Embed Size (px)

Citation preview

©2015, College for Financial Planning, all rights reserved.

Session 4Defined Benefit Plans and Discrimination

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMRetirement Planning & Employee Benefits

Session Details

Module 2

Chapter(s)

1, 3

LOs 2-1 Describe the basic characteristics of a traditional defined benefit plan.

2-3 Calculate and analyze whether a defined benefit plan meets participation and eligibility requirements.

4-2

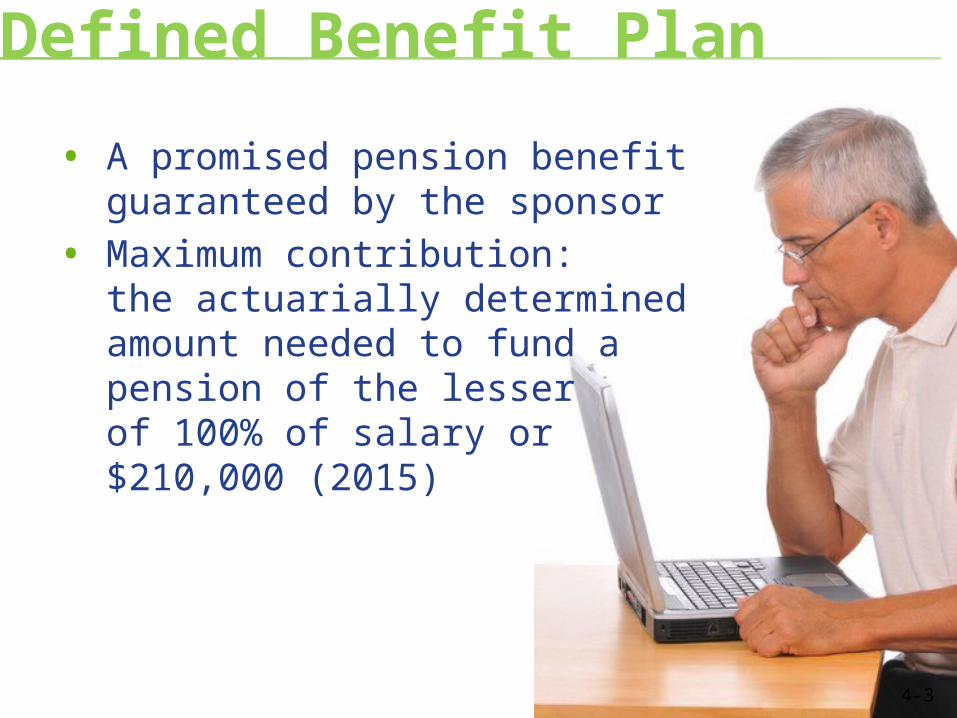

Defined Benefit Plan

• A promised pension benefit guaranteed by the sponsor

• Maximum contribution: the actuarially determined amount needed to fund a pension of the lesser of 100% of salary or $210,000 (2015)

4-3

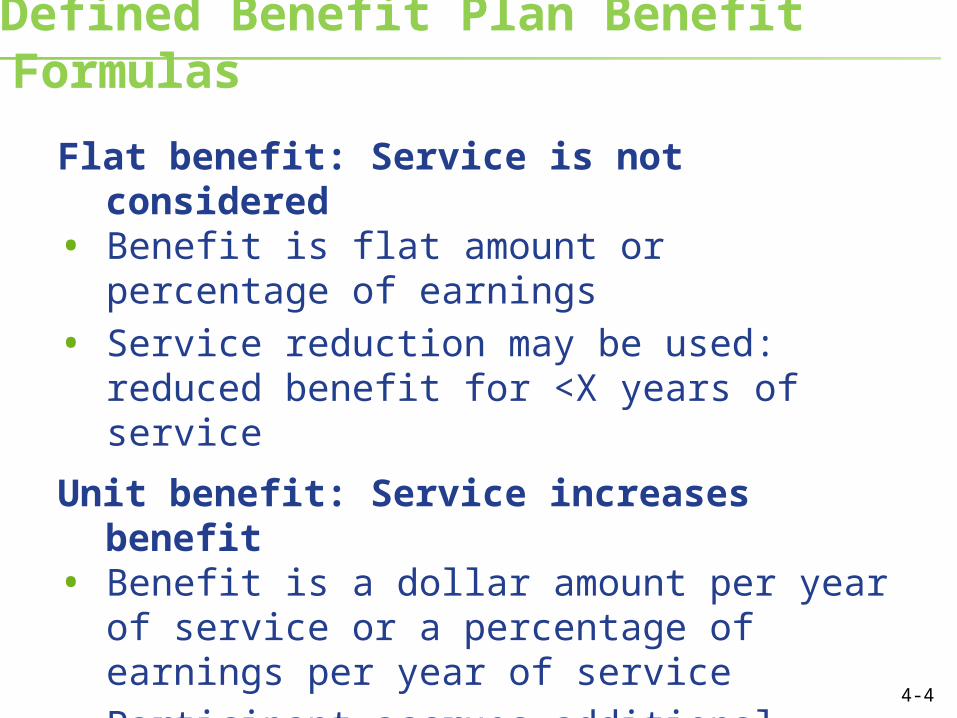

Defined Benefit Plan Benefit Formulas

Flat benefit: Service is not considered• Benefit is flat amount or percentage of

earnings• Service reduction may be used: reduced

benefit for <X years of service

Unit benefit: Service increases benefit• Benefit is a dollar amount per year of

service or a percentage of earnings per year of service

• Participant accrues additional benefit each year

• Service limitation may be used; considers years of service up to specified maximum

4-4

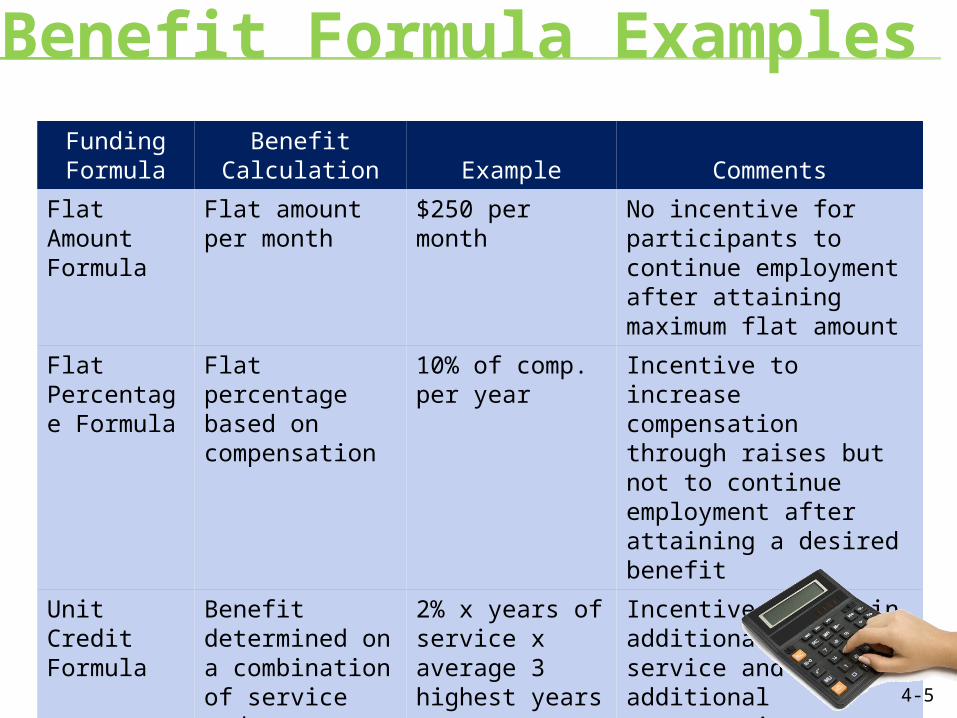

Benefit Formula ExamplesFunding Formula

Benefit Calculation Example Comments

Flat Amount Formula

Flat amount per month

$250 per month

No incentive for participants to continue employment after attaining maximum flat amount

Flat Percentage Formula

Flat percentage based on compensation

10% of comp. per year

Incentive to increase compensation through raises but not to continue employment after attaining a desired benefit

Unit Credit Formula

Benefit determined on a combination of service and compensation

2% x years of service x average 3 highest years pay

Incentive to attain additional years of service and additional compensation to increase ultimate benefit

4-5

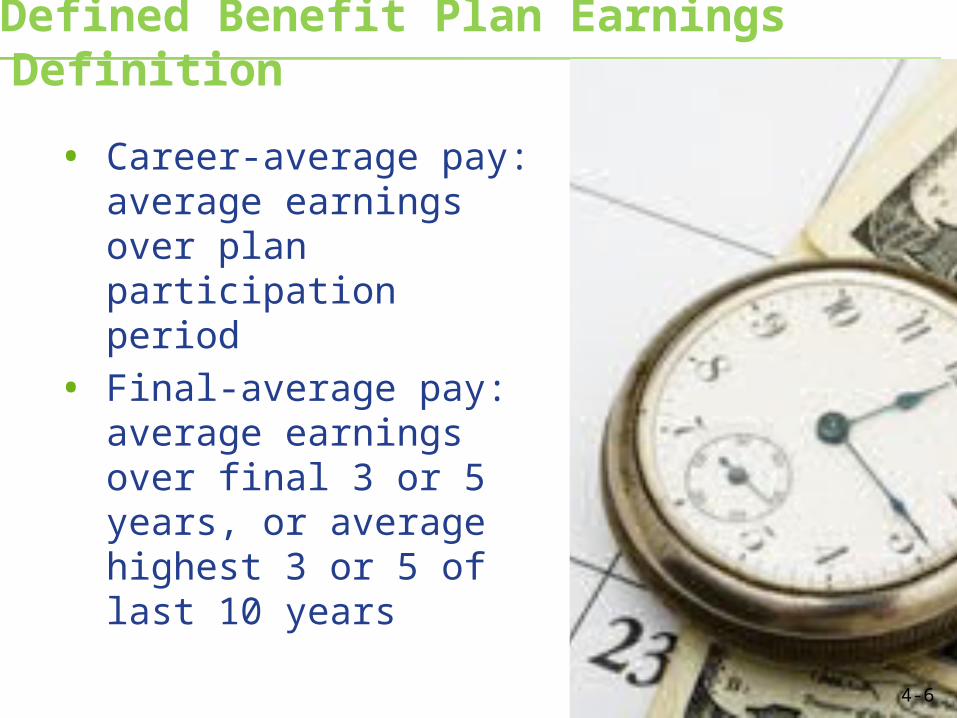

Defined Benefit Plan Earnings Definition

• Career-average pay: average earnings over plan participation period

• Final-average pay: average earnings over final 3 or 5 years, or average highest 3 or 5 of last 10 years

4-6

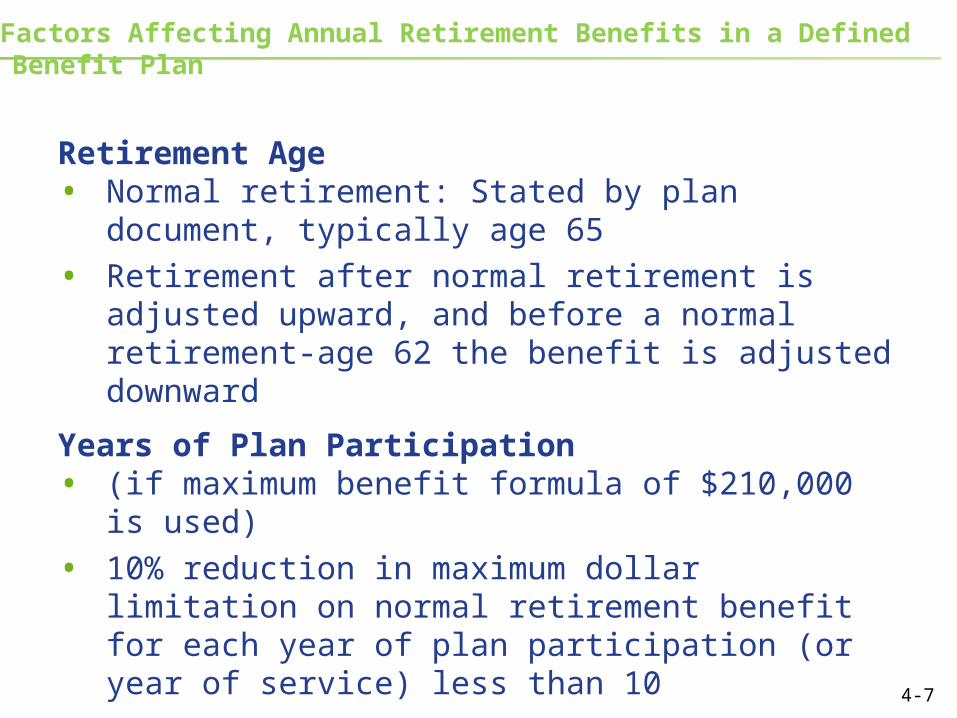

Factors Affecting Annual Retirement Benefits in a Defined Benefit Plan

Retirement Age• Normal retirement: Stated by plan document,

typically age 65

• Retirement after normal retirement is adjusted upward, and before a normal retirement-age 62 the benefit is adjusted downward

Years of Plan Participation • (if maximum benefit formula of $210,000 is

used)

• 10% reduction in maximum dollar limitation on normal retirement benefit for each year of plan participation (or year of service) less than 10

4-7

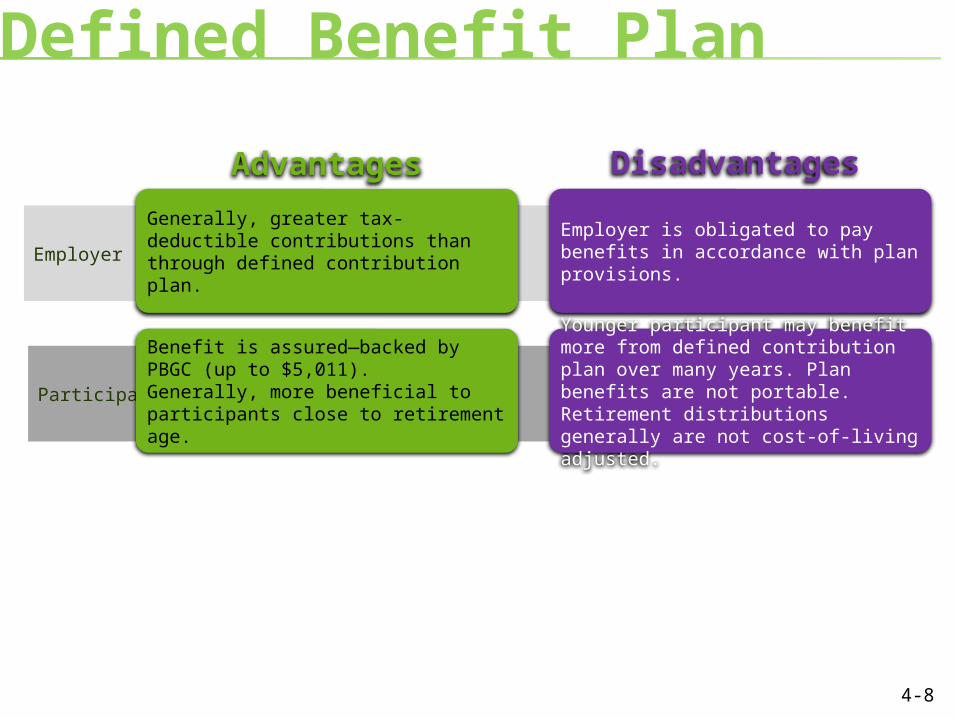

Defined Benefit Plan

Participant

Employer

Advantages

Generally, greater tax-deductible contributions than through defined contribution plan.

Benefit is assured—backed by PBGC (up to $5,011). Generally, more beneficial to participants close to retirement age.

Disadvantages

Employer is obligated to pay benefits in accordance with plan provisions.

Younger participant may benefit more from defined contribution plan over many years. Plan benefits are not portable. Retirement distributions generally are not cost-of-living adjusted.

4-8

Defined Benefit Plan Minimum Participation Test

Defined benefit plans also must satisfy the minimum

participation (50/40) test. The plan must benefit at least

the lesser of• 50 employees, or

• the greater of:o 40% of all the company’s ERISA eligible

employees, oro two employees (one employee if there is only

one employee)

4-9

Minimum Coverage Tests

• A qualified plan must satisfy one of two coverage tests for at least one day of each quarter:o Ratio Percentage Test: Percentage of eligible

non-HCEs benefiting under plan must be at least 70% of percentage of HCEs benefiting

o Average Benefits Test: Average benefit, as a percentage of compensation, for non-HCEs must be at least 70% of that for HCEs

• Employees excluded from the coverage tests: under age 21, or less than one year of service, or covered by a collective bargaining agreement

4-10

Highly Compensated Employee

• Was a “5% owner” (ownership of >5%) in the determination year or in the preceding plan year or

• In 2015, a person whose compensation was in excess of $115,000 in the previous year (2014) is a highly compensated person. o Employer has the option to

limit highly compensated to the top-paid 20% employees based upon preceding year’s compensation.

4-11

Question 1

Which of the following best describes the average benefits test?a. The percentage of NHCs benefited by the

plan must be at least 70% of the percentage of HCs benefited by the plan.

b. Plan benefits for NHCs must be 70% of all employees’ benefits.

c. The plan must benefit a nondiscriminatory classification of employees and the average benefit percentage for NHCs must be 70% of the average benefit percentage for HCs.

d. The plan must benefit at least 70% of all employees. 4-12

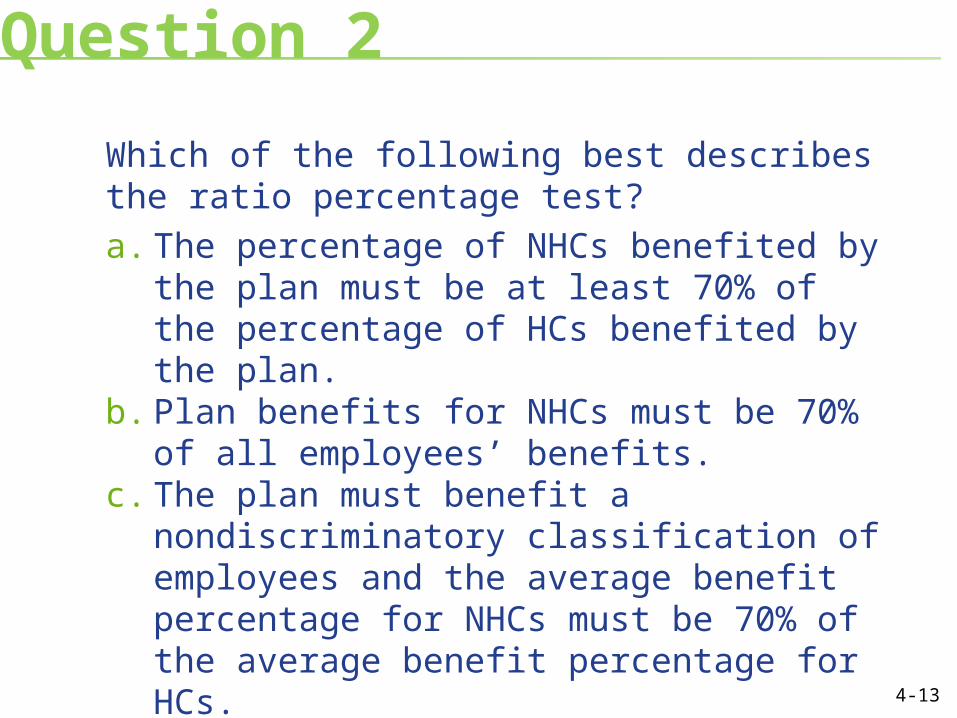

Question 2

Which of the following best describes the ratio percentage test?a. The percentage of NHCs benefited by the

plan must be at least 70% of the percentage of HCs benefited by the plan.

b. Plan benefits for NHCs must be 70% of all employees’ benefits.

c. The plan must benefit a nondiscriminatory classification of employees and the average benefit percentage for NHCs must be 70% of the average benefit percentage for HCs.

d. The plan must benefit at least 70% of all employees. 4-13

©2015, College for Financial Planning, all rights reserved.

Session 4End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMRetirement Planning & Employee Benefits