Embed Size (px)

Citation preview

2012 RegionalEconomic Outlook

May 2012

minneapolisfed.org

Disclaimer

The views expressed here are the presenter's and not necessarily those of the Federal Reserve Bank of Minneapolis or the Federal Reserve System.

minneapolisfed.org

Agenda

Ninth District Economy– Outlook

• Surveys• Models

– Sector Analysis• Agriculture• Manufacturing• Home building

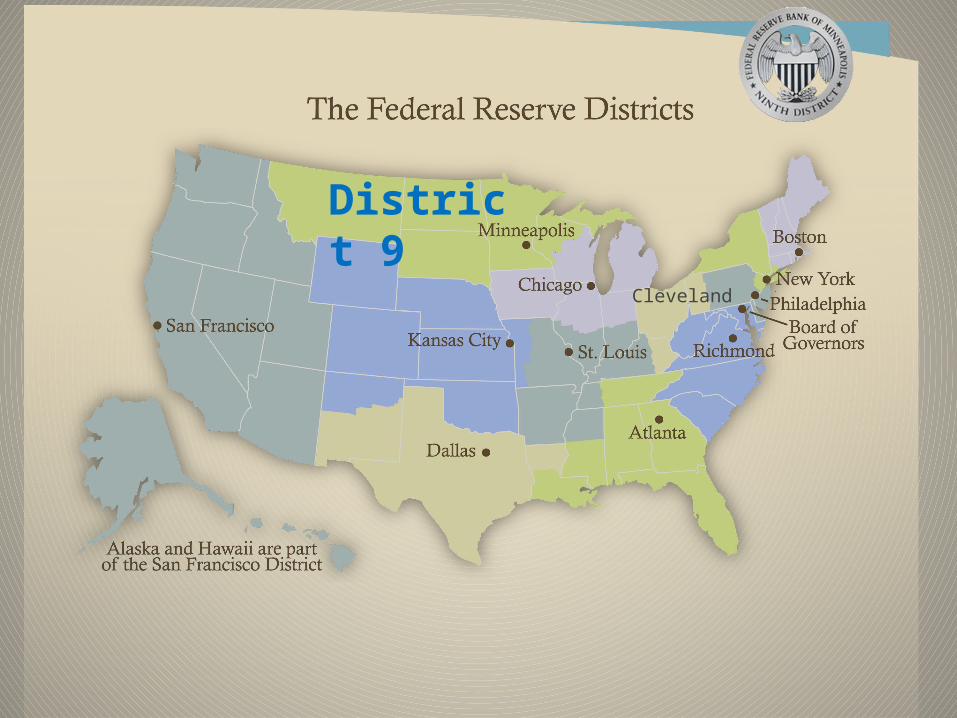

District 9

Cleveland

Ninth District Economy: Growth in 2012

• Business leaders remain optimistic

• Employment up, modest unemployment rate reductions

• Small wage and price increases

• Agriculture sector strong & manufacturing upbeat

• Slow home building sector

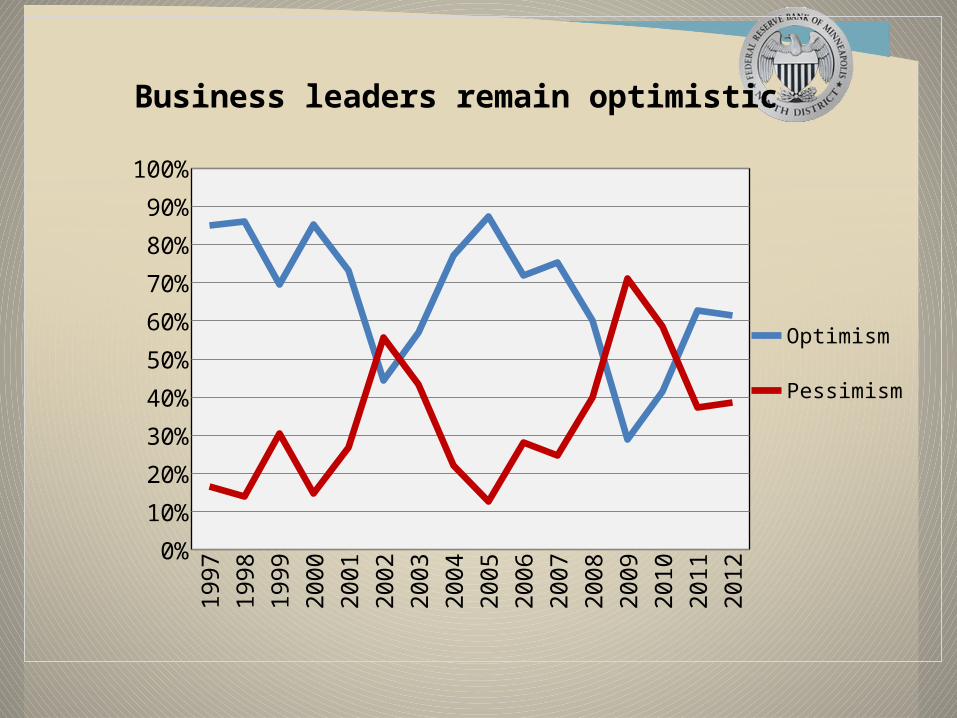

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Business leaders remain optimistic

Optimism

Pessimism

Employment expected to expand across the district

MN MT ND SD WI UP0.0

1.0

2.0

3.0

4.0

5.0

6.0

2011

2012

Nonfarm employment forecastPercent change from a year earlier – 4th quarter

Agriculture

Construction

DISTRICT

Services

Manufacturing

Retail

0 20 40 60 80 100

2011 Out-look

2012 Out-look

Diffusion index*

Business leaders expect increased employment at their companies

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

MN MT ND SD WI UP0

1

2

3

4

5

6

7

8

9

10

2011

2012

Unemployment rate – 4th quarter

Unemployment rates will decrease modestly

0% to 1%

2% to 3%

4% to 5%

Above 5%

0 10 20 30 40 50 60

2011 Out-look

2012 Out-look

Percent of respondents

Business leaders anticipate small wage increases

Agriculture

Retail

DISTRICT

Services

Manufacturing

Construction

0 10 20 30 40 50 60 70 80 90 100

2011 Out-look

2012 Out-look

Diffusion index*

Business leaders foresee some price increases

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

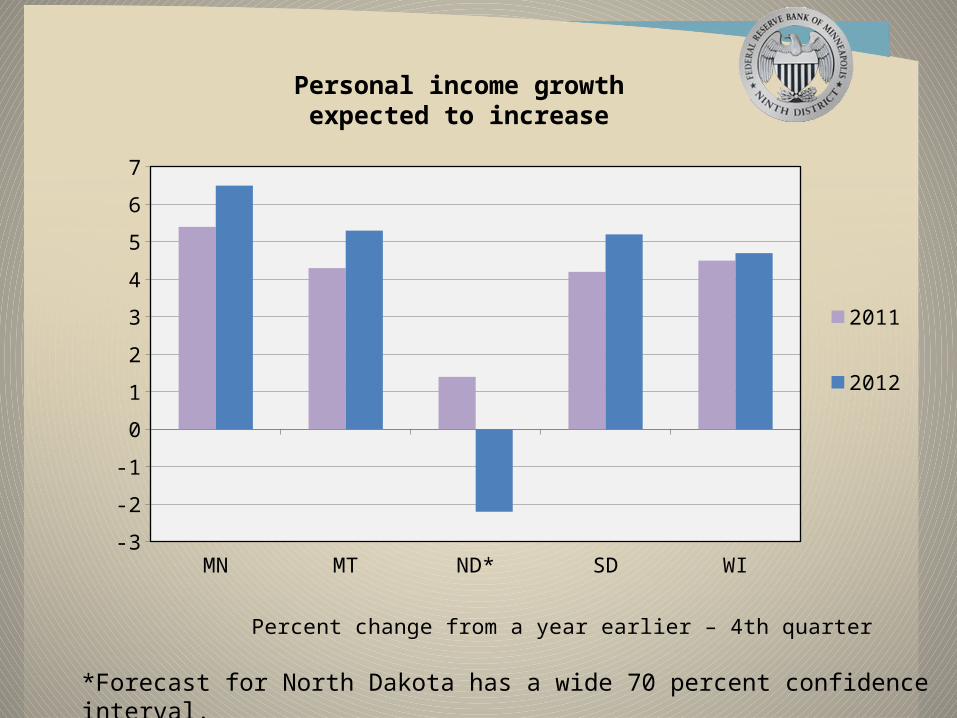

Personal income growth expected to increase

MN MT ND* SD WI-3

-2

-1

0

1

2

3

4

5

6

7

2011

2012

Percent change from a year earlier – 4th quarter

*Forecast for North Dakota has a wide 70 percent confidence interval.

Manufacturing survey reveals growth in 2011; faster growth expected in 2012

Investment

Employment

Profits

Production level

0 20 40 60 80 100

2011 Ac-tual

2012 Outlook

Diffusion index*

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

However, manufacturing respondents to business poll expect more modest growth in

2012

Investment in plant and equipment

Employment

Sales

0 20 40 60 80 100

2011 Out-look

2012 Out-look

Diffusion index*

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

Source: Lender Processing Services (LPS)

Source: Lender Processing Services (LPS)

Delinquent Payment: 90+ PD, Foreclosure

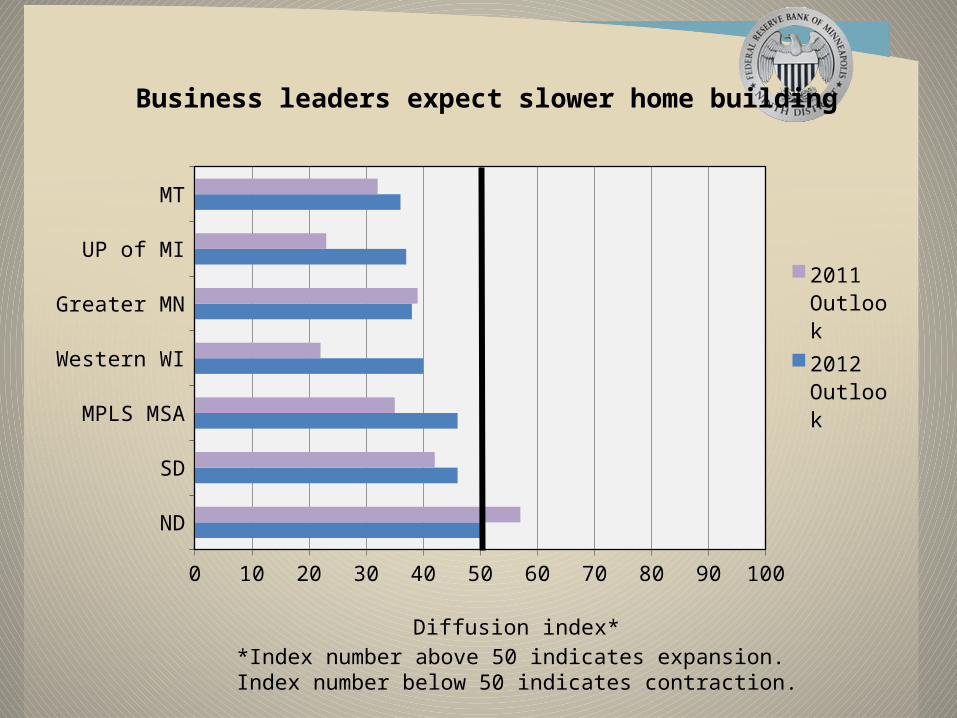

ND

SD

MPLS MSA

Western WI

Greater MN

UP of MI

MT

0 10 20 30 40 50 60 70 80 90 100

2011 Outlook

2012 Outlook

Diffusion index*

Business leaders expect slower home building

*Index number above 50 indicates expansion. Index number below 50 indicates contraction.

Ninth District Economy: Growth in 2012

• Business leaders remain optimistic

• Employment up, modest unemployment rate reductions

• Small wage and price increases

• Agriculture sector strong & manufacturing upbeat

• Slow home building sector

Questions?

![Take Charge of Your Money when you leave your job LFD0405-0574 [Presenter's Name] [Presenter's Title] [Presenter's Firm Information] [Date of Presentation]](https://img.pdfslide.net/doc/110x75/56649e845503460f94b85de9/take-charge-of-your-money-when-you-leave-your-job-lfd0405-0574-presenters.jpg)