Embed Size (px)

Citation preview

2013 Budget Review

June 2013

2 2013 Budget Review ª Eastern Africa

ASSURANCE • Accounting Compliance and Reporting • Financial Statements Audit • Financial Accounting and

Advisory Services • Fraud, Investigations and Dispute

Services (FIDS) • Climate Change and

Sustainability Services

TAX • Business Tax Advisory • Compliance Reporting: - Bookkeeping,

Payroll & Tax Accounting • Revenue Authority Dispute

Resolution Services • Transaction Tax: - Tax modelling

and documentation, Tax due diligence, Pre-deal structuring & Post-deal implementation

• International Tax Services: - Transfer Pricing, Tax Efficient Supply Chain Management

• Human Capital: - Expatriate Tax & Immigration Services

• Africa Tax Coordination Services

TRANSACTION ADVISORY SERVICES (TAS) • Infrastructure Advisory: -

Modelling, Public Private Partnerships & Concessioning

• Project Finance • Transaction Support: - Due Diligence • Valuation & Business Modelling • Transaction Integration • Transaction Real Estate: - Feasibility

studies and financing • Mergers & Acquisition (Deals) Advisory • Restructuring: - Insolvency & liquidation

ADVISORYIT risk and assurance • IT transformation • IT assurance & risk management • Information management and analytics

Performance Improvement • Finance • Customer • IT advisory • Supply chain • People and organisation • Performance and reward

Risk Advisory • Actuarial services • Internal audit • Internal controls • Risk management

Our ServicesOur African Footprints

In our region- Kenya, Uganda, Rwanda, Tanzania, Ethiopia and South Sudan we aim to be the leading and fastest growing firm.

Be the Best & First Choice

Our Mission

To attract and retain the best people and to operate with the highest integrity and professional excellence in adding value to our clients, and in achieving the highest growth in the markets that we serve.

Our Vision

To be recognised as the professional services firm of choice and trusted business advisor who contributes most to our people, our clients and most stake holders by creating confidence and value through Quality in Everything We Do.

Our Values StatementsWho we are and what we stand for: • People who demonstrate integrity,

respect, and teaming. • People with energy, enthusiasm, and

the courage to lead. • People who build relationships based

on doing the right thing.

3 2013 Budget Review ª Eastern Africa

Our Services Contents

2013 KENYA HIGHLIGHTS 4

ECONOMIC PERFORMANCE 5

BUSINESS AND PERSONAL TAXATION 10

CUSTOMS AND EXCISE DUTY 12

OTHER LEGISLATION 14

2013 UGANDA HIGHLIGHTS 16

2013 TANZANIA HIGHLIGHTS 17

2013 RWANDA HIGHLIGHTS 18

4 2013 Budget Review ª Eastern Africa

The global economy is expected to steadily grow at rates of 3.4% and 4.0% in 2013 and 2014 respectively. The Kenyan economy is expected to grow at 5.8% in 2013 up from 4.6% in 2012 and rising to 7% in the medium term according to government growth projections.

The average inflation rate in the country is expected to decline to 5% from 7% in the foreseeable future.

Corporation Tax • Capital gains tax to be re-introduced

Personal Taxes • Exemption of group life and group

personal accident policy premiums paid by employer

• Exemption period for persons with disability to be extended from three to five years

2013 KENYA HIGHLIGHTS

Value Added Tax (VAT) • The Cabinet Secretary has promised to

re-table the VAT Bill before parliament.

Customs Duty • Customs warehouse rent introduced • Exemption on importation of items used

to facilitate railway operations • Railway development levy of 1.5% on all

imported goods introduced • Proposal to increase import duty on;

ª millstones and grindstones from 0% to 25%

ª welding electrodes from 10% to 25% ª plastic tubes from 10% to 25%

Excise Duty

• Proposal to make new Excise Duty legislation which is aligned to the constitution

• Remission on senator keg beer reduced from 100% to 50%

Financial Sector • Amendments proposed to relax the

ownership structure of the insurance companies, brokerage firms and insurance agents. These amendments are aimed at lifting the hitherto requirement which restricted ownership of the aforementioned entities to Kenyan citizens only.

• The Insurance Act and the Retirement Benefits Authority Act to be overhauled to align them with best international practices and the Constitution.

Miscellaneous Provisions • Additional regulations proposed to

ensure effective streamlining of the Public Finance Management Act

• The Biashara Kenya Bill to be formulated to expand economic opportunities for women, youth and persons with disability

• Proposal to reform the Public Procurement Act in order to streamline the procurement process

• Proposal to establish a single tax appeal body to be tabled before parliament to improve dispute resolution framework

• The Capital Markets Authority Act to be amended with a view to fast track the integration of the East African Community

5 2013 Budget Review ª Eastern Africa

ECONOMIC PERFORMANCE

Global Economic Outlook

• During the year 2012, the global economy experienced a slowed recovery against the backdrop of a recession in the Euro Area and unexpected reduction in economic activities of many emerging market economies. While there was reduced domestic demand in high-income countries, capital flows to developing countries increased marginally. Growth in global trade volumes declined to 2.8% in 2012 compared to 6% in 2011. As a result, the world economy shrunk to 3.2% growth in 2012 compared to 3.9% registered in 2011

• Europe economic performance still appears to be depressed. However, as a result of moderate increase in private consumption the USA economy grew by 2.2% in 2012 compared to 1.8% recorded in 2011. Japan experienced an improved real GDP growth of 1.6% in 2012 explained by the significant reconstruction spending arising from the destruction caused by the 2011 East Japan Earthquake and Tsunami

• Growth in several major developing countries (Brazil, India and, to a lesser extent, Russia, South Africa and Turkey) was significantly slower in the year 2012 than it was in year 2011, mainly reflecting policy tightening initiated in late 2011 and early 2012 and weaker demand from the advanced economies

• Despite a strengthening of activity in the United States and Japan, global growth and world trade still remains low and the world economy finds itself in downside scenario. The medium-term challenge represented by high debts and slow growth in high-income countries has not been resolved and could trigger sudden adverse shocks. If the debt crisis in Euro area expands and large economies deny financing to several additional European economies in the crisis, the outturns could be much worse. Additional risks to the

outlook include the political tensions in the Middle East.

African Economic Outlook • In 2012, Africa economy remained

robust despite headwinds from the global economy. African growth remained relatively broad-based and stable, with oil production, mining, agriculture, services and domestic demand as the main drivers, mitigating the adverse effects from global turbulences. Trade growth was supported by the increasing diversification of trading partners, particularly with China. On average, Sub Sahara Africa economy grew by 5.3% in 2012. However, growth was subdued in several African countries due to poor export performance, political and social tensions especially in Mali and Guinea.

• It is expected that Africa economy performance will remain favourable, supported by expanding extractive sector and increasing Foreign Direct Investments (FDIs) due to persistent EURO crises as well as gradual improvement of global economic conditions mainly in USA and Japan. However, risks to economic growth remain weighted on the downside as heightened uncertainty from the Euro Area crisis and Mid-East political tension may shave growth in Sub-Saharan Africa downwards in the year 2013, as merchandise exports, tourism receipts, commodity prices and remittances, all important growth drivers remain highly vulnerable.

6 2013 Budget Review ª Eastern Africa

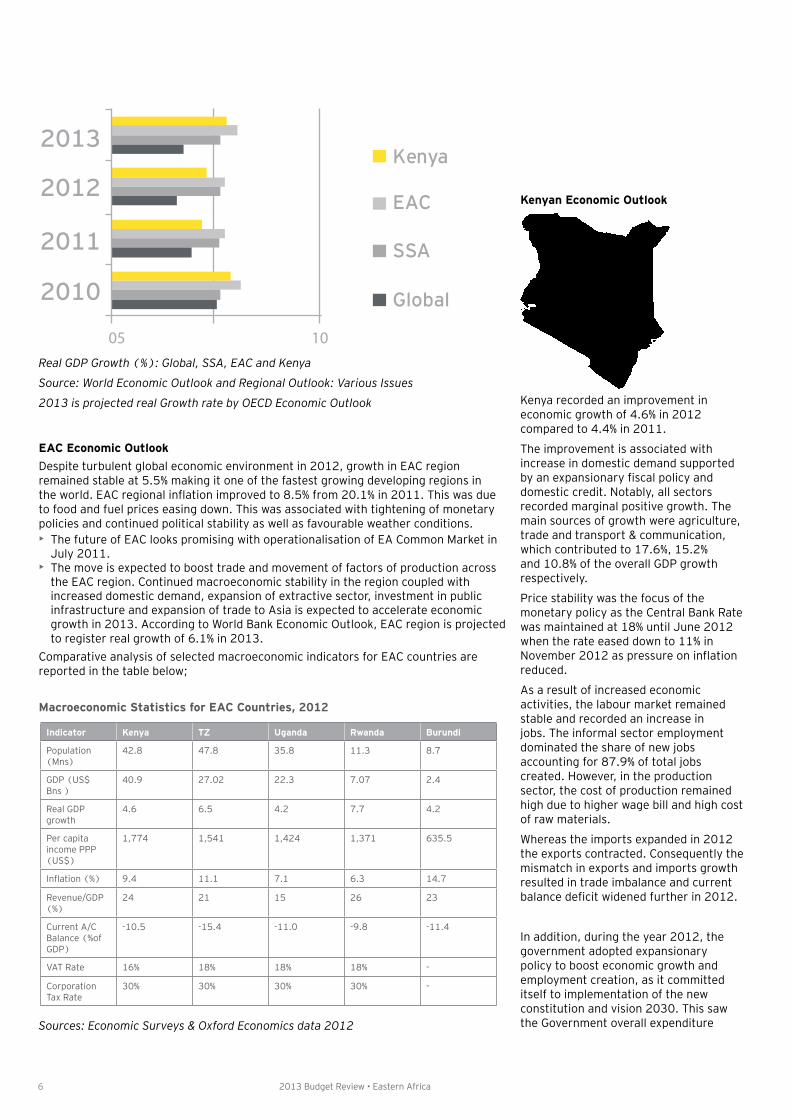

Real GDP Growth (%): Global, SSA, EAC and Kenya

Source: World Economic Outlook and Regional Outlook: Various Issues

2013 is projected real Growth rate by OECD Economic Outlook

EAC Economic Outlook

Despite turbulent global economic environment in 2012, growth in EAC region remained stable at 5.5% making it one of the fastest growing developing regions in the world. EAC regional inflation improved to 8.5% from 20.1% in 2011. This was due to food and fuel prices easing down. This was associated with tightening of monetary policies and continued political stability as well as favourable weather conditions.

• The future of EAC looks promising with operationalisation of EA Common Market in July 2011.

• The move is expected to boost trade and movement of factors of production across the EAC region. Continued macroeconomic stability in the region coupled with increased domestic demand, expansion of extractive sector, investment in public infrastructure and expansion of trade to Asia is expected to accelerate economic growth in 2013. According to World Bank Economic Outlook, EAC region is projected to register real growth of 6.1% in 2013.

Comparative analysis of selected macroeconomic indicators for EAC countries are reported in the table below;

Macroeconomic Statistics for EAC Countries, 2012

Sources: Economic Surveys & Oxford Economics data 2012

Kenyan Economic Outlook

Kenya recorded an improvement in economic growth of 4.6% in 2012 compared to 4.4% in 2011.

The improvement is associated with increase in domestic demand supported by an expansionary fiscal policy and domestic credit. Notably, all sectors recorded marginal positive growth. The main sources of growth were agriculture, trade and transport & communication, which contributed to 17.6%, 15.2% and 10.8% of the overall GDP growth respectively.

Price stability was the focus of the monetary policy as the Central Bank Rate was maintained at 18% until June 2012 when the rate eased down to 11% in November 2012 as pressure on inflation reduced.

As a result of increased economic activities, the labour market remained stable and recorded an increase in jobs. The informal sector employment dominated the share of new jobs accounting for 87.9% of total jobs created. However, in the production sector, the cost of production remained high due to higher wage bill and high cost of raw materials.

Whereas the imports expanded in 2012 the exports contracted. Consequently the mismatch in exports and imports growth resulted in trade imbalance and current balance deficit widened further in 2012.

In addition, during the year 2012, the government adopted expansionary policy to boost economic growth and employment creation, as it committed itself to implementation of the new constitution and vision 2030. This saw the Government overall expenditure

Indicator Kenya TZ Uganda Rwanda Burundi

Population (Mns)

42.8 47.8 35.8 11.3 8.7

GDP (US$ Bns )

40.9 27.02 22.3 7.07 2.4

Real GDP growth

4.6 6.5 4.2 7.7 4.2

Per capita income PPP (US$)

1,774 1,541 1,424 1,371 635.5

Inflation (%) 9.4 11.1 7.1 6.3 14.7

Revenue/GDP (%)

24 21 15 26 23

Current A/C Balance (%of GDP)

-10.5 -15.4 -11.0 -9.8 -11.4

VAT Rate 16% 18% 18% 18% -

Corporation Tax Rate

30% 30% 30% 30% -

2013

2012

2011

2010

Kenya

EAC

SSA

Global

05 10

7 2013 Budget Review ª Eastern Africa

expand to KShs 1.45 trillion in 2012/2013 compared to KShs 1.165 Trillion in 2011/2012. Over two thirds of government expenditure went to current expenditure while development expenditure accounted for a third. Most of development expenditure went to infrastructural expansion and development, while a large amount of current expenditure was spent on public sector workers’ wages and salaries as the government commenced implementation of the new constitution.

Selected Macroeconomic Indicators

Inflation: Average overall annual inflation decreased from 14.0% in 2011 to 9.4% in 2012. The decline is attributed largely to better food supply resulting from favourable weather conditions experienced during the year and tight monetary policy that was adopted by CBK at the beginning of 2012.

Exchange Rate: Overall, the Kenya Shilling depreciated against most world currencies as measured by trade weighted exchange rate index, which rose by 1.5% to 110.8 in 2012 from 109.3 in 2011. The depreciation could be attributed to the global economic volatility resulting from Euro Zone credit crisis and currency speculation activities in the foreign exchange market. This was coupled by high current account deficit resulting from higher imports vis-a-vis exports. However the shilling was strong against some currencies like the Japanese Yen, Pakistan Rupee and Indian Rupee. Equally, the shilling gained relatively against the other East African Community member currencies.

Interest Rate: In 2012, Central bank principal interest rates decreased compared to end of 2011 as the CBK intervened to contain weak shillings and high inflation. The CBR, the Repo rate, the 91 day Treasury Bills rate and inter-bank rate dropped substantially to stand at 11%, 6.9%, 8.3% and 5.9% respectively at the end of 2012. The commercial bank lending rates and overdraft interest rates eased to 18.1% and 17.9% respectively lower than 2011. The average deposit rates remained low at 6.8% while saving deposit rates increased to 1.6% compared to 1.46 in 2011. On average, the interest rate spread has been on a downward trend falling from 13.05 points in December 2011 to 11.35 points in December 2012.

The decline in interest rates implies a decrease in cost of borrowing by consumers in the local financial markets, which has a positive effect on overall domestic consumption (and demand).

Inflation Rate and Selected Nominal Interest Rates Reported at end of each Year (%)

Source: Economic survey 2013

25.00%

20.00%

15.00%

10.00%

5.00%

0.00%

2010 2011 2012

91 Day Bill

CBR

Average Deposit Rate

Loans & Advances Rate

8 2013 Budget Review ª Eastern Africa

Capital Market

Equity market remained active in 2012; however, the market recorded a drop in performance. The value of shares traded in the NSE dropped by 3.5% from 5.7 billion in 2011 to 5.5 billion in 2012. NSE index went up by 29% to 4,133 in 2012 compared to the 2011 index of 3,205 points. Market capitalisation as at end of December 2012 increased by 46.5% to stand at KShs 1,272 billion compared to KShs 868 billion recorded in the year 2011. The bond market recorded an increase in turnover by 16.7% to KShs 565 billion in 2012 up from Kshs 446 billion in 2011.

Sector Analysis

Agriculture and forestry sector recorded the highest contribution to the GDP growth in 2012 accounting for 17.6% of the overall performance, which reflected a recovery from adverse weather in 2011.

Contribution of trade, transport and communication, manufacturing and financial intermediation sectors to the GDP in the year 2012 declined marginally, with each contributing 15.2%, 10.8%, 6.5%, and 6.1% respectively.

Sectors Contribution to GDP & Sources of Growth

Source: Economic Survey 2013

Agriculture

Agriculture continued to be a key contributor to the economy. The sector recorded a growth of 3.8% compared to a growth of 1.5% in 2011. The positive growth is mainly due to favourable weather conditions experienced during the year under review.

Transport and Communication

The sector posted a slower performance by registering a growth of 4% in 2012 compared to a growth of 4.7% in 2011. This was mainly attributed to transport and storage subsector, which recorded a slower rate of growth at 3.1% in 2012 compared to 4.9% in 2011. However the total quantity of import and export handled at the port of Mombasa increased by 10.6% and 9.2% respectively in 2012. On the other hand, aviation subsector was adversely affected by sluggish recovery of the global economy especially in Euro Zone.

However, communication subsector, especially mobile telephony continued to thrive with subscriber base expanding to 29.7 million up from 25.3 million in 2011. The growth of the subsector is further associated with growth in internet market and mobile money transfer services.

Manufacturing

The sector contributed about 9.2% of GDP in 2012 recording a slower growth of 3.1% compared to 3.4% in 2011. The slow growth is largely attributed to high cost of production and strong competition from imported goods. There is need to address challenges facing the sector if the country is to achieve Vision 2030; the vision identifies manufacturing sector as the leading sector to propel the country’s economic growth. There is need therefore to diversify industrial production and value adding in agricultural sector as a means of promoting agribusinesses, which can eventually grow to large industries.

Financial sector

The sector recorded a slower growth of 6.5% in 2012 compared to 7.8% recorded in 2011. The low performance is associated with a decline in credit from 30.8% in 2011 to 10.8% following tightening of the monetary policy in 2011. The Central bank rate decreased from 18% in December 2011 to a low of 11% in December 2012. The intervention of Central Bank saw principal interest rates decrease as at the end of December 2012 compared to end of 2011. On average consumer prices declined resulting to a decrease in inflation from 14.0% in 2011 to 9.4% in 2012.

Industry % Contribution to GDP Sources of Growth in %

2011 2012 2011 2012

Agriculture & Forestry

24.40% 25.90% 7.60% 17.60%

Manufacturing 9.60% 9.20% 7.60% 6.50%

Electricity and water supply

0.90% 1.40% -1.30% 4.80%

Mining and Quarrying

0.70% 0.70% 0.70% 0.40%

Wholesales & Retail Trade

10.60% 10.20% 17.40% 15.20%

Hotels & Restaurants

1.70% 1.60% 1.50% 0.80%

Building & Construction

4.10% 4.10% 3.50% 3.70%

Transport and Communication

9.70% 9.30% 12.70% 10.80%

Financial Intermediation

6.40% 5.20% 7.30% 6.10%

Real Estate, Renting & Business services

4.50% 4.30% 4.30% 3.80%

Education 5.80% 5.50% 6.50% 6.10%

Health and Social Services

2.40% 2.40% 1.70% 1.60%

9 2013 Budget Review ª Eastern Africa

Economic Outlook for 2013 and Beyond

Kenya’s growth is expected to reach 5.65% in 2013. The projected growth is anchored on the just concluded peaceful General Elections of March 2013 and a smooth transition of power, which has renewed business confidence, thus strengthening prospects for the economy. Projected economic growth and development will be supported by continued macroeconomic stability, expanded infrastructure development and capacity that will enhance regional and global competitiveness, improved business environment, balanced regional development and competitive sound financial sector. Domestic investment is expected to increase as political risks diminish. Further, the discovery of oil and gas reserves in Kenya will attract high Foreign Direct Investments (FDI) flows to finance exploration during the year 2013 and beyond.

We expect the Government to continue with expansionary policy aimed at accelerating high growth rate, employment creation and improved food security while addressing development agenda as envisioned in the Vision 2030 and the new constitution (especially new initiated devolution). Most of current expenditure will be used to fund Government bureaucracies as the country moves to set up structures for the devolved government.

Fiscal consolidation needs to be a priority as the new Government continues to restructure its administration. This notwithstanding, it is expected that with the devolved government in place there will be a positive contribution to the development of the country’s economy. Political uncertainties, marginalization, excessive waste of natural resources, excessive political intolerance, gagging as well as cut-throat political competition have become the order of the day. The devolved government is therefore a new dawn and it is expected that Kenyans will be electing responsible leaders who are development oriented to govern the devolved units.

In trying to achieve the projected economic growth the new Government needs to be aware of the following risks: the impact of continued sluggish performance in the Euro Zone and the possible fiscal cliff in the USA; the potential impact of monetary policies that

are too accommodative and possible disturbances in the commodity markets; the need to balance between fighting inflation and supporting growth; possible fluctuations in the foreign exchange rate and other economic disturbances; the growing current account deficit; and the potential fiscal risk that may arise from the devolution of power to 47 county governments.

To consolidate on gains made, the Government’s monetary policy needs to ensure low inflation, favourable long-term interest rates and competitive exchange rates. The fiscal policy will include tax reforms geared to ensuring efficient and effective collection of revenue, deepening of tax reforms to enhance tax compliance and reduced tax evasion.

Further, the Government needs to focus on enhancing productivity of the various inputs and processes involved in the economic production processes. The focus has to be on addressing supply constraints in the different sectors of the economy and to adopt policies that exploit and enhance domestic inter-linkages in the economy and further boost productivity growth.

The business environment needs urgent upgrading especially with regard to business regulation and procedures, service delivery by public institutions, law and order and resolution of commercial disputes. Finally, there is need to concentrate on improving technological readiness, especially innovation and adoption of improved technologies. The cluster development strategy, which involves putting similar businesses into one category in order to address their needs based on their uniqueness, is increasingly being adopted as an economic tool for improving growth and competitiveness. It is, therefore, advisable that the country considers the use of this strategy in its development efforts.

BUDGET REVIEW 2013/2014Expenditure

The expenditure has been estimated at KShs 1.6Trillion.

This is made up of 58% government recurrent expenditure and 42 % development expenditure.

Expenditure AllocationThe estimated expenditure has been allocated as detailed in the chart below:

Revenue Estimates

The Revenue estimates for 2013/14 fiscal year is KShs 1.027 Trillion representing 7.5% increase over 2012/13 budget estimate. The revenue is made up of 93% in form of ordinary revenue and 7% from Appropriation-in Aid. This total revenue represents 24.5% of the GDP.

2013/14 Expenditure Allocation

Environmental, water & housingAgricultureEnergy & infrastructureNational healthSecurityGovernanceEducationOthers

21%

10%7%

3%

22%

4%6%

27%

10 2013 Budget Review ª Eastern Africa

BUSINESS TAXATIONCapital Gains Tax

The Capital Gains Tax (CGT) was introduced on 1 January 1975. CGT was subjected to property (land and buildings) and marketable securities. The withholding tax rate applicable was 2.5% and 7.5% for property and marketable securities respectively.

The CGT on property was subjected to a reduction formula in a bid to enable inflation indexing. This avoided the taxation of gains accrued as a result on inflationary effects.

To propagate the growth of capital markets and encourage property owners dispose of idle land for development, the taxation of gains arising from property and marketable securities was suspended in 1985. The Minister for Finance, through 2006 Finance Bill, made an attempt to re-introduce the CGT but the amendment was reversed through a

motion in the National Assembly.

To increase revenue towards National Development, the Cabinet Secretary has initiated a review of the capital gains tax regime. This will bring to tax income from sources considered capital in nature which have previously been exempt from Income tax in Kenya.

Implications of reintroducing capital gains include:

• The introduction of CGT might act as a disincentive to property market since it is an additional cost to the transferors, and by extension the transferees who will have to bear the additional cost of tax to cater for the transferors full return on investment.

• The economy may be marked by slow growth in our capital markets due to increased cost relating to CGT.

• The government is expected to spend more upon purchase of land to resettle landless citizens and expand infrastructure projects.

BUSINESS AND PERSONAL TAXATION

11 2013 Budget Review ª Eastern Africa

Taxation of winnings from Gaming and Betting

The Finance Bill 2011 introduced withholding tax on winnings from betting and gaming at a rate of 20%. However, this was repealed by the Finance Act 2012 but will be re-introduced in the Finance Bill 2013. This amendment captures gains from casinos and lotteries and is a clear move by the Cabinet Secretary to bring such income chargeable to tax in Kenya. Previously these were deemed “windfall gains” not subject to withholding tax.

Compounding of Tax Offences

Under Section 114 of the Income Tax Act, the Commissioner could, with the approval of the Minister compound an offence and order a tax payer to pay the associated fine. The Cabinet Secretary has proposed to improve the compounding framework with a view of encouraging tax payers with tax offences to engage KRA and settle disputes outside court. One way of achieving this intention would be to eliminate the bottlenecks associated with the approval by the Cabinet Secretary in the compounding process.

Offences by corporate bodies

The Cabinet Secretary has proposed to amend the Income Tax Act to empower the Commissioner to collect tax from officers of corporate bodies where a body corporate is convicted of an offence. This provision had been introduced in the 2011 Finance Bill but was repealed in the Finance Act 2012.

By shifting tax risks to the Senior Officers of a company, this measure is geared towards enhancing tax compliance. Whereas the Cabinet Secretary’s intent is to promote tax compliance among taxpayers, this amendment can be viewed as punitive to such officials of the company.

Rental Income

The Cabinet Secretary has issued a directive to KRA to leverage on technology in mapping out all rental properties in urban areas to ensure that rental income is subjected to tax. This is in the backdrop of failure by the KRA to achieve the targeted revenue levels in this sector.

Tax Rates

There have been no changes in the corporate tax rates which has remained at 30%.

PERSONAL TAXATIONInsurance Premiums

Currently, an amount paid by an employer as a premium for insurance on the life of his employee and for the benefit of that employee or any of his dependants other than that contributed to a pension scheme, is deemed to be a taxable benefit.

However, there is controversy as to whether group life policies and group personal accident policies are a taxable benefit on employees.

The Cabinet Secretary has proposed that premiums paid by the employer to such covers be exempt where they do not confer a benefit on the employee.

Persons with Disabilities

In 2009, the Minister amended the Persons with Disabilities Act to exempt employees with disabilities from tax on all income accruing from their employment. The period of validity of their exemption certificate is 3 years.

The Cabinet Secretary in his speech proposed to extend the exemption period to 5 years which will be in harmony with the exemption provided for under Paragraph 10 of the 1st schedule to the Income Tax Act.

Tax Rates, Personal Relief and Tax Bands

No changes in tax rates, personal reliefs or brackets. Top personal tax remains at 30%.

12 2013 Budget Review ª Eastern Africa

CUSTOMS AND EXCISE DUTY

CUSTOMS

The Ministers for Finance from the EAC Partner States, agreed to effect changes in the Common External Tariff (CET) and amend the EAC Customs Management Act, 2004 as follows:-

Kenya Specific Custom AmendmentsCustoms warehouse rent

In a bid to reduce congestion at the ports, the Minister proposed to introduce customs warehouse rent for entered goods which remain at the port for a period exceeding 21 days from date of commencement of discharge of the carrier. In the past, traders have left their cargo at the ports while mobilizing funds to pay taxes for long periods of time hence congesting the port without payment of demurrage/rent.

Not only will this proposed measure decongest the port but enable the Government to raise more revenue.

General Amendments Affecting All EAC Partner StatesDuty Exemptions • Import duty to be exempted on

importation of items used to facilitate railway operations

• Exemption of plastic bag biogas digesters

Railway Development Levy • Introduction of a railway development

levy of 1.5% on all imported goods – to fund construction of a standard gauge railway line from Mombasa to Kisumu (expected to be completed in 3 years time).

Proposal to increase import duty on the following: • welding electrodes from 10% to 25% • millstones and grindstones from 0%

to 25% • plastic tubes for packing of toothpaste,

cosmetics and similar products from 10% to 25%

EAC integration developments

The 2013/14 EAC Budget speech was presented to the East African Legislative Assembly on 30 May 2013. The Customs and International Trade related priorities for the coming financial year included:

• Consolidating the Common Market with

13 2013 Budget Review ª Eastern Africa

emphasis on operationalization of the free movement of labour provisions as well as the integration of the regional financial markets to enhance movement of capital

• Interventions in the Customs Union leading to establishment of a single customs territory. Under the single customs territory, payment of duty will be at the first port of entry, legal framework will be common to all EAC states, circulation of goods will have minimum border control and there will be an interconnected payment system

• Completion of the movement towards the East African Monetary Union

• Investment promotion and private sector development through the public private partnership framework with a regional dimension

• Cooperation in cross border infrastructure through joint projects to improve infrastructure

EXCISE DUTYTax Remission

The remission on Senator Keg beer has been reduced from 100% to 50%

stated at the time that the Bill would be easier to administer and that it would resolve the perennial VAT refund issues faced by taxpayers. In his ministerial statement read on 8th June 2011 in place of the 2011/2012 budget, the Minister reported that a task force he had constituted had completed the work, and that a draft VAT Bill was ready. The proposed VAT Bill was released on 26th July 2011. The Bill was not enacted after intense lobbying by the stakeholders.

After considering the views of the various stakeholders, the Minister reintroduced the Bill during the 2012/2013 budget, which was again not enacted in 2012/13.

In the 2013 Budget speech, the Cabinet Secretary has promised to re-table the VAT Bill, which aims to simplify, modernize and reduce cost of compliance. The enactment of the VAT Bill is expected to raise an additional Kshs 10 Billion to the Exchequer. The Cabinet Secretary has promised to release the Bill in due course.

Description/ item As per the VAT Act As per the VAT Bill 2012

Reverse VAT Account for both taxable and exempt supplies

Account for only exempt supplies

VAT Rate on electricity and heavy industrial oils 12% 16%

Remission Provided for scrapped

Withhold VAT system Provided for scrapped

Advance rulings No provision Introduced

Supplies to Oil and Gas Exploration companies Taxable at 16% Zero rated

Appointment of Tax Representative No provision Introduced

Period of claiming input tax 12 months 3 months

Processed milk, maize and wheat flour, bread, air craft & spare parts, equipment for electric power generation, books & journals, computer and computer software, agricultural tractors, ploughs, dairy machine, poultry incubators, machinery for sugar manufacture, fertilizers, sanitary towels, napkins, feeding bottles

Zero rated VAT at 16%

Exportation of goods and taxable services, medicaments Zero rated Zero rated

Cut flowers, wood charcoal, bran, cinematographic film, wooden coffins, hides and skins, credit rating bureau services, tour operation, travel agency services, transportation of tourists, landing and parking services provided for aircraft

Exempt VAT @ 16%

Financial services, insurance services, petroleum oils, motor spirit, aviation spirit, natural gases in gaseous status

Exempt Exempt

Unprocessed milk Zero rated Exempt

on the basis that the initial objective of discouraging illicit brews was not achieved. Instead, the government has extended the 50% remission to brewers of beer made of millet, sorghum and cassava. The Senator Keg will however enjoy 50% remission only for a period of the next 3 years.

This will increase the cost of the Senator Keg but at the same time stimulate agricultural activity by increasing demand for millet, sorghum and cassava.

Administrative Proposal

The Cabinet Secretary has proposed capital to align excise duty legislation with the constitution and also issue a gazette notice that will give guidelines on effective operation of the excisable goods management system.

VALUE ADDED TAX (VAT)

In the 2011 Budget speech, the then Deputy Prime Minister and Minister for Finance promised to overhaul the VAT legislation and submit a new Bill. He

Below is a summary of comparison between the VAT Bill 2012 and the VAT Act:

14 2013 Budget Review ª Eastern Africa

Financial Sector Banking Act (Cap. 488)

Banking Act stipulates penalties for various offences key among them advancement of loans or credit facilities contrary to the provisions of the Act, as follows:

• A fine not exceeding KShs 150,000 for a body corporate; and

• A fine not exceeding Kshs 50,000 or imprisonment for a term not exceeding two years or both for a person or an officer of an institution.

The Act has been amended to increase the above penalties with the aim of deterring unethical or illegal banking activities.

Insurance Act (Cap. 487)

Insurance Act Overhaul: IRA has been mandated to initiate an overhaul of the Insurance Act to align it with best international practices and the Constitution. The overhauling process is expected to bring forth two pieces of legislation as follows:

• Legislation on the establishment of IRA and;

• Legislation covering regulatory issues of the market.

The drafts of the above pieces of legislation are expected by 30 September 2013. The overhaul is aimed at strengthening the regulatory framework to ensure a stable and growing insurance sector.

Insurance Firms: Only body corporates with at least one third of the controlling interest (whether in terms of shares, paid up share capital or voting rights) wholly owned by citizens of Kenya or by partnerships whose partners are all citizens of Kenya or by a body corporate whose shares are owned by citizens of Kenya or is wholly owned by the Government, are eligible for registration.

Proposed amendment opens up the ownership of insurance companies and brokerage firms to citizens of the EAC.

The amendment is expected to enhance the implementation of the EAC Common Market protocol and deepening regional integration.

OTHER LEGISLATION

Insurance Agency: ownership of insurance agencies are currently restricted to Kenyan citizens.

A proposal has been made to open up the ownership of insurance agencies to foreigners.

This amendment is aimed at encouraging multinational banks to conduct bancassurance and deepen insurance penetrations in Kenya.

Insurance Regulatory Authority (IRA): The IRA had been given leeway to appoint any person regardless of his/her competency to assume the management, control and conduct of the affairs and business of an insurer. The requirement to appoint persons familiar with the business of insurers was restricted to appointment to the board of directors to hold office as directors.

The amendment mandates IRA to appoint a competent person familiar with the business of the insurer while intervening in the management of such an insurer.

The move will shield policyholders from the lengthy resolution mechanisms that tend to delay compensation.

Policyholders Compensation Fund: the fund’s role was principally compensation of policyholders upon insolvency of an insurer.

The amendment expands the mandate of the Fund to include participation in the liquidation process of insurance companies.

Microfinance Act

The Microfinance Act became operational in 2008 and was aimed at streamlining the operations of the microfinance institutions in Kenya.

The Government proposes to amend the Act to give powers to the Central Bank to promptly move into a troubled microfinance institution to forestall the deepening of a financial crisis.

Retirement Benefits Act (No. 3 of 1997)

Retirement Benefits Authority (RBA) has been mandated to initiate an overhaul of the RBA Act to align it with the best international practices and the Constitution.

15 2013 Budget Review ª Eastern Africa

Draft legislation expected by 31 December 2013.

Public Finance Management Act

The Public Finance Management Act was enacted in 2012 with the aim of streamlining the management of public finance consistent with Chapter 12 of the 2010 Constitution of Kenya which provides the principles and framework of public finance, among them openness, accountability, public participation and equity.

To ensure effective implementation of the Public Finance Management Act, the government proposes to introduce additional regulations.

Biashara Kenya Bill

Unemployment among the youth, women and persons with disability is high in Kenya yet they have talents and skills that can be tapped.

Youth, Women and Persons with Dis-ability

To ensure the participation in economic opportunities, the government will be formulating the Biashara Kenya Bill, which shall provide a one stop shop solution to small and medium size enterprises covering the entire business chain – such as skill and business development, product standardization and branding, access to credit, business incubation services and market access.

Proposal to amend the Public Procure-ment and Disposal Act

The government proposes to reform the Public Procurement and

Under this regime, there have been concerns over independence, transparency of appointment of tribunal members and also delays in resolving disputes.

To improve dispute resolution framework, the government proposes to establish a single tax appeal body to deal with all appeals arising from all taxes. This will also instill professionalism and fast track conclusion of tax cases in compliance with the constitution.

The Capital Markets Authority Act 485

With a view to fast track the East African Community integration, the government proposes to amend this Act to provide for the cross-licensing of persons within the East African Region on equal terms as long as they are licensed in their respective countries and to enable the CMA to issue regional fixed income securities such as treasury bills and bonds. Licenses and fixed income securities are currently only valid in the respective countries of issuance. These are new initiatives meant to foster intra-regional capital flows.

The government also proposes to make provisions to enable pooling of resources through Real Estate Investment Trusts (REITs) to foster real estate development.

Owing to waning public confidence in the integrity of the capital markets, the government proposes to make insider trading an offence of strict liability and identify offences of common market manipulation. This will act as a deterrent to those participating in market manipulation for personal gain.

The Kenya Deposit Insurance Act

Kenya Deposit Insurance Act was enacted in 2012 and seeks to provide for the establishment of a deposit insurance system and the receivership and liquidation of deposit taking institutions. With a view to ensuring adequate protection of depositors, the government proposes to expand the Fund’s mandate and enhance its corporate governance.

Disposal Act, to streamline the procurement process by making it more transparent and supportive of the economic transformation.

This will be done by reducing the time it takes to award the tender to not more than 30 days; ensuring that preference is given to the youth, women and persons with disability whose allocation has been increased from 10% to 30% and local firms that manufacture, assemble, grow, extract or mine goods in priority areas such as construction materials and related supplies, furniture, motor vehicles and foodstuffs.

Railway Development Levy

The government proposes to introduce a Railway Development Levy of 1.5% on all imported goods in order to mobilize funds for the construction of a standard gauge railway line from Mombasa to Kisumu. This will be a key milestone since infrastructure is a key pillar of Vision 2030.The railway line will reduce the cost of transport and the cost of doing business by improving cargo off take from the port of Mombasa; saving our roads from depletion and high maintenance costs and saving on time taken to transport goods from the port of Mombasa to the borders thereby boosting trade and investments.

Tax Appeals Tribunal

There is no standardized procedure or forum for tax dispute resolution. For instance, income tax disputes are handled by the Local Committee, Income Tax Tribunal or the High Court; VAT disputes are handled by the VAT Tribunal, while Customs and Excise disputes are dealt with by the Custom & Excise Appeals Tribunal.

16 2013 Budget Review ª Eastern Africa

The government’s focus is on raising tax revenue, enhancing transparency, improving compliance and encouraging investment.

Corporation tax • No change in corporation tax rate. The

rate remain at 30%

Income tax • Scope of withholding tax on agents

widened to include more tax payers • Enacting a legal framework to collect

small and medium tax payers • Measures to enable URA access

financial information introduced

Value Added Tax (VAT) • No change to the VAT rates. The rates

remain at 0% and 18% • Reintroduction of VAT on supply of

water for domestic use • Hotel accommodation services and

wheat flour brought under taxable • Rationalization of VAT exemptions

Excise Duty • Duty on diesel and petrol increased by

UShs 50 per litre • Duty of UShs 200 per litre on Kerosene

re-introduced • Duty on cigarettes increased • Duty on undenatured spirits increased

from 70% to 140%

• 20% duty introduced on gambling • 10% duty tax on mobile money

transfer and other money transfer operators introduced

Stamp Duty • Introduction of an extra UShs 30,000

of stamp duty on third party insurance policies for motor vehicles

Non tax revenue • Increase of motor cycle registration

fees from UShs 130,000 to UShs 200,000.

• Increase of motor vehicle registration fees by UShs 200,000

• Introduction of a levy on incoming international calls

Reform of tax laws in respect of • Excise duty, Stamp duty, Lotteries,

Gaming and Pool Betting among others • Elimination of exemptions under VAT

and Income Tax Acts • URA To collect all fees and other

charges • Taxation of petroleum and mineral

sector

Decisions made at the EAC Pre-Budget Consultations by the Ministers for Finance. • 0% import duty on Uganda’s raw

materials terminated.

2013 UGANDA HIGHLIGHTS

17 2013 Budget Review ª Eastern Africa

Economic Performance

Real GDP is projected to grow by 7.0% in 2013 and 7.2 percent in 2014.

A single digit annual inflation rate which is expected to decline to 6.0 percent by June 2014

Pay as You Earn (PAYE) • Minimum tax on income of a resident

individual to be reduced from 14% to 13%

Corporation tax • No change in corporation tax rate • 10% withholding tax on commissions

on mobile money transfer services introduced

• 5% withholding tax on services irrespective of whether supplier has tax identification number or not introduced

• 2% withholding tax introduced on supply of goods to government

• Exemption of withholding tax on rental charges of aircraft lease paid to a non-resident by a person engaged in air transport business abolished

Value Added Tax (VAT) • VAT exemption on tourist services to be

abolished • Special relief to domestic producers of

textile who use locally produced cotton to be introduced

Excise Duty • Duty on non-utility vehicles aged more

than 10 years increased from 20% to 25%

2013 TANZANIA HIGHLIGHTS

• Duty rate of 5% on utility vehicles aged more than 10 years introduced

• Duty on various petroleum products amended

• Duty of 15% introduced on imported furniture

• Duty of 14.5% introduced on all mobile services

• Duty on telecommunication services widened to include landlines and wireless telecom services

• Proposal to adjust the specific duty structure on various non-petroleum products by 10%

• Duty rates on various categories of cigarettes amended

Road and Fuel Tolls Act

Proposal to increase fuel levy from TShs 200 per litre to TShs 263 per litre

Skills Development Levy Act

Proposal to reduce the skills development levy from 6% to 5%

Road Traffic Act

Proposal to increase annual motor vehicle license fees

Petroleum Act

Petroleum Levy of TShs 50 per litre introduced

Tanzania Investment Act

The Act to be amended to impose 25% of the applicable import duty rate on goods referred to as “deemed capital goods”

Various Fees and Levies

Proposal to amend rates of fees and various levies charged by Ministries, Regions and Independent Departments in order to rationalize with the current level of economic growth

18 2013 Budget Review ª Eastern Africa

Rwanda continued to achieve moderate inflation, with annual headline inflation falling from 8.3 percent in December 2011 to 3.9 percent in December 2012 and to 3.3 percent in March 2013. Exports in value terms grew by 27 percent in 2012; import growth was 26 percent, leading to a widening trade deficit.

Business taxation • No change in corporation tax rates • Introduction of a royalty tax on the

following minerals: ª 4% royalty tax on the value of extracted minerals on basic metals and

ª 6% on both precious metals and precious stones

Personal taxation • No change in personal tax rates

Value Added Tax • Introduction of Electronic Billing

Machines. The new VAT law requires registered taxpayers to use Electronic Billing Machines (EBM).

International tax • Revision of the Double Taxation

Avoidance Agreement (DTAA) between Rwanda and Mauritius

Miscellaneous – revenue collection measures • Introduction of E-filing and E-payment

of taxes • Introduction of mobile technology in

payment and filing of taxes. • Introduction of Electronic Single

Window • Introduction of Electronic cargo

tracking equipment • Revision of investment code to adapt to

the prevailing business environment. • Introduction of Gold Card Scheme for

compliant taxpayers

2013 RWANDA HIGHLIGHTS

19 2013 Budget Review ª Eastern Africa

ContactsNAME TITLE EMAIL ADDRESS

Partners

Gitahi Gachahi Chief Executive Officer [email protected]

Catherine Mbogo Regional Leader, Tax [email protected]

Geoffrey Karuu Tax Partner, Kenya [email protected]

Herbert Wasike Chief Operating Officer & Regional Leader, Assurance [email protected]

Joseph Sheffu Regional Representative to the ASA Partners’ Forum & Country Leader, Tanzania [email protected]

Zemedeneh Negatu Regional Leader, Transactions Advisory Services (TAS) & Country Leader, Ethiopia [email protected]

Amaha Bekele Regional Leader , ITRA [email protected]

Celestine Munda Regional Leader, Advisory [email protected]

Patrick M Kamau Country Leader, South Sudan [email protected]

Joseph K Cheboror Assurance Partner, Kenya [email protected]

Peter Anchinga Assurance Partner, Kenya [email protected]

Churchill Atinda Assurance Partner, Kenya [email protected]

Peter Kahi Fraud Investigations & Dispute Services (FIDS) Partner, Kenya [email protected]

Avani S. Gilani Assurance Partner, Kenya [email protected]

Muhammed SSempijja Country Leader, Uganda [email protected]

Michael Kimoni Assurance Partner, Uganda [email protected]

Geoffrey Byamugisha Assurance Partner, Uganda [email protected]

Allan Gichuhi Country Leader, Rwanda [email protected]

Neema Kiure Mssusa Assurance Partner, Tanzania [email protected]

Yared Berhane Advisory Partner, Ethiopia [email protected]

Laban Gathungu Advisory Partner, Kenya Laban.Gathunguke.ey.com

Anthony Muthusi Transactions Advisory Services (TAS) Partner, Kenya [email protected]

Julius Ngonga Transactions Advisory Services (TAS) Partner, Kenya [email protected]

Silke Mattern Tax Partner, Tanzania [email protected]

Russell Maynard Tax Partner, Tanzania [email protected]

KENYA (country code 254)Nairobi Ernst & YoungP.O. Box 44286-00100 GPO, Nairobi, KenyaKenya Re Towers, Upper Hill, off Ragati Road, Nairobi, KenyaTel: +254-20-2715300Mobile: +254-0722-806613, +254-0722-205393, +254-0733-687081Email: [email protected]

NakuruP.O.Box 45 - 20100 GPO, Nakuru, KenyaKenya Commercial Bank Bldg, Kenyatta AvenueTel: +254-51/2211591/2 Email: [email protected]

MombasaP.O. Box 99361-80107, Mombasa, KenyaMombasa Trade Centre, 6th Floor North Tower,Nkrumah Road, MombasaTel: +254-041-2313292/3Email: [email protected]

UGANDA (country code 256)KampalaP.O. Box 7215, Kampala, UgandaErnst & Young House, 18, Clement Hill Road,Shimoni Office VillageTel: +256-414343520/4, +256-414349534/7Email: [email protected]

Rwanda (country code 250)KigaliP O Box 3638, KigaliBank of Kigali Building, Avenue de la PaixTel: +250-788-309977, +250-788-303322Email : [email protected]

TANZANIA (country code 255)P O Box 3638, KigaliBank of Kigali Building, Avenue de la PaixTel: +250-788-309977, +250-788-303322Email : [email protected]

ETHIOPIA (country code 251)Addis AbabaP.O. Box 24875-1000, Addis Ababa, EthiopiaAfrica Avenue, Mega Building, 11th FloorTel +251-11-5504933 Fax: +251-11-5504932E-mail: [email protected]

DJIBOUTI & SomaliaRefer all engagements and enquiries to GitahiGachahi, Nairobi, Kenya,Tel: +254-20-2715300

SOUTH SUDAN (country code 211)Tong Ping, Off Airport Road, off UNMISS Road, Vivacell/SPLM Driveway,Central Equatorial, Juba, South SudanTel: +211 920002151/2 | Office: +211 959003340/1Email: [email protected]

Ernst & Young

Assurance | Tax | Transactions | Advisory

About Ernst & YoungErnst & Young is a global leader in Assurance, Tax, Transaction and Advisory Services. Worldwide, our 167,000 people are united by our shared values and an unwavering commitment to quality. At Ernst & Young we are committed to achieving potential. It’s how we make a difference for our people, our clients and our wider communities.

About Ernst & Young Tax ServicesEffective compliance and open, transparent reporting are the foundations of a successful tax function. Tax strategies that align with the needs of your business and recognize the potential of change are crucial to sustainable growth. So we create highly networked teams who can advise on planning, compliance and reporting and help you maintain effective tax authority relationships — wherever you operate. Our technical networks across the globe can work with you to reduce inefficiencies, mitigate risk and improve opportunity. Our 29,000 tax professionals, in more than 140 countries, are committed to giving you the quality, consistency and customization you need to support your tax function. It is how Ernst & Young makes a difference.

For more information, please visit www.ey.com/easternafrica

“Information in this publication is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place of professional advice. Ernst & Young accepts no responsibility for any loss arising from any action taken or not taken by anyone using this material.”

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

©2013 EYGM Limited.All Rights Reserved.