Embed Size (px)

Citation preview

2013 Mortgage Barometer ReportAn annual study of the mortgage market in AustraliaPrepared by Gfk Australia for QBE LMI

Note: DISCLAIMER: The information contained in this publication has been obtained from GfK Australia and does not necessarily represent the views or opinions of QBE Lenders’ Mortgage Insurance Limited (QBE LMI). This publication is provided for informational purposes only and is not intended to constitute legal, financial or other professional advice and has not been provided with regard to the investment objectives or circumstances of any particular reader. While based on information believed to be reliable, no guarantee is given that it is accurate or complete and no warranties are made by QBE LMI as to the accuracy, completeness or usefulness of any of the information in this publication. The opinions, forecasts, assumptions, estimates, derived valuations and target price(s) (if any) contained in this material are as of the date indicated and are subject to change at any time without prior notice. The information referred to may not be suitable for specific investment objectives, financial situation or individual needs of recipients and should not be relied upon in substitution for the exercise of independent judgment. Recipients should obtain their own appropriate professional advice. Neither QBE LMI nor other persons shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary damages, including lost profits arising in any way from the information contained in this material. This material may not be reproduced, redistributed, or copied in whole or in part for any purpose without QBE LMI’s prior expressed consent. QBE Lenders’ Mortgage Insurance Limited ABN 70 000 511 071.

Table of Contents

Introduction 5Executive Summary 6Property market sentiment 7 Chart 1: Housing economic indicators 7

Chart 2: Perceptions of buying residential property 8

Chart 3: Perceptions of property pricing and affordability 9

Chart 4: Perceptions of property market value in 2013 10

Chart 5: Impact of increasing unaffordability of property on intentions to buy 10

Chart 6: Impact of an interest rate rise on you and your finances 11

Chart 7: Impact of an interest rate rise mortgage type 11

Topical influences on the property market 12 Chart 8: Reaction of banks to changes in official cash rate 12

Chart 9: Impact of the Election/extended campaign period on intention to buy 13

Chart 10: Influences on financial strain in the last 12 months 14

Chart 11: Impact of First Home Buyer grant changes on intention to buy 15

Chart 12: Impact of superannuation legislation changes on intention to buy 16

What’s happening in the mortgage market? 17 Chart 13: Actual and intended LVR by when bought/intend to purchase property 17

Chart 14: Current and intended LVR and loan size 18

Chart 15: Changes in minimum monthly mortgage repayments, ABS statistics 19

Chart 16: Reasons for applying for mortgages through a broker versus direct through the lender 20

Chart 17: Reasons for choosing a Big 4 bank over other lenders 21

What does the future mortgage market look like? 22 Chart 18: Type of property looking to buy - New developments 22

Chart 19: Type of property looking to but - Existing dwellings 23

Chart 20: Key sub-group differences 24

Methodology 25Sample profiles 26Appendix 41

5An annual study of the mortgage market in Australia

Introduction

Welcome to the third annual QBE LMI report into mortgage and property market sentiment and behaviour, Mortgage Barometer.

This report has been prepared exclusively for QBE LMI by GfK Australia, based upon a survey of 1,017 Australian target market respondents:

• current mortgage holders (Mortgagors); and

• those intending to buy residential property, either as an investment or home in the next five years (Intenders).

The survey was developed by GfK Australia in consultation with QBE LMI, and fieldwork was conducted via an online panel from May 1 to May 13, 2013. For more information on the survey sample, please see the methodology section at the end of this report.

This year the report focuses on some of the topical influences on market sentiment, but where relevant, year-on-year changes are reported. Summary statistics for key subgroups are available at the end of the report.

The information, views and opinions in this report are based on research carried out by GfK Australia and the results of the survey.

6 2013 Mortgage Barometer Report

• Propertyappetiteisincreasing– near-record-low interest rates are starting to stimulate the property market, with house prices and loan growth increasing, and more Australian adults looking to buy property in the next 12 months (26% in 2013 compared to 20% in 2012).

• Next12monthsseenastherighttimetobuy – more than a third of respondents believe prices will be higher in 2013.

• Near-recordlowsininterestratesarehavingapositiveimpact – half of current mortgage holders surveyed say cuts are a welcome relief and more than one in three Intenders are encouraged to buy sooner.

• Generalexpectationisforrobustgrowth – 47% think that property prices will increase strongly in the next three years and interest rates will stay stable (28% believe they will rise, 28% believe they will fall)

• Butaffordabilityremainsatopofmindconcern – almost half of respondents think property is overvalued despite improvements in housing affordability for the last eight quarters.

– Only one in three respondents report experiencing no financial strain.

– 69% of First Home Buyer respondents worry they’ll never be able to afford their own home.

– Mortgage strain exists for one in five Mortgagors, and may be on the rise according to the Fitch Dinkum Index1.

– Loan-to-Value Ratios (LVRs) are increasing, even though loan repayments are decreasing.

• Investmentinpropertyisincreasing – economic uncertainty in the share market and low interest rates are pushing investors back to bricks and mortar.

– Changes to superannuation legislation are likely to lead to a small increase in property ownership, particularly for those with an SMSF.

• Anumberoffactorsaredelayingmarketentry:

– The Election – an expected change of government and the lengthy campaign in 2013 are causing Intenders to hold off on buying until after the Election.

– Changes to First Home Buyer grants – the number of First Home Buyers is decreasing and two in three First Home Buyers in NSW and QLD say the changes are having an impact on their purchasing intentions.

• Whatrespondentsarelookingtobuyischanging:

– Stronger interest in new developments (new houses 35% in 2013 compared to 29% in 2012).

– Slight push in interest to city fringes.

– One in three state they would look in a different location if affordability declines.

• FinancialstabilityisstillabigsellingpointfortheBig4banks – existing relationships help retain customers, and the majority of Mortgagors are still applying for mortgages directly with the bank rather than through a broker.

1 Fitch Ratings, Sydney (April 9 2013). http://www.fitchratings.com/creditdesk/press_releases/detail.cfm?pr_id=787983

Executive Summary

7An annual study of the mortgage market in Australia

Property remains a desirable investment, with appetite for property increasing

Poor economic news from Europe and the US in recent years has cast uncertainty over the property market in Australia, with low homebuyer confidence in 2012 and ample deliberation over whether the property market would soften. Confidence appears to have turned around in 2013, with first quarter economic indicators showing about a 10% increase in consumer sentiment and time to buy dwelling indices, as well as increases in average house prices and mortgage sizes (Chart 1). This supports claims from the Reserve Bank of Australia (RBA) in April 2013 that near-record-lowinterestratesarestartingtoboosttheeconomy,withhousepricesandloangrowthincreasing2.

Chart 1: Housing economic indicators

Q1 2011 Q1 2012 Q1 2013

O�icial cash ratea 4.75% 4.25% 3.00%

HIA housing affordabilityb 55.7 64.8 68.9#

Consumer Sentiment Indexc 105.3* 94.5* 104.9*

Time to buy dwelling Indexc 108.6* 120.5* 128.4*

Average house price Index – established housesd 147.8 146.3 148.8

Average house price Index – project homesd 131.3 132.1 136.2

Average loan sized $285,500 $284,500 $301,000

# December 2012 �igure, * Figures from April

a RBA Interest Rate Decisions 20011�2013.

b HIA�Commonwealth Bank Affordability Report, December Quarter 2012

c Westpac-Melbourne Institute Survey of Consumer Sentiment, April 2013

d ABS House Price Indexes: Eight Capital Cities, Mar 2013. http://www.abs.gov.au/ausstats/[email protected]/mf/6416.0

Low interest rates and property price dips from 2010 to 2012 have had a positive effect on the appetite for property. 13.2% of Australian adults (26% of total sample) are looking to buy residential property in the next 12 months compared to 5.2% who bought in the previous 12 months, and 69% of respondents intend to purchase property in the next five years (up from 61% in 2012).

2 Kent C. Recent Developments in the Australian Housing Market (March 14 2013). http://www.rba.gov.au/speeches/2013/sp-ag-140313.html

Property market sentiment

8 2013 Mortgage Barometer Report

Property increasingly seen as a sound investment

‘’With share market volatility and low interest rates, there’s a lack of options so it’s left investors to go back to what they know best – property3’ Leith van Onselen, MacroBusiness Economist.

In 2013, significantly more respondents rated property as an effective way to quickly build wealth or as a means of funding retirement - making it the number one perceived function of property, particularly for those aged 55 and over (37% vs. 22% for all respondents). In addition, significantly fewer respondents now believe property should only be one part of a diversified portfolio (Chart 2). The slow recovery of the share market post-Global Financial Crisis (GFC) has likely had a large part to play in these perceptions, with dwelling values outperforming the ASX 200 Index on capital appreciation over the last decade to 2012, and proving to be far more stable (largest 12-month fall of 5% vs. 40%+ for shares)4.

Chart 2: Perceptions of buying residential property (2012 vs. 2013)

7% 9%

29% 17%

19%

19%

17% 22%

8% 14%

16% 17%

2012 2013

Reliable blue-chip investment

An effective way to build wealth relatively quickly

An investment to fund retirement

A home for retirement

Should only be one part of a diversi�ied asset allocation strategy

Can be risky

Base: Total sample: 2012 n=1,162, 2013 n=1,017

Now is the right time to buy; low interest rates paying off

A drop in the official cash rate to near-record lows (down 125 basis points in the year to April 2013), combined with Q1 2013 indications that property prices are on the rise, has triggered perceptions that now is the best time to buy. Oneinthree(32%)currentMortgagorsandIntendersthinkyoushouldbuyinthenextsixmonths, with half (52%) believing within the next 12 months is best (compared to 26% and 40% respectively in 2012).

For those who believe that the next year is not the best time to buy, open-ended explanations as to why often touched on the belief that house prices will drop further and/or personal financial limitations.

Ratecutshavehadapositiveimpactonthemarket, with half (53%) of current Mortgagors surveyed declaring the cuts were a welcome relief and more than one in eight (13%) saying it has made things considerably easier. This is particularly true for singles (23%), families with primary school aged children (18%) and for current Mortgagors intending to buy again (18%).

Recentratecutsarealsoencouragingfasterentryintothepropertymarket for one in three of those intending to buy in the next five years. Rate cuts are particularly motivating for those looking to invest (42%) and singles (47%). Only one in 10 potential purchasers (12%) are holding off on buying in the hope of more rate cuts. The further rate cut in May 2013 (post-survey) is likely to have further encouraged property purchase based on this data.

3 Johanson S & Vedelago C. Investors help lift property market out of the slump (May 4 2013). http://www.smh.com.au/business/investors-help-lift-property-market-out-of-the-slump-20130503-2iygh.html

4 Lawless T. Shares or Property – what’s the better performer? (November 2 1012). http://blog.rpdata.com/2012/11/shares-or-property-whats-the-better-performer/

9An annual study of the mortgage market in Australia

Despite an appetite for property, affordability is a growing concern

The Economist magazine’s 2013 global housing index5 reports that Australia has moved from the fifth to the fourth most overvalued global property market and those intending to buy property in the next five years are well aware of this. Themajorityofsurveyrespondents(59%)ratepropertyasunaffordable, with one in four stating that prices are so high they can’t afford what they want, despite measures of affordability having improved for the past eight quarters since the house price peak in mid-2010 (Chart 1).

AffordabilityisaparticularissueforFirstHomeBuyers, of whom 84% believe property prices are close to reaching or are above what they can afford, and 69% worry they’ll never be able to afford their own home (compared to 24% of all respondents).

This is a sentiment felt by the majority of survey respondents, with 82%agreeingthatfuturegenerationswillfindithardertopurchasetheirfirsthome and 70% worried about the level of debt people are getting into to buy property. Other factors contributing to concerns about affordability include foreign investment and the impact of the financial situation in Europe and the US on interest rates in Australia (Chart 3).

Chart 3: Respondents’ perception of property pricing and affordability

8%

13%

20%

24%

22%

22%

56%

38%

47%

11%

82%

70%

56%

48%

51%

47%

24%

28%

27%

72%

Future generations will �ind it harder to purchase their �irst home

I'm worried about the debt people are getting into to buy property

I'm worried foreign investment will make property unaffordable

It’s more important to get into the market now than to save a bigger deposit

I'm worried about the impact of the Europe/US �inancial situation on interest rates

I think property prices will increase strongly in the next three years

I'm worried I’ll never be able to afford my own home

I think the housing price 'bubble' will burst and prices will fall

I'd consider an interest only loan to purchase a more expensive property

I am better off owning a home than renting

Disagree Agree

Despite this sentiment, the Australian dream of home ownership is still strong with almostthreequartersofrespondentsbelievingtheyarebetteroffowningahomethanrenting, a belief supported by the current inflated rental market in Australia (Australia ranks third on The Economist rent affordability measure).

Australians are “paying double what they were 10 years ago to get into the (property) market”, despite wages rising “by half that.” Steve Mickenbecker, Canstar6.

Although there is general agreement that now is a good time to buy property, the generalsentimentisthatpropertypricesareexpensiveandsettorise. More than a third of respondents believe prices will be higher in 2013, while one in ten respondents believe there will be an expected increase of at least 10% (Chart 4).

ThisviewisparticularlystrongamongstFirstHomeBuyers with more than three quarters believing housing is overvalued. Owner-Occupiers, however, are less likely to see the market as inflated (possibly due to the benefit of hindsight or post-purchase rationalisation).

5 The Economist house-price indicators (May 2013). http://www.economist.com/news/finance-and-economics/21578043-our-latest-round-up-house-prices-reveals-some-sharp-contrasts-boom-and-gloom

6 Mickenbecker S. Housing Affordability interview, Seven media Group (April 2013). http://au.finance.yahoo.com/video/reducing-private-health-premiums-023055241.html

10 2013 Mortgage Barometer Report

Perceptionsofpropertyvaluedifferbystate: those residing in NSW/ACT and WA are most likely to rate the market as overvalued (54% and 53% respectively) whilst almost half (44%) of Queenslanders rate property as undervalued. Compared to other Australians, Queenslanders are also significantly less likely to believe that property prices will increase in 2013 (32% compared to 50% across other states), potentially as a result of the property slump on the Gold Coast.

Home buyers are confronting perceptions of decreased property affordability by considering their options in terms of style, size and location of properties sought (Chart 5).

Chart 4: Perceptions of property market value in 2013

Base: Total sample: 2013 n=1017, First Home Buyers n=115, Owner-Occupiers n=558

-18% -11% -22%

-9% -2% -10%

28% 28% 26%

20%

48%

15%

Total First Home Buyer

Owner- Occupier

Property value in 2013

Overvalued (more than 10%)

Somewhat overvalued (up to 10%)

Undervalued (more than 10%)

Somewhat undervalued (up to 10%)

16%

8%

38%

9%

Total

Prices in 2013 vs. 2012

Higher (more than 10%)

Somewhat higher (up to 10%)

Lower (more than 10%)

Somewhat lower (up to 10%)

Chart 5: Impact of increasing unaffordability of property on intentions to buy

May have to give up on buying property

Will probably end up buying something smaller

Will probably end up buying something in another location

May end up buying something different to what and 'trade up‘ in the future

Considering a larger loan than what I had considered previously

Considering buying an investment property instead of a property to live in

22%

39%

35%

24%

18%

17%

Base: Intending to buy property in the next �ive years and believe affordability will decrease, n=389

As we saw in 2012, opinionsaresplitaboutwhetherinterestrateswillchangeinthesecondhalfof2013. While 28% of all respondents say they will rise, 28% believe they will fall.

11An annual study of the mortgage market in Australia

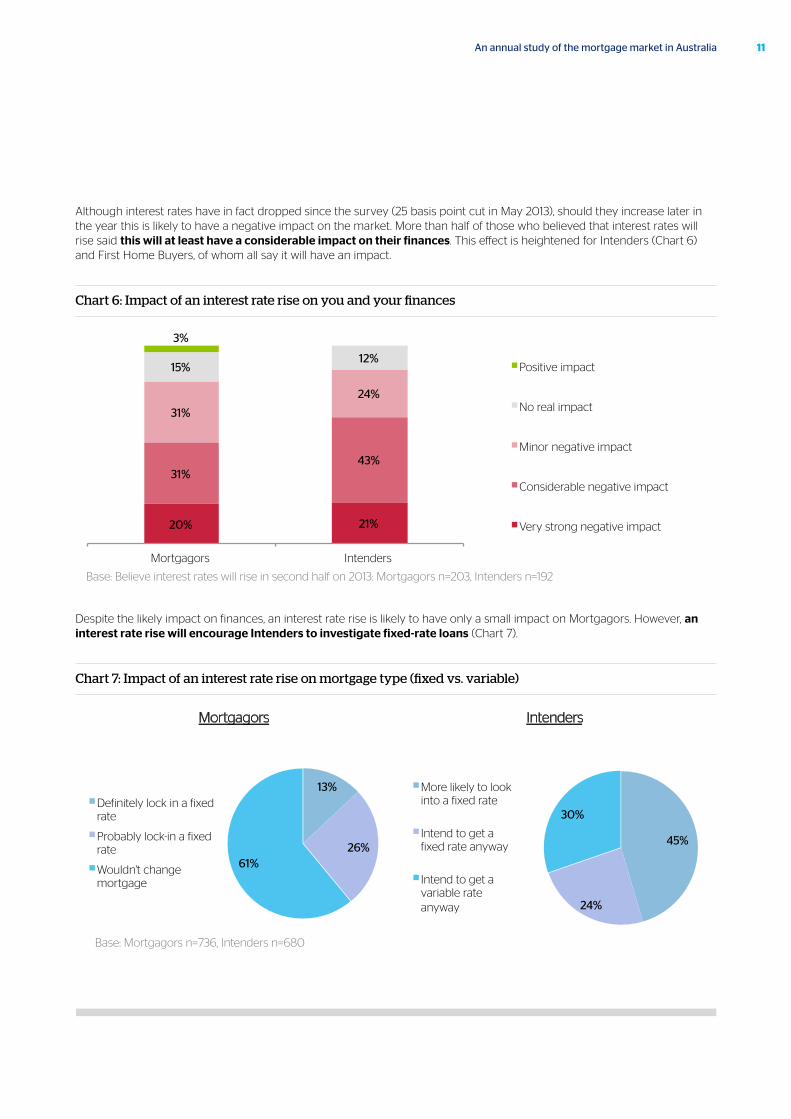

Although interest rates have in fact dropped since the survey (25 basis point cut in May 2013), should they increase later in the year this is likely to have a negative impact on the market. More than half of those who believed that interest rates will rise said thiswillatleasthaveaconsiderableimpactontheirfinances. This effect is heightened for Intenders (Chart 6) and First Home Buyers, of whom all say it will have an impact.

Chart 6: Impact of an interest rate rise on you and your finances

20% 21%

31% 43%

31%

24%

15% 12%

3%

Mortgagors Intenders

Positive impact

No real impact

Minor negative impact

Considerable negative impact

Very strong negative impact

Base: Believe interest rates will rise in second half on 2013: Mortgagors n=203, Intenders n=192

Despite the likely impact on finances, an interest rate rise is likely to have only a small impact on Mortgagors. However, aninterestraterisewillencourageIntenderstoinvestigatefixed-rateloans (Chart 7).

Chart 7: Impact of an interest rate rise on mortgage type (fixed vs. variable)

13%

26% 61%

Mortgagors

Definitely lock in a fixed rate

Probably lock-in a fixed rate

Wouldn't change mortgage

45%

24%

30%

Intenders

More likely to look into a fixed rate

Intend to get a fixed rate anyway

Intend to get a variable rate anyway

Base: Mortgagors n=736, Intenders n=680

Topical influences on the property market

In 2012, a failure by banks and other lenders to pass on interest rate cuts in full blew out the gap between the RBA rate and mortgage rates to an 18-year high, with households paying on average 3% above the official cash rate for home loans7. Despite the banks’ cost of lending increasing about 150 basis points relative to the cash rate since the onset of the GFC8, the market appears to generally criticise banks as being more focused on shareholder profits than customer wellbeing (Chart 8).

Chart 8: Reaction of banks to changes in official cash rate

Base: Those who think rates will rise in the second half of 2013 n=277; Those who think rates will fall n=292

14%

41%

44%

If interest rates rise banks will...

Increase rates beyond the full rise

Pass on the full rise

Pass on only some of the rise

6%

38%

52%

4%

If interest rates drop banks will...

Pass on none of the cut

Pass on only some of the cut

Pass on most of the cut

Pass on the full cut

Interestingly, the banks have picked up on the negative consumer sentiment and in May 2013 swiftly passed on the RBA rate cut of 25 basis points in full, and ANZ actually bettered its rivals with a 27 basis point cut to its standard variable rate off the back of reported easing of cost of funds9.

An expected change of government and lengthy election campaign is deterring the purchase of property

In January this year the Prime Minister, Julia Gillard, announced that the Federal Election would be held on September 14, unofficially prompting an abnormally long election campaign. An expected change in government (only 14% believe that the ALP will win) and/or the lengthy campaign period is causing a delay for the majority of those respondents intending to buy property (Chart 9).

7 HIA economics group Monetary Policy and Mortgage Interest rates, February 2013 http://economics.hia.com.au/media/Interest%20rates%20and%20monetary%20policy%20-%20Fact%20Sheet%20Feb%202013.pdf

8 Roberston B & Rush A, Developments in Banks' Funding Costs and Lending Rate. RBA bulletin, March 2013 http://www.rba.gov.au/publications/bulletin/2013/mar/7.html

9 ANZ May 2013 Interest Rate Review (May 10 2013).

12 2013 Mortgage Barometer Report

Chart 9: Impact of the Election/extended campaign period on intention to buy

25% 30%

18% 15%

9%

Long campaign Want to see what economy is like post-

election

Want to see who wins Long campaign will effect economy

Campaign will put rate changes on hold

56% will delay purchasing until after the election

Base: Those intending to buy residential property in the next �ive years, n=680

Threeinfourrespondents(72%)believetheelectionwillhavenoimpactontheofficialcashrate but, interestingly, the political party that respondents expect to win impacts on whether they think rates will rise or fall:

• For the majority who think the Liberal National Party (LNP) will win, 21% say rates will rise after the election, 8% say they’ll drop.

• For those who think the Australian Labor Party (ALP) will win, 8% say rates will rise after the election, 20% say they’ll drop.

13An annual study of the mortgage market in Australia

14 2013 Mortgage Barometer Report

Mortgage strain is low, despite increased cost of living and high financial strain

Onlyoneinthreesurveyrespondentsreportedexperiencingnofinancialstrain, with an increase in the cost of living proving to be the largest financial stressor (Chart 10). Mortgage strain ranked fourth as a financial stressor, affecting less than one in five.

Chart 10: Influences on financial strain in the last 12 months

No financial strain

Cost of living has increased

I've recently had increased expenses (e.g. kids started school)

I/my partner recently experienced a reduction in the amount of work available

My mortgage repayments

I /my family has recently had unexpected medical bills

I /my partner have recently lost our job

Changes to the private health rebate have placed extra strain on my budget

I've recently made another large purchase (e.g. new car, holiday)

I /my partner have recently taken a pay cut

31%

41%

18%

15%

12%

12%

14%

12%

11%

8%

Base: Total sample, n=1,017, multiple responses accepted

Further changes to the First Home Buyer incentives hits hard

New housing statistics from the Australian Bureau of Statistics (ABS) (2013) reveal that changestotheFirstHomeBuyerincentiveinNSWandQLD(Table1)havehadasignificantimpact.As of February 2013, the number of First Home Buyers as a percentage of total owner-occupied housing commitments has fallen by more than 5% since September 2012 and now sits at 14% nationally, an eight year low10 . This is due to record low First Home Buyer commitments in NSW and QLD (both less than 10%) – a plunge of more than 10% since the grants were replaced, while other states saw First Home Buyer commitments rise. There are concerns that VIC will follow suit as it replaces its First Home Owner Grant with a $10,000 new home owner grant as of 30 June 2013.

Table 1In October 2012, the state governments in NSW and QLD changed the concessions offered to First Home Buyers. The $7,000 First Home Owner Grant was replaced by a $15,000 grant only available to first home owners who purchase or build a new eligible home (including off-the-plan) up to the value of:

• $650,000 in NSW

• $750,000 in QLD

In NSW, the grant will reduce to $10,000 as of 1 January 2014.

10 ABS Housing Finance Australia 5609, March 2013 http://www.abs.gov.au/ausstats/[email protected]/mf/5609.0

15An annual study of the mortgage market in Australia

Survey respondents report less utilisation of the First Home Buyers grant for deposits, dropping from 17% in 2012 to 14% in 2013, with onlyoneinthreesayingthegrantchangeshavehadnoimpact on their decision to buy. Over one quarter of First Home Buyer respondents say it will considerably reduce their likelihood of entering the property market in the next year, while others indicate it will change the type of properties they can purchase (Chart 11).

Chart 11: Impact of First Home Buyer grant changes on intention to buy

28% 27%

20% 19%

13%

Considering a different location

Considering a smaller property

Considering buying something else and

upgrading

Will need to borrow (more) money from

family/friends

Considering a larger loan

Base: First Home Buyers in NSW and QLD, n=59

Changes to superannuation legislation likely to increase property investment, though outside of superannuation

Self-managed superannuation funds (SMSFs) have increased in popularity during their 18-year history by over 700%11, and thevalueofpropertyheldinSMSFsisgrowingbymorethan10%perannumaccordingtotheAustralianTaxationOffice(ATO), with trustees moving away from cash and instead looking to house their money in direct property12.

One in six (15%) current Mortgagors and Intenders currently have an SMSF and, of these, 22%alreadyownpropertyintheirSMSF, with another 22% planning to own property within their SMSF.

Table 2In 2013, the Federal Government proposed changes to superannuation legislation. From 1 July 2014, earnings of more than $100,000 on superannuation pensions and annuities will be taxed at 15 per cent instead of being tax-free.

At a rate of return of 5 per cent per annum, the Government expects the change will only affect people with more than $2 million in superannuation assets.

However this will have implications for the treatment of capital gains, which does not currently attract any taxation. Under the proposed changes, capital gains in excess of $100,000 on assets purchased after 1 July 2014 will be taxed at 15 per cent.

11 Self-managed super fund statistical report - March 2013, Population and Asset Allocation Tables. http://www.ato.gov.au/superfunds/content.aspx?menuid=49150&doc=/content/00353227.htm&page=8&H8

12 Multiport SMSF Investment Patterns Survey , March 2013 http://www.multiport.com.au/market-news/smsf-investment-patterns-survey.aspx

Changes to superannuation legislation proposed to commence in July 2014 (Table 2) are likely to have a small net positive effect on investment in the property market, though at a total level the impact is likely to encourage people to purchase outside of superannuation. Noticeably, the legislationchangesarelikelytohaveaverypositiveimpactonpropertypurchasesforthosewhoalreadyhaveanSMSF; particularly those who already hold property in their SMSF, as well as those in high income households (household income above $150,000) (Chart 12).

Chart 12: Impact of superannuation legislation changes on intention to buy

6% 7% 9%

22% 9%

18%

Total Have SMSF

More likely to buy property outside of super fund

More likely to buy property within super fund

Less likely to buy property within super fund

Base: Total sample, n=1,017; have SMSF, n=153; have property in SMSF, n=33

16 2013 Mortgage Barometer Report

17An annual study of the mortgage market in Australia

Loan-to-Value Ratio (LVR) is on the increase

Those about to enter the property market have high aspirations, so despite lessons that perhaps should have been learnt post-GFC (namely, over indebtedness), intendedLVRsareslowlyincreasing (Chart 13) from around 62% for purchases in 2012/13 to 65% for purchases more than one year from now (note, these are slight underestimates compared to actual ABS LVR figures which range in the low 70%13).

Chart 13: Actual and intended LVR by when bought/intend to purchase property

48% 50% 58%

62% 61% 65% 65%

5+ years ago n=295

4-5 years ago n=119

2-3 years ago n=176

last 12 months n=108

next 12 months n=208

1-2 years from now

n=129

3-5 years from now

n=224

This is likely to reflect the growing average loan size. ABSstatisticsconfirmthataveragemortgagerepaymentshaveleaptby105%overthepastdecade14 and survey respondents suggest that loan sizes are continuing to grow. The upper range of what Intenders are willing to borrow is well into the $400,000s whilst the average loan size at the start of 2013 was close to $300,000 (Chart 14).

13 AFG Mortgage Index May 2013 http://www.afgonline.com.au/afgretail_server/get-pdf?id=01_00311414 HIA-Commonwealth Bank Affordability Report, December Quarter 2012

What’s happening in the mortgage market?

18 2013 Mortgage Barometer Report

Chart 14: Current and intended LVR and loan size

Base: Mortgagors, n=698; First Home Owners, n=122; Current Investors, n=170; Owner Occupiers, n=519 Intenders, n=567; First Home Buyers, n=111; Potential Investors, n=263

Mortgagors

Intenders

Avg. Current LVR 53% 62% 55% 51%

Avg. Current Loan $295,000 $290,000 $382,000 $283,000

All current Mortgagors First Home Owners Current Investors Owner-Occupiers

Avg. Desired LVR 43-64% 44-62% 45-67%

Avg. Desired Loan $264,000- $411,000

$238,000- $373,000

$266,000- $429,000

All purchase intenders First Home Buyers Potential Investors

Housingloansarethereforebecomingalongertermcommitment; with the average life of a loan now 15 years (for Owner-Occupiers and Investors). According to the survey, one in three Owner-Occupiers and Investors (34%) say it will take more than 20 years to pay off their loan, while more than one in two (56%) First Home Buyers expect to take more than 20 years to pay off their home loan.

The proportion of buyers who have a deposit of less than 20% is stable (19% in 2012). The majority of people will source their deposit from savings (63%).

Low interest rates are helping Mortgagors get ahead

“It’s almost as if there was an obsession with taking on debt prior to the Global Financial Crisis, now we’ve got a bit of an obsession with paying down debt.” Dr Oliver, AMP Chief Economist15.

The RBA noted this year that Australians have been taking advantage of the near-record low interest rates, and hence lower minimum repayments, to get ahead on their mortgages.

15 Elsworth S. Aussies are $160bn ahead on mortgages (March 2013). http://www.news.com.au/realestate/aussies-are-160bn-ahead-on-mortgages/story-fncq3era-1226609151657

19An annual study of the mortgage market in Australia

Chart 15: Changes in minimum monthly mortgage repayments16

Total Sydney Melbourne Brisbane Perth Adelaide

Dec-11 $2,972 $3,728 $3,260 $3,078 $3,288 $2,651

Mar-12 $2,840 $3,794 $3,078 $2,965 $3,331 $2,555

Jun-12 $2,812 $3,703 $3,090 $3,008 $3,184 $2,428

Sep-12 $2,686 $3,543 $2,983 $2,842 $3,105 $2,391

Dec-12 $2,633 $3,471 $2,937 $2,770 $3,064 $2,315

Australian families are now a record 14% ($160 billion) ahead on their mortgages, squirrelingawayanextra$30billionsincethestartoftheGFC15.Almosthalf(46%)ofMortgagorssurveyedsaytheypaidoffmorethantheirminimumloanrepaymentsinthelast12months.

But mortgage strain is still a concern

Oneinfive(21%)Mortgagorssurveyedsaytheyhavestruggledat least a few times in the last 12 months to make minimum mortgage repayments, with a similar number (19%) agreeing that their mortgage repayments have placed them under financial strain. 4% say they frequently struggled to make their minimum repayments. The results of the survey would suggest that experience of mortgage strain is not explicitly linked to household income.

According to the latest Fitch Dinkum Index therehasbeenaslightdeteriorationinmortgageperformance in Australia in Q4 2012, with a 10 basis point increase in the number of borrowers falling behind on their mortgage repayments by one month or more (now 1.45%)17.

Costoflivingisthestrongesteconomicdriverofaffordability amongst survey respondents; job losses and reduction in work hours are the most common correlations with those experiencing difficulty in making minimum repayments.

Rate of mortgage refinancing has dropped, perhaps due to lower rate pressure

In 2013, only 13% of surveyed Mortgagors had refinanced their loan in the last 12 months, down from 17% in 2012. Slightly more (21%) think they will refinance in the next 12 months.

Refinancing seems bound to rate chasing rather than dissatisfaction with lenders, with 74% of refinancers staying with the same lender and only 37% of potential refinancers looking for a new lender.

Going direct to lenders is still the norm

Overathird(38%)ofmortgageseekersconsultedamortgagebroker during the loan application process, with 61% applying directly through a lender and 22% going with their current bank. Interestingly, First Home Buyers are no likelier to consult brokers, though they are more likely to consult family and friends (32% vs. 12% of all mortgage seekers) and do their own research (57% vs. 37% of all mortgage seekers).

Therespondents’primarymotivationforapplyingthroughamortgagebrokerisconvenience, rather than the belief they will get a better deal, with the key benefit being that brokers take on the responsibility of conducting the research and are better at explaining different mortgage options (Chart 16). One in five of those respondents who apply for a mortgage directly through a bank actually prefer not to enlist the help of a broker.

16 HIA-Commonwealth Bank Affordability Report, December Quarter 201217 Fitch Ratings, Sydney (April 9 2013). http://www.fitchratings.com/creditdesk/press_releases/detail.cfm?pr_id=787983

20 2013 Mortgage Barometer Report

Chart 16: Reasons for applying for mortgages through a broker versus direct through the lender

58%

51%

40%

20%

37%

31%

6%

48%

32%

16%

19%

24%

22%

More convenient

Do the research for me

I think I will get a better deal

Less paperwork involved

Helps me understand the different mortgage options

Helps me to get a mortgage tailored to my needs

I prefer not to deal with banks/brokers Broker Direct

Base: Applied/will apply for a mortgage through a broker, n=347; Applied/will apply direct through the lender, n=570

Big 4 lenders hold market share because of their size

Just under two thirds (62%) of all current and potential Mortgagors chose/will choose one of the Big 4 banks (The Commonwealth Bank, NAB, Westpac and ANZ) for their mortgage. Investors are slightly more likely (67%) to go with a Big 4 bank.

Many current Mortgagors have a mortgage with a smaller bank or lender (27%) whereas those intending to get a mortgage are less likely to report wanting to go with one of these lenders (19%).

The primary motivation for taking out a mortgage with a Big 4 bank is an existing relationship (44% vs. 32% for other lenders), but thekeydifferentiatorbetweentheBig4banksandotherlendersistheperceivedfinancialsecurityoftheBig4 (32% vs. 6%). Financial security is particularly important for Investors (28%) and First Home Buyers (57%). First Home Buyers also particularly value the reputation of the Big 4 banks (39%).

Meanwhile, other lenders are chosen for offering better rates, having more suitable products and for caring for their customers (Chart 17).

21An annual study of the mortgage market in Australia

Chart 17: Reasons for choosing a Big 4 bank over other lenders

Base: Have/intend to have mortgage with Big 4 bank, n=552; Have/intend to have mortgage with another lender, n=305

44%

34%

32%

24%

23%

31%

44%

6%

48%

15%

37%

17%

I have other banking products with them

Have the mortgage which best suits my needs

Better financial security

Better rates

Better reputation

Care more about their customers

Not all about shareholders/profits Big 4

Other FS

Chart 16: Reasons for applying for mortgages through a broker versus direct through the lender

58%

51%

40%

20%

37%

31%

6%

48%

32%

16%

19%

24%

22%

More convenient

Do the research for me

I think I will get a better deal

Less paperwork involved

Helps me understand the different mortgage options

Helps me to get a mortgage tailored to my needs

I prefer not to deal with banks/brokers Broker Direct

Base: Applied/will apply for a mortgage through a broker, n=347; Applied/will apply direct through the lender, n=570

Big 4 lenders hold market share because of their size

Just under two thirds (62%) of all current and potential Mortgagors chose/will choose one of the Big 4 banks (The Commonwealth Bank, NAB, Westpac and ANZ) for their mortgage. Investors are slightly more likely (67%) to go with a Big 4 bank.

Many current Mortgagors have a mortgage with a smaller bank or lender (27%) whereas those intending to get a mortgage are less likely to report wanting to go with one of these lenders (19%).

The primary motivation for taking out a mortgage with a Big 4 bank is an existing relationship (44% vs. 32% for other lenders), but thekeydifferentiatorbetweentheBig4banksandotherlendersistheperceivedfinancialsecurityoftheBig4 (32% vs. 6%). Financial security is particularly important for Investors (28%) and First Home Buyers (57%). First Home Buyers also particularly value the reputation of the Big 4 banks (39%).

Meanwhile, other lenders are chosen for offering better rates, having more suitable products and for caring for their customers (Chart 17).

22 2013 Mortgage Barometer Report

What does the future mortgage market look like?Property preferences are changing

Whilstexistinghousesarestillthepreferredpropertytypeofrespondents,interestinthismarketisdeclininginfavourofgrowinginterestinnewdevelopments (Chart 18 and 19). Changes to First Home Buyer grants appear to be having an effect, with First Home Buyers more likely to consider new houses (up to one in two in this group) and units (one in three). The effect, however, is not limited to this group with Investors and Owner-Occupiers also more interested in buying new developments in 2013 than in 2012 (8% and 5% increase, respectively).

Chart 18: Type of property looking to buy - New developments

29% 13% 15%

5% 4%

35% 19% 16%

6% 7%

2012 2013

34% 21% 19%

10% 6%

49% 30% 22%

8% 8%

26% 8% 14%

3% 4%

34% 18% 13% 6% 6%

27% 10% 6% 0% 2%

32% 22% 17%

8% 8%

Base: Intend to buy in the next five years. Total, 2012 n=488, 2013 n=680 First Home Buyers 2013 n=115, Owner-Occupiers 2013 n=285, Investors 2013 n=316

New developments

Majority still want to purchase in capital cities

Compared to 2012, thereislittlechangeinwherepeoplewanttobuy. Less than 10% want to buy in another state and just under three in four (73%) want to buy in capital cities. There is a slight shift in city location preferences, with 48% saying they’re looking to buy in the outer suburbs (compared to 42% in 2012).

For those looking to buy in Sydney, the most popular areas are the Inner West (42%), followed by Parramatta (29%) and the Lower North Shore (27%). The Lower North Shore is a particular hot spot for First Home Buyers in Sydney, with almost one in two (47%) ranking this area as a place they’re looking to buy.

23An annual study of the mortgage market in Australia

Within Melbourne, the most popular areas to buy are in the East: Both the South East (40%) and Eastern Melbourne (31%), as well as the CBD (25%). First Home Buyers in Melbourne are particularly interested in the city and fringe: 42% say they’re looking to buy in the CBD, 40% in the Inner West and 39% in the Inner North.

Chart 19: Type of property looking to buy - Existing dwellings

Total

First Home Buyers

Owner-occupiers

Investors

House Unit Town- house

Terrace Semi Land Holiday house

69%

21% 24% 9% 9% 7% 0%

56%

24% 20% 7% 8% 6% 2%

2012 2013

69%

31% 34%

11% 12% 7% 0%

61%

32% 27% 10% 12% 7% 1%

68%

14% 17% 8% 7% 6% 0%

59%

24% 18% 5% 7% 5% 3%

69%

15% 23% 6% 8% 13%

0%

55%

30% 24% 9% 10% 5% 4%

Base: Intend to buy in the next five years Total, 2012 n=488, 2013 n=680 First Home Buyers 2013 n=115, Owner-Occupiers 2013 n=285, Investors 2013 n=316

Existing Dwellings

First Home Buyer profile hasn’t changed

Although ABS data shows that First Home Buyers are shrinking as a proportion of the total property market18, who they are is not changing. As we saw in 2012, First Home Buyers tend to be under 35 years old, have a household income of under $100,000, and are SINKs (Single Income, No Kids) or DINKs (Double Income, No Kids).

Apartfromdemographics,FirstHomeBuyersalsodifferintermsofhousingpreferences from the rest of those intending to buy residential property in the next five years (Chart 20). First Home Buyers are not only more eager to enter the market (44% want to buy in the next 12 months vs. 26% of all respondents), but they’re also more likely to be interested in new developments, particularly new houses (67% and 49% respectively vs. 53% and 35% for all respondents). This difference has been heightened with the roll out of new changes to First Home Buyer incentives.

18 ABS Housing Finance Australia 5609, March 2013 http://www.abs.gov.au/ausstats/[email protected]/mf/5609.0

24 2013 Mortgage Barometer Report

Chart 20: Key sub-group differences

Total sample n=1,017 Owner-Occupiers n=558 First Home Buyers n=115 Current Investors n=176

33% under 35 22% under 35 67% under 35 64% under 45

51% Families 59% Families 26% SINKs, 24% DINKs 38% Young Families

63% HH income <$100k 18% investments >$550k

58% HH income <$100k 19% investments >$550k

67% HH income <$100k 8% investments >$550k

43% HH income <$100k

47% investments >$550k

26% will buy in the next 12 months

21% will buy in the next 12 months

44% will buy in the next 12 months

39% will buy in the next 12 months

Looking to buy… Looking to buy… Looking to buy… Looking to buy…

New developments 53% New developments 51% New developments 67% New developments 49%

Existing dwellings 74% Existing dwellings 73% Existing dwellings 81% Existing dwellings 73%

Current mortgage: $295,000 Current mortgage: $283,000 Intended mortgage: Current mortgage:

$381,000 $373,000

The investment market is recovering

ABS statistics reveal thatloanstoinvestorshavesoared16%inthelastyear, compared to only 6.6% growth for the traditional property heartland Owner-Occupiers19.

Survey data also confirms an increased interest in investing; of those looking to buy residential property in the next five years, 42% said they were doing so for an investment (up from 26% in 2012). Currently 7.9% of Australians aged 18 plus classify themselves as Investors, while a further 13.8% intend to become investors in 2013.

PotentialInvestorsarethemostlikelyofanyIntenderstothinkthenextsixmonths is the best time to buy (31% vs. 24% of all intenders), and 18% will buy in the next six months (on average).

Whilst property investments are taking off, so is an interest in new developments (Chart 18), though Investors are still likely to stick to investing in their local area (84%). Like all people entering the property market, the greatest interest lies in the inner city/city fringe (24%and 35% of investors respectively).

Investors tend to be slightly younger than other property owners and Intenders (First Home Buyers aside) and are more economically advantaged (only 43% have household income under $100,000 and 47% have assets over $550,000 compared to 18% for all respondents).

19 ABS Housing Finance Australia 5609, March 2013 http://www.abs.gov.au/ausstats/[email protected]/mf/5609.0

25An annual study of the mortgage market in Australia

MethodologyThe survey upon which this report is based was an online survey targeting Australian adults (aged 18+) who either have a current residential mortgage or who intend to buy residential property (as an investment or a home) in the next 5 years.

The survey was developed by GfK Australia in consultation with QBE, and fieldwork was conducted via an online panel from 1 May to 13 May 2013.

Data was weighted to the Australian population according to 2011 census data.

Minimum samples of n=500 were set for the two core target sample groups: Mortgagors and Intenders, which were met through natural fall out of the sample. Of the 1,107 responses collected, 763 were Mortgagors and 680 were Intenders, with 399 qualifying for both. Throughout the report the following subgroups are referred to as follows:

• Mortgagors (have a current residential mortgage)

– 34.1% of the population, 68% of the sample, n=763

• Intenders (intend to buy a residential property in the next five years)

– 34.9% of the population, 69% of the sample, n=680

• First Home Buyers (house hunters looking for their first home)

– 6.3% of the population, 11% of the sample, n=115

• Owner-Occupiers (have a mortgage for the home they live in)

– 26.0% of the population, 55% of the sample, n=558

• Current Investors (currently have a mortgage for an investment property)

– 7.9% of the population, 17% of the sample, n=176

• Potential Investors (intend to buy an investment property in the next 5 years)

– 13.8% of the population, 28% of the sample, n=286

• First Home Owners (currently have a mortgage on their first home)

– 5.8% of the population, 12% of the sample, n=127

The total target sample is 50.2% of the Australian adult population.

26 2013 Mortgage Barometer Report

Sample profiles

27An annual study of the mortgage market in Australia

Total market profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 30.4 First home owner 16.8 In last 12 months 15.2

Mortgagor and intend to buy 37.5 Owner-occupier only 58.8 2-3 years ago 24.7

No mortgage, intend to buy 32.1 Investor only 6.6 4-5 years ago 16.6

Nett mortgagor 67.9 Investor & owner-occupier 17.2 More than 5 years ago 43.5

Nett intend to buy 69.5 Holiday house 1.0 When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 6.6 First Home Buyer 17.1 Existing house 56.4

In next 4-6 months 11.5 Subsequent home buyer 64.2 Existing unit 24.5

In next 7-12 months 18.8 Investor 41.7 Other existing property 23.0

In next 13-24 months 23.2 New house 35.2

In next 3-5 years 39.8 New unit 19.1

Other new development 19.1

Land 5.6

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 82.1 In the 2nd half of 2013…

I am better off owning a home than renting 71.8 Will rise by more than 0.5% 5.0

Property prices will increase strongly in the next three years 47.2 Will rise by up to 0.5% 22.8

The housing price 'bubble' will burst and prices will fall 27.9 Will stay the same 43.0

Worry I’ll never be able to afford my own home 24.3 Will drop by up to 0.5% 26.8

Property is undervalued 25.4 Will drop by more than 0.5% 2.4

Property is overvalued 45.2

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 27.0 Next 6 months 31.9

Property will become increasingly unaffordable in the next year 47.9 In 7-12 months’ time 23.8

13-18 months’ time 15.5

Avg. Mortgage Avg. LVR Had/have <20% deposit

Loan with Big 4 bank

Use mortgage

broker Current mortgagors $295,000 52.8 11.1% 61.7% 38.8% Intend to buy in next 5 years $411,111 63.6 19.6% 62.3% 37.3%

Gender % Age % Life Stage %

Male 50.8 18-24 years 9.5 SINKs 13.4

Female 49.2 25-34 years 23.2 DINKs 15.5

35-44 years 24.2 Family, primary aged kids 29.3

45-54 years 20.9 Family, high school aged kids 11.0

55-65 years 13.9 Adult family 10.4

Over 65 years 8.3 Older (55+) singles/couples 9.4

Retirees 10.7 State/Terr itory % Location % Marital Status %

NSW & ACT 33.0 Capital city 63.9 Single 18.3

VIC & TAS 27.5 Regional centre 27.4 Live with partner/married 71.7

QLD 19.4 Rural area 8.8 Separated/Divorced/Widowed 9.5

WA 11.3

SA & NT 8.8 Education % Household Income# % Investments# %

Primary 0.2 Sole income earner 32.0 No investments 20.4

Part of high school 8.5 Main income earner 22.8 $50,000 or less 17.2

Completed high school 16.8 $50,000 or less 21.8 $50,001 - $150,000 16.3

Diploma or certificate 31.8 $50,001 - $75,000 18.6 $150,001 - $250,000 16.7

Degree qualification 29.7 $75,001 - $100,000 22.1 $250,001 - $350,000 11.3

Postgraduate qualification 13.1 $100,001 - $150,000 24.3 $350,001 - $550,000 5.8

$150,001 - $200,000 8.8 $550,001 - $1 million 6.1

More than $200,000 4.3 More than $1 million 6.1

Base: Total sample, n=1,017* Percentage of all current Mortgagors n=736 ^ Percentage of all those intending to purchase residential property in the next 5 years n=680 # Percentage excluding don’t know /prefer not to say responses

28 2013 Mortgage Barometer Report

Current Mortgagors profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 46.2 First home owner 16.8 In last 12 months 15.2

Mortgagor and intend to buy 53.8 Owner-occupier only 58.8 2-3 years ago 24.7

No mortgage, intend to buy 0 Investor only 6.6 4-5 years ago 16.6

Nett mortgagor 100 Investor & owner-occupier 17.2 More than 5 years ago 43.5

Nett intend to buy 53.8 Holiday house 1.0 When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 7.5 First Home Buyer 0.0 Existing house 54.9

In next 4-6 months 11.2 Subsequent home buyer 100 Existing unit 25.0

In next 7-12 months 19.9 Investor 57.6 Other existing property 21.7

In next 13-24 months 19.4 New house 36.2

In next 3-5 years 41.9 New unit 19.5

Other new development 19.4

Land 5.6

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 83.4 In the 2nd half of 2013…

I am better off owning a home than renting 73.4 Will rise by more than 0.5% 4.7

Property prices will increase strongly in the next three years 48.8 Will rise by up to 0.5% 23.1

The housing price 'bubble' will burst and prices will fall 26.5 Will stay the same 42.0

Worry I’ll never be able to afford my own home 17.8 Will drop by up to 0.5% 28.3

Property is undervalued 30.3 Will drop by more than 0.5% 2.0

Property is overvalued 41.9

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 17.9 Next 6 months 34.7

Property will become increasingly unaffordable in the next year 39.4 In 7-12 months’ time 24.7

13-18 months’ time 14.2

Avg. Mortgage

Avg. Loan-to-value rat io

Had/have <20% deposit

Loan with Big 4 bank

Use mortgage broker

Current mortgagors $295,000 52.8 11.1% 61.7% 38.8%

Intend to buy in next 5 years $428,000 64.3 19.3% 68.2% 41.4% Gender % Age % Life Stage %

Male 51.0 18-24 years 6.3 SINKs 11.6

Female 49.0 25-34 years 24.5 DINKs 16.2

35-44 years 26.2 Family, primary aged kids 33.0

45-54 years 22.8 Family, high school aged kids 12.1

55-65 years 13.6 Adult family 8.8

Over 65 years 6.7 Older (55+) singles/couples 9.3

Retirees 8.8 State/Terr itory % Location % Marital Status %

NSW & ACT 32.2 Capital city 66.0 Single 13.3

VIC & TAS 28.7 Regional centre 25.0 Live with partner/married 76.7

QLD 19.0 Rural area 9.0 Separated/Divorced/Widowed 9.4

WA 10.8

SA & NT 9.3 Education % Household Income# % Investments# %

Primary 0.1 Sole income earner 31.7 No investments 18.6

Part of high school 9.2 Main income earner 22.1 $50,000 or less 16.3

Completed high school 16.2 $50,000 or less 17.9 $50,001 - $150,000 17.4

Diploma or certificate 31.1 $50,001 - $75,000 16.2 $150,001 - $250,000 16.8

Degree qualification 29.8 $75,001 - $100,000 25.1 $250,001 - $350,000 12.2

Postgraduate qualification 13.5 $100,001 - $150,000 26.5 $350,001 - $550,000 6.1

$150,001 - $200,000 9.5 $550,001 - $1 million 6.7

More than $200,000 4.8 More than $1 million 5.9

Base: Current Mortgagors, n=736 * Percentage of all current Mortgagors n=680 ^ Percentage of all those intending to purchase n=399 # Percentage excluding don’t know /prefer not to say responses xx Significantly higher than Intenders xx Significantly lower than Intenders

29An annual study of the mortgage market in Australia

Property Intenders (will purchase residential property in the next 5 years) profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 0 First home owner 19.3 In last 12 months 16.8

Mortgagor and intend to buy 57.7 Owner-occupier 47.2 2-3 years ago 31.0

No mortgage, intend to buy 42.3 Investor 9.4 4-5 years ago 16.7

Nett mortgagor 42.3 Investor & owner-occupier 23.4 More than 5 years ago 35.5

Nett intend to buy 100 Holiday house 0.8 When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 6.6 First Home Buyer 17.1 Existing house 56.4

In next 4-6 months 11.5 Subsequent home buyer 64.2 Existing unit 24.5

In next 7-12 months 18.8 Investor 41.7 Other existing property 23.0

In next 13-24 months 23.2 New house 35.2

In next 3-5 years 39.8 New unit 19.1

Other new development 19.1

Land 5.6

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 81.4 In the 2nd half of 2013…

I am better off owning a home than renting 69.8 Will rise by more than 0.5% 5.5

Property prices will increase strongly in the next three years 46.7 Will rise by up to 0.5% 23.5

The housing price 'bubble' will burst and prices will fall 31.4 Will stay the same 41.1

Worry I’ll never be able to afford my own home 30.9 Will drop by up to 0.5% 27.1

Property is undervalued 25.6 Will drop by more than 0.5% 2.8

Property is overvalued 51.9

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 24.7 Next 6 months 27.2

Property will become increasingly unaffordable in the next year 41.0 In 7-12 months’ time 26.1

13-18 months’ time 16.1

Avg. Mortgage

Avg. Loan-to-value rat io

Had/have <20% deposit

Loan with Big 4 bank

Use mortgage broker

Current mortgagors $310,000 53.8 11.3% 68.2% 41.4%

Intend to buy in next 5 years $412,000 63.6 19.6% 62.3% 37.3% Gender % Age % Life Stage %

Male 52.6 18-24 years 12.1 SINKs 15.8

Female 47.4 25-34 years 26.7 DINKs 16.4

35-44 years 24.3 Family, primary aged kids 30.3

45-54 years 19.6 Family, high school aged kids 10.7

55-65 years 11.1 Adult family 10.7

Over 65 years 6.2 Older (55+) singles/couples 7.1

Retirees 8.6 State/Terr itory % Location % Marital Status %

NSW & ACT 34.0 Capital city 66.0 Single 22.5

VIC & TAS 28.6 Regional centre 27.0 Live with partner/married 70.0

QLD 19.4 Rural area 7.0 Separated/Divorced/Widowed 7.1

WA 9.6

SA & NT 8.4 Education % Household Income# % Investments# %

Primary 0.3 Sole income earner 32.6 No investments 17.5

Part of high school 5.7 Main income earner 26.1 $50,000 or less 17.0

Completed high school 16.0 $50,000 or less 20.4 $50,001 - $150,000 14.4

Diploma or certificate 30.5 $50,001 - $75,000 17.8 $150,001 - $250,000 18.8

Degree qualification 33.9 $75,001 - $100,000 21.9 $250,001 - $350,000 11.3

Postgraduate qualification 13.7 $100,001 - $150,000 24.8 $350,001 - $550,000 6.5

$150,001 - $200,000 10.1 $550,001 - $1 million 6.5

More than $200,000 5.0 More than $1 million 8.0

Base: Intenders, n=680 * Percentage of all current Mortgagors n=399 ^ Percentage of all those intending to purchase n=380 # Percentage excluding don’t know /prefer not to say responses xx Significantly higher than Mortgagors xx Significantly lower than Mortgagors

Current Mortgagors profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 46.2 First home owner 16.8 In last 12 months 15.2

Mortgagor and intend to buy 53.8 Owner-occupier only 58.8 2-3 years ago 24.7

No mortgage, intend to buy 0 Investor only 6.6 4-5 years ago 16.6

Nett mortgagor 100 Investor & owner-occupier 17.2 More than 5 years ago 43.5

Nett intend to buy 53.8 Holiday house 1.0 When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 7.5 First Home Buyer 0.0 Existing house 54.9

In next 4-6 months 11.2 Subsequent home buyer 100 Existing unit 25.0

In next 7-12 months 19.9 Investor 57.6 Other existing property 21.7

In next 13-24 months 19.4 New house 36.2

In next 3-5 years 41.9 New unit 19.5

Other new development 19.4

Land 5.6

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 83.4 In the 2nd half of 2013…

I am better off owning a home than renting 73.4 Will rise by more than 0.5% 4.7

Property prices will increase strongly in the next three years 48.8 Will rise by up to 0.5% 23.1

The housing price 'bubble' will burst and prices will fall 26.5 Will stay the same 42.0

Worry I’ll never be able to afford my own home 17.8 Will drop by up to 0.5% 28.3

Property is undervalued 30.3 Will drop by more than 0.5% 2.0

Property is overvalued 41.9

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 17.9 Next 6 months 34.7

Property will become increasingly unaffordable in the next year 39.4 In 7-12 months’ time 24.7

13-18 months’ time 14.2

Avg. Mortgage

Avg. Loan-to-value rat io

Had/have <20% deposit

Loan with Big 4 bank

Use mortgage broker

Current mortgagors $295,000 52.8 11.1% 61.7% 38.8%

Intend to buy in next 5 years $428,000 64.3 19.3% 68.2% 41.4% Gender % Age % Life Stage %

Male 51.0 18-24 years 6.3 SINKs 11.6

Female 49.0 25-34 years 24.5 DINKs 16.2

35-44 years 26.2 Family, primary aged kids 33.0

45-54 years 22.8 Family, high school aged kids 12.1

55-65 years 13.6 Adult family 8.8

Over 65 years 6.7 Older (55+) singles/couples 9.3

Retirees 8.8 State/Terr itory % Location % Marital Status %

NSW & ACT 32.2 Capital city 66.0 Single 13.3

VIC & TAS 28.7 Regional centre 25.0 Live with partner/married 76.7

QLD 19.0 Rural area 9.0 Separated/Divorced/Widowed 9.4

WA 10.8

SA & NT 9.3 Education % Household Income# % Investments# %

Primary 0.1 Sole income earner 31.7 No investments 18.6

Part of high school 9.2 Main income earner 22.1 $50,000 or less 16.3

Completed high school 16.2 $50,000 or less 17.9 $50,001 - $150,000 17.4

Diploma or certificate 31.1 $50,001 - $75,000 16.2 $150,001 - $250,000 16.8

Degree qualification 29.8 $75,001 - $100,000 25.1 $250,001 - $350,000 12.2

Postgraduate qualification 13.5 $100,001 - $150,000 26.5 $350,001 - $550,000 6.1

$150,001 - $200,000 9.5 $550,001 - $1 million 6.7

More than $200,000 4.8 More than $1 million 5.9

Base: Current Mortgagors, n=736 * Percentage of all current Mortgagors n=680 ^ Percentage of all those intending to purchase n=399 # Percentage excluding don’t know /prefer not to say responses xx Significantly higher than Intenders xx Significantly lower than Intenders

30 2013 Mortgage Barometer Report

First Home Buyers profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 0.0 First home owner N/A In last 12 months N/A

Mortgagor and intend to buy 0.0 Owner-occupier N/A 2-3 years ago N/A

No mortgage, intend to buy 100 Investor N/A 4-5 years ago N/A

Nett mortgagor 0.0 Investor & owner-occupier N/A More than 5 years ago N/A

Nett intend to buy 100 Holiday house N/A When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 5.9 First Home Buyer 100 Existing house 61.2

In next 4-6 months 12.2 Subsequent home buyer 0.0 Existing unit 32.4

In next 7-12 months 26.0 Investor 3.5 Other existing property 31.1

In next 13-24 months 24.6 New house 48.7

In next 3-5 years 31.3 New unit 29.8

Other new development 23.0

Land 7.0

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 84.2 In the 2nd half of 2013…

I am better off owning a home than renting 64.0 Will rise by more than 0.5% 7.5

Property prices will increase strongly in the next three years 42.3 Will rise by up to 0.5% 25.0

The housing price 'bubble' will burst and prices will fall 37.7 Will stay the same 46.2

Worry I’ll never be able to afford my own home 69.2 Will drop by up to 0.5% 19.3

Property is undervalued 12.5 Will drop by more than 0.5% 1.9

Property is overvalued 76.4

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 51.3 Next 6 months 28.6

Property will become increasingly unaffordable in the next year 50.1 In 7-12 months’ time 24.6

13-18 months’ time 14.5

Avg. Mortgage

Avg. Loan-to-value rat io

Had/have <20% deposit

Loan with Big 4 bank

Use mortgage broker

Current mortgagors N/A N/A N/A N/A N/A

Intend to buy in next 5 years $373,000 61.9 21.2% 46.2% 30.9% Gender % Age % Life Stage %

Male 52.4 18-24 years 29.5 SINKs 25.9

Female 47.6 25-34 years 37.5 DINKs 24.0

35-44 years 25.1 Family, primary aged kids 31.0

45-54 years 7.2 Family, high school aged kids 0.9

55-65 years 0.7 Adult family 16.6

Over 65 years 0.0 Older (55+) singles/couples 1.6

Retirees 0.0 State/Terr itory % Location % Marital Status %

NSW & ACT 35.5 Capital city 69.3 Single 43.1

VIC & TAS 30.6 Regional centre 25.1 Live with partner/married 53.3

QLD 18.4 Rural area 5.7 Separated/Divorced/Widowed 2.5

WA 8.1

SA & NT 7.4 Education % Household Income# % Investments# %

Primary 0.0 Sole income earner 34.6 No investments 34.8

Part of high school 4.8 Main income earner 24.7 $50,000 or less 26.9

Completed high school 19.9 $50,000 or less 22.2 $50,001 - $150,000 12.8

Diploma or certificate 30.5 $50,001 - $75,000 29.5 $150,001 - $250,000 14.3

Degree qualification 33.0 $75,001 - $100,000 15.3 $250,001 - $350,000 2.8

Postgraduate qualification 11.8 $100,001 - $150,000 23.7 $350,001 - $550,000 3.2

$150,001 - $200,000 7.1 $550,001 - $1 million 1.5

More than $200,000 2.2 More than $1 million 3.7

Base: First Home Buyers n=115, * Percentage of all current Mortgagors n=0 ^ Percentage of all those intending to purchase n=115 # Percentage excluding don’t know /prefer not to say responses xx Significantly higher than other groups xx Significantly lower than other groups

31An annual study of the mortgage market in Australia

Owner-Occupier profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 49.4 First home owner 0.0 In last 12 months 13.2

Mortgagor and intend to buy 49.9 Owner-occupier 77.5 2-3 years ago 20.5

No mortgage, intend to buy 0.7 Investor 0.0 4-5 years ago 16.4

Nett mortgagor 99.3 Investor & owner-occupier 22.5 More than 5 years ago 49.9

Nett intend to buy 50.6 Holiday house 0.4 When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 4.9 First Home Buyer N/A Existing house 58.8

In next 4-6 months 4.3 Subsequent home buyer N/A Existing unit 23.5

In next 7-12 months 11.1 Investor N/A Other existing property 20.0

In next 13-24 months 9.4 New house 33.5

In next 3-5 years 21.0 New unit 17.7

Other new development 15.8

Land 5.1

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 83.5 In the 2nd half of 2013…

I am better off owning a home than renting 77.7 Will rise by more than 0.5% 4.1

Property prices will increase strongly in the next three years 47.0 Will rise by up to 0.5% 22.5

The housing price 'bubble' will burst and prices will fall 26.6 Will stay the same 40.2

Worry I’ll never be able to afford my own home 13.8 Will drop by up to 0.5% 31.0

Property is undervalued 31.6 Will drop by more than 0.5% 2.2

Property is overvalued 41.8

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 16.4 Next 6 months 34.6

Property will become increasingly unaffordable in the next year 37.8 In 7-12 months’ time 23.6

13-18 months’ time 13.3

Avg. Mortgage

Avg. Loan-to-value rat io

Had/have <20% deposit

Loan with Big 4 bank

Use mortgage broker

Current mortgagors $283,000 51.04 10.1% 59.6% 36.3% Intend to buy in next 5 years $378,000 63.4 17.7% 67.6% 38.8% Gender % Age % Life Stage %

Male 49.6 18-24 years 3.9 SINKs 11.1

Female 50.4 25-34 years 18.0 DINKs 13.5

35-44 years 27.0 Family, primary aged kids 30.1

45-54 years 26.1 Family, high school aged kids 12.4

55-65 years 16.5 Adult family 10.4

Over 65 years 8.5 Older (55+) singles/couples 11.3

Retirees 10.7 State/Terr itory % Location % Marital Status %

NSW & ACT 30.0 Capital city 62.5 Single 12.4

VIC & TAS 28.1 Regional centre 27.5 Live with partner/married 76.6

QLD 20.3 Rural area 10.0 Separated/Divorced/Widowed 10.6

WA 11.9

SA & NT 9.7 Education % Household Income# % Investments# %

Primary 0.0 Sole income earner 31.3 No investments 20.4

Part of high school 10.6 Main income earner 22.4 $50,000 or less 16.1

Completed high school 18.1 $50,000 or less 19.7 $50,001 - $150,000 16.5

Diploma or certificate 30.8 $50,001 - $75,000 16.4 $150,001 - $250,000 16.2

Degree qualification 27.5 $75,001 - $100,000 21.7 $250,001 - $350,000 12.0

Postgraduate qualification 13.0 $100,001 - $150,000 27.5 $350,001 - $550,000 5.5

$150,001 - $200,000 9.3 $550,001 - $1 million 7.7

More than $200,000 5.5 More than $1 million 5.6

Base: Owner-occupiers n=558 * Percentage of all current mortgagors n=558 ^ Percentage of all those intending to purchase n=285 # Percentage excluding don’t know /prefer not to say responses xx Significantly higher than other groups xx Significantly lower than other groups

First Home Buyers profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 0.0 First home owner N/A In last 12 months N/A

Mortgagor and intend to buy 0.0 Owner-occupier N/A 2-3 years ago N/A

No mortgage, intend to buy 100 Investor N/A 4-5 years ago N/A

Nett mortgagor 0.0 Investor & owner-occupier N/A More than 5 years ago N/A

Nett intend to buy 100 Holiday house N/A When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 5.9 First Home Buyer 100 Existing house 61.2

In next 4-6 months 12.2 Subsequent home buyer 0.0 Existing unit 32.4

In next 7-12 months 26.0 Investor 3.5 Other existing property 31.1

In next 13-24 months 24.6 New house 48.7

In next 3-5 years 31.3 New unit 29.8

Other new development 23.0

Land 7.0

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 84.2 In the 2nd half of 2013…

I am better off owning a home than renting 64.0 Will rise by more than 0.5% 7.5

Property prices will increase strongly in the next three years 42.3 Will rise by up to 0.5% 25.0

The housing price 'bubble' will burst and prices will fall 37.7 Will stay the same 46.2

Worry I’ll never be able to afford my own home 69.2 Will drop by up to 0.5% 19.3

Property is undervalued 12.5 Will drop by more than 0.5% 1.9

Property is overvalued 76.4

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 51.3 Next 6 months 28.6

Property will become increasingly unaffordable in the next year 50.1 In 7-12 months’ time 24.6

13-18 months’ time 14.5

Avg. Mortgage

Avg. Loan-to-value rat io

Had/have <20% deposit

Loan with Big 4 bank

Use mortgage broker

Current mortgagors N/A N/A N/A N/A N/A

Intend to buy in next 5 years $373,000 61.9 21.2% 46.2% 30.9% Gender % Age % Life Stage %

Male 52.4 18-24 years 29.5 SINKs 25.9

Female 47.6 25-34 years 37.5 DINKs 24.0

35-44 years 25.1 Family, primary aged kids 31.0

45-54 years 7.2 Family, high school aged kids 0.9

55-65 years 0.7 Adult family 16.6

Over 65 years 0.0 Older (55+) singles/couples 1.6

Retirees 0.0 State/Terr itory % Location % Marital Status %

NSW & ACT 35.5 Capital city 69.3 Single 43.1

VIC & TAS 30.6 Regional centre 25.1 Live with partner/married 53.3

QLD 18.4 Rural area 5.7 Separated/Divorced/Widowed 2.5

WA 8.1

SA & NT 7.4 Education % Household Income# % Investments# %

Primary 0.0 Sole income earner 34.6 No investments 34.8

Part of high school 4.8 Main income earner 24.7 $50,000 or less 26.9

Completed high school 19.9 $50,000 or less 22.2 $50,001 - $150,000 12.8

Diploma or certificate 30.5 $50,001 - $75,000 29.5 $150,001 - $250,000 14.3

Degree qualification 33.0 $75,001 - $100,000 15.3 $250,001 - $350,000 2.8

Postgraduate qualification 11.8 $100,001 - $150,000 23.7 $350,001 - $550,000 3.2

$150,001 - $200,000 7.1 $550,001 - $1 million 1.5

More than $200,000 2.2 More than $1 million 3.7

Base: First Home Buyers n=115, * Percentage of all current Mortgagors n=0 ^ Percentage of all those intending to purchase n=115 # Percentage excluding don’t know /prefer not to say responses xx Significantly higher than other groups xx Significantly lower than other groups

32 2013 Mortgage Barometer Report

Current Investors profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 25.6 First home owner 0.0 In last 12 months 20.7

Mortgagor and intend to buy 73.5 Owner-occupier 0.0 2-3 years ago 37.4

No mortgage, intend to buy 1.9 Investor 28.3 4-5 years ago 14.7

Nett mortgagor 100 Investor & owner-occupier 71.7 More than 5 years ago 27.2

Nett intend to buy 74.4 Holiday house 0.6 When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 8.5 First Home Buyer N/A Existing house 57.1

In next 4-6 months 8.8 Subsequent home buyer N/A Existing unit 27.6

In next 7-12 months 20.1 Investor N/A Other existing property 23.3

In next 13-24 months 10.3 New house 29.9

In next 3-5 years 26.4 New unit 19.4

Other new development 18.6

Land 7.3

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 84.6 In the 2nd half of 2013…

I am better off owning a home than renting 69.4 Will rise by more than 0.5% 3.4

Property prices will increase strongly in the next three years 52.6 Will rise by up to 0.5% 28.0

The housing price 'bubble' will burst and prices will fall 29.4 Will stay the same 35.1

Worry I’ll never be able to afford my own home 18.9 Will drop by up to 0.5% 30.2

Property is undervalued 34.6 Will drop by more than 0.5% 3.4

Property is overvalued 37.7

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 10.9 Next 6 months 37.4

Property will become increasingly unaffordable in the next year 39.7 In 7-12 months’ time 31.5

13-18 months’ time 13.0

Avg. Mortgage

Avg. Loan-to-value rat io

Had/have <20% deposit

Loan with Big 4 bank

Use mortgage broker

Current mortgagors $382,000 54.9 12.9% 62.3% 45.8% Intend to buy in next 5 years $516,000 64.1 19.1% 62.2% 47.0% Gender % Age % Life Stage %

Male 55.0 18-24 years 4.2 SINKs 10.0

Female 45.0 25-34 years 28.0 DINKs 19.0

35-44 years 31.4 Family, primary aged kids 37.9

45-54 years 23.0 Family, high school aged kids 11.4

55-65 years 12.4 Adult family 9.6

Over 65 years 1.0 Older (55+) singles/couples 7.0

Retirees 3.8 State/Terr itory % Location % Marital Status %

NSW & ACT 34.1 Capital city 74.7 Single 12.8

VIC & TAS 27.8 Regional centre 20.6 Live with partner/married 80.8

QLD 17.4 Rural area 4.7 Separated/Divorced/Widowed 5.8

WA 11.5

SA & NT 9.2 Education % Household Income# % Investments# %

Primary 0.0 Sole income earner 23.7 No investments 2.2

Part of high school 6.2 Main income earner 29.2 $50,000 or less 6.8

Completed high school 16.0 $50,000 or less 7.2 $50,001 - $150,000 9.9

Diploma or certificate 29.5 $50,001 - $75,000 8.5 $150,001 - $250,000 19.4

Degree qualification 33.5 $75,001 - $100,000 27.7 $250,001 - $350,000 15.0

Postgraduate qualification 14.7 $100,001 - $150,000 35.3 $350,001 - $550,000 15.5

$150,001 - $200,000 14.6 $550,001 - $1 million 15.2

More than $200,000 6.8 More than $1 million 16.0

Base: Current Investors n=176 * Percentage of all current mortgagors n=176 ^ Percentage of all those intending to purchase n=131 # Percentage excluding don’t know /prefer not to say responses xx Significantly higher than other groups xx Significantly lower than other groups

33An annual study of the mortgage market in Australia

Potential Investors profile

Property Ownership % Mortgagor type^ % Mortgage recency^ %

Mortgagor, no intention 0.0 First home owner 19.1 In last 12 months 19.0

Mortgagor and intend to buy 79.7 Owner-occupier 37.2 2-3 years ago 33.7

No mortgage, intend to buy 20.3 Investor 12.9 4-5 years ago 18.4

Nett mortgagor 79.7 Investor & owner-occupier 30.8 More than 5 years ago 28.9

Nett intend to buy 100 Holiday house 0.8 When intend to buy* % Intender status* % Intended property type* %

Within next 3 months 8.5 First Home Buyer 7.8 Existing house 54.6

In next 4-6 months 9.8 Subsequent home buyer 8.9 Existing unit 31.3

In next 7-12 months 21.2 Investor 25.7 Other existing property 27.6

In next 13-24 months 19.9 New house 30.6

In next 3-5 years 40.6 New unit 23.7

Other new development 21.1

Land 4.3

Sentiment % Interest Rates# %

Future generations will find it harder to buy their first home 7.3 In the 2nd half of 2013…

I am better off owning a home than renting 12.6 Will rise by more than 0.5% 5.4

Property prices will increase strongly in the next three years 23.9 Will rise by up to 0.5% 25.5

The housing price 'bubble' will burst and prices will fall 38.6 Will stay the same 37.1

Worry I’ll never be able to afford my own home 59.2 Will drop by up to 0.5% 28.0

Property is undervalued 28.4 Will drop by more than 0.5% 4.0

Property is overvalued 45.2

Amongst intenders… % Best t ime to buy# %

Prices are high and I cannot afford what I want 17.4 Next 6 months 27.1

Property will become increasingly unaffordable in the next year 41.1 In 7-12 months’ time 27.0

13-18 months’ time 16.6

Avg. Mortgage

Avg. Loan-to-value rat io

Had/have <20% deposit

Loan with Big 4 bank

Use mortgage broker

Current mortgagors $337,000 55.61 12.3% 66.9% 41.6% Intend to buy in next 5 years $425,000 66.78 19.9% 69.7% 45.1% Gender % Age % Life Stage %

Male 55.9 18-24 years 8.1 SINKs 14.7

Female 44.1 25-34 years 28.2 DINKs 17.1

35-44 years 28.3 Family, primary aged kids 33.3

45-54 years 25.2 Family, high school aged kids 15.7

55-65 years 7.8 Adult family 11.2

Over 65 years 2.3 Older (55+) singles/couples 4.2

Retirees 3.4 State/Terr itory % Location % Marital Status %

NSW & ACT 35.0 Capital city 70.8 Single 19.1

VIC & TAS 29.8 Regional centre 25.4 Live with partner/married 76.1