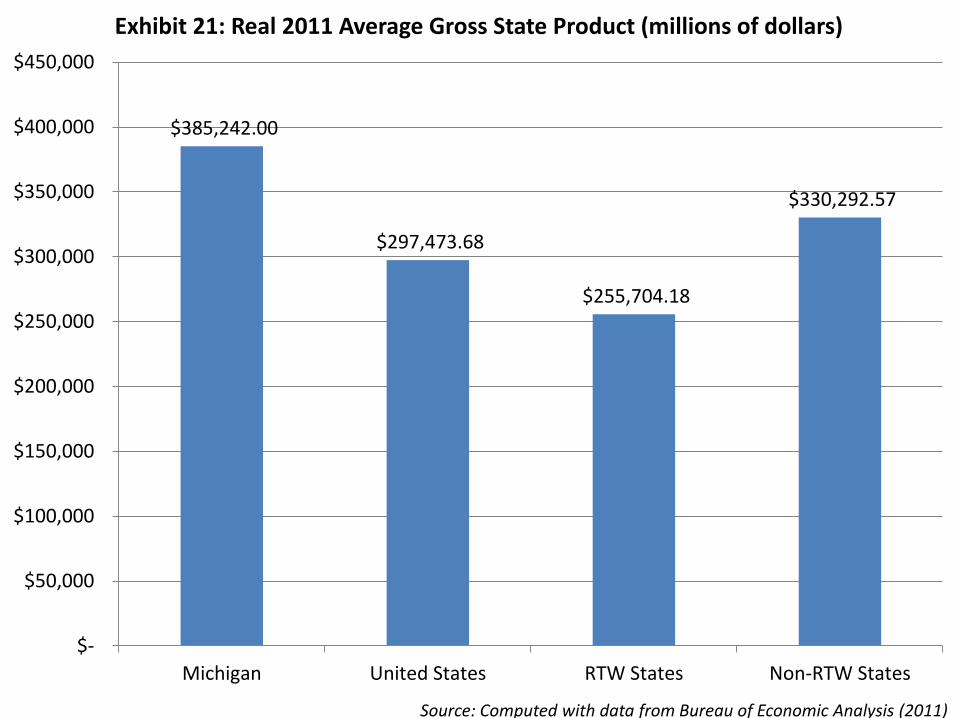

2. Real Gross State Product (GSP) Growth From 1998-2011 Michigan Real Gross

State Product (GSP) lagged the national

average significantly. While the U.S.

economy grew from an overall Gross

Domestic Product (GDP) level of more

than $8 trillion in 1998 to just under $15

trillion in 2011 or 71.5%, the Michigan

economy grew by only 26.5% over the

same period. Gross State Product grew at

an average rate of 85% over the same

period in RTW states while realizing a

slower growth rate in NRTW states of

64.2% (see Exhibit 17).

3. Net Population Migration

Michigan’s population net migration from

2000-2010 was among the worst in the

United States with a loss of 554,374 people.

Net migration is defined by the difference

in people leaving a state relative to people

migrating to a state over a given period of

time. The overall U.S. population net

migration for the same period was just

under 1,000,000 people net positive with

RTW states experiencing a positive net

migration total of just under 6,000,000 and

2012 Michigan Economic Competitiveness Study Executive Brief

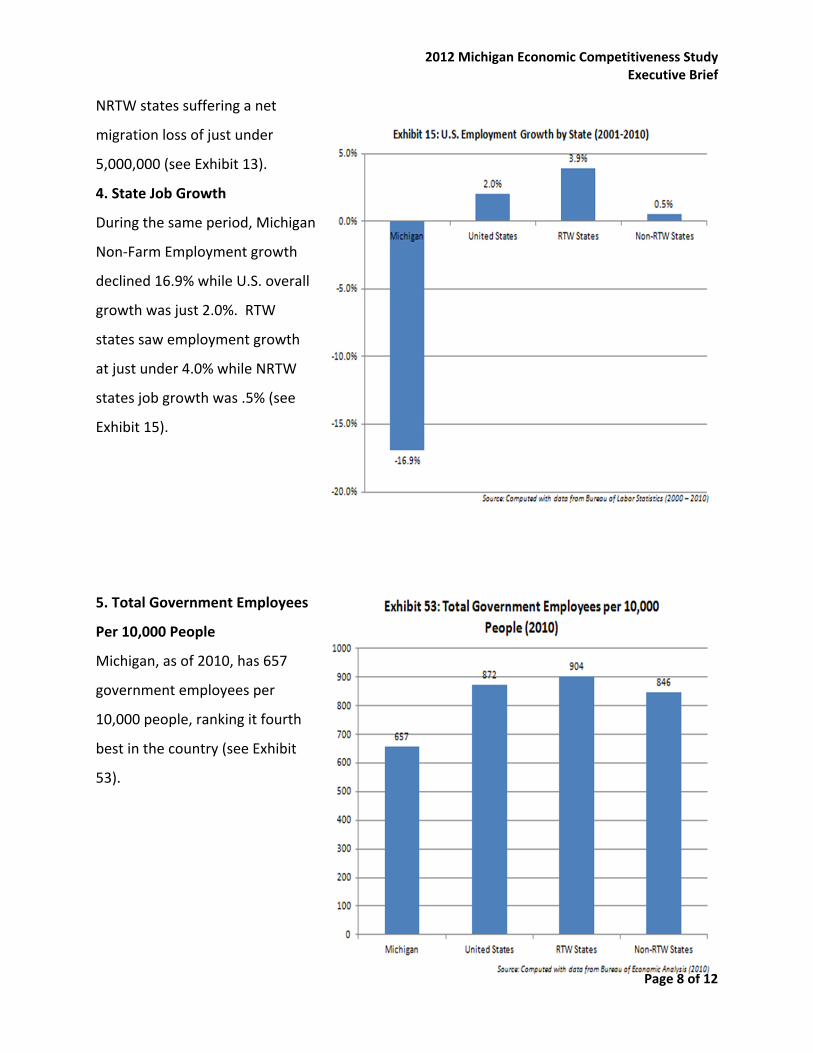

Page 8 of 12

NRTW states suffering a net

migration loss of just under

5,000,000 (see Exhibit 13).

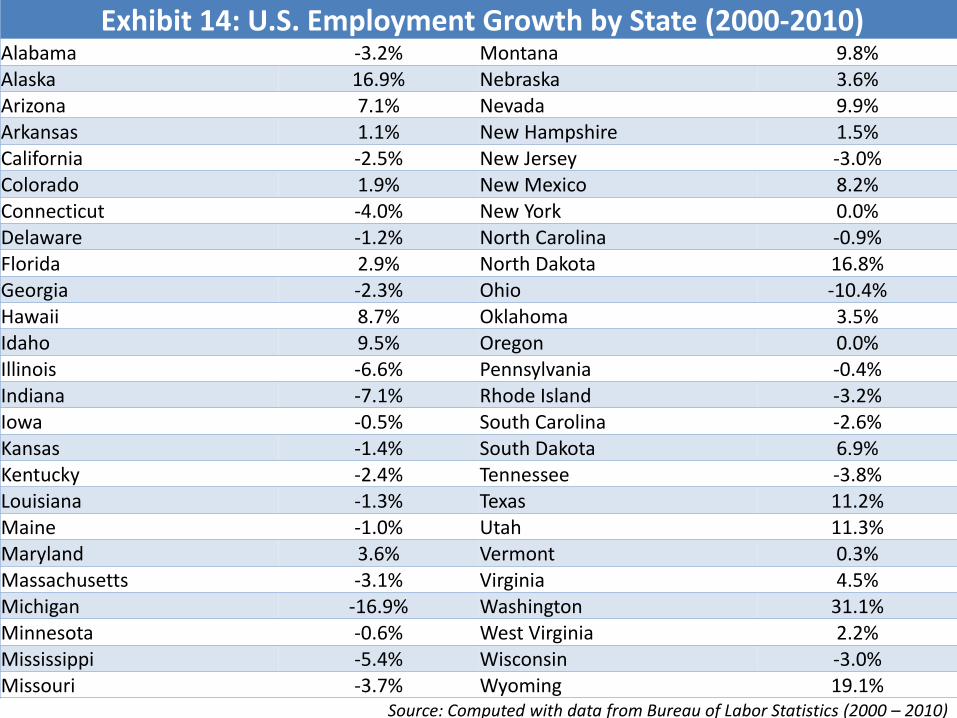

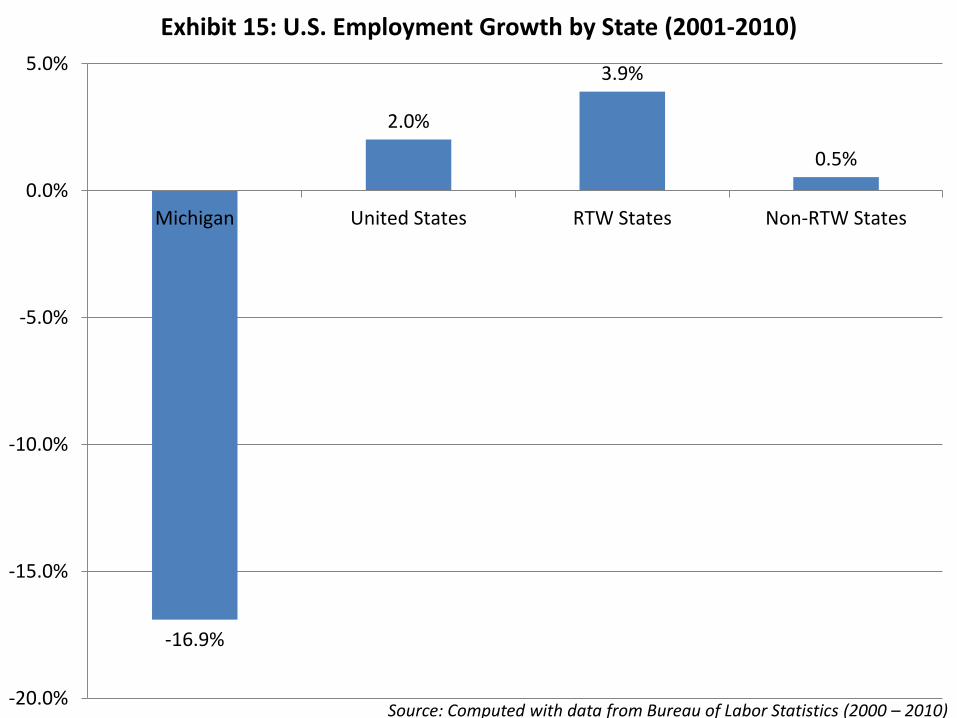

4. State Job Growth

During the same period, Michigan

Non-Farm Employment growth

declined 16.9% while U.S. overall

growth was just 2.0%. RTW

states saw employment growth

at just under 4.0% while NRTW

states job growth was .5% (see

Exhibit 15).

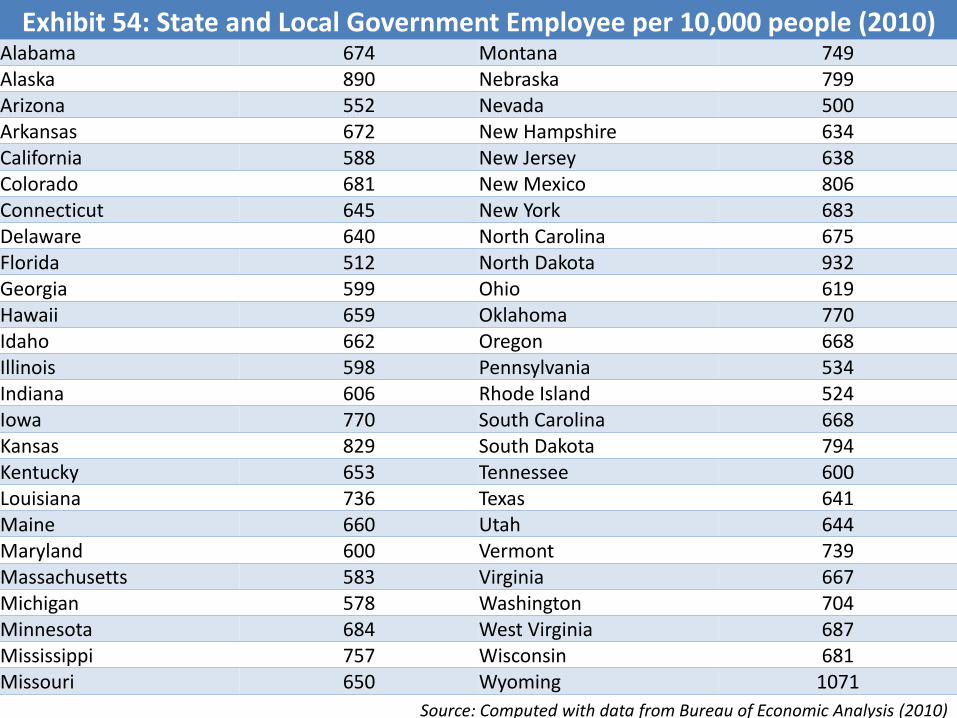

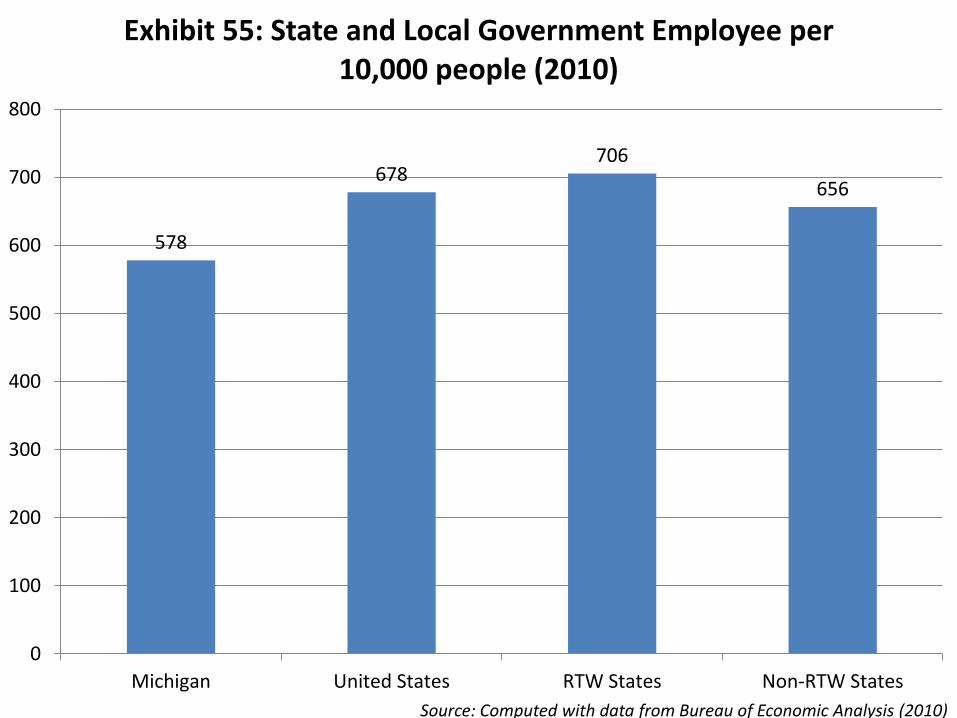

5. Total Government Employees

Per 10,000 People

Michigan, as of 2010, has 657

government employees per

10,000 people, ranking it fourth

best in the country (see Exhibit

53).

2012 Michigan Economic Competitiveness Study Executive Brief

Page 9 of 12

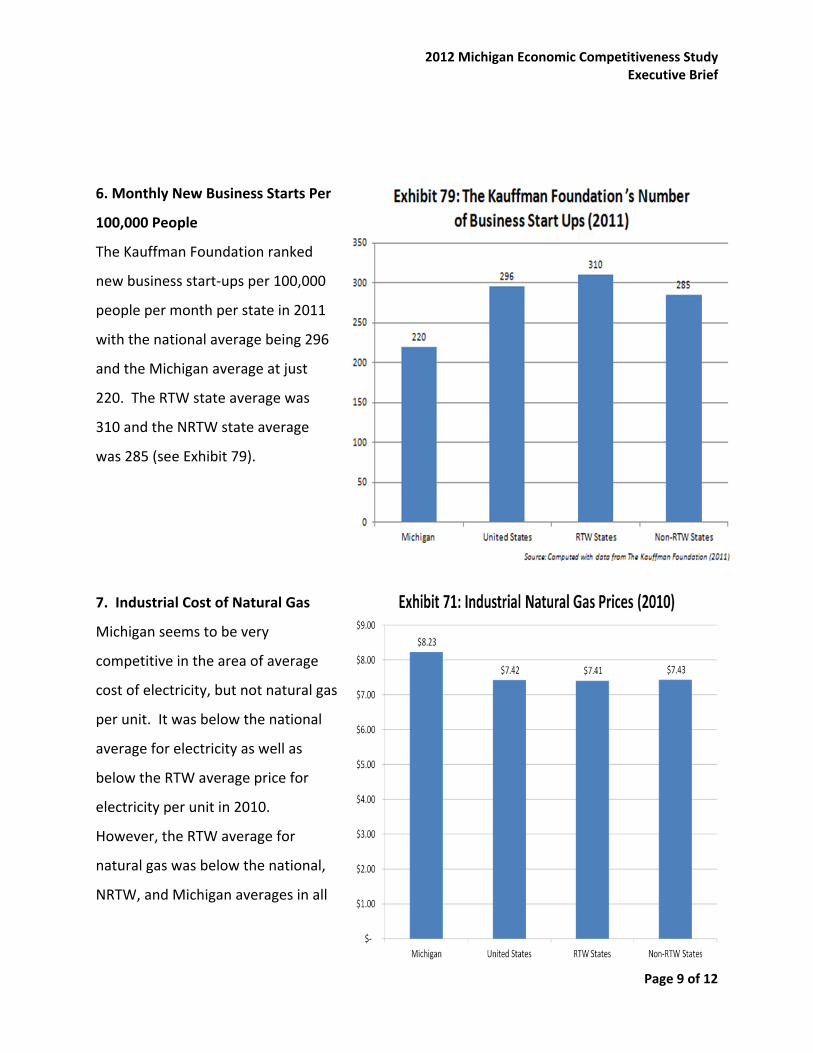

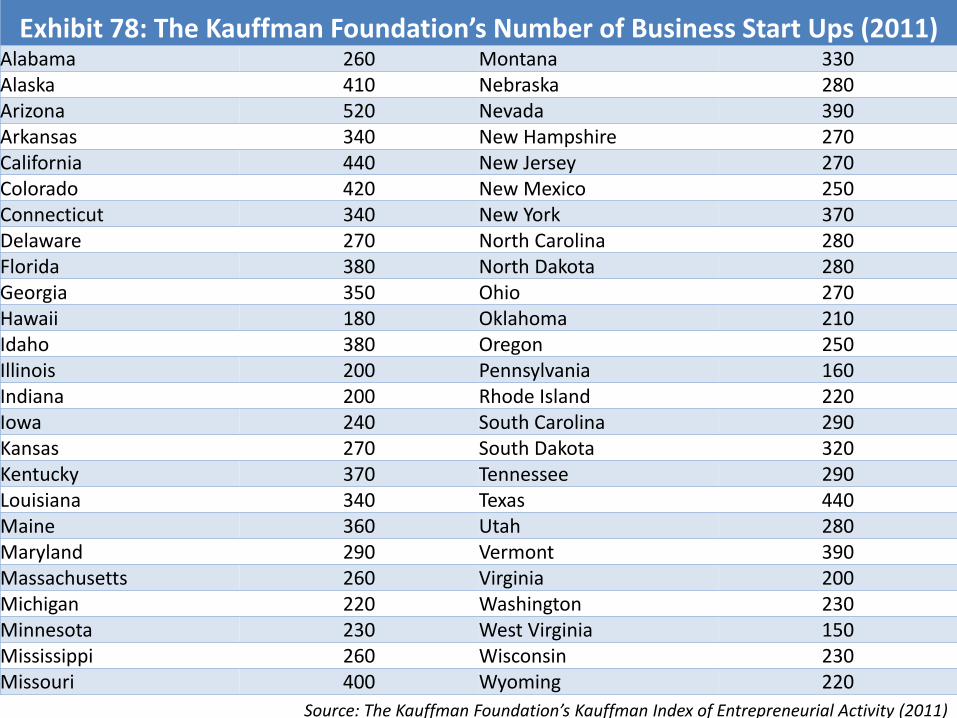

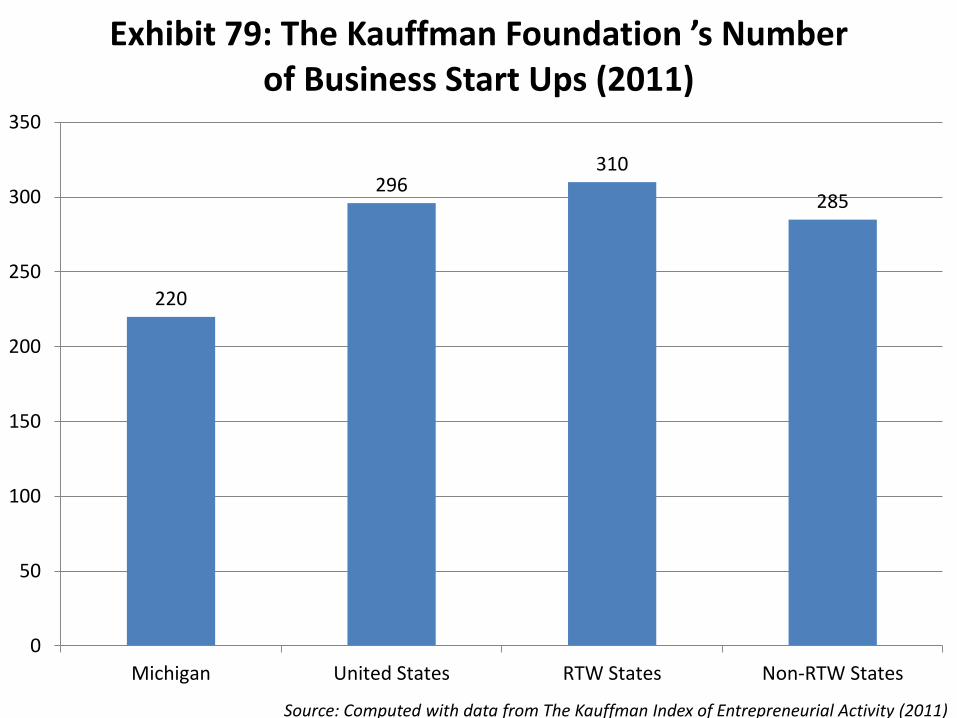

6. Monthly New Business Starts Per

100,000 People

The Kauffman Foundation ranked

new business start-ups per 100,000

people per month per state in 2011

with the national average being 296

and the Michigan average at just

220. The RTW state average was

310 and the NRTW state average

was 285 (see Exhibit 79).

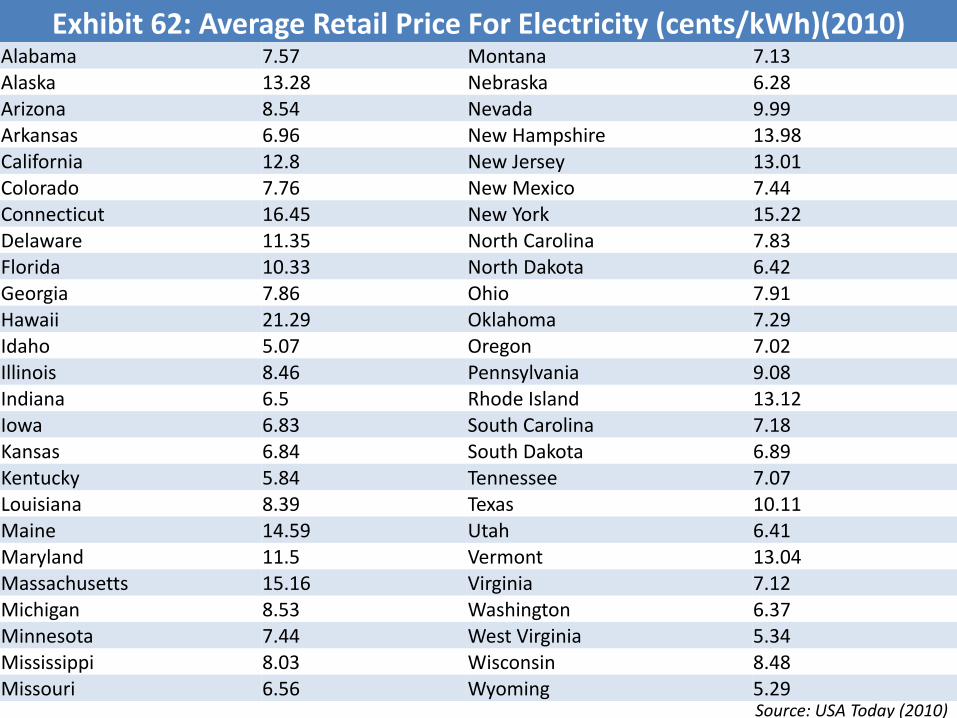

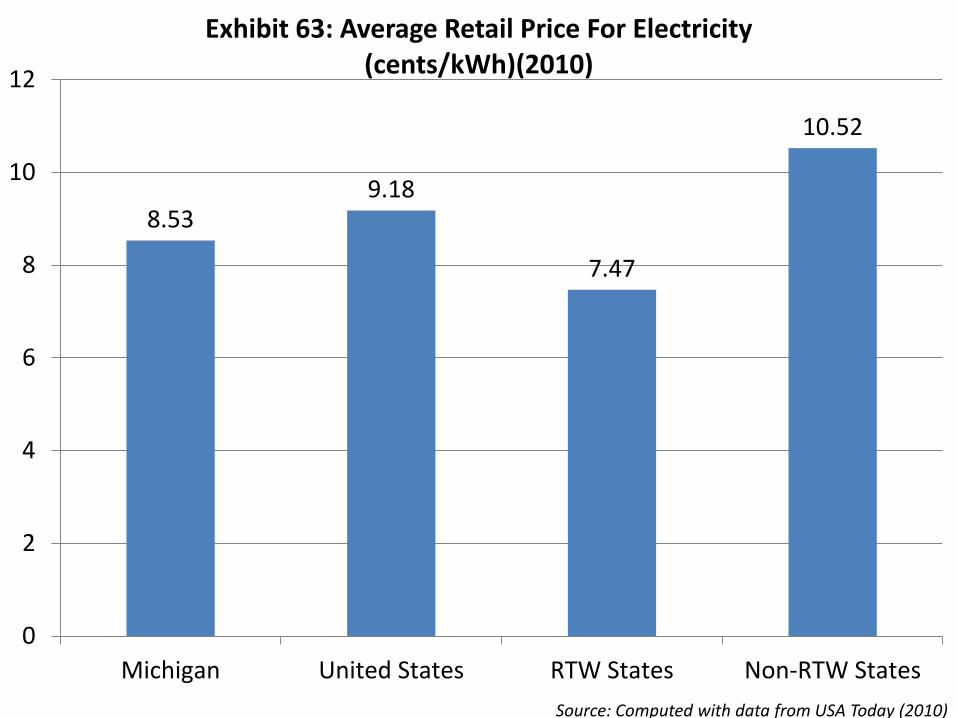

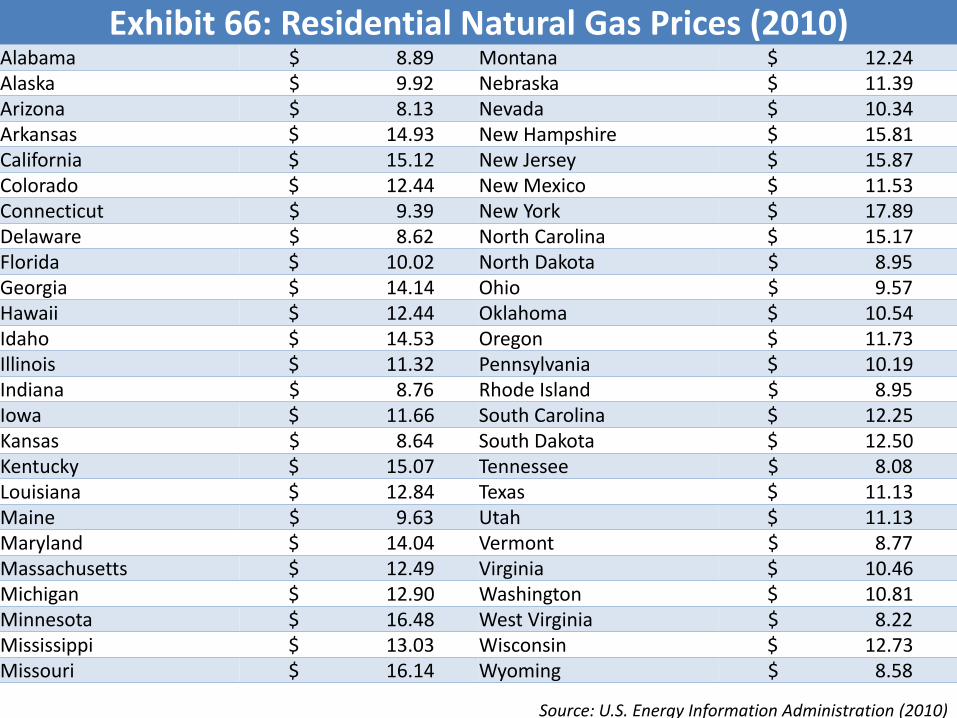

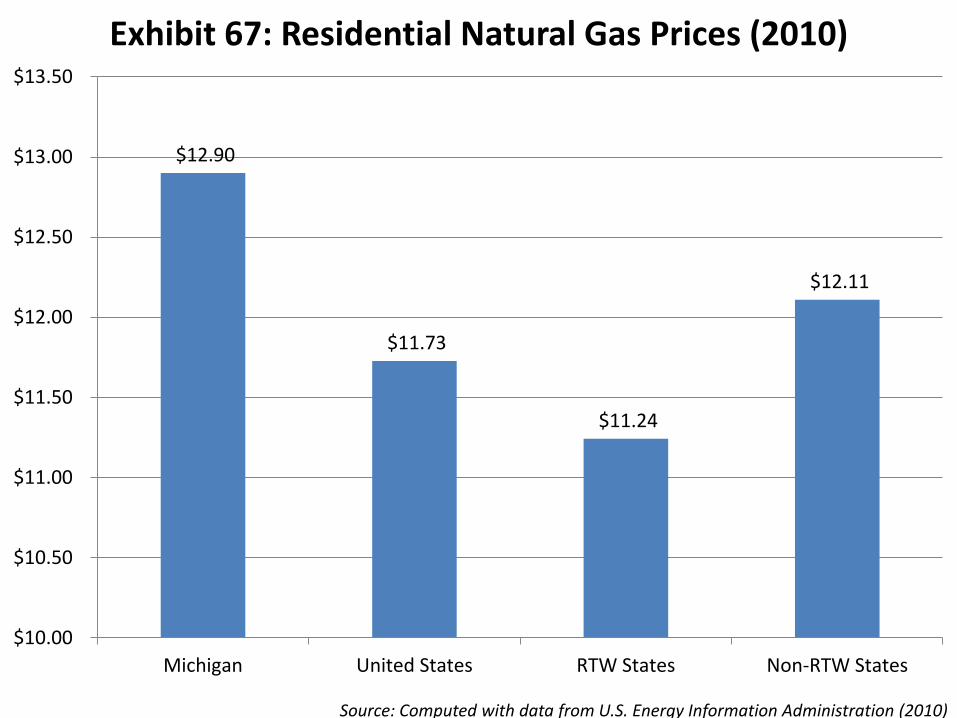

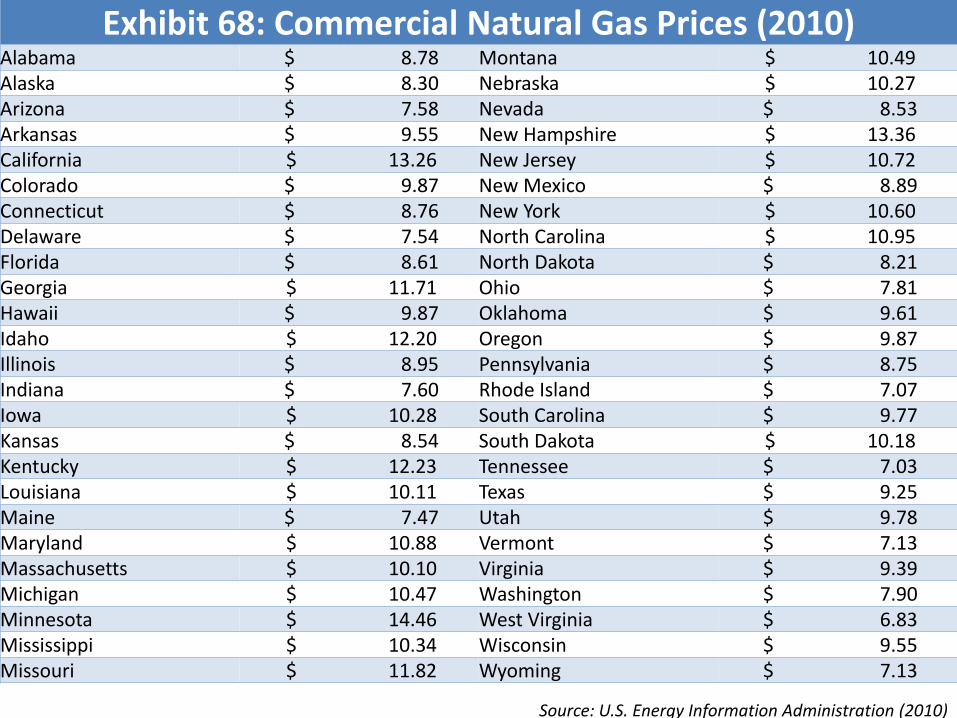

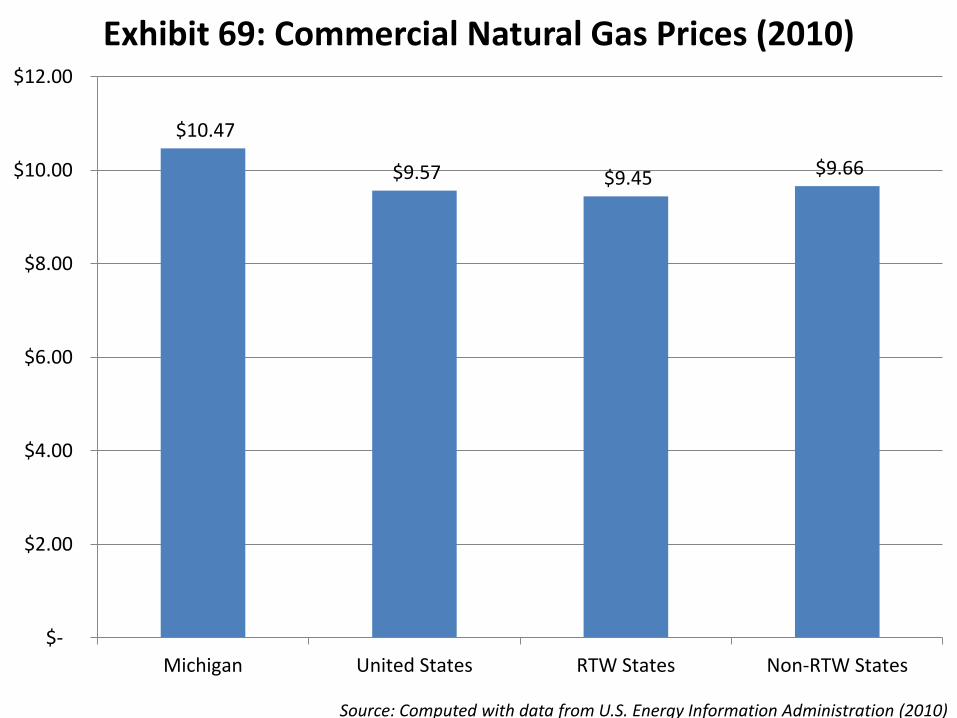

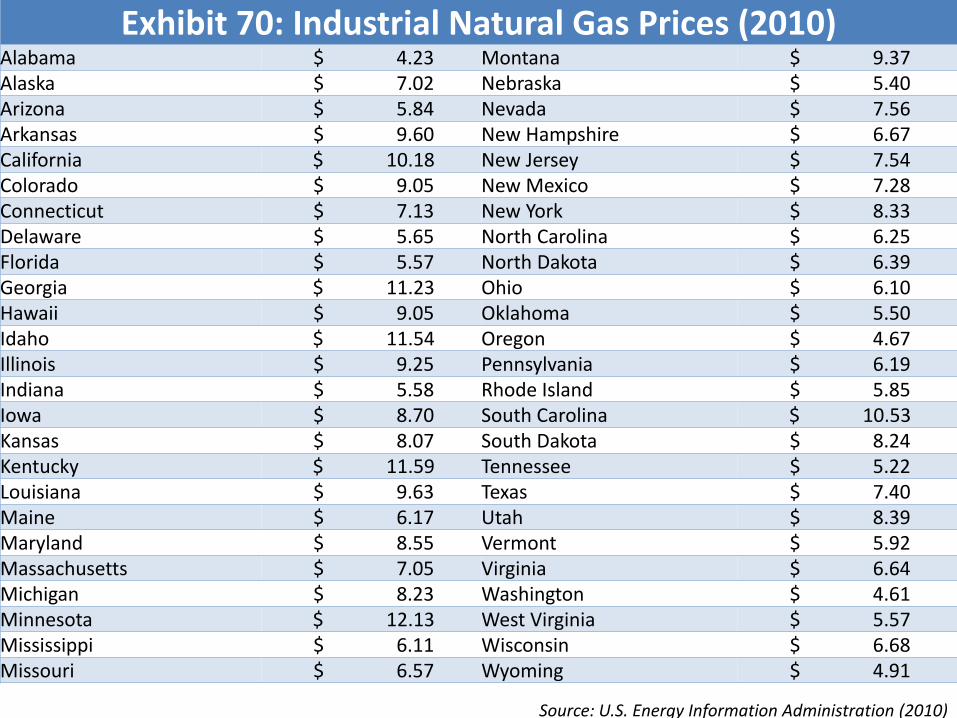

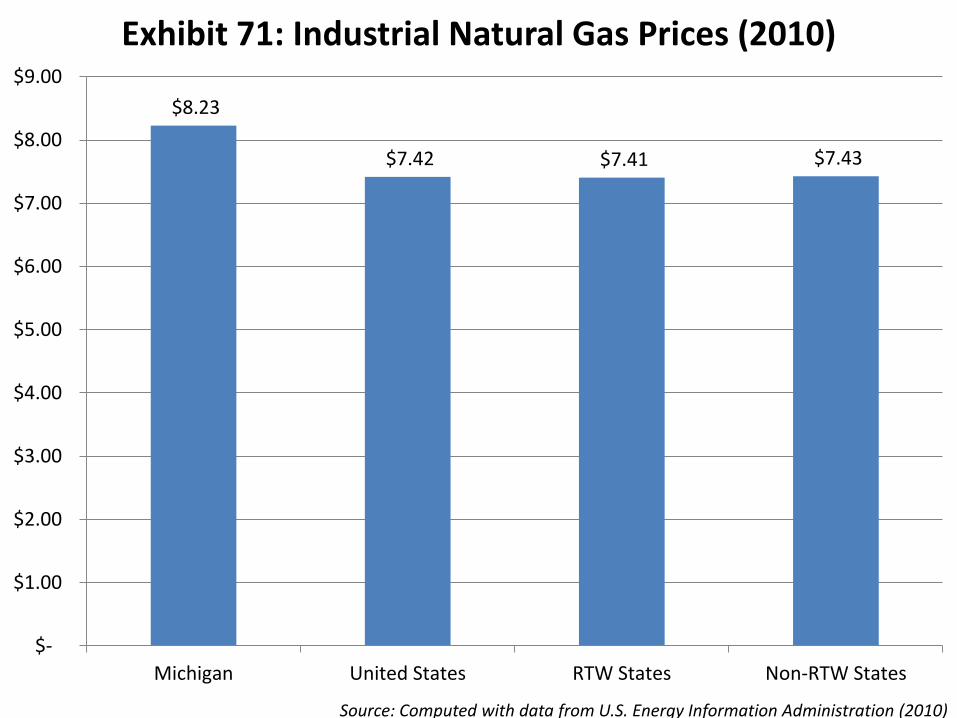

7. Industrial Cost of Natural Gas

Michigan seems to be very

competitive in the area of average

cost of electricity, but not natural gas

per unit. It was below the national

average for electricity as well as

below the RTW average price for

electricity per unit in 2010.

However, the RTW average for

natural gas was below the national,

NRTW, and Michigan averages in all

2012 Michigan Economic Competitiveness Study Executive Brief

Page 10 of 12

three natural gas categories we studied for 2010 (see Exhibit 71).

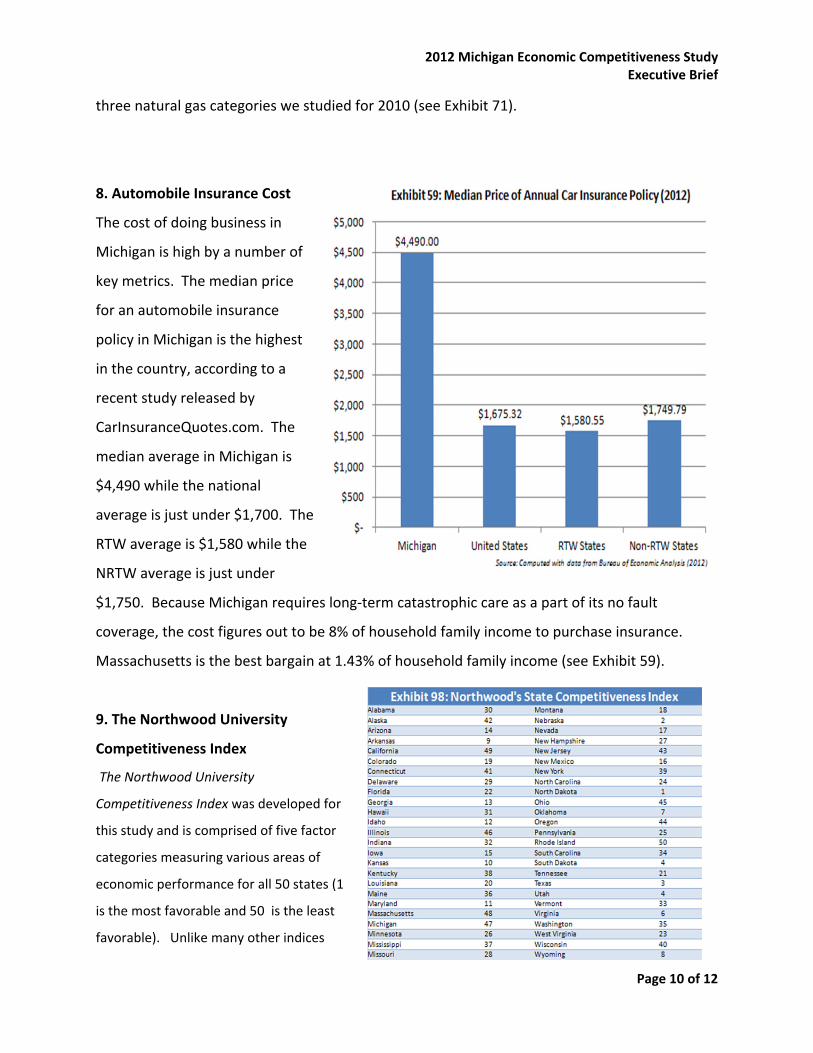

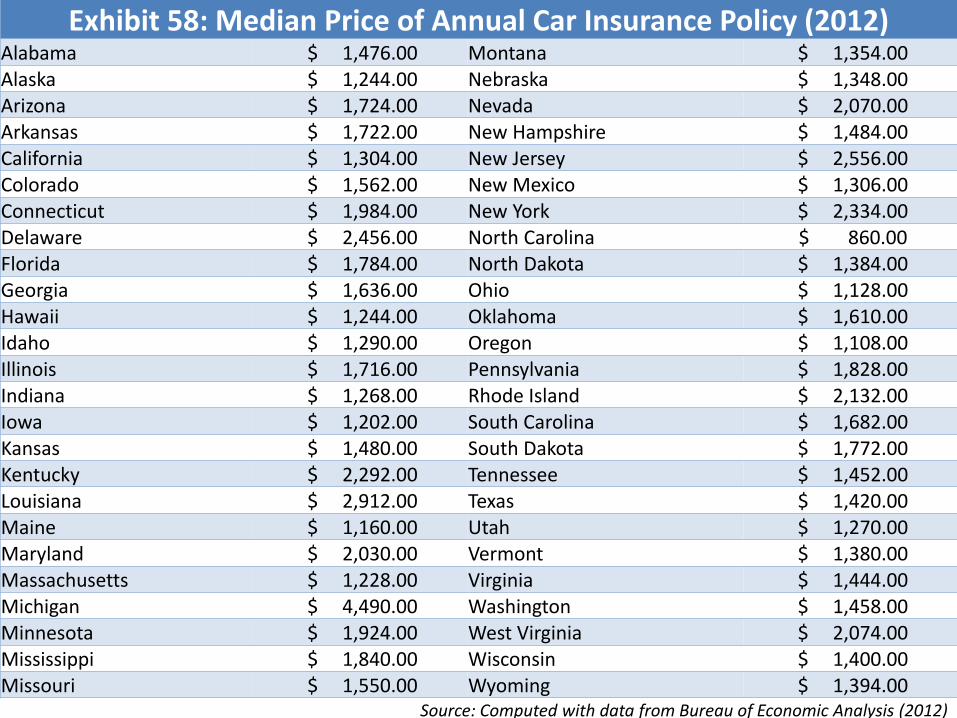

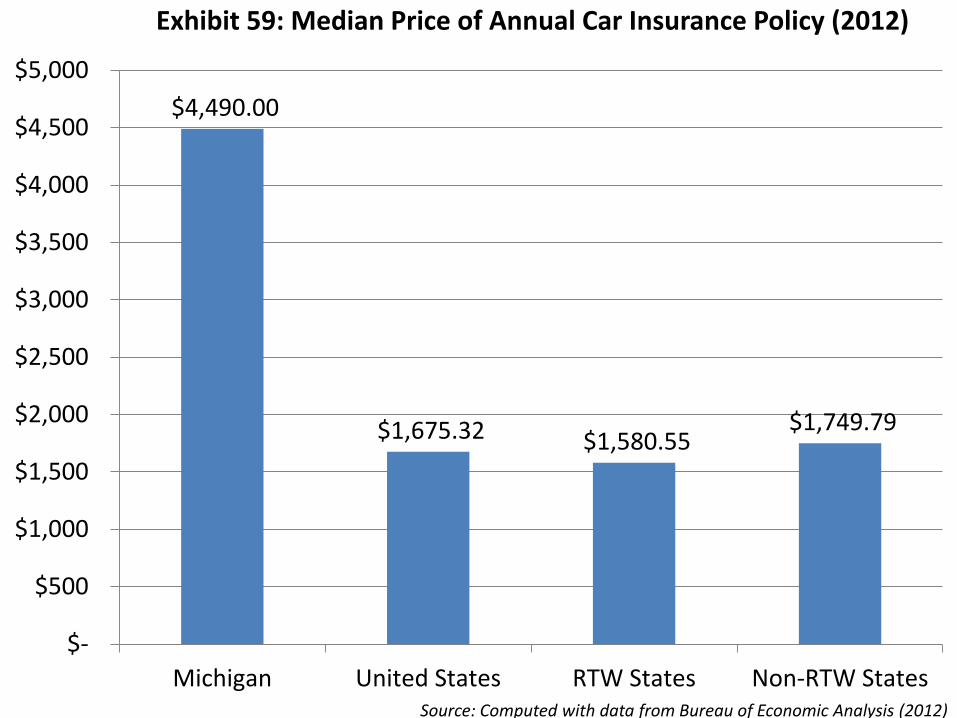

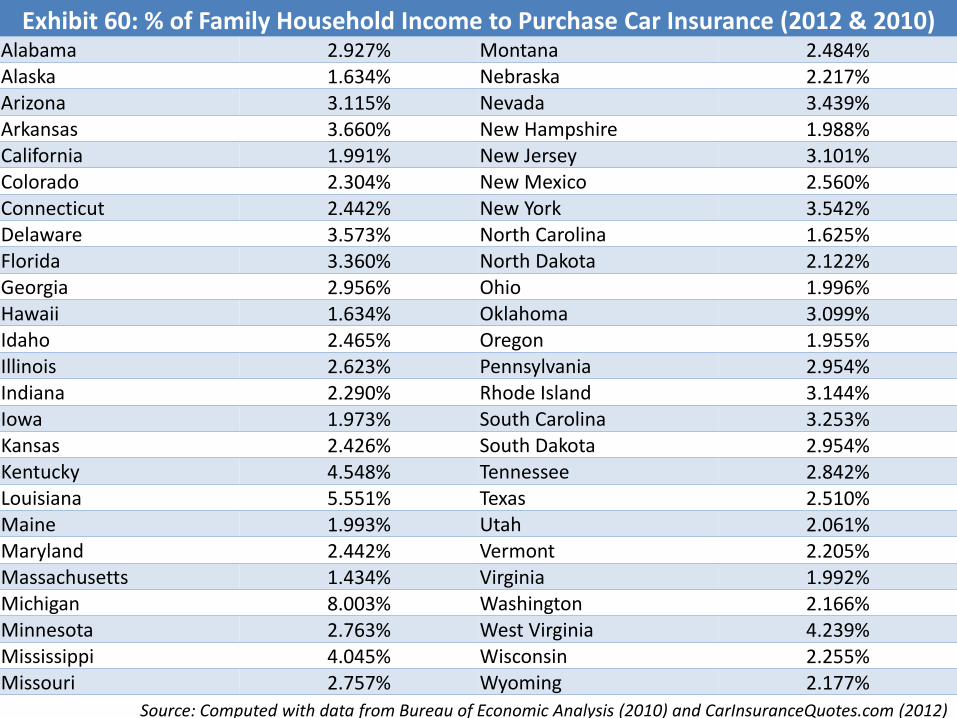

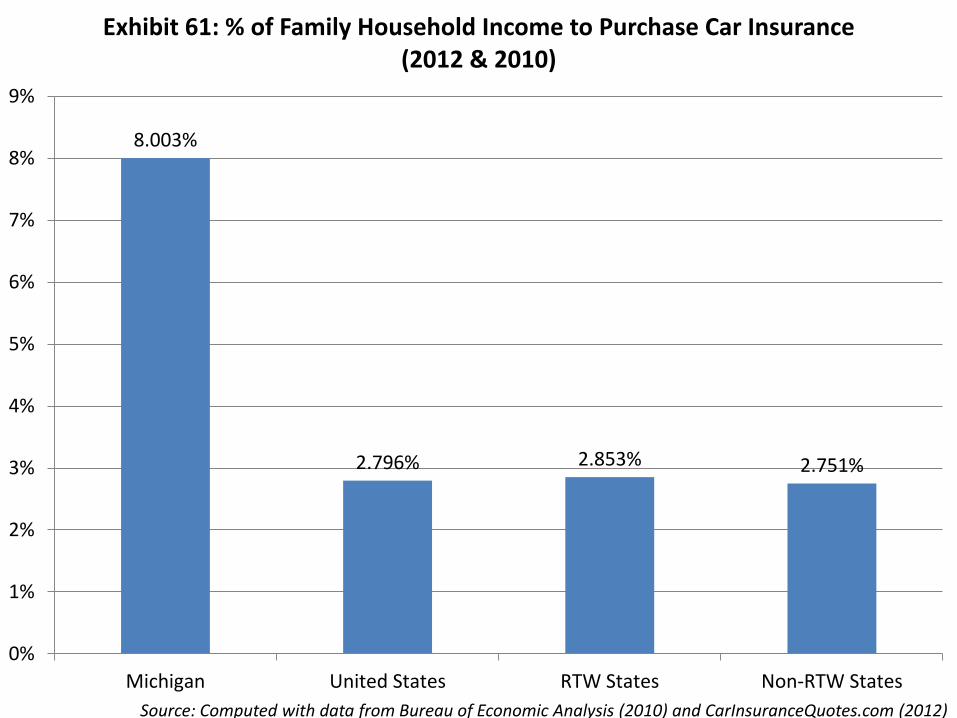

8. Automobile Insurance Cost

The cost of doing business in

Michigan is high by a number of

key metrics. The median price

for an automobile insurance

policy in Michigan is the highest

in the country, according to a

recent study released by

CarInsuranceQuotes.com. The

median average in Michigan is

$4,490 while the national

average is just under $1,700. The

RTW average is $1,580 while the

NRTW average is just under

$1,750. Because Michigan requires long-term catastrophic care as a part of its no fault

coverage, the cost figures out to be 8% of household family income to purchase insurance.

Massachusetts is the best bargain at 1.43% of household family income (see Exhibit 59).

9. The Northwood University

Competitiveness Index

The Northwood University

Competitiveness Index was developed for

this study and is comprised of five factor

categories measuring various areas of

economic performance for all 50 states (1

is the most favorable and 50 is the least

favorable). Unlike many other indices

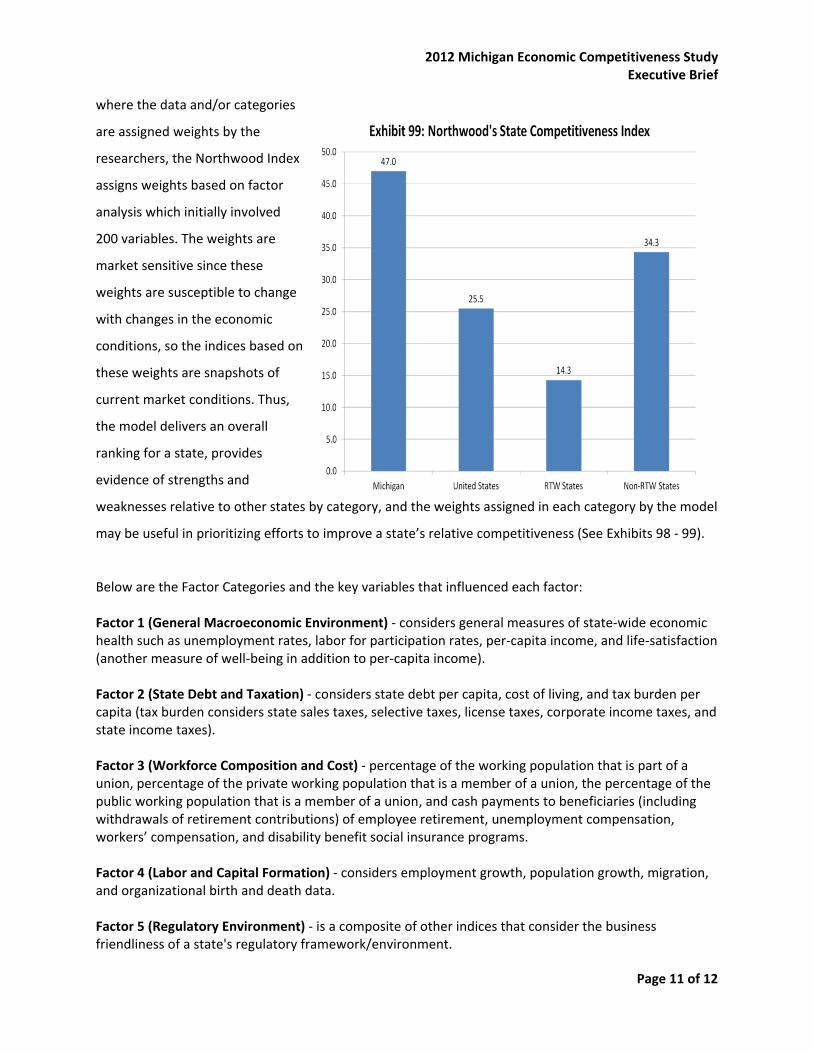

2012 Michigan Economic Competitiveness Study Executive Brief

Page 11 of 12

where the data and/or categories

are assigned weights by the

researchers, the Northwood Index

assigns weights based on factor

analysis which initially involved

200 variables. The weights are

market sensitive since these

weights are susceptible to change

with changes in the economic

conditions, so the indices based on

these weights are snapshots of

current market conditions. Thus,

the model delivers an overall

ranking for a state, provides

evidence of strengths and

weaknesses relative to other states by category, and the weights assigned in each category by the model

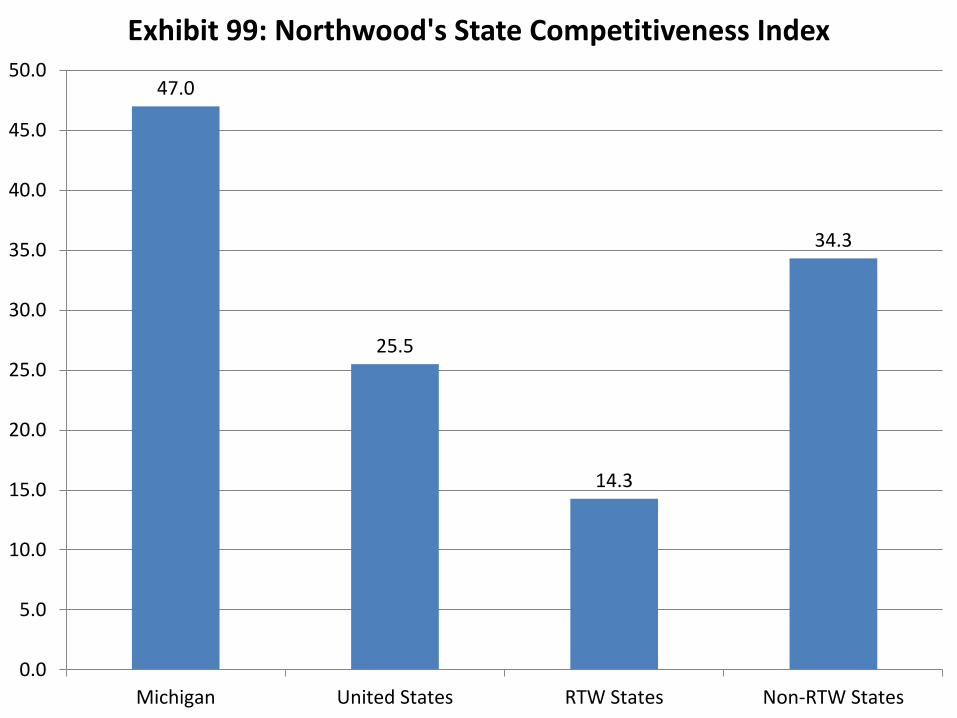

may be useful in prioritizing efforts to improve a state’s relative competitiveness (See Exhibits 98 - 99).

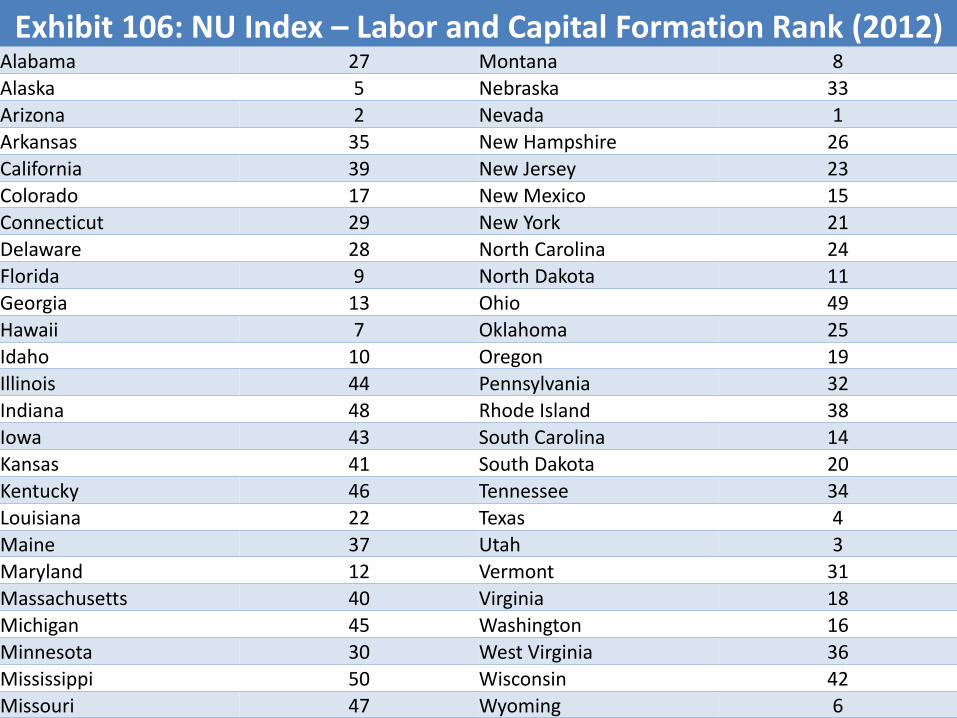

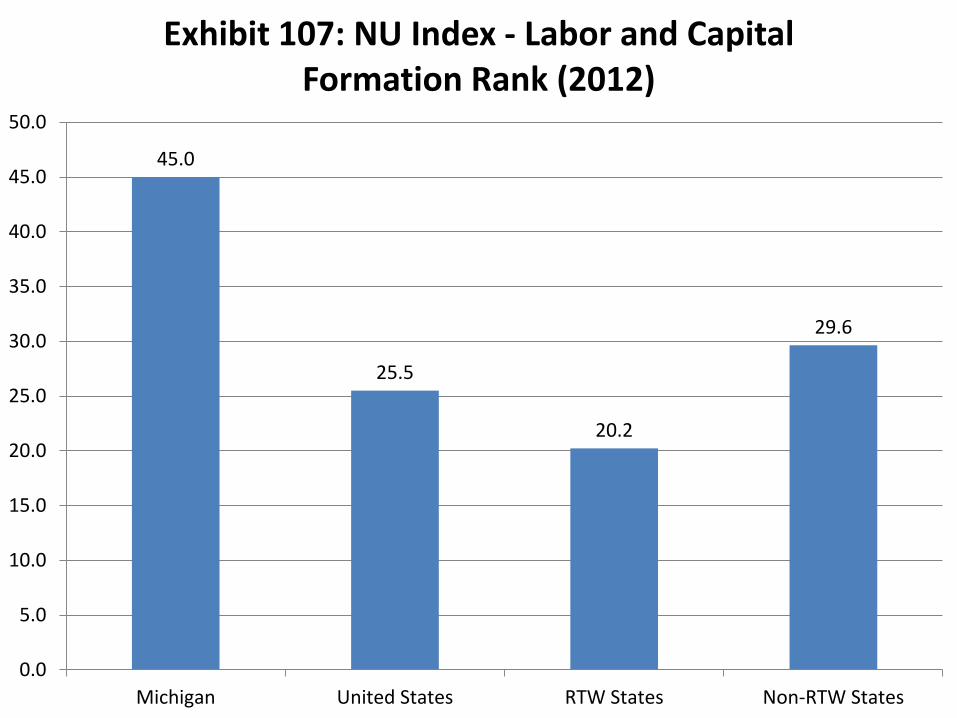

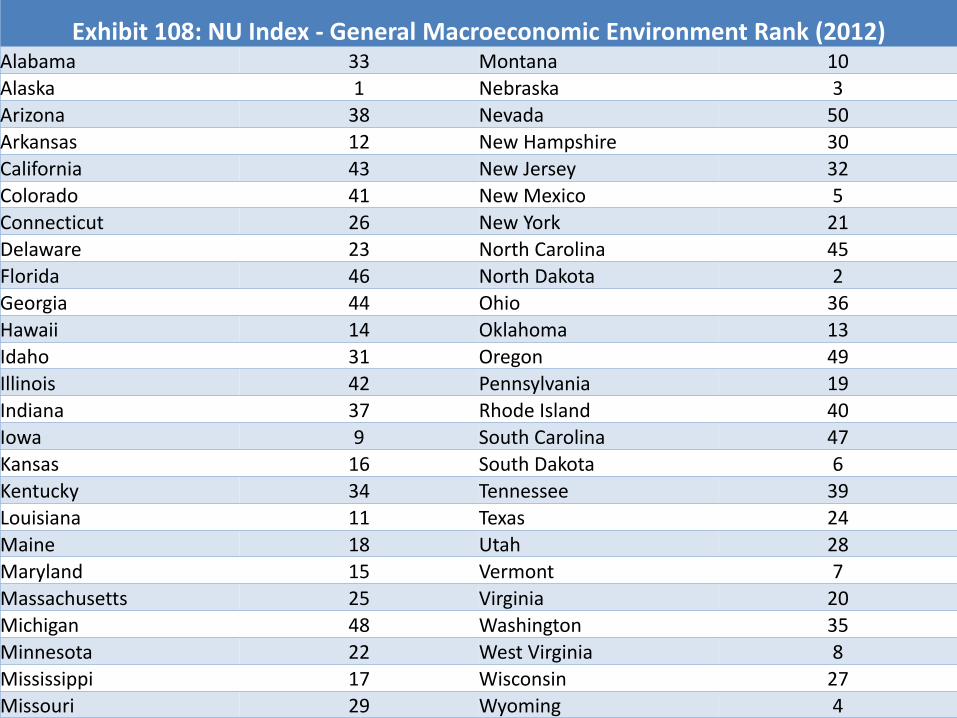

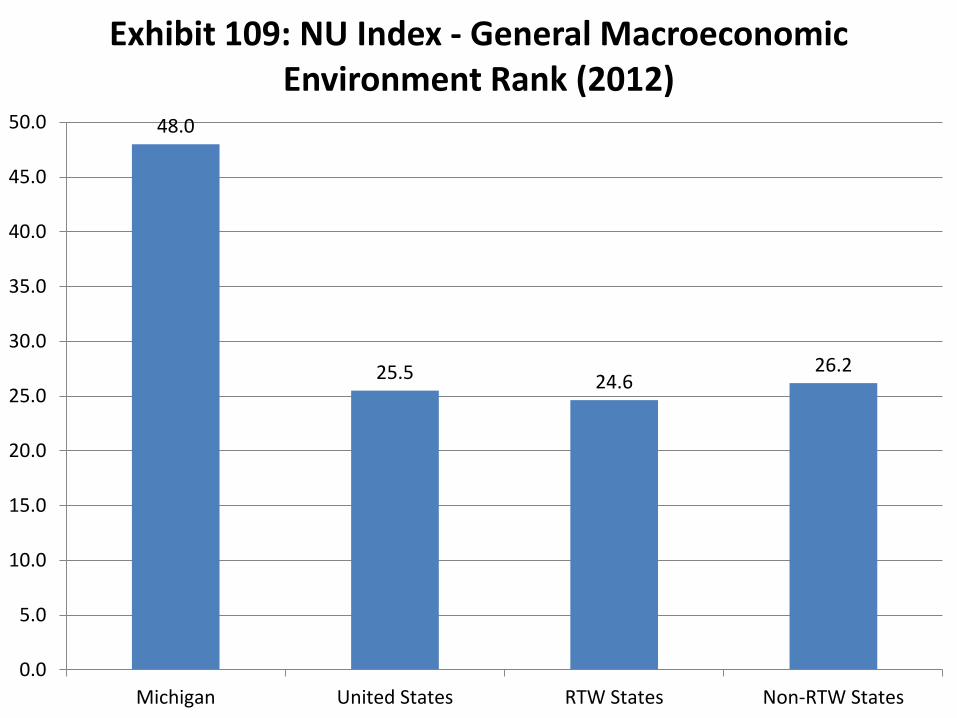

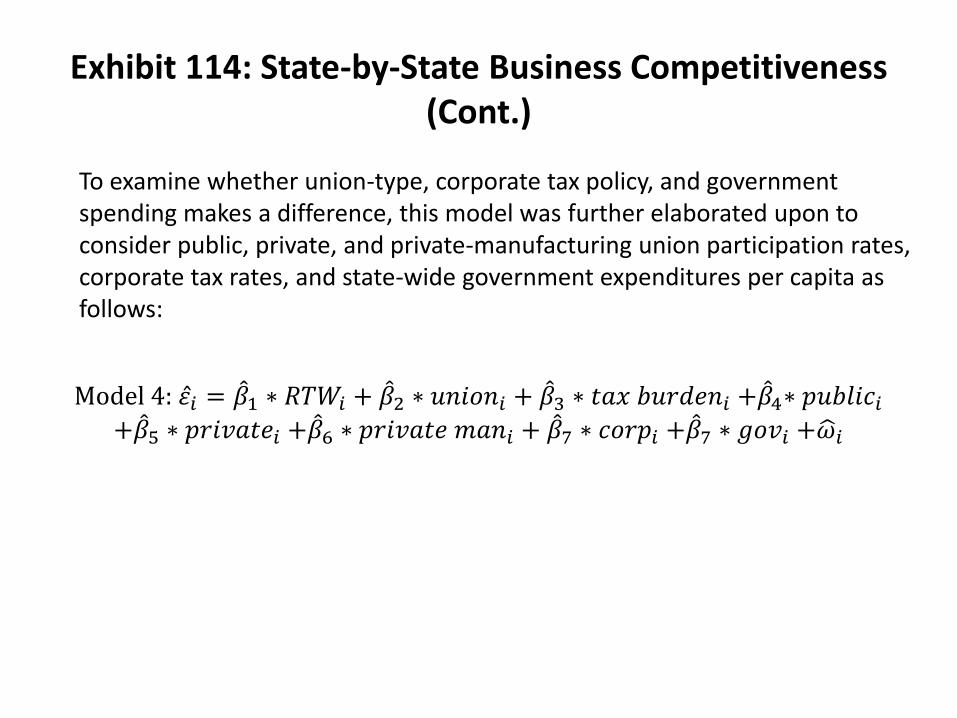

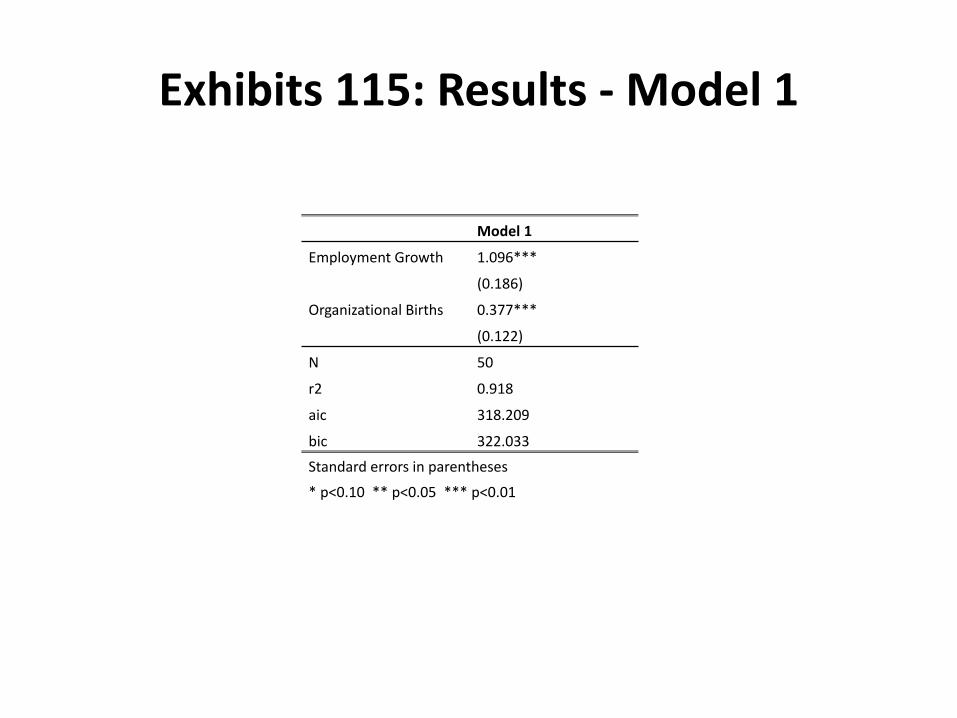

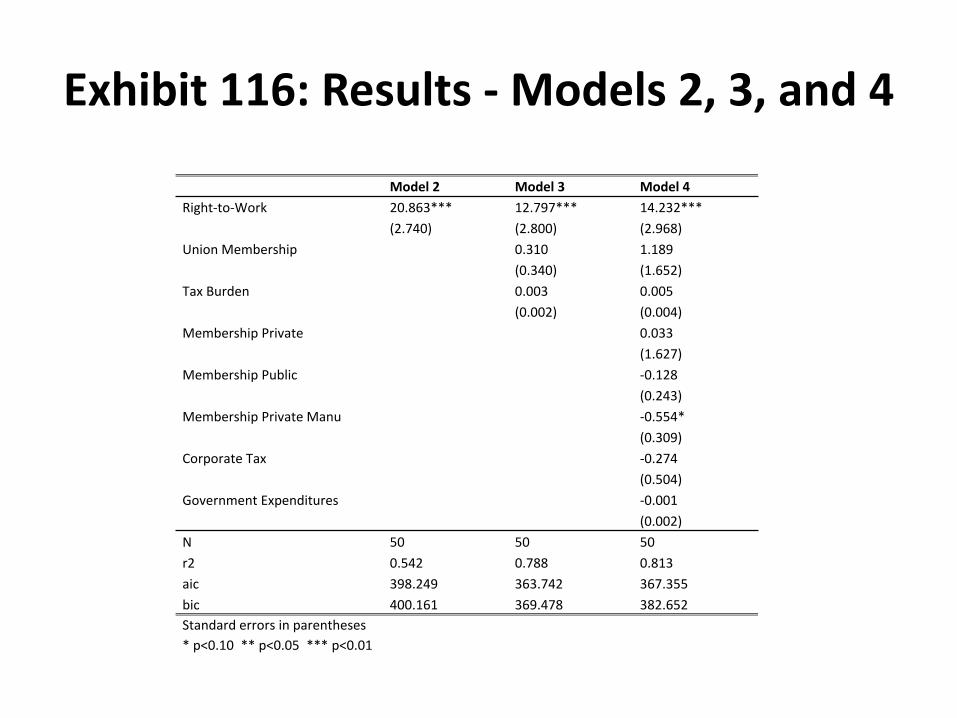

Below are the Factor Categories and the key variables that influenced each factor: Factor 1 (General Macroeconomic Environment) - considers general measures of state-wide economic health such as unemployment rates, labor for participation rates, per-capita income, and life-satisfaction (another measure of well-being in addition to per-capita income). Factor 2 (State Debt and Taxation) - considers state debt per capita, cost of living, and tax burden per capita (tax burden considers state sales taxes, selective taxes, license taxes, corporate income taxes, and state income taxes). Factor 3 (Workforce Composition and Cost) - percentage of the working population that is part of a union, percentage of the private working population that is a member of a union, the percentage of the public working population that is a member of a union, and cash payments to beneficiaries (including withdrawals of retirement contributions) of employee retirement, unemployment compensation, workers’ compensation, and disability benefit social insurance programs. Factor 4 (Labor and Capital Formation) - considers employment growth, population growth, migration, and organizational birth and death data. Factor 5 (Regulatory Environment) - is a composite of other indices that consider the business friendliness of a state's regulatory framework/environment.

2012 Michigan Economic Competitiveness Study Executive Brief

Page 12 of 12

Based on the most current available data, Michigan’s economic performance in the five categories is:

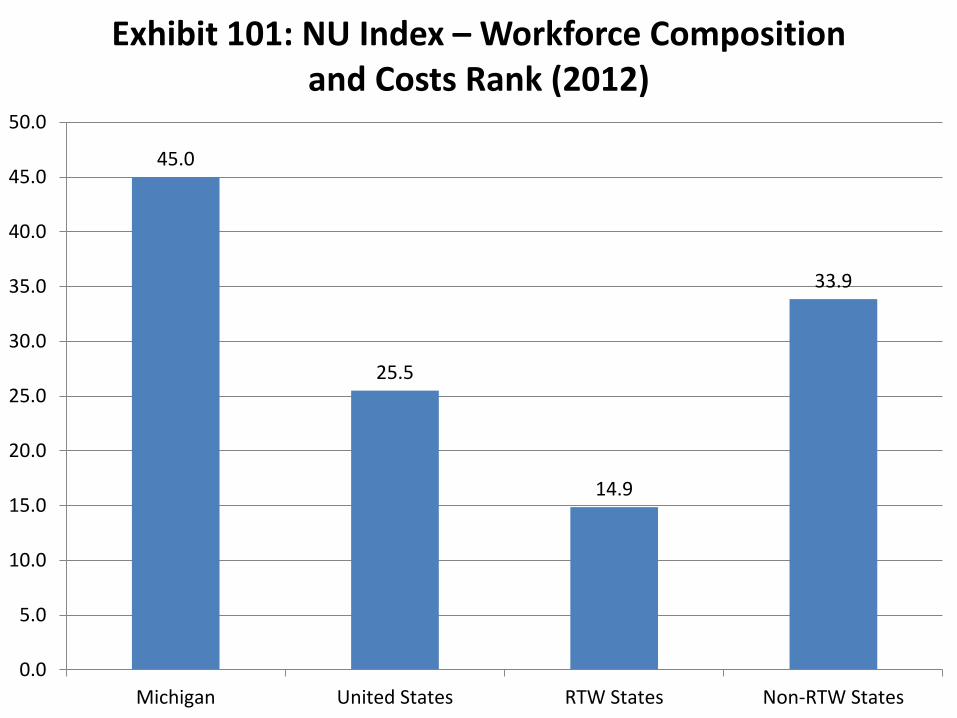

1. General Macroeconomic Environment - 48th 2. Debt and Taxation - 10th 3. Workforce Composition and Costs - 45th 4. Labor and Capital Formation - 45th 5. Regulatory Environment - 24th

Overall, Michigan ranks 47th out of the 50 states in the Index. Consequently, the state’s relatively strong

performance in terms of Debt and Taxation and Regulatory Environment are outweighed by its relatively

weak performance in the factor categories of the General Macroeconomic Environment, Workforce

Composition and Costs, and Labor and Capital Formation. A careful analysis of factors 1, 3 and 4 coupled

with sound public policies designed to address said issues will enhance Michigan competitiveness in the

future.

Conclusion

It is important that the reader understands how large and important the Michigan economy still is

within the U.S. and global economy. Michigan’s GSP is roughly equivalent to the GDP of the country of

Austria which would make Michigan one of the 30 largest economies in the world if it were a country.

However, this study does not paint a rosy picture of Michigan’s competitive position relative to most

other U.S. states. Michigan’s ranking on The Northwood University Competitiveness Index of 47 indicates

Michigan has tremendous room for improvement but also reasons for optimism. This study’s regression

analysis indicates that RTW states have a strong statistically significant relationship on productivity

growth. However, effect of RTW legislation is often hard to isolate since most RTW states are business

friendly. Since RTW states are generally business friendly, capital formation is higher resulting in higher

productivity growth. This study indicates further consideration is needed to better determine the causal

relationship between RTW legislation and competitiveness. The research contained in this study should

serve as a guidepost and tool for benchmarking for Michigan public policy leaders. For many years

Michigan was the economic catalyst for much of the U.S. economy; Detroit put America and much of the

world on wheels, and Michigan was the “Arsenal of Democracy” in World War II. Can Michigan return to

the position of greatness it once occupied in the U.S. business structure? The answer is unequivocally

yes, but only if we confront the economic reality facing this great state. Michigan must set its sights

high and benchmark to best economic and political practices of this country’s top performing states.

Finally, this study references reasons for optimism found by studying the countries of Canada and New

Zealand, which have recently experienced reform in their business climates.

1

Introduction

The following research and conclusions emanate from a series of meetings and discussions between the study authors and members of the Michigan Chamber Foundation board and staff. The study has been conceived and is designed to take a careful and unbiased look at economic competitiveness in general and the U.S. and Michigan economies in detail.

The U.S., and therefore the Michigan economy, is part of a highly complex global economy which faces constant and often radical change. The study briefly outlines the current state of U.S. competitiveness in the global economy and then focuses on Michigan’s economic performance relative to the other 49 U.S. states. The purpose of the study is to conduct a comprehensive analysis of the Michigan economy and evaluate its rank and performance across a number of metrics including but not limited to Gross State Product (GSP) growth, tax policy, regulatory policy, and cost of doing business.

This study also focuses on the issue of Right to Work legislation at both a theoretical and an empirical level. The results are interesting to say the least. Although the topic is controversial in some quarters, it deserves serious discussions at all levels of the decision making process. After comparing Michigan to many national norms, the same details were used to compare Michigan’s performance to Right to Work (RTW) states and Non-Right to Work (NRTW) states to see if there might be significant differences relative to this metric as well. The results are interesting and unique and make a compelling case for bi-partisan discussion, action and objective pro-business reforms.

The U.S. in a Complex Global Economy

Economists fundamentally agree about the source of economic growth. There are definite reasons why some nations grow and others don't. Robert Barro (1991) in his seminal paper “Economic Growth in a Cross Section of Countries” tried to answer that question. He studied the key economic and political factors that determined 98 countries’ competitiveness that led to economic growth and improved standards of living. It is clear from his studies and others that economic growth is helped by investments in human capital, lower tax rate, less regulatory burden on businesses and emphasis on the overall human development matrix. It is also clear that U.S. has been steadily falling behind in these critical investment areas, or at least unable to keep up with the investments vis-à-vis many of its competitors. Also, government is becoming

2

increasingly more important in the overall scheme of things as compared to the private sector. In addition, the federal government budget deficit and national debt have grown alarmingly high, and the financing of the deficit, along with additional post-recession banking regulation, has been instrumental in decreasing the cost of capital, making it difficult for private businesses to invest in critical areas. Many economists argue that these unprecedented increases in government spending and new regulation have been the main reasons behind the relative decline in American competitiveness. In the appendix of this paper tables and charts are provided that highlight this decline in US competitiveness across a variety of factors.

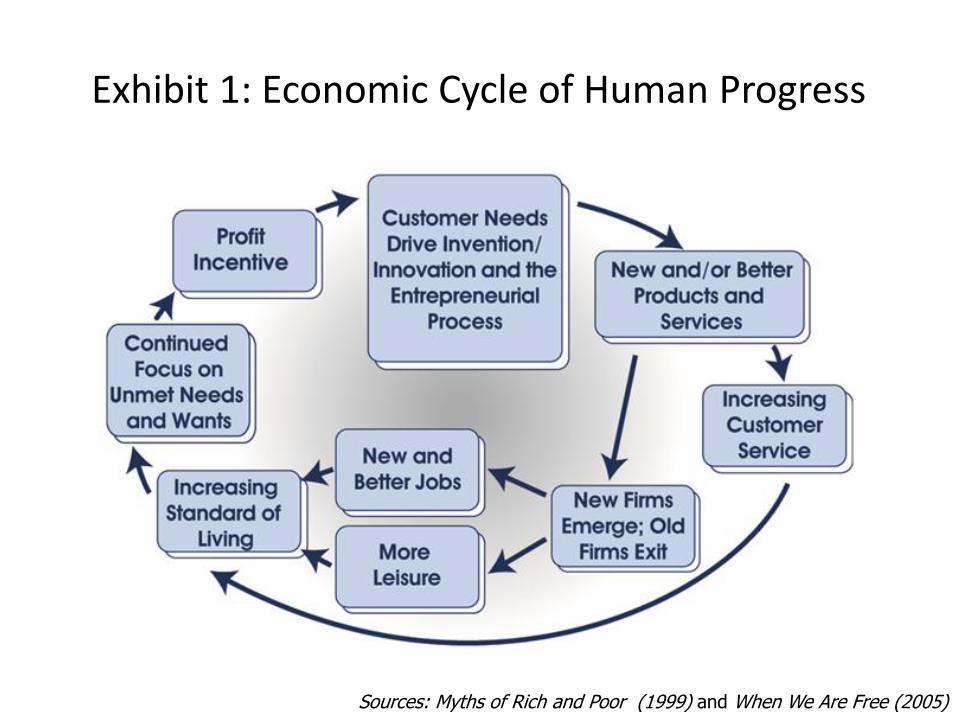

It is important to note that the 20th century was clearly was the “American Century.” The 1900s saw the United States become the world’s largest, most productive and most competitive economy while also becoming the world leader in invention and innovation. The U.S. was the envy of the world, producing new technologies and abandoning old ones while successfully commercializing the best at a rate the rest of the world could only dream of (see Exhibit 1). While the American competitive free enterprise system produced individual giants like Ford, GM, Standard Oil and U.S. Steel and billionaires named Rockefeller, Carnegie and Ford, the educated middle class realized rapid income growth and soaring standards of living that was the U.S. hallmark during this time (U.S. Department of Commerce, 2012).

U.S. economic performance was nothing short of exceptional during the 20th century driven by inventors and innovators. The U.S. became the world’s most entrepreneurial, most educated and most competitive economy and remained that way throughout most of the century. This creation of millions of jobs and newly founded businesses and industries, combined with phenomenal economic performance allowed America to comfortably shoulder the burden of World War I and II and to realize a 213 % increase in real disposable personal income from $9,240 in 1950 to $28,899 in 2010 (U.S. Bureau of Economic Analysis, 2010).

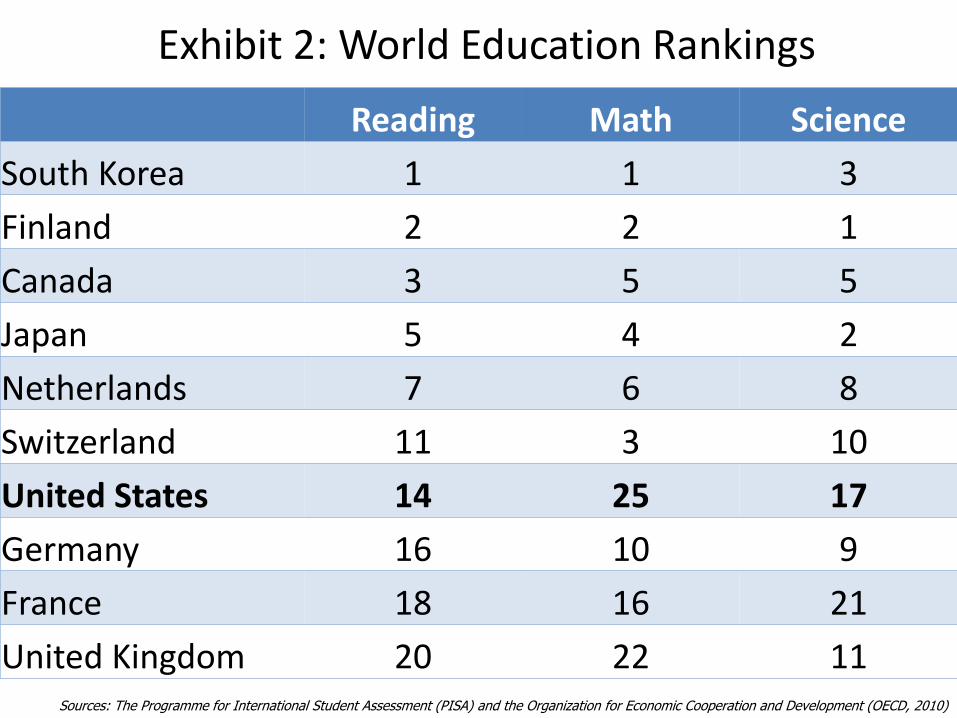

Toward the end of the 20th century grave concerns were voiced as to whether or not the U.S. could or would remain in its position of prominence atop the global economy. Income growth and job growth began to slow toward the end of the 20th century and have continued to slow into the 21st century (U.S. Department of Commerce, 2012). Simultaneously other countries began to appear on the global economic stage as viable competitors to the United States. Over the last decade or more, evidence of a decline in American competitiveness has continued to mount. As an example, U.S. 15 year olds ranked just 25th in math among the 34 industrialized countries that make up the Organization for Economic Cooperation and Development (OECD) countries and scored in the middle in science and reading on the Program for International Student Assessment (PISA) test given to students in more than 70 countries in 2009 as reported in December, 2010. The test is given every three years with the Shanghai region of China finishing number one among the 72 countries taking the exam (see Exhibit 2). In response to

3

this report, U.S. Secretary of Education Arne Duncan stated that “the brutal fact here is there are many countries that are far ahead of the U.S. and improving more rapidly than we are. This should be a massive wake-up call to the entire country” (Bloomberg, 2010).

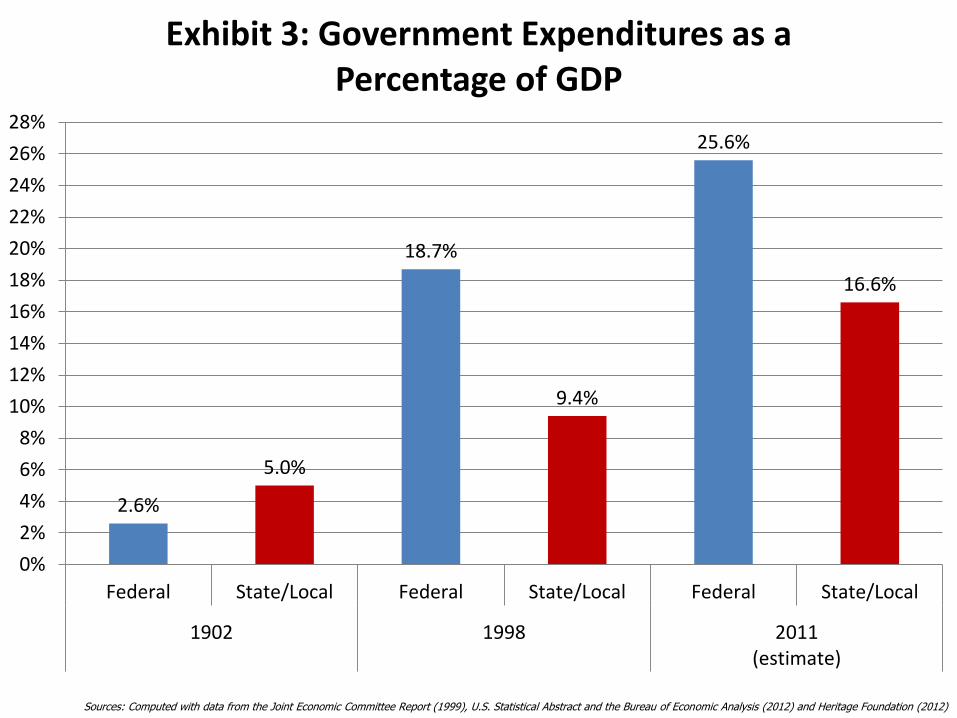

In addition, according to the Congressional Budget Office and the Heritage Foundation, government at all levels in the United States consumed less than 8 % of GDP by expenditures in 1902 and today consumes more than 42 % (see Exhibit 3). We believe that 8 % government expenditures as a percent of GDP is unrealistically too low in today’s complex global economy; yet we also believe that 42 % is excessively high, creating a crushing burden on business and economic growth in the United States.

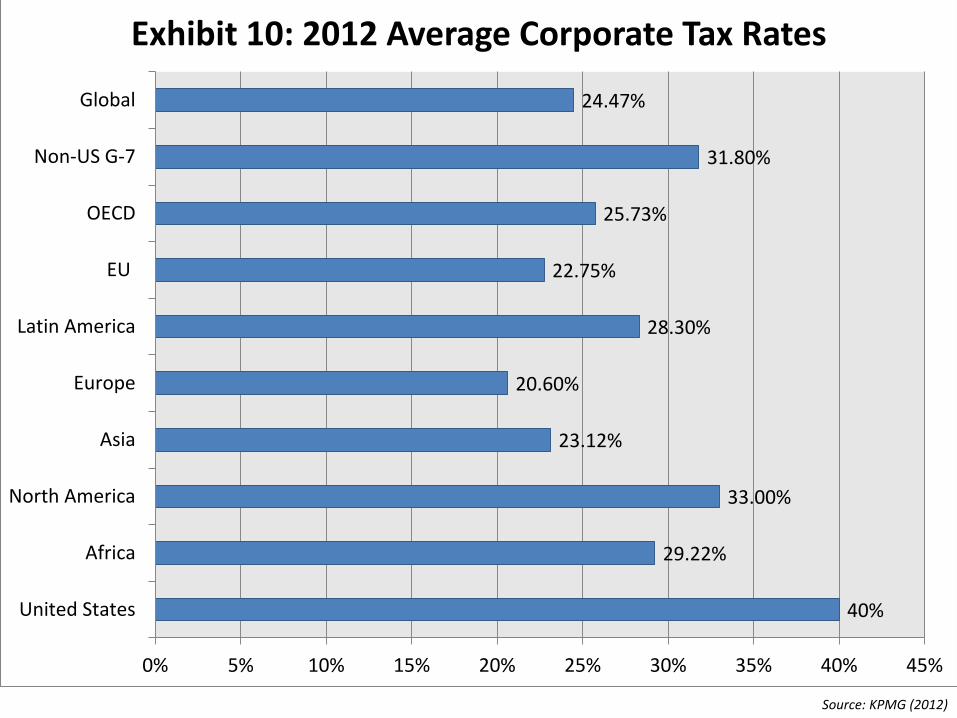

Additionally, The U.S. tax system is becoming more and more burdensome to U.S. competitiveness relative to the rest of the world. According to the Tax Foundation, the U.S. now has the highest corporate income tax rate in the industrialized world at 39.2 %, not because the U.S. has raised taxes but rather because many of its competitors have lowered their rates over the last decade (see Exhibit 4). The U.S. also has among the highest long-term and integrated capital gains tax rates in the industrialized world at 19 % and 51 % respectively (see Exhibit 5).

In reviewing the 16 key indicators (including the number of scientists and engineers, corporate and government R&D, venture capital, productivity, trade performance and others) contained in the July 2011 Atlantic Century (Atkinson, 2011) report, the results show the U.S. ranked number four behind Singapore, Finland and Sweden.

While a fourth place ranking doesn’t appear to be too bad, additional studies and data sources paint a picture of a less nimble and less competitive U.S. economy and business environment. The 2012 Heritage Foundation/Wall Street Journal’s Index of Economic Freedom measures political freedom, prosperity, and economic freedom across 10 metrics to gauge the economic success of 184 countries around the world. In 1995 the U.S. was ranked 4th in the world on the index, and in 2012 the U.S. dropped to 10th (see Exhibit 6). Another measure of economic competitiveness is the highly regarded International Institute for Management Development’s (IMD) Global Competitiveness Index, which consists of 323 variables and four sub-indices (Economic Performance, Government Efficiency, Business Efficiency and Infrastructure) and measures the competitiveness of nations by analyzing how they create a competitive business environment. The U.S. has dropped from being ranked number one on the 1999-2000 index to number five on the 2011-12 index behind Switzerland, Singapore, Sweden and Finland (see Exhibit 7).

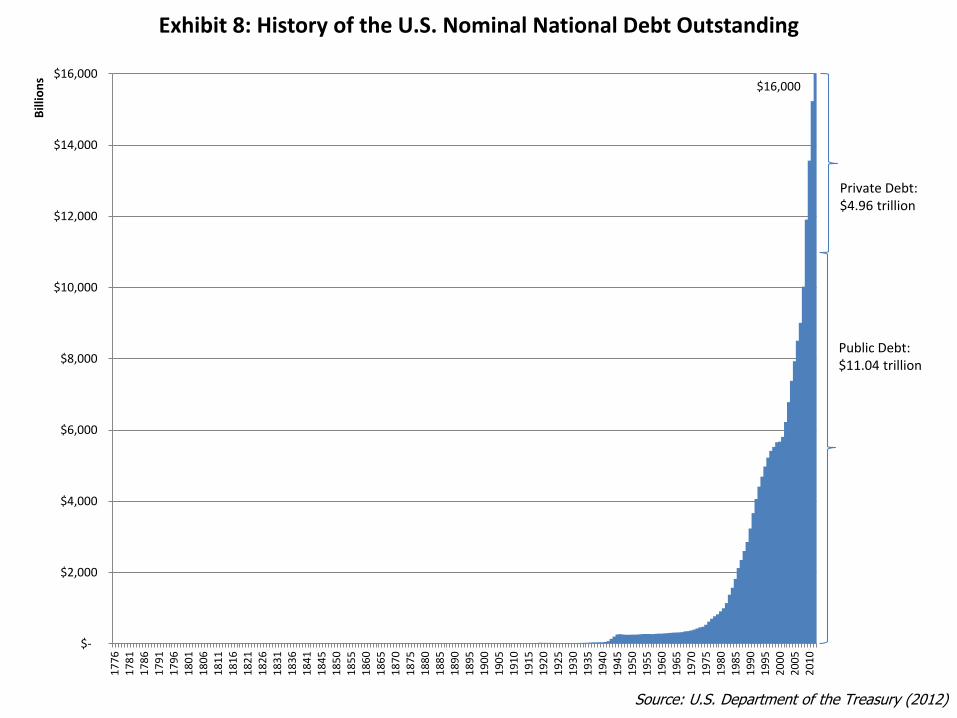

U.S. competitiveness is being adversely impacted by a number of factors, including a mounting national debt which now stands at $16 trillion and is greater than 100% of projected 2012 GDP.

4

The national debt of the United States took more than 205 years to reach the one trillion dollar mark, and in roughly 30 years it increased 15 fold (see Exhibit 8). According to the U.S. Department of the Treasury and the U.S. Congressional Budget Office (CBO), U.S. gross interest rate payments on treasury debt securities in 2011 was $454 billion dollars (more than the total GDP of some of the most advanced economies in the world). It is also important to note that the debt was serviced at a historically low average interest rate of just 2.62 % (see Exhibit 9). There is concern with the future burden of gross interest rate payments in the United States if the economy recovers or if it enters an inflationary spiral; in either case, interest rates will rise as will the cost of servicing the national debt.

Many believe that the solution to the U.S. deficit problem is simply to raise taxes, especially on those in the top 1 % on personal income and on corporations. According to the Tax Foundation in 2009 (the most recent tax data available), the top 1 % of income earners paid 36.7 % of total U.S. personal income taxes while the top 10 % percent paid 70.5 % (Tax Foundation, 2012). Additionally, in 2012 the U.S. gained the dubious distinction of having the highest corporate income tax rate in the industrialized world, making the U.S. and the North American region less competitive (see Exhibit 10).

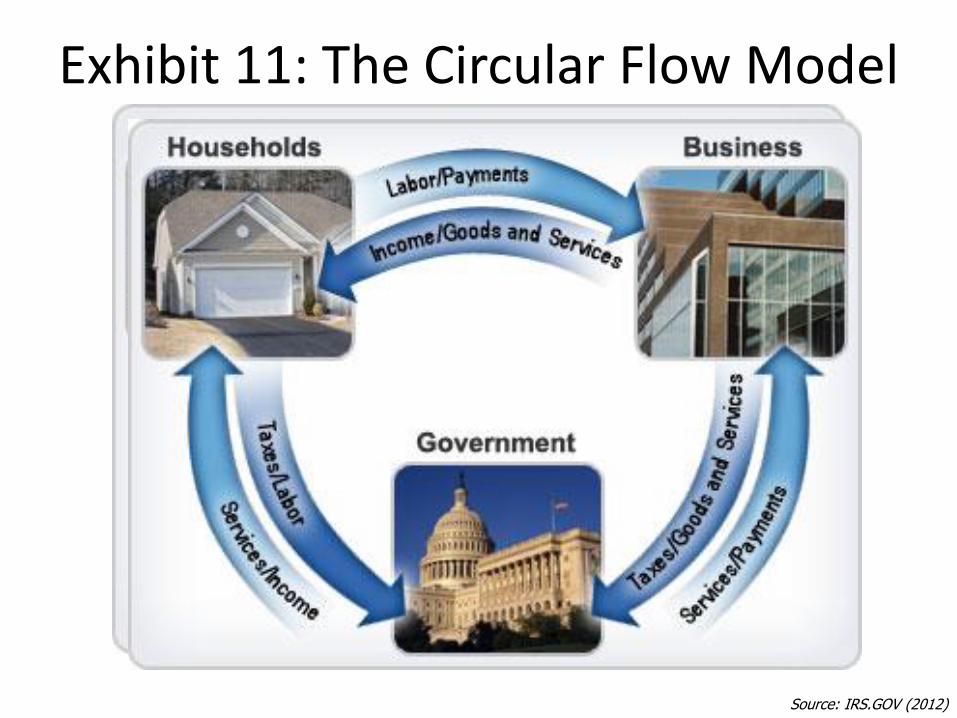

Somewhere over the last one hundred years the United States as a country has lost sight of what made it great. There is less understanding of the contributions of (a) economic and political freedom and (b) entrepreneurship and investment to (c) business success, infrastructure development and rising standards of living. Productivity and wealth generated by a free and dynamic business sector allow for households to prosper and government to exist and operate and play a vital role in the economy. All three of the macro flow variables (households, business and government) are important (see Exhibit 11). The mix of resource allocation among households, businesses, and government needs to be closely reexamined as government is consuming an ever-increasing share of U.S. GDP thus thwarting U.S. competitiveness and growth.

Michigan in a Changing U.S. Economy

The U.S. economy’s pace for invention, innovation and new business formation was staggering throughout the 20th century, and Michigan was at the epicenter of much of that growth. Michigan- based companies like Amway, Chrysler, The Dow Chemical Company, The Ford Motor Company, General Motors, Kellogg, Upjohn and Whirlpool were complemented and supplemented by thousands of small and medium-sized entrepreneurial organizations, making Michigan a center for business excellence (U.S. Department of Commerce Report, 2012). A

5

further measure of Michigan’s success in that period is the fact that Detroit had the highest per capita average income in the United States in 1950 (Skorup, 2009)

However, Michigan began to lose its competitive edge to lower-cost U.S. states and foreign countries starting in the 1970s and continuing into the 21st century. Today, the Michigan economy is still heavily reliant upon the automobile industry and has not attracted sufficient new businesses to the state or developed home-grown entrepreneurs to ensure strong economic growth and wide scale economic diversification. The following analysis will shed some light on the factors impeding economic growth in Michigan while comparing Michigan to numerous national averages and the average for U.S. Right to Work (RTW) states and U.S. Non-Right to Work (NRTW) states.

Population, Employment and GDP Growth in Michigan and the United States

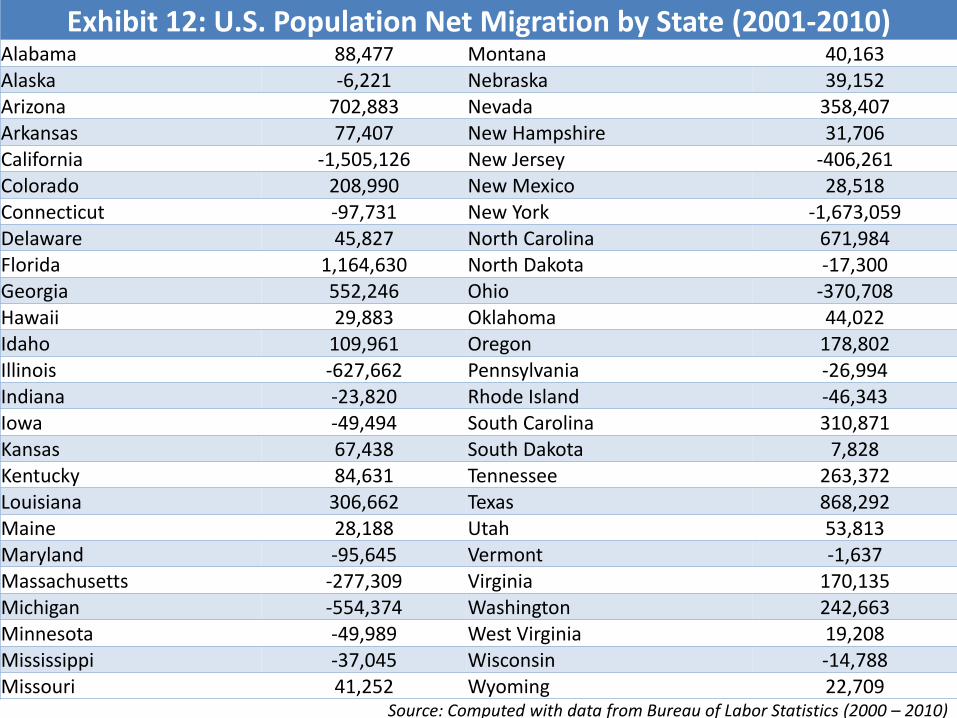

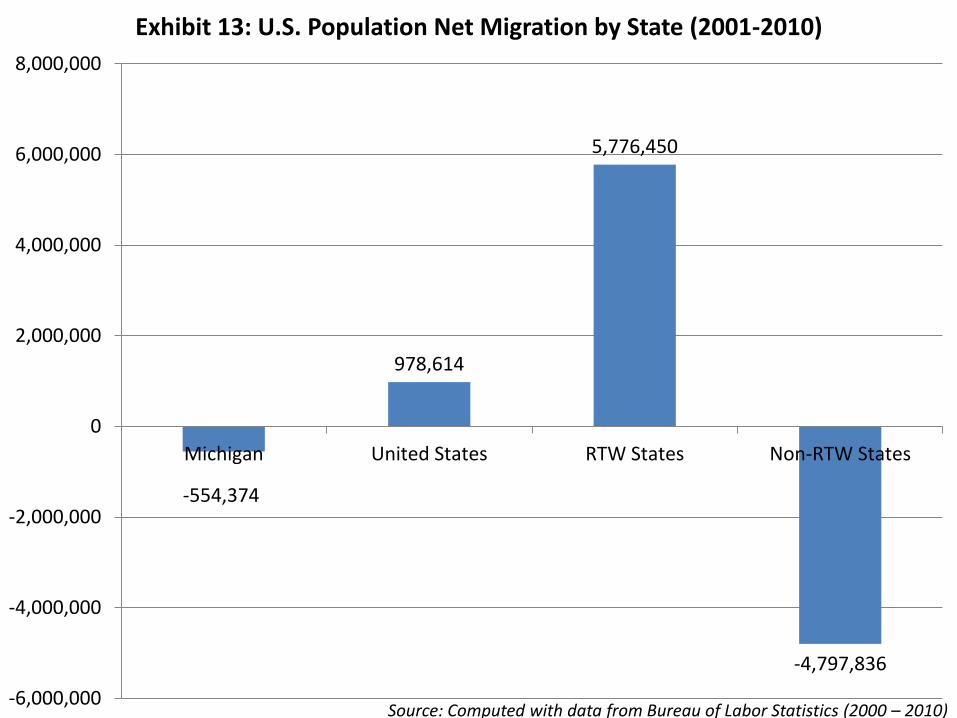

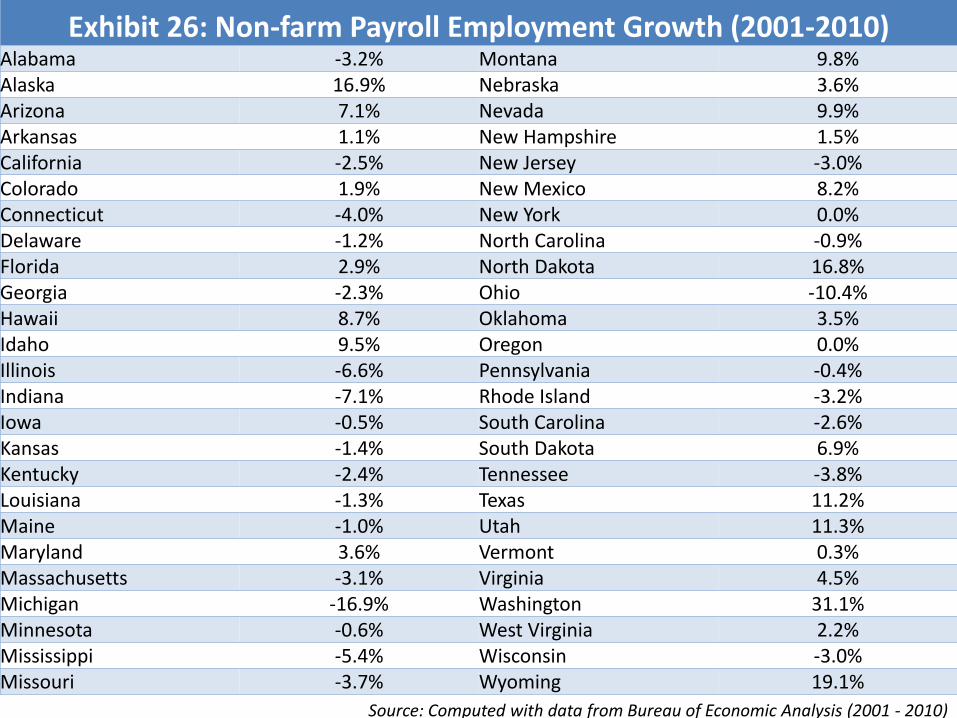

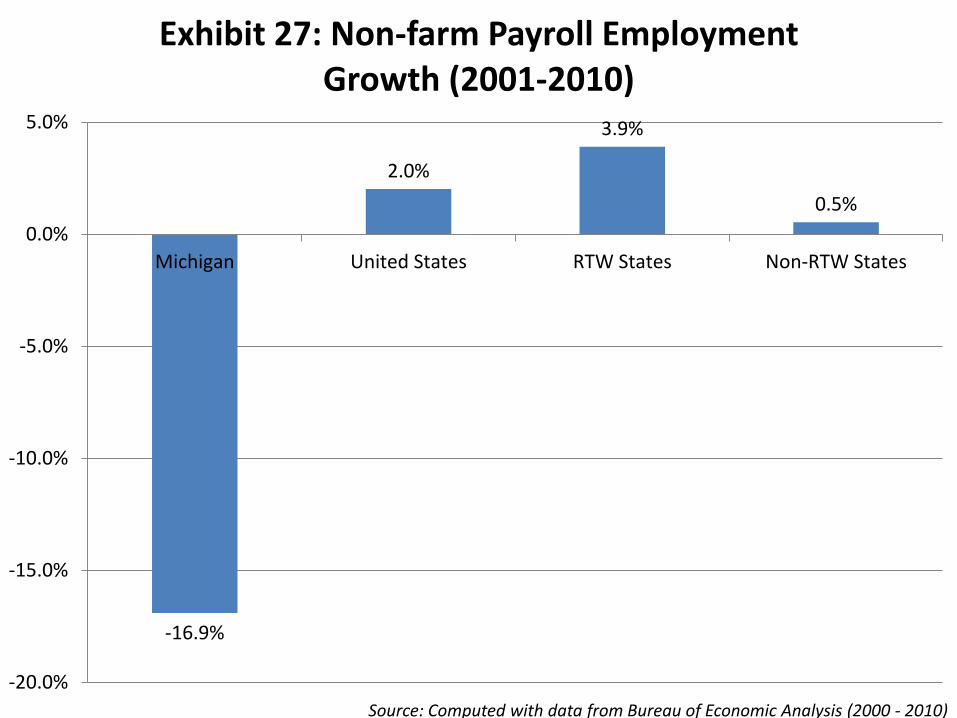

Michigan’s U.S. population net migration from 2000-2010 was among the worst in the United States with a net loss of 554,374 people. Net migration is defined as the difference in people leaving a state relative to people migrating to a state over a given period of time. The overall U.S. population net migration for the same period was just under 1,000,000 people net positive with RTW states experiencing a positive net migration total of just under 6,000,000 and NRTW states suffering a net migration loss of just under 5,000,000 (see Exhibits 12 and 13). During the same period, Michigan Non-Farm Employment growth declined 16.9% while the U.S. overall average grew just 2.0 %. RTW states saw employment growth at just under 4.0 % while NRTW states’ job growth was 0.5 % (see Exhibits 14 and 15).

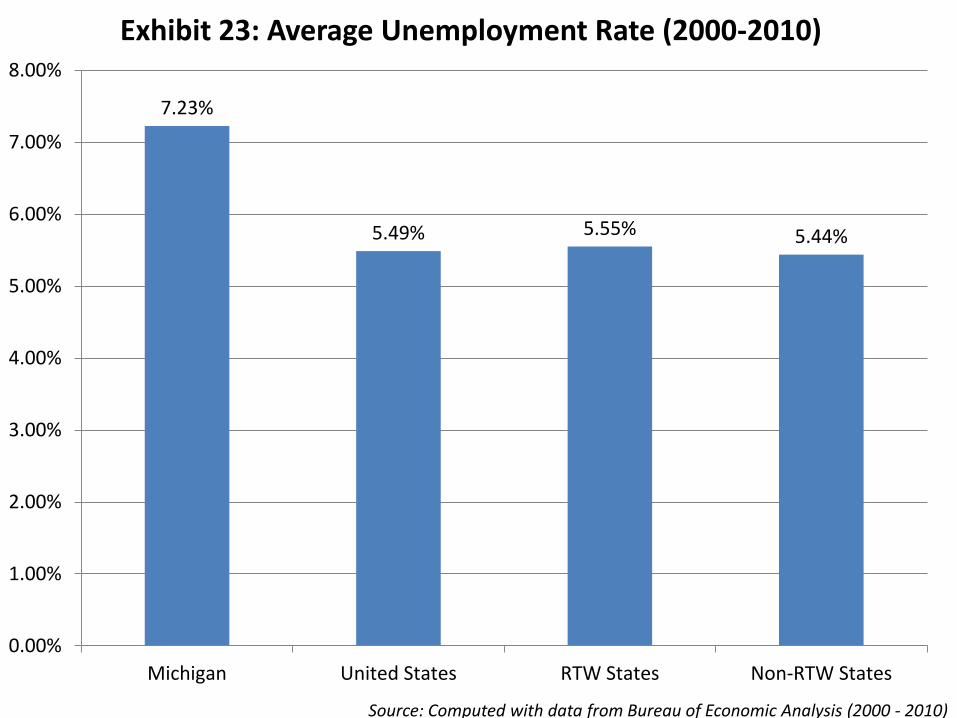

From 1998-2011 Michigan Gross State Product (GSP) lagged the national average significantly. While the U.S. economy grew from an overall Gross Domestic Product (GDP) level of more than $8 trillion in 1998 to just under $15 trillion in 2011 or 71.5 %, the Michigan economy grew by only 26.5 % over the same period. Gross State Product grew at an average rate of 85 % over the same period in RTW states while realizing a slower growth rate in NRTW states of 64.2 % (see Exhibits 16-21). As one should expect, poor growth or negative growth in GSP is generally correlated with higher levels of unemployment. From 2000-10, the average unemployment rate in Michigan was 7.23 % while the average for the United States was 5.49 %. Somewhat surprising is the fact that average unemployment in RTW states was 5.55 % while NRTW states averaged 5.44 % over the same period (see Exhibits 22 and 23).

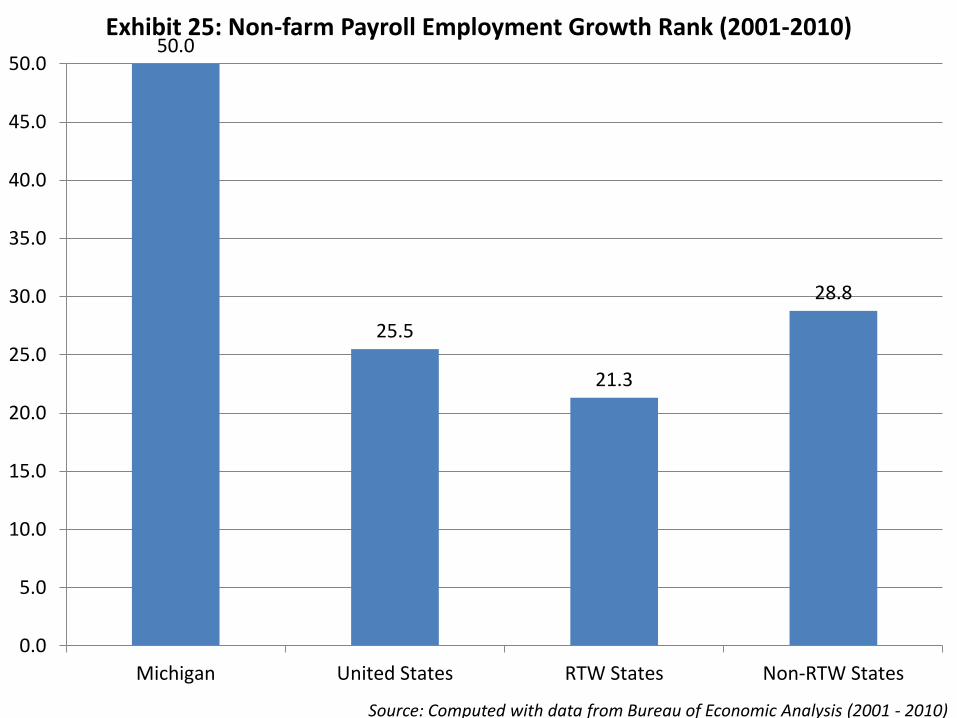

Employment growth in the Non-Farm segment of the U.S. economy from 2000-2010 averaged just 2.0 %, as noted earlier. Michigan’s job creation was negative, ranked dead last out of the fifty states for job growth during this period. The average rank for job growth in RTW states over the same period was 21.3 while the average rate out of 50 states for NRTW states was 28.8 (see Exhibits 24-27). In addition, Michigan was the only state to realize net population loss

6

based on the 2010 U.S. Census. Michigan clearly underperformed versus the U.S. and RTW averages in the areas of economic growth, population, migration, and job creation.

Household Income Growth and Minimum Wage in Michigan and the United States

Personal income per capita growth in Michigan grew 20.3 % from 2000-2010 while the U.S. average income grew at 36.4 % over the same period. Personal income growth over the period grew at just under 40 % in RTW states and at 34.2 % in NRTW states (see Exhibits 28 and 29).

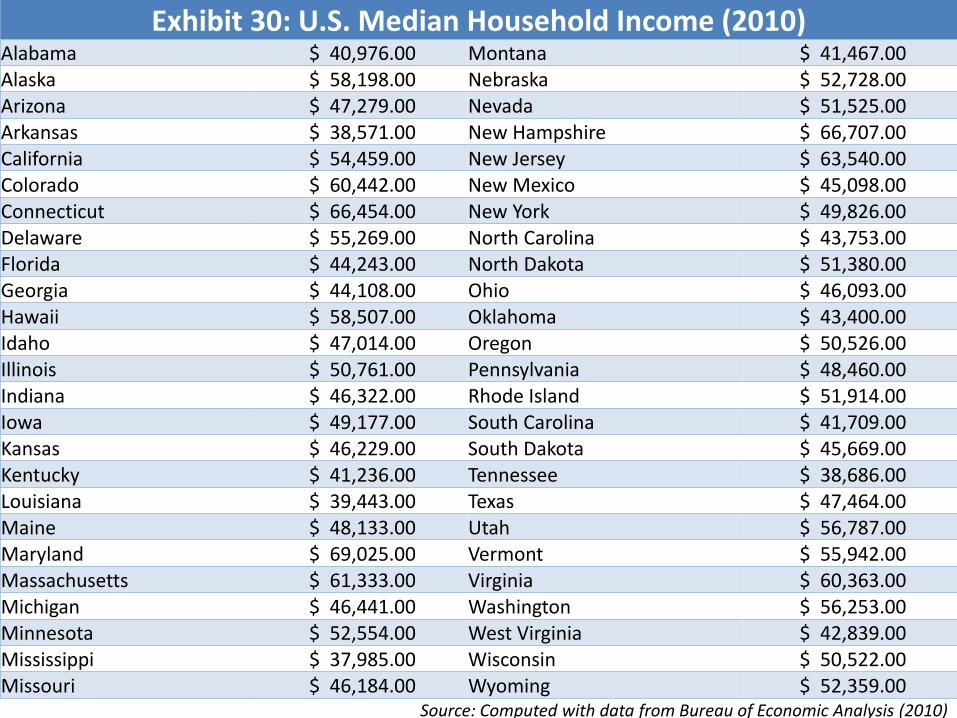

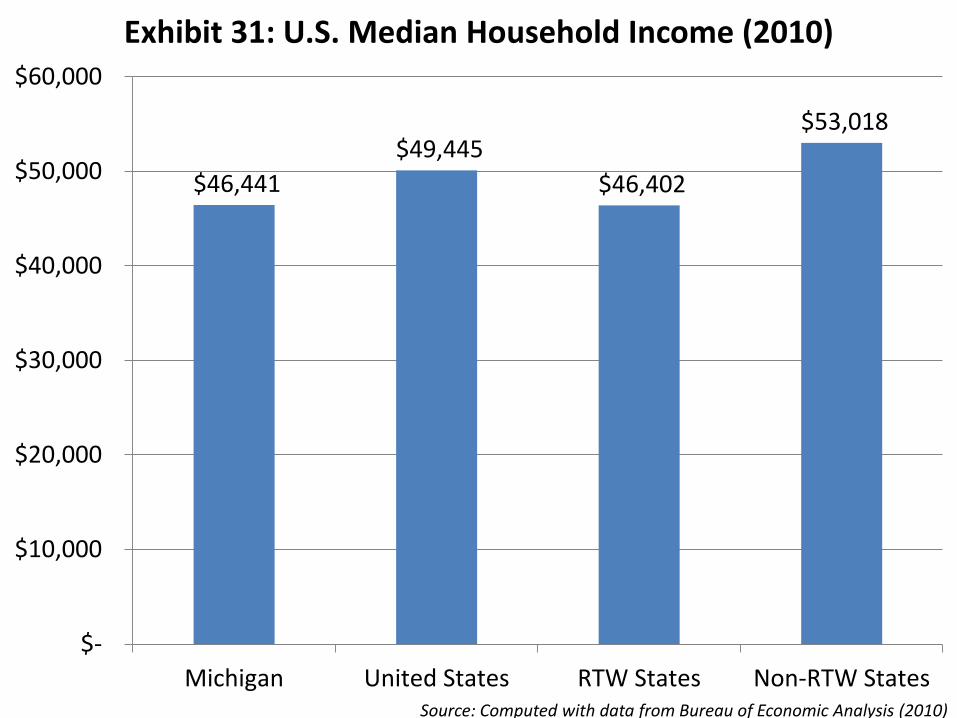

Household income can be measured by median income (generally the parent or parents in the household). Michigan lags the national average while having roughly the same averages as the RTW states. NRTW states have higher average incomes, but the margin is narrowing relative to RTW states due to more rapid income growth and GSP growth in RTW states over the past decade (see Exhibits 30-31).

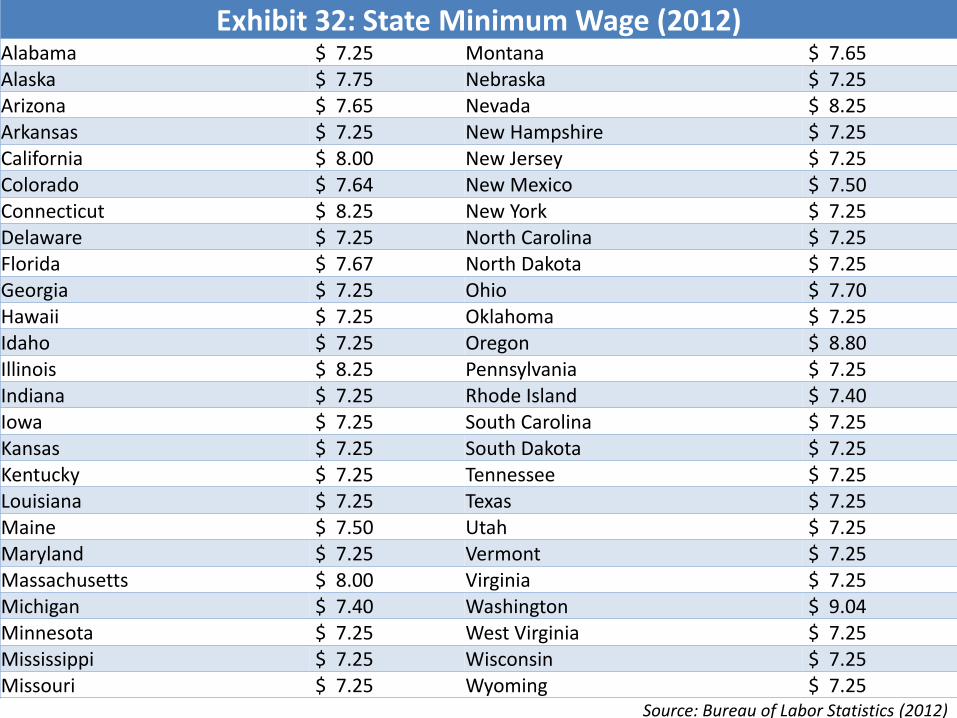

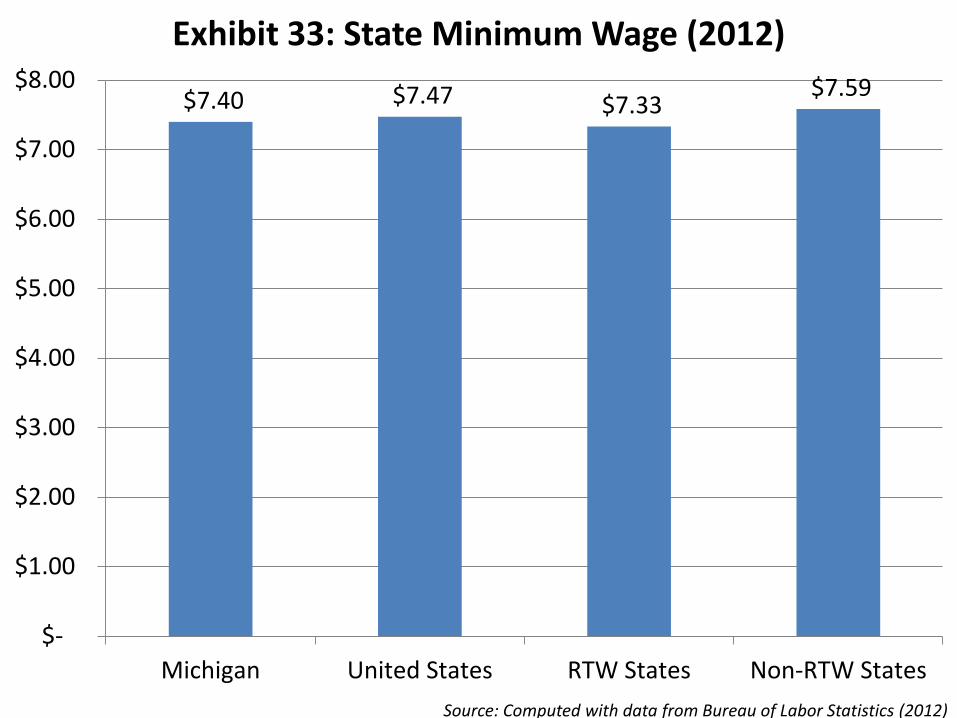

Minimum wage rates are often considered to be a barrier to entry for young and/or unskilled workers who either lack necessary skills or job experience or both. The U.S. federally mandated minimum wage floor is $7.25, thus no state may set their minimum wage below this rate. The Michigan minimum wage for 2012 is $7.40. Michigan is $.07 below the national average and only $.07 above the RTW average. There is a $.26 differential premium between RTW and NRTW states regarding minimum wage rates (see Exhibits 32 and 33).

Assessing the Cost of Government in Michigan and the United States

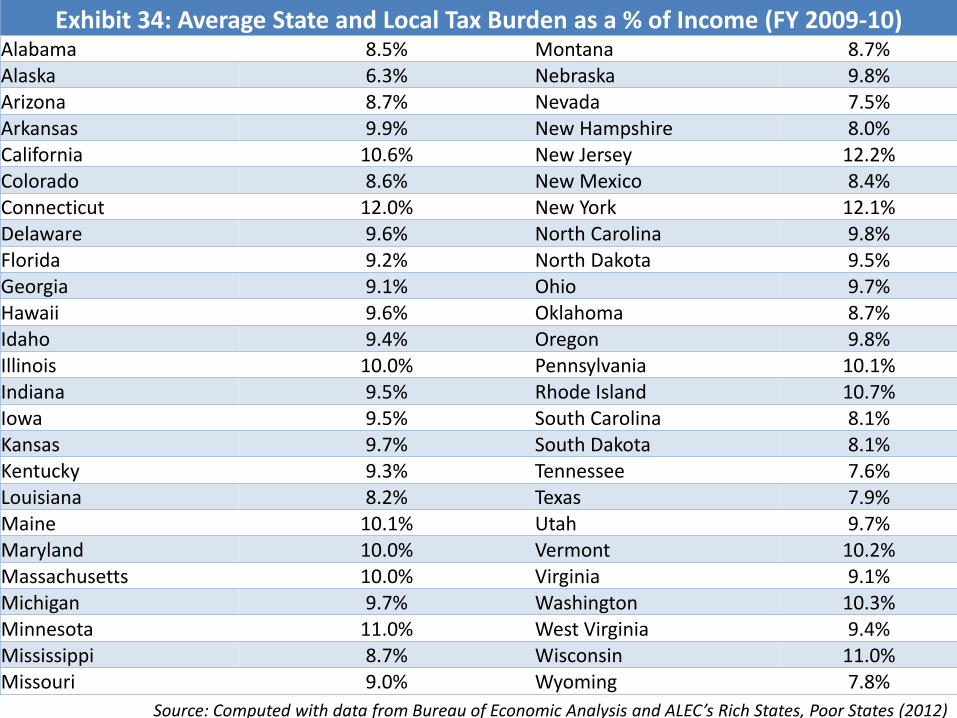

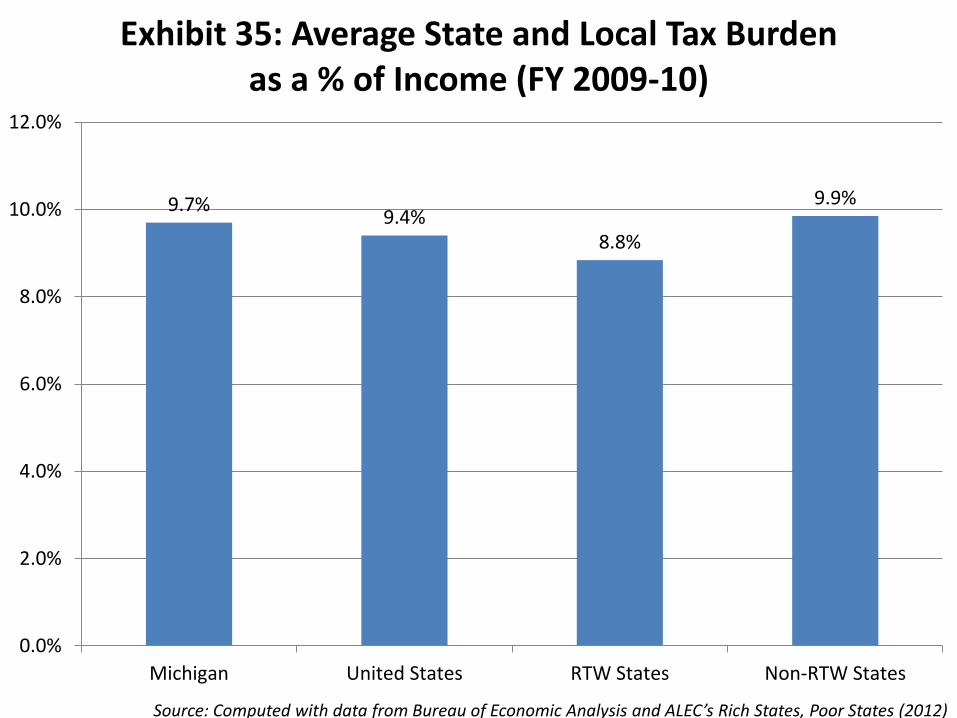

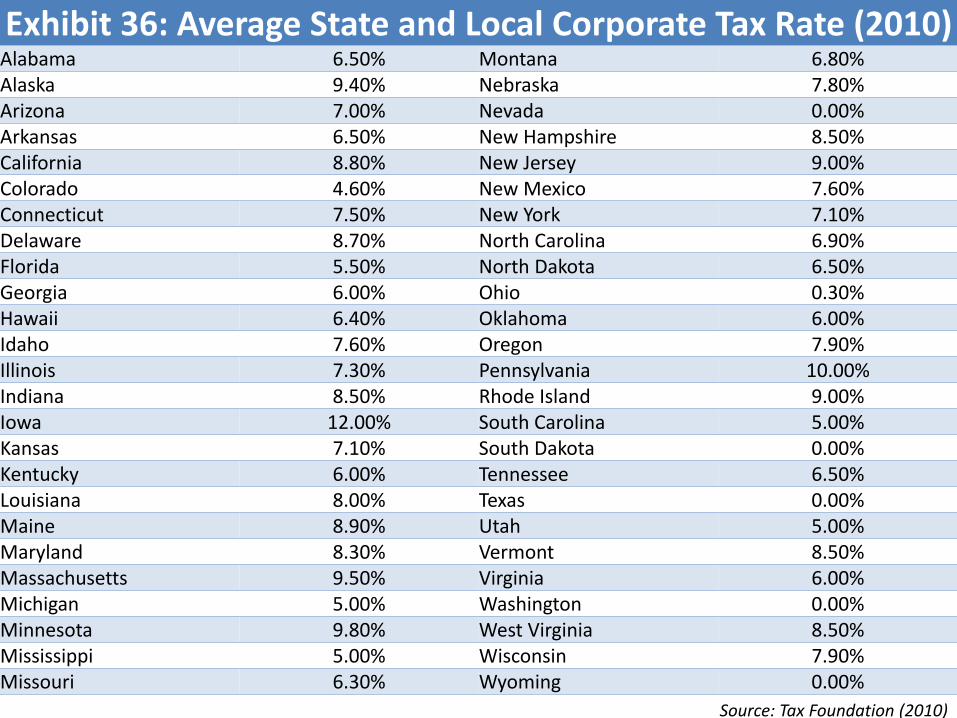

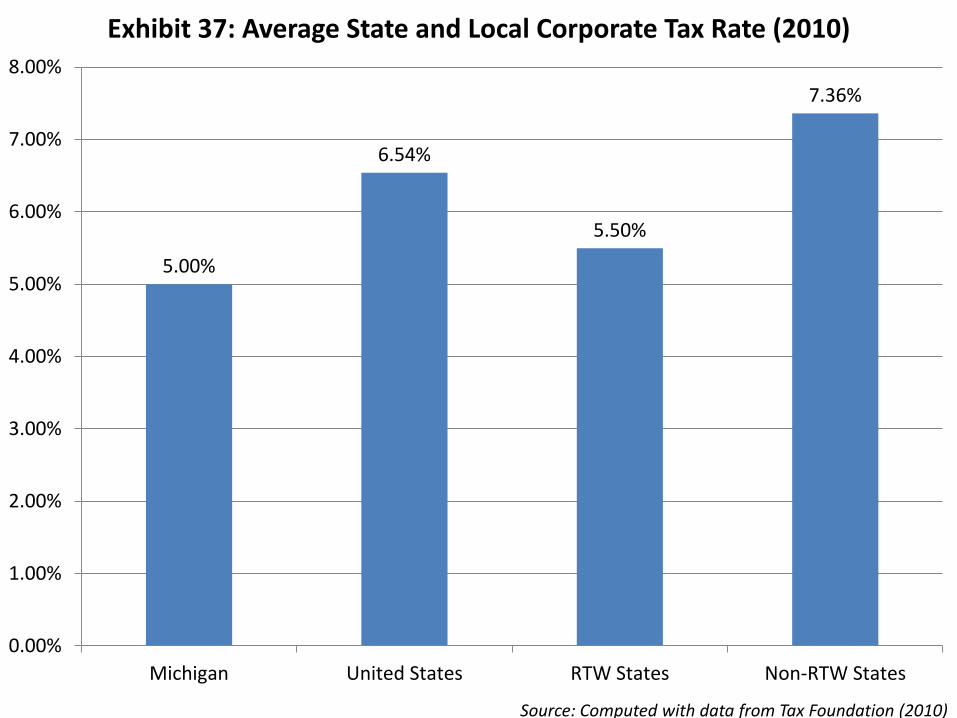

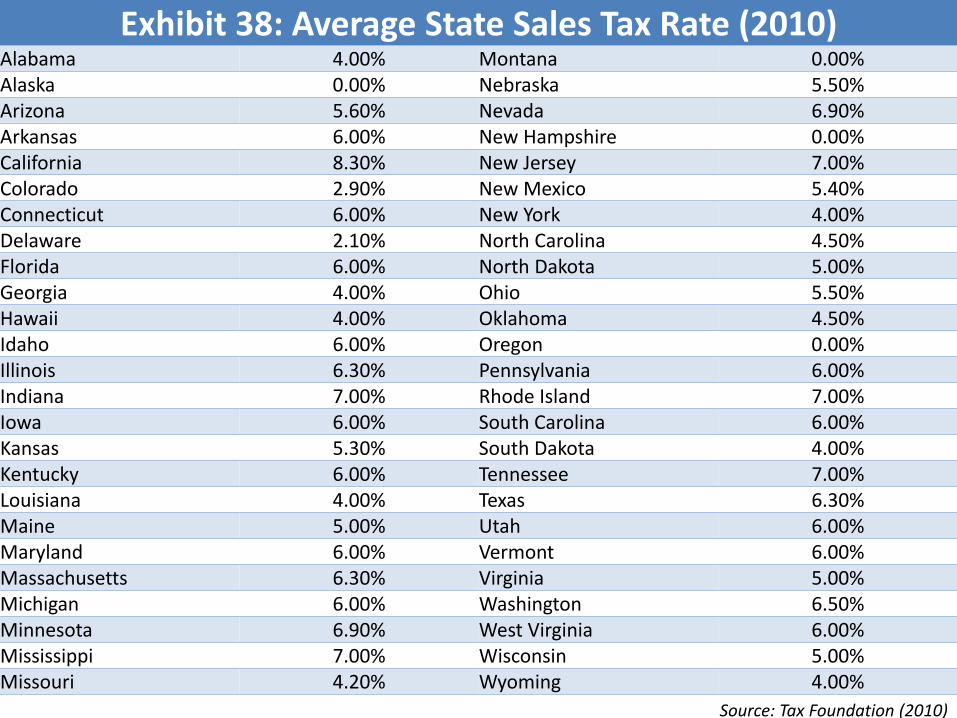

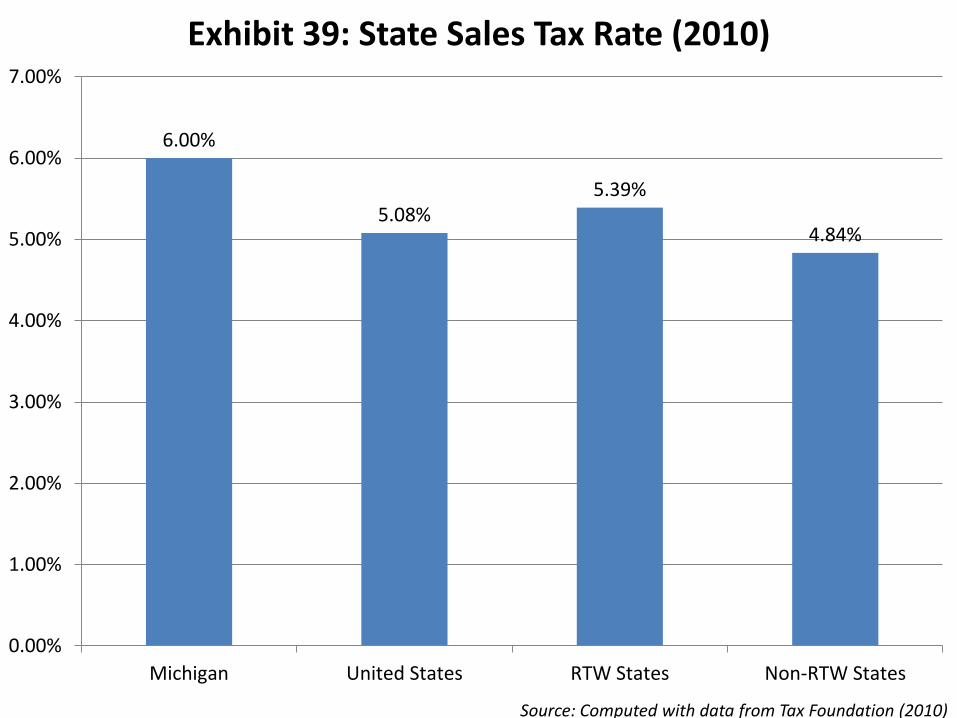

Tax burdens, especially on business, have a generally negative effect on job creation, job growth and in attracting new businesses. The average state and local income tax burden as a % of income in Michigan in 2010 was 9.7 % with the U.S. average at 9.4 %. The average in RTW states was 8.8 % while the average in NRTW states was 9.9 %, more than a full point higher (see Exhibits 34 and 35). The average combined state and local tax rate on corporations in Michigan in 2010 was 5 % (see Exhibit 36-41).

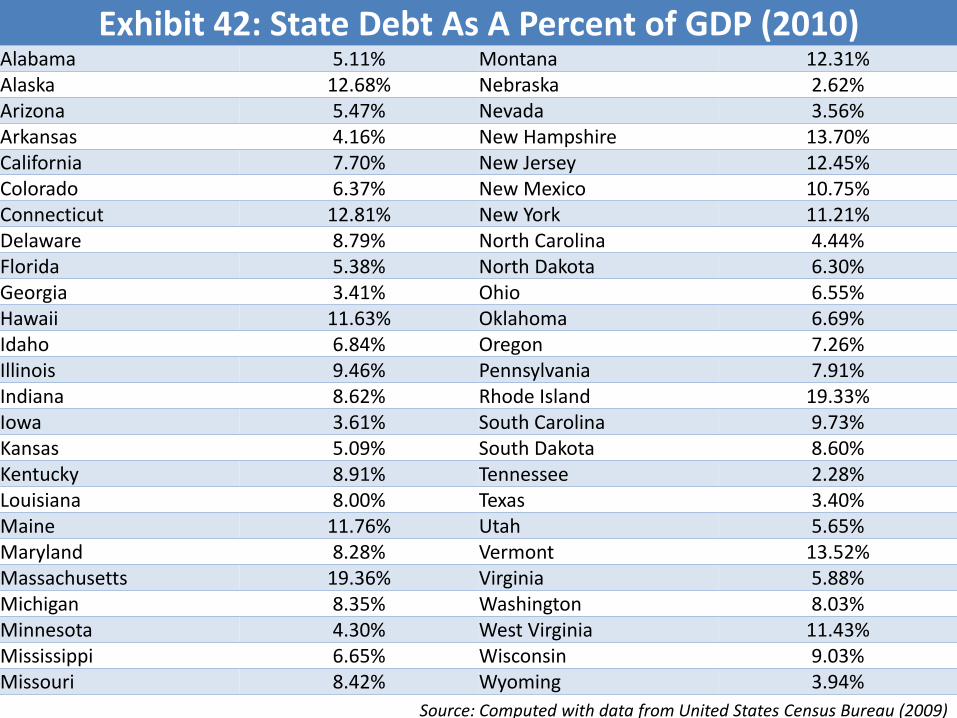

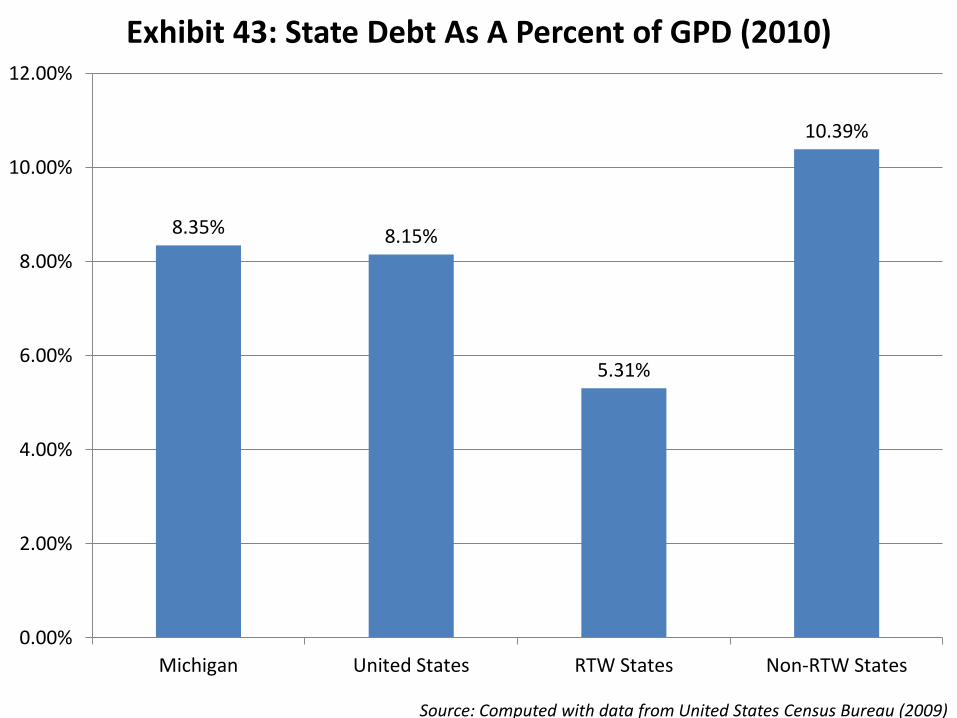

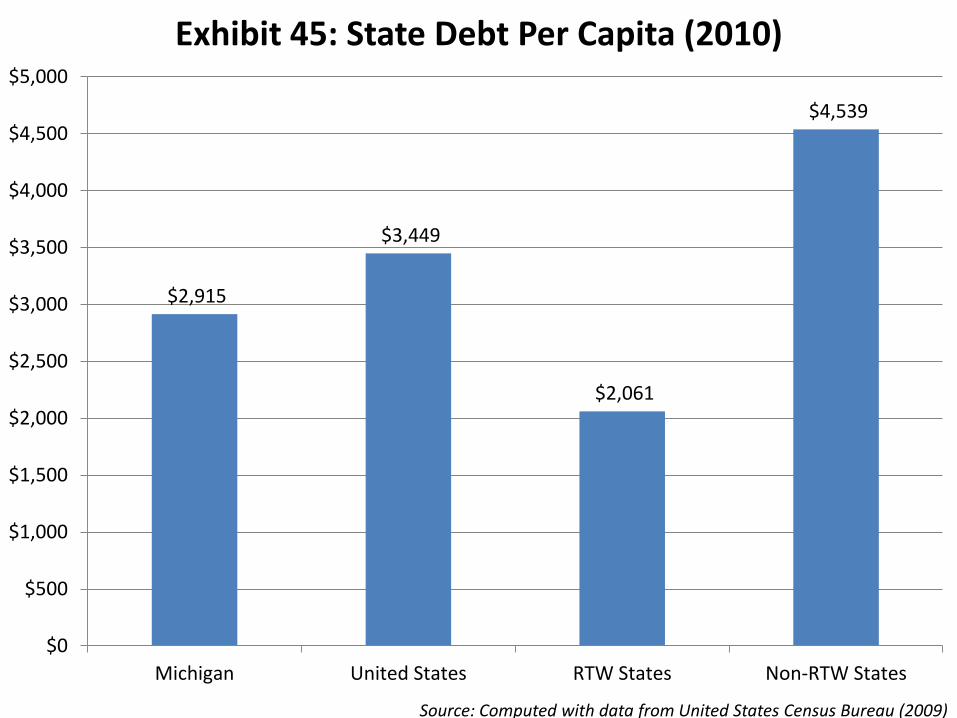

Like the federal government and many other states, Michigan’s state debt as a % of Michigan Gross State Product (GSP) is a problem and is slightly above the national average of 8.35% of GSP. This compares to 5.31 % on average in RTW states and 10.39 % in NRTW states (see Exhibits 42 and 43). State debt per capita in Michigan is relatively low compared to NRTW states at $2,915 per capita, with the U.S. average at $3,449 and the NRTW state average at $4539 . However, the RTW average is considerably lower at $2,061 (see Exhibit 44 and 45). In examining state debt as a % of tax revenue, Michigan fared well with the national average at

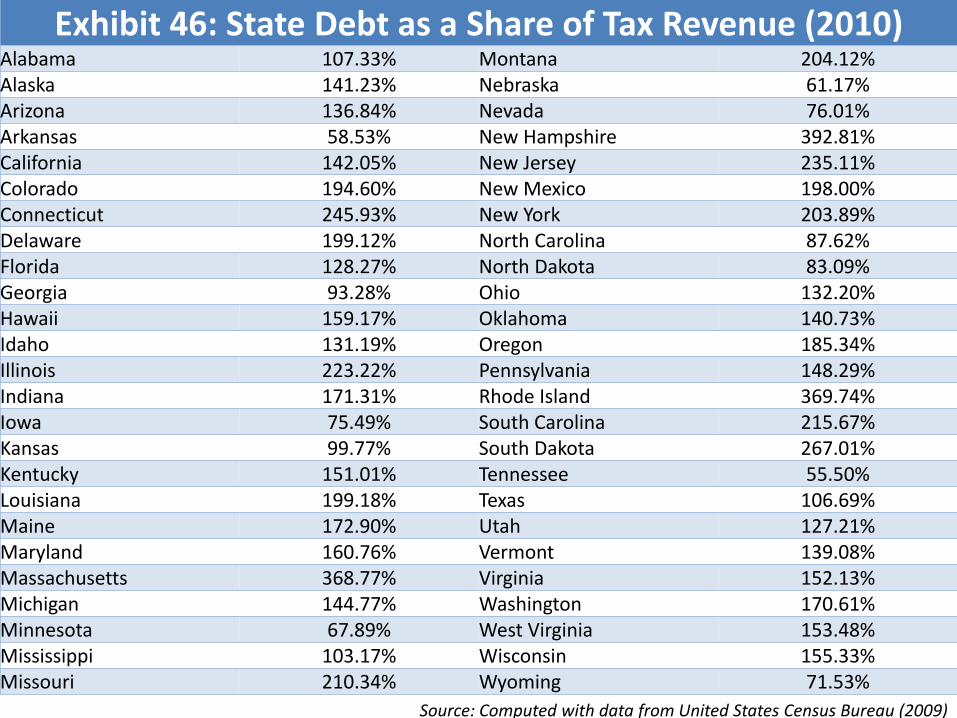

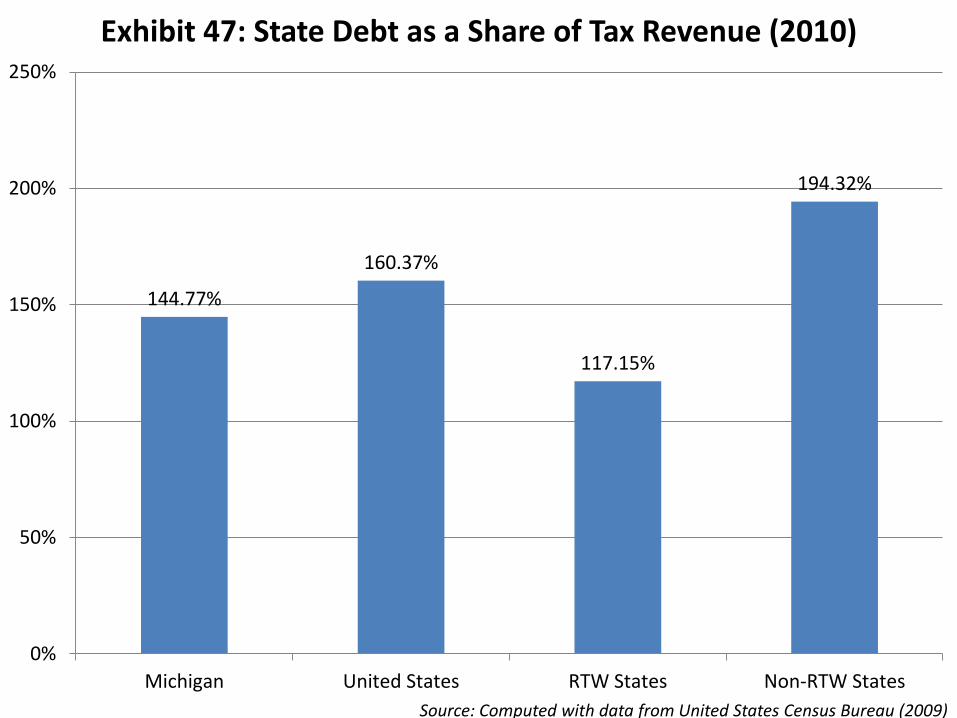

7

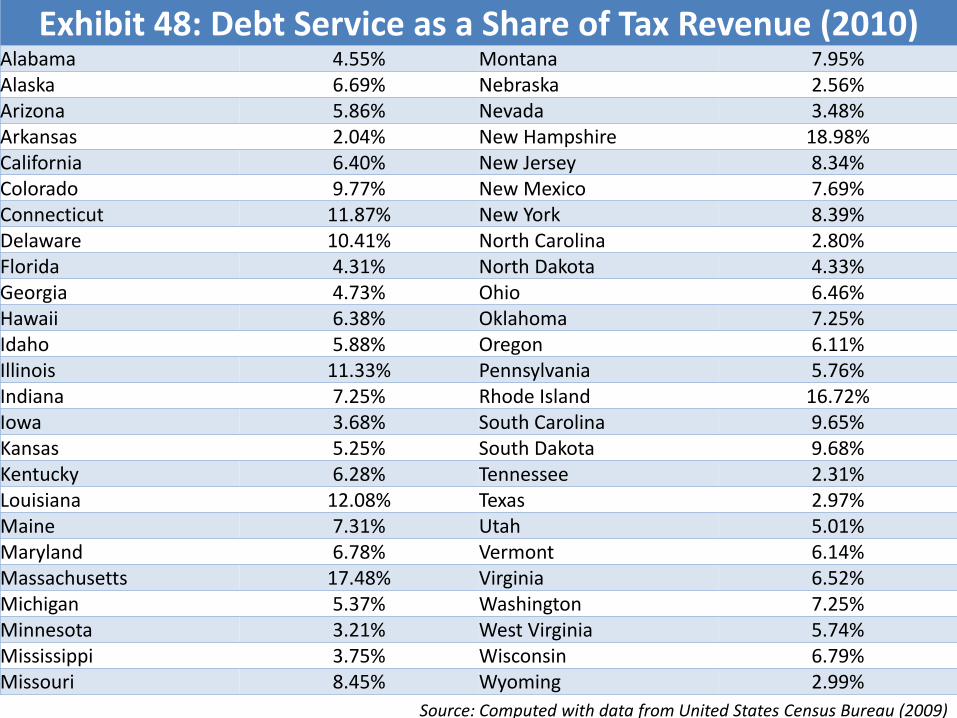

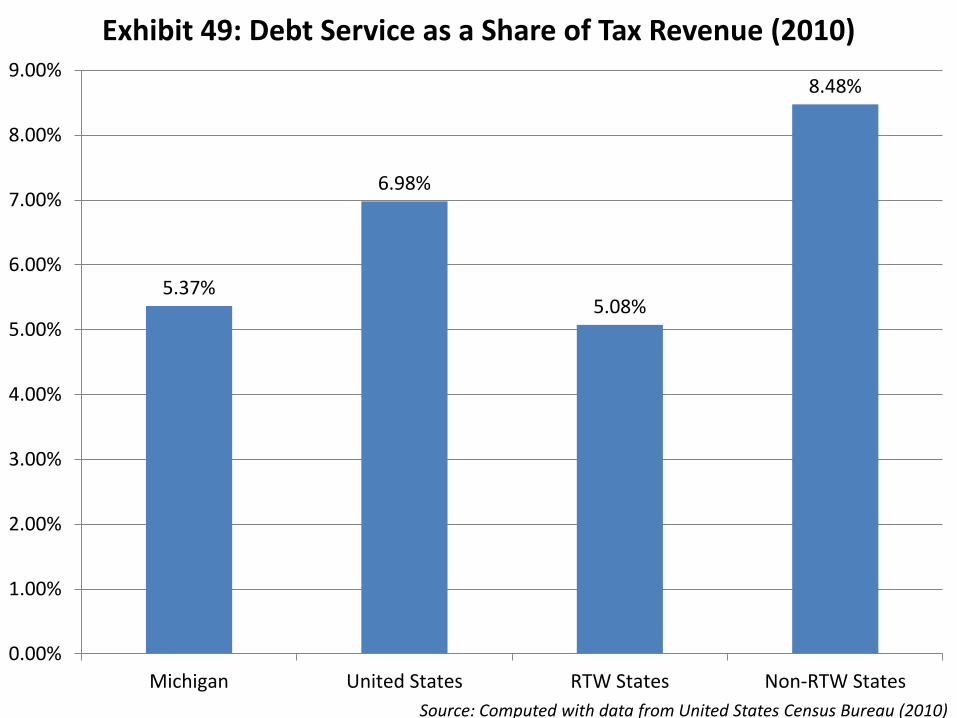

160.37 % and the Michigan average at 144.77 %, while RTW states’ state debt as a share of tax revenue was just over 117.15 % and NRTW states average 194.32 % (see Exhibits 46 and 47). Michigan’s debt service as a share of GDP tax revenue is also below the national average at 5.37 % and below the RTW average at 5.08 % (see Exhibits 48 and 49).

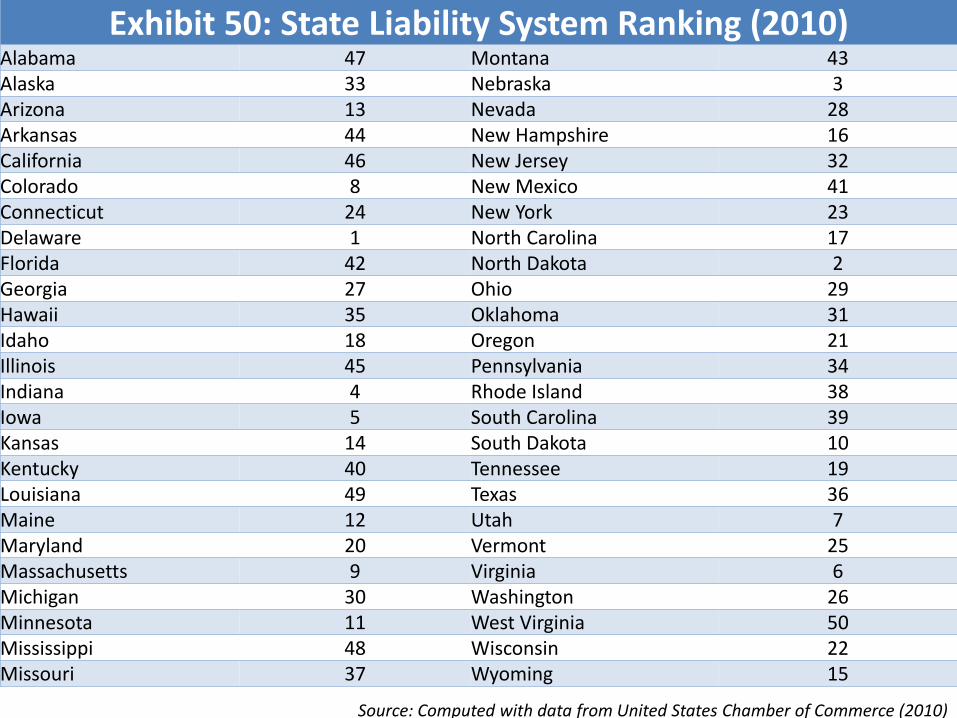

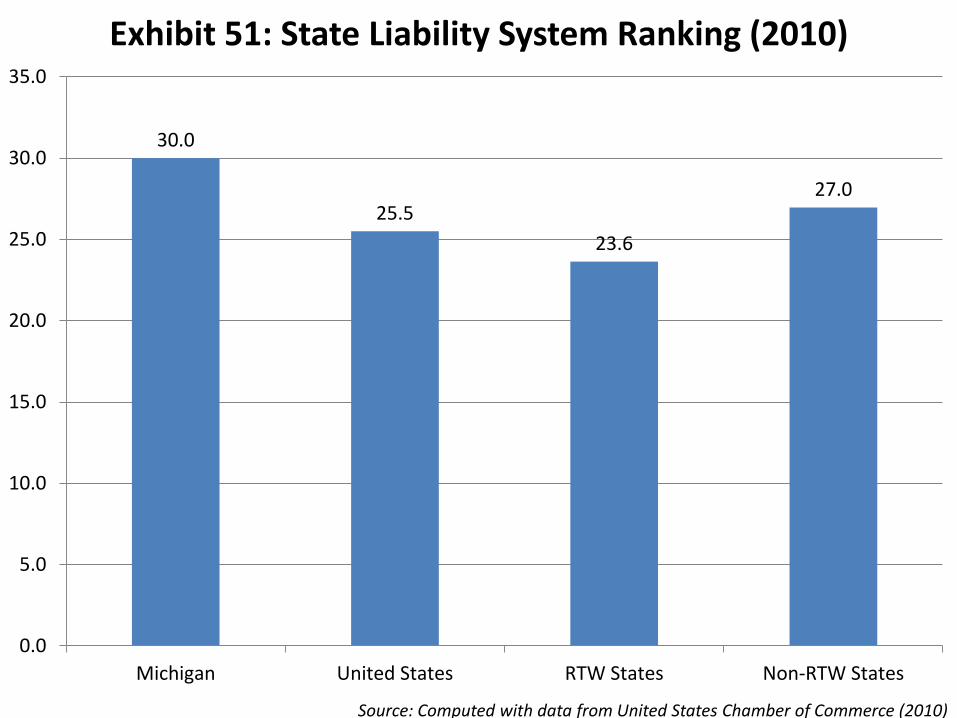

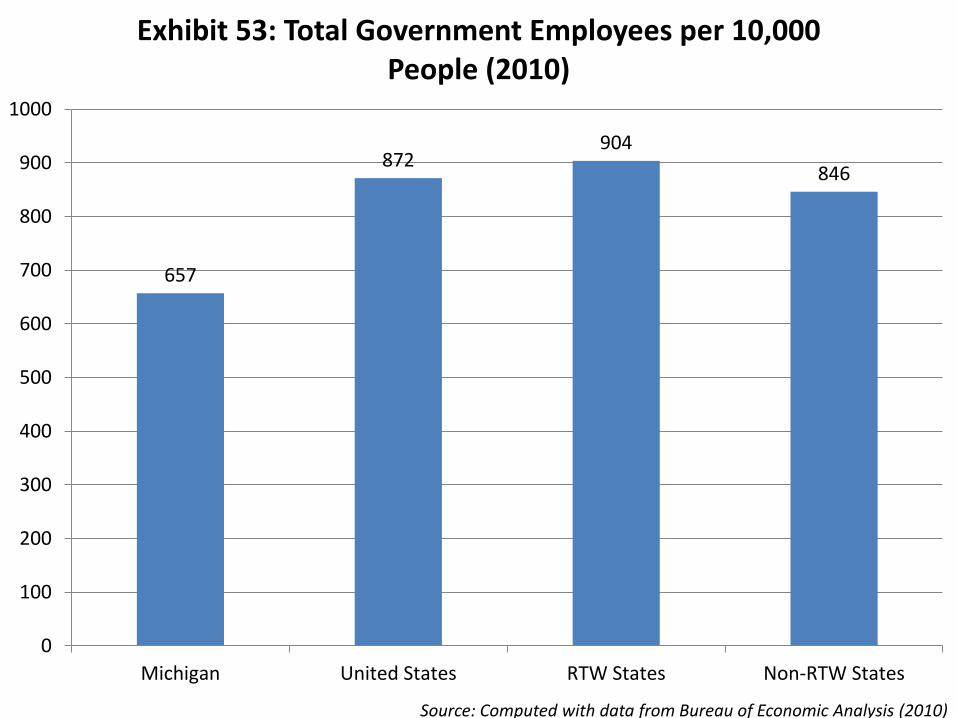

Michigan’s state liability ranking is 30 out of 50 with RTW states average rank at 23.6 and NRTW states at 27 (see Exhibits 50 and 51). The effects of a challenging economy in Michigan have caused the state to see a reduction in the number of government employees at all levels over the past decade (citation). As of 2010 Michigan has 657 government employees per 10,000 people, ranking it fourth lowest in the country (see Exhibits 52 and 53). Looking at state and local government employees alone, Michigan ranks among the ten leanest-government states in the country (see Exhibits 54 and 55).

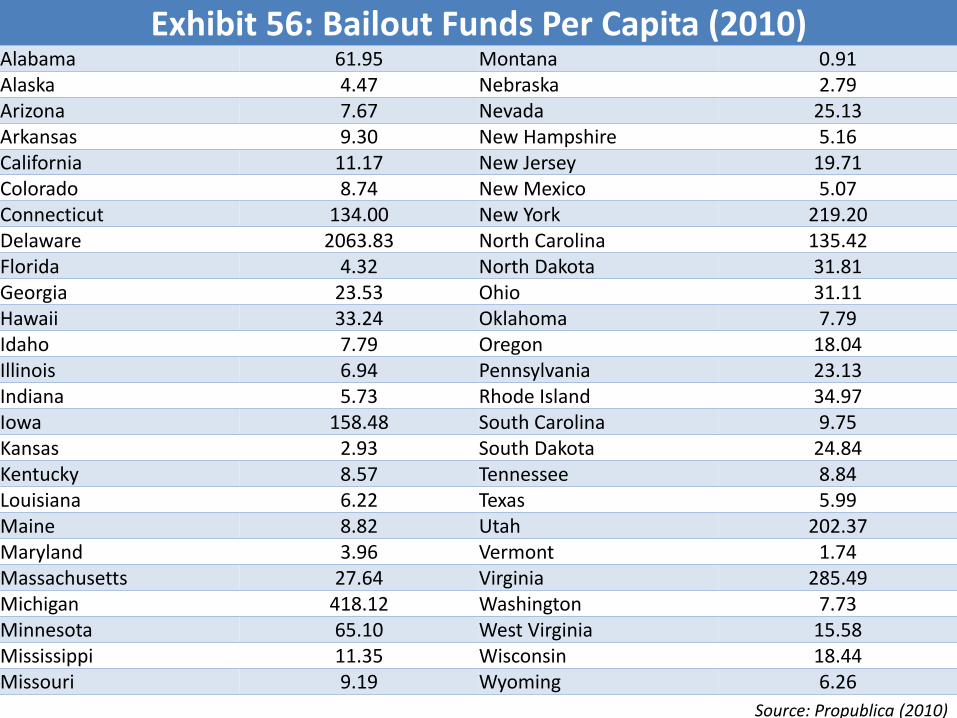

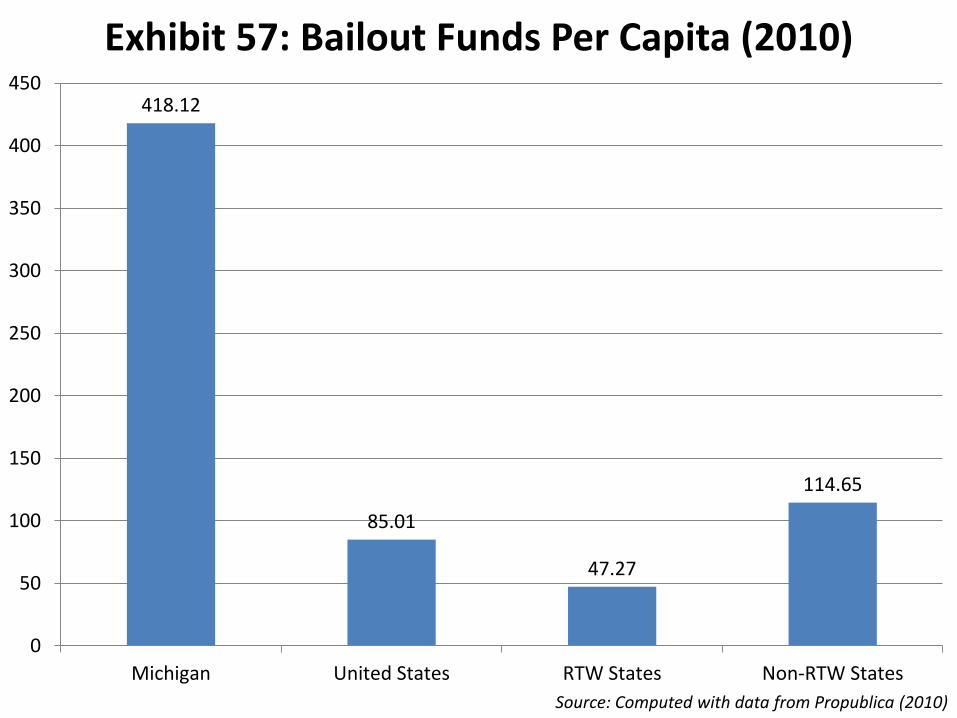

Government operating efficiencies notwithstanding, Michigan received the highest level of federal bailout funds per capita associated with the financial crisis of 2008-2009. It can be argued that without said funds, the economic downturn in Michigan and in the U.S. automobile industry would have been dramatically worse, yet many debate the long-term effect the bailout will have on the competitiveness of both Michigan and the U.S. automobile industry (see Exhibits 56 and 57).

Cost of Key Goods and Services in Michigan and Nationally

The cost of doing business in Michigan is high by a number of key metrics. The median price for an automobile insurance policy in Michigan is the highest in the country, according to a recent study released by CarInsuranceQuotes.com (Johnson, 2012). The median average in Michigan is $4,490 while the national average is just under $1,700. The RTW average is $1,580 while the NRTW average is just under $1,750. Because Michigan requires long term catastrophic care as a part of its no fault coverage, the cost figures out to be 8 % of household family income to purchase insurance. Massachusetts is the best bargain at 1.43 % of household family income (see Exhibits 58-61).

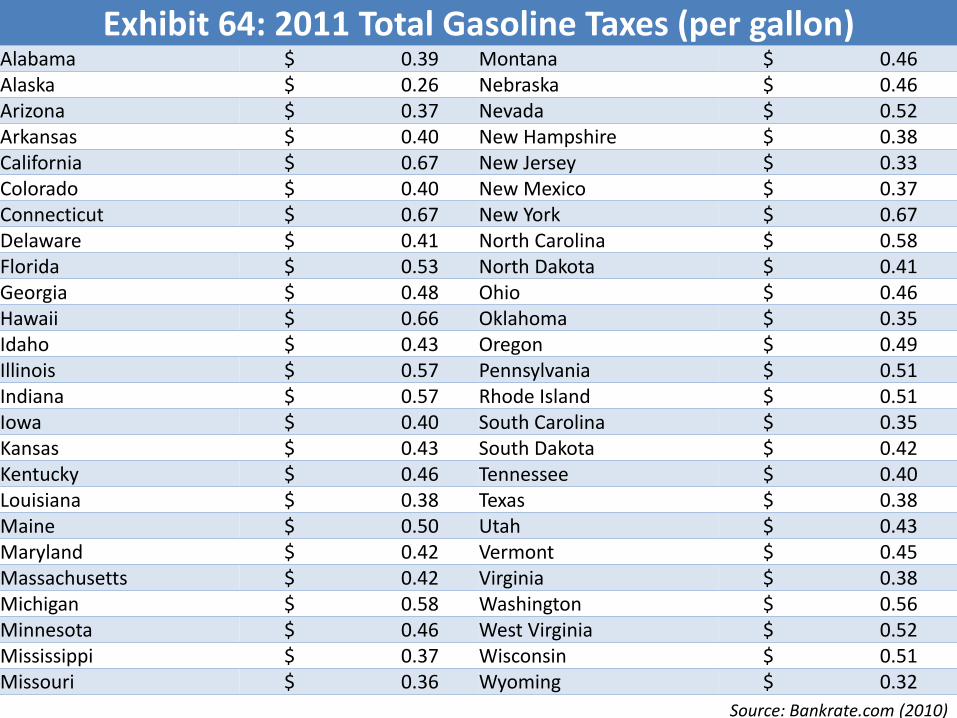

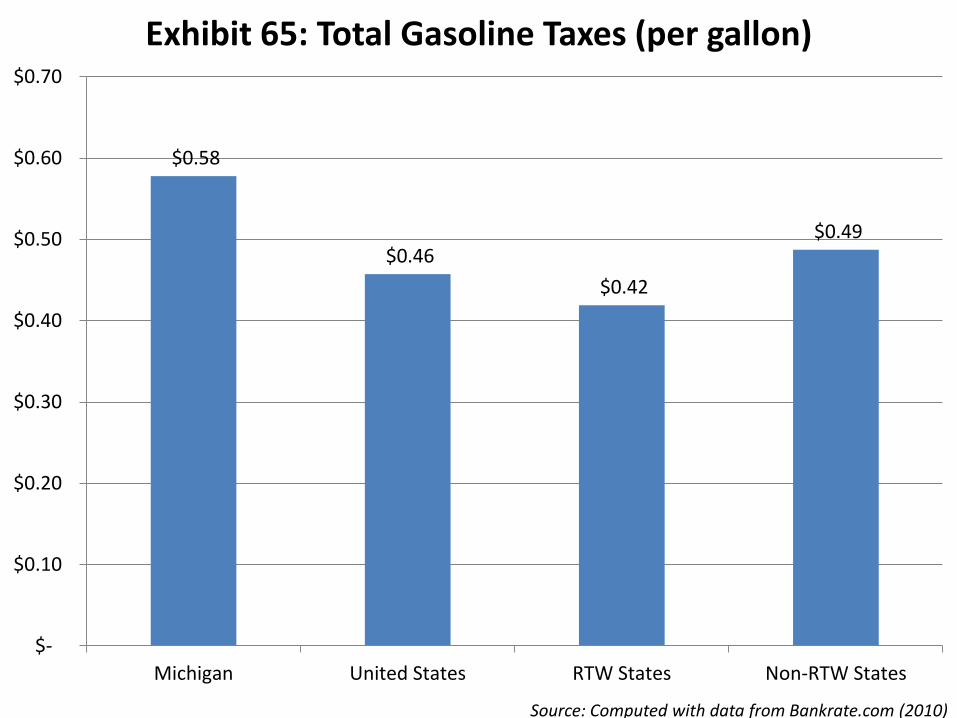

Michigan seems to be very competitive in the area of average cost of electricity, but not natural gas per unit or gasoline taxes. It was below the national average for electricity as well as below the RTW average price for electricity per unit in 2010. However, in 2012 Michigan’s gasoline tax is well above the national, NTRW, and RTW state averages with the fourth highest total gasoline tax in the nation. Moreover, the RTW average for natural gas was below the national, NRTW, and Michigan averages in all three natural gas categories studied for 2010 (see Exhibits 62-71).

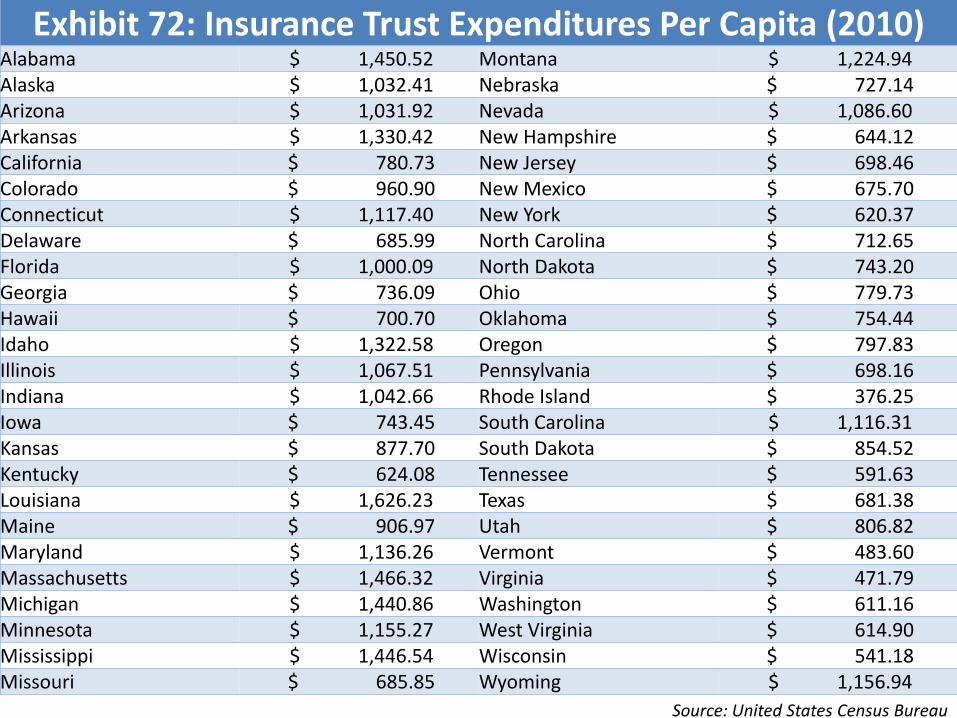

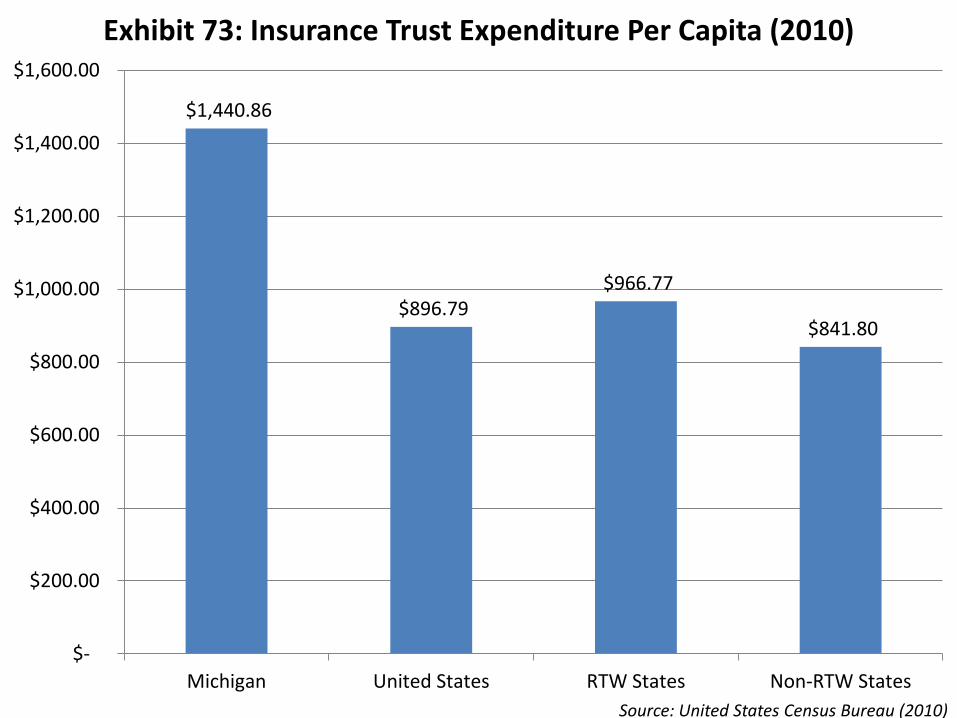

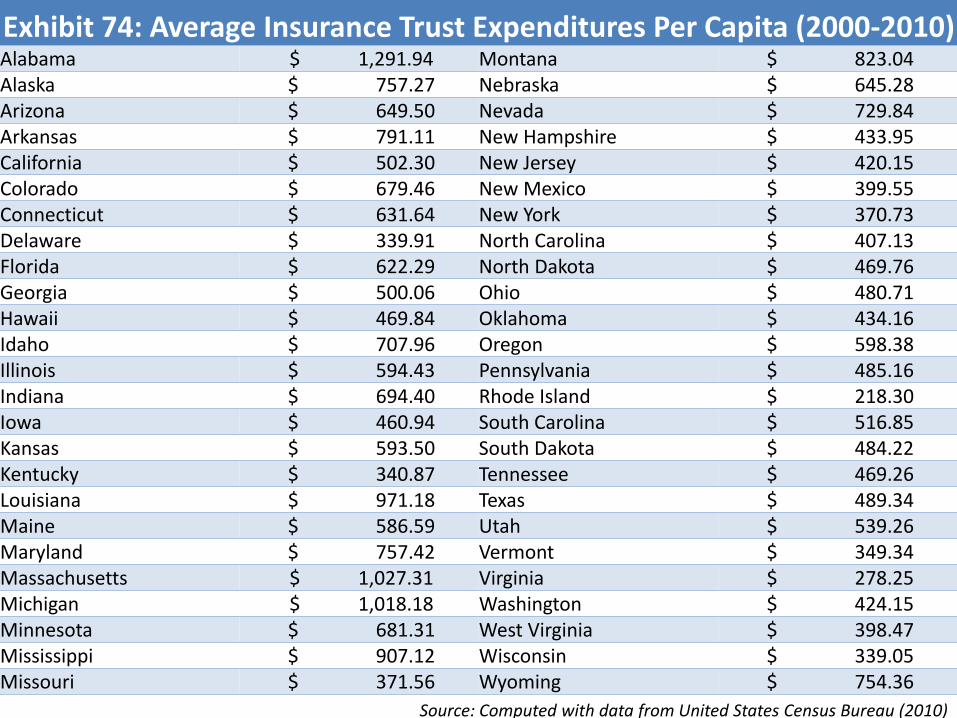

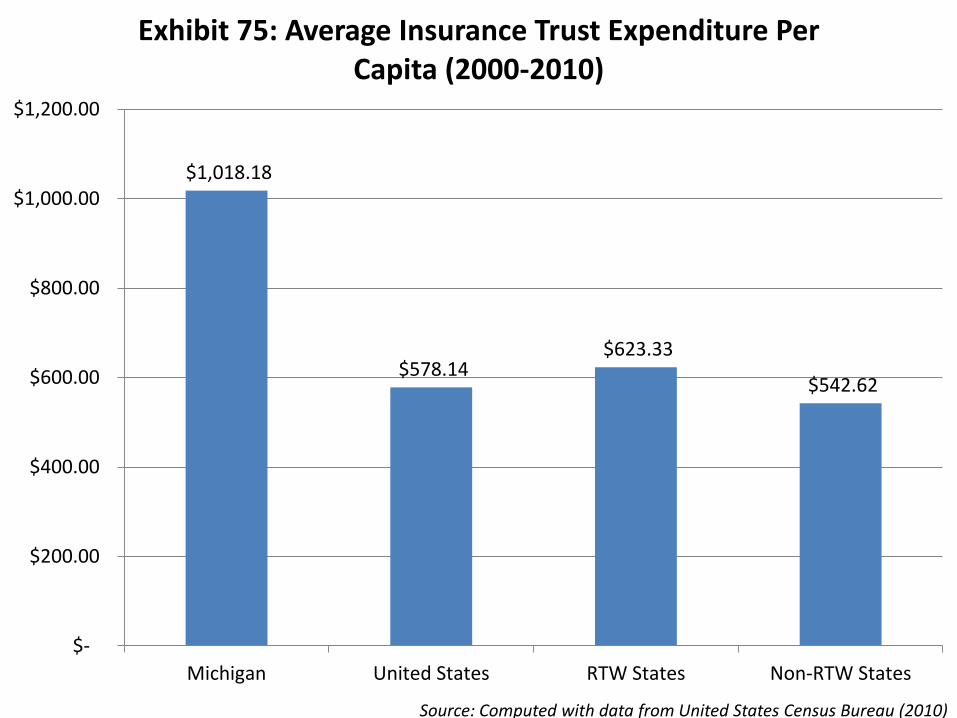

8

Finally, the average insurance trust expenditure in Michigan was among the highest in the country at $1,018.18 per capita in 2010. The national average was less than $600 while the RTW cost was above the NRTW level, which was a rare occurrence in this study (see Exhibits 72-75).

Competitiveness Metrics in Michigan and the United States

In this section a number of measurement tools related to the business environment and business competitiveness of a state and the subsequent rankings are compiled. They are broken-down to compare Michigan with RTW and NRTW states.

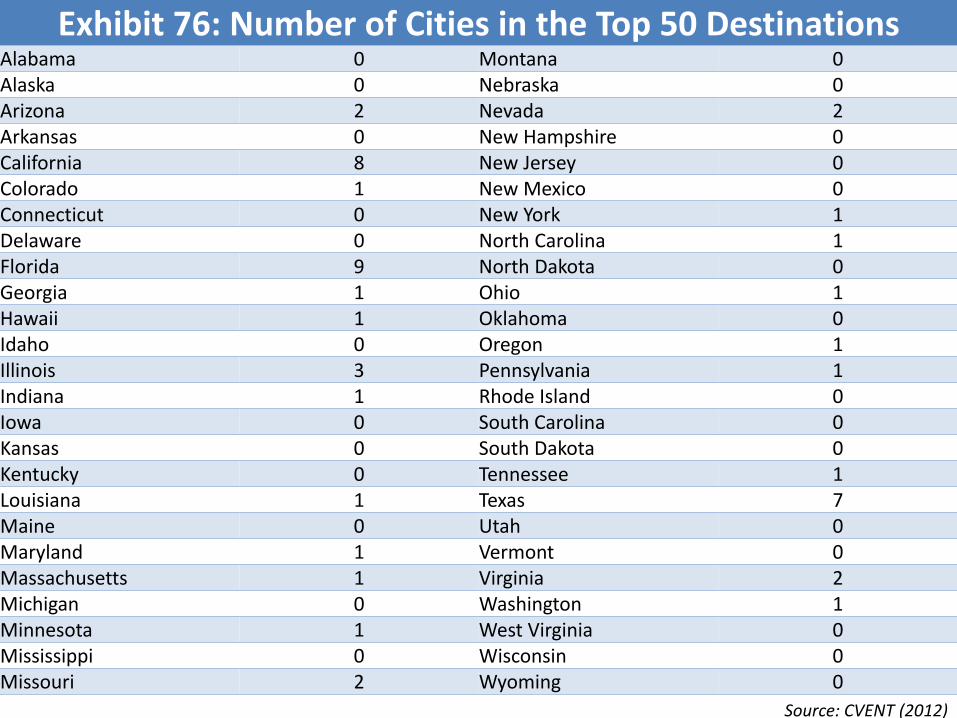

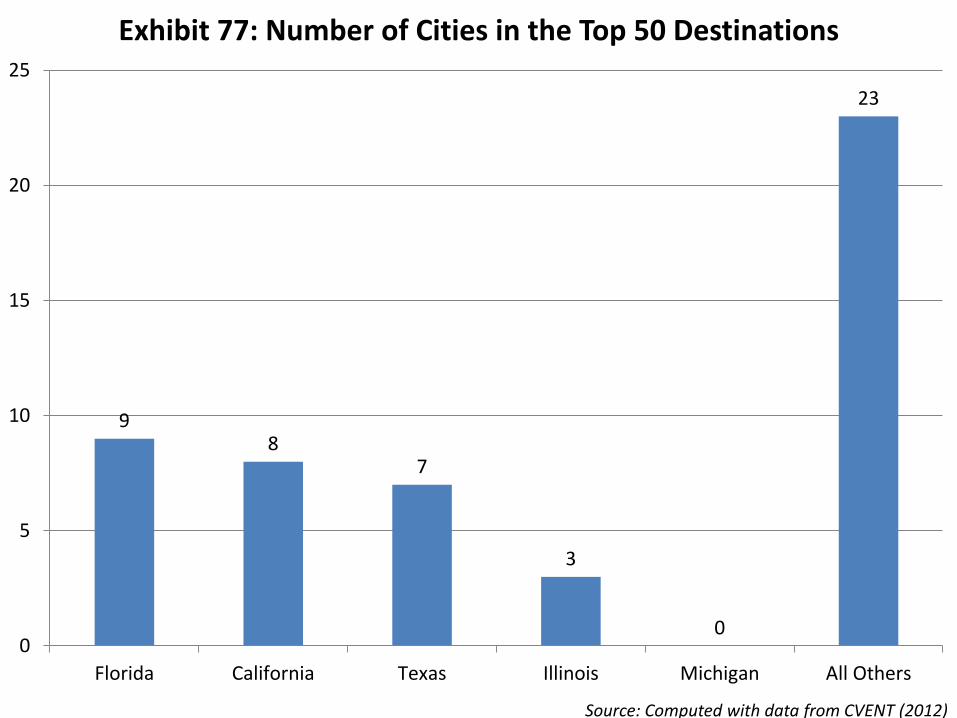

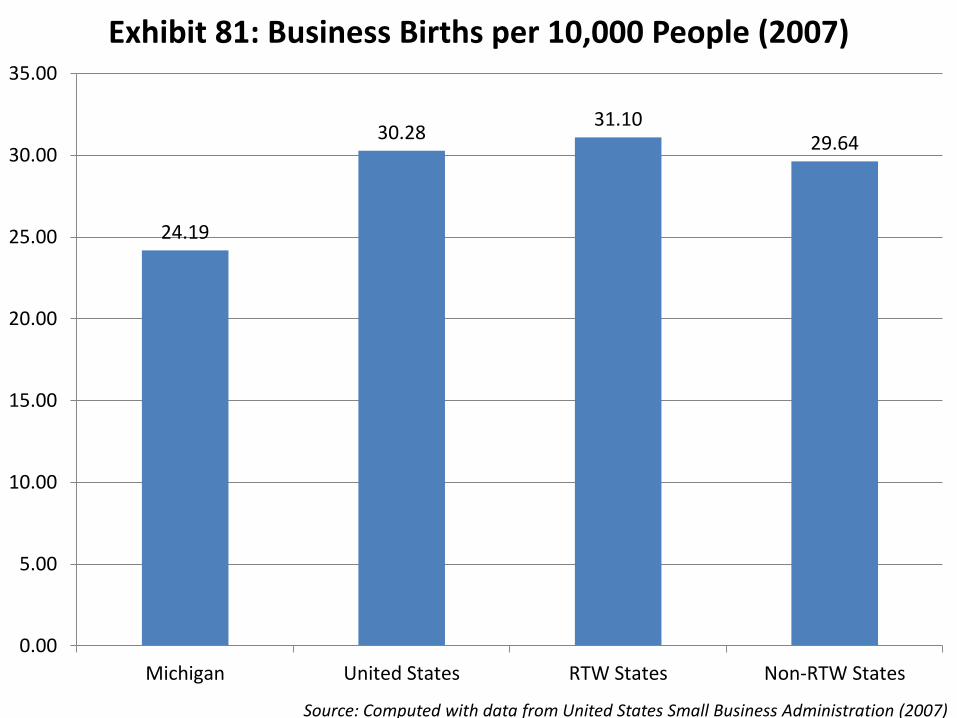

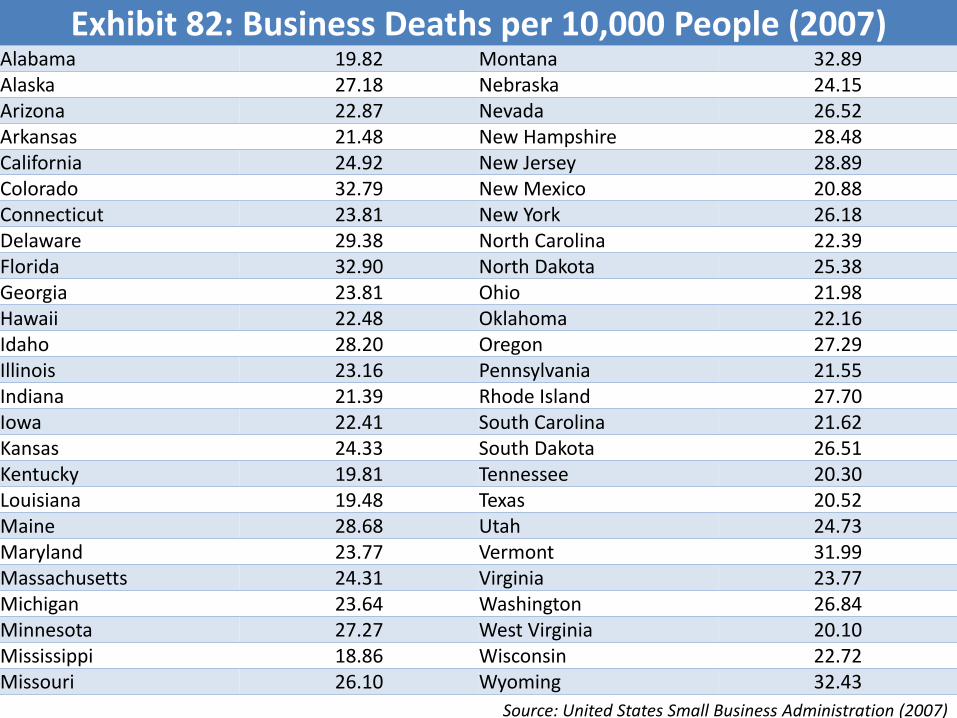

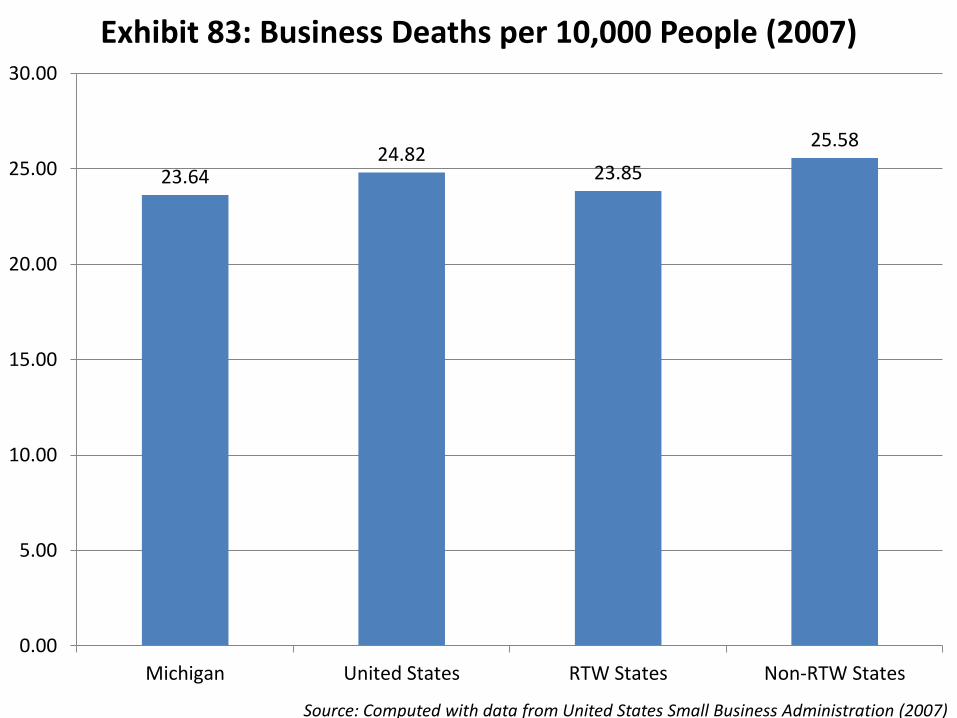

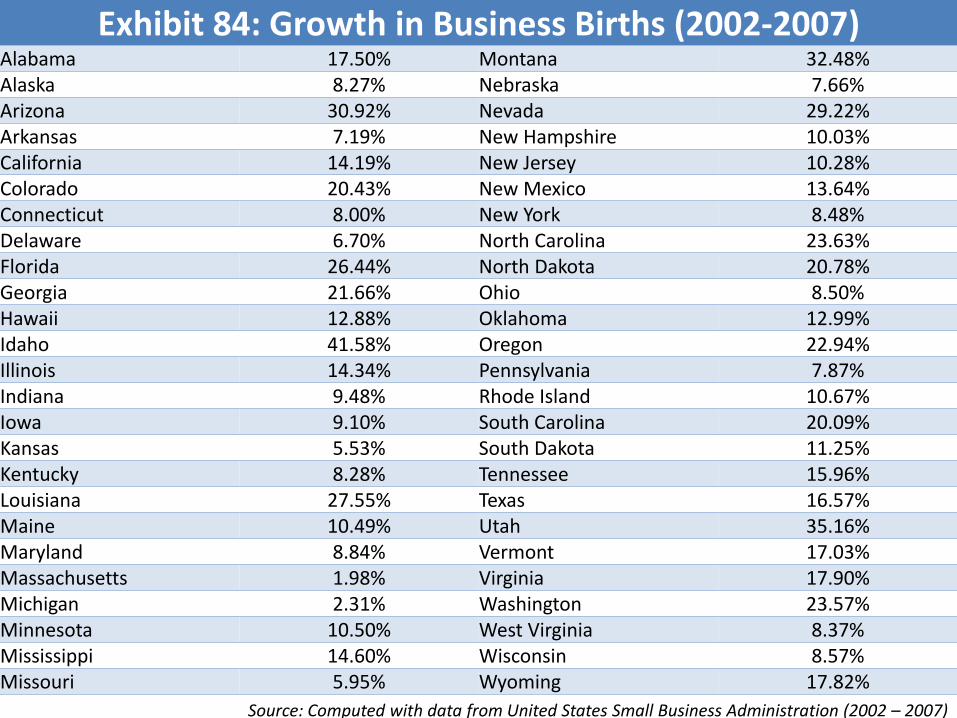

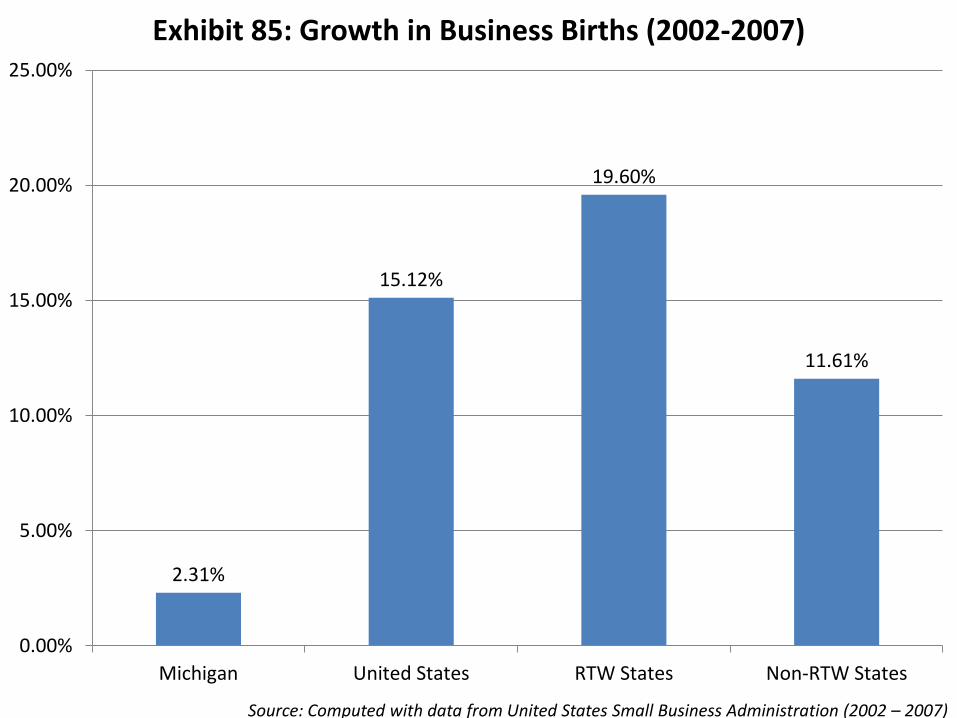

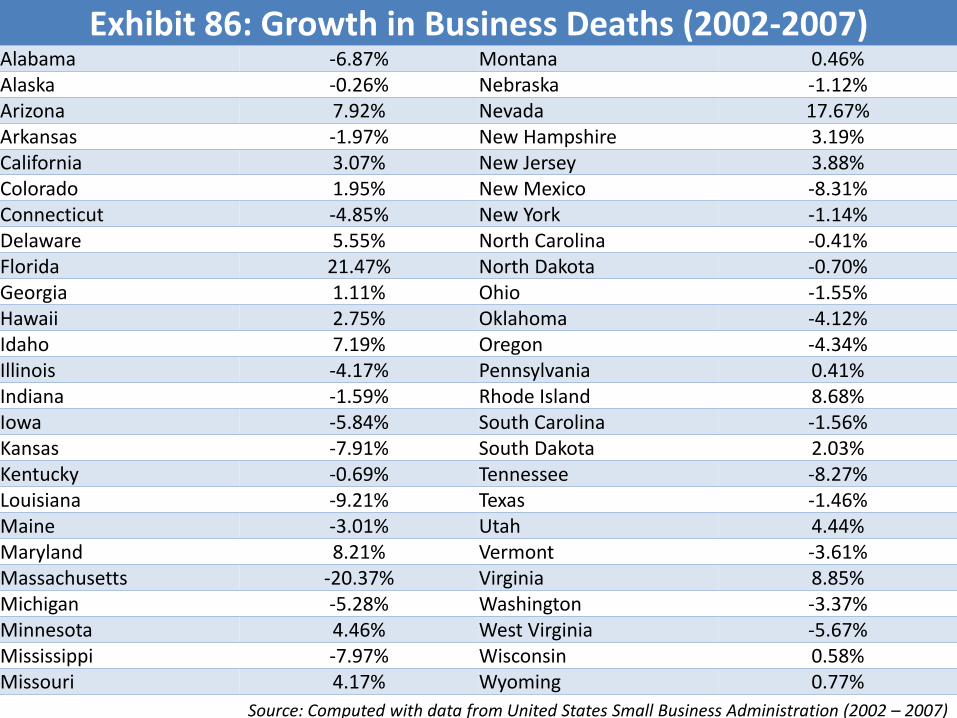

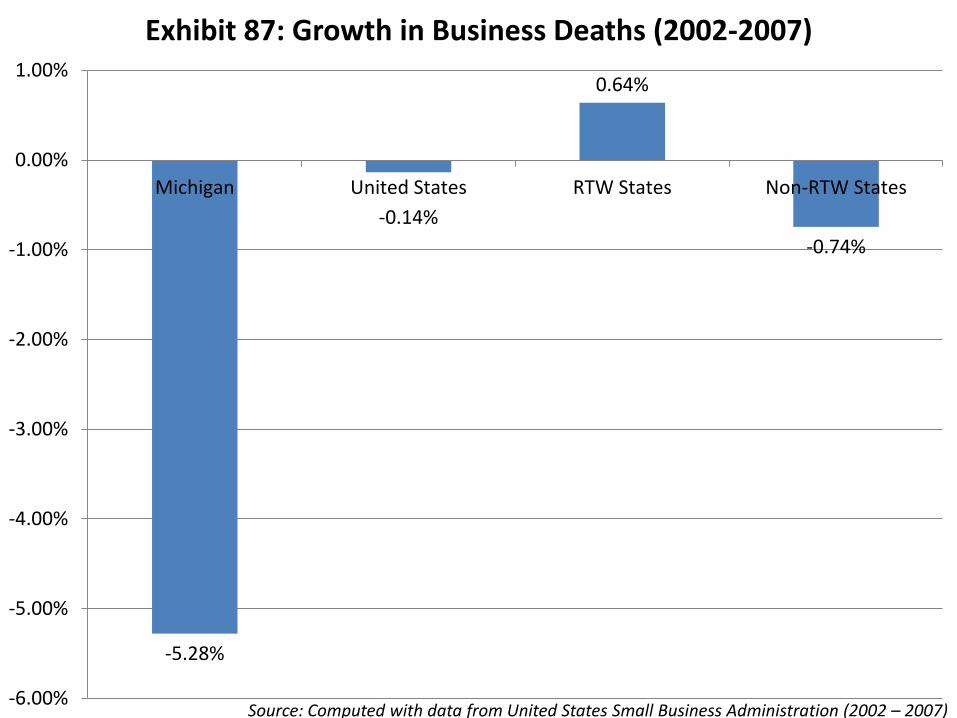

A study by hospitality marketing research firm Cvent noted the top 50 cities for meetings and conventions, and Michigan did not have one city in the top 50 (see Exhibit 76 and 77). Also, the Kauffman Foundation ranked new business start-ups per 100,000 people per month per state in 2011 with the national average being 296 and the Michigan average at just 220. The RTW state average was 310 and the NRTW state average was 285 (see Exhibits 78 and 79). There is some interesting data on business births and deaths from 2002-2007. Michigan trails the national average and the RTW average in births. RTW states are producing new organizations at a faster pace than NRTW states as well (See exhibits 80-87).

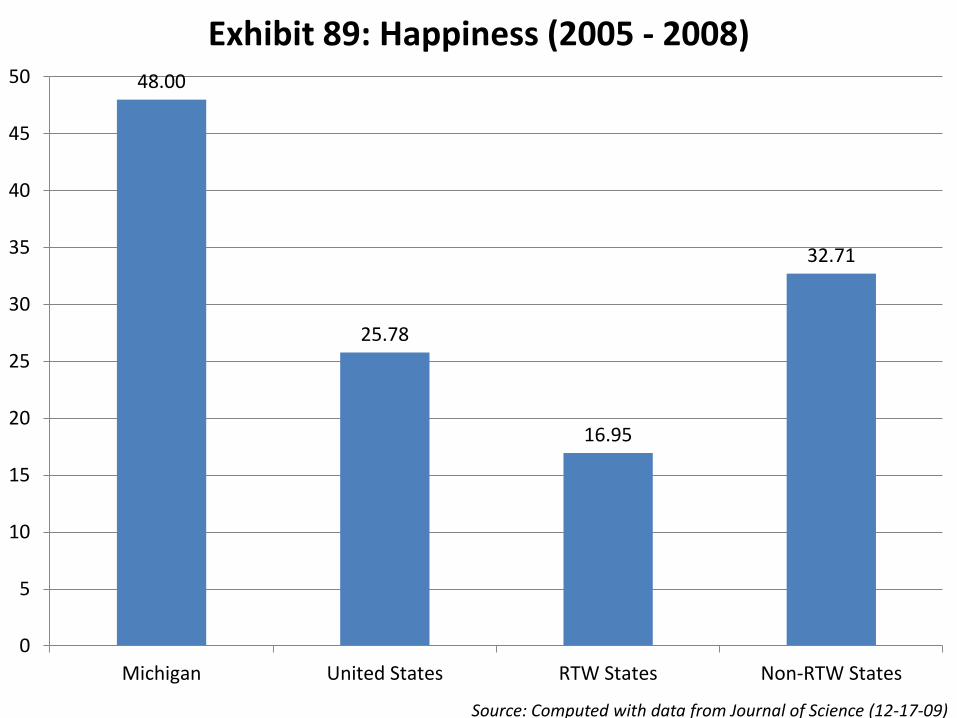

Professors from the University of Warwick in England and Hamilton College in New York have done some path-breaking work trying to measure happiness and quality of life, having published it in the journal Science. The survey rankings from 2005-2008 were used to compare Michigan to RTW and NRTW states. Michigan ranked 48th or third “least happy” overall with RTW states citizens seeming to be much happier at an average rank of 16.95 while NRTW states had an average happiness rank of 32.71 (see Exhibits 88 and 89).

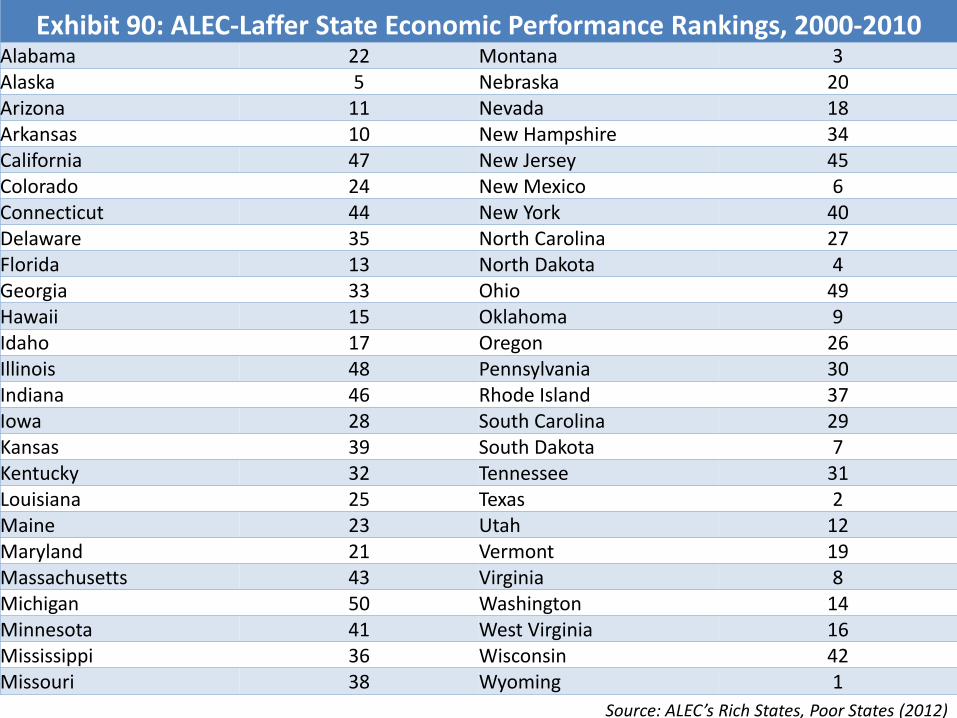

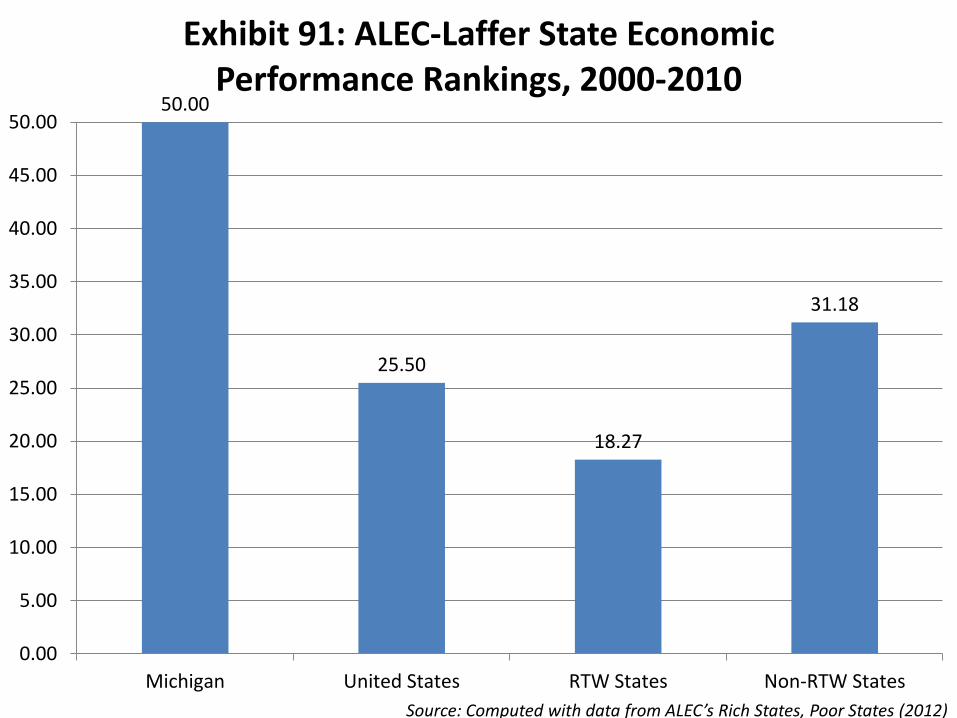

The American Legislative Exchange Council annually ranks states on economic performance considering seven factors ranging from corporate tax rates and GSP growth to non-farm payroll growth and population growth. The 2011 rankings of the above variables showed that Michigan ranked dead last at 50 in economic performance with the average ranking for RTW states being 18.27 and NRTW states averaging 31.18 (see Exhibits 90 and 91).

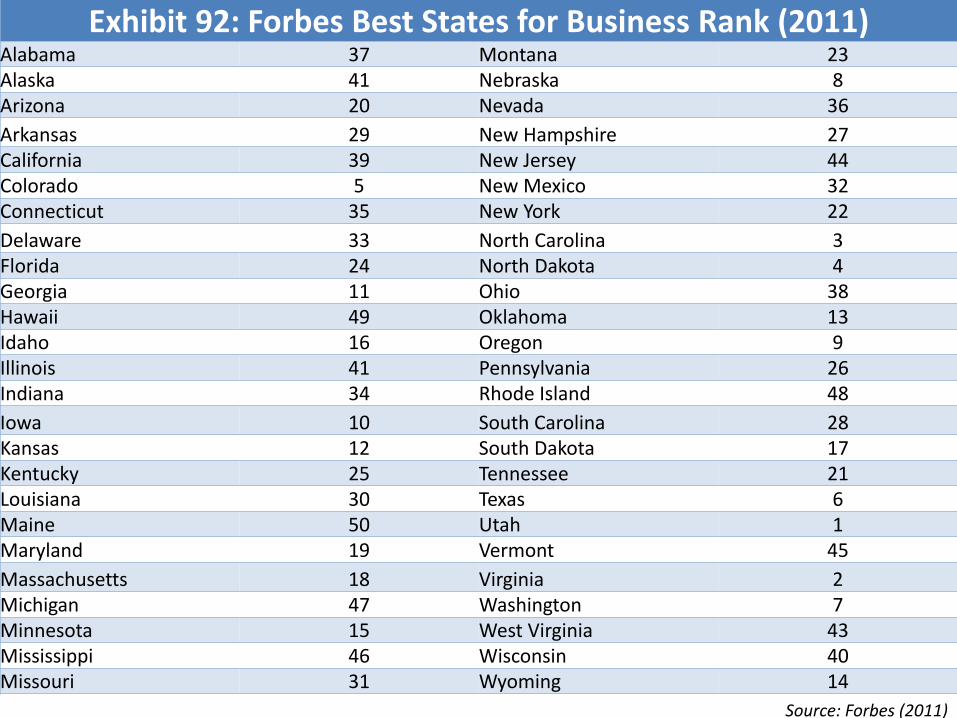

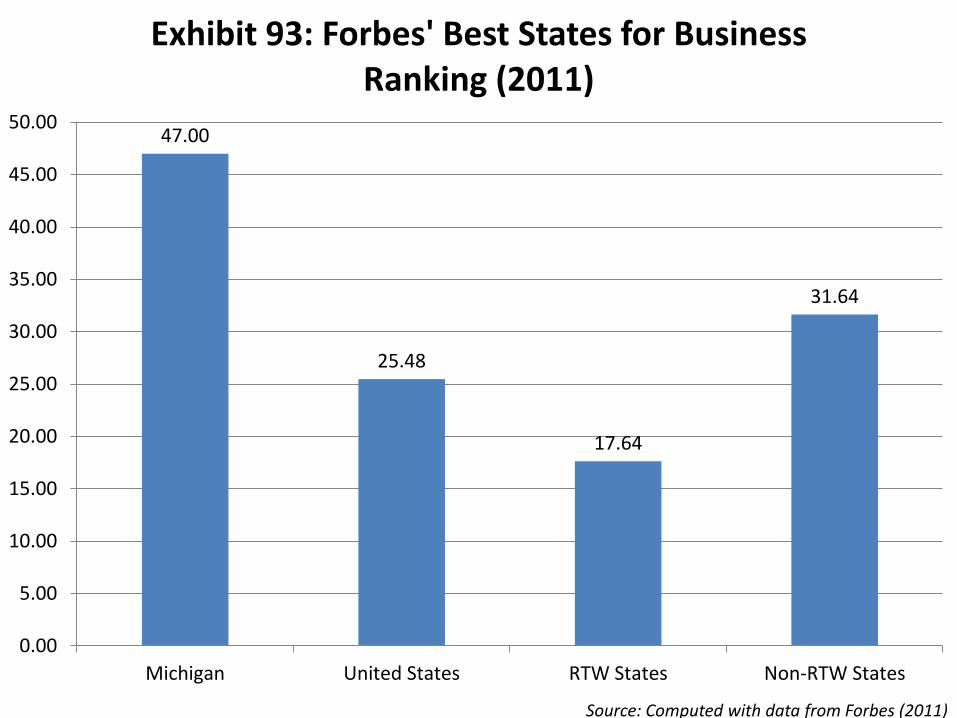

The 2011 Forbes Best States for Business Index and broke it down to compare Michigan to RTW and NRTW states. The Forbes Index considers seven variables ranging from business costs and the regulatory environment to the economic climate and a state’s growth prospects. Michigan ranked 47 overall out of 50 with 1 being the highest and 50 being the lowest. RTW states average 17.64 on the Forbes Index while NRTW states measured 31.64 (see Exhibits 92 and 93). A similar analysis was conducted with data from the 2011 CNBC Index of America’s Top States

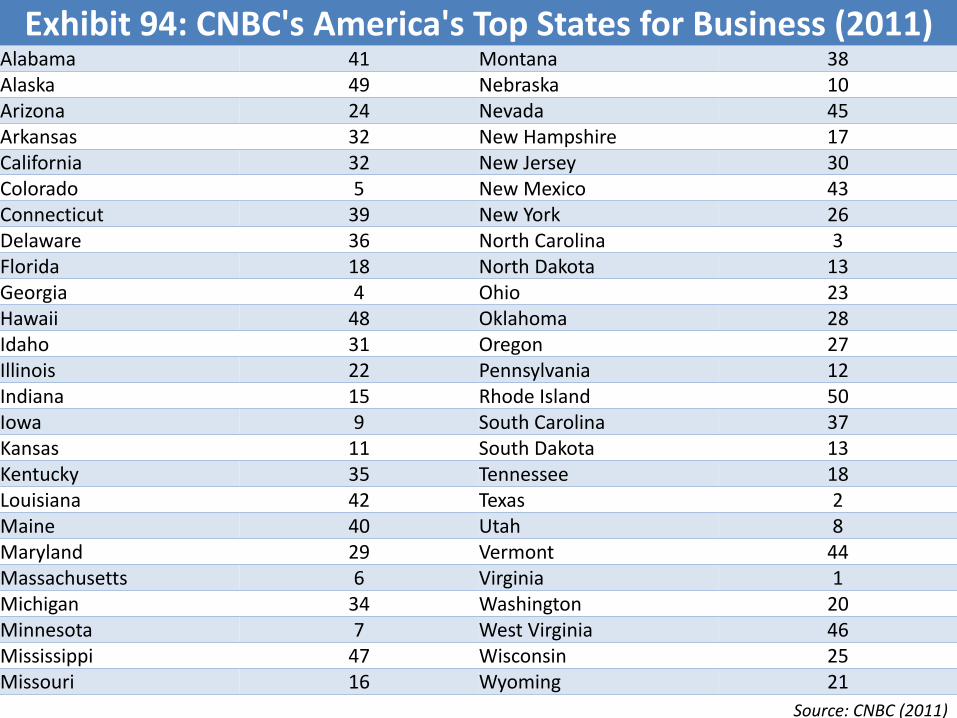

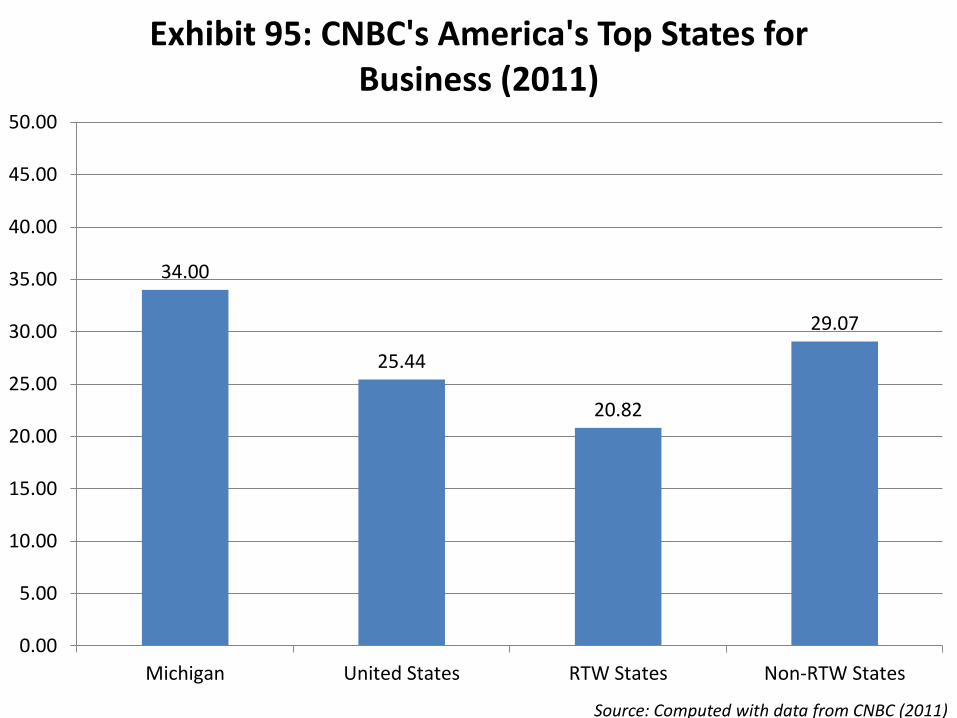

9

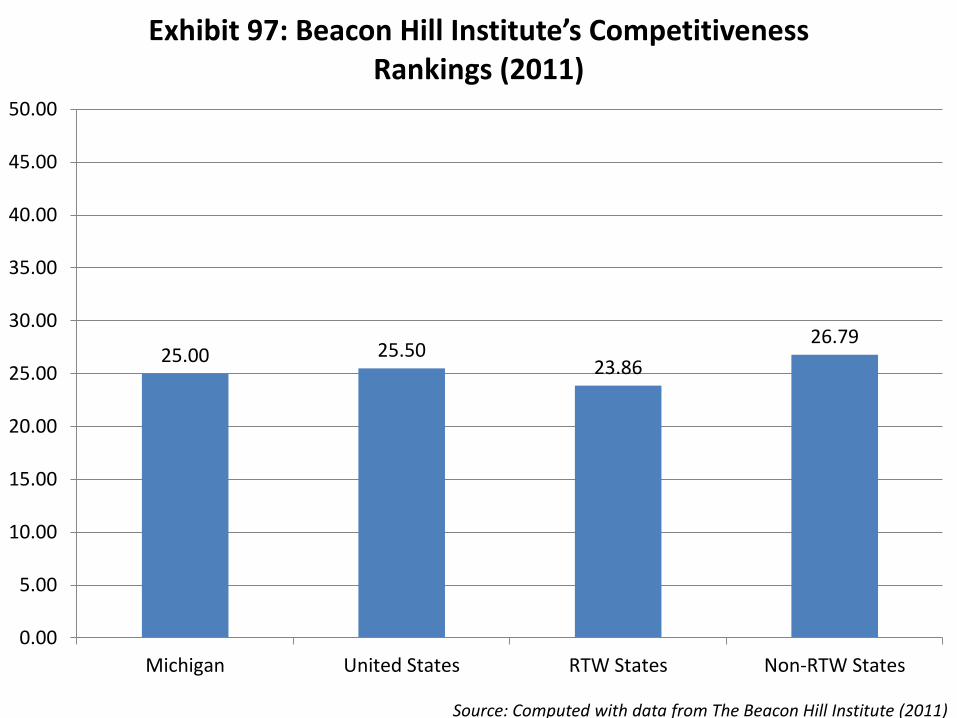

for Business. The ten general variables used by CNBC range from education and infrastructure to cost of living and cost of business. Michigan fared a little better here with an overall rank of 34 out of 50 (50 being least favorable) with RTW states averaging just under 21 and NRTW states averaging 29 (see Exhibits 94 and 95). Michigan fared best on the Beacon Hill Institute’s Competitiveness Index which includes government and fiscal policy, security, infrastructure, human resources, technology, business incubation, openness, and environmental policy factors with a ranking of 25 (1 being most favorable) while RTW states averaged just below than 24 and NRTW states averaged just under 27 (see Exhibits 96 and 97).

The Northwood University Competitiveness Index

Michigan does not fare well in most measures of competitiveness on any of the indices or in the studies mentioned above for happiness, business climate, competitiveness, or economic performance in general. To define the combined effects of the data, roughly 200 variables were examined in this study for all 50 states and a factor analysis was conducted to find five categories or aggregate factors.

Unlike many other indices where the data and/or categories are assigned weights by the researchers, the Northwood Index assigns weights based on factor analysis. The weights are market sensitive since they change with changes in the economic conditions, and the indices are therefore subject to change as the values of the data change over time. Thus, the model delivers an overall ranking for a state, provides evidence of strengths and weaknesses relative to other states by category, and the weights assigned in each category by the model may be useful in prioritizing efforts to improve a state’s relative competiveness.

The Factor Categories and the key variables that influenced each factor are:

Factor 1 (General Macroeconomic Environment) - considers general measures of state-wide economic health such as unemployment rates, labor force participation rates, per-capita income, and life-satisfaction (another measure of well-being in addition to per-capital income).

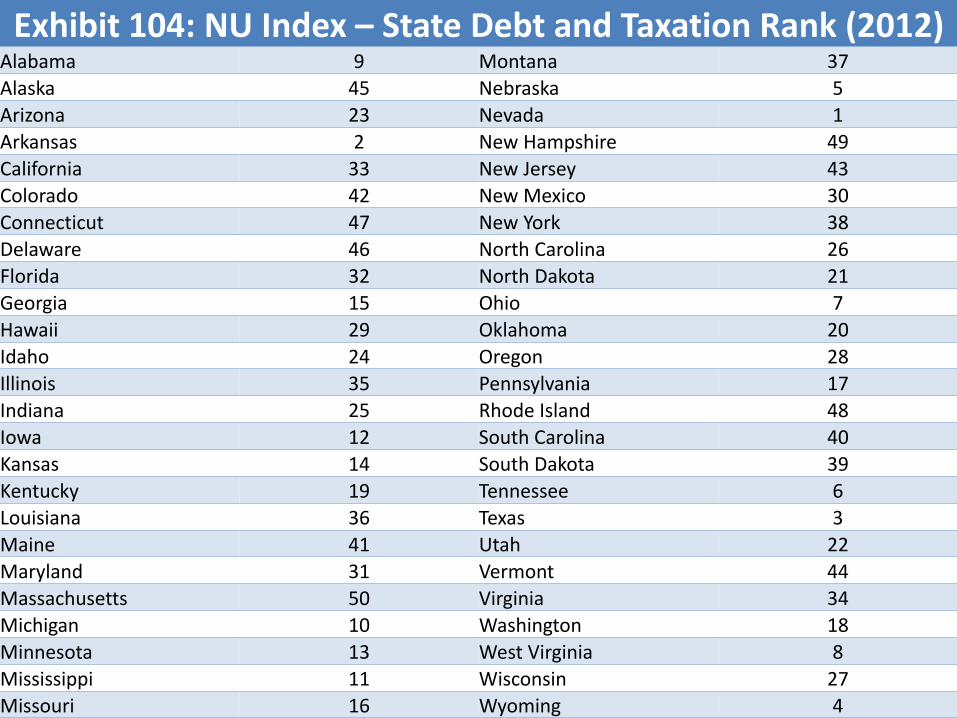

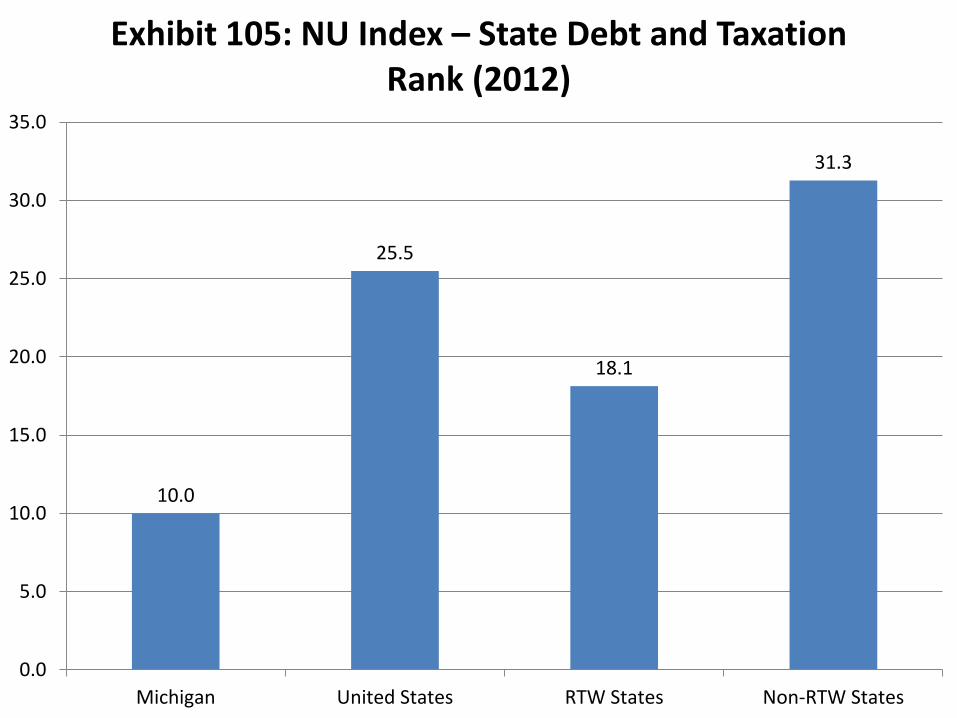

Factor 2 (State Debt and Taxation) - considers state debt per capita, cost of living, and tax burden per capita (tax burden considers state sales taxes, selective taxes, license taxes, corporate income taxes, and state income taxes).

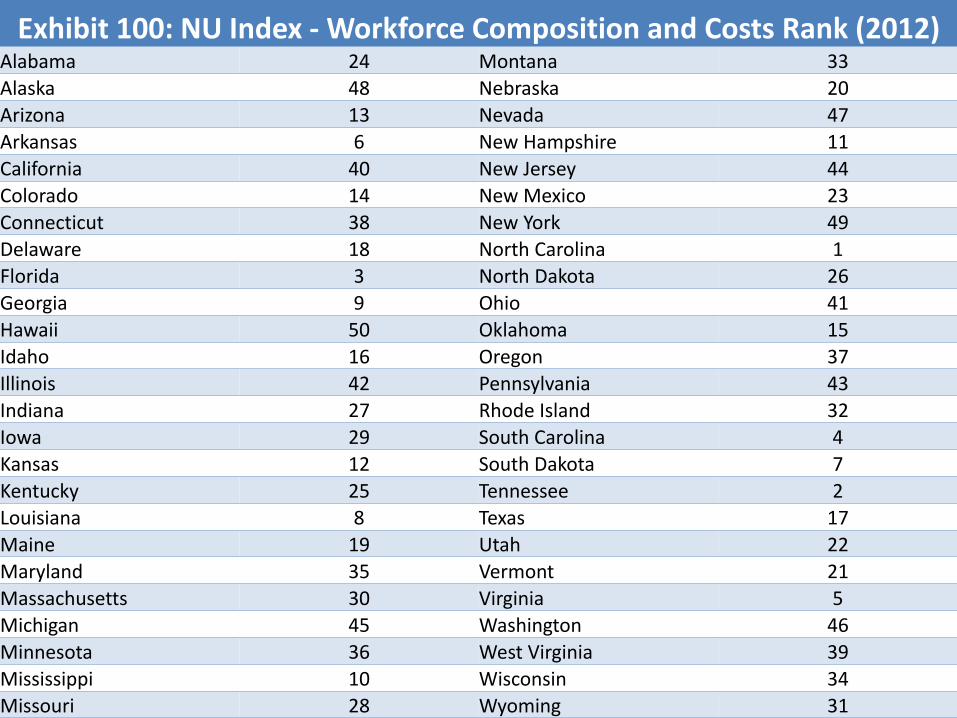

Factor 3 (Workforce Composition and Cost) – considers % of the working population that is part of a union, % of the private working population that is a member of a union, the % of the public working population that is a member of a union, and cash payments to beneficiaries (including withdrawals of retirement contributions) of employee retirement, unemployment compensation, workers’ compensation, and disability benefit social insurance programs.

10

Factor 4 (Labor and Capital Formation) - considers employment growth, population growth, migration, and organizational birth and death data.

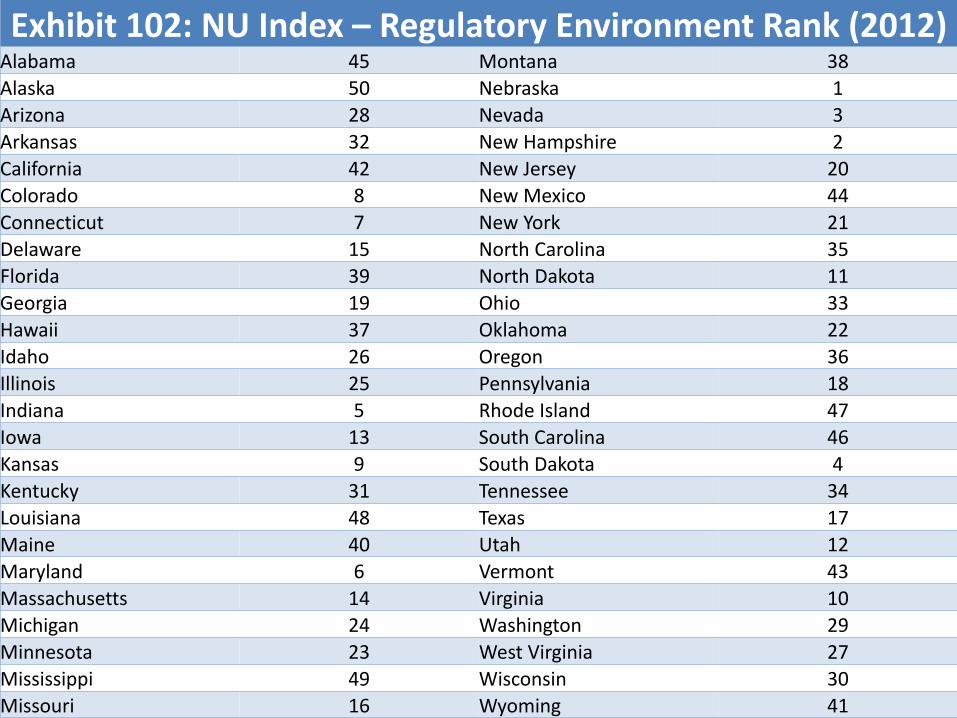

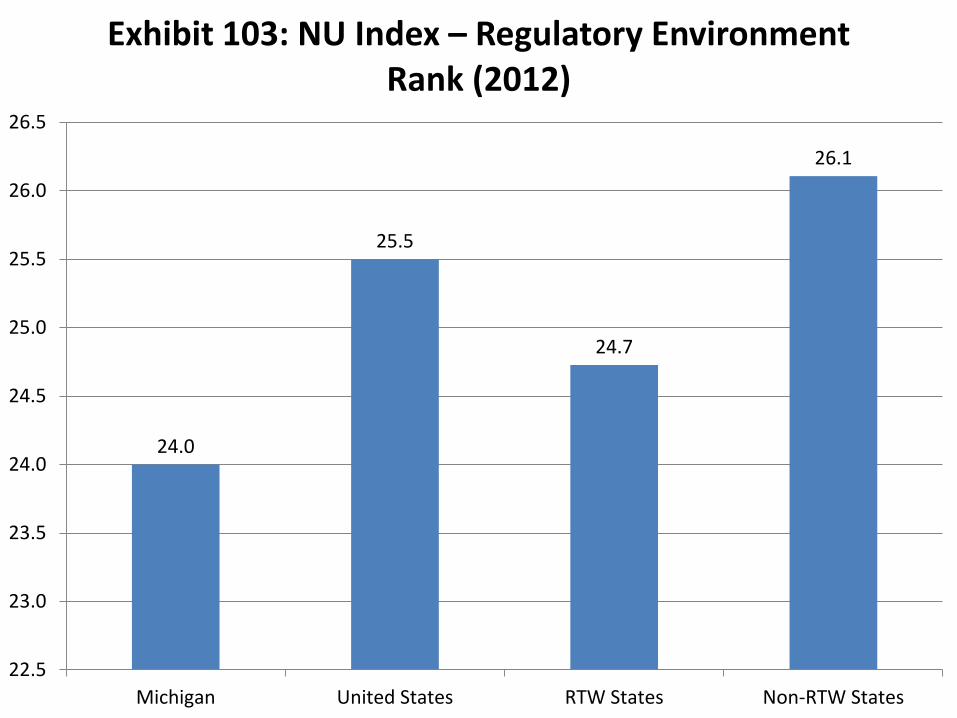

Factor 5 (Regulatory Environment) – represents a composite of other indices that consider the business friendliness of a state's regulatory framework/environment.

Based on the most current available data, Michigan’s economic performance in the five categories is:

1. General Macroeconomic Environment - 48th

2. Debt and Taxation - 10th

3. Workforce Composition and Costs - 45th

4. Labor and Capital Formation - 45th

5. Regulatory Environment - 24th

Overall, Michigan ranks 47th out of the 50 states in the Index. Consequently, the state’s relatively strong performance in terms of Debt and Taxation and Regulatory Environment are outweighed by its relatively weak performance in the factor categories of the General Macroeconomic Environment, Workforce Composition and Costs, and Labor and Capital Formation. In addition, RTW states averaged 15 and NRTW states averaged 33.8 (see Exhibits 98 to 109). A careful analysis of factors 1, 3 and 4 coupled with sound public policies designed to address said issues will enhance Michigan competitiveness in the future which should be demonstrated by an improvement in Michigan’s position within the Index.

Right to Work (RTW) and Non-Right to Work States

Introduction to the Right to Work Debate

Having come out of the second-worst economic downturn of the past 100 years and faced with a sluggish recovery, the Right To Work (RTW) concept is among the most controversial issues facing the nation today. Two recent political battles -- Indiana’s adoption of a RTW law and the failed attempt by organized labor to engineer the recall of Wisconsin Governor Scott Walker, as well as the impending placement of the “Protect Our Jobs” Amendment on the November 2012 (see Appendix) Michigan ballot-- are indicative of this.

11

Both the opponents and the proponents of RTW base their arguments in several different contextual frames. One approach is the use of rights-based legal theory that shows that RTW laws are legally neutral insomuch as they give no legal advantage to workers, employers, or labor organizations and therefore maximize individuals’ freedom of contract and freedom of association; with which this section begins. However, the pure legal or ethical value placed on individuals’ fundamental rights and freedoms alone is not the basis of existing law. Sound public policy, while rightly determining the extent and boundaries of individual rights, must also look to maximize economic opportunity in terms of general economic growth, job creation, investment, and the standards of living afforded to those served by policymakers.

Understanding this, the approach taken here in examining RTW follows the sentiments of Massachusetts Institute of Technology’s Thomas A. Kochan in his recent piece “Resolving America's Human Capital Paradox: A Jobs Compact for the Future” (2012), where he states:

The purpose of a 21st century labor law and policy should be twofold: 1) to protect and support worker rights to choose whether or not to be represented by a union, and 2) to promote and sustain positive labor management relations—ones that have demonstrated their value in supporting high-productivity and high-wage practices and relationships.

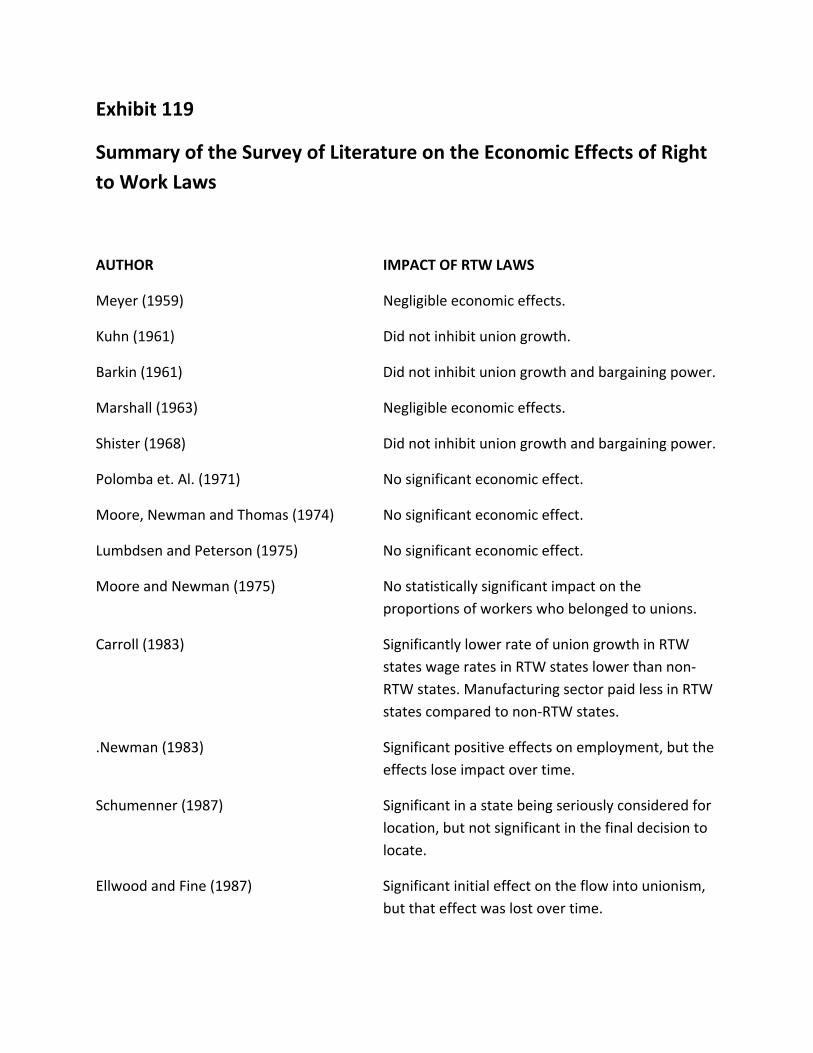

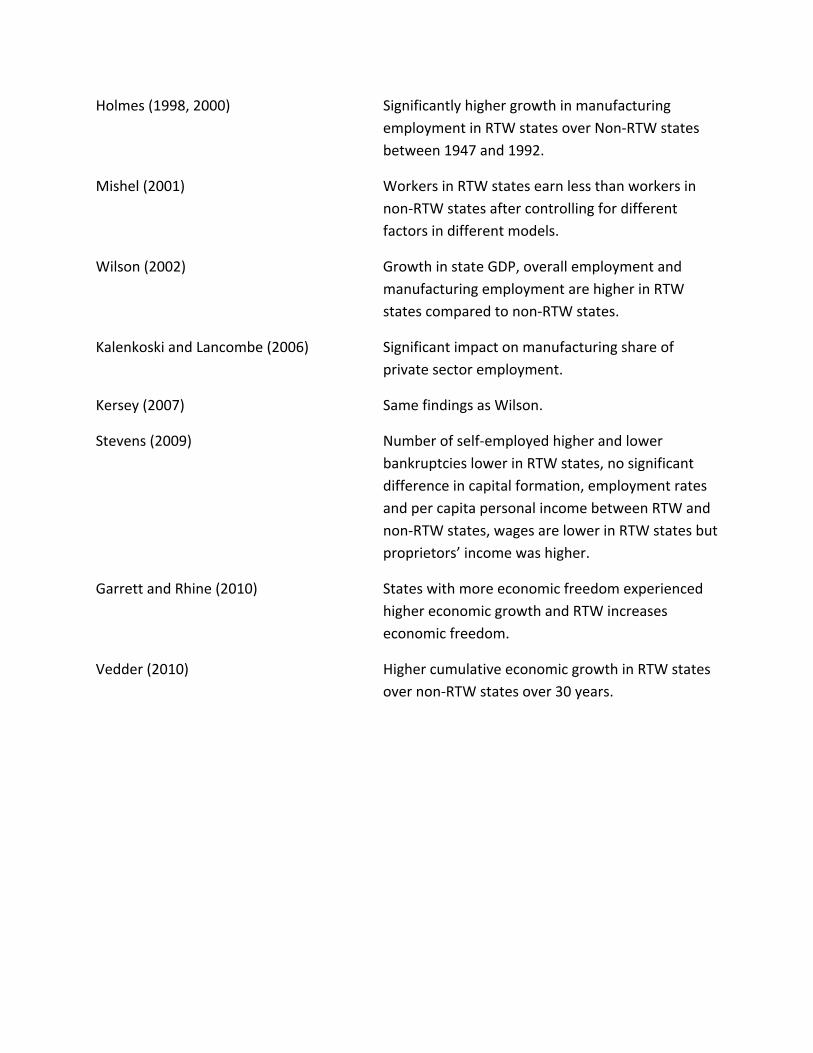

This section continues with a general exposition of the primary pro and anti-RTW positions, followed by the basic economic arguments surrounding RTW and a review of the literature surrounding the economic effects of RTW laws (See Exhibit 119), which also serves to illustrate the technical challenges associated with such studies. This is followed with a discussion and analysis of recent data, finishing with the identification of opportunities for further inquiry.

A Legal History and Analysis of Right to Work

The Right to Organize (or Not) The legal status conferred to workers’ rights to organize for their mutual benefit can be viewed to fall on a spectrum or continuum defined by common law concepts of freedom of association and freedom of contract. At one end of the continuum, organized labor is viewed as a criminal conspiracy against the employer, and the freedom of association and contract as applied to workers with other workers is thwarted for the benefit of the employer. At the opposite end of the continuum, employment can only be legally obtained through membership in a labor organization, and employers must only hire through the union. Here, under compulsory

12

unionization, freedom of association and contract between individual workers and employers is undermined, and the law favors organized labor. The midpoint of this continuum represents the position where both individual workers are free to associate with other workers, or not, and labor organizations are free to negotiate with employers as they choose. Employers, likewise, are free to choose whom they hire, maximizing freedom of association and freedom of contract for all involved and effectively guaranteeing workers the right to work wherever they can find employment. Hunter (1999) considered this midpoint to be the legally-neutral position insomuch as at that point, the law does not favor one person or group of persons over another. When viewed from a historical perspective over the last 200 years, the law governing the rights of workers to act individually or through labor organizations has occupied most points on this continuum at one time or another.

Early Common Law in the United States A series of cases in the 19th century shows the gradual change in the common law treatment of labor organizations and the acceptance of collective bargaining. At the time of the founding, the legal treatment of trade unions and workers was almost exclusively seated in the common law of contract and association where trade associations developed for the purposes of mutual aid, worker training, and improving worker-management relations. However, in Commonwealth v. Pullis (1806), the Philadelphia Mayor’s Court held that a union of shoemakers, striking to earn higher wages, were engaging in a conspiracy against their employer, and each member was fined a week’s wages and the union was required to pay all court costs. The court’s holding made all labor union activity directed against an employer illegal in industrial Pennsylvania and potentially served as legal precedent elsewhere.

However, by 1842 in Commonwealth v. Hunt, the Supreme Judicial Court of Massachusetts found that workers had a right to organize, collectively bargain and strike as long as they did not use violence or illegal means to accomplish their goals. More than fifty years later, in Vegelahn v. Gunter (1896) the Massachusetts Court clarified its earlier position by stating that the right to strike stopped at the point where the strikers interfered with the ongoing operations of the business, including the employer hiring replacement workers. The Massachusetts Court cited In re Debs (1894) where the United States Supreme Court determined that an injunction against a labor strike is allowed when there is evidence of harm to business or the general public. Thus, by the end of the 19th century, organized labor had moved from illegality to legally-neutral status, even if that was not yet fully-defined.

Federal Law and Labor Unions Moving into the 20th century, legal neutrality towards organized labor began to face new challenges. In 1890, Congress passed the Sherman Antitrust Act which prohibits activities that reduce market competition. The Act was applied to labor unions in Loewe v. Lawlor (1908)

13

where the United States Supreme Court found that union strikes, boycotts and secondary boycotts (of suppliers or customers) were illegal if they interfered with interstate commerce by limiting competition. The court also found that individual union members could be charged under the Act if it could be shown they had engaged in conspiracy to cause such interference.

In response to the Loewe decision, labor unions successfully lobbied Congress to exempt union activities from the Sherman Act through passage of the Clayton Act in 1914. While further defining additional illegal activities in restraint of trade, Section 6 of the Clayton Act allows labor unions the right to boycott, peacefully strike and picket, and engage in collective bargaining regardless of any effect on interstate commerce. In subsequent cases the Supreme Court further clarified the extent to which Section 6 of the Clayton Act protected organized labor activities.

In 1921, the Supreme Court heard the case of Duplex Printing Press Co. v. Deering. In this case, the Court found that even under Section 6, secondary boycotts and other activities directed towards a company with which the union was not directly concerned were in violation of the Sherman Act. A year later, the Court expanded this ruling to apply to union activities directed at non-union companies in the same industry in United Mine Workers v. Coronado Coal (1922).

In addition to these adjustments to the legal standing of organized labor, federal rules surrounding collective bargaining began to take shape. During the First World War, President Woodrow Wilson created the National War Labor Board to direct various national resources to the war effort. The general principle followed by the Board was that in exchange for giving up the right to strike, unions would be guaranteed the right to good-faith collective bargaining with employers through “arbitration, mediation, and conciliation” providing a mechanism to mend labor-management disputes that might have otherwise interfered with war production.

After the Sherman and Clayton Acts, their interpretation by the Supreme Court, and moving towards the Great Depression and the New Deal, the legal status of labor unions remained largely in the position of legal neutrality. Individuals and unions both had the right to seek work from employers and employers retained the right to deal with unions or not. Unions were not only allowed but guaranteed the right to collectively bargain under certain circumstances and to recruit new members as long as these activities did not interfere with individual choice or restrain trade.

The only exceptions to unions’ general legal status heading into the New Deal were the railroad workers’ unions. As early as the Erdman Act of 1898, Congress created the means for the railroads and the railroad workers’ unions to settle labor disputes without interruption to rail services, which were seen as vital to the functioning of the economy. The Erdman Act allowed voluntary but binding arbitration, enforceable in federal court. Moreover, in 1920 Congress

14

passed the Esch–Cummins Act, (otherwise known as the Railroad Transportation Act), establishing the Railroad Labor Board which in turn granted railroad unions exclusive representation in labor disputes and disallowed individuals’ rights to negotiate for themselves. However, in Davis v. Wechsler (1923), the Supreme Court held that it was unconstitutional to deny individuals the right to negotiate with the railroads independently from the union.

In 1926 in response to the Davis decision, Congress passed the Railway Labor Act. The Act explicitly granted workers the right to organize and created for the railroad companies a legal “duty to bargain” with railroad unions. The Act was amended to include airlines in 1936. In 1951, the Act was once again amended to permit compulsory unionization, making it illegal for a railroad or airline to hire outside the labor unions representing their workers. These provisions are still in effect today. These amendments notwithstanding, the “new” requirements under the Railway Labor Act would set the stage for additional federal regulation regarding the rights of unions moving into the Great Depression.

In 1932, President Herbert Hoover signed the Norris-LaGuardia Act. In general, the Act limited the legal power of employers over labor unions as opposed to directly empowering unions. It prohibited the creation of worker agreements to refrain from future union membership (so-called “yellow-dog contracts”) and it disallowed such agreements already in existence from being entered into the record in a federal case. It also exempted unions from potential violations of antitrust law under the Sherman Act. The Act furthermore prohibited employers from filing private damage suits arising from or injunctions against striking labor unions.

A year later, the National Industrial Recovery Act (NIRA) was signed into law by President Franklin Roosevelt. NIRA was intended as a general plan to promote economic recovery and only a small part of it, Title I, Section 7(a) applied directly to labor unions. That section gave all workers statutory rights to organize labor unions and bargain collectively. In Schechter Poultry Corp. v. United States (1935), the Supreme Court found NIRA unconstitutional on the grounds that Title I was vague in its construction and delegated overbroad authority to the executive branch, but the language in Title I, Section 7(a) was never specifically cited in the Court’s opinion, leaving the labor issue open for further legislation.

The Wagner Act The basis of all modern federal law regarding the legal status of organized labor in the private sector is the National Labor Relations Act, often referred to as the NLRA or Wagner Act. The Act was passed by Congress and signed into law by President Roosevelt in early July 1935, roughly six weeks after the Court’s decision in Schechter. The NLRA created legal rights and obligations for both employers and unions. For employers it became an “unfair labor practice” to fail to “bargain in good faith,” or to interfere with 1) workers organizing into labor unions, 2)

15

workers engaging in collective bargaining through labor unions, and 3) concerted labor activities such as striking and picketing.

For unions, the NLRA established a process for workers to adopt membership in a particular union. If a majority of workers voted in favor of union representation, the elected union was allowed to establish one of three different worker-union relationships. The first, referred to as a “closed shop,” required workers to be a member of the union prior to employment. Second, unions could establish a “union shop” by allowing companies to hire non-union members, but requiring those workers to join the union within some set time following their hiring. Third, the union could declare itself an “agency shop” where union membership is not required but where all workers are required to pay dues for all union activities through which they receive benefit. In addition, a new federal agency, the National Labor Relations Board (NLRB), was created to oversee the enactment of the NLRA and enforce its various provisions.

As a result (with the single exception of the railroad industry), the common-law based legal foundation of business-labor relations that had emerged through the common law over one hundred years was largely discarded. By allowing unions to operate closed shops, union membership could become compulsory, employees could be denied access to jobs and employers would have no opportunity to contract with workers of their own choosing.

The Taft-Hartley Act The NLRA operated as the law of the land from its passage until after World War II. In 1947, Congress enacted the Labor-Management Relations Act (commonly known as the Taft-Hartley Act), by overriding President Harry S. Truman’s veto. The goal of the Act was to amend the NLRA to reduce the degree of power afforded labor unions by re-establishing legal rights of individual workers and mandating administrative changes within the NLRB. The major provisions the Taft-Hartley amendments were nearly as broad if not as deep as the NLRA itself.

First, Taft-Hartley recognizes the right of individual workers to refrain from union activities. Second, the Act adds prohibitions on unfair union labor practices and further defines requirements for both unions and businesses in collective bargaining. Third, it specifically prohibits coercive conduct against neutral persons in certain circumstances such as disputes among two or more unions at a workplace regarding work assignments, and prescribes standards for injunctive relief in such circumstances. Fourth, the Act allows both labor and management to file suit for breach of a labor contract. Fifth, it eliminates the closed-shop option for union organization but still allows for union and agency shop arrangements.

Last, and most importantly, section 14 (b) of the Taft-Hartley Act states that the act “shall not be construed as authorizing the execution or application of agreements requiring membership

16

in a labor organization as a condition of employment in any State or Territory in which such execution or application is prohibited by State or Territorial law.”

The language of section 14(b) allows the individual states to “opt out” of the union shop requirements of the NLRA, effectively making the agency shop structure the only legal method of union organization within those states. In opting out, and disallowing a union membership requirement for purposes of employment, several states took the opportunity to re-establish the legal neutrality and maximum freedom of association and contract that have become known as the “right to work.”

The Right to Work States In 1944, three years prior to the passage of the Taft-Hartley Act, Florida and Arkansas established right to work provisions in their state constitutions, expressly forbidding employers from hiring workers based on their status as a member or non-member of a labor union, even though these provisions were contrary to existing federal law under the Wagner Act. In 1946, three states, Arizona, Nebraska, and South Dakota, adopted similar constitutional provisions. Both before and after passage of Taft –Hartley in 1947, the legislatures of six additional states-- Georgia, Iowa, North Carolina, Texas, Tennessee and Virginia--enacted right to work statutes.

Various organized labor groups in Arizona, Nebraska and North Carolina challenged the state laws almost immediately upon passage in their respective state courts where they were all upheld. The state cases from Nebraska and North Carolina reached the United States Supreme Court on appeal in late 1948 in Lincoln Federal Labor Union v. Northwestern Iron & Metal Co. where the Court held that state laws can forbid union membership as a requirement for employment when they create equal rights to employment for both union and non-union workers.

Since 1947, twelve additional states have enacted right to work laws either through statute, constitutional amendment in the case of Oklahoma and Kansas, or in the case of Mississippi, first by statue and later by constitutional amendment. Chronologically, they are: North Dakota (1948), Nevada (1952), Alabama (1953), South Carolina (1954), Mississippi (1954, 1960), Utah (1955), Kansas (1958), Wyoming (1963), Louisiana (1976), Idaho (1985), Oklahoma (2001), and most recently, Indiana (2012). In addition to these states, the Territory of Guam adopted right to work legislation in 2001.

Indiana is the only state to have had right to work legislation implemented and then repealed. As summarized by Vedder, et al. (2011), the state originally passed right to work legislation in 1957, but in the time between its enactment and when it was scheduled to go into effect, several unions negotiated contract extensions that would be honored under the law until they expired. Union leaders then brought suit against the state, arguing that agency shop contracts

17

that charged workers dues but that did not require union membership were permitted under state law. In 1959 the Indiana Court of Appeals ruled in favor of the unions in Meade Electric Co. v. Hagberg. This decision ostensibly resulted in no greater employment opportunity for individual workers under the law than under a union shop setting, and as a consequence the law was repealed in 1965.

The Right to Work in Michigan Michigan workers played a central role in the development of labor unions in the interwar period and have held a position of power in the state since the 1940s. It has only been in the face of a weakened economy and job losses in the automobile industry that right to work legislation under the provisions of section 14(b) of Taft-Hartley has been considered.

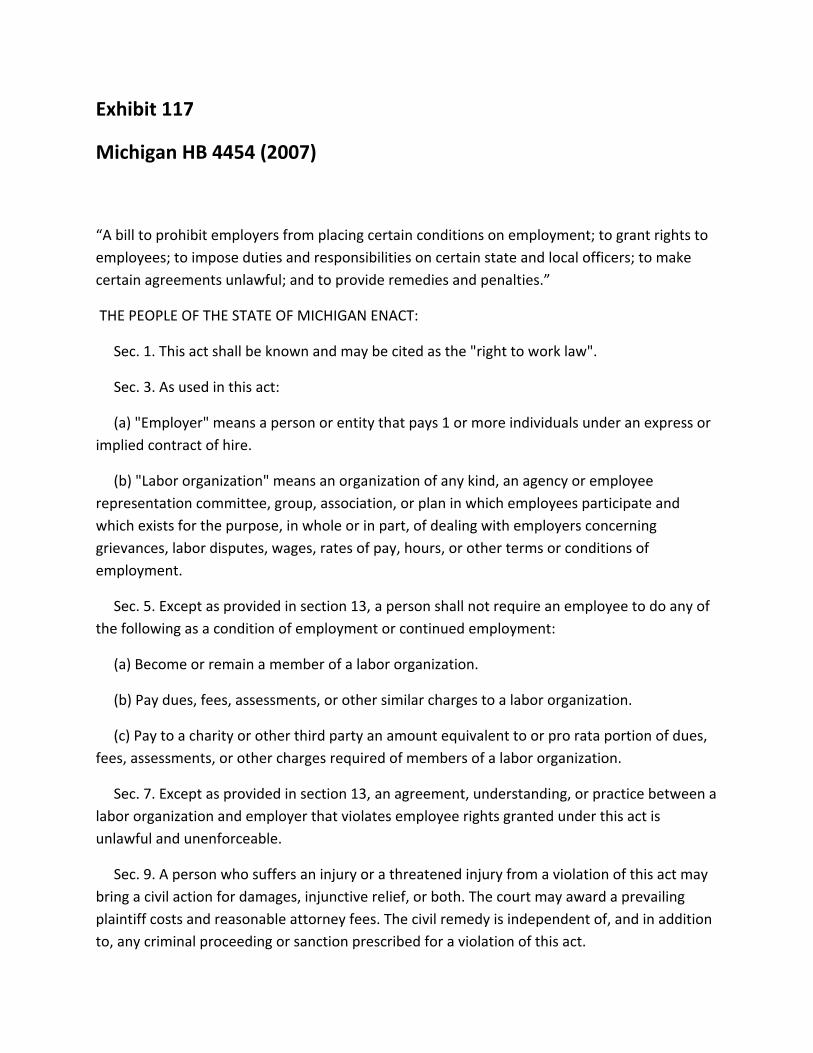

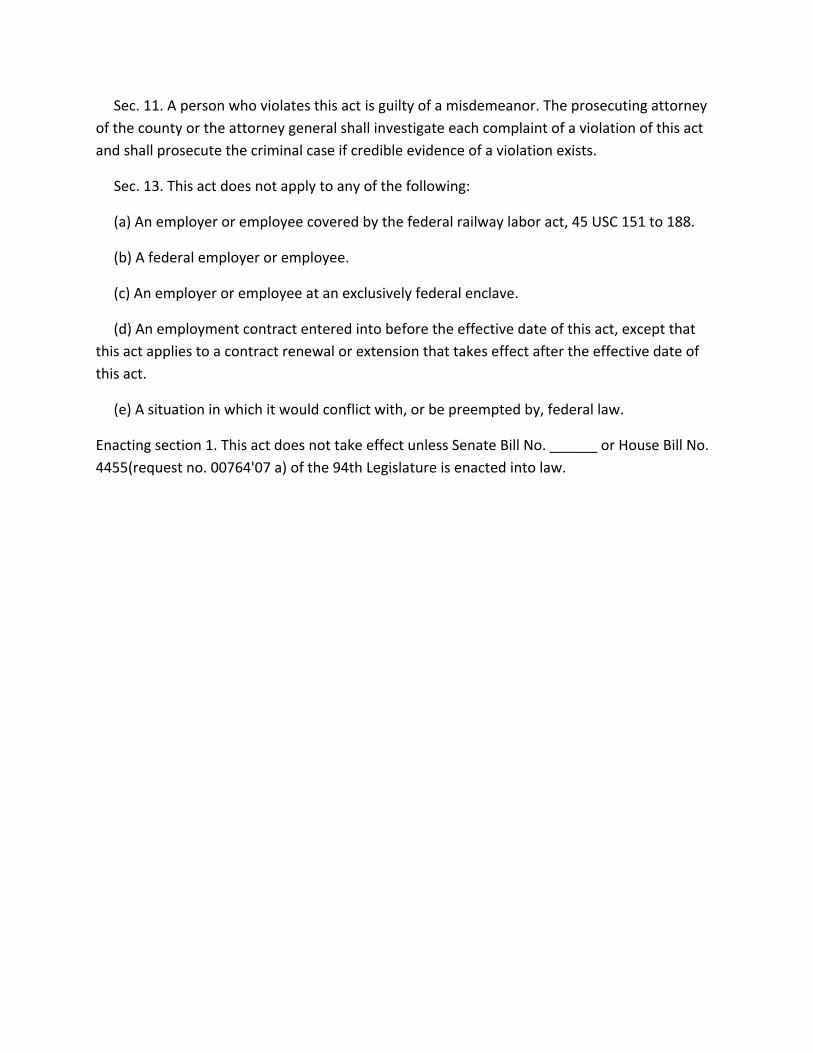

On March 13, 2007, Representative Jacob Hoogendyk, et al., introduced House Bill 4457 “The right work law”(see Exhibit 117), described in its preamble as:

A bill to prohibit employers from placing certain conditions on employment; to grant rights to employees; to impose duties and responsibilities on certain state and local officers; to make certain agreements unlawful; and to provide remedies and penalties.

Upon introduction the bill was referred to the House Committee on Labor, where it was never opened for comment or discussion. Senate Bill 0607 (2007) with identical language was introduced by Senator Nancy Cassis and assigned to the Senate Committee on Commerce and Tourism on June 26, 2007. This Committee also failed to take up the bill for discussion. On December 2, 2008, the bill was dismissed on an adverse roll call vote, maintaining the status quo with Michigan workers and employers continuing to abide by the union-shop provisions of the Wagner Act.

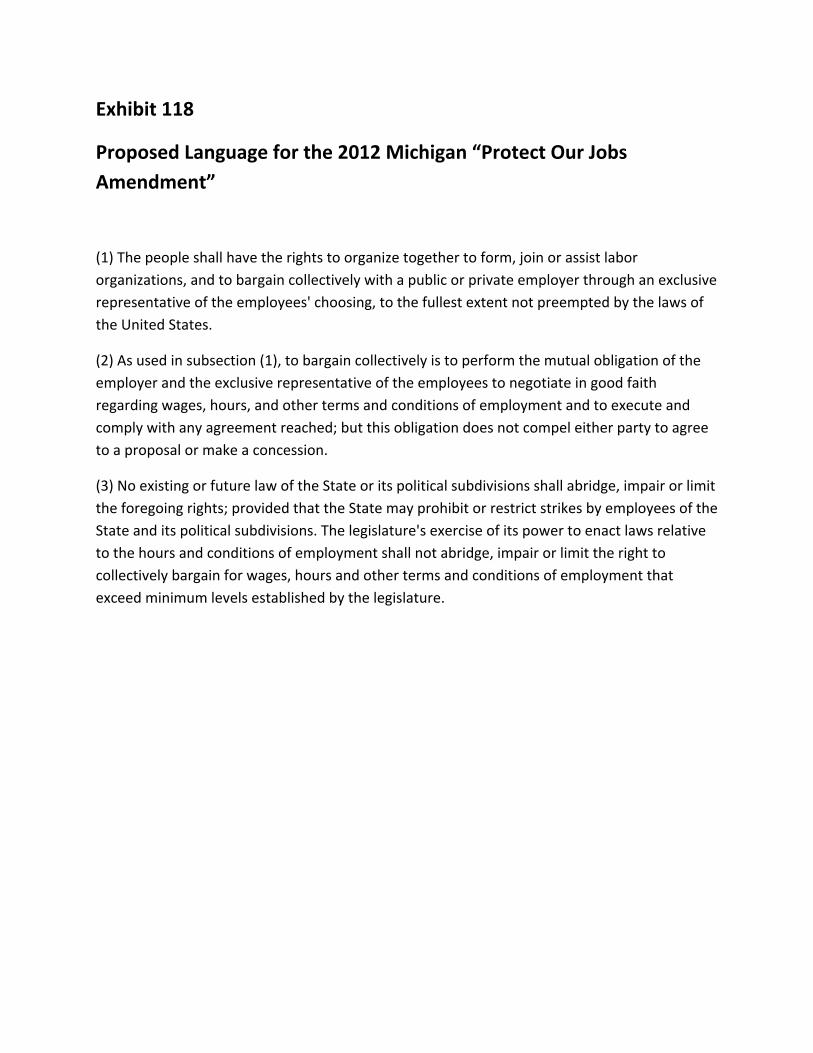

More recently, organized labor has promoted a ballot initiative known as the “Protect Our Jobs” amendment to the Michigan Constitution for November 2012 election (see Exhibit 118). The amendment as currently written would establish a Constitutional right for both private and public workers to organize, forgo binding arbitration for the settlement of disputes with management, and bargain to have their dues withheld and submitted to their union by their employer. The language of the amendment would apply retroactively. Critics of the amendment claim that its enactment would affect between 80 and 120 current laws, most of which would need to be reevaluated in the courts, prompting a spate of lawsuits. The State Board of Canvassers declined to put the proposal on the November ballot primarily because it believed that the ballot language needed to discuss this impact on existing laws. Supporters of the proposal challenged the Board, and on August 27, 2012 the Michigan Court of Appeals decided that this was not a requirement for a valid ballot initiative. Upon review, the Michigan Supreme Court agreed with Court of Appeals on September 6, 2012.

18

Review of the Economic Literature on Right to Work

As outlined in the previous section, an underlying and fundamental principle in the American political and economic system is the idea of freedom of association. Individuals should have the personal liberty to freely associate with any other members of society for lawful and commonly shared goals, purposes, and activities. This principle also implies the opposite: that individuals may not be compelled or coerced into joining or participating in any association without their voluntary consent. The underlying premise of a free society is the right of individuals to say, “No,” whether this involves joining a church, entering into a contract, participating in any social club or group, or membership in a labor union (Baird, 1988). Broadly, the arguments against an individual employee’s right to work without membership in a union have been of three general types: First, only unified union membership can protect all workers against the superior bargaining power of the employer; Second, only compulsory membership can protect other workers from the “unfair” competition of non-union members that may result in the wages of all workers in that industry being pushed below their “fair market value”; and third, only mandatory union membership (and dues paying) prevents non-union members from a “free ride” at the expense of union workers in a company or industry. The Superior Bargaining Power of the Employer The inferior position of the individual worker is claimed to be due to a number of factors. First, it is argued that the individual worker must accept the wage offered by the employer, since if she or he does not accept it, there are always many other workers looking for jobs ready to take that place. This ignores the fact that competition is two-sided in virtually every modern, developed market, and especially in a country like the United States. Any employer who fails to offer a wage tending to reflect the anticipated value that the worker contributes to a company’s profitability runs the risk that the potential employee with useful and productive skills will search out alternative employment where those skills are more highly valued by another employer wishing to get ahead of the competition. The same applies to currently employed workers who, if they believe that they are not receiving a wage commensurate with their actual market value, will see the advantage of changing employers in the same or a related market. This forces any employer attempting to “low ball” workers to raise the wage offers, or run the risk of losing a growing number of qualified workers without whom she or he may not be able to retain the market position relative to his or her rivals.

19

Another argument claims that the individual worker has an inferior bargaining position because the individual worker cannot “wait” to look for a better job. First, if the worker does not earn wages she or he cannot eat. The employer can wait to find a worker willing to take any salary she or he wishes to offer because, she or he has “capital” to live off until such a worker comes along who will accept the lower wage the employer wishes to pay. Second, it is stated that labor is a perishable “commodity.” It cannot be “stored” to sell on another day. So if the worker does not take the wage offered that lost day’s labor can never be regained. However, there are limits to any such claimed “waiting” advantage on the part of the employer. First, every day of less output produced because needed workers are not yet hired is a day with lost sales revenues resulting from reduced output that could have been produced and sold on the market. Thus, waiting to find workers who might be willing to accept wages less than their real market value imposes a cost on the employer in the form of smaller profits and less market share that could have been acquired, if a wage more in line with workers’ worth was offered and accepted. Second, financial capital may be “stored” rather than invested in hiring workers and producing output. It can be held as cash or loaned out (short-term) for some interest return. However, delaying the hiring of workers who would otherwise have gladly worked at reasonable market-valued wages results in prospective employers earning neither profit nor interest if a part of his or her financial capital is held as cash. And even if lent out to earn short-term interest, the potential employer loses every day the difference between the interest s/he may earn and the greater profits that could have been had by not delaying hiring needed workers for production that could have been manufactured and sold (Hutt, 1954; 1973, pp. 61-76; Machlup, 1952, pp. 348-352; Chamberlin, 1951, pp. 168-187).

Unions Protect Wages from Unfair Non-Union Competition It is argued that unions are able to collectively negotiate wages above what individual workers were individually could negotiate on their own. If non-union workers could compete for union jobs, those union-secured, higher wages would be competed down. Thus, all workers will be better off if required to join and jointly negotiate through the representing union. Labor, however, like every other good or service offered on the market, is subject to the law of supply and demand. If a union successfully negotiates a wage above the one that would have been competitively established on the market, fewer workers may be employed, since the higher the wage the less profitable the number of workers potential employers find it attractive to hire (or retain). In other words, wages that compulsory unions may successfully impose runs the risk of pricing some workers out of the labor market (Velasco, 1973).

20

In this instance, the “conflict” is not between “labor” and “management,” but instead between union workers and non-union workers. The union “locks out” members of the labor force who would have been willing to work for prospective employers on terms mutually attractive to the two sides. This forces the locked out and displaced workers to search out alternative gainful employment in jobs and with employers who may be less well paying and not as attractive. The union members’ gains are, as a consequence, at the expense of other workers, who must find employment in other markets. As non-union workers fill these other markets, wages in that alternative part of the labor market fall below what would have prevailed if the all the jobs had been available to all the workers. This process can and often does entail workers having to migrate out of the state where they had previously found work, or where they would have chosen to reside, if not for compulsory union membership rules pushing non-union workers out of that part of the labor market, and that part of the country in which “closed shop” conditions prevail (Hayek, 1960, pp. 267-284; Knight, 1959, pp. 21-45).

The Need for Union Membership to Avoid Non-Union Free Riders It has been argued that the higher wages and better working conditions negotiated by a labor union benefit not only the union members but all other workers in the company or industry who are covered by the union terms of employment. If non-union members are able to benefit from the “positive” results of union activities, it is only reasonable that they should be required to bear a part of the costs of obtaining those favorable work conditions and wages. Thus, non-union workers should, if not required to join the union, to be at least obligated to pay union dues to assist in defraying the organizational and related expenses to provide those benefits. At the same time, the potential for “free riding” reduces the incentive to belong to a union, and thus may result in fewer union members and weaker unions unable to effectively negotiate on behalf of workers’ interest (Ickniowski and Zax, 1991). The free rider problem can only arise when the gains from the actions of some cannot be prevented from benefiting others who have not participated in covering the costs that have generated those “positive” results. However, excludability is possible in the case of union-generated wages or work conditions by simply stipulating in the negotiated union contract that the terms of that contract apply only to union members. If non-union workers are unable to obtain from the employers wages and work conditions equal to or better than those arranged by the union, that will act as a positive incentive for non-union employees to join the union. If, however, non-union employees are able to negotiate for themselves wages and work conditions not much different from (or even superior to) those

21

covered by the union contract, it would demonstrate clearly that union membership and dues are superfluous (Baird, p. 37).

In addition to the economic considerations raised by organized labor, a number of arguments have been offered in support of Right-to-Work Laws, among them: the case for personal freedom; the gains from competition; the benefits from labor mobility and workplace flexibility; and the efficient use of scarce resources for improved productivity. The Case for Personal Freedom The hallmark of a free society is the extent to which the individual has the liberty to make decisions guiding his or her own life, including the occupation or profession she or he chooses to follow to earn a living and that gives meaning and enjoyment to his or her daily activities. By definition then, union shops exclude workers who would otherwise find gainful employment on the basis of free and voluntary contract between themselves and willing employers. This is a restraint not only on trade in general, but a restriction on the personal freedom of workers to enter into consensual association with others for peaceful and lawful mutual benefit. The same applies to compulsory payment of union dues as a “tribute” to a union for the right to work for a particular employer or in a specific industry. Indeed, it can be argued that it is a form of imposed tax for the privilege of working within the “jurisdiction” over which the union claims authority (Richberg, 1957, pp. 114- 126).