Embed Size (px)

Citation preview

2016 Highlights & 2017 Survey Findings

John P. Heimlich

Vice President & Chief Economist

Quarterly Media Briefing

March 20, 2017

U.S. Airlines Set Multiple Traffic and Capacity Records in 2016; Load Factor Fell

airlines.org 2

466

45

2

475

48

9

529

548

581

595

613

636

666

62

2

614

647

704

739

745

770

743

70

4

720

731

737

743

763

798

823

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Passengers Enplaned (Millions) – Jan-Dec Revenue Passenger Miles (Billions) – Jan-Dec

458

448

47

9

490

519

541

57

9

603

618

652

693

652

64

2

657

734

779

79

7

829

812

769

79

8

814

823

840

863

902

933

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Available Seat Miles (Billions) – Jan-Dec

733

715

75

3

772

784

807

835

857

873

91

8

957

931

895

895

972

1,0

03

1

,00

6

1,0

38

1

,02

1

957

973

993

995

1,0

11

1

,03

4

1,0

77

1

,11

9

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Load Factor (Percent) – Jan-Dec

62.4

6

2.6

6

3.6

6

3.5

6

6.2

6

7.0

6

9.3

7

0.4

7

0.7

7

1.0

7

2.4

7

0.0

7

1.8

7

3.5

7

5.5

7

7.6

7

9.2

7

9.9

7

9.5

8

0.4

8

2.1

8

2.0

8

2.8

8

3.1

8

3.4

8

3.8

8

3.4

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Source: U.S. Bureau of Transportation Statistics T1, systemwide scheduled service on U.S. airlines

+3.1%

+3.9%

+3.5%

(0.35)

U.S. Airlines Transported More Cargo in 2016; Most Tons Enplaned Since 2007

airlines.org 3

36.5

50.8

0

10

20

30

40

50

60

70

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Carg

o R

eve

nu

e T

on

Mil

es

(B

illio

ns)

Ca

rgo

Re

ve

nu

e T

on

s E

np

lan

ed

pe

r Da

y (0

00

)

Source: U.S. Bureau of Transportation Statistics T1 and T100, systemwide, all services on U.S. passenger and cargo airlines

Billion RTMs per Year (Left Axis)

000 Tons per Day (Right Axis)

SPRING 2017 AIR TRAVEL:

DEMAND FORECAST AND DRIVERS

airlines.org 4

A4A Projects Spring* 2017 Air Travel to Rise 4 Percent to All-Time High

Airlines Adding 110,000 Seats/Day to Accommodate 89,000 Additional Passengers/Day

airlines.org 5

11

8.8

11

9.6

107.8

11

0.6

12

3.5

13

1.4

13

1.8

13

5.1

13

3.7

12

3.0

12

4.2

12

6.8

12

8.4

12

8.2

13

2.2

13

6.2

13

9.5

14

4.9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

F

Source: A4A and BTS T100 segment data – U.S. carriers only; scheduled and nonscheduled services

U.S. Airline Onboard Passengers (Millions) – All Services, March 1 through April 30

145M passengers (nearly 2.4M/day)

• Includes 18M (296K/day) traveling internationally

• Projected average load factor: low-to-mid-80s

• YOY: passengers up 89K/day, seats up 110K/day

+ 4%

* For this purpose, defined as March 1 through April 30

Drivers of year-over-year growth

• Rising GDP and employment

• Higher personal incomes, household net worth

• Continued air travel affordability

U.S. Household Net Worth Reached All-Time High in 2016; Job Growth Strong

airlines.org

1.7

2.4 2.6

1.6

2.3

0

1

2

3

2013 2014 2015 2016 2017F

Real GDP Growth Rate (% CAGR)

6

Monthly Employment Growth (000)

192

250 226

187

238 235

0

100

200

300

2013 2014 2015 2016 Jan Feb

Sources: BEA, BLS, Federal Reserve and IHS Economics; U.S. GDP real annual average growth rate (%), U.S. nonfarm payroll employment growth (month-over-month, in

000s, seasonally adjusted), U.S. disposable personal income per capita (chained 2009 dollars, SAAR); U.S. household net worth in current dollars, not seasonally adjusted

36.4 37.4 38.4 39.2

0

10

20

30

40

50

2013 2014 2015 2016

Th

ou

san

ds

Real ($2009) Personal Incomes ($000) Household Net Worth ($ Trillion, NSA)

78.9 83.9 87.3 92.8

0

50

100

150

2013 2014 2015 2016

Average Round-Trip Airfare Down $27.82 (7%) Since 2014; Fees Up 37¢ (1.6%)

Airfare Has Constituted 94 Percent of Total Ticket Price in Each of the Past Six Years

airlines.org 7

Source: A4A analysis of data from BTS Data Bank 1B (10% sample of tickets: all cabins and fare basis codes) and DOT Form 41

31

5.1

2

34

2.9

5 35

4.6

3

36

2.9

1 3

76

.24

36

3.2

3

34

8.8

9

$300

$310

$320

$330

$340

$350

$360

$370

$380

2010

2011

2012

2013

2014

2015

1H

16

Airfare* (~94% of total)

21

.77

21

.71

22

.38

22

.41

22

.87

22

.87

$0

$5

$10

$15

$20

$25

20

10

20

11

20

12

20

13

20

14

20

15

Ancillary* (~6% of total) Airfare + Ancillary*

33

6.8

9

36

4.6

6

37

7.0

0

38

5.3

2 39

9.1

1

38

6.1

1

37

1.7

9

$300

$320

$340

$360

$380

$400

2010

2011

2012

2013

2014

2015

1H

16

* Domestic round-trip average

With Personal Incomes Outpacing the Price of Air Travel, Americans Can Purchase

~2.5 Times the Amount of Air Travel They Could at the Outset of Deregulation

Adjusted for Inflation, Domestic Air Travel Remains 40+ Percent Below 1980 Levels

airlines.org

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1979

1983

1987

1991

1995

1999

2003

2007

2011

2015

2019

Fare Fare + Ancillary

Domestic R/T Airfare as Share (%) of

Per-Capita Disposable Personal Income

8

Source: A4A analysis of data from BEA, BLS and BTS Data Bank 1B (10% sample of tickets for all cabins and fare basis codes)

$300

$350

$400

$450

$500

$550

$600

$650

1979

1983

1987

1991

1995

1999

2003

2007

2011

2015

2019

Fare Fare + Ancillary

Domestic R/T Airfare Adjusted for

Inflation (in CY2015 Dollars)

Sources: BTS and DOT Air Travel Consumer Report (http://www.dot.gov/airconsumer/air-travel-consumer-reports)

airlines.org 9

U.S. Airlines Saw Continued Improvements in DOT Operational Metrics in 2016

Gains Driven by Investments in Aircraft, Systems, Procedures, Staffing

97.82

98.46

98.83

2014

2015

2016

Flight Completion Factor (%) – Jan-Dec

99.64

99.68

99.73

2014

2015

2016

Properly Handled Bag Rate (%) – Jan-Dec

0.92

0.76

0.62

2014

2015

2016

Oversales per 10,000 Customers – Jan-Dec

On-Time Arrival Rate (%) – Jan-Dec

76.25

79.92

81.42

2014

2015

2016Best since 1992

Best ever recorded

Best since 2012

Best ever recorded

2016 HIGHLIGHTS AND 2017 INSIGHTS

airlines.org 10

Steadier Oil and Jet-Fuel Prices Boosting Seats, Wages and Reinvestment

Every Penny per Gallon per Year Equates to ~$190M in U.S. Airline Industry Fuel Expenses

EIA Spot Price* of Crude Oil/Barrel (Brent)

airlines.org 11

0.6

1

0.8

5

2.1

5

3.0

0

3.0

6

2.9

2

2.6

9

1.5

2

1.2

5

1.5

3

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

199

1

200

0

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

EIA Spot Price* of Jet Fuel/Gallon (U.S. Gulf) 2

0 29

80

111

112

10

9

99

52

44

55

$0

$20

$40

$60

$80

$100

$120

199

1

200

0

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

Source: A4A and Energy Information Administration (http://www.eia.gov/dnav/pet/pet_pri_spt_s1_d.htm) * 2017 reflects year-to-date average

2016 Revenues Down 1% As 5.2% Lower Fares1 Offset 3.1% More Passenger Traffic

2016 Expenses Up 0.9% As Higher Labor and Other Expenses Offset Lower Fuel

airlines.org 12

% Change YOY in Operating Revenues

3.1

(5.2)

(9.8)

6.2

(1.0)

Source: A4A analysis of reports by Alaska/Virgin America, Allegiant, American, Delta, Hawaiian, JetBlue, Southwest, Spirit and United

% Change YOY in Operating Expenses

9.3

(17.0)

2.5 2.0

6.4 4.4

0.9

1. Yield = fare per mile (cents per RPM)

2. Sale of frequent flyer award miles to airline business partners, pet transportation, in-sourced aircraft and engine repair, flight simulator rentals, inflight sales, etc.

3. Professional fees, food/beverage, insurance, commissions, GDS fees, communications, advertising, utilities, office supplies, crew hotels, nonfuel payments to regionals

airlines.org 13

Faster-Falling Revenues Drove Modest Reduction in 2016 U.S. Airline Profitability

Pre-Tax Profit Margin of 14.2 Percent Remains Below Average for U.S. Companies

$158.6

$157.1

2015

2016

Operating Revenues (Billions) – Jan-Dec

$23.3

$22.3

2015

2016

Pre-Tax Income (Billions) – Jan-Dec

14.7

14.2

2015

2016

Pre-Tax Profit Margin (%) – Jan-Dec

Operating Expenses (Billions) – Jan-Dec

$131.3

$132.5

2015

2016

Source: A4A analysis of reports by Alaska/Virgin America, Allegiant, American, Delta, Hawaiian, JetBlue, Southwest, Spirit and United

In 2016, U.S. Airlines* Posted Respectable Margins, Averaging 14.2% Before Taxes

U.S. Passenger Airline* Profitability Was Substantially Below Starbucks/McDonald’s/Apple

airlines.org

28.5 27.9 26.7 26.6

24.8

19.7

14.2

4.5

1.0

Ap

ple

McD

on

ald

´s

Dis

ne

y

Com

cast

CS

X

Sta

rbucks

Air

lines*

Fo

rd

Chip

otle

14

* A4A analysis of reports by Alaska/Virgin America, Allegiant, American, Delta, Hawaiian, JetBlue, Southwest, Spirit and United

2016 Pre-Tax Profit Margin

(% of Operating Revenues)

$2

2.3

B

$6

1.3

B

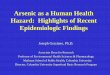

Since the Great Recession,* U.S. Airlines Have Been Closing the Gap to Average

U.S. Corporate Profitability; YTD16 Gap (14.2% vs. 15.8%) Is Narrowest on Record

airlines.org

Source: ATA Annual Reports (1970-1976), A4A Passenger Airline Cost Index (1977-present); Bureau of Economic Analysis NIPA Table 1.14

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

YT

D1

6

20

18

20

20

U.S. Recession

U.S. Passenger Airlines

All U.S. Corporations

Pre-Tax Profit Margin (%)

15

* Dec-2007-Jun-2009

U.S. Airlines Are Putting More Than $20 per Passenger* Right Back Into the Product

Use of Operating Cash from 2010-2016 Included $82B of Capital Reinvestment

airlines.org 16

* SEC filings of Alaska/Allegiant/American/Delta/Hawaiian/JetBlue/Southwest/Spirit/United/Virgin America

$17.5B

Enhance

Product

$13.1B

Reward

Shareholders

$8.5B

Retire

Debt

2016 2010-2015

$64.9B

Enhance

Product

$17.4B

Reward

Shareholders

$54.3B

Retire

Debt

airlines.org 17

Following 2001-2009 Financial Hemorrhaging, U.S. Airlines Have Retired $63B in Debt

Carriers Ended 2016 With $75B in Gross Debt1 and $22B in Liquidity2

Source: SEC filings of AAL/ALGT/AAL/DAL/HA/JBLU/LUV/SAVE/UAL/VA

$9.1 $11.2 $7.5 $7.9

$10.5 $8.0 $8.5

$62.8

$0

$20

$40

$60

$80

2010 2011 2012 2013 2014 2015 2016

Th

ou

san

ds

Annual Cumulative

Payments on Long-Term Debt and Capital Lease Obligations (Billions)

1 Includes 7x annual aircraft rents (capitalized operating leases) 2 Cash, cash equivalents and short-term investments

Year-End 2016

$75.1B gross debt1

$21.6B liquidity2

Improving Finances Enabling Significant Reinvestment in Customer Experience

2016 Capital Outlays Averaged Almost $1.5B per Month, Exceeding 2015 Rate

airlines.org 18

1.29

1.15

0.64 0.55

0.49 0.43

0.55

0.82

1.04 1.16

1.41 1.46

2000 2001 2002 2003-08 2009 2010 2011 2012 2013 2014 2015 2016 2017

* SEC filings of Alaska, Allegiant, American, Delta, Hawaiian, JetBlue, Southwest, Spirit, United and Virgin America

U.S. Passenger Airline* Capital Expenditures ($ Billions per Month)

Exp

ecte

d d

eliv

ery

of 3

37

aircra

ft

Inclu

ded

deli

very

of

1x p

lan

e/d

ay

Improving Finances Enabling Significant Reinvestment in Customer Experience

airlines.org 19

» New or refurbished aircraft, larger overhead bins for luggage

» Availability of lie-flat seating with AC power and USB, proliferation of Wi-Fi and inflight entertainment

» Expanded route networks (scope and frequency) and schedules (seat growth)

» Improved airport check-in areas, lounges, gate amenities, baggage systems, ground equipment

» Investments in new automated security screening lanes (including automatic bin returns)

» Continued development and roll-out of mobile technology and website/kiosk functionality

» Increasing operational reliability (controlled for weather conditions)

» Enhanced tools (computers, tablets, software) and training for customer-contact employees

2,5

74

2,4

94

2,5

46

2,4

51

2,2

92

2,2

85

2,2

94

2,2

59

2,2

74

2,2

89

2,3

66

2,4

54

2,5

46

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

As Airlines See Higher Returns on Capital, Customers Are Seeing More Seats

Domestic Supply at Highest Level Since 2005; International Supply at All-Time High

airlines.org

Domestic USA (Thousand Daily Seats)

20

Source: Innovata (via Diio Mi) published schedules as of Mar. 10, 2017, for all airlines providing scheduled passenger service from U.S. airports to all destinations

27

2

27

8

28

8

29

2

27

5

28

2

29

2

29

9

31

0

33

0

35

1

36

8

39

2

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

International (Thousand Daily Seats)

Up

3.7

% Y

OY

Up

6.4

% Y

OY

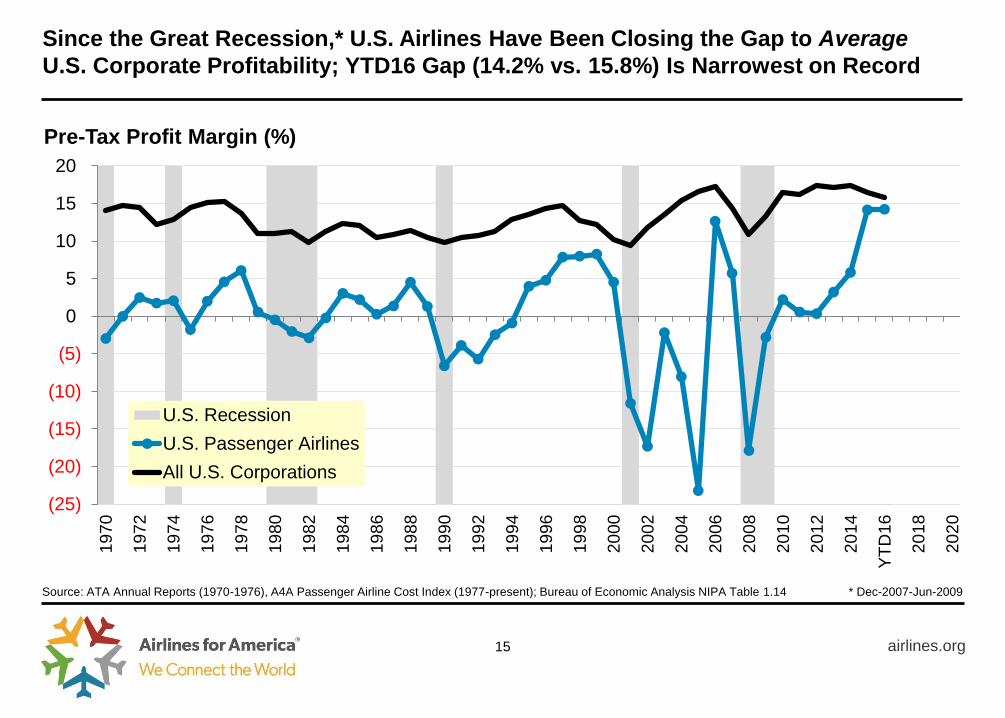

In Addition to Expanding Schedules, Airlines Are Deploying Larger Aircraft

Replacement of 50-Seaters With Larger Regional Jets Is Biggest Driver of Jump

airlines.org 21

38 37 36 35 32 27 25 23

15 15 15 16 18

20 21 22

48 48 49 49 51 53 54 55

2010

2011

2012

2013

2014

2015

2016

2017

1-50 Seats 51-100 Seats >100 Seats

% of Domestic Departures by Aircraft Size1

Source: Innovata (via Diio Mi) published schedules as of Jan. 27, 2017 1

05

.5

10

6.5

106.3

10

7.7

111

.1

11

6.0

11

6.7

11

8.0

2010

2011

2012

2013

2014

2015

2016

2017

Average Seats per Domestic Departure2

1. All carriers

2. AAL, ALGT, ALK, DAL, HA, JBLU, LUV, SAVE, UAL networks

Use of Larger RJs and Mainline Replacement of RJs Boosting Avg. Seats per Flight

Selected Examples of Airline Deployment of Larger Aircraft on Domestic Routes

airlines.org 22

Source: Innovata (via Diio Mi) published schedules as of Mar. 3, 2017, comparing 3/6/2017 to 3/9/2015

Airline Hub Spoke Mar-2015 Mar-2017

Alaska Seattle Omaha RJ-70 B737

American Dallas/Ft. Worth Greensboro RJ-50 RJ-76

Dallas/Ft. Worth Madison RJ-50 RJ-76

Dallas/Ft. Worth Mobile RJ-50 RJ-76

Dallas/Ft. Worth Tallahassee RJ-50 RJ-76

Los Angeles Albuquerque RJ-50 RJ-76

Los Angeles El Paso RJ-50 RJ-76

Los Angeles Phoenix RJ-76 A321/B757

Delta Atlanta Scranton RJ-76 B717

Atlanta Sioux Falls RJ-76 B717

Cincinnati Hartford RJ-50 RJ-76

Cincinnati Raleigh-Durham RJ-50 RJ-76

United Chicago Rochester 4x RJ-50, 2x A319 2x RJ-50, 4x A319

Denver Des Moines RJ-50/70 A319/B737

Newark Cincinnati RJ-50 RJ-70/76

Newark Jacksonville RJ-50/70 RJ-50/A320

San Francisco Eugene RJ-50 A319/A320

San Francisco Reno RJ-50/70 RJ/B737

Wash. Dulles New York LGA RJ-50 RJ-70

Wash. Dulles Philadelphia RJ-50 RJ-70

U.S. Airports of All Sizes Have Realized Air Service Gains Over Past Two Years

176 Small and Non-Hub Markets Saw Seats Grow at Least Half a Percent

airlines.org 23

27

27

57

118

229

1

13

97

111

1

1

1

2

3

2

3

17

22

Large

Medium

Small

Non

Total

Grew ≥ 0.5% Shrank ≥ 0.5% New Cut Other

Number of U.S. Airports by Change in Scheduled Seats from 3Q15 to 3Q17 by DOT “Hub” Size

Source: Innovata (via Diio Mi) published schedules as of Mar. 10, 2017, for all airlines providing scheduled passenger service from U.S. airports to all destinations

+ 8.0%

+ 10.2%

+ 12.2%

+ 4.6%

+ 8.4%

198

151

161

134

37

17

2016

2017

Added

Discontinued

Net Change

airlines.org

Airlines Added 198 New U.S.-Based Routes in 2016, Have Added 151 More in 2017

Over Two Years, Fliers See Net Expansion of 54 Nonstop Routes to/from U.S. Airports

Year-Over-Year Change in Number of Scheduled-Service Routes to/from U.S. Airports

24

Source: Innovata (via Diio Mi) published schedules from March 2017 and July 2016 for all airlines providing scheduled service from U.S. airports to all destinations

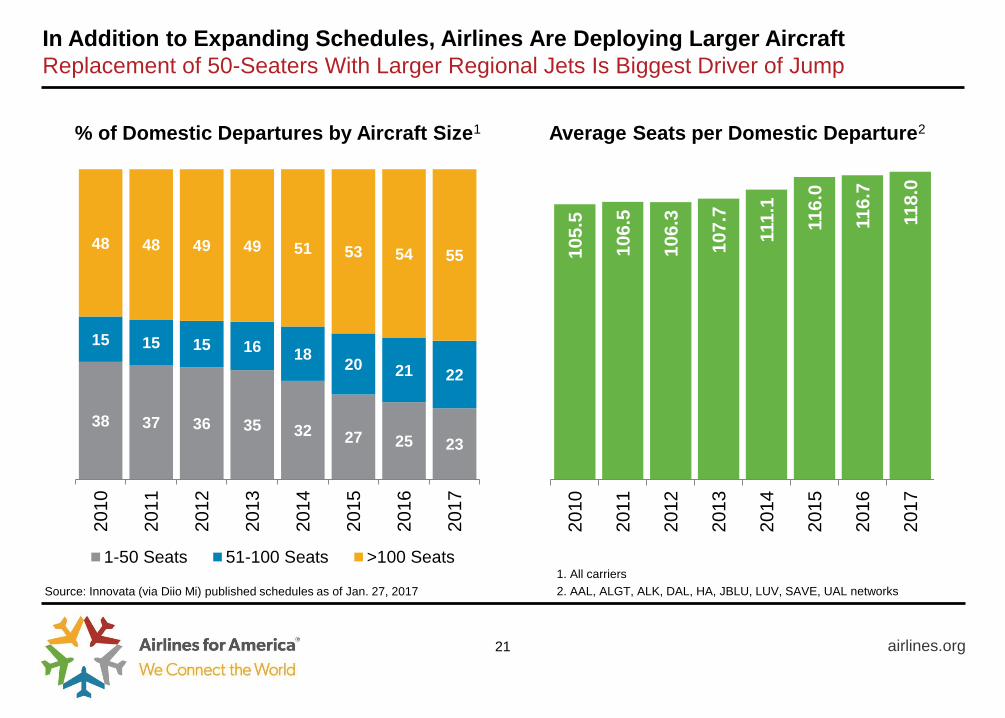

In 2016, U.S. Passenger Airline Jobs Averaged Highest Level Since 2007

December 2016 Was 38th Consecutive Month of YOY Gains

airlines.org 25

Source: Bureau of Transportation Statistics for scheduled U.S. passenger airlines

520.6

413.1 407.6 385.9 378.3

395.5 411.1

2000 2007 2008 2009 2010 2015 2016

Full-Time Equivalent (FTE) U.S. Scheduled Passenger Airline Employees (000s)

Since April 2015, U.S. Airline Job Growth Has Exceeded Overall U.S. Job Growth

Airline Employment Growing at 4% – More Than Double the Rate of Overall U.S. Jobs

airlines.org

Source: Bureau of Labor Statistics and Bureau of Transportation Statistics

(2)

(1)

0

1

2

3

4

5Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Ye

ar-

Ove

r-Y

ea

r C

ha

ng

e (

%)

U.S. Passenger Airlines FTEs U.S. Nonfarm Jobs

26

U.S. Airlines* Continue to Pump More Wages and Benefits into the Economy

Airlines* Spent $3.7 Billion/Month on the Workforce in 2016 – Up 44 Percent from 2010

airlines.org 27

2.55 2.61

2.73 2.76

2.99

3.35

3.66

2010 2011 2012 2013 2014 2015 2016

* SEC filings of Alaska/Virgin America, Allegiant, American, Delta, Hawaiian, JetBlue, Southwest, Spirit, United

Total Employee Wages and Benefits*

($ Billions per Month)

U.S. Passenger Airline Wages Averaged 38% More Than U.S. Private Sector in 2015

From 2010 to 2015, Airline Wages Rose 29% (More Than Double 13% for Overall USA)

airlines.org 28

Source: BEA NIPA Table 6.6D and A4A Passenger Airline Cost Index

$51.9 $53.5

$54.9 $55.4 $56.4 $58.7

$62.6 $63.1

$67.3 $70.0

$74.5

$80.9

$84.4

$50

$55

$60

$65

$70

$75

$80

$85

$90

2010 2011 2012 2013 2014 2015 YTD16 2017

Th

ou

san

ds

USA* Airlines

Wages and Salaries (000) per Full-Time Equivalent Employee (FTE)

* For al private industries

+38%

N/A

airlines.org 29

In 2016, U.S. Airlines Continued Efforts to Retain and Lure New Equity Investors,

Returning $13B to Shareholders Via Stock Buybacks ($12B) and Dividends ($1B)

Stock Repurchases (Billions) Dividends (Billions)

$1.2

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

2010 2011 2012 2013 2014 2015 2016

$12.0

$0

$2

$4

$6

$8

$10

$12

$14

2010 2011 2012 2013 2014 2015 2016

* SEC filings of Alaska, Allegiant, American, Delta, Hawaiian, JetBlue, Southwest, Spirit, United and Virgin America

JANUARY 2017 AIR TRAVEL SURVEY FINDINGS

airlines.org 30

Ipsos Research Approach

airlines.org

» A4A again selected Ipsos Public Affairs (“Ipsos”), one of the top polling firms1 in the country.

» Ipsos conducted a poll2 January 6-13, 2017 on behalf of Airlines for America (A4A). For the

survey, a sample of 5,047 adults age 18+ from the continental U.S., Alaska and Hawaii was

interviewed online in English.

» The sample for this study was randomly drawn from Ipsos’s online panel,3 partner online

panel sources, and “river” sampling4 and does not rely on a population frame in the

traditional sense. Ipsos uses fixed sample targets, unique to each study, in drawing sample.

» After a sample has been obtained from the Ipsos panel, Ipsos calibrates respondent

characteristics to be representative of the U.S. population using standard procedures such

as raking-ratio adjustments. The source of these population targets is U.S. Census 2015

American Community Survey data. The sample drawn for this study reflects fixed sample

targets on demographics. Post-hoc weights were made to the population characteristics on

gender, age, region, race/ethnicity and income.

31

Source: Ipsos survey of American adults (January 2017)

1. https://projects.fivethirtyeight.com/pollster-ratings/

2. http://www.ipsos-na.com/news-polls/pressrelease.aspx?id=7585

3. http://www.ipsos-na.com/dl/pdf/research/public-affairs/Ipsos_IIS_NAAccessPanelsRecruitment_.pdf

4. http://www.ipsos-na.com/dl/pdf/research/public-affairs/Ipsos_IIS_AmparioOverview.pdf

Ipsos Poll Accuracy

airlines.org

» Statistical margins of error are not applicable to online polls. All sample surveys and polls

may be subject to other sources of error, including, but not limited to coverage error and

measurement error. Where figures do not sum to 100, this is due to the effects of rounding.

» The precision of Ipsos online polls is measured using a credibility interval.1 In this case, the

poll has a credibility interval of plus or minus 1.6 percentage points for all respondents.

» Ipsos calculates a design effect (DEFF) for each study based on the variation of the weights,

following the formula of Kish (1965). This study had a credibility interval adjusted for design

effect of the following (n=5,047, DEFF=1.5, adjusted Confidence Interval=3.1).

32

1. http://www.ipsos-na.com/dl/pdf/research/public-affairs/IpsosPA_CredibilityIntervals.pdf Source: Ipsos survey of American adults (January 2017)

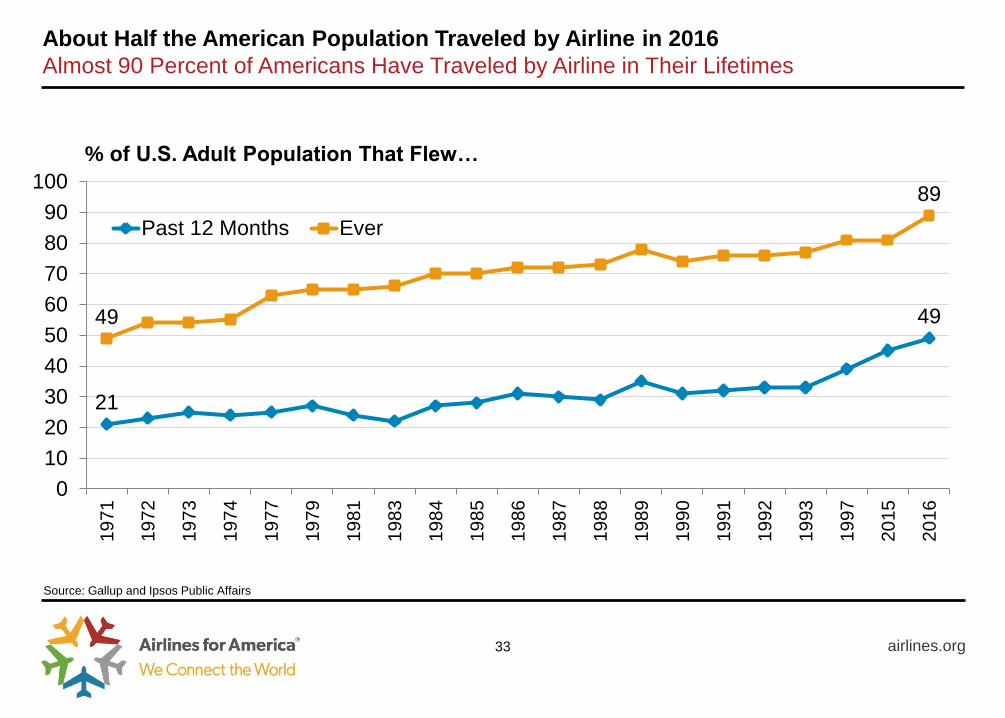

About Half the American Population Traveled by Airline in 2016

Almost 90 Percent of Americans Have Traveled by Airline in Their Lifetimes

airlines.org

21

49 49

89

0

10

20

30

40

50

60

70

80

90

100

1971

1972

1973

1974

1977

1979

1981

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1997

2015

2016

Past 12 Months Ever

% of U.S. Adult Population That Flew…

Source: Gallup and Ipsos Public Affairs

33

18%

51%

31%

Personal Non-leisure*

Personal Leisure

Business 1.4 0.7

2.3 1.1

0.8 0.4

4.5 2.2

Per 2016 Flier

Composition of Airline Trips Taken by Primary Purpose in 2016

airlines.org

Half of 2016 Airline Trips Were Taken Primarily for Leisure; 31 Percent for Business

34

* Includes traveling to/from college, family event, job interview, funeral, medical matters

Per American

35%

44%

14%

5%

1%

43%

42%

10%

5%

1%

Very satisfied

Somewhat satisfied

Neutral

Somewhat dissatisfied

Very dissatisfied

2015

2016

airlines.org

85 Percent of 2016 Fliers Reported Being Somewhat or Very Satisfied

Satisfaction Up From 2015; Those Who Were “Very Dissatisfied” Unchanged at 1 Percent

Satisfaction with “Overall Experience With Air Travel” in 2016

35

Source: Ipsos surveys of American adults (December 2015 and January 2017)

2016 Fliers Most Satisfied With Checking In, Followed by Shopping/Booking Flights

Fliers Gave All Six Categories an Average Score Exceeding 3

airlines.org 36

In 2016, on a scale of 1 (lowest) to 5 (highest), how would you

rate your overall satisfaction with each of the following?

Source: Ipsos survey of American adults (January 2017)

3.94

3.90

3.70

3.69

3.55

3.46

Checking in for the flight

Shopping/purchasing ticket

Boarding process

On-time reliability

Awaiting checked baggage

Getting through security

48

39

10 2

0.3

All were satisfactory

Most were satisfactory

About half and half

Most were unsatisfactory

All were unsatisfactory

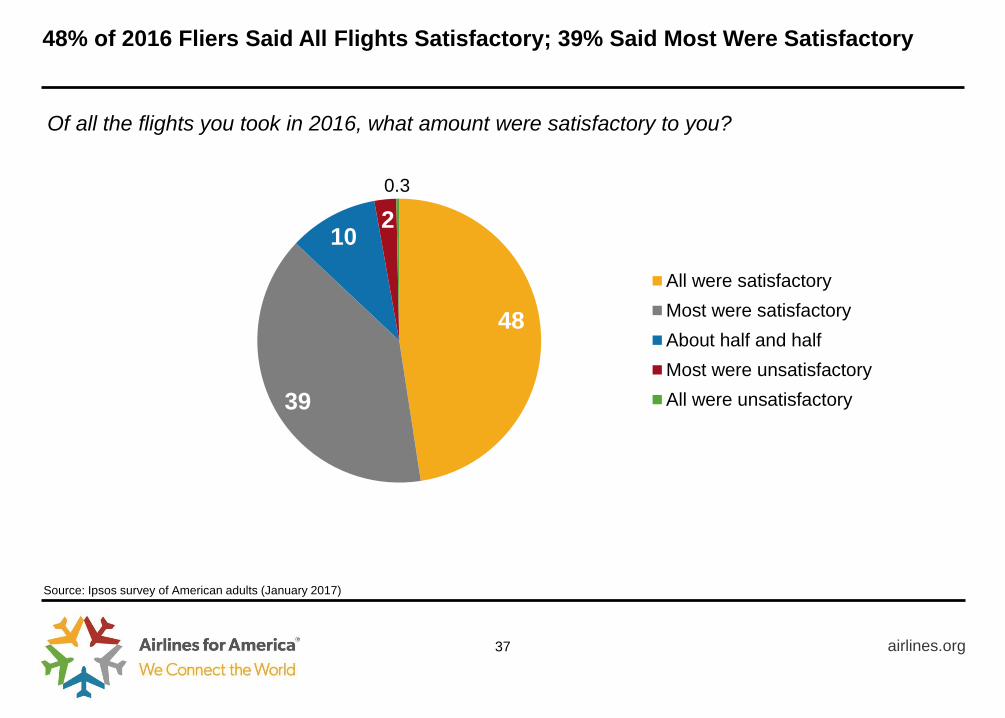

48% of 2016 Fliers Said All Flights Satisfactory; 39% Said Most Were Satisfactory

airlines.org 37

Source: Ipsos survey of American adults (January 2017)

Of all the flights you took in 2016, what amount were satisfactory to you?

Flier Satisfaction Rises Markedly With Enrollment in Expedited Screening Programs

Airline/Government Collaboration Boosting Participation in DHS Trusted Traveler Programs

airlines.org

Very, 36%

Very, 50%

Very, 68%

Somewhat, 46%

Somewhat, 38%

Somewhat, 24%

Neither

TSA Pre✓®

Global Entry

% of 2016 Fliers Indicating “Very Satisfied” With Overall Air Travel Experience

Sources: Ipsos survey of American adults (January 2017), Transportation Security Administration, Customs and Border Protection

38

Millions of Persons Enrolled in DHS Trusted Traveler Programs (Dec. 31)

0.8

2.0

4.2

3.1

4.0

5.3

2014

2015

2016

TSA Pre✓ Global Entry/NEXUS/SENTRI

92%

88%

82%

Most Americans Will Fly as Much or More in 2017 as They Did in 2016

airlines.org

28%

56%

17%

More Same Fewer

39

Including both business travel and personal travel, do you think you

will take more or fewer airline trips in 2017 than you did in 2016?

Source: Ipsos survey of American adults (January 2017)

2016 Operational and Financial Recap: U.S. Passenger Airlines

airlines.org 40

» In 2016, airlines:

Achieved the seventh consecutive year of consummate safety performance

Posted gains or high-water marks on multiple operational fronts

Carried a record level of traffic and operated a record level of capacity, with the highest two-year

growth in capacity since 2003-2005 contributing to lower average fares and load factors

Recorded a modest reduction in profits, as lower operating revenues (lower fares offset higher traffic)

were met with higher operating expenses (increases in labor/airport/aircraft/other offset lower fuel)

Saw profitability (14% pre-tax margin) continue to lag the U.S. corporate average (16% margin)

» Cash flow generated allowed U.S. airlines to retire expensive debt, acquire new aircraft,

upgrade facilities, expand inflight entertainment options, boost inflight Wi-Fi speeds,

deploy more seats in the marketplace, increase staffing and wages, reward investors

» Airlines continue to add seats at airports large and small, as competition intensified

across the United States and consumers benefited from expanding route maps

» Satisfaction rose from 2015, and market research affirms that participation in expedited

screening programs markedly improves the air travel experience; enrollment rising

www.airlines.org