Embed Size (px)

Citation preview

2015 AFPTransaction Banking SurveyREPORT OF SURVEY RESULTS

Underwritten by

KEY FINDINGS

2015 AFP Transaction Banking Survey

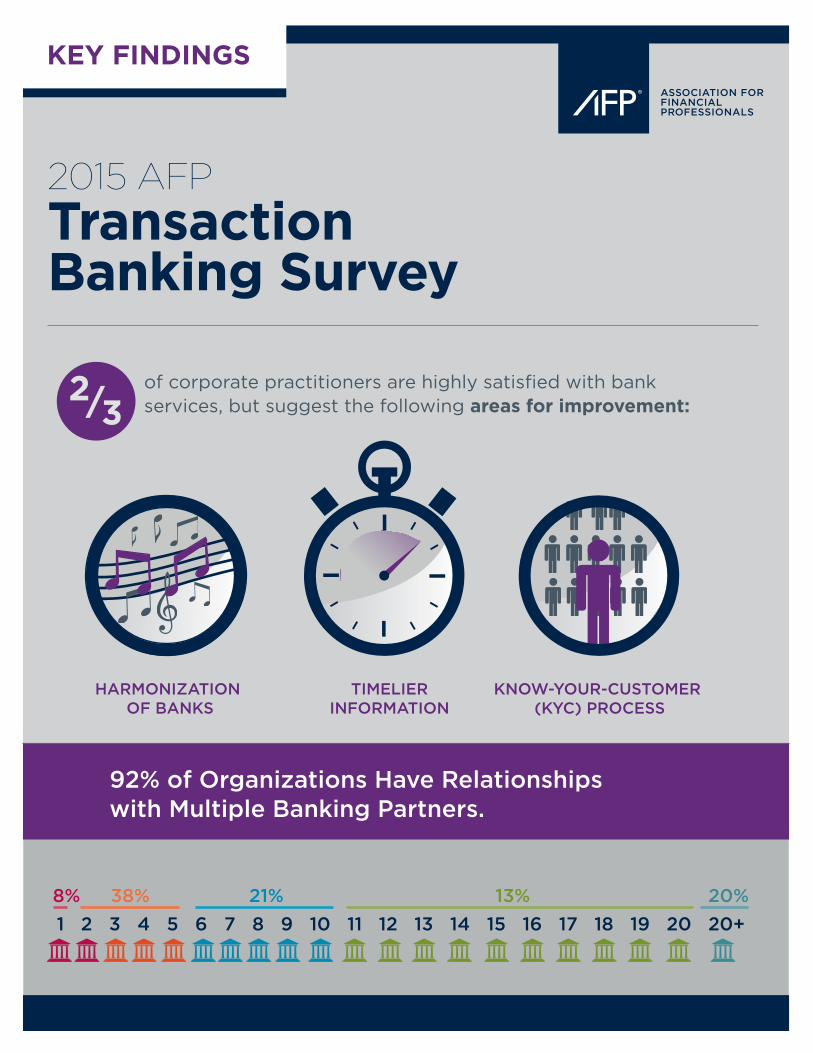

of corporate practitioners are highly satisfied with bank services, but suggest the following areas for improvement:

HARMONIZATION OF BANKS

TIMELIERINFORMATION

KNOW-YOUR-CUSTOMER (KYC) PROCESS

2/3

92% of Organizations Have Relationships with Multiple Banking Partners.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 20+8% 38% 21% 13% 20%

Association for Financial Professionals

4520 East-West Highway, Suite 750

Bethesda, MD 20814

Phone 301.907.2862

Fax 301.907.2864

www.AFPonline.org

2015 AFP

Transaction Banking SurveyREPORT OF SURVEY RESULTS

September 2015

Underwritten by

Transaction banking has been a major growth driver for banks over the last five years, yet this growth has often been impeded by heightened competition, changing corporate treasurer expectations, and the impact of new regulations. Leading banks are keeping a keen eye on what is happening in the transaction banking market and evaluating their business and IT priorities accordingly.

For the third consecutive year, CGI is pleased to sponsor the Association for Financial Professionals® 2015 Transaction Banking Survey to help support banks’ growth strategies. This influential survey provides detailed insight into the transaction banking industry through the eyes of corporates and their bank service providers. It examines the needs and challenges of corporates, and also investigates the bank-to-corporate relationship from end-to-end.

The 2015 survey reveals another year of changing market dynamics, with nearly 50 percent of corporate respondents indicating they are looking to review or renegotiate their current bank partner relationships, despite high levels of corporate treasurer satisfaction. Regulatory changes, cash management and associated payments, FX, and open account services are driving this re-evaluation, as well as experimentation with non-bank providers. This is especially true with mid-tier corporates ($500k-$4.9bn in revenue).

Banks are taking note of this willingness to experiment outside the banking industry. One in three corporate respondents are open to looking at various new non-bank alternatives, including non-bank payment networks (38 percent), mobile wallet or similar providers (35 percent), and third-party know your customer (KYC) solution providers (30 percent).

Paradoxically, 58 percent of corporate treasurers haven’t changed their existing portfolio of financial relationships (33 percent of corporates have 11 or more relationships), citing financial stability and long-term strategic support as key reasons. However, there is a strong desire to consolidate relationships to drive economies of scale.

While many banks offer single-bank portals, corporates are looking to move to multi-bank portals due to increasing treasury department consolidation. There is a significant opportunity for banks to enhance their offer-ings by harmonizing standards among banks, offering real-time information and streamlining the KYC process.

Corporates are frustrated by the lack of consistent file formats and data standards, as well as IT testing costs among their various bank service providers. Their demands also reflect the rising importance of online and mobile services, with nearly 60 percent of corporates citing both as important criteria in selecting a bank.

Ultimately, developing and building strong partnerships with corporates is key to bank growth and success. Corporates desire a solid strategic partner with whom they can implement long-term successful solutions. It’s important for bank partners to make a conscientious effort to understand their corporate customers’ business and operations, so that the bank-to-corporate partnership can be elevated to the next level. Ninety-four percent of corporates agree with this view.

It is encouraging to see then, that when considering their future growth strategies 43 percent of bank respondents suggest that enhancing the customer experience is their top focus, ahead of cost efficiency (23 percent) and innovative offerings (24 percent). To execute any of these strategies, technology plays a key role, with both corporates and banks citing technology-based capabilities as a key determination factor in selecting a bank partner.

Improvements in standardization, access, and information delivery would lead to greater efficiencies and strengthen the bank-to-corporate relationship. Going forward, leading banks are also focusing on digital banking; offering multi-bank portals, value-add services and real-time payments is high on their IT agendas.

CGI is a global leader in providing business consulting, systems integration, outsourcing and software to wholesale banks around the world. We hope this report will provide you with useful insight into the transactional bank-to-cor-porate relationship and assist you when considering your future growth strategy. If you wish to discuss this research in more detail or learn more about how we can support you, please contact us at [email protected].

Penny HembrowVice-President, Global BankingCGI

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 1

2015 AFP Transaction Banking Survey

IntroductionOrganizations and their banking service providers share an important relationship.

Regardless of their size almost all companies perform tasks which include processing cash,

meeting payroll, and paying vendors and for other services. Larger companies may need

their banks to provide a host of services both domestically and internationally and thus

have greater expectations of their banking partners. While smaller organizations may make

fewer demands on their banks in terms of services and global reach, they might want more

of a partnership with their banks; in some instances companies may even expect their bank

relationship officers to take on the role of strategic consultants.

Transaction banking services, or transaction banking, has evolved and is continuing to

change in the wake of new regulations. Just this year several banks have pulled back on

some of their strategies; some have reduced staff in key divisions. Banks have also been

exiting businesses in various markets. Banks chartered in the UK have had the largest

impact on their clients’ treasury departments. As new rules under Basel III are introduced,

more changes are expected and transaction services will definitely be affected. Because

banks are changing their strategies, organizations’ Treasury departments around the world

are also actively pursuing alternative strategies, engaging new banking partners or

extending their current relationships as a result. The ultimate solution sounds simple:

prudent bank relationship management. But companies also need to be open to developing

relationships with banking providers that might not have been considered in the past.

In June 2015, the Association for Financial Professionals® (AFP) conducted a survey of

corporate practitioners to gauge their organizations’ level of satisfaction with their banking

service providers. Additionally, the survey assessed the number of banking relationships

maintained, factors considered when selecting banking partners, banking channels and

access preferences. The survey also reached out to banking service providers to assess the

barriers they are facing, the services they are providing, and to examine whether they have

a grasp of their clients’ expectations. The survey results and conclusions in this

2015 AFP Transaction Banking Survey Report are based on the responses of 269 corporate

practitioner subscribers and 515 banking service providers. Many of the companies and

banking service providers that participated in this survey have operations that span the

globe and conduct business across multiple regions. For more detailed demographic

information see page 30.

AFP thanks CGI for its underwriting support of the 2015 AFP Transaction Banking Survey.

The research department of the Association for Financial Professionals® designed,

implemented and analyzed survey results. AFP is solely responsible for the content of

this report.

2 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Client Experience/SatisfactionClient Overall Satisfaction The majority of organizations are satisfied with their banking partners’ services. Two-thirds

of finance professionals indicate they are satisfied with the services their organizations’

banks provide, rating bank services a “4” or “5” on a 5-point scale. The share is slightly

smaller than the 70 percent that held this view in last year’s survey.

There are minor differences in client satisfaction levels across company demographics.

The largest percentage of corporate practitioners rating their banking partner services highly

are from companies operating primarily in North America (72 percent). Still, nearly two-thirds

of finance professionals based in Asia Pacific (63 percent) and Western Europe (64 percent)

rate their companies’ banking partner services a “4 or 5” on a 5-point scale.

With economic disparities across regions, the various regulations in place and overall

business expectations, it is not surprising that in Western Europe and Asia Pacific com-

panies’ levels of satisfaction with their banks are slightly lower than for those in the U.S.

Negative interest rates in Europe are likely the primary driver for any dissatisfaction among

finance professionals in that region, especially if banking counterparts are passing the cost

of the European Central Bank’s (ECB) negative deposit rates along to their clients.

More than 2/3rds of finance professionals

are highly satisfied with

their banks’ servicesOverall Satisfaction with Service Provided by Main Banking Partners(Percentage Distribution of Corporate Practitioners Rating Service “4” or “5” on a 5-point scale)

Highly satisfied (4 or 5 rating)

Less than highly satisfied (1, 2 or 3 rating)68%

32%

Overall Satisfaction with Service Provided by Main Banking Partners(Percentage Distribution of Corporate Practitioners Rating Service “4” or “5” on a 5-point scale)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Very Satisfied (5) 16% 18% 17% 13% 16% 13% 13% 21% 13%

(4) 52 52 53 54 47 54 50 51 51

(3) 29 26 28 28 31 31 34 26 30

(2) 3 5 2 4 6 3 3 3 6

Not Satisfied at All (1) – – – – – – – – –

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 3

2015 AFP Transaction Banking Survey

Reviewing Banking Relationships While a slight majority of corporate practitioners (52 percent) participating in the survey

indicate their organizations are not going to review strategy with their main banking partners,

nearly half (48 percent) plan to do so. About one-fourth (23 percent) of companies are nego-

tiating banking contracts and 25 percent are either actively seeking new banking partners in

key areas or have plans to move their business accordingly.

While there is not much variance across organization demographics, a larger share of compa-

nies that operate primarily in North America are more inclined to maintain the status quo with

their banking partners than are those organizations in Asia Pacific and Western Europe.

Review of Strategic Relationship with Main Banking Partner (Percentage Distribution of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Renegotiating banking contracts 23% 24% 15% 28% 21% 25% 20% 20% 23%

Seeking new banking partners in key geographies 16 18 23 9 18 21 14 15 18

Will have to move business accordingly 9 6 8 13 11 8 11 8 9

Not reviewing strategy with main banking partners 52 52 54 51 49 46 54 56 50

Of those organizations with plans to assess their current strategic relationships with their

main banking partners, a majority are planning to focus on cash management (62 percent)

and payments (58 percent). Other product areas of concern are foreign exchange (FX,

including hedging) cited by 45 percent of corporate practitioners, open account (42 percent)

and trade finance (40 percent).

Again there are differences across company demographics. A greater share (79 percent)

of mid-size organizations—those with annual revenues between $500 million and

$4.9 billion—have plans to review cash management compared to the shares of their

counterparts at smaller (50 percent) and larger organizations (61 percent). Foreign exchange

is also on the list of products to be reviewed by a greater share of mid-size companies

(54 percent) than larger or smaller organizations (43 percent and 50 percent, respectively).

Results also differ depending on ownership type. Publicly traded companies are more

likely to spotlight cash management, payments, FX, depository services and pooling/net-

ting than are privately held organizations. On the flip side, privately held companies are

more likely than publicly traded ones to review trade finance and liquidity.

Although it is a product area of prime concern for companies in all three regions, cash

management is a focus for a larger share of North American companies (76 percent) than

those operating primarily in Asia Pacific (66 percent) or Western Europe (70 percent).

Conversely, foreign exchange (including hedging) is more likely to be cited as a product

under review by finance professionals representing those companies that operate primarily in

Asia Pacific (55 percent) and Western Europe (58 percent) than those from North America

(46 percent).

52% of corporate

practitioners do not

plan to review strategy

with their organizations’

banking partners

4 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Often due to regulatory changes, banks need to revise their balance sheets; thus many

cash management products are affected by those same regulatory changes. In addition,

many banks are eager to increase their share of the wallet with their corporate clients and

consequently corporate Treasury departments try to find ways to support their banking

service providers. Treasury departments may take a product-by-product approach and add

“best in class” products. Companies and their Treasury departments may also rely on a

consortium of banks rather than limiting their interactions with one bank or a few banking

partners. Other factors influencing a company’s need to review products or renegotiate a

banking relationship contract include changes in geographies (where companies are based)

or expanding operations into new markets.

Products Under Review(Percent of Corporate Practitioners Planning to Assess Current Relationships with their Main Banking Partners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Cash management 62% 50% 79% 61% 64% 59% 66% 76% 70%

Payments 58 57 61 61 61 56 61 58 58

FX (including hedging) 45 50 54 43 58 38 55 46 58

Open account (payables and receivables) 42 40 46 48 44 41 43 56 44

Trade finance (letters of credit, collections) 40 47 46 35 36 49 39 32 37

Credit 35 40 29 48 39 41 36 38 37

Depository services 32 37 32 30 33 23 27 32 28

Pooling/netting 31 27 39 43 44 28 43 38 44

Liquidity 29 40 32 17 22 33 36 32 28

Investment banking/capital markets 22 30 18 13 19 18 23 16 14

Forecasting 12 13 11 13 14 10 11 12 9

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 5

2015 AFP Transaction Banking Survey

Reliability of Non-Bank Services or New Technologies No single non-bank service or technology received a majority vote (more than 50%) from

corporate practitioner respondents. The three items considered most reliable by about

one-third of finance professionals are alternative (non-bank) payment networks (38 percent),

mobile wallet or similar providers (35 percent) and third party KYC (“know your customer”)

service providers (30 percent). One likely reason for these relatively low percentages is

that some of these services are industry specific. Additionally, KYC providers are relatively

recent entrants.

Products Under Review(Percent of Corporate Practitioners Planning to Assess Current Relationships with their Main Banking Partners)

Reliability of Non-Bank Services and New Technologies(Percent of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Alternative (non-bank) payment networks 38% 40% 32% 44% 37% 32% 33% 38% 31%

Mobile wallet or similar providers 35 42 26 44 24 43 32 36 35

Third party KYC service providers 30 30 29 30 34 28 37 23 27

Third party on-boarding service providers 24 19 32 30 41 19 29 20 35

Non-bank FX providers 24 28 24 22 22 28 26 26 33

NFC Enabled Mobile Pay 18 21 18 19 15 23 14 21 17

Cryptocurrencies 7 7 6 11 5 9 9 7 8

Block-chain or decentralized consensus ledgers 6 7 6 7 5 11 9 5 6

Other 4 2 6 7 10 2 5 3 6

Bank Growth Strategies When considering future growth strategies, 43 percent of banking service providers are moving

towards a global banking model while 27 percent have plans to adopt a regional model. Three

out of ten banks are considering a blended regional and global banking approach.

Half of banking service providers (51 percent) that participated in this survey plan to focus

on their customers’ experiences when considering their business growth strategies. Other

areas banks plan on emphasizing are cost efficiency and innovative offerings (each cited by

23 percent of bank respondents).

6 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

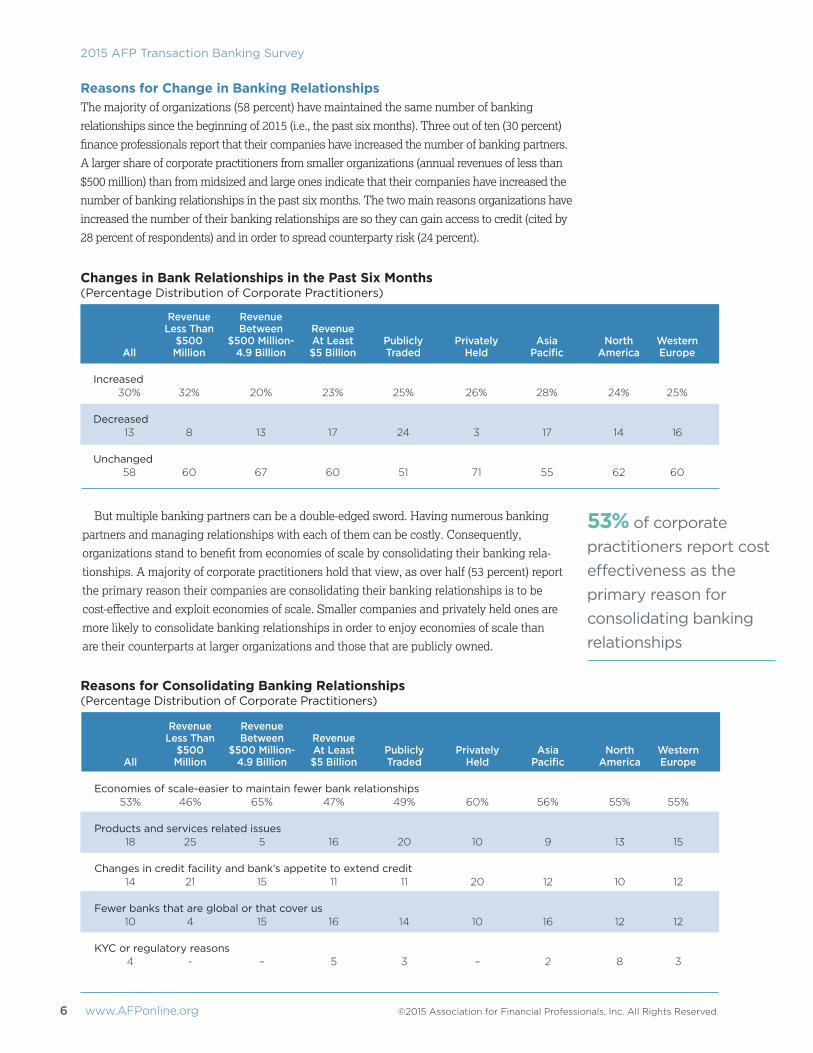

Reasons for Change in Banking Relationships The majority of organizations (58 percent) have maintained the same number of banking

relationships since the beginning of 2015 (i.e., the past six months). Three out of ten (30 percent)

finance professionals report that their companies have increased the number of banking partners.

A larger share of corporate practitioners from smaller organizations (annual revenues of less than

$500 million) than from midsized and large ones indicate that their companies have increased the

number of banking relationships in the past six months. The two main reasons organizations have

increased the number of their banking relationships are so they can gain access to credit (cited by

28 percent of respondents) and in order to spread counterparty risk (24 percent).

Changes in Bank Relationships in the Past Six Months(Percentage Distribution of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Increased 30% 32% 20% 23% 25% 26% 28% 24% 25%

Decreased 13 8 13 17 24 3 17 14 16

Unchanged 58 60 67 60 51 71 55 62 60

But multiple banking partners can be a double-edged sword. Having numerous banking

partners and managing relationships with each of them can be costly. Consequently,

organizations stand to benefit from economies of scale by consolidating their banking rela-

tionships. A majority of corporate practitioners hold that view, as over half (53 percent) report

the primary reason their companies are consolidating their banking relationships is to be

cost-effective and exploit economies of scale. Smaller companies and privately held ones are

more likely to consolidate banking relationships in order to enjoy economies of scale than

are their counterparts at larger organizations and those that are publicly owned.

Reasons for Consolidating Banking Relationships(Percentage Distribution of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Economies of scale-easier to maintain fewer bank relationships 53% 46% 65% 47% 49% 60% 56% 55% 55%

Products and services related issues 18 25 5 16 20 10 9 13 15

Changes in credit facility and bank’s appetite to extend credit 14 21 15 11 11 20 12 10 12

Fewer banks that are global or that cover us 10 4 15 16 14 10 16 12 12

KYC or regulatory reasons 4 - – 5 3 – 2 8 3

53% of corporate practitioners report cost effectiveness as the primary reason for consolidating banking relationships

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 7

2015 AFP Transaction Banking Survey

Client Overall Satisfaction with Specific Services Companies’ levels of satisfaction with specific services vary, although a majority of corporate

practitioners rate most services either a “4” or “5” on a 5-point scale. Payments and cash manage-

ment are the most highly rated, with 77 percent and 71 percent of finance professionals scoring

those services as a “4” or “5,” respectively. Those shares are significantly larger than in last year’s

survey in which 56 percent of respondents rated payments highly and 54 percent rated cash

management a “4” or “5.” Following closely behind are FX services (including hedging) with 69

percent of corporate practitioners rating it highly, credit and trade finance (68 percent), and liquid-

ity (66 percent).

Similar to results in last year’s survey, forecasting scored a “4” or “5” with the smallest share of

respondents—41 percent—although that share is much larger than the 22 percent last year. But this

result should not be surprising. Cash forecasting is unique to each company and the forecasting

process differs at each organization. With such unique structures in place, unless banking providers

are able to customize their forecasting services, it is likely that corporate practitioners will continue to

be less satisfied with this feature compared to others.

Satisfaction levels differ across organization demographics. Corporate practitioner respondents

from privately held companies are less satisfied with payments than are those from publicly traded

organizations (60 percent versus 75 percent). Smaller companies with annual revenues less than

$500 million are not as satisfied (60 percent) with the foreign exchange services provided by their

banks as are their counterparts at mid-sized organizations (73 percent) and larger organizations

(76 percent). Open account payables are rated higher by smaller organizations than larger ones.

Reasons for Consolidating Banking Relationships(Percentage Distribution of Corporate Practitioners)

Overall Satisfaction Provided by Main Banking Partners for Each Service(Percent of Corporate Practitioners Rating Service a “4” or “5” on a 5-point scale)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Payments 77% 79% 78% 73% 75% 60% 69% 67% 63%

Cash management 71 66 77 69 61 65 61 65 59

FX (including hedging) 69 60 73 76 71 75 71 79 65

Credit 68 68 74 64 71 71 74 73 67

Trade finance (letters of credit, collections) 68 65 70 71 68 56 62 63 62

Liquidity 66 65 63 64 38 41 43 35 45

Open account (payables and receivables) 62 67 59 60 73 54 69 67 73

Pooling/netting 61 50 64 75 63 54 63 63 64

Investment banking/capital markets 58 56 60 59 69 67 72 76 71

Forecasting 41 44 33 41 69 62 72 71 70

8 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Valuable Aspects in Relationship with Main Banking PartnersTo ensure a successful partnership, organizations and their banking service providers

need to develop and then foster a strong relationship. Banking partners need to make a

conscientious effort to understand their clients’ businesses and operations. That simple

approach can help move a company/bank partnership to a higher level.

A vast majority of corporate practitioners—94 percent—agree with that view. Many also

believe that it would be valuable if their bank providers acted as a strategic partner and

worked with companies on longer-term solutions (90 percent). Additionally, a similar share

of finance professionals (85 percent) indicate they would like to see their banks’ relation-

ship officers act as strategic consultants rather than simply sell them banking services.

These results validate the view that clients would like to work with their banks more

closely and view them as business partners rather than just banking service providers.

Ultimately, a successful company/bank relationship is one in which a banking partner

fully understands a client’s business; this allows an organization’s Treasury function to

focus on more strategic solutions rather than worry about educating banking partners on

how the business operates. A knowledgeable banking partner that understands a client’s

business becomes a true resource to Treasury and can provide more value-added services.

Valuable Aspects in Relationships with Main Banking Partners(Percent of Corporate Practitioners Rating the Level of Value a “4” or “5” on a 5-point scale)

Bank’s understanding of the organization’s business and operations

Bank acts as a strategic partner and works for longer term solutions

Relationship officer’s ability to not just sell the organization on products, but acts as a value-added consultant

Bank provides credit and/or unique capabilities

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

94%

90%

85%

77%

The vast majority of both corporate practitioners and banking service providers indicate that financial stability of the bank and strategic support are the most important factors when establishing a banking relationship

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 9

2015 AFP Transaction Banking Survey

Bank SelectionCorporate Practitioner Perspective Treasury professionals consider a number of factors when establishing a bank relationship.

The two most important criteria cited by a vast majority of respondents are:

• Financial stability of the bank (92 percent rating it either “4” or “5” on a 5-point scale)

• Selecting a provider that best supports the organization from a strategic standpoint

(91 percent)

Other factors considered important by a majority of respondents are technology platform

and capabilities (cited by 84 percent of respondents), selecting the best in class providers of

products (82 percent) and the global footprint of the bank (67 percent). Of least importance to

finance professionals is finding providers for services and then seeking credit to obtain them

(35 percent).

Factors Considered When Organizations Establish a Banking Relationship(Percent of Corporate Practitioners Rating the Level of Value a “4” or “5” on a 5-point scale)

Financial stability of the bank

Selecting a provider that best supports the organization from a strategic standpoint

Technology platform and capabilities

Selecting the best in class providers of products

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

92%

91%

84%

82%

Global footprint of the bank

Selecting the lowest cost providers of products

Historical relationship between the bank and the organization

Online and mobile service and product offerings

67%

66%

63%

59%

Allocating bank relationship services in proportion to credit supported

Finding providers for services and seeking to obtain credit from them

56%

35%

10 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Large organizations with annual revenues of at least $5 billion, publicly traded compa-

nies, and those with operations primarily in Asia Pacific and Western Europe are far more

likely than other organizations to consider the global footprint of the bank an important

factor when selecting a banking partner. This is understandable: larger companies and

those which are publicly traded are more likely to conduct business globally than are

smaller ones and those which are privately held. A larger share (66 percent) of finance

professionals from smaller companies with annual revenues less than $500 million cite the

historical relationship between the bank and the organization as an important factor when

starting a bank relationship than do finance professionals from mid-size (57 percent) and

larger organizations (54 percent).

Factors Considered when Establishing a Banking Relationship(Percent of Corporate Practitioners Rating the Level of Importance a “4” or “5” on a 5-point scale)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Financial stability of the bank 92% 90% 93% 93% 96% 89% 92% 96% 94%

Selecting a provider that best supports the organization from a strategic standpoint 91 90 90 98 99 86 95 91 89

Technology platform and capabilities 84 84 82 87 84 84 84 87 83

Selecting the best in class providers of products 82 75 90 79 83 79 85 84 81

Global footprint of the bank 67 55 57 79 80 68 80 69 77

Online and mobile service and product offerings 59 69 57 70 66 61 62 65 62

Selecting the lowest cost providers of products 66 65 62 61 70 52 65 60 61

Historical relationship between the bank and the organization 63 66 57 54 58 58 52 55 51

Allocating bank relationship services in proportion to credit supported 56 57 49 62 62 54 61 54 64

Finding providers for services and then seeking to obtain credit from them 35 45 27 32 33 36 36 26 33

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 11

2015 AFP Transaction Banking Survey

Banking Service Provider Perspective Banks should have a strong understanding of their client’s expectations in a banking

provider. The attributes that banking service providers indicate are important to their clients

when selecting a bank partner are similar to those cited by corporate practitioners. Those

include the top-two-ranked attributes: a bank’s financial stability and a bank that best

supports the organization from a strategic standpoint.

There are a few discrepancies between the two groups. For example, while two-thirds

(67 percent) of corporate practitioners report a bank’s global footprint is an important

selection criteria, 56 percent of banking service providers see this as an important

consideration when their clients choose a bank.

Factors Considered Important by Clients when Establishing a Banking Relationship(Percent of Banking Service Providers Rating the Level of Importance a “4” or “5” on a 5-point scale)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

92%

90%

84%

80%

74%

74%

64%

56%

Financial stability of the bank

Supports the organization from a strategic standpoint

Technology platform and capabilities

Selecting the best in class providers of products

Historical relationship between the bank and the organization

Allocating bank relationship services in proportion to credit supported

Online and mobile service and product offerings

Global footprint of the bank

Selecting the lowest cost providers of products

Finding providers for services and seeking to obtain credit from them

51%

42%

12 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Mobile Solutions Slightly more than half of corporate practitioners cite online and mobile services as

important criteria when selecting their bank. Banks are responding to that demand, with

the majority of banks offering such services in a variety of areas.

Two-thirds of banking service providers participating in the survey offer mobile solutions

to their corporate clients. An overwhelming majority of that two-thirds offer payments and

cash management solutions, 92 percent and 89 percent, respectively. Much smaller shares

of banking service providers have expanded their services in the areas of bank-assisted open

account, forecasting and approved payables finance.

Banks Offering Mobile Solutions for Corporate Clients(Percent of Banking Service Providers)

Payments

Cash management

FX

Trade finance

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

92%

89%

64%

58%

Liquidity

Pooling/netting

Integrated payables

Receivables finance

56%

48%

41%

38%

Integrated receivables

Forecasting

36%

28%

Bank-assisted open account

Approved payables finance (reverse factoring)

28%

25%

The vast majority

of mobile solutions

offered by banks

are payments and

cash management

solutions

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 13

2015 AFP Transaction Banking Survey

Product Areas Covered by Online or Mobile Banking Solutions (Percent of Banking Services Providers)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Asia North Western

All Million 4.9 Billion $5 Billion Pacific America Europe

Payments 92% 86% 97% 95% 97% 93% 96%

Cash management 89 86 92 93 89 90 90

FX 64 44 60 72 75 65 75

Trade finance 58 30 52 66 73 55 66

Liquidity 56 26 47 68 65 53 66

Pooling/netting 48 19 43 59 58 45 61

Integrated payables 41 19 25 56 53 48 48

Receivables finance 38 14 33 45 52 39 46

Integrated receivables 36 11 28 51 49 42 42

Bank-assisted open account 28 26 28 27 31 29 30

Forecasting 28 12 25 33 35 31 37

Approved payables finance (reverse factoring) 25 9 18 33 38 25 30

14 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Banking ActivityNumber of Banking PartnersThe number of banking partners with which organizations work regularly varies greatly. The

typical organization works with six to ten banks. Forty-six percent of organizations work with

one to five banks on a regular basis, one-third maintains relationships with six to 20 banks,

and 20 percent maintain relationships with 21 or more banks.

54% of organizations work with more than 5 banks on a regular basis

Number of Banks Organizations Work on a Regular Basis(Percentage Distribution of Corporate Practitioners)

1 bank

2-5 banks

6-10 banks

11-20 banks

21 or more banks

38%

8%

21%

13%

20%

Not surprisingly, smaller organizations tend to have far fewer banking relationships than

do larger companies. Seventy-four percent of organizations with annual revenues under $500

million work with five or fewer banks; only five percent have relationships with 21 or more

banks. In contrast, 36 percent of large organizations (those with annual revenues of at least

$5 billion) work with 21 or more banks and 26 percent from this group work with five or

fewer banks.

Number of Banks Organizations Work with on a Regular Basis(Percentage Distribution of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

1 8% 19% 3% – 1% 15% 3% 11% 3%

2-5 38 55 38 26 32 42 28 35 29

6-10 21 16 27 19 20 20 24 20 21

11-20 13 5 13 19 15 10 15 11 18

21+ 20 5 18 36 31 13 30 23 29

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 15

2015 AFP Transaction Banking Survey

Bank Accounts Maintained The typical organization maintains 26-75 bank accounts. That is well off the 76-149 bank

accounts maintained by the typical company last year. As with number of banking partners,

the number of bank accounts used or maintained by companies varies widely. One-fourth of

organizations have 10 or fewer accounts; 30 percent have 150 or more bank accounts.

An organization’s size plays a significant role in the number of bank accounts maintained.

Half of small organizations with annual revenues of less than $500 million have ten or fewer

bank accounts. Sixty-four percent of those with annual revenues of at least $5 billion have

150 or more accounts.

Number of Bank Accounts Used or Maintained(Percentage Distribution of Corporate Practitioners)

25%

20%

18%

30%

7%

1-10

11-25

26-75

76-150

More than 150

Number of Bank Accounts Used or Maintained(Percentage Distribution of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

1-10 25% 50% 7% 11% 10% 38% 13% 18% 9%

11-25 20 27 23 6 17 20 20 16 14

26-75 18 11 20 13 15 10 10 18 11

76-150 7 2 15 6 7 10 13 10 16

150+ 30 10 35 64 51 23 43 39 50

16 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Centralized Treasury Functions Banking relationships can be influenced by an organization’s Treasury structure; that is,

whether Treasury processes are centralized or decentralized. Services that are directly

impacted by an organization’s income statement are normally centralized; this allows for

greater control of complex services and the expertise in a centralized service function is

naturally more concentrated. Foreign exchange and risk management are the two most

commonly centralized services (at 71 percent and 69 percent of companies, respectively).

Cash pooling/netting, investment services and credit services are centralized in at least 60

percent of organizations.

Services that are more decentralized have a higher dependence on local knowledge of

particular markets where such services are provided. Accounts Receivable and Accounts

Payable are two examples of these types of decentralized services. Regional shared service

centers typically support these initiatives.

71%

69%

64%

63%

60%

53%

51%

51%

Centralized Treasury Functions(Percent of Corporate Practitioners)

FX

Risk management

Cash pooling/netting

Investment services

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Credit services

All payment services

Trade finance

Accounts payable

Accounts receivable

Channel management

48%

32%

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 17

2015 AFP Transaction Banking Survey

Centralization and Decentralization of Treasury Functions(Percent of Corporate Practitioners)

Decentralized/ N/A or Centralized Regionalized Do Not Use

FX 71% 16% 13%

Risk management 69 24 7

Cash pooling/netting 64 19 17

Investment services 63 22 15

Credit services 60 26 14

All payment services 53 44 3

Accounts payable 51 43 6

Trade finance 51 26 23

Accounts receivable 48 45 7

Channel management 32 26 42

18 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Banking ChannelsFinance professionals use a variety of channels to access their banking partners’ services.

Most common is the single integrated bank portal; 61 percent of corporate practitioner

respondents indicate that their organizations access services provided by at least one of their

banking partners via an integrated bank portal. Other channels include:

• multiple ports (separate channels for specific services at the bank) (cited by 36 percent

of corporate practitioner respondents)

• Treasury workstation or host-to-host (31 percent)

• via SWIFT solution (26 percent)

• mobile apps from a banking partner (13 percent)

• access bank information by either paper or fax (11 percent)

Having a single integrated bank portal is the more preferred choice of smaller organi-

zations and those that are privately held. Larger organizations and publicly traded ones

are far more likely to opt for Treasury workstations or host-to-host systems than are their

counterparts at smaller companies and privately held ones.

Channel Used When Connecting/Accessing Banks(Percent of Corporate Practitioners)

Single integrated bank portal

Multiple portals(separate channels for specific services at the same bank)

Treasury workstation or host-to-host

Via SWIFT solution

0% 10% 20% 30% 40% 50% 60% 70%

61%

36%

31%

26%

Mobile apps

Paper based/fax

13%

11%

61% of survey

respondents use

a single integrated

portal as

their preferred

banking channel

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 19

2015 AFP Transaction Banking Survey

Bank Access Treasury Workstation Fifty-three percent of organizations use Treasury work stations—and of those a little more

than half use an in-house/installed version and the remaining use a software service/ASP.

This is very similar to last year’s survey results in which 56 percent of corporate practitioner

survey respondents reported using a Treasury workstation.

Forty-one percent of companies are neither using a Treasury workstation nor do they

plan to install one in the near future. A very small share—six percent—does plan to install a

Treasury workstation within the next 12-18 months.

Channels Used to Connect/Access with Banks(Percent of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Single integrated bank portal 61% 68% 56% 53% 46% 68% 55% 64% 56%

Multiple portals (separate channels for specific services at the same bank) 36 32 44 38 41 38 38 41 44

Treasury workstation or host to host 31 10 34 57 45 22 45 34 48

Via SWIFT solution 26 20 20 36 37 21 38 28 34

Mobile apps 13 18 10 9 11 13 10 13 6

Paper based/fax 11 17 8 6 6 16 11 10 10

Use of a Treasury Workstation(Percentage Distribution of Corporate Practitioners)

29%

24%

41%

6%Yes—Implemented in-house/Installed version

Yes—As a software service/ASP

No—Currently not using a Treasury workstation

No—Plan to implement a Treasury workstation within the next 12-18 months

53% of

corporate

practitioners

use treasury

workstations

20 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

There are sharp differences in the use of Treasury workstations based on organization

demographics. Larger organizations (those with annual revenues of at least $5 billion) are

more than twice as likely as smaller ones (with annual revenues of less than $500 million) to

have Treasury workstations (75 percent versus 33 percent). Slightly more than half

(55 percent) of mid-size companies (those with annual revenues between $500 million -

$4.9 billion) have Treasury workstations. A greater share of publicly traded companies than

privately held ones use them (66 versus 41 percent). There are regional differences as well.

Larger shares of companies operating primarily in Asia Pacific (40 percent) or Western

Europe (38 percent) have Treasury workstations implemented in-house/installed versus their

counterparts at companies with operations primarily in North America (24 percent).

Building a business case for a Treasury workstation—justifying the cost and the

necessary IT support—are two major hurdles companies and their Treasuries often have

to overcome as they move from Excel to a Treasury workstation. This explains in part the

greater prevalence of Treasury workstations at larger companies. Those (larger)

organizations typically have more established policies and procedures. Consequently, their

Treasury functions (or senior management) are better able to justify the cost of a Treasury

workstation in order to minimize errors and adhere to compliance and controls. In addition,

the more global an organization the greater is the need for enhanced Treasury workstation

capabilities. Companies that operate in a variety of countries and across borders often

need a more customized solution than an off-the-shelf SaaS/ASP version can deliver.

Use of Treasury Workstation(Percentage Distribution of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Yes – Implemented in-house/Installed version 29% 23% 22% 45% 31% 30% 40% 24% 38%

Yes – As a software service/ASP 24 10 33 30 35 11 32 31 32

No, we are not using a Treasury workstation 41 61 38 21 27 52 27 41 27

No, but we plan on implementing a Treasury workstation within the next 12-18 months 6 6 7 4 7 7 1 4 4

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 21

2015 AFP Transaction Banking Survey

Preferred Bank AccessWhile a single integrated bank portal is the most commonly used form of bank access, the

use of a multi-bank portal—one portal providing shared access to multiple banks—is often

cited as a preferred form of access. Forty-five percent of corporate practitioners indicate

that their organizations prefer a multi-bank portal, 27 percent prefer single-sign on for each

bank to access all services, and only four percent prefer separate access/log in for specific

services at each bank. These results are comparable to those reported in last year’s survey:

41 percent of corporate practitioners preferred multi-bank portal access and 22 percent

preferred single sign-on access.

About half of both smaller companies with annual revenues of less than $500 million

(48 percent) and mid-size companies with annual revenues of between $500 million and

$4.9 billion (52 percent) favor access via a single portal providing shared access to multiple

banks. One-third of larger companies (with annual revenues of at least $5 billion) cite the

same preference.

There is a tradeoff between cost and bank agnostic solutions. Multi-bank portals are the

choice for many, but the downside is the banking provider will have visibility into all of the

bank activity that the portal utilizes. The advantage from an administrative standpoint is that

there is only one sign-on/token to manage. For some, this is a more cost-effective solution

than using a SWIFT connection which allows for more bank agnostic capabilities.

Preferred Bank Access Methods(Percentage Distribution of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Multi-bank portal (one portal providing shared access to multiple banks) 45% 48% 52% 34% 43% 51% 43% 43% 49%

Single sign-on for each bank to access all of the bank’s services 27 38 17 23 21 21 18 28 12

Via a SWIFT service bureau 10 3 12 19 14 9 17 13 20

Via SWIFT direct 8 5 5 11 13 4 8 6 6

Via SWIFT Alliance Lite2 6 2 9 9 6 7 8 4 7

Separate access/log in for specific services at each bank 4 5 3 4 3 6 5 4 4

Via other network providers 1 - 2 – – 1 1 2 1

22 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Types of Access to Bank Services Forty-five percent of finance professionals indicate they prefer multi-bank access and 39

percent of banking service providers are responding to that preference by providing their

clients with shared multi-bank portal access via online offerings. Two-thirds of banks are

offering their corporate clients mobile services and a similar percentage have the capability

of a single portal with access to all services. Fifty-four percent are offering their clients a

single sign-on feature. Larger banks (those with annual revenues of at least $5 billion) offer

their clients greater access to online offerings than do smaller ones.

Last year’s survey report noted that mobile services and the single-sign on capability

to access multiple banks were offered by 65 percent and 61 percent of banking providers,

respectively. This year’s survey results are similar: 41 percent of banking service providers

report offering their clients the shared multi-bank portal access.

Online and Mobile Services Provided for Corporate Clients (Percent of Banking Services Providers)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Asia North Western

All Million 4.9 Billion $5 Billion Pacific America Europe

Mobile 67% 52% 64% 75% 72% 70% 69%

Integrated (one portal for the bank with all services) 66 50 61 76 79 70 73

Single sign-on 54 37 49 66 60 66 63

Integrated (shared multi-bank portal access) 39 13 41 48 47 44 49

Separate sign-on (for specific services) 36 37 30 40 35 38 40

Do not provide online access 2 5 _ 1 1 _ 1

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 23

2015 AFP Transaction Banking Survey

Areas for ImprovementWhile a majority of corporate practitioners are satisfied with their banking partners’

services, they also believe there are opportunities for banks to improve their offerings.

Similar to results in last year’s survey, harmonization of standards between banks topped

the list; 58 percent of corporate practitioners cite this as an approach that would improve

their banking partners’ services. Still, that share is lower than the 67 percent reported last

year. More timely information and a streamlined KYC process ranked second and third

as those services corporate practitioners would like to see improved (cited by 54 and 51

percent of respondents, respectively).

Desired Areas of Improvement for Banks(Percent of Corporate Practitioners)

Harmonization of standards between banks

More timely information (e.g., real time instead of next day)

Streamlined KYC process

Payment (remittance) tracking and reconciliation

0% 10% 20% 30% 40% 50% 60%

58%

54%

51%

44%

Integration of data from many banks 44%

Improved ability to compare alternative services and prices (e.g., lending, factoring, swaps and other options)

Proactive guidance and advice

Greater support in service onboarding, including set-up and data input

38%

37%

34%

31%

SWIFT connectivity or being SWIFT capable

Additionalservices

24%

2%

Single entry of corporate data and preferences (for all services)

The most common

areas for improvements

cited by corporate

practitioners are

harmonization of

standards between

banks, more timely

information and

a streamlined

KYC process

24 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Why the consistent results regarding harmonization of standards? Various key services

require harmonization of standards between banks, such as enabling eBAM across a multi-

bank channel utilizing a single solution or utilizing bank billing standard formatted files.

These features are important as companies seek to have greater transparency in their bank

relationships to help manage costs, risk and maintain stronger bank relationships.

Over 80 percent of finance professionals from large organizations (those with annual

revenues of at least $5 billion) indicate that harmonization of standards between banking

providers is a top area for improvement. Those from smaller organizations (with annual rev-

enues of less than $500 million) consider harmonization a lower priority (46 percent).

Desired Areas of Improvements for Banks(Percent of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

Harmonization of standards between banks 58% 46% 52% 81% 68% 57% 63% 59% 68%

More timely information (e.g., real time instead of next day) 54 63 40 62 52 60 55 45 51

Streamlined KYC process 51 37 50 68 56 49 60 58 57

Integration of data from many banks 44 49 35 47 42 43 52 44 43

Payment (remittance) tracking and reconciliation 44 46 37 55 44 40 36 45 43

Single entry of corporate data and preferences (for all services) 38 37 38 38 32 42 43 38 39

Improved ability to compare alternative services and prices (e.g., lending, factoring, swaps, other options) 37 42 32 40 38 39 43 32 34

Proactive guidance and advice 34 33 32 34 25 36 34 31 32

Greater support in service onboarding, including set-up and data input 31 30 28 34 35 30 35 30 34

SWIFT connectivity or being SWIFT capable 24 30 17 23 24 27 27 21 22

Additional services 2 - 5 2 4 – 3 4 5

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 25

2015 AFP Transaction Banking Survey

ChallengesChallenges Faced When Integrating with a Bank for Cash Management ServicesPractitioners did highlight some challenges their organizations face when integrating with

a bank for cash management services. A majority of corporate practitioners cites file

formatting issues (57 percent) and the testing of IT procedures for bank services (52

percent) as the greatest constraints they face. A greater share of finance professionals from

large organizations (annual revenues of at least $5 billion) notes these two issues as

restrictions compared to respondents from smaller companies.

File formatting issues are greater obstacles for companies that operate primarily in North

America (62 percent) and Western Europe (61 percent) than for those in Asia Pacific

(51 percent). Publicly traded companies are more impacted by testing IT procedures for

bank services; 59 percent of finance professionals from these companies consider this a

challenge while 43 percent of those from privately held companies hold the same view.

When a company changes banks for certain cash management services, new file

protocols, delivery methods and security measures have to be tested. For instance, file

formatting is an issue for the majority of corporate practitioners due to the variability of

standards being utilized. At many organizations, there are different formats for delivery

utilizing the same standard. EDI—electronic data exchange—is an example of where the

standard can change based on the data format version utilized. Negotiating with the bank

on the file format is often when companies have to make concessions in the interest of

implementing a new solution. Testing this and other such services can add time to the

process in onboarding since the methods are typically different and require a company’s IT

support. It can often be a challenge to procure those IT resources.

Challenges Faced When Integrating with a Bank for Cash Management Services (Percent of Corporate Practitioners)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Publicly Privately Asia North Western All Million 4.9 Billion $5 Billion Traded Held Pacific America Europe

File formatting issues 57% 58% 51% 67% 54% 60% 52% 62% 61%

Testing IT procedures for bank services 52 38 47 67 59 43 63 55 60

Ease of implementation 41 46 35 43 37 45 41 42 42

KYC onboarding 37 25 40 48 43 34 51 43 48

Use of their security protocols 32 33 26 41 31 31 28 33 26

Differences between what was sold vs. what is to be implemented 30 29 21 46 38 28 35 25 32

Other 2 2 5 – – 6 2 2 3

Corporate practitioners

cite file formatting

issues and the testing

of IT procedures for

bank services as the

greatest constraints

they face

26 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

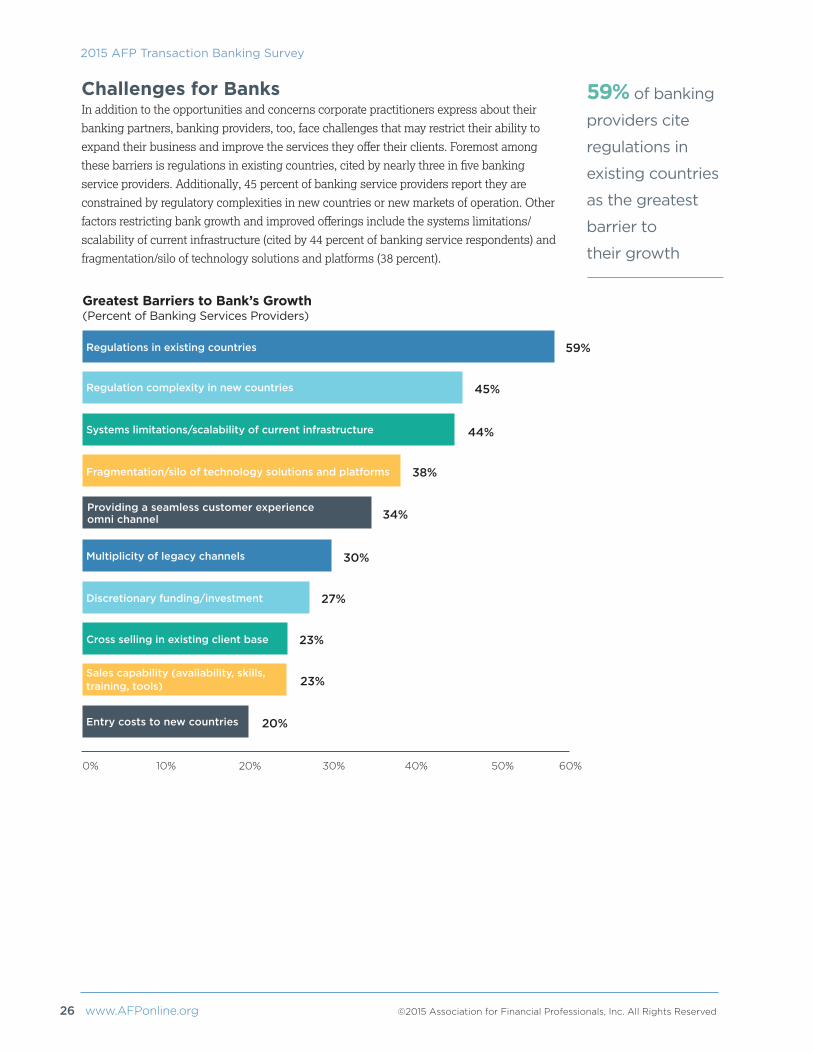

Challenges for BanksIn addition to the opportunities and concerns corporate practitioners express about their

banking partners, banking providers, too, face challenges that may restrict their ability to

expand their business and improve the services they offer their clients. Foremost among

these barriers is regulations in existing countries, cited by nearly three in five banking

service providers. Additionally, 45 percent of banking service providers report they are

constrained by regulatory complexities in new countries or new markets of operation. Other

factors restricting bank growth and improved offerings include the systems limitations/

scalability of current infrastructure (cited by 44 percent of banking service respondents) and

fragmentation/silo of technology solutions and platforms (38 percent).

Greatest Barriers to Bank’s Growth(Percent of Banking Services Providers)

Regulations in existing countries

Regulation complexity in new countries

Systems limitations/scalability of current infrastructure

Fragmentation/silo of technology solutions and platforms

0% 10% 20% 30% 40% 50% 60%

59%

45%

44%

38%

Providing a seamless customer experience omni channel 34%

Discretionary funding/investment

Cross selling in existing client base

Sales capability (availability, skills, training, tools)

30%

27%

23%

23%

Entry costs to new countries 20%

Multiplicity of legacy channels

59% of banking

providers cite

regulations in

existing countries

as the greatest

barrier to

their growth

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 27

2015 AFP Transaction Banking Survey

The majority of finance professionals from large banks (with annual revenues greater than

$5 billion) cite complex regulations in other countries as a constraint holding back their

expansion. Larger banks have a wider scale of operations, due to their broader footprint,

client mix and extensive offering of products and services and therefore are impacted more by

regulations in various countries.

Greatest Barriers to Bank Growth (Percent of Banking Services Providers)

Revenue Revenue Less Than Between Revenue $500 $500 Million- At Least Asia North Western

All Million 4.9 Billion $5 Billion Pacific America Europe

Regulations in existing countries 59% 44% 49% 69% 70% 69% 70%

Regulation complexity in new countries 45 41 30 53 63 47 56

Systems limitations/scalability of current infrastructure 44 51 46 45 39 44 36

Fragmentation/silo of technology solutions and platforms 38 39 43 45 36 40 36

Providing a seamless customer experience omni channel 34 38 41 39 31 37 31

Multiplicity of legacy channels 30 30 41 31 41 27 33

Discretionary funding/investment 27 23 21 33 30 29 22

Sales capability (availability, skills, training, tools) 23 31 25 23 17 22 15

Cross selling in existing client base 23 20 28 23 20 20 21

Entry costs to new countries 20 20 23 21 26 18 22

28 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

Conclusion The 2015 AFP Transaction Banking Services Survey highlights the multifaceted relationships

between corporate practitioners and their banking partners. As companies expand their

business operations and grow increasingly competitive, they also aim to contain their risks

and minimize exposure by maintaining relationships with providers that understand the

complexity of their businesses.

Organizations around the globe continue to be satisfied with services their banking part-

ners are providing them. Similar to last year, organizations with operations primarily in North

America are more satisfied with the services their banking providers deliver than are those in

Asia Pacific and Western Europe. There are some discrepancies with satisfaction among the

individual services offered by banking providers; payments and cash management are the

two most highly rated services by a majority of survey respondents; forecasting continues to

score the lowest score (as it did last year).

Although a slight majority of corporate practitioners indicates their organizations do not

plan to renegotiate banking contracts with their current partners or plan to seek out new

partners, slightly less than half report their companies are leaning towards doing so. For

those that are planning on a reassessment of their banking services, the majority plan to

focus on cash management and payments. This finding reiterates the crucial role these two

services play in a transaction banking relationship.

Financial stability of banks and selecting a bank that provides strategic support are of

paramount importance to corporate clients when establishing a relationship with a banking

partner. Banks also recognize that these are the top concerns of their corporate clients.

Even though a majority of corporate practitioners are satisfied with their banking partners’

services, they do believe there is scope for banks to improve their offerings by implementing

greater harmonization of standards between banks and offering more timely information

and a more streamlined “know your customer” (KYC) process. Such improvements would

lead to greater efficiencies at companies. Additionally, banks could focus on improving their

forecasting function which is clearly not up to their clients’ standards.

Virtually all corporate practitioners indicate that having their banking providers

understand their business and operations would be very valuable. Many indicate they would

like their banking service providers act as strategic partners and work together with them on

longer-term solutions.

Similar to results in previous surveys, a vast majority of organizations work with multiple

banking partners; three-fourths maintain more than 10 accounts with their banks. Finance

professionals use a variety of channels to access their banking services, with the single

integrated bank portal being most common. Despite that, the use of a multi-bank portal—

one portal providing shared access to multiple banks—is often cited as a preferred form

of access.

While corporate practitioners are generally satisfied with the services their banking

partners provide, it is clear there are opportunities for banks to do more to deliver on those

products and services in order to gain a competitive advantage. By considering and taking

into account the feedback provided by their clients, banks can gain an edge in the tightly

competitive banking services arena.

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 29

2015 AFP Transaction Banking Survey

Key takeaways from the survey results:

• Two-thirds of finance professionals indicate they are satisfied with the services their

organizations’ banks provide.

• Among the services bank partners provide, payments and cash management are the

ones most highly rated; 78 percent of respondents ranked payments service a “4” or “5”

(on a 5-point scale); 71 percent ranked cash management a “4” or “5”.

• A vast majority of corporate practitioners believes that having their banking service

providers understand their business and operations is very valuable. Indeed, many

indicate that they would like their banking service providers to play a more strategic role

in their business (90 percent).

• Treasury professionals cite financial stability of the bank (92 percent) and strategic

support (91 percent) as factors they consider when establishing a banking relationship.

• Areas for improvements in banks include harmonization of banks (cited by 58 percent of

corporate practitioners), timelier information (54 percent) and a streamlined KYC process

(51 percent).

• A typical organization works with six to ten banks and 92 percent of organizations have

relationships with multiple banking providers.

• While a single integrated bank portal is the most commonly used one, the use of a

multi-bank portal—one portal providing shared access to multiple banks—is often cited

as a preferred form of access.

• About one out of three corporate practitioners is open to new non-bank

payment alternatives.

• Just under half of corporate respondents are planning to review their banking strategy

with their banking partners.

30 www.AFPonline.org ©2015 Association for Financial Professionals, Inc. All Rights Reserved

2015 AFP Transaction Banking Survey

About the SurveyIn June 2015, the research department of the Association for Financial Professionals® (AFP)

conducted the 2015 AFP Transaction Banking Survey. The survey was sent to AFP corporate

practitioner subscribers and banking services members. The primary purpose of this survey

was to better understand attitudes and emerging trends in banking services and also identify

how banking services are meeting the needs of finance professionals.

A total of 784 responses were received, 269 of which were from corporate practitioners and

515 from banking services providers. Due to the sample size obtained, regional analysis was

limited to responses from the Asia Pacific, North America and Western Europe regions.

AFP thanks CGI for its underwriting support of the 2015 AFP Transaction Banking Survey.

Both questionnaire design and the final report along with its all content and conclusions are

the sole responsibility of the Association for Financial Professionals®.

The following tables present the demographic profile of survey respondents.

Type of Organization(Percentage Distribution of Organizations)

Corporate practitioner working in my organization’s treasury/finance function 34%

Banking services provider 66

Ownership Type (Percentage Distribution of Corporate Practitioners)

Publicly traded 41%

Privately held 42

Non-profit 5

Government (or government-owned entity) 12

Annual Revenue (USD) (Percentage Distribution of Organizations)

Corporate Banking All Practitioners Service Providers

Under $50 million 9% 11% 7%

$50-99.9 million 6 9 3

$100-249.9 million 6 7 5

$250-499.9 million 7 9 6

$500-999.9 million 10 15 7

$1-4.9 billion 17 21 15

$5-9.9 billion 9 8 10

$10-20 billion 12 8 14

Over $20 billion 24 12 32

©2015 Association for Financial Professionals, Inc. All Rights Reserved www.AFPonline.org 31

2015 AFP Transaction Banking Survey

Scope of Organization’s Operations(Percentage Distribution of Organizations)

Corporate Banking All Practitioners Service Providers

Our business operates globally (across multiple regions) 63% 58% 66%

Our business operates within a single country 20 27 15

We primarily operate within one geographic region 17 14 19

Primary Geographic Region (Percentage Distribution of Organizations)

Corporate Banking All Practitioners Service Providers

Asia Pacific 23% 17% 27%

Central & Eastern Europe 6 5 7

Latin & South America 3 5 3

Middle East & Africa 12 14 11

North America 35 40 33

Western Europe 20 20 20

Industry Sector (Percentage Distribution of Corporate Practitioners)

Banking/Financial services 13%

Business services/Consulting 5

Construction 4

Energy (including utilities) 10

Government 6

Health services 5

Hospitality/Travel 1

Insurance 3

Manufacturing 25

Non-profit (including education) 3

Real estate 3

Retail (including wholesale/distribution) 6

Software/Technology 4

Telecommunications/Media 7

Transportation 4

AFP ResearchAFP Research provides financial professionals with proprietary and timely research that

drives business performance. AFP Research draws on the knowledge of the Association’s

members and its subject matter experts in areas that include bank relationship management,

risk management, payments, and financial accounting and reporting. Studies report on

a variety of topics, including AFP’s annual compensation survey, are available online at

www.AFPonline.org/research.

About the Association for Financial ProfessionalsHeadquartered outside Washington, D.C., the Association for Financial Professionals (AFP)

is the professional society that represents finance executives globally. AFP established and

administers the Certified Treasury ProfessionalTM and Certified Corporate FP&A ProfessionalTM

credentials, which set standards of excellence in finance. The quarterly AFP Corporate

Cash IndicatorsTM serve as a bellwether of economic growth. The AFP Annual Conference

is the largest networking event for corporate finance professionals in the world.

AFP, Association for Financial Professionals, Certified Treasury Professional, and

Certified Corporate Financial Planning & Analysis Professional are registered trademarks

of the Association for Financial Professionals. © 2015 Association for Financial

Professionals, Inc. All Rights Reserved.

General Inquiries [email protected]

Web Site www.AFPonline.org

Phone 301.907.2862

www.cgi.com/banking

Since our founding in 1976, CGI has been at the forefront of change within financial services. With 16,000+ financial services professionals, we work with more than 2,500 financial institutions in 40+ countries, including 24 of the top 30 banks worldwide. We are helping our retail and wholesale banking clients reduce costs, achieve strategic objectives and drive competitive advantage.

Excellence in Banking

To find out how we can help you visit

www.cgi.com/banking