Embed Size (px)

Citation preview

Page

March 2016

1

Keysight TechnologiesInvestor Presentation

Page 2

This presentation contains forward-looking statements including, without limitation, statements

regarding trends, seasonality, cyclicality and growth in, and drivers of, the markets we sell into, our

strategic direction, our future effective tax rate and tax valuation allowance, earnings from our foreign

subsidiaries, remediation activities, new product and service introductions, the ability of our products to

meet market needs, changes to our manufacturing processes, the use of contract manufacturers, the

impact of local government regulations on our ability to pay vendors or conduct operations, our liquidity

position, our ability to generate cash from operations, growth in our businesses, our investments, our

stock repurchase program, the potential impact of adopting new accounting pronouncements, our

financial results, our purchase commitments, our contributions to our pension plans, the selection of

discount rates and recognition of any gains or losses for our benefit plans, our cost-control activities,

savings and headcount reduction recognized from our restructuring programs and other cost saving

initiatives, and other regulatory approvals, the integration of our acquisitions and other transactions, our

transition to lower-cost regions, and the existence of economic instability, that involve risks and

uncertainties. Our actual results could differ materially from the results contemplated by these forward-

looking statements due to various factors, including those discussed in our Quarterly Report on Form

10-Q filed with the Securities and Exchange Commission on March 4, 2016.

Safe Harbor

Page 3

Executive Overview

4 Growth Initiatives – Wireless, Modular, Software and Services

Advanced Manufacturing Strategy & Capabilities

Agenda

Page

KEYSIGHT TODAY:

Market and Technology Leader

4

17%

49%

34%

18%

44%

38%

FY15 Revenue by Geography(1)

~10,250 Headcount

Americas

Europe

Asia Pacific

Europe

Asia Pacific

Americas

~15,500Number of customers(2)

100+Countries served

13Countries with R&D centers

$2.9BFY15 Revenue(1)

19.5%FY15 Operating Margin(1)

Data as of October 31, 2015

(1) Non-GAAP measure

(2) Excludes indirect channels

(3) Sites with greater than 70 manufacturing employees

3Manufacturing sites(3)

$2.52 FY15 EPS(1)

Page

Our Value to Customers - Unmatched in the Industry

5

We help customers bring breakthrough electronic

products to market faster and at a lower cost

Simulate Manufacture OptimizePrototype

RadarAvionics Surveillance Satellites

ComputersAutomotive electronics

Wireless base stations

Cloud devices & interfaces

Smart phones

Customer Lifecycle

Page

The Keysight AdvantageCommitment to Value Creation

6

Technology and market leader in ever-evolving technology

market

Leader in profitable

market

Target fast growing areas and expand Served

Addressable Market (SAM)

Proven operating performance and cash generation

across cycles

Transform for

growth

Strong business

model

6

Page

• U.S. Cash

Generation

• Appropriate

Leverage

• Strategic

Alignment

• Growth

• Value

Creation

• Cost Structure

Flexibility

• Cost

Reductions

• Margin

Expansion

• R&D

Investment

• SAM

Expansion

• Profit

Leverage

A Strong Framework for Value Creation

7

OrganicGrowth

Business Model

Mergers & Acquisitions

Return of Capital

Page

Building Strong Track Record as Independent Public Company

8

Post-Separation Stabilization Complete

• 6 months ahead of plan

Transforming for Growth

• Organizational realignment to end markets

• Progress on growth initiatives

• Investing prudently

Leveraging the Business Model

• Solid Financial Results FY’15 & Q1’16

• Flexing the cost structure

Executing Strategy and Effectively Deploying Capital

• Anite and Electroservices acquisitions

• Increased R&D investment

• Announced share repurchase

New

New

Page

• Complete

wireless

ecosystem

• Aerospace &

Defense

• Automotive

• Energy

• Semiconductor

• General

Electronics

• Repair &

Calibration

• Asset

Management

• Professional

Services

• Remarketing

• Americas

• Europe

• Asia

• Japan

• Software

Technology

• Hardware

Technology

Organizing to Grow

9

Communications

Solutions Group

Industrial

Solutions Group

Services

Solutions Group

Mike

Gasparian

Gooi Soon

Chai

John Page

Worldwide Sales

Guy

Séné

Corporate

Planning and

Technology

Jay

Alexander

Aligned with End MarketsFirst to Market Trusted Advisor

New

Page

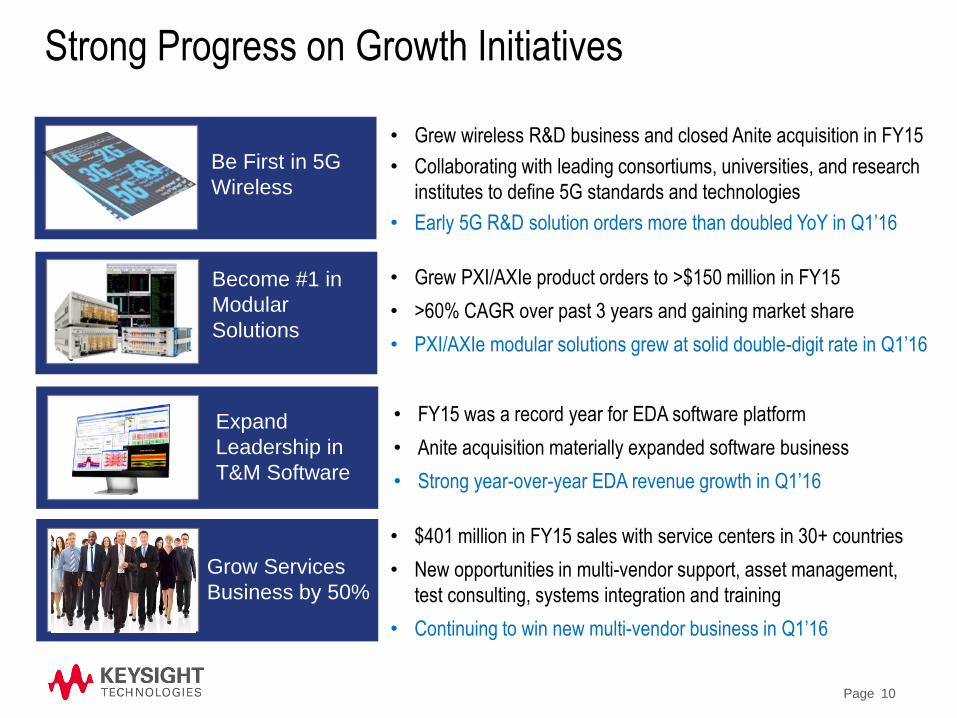

Strong Progress on Growth Initiatives

10

Be First in 5G

Wireless

Become #1 in

Modular

Solutions

Expand

Leadership in

T&M Software

Grow Services

Business by 50%

• Grew PXI/AXIe product orders to >$150 million in FY15

• >60% CAGR over past 3 years and gaining market share

• PXI/AXIe modular solutions grew at solid double-digit rate in Q1’16

• Grew wireless R&D business and closed Anite acquisition in FY15

• Collaborating with leading consortiums, universities, and research

institutes to define 5G standards and technologies

• Early 5G R&D solution orders more than doubled YoY in Q1’16

• FY15 was a record year for EDA software platform

• Anite acquisition materially expanded software business

• Strong year-over-year EDA revenue growth in Q1’16

• $401 million in FY15 sales with service centers in 30+ countries

• New opportunities in multi-vendor support, asset management,

test consulting, systems integration and training

• Continuing to win new multi-vendor business in Q1’16

Page

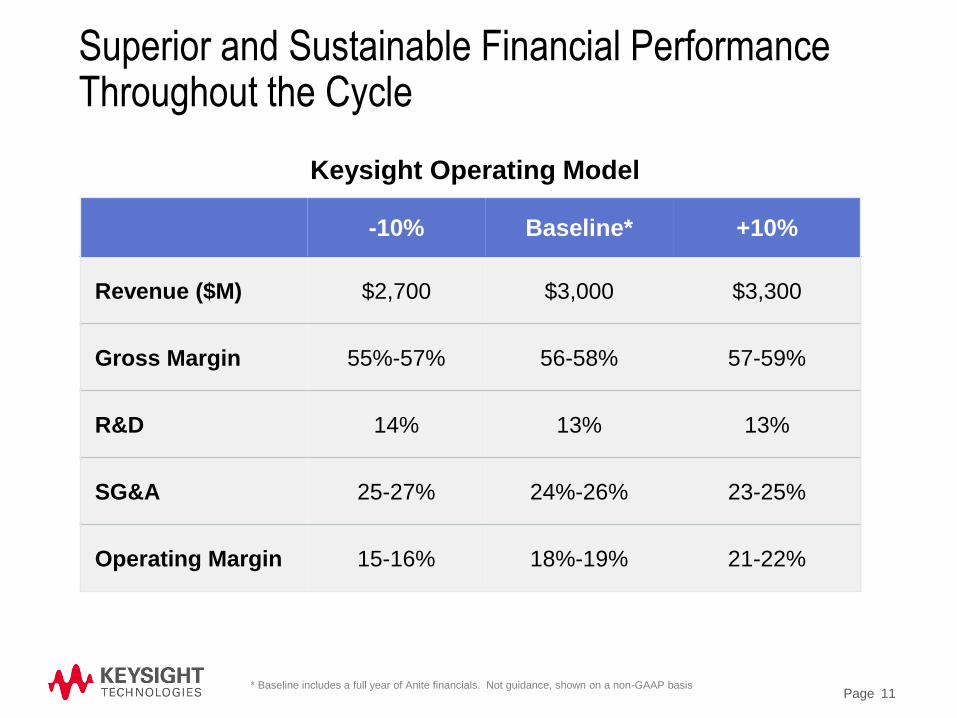

Superior and Sustainable Financial Performance Throughout the Cycle

11

-10% Baseline* +10%

Revenue ($M) $2,700 $3,000 $3,300

Gross Margin 55%-57% 56-58% 57-59%

R&D 14% 13% 13%

SG&A 25-27% 24%-26% 23-25%

Operating Margin 15-16% 18%-19% 21-22%

Keysight Operating Model

* Baseline includes a full year of Anite financials. Not guidance, shown on a non-GAAP basis

Page

Long-Term Expectations

12

RevenueGrowth

Op MarginIncremental

ProfitabilityOver the Cycle

Sustainable

4% CAGR

40% on

growth of 4%

or greater

Average

operating margin

of >20%*

Committed Return of Capital

Yields 8-10% EPS* Growth

* Non-GAAP

Page

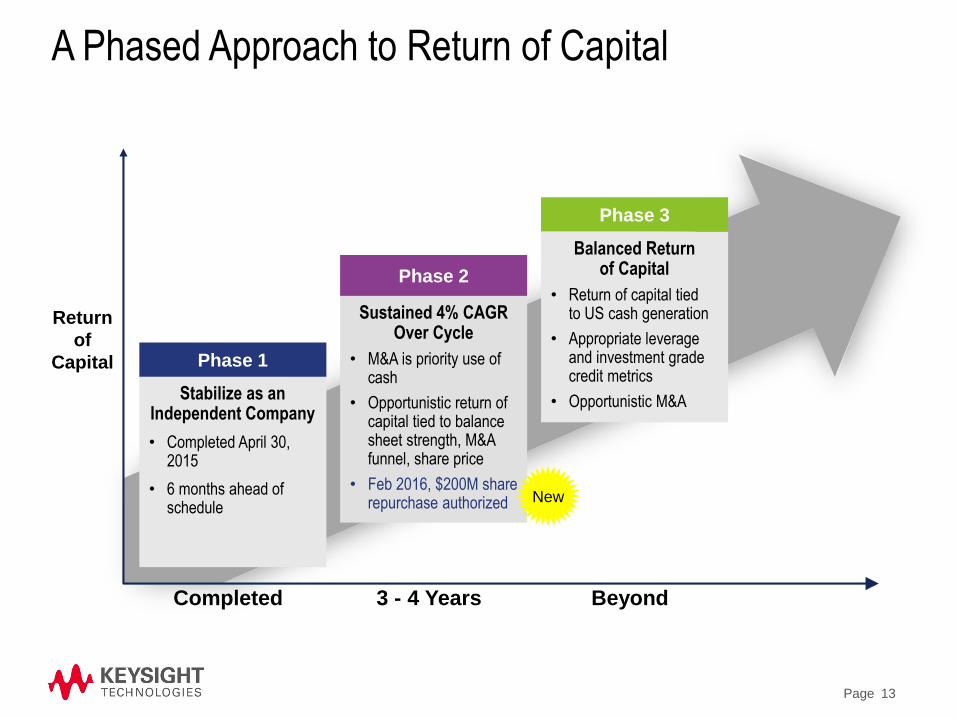

A Phased Approach to Return of Capital

13

Completed 3 - 4 Years Beyond

Stabilize as an Independent Company

• Completed April 30, 2015

• 6 months ahead of schedule

Phase 1

Sustained 4% CAGR Over Cycle

• M&A is priority use of cash

• Opportunistic return of capital tied to balance sheet strength, M&A funnel, share price

• Feb 2016, $200M share repurchase authorized

Phase 2

Balanced Returnof Capital

• Return of capital tied to US cash generation

• Appropriate leverage and investment grade credit metrics

• Opportunistic M&A

Phase 3

Return

of

Capital

New

Page

• Aligns with strategic growth priorities

• Increases proportion of total revenue from R&D market

• Expands Served Addressable Market (SAM)

• Focuses on faster growing market segments

or adds key technology

• ROIC materially above cost of capital (15% by year 5)

• Quickly accretive (within 18 months)

• Valuation aligns with appropriate market multiples

Keysight’s Discipline and Clear Criteria for Acquisitions

14

Strategic

Alignment

Value

Creation

Growth

The Example

Page

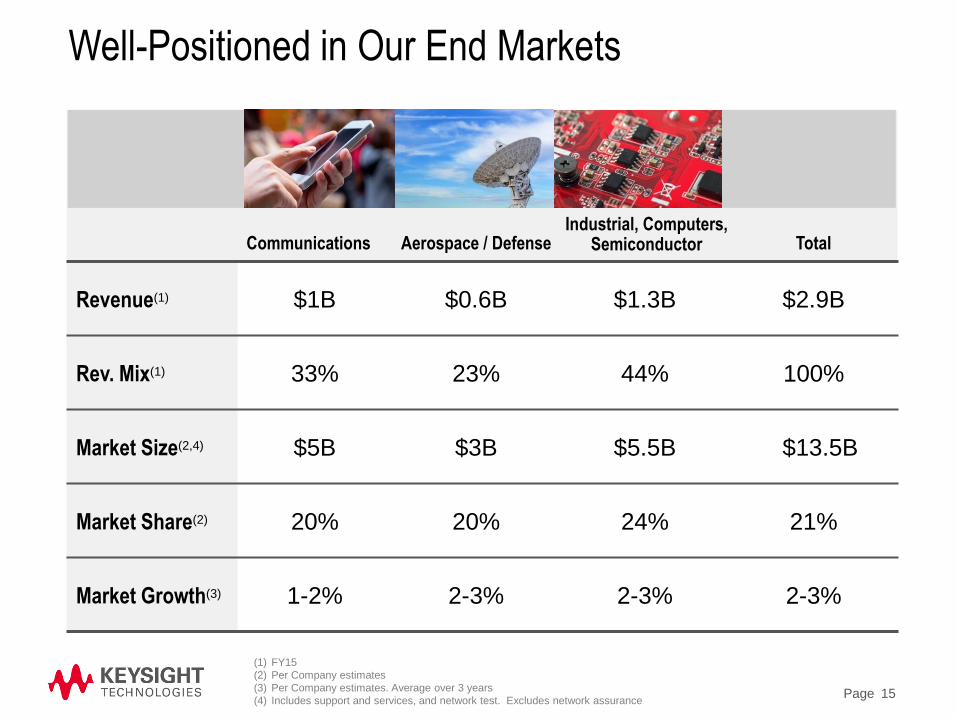

Well-Positioned in Our End Markets

15

Communications Aerospace / DefenseIndustrial, Computers,

Semiconductor

Revenue(1) $1B $0.6B $1.3B $2.9B

Rev. Mix(1) 33% 23% 44% 100%

Market Size(2,4) $5B $3B $5.5B $13.5B

Market Share(2) 20% 20% 24% 21%

Market Growth(3) 1-2% 2-3% 2-3% 2-3%

(1) FY15

(2) Per Company estimates

(3) Per Company estimates. Average over 3 years

(4) Includes support and services, and network test. Excludes network assurance

Total

Page

Why Electronic Design and Test is an Attractive Industry for Keysight

16

New Customer Needs

Deep Experience Required

Large Installed Base

Intellectual Property

Operational Excellence

Strong Profit & Cash Flow

• Drive evolving electronic design and

test solutions

• Technical knowledge gained only through

years of practical experience

• Well-positioned with loyal customers

• Performance advantages from proprietary

semiconductor technologies

• Optimized manufacturing and supply chain

• Delivering 18-19% operating margins over

cycle and strong cash flow

SAM Expansion• Opportunity to expand SAM in adjacent

markets

Page

Multiple Growth Drivers Provide Diversification

17

Growth Drivers

Communications• Evolving standards

• All data, all the time

• Internet of Things

Aerospace / Defense• World instability

• Defense modernization

Industrial • Electronic content proliferation

Computer• Services, data access

• Cloud computing

Semiconductor • World-wide demand

Services and Support • Customer outsourcing

Page

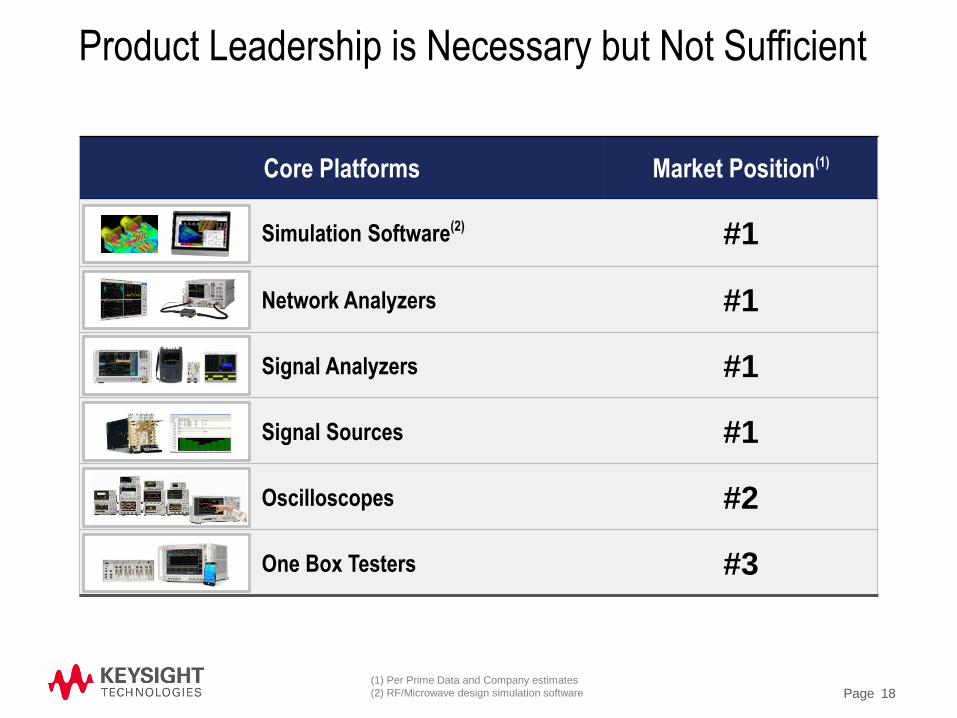

Core Platforms Market Position(1)

Simulation Software(2) #1

Network Analyzers #1

Signal Analyzers #1

Signal Sources #1

Oscilloscopes #2

One Box Testers #3

Product Leadership is Necessary but Not Sufficient

18(1) Per Prime Data and Company estimates

(2) RF/Microwave design simulation software

Page 19

Executive Overview

4 Growth Initiatives – Wireless, Modular, Software and Services

Advanced Manufacturing Strategy & Capabilities

Agenda

Page

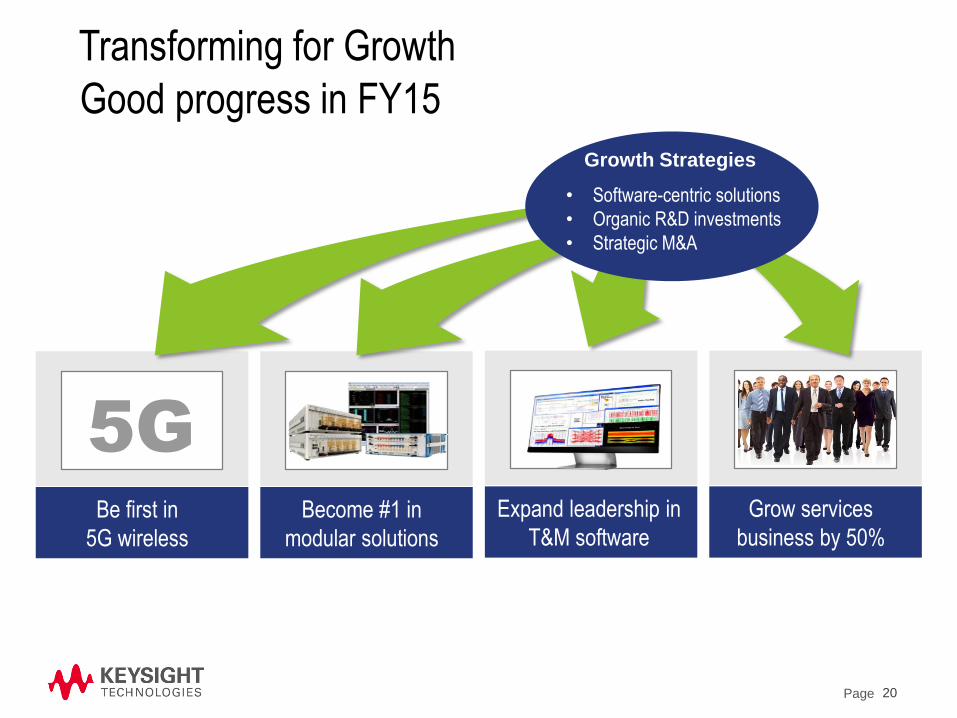

Transforming for Growth

Good progress in FY15

20

Be first in

5G wireless

Growth Strategies

Become #1 in

modular solutions

Expand leadership in

T&M software

Grow services

business by 50%

• Software-centric solutions

• Organic R&D investments

• Strategic M&A

5G

Page

Wireless & Software Growth Initiatives

21

Page

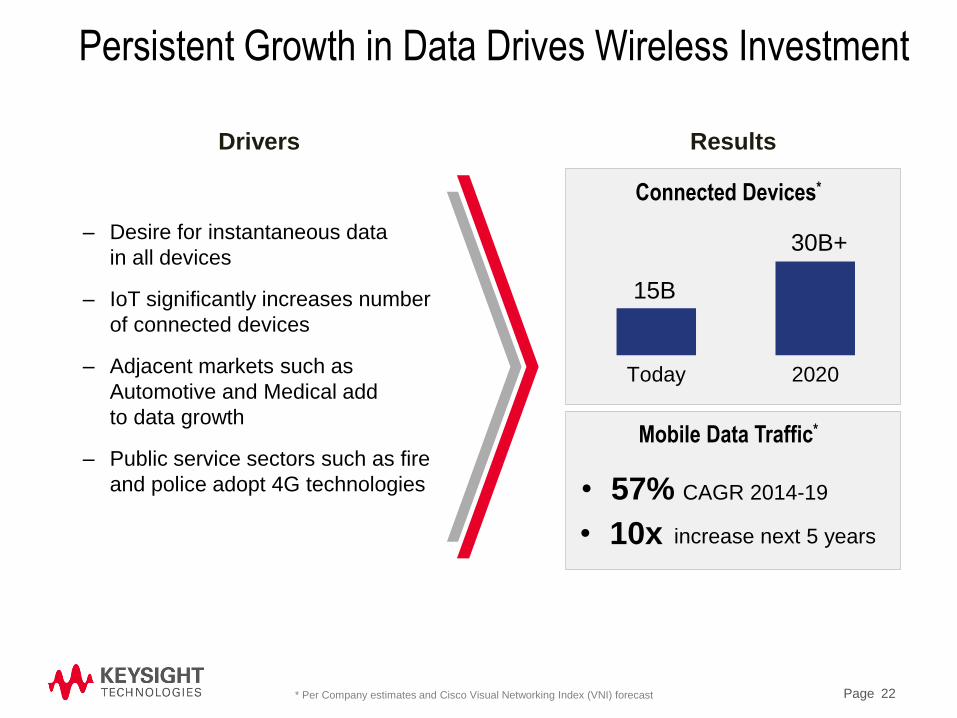

Persistent Growth in Data Drives Wireless Investment

22

– Desire for instantaneous data

in all devices

– IoT significantly increases number

of connected devices

– Adjacent markets such as

Automotive and Medical add

to data growth

– Public service sectors such as fire

and police adopt 4G technologies

30B+

Mobile Data Traffic*

15B

Drivers Results

• 57% CAGR 2014-19

• 10x increase next 5 years

Today 2020

Connected Devices*

* Per Company estimates and Cisco Visual Networking Index (VNI) forecast

Page

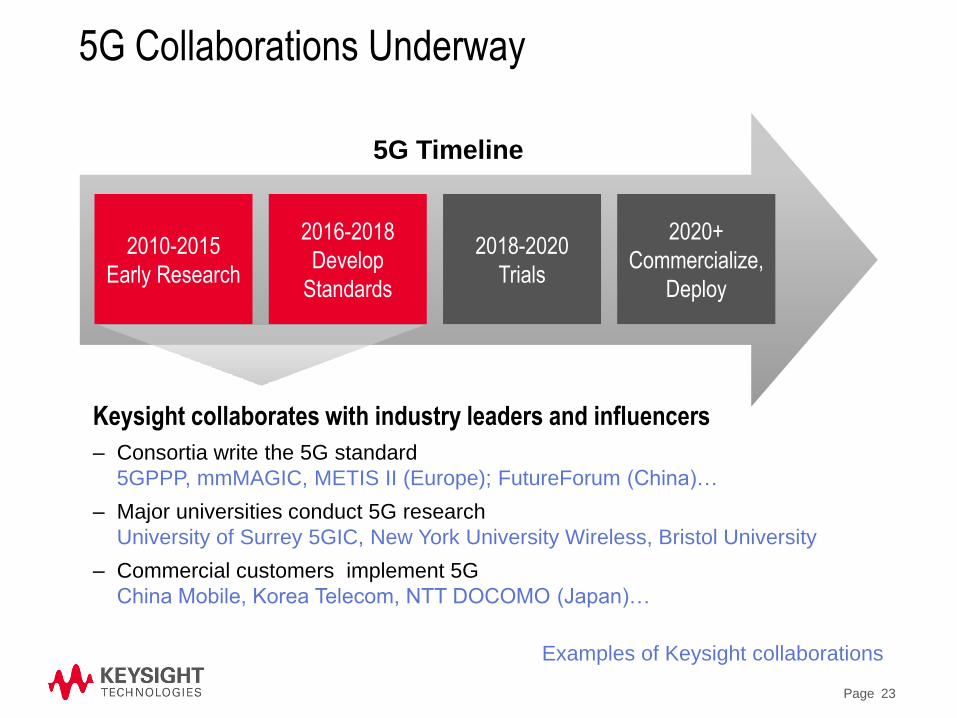

5G Collaborations Underway

23

Keysight collaborates with industry leaders and influencers

– Consortia write the 5G standard

5GPPP, mmMAGIC, METIS II (Europe); FutureForum (China)…

– Major universities conduct 5G research

University of Surrey 5GIC, New York University Wireless, Bristol University

– Commercial customers implement 5G

China Mobile, Korea Telecom, NTT DOCOMO (Japan)…

5G Timeline

2010-2015

Early Research

2016-2018

Develop

Standards

2018-2020

Trials

2020+

Commercialize,

Deploy

Examples of Keysight collaborations

Page

Delivering First-to-Market Solutions for 5G

24

Keysight introduced 10 targeted 5G

solutions in the past year

Simulate Prototype Manufacture Optimize

Ramping in 1-3 years

Page

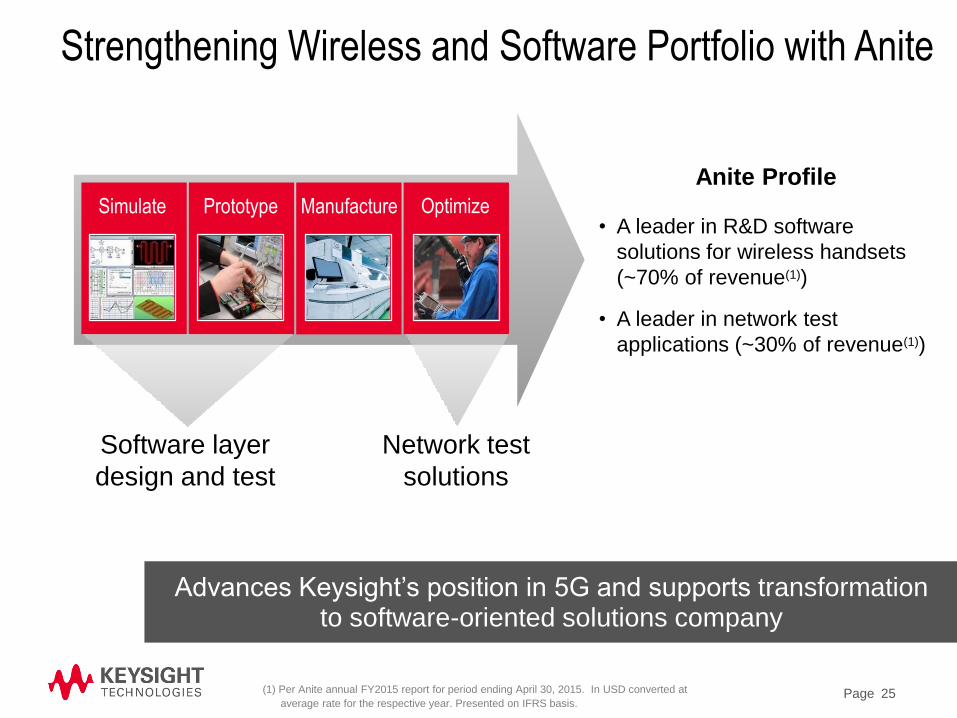

Advances Keysight’s position in 5G and supports transformationto software-oriented solutions company

Strengthening Wireless and Software Portfolio with Anite

25

Anite Profile

• A leader in R&D software

solutions for wireless handsets

(~70% of revenue(1))

• A leader in network test

applications (~30% of revenue(1))

Software layer

design and test

Network test

solutions

Simulate Prototype Manufacture Optimize

(1) Per Anite annual FY2015 report for period ending April 30, 2015. In USD converted at

average rate for the respective year. Presented on IFRS basis.

Page

Simulate Prototype Manufacture Optimize

Simulation Software Measurement Software

Keysight’s Software Business Today –Well-Positioned and Growing

26

– Revenues over $400M*

– $2B market for electronic test software, ~7% CAGR*

– Gross margins ~30 points above Keysight aggregate

– Growth opportunities across all end markets

* FY15. Per Company estimates. Includes full year of Anite

Page

Anite Expands Keysight’s Software Revenue Mix

27

Anite’s revenue mix advances the shift toward software

Anite Revenue Mix(2)Keysight Revenue Mix(1)

SW

Services

HW

HW

SW

(1) FY15

(2) Per Anite 2015 annual report ending April 30, 2015. Includes product software and IP licenses,

plus software maintenance and support.

Page

Software Growth Strategy

28

Expand simulation business− to address growth opportunities in High-Speed

Digital and Power design

Deliver solutions focused on growth segments− deliver R&D (prototype test) solutions focused on

growth segments such as 5G Communications,

Power, and Automotive

Pursue selective acquisitions − like Anite to increase our overall software content

Grow subscriptions and services− implement software capabilities to enable revenue

growth from subscriptions and from services

Page

Modular Solutions Growth Initiative

29

Page

Keysight Intends to be #1 in Modular Solutions

30

Keysight is growing much faster than

overall modular solutions market

Keysight has a highly differentiated position

Keysight is the trusted advisor for customers’

application needs

Page

43%Other

Modular

57%PXI/AXIe

Modular

Fast Growing ModularStill Small Portion of Total Market

31

2014 Modular Solutions

$1.1 Billion*

2015 Total Market

$13.5 Billion*

* Per Company estimates

0

2

4

6

8

10

12

14

16

18

2015 2016 2017 2018 2019 2020

$B$625M*

PXI/AXIe

Modular

15% CAGR*

to 2020

PXI/AXIe

Modular

15% CAGR*

Keysight’s double-digit growth

continued in Q1 FY16

Page

$59M

$93M

FY13 FY14 FY15

Strong Keysight Growth in PXI/AXIe Modular Solutions

32

− Growing core catalog: Now >150 modular products and solutions

− Introducing state-of-the-art modules that are winning new business and taking share

− Winning systems deals in large accounts with high performance, smaller footprint, fast test speed, high reliability, and expert application support

Key Initiatives

* Excludes ~$50M in FY15 non-PXI/AXIe modular orders

Keysight PXI/AXIe Orders

*

59%CAGR

>$150M

Page

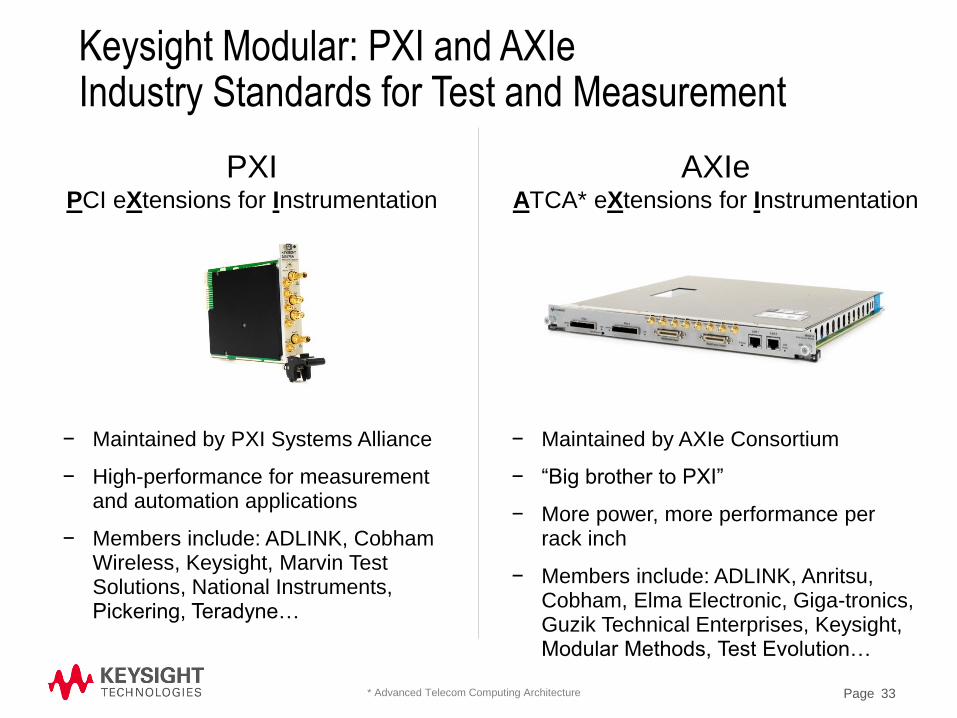

Keysight Modular: PXI and AXIeIndustry Standards for Test and Measurement

33

PXIPCI eXtensions for Instrumentation

AXIeATCA* eXtensions for Instrumentation

− Maintained by PXI Systems Alliance

− High-performance for measurement and automation applications

− Members include: ADLINK, Cobham Wireless, Keysight, Marvin Test Solutions, National Instruments, Pickering, Teradyne…

− Maintained by AXIe Consortium

− “Big brother to PXI”

− More power, more performance per rack inch

− Members include: ADLINK, Anritsu, Cobham, Elma Electronic, Giga-tronics, Guzik Technical Enterprises, Keysight, Modular Methods, Test Evolution…

* Advanced Telecom Computing Architecture

Page 34

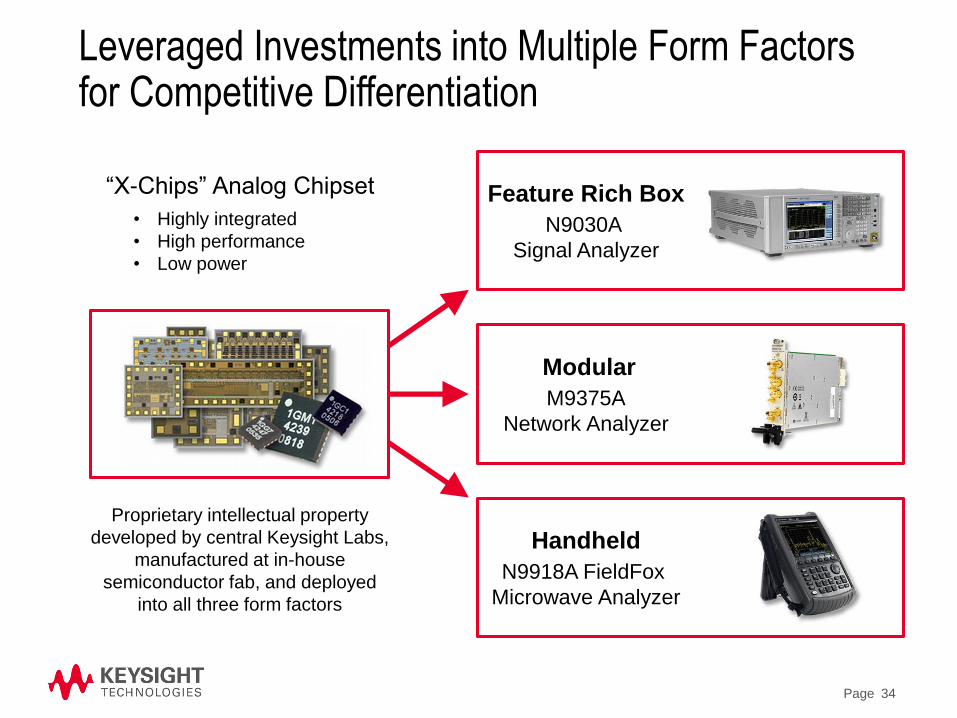

“X-Chips” Analog Chipset

• Highly integrated

• High performance

• Low power

Handheld

N9918A FieldFox

Microwave Analyzer

Feature Rich Box

N9030A

Signal Analyzer

Modular

M9375A

Network Analyzer

Proprietary intellectual property

developed by central Keysight Labs,

manufactured at in-house

semiconductor fab, and deployed

into all three form factors

Leveraged Investments into Multiple Form Factors for Competitive Differentiation

Page

Unique Value: Keysight Offers All Form Factors Meeting the Needs of Customer Applications

35

Feature Rich Box Modular Handheld

• R&D

• Validation

• Complex device manufacturing

• Full measurement set

• One-button measurements

• Shared equipment in lab

• Manufacturing

• R&D

• Validation

• Small footprint

• Flexible configuration

• Multi-channel applications

• Installation

• Maintenance

• Portability

• Harsh environments

Customer

Best For

Page

Highly Differentiated Position:A Trusted Advisor with >75 Years of Expertise

36

– Only supplier that offers all form factors to provide complete solutions

that best fit customer needs

– Leverage leading-performance technologies into multiple form factors

– Use common measurement software across all form factors to ensure

measurement accuracy and consistency

– Provide global support network

– Deliver world-class product reliability

Page

Services Growth Initiative

37

Page

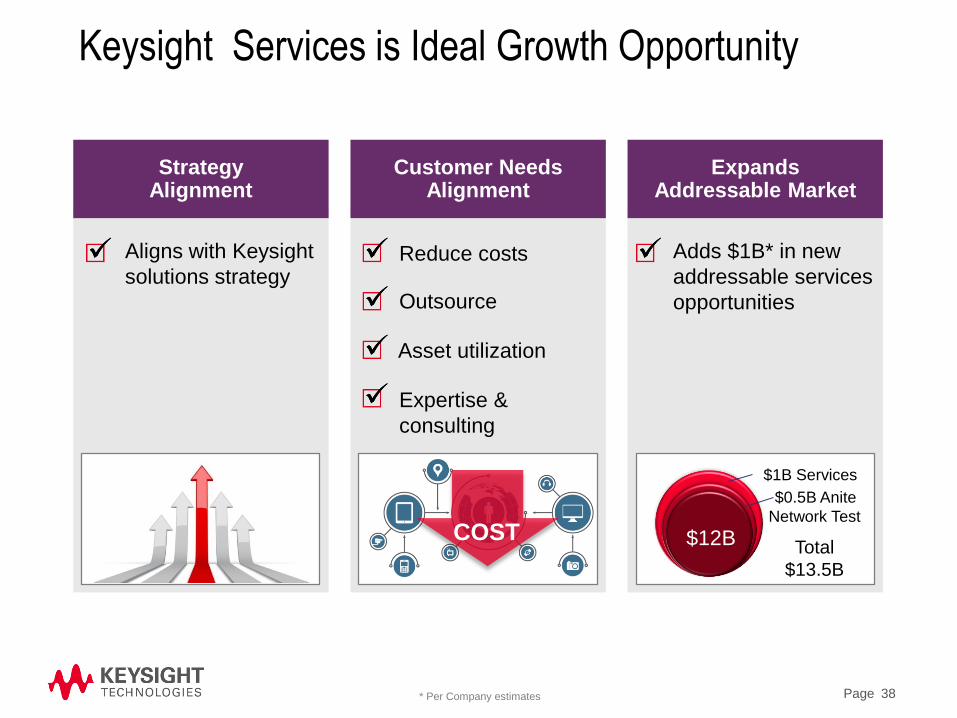

Keysight Services is Ideal Growth Opportunity

38

Adds $1B* in new

addressable services

opportunities

Aligns with Keysight

solutions strategy

StrategyAlignment

Customer Needs Alignment

ExpandsAddressable Market

$1B Services

$0.5B Anite

Network Test

$12B Total

$13.5B

Outsource

Reduce costs

Asset utilization

Expertise &

consulting

COST

* Per Company estimates

Page

Today: Strong Customer Services Foundation

39

– Calibration

– Repair

– Used equipment

– Global footprint

• Service centers in 30

countries

• Affiliated with 35 calibration

standards bodies in 17

countries

$401M FY15 Services Revenue

– Third-party maintainers

– Original equipment manufacturers

Competitors

Business Focus

Used

Equipment Calibration

Repair

Page

Goal: Increase Services Revenue 50% by 2020

40

2015

$401M Revenue

2020

$600M Revenue

8%CAGR

CalibrationUsed

Equipment

Repair

Used

Equipment

Calibration

“Plus”

Repair

Page

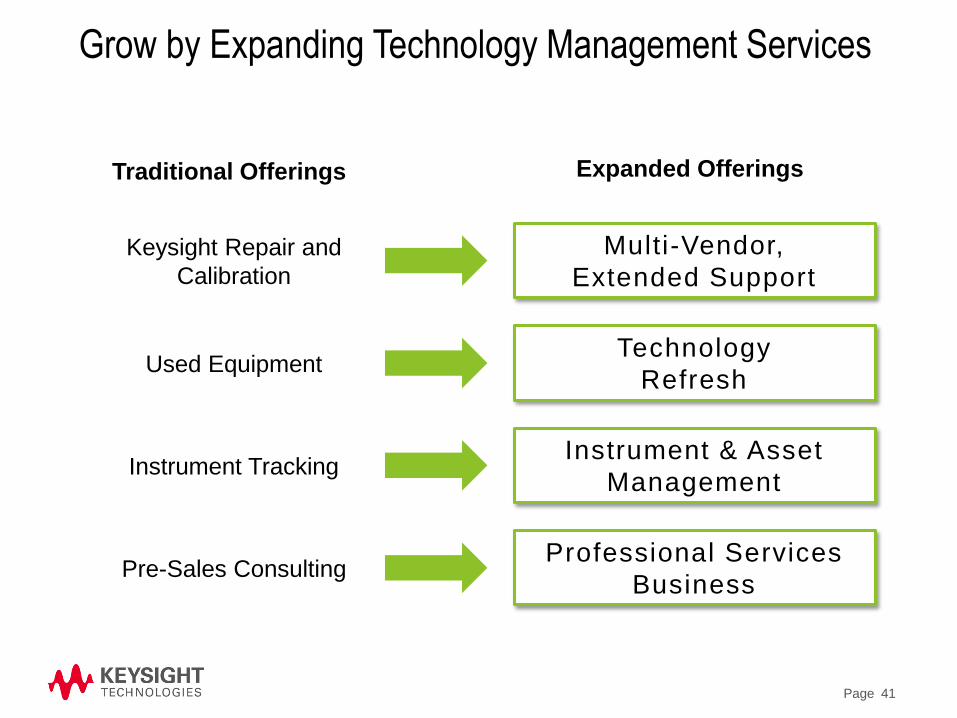

Grow by Expanding Technology Management Services

41

Multi-Vendor,

Extended SupportKeysight Repair and

Calibration

Traditional Offerings

Technology

RefreshUsed Equipment

Instrument & Asset

ManagementInstrument Tracking

Pre-Sales ConsultingProfessional Services

Business

Expanded Offerings

Page

Moving Up the Customer Value Chain Drives Growth

42

Calibration

Asset mgmt. and technology refresh

Professional services

Repair

Multi-vendor calibration

Page

Attractive Characteristics of the Services Business

43

– Immediate opportunities large installed base

– Increases served addressable market access new dollars

– Greater account control strategic selling

– Stable revenue stream less cyclicality,

multi-year contracts

Page 44

Executive Overview

4 Growth Initiatives – Wireless, Modular, Software and Services

Advanced Manufacturing Strategy & Capabilities

Agenda

Page

Manufacturing Strategy

45

• Relentless focus on cost savings− Manufacturing in a low cost region

− LEAN at Keysight

• Develop new technologies capability− new materials / new manufacturing process

• Design for supply chain − rapid launch and ramp-to-volume of new products

• Continued commitment to quality− culture of quality, customer satisfaction

− compliance regulatory requirements

Cost savings to maintain favorable

margins

Page

• Global sourcing

• Outsourcing

• World’s largest

Test & Measurement

facility in Asia

• State of the art

technology centers

providing performance

differentiation in

products / solutions

• Multi discipline

competencies

• Value Engineering

Strengths We Are Building On

46

Total Quality Management

Low Cost Region

Manufacturing

Unique Engineering

Capability

Advanced Technology

Capability

Flexible

Supply Base

Page

Key Messages

47

Technology and market leader in

ever-evolving technology market

4% revenue CAGR

Deliver >20% operating margin

8-10% EPS growth

Transformation

Objectives

Over the CycleLeader in profitable

market

Target fast growing areas

and expand Served Addressable

Market (SAM)

Proven operating performance

and cash generation across cycles

Transform for

growth

Strong business

model