Embed Size (px)

Citation preview

EZLAND PRESENTATION

AFFORDABLE HOUSING MARKET OVERVIEWS

JANUARY 2016

Ho Chi Minh

Market Overviews

Ho Chi Minh

EZLAND PRESENTATION

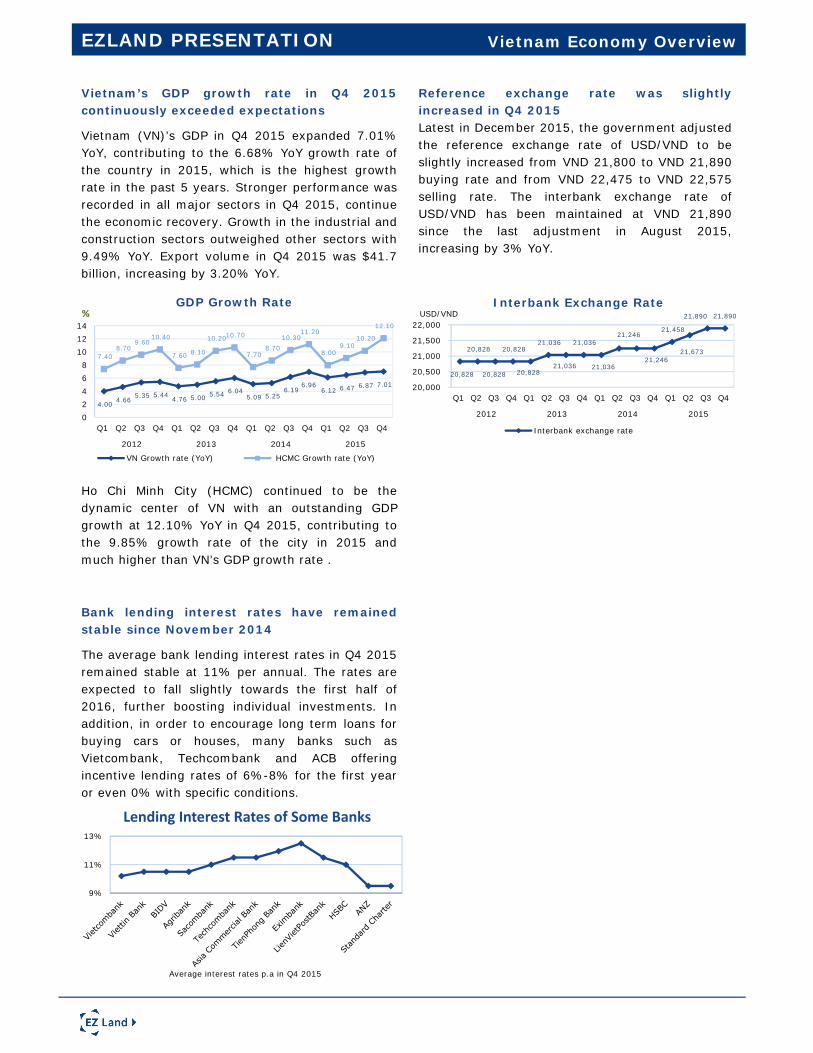

Vietnam’s GDP growth rate in Q4 2015continuously exceeded expectations

Vietnam (VN)’s GDP in Q4 2015 expanded 7.01%YoY, contributing to the 6.68% YoY growth rate ofthe country in 2015, which is the highest growthrate in the past 5 years. Stronger performance wasrecorded in all major sectors in Q4 2015, continuethe economic recovery. Growth in the industrial andconstruction sectors outweighed other sectors with9.49% YoY. Export volume in Q4 2015 was $41.7billion, increasing by 3.20% YoY.

Bank lending interest rates have remainedstable since November 2014

The average bank lending interest rates in Q4 2015remained stable at 11% per annual. The rates areexpected to fall slightly towards the first half of2016, further boosting individual investments. Inaddition, in order to encourage long term loans forbuying cars or houses, many banks such asVietcombank, Techcombank and ACB offeringincentive lending rates of 6%-8% for the first yearor even 0% with specific conditions.

Ho Chi Minh City (HCMC) continued to be thedynamic center of VN with an outstanding GDPgrowth at 12.10% YoY in Q4 2015, contributing tothe 9.85% growth rate of the city in 2015 andmuch higher than VN’s GDP growth rate .

EZLAND PRESENTATION Vietnam Economy Overview

Reference exchange rate was slightlyincreased in Q4 2015Latest in December 2015, the government adjustedthe reference exchange rate of USD/VND to beslightly increased from VND 21,800 to VND 21,890buying rate and from VND 22,475 to VND 22,575selling rate. The interbank exchange rate ofUSD/VND has been maintained at VND 21,890since the last adjustment in August 2015,increasing by 3% YoY.

9%

11%

13%

Lending Interest Rates of Some Banks

Average interest rates p.a in Q4 2015

4.00 4.66 5.35 5.44 4.76 5.00 5.54 6.04

5.09 5.25 6.19

6.966.12 6.47 6.87 7.01

7.40 8.70

9.60 10.40

7.60 8.10

10.20 10.70

7.70 8.70

10.30 11.20

8.00 9.10

10.20

12.10

02468

101214

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015

GDP Growth Rate

VN Growth rate (YoY) HCMC Growth rate (YoY)

%

20,828

20,828

20,828

20,828

20,828

21,036

21,036

21,036

21,036

21,246

21,246

21,458

21,673

21,890 21,890

20,000

20,500

21,000

21,500

22,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015

USD/VNDInterbank Exchange Rate

Interbank exchange rate

EZLAND PRESENTATION Vietnam Economy Overview (cont.)

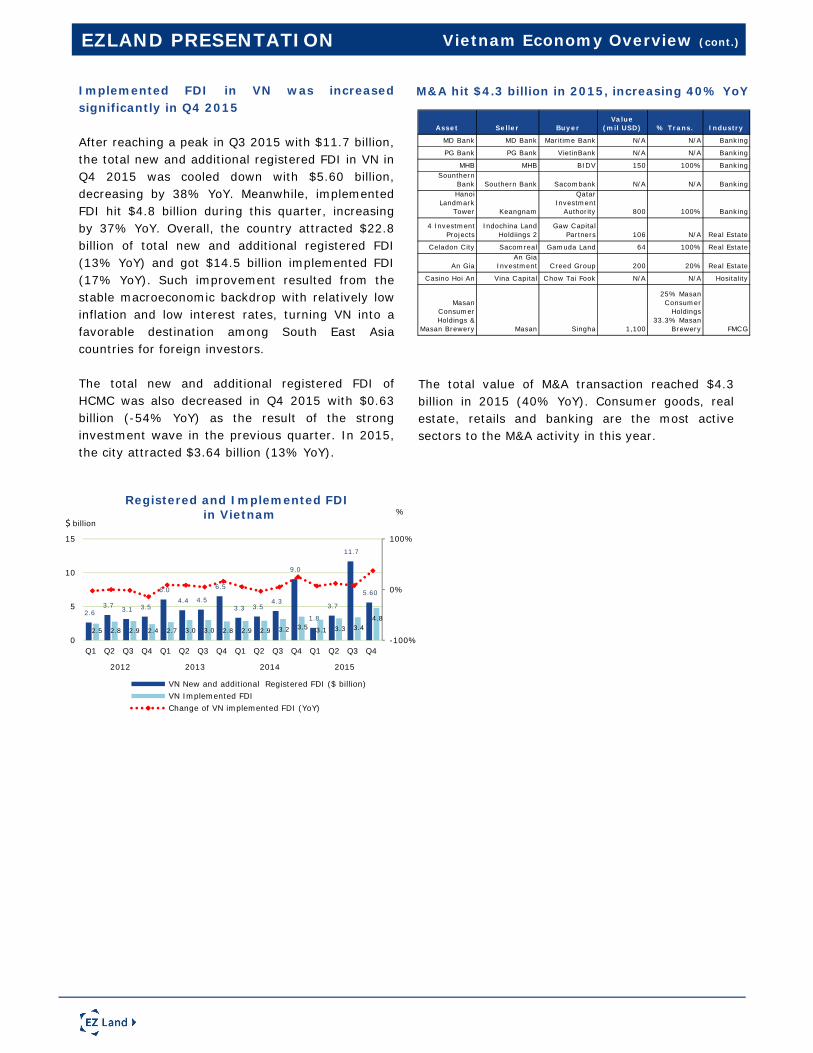

M&A hit $4.3 billion in 2015, increasing 40% YoYImplemented FDI in VN was increasedsignificantly in Q4 2015

After reaching a peak in Q3 2015 with $11.7 billion,the total new and additional registered FDI in VN inQ4 2015 was cooled down with $5.60 billion,decreasing by 38% YoY. Meanwhile, implementedFDI hit $4.8 billion during this quarter, increasingby 37% YoY. Overall, the country attracted $22.8billion of total new and additional registered FDI(13% YoY) and got $14.5 billion implemented FDI(17% YoY). Such improvement resulted from thestable macroeconomic backdrop with relatively lowinflation and low interest rates, turning VN into afavorable destination among South East Asiacountries for foreign investors.

The total new and additional registered FDI ofHCMC was also decreased in Q4 2015 with $0.63billion (-54% YoY) as the result of the stronginvestment wave in the previous quarter. In 2015,the city attracted $3.64 billion (13% YoY).

2.6 3.7 3.1 3.5

6.0 4.4 4.5

6.5

3.3 3.5 4.3

9.0

1.8

3.7

11.7

5.60

2.5 2.8 2.9 2.4 2.7 3.0 3.0 2.8 2.9 2.9 3.2 3.5 3.1 3.3 3.4 4.8

-100%

0%

100%

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012 2013 2014 2015

Registered and Implemented FDIin Vietnam

VN New and additional Registered FDI ($ billion)VN Implemented FDIChange of VN implemented FDI (YoY)

$ billion%

Asset Seller BuyerValue

(mil USD) % Trans. Industry

MD Bank MD Bank Maritime Bank N/A N/A Banking

PG Bank PG Bank VietinBank N/A N/A Banking

MHB MHB BIDV 150 100% BankingSounthern

Bank Southern Bank Sacombank N/A N/A BankingHanoi

Landmark Tower Keangnam

Qatar Investment

Authority 800 100% Banking

4 Investment Projects

Indochina Land Holdiings 2

Gaw Capital Partners 106 N/A Real Estate

Celadon City Sacomreal Gamuda Land 64 100% Real Estate

An GiaAn Gia

Investment Creed Group 200 20% Real Estate

Casino Hoi An Vina Capital Chow Tai Fook N/A N/A Hositality

Masan Consumer Holdings &

Masan Brewery Masan Singha 1,100

25% Masan Consumer

Holdings33.3% Masan

Brewery FMCG

The total value of M&A transaction reached $4.3billion in 2015 (40% YoY). Consumer goods, realestate, retails and banking are the most activesectors to the M&A activity in this year.

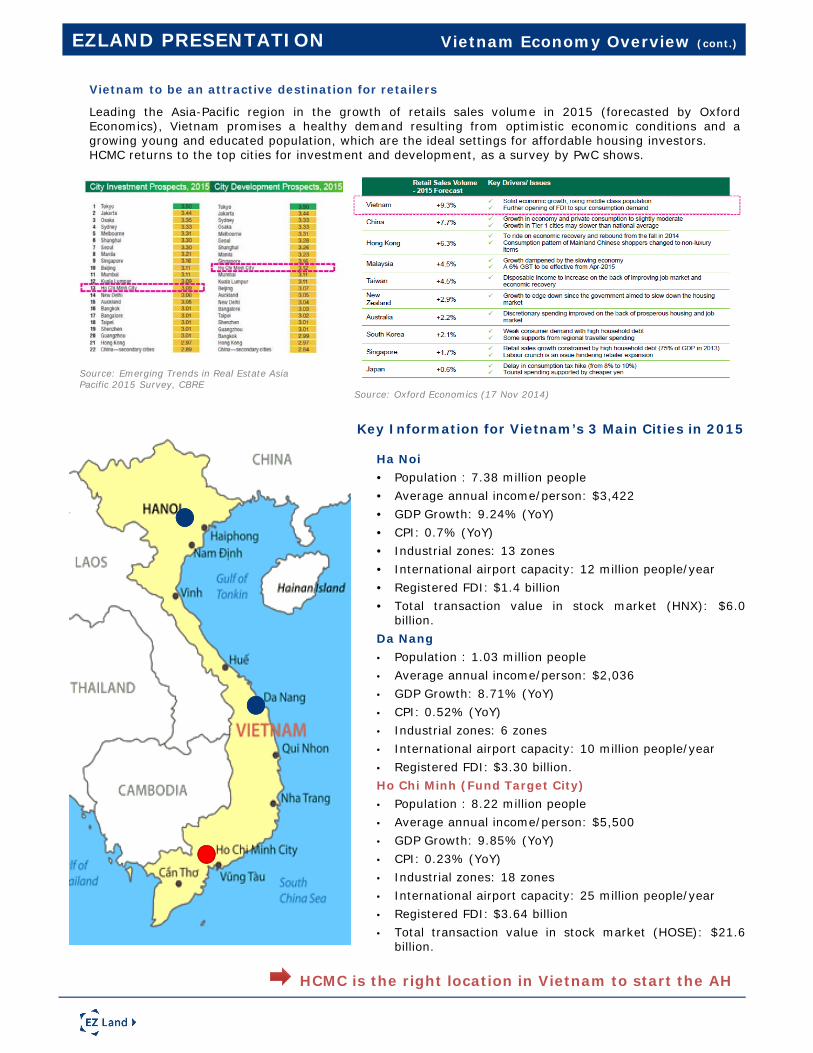

Key Information for Vietnam’s 3 Main Cities in 2015

Ha Noi• Population : 7.38 million people• Average annual income/person: $3,422• GDP Growth: 9.24% (YoY)• CPI: 0.7% (YoY)• Industrial zones: 13 zones• International airport capacity: 12 million people/year• Registered FDI: $1.4 billion• Total transaction value in stock market (HNX): $6.0

billion.Da Nang• Population : 1.03 million people• Average annual income/person: $2,036• GDP Growth: 8.71% (YoY)• CPI: 0.52% (YoY)• Industrial zones: 6 zones• International airport capacity: 10 million people/year• Registered FDI: $3.30 billion.Ho Chi Minh (Fund Target City)• Population : 8.22 million people• Average annual income/person: $5,500• GDP Growth: 9.85% (YoY)• CPI: 0.23% (YoY)• Industrial zones: 18 zones• International airport capacity: 25 million people/year• Registered FDI: $3.64 billion• Total transaction value in stock market (HOSE): $21.6

billion.

HCMC is the right location in Vietnam to start the AH

EZLAND PRESENTATION Vietnam Economy Overview (cont.)

Vietnam to be an attractive destination for retailers

Leading the Asia-Pacific region in the growth of retails sales volume in 2015 (forecasted by OxfordEconomics), Vietnam promises a healthy demand resulting from optimistic economic conditions and agrowing young and educated population, which are the ideal settings for affordable housing investors.HCMC returns to the top cities for investment and development, as a survey by PwC shows.

Source: Emerging Trends in Real Estate Asia Pacific 2015 Survey, CBRE

Source: Oxford Economics (17 Nov 2014)

AFFORDABLE HOUSING FUND

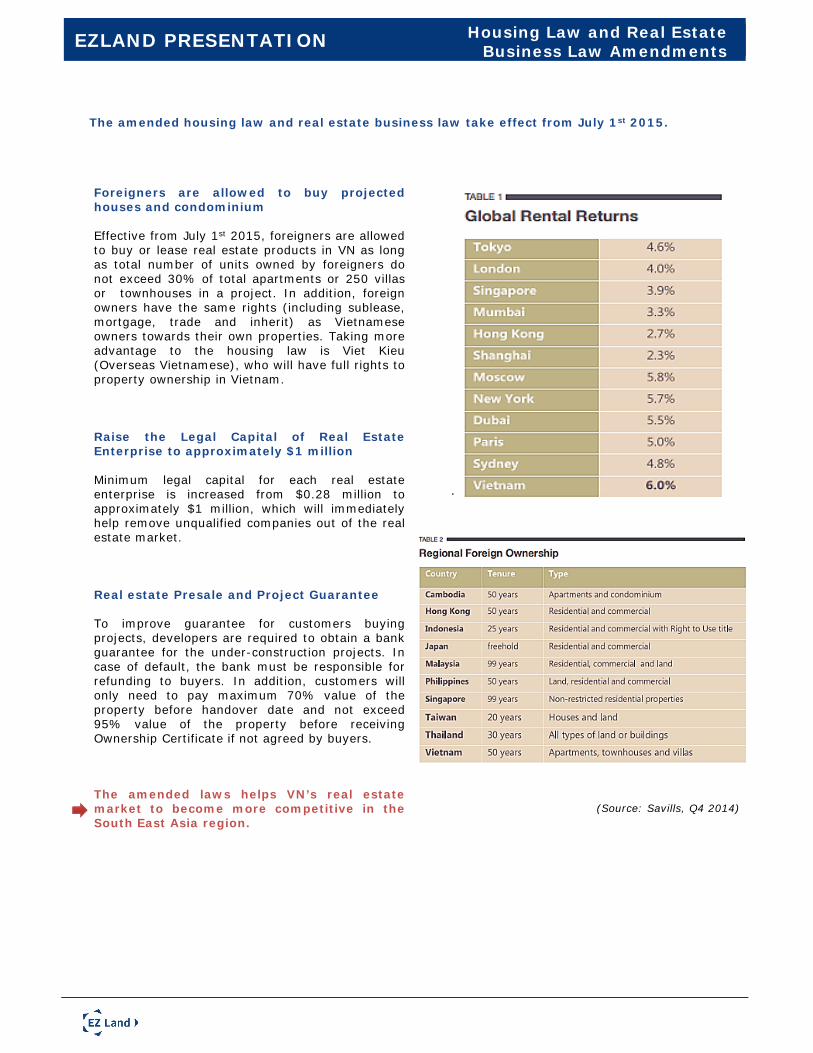

The amended housing law and real estate business law take effect from July 1st 2015.

Foreigners are allowed to buy projectedhouses and condominium

Effective from July 1st 2015, foreigners are allowedto buy or lease real estate products in VN as longas total number of units owned by foreigners donot exceed 30% of total apartments or 250 villasor townhouses in a project. In addition, foreignowners have the same rights (including sublease,mortgage, trade and inherit) as Vietnameseowners towards their own properties. Taking moreadvantage to the housing law is Viet Kieu(Overseas Vietnamese), who will have full rights toproperty ownership in Vietnam.

Raise the Legal Capital of Real EstateEnterprise to approximately $1 million

Minimum legal capital for each real estateenterprise is increased from $0.28 million toapproximately $1 million, which will immediatelyhelp remove unqualified companies out of the realestate market.

Real estate Presale and Project Guarantee

To improve guarantee for customers buyingprojects, developers are required to obtain a bankguarantee for the under-construction projects. Incase of default, the bank must be responsible forrefunding to buyers. In addition, customers willonly need to pay maximum 70% value of theproperty before handover date and not exceed95% value of the property before receivingOwnership Certificate if not agreed by buyers.

The amended laws helps VN’s real estatemarket to become more competitive in theSouth East Asia region.

(Source: Savills, Q4 2014)

EZLAND PRESENTATION Housing Law and Real Estate Business Law Amendments

MARKET UPDATE

Ho Chi Minh

EZLAND PRESENTATION

Page 2 of 19

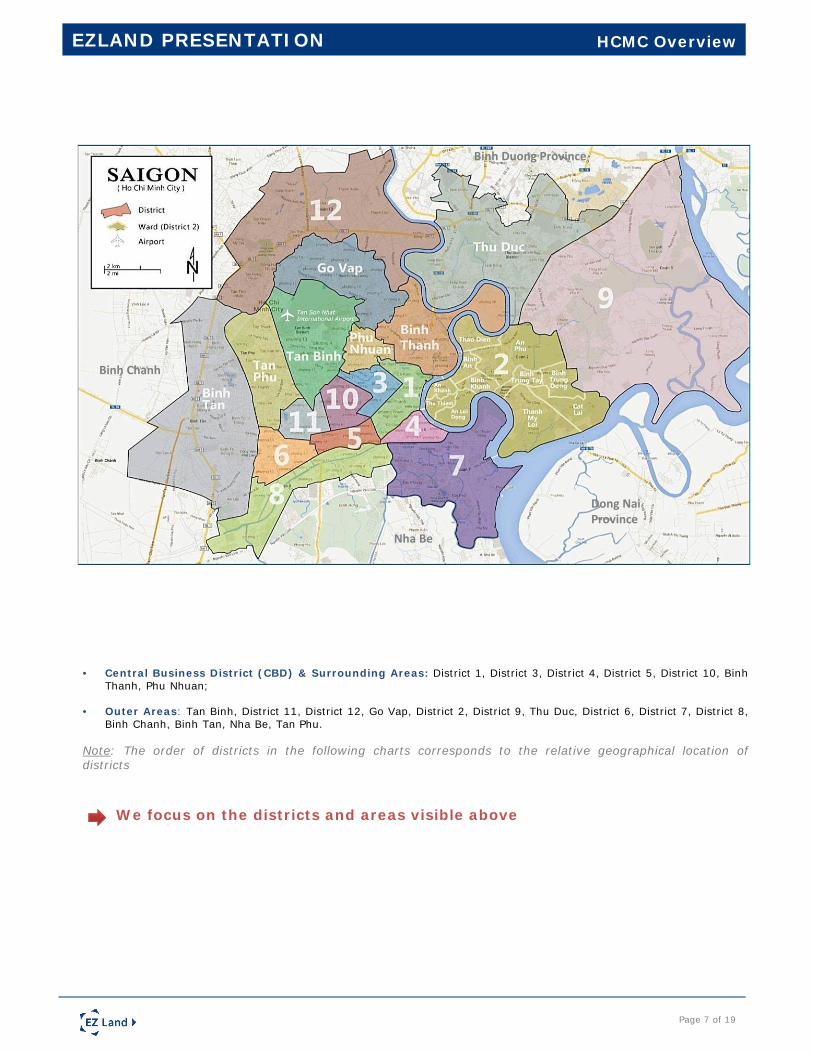

• Central Business District (CBD) & Surrounding Areas: District 1, District 3, District 4, District 5, District 10, BinhThanh, Phu Nhuan;

• Outer Areas: Tan Binh, District 11, District 12, Go Vap, District 2, District 9, Thu Duc, District 6, District 7, District 8,Binh Chanh, Binh Tan, Nha Be, Tan Phu.

Note: The order of districts in the following charts corresponds to the relative geographical location ofdistricts

Binh Chanh

Nha Be

Dong Nai Province

Binh Duong Province

We focus on the districts and areas visible above

Page 7 of 19

EZLAND PRESENTATION HCMC Overview

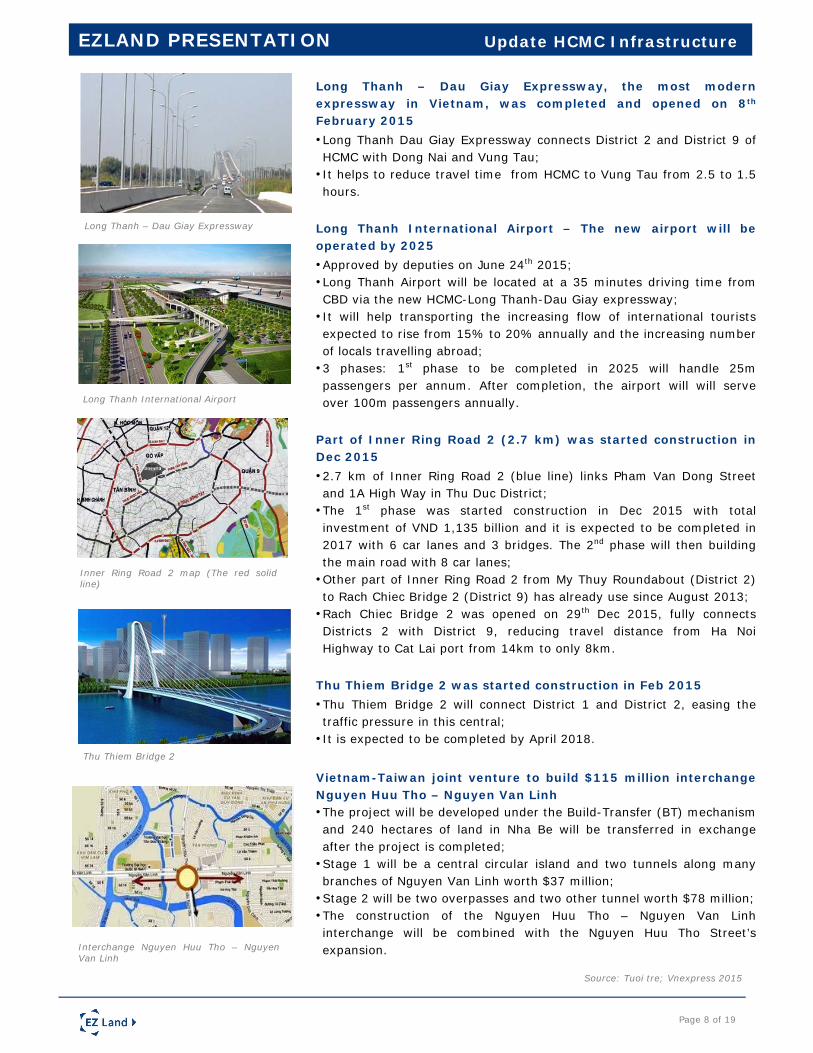

Long Thanh – Dau Giay Expressway, the most modernexpressway in Vietnam, was completed and opened on 8th

February 2015• Long Thanh Dau Giay Expressway connects District 2 and District 9 ofHCMC with Dong Nai and Vung Tau;

• It helps to reduce travel time from HCMC to Vung Tau from 2.5 to 1.5hours.

Long Thanh International Airport – The new airport will beoperated by 2025• Approved by deputies on June 24th 2015;• Long Thanh Airport will be located at a 35 minutes driving time fromCBD via the new HCMC-Long Thanh-Dau Giay expressway;

• It will help transporting the increasing flow of international touristsexpected to rise from 15% to 20% annually and the increasing numberof locals travelling abroad;

• 3 phases: 1st phase to be completed in 2025 will handle 25mpassengers per annum. After completion, the airport will will serveover 100m passengers annually.

Part of Inner Ring Road 2 (2.7 km) was started construction inDec 2015• 2.7 km of Inner Ring Road 2 (blue line) links Pham Van Dong Streetand 1A High Way in Thu Duc District;

• The 1st phase was started construction in Dec 2015 with totalinvestment of VND 1,135 billion and it is expected to be completed in2017 with 6 car lanes and 3 bridges. The 2nd phase will then buildingthe main road with 8 car lanes;

• Other part of Inner Ring Road 2 from My Thuy Roundabout (District 2)to Rach Chiec Bridge 2 (District 9) has already use since August 2013;

• Rach Chiec Bridge 2 was opened on 29th Dec 2015, fully connectsDistricts 2 with District 9, reducing travel distance from Ha NoiHighway to Cat Lai port from 14km to only 8km.

Thu Thiem Bridge 2 was started construction in Feb 2015• Thu Thiem Bridge 2 will connect District 1 and District 2, easing thetraffic pressure in this central;

• It is expected to be completed by April 2018.

Vietnam-Taiwan joint venture to build $115 million interchangeNguyen Huu Tho – Nguyen Van Linh• The project will be developed under the Build-Transfer (BT) mechanismand 240 hectares of land in Nha Be will be transferred in exchangeafter the project is completed;

• Stage 1 will be a central circular island and two tunnels along manybranches of Nguyen Van Linh worth $37 million;

• Stage 2 will be two overpasses and two other tunnel worth $78 million;• The construction of the Nguyen Huu Tho – Nguyen Van Linhinterchange will be combined with the Nguyen Huu Tho Street’sexpansion.

EZLAND PRESENTATION Update HCMC Infrastructure

Long Thanh – Dau Giay Expressway

Thu Thiem Bridge 2

Inner Ring Road 2 map (The red solidline)

Page 8 of 19

Long Thanh International Airport

Source: Tuoi tre; Vnexpress 2015

Interchange Nguyen Huu Tho – NguyenVan Linh

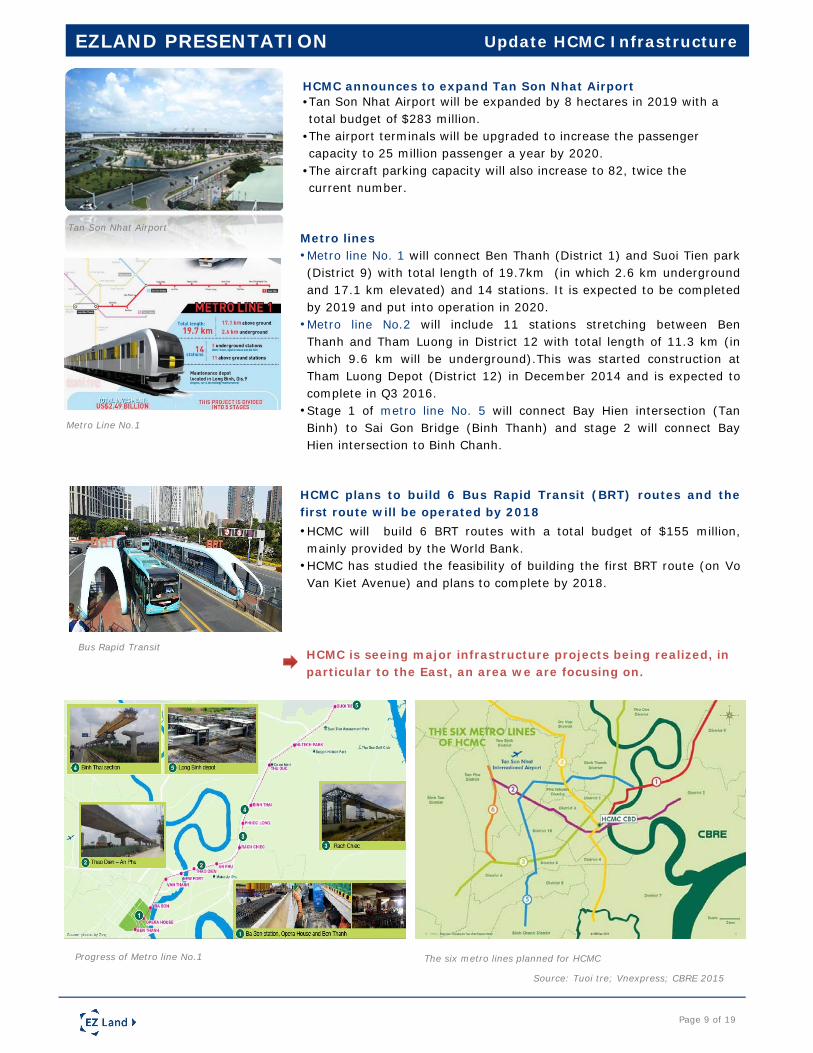

Metro lines• Metro line No. 1 will connect Ben Thanh (District 1) and Suoi Tien park(District 9) with total length of 19.7km (in which 2.6 km undergroundand 17.1 km elevated) and 14 stations. It is expected to be completedby 2019 and put into operation in 2020.

• Metro line No.2 will include 11 stations stretching between BenThanh and Tham Luong in District 12 with total length of 11.3 km (inwhich 9.6 km will be underground).This was started construction atTham Luong Depot (District 12) in December 2014 and is expected tocomplete in Q3 2016.

• Stage 1 of metro line No. 5 will connect Bay Hien intersection (TanBinh) to Sai Gon Bridge (Binh Thanh) and stage 2 will connect BayHien intersection to Binh Chanh.

HCMC plans to build 6 Bus Rapid Transit (BRT) routes and thefirst route will be operated by 2018• HCMC will build 6 BRT routes with a total budget of $155 million,mainly provided by the World Bank.

• HCMC has studied the feasibility of building the first BRT route (on VoVan Kiet Avenue) and plans to complete by 2018.

HCMC is seeing major infrastructure projects being realized, inparticular to the East, an area we are focusing on.

EZLAND PRESENTATION Update HCMC Infrastructure

Page 9 of 19

Bus Rapid Transit

Metro Line No.1

Progress of Metro line No.1 The six metro lines planned for HCMC

Tan Son Nhat Airport

HCMC announces to expand Tan Son Nhat Airport•Tan Son Nhat Airport will be expanded by 8 hectares in 2019 with a total budget of $283 million.

•The airport terminals will be upgraded to increase the passenger capacity to 25 million passenger a year by 2020.

•The aircraft parking capacity will also increase to 82, twice the current number.

Source: Tuoi tre; Vnexpress; CBRE 2015

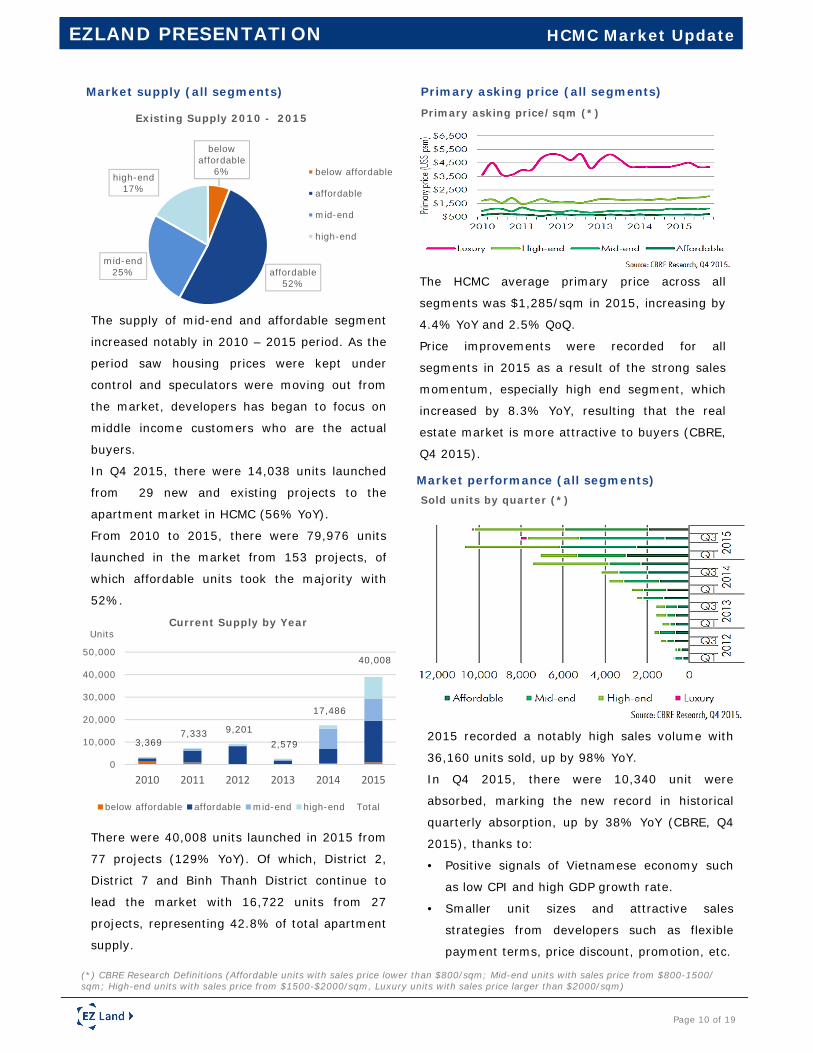

The supply of mid-end and affordable segment

increased notably in 2010 – 2015 period. As the

period saw housing prices were kept under

control and speculators were moving out from

the market, developers has began to focus on

middle income customers who are the actual

buyers.

In Q4 2015, there were 14,038 units launched

from 29 new and existing projects to the

apartment market in HCMC (56% YoY).

From 2010 to 2015, there were 79,976 units

launched in the market from 153 projects, of

which affordable units took the majority with

52%.

There were 40,008 units launched in 2015 from

77 projects (129% YoY). Of which, District 2,

District 7 and Binh Thanh District continue to

lead the market with 16,722 units from 27

projects, representing 42.8% of total apartment

supply.

3,369 7,333 9,201

2,579

17,486

40,008

0

10,000

20,000

30,000

40,000

50,000

2010 2011 2012 2013 2014 2015

Current Supply by Year

below affordable affordable mid-end high-end Total

EZLAND PRESENTATION HCMC Market Update

Page 10 of 19

Market supply (all segments)

The HCMC average primary price across all

segments was $1,285/sqm in 2015, increasing by

4.4% YoY and 2.5% QoQ.

Price improvements were recorded for all

segments in 2015 as a result of the strong sales

momentum, especially high end segment, which

increased by 8.3% YoY, resulting that the real

estate market is more attractive to buyers (CBRE,

Q4 2015).

Primary asking price (all segments)

Primary asking price/sqm (*)

Market performance (all segments)Sold units by quarter (*)

2015 recorded a notably high sales volume with

36,160 units sold, up by 98% YoY.

In Q4 2015, there were 10,340 unit were

absorbed, marking the new record in historical

quarterly absorption, up by 38% YoY (CBRE, Q4

2015), thanks to:

• Positive signals of Vietnamese economy such

as low CPI and high GDP growth rate.

• Smaller unit sizes and attractive sales

strategies from developers such as flexible

payment terms, price discount, promotion, etc.

Units

(*) CBRE Research Definitions (Affordable units with sales price lower than $800/sqm; Mid-end units with sales price from $800-1500/ sqm; High-end units with sales price from $1500-$2000/sqm, Luxury units with sales price larger than $2000/sqm)

below affordable

6%

affordable52%

mid-end25%

high-end17%

Existing Supply 2010 - 2015

below affordable

affordable

mid-end

high-end

500

700

900

1,100

Affordable Average Asking Price/sqm Q4 2015 by District

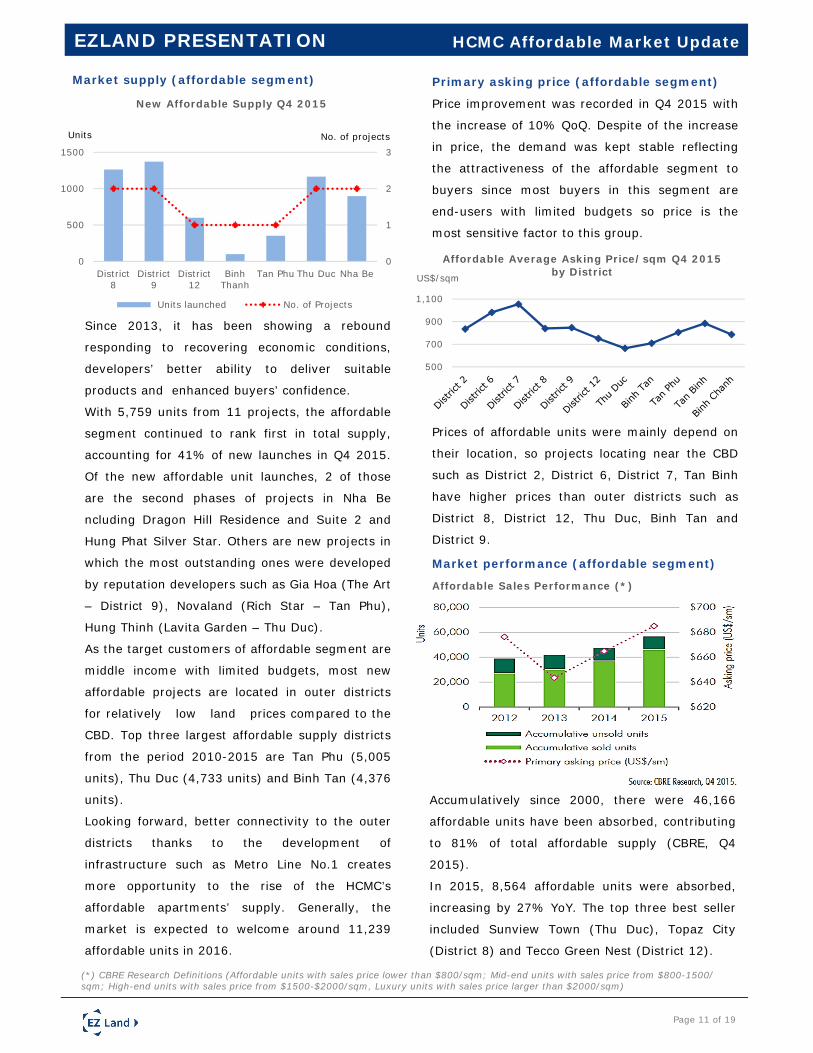

Since 2013, it has been showing a rebound

responding to recovering economic conditions,

developers’ better ability to deliver suitable

products and enhanced buyers’ confidence.

With 5,759 units from 11 projects, the affordable

segment continued to rank first in total supply,

accounting for 41% of new launches in Q4 2015.

Of the new affordable unit launches, 2 of those

are the second phases of projects in Nha Be

ncluding Dragon Hill Residence and Suite 2 and

Hung Phat Silver Star. Others are new projects in

which the most outstanding ones were developed

by reputation developers such as Gia Hoa (The Art

– District 9), Novaland (Rich Star – Tan Phu),

Hung Thinh (Lavita Garden – Thu Duc).

As the target customers of affordable segment are

middle income with limited budgets, most new

affordable projects are located in outer districts

for relatively low land prices compared to the

CBD. Top three largest affordable supply districts

from the period 2010-2015 are Tan Phu (5,005

units), Thu Duc (4,733 units) and Binh Tan (4,376

units).

Looking forward, better connectivity to the outer

districts thanks to the development of

infrastructure such as Metro Line No.1 creates

more opportunity to the rise of the HCMC’s

affordable apartments’ supply. Generally, the

market is expected to welcome around 11,239

affordable units in 2016.

Market supply (affordable segment)

EZLAND PRESENTATION HCMC Affordable Market Update

Prices of affordable units were mainly depend on

their location, so projects locating near the CBD

such as District 2, District 6, District 7, Tan Binh

have higher prices than outer districts such as

District 8, District 12, Thu Duc, Binh Tan and

District 9.

Page 11 of 19

Accumulatively since 2000, there were 46,166

affordable units have been absorbed, contributing

to 81% of total affordable supply (CBRE, Q4

2015).

In 2015, 8,564 affordable units were absorbed,

increasing by 27% YoY. The top three best seller

included Sunview Town (Thu Duc), Topaz City

(District 8) and Tecco Green Nest (District 12).

Market performance (affordable segment)

Units No. of projects

Primary asking price (affordable segment)

US$/sqm

Price improvement was recorded in Q4 2015 with

the increase of 10% QoQ. Despite of the increase

in price, the demand was kept stable reflecting

the attractiveness of the affordable segment to

buyers since most buyers in this segment are

end-users with limited budgets so price is the

most sensitive factor to this group.

0

1

2

3

0

500

1000

1500

District8

District9

District12

BinhThanh

Tan Phu Thu Duc Nha Be

New Affordable Supply Q4 2015

Units launched No. of Projects

(*) CBRE Research Definitions (Affordable units with sales price lower than $800/sqm; Mid-end units with sales price from $800-1500/ sqm; High-end units with sales price from $1500-$2000/sqm, Luxury units with sales price larger than $2000/sqm)

Affordable Sales Performance (*)

EZLAND PRESENTATION HCMC Affordable Market Update

Page 12 of 19

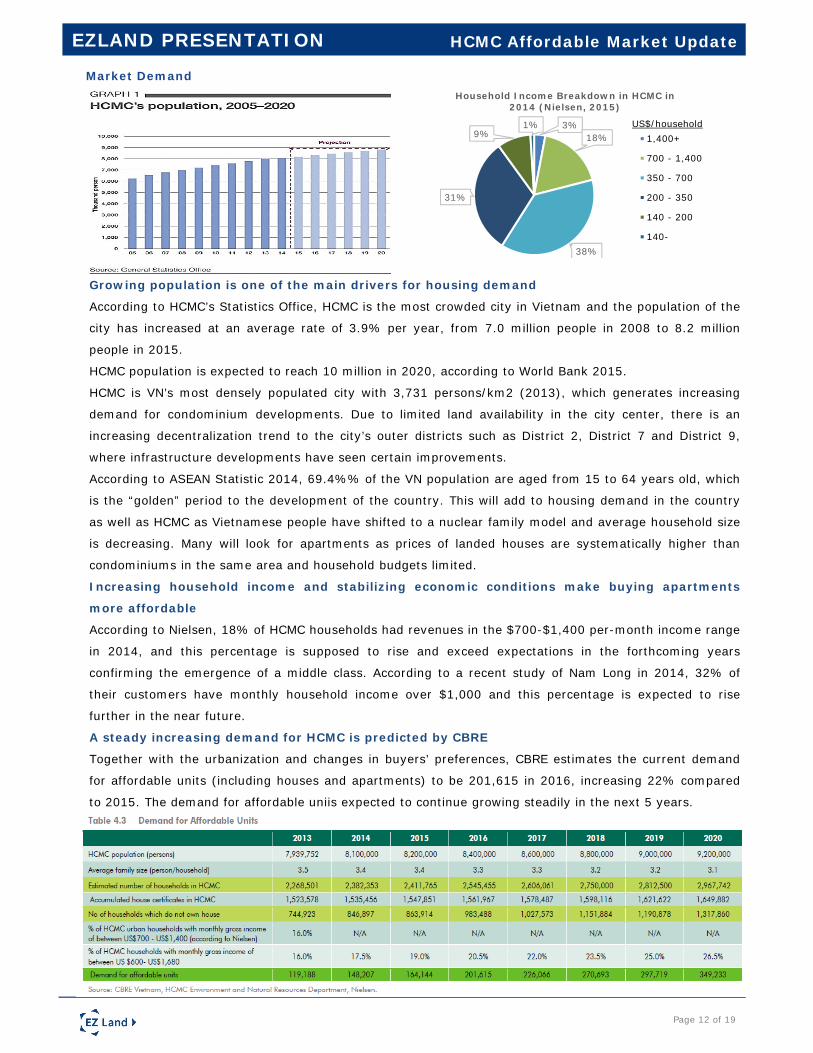

Market Demand

Growing population is one of the main drivers for housing demand

According to HCMC’s Statistics Office, HCMC is the most crowded city in Vietnam and the population of the

city has increased at an average rate of 3.9% per year, from 7.0 million people in 2008 to 8.2 million

people in 2015.

HCMC population is expected to reach 10 million in 2020, according to World Bank 2015.

HCMC is VN’s most densely populated city with 3,731 persons/km2 (2013), which generates increasing

demand for condominium developments. Due to limited land availability in the city center, there is an

increasing decentralization trend to the city’s outer districts such as District 2, District 7 and District 9,

where infrastructure developments have seen certain improvements.

According to ASEAN Statistic 2014, 69.4%% of the VN population are aged from 15 to 64 years old, which

is the “golden” period to the development of the country. This will add to housing demand in the country

as well as HCMC as Vietnamese people have shifted to a nuclear family model and average household size

is decreasing. Many will look for apartments as prices of landed houses are systematically higher than

condominiums in the same area and household budgets limited.

Increasing household income and stabilizing economic conditions make buying apartments

more affordable

According to Nielsen, 18% of HCMC households had revenues in the $700-$1,400 per-month income range

in 2014, and this percentage is supposed to rise and exceed expectations in the forthcoming years

confirming the emergence of a middle class. According to a recent study of Nam Long in 2014, 32% of

their customers have monthly household income over $1,000 and this percentage is expected to rise

further in the near future.

A steady increasing demand for HCMC is predicted by CBRE

Together with the urbanization and changes in buyers’ preferences, CBRE estimates the current demand

for affordable units (including houses and apartments) to be 201,615 in 2016, increasing 22% compared

to 2015. The demand for affordable uniis expected to continue growing steadily in the next 5 years.

3%18%

38%

31%

9%1%

Household Income Breakdown in HCMC in 2014 (Nielsen, 2015)

1,400+

700 - 1,400

350 - 700

200 - 350

140 - 200

140-

US$/household

10.2%10.5%10.5%10.5%10.5%

11.0%11.5%11.5%

12.0%12.5%12.5%12.5%

11.5%11.0%11.0%

10.4%

9.5% 9.5%10.0%

9.5%

9%

11%

13%

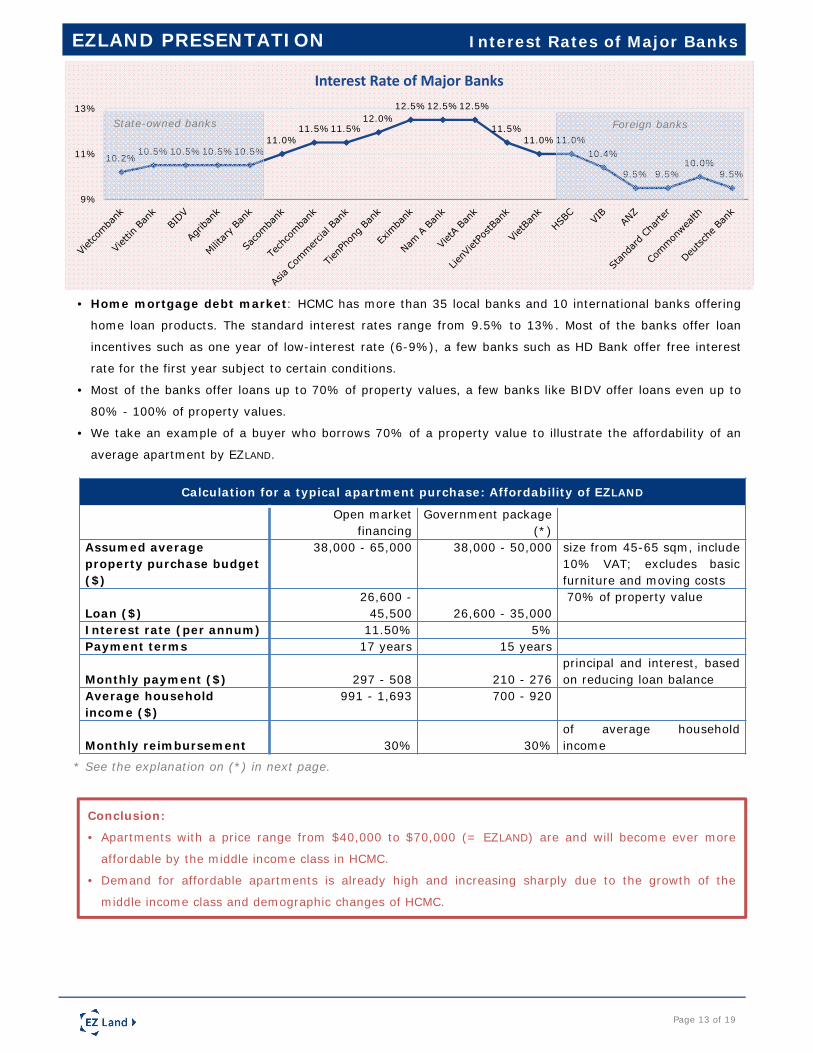

Interest Rate of Major Banks

• Home mortgage debt market: HCMC has more than 35 local banks and 10 international banks offering

home loan products. The standard interest rates range from 9.5% to 13%. Most of the banks offer loan

incentives such as one year of low-interest rate (6-9%), a few banks such as HD Bank offer free interest

rate for the first year subject to certain conditions.

• Most of the banks offer loans up to 70% of property values, a few banks like BIDV offer loans even up to

80% - 100% of property values.

• We take an example of a buyer who borrows 70% of a property value to illustrate the affordability of an

average apartment by EZLAND.

Calculation for a typical apartment purchase: Affordability of EZLAND

Open market financing

Government package (*)

Assumed average property purchase budget($)

38,000 - 65,000 38,000 - 50,000 size from 45-65 sqm, include10% VAT; excludes basicfurniture and moving costs

Loan ($)26,600 -

45,500 26,600 - 35,00070% of property value

Interest rate (per annum) 11.50% 5%Payment terms 17 years 15 years

Monthly payment ($) 297 - 508 210 - 276principal and interest, basedon reducing loan balance

Average household income ($)

991 - 1,693 700 - 920

Monthly reimbursement 30% 30%of average householdincome

Conclusion:

• Apartments with a price range from $40,000 to $70,000 (= EZLAND) are and will become ever more

affordable by the middle income class in HCMC.

• Demand for affordable apartments is already high and increasing sharply due to the growth of the

middle income class and demographic changes of HCMC.

EZLAND PRESENTATION Interest Rates of Major Banks

Page 13 of 19

State-owned banks Foreign banks

* See the explanation on (*) in next page.

EZLAND PRESENTATION Affordable Condominium Shortfall

Page 14 of 19

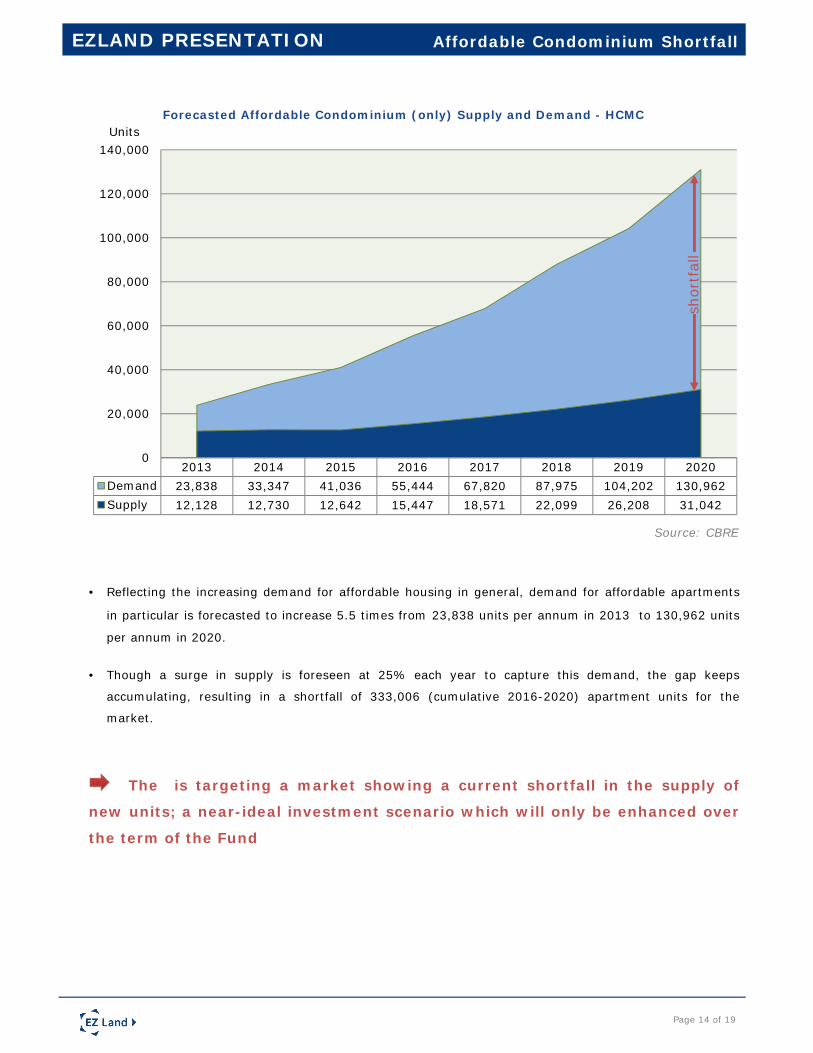

2013 2014 2015 2016 2017 2018 2019 2020Demand 23,838 33,347 41,036 55,444 67,820 87,975 104,202 130,962Supply 12,128 12,730 12,642 15,447 18,571 22,099 26,208 31,042

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Forecasted Affordable Condominium (only) Supply and Demand - HCMCUnits

Source: CBRE

• Reflecting the increasing demand for affordable housing in general, demand for affordable apartments

in particular is forecasted to increase 5.5 times from 23,838 units per annum in 2013 to 130,962 units

per annum in 2020.

• Though a surge in supply is foreseen at 25% each year to capture this demand, the gap keeps

accumulating, resulting in a shortfall of 333,006 (cumulative 2016-2020) apartment units for the

market.

The is targeting a market showing a current shortfall in the supply of

new units; a near-ideal investment scenario which will only be enhanced over

the term of the Fund

shor

tfal

l

EZLAND PRESENTATION

Page 19 of 19

THANK YOU!

Contact us

Address: Suite 2105, Melinh Point Tower, No. 2 Ngo Duc Ke Street, District 1, HCMC, VietnamTel: (08) 3827 5000Fax: (08) 3827 5050

© 2016 EZLAND Vietnam Co., Ltd. All materials presented in this report, unless specifically indicated otherwise, is under copyright and proprietary to EZLAND. Information contained herein, including projections, has been obtained from materials and sources believed to be reliable at the date of publication. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. Readers are for EZLAND professionals, and is not to be used or considered as an offer or the solicitation of an offer to sell or buy or subscribe for securities irresponsible for independently assessing the relevance, accuracy, completeness and currency of the information of this publication. This report is presented for information purposes only, exclusively r other financial instruments. All rights to the material are reserved and none of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party without prior express written permission of EZLAND. Any unauthorized publication or redistribution of EZLAND research reports is prohibited. EZLAND will not be liable for any loss, damage, cost or expense incurred or arising by reason of any person using or relying on information in this publication.