Embed Size (px)

Citation preview

TRANSACTIONAL TRACK Estate Planning

2:45 p.m.- 3:45 p.m.

Presented byJanice KerkoveBradley & Riley

2007 First Ave. SECedar Rapids, IA 52406

Phone: 319-861-8763

2014 Nuts & Bolts SeminarCoralville

2014 Nuts & Bolts SeminarCoralville

THURSDAY, OCTOBER 30, 2014THURSDAY, OCTOBER 30, 2014

Copyright © 2014 Bradley & Riley PC - All rights reserved.

NUTS & BOLTS OFESTATE PLANNING

October 30, 2014 Janice J. Kerkove [email protected]

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 1

Copyright © 2014 Bradley & Riley PC - All rights reserved.

NUTS & BOLTS OFESTATE PLANNING

October 30, 2014 Janice J. Kerkove [email protected]

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

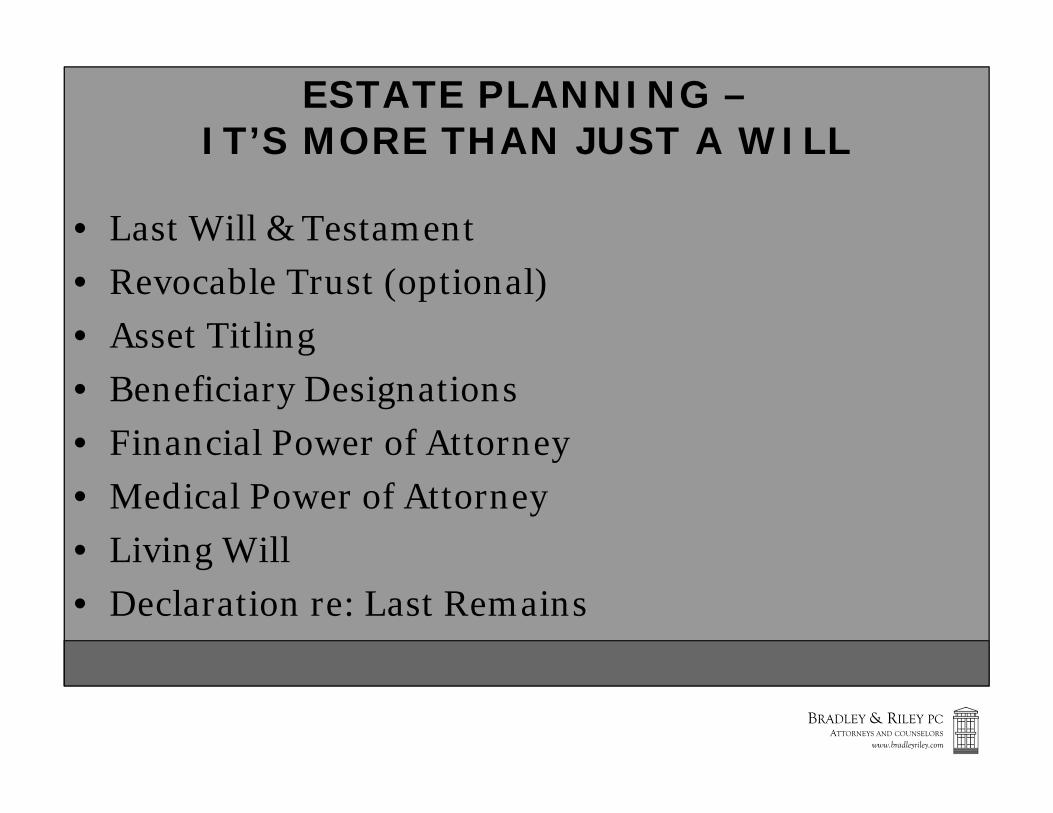

ESTATE PLANNING –IT’S MORE THAN JUST A WILL

• Last Will & Testament• Revocable Trust (optional)• Asset Titling• Beneficiary Designations• Financial Power of Attorney• Medical Power of Attorney• Living Will• Declaration re: Last Remains

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

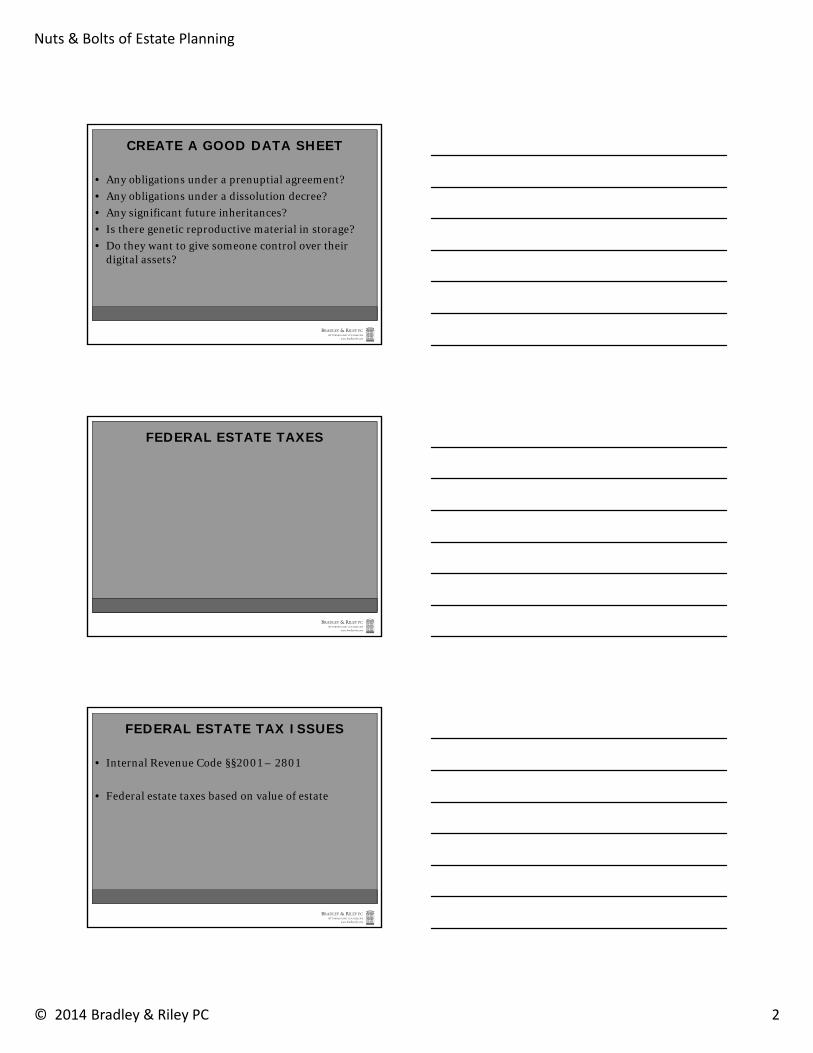

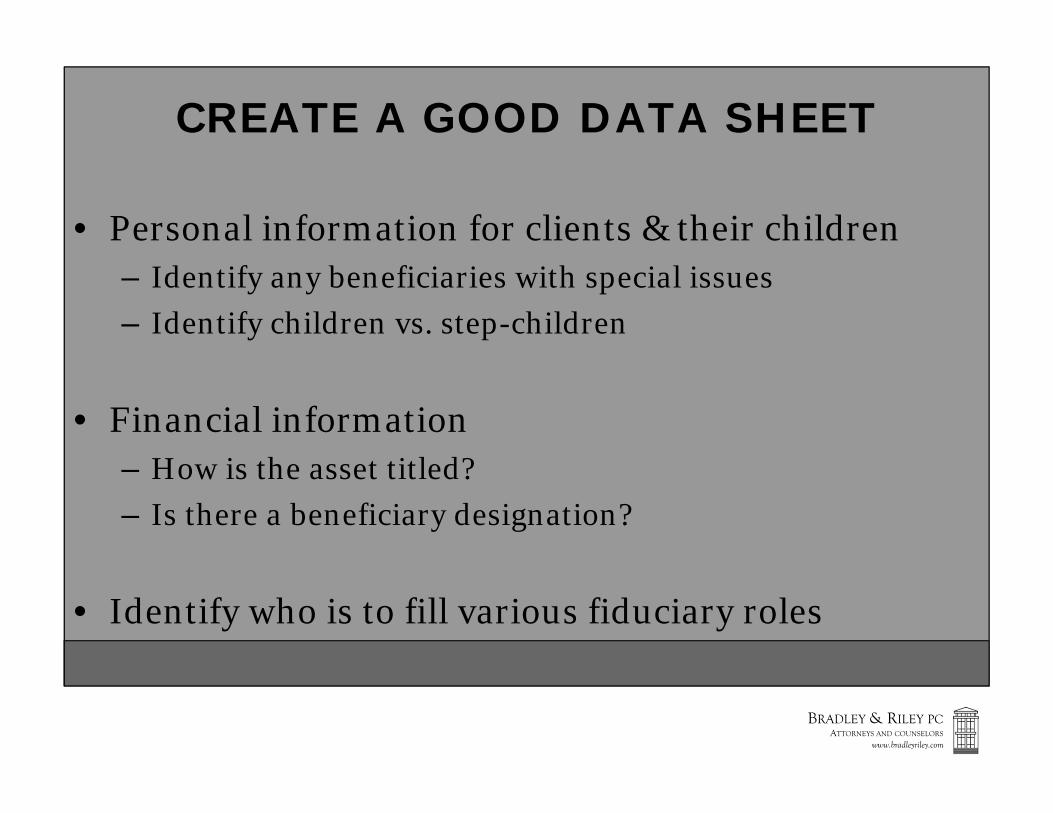

CREATE A GOOD DATA SHEET

• Personal information for clients & their children– Identify any beneficiaries with special issues– Identify children vs. step-children

• Financial information– How is the asset titled?– Is there a beneficiary designation?

• Identify who is to fill various fiduciary roles

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 2

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

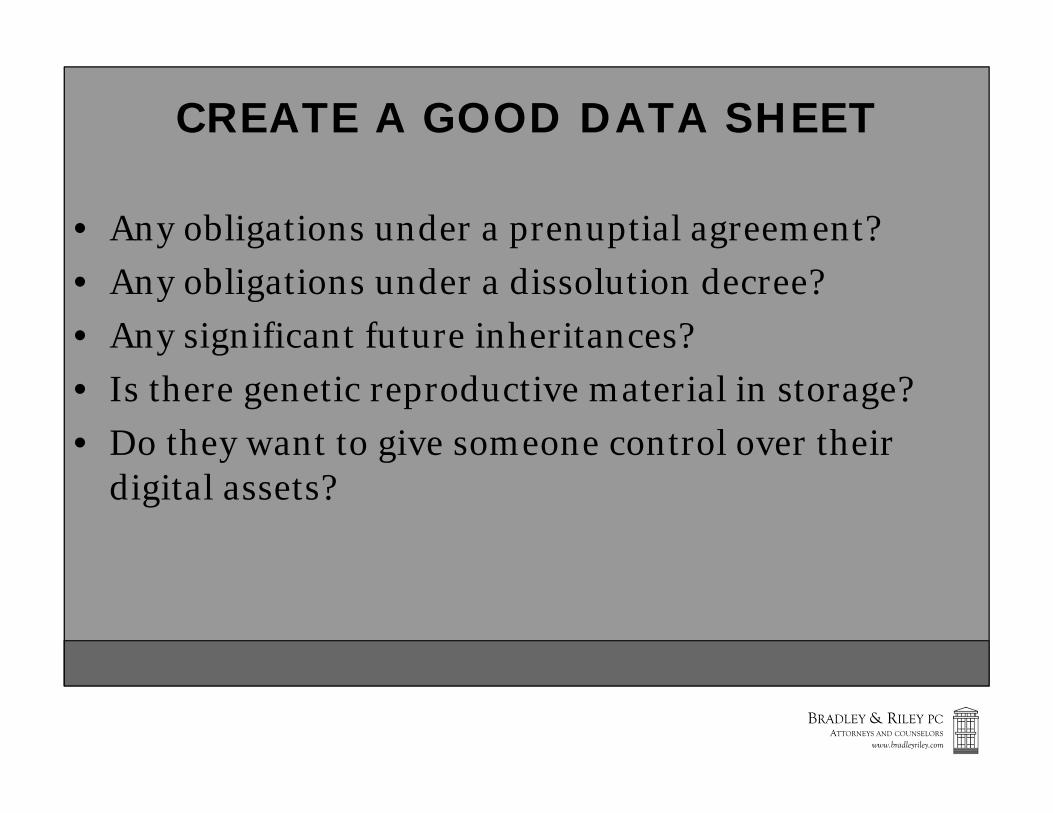

CREATE A GOOD DATA SHEET

• Any obligations under a prenuptial agreement?• Any obligations under a dissolution decree?• Any significant future inheritances? • Is there genetic reproductive material in storage?• Do they want to give someone control over their

digital assets?

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FEDERAL ESTATE TAXES

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FEDERAL ESTATE TAX ISSUES

• Internal Revenue Code §§2001 – 2801

• Federal estate taxes based on value of estate

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 3

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

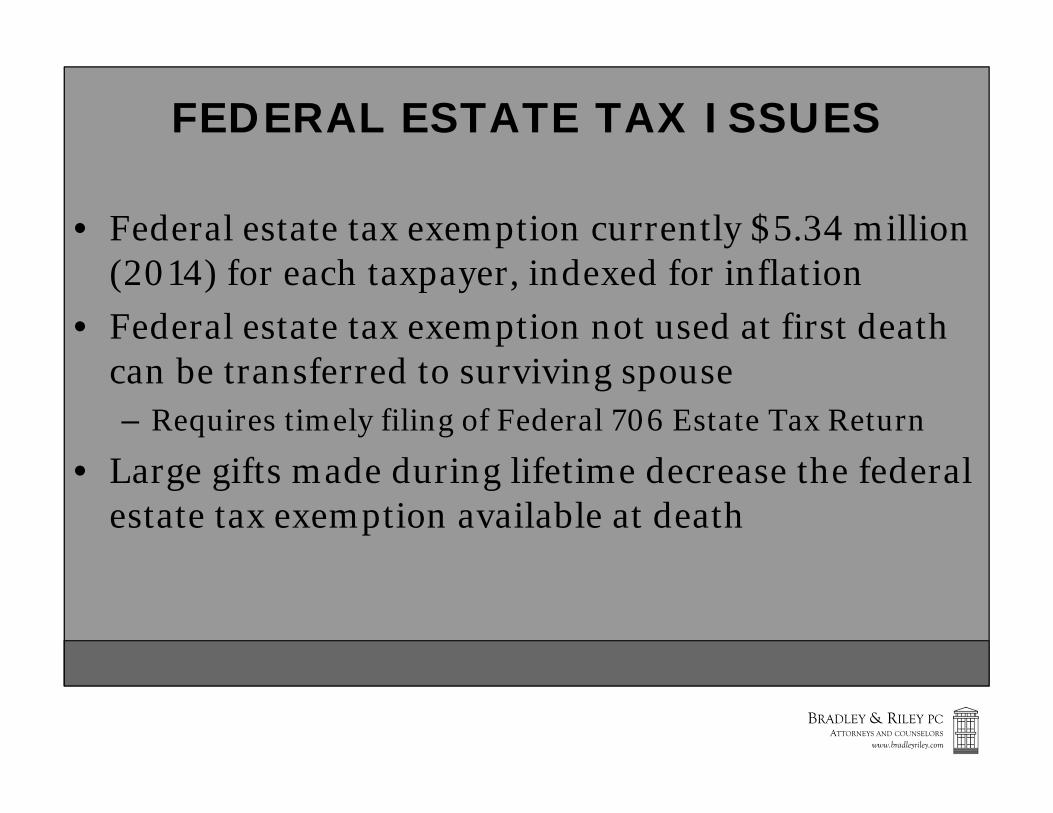

FEDERAL ESTATE TAX ISSUES

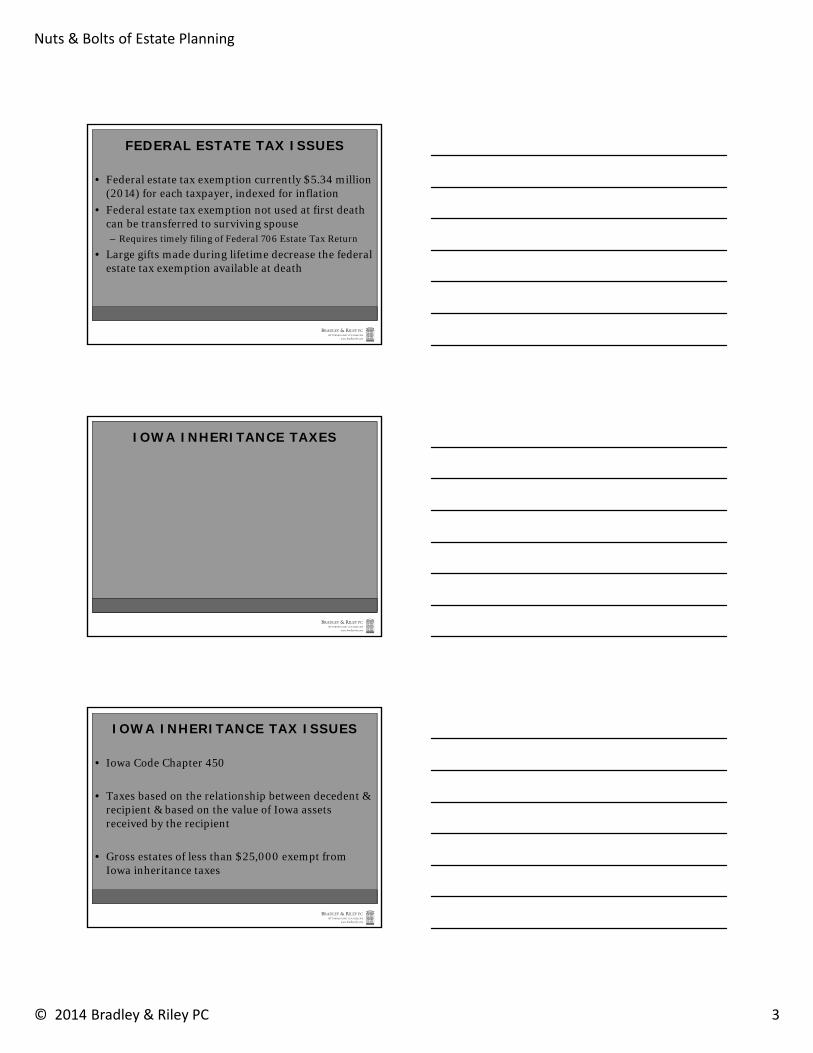

• Federal estate tax exemption currently $5.34 million (2014) for each taxpayer, indexed for inflation

• Federal estate tax exemption not used at first death can be transferred to surviving spouse– Requires timely filing of Federal 706 Estate Tax Return

• Large gifts made during lifetime decrease the federal estate tax exemption available at death

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA INHERITANCE TAXES

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA INHERITANCE TAX ISSUES

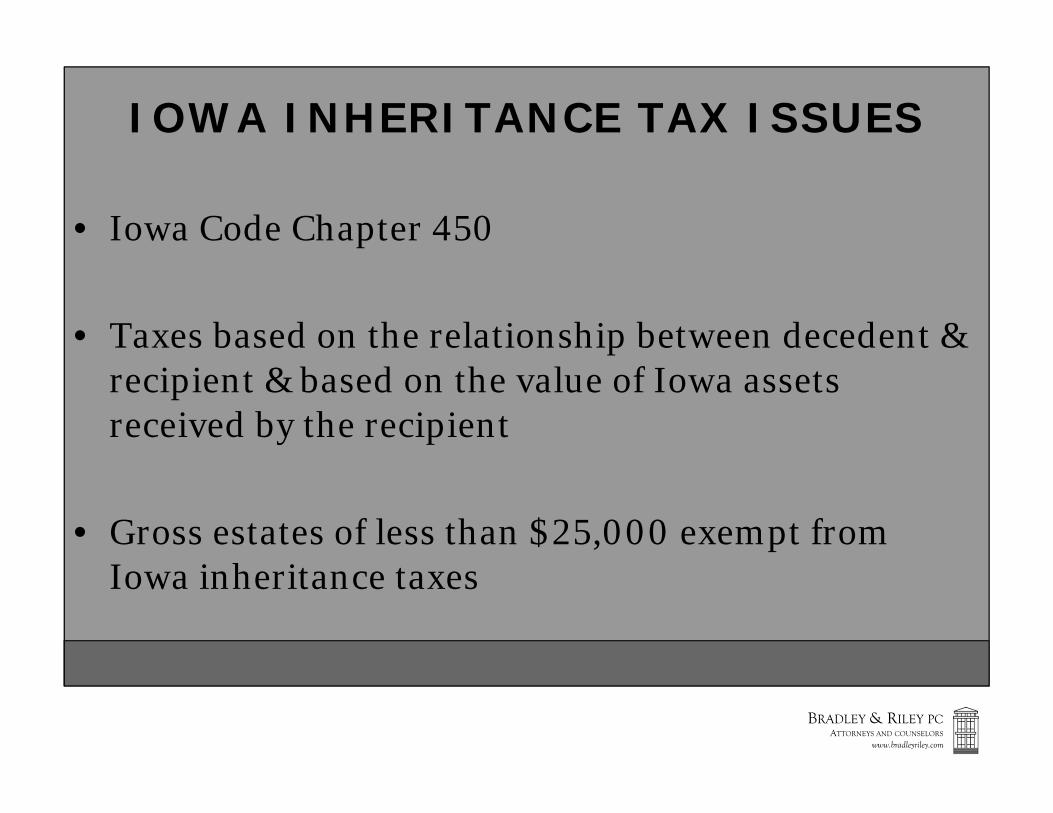

• Iowa Code Chapter 450

• Taxes based on the relationship between decedent & recipient & based on the value of Iowa assets received by the recipient

• Gross estates of less than $25,000 exempt from Iowa inheritance taxes

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 4

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA INHERITANCE TAX ISSUES

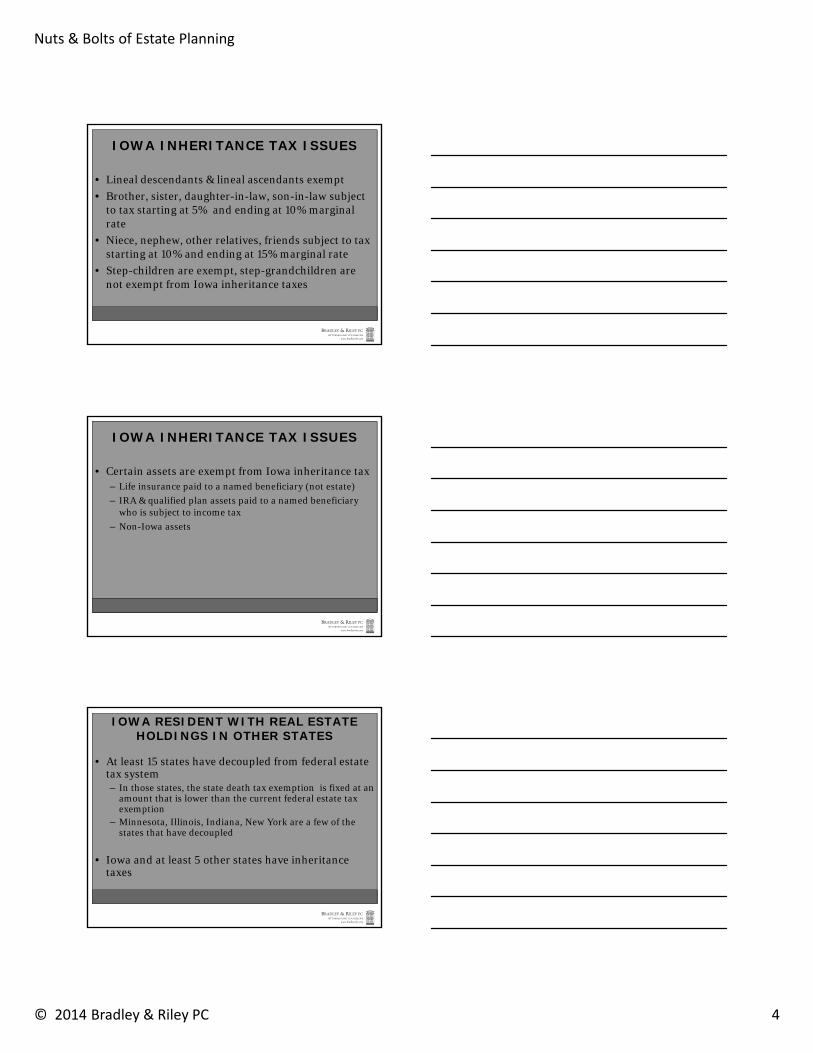

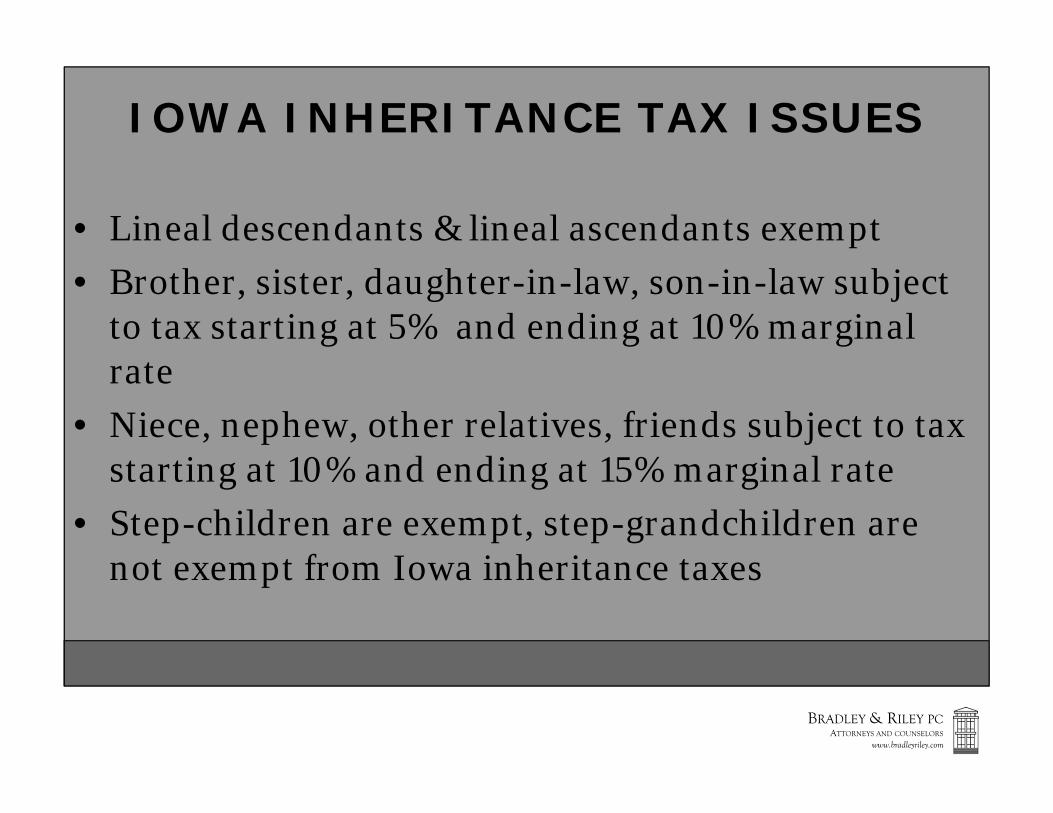

• Lineal descendants & lineal ascendants exempt• Brother, sister, daughter-in-law, son-in-law subject

to tax starting at 5% and ending at 10% marginal rate

• Niece, nephew, other relatives, friends subject to tax starting at 10% and ending at 15% marginal rate

• Step-children are exempt, step-grandchildren are not exempt from Iowa inheritance taxes

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA INHERITANCE TAX ISSUES

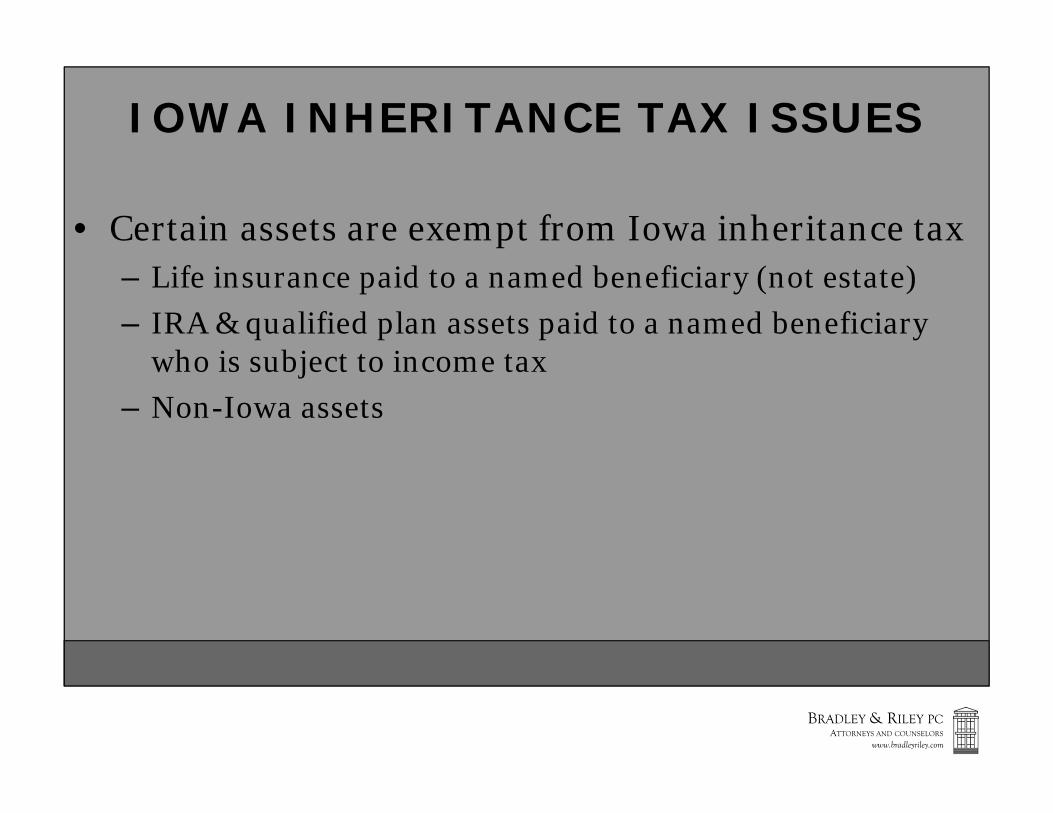

• Certain assets are exempt from Iowa inheritance tax– Life insurance paid to a named beneficiary (not estate)– IRA & qualified plan assets paid to a named beneficiary

who is subject to income tax – Non-Iowa assets

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA RESIDENT WITH REAL ESTATE HOLDINGS IN OTHER STATES

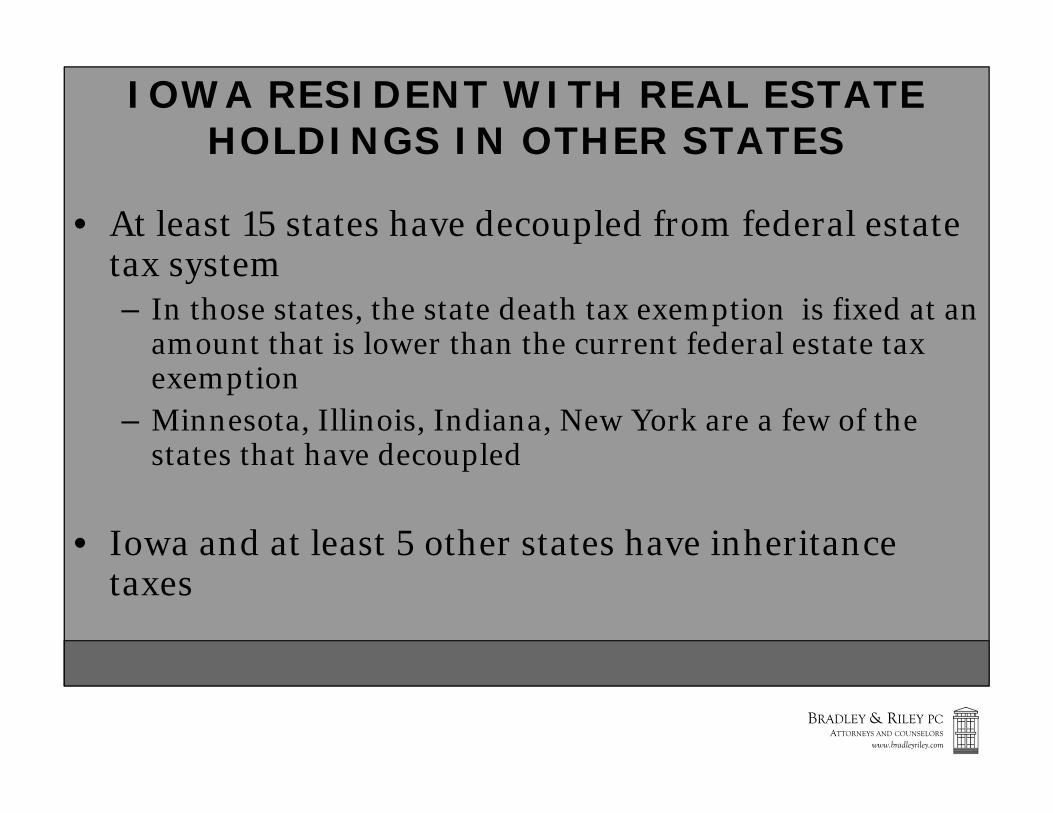

• At least 15 states have decoupled from federal estate tax system– In those states, the state death tax exemption is fixed at an

amount that is lower than the current federal estate tax exemption

– Minnesota, Illinois, Indiana, New York are a few of the states that have decoupled

• Iowa and at least 5 other states have inheritance taxes

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 5

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

WILLS VS. REVOCABLE TRUSTS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

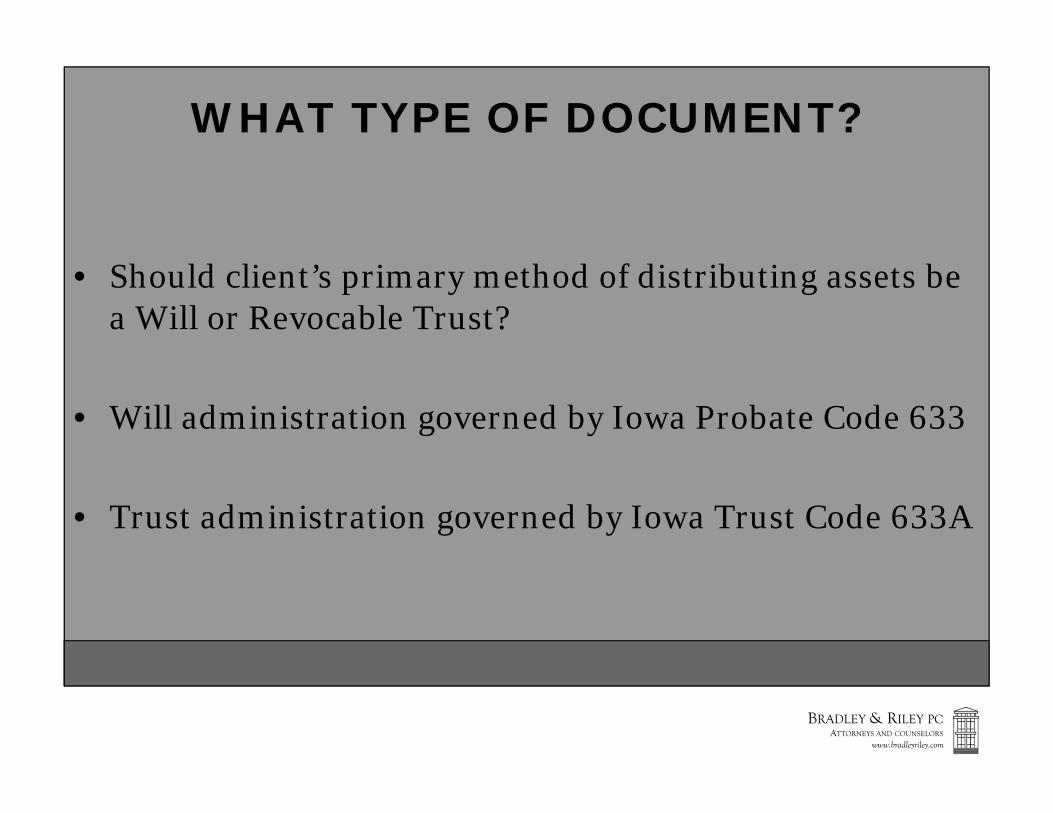

WHAT TYPE OF DOCUMENT?

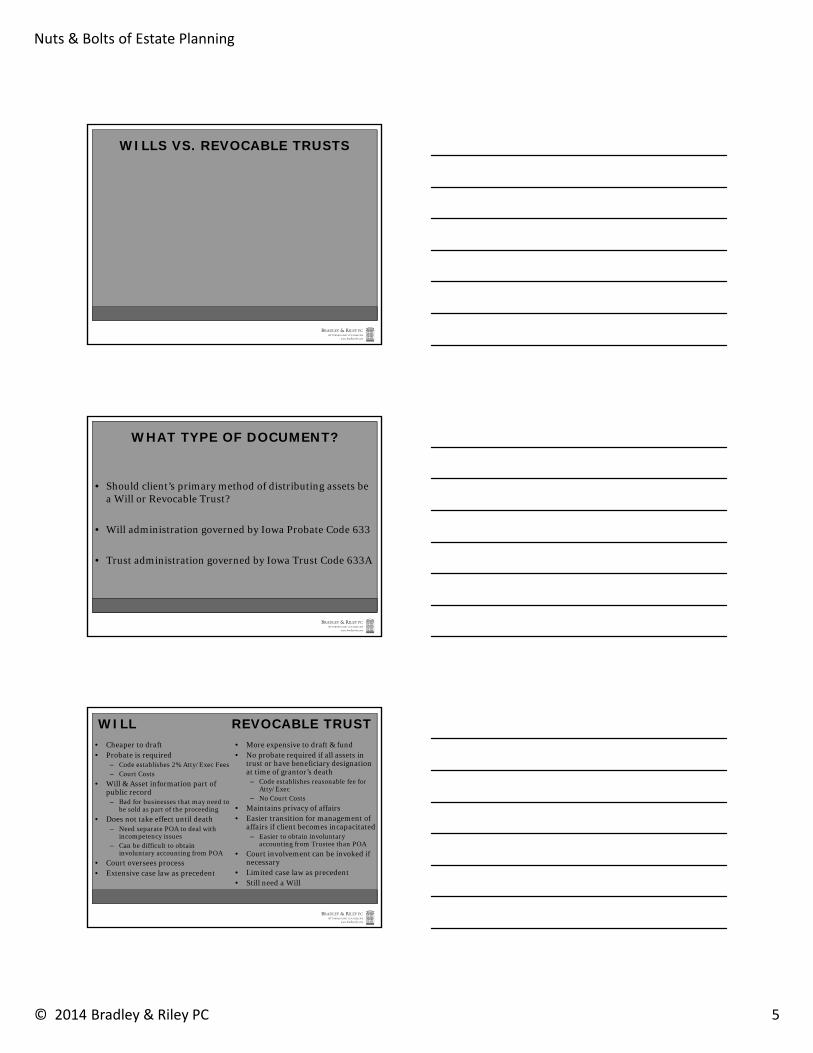

• Should client’s primary method of distributing assets be a Will or Revocable Trust?

• Will administration governed by Iowa Probate Code 633

• Trust administration governed by Iowa Trust Code 633A

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

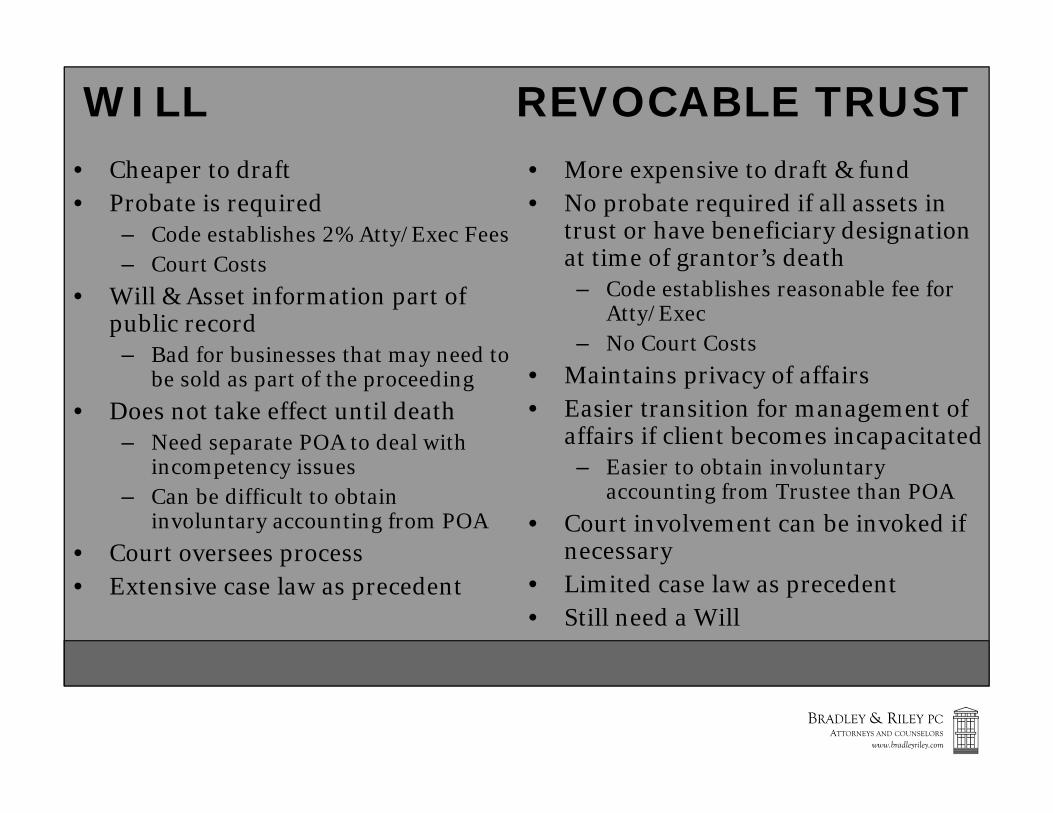

WILL REVOCABLE TRUST• Cheaper to draft• Probate is required

– Code establishes 2% Atty/Exec Fees– Court Costs

• Will & Asset information part of public record– Bad for businesses that may need to

be sold as part of the proceeding• Does not take effect until death

– Need separate POA to deal with incompetency issues

– Can be difficult to obtain involuntary accounting from POA

• Court oversees process• Extensive case law as precedent

• More expensive to draft & fund• No probate required if all assets in

trust or have beneficiary designation at time of grantor’s death– Code establishes reasonable fee for

Atty/Exec– No Court Costs

• Maintains privacy of affairs• Easier transition for management of

affairs if client becomes incapacitated– Easier to obtain involuntary

accounting from Trustee than POA• Court involvement can be invoked if

necessary• Limited case law as precedent• Still need a Will

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 6

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

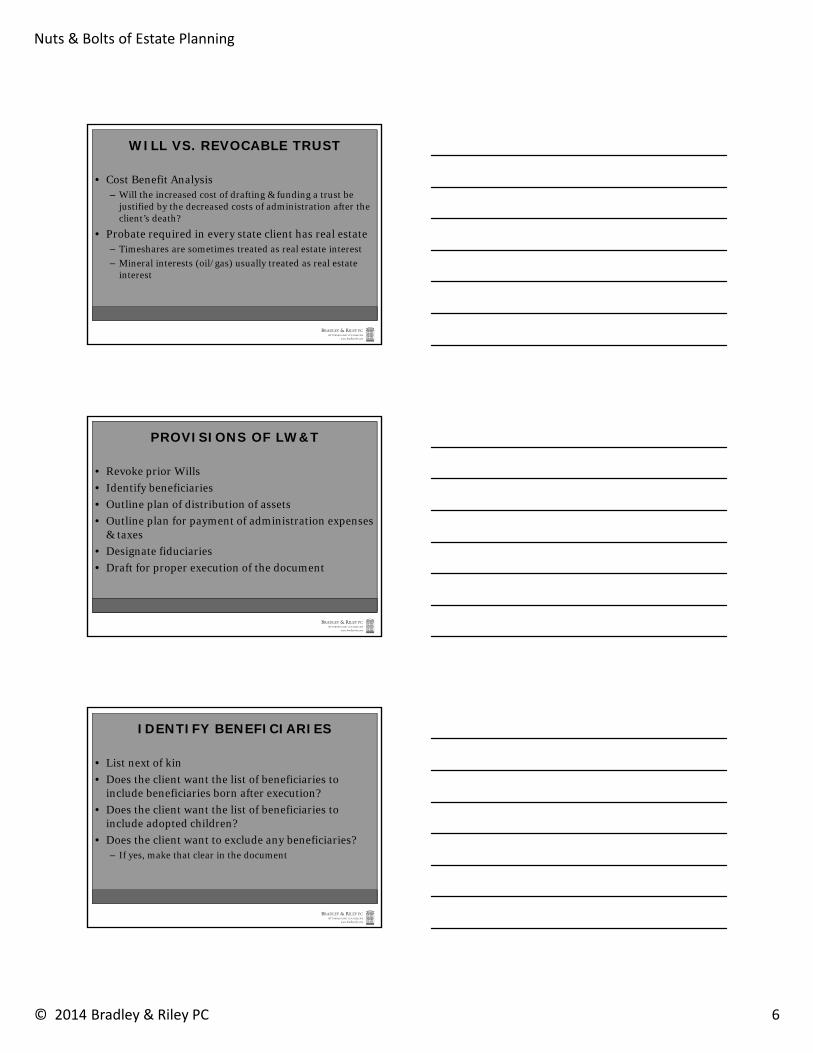

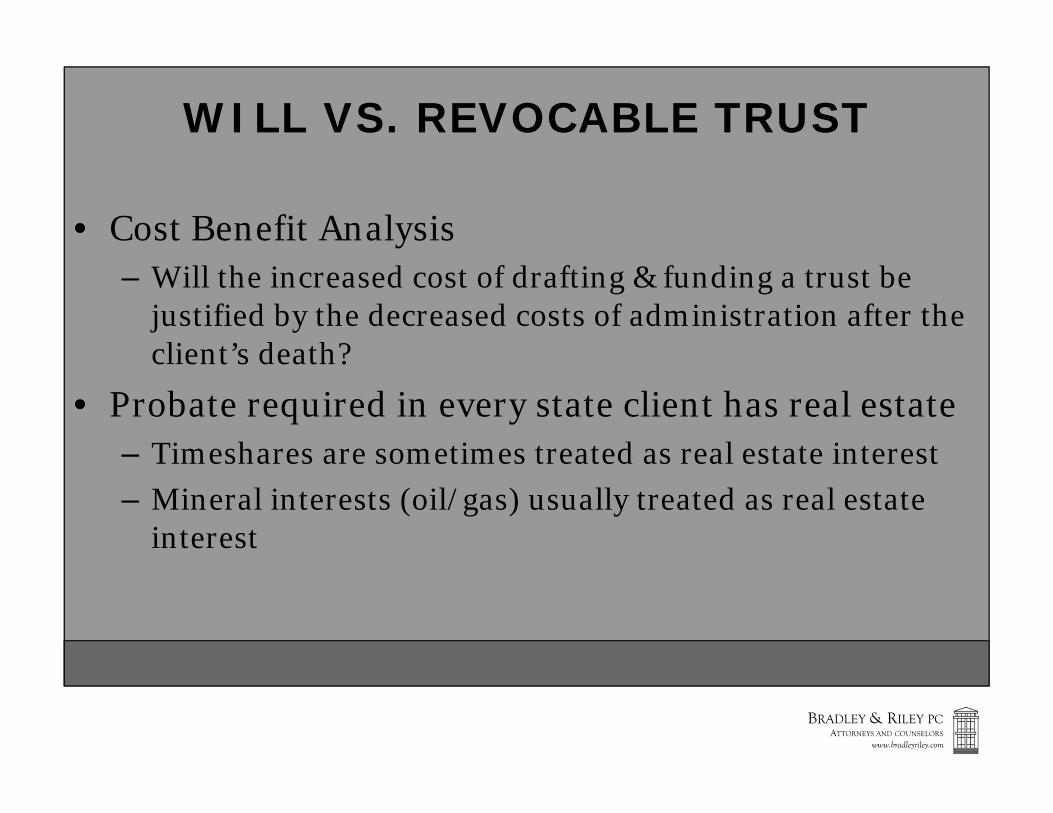

WILL VS. REVOCABLE TRUST

• Cost Benefit Analysis– Will the increased cost of drafting & funding a trust be

justified by the decreased costs of administration after the client’s death?

• Probate required in every state client has real estate– Timeshares are sometimes treated as real estate interest– Mineral interests (oil/gas) usually treated as real estate

interest

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

PROVISIONS OF LW&T

• Revoke prior Wills• Identify beneficiaries• Outline plan of distribution of assets• Outline plan for payment of administration expenses

& taxes• Designate fiduciaries • Draft for proper execution of the document

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IDENTIFY BENEFICIARIES

• List next of kin• Does the client want the list of beneficiaries to

include beneficiaries born after execution?• Does the client want the list of beneficiaries to

include adopted children?• Does the client want to exclude any beneficiaries?

– If yes, make that clear in the document

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 7

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

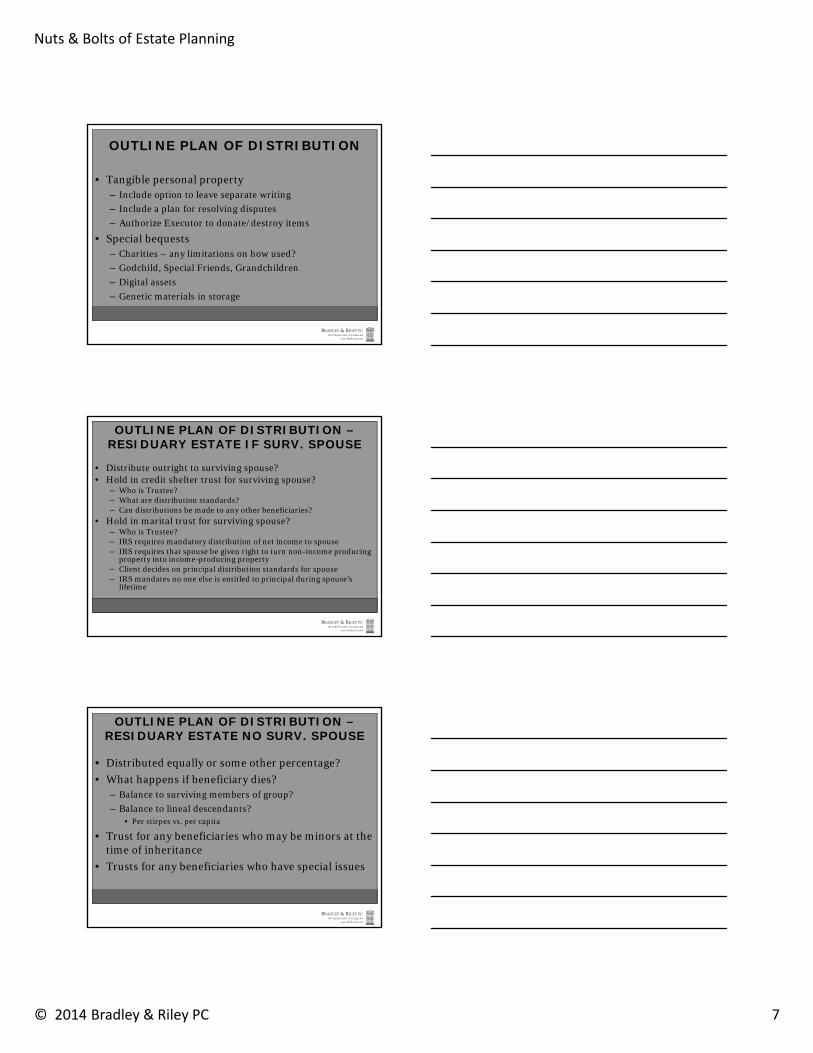

OUTLINE PLAN OF DISTRIBUTION

• Tangible personal property– Include option to leave separate writing– Include a plan for resolving disputes– Authorize Executor to donate/destroy items

• Special bequests– Charities – any limitations on how used?– Godchild, Special Friends, Grandchildren– Digital assets– Genetic materials in storage

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

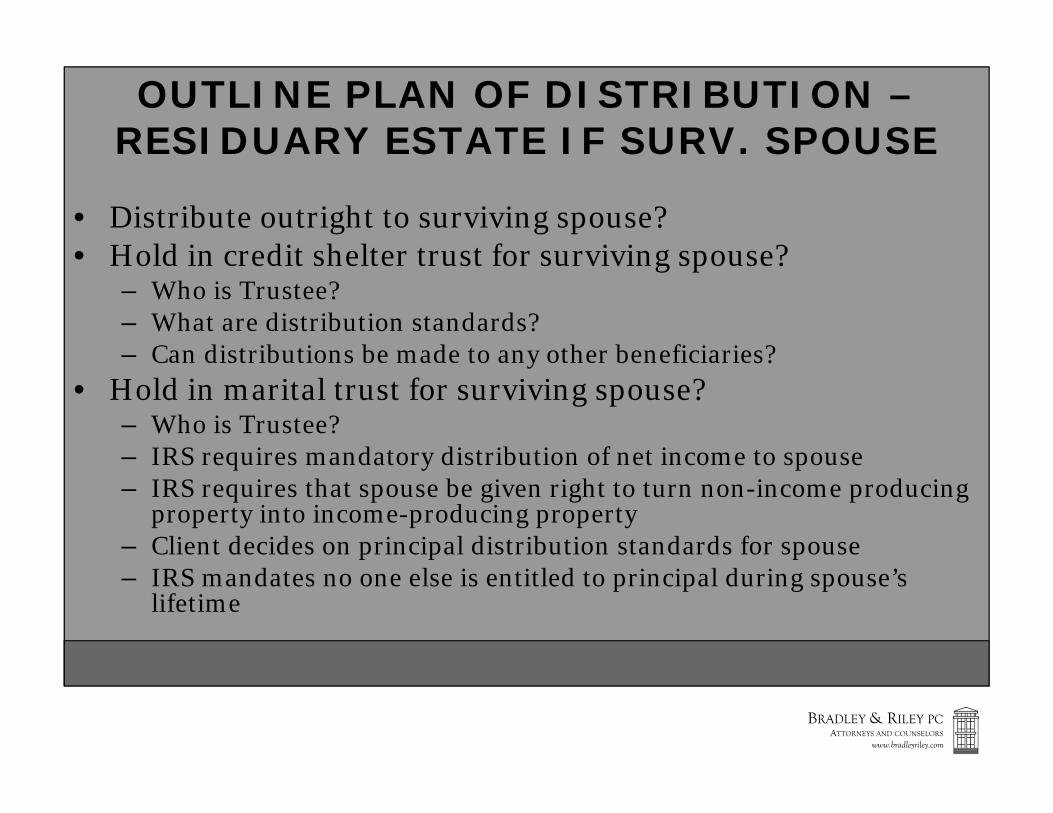

OUTLINE PLAN OF DISTRIBUTION –RESIDUARY ESTATE IF SURV. SPOUSE

• Distribute outright to surviving spouse?• Hold in credit shelter trust for surviving spouse?

– Who is Trustee?– What are distribution standards?– Can distributions be made to any other beneficiaries?

• Hold in marital trust for surviving spouse?– Who is Trustee?– IRS requires mandatory distribution of net income to spouse– IRS requires that spouse be given right to turn non-income producing

property into income-producing property– Client decides on principal distribution standards for spouse– IRS mandates no one else is entitled to principal during spouse’s

lifetime

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

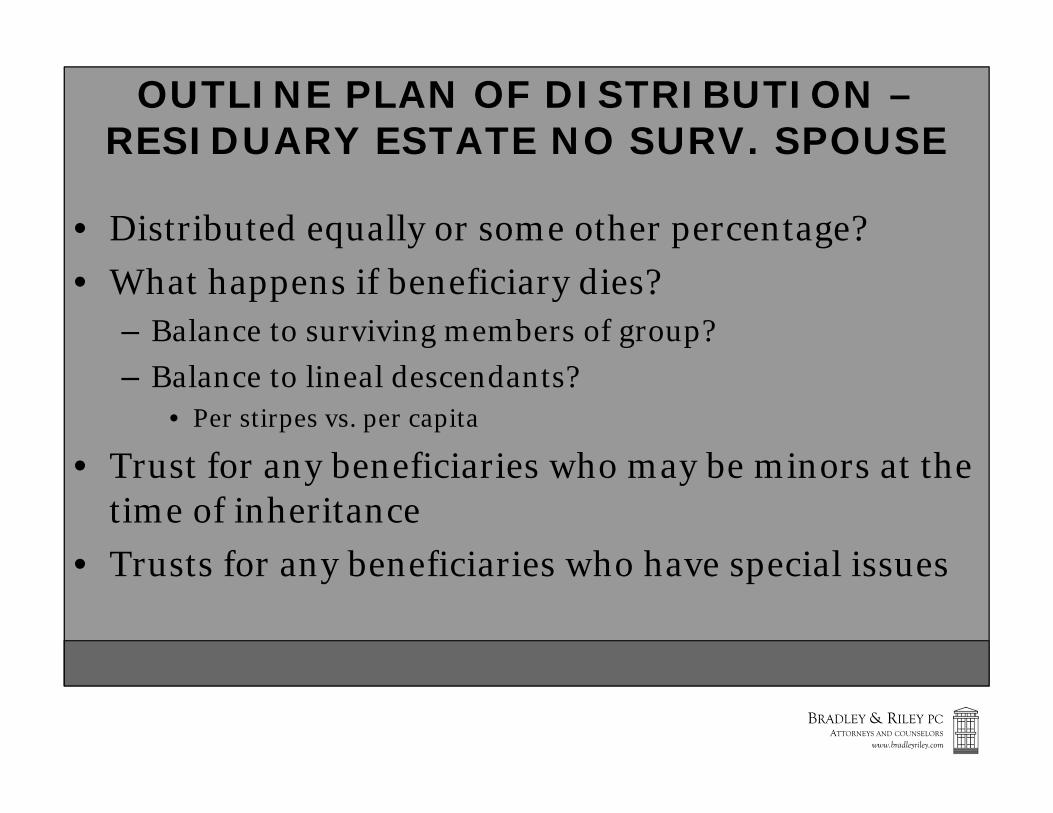

OUTLINE PLAN OF DISTRIBUTION –RESIDUARY ESTATE NO SURV. SPOUSE

• Distributed equally or some other percentage?• What happens if beneficiary dies?

– Balance to surviving members of group?– Balance to lineal descendants?

• Per stirpes vs. per capita

• Trust for any beneficiaries who may be minors at the time of inheritance

• Trusts for any beneficiaries who have special issues

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 8

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

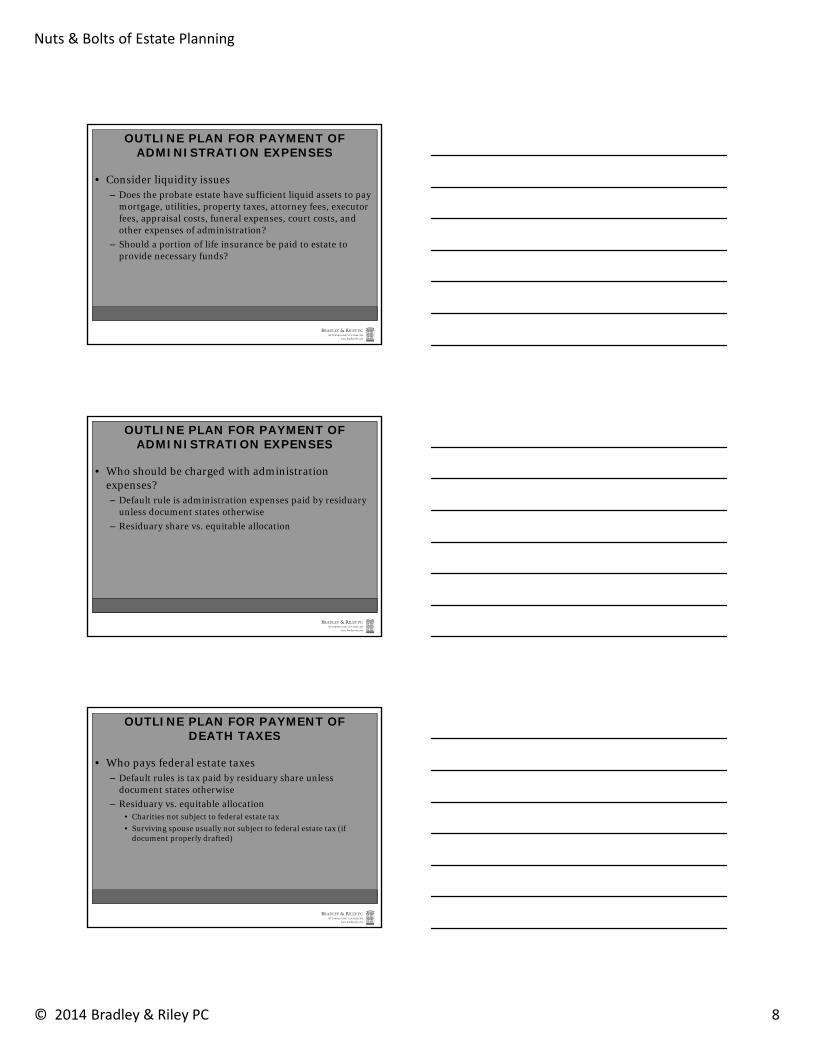

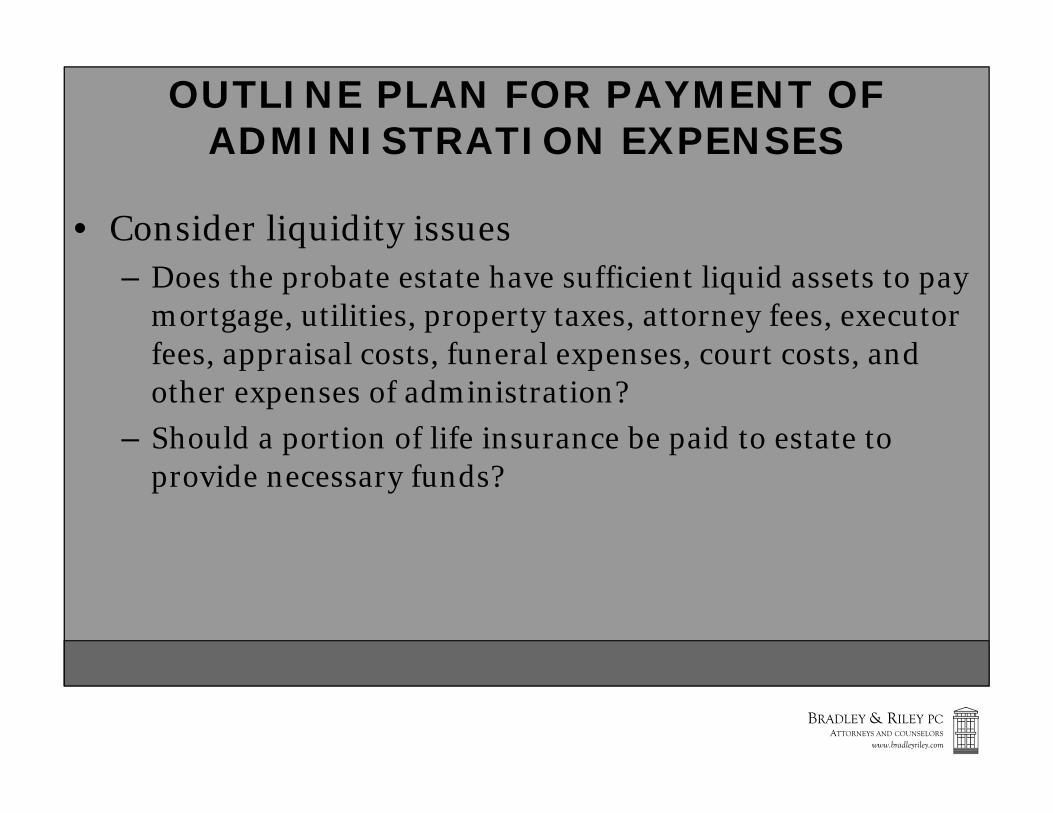

OUTLINE PLAN FOR PAYMENT OFADMINISTRATION EXPENSES

• Consider liquidity issues– Does the probate estate have sufficient liquid assets to pay

mortgage, utilities, property taxes, attorney fees, executor fees, appraisal costs, funeral expenses, court costs, and other expenses of administration?

– Should a portion of life insurance be paid to estate to provide necessary funds?

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

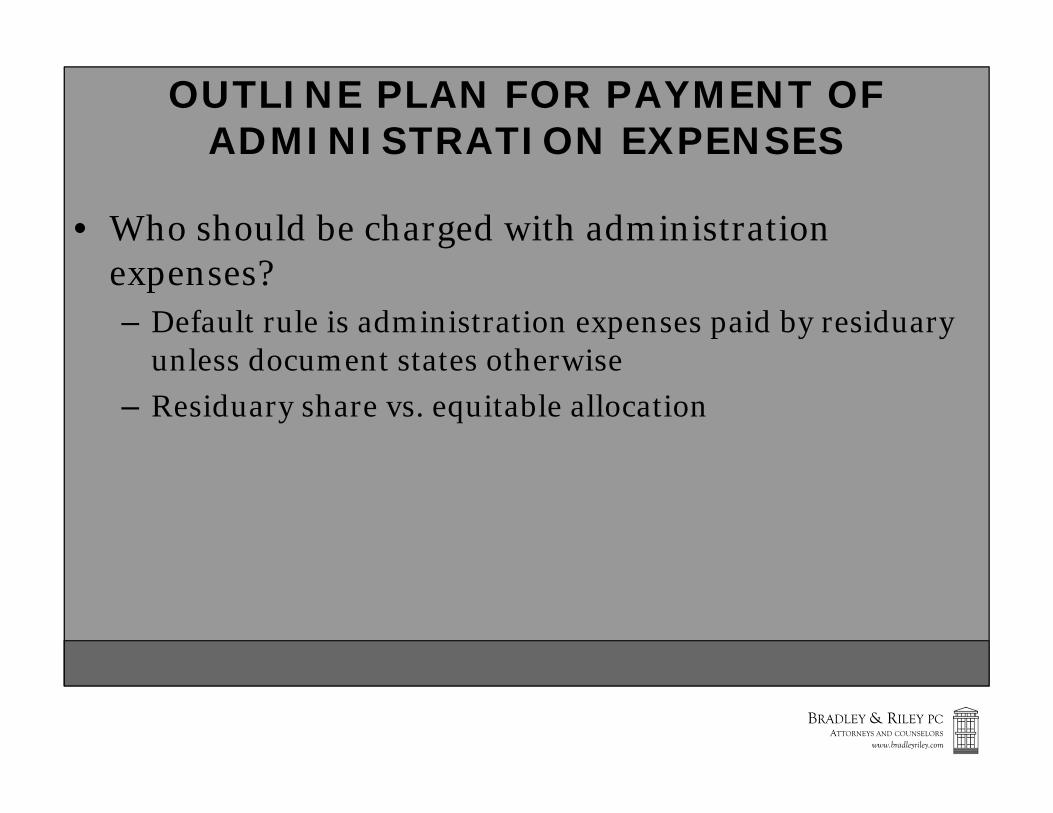

OUTLINE PLAN FOR PAYMENT OFADMINISTRATION EXPENSES

• Who should be charged with administration expenses?– Default rule is administration expenses paid by residuary

unless document states otherwise– Residuary share vs. equitable allocation

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

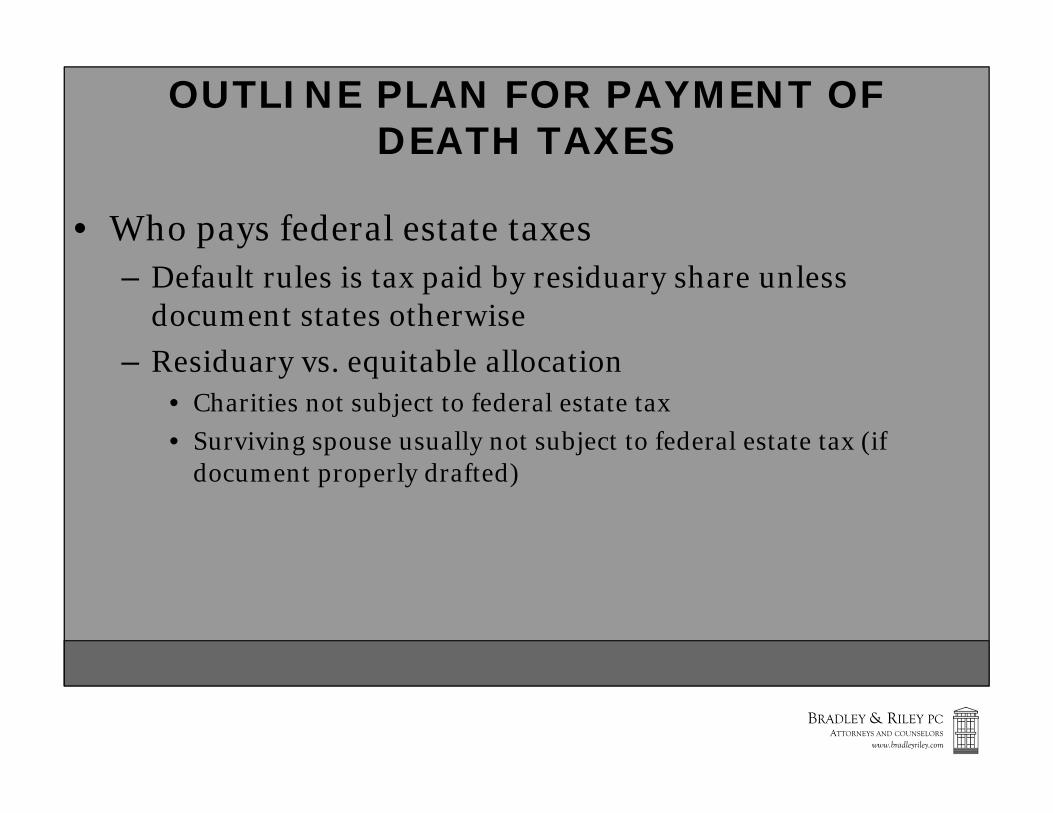

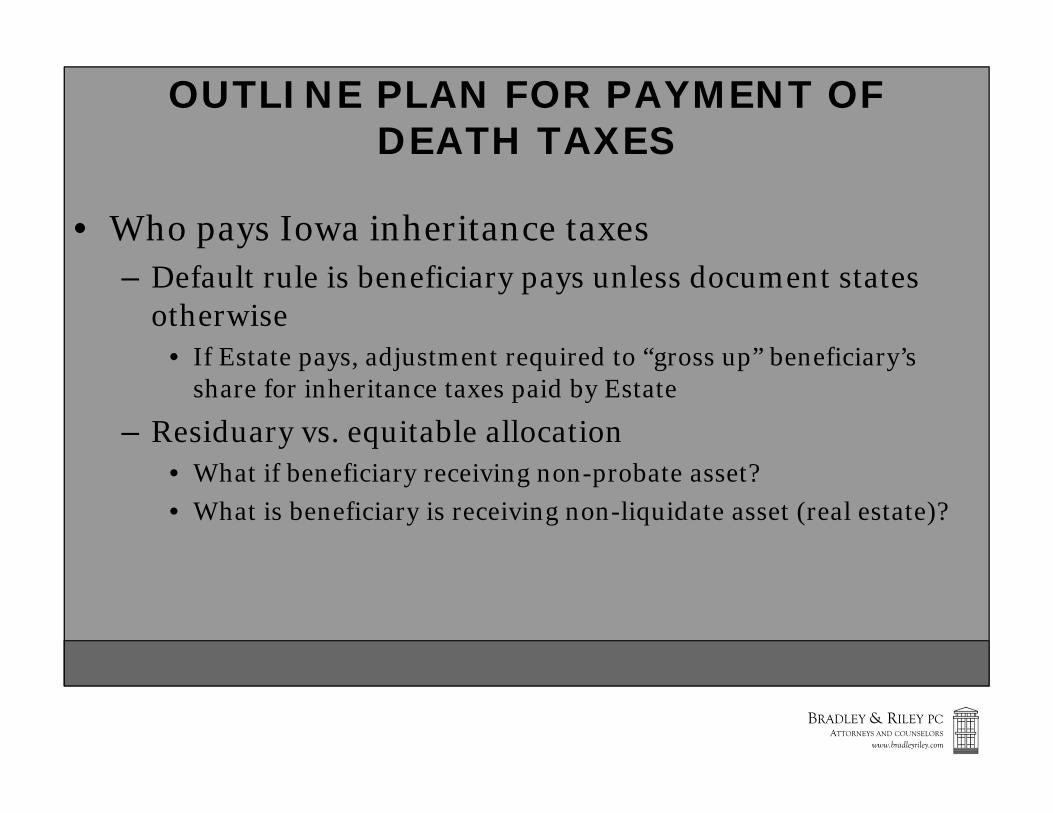

OUTLINE PLAN FOR PAYMENT OF DEATH TAXES

• Who pays federal estate taxes– Default rules is tax paid by residuary share unless

document states otherwise– Residuary vs. equitable allocation

• Charities not subject to federal estate tax• Surviving spouse usually not subject to federal estate tax (if

document properly drafted)

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 9

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

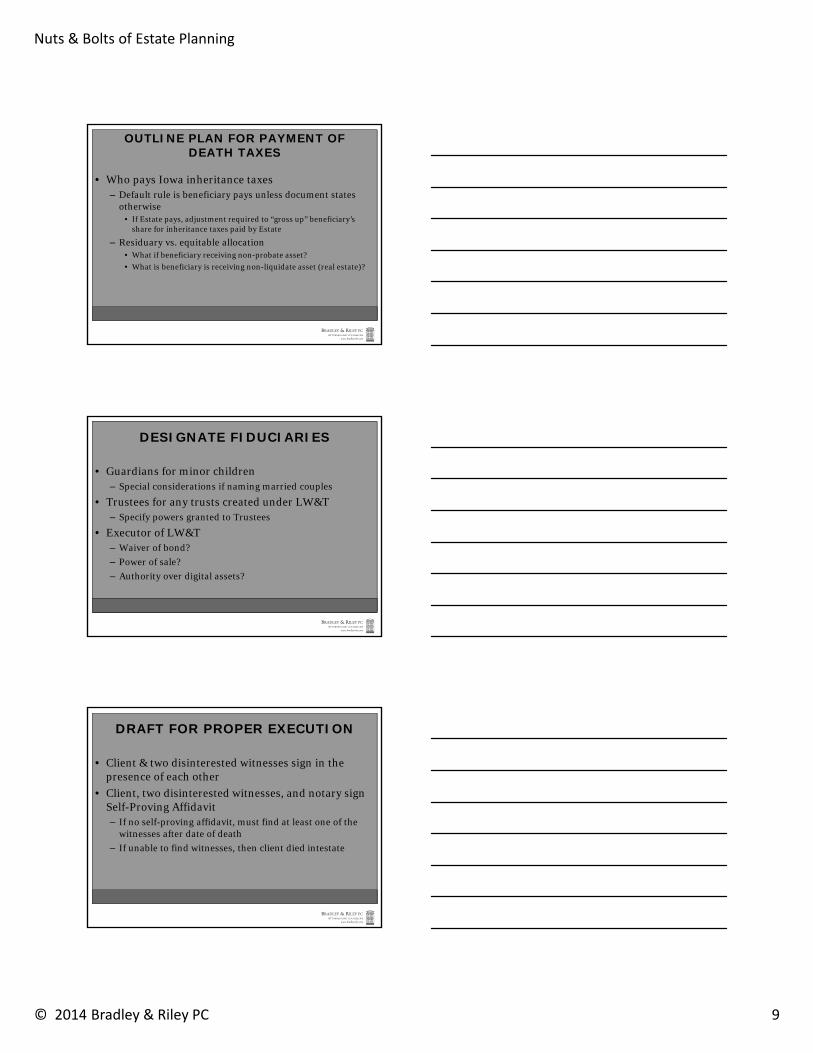

OUTLINE PLAN FOR PAYMENT OF DEATH TAXES

• Who pays Iowa inheritance taxes– Default rule is beneficiary pays unless document states

otherwise• If Estate pays, adjustment required to “gross up” beneficiary’s

share for inheritance taxes paid by Estate

– Residuary vs. equitable allocation • What if beneficiary receiving non-probate asset?• What is beneficiary is receiving non-liquidate asset (real estate)?

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

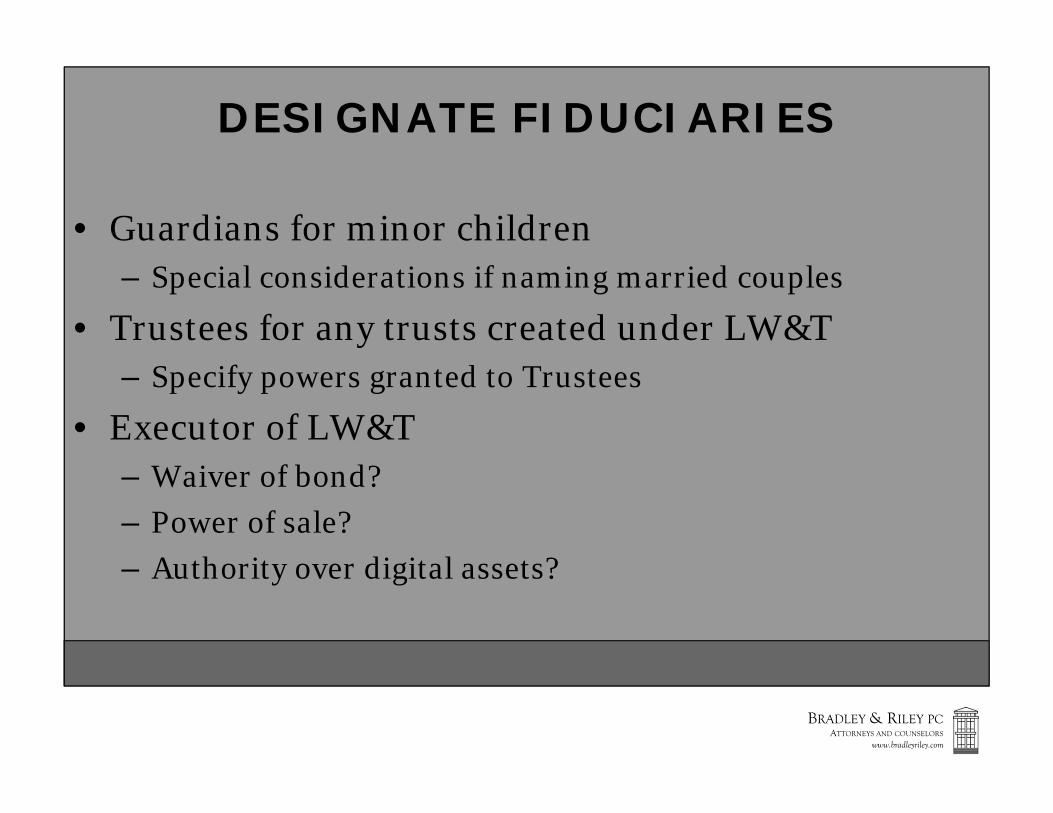

DESIGNATE FIDUCIARIES

• Guardians for minor children– Special considerations if naming married couples

• Trustees for any trusts created under LW&T– Specify powers granted to Trustees

• Executor of LW&T– Waiver of bond?– Power of sale?– Authority over digital assets?

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

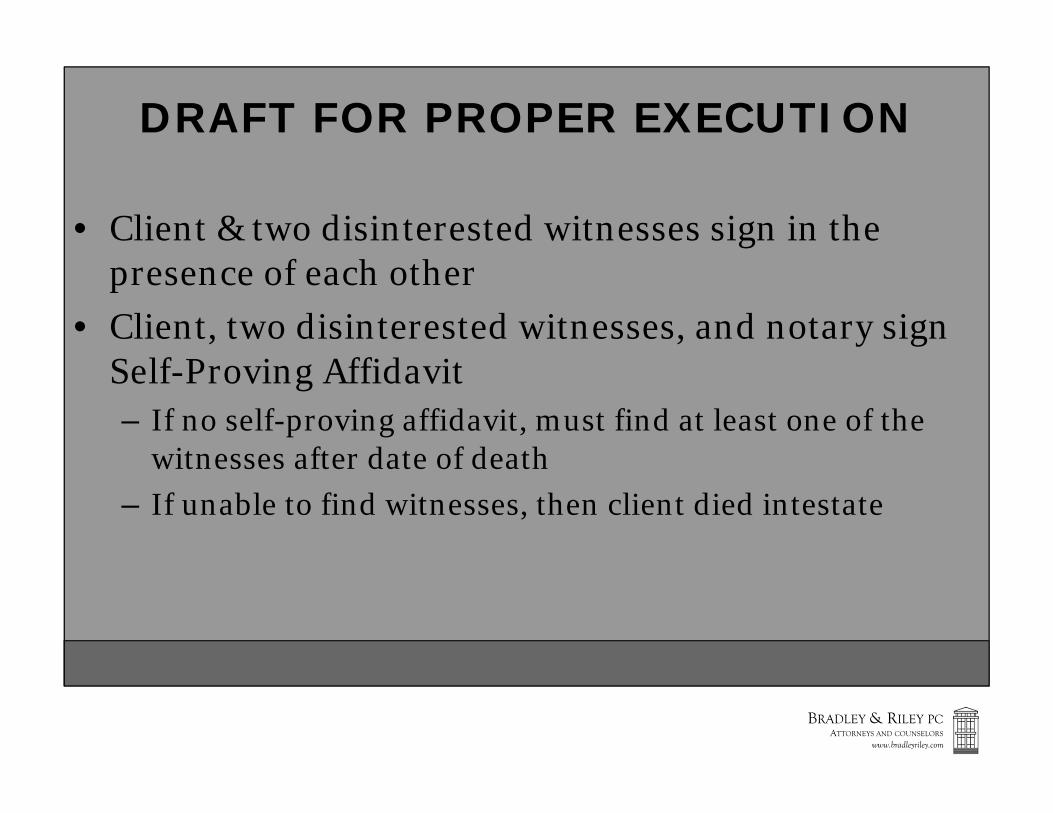

DRAFT FOR PROPER EXECUTION

• Client & two disinterested witnesses sign in the presence of each other

• Client, two disinterested witnesses, and notary sign Self-Proving Affidavit– If no self-proving affidavit, must find at least one of the

witnesses after date of death– If unable to find witnesses, then client died intestate

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 10

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

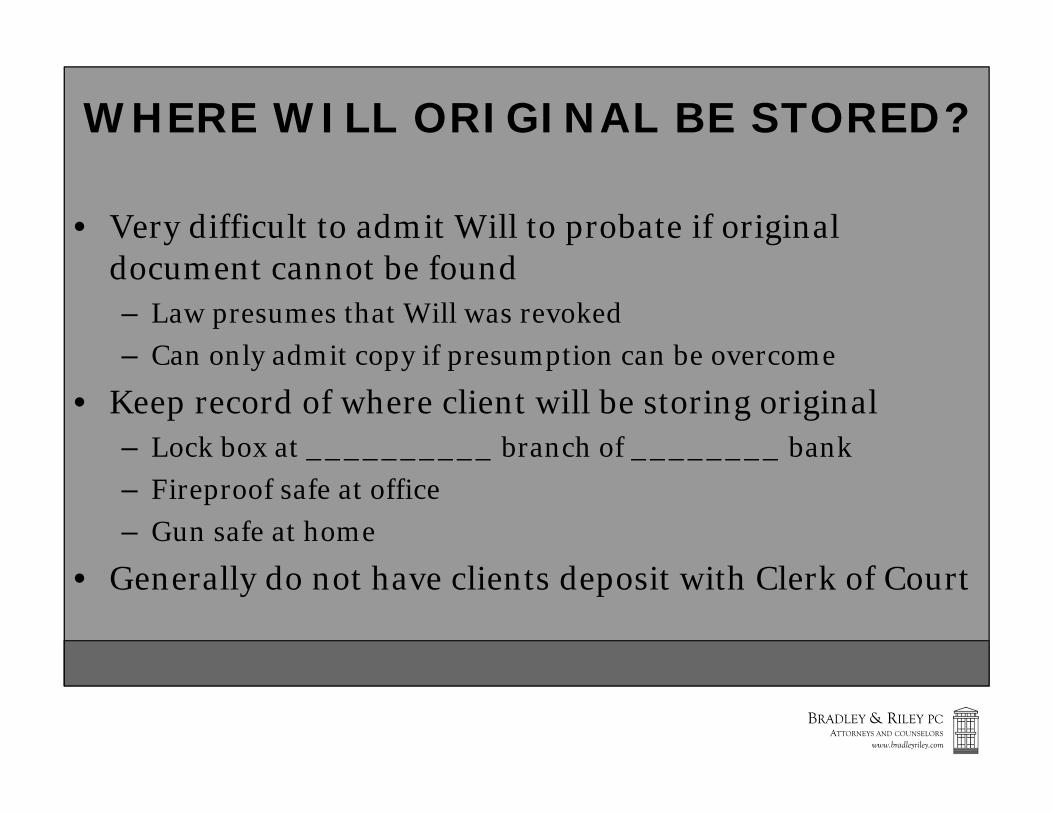

WHERE WILL ORIGINAL BE STORED?

• Very difficult to admit Will to probate if original document cannot be found– Law presumes that Will was revoked– Can only admit copy if presumption can be overcome

• Keep record of where client will be storing original– Lock box at __________ branch of ________ bank– Fireproof safe at office– Gun safe at home

• Generally do not have clients deposit with Clerk of Court

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

TITLING OF ASSETS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

TITLING ASSETS –JOINT TENANCY

• Joint tenancy with rights of survivorship vs. tenants in common ownership

• Joint tenancy ownership with rights of survivorship overrides terms of Will or Trust– Assets pass directly to the surviving joint tenant and are

never under the control of the Executor or Trustee

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 11

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

TITLING OF ASSETS –JOINT TENANCY

• If married couple has no federal estate tax concerns, assets can be held in joint tenancy to avoid probate at first spouse’s death

• If not a married couple or if there are federal estate tax concerns, joint tenancy ownership is not recommended

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

TITLING OF ASSETS –JOINT TENANCY WITH NON-SPOUSE

• Beware of titling assets jointly with non-spouses• Joint owner has immediate access to the joint

tenancy accounts – does not require client’s permission to withdraw funds

• Asset becomes subject to claims from their creditors, ex-spouse, etc.

• Asset automatically passes to surviving joint tenant -there is no legal obligation for joint tenant to share proceeds with other intended beneficiaries

• Can increase income tax liability when assets are sold in the future

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 12

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

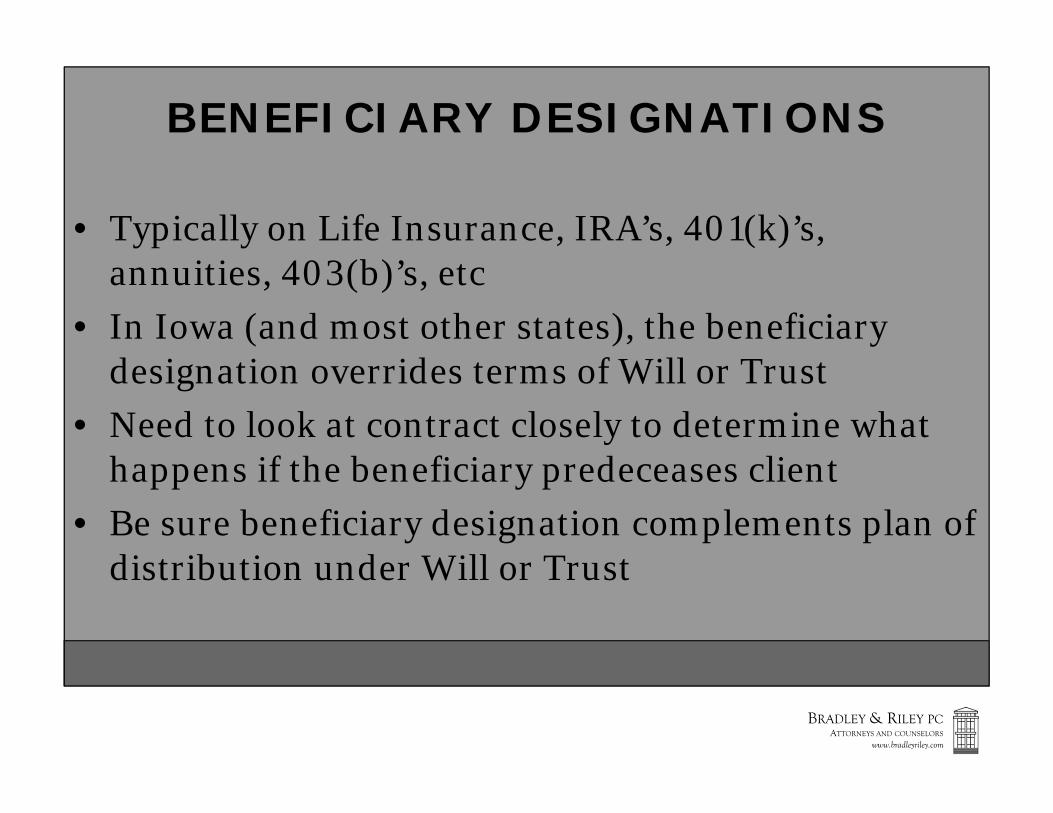

BENEFICIARY DESIGNATIONS

• Typically on Life Insurance, IRA’s, 401(k)’s, annuities, 403(b)’s, etc

• In Iowa (and most other states), the beneficiary designation overrides terms of Will or Trust

• Need to look at contract closely to determine what happens if the beneficiary predeceases client

• Be sure beneficiary designation complements plan of distribution under Will or Trust

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

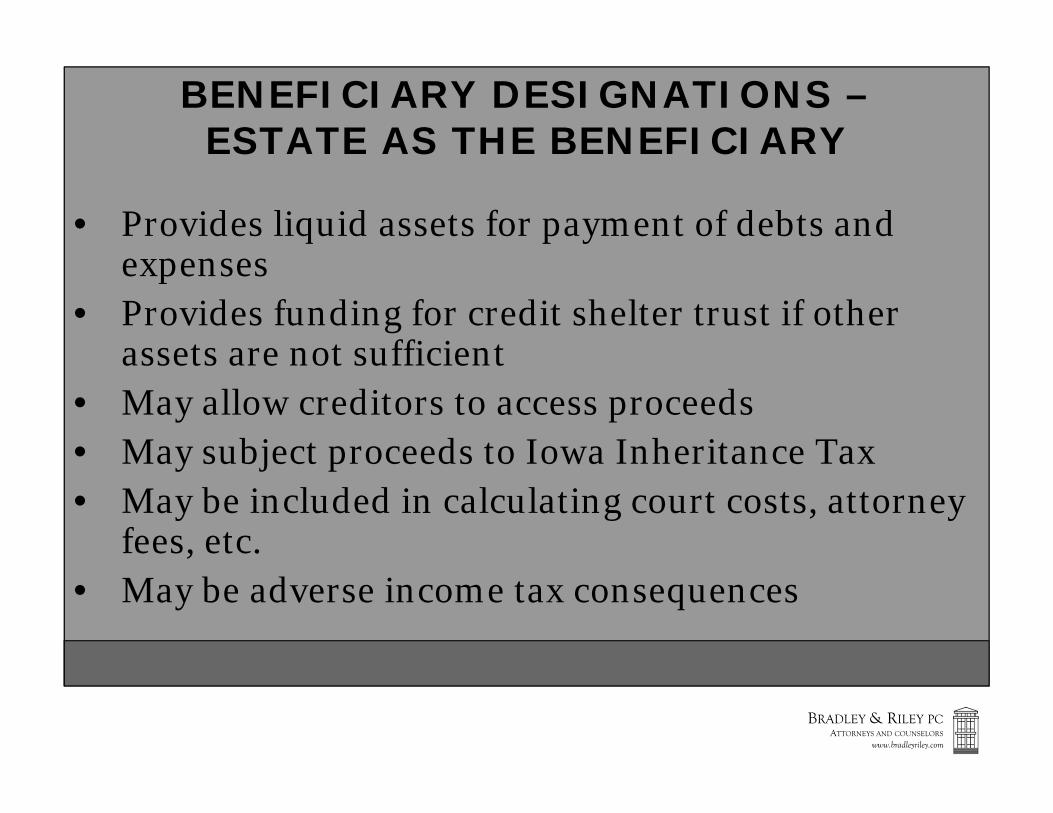

BENEFICIARY DESIGNATIONS –ESTATE AS THE BENEFICIARY

• Provides liquid assets for payment of debts and expenses

• Provides funding for credit shelter trust if other assets are not sufficient

• May allow creditors to access proceeds• May subject proceeds to Iowa Inheritance Tax• May be included in calculating court costs, attorney

fees, etc.• May be adverse income tax consequences

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

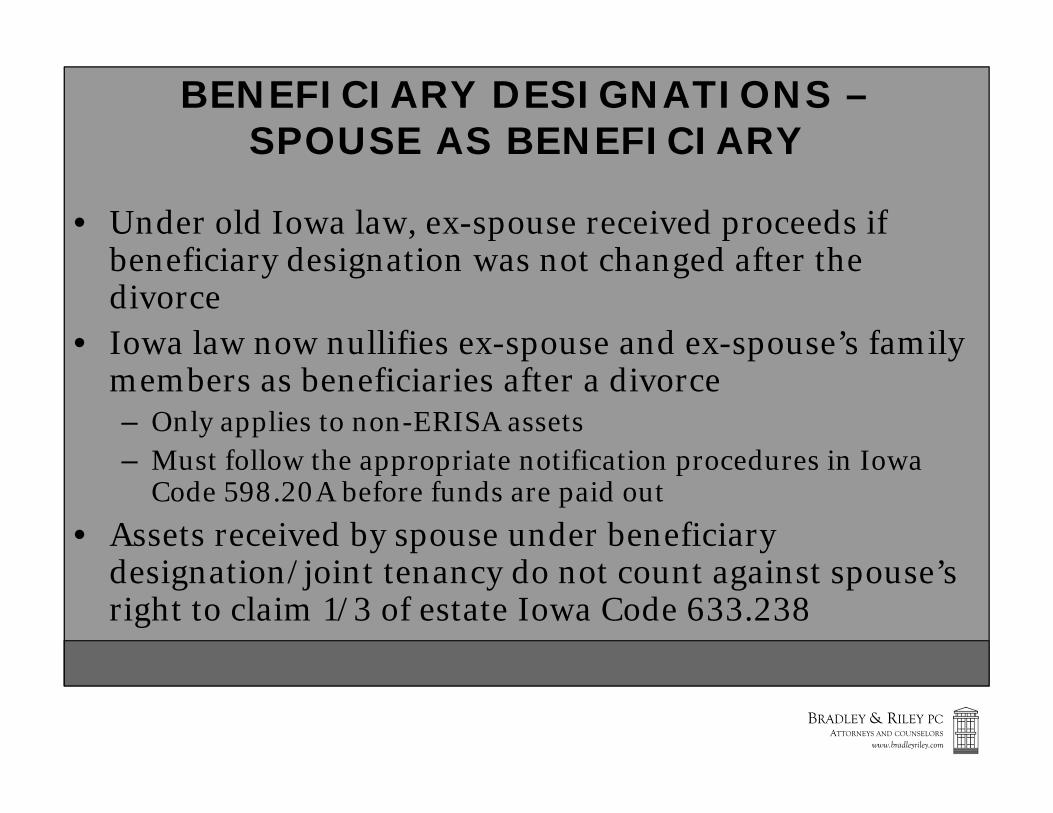

BENEFICIARY DESIGNATIONS –SPOUSE AS BENEFICIARY

• Under old Iowa law, ex-spouse received proceeds if beneficiary designation was not changed after the divorce

• Iowa law now nullifies ex-spouse and ex-spouse’s family members as beneficiaries after a divorce – Only applies to non-ERISA assets– Must follow the appropriate notification procedures in Iowa

Code 598.20A before funds are paid out• Assets received by spouse under beneficiary

designation/joint tenancy do not count against spouse’s right to claim 1/3 of estate Iowa Code 633.238

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 13

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –MULTIPLE CHILDREN AS BENE’S

• Important to determine what happens if a child predeceases the owner

• Default plan rules usually call for distribution to the surviving children

• Most clients prefer that lineal descendants of deceased child take which requires adding of “per stirpes” language to the designation

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –TAX DEFERRED ASSETS

• Beneficiary designations on IRA’s or qualified plans should be properly drafted to provide beneficiary with flexibility to obtain maximum deferral/stretch for income tax purposes

• If client has charitable bequests, consider making the charities the beneficiaries of tax-deferred accounts as the charities will not pay income tax

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –POD/TOD

• POD designations used on bank accounts• TOD designations used on brokerage accounts,

savings bonds or stock – Iowa Code Chapter 633D• Cannot be used in Iowa for real estate holdings• Designates beneficiary who is to receive asset upon

death of owner - designation is revocable• Beneficiary has no rights to asset until client’s death

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 14

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –POD/TOD

• Asset passes to designee outside of probate• Beneficiary has no obligation to share with other

intended beneficiaries• Beneficiary may not be required to use funds for

funeral, burial, taxes, or other administration expenses

• If most assets pass by joint tenancy ownership or beneficiary designation, then no assets available for personal representative to pay administration expenses, including carrying costs of real estate, etc.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

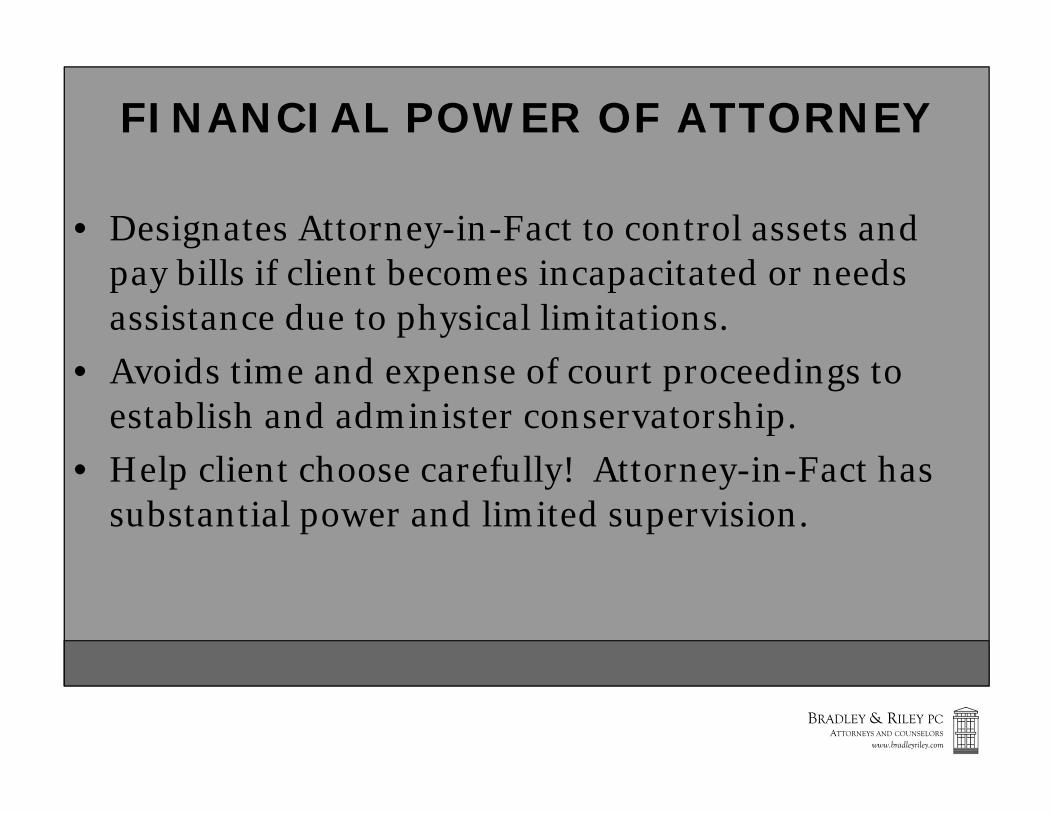

FINANCIAL POWER OF ATTORNEY

• Designates Attorney-in-Fact to control assets and pay bills if client becomes incapacitated or needs assistance due to physical limitations.

• Avoids time and expense of court proceedings to establish and administer conservatorship.

• Help client choose carefully! Attorney-in-Fact has substantial power and limited supervision.

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 15

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

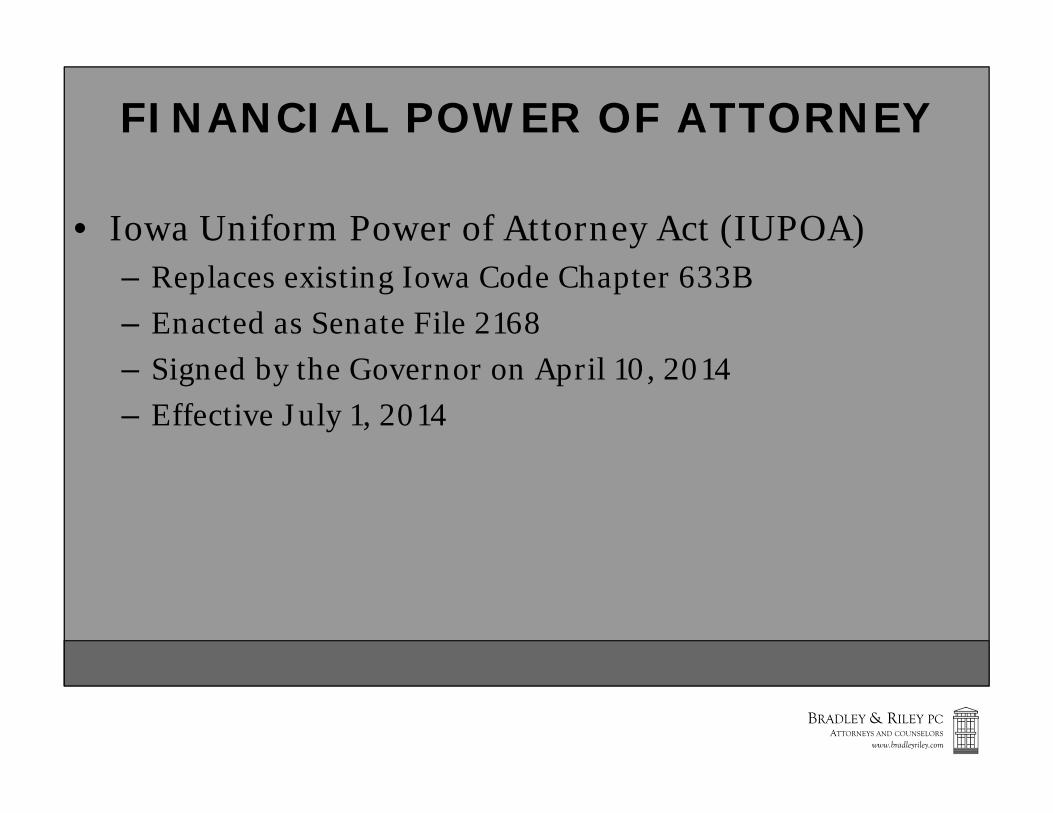

FINANCIAL POWER OF ATTORNEY

• Iowa Uniform Power of Attorney Act (IUPOA)– Replaces existing Iowa Code Chapter 633B– Enacted as Senate File 2168– Signed by the Governor on April 10, 2014– Effective July 1, 2014

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

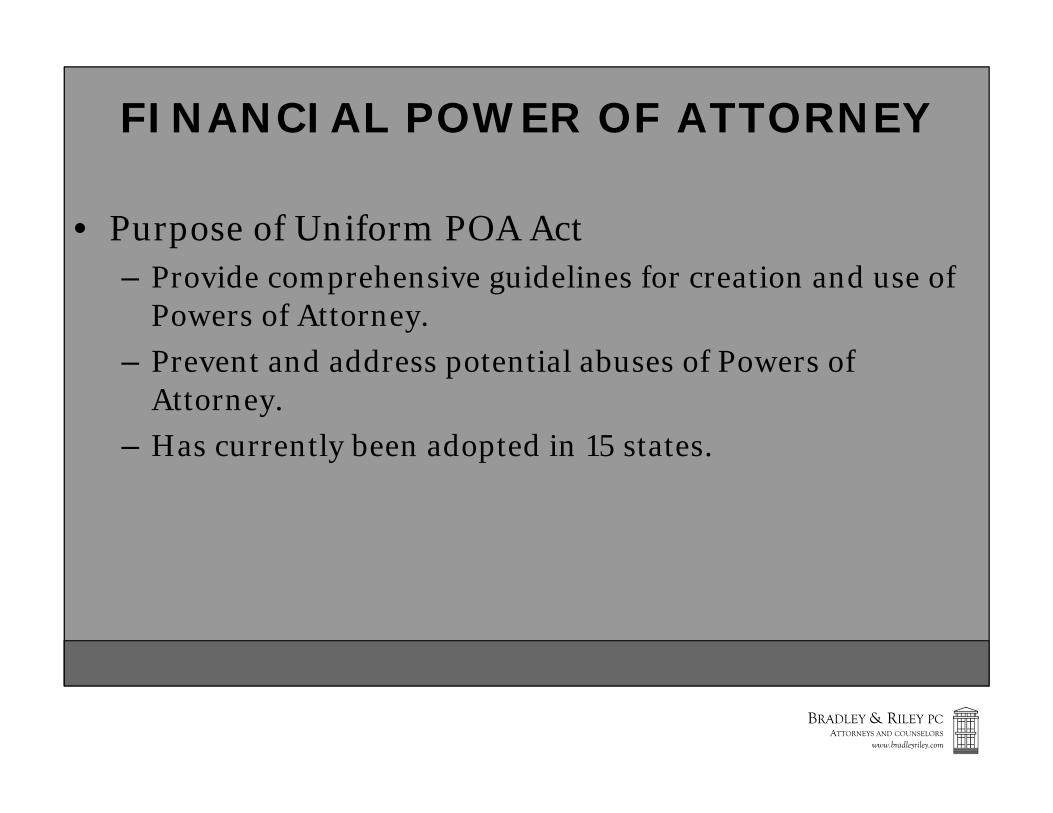

FINANCIAL POWER OF ATTORNEY

• Purpose of Uniform POA Act– Provide comprehensive guidelines for creation and use of

Powers of Attorney.– Prevent and address potential abuses of Powers of

Attorney.– Has currently been adopted in 15 states.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

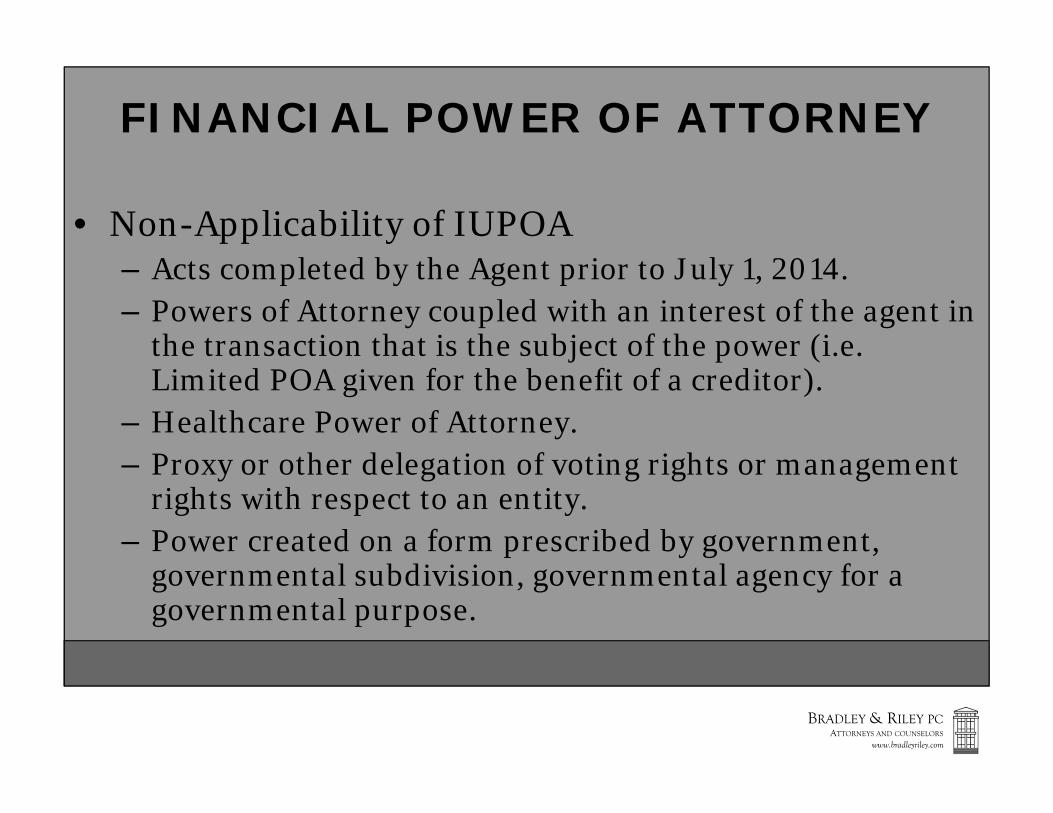

• Non-Applicability of IUPOA– Acts completed by the Agent prior to July 1, 2014.– Powers of Attorney coupled with an interest of the agent in

the transaction that is the subject of the power (i.e. Limited POA given for the benefit of a creditor).

– Healthcare Power of Attorney.– Proxy or other delegation of voting rights or management

rights with respect to an entity.– Power created on a form prescribed by government,

governmental subdivision, governmental agency for a governmental purpose.

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 16

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

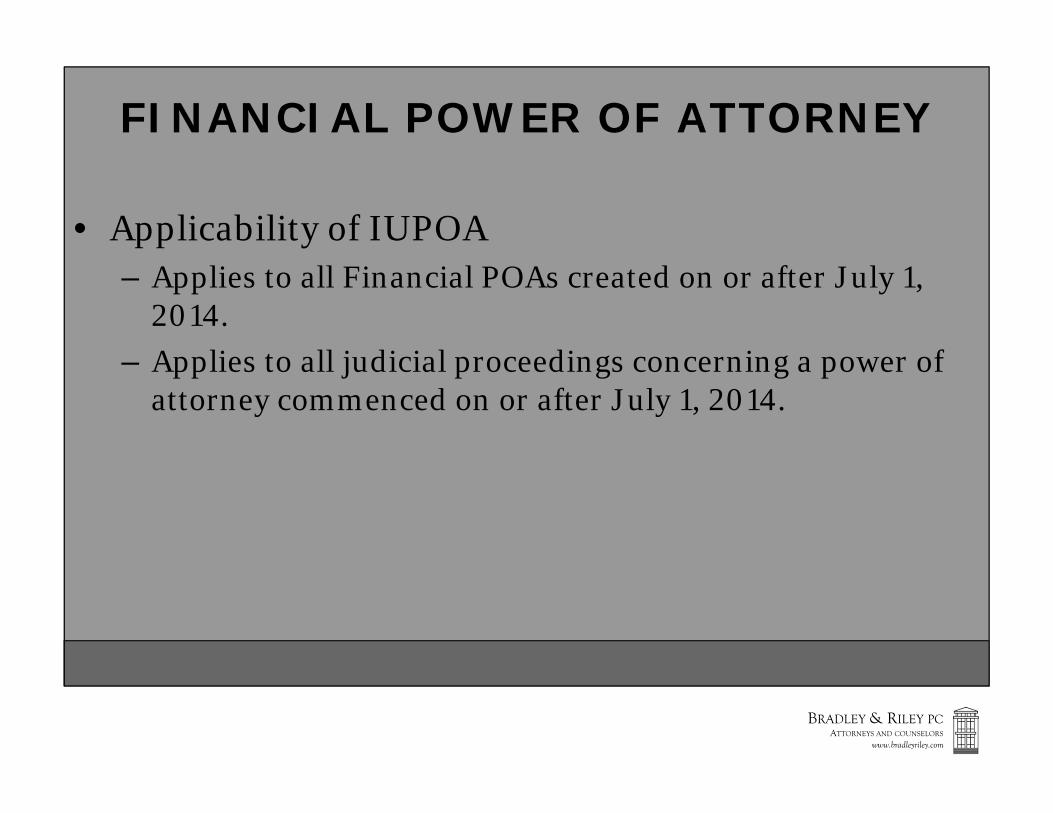

• Applicability of IUPOA– Applies to all Financial POAs created on or after July 1,

2014.– Applies to all judicial proceedings concerning a power of

attorney commenced on or after July 1, 2014.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

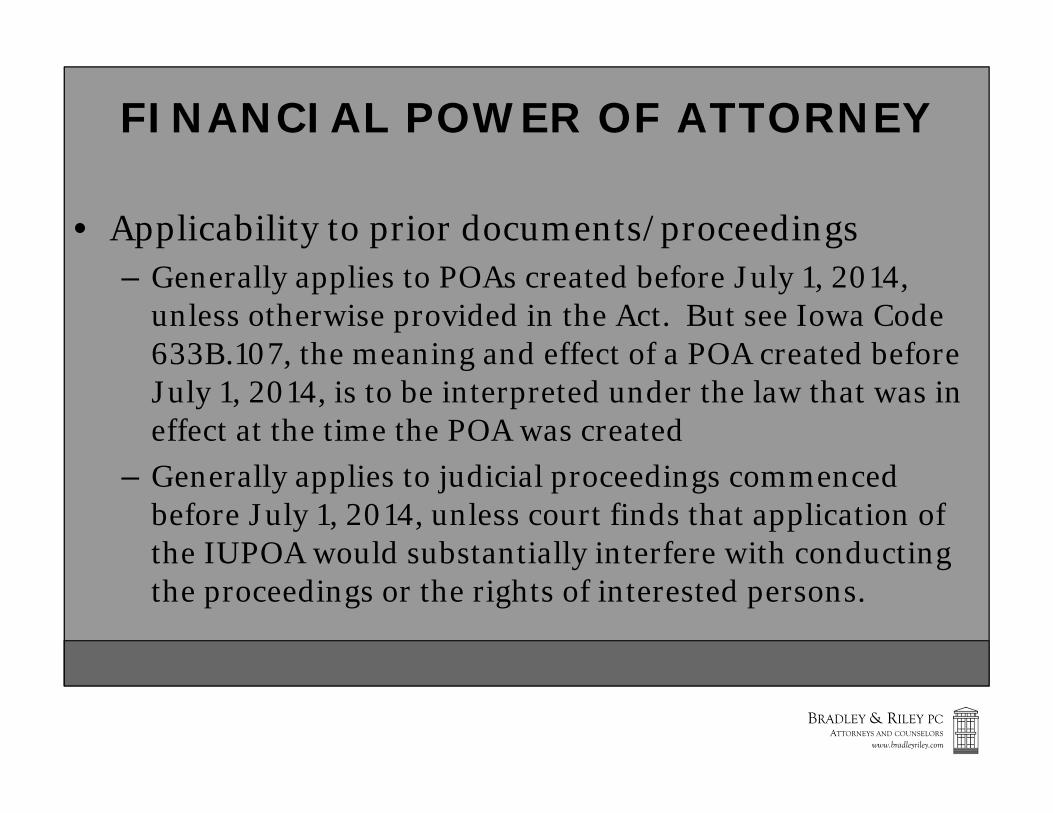

• Applicability to prior documents/proceedings– Generally applies to POAs created before July 1, 2014,

unless otherwise provided in the Act. But see Iowa Code 633B.107, the meaning and effect of a POA created before July 1, 2014, is to be interpreted under the law that was in effect at the time the POA was created

– Generally applies to judicial proceedings commenced before July 1, 2014, unless court finds that application of the IUPOA would substantially interfere with conducting the proceedings or the rights of interested persons.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

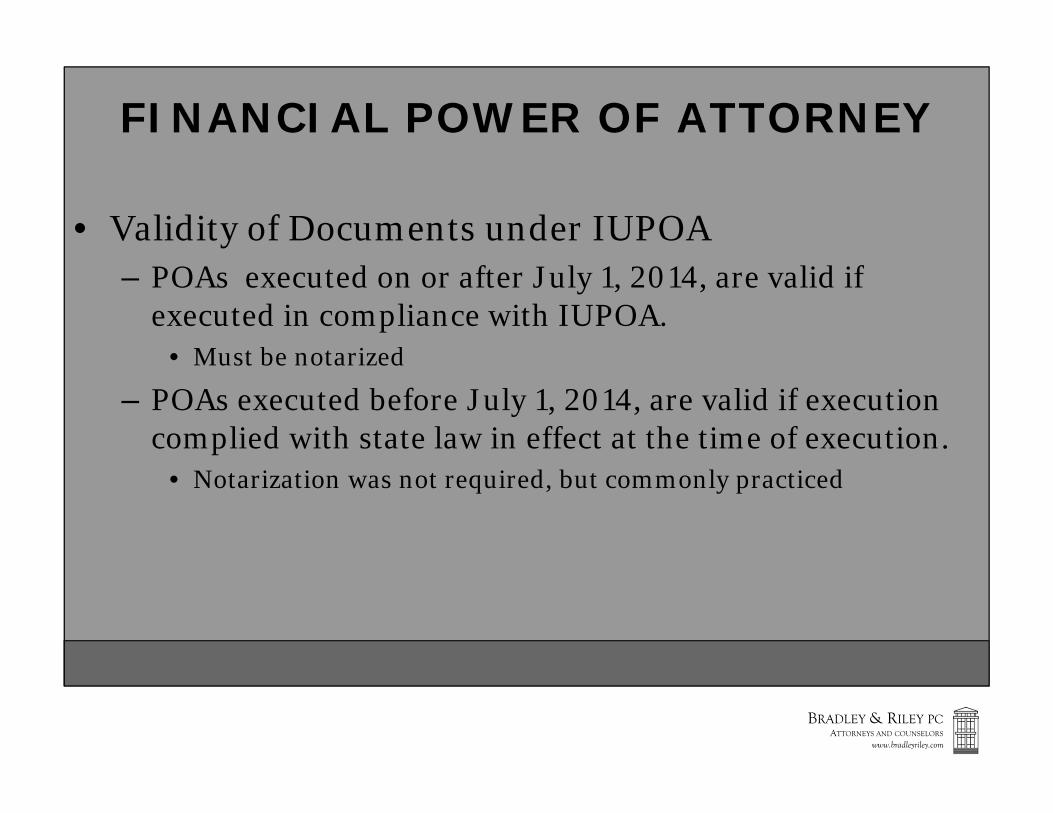

• Validity of Documents under IUPOA– POAs executed on or after July 1, 2014, are valid if

executed in compliance with IUPOA.• Must be notarized

– POAs executed before July 1, 2014, are valid if execution complied with state law in effect at the time of execution.

• Notarization was not required, but commonly practiced

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 17

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

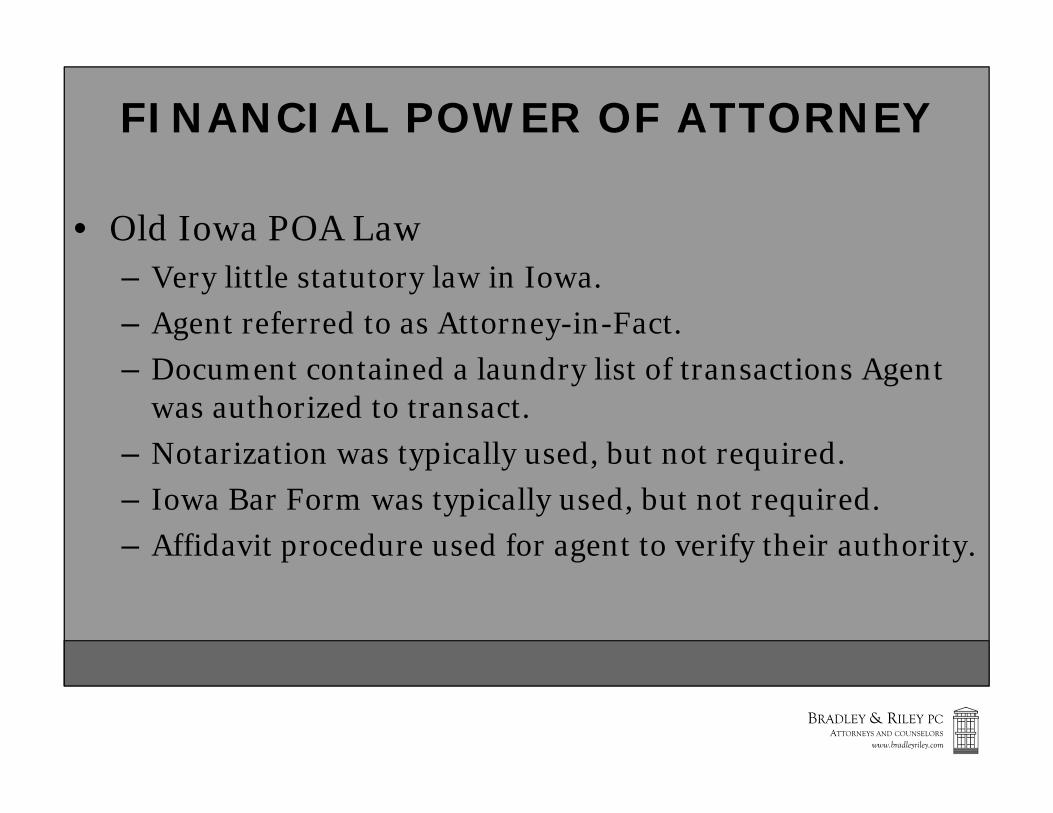

FINANCIAL POWER OF ATTORNEY

• Old Iowa POA Law– Very little statutory law in Iowa.– Agent referred to as Attorney-in-Fact.– Document contained a laundry list of transactions Agent

was authorized to transact.– Notarization was typically used, but not required.– Iowa Bar Form was typically used, but not required.– Affidavit procedure used for agent to verify their authority.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

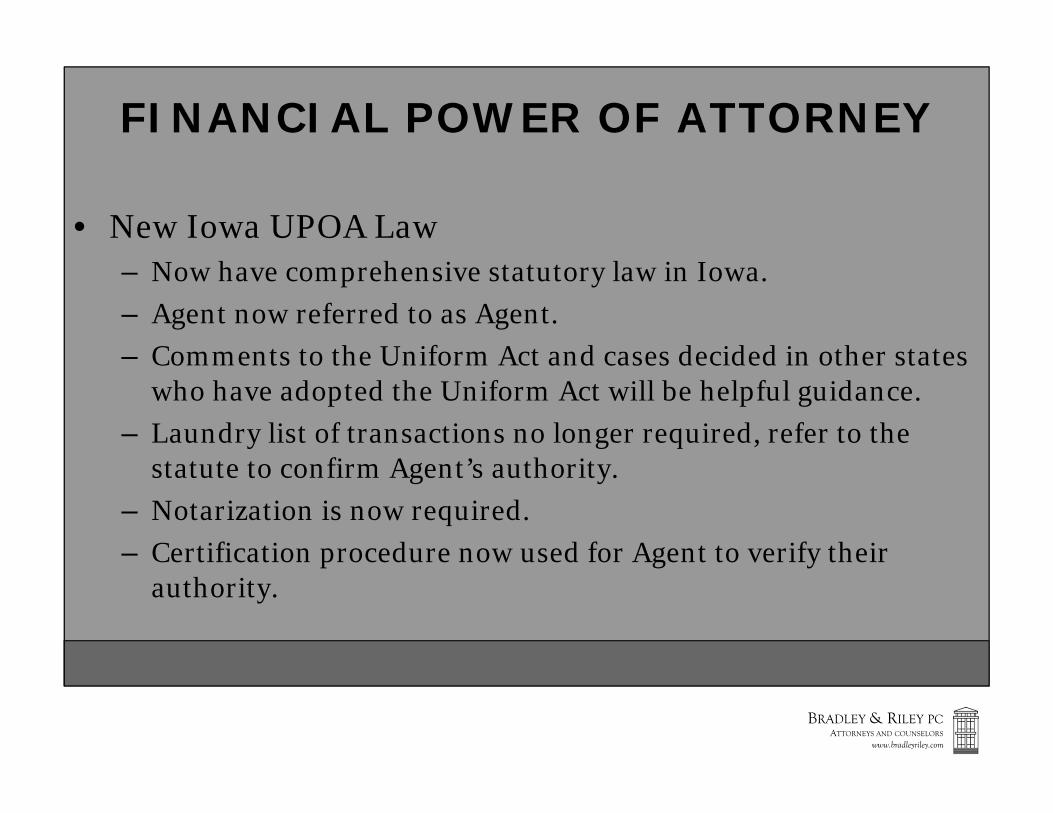

FINANCIAL POWER OF ATTORNEY

• New Iowa UPOA Law– Now have comprehensive statutory law in Iowa.– Agent now referred to as Agent.– Comments to the Uniform Act and cases decided in other states

who have adopted the Uniform Act will be helpful guidance.– Laundry list of transactions no longer required, refer to the

statute to confirm Agent’s authority.– Notarization is now required.– Certification procedure now used for Agent to verify their

authority.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

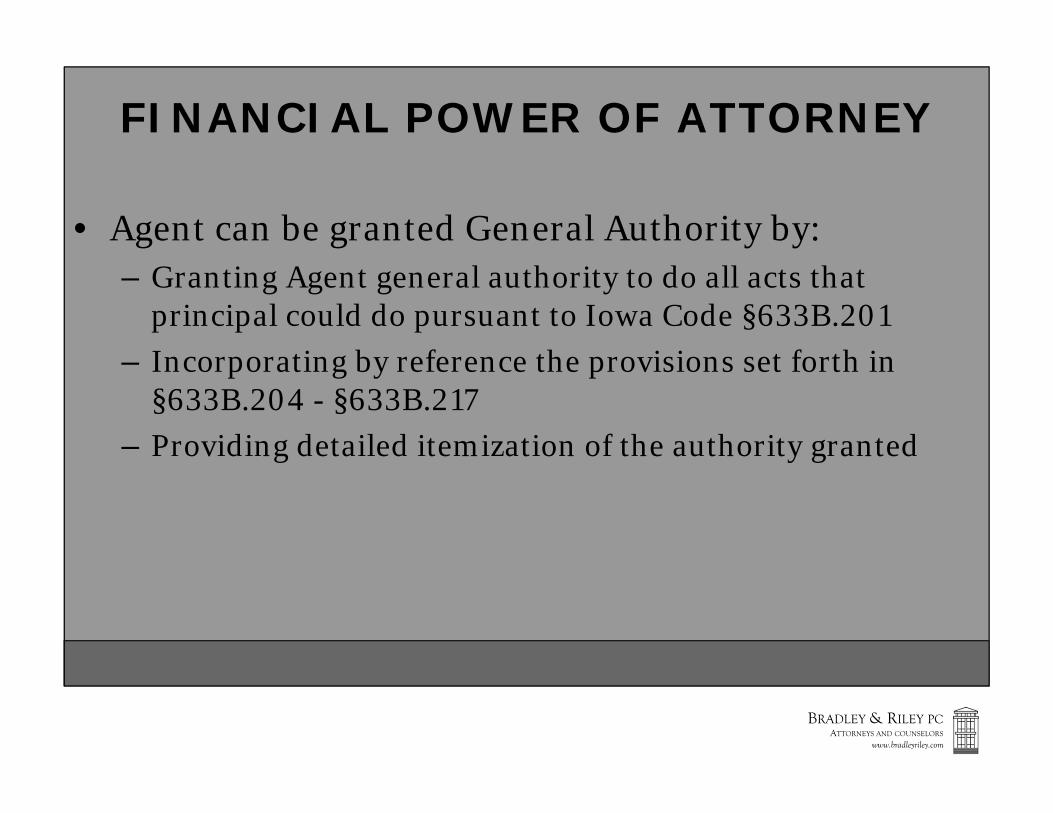

• Agent can be granted General Authority by:– Granting Agent general authority to do all acts that

principal could do pursuant to Iowa Code §633B.201– Incorporating by reference the provisions set forth in

§633B.204 - §633B.217– Providing detailed itemization of the authority granted

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 18

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

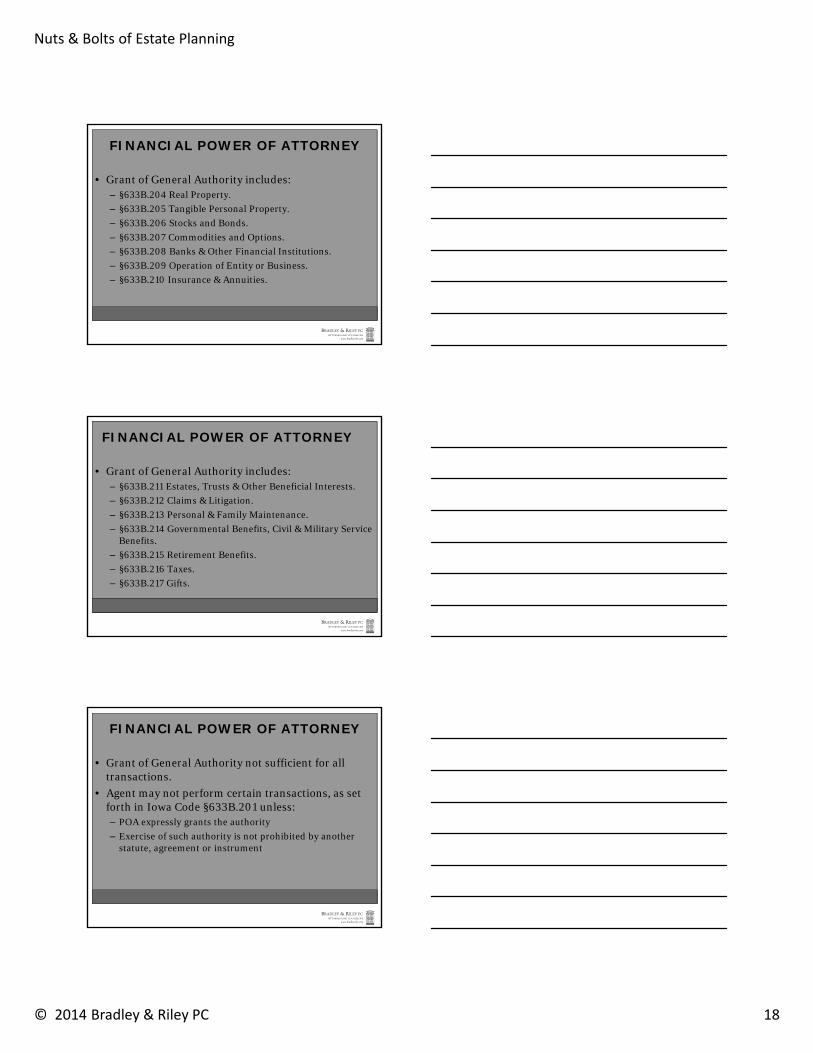

FINANCIAL POWER OF ATTORNEY

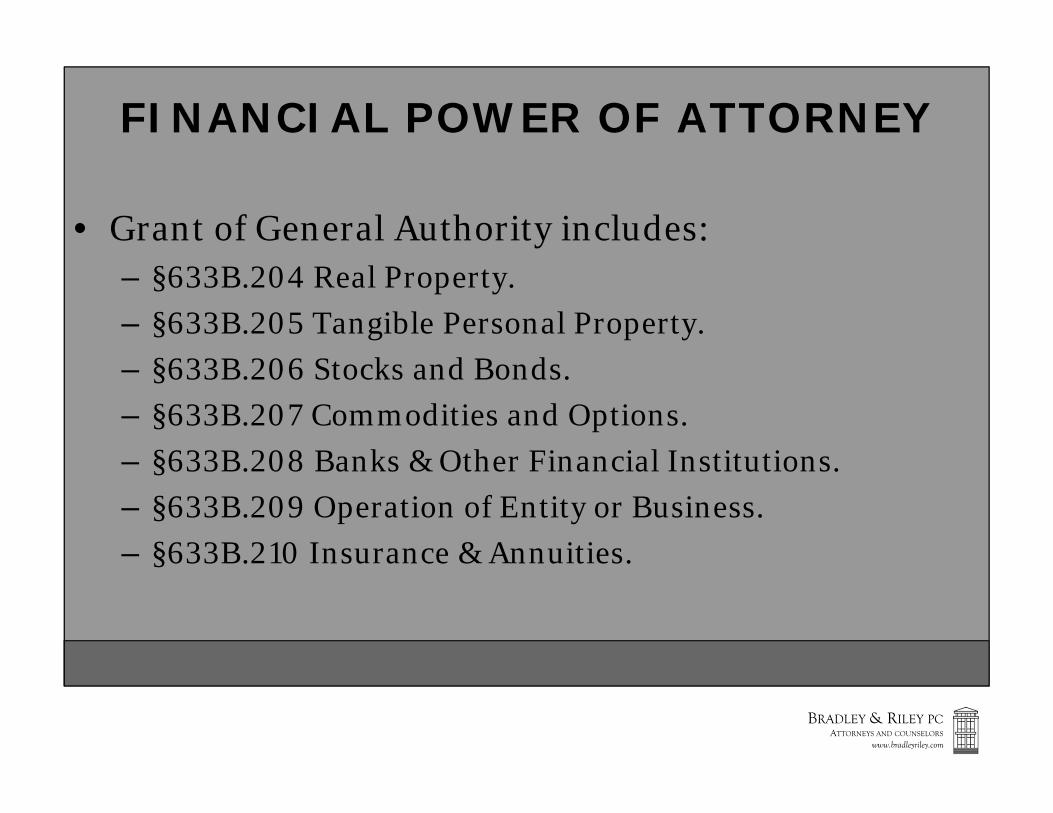

• Grant of General Authority includes:– §633B.204 Real Property.– §633B.205 Tangible Personal Property.– §633B.206 Stocks and Bonds.– §633B.207 Commodities and Options.– §633B.208 Banks & Other Financial Institutions.– §633B.209 Operation of Entity or Business.– §633B.210 Insurance & Annuities.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

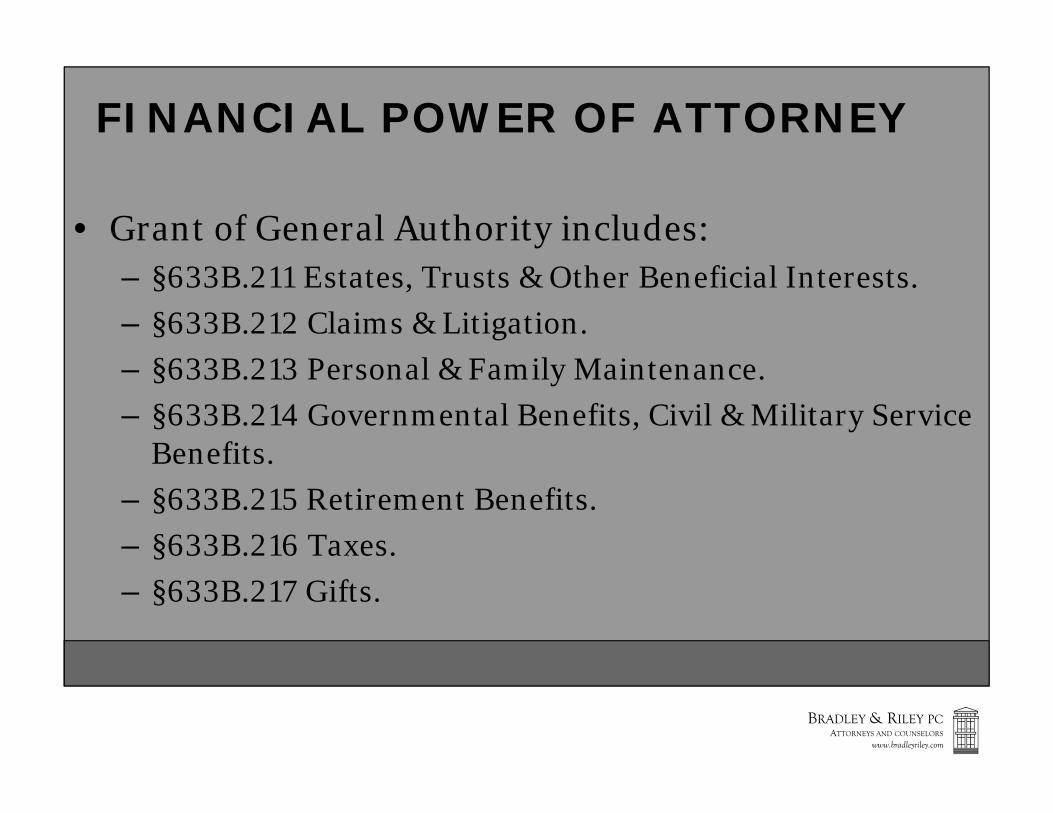

• Grant of General Authority includes:– §633B.211 Estates, Trusts & Other Beneficial Interests.– §633B.212 Claims & Litigation.– §633B.213 Personal & Family Maintenance.– §633B.214 Governmental Benefits, Civil & Military Service

Benefits.– §633B.215 Retirement Benefits.– §633B.216 Taxes.– §633B.217 Gifts.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

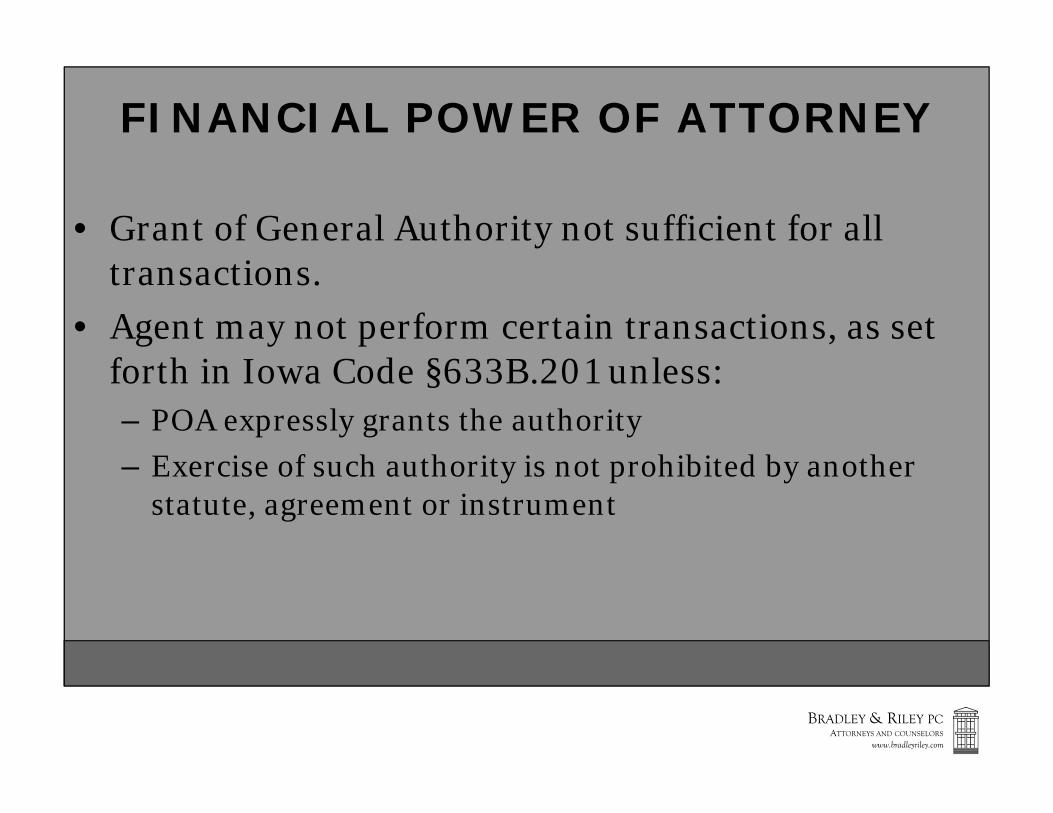

• Grant of General Authority not sufficient for all transactions.

• Agent may not perform certain transactions, as set forth in Iowa Code §633B.201 unless:– POA expressly grants the authority– Exercise of such authority is not prohibited by another

statute, agreement or instrument

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 19

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

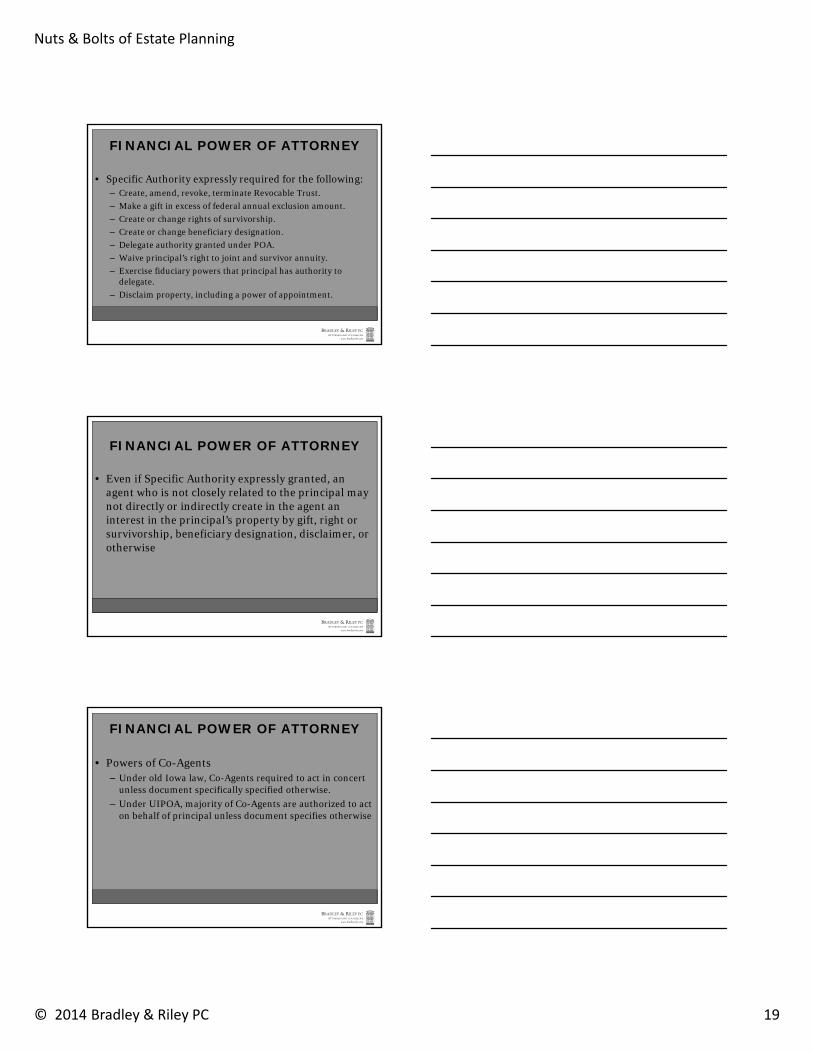

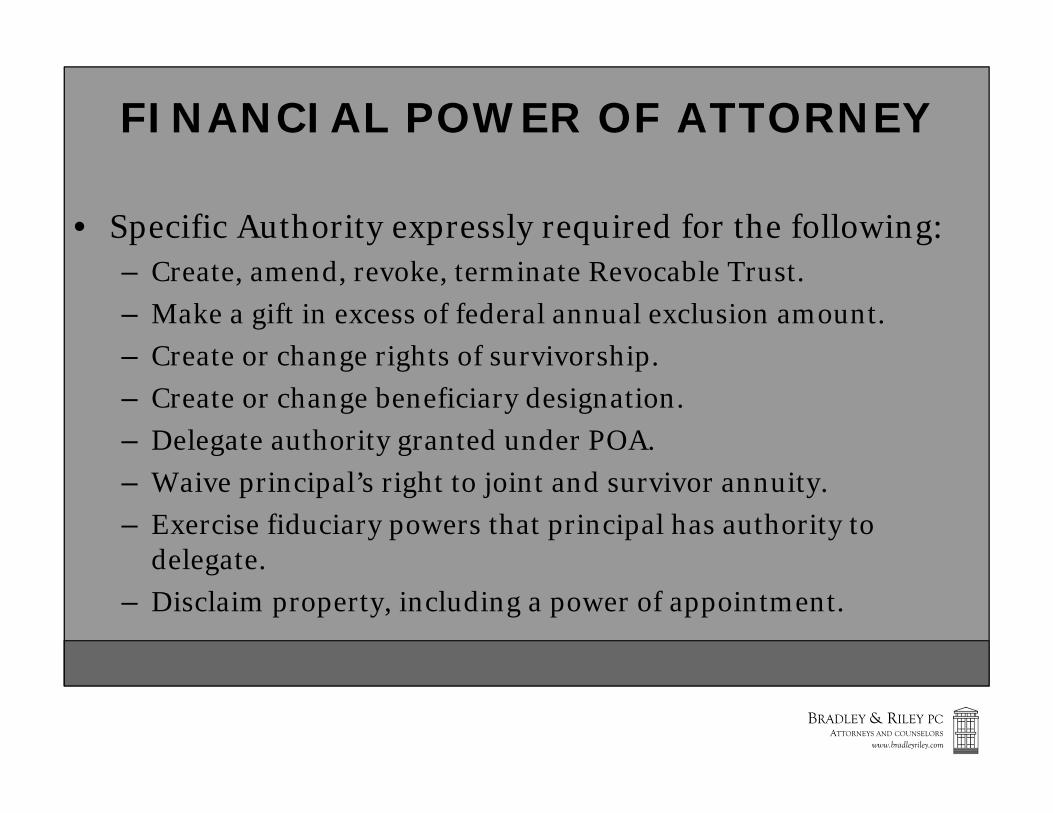

• Specific Authority expressly required for the following:– Create, amend, revoke, terminate Revocable Trust.– Make a gift in excess of federal annual exclusion amount.– Create or change rights of survivorship.– Create or change beneficiary designation.– Delegate authority granted under POA.– Waive principal’s right to joint and survivor annuity.– Exercise fiduciary powers that principal has authority to

delegate.– Disclaim property, including a power of appointment.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

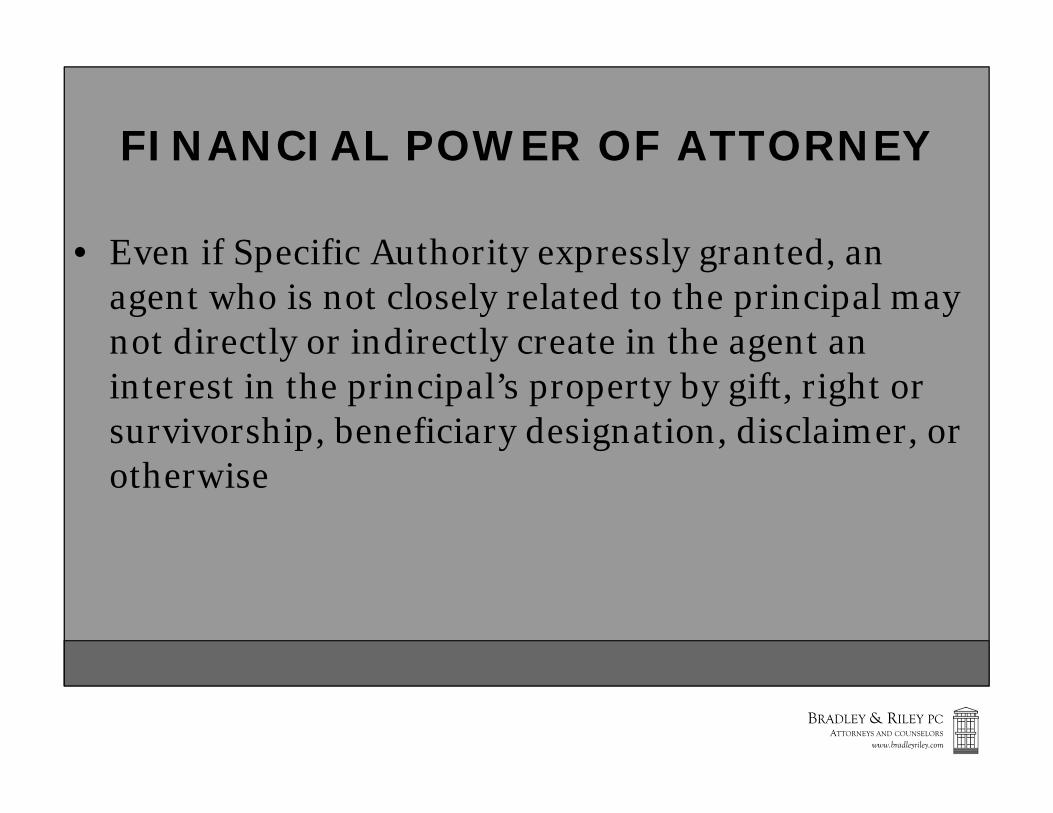

• Even if Specific Authority expressly granted, an agent who is not closely related to the principal may not directly or indirectly create in the agent an interest in the principal’s property by gift, right or survivorship, beneficiary designation, disclaimer, or otherwise

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Powers of Co-Agents– Under old Iowa law, Co-Agents required to act in concert

unless document specifically specified otherwise.– Under UIPOA, majority of Co-Agents are authorized to act

on behalf of principal unless document specifies otherwise

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 20

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

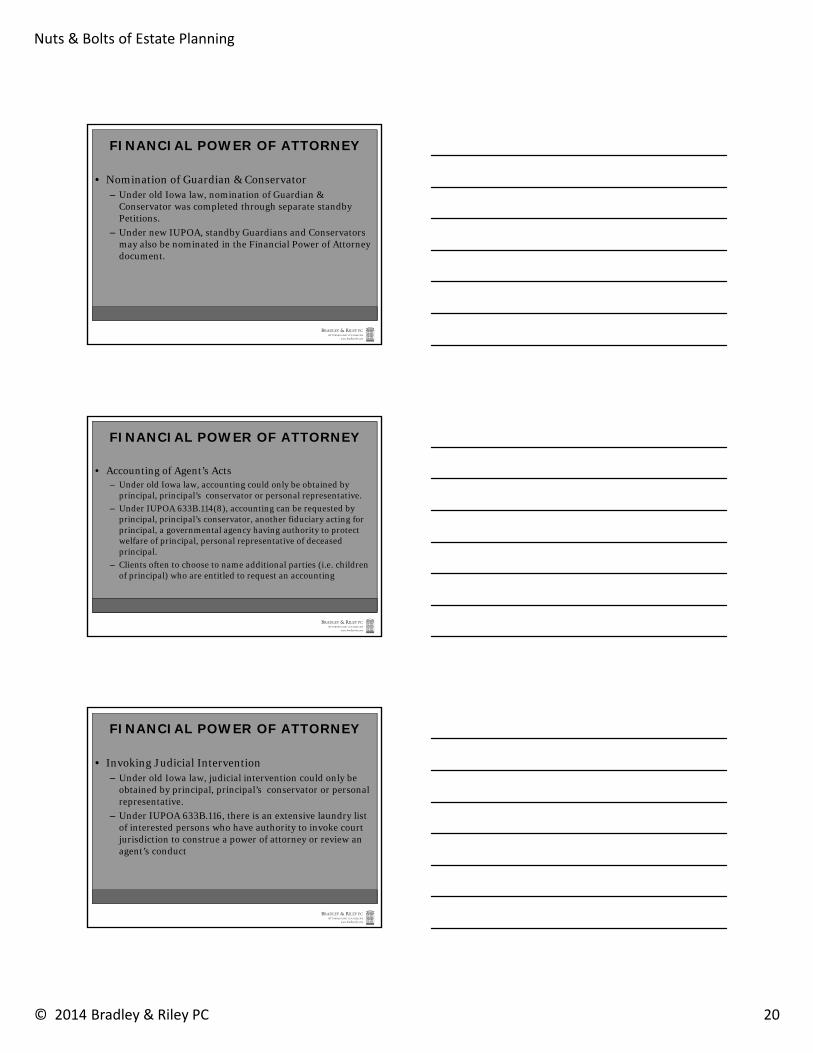

• Nomination of Guardian & Conservator– Under old Iowa law, nomination of Guardian &

Conservator was completed through separate standby Petitions.

– Under new IUPOA, standby Guardians and Conservators may also be nominated in the Financial Power of Attorney document.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Accounting of Agent’s Acts– Under old Iowa law, accounting could only be obtained by

principal, principal’s conservator or personal representative.– Under IUPOA 633B.114(8), accounting can be requested by

principal, principal’s conservator, another fiduciary acting for principal, a governmental agency having authority to protect welfare of principal, personal representative of deceased principal.

– Clients often to choose to name additional parties (i.e. children of principal) who are entitled to request an accounting

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Invoking Judicial Intervention– Under old Iowa law, judicial intervention could only be

obtained by principal, principal’s conservator or personal representative.

– Under IUPOA 633B.116, there is an extensive laundry list of interested persons who have authority to invoke court jurisdiction to construe a power of attorney or review an agent’s conduct

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 21

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

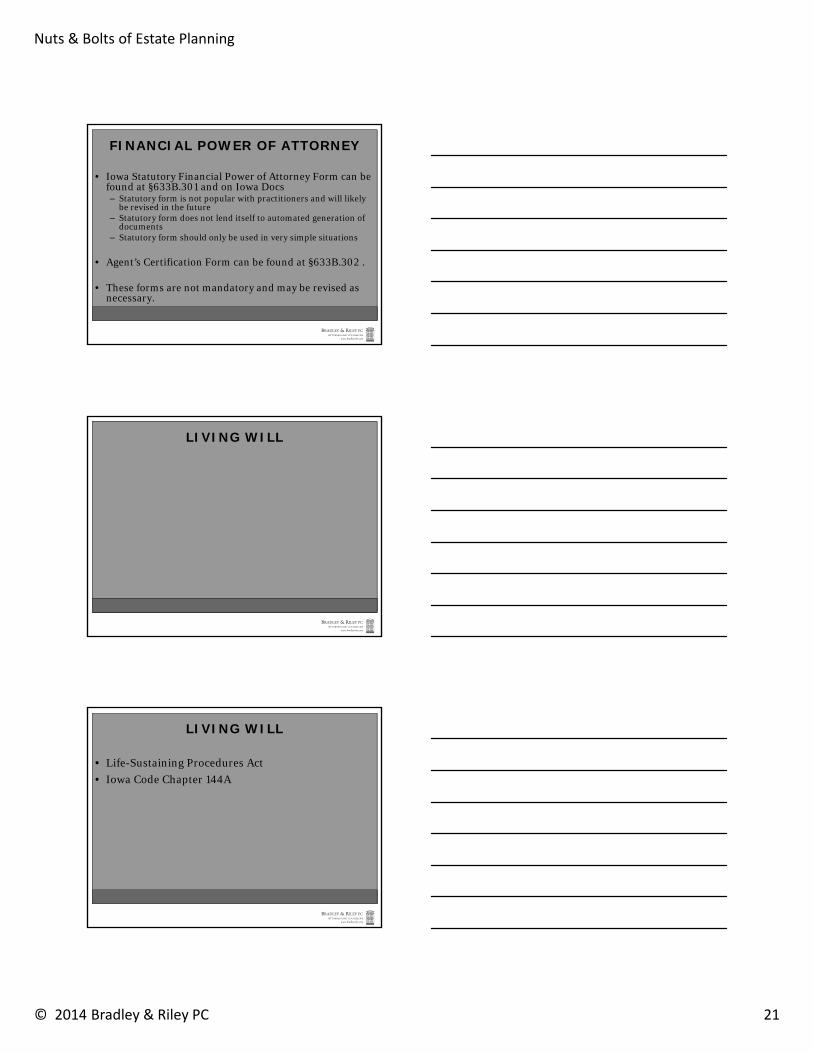

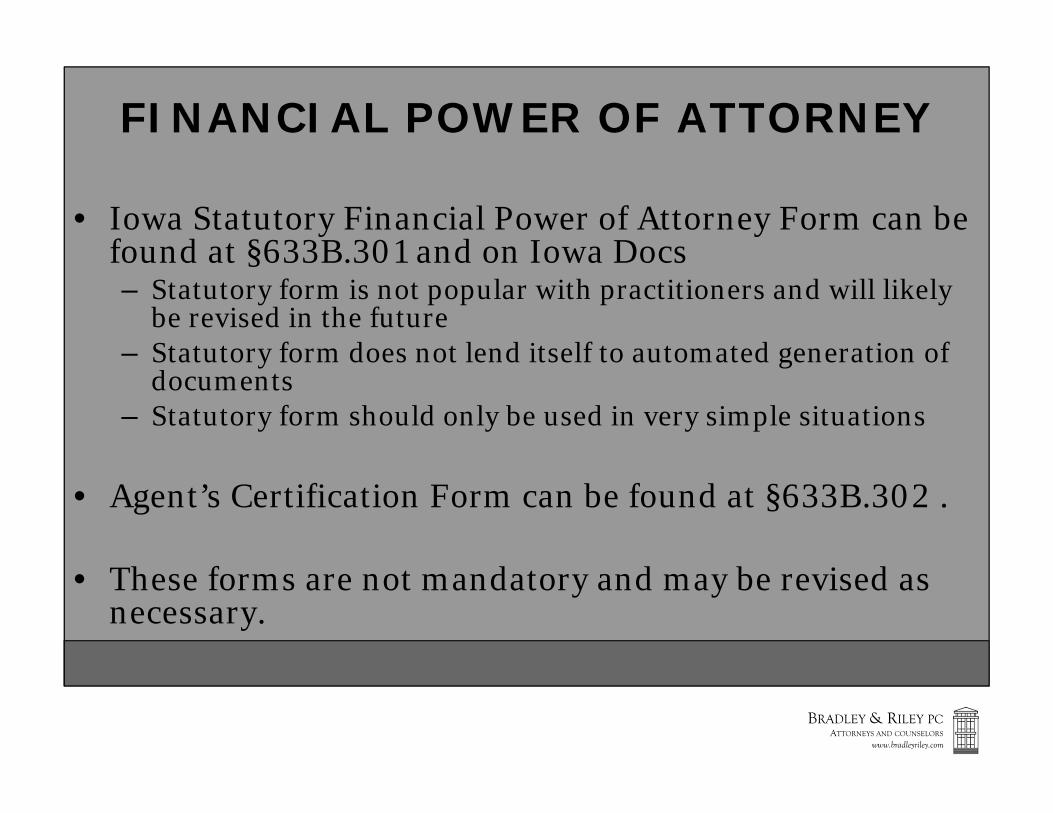

• Iowa Statutory Financial Power of Attorney Form can be found at §633B.301 and on Iowa Docs– Statutory form is not popular with practitioners and will likely

be revised in the future– Statutory form does not lend itself to automated generation of

documents– Statutory form should only be used in very simple situations

• Agent’s Certification Form can be found at §633B.302 .

• These forms are not mandatory and may be revised as necessary.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

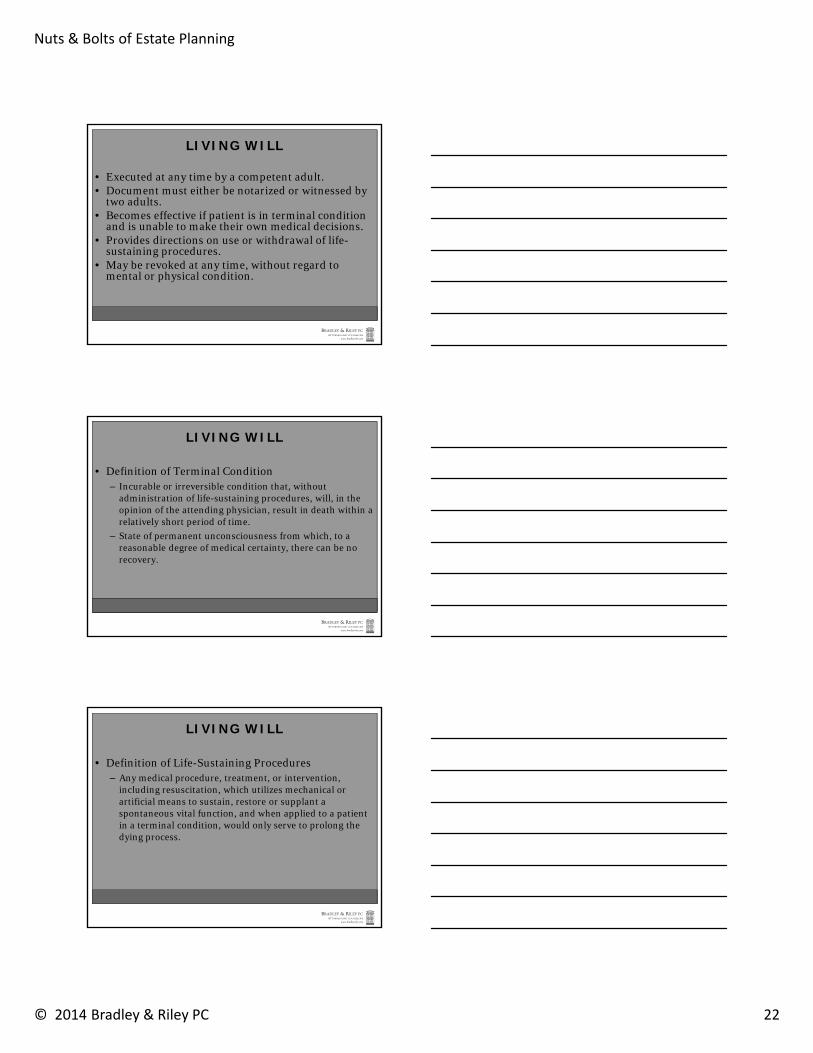

LIVING WILL

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

• Life-Sustaining Procedures Act• Iowa Code Chapter 144A

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 22

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

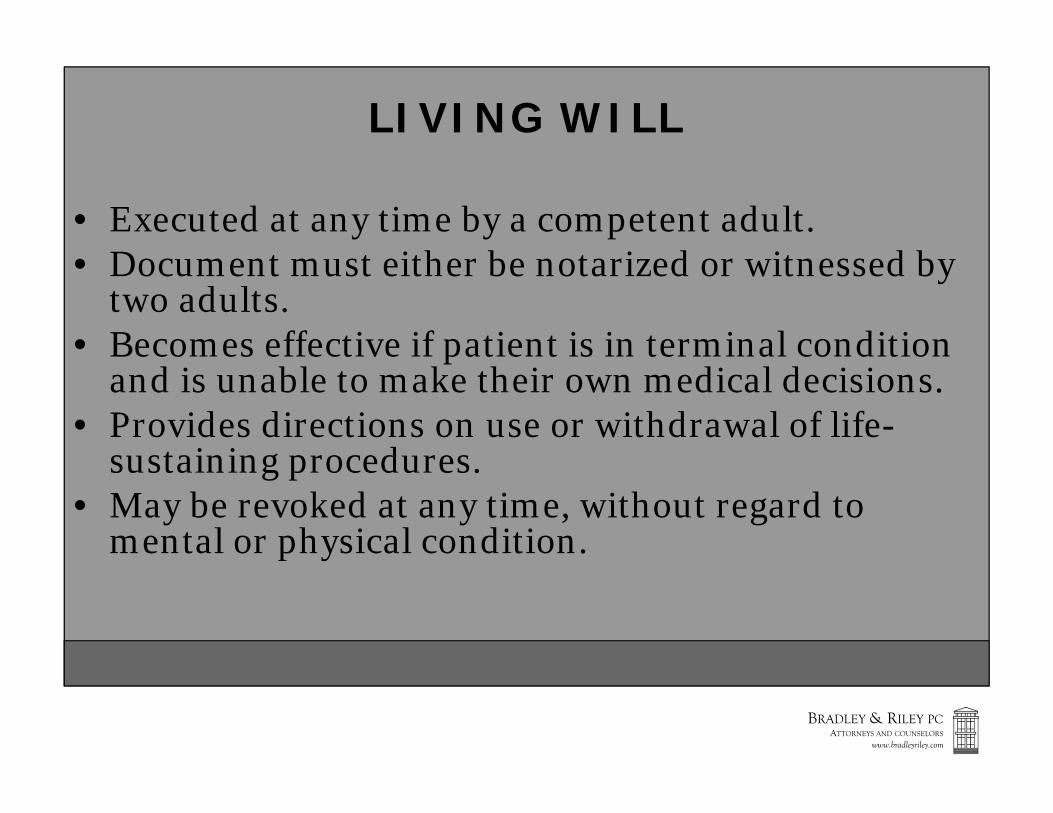

• Executed at any time by a competent adult.• Document must either be notarized or witnessed by

two adults.• Becomes effective if patient is in terminal condition

and is unable to make their own medical decisions.• Provides directions on use or withdrawal of life-

sustaining procedures.• May be revoked at any time, without regard to

mental or physical condition.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

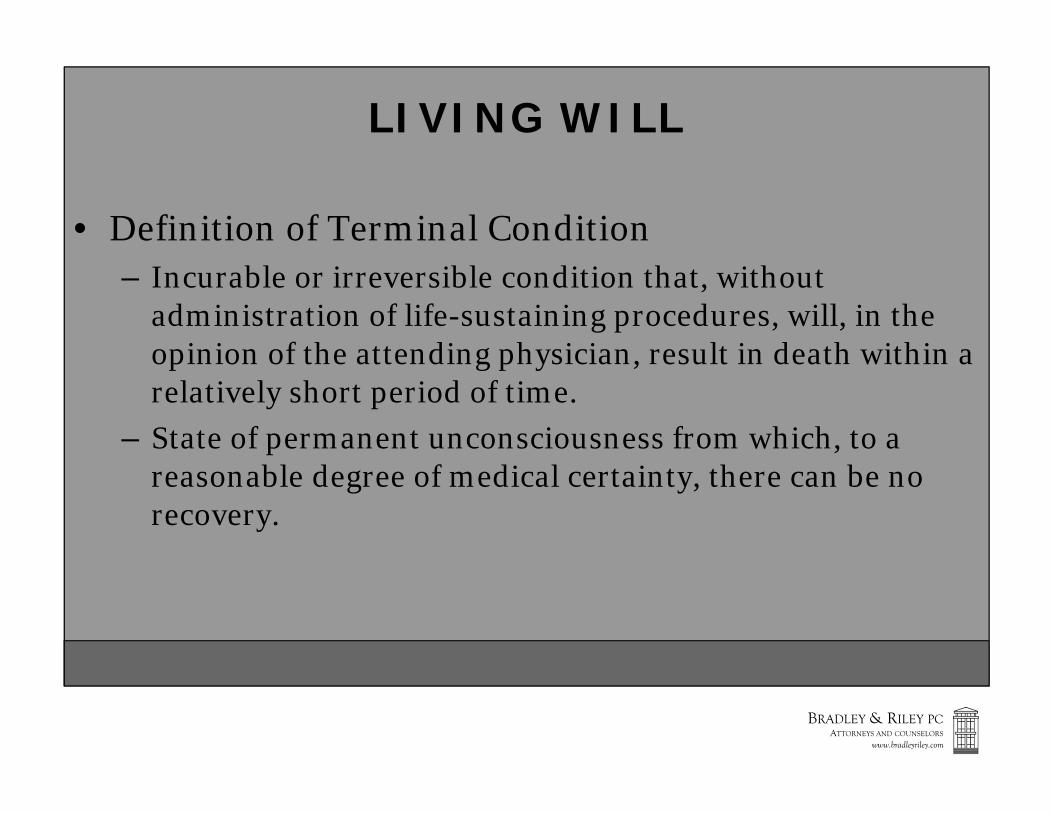

LIVING WILL

• Definition of Terminal Condition– Incurable or irreversible condition that, without

administration of life-sustaining procedures, will, in the opinion of the attending physician, result in death within a relatively short period of time.

– State of permanent unconsciousness from which, to a reasonable degree of medical certainty, there can be no recovery.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

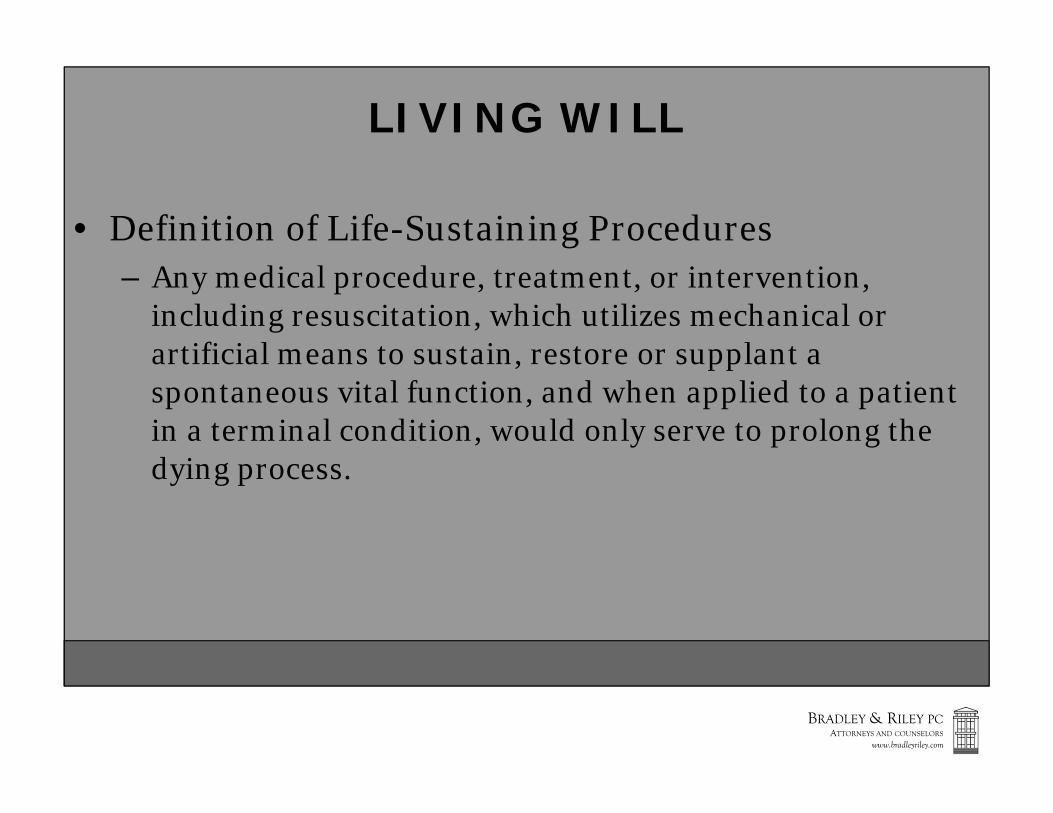

LIVING WILL

• Definition of Life-Sustaining Procedures– Any medical procedure, treatment, or intervention,

including resuscitation, which utilizes mechanical or artificial means to sustain, restore or supplant a spontaneous vital function, and when applied to a patient in a terminal condition, would only serve to prolong the dying process.

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 23

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

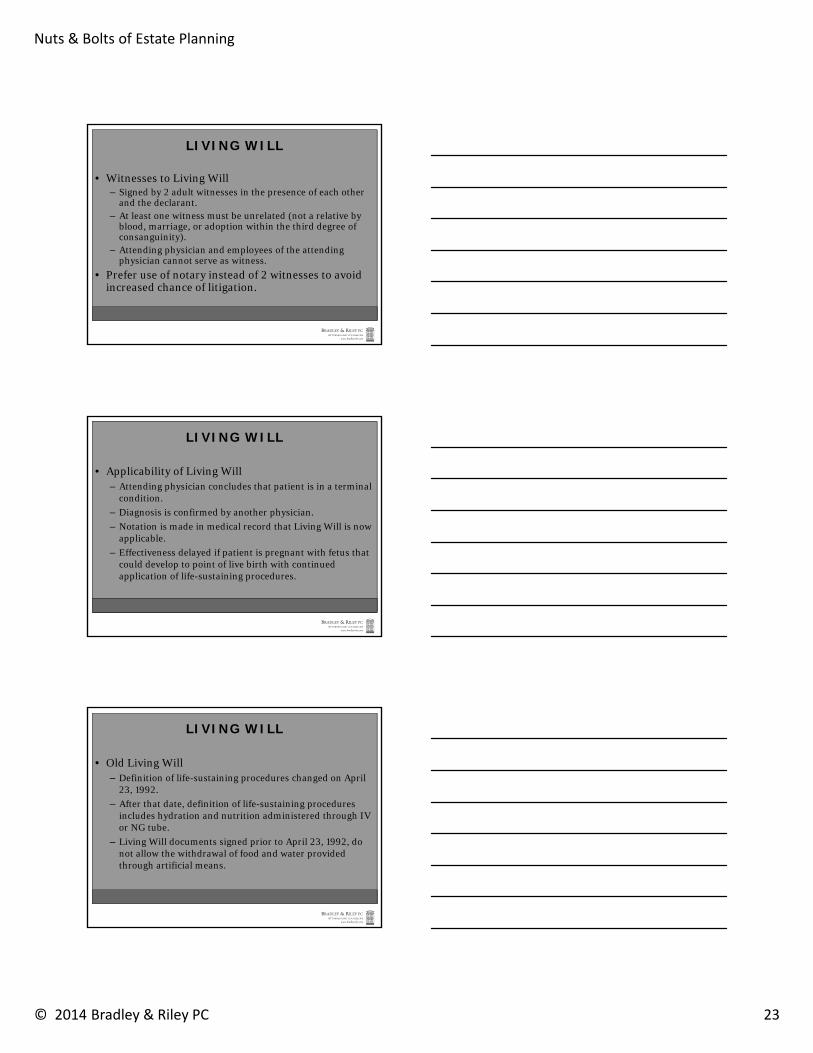

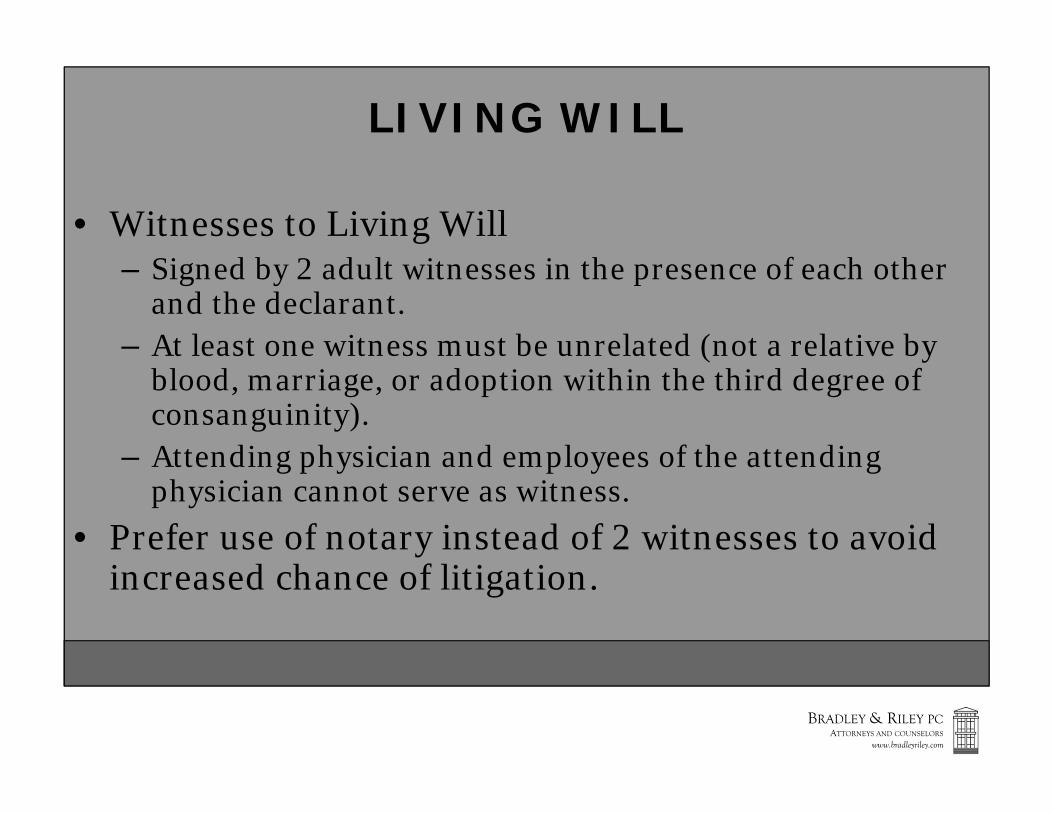

LIVING WILL

• Witnesses to Living Will– Signed by 2 adult witnesses in the presence of each other

and the declarant.– At least one witness must be unrelated (not a relative by

blood, marriage, or adoption within the third degree of consanguinity).

– Attending physician and employees of the attending physician cannot serve as witness.

• Prefer use of notary instead of 2 witnesses to avoid increased chance of litigation.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

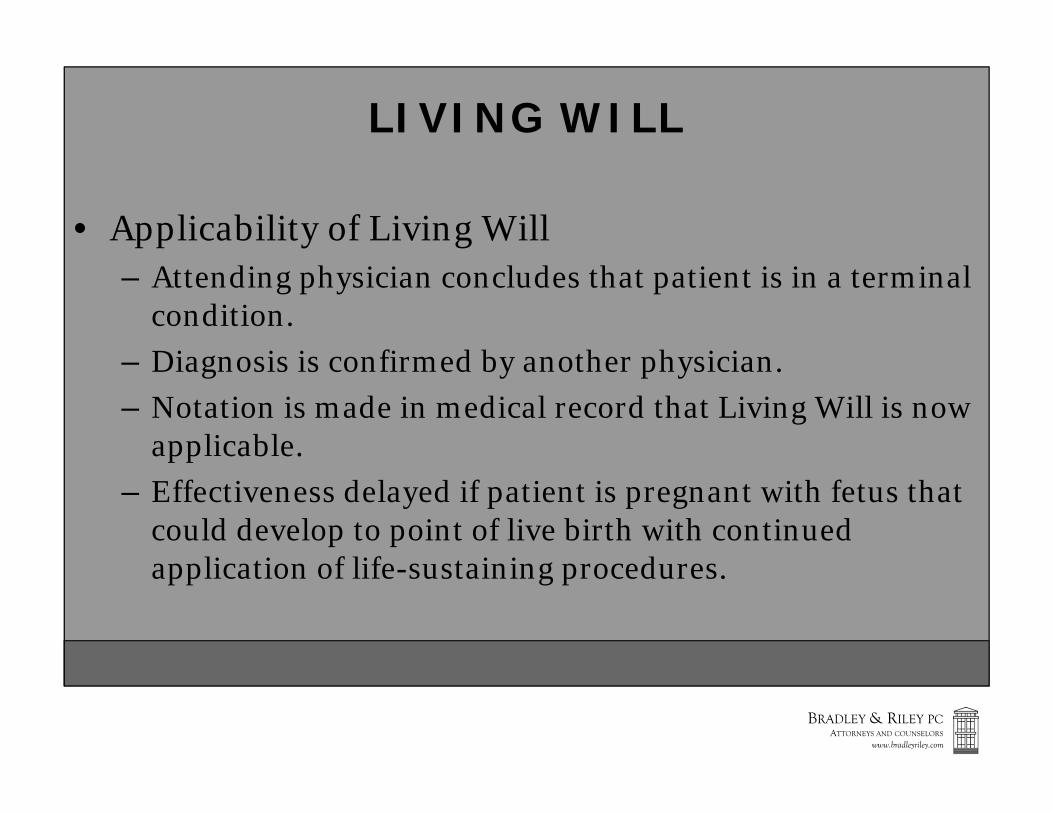

LIVING WILL

• Applicability of Living Will– Attending physician concludes that patient is in a terminal

condition.– Diagnosis is confirmed by another physician.– Notation is made in medical record that Living Will is now

applicable.– Effectiveness delayed if patient is pregnant with fetus that

could develop to point of live birth with continued application of life-sustaining procedures.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

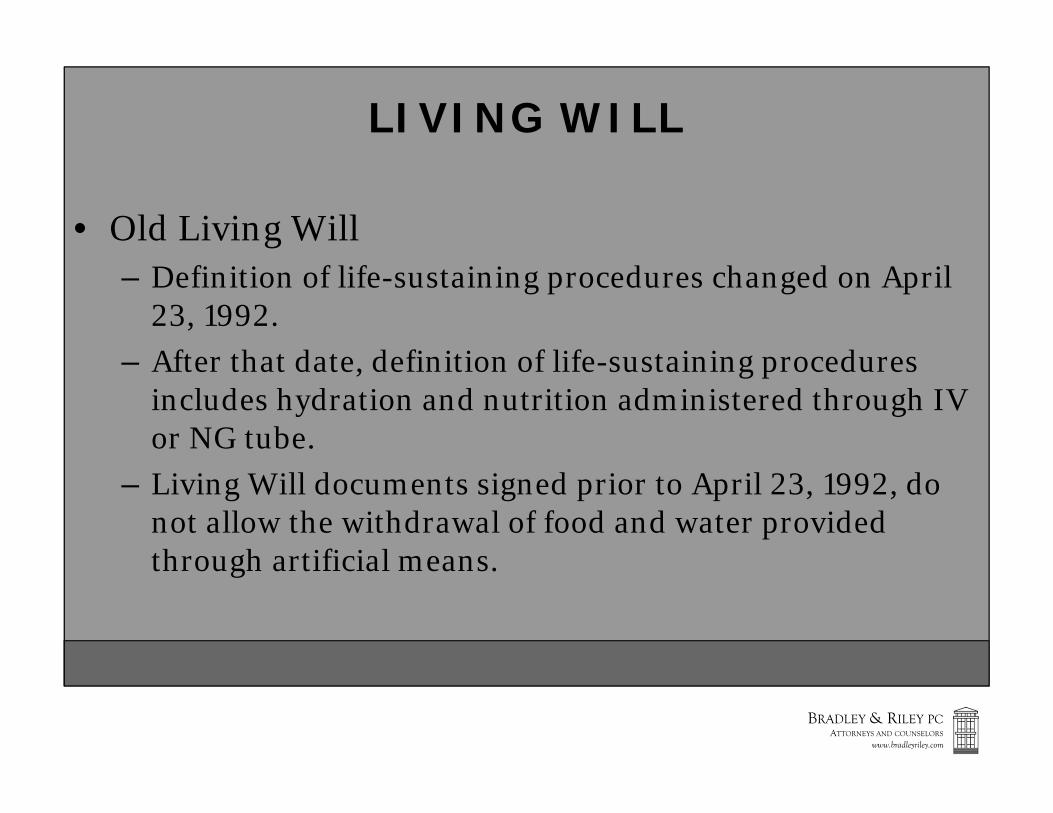

LIVING WILL

• Old Living Will– Definition of life-sustaining procedures changed on April

23, 1992.– After that date, definition of life-sustaining procedures

includes hydration and nutrition administered through IV or NG tube.

– Living Will documents signed prior to April 23, 1992, do not allow the withdrawal of food and water provided through artificial means.

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 24

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

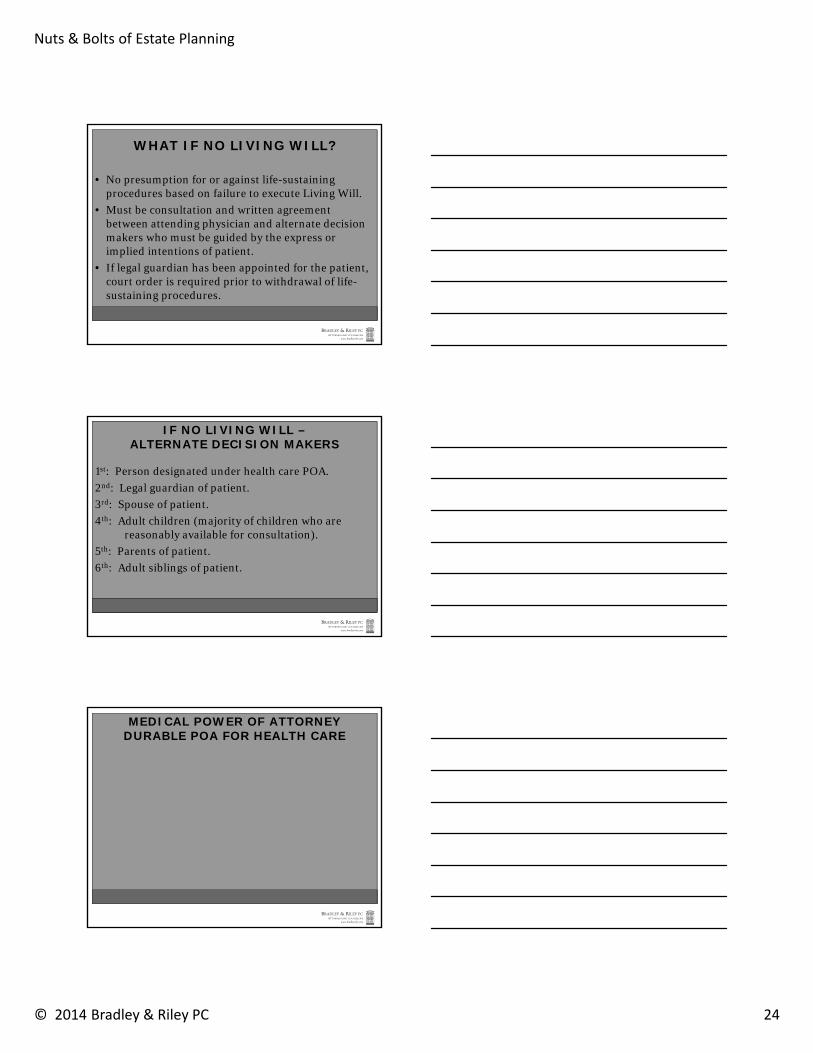

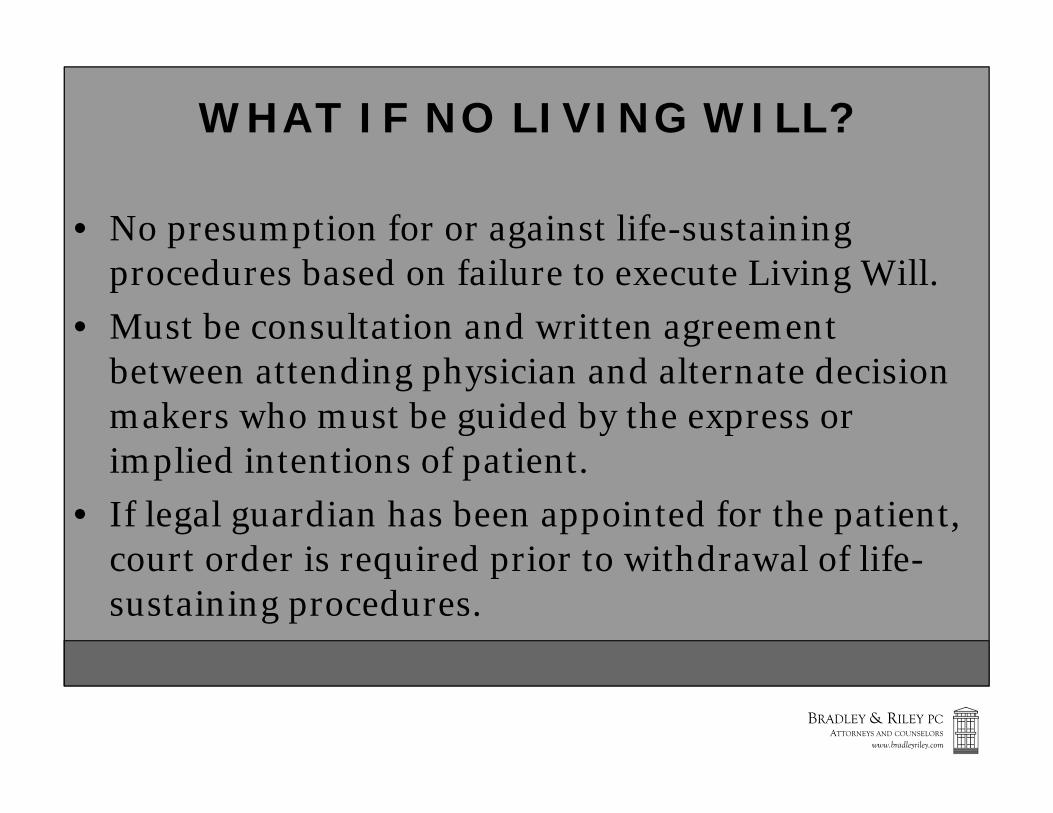

WHAT IF NO LIVING WILL?

• No presumption for or against life-sustaining procedures based on failure to execute Living Will.

• Must be consultation and written agreement between attending physician and alternate decision makers who must be guided by the express or implied intentions of patient.

• If legal guardian has been appointed for the patient, court order is required prior to withdrawal of life-sustaining procedures.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

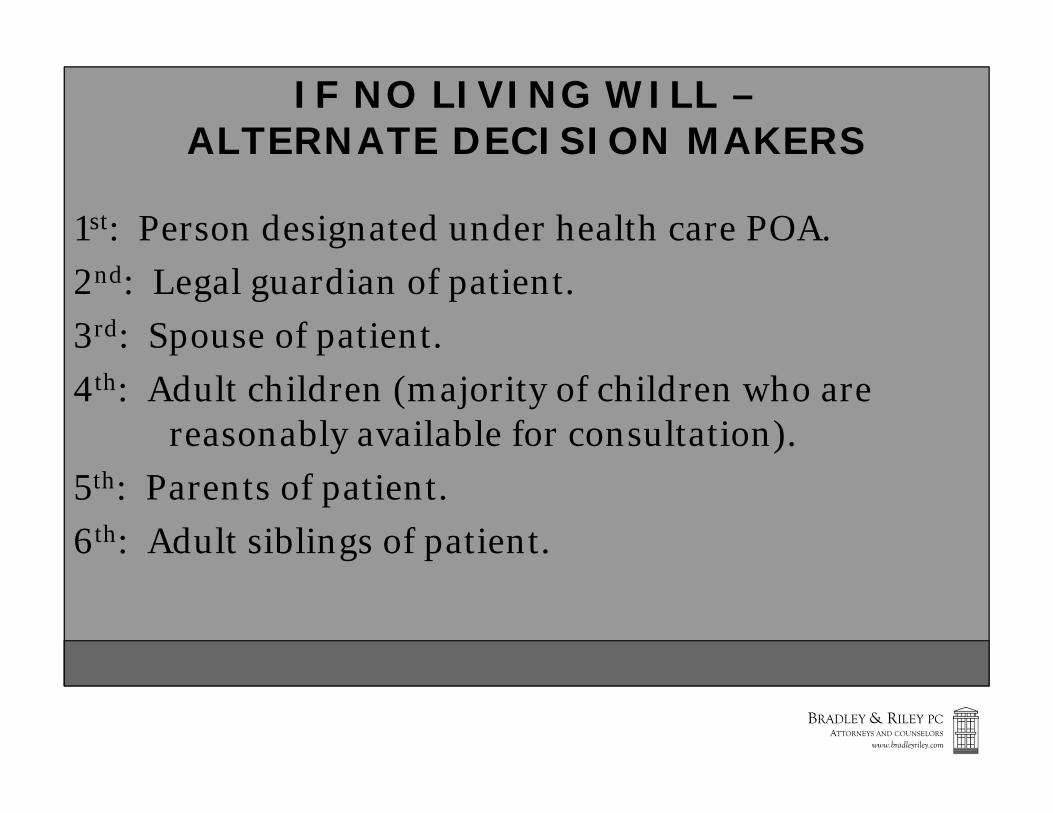

IF NO LIVING WILL –ALTERNATE DECISION MAKERS

1st: Person designated under health care POA.2nd: Legal guardian of patient.3rd: Spouse of patient.4th: Adult children (majority of children who are

reasonably available for consultation).5th: Parents of patient.6th: Adult siblings of patient.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEYDURABLE POA FOR HEALTH CARE

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 25

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

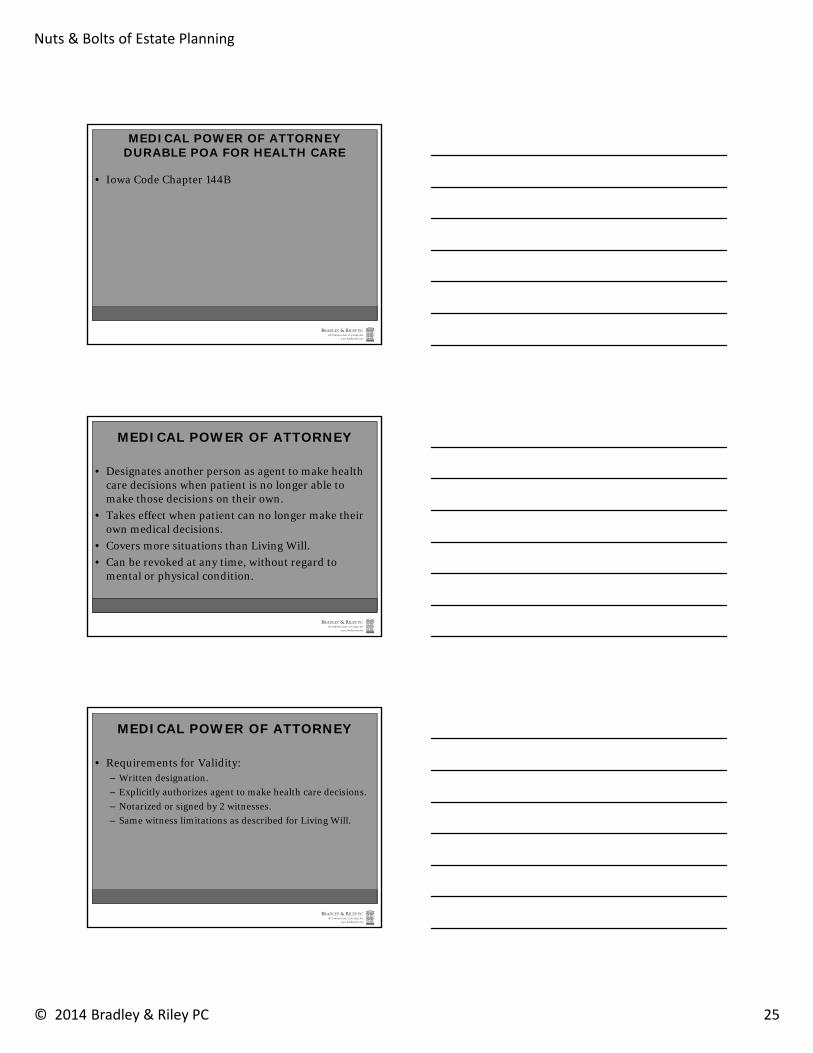

MEDICAL POWER OF ATTORNEYDURABLE POA FOR HEALTH CARE

• Iowa Code Chapter 144B

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEY

• Designates another person as agent to make health care decisions when patient is no longer able to make those decisions on their own.

• Takes effect when patient can no longer make their own medical decisions.

• Covers more situations than Living Will.• Can be revoked at any time, without regard to

mental or physical condition.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEY

• Requirements for Validity:– Written designation.– Explicitly authorizes agent to make health care decisions. – Notarized or signed by 2 witnesses.– Same witness limitations as described for Living Will.

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 26

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEY

• Ineligible Decision Makers under Medical POA:– Attending physician cannot serve as agent.– Employee of the attending physician cannot serve as

agent, unless the individual is related to patient by blood, marriage, or adoption within the 3rd degree of consanguinity.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

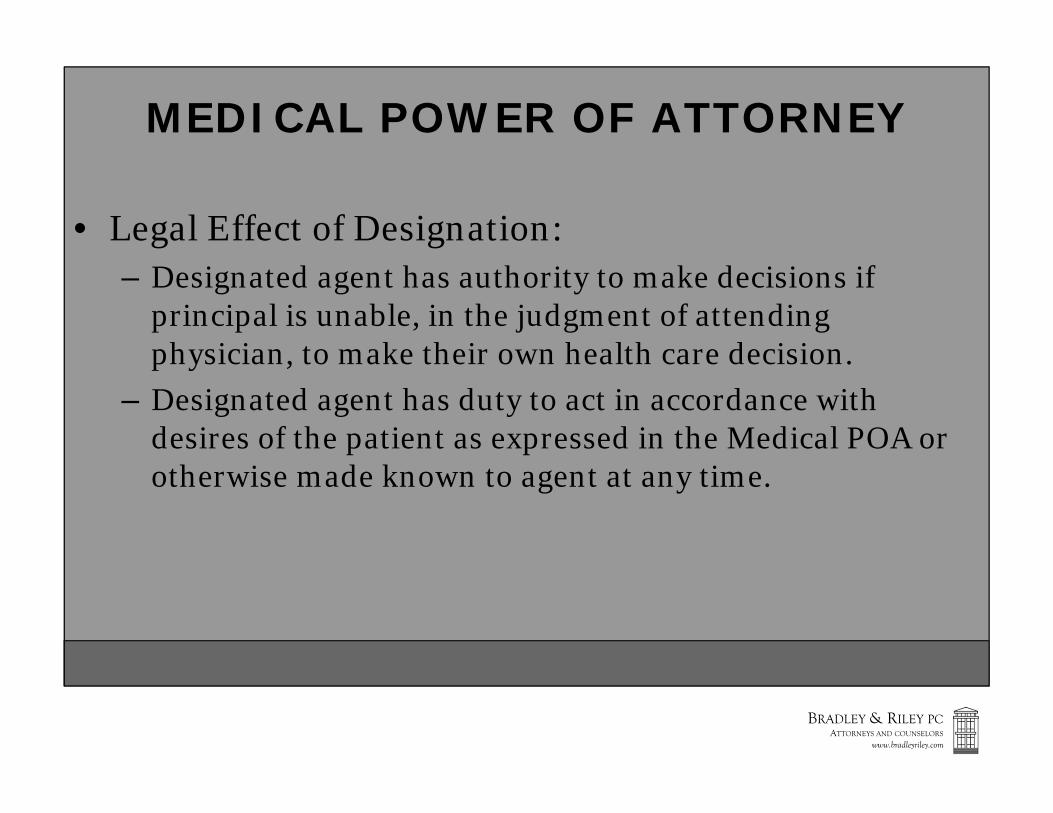

MEDICAL POWER OF ATTORNEY

• Legal Effect of Designation:– Designated agent has authority to make decisions if

principal is unable, in the judgment of attending physician, to make their own health care decision.

– Designated agent has duty to act in accordance with desires of the patient as expressed in the Medical POA or otherwise made known to agent at any time.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

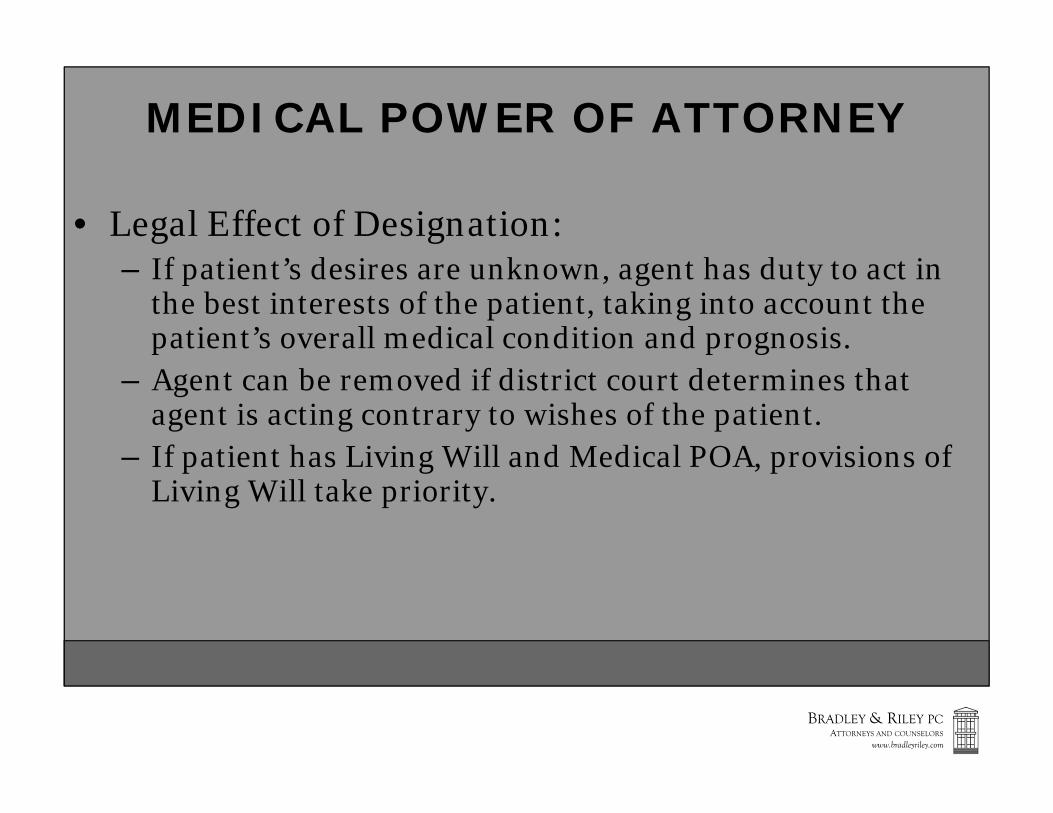

MEDICAL POWER OF ATTORNEY

• Legal Effect of Designation:– If patient’s desires are unknown, agent has duty to act in

the best interests of the patient, taking into account the patient’s overall medical condition and prognosis.

– Agent can be removed if district court determines that agent is acting contrary to wishes of the patient.

– If patient has Living Will and Medical POA, provisions of Living Will take priority.

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 27

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

RELATED MEDICAL DOCUMENTS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

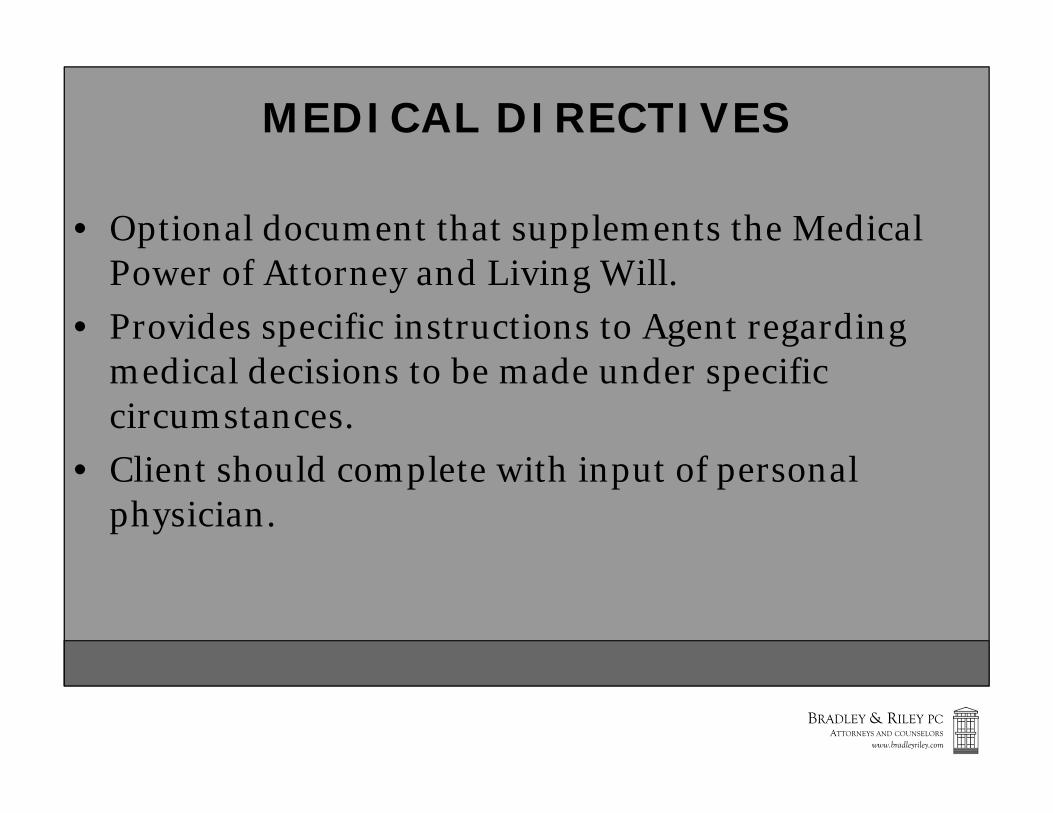

MEDICAL DIRECTIVES

• Optional document that supplements the Medical Power of Attorney and Living Will.

• Provides specific instructions to Agent regarding medical decisions to be made under specific circumstances.

• Client should complete with input of personal physician.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

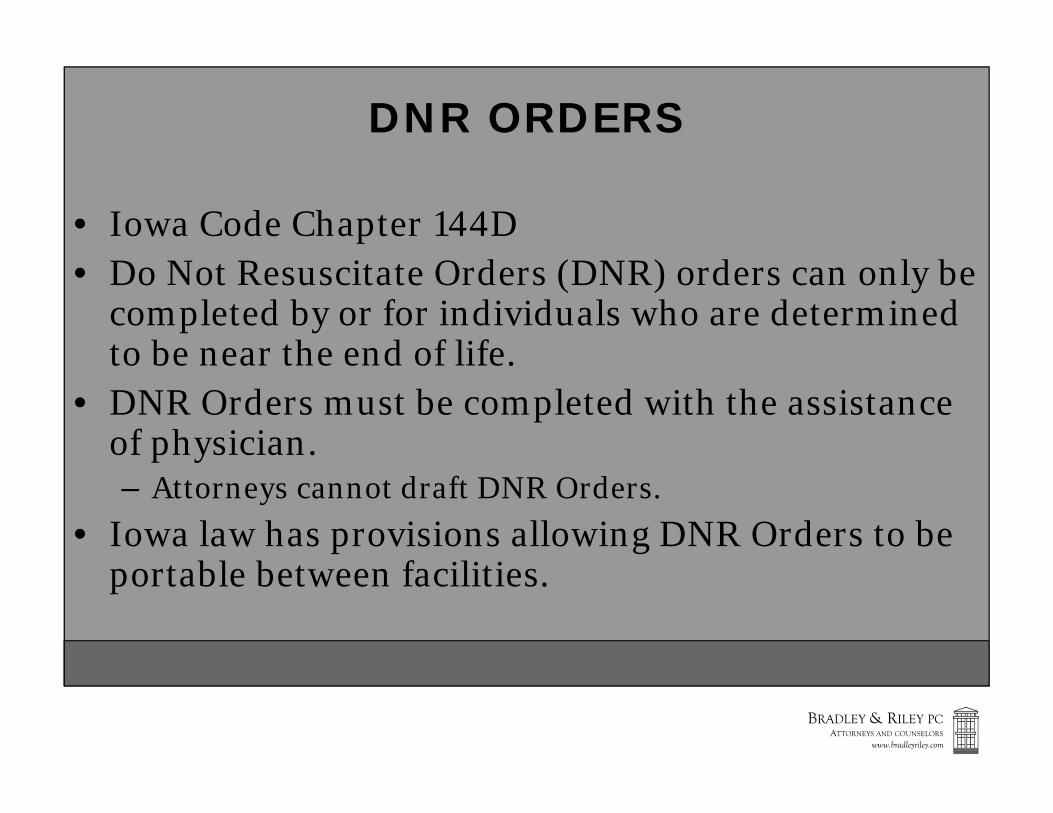

DNR ORDERS

• Iowa Code Chapter 144D• Do Not Resuscitate Orders (DNR) orders can only be

completed by or for individuals who are determined to be near the end of life.

• DNR Orders must be completed with the assistance of physician.– Attorneys cannot draft DNR Orders.

• Iowa law has provisions allowing DNR Orders to be portable between facilities.

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 28

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

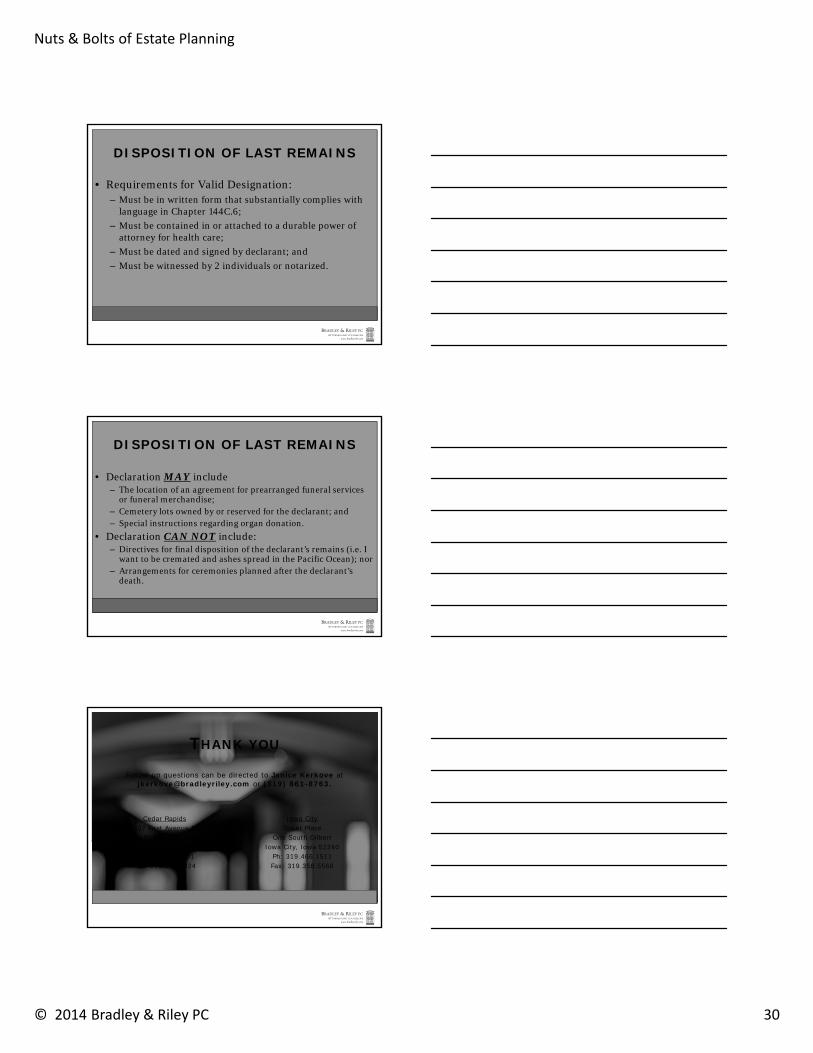

DISPOSITION OF LAST REMAINS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

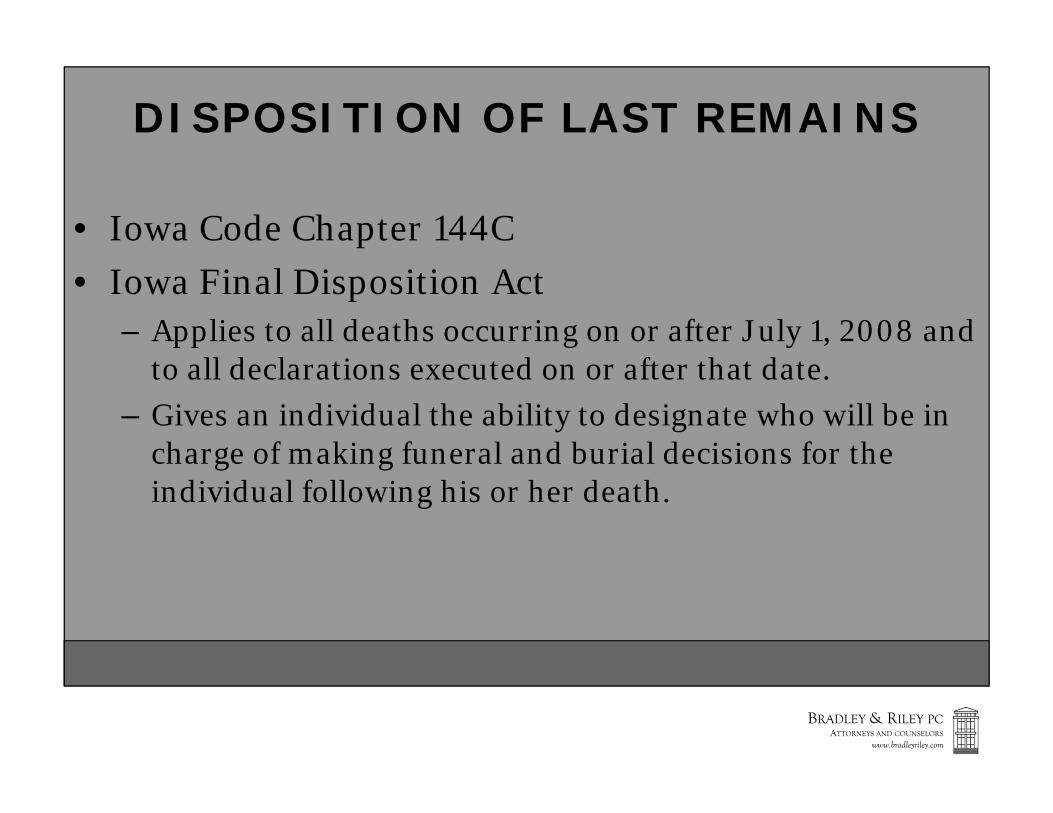

DISPOSITION OF LAST REMAINS

• Iowa Code Chapter 144C• Iowa Final Disposition Act

– Applies to all deaths occurring on or after July 1, 2008 and to all declarations executed on or after that date.

– Gives an individual the ability to designate who will be in charge of making funeral and burial decisions for the individual following his or her death.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

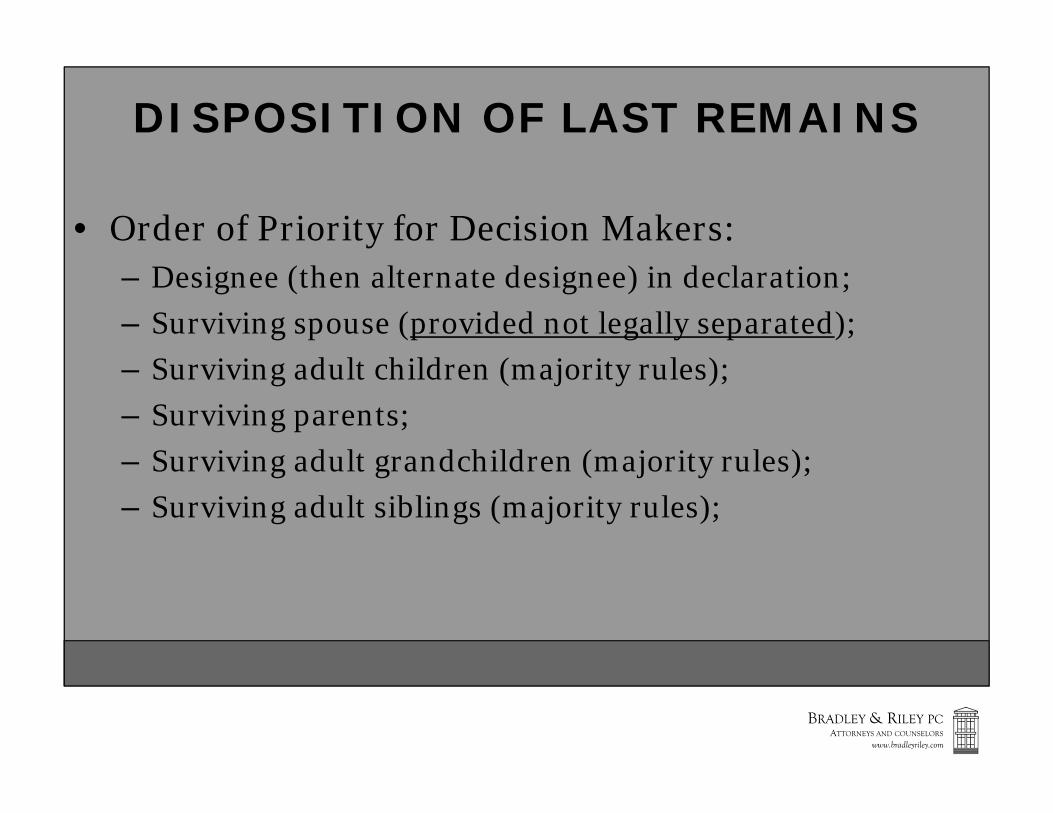

• Order of Priority for Decision Makers:– Designee (then alternate designee) in declaration;– Surviving spouse (provided not legally separated);– Surviving adult children (majority rules);– Surviving parents;– Surviving adult grandchildren (majority rules);– Surviving adult siblings (majority rules);

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 29

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

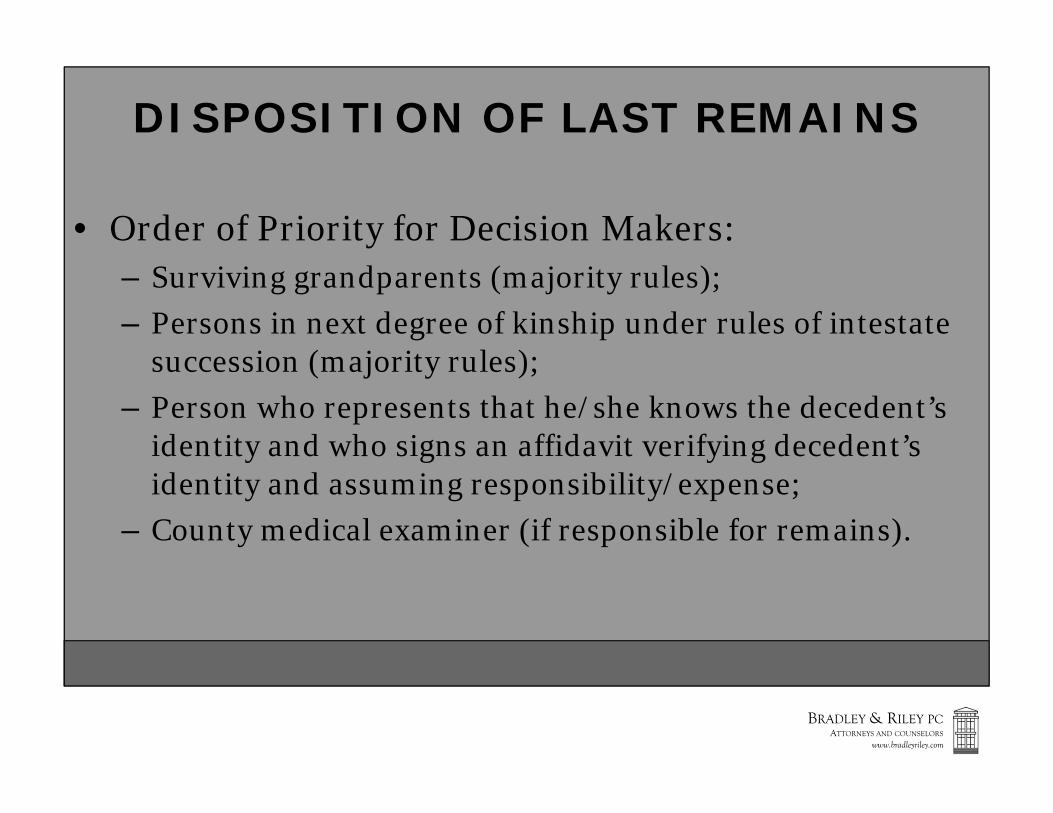

DISPOSITION OF LAST REMAINS

• Order of Priority for Decision Makers:– Surviving grandparents (majority rules);– Persons in next degree of kinship under rules of intestate

succession (majority rules);– Person who represents that he/she knows the decedent’s

identity and who signs an affidavit verifying decedent’s identity and assuming responsibility/expense;

– County medical examiner (if responsible for remains).

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

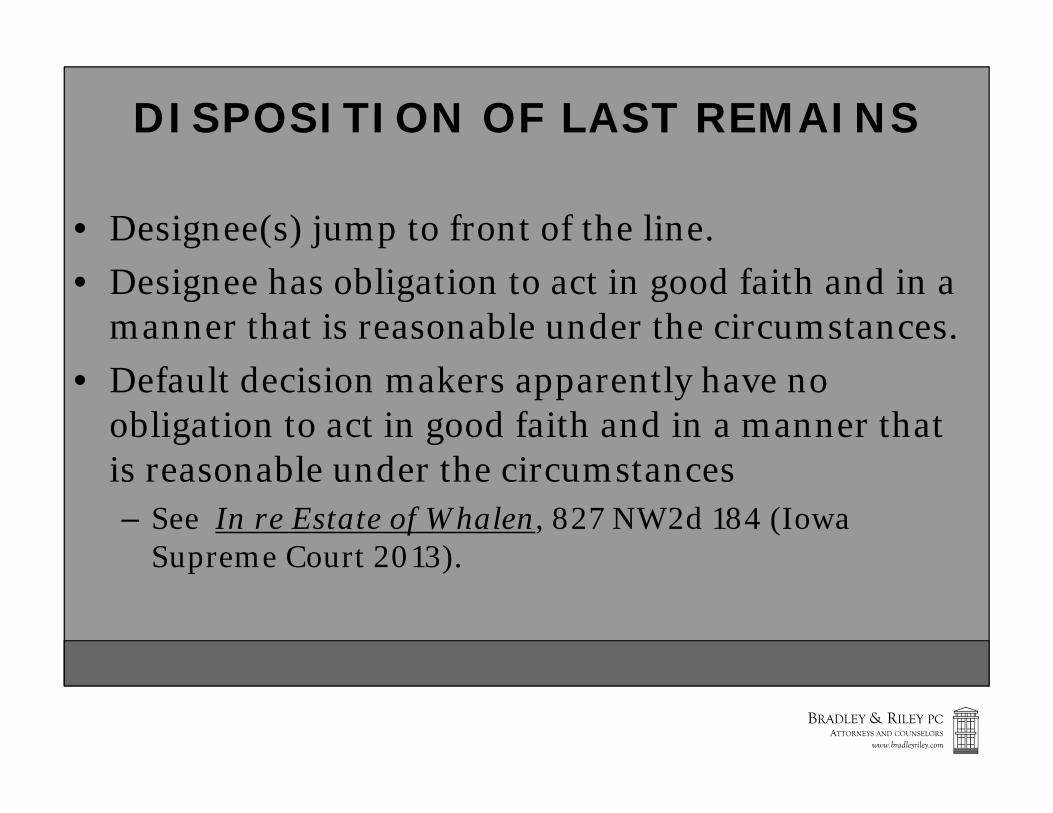

• Designee(s) jump to front of the line.• Designee has obligation to act in good faith and in a

manner that is reasonable under the circumstances. • Default decision makers apparently have no

obligation to act in good faith and in a manner that is reasonable under the circumstances– See In re Estate of Whalen, 827 NW2d 184 (Iowa

Supreme Court 2013).

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

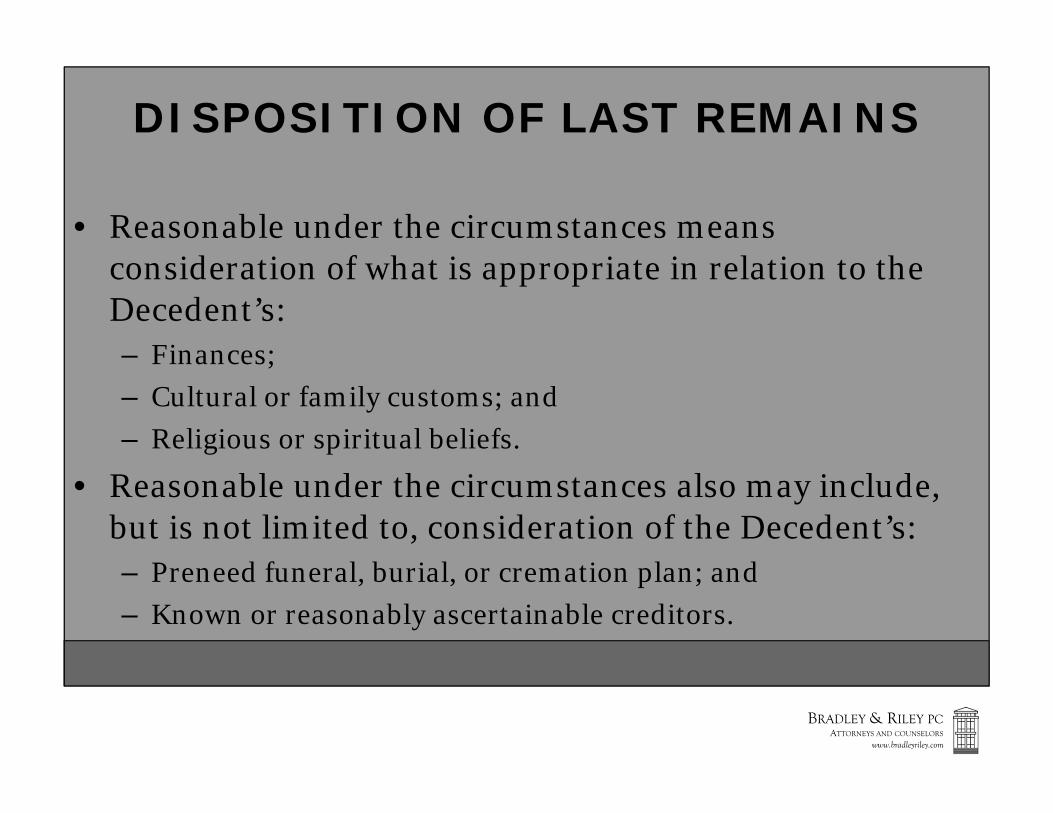

• Reasonable under the circumstances means consideration of what is appropriate in relation to the Decedent’s:– Finances;– Cultural or family customs; and– Religious or spiritual beliefs.

• Reasonable under the circumstances also may include, but is not limited to, consideration of the Decedent’s:– Preneed funeral, burial, or cremation plan; and– Known or reasonably ascertainable creditors.

Nuts & Bolts of Estate Planning

© 2014 Bradley & Riley PC 30

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

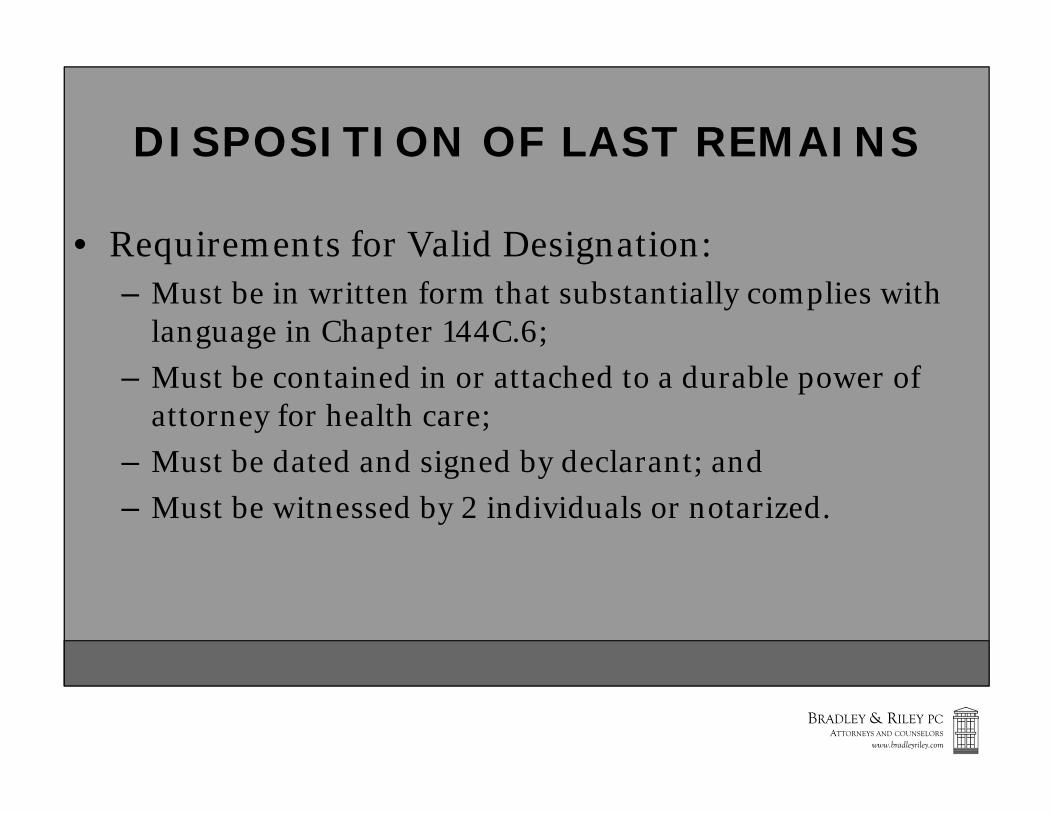

• Requirements for Valid Designation:– Must be in written form that substantially complies with

language in Chapter 144C.6;– Must be contained in or attached to a durable power of

attorney for health care;– Must be dated and signed by declarant; and– Must be witnessed by 2 individuals or notarized.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

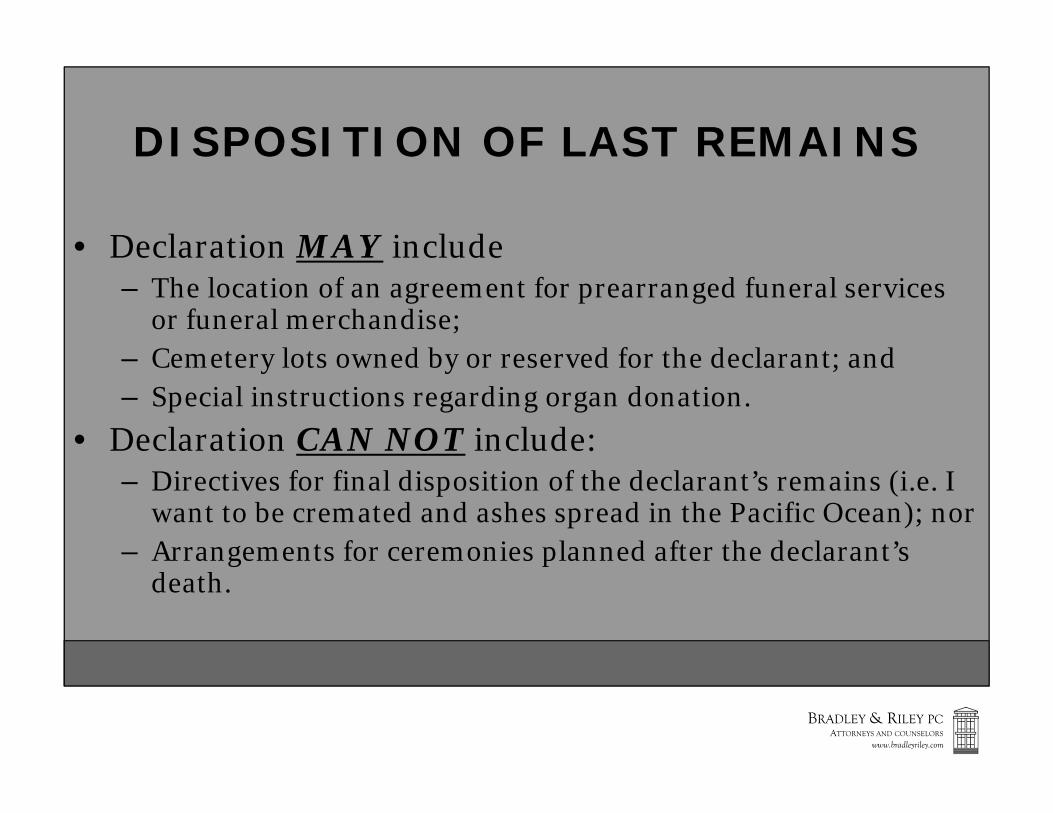

DISPOSITION OF LAST REMAINS

• Declaration MAY include– The location of an agreement for prearranged funeral services

or funeral merchandise;– Cemetery lots owned by or reserved for the declarant; and– Special instructions regarding organ donation.

• Declaration CAN NOT include:– Directives for final disposition of the declarant’s remains (i.e. I

want to be cremated and ashes spread in the Pacific Ocean); nor– Arrangements for ceremonies planned after the declarant’s

death.

Cedar Rapids2007 First Avenue SE

PO Box 2804Cedar Rapids, Iowa 52406

Ph: 319.363.0101Fax: 319.363.9824

Iowa CityTower Place

One South GilbertIowa City, Iowa 52240

Ph: 319.466.1511 Fax: 319.358.5560

THANK YOU

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

Follow up questions can be directed to Janice Kerkove at [email protected] or (319) 861-8763.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

ESTATE PLANNING –IT’S MORE THAN JUST A WILL

• Last Will & Testament• Revocable Trust (optional)• Asset Titling• Beneficiary Designations• Financial Power of Attorney• Medical Power of Attorney• Living Will• Declaration re: Last Remains

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

CREATE A GOOD DATA SHEET

• Personal information for clients & their children– Identify any beneficiaries with special issues– Identify children vs. step-children

• Financial information– How is the asset titled?– Is there a beneficiary designation?

• Identify who is to fill various fiduciary roles

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

CREATE A GOOD DATA SHEET

• Any obligations under a prenuptial agreement?• Any obligations under a dissolution decree?• Any significant future inheritances? • Is there genetic reproductive material in storage?• Do they want to give someone control over their

digital assets?

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FEDERAL ESTATE TAXES

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FEDERAL ESTATE TAX ISSUES

• Internal Revenue Code §§2001 – 2801

• Federal estate taxes based on value of estate

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FEDERAL ESTATE TAX ISSUES

• Federal estate tax exemption currently $5.34 million (2014) for each taxpayer, indexed for inflation

• Federal estate tax exemption not used at first death can be transferred to surviving spouse– Requires timely filing of Federal 706 Estate Tax Return

• Large gifts made during lifetime decrease the federal estate tax exemption available at death

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA INHERITANCE TAXES

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA INHERITANCE TAX ISSUES

• Iowa Code Chapter 450

• Taxes based on the relationship between decedent & recipient & based on the value of Iowa assets received by the recipient

• Gross estates of less than $25,000 exempt from Iowa inheritance taxes

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA INHERITANCE TAX ISSUES

• Lineal descendants & lineal ascendants exempt• Brother, sister, daughter-in-law, son-in-law subject

to tax starting at 5% and ending at 10% marginal rate

• Niece, nephew, other relatives, friends subject to tax starting at 10% and ending at 15% marginal rate

• Step-children are exempt, step-grandchildren are not exempt from Iowa inheritance taxes

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA INHERITANCE TAX ISSUES

• Certain assets are exempt from Iowa inheritance tax– Life insurance paid to a named beneficiary (not estate)– IRA & qualified plan assets paid to a named beneficiary

who is subject to income tax – Non-Iowa assets

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IOWA RESIDENT WITH REAL ESTATE HOLDINGS IN OTHER STATES

• At least 15 states have decoupled from federal estate tax system– In those states, the state death tax exemption is fixed at an

amount that is lower than the current federal estate tax exemption

– Minnesota, Illinois, Indiana, New York are a few of the states that have decoupled

• Iowa and at least 5 other states have inheritance taxes

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

WILLS VS. REVOCABLE TRUSTS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

WHAT TYPE OF DOCUMENT?

• Should client’s primary method of distributing assets be a Will or Revocable Trust?

• Will administration governed by Iowa Probate Code 633

• Trust administration governed by Iowa Trust Code 633A

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

WILL REVOCABLE TRUST• Cheaper to draft• Probate is required

– Code establishes 2% Atty/Exec Fees– Court Costs

• Will & Asset information part of public record– Bad for businesses that may need to

be sold as part of the proceeding• Does not take effect until death

– Need separate POA to deal with incompetency issues

– Can be difficult to obtain involuntary accounting from POA

• Court oversees process• Extensive case law as precedent

• More expensive to draft & fund• No probate required if all assets in

trust or have beneficiary designation at time of grantor’s death– Code establishes reasonable fee for

Atty/Exec– No Court Costs

• Maintains privacy of affairs• Easier transition for management of

affairs if client becomes incapacitated– Easier to obtain involuntary

accounting from Trustee than POA• Court involvement can be invoked if

necessary• Limited case law as precedent• Still need a Will

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

WILL VS. REVOCABLE TRUST

• Cost Benefit Analysis– Will the increased cost of drafting & funding a trust be

justified by the decreased costs of administration after the client’s death?

• Probate required in every state client has real estate– Timeshares are sometimes treated as real estate interest– Mineral interests (oil/gas) usually treated as real estate

interest

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

PROVISIONS OF LW&T

• Revoke prior Wills• Identify beneficiaries• Outline plan of distribution of assets• Outline plan for payment of administration expenses

& taxes• Designate fiduciaries • Draft for proper execution of the document

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IDENTIFY BENEFICIARIES

• List next of kin• Does the client want the list of beneficiaries to

include beneficiaries born after execution?• Does the client want the list of beneficiaries to

include adopted children?• Does the client want to exclude any beneficiaries?

– If yes, make that clear in the document

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

OUTLINE PLAN OF DISTRIBUTION

• Tangible personal property– Include option to leave separate writing– Include a plan for resolving disputes– Authorize Executor to donate/destroy items

• Special bequests– Charities – any limitations on how used?– Godchild, Special Friends, Grandchildren– Digital assets– Genetic materials in storage

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

OUTLINE PLAN OF DISTRIBUTION –RESIDUARY ESTATE IF SURV. SPOUSE

• Distribute outright to surviving spouse?• Hold in credit shelter trust for surviving spouse?

– Who is Trustee?– What are distribution standards?– Can distributions be made to any other beneficiaries?

• Hold in marital trust for surviving spouse?– Who is Trustee?– IRS requires mandatory distribution of net income to spouse– IRS requires that spouse be given right to turn non-income producing

property into income-producing property– Client decides on principal distribution standards for spouse– IRS mandates no one else is entitled to principal during spouse’s

lifetime

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

OUTLINE PLAN OF DISTRIBUTION –RESIDUARY ESTATE NO SURV. SPOUSE

• Distributed equally or some other percentage?• What happens if beneficiary dies?

– Balance to surviving members of group?– Balance to lineal descendants?

• Per stirpes vs. per capita

• Trust for any beneficiaries who may be minors at the time of inheritance

• Trusts for any beneficiaries who have special issues

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

OUTLINE PLAN FOR PAYMENT OFADMINISTRATION EXPENSES

• Consider liquidity issues– Does the probate estate have sufficient liquid assets to pay

mortgage, utilities, property taxes, attorney fees, executor fees, appraisal costs, funeral expenses, court costs, and other expenses of administration?

– Should a portion of life insurance be paid to estate to provide necessary funds?

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

OUTLINE PLAN FOR PAYMENT OFADMINISTRATION EXPENSES

• Who should be charged with administration expenses?– Default rule is administration expenses paid by residuary

unless document states otherwise– Residuary share vs. equitable allocation

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

OUTLINE PLAN FOR PAYMENT OF DEATH TAXES

• Who pays federal estate taxes– Default rules is tax paid by residuary share unless

document states otherwise– Residuary vs. equitable allocation

• Charities not subject to federal estate tax• Surviving spouse usually not subject to federal estate tax (if

document properly drafted)

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

OUTLINE PLAN FOR PAYMENT OF DEATH TAXES

• Who pays Iowa inheritance taxes– Default rule is beneficiary pays unless document states

otherwise• If Estate pays, adjustment required to “gross up” beneficiary’s

share for inheritance taxes paid by Estate

– Residuary vs. equitable allocation • What if beneficiary receiving non-probate asset?• What is beneficiary is receiving non-liquidate asset (real estate)?

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DESIGNATE FIDUCIARIES

• Guardians for minor children– Special considerations if naming married couples

• Trustees for any trusts created under LW&T– Specify powers granted to Trustees

• Executor of LW&T– Waiver of bond?– Power of sale?– Authority over digital assets?

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DRAFT FOR PROPER EXECUTION

• Client & two disinterested witnesses sign in the presence of each other

• Client, two disinterested witnesses, and notary sign Self-Proving Affidavit– If no self-proving affidavit, must find at least one of the

witnesses after date of death– If unable to find witnesses, then client died intestate

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

WHERE WILL ORIGINAL BE STORED?

• Very difficult to admit Will to probate if original document cannot be found– Law presumes that Will was revoked– Can only admit copy if presumption can be overcome

• Keep record of where client will be storing original– Lock box at __________ branch of ________ bank– Fireproof safe at office– Gun safe at home

• Generally do not have clients deposit with Clerk of Court

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

TITLING OF ASSETS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

TITLING ASSETS –JOINT TENANCY

• Joint tenancy with rights of survivorship vs. tenants in common ownership

• Joint tenancy ownership with rights of survivorship overrides terms of Will or Trust– Assets pass directly to the surviving joint tenant and are

never under the control of the Executor or Trustee

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

TITLING OF ASSETS –JOINT TENANCY

• If married couple has no federal estate tax concerns, assets can be held in joint tenancy to avoid probate at first spouse’s death

• If not a married couple or if there are federal estate tax concerns, joint tenancy ownership is not recommended

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

TITLING OF ASSETS –JOINT TENANCY WITH NON-SPOUSE

• Beware of titling assets jointly with non-spouses• Joint owner has immediate access to the joint

tenancy accounts – does not require client’s permission to withdraw funds

• Asset becomes subject to claims from their creditors, ex-spouse, etc.

• Asset automatically passes to surviving joint tenant -there is no legal obligation for joint tenant to share proceeds with other intended beneficiaries

• Can increase income tax liability when assets are sold in the future

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS

• Typically on Life Insurance, IRA’s, 401(k)’s, annuities, 403(b)’s, etc

• In Iowa (and most other states), the beneficiary designation overrides terms of Will or Trust

• Need to look at contract closely to determine what happens if the beneficiary predeceases client

• Be sure beneficiary designation complements plan of distribution under Will or Trust

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –ESTATE AS THE BENEFICIARY

• Provides liquid assets for payment of debts and expenses

• Provides funding for credit shelter trust if other assets are not sufficient

• May allow creditors to access proceeds• May subject proceeds to Iowa Inheritance Tax• May be included in calculating court costs, attorney

fees, etc.• May be adverse income tax consequences

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –SPOUSE AS BENEFICIARY

• Under old Iowa law, ex-spouse received proceeds if beneficiary designation was not changed after the divorce

• Iowa law now nullifies ex-spouse and ex-spouse’s family members as beneficiaries after a divorce – Only applies to non-ERISA assets– Must follow the appropriate notification procedures in Iowa

Code 598.20A before funds are paid out• Assets received by spouse under beneficiary

designation/joint tenancy do not count against spouse’s right to claim 1/3 of estate Iowa Code 633.238

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –MULTIPLE CHILDREN AS BENE’S

• Important to determine what happens if a child predeceases the owner

• Default plan rules usually call for distribution to the surviving children

• Most clients prefer that lineal descendants of deceased child take which requires adding of “per stirpes” language to the designation

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –TAX DEFERRED ASSETS

• Beneficiary designations on IRA’s or qualified plans should be properly drafted to provide beneficiary with flexibility to obtain maximum deferral/stretch for income tax purposes

• If client has charitable bequests, consider making the charities the beneficiaries of tax-deferred accounts as the charities will not pay income tax

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –POD/TOD

• POD designations used on bank accounts• TOD designations used on brokerage accounts,

savings bonds or stock – Iowa Code Chapter 633D• Cannot be used in Iowa for real estate holdings• Designates beneficiary who is to receive asset upon

death of owner - designation is revocable• Beneficiary has no rights to asset until client’s death

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

BENEFICIARY DESIGNATIONS –POD/TOD

• Asset passes to designee outside of probate• Beneficiary has no obligation to share with other

intended beneficiaries• Beneficiary may not be required to use funds for

funeral, burial, taxes, or other administration expenses

• If most assets pass by joint tenancy ownership or beneficiary designation, then no assets available for personal representative to pay administration expenses, including carrying costs of real estate, etc.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Designates Attorney-in-Fact to control assets and pay bills if client becomes incapacitated or needs assistance due to physical limitations.

• Avoids time and expense of court proceedings to establish and administer conservatorship.

• Help client choose carefully! Attorney-in-Fact has substantial power and limited supervision.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Iowa Uniform Power of Attorney Act (IUPOA)– Replaces existing Iowa Code Chapter 633B– Enacted as Senate File 2168– Signed by the Governor on April 10, 2014– Effective July 1, 2014

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Purpose of Uniform POA Act– Provide comprehensive guidelines for creation and use of

Powers of Attorney.– Prevent and address potential abuses of Powers of

Attorney.– Has currently been adopted in 15 states.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Non-Applicability of IUPOA– Acts completed by the Agent prior to July 1, 2014.– Powers of Attorney coupled with an interest of the agent in

the transaction that is the subject of the power (i.e. Limited POA given for the benefit of a creditor).

– Healthcare Power of Attorney.– Proxy or other delegation of voting rights or management

rights with respect to an entity.– Power created on a form prescribed by government,

governmental subdivision, governmental agency for a governmental purpose.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Applicability of IUPOA– Applies to all Financial POAs created on or after July 1,

2014.– Applies to all judicial proceedings concerning a power of

attorney commenced on or after July 1, 2014.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Applicability to prior documents/proceedings– Generally applies to POAs created before July 1, 2014,

unless otherwise provided in the Act. But see Iowa Code 633B.107, the meaning and effect of a POA created before July 1, 2014, is to be interpreted under the law that was in effect at the time the POA was created

– Generally applies to judicial proceedings commenced before July 1, 2014, unless court finds that application of the IUPOA would substantially interfere with conducting the proceedings or the rights of interested persons.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Validity of Documents under IUPOA– POAs executed on or after July 1, 2014, are valid if

executed in compliance with IUPOA.• Must be notarized

– POAs executed before July 1, 2014, are valid if execution complied with state law in effect at the time of execution.

• Notarization was not required, but commonly practiced

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Old Iowa POA Law– Very little statutory law in Iowa.– Agent referred to as Attorney-in-Fact.– Document contained a laundry list of transactions Agent

was authorized to transact.– Notarization was typically used, but not required.– Iowa Bar Form was typically used, but not required.– Affidavit procedure used for agent to verify their authority.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• New Iowa UPOA Law– Now have comprehensive statutory law in Iowa.– Agent now referred to as Agent.– Comments to the Uniform Act and cases decided in other states

who have adopted the Uniform Act will be helpful guidance.– Laundry list of transactions no longer required, refer to the

statute to confirm Agent’s authority.– Notarization is now required.– Certification procedure now used for Agent to verify their

authority.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Agent can be granted General Authority by:– Granting Agent general authority to do all acts that

principal could do pursuant to Iowa Code §633B.201– Incorporating by reference the provisions set forth in

§633B.204 - §633B.217– Providing detailed itemization of the authority granted

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Grant of General Authority includes:– §633B.204 Real Property.– §633B.205 Tangible Personal Property.– §633B.206 Stocks and Bonds.– §633B.207 Commodities and Options.– §633B.208 Banks & Other Financial Institutions.– §633B.209 Operation of Entity or Business.– §633B.210 Insurance & Annuities.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Grant of General Authority includes:– §633B.211 Estates, Trusts & Other Beneficial Interests.– §633B.212 Claims & Litigation.– §633B.213 Personal & Family Maintenance.– §633B.214 Governmental Benefits, Civil & Military Service

Benefits.– §633B.215 Retirement Benefits.– §633B.216 Taxes.– §633B.217 Gifts.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Grant of General Authority not sufficient for all transactions.

• Agent may not perform certain transactions, as set forth in Iowa Code §633B.201 unless:– POA expressly grants the authority– Exercise of such authority is not prohibited by another

statute, agreement or instrument

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Specific Authority expressly required for the following:– Create, amend, revoke, terminate Revocable Trust.– Make a gift in excess of federal annual exclusion amount.– Create or change rights of survivorship.– Create or change beneficiary designation.– Delegate authority granted under POA.– Waive principal’s right to joint and survivor annuity.– Exercise fiduciary powers that principal has authority to

delegate.– Disclaim property, including a power of appointment.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Even if Specific Authority expressly granted, an agent who is not closely related to the principal may not directly or indirectly create in the agent an interest in the principal’s property by gift, right or survivorship, beneficiary designation, disclaimer, or otherwise

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Powers of Co-Agents– Under old Iowa law, Co-Agents required to act in concert

unless document specifically specified otherwise.– Under UIPOA, majority of Co-Agents are authorized to act

on behalf of principal unless document specifies otherwise

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Nomination of Guardian & Conservator– Under old Iowa law, nomination of Guardian &

Conservator was completed through separate standby Petitions.

– Under new IUPOA, standby Guardians and Conservators may also be nominated in the Financial Power of Attorney document.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Accounting of Agent’s Acts– Under old Iowa law, accounting could only be obtained by

principal, principal’s conservator or personal representative.– Under IUPOA 633B.114(8), accounting can be requested by

principal, principal’s conservator, another fiduciary acting for principal, a governmental agency having authority to protect welfare of principal, personal representative of deceased principal.

– Clients often to choose to name additional parties (i.e. children of principal) who are entitled to request an accounting

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Invoking Judicial Intervention– Under old Iowa law, judicial intervention could only be

obtained by principal, principal’s conservator or personal representative.

– Under IUPOA 633B.116, there is an extensive laundry list of interested persons who have authority to invoke court jurisdiction to construe a power of attorney or review an agent’s conduct

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

FINANCIAL POWER OF ATTORNEY

• Iowa Statutory Financial Power of Attorney Form can be found at §633B.301 and on Iowa Docs– Statutory form is not popular with practitioners and will likely

be revised in the future– Statutory form does not lend itself to automated generation of

documents– Statutory form should only be used in very simple situations

• Agent’s Certification Form can be found at §633B.302 .

• These forms are not mandatory and may be revised as necessary.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

• Life-Sustaining Procedures Act• Iowa Code Chapter 144A

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

• Executed at any time by a competent adult.• Document must either be notarized or witnessed by

two adults.• Becomes effective if patient is in terminal condition

and is unable to make their own medical decisions.• Provides directions on use or withdrawal of life-

sustaining procedures.• May be revoked at any time, without regard to

mental or physical condition.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

• Definition of Terminal Condition– Incurable or irreversible condition that, without

administration of life-sustaining procedures, will, in the opinion of the attending physician, result in death within a relatively short period of time.

– State of permanent unconsciousness from which, to a reasonable degree of medical certainty, there can be no recovery.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

• Definition of Life-Sustaining Procedures– Any medical procedure, treatment, or intervention,

including resuscitation, which utilizes mechanical or artificial means to sustain, restore or supplant a spontaneous vital function, and when applied to a patient in a terminal condition, would only serve to prolong the dying process.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

• Witnesses to Living Will– Signed by 2 adult witnesses in the presence of each other

and the declarant.– At least one witness must be unrelated (not a relative by

blood, marriage, or adoption within the third degree of consanguinity).

– Attending physician and employees of the attending physician cannot serve as witness.

• Prefer use of notary instead of 2 witnesses to avoid increased chance of litigation.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

• Applicability of Living Will– Attending physician concludes that patient is in a terminal

condition.– Diagnosis is confirmed by another physician.– Notation is made in medical record that Living Will is now

applicable.– Effectiveness delayed if patient is pregnant with fetus that

could develop to point of live birth with continued application of life-sustaining procedures.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

LIVING WILL

• Old Living Will– Definition of life-sustaining procedures changed on April

23, 1992.– After that date, definition of life-sustaining procedures

includes hydration and nutrition administered through IV or NG tube.

– Living Will documents signed prior to April 23, 1992, do not allow the withdrawal of food and water provided through artificial means.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

WHAT IF NO LIVING WILL?

• No presumption for or against life-sustaining procedures based on failure to execute Living Will.

• Must be consultation and written agreement between attending physician and alternate decision makers who must be guided by the express or implied intentions of patient.

• If legal guardian has been appointed for the patient, court order is required prior to withdrawal of life-sustaining procedures.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

IF NO LIVING WILL –ALTERNATE DECISION MAKERS

1st: Person designated under health care POA.2nd: Legal guardian of patient.3rd: Spouse of patient.4th: Adult children (majority of children who are

reasonably available for consultation).5th: Parents of patient.6th: Adult siblings of patient.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEYDURABLE POA FOR HEALTH CARE

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEYDURABLE POA FOR HEALTH CARE

• Iowa Code Chapter 144B

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEY

• Designates another person as agent to make health care decisions when patient is no longer able to make those decisions on their own.

• Takes effect when patient can no longer make their own medical decisions.

• Covers more situations than Living Will.• Can be revoked at any time, without regard to

mental or physical condition.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEY

• Requirements for Validity:– Written designation.– Explicitly authorizes agent to make health care decisions. – Notarized or signed by 2 witnesses.– Same witness limitations as described for Living Will.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEY

• Ineligible Decision Makers under Medical POA:– Attending physician cannot serve as agent.– Employee of the attending physician cannot serve as

agent, unless the individual is related to patient by blood, marriage, or adoption within the 3rd degree of consanguinity.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEY

• Legal Effect of Designation:– Designated agent has authority to make decisions if

principal is unable, in the judgment of attending physician, to make their own health care decision.

– Designated agent has duty to act in accordance with desires of the patient as expressed in the Medical POA or otherwise made known to agent at any time.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL POWER OF ATTORNEY

• Legal Effect of Designation:– If patient’s desires are unknown, agent has duty to act in

the best interests of the patient, taking into account the patient’s overall medical condition and prognosis.

– Agent can be removed if district court determines that agent is acting contrary to wishes of the patient.

– If patient has Living Will and Medical POA, provisions of Living Will take priority.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

RELATED MEDICAL DOCUMENTS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

MEDICAL DIRECTIVES

• Optional document that supplements the Medical Power of Attorney and Living Will.

• Provides specific instructions to Agent regarding medical decisions to be made under specific circumstances.

• Client should complete with input of personal physician.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DNR ORDERS

• Iowa Code Chapter 144D• Do Not Resuscitate Orders (DNR) orders can only be

completed by or for individuals who are determined to be near the end of life.

• DNR Orders must be completed with the assistance of physician.– Attorneys cannot draft DNR Orders.

• Iowa law has provisions allowing DNR Orders to be portable between facilities.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

• Iowa Code Chapter 144C• Iowa Final Disposition Act

– Applies to all deaths occurring on or after July 1, 2008 and to all declarations executed on or after that date.

– Gives an individual the ability to designate who will be in charge of making funeral and burial decisions for the individual following his or her death.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

• Order of Priority for Decision Makers:– Designee (then alternate designee) in declaration;– Surviving spouse (provided not legally separated);– Surviving adult children (majority rules);– Surviving parents;– Surviving adult grandchildren (majority rules);– Surviving adult siblings (majority rules);

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

• Order of Priority for Decision Makers:– Surviving grandparents (majority rules);– Persons in next degree of kinship under rules of intestate

succession (majority rules);– Person who represents that he/she knows the decedent’s

identity and who signs an affidavit verifying decedent’s identity and assuming responsibility/expense;

– County medical examiner (if responsible for remains).

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

• Designee(s) jump to front of the line.• Designee has obligation to act in good faith and in a

manner that is reasonable under the circumstances. • Default decision makers apparently have no

obligation to act in good faith and in a manner that is reasonable under the circumstances– See In re Estate of Whalen, 827 NW2d 184 (Iowa

Supreme Court 2013).

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

• Reasonable under the circumstances means consideration of what is appropriate in relation to the Decedent’s:– Finances;– Cultural or family customs; and– Religious or spiritual beliefs.

• Reasonable under the circumstances also may include, but is not limited to, consideration of the Decedent’s:– Preneed funeral, burial, or cremation plan; and– Known or reasonably ascertainable creditors.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

• Requirements for Valid Designation:– Must be in written form that substantially complies with

language in Chapter 144C.6;– Must be contained in or attached to a durable power of

attorney for health care;– Must be dated and signed by declarant; and– Must be witnessed by 2 individuals or notarized.

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

DISPOSITION OF LAST REMAINS

• Declaration MAY include– The location of an agreement for prearranged funeral services

or funeral merchandise;– Cemetery lots owned by or reserved for the declarant; and– Special instructions regarding organ donation.

• Declaration CAN NOT include:– Directives for final disposition of the declarant’s remains (i.e. I

want to be cremated and ashes spread in the Pacific Ocean); nor– Arrangements for ceremonies planned after the declarant’s

death.

Cedar Rapids2007 First Avenue SE

PO Box 2804Cedar Rapids, Iowa 52406

Ph: 319.363.0101Fax: 319.363.9824

Iowa CityTower Place

One South GilbertIowa City, Iowa 52240

Ph: 319.466.1511 Fax: 319.358.5560

THANK YOU

BRADLEY & RILEY PCATTORNEYS AND COUNSELORS

www.bradleyriley.com

Follow up questions can be directed to Janice Kerkove at [email protected] or (319) 861-8763.