Embed Size (px)

DESCRIPTION

power

Citation preview

www.arifirfanullah.com Page 1

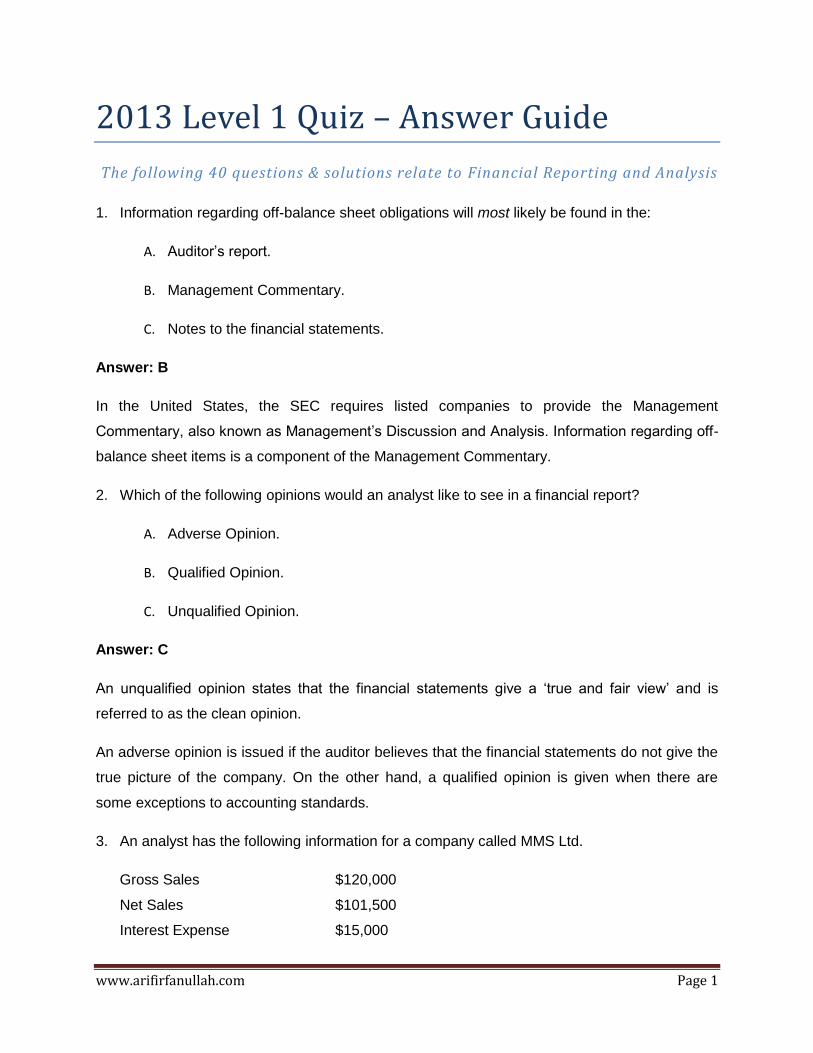

2013 Level 1 Quiz – Answer Guide

The following 40 questions & solutions relate to Financial Reporting and Analysis

1. Information regarding off-balance sheet obligations will most likely be found in the:

A. Auditor’s report.

B. Management Commentary.

C. Notes to the financial statements.

Answer: B

In the United States, the SEC requires listed companies to provide the Management

Commentary, also known as Management’s Discussion and Analysis. Information regarding off-

balance sheet items is a component of the Management Commentary.

2. Which of the following opinions would an analyst like to see in a financial report?

A. Adverse Opinion.

B. Qualified Opinion.

C. Unqualified Opinion.

Answer: C

An unqualified opinion states that the financial statements give a ‘true and fair view’ and is

referred to as the clean opinion.

An adverse opinion is issued if the auditor believes that the financial statements do not give the

true picture of the company. On the other hand, a qualified opinion is given when there are

some exceptions to accounting standards.

3. An analyst has the following information for a company called MMS Ltd.

Gross Sales $120,000

Net Sales $101,500

Interest Expense $15,000

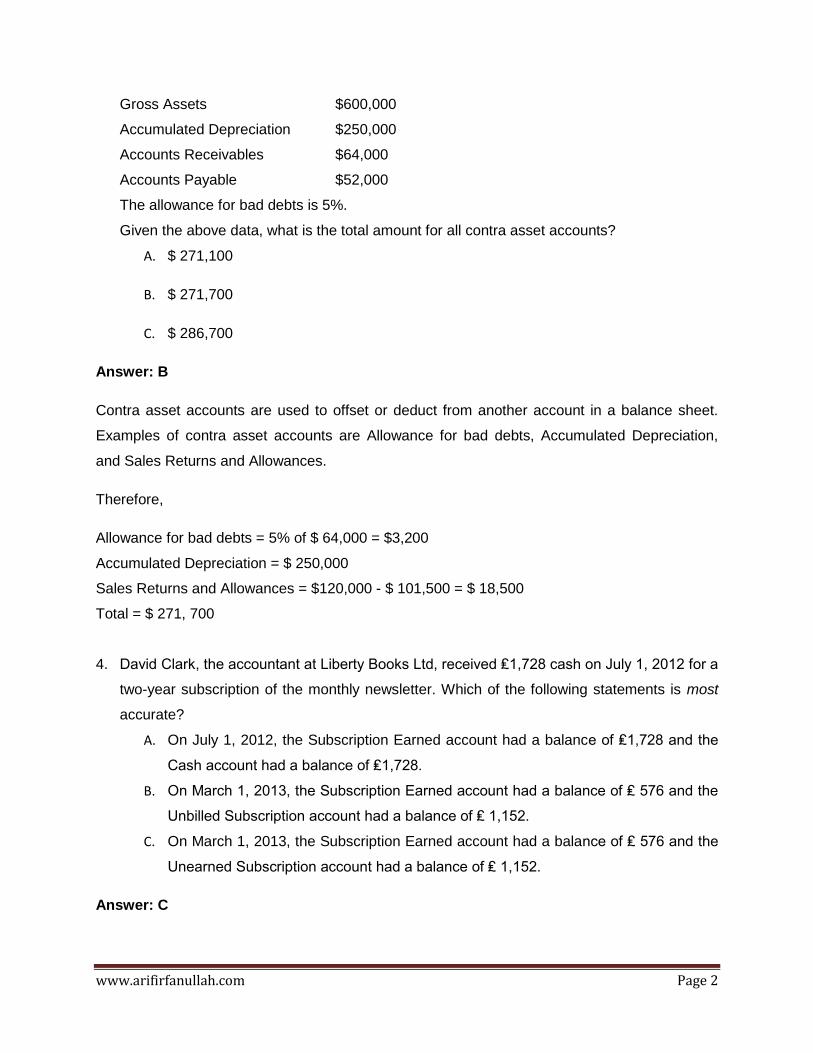

www.arifirfanullah.com Page 2

Gross Assets $600,000

Accumulated Depreciation $250,000

Accounts Receivables $64,000

Accounts Payable $52,000

The allowance for bad debts is 5%.

Given the above data, what is the total amount for all contra asset accounts?

A. $ 271,100

B. $ 271,700

C. $ 286,700

Answer: B

Contra asset accounts are used to offset or deduct from another account in a balance sheet.

Examples of contra asset accounts are Allowance for bad debts, Accumulated Depreciation,

and Sales Returns and Allowances.

Therefore,

Allowance for bad debts = 5% of $ 64,000 = $3,200

Accumulated Depreciation = $ 250,000

Sales Returns and Allowances = $120,000 - $ 101,500 = $ 18,500

Total = $ 271, 700

4. David Clark, the accountant at Liberty Books Ltd, received ₤1,728 cash on July 1, 2012 for a

two-year subscription of the monthly newsletter. Which of the following statements is most

accurate?

A. On July 1, 2012, the Subscription Earned account had a balance of ₤1,728 and the

Cash account had a balance of ₤1,728.

B. On March 1, 2013, the Subscription Earned account had a balance of ₤ 576 and the

Unbilled Subscription account had a balance of ₤ 1,152.

C. On March 1, 2013, the Subscription Earned account had a balance of ₤ 576 and the

Unearned Subscription account had a balance of ₤ 1,152.

Answer: C

www.arifirfanullah.com Page 3

Unearned or deferred revenue is when the company receives cash prior to earning the revenue

while unbilled revenue arises when a company earns revenue prior to receiving cash.

On July 1, 2012, David Clark would record ₤1,728 as an increase in Cash and an increase in

Unearned Subscription.

Eight months later, on March 1, 2013, the amount of Subscription Earned is:

Therefore, eight months later, subscription earned

The balances would thus be ₤576 in Subscription Earned account and ₤1,152 in Subscription

Unearned account.

5. Michael wishes to analyze the financial position of the company GHI Ltd. Which of the

following should Michael look into?

A. Assets

B. Expenses

C. Revenue

Answer: A

The financial statement components that are related to the financial position of the company

include Assets, Liabilities, and Equity. Expenses and Revenue are used to measure the

performance of the company.

6. Which of the following are two fundamental qualitative characteristics of Financial Reports?

A. Comparability and Timeliness

B. Comparability and Relevance

C. Faithful Representation and Relevance

Answer: C

Faithful Representation and Relevance are two fundamental qualitative characteristics of

Financial Reports. Comparability and Timeliness are enhancing qualitative characteristics.

www.arifirfanullah.com Page 4

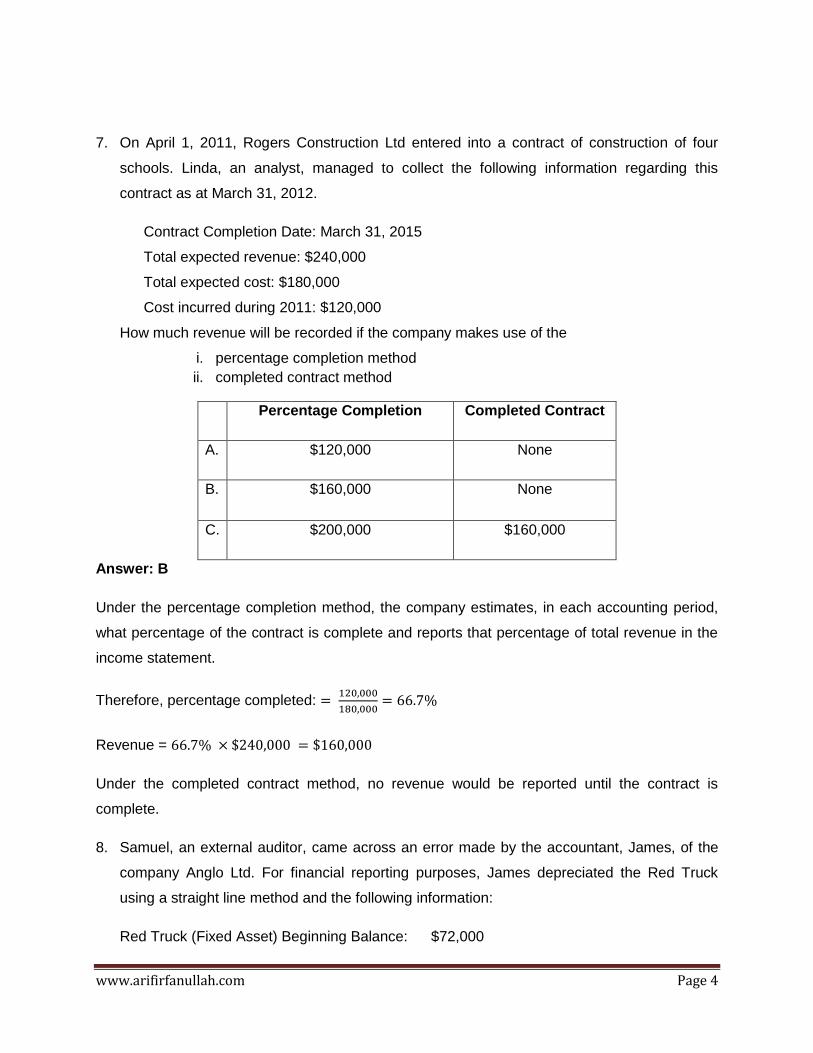

7. On April 1, 2011, Rogers Construction Ltd entered into a contract of construction of four

schools. Linda, an analyst, managed to collect the following information regarding this

contract as at March 31, 2012.

Contract Completion Date: March 31, 2015

Total expected revenue: $240,000

Total expected cost: $180,000

Cost incurred during 2011: $120,000

How much revenue will be recorded if the company makes use of the

i. percentage completion method

ii. completed contract method

Percentage Completion Completed Contract

A. $120,000 None

B. $160,000 None

C. $200,000 $160,000

Answer: B

Under the percentage completion method, the company estimates, in each accounting period,

what percentage of the contract is complete and reports that percentage of total revenue in the

income statement.

Therefore, percentage completed:

Revenue =

Under the completed contract method, no revenue would be reported until the contract is

complete.

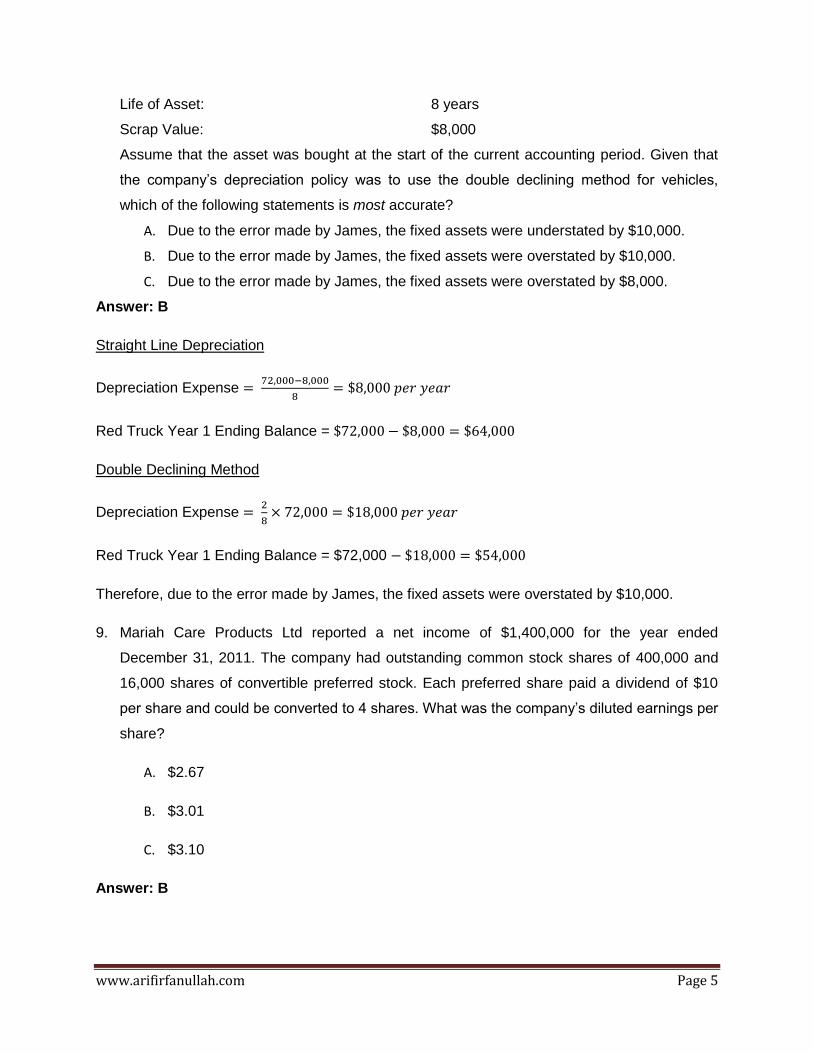

8. Samuel, an external auditor, came across an error made by the accountant, James, of the

company Anglo Ltd. For financial reporting purposes, James depreciated the Red Truck

using a straight line method and the following information:

Red Truck (Fixed Asset) Beginning Balance: $72,000

www.arifirfanullah.com Page 5

Life of Asset: 8 years

Scrap Value: $8,000

Assume that the asset was bought at the start of the current accounting period. Given that

the company’s depreciation policy was to use the double declining method for vehicles,

which of the following statements is most accurate?

A. Due to the error made by James, the fixed assets were understated by $10,000.

B. Due to the error made by James, the fixed assets were overstated by $10,000.

C. Due to the error made by James, the fixed assets were overstated by $8,000.

Answer: B

Straight Line Depreciation

Depreciation Expense

Red Truck Year 1 Ending Balance =

Double Declining Method

Depreciation Expense

Red Truck Year 1 Ending Balance = $72,000

Therefore, due to the error made by James, the fixed assets were overstated by $10,000.

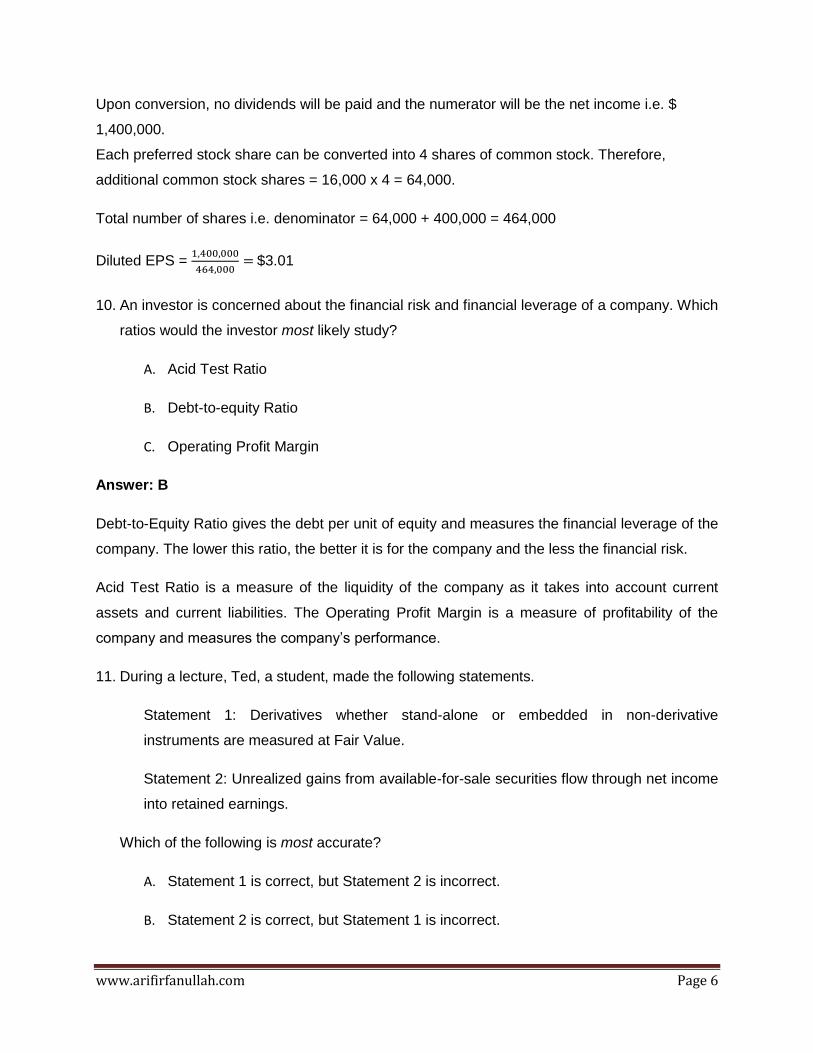

9. Mariah Care Products Ltd reported a net income of $1,400,000 for the year ended

December 31, 2011. The company had outstanding common stock shares of 400,000 and

16,000 shares of convertible preferred stock. Each preferred share paid a dividend of $10

per share and could be converted to 4 shares. What was the company’s diluted earnings per

share?

A. $2.67

B. $3.01

C. $3.10

Answer: B

www.arifirfanullah.com Page 6

Upon conversion, no dividends will be paid and the numerator will be the net income i.e. $

1,400,000.

Each preferred stock share can be converted into 4 shares of common stock. Therefore,

additional common stock shares = 16,000 x 4 = 64,000.

Total number of shares i.e. denominator = 64,000 + 400,000 = 464,000

Diluted EPS =

$3.01

10. An investor is concerned about the financial risk and financial leverage of a company. Which

ratios would the investor most likely study?

A. Acid Test Ratio

B. Debt-to-equity Ratio

C. Operating Profit Margin

Answer: B

Debt-to-Equity Ratio gives the debt per unit of equity and measures the financial leverage of the

company. The lower this ratio, the better it is for the company and the less the financial risk.

Acid Test Ratio is a measure of the liquidity of the company as it takes into account current

assets and current liabilities. The Operating Profit Margin is a measure of profitability of the

company and measures the company’s performance.

11. During a lecture, Ted, a student, made the following statements.

Statement 1: Derivatives whether stand-alone or embedded in non-derivative

instruments are measured at Fair Value.

Statement 2: Unrealized gains from available-for-sale securities flow through net income

into retained earnings.

Which of the following is most accurate?

A. Statement 1 is correct, but Statement 2 is incorrect.

B. Statement 2 is correct, but Statement 1 is incorrect.

www.arifirfanullah.com Page 7

C. Both Statements are incorrect.

Answer: A

Derivatives are measured at Fair Value rather than at Historical Cost. On the other hand,

unrealized gains from available-for-sale securities are a component of accumulated other

comprehensive income. Therefore, Statement 1 is correct but Statement 2 is incorrect.

12. Following is an extract from the cash flow statement of a hypothetical company Guitars Ltd.

Sales proceeds from sale of minivan $14,000

Cash paid for purchase of equipment $25,000

Interest received $2,850

Jonathan saw the above extract and stated, ‘This extract shows cash flows from investing

activities and the company clearly follows the US GAAP classification of cash flows’

Which of the following statements is most accurate?

A. Jonathan is correct about the ‘cash flows from investing activities’ part but is not

correct about the ‘US GAAP classification.’

B. Jonathan is correct about the ‘US GAAP classification’ part but is not correct about

the ‘cash flows from investing activities.’

C. Jonathan’s statement is incorrect with respect to both ‘cash flows from investing

activities’ and ‘US GAAP classification’ parts.

Answer: A

Sales proceeds from sale of fixed assets and cash paid for purchase of fixed assets are

considered part of the Cash flows from Investing Activities in the Cash Flow Statement. Interest

Received can be recorded as part of Cash flows from Investing Activities under the

classifications by IFRS. Therefore, Jonathan is correct about ‘cash flows from investing

activities’ part but incorrect about the ‘US GAAP classification’ part. Under US GAAP, interest

received is recorded as an Operating Cash Flow.

13. For the year ended June 30, 2009, Advant Corporation reported sales revenue of PKR300,

000. Given that accounts receivables decreased by PKR 20,000 and accounts payable

www.arifirfanullah.com Page 8

increased by PKR 8,000 during the year, what is the closest amount of cash collections for

the year?

A. PKR 308,000

B. PKR 320,000

C. PKR 328,000

Answer: B

Cash collections = PKR 300,000 + PKR 20,000 = PKR 320,000

The change in accounts payable does not affect cash collections.

14. Norah, an analyst, wishes to calculate the payables payment period for a company. The

revenue of the company for the year ended equaled $250,000 and the gross profit margin

was 25%. Given an average accounts payable balance of $17,500, the payables payment

period for the company is closest to:

A. 27 days

B. 34 days

C. 42 days

Answer: B

Payables Payment Period

Cost of goods sold = 0.75 x 250,000 = 187,500

Payables Payment Period =

15. William, an investor, has the following information for a hypothetical company AFC Ltd.

Net Profit Margin = 10%

Asset Turnover = 45%

Financial Leverage = 1.6

Given that the company had revenue of $100,000 for the year ended, the equity of the

company is closest to:

www.arifirfanullah.com Page 9

A. $62,500

B. $125,000

C. $138,900

Answer: C

Return on Equity =

Return on Equity =

Net Income =

Equity =

16. Primer Ltd started business in 2011 and uses the FIFO method to value its inventory. In May

2011, 67,500 units of inventory were purchased at $6 each and sold 60,000 units at $10

each. In September 2011, it purchased another 40,000 units at $8 each and sold 25,000

units at $13 each. What was the ending inventory balance in December 2011?

A. $135,000

B. $165,000

C. $180, 000

Answer: C

As the company uses the ‘First in First Out’ method of inventory valuation, the first batch of

67,500 units shall first be used up and sold. The number of units sold from the second batch of

inventory is calculated as follows:

Batch 1 Units bought 67,500 Units sold 60,000 Units remaining 7,500 Batch 2 Units bought 40,000 Units sold From batch 1 7,500 From batch 2 17,500 Units remaining 22,500

www.arifirfanullah.com Page 10

Ending Inventory = 22,500 x $8 = $180,000

17. In an inflationary environment, assuming stable inventory quantities, which of the following

most accurately describes the effect on Cost of Goods Sold of using FIFO as compared to

LIFO?

A. Lower

B. The Same

C. Higher

Answer: A

Compared to LIFO, Cost of Goods Sold calculated under FIFO would be lower because the

ending inventory would comprise of inventory at higher prices as the most recent units shall be

assumed unsold. As a result, the Cost of Goods Sold value would be lower.

18. Gray Inc. purchased tractors two years ago for $90,000. The tractors had a fair value of

$78,000 at the end of last year. Market analysis revealed that the fair value this year is

$94,000. What amount, if any, will be recognized in the net income assuming that Gray Inc.

uses the revaluation model?

A. $ 0

B. $ 12,000

C. $ 16,000

Answer: B

Using the revaluation model, the tractors are to be reported at fair value. At the end of last year,

a loss of $ 12,000 was recognized in the income statement. Any recovery that shall be reported

in the income statement in the following years shall only be to the extent of the loss. Therefore,

at the end of this year, $12,000 shall be recognized in the net income and $ 4,000 shall be

recognized as a revaluation surplus in shareholder equity.

19. Orange Ltd sold an intangible asset with acquisition cost of $13 million for $2.6 million.

Given that the accumulated amortization on the asset was $9.8 million, which of the

following is most likely the gain or loss reported on the sale of the asset?

www.arifirfanullah.com Page 11

A. $ 0.6 million loss

A. $ 0.6 million gain

B. $ 10.4 million loss

Answer: A

Gain or Loss on Sale = Sales proceeds – Carrying value

Gain or Loss on Sale = 2.6 - (13 – 9.8) = - 0.6

Therefore, a loss of $0.6 million was incurred upon sale of asset.

20. Brian’s business does not do well in its first year of operation and reports a loss of $12,000.

Given the tax rate of 35%, which of the following shall be reported in the balance sheet?

A. Deferred Tax Asset $4,200

B. Deferred Tax Asset of $12,000

C. Deferred Tax Liability of $ 4,200

Answer: A

The tax loss carry-forward is shown on the balance sheet as deferred tax asset and is equal to

the loss incurred multiplied by the tax rate.

Therefore, deferred tax asset = 12,000 x 35% = $4200.

21. Which of the following is created when the income tax expense is higher than taxes

payable?

A. Deferred Tax Asset

B. Deferred Tax Liability

C. Permanent Difference

Answer: B

A deferred tax liability is created when the income tax expense is higher than taxes payable. On

the other hand, a deferred tax asset is created when taxes payable are higher than the income

tax expense.

www.arifirfanullah.com Page 12

Permanent difference is a difference between taxable income and pretax income and does not

create deferred tax assets or deferred tax liabilities.

22. The following statements were made by three university students.

Scott: A bond is issued at a premium when the coupon rate of 10% is less than the market

prevailing rates of 12%.

Dave: Under the operating lease, being the lessee, I will be entitled to the legal ownership of

the asset.

Mandy: The pension expense is the agreed upon amount contributed by the company under

a defined contribution plan.

How many statements are least accurate?

A. 1

B. 2

C. 3

Answer: B

A bond is issued at a discount when the coupon rate of 10% is less than the market prevailing

rates of 12%.

The financial lease allows for risks and rewards to be transferred and the lessee to be entitled to

the legal ownership of the asset, while the operating lease does not.

The pension expense is the agreed upon amount contributed by the company under a defined

contribution plan.

Therefore, 2 statements are inaccurate.

23. Given that a 5 year bond was issued at the beginning of June 2012 with a face value of $1

million and coupon rate of 12%. The market rates at the time of issue were 15%. The

balance sheet liability at the end of the first semiannual period is closest to:

A. $ 889,761

B. $ 904,317

www.arifirfanullah.com Page 13

C. $ 957,039

Answer: B

The liability at the start of the year is the Present Value

N = 10

I/Y = 15/2 = 7.5

FV = $1,000,000

PMT = $1,000,000 x (0.12/2)

Thus, PV = $897,039

The interest expense is the effective interest rate times the balance sheet liability:

(15/2) x 897,039 = $67, 278

As the bond was issued at a discount, the value of the liability will change over time and the

difference between the interest rate and actual cash payment will be added to the initial liability

amount.

The cash payment equals coupon rate x par value = (0.12/2) x 1,000,000 = $60,000

The difference is therefore $67,278 - $60,000 = $7,278

The liability at the end of the first semiannual period equals $897,039 + $7, 278 = $ 904,317

24. Revenues and expenses based on significant estimates that involve subjective judgments

can best be categorized as a part of which of the following fraud risk factors?

A. Attitudes and Rationalization

B. Incentives and Pressure

C. Opportunities

Answer: C

Revenues and expenses based on significant estimates that involve subjective judgments allow

for opportunities to conduct fraudulent activity. Thus it’s best categorized as ‘Opportunities’.

25. Which of the following statements is most likely to cause earnings before interest and tax

(EBIT) to fall immediately?

A. Classifying a Financial Lease as an Operating Lease

www.arifirfanullah.com Page 14

B. Giving out cash dividends

C. Increasing the salvage value of depreciable assets

Answer: A

By classifying a Financial Lease as an Operating Lease, the rent expense increases and causes

the EBIT to fall.

Cash dividends are paid out from Net Income and therefore EBIT is not affected.

Increasing the salvage value reduces the depreciation expense and thus increases EBIT.

26. A company wishes to improve its Operating Cash flow. Which of the following actions is the

company most likely to take?

A. Decreasing the payables payment period.

B. Securitizing its receivables.

C. Selling off unused fixed assets.

Answer: B

When receivables are securitized, they are transferred to a special purpose entity and sold

further once a pool of receivables is created. This improves the operating cash flows because

the transaction is recorded as a sale.

Decreasing the payables payment period means that the vendors need to be paid off more

quickly than before and this decreases the operating cash flow rather than improving it.

Unused fixed assets may be sold or disposed off but this transaction impacts the Cash Flow

from Investing Activities.

27. Phil, an analyst, was studying two competitors of which Company A used the LIFO method

of inventory valuation and Company B used the FIFO method. In order to adjust inventory of

Company A, Phil made use of the following data.

January 1, 2012 December 31, 2012

Inventory ¥50,000 Increased by 25%

www.arifirfanullah.com Page 15

LIFO Reserve ¥6,000 Increased by 15%

Which of the following values for Ending Inventory in accordance to FIFO method did Phil

derive?

A. ¥62, 500

B. ¥63, 400

C. ¥69, 400

Answer: C

LIFO Ending Inventory can be adjusted to a FIFO basis by adding the LIFO reserve. Therefore,

Ending Inventory = ¥50,000 x 1.25 = ¥62,500

LIFO Reserve = ¥6,000 x 1.15 = ¥6,900

Ending Inventory FIFO = ¥62,500 + ¥6,900 = ¥69,400

28. Little Lego had a current ratio of 1.25 and a quick ratio of 0.75. If it wishes to purchase new

inventory and finance it through bank overdraft, what would be the most likely impact on the

two aforementioned ratios?

A. None of the ratios will decrease.

B. Only one ratio would decrease.

C. Both ratios will decrease.

Answer: C

Assume that the current assets are 2.5 units, current liabilities are 2 units and inventory is 1 unit.

By purchasing inventory worth 1 more unit via short term debt, current assets are 3.5 units,

current liabilities are 3 units and inventory is 2 units.

The current ratio =

and quick ratio =

Thus both ratios will decrease.

www.arifirfanullah.com Page 16

29. Which of the following most accurately describes the

relationship in the DuPont

Equation?

A. Tax Burden

B. Interest Burden

C. EBIT Margin

Answer: A

Net Income/EBT is the Tax Burden and measures the effect of taxes on the ROE. It is reflective

of 1-tax rate.

Interest Burden is EBT/EBIT whereas EBIT Margin is EBIT/Revenue.

30. Which of the following is least likely included in a common size balance sheet or common

size income statement?

A. Operating Profit Margin

B. Pre Tax Margin

C. Current Ratio

Answer: C

Operating Margin and Pre Tax Margins are percentages expressed as a percentage of Net

Revenues. On the other hand, Current Ratio =

and in common size balance

sheet analysis, Current Assets are presented as a percentage of Total Assets not that of

Current Liabilities.

31. While studying the financial statements of Gram International Ltd, an analyst came across

the following information.

Net Income $45 million

Depreciation $16 million

Decrease in inventory $2.4 million

Decrease in Rent Payable $1.8 million

www.arifirfanullah.com Page 17

Increase in Bonds Payable $15 million

Net Capital Expenditure $10 million

Which of the following is the most accurate value of Free Cash Flow to the Firm (FCFF)?

A. $50.6 million

B. $51.6 million

C. $66.6 million

Answer: B

Operating Cash Flow = Net Income – Depreciation + Decrease in Inventory – Decrease in

Rent Payable

Operating Cash Flow = 45 + 16 +2.4 – 1.8 = $61.6 million

Free Cash Flow to the Firm = Operating Cash Flow – Net Capital Expenditure

Free Cash Flow to the Firm = 61.6 – 10 = $51.6 million.

32. Which of the following is least likely affected because of reporting a lease as an operating

lease rather than a financing lease by a lessee?

A. Debt-to-Equity Ratio

B. Operating Expenses

C. Total Cash Flow

Answer: C

Classifying the lease as financing or operating does not affect the Total Cash Flow. It only

determines the extent to which the lease payments are classified as Operating or Financing

Cash Flows.

An operating lease does not require recognition of a liability but a finance lease does, the debt-

to-equity ratio differs.

Under an operating lease, the lessee reports rent expense in the income statement and

therefore Operating Expenses differ for Operating and Financial Lease.

www.arifirfanullah.com Page 18

33. Cheesy Pizzas rented out a new place to open up another outlet. The rent paid at the end of

the year 2012 amounted to $2400 and was to cover the rent expense for five months up till

May 31, 2013. The impact on the 2012 balance sheet can best be described as:

A. A decrease in Cash and an increase in rent expense.

B. A decrease in Cash and an increase in a prepaid liability account.

C. A decrease in Cash and an increase in a prepaid asset account.

Answer: C

When Cash is paid in advance for an expense not yet incurred, Cash decreases and a prepaid

asset account is created.

Rent expense will only increase in the Income Statement when incurred.

A prepaid liability account is only created if the expense is recorded before the cash payment

has been made.

34. Mini Tablets Ltd’s liabilities include a Treasury Bills that mature in 3 months, Commercial

Paper due in 270 days, vendors that have to be paid within 7 weeks, and notes payable due

in 15 months. Which of these will be included in the Current Liabilities in Mini Tablet Ltd’s

balance sheet?

A. All but the Commercial Paper

B. All but the Notes Payable

C. All of the aforementioned liabilities

Answer: B

Current Liabilities are due within one year which is the standard operating cycle for most of the

organizations. Therefore, all liabilities except Notes Payables should be classified as Current

Liabilities in Mini Tablet Ltd’s Balance Sheet.

35. Outstanding common stock shares for Little Woods Inc were 120,000 on January 1, 2011.

The company repurchased 20,000 shares on June 1 followed by a stock split of 2 on July 1.

Which of the following is the most accurate value for weighted average shares outstanding

for the year?

www.arifirfanullah.com Page 19

A. 173,333

B. 200,000

C. 216,667

Answer: C

The number of shares outstanding for the first 5 months is 120,000 and for the remaining 7

months are 100,000. These should be multiplied by 2 to take into account the effect of a stock

split.

= 216, 667

36. An analyst makes the following statements regarding Financial Statements.

Statement I: The periodic as well as annual financial statements should be audited before

they are presented to investors.

Statement II: The footnotes to financial statements include legal proceedings as well as

commitments and contingencies.

Are the analyst’s statements accurate?

A. Both of these statements is accurate

B. Neither of these statements is accurate

C. Only one of these statements is accurate

Answer: C

The annual financial statements are audited, while the periodic statements are not audited.

Thus Statement I is inaccurate.

Statement II is accurate.

37. Given below is selected data from Panama Ltd’s financial statements for the year 2010 and

2011.

2011 2010

10%, $100 par, Preferred Stock $20 million $20 million

www.arifirfanullah.com Page 20

$10 par, Common Stock $8 million $7 million

Additional paid-in capital, Common Stock $30 million $25 million

Retained Earnings $40 million $36 million

Treasury Stock $3 million $1 million

Net Income $15 million $12 million

To calculate Return on Equity, which of the following most accurately gives the value of

average common equity?

A. $35 million

B. $71 million

C. $73 million

Answer: B

Common Equity = Common Stock + Additional Paid-in Capital + Retained Earnings – Treasury

Stock

Common Equity, 2010 = 7 + 25 + 36 – 1 = 67

Common Equity, 2011 = 8 + 30 + 40 – 3 = 75

Average Common Equity =

38. Which of the following is the most likely impact of using FIFO rather than LIFO in an

economy experiencing inflation?

A. Lower Ending Inventory

B. Higher Inventory Turnover

C. Higher Income Taxes

Answer: C

During inflation, using FIFO as a method of inventory valuation results in ending inventory

comprising of higher priced goods and therefore a higher value of Ending Inventory. As the

Ending Inventory is greater, Cost of Goods Sold is lower and therefore the Inventory Turnover is

www.arifirfanullah.com Page 21

lower. A lower Cost of Goods Sold value causes Gross Profit and therefore Net Profit to be

higher and thus income taxes are higher.

39. Which of the following industries is most likely to have low accounts receivables?

A. Telecommunications

B. Machinery and other industrials

C. Consumer Discretionary

Answer: A

Telecommunications has the lowest accounts receivables as it has negligible credit sales

compared to Industrials and Consumer Discretionary.

40. Which of the following documents sorts out business transactions by account?

A. General Journal

B. General Ledger

C. Adjusted Trial Balance

Answer: B

A general journal sorts out business transactions by date whereas a general ledger sorts out

business transactions by account in the form of T-Accounts.

An adjusted trial balance lists account balances once adjusting entries have been made.