Embed Size (px)

Citation preview

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

The information contained in this update may be acted on only by a subscriber and only after a review and understanding of the information contained in previous issues of The Dines Letter

(TDL) plus the “Introductory Subscriber Kit” sent to all new subscribers to The Dines Letter (TDLrs). All conditions and restrictions contained in The Dines Letter are incorporated into this

update by reference and apply as if fully set forth herein.

January 4, 2017

VOLUME 57 NUMBER 1&2

DJI 19,942.16

DJT 9,115.72

DJU 659.28

NASDAQ 5,477.00

Gold 1,164.70

Silver 16.49

2017 ANNUAL FORECAST ISSUE DOUBLE ISSUE

Page 1. Which Way Stock Markets? Which Stocks to Buy? 5. Will Trump Trigger a Gold and Silver Bull Market?

7. TDL’s Latest on Silver; a Sensational Prediction! 9. Raw Materials and Even Uranium 10. Biggest Winners in 2016 11. When Inflation? And Gold? 12. Debt’s Impact on Gold 15. Latest from “The Original Potbug”; Go For Blood! 17. Latest on Geopolitics in the World 20. Health: The Coming Physical Immortality 21. TPG: TDL’s Political Gamut, Optimistic? 24. Nostradinesus: Terror Will Come to Russia 27. Seasonalities, For Advanced Market Students 31. TDL’s Long-Term Charts 35. Presstime Gold Flash; Proof that Trump is a Goldbug?

TABLE OF CONTENTS

What’s the use of worrying? It never was worthwhile, So, pack up your troubles in your old kit-bag, And smile, smile, smile. George Asaf (1915)

He buys honey too dear who licks it from thorns. Proverb

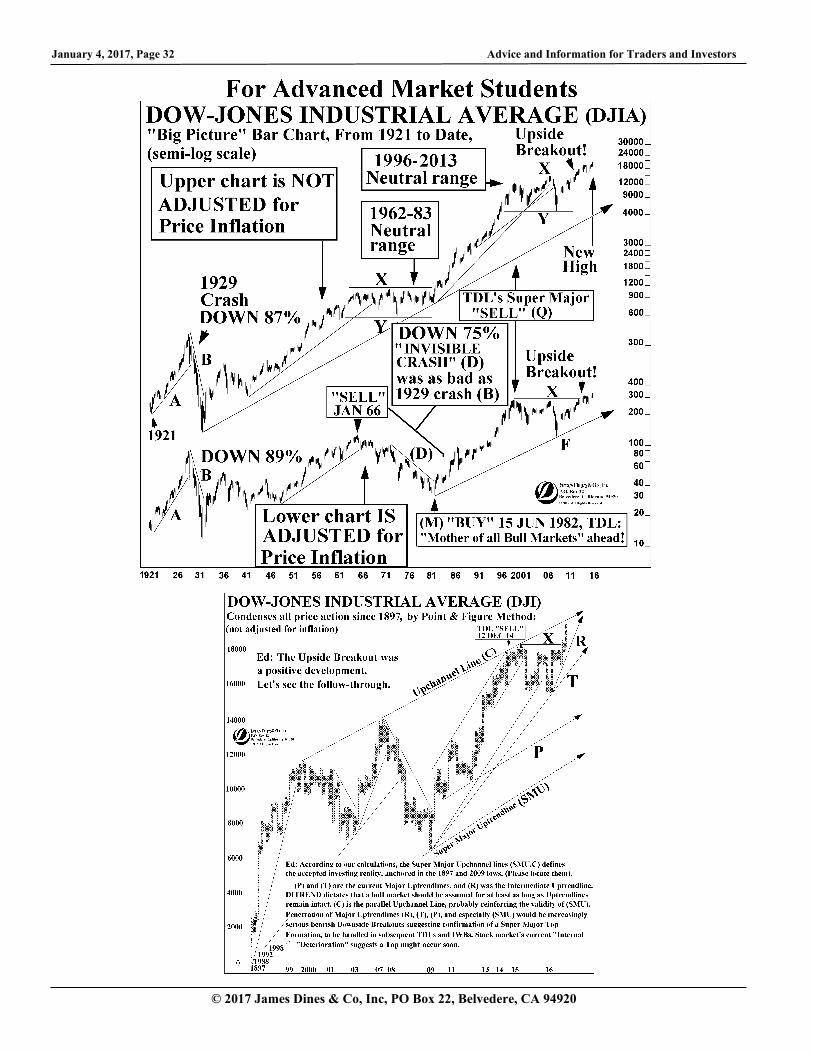

One of the very best calls in TDL’s history was the “Buy” signal within only four days from the rock bottom low of this bull market, at 6,763 on 2 Mar 09, daring to buy when the frightened world was in the throes of the notorious banking crisis and stock-market crash. (See “A” on chart, at bottom right). Subsequently, the DJI (Dow-Jones Industrial Index) rose relentlessly for six straight years, during which we correctly maintained our optimistic stance.

But on 12 Dec 14 we issued a “Sell” signal (at Q)because we observed one of the telltale signs of a Top – “Internal Deterioration” – one of our discoveries – when increasing numbers of leading stocks stop going up, and even decline. Internal Deterioration is so subtle that it doesn’t always show up in traditional Advance/Decline Indicators.

We remained bearish for the next two years (2015 and 2016) despite numerous False Upside Breakouts (with one brief and unimportant exception). In those two years the leading averages flattened out (see X,Y), and we knew it was either a Top or a platform for a new upward leg. Similarly, averages worldwide also began

to flatten out. International currencies began declining in 2016, and many of China’s stocks also developed miserable Internal Deterioration. We were convinced that there was a risk of the market

WHICH WAY STOCK MARKETS?

WHICH STOCKS TO BUY?

January 4, 2017, Page 2 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

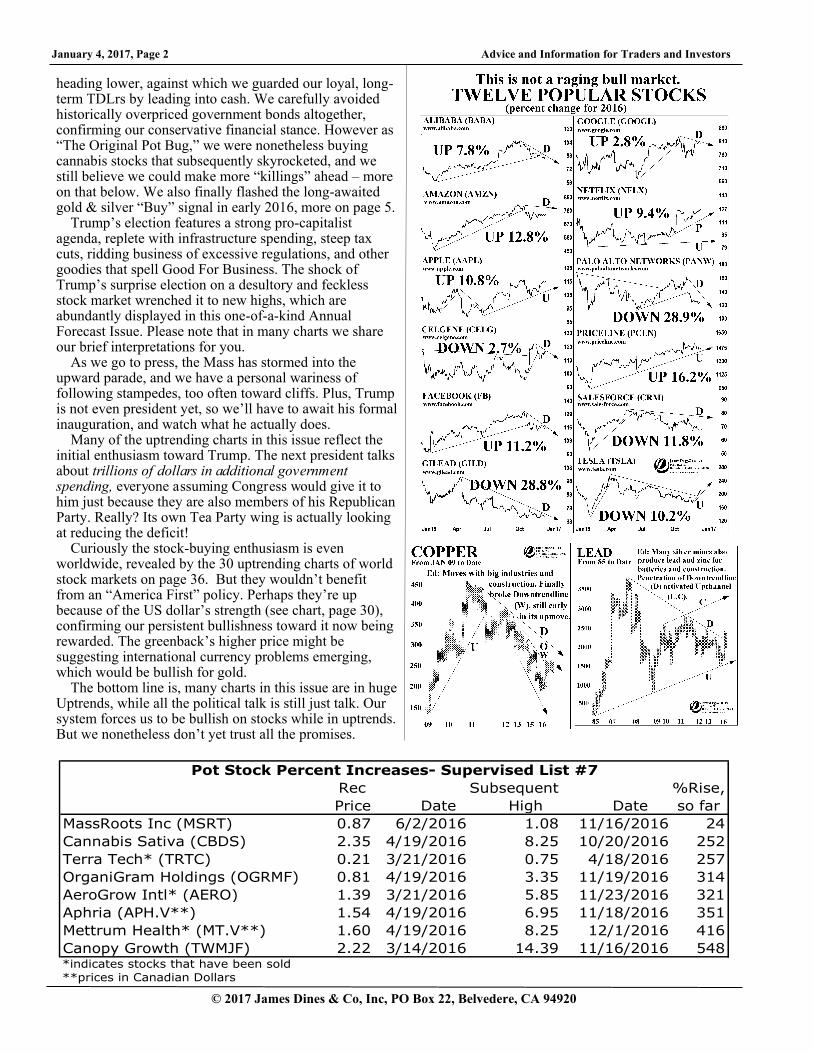

heading lower, against which we guarded our loyal, long-term TDLrs by leading into cash. We carefully avoided historically overpriced government bonds altogether, confirming our conservative financial stance. However as “The Original Pot Bug,” we were nonetheless buying cannabis stocks that subsequently skyrocketed, and we still believe we could make more “killings” ahead – more on that below. We also finally flashed the long-awaited gold & silver “Buy” signal in early 2016, more on page 5.

Trump’s election features a strong pro-capitalist agenda, replete with infrastructure spending, steep tax cuts, ridding business of excessive regulations, and other goodies that spell Good For Business. The shock of Trump’s surprise election on a desultory and feckless stock market wrenched it to new highs, which are abundantly displayed in this one-of-a-kind Annual Forecast Issue. Please note that in many charts we share our brief interpretations for you.

As we go to press, the Mass has stormed into the upward parade, and we have a personal wariness of following stampedes, too often toward cliffs. Plus, Trump is not even president yet, so we’ll have to await his formal inauguration, and watch what he actually does.

Many of the uptrending charts in this issue reflect the initial enthusiasm toward Trump. The next president talks about trillions of dollars in additional government spending, everyone assuming Congress would give it to him just because they are also members of his Republican Party. Really? Its own Tea Party wing is actually looking at reducing the deficit!

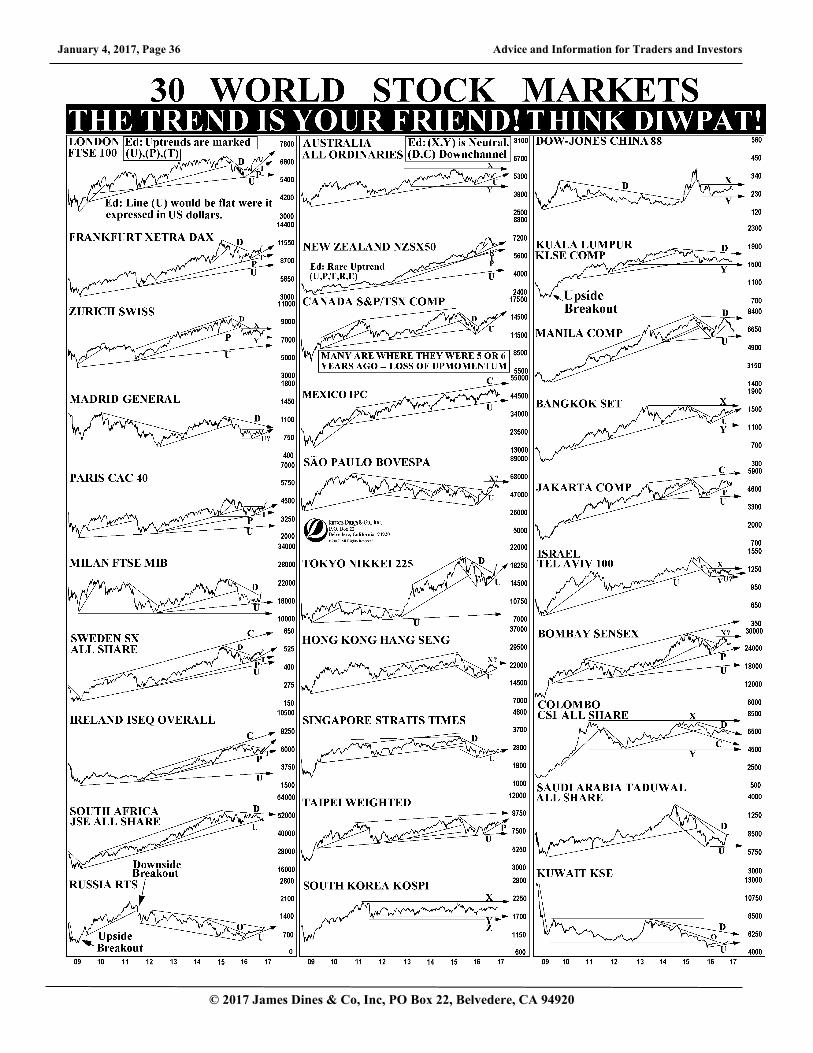

Curiously the stock-buying enthusiasm is even worldwide, revealed by the 30 uptrending charts of world stock markets on page 36. But they wouldn’t benefit from an “America First” policy. Perhaps they’re up because of the US dollar’s strength (see chart, page 30), confirming our persistent bullishness toward it now being rewarded. The greenback’s higher price might be suggesting international currency problems emerging, which would be bullish for gold.

The bottom line is, many charts in this issue are in huge Uptrends, while all the political talk is still just talk. Our system forces us to be bullish on stocks while in uptrends. But we nonetheless don’t yet trust all the promises.

Rec Subsequent %Rise,

Price Date High Date so far

MassRoots Inc (MSRT) 0.87 6/2/2016 1.08 11/16/2016 24

Cannabis Sativa (CBDS) 2.35 4/19/2016 8.25 10/20/2016 252

Terra Tech* (TRTC) 0.21 3/21/2016 0.75 4/18/2016 257

OrganiGram Holdings (OGRMF) 0.81 4/19/2016 3.35 11/19/2016 314

AeroGrow Intl* (AERO) 1.39 3/21/2016 5.85 11/23/2016 321

Aphria (APH.V**) 1.54 4/19/2016 6.95 11/18/2016 351

Mettrum Health* (MT.V**) 1.60 4/19/2016 8.25 12/1/2016 416

Canopy Growth (TWMJF) 2.22 3/14/2016 14.39 11/16/2016 548*indicates stocks that have been sold

**prices in Canadian Dollars

Pot Stock Percent Increases- Supervised List #7

Advice and Information for Traders and Investors January 4, 2017, Page 3

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

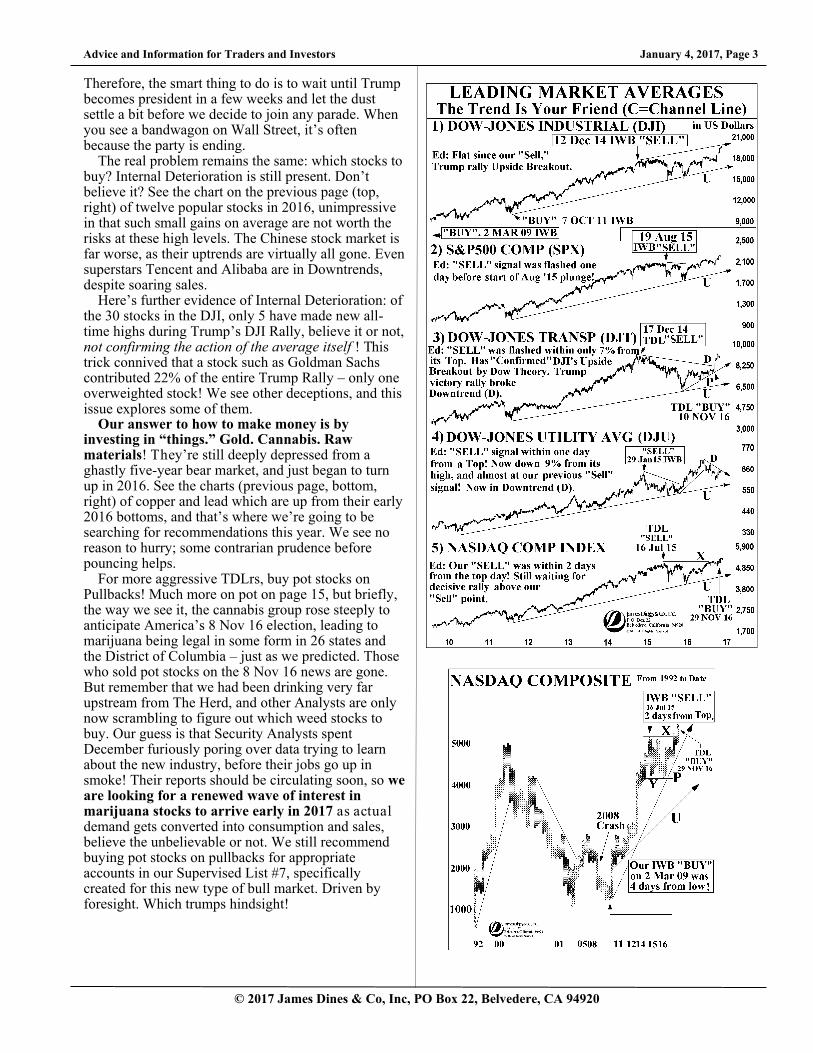

Therefore, the smart thing to do is to wait until Trump becomes president in a few weeks and let the dust settle a bit before we decide to join any parade. When you see a bandwagon on Wall Street, it’s often because the party is ending.

The real problem remains the same: which stocks to buy? Internal Deterioration is still present. Don’t believe it? See the chart on the previous page (top, right) of twelve popular stocks in 2016, unimpressive in that such small gains on average are not worth the risks at these high levels. The Chinese stock market is far worse, as their uptrends are virtually all gone. Even superstars Tencent and Alibaba are in Downtrends, despite soaring sales.

Here’s further evidence of Internal Deterioration: of the 30 stocks in the DJI, only 5 have made new all-time highs during Trump’s DJI Rally, believe it or not, not confirming the action of the average itself ! This trick connived that a stock such as Goldman Sachs contributed 22% of the entire Trump Rally – only one overweighted stock! We see other deceptions, and this issue explores some of them.

Our answer to how to make money is by investing in “things.” Gold. Cannabis. Raw materials! They’re still deeply depressed from a ghastly five-year bear market, and just began to turn up in 2016. See the charts (previous page, bottom, right) of copper and lead which are up from their early 2016 bottoms, and that’s where we’re going to be searching for recommendations this year. We see no reason to hurry; some contrarian prudence before pouncing helps.

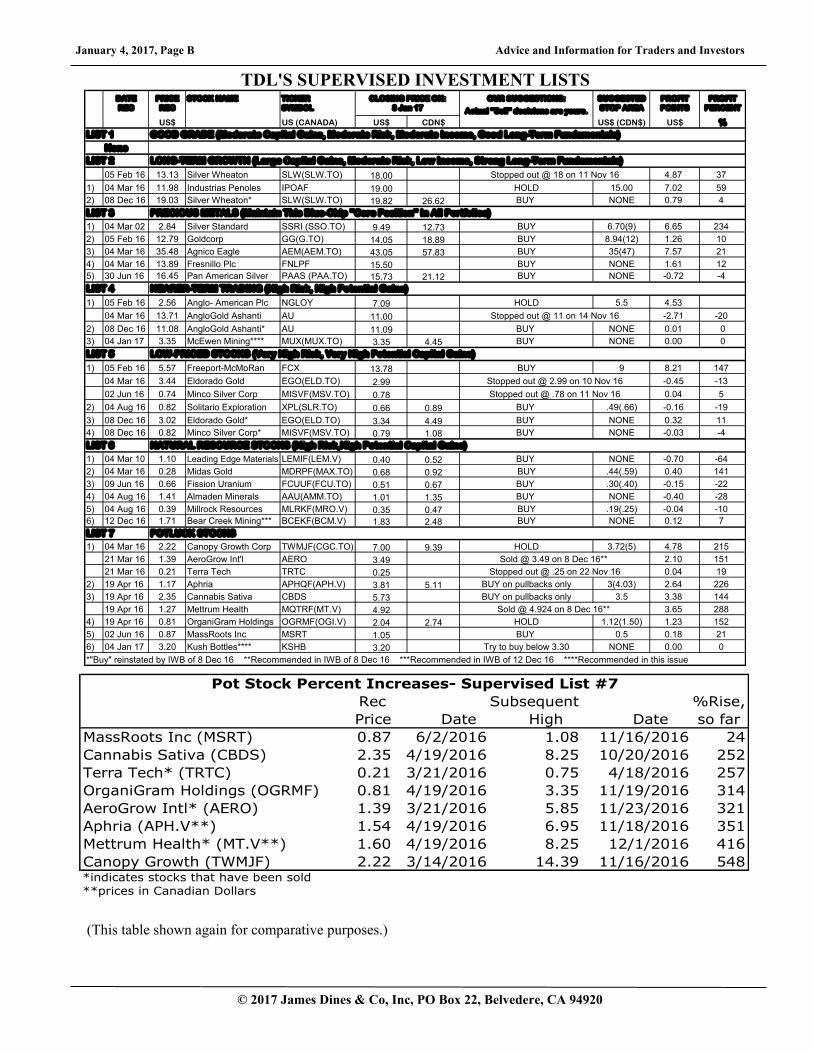

For more aggressive TDLrs, buy pot stocks on Pullbacks! Much more on pot on page 15, but briefly, the way we see it, the cannabis group rose steeply to anticipate America’s 8 Nov 16 election, leading to marijuana being legal in some form in 26 states and the District of Columbia – just as we predicted. Those who sold pot stocks on the 8 Nov 16 news are gone. But remember that we had been drinking very far upstream from The Herd, and other Analysts are only now scrambling to figure out which weed stocks to buy. Our guess is that Security Analysts spent December furiously poring over data trying to learn about the new industry, before their jobs go up in smoke! Their reports should be circulating soon, so we are looking for a renewed wave of interest in marijuana stocks to arrive early in 2017 as actual demand gets converted into consumption and sales, believe the unbelievable or not. We still recommend buying pot stocks on pullbacks for appropriate accounts in our Supervised List #7, specifically created for this new type of bull market. Driven by foresight. Which trumps hindsight!

January 4, 2017, Page 4 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

Advice and Information for Traders and Investors January 4, 2017, Page 5

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

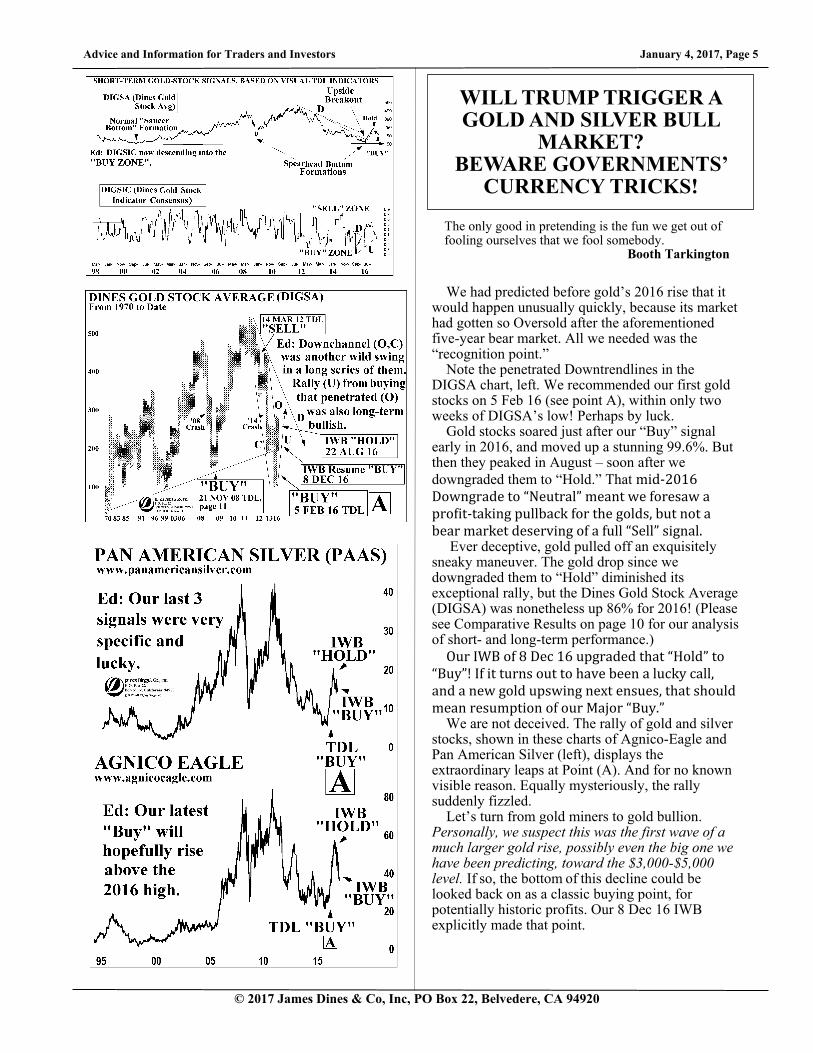

We had predicted before gold’s 2016 rise that it would happen unusually quickly, because its market had gotten so Oversold after the aforementioned five-year bear market. All we needed was the “recognition point.”

Note the penetrated Downtrendlines in the DIGSA chart, left. We recommended our first gold stocks on 5 Feb 16 (see point A), within only two weeks of DIGSA’s low! Perhaps by luck.

Gold stocks soared just after our “Buy” signal early in 2016, and moved up a stunning 99.6%. But then they peaked in August – soon after we

downgraded them to “Hold.” That mid-2016 Downgrade to “Neutral” meant we foresaw a profit-taking pullback for the golds, but not a bear market deserving of a full “Sell” signal.

Ever deceptive, gold pulled off an exquisitely sneaky maneuver. The gold drop since we downgraded them to “Hold” diminished its exceptional rally, but the Dines Gold Stock Average (DIGSA) was nonetheless up 86% for 2016! (Please see Comparative Results on page 10 for our analysis of short- and long-term performance.)

Our IWB of 8 Dec 16 upgraded that “Hold” to “Buy”! If it turns out to have been a lucky call, and a new gold upswing next ensues, that should mean resumption of our Major “Buy.”

We are not deceived. The rally of gold and silver stocks, shown in these charts of Agnico-Eagle and Pan American Silver (left), displays the extraordinary leaps at Point (A). And for no known visible reason. Equally mysteriously, the rally suddenly fizzled.

Let’s turn from gold miners to gold bullion. Personally, we suspect this was the first wave of a much larger gold rise, possibly even the big one we have been predicting, toward the $3,000-$5,000 level. If so, the bottom of this decline could be looked back on as a classic buying point, for potentially historic profits. Our 8 Dec 16 IWB explicitly made that point.

WILL TRUMP TRIGGER A GOLD AND SILVER BULL

MARKET? BEWARE GOVERNMENTS’

CURRENCY TRICKS!

The only good in pretending is the fun we get out of fooling ourselves that we fool somebody. Booth Tarkington

January 4, 2017, Page 6 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

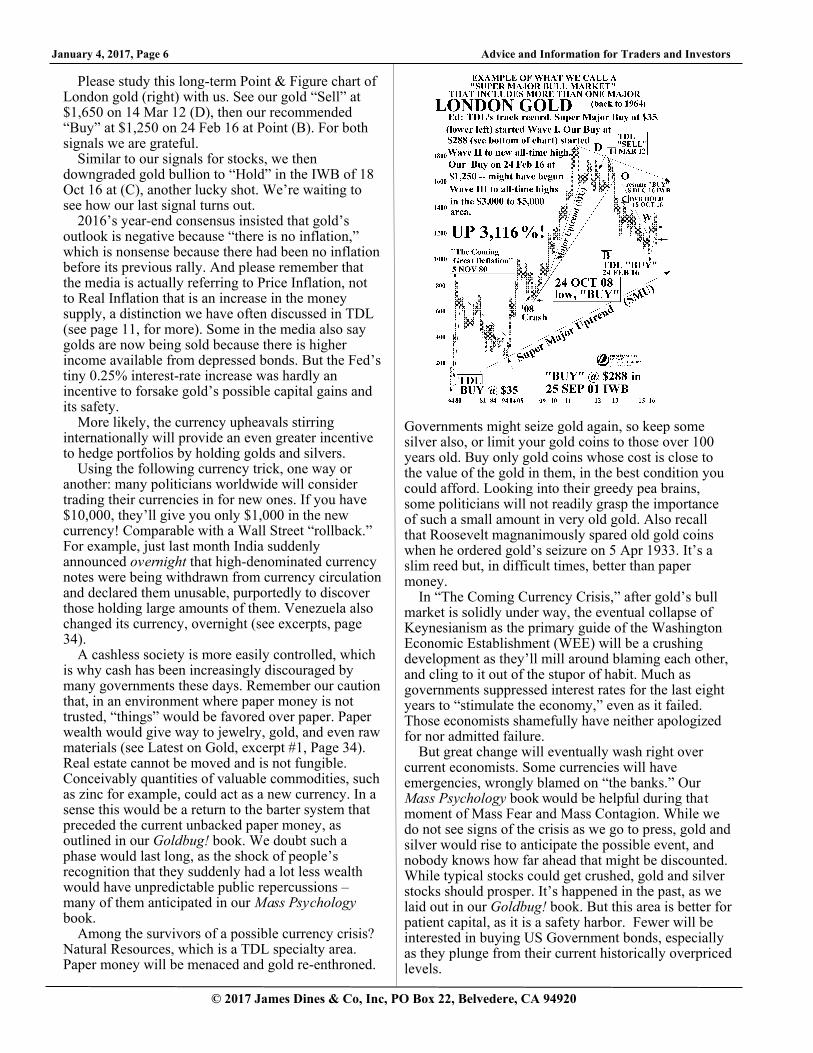

Please study this long-term Point & Figure chart of London gold (right) with us. See our gold “Sell” at $1,650 on 14 Mar 12 (D), then our recommended “Buy” at $1,250 on 24 Feb 16 at Point (B). For both signals we are grateful.

Similar to our signals for stocks, we then downgraded gold bullion to “Hold” in the IWB of 18 Oct 16 at (C), another lucky shot. We’re waiting to see how our last signal turns out.

2016’s year-end consensus insisted that gold’s outlook is negative because “there is no inflation,” which is nonsense because there had been no inflation before its previous rally. And please remember that the media is actually referring to Price Inflation, not to Real Inflation that is an increase in the money supply, a distinction we have often discussed in TDL (see page 11, for more). Some in the media also say golds are now being sold because there is higher income available from depressed bonds. But the Fed’s tiny 0.25% interest-rate increase was hardly an incentive to forsake gold’s possible capital gains and its safety.

More likely, the currency upheavals stirring internationally will provide an even greater incentive to hedge portfolios by holding golds and silvers.

Using the following currency trick, one way or another: many politicians worldwide will consider trading their currencies in for new ones. If you have $10,000, they’ll give you only $1,000 in the new currency! Comparable with a Wall Street “rollback.” For example, just last month India suddenly announced overnight that high-denominated currency notes were being withdrawn from currency circulation and declared them unusable, purportedly to discover those holding large amounts of them. Venezuela also changed its currency, overnight (see excerpts, page 34).

A cashless society is more easily controlled, which is why cash has been increasingly discouraged by many governments these days. Remember our caution that, in an environment where paper money is not trusted, “things” would be favored over paper. Paper wealth would give way to jewelry, gold, and even raw materials (see Latest on Gold, excerpt #1, Page 34). Real estate cannot be moved and is not fungible. Conceivably quantities of valuable commodities, such as zinc for example, could act as a new currency. In a sense this would be a return to the barter system that preceded the current unbacked paper money, as outlined in our Goldbug! book. We doubt such a phase would last long, as the shock of people’s recognition that they suddenly had a lot less wealth would have unpredictable public repercussions – many of them anticipated in our Mass Psychology book.

Among the survivors of a possible currency crisis? Natural Resources, which is a TDL specialty area. Paper money will be menaced and gold re-enthroned.

Governments might seize gold again, so keep some silver also, or limit your gold coins to those over 100 years old. Buy only gold coins whose cost is close to the value of the gold in them, in the best condition you could afford. Looking into their greedy pea brains, some politicians will not readily grasp the importance of such a small amount in very old gold. Also recall that Roosevelt magnanimously spared old gold coins when he ordered gold’s seizure on 5 Apr 1933. It’s a slim reed but, in difficult times, better than paper money.

In “The Coming Currency Crisis,” after gold’s bull market is solidly under way, the eventual collapse of Keynesianism as the primary guide of the Washington Economic Establishment (WEE) will be a crushing development as they’ll mill around blaming each other, and cling to it out of the stupor of habit. Much as governments suppressed interest rates for the last eight years to “stimulate the economy,” even as it failed. Those economists shamefully have neither apologized for nor admitted failure.

But great change will eventually wash right over current economists. Some currencies will have emergencies, wrongly blamed on “the banks.” Our Mass Psychology book would be helpful during that moment of Mass Fear and Mass Contagion. While we do not see signs of the crisis as we go to press, gold and silver would rise to anticipate the possible event, and nobody knows how far ahead that might be discounted. While typical stocks could get crushed, gold and silver stocks should prosper. It’s happened in the past, as we laid out in our Goldbug! book. But this area is better for patient capital, as it is a safety harbor. Fewer will be interested in buying US Government bonds, especially as they plunge from their current historically overpriced levels.

Advice and Information for Traders and Investors January 4, 2017, Page 7

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

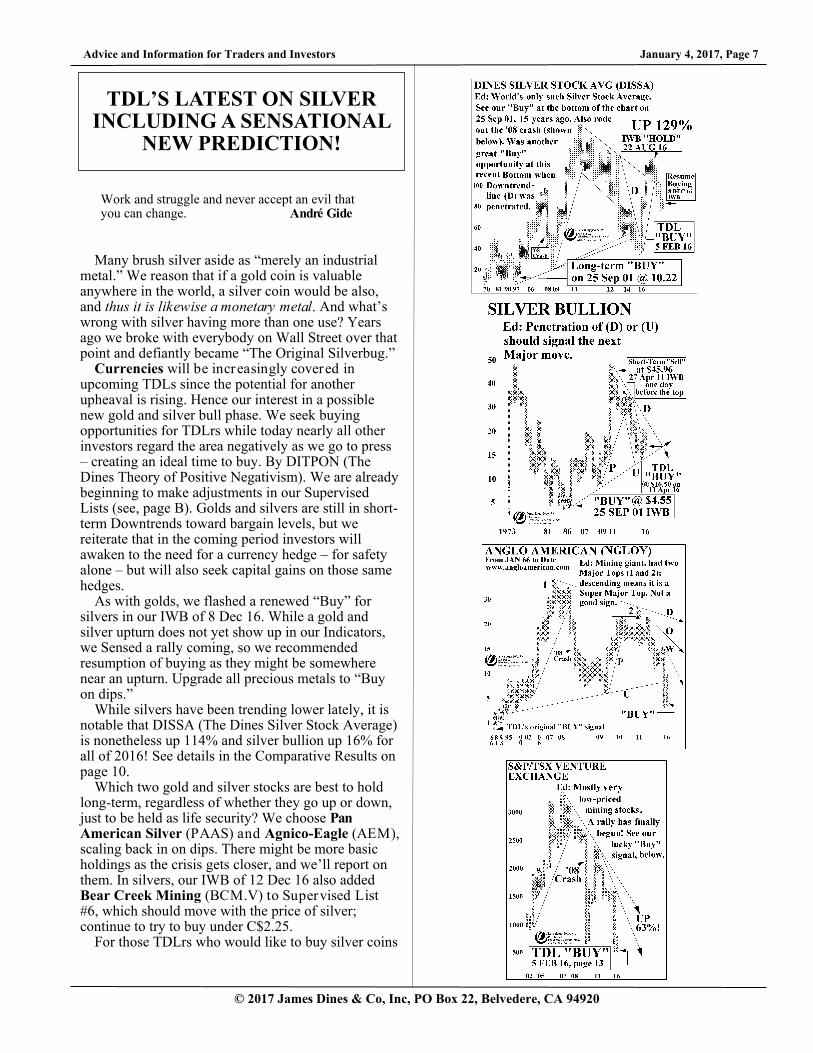

Many brush silver aside as “merely an industrial metal.” We reason that if a gold coin is valuable anywhere in the world, a silver coin would be also, and thus it is likewise a monetary metal. And what’s wrong with silver having more than one use? Years ago we broke with everybody on Wall Street over that point and defiantly became “The Original Silverbug.”

Currencies will be increasingly covered in upcoming TDLs since the potential for another upheaval is rising. Hence our interest in a possible new gold and silver bull phase. We seek buying opportunities for TDLrs while today nearly all other investors regard the area negatively as we go to press – creating an ideal time to buy. By DITPON (The Dines Theory of Positive Negativism). We are already beginning to make adjustments in our Supervised Lists (see, page B). Golds and silvers are still in short-term Downtrends toward bargain levels, but we reiterate that in the coming period investors will awaken to the need for a currency hedge – for safety alone – but will also seek capital gains on those same hedges.

As with golds, we flashed a renewed “Buy” for silvers in our IWB of 8 Dec 16. While a gold and silver upturn does not yet show up in our Indicators, we Sensed a rally coming, so we recommended resumption of buying as they might be somewhere near an upturn. Upgrade all precious metals to “Buy on dips.”

While silvers have been trending lower lately, it is notable that DISSA (The Dines Silver Stock Average) is nonetheless up 114% and silver bullion up 16% for all of 2016! See details in the Comparative Results on page 10.

Which two gold and silver stocks are best to hold long-term, regardless of whether they go up or down, just to be held as life security? We choose Pan American Silver (PAAS) and Agnico-Eagle (AEM), scaling back in on dips. There might be more basic holdings as the crisis gets closer, and we’ll report on them. In silvers, our IWB of 12 Dec 16 also added Bear Creek Mining (BCM.V) to Supervised List #6, which should move with the price of silver; continue to try to buy under C$2.25.

For those TDLrs who would like to buy silver coins

TDL’S LATEST ON SILVER INCLUDING A SENSATIONAL

NEW PREDICTION!

Work and struggle and never accept an evil that you can change. André Gide

January 4, 2017, Page 8 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

we recommend as our first choice, the beautiful Walking Liberty half-dollar coin, still easily obtained near its Melt Price in “brilliant, uncirculated” – even proof condition. It is wise to stretch your budget as much as feasible when purchasing such gold and silver coins because they should rise in their eventual bull market first and farthest, driven by speculators joining the current numismatists. As sage advice, never maintain such coins anywhere near your residence or on your person, and keep your ownership confidential.

Before you brush off the shocking prediction afterwards, here’s what Barron’s wrote about us on 14 Jan 1980 when we made a comparable prediction:

“The Dow-Jones Industrial Average came remarkably close to fulfilling a prediction made a decade ago by James Dines, who accurately bills himself as “The Original Goldbug,” namely that someday the two would cross. Nobody believed him then, but last week the gap between the DJI and the gold quotation had never been smaller, Dines’ stature never greater. James Dines’ prediction – that the price of bullion would someday cross the Dow-Jones Industrial Average – begins to look like one of the most fantastic investment calls on record.” Barron’s

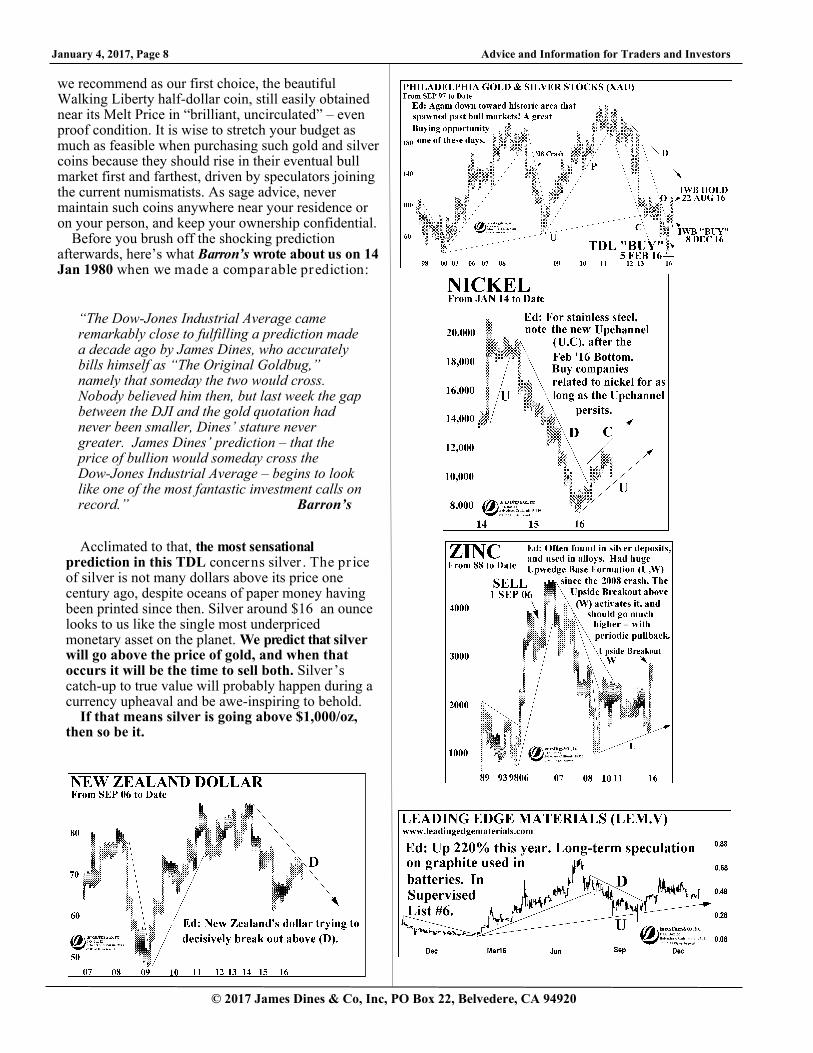

Acclimated to that, the most sensational prediction in this TDL concerns silver . The pr ice of silver is not many dollars above its price one century ago, despite oceans of paper money having been printed since then. Silver around $16 an ounce looks to us like the single most underpriced monetary asset on the planet. We predict that silver will go above the price of gold, and when that occurs it will be the time to sell both. Silver ’s catch-up to true value will probably happen during a currency upheaval and be awe-inspiring to behold.

If that means silver is going above $1,000/oz, then so be it.

Advice and Information for Traders and Investors January 4, 2017, Page 9

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

Prices of Raw Materials are still in uptrends, normally bullish for the economy. But how much of the projected demand represents China’s desperate buying to boost its own economy, plus Trump’s increasing American infrastructure spending? And how long might that last? Much of the “Trump Rally” was based on his construction background and vows to rebuild America’s infrastructure, as mentioned, which require natural resources. We recall a past raw materials boom when we successfully predicted China’s infrastructure needs provided the best way to invest in that country after Mao’s death, because its stock market was so underdeveloped at the time we couldn’t figure out which Chinese stocks to recommend to our loyal, long-term TDLrs.

Here we are again. If Trump could pull it off, raw materials should be at the forefront of investment opportunities. We share some of our personal raw materials charts in this TDL, so you could see for yourself, not comparably available elsewhere. We will be studying these in 2017’s upcoming TDLs for new stock recommendations. Also, see Freeport-McMoran (right), already up 366%, recommended by TDL at $5.57 on 5 Feb 16, a neat shot near rock bottom (E).

More charts of industrial metals appear on the previous page. We have repeatedly presented these for over a year in TDL, now quietly in Saucer Bottom Base Formations even while the group has been drenched in public pessimism.

Uranium: Recapitulating our latest Inter im Warning Bulletin (12 Dec 16), Trump rejects climate change, even calling it a hoax. It’s not easy trying to figure out what he’ll actually do about increased emissions from a booming and resurgent coal industry. Somewhere ahead we suspect he’ll include nuclear power in America’s energy mix to make up for coal’s increased emissions. Why? Perhaps it’s because he conspicuously (to us) has not used the words “nuclear power.” We’re not aware of any other prominent forecaster being bullish on uranium these days. Understandably so, with uranium ore’s price locked in a Downtrend. Trump tweeted on 22 Dec 16 that the US should greatly expand its nuclear capability in response to Putin’s speech, which might be perceived as a favorable starting point for a nuclear energy policy as well.

When we predicted the last bull market in uranium

TDL’S LATEST ON RAW MATERIALS. EVEN URANIUM.

Everyone else at the table got up to dance, except him and me. There I was trapped. Trapped like a trap in a trap. Dorothy Parker, After Such Pleasures

stocks we partially based it on an Upside Breakout in the price action of uranium itself, within less than one dollar from the low at $7.10/lb. This time, Alternation would indicate that uranium stocks would lead uranium metal’s price.

We’ve been monitoring uranium stocks daily for years, waiting for a resumption of their Super Major Uptrends (consisting of more than one Major). Fission Uranium, already in our Supervised List #6, jumped 41%, from C$.49 on 7 Nov 16 to C$.69 on 12 Dec 16, most of the impressive gain in only 3 trading sessions! Other uranium stocks are also edging up, an apparent Confirmation of our recent increasing focus on uranium. Even beaten-down Cameco (CCJ) has risen 46% from $7.40 to $10.77 since 1 Nov 16.

The raw-materials bear market of the last five years is over, accelerated by President-elect Trump’s pledge to “rebuild America.” Indeed, steel and coal prices have been big beneficiaries. An equal amount invested into each of the low-priced stocks in Supervised List #6 should be a very rewarding portfolio in the next couple of years, if Trump succeeds.

January 4, 2017, Page 10 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

BIGGEST WINNERS: 2016 Comparative Annual Results At the moment, the financial news media is strongly celebrating the Trump rally as leading stock

market indices keep making new all-time highs. The jump started on 9 Nov 16, as Trump's election along with Republican control of Congress effectively changed the market’s narrative that had previously stalled for the last 2 years. Shifting our focus from currently evolving trendlines to a longer and more sobering perspective of annual results, we find surprising and unexpected highly ranked performance from shares in silver, gold and palladium, and in silver and gold bullions – particularly in 2016. See left-hand column, in bold font. Much of our bullishness on the natural resource sector was based on its deeply Oversold condition that existed at the start of 2016, and the accompanying results show sufficient profits were generated to weather the current Consolidation so far.

Broad market indices including the tech sector also figured prominently in 2016 with double-digit gains. Ranks #5, 7, 8, 9 and 10 went to the DJT, DJU, DJI, Morgan Stanley Hi Tech Index and the S&P 500 respectively. Thanks to the Federal Reserve's easy-money policy, investors were drawn to the "passive" investments we discussed in our last TDL (4 Nov 16, page 4), driving indices higher.

It is notable too that gold (#11) and the resource-heavy NYSE MKT (#13), outperformed Mutual Funds (#14), perhaps echoing the resurgence of commodities on the one hand, and the woes of major hedge funds that did not fare well on the other hand, despite late 2016’s strength in market averages.

Current Outlook: Just peeking into “Sell” territory. DIGFOI is possibly reflecting current market strength and will reach a Top within the next few months. DIGFOI contains no theoretical backward projections – all entries were calculated at the time, by your editor, personally – and is surely the market's longest-running Technical summation of its type.

Advice and Information for Traders and Investors January 4, 2017, Page 11

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

As previously mentioned, new subscribers should please be clear that “inflation” does not mean “higher prices.” This incorrect definition is cleverly used by sly economists to conceal what is really happening. In fact, inflation is an increase in the money supply that sometimes, but not always results in higher prices. The distinction is profound. “Real Inflation” never exists when the money supply is stable and honest, truthfully representing the postponed pleasures of savers – not yet looted by the State’s printing presses.

When there is no link between paper and anything tangible, currencies fluctuate like boats without keels, vulnerable to sudden capsizing, which menaces prosperity because currencies need to be stable as a measure of value, to replace inefficient barter. Gold is the most traditional store of wealth and a common price denominator of items to be traded. Goldbugs insist that paper money must be a valid medium of exchange, an honest store of value, an invariable unit of measure, also linked to gold and/or silver in some way.

In recent years, the financial media and economists have been publicly baffled by the mystery of why there has been so little Price Inflation despite all the currency printed. That untold trillions of dollars have been created without resulting in what governments loosely and simply call inflation has left the WEE (Washington Economic Establishment) bewildered, albeit grateful. Economists claim that there is no inflation, partially because they insist on defining inflation as higher prices. The reality is that rising Price Inflation began to roll over into a Real Deflation during the 2008 stock-market smash. We include the stock market in our definition of the money supply. Thus, the paper printed since 2008 was largely swallowed by that Real Deflation, usually by creating real downside pressure on prices – or bankruptcies – like the stock and bond crashes starting around 2008.

In fact, the amount of paper money in Real

FOR SERIOUS MARKET STUDENTS: WHEN WILL INFLATION SUDDENLY

LEAP INTO THE HEADLINES? AND GOLD?

Reality is a crutch for people who can’t cope with drugs. Lily Tomlin, Trust Me (I’m a Doctor)

Inflation has soared to stratospheric levels, and has been having a huge impact on the economy, temporarily staving off the full brunt of Price Deflation.

Normally trillions of dollars being printed and squandered worldwide cause prices to rise naturally, with more pieces of paper chasing the same amount of goods and services. Fair enough. But eventually the cyclical deflationary liquidation of all that surplus paper wipes out that unbacked paper, and that’s what a Real Deflation is – the cure of a previous Real Inflation. Again, since Real Deflations wipe out excess paper through bankruptcies, or crashes in bonds and stocks. Our predicted “The Coming Bond Crash” should be an example of excess fiat money disappearing into what we once labelled “Money Heaven.”

In fact, the very lack of higher prices despite big deficits is a key to recognizing that a deflation is present. In other words, the so-called mystery is that the currency cycle is now at a stage of liquidation of surplus paper. We believe that is partially why the whole world has been in a state of economic malaise for the last eight years; because as noted, nearly all nations followed the same Keynesian madness of economics that states running up non-stop debt and printing too much paper money was a path to infinite prosperity. This folly has been rejected by TDL since the link between gold and paper dollars was severed. Indeed, it has caused the very economic trouble that is a source of the unrest among the middle class in America that paved the way for Trump to win, and is now spreading to many other countries worldwide, by Mass Contagion. The middle class has been feeling sated while eating ersatz bread – fortified with sawdust to save wheat – but now are malnourished enough to demand jobs.

If the Federal Reserve, part of the WEE, tries to inflate the deflation away by accelerating the printing presses, it instead risks being punished by a hyperinflation, which would be even worse. We blame the Keynesian economists all America’s presidents have blindly followed for many decades.

Even less discussed anywhere these days is hyperinflation, explained in detail in our Goldbug! book. We describe a hyperinflation as the “supernova of inflations.” Hyperinflations occur when there is an acceleration of overprinting during a deflation that brings runaway higher prices for whichever reason. A hyperinflation is a collapse of a currency. Current examples these days are Venezuela and Zimbabwe, with many others at risk, including Brazil, Japan, India and possibly America. We are grateful to report we see no hyperinflation as of today, depending on what Trump actually does once he is in office after 20 Jan 2017. A year of hope, but with serious risk for mistakes.

To truly understand the above, we recommend our Goldbug! book, deemed “The Bible of the Goldbugs.”

January 4, 2017, Page 12 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

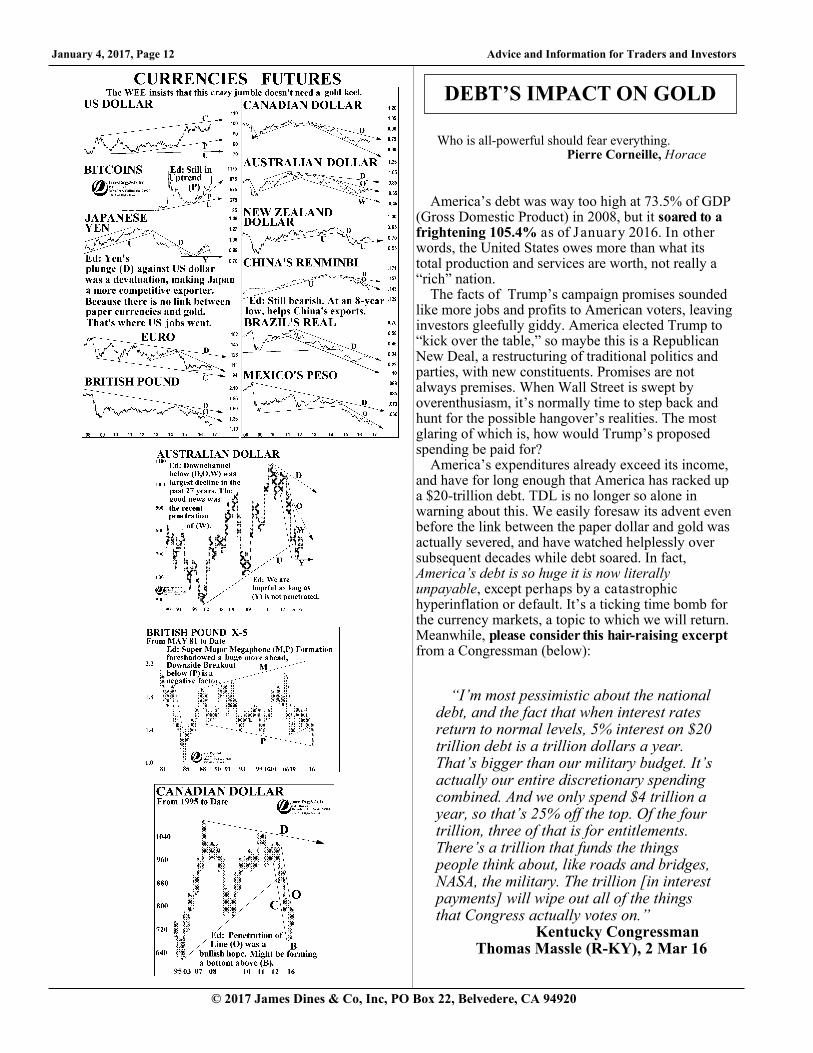

America’s debt was way too high at 73.5% of GDP (Gross Domestic Product) in 2008, but it soared to a frightening 105.4% as of January 2016. In other words, the United States owes more than what its total production and services are worth, not really a “rich” nation.

The facts of Trump’s campaign promises sounded like more jobs and profits to American voters, leaving investors gleefully giddy. America elected Trump to “kick over the table,” so maybe this is a Republican New Deal, a restructuring of traditional politics and parties, with new constituents. Promises are not always premises. When Wall Street is swept by overenthusiasm, it’s normally time to step back and hunt for the possible hangover’s realities. The most glaring of which is, how would Trump’s proposed spending be paid for?

America’s expenditures already exceed its income, and have for long enough that America has racked up a $20-trillion debt. TDL is no longer so alone in warning about this. We easily foresaw its advent even before the link between the paper dollar and gold was actually severed, and have watched helplessly over subsequent decades while debt soared. In fact, America’s debt is so huge it is now literally unpayable, except perhaps by a catastrophic hyperinflation or default. It’s a ticking time bomb for the currency markets, a topic to which we will return. Meanwhile, please consider this hair-raising excerpt from a Congressman (below):

DEBT’S IMPACT ON GOLD

Who is all-powerful should fear everything. Pierre Corneille, Horace

“I’m most pessimistic about the national debt, and the fact that when interest rates return to normal levels, 5% interest on $20 trillion debt is a trillion dollars a year. That’s bigger than our military budget. It’s actually our entire discretionary spending combined. And we only spend $4 trillion a year, so that’s 25% off the top. Of the four trillion, three of that is for entitlements. There’s a trillion that funds the things people think about, like roads and bridges, NASA, the military. The trillion [in interest payments] will wipe out all of the things that Congress actually votes on.” Kentucky Congressman Thomas Massle (R-KY), 2 Mar 16

Advice and Information for Traders and Investors January 4, 2017, Page 13

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

Perhaps there’s no point in our worrying any longer about America’s debt. World trade is such that America could not possibly earn enough money exporting to other nations, particularly since they are more interested in exporting into our market. Our new president might make a meaningful change in trajectory, but we’ll need to see trendlines actually broken before altering our conclusions. We would not be surprised by Trump announcing, out of the blue, that America would only pay a percentage of its debt to bond holders, perhaps 50%, which would cause Government bond markets to plunge. However the Fourteenth Amendment to the US Constitution says, in section 4, “The validity of the public debt of the United States, authorized by law . . . shall not be questioned.” This might inhibit Trump.

Once more, let it sink in that while America’s debt is still postponable, it’s impossible to pay. If you spent one-million dollars a day, every single day, since Julius Caesar was born on 12 July 100BC, you could not spend as much as one trillion dollars. And America owes $19.9 trillion, rising around one trillion a year. It would be unrealistic to expect the American public to endure suffering comparable with conditions of the First Great Depression of the early 1930s to repay it – if only because this time so many people have guns.

Something about debt is going to break. Much of it was run up when interest rates were near zero, suppressed by the Keynesian economists in the Fed, to conceal their borrowing costs. The inevitable consequences belie what is widely called “cheap money” to borrow. When interest rates rise to historically “normal” heights, they will have the impact cited in the Congressman’s excerpt (on the previous page). It’s never too early to begin pondering on what that might mean, or your taking precautions to survive.

But, there’s more. America’s total debt (state, mortgage, auto, student) is another $40 trillion dollars, double the federal debt! It’s out-of-control, and unstoppable, but politicians have just been going with it, assuming they’d be safely dead before America’s unlimited credit card got cancelled. Since trouble will be expressed as a currency crisis, we again conclude that it is wise to buy gold and silver stocks and coins. Thus resurfaces our original prediction of gold and silver rising in what we call a “Super Major” bull market, consisting of several Major ones. The chart of gold bullion (top, right, page 6) back to 1964 shows two of them so far as part of the first and second Major waves. Again, we predict that somewhere yet ahead is the wave that should carry gold to our longstanding long-term target of at least $3,000/oz to $5,000/oz. Waiting for that wave, we pondered which gold and silver stocks should benefit most from higher prices. Which

might have the most upside potential? Please refer to our feature on silver in this issue (page 7), for specific recommendations.

Let’s return to how Trump might pay for the tax cuts and increased spending for the military and infrastructure. The biggest menace as we see it is the continued piling of more debt on to America’s already towering load. Is Trump’s plan akin to just another government stimulus injection of more paper money that might lead to Price Inflation, or even a hyperinflation? His proposed spending has been estimated to add a budget deficit of $8 trillion over the next 10 years, 40% over the current $20 trillion, measurably not much different from the recent deficits. Trump explains this away, saying it will be “deficit neutral” by blocking unfair imports, charging foreign exporters for access to American markets and enacting an “America First” business stance, with heavy tariffs, even if it leaves America a closed unit by reducing current free trade. We once more ponder whether the era of international free trade is ending, as it did during what we call “The First Great Depression.” Is Trump really planning to use access to the US market as a bargaining chip? We have many dizzying considerations, and see these parsed nowhere else yet.

January 4, 2017, Page 14 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

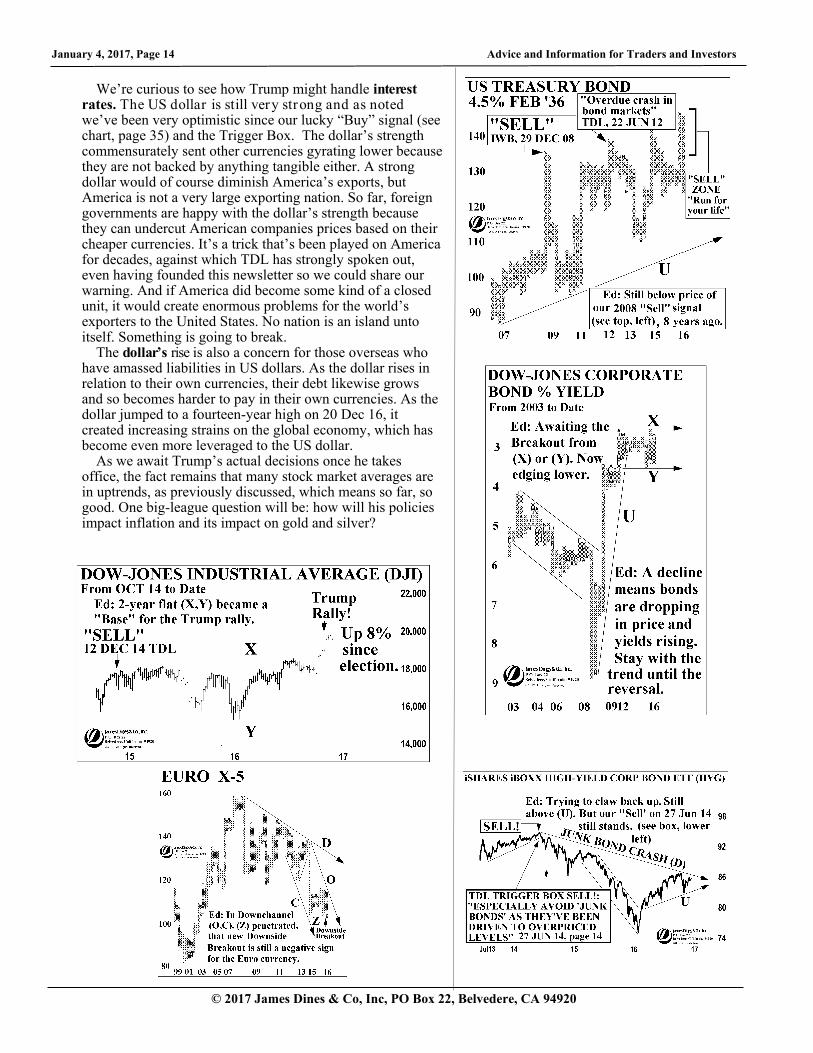

We’re curious to see how Trump might handle interest rates. The US dollar is still very strong and as noted we’ve been very optimistic since our lucky “Buy” signal (see chart, page 35) and the Trigger Box. The dollar’s strength commensurately sent other currencies gyrating lower because they are not backed by anything tangible either. A strong dollar would of course diminish America’s exports, but America is not a very large exporting nation. So far, foreign governments are happy with the dollar’s strength because they can undercut American companies prices based on their cheaper currencies. It’s a trick that’s been played on America for decades, against which TDL has strongly spoken out, even having founded this newsletter so we could share our warning. And if America did become some kind of a closed unit, it would create enormous problems for the world’s exporters to the United States. No nation is an island unto itself. Something is going to break.

The dollar’s rise is also a concern for those overseas who have amassed liabilities in US dollars. As the dollar rises in relation to their own currencies, their debt likewise grows and so becomes harder to pay in their own currencies. As the dollar jumped to a fourteen-year high on 20 Dec 16, it created increasing strains on the global economy, which has become even more leveraged to the US dollar.

As we await Trump’s actual decisions once he takes office, the fact remains that many stock market averages are in uptrends, as previously discussed, which means so far, so good. One big-league question will be: how will his policies impact inflation and its impact on gold and silver?

Advice and Information for Traders and Investors January 4, 2017, Page 15

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

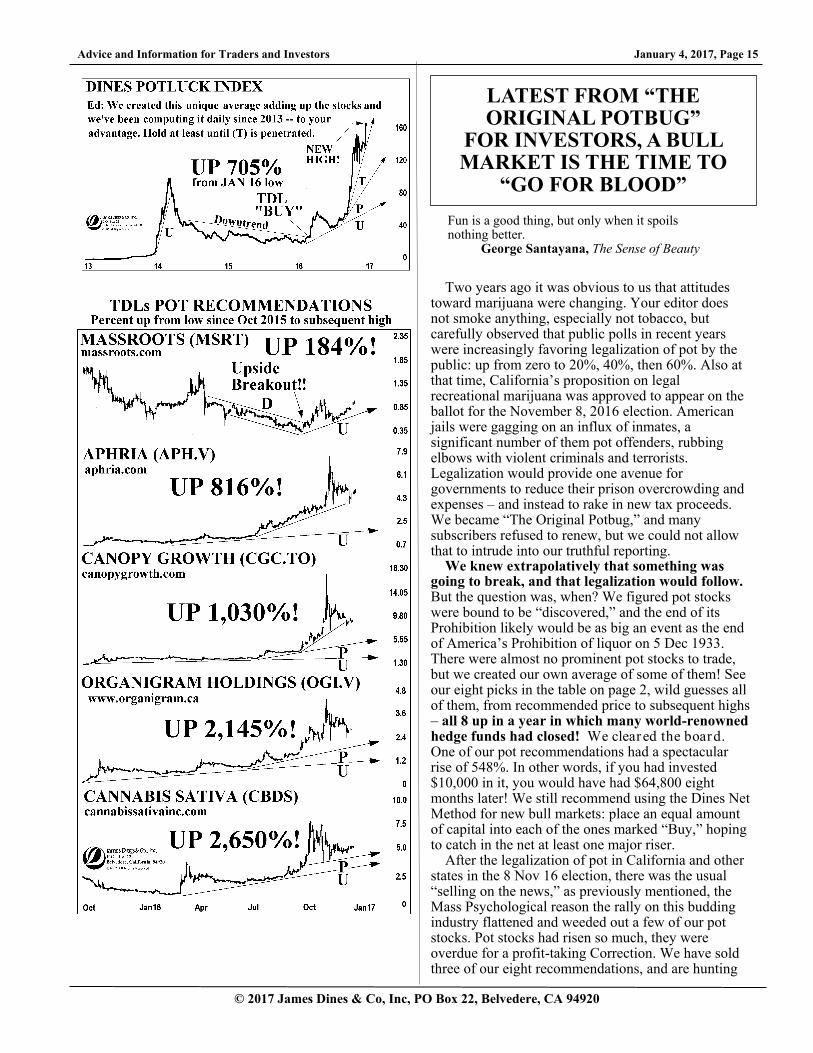

Two years ago it was obvious to us that attitudes toward marijuana were changing. Your editor does not smoke anything, especially not tobacco, but carefully observed that public polls in recent years were increasingly favoring legalization of pot by the public: up from zero to 20%, 40%, then 60%. Also at that time, California’s proposition on legal recreational marijuana was approved to appear on the ballot for the November 8, 2016 election. American jails were gagging on an influx of inmates, a significant number of them pot offenders, rubbing elbows with violent criminals and terrorists. Legalization would provide one avenue for governments to reduce their prison overcrowding and expenses – and instead to rake in new tax proceeds. We became “The Original Potbug,” and many subscribers refused to renew, but we could not allow that to intrude into our truthful reporting.

We knew extrapolatively that something was going to break, and that legalization would follow. But the question was, when? We figured pot stocks were bound to be “discovered,” and the end of its Prohibition likely would be as big an event as the end of America’s Prohibition of liquor on 5 Dec 1933. There were almost no prominent pot stocks to trade, but we created our own average of some of them! See our eight picks in the table on page 2, wild guesses all of them, from recommended price to subsequent highs – all 8 up in a year in which many world-renowned hedge funds had closed! We cleared the board. One of our pot recommendations had a spectacular rise of 548%. In other words, if you had invested $10,000 in it, you would have had $64,800 eight months later! We still recommend using the Dines Net Method for new bull markets: place an equal amount of capital into each of the ones marked “Buy,” hoping to catch in the net at least one major riser.

After the legalization of pot in California and other states in the 8 Nov 16 election, there was the usual “selling on the news,” as previously mentioned, the Mass Psychological reason the rally on this budding industry flattened and weeded out a few of our pot stocks. Pot stocks had risen so much, they were overdue for a profit-taking Correction. We have sold three of our eight recommendations, and are hunting

LATEST FROM “THE ORIGINAL POTBUG”

FOR INVESTORS, A BULL MARKET IS THE TIME TO

“GO FOR BLOOD”

Fun is a good thing, but only when it spoils nothing better. George Santayana, The Sense of Beauty

January 4, 2017, Page 16 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

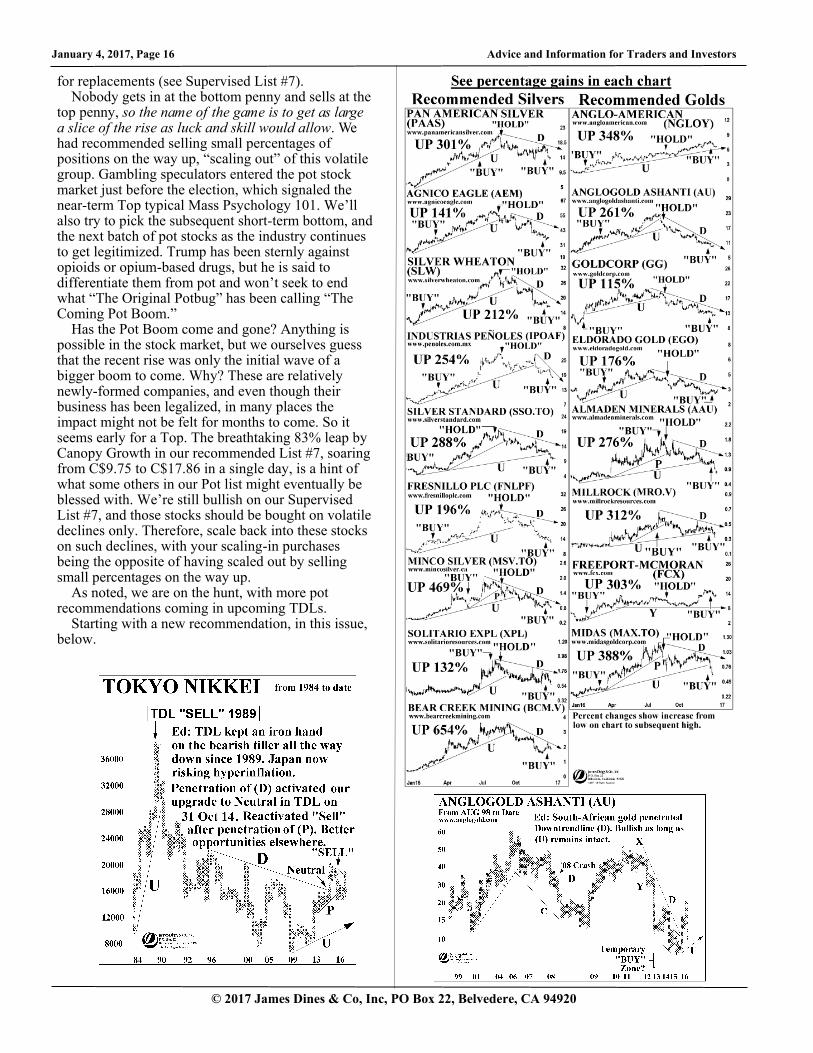

for replacements (see Supervised List #7). Nobody gets in at the bottom penny and sells at the

top penny, so the name of the game is to get as large a slice of the rise as luck and skill would allow. We had recommended selling small percentages of positions on the way up, “scaling out” of this volatile group. Gambling speculators entered the pot stock market just before the election, which signaled the near-term Top typical Mass Psychology 101. We’ll also try to pick the subsequent short-term bottom, and the next batch of pot stocks as the industry continues to get legitimized. Trump has been sternly against opioids or opium-based drugs, but he is said to differentiate them from pot and won’t seek to end what “The Original Potbug” has been calling “The Coming Pot Boom.”

Has the Pot Boom come and gone? Anything is possible in the stock market, but we ourselves guess that the recent rise was only the initial wave of a bigger boom to come. Why? These are relatively newly-formed companies, and even though their business has been legalized, in many places the impact might not be felt for months to come. So it seems early for a Top. The breathtaking 83% leap by Canopy Growth in our recommended List #7, soaring from C$9.75 to C$17.86 in a single day, is a hint of what some others in our Pot list might eventually be blessed with. We’re still bullish on our Supervised List #7, and those stocks should be bought on volatile declines only. Therefore, scale back into these stocks on such declines, with your scaling-in purchases being the opposite of having scaled out by selling small percentages on the way up.

As noted, we are on the hunt, with more pot recommendations coming in upcoming TDLs.

Starting with a new recommendation, in this issue, below.

Advice and Information for Traders and Investors January 4, 2017, Page 17

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

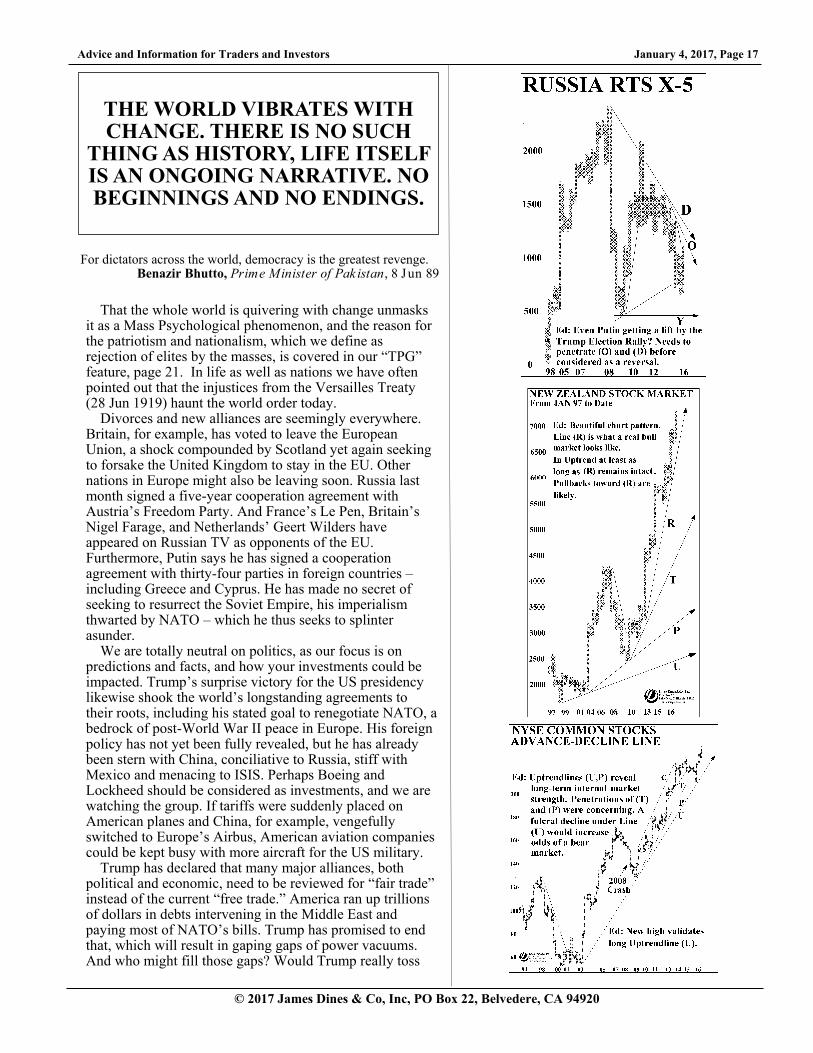

That the whole world is quivering with change unmasks it as a Mass Psychological phenomenon, and the reason for the patriotism and nationalism, which we define as rejection of elites by the masses, is covered in our “TPG” feature, page 21. In life as well as nations we have often pointed out that the injustices from the Versailles Treaty (28 Jun 1919) haunt the world order today.

Divorces and new alliances are seemingly everywhere. Britain, for example, has voted to leave the European Union, a shock compounded by Scotland yet again seeking to forsake the United Kingdom to stay in the EU. Other nations in Europe might also be leaving soon. Russia last month signed a five-year cooperation agreement with Austria’s Freedom Party. And France’s Le Pen, Britain’s Nigel Farage, and Netherlands’ Geert Wilders have appeared on Russian TV as opponents of the EU. Furthermore, Putin says he has signed a cooperation agreement with thirty-four parties in foreign countries – including Greece and Cyprus. He has made no secret of seeking to resurrect the Soviet Empire, his imperialism thwarted by NATO – which he thus seeks to splinter asunder.

We are totally neutral on politics, as our focus is on predictions and facts, and how your investments could be impacted. Trump’s surprise victory for the US presidency likewise shook the world’s longstanding agreements to their roots, including his stated goal to renegotiate NATO, a bedrock of post-World War II peace in Europe. His foreign policy has not yet been fully revealed, but he has already been stern with China, conciliative to Russia, stiff with Mexico and menacing to ISIS. Perhaps Boeing and Lockheed should be considered as investments, and we are watching the group. If tariffs were suddenly placed on American planes and China, for example, vengefully switched to Europe’s Airbus, American aviation companies could be kept busy with more aircraft for the US military.

Trump has declared that many major alliances, both political and economic, need to be reviewed for “fair trade” instead of the current “free trade.” America ran up trillions of dollars in debts intervening in the Middle East and paying most of NATO’s bills. Trump has promised to end that, which will result in gaping gaps of power vacuums. And who might fill those gaps? Would Trump really toss

THE WORLD VIBRATES WITH CHANGE. THERE IS NO SUCH

THING AS HISTORY, LIFE ITSELF IS AN ONGOING NARRATIVE. NO BEGINNINGS AND NO ENDINGS.

For dictators across the world, democracy is the greatest revenge. Benazir Bhutto, Prime Minister of Pak istan, 8 Jun 89

January 4, 2017, Page 18 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

dependent Europe and the Middle East out the door, or might he negotiate something else?

China looms large in our thinking. A very aggressive military hegemony, demanding control of all the South and East China Seas including historic international waters, it will surely be challenged by Trump. The only other power capable of challenging China would be Russia, its recent new ally, with the possible exception of two smaller powers in Asia, Japan and South Korea – were Trump to obtain nuclear weapons for them.

We began to change our Intermediate-term forecast on China in 2007, having been bullish on it for many decades previously, as the trend to democracy in China reversed Southward toward TPG Box #9. Worse, as notorious copiers and copyright thieves, China also made off with America’s Keynesian economic theories hook, line and sinker. Particularly running their printing presses in overdrive after its 2008 international market plunges. We flashed a near-term “Sell” on Chinese markets on 23 May 2014, near their peaks, even though China’s foreign-exchange reserves had soared to a breathtaking four-trillion dollars in 2014 by having sold cheap items in its role as factory of the world. We expressed outrage at their trade imbalances because China would not need to bother converting America to communism – they could just buy it! Indeed, China has since then purchased mines, commercial real-estate, farmland, and leading high-tech companies – worldwide. TDL has been a helpless spectator, watching adult fools letting China print its currency without limit, then convert it to dollars to buy real assets to be held forever, historic bargains not matched since America bought Alaska from Russia for $7.2 million in 1867.

But things are about to change. Since our last short-term “Sell” for China’s stocks, that country’s Forex (foreign exchange) has declined a whopping one-fifth to $3.22 trillion from its peak of $3.99 trillion in June 2014, another sign that our “Sell” on China might have nailed its top with deadly accuracy.

And there it was on 19 Dec 16, on the front page of the Wall Street Journal no less, the headline, “Bond Rout Poses New Risk for China. China’s $8-Trillion Plus Bond Market Last Week Saw Its Government Bonds Plunging.”

Let China’s possible bond crisis sink in. China’s military aggressiveness coincided with our

prediction of its bank and real-estate crash beginning to come true, though denied by China instead as a minor “slowdown.” How? Exports of Chinese goods are declining because of generally anemic worldwide economic growth. So China decided to expand internally. China meanwhile is gagging on debt accumulated by its Keynesian economists, running printing presses non-stop, with that cash flushing into a real-estate bubble – or fleeing overseas. We take the admitted solitary position that China is on the verge of a steep economic downturn that normally results in more dictatorial power by its leaders – as in wartime. In other

Advice and Information for Traders and Investors January 4, 2017, Page 19

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

words, China is spoiling for a fight, just as aggressive Trump arrives on the scene.

Trump’s aforementioned economic demand for fair trade could not have come at a worse moment for China, now happily enjoying a trade surplus of $44.6 billion last November, and an annual total of $593 billion last year. Trump has repeatedly vowed he would seek to balance it toward zero. Will the cornered Chinese dragon lash out at someone? East Asian nations? America? There is potential for war.

Furthermore, our longstanding prediction of an eventual war for empty Siberia, to provide living room for China’s teeming masses, still stands. But a short-term change has cropped up. Russia, hurting from the economic sanctions inflicted on it after its expensive invasions of Crimea and East Ukraine, has cozied up to China as a partner to replace the EU – again, just at the moment Trump threatens to trash previous trade agreements that would have excluded China and Russia! Now those two nations could form their own trade community, freezing America out. Let’s see how Trump handles these probabilities, hopefully without a war.

In the 1930s, Japan's emperor Hirohito was leading Japan toward war to kick America out of the West Pacific, and now it is Kim Jong Un of North Korea’s turn. When America punished Japan for having invaded Manchuria and China by blocking its oil imports, Japan’s General Staff attacked America’s fleet on 7 Dec 1941 in Pearl Harbor, to ensure unimpeded access to Southeast Asia’s oil and other natural resources, and started WWII in the Pacific.

China sees America as a successful neighbor on the opposite side of the Pacific lake, but one with close ties to several nations east of China. North Korea continues threatening to hurl nuclear weapons at America. China is its only supplier and could stop it, but clearly doesn’t want to. Perhaps this is their bargaining chip with Trump. Or would Trump threaten to sell nuclear weapons to South Korea and Japan for self-defense? Or to Taiwan? Or build an Alaskan nuclear base on an Aleutian Island? We have not seen these considerations appear anywhere in the mainstream media yet.

Returning to Russia, hurt by sanctions and war expenses, it is now desperate enough for money that it has recently sold some of its top weapons systems to China, even while complaining that China would back-engineer them by taking them apart, so as to later sell them in competition with Russia!

Putin’s game is different. As stated above, he wants to break up NATO, so he could start picking off East European nations – either the small Baltic ones, or finishing off Ukraine. A signal of its advent would be his seizing the relatively unknown city of Mariupol. We believe he was about to attack there but, sizing up the chess board laid out in front of his entire western border, instead took advantage of a tactical opportunity to go into Syria. When America refused to topple Syria’s Assad, hoping he’d fall by himself, Assad publicly begged for help for his failing military. Putin leaped in. Why? To dismember Syria. With Assad as Russia’s puppet, the west coast of Syria would be a warm-water naval base for a future Russian fleet; a southern portion of Syria

January 4, 2017, Page 20 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

would be allied with Iran to encircle its mortal enemy Saudi Arabia; a northern part of Syria to Turkey and/or the Kurds; and nothing for America or Europe except floods of refugees that would push ex-NATO members falling into Putin’s lap. Putin had to hurry before Trump took office, plus he needed to crush Assad’s opponents quickly so as to cut Russia’s expenses. Thus, Putin employed Russian brutality that led to horrors in Aleppo using outlawed poison gas and barrel bombs on civilians, butchery of the type seen in Chechnya after its uprising – just kill everybody and then deny accusations of war crimes. National Low States bring “surprising bad luck.”

Russia will pay the price for getting into a multi-century civil war on the Shias’ side, disregarding the large Sunni majority in Russia. We again predict that bombs will soon be going off in Russia, as first predicted in the TDL of 7 Jul 2000, believe the unbelievable or not. For more see our Nostradinesus feature, page 24. Sadly, Russia’s Islamic nightmares have only just begun, and will last for centuries to come. We’ll get back to Russia and India in future TDLs. TDL is “The Original India Bug.”

Bottom line: the risk of war in 2017 is rising, gold and silver would be the traditional beneficiaries, and we could see a serious upmove in those two metals in 2017.

Is there any good news? Yes. As noted, TPG (see feature on page 21) projects a period of peace and prosperity, although its precise timing is uncertain.

1. We have long been bravely predicting physical immortality, and even now few believe it. Actually, we had been pondering it for many years, before our first announcement. We first reported our conclusion on 7 Nov 1981, as the keynote speaker at the James Blanchard conference in New Orleans, at that time we spoke out about immortality cautiously because it was such a scorned position. We predicted that the secret of aging would be discovered “within twenty-five years,” and indeed 90% of the human genome had been mapped by 2001. Since aging must be somewhere in that genome, and it is of finite length, we figured that human ingenuity would locate our time clock and change it. And the disease progeria should disclose its location. Also some viruses are immortal, so they already have cracked their own genetic secret.

Indeed, there have been a storm of discoveries relating to aging since our last update, and heavy-duty computerized analysis begun by numerous institutions.

One breakthrough is CRISPR, which stands for “clustered regularly interspaced short palindromic repeats.” Using this gene-altering tool, that promises to cure to everything from blindness to cancer, scientists can now manipulate the genes of any living creature with unprecedented ease. It can even be used to destroy an entire species, and we personally believe it should be done for any mosquito that carries human-killing diseases. (For a more detailed discussion of CRISPR, please see TDL of 5 Aug 16, page 11.)

The excerpts in this issue (pages 21 and 33) share some of the discoveries that should encourage everyone reading this to take better care of themselves, because we all might last far longer than we suspect. We hereby predict that somebody reading this newsletter will be immortal, believe the unbelievable or not!

Finally, we suggest reading the book The Immortality Edge by Michael Fossel, MD, Greta Blackburn, and Dave Woynarowski, MD, published by Wiley.

TDL’S LATEST ON HEALTH: “THE COMING PHYSICAL

IMMORTALITY”

Every time a human dies, a library burns. Anders Sandberg

(Legal Disclaimer: Since we are not doctors, never follow anything based on the Health Features in TDL, without first consulting with your doctor or other trusted health professional.)

Advice and Information for Traders and Investors January 4, 2017, Page 21

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

At the Salk Institute in California, the first attempt to reverse aging by reprogramming the genome has rejuvenated the organs of mice and lengthened their life spans by 30%. The issue of the journal Cell is “novel and exciting,” said Jan Vijg, an expert of aging at the Albert Einstein College of Medicine in New York. The finding is based on an animal’s biological clock being able to be wound back to a more youthful state. Ten years ago, the Japanese biologist Shinya Yamanaka amazed researchers by identifying four critical genes that reset the clock of the fertilized egg. The four genes are so powerful that they will reprogram even the genome of skin or intestinal cells back to the embryonic state. The clock of the aging process is created by the epigenome, the system of proteins that clads the cell’s DNA and controls which genes are active and which are suppressed. Only in the last few years have biologists come to realize that the state of the epigenome may be a major cause of aging. Nicholas Wade, New Y ork Times, 16 Dec 16 Ed: Science is closing in on “The Coming Secrets of Aging,” the goal being Physical Immortality, believe the unbelievable or not.

2. More wonderful news! We first reported on Ebola on 28 Aug 1998, followed by in-depth coverage beginning with the TDL of 28 Mar 14, with periodic updates since that time. When the world’s international health organizations did not take Ebola seriously, because they said it merely killed briefly and then disappeared, TDL was infuriated. It had not disappeared – it was so deadly it killed everybody in an African village and of course seemingly disappeared. TDL spoke out forcefully about Ebola’s danger, to no avail.

At the onset of the last Ebola outbreak, on 28 Mar 14 (page 10), months before its peak, TDL broke the news of a new epidemic in the latest episode of “The Coming Germ Wars.” We warned TDLrs to avoid travel to any affected areas. After many deaths, proper disease control tamed it.

Finally, last month, the medical establishment developed a vaccine (rVSV-ZEBOV) that, in fact, has been declared 100% effective on one strain of the virus! We ourselves, would get that vaccination if traveling anywhere in Africa, or any area with that past history. Because this mutating pathogen will be back.

(For more on health, please turn to page 33 for our carefully selected, and important excerpts.)

Libraries worldwide are loaded with books on psychology, but they’re all about individuals. Oddly, we are aware of only three books ever written on Mass Psychology, one of them admittedly dared to have been written by your editor. The dearth of information on this topic is odd because we all obviously react to each other in crowds, swept up as if by an invisible force in a mob, or in strong stock-market movements of the moment. Indeed, one is going on today, as the worldwide Mass has produced a rising number of powerful nationalist leaders that sent many stock markets skyward.

It’s no coincidence that this is happening across the world at the same time. Turkey for example is becoming a police state, power expanded on the pretext of state security by Erdogan seeking revenge for a failed coup against him. The Philippines’ leader openly admitted on television to having personally fatally shot drug dealers. China is slipping back to Mao Tse Tung’s tight communist controls. Russia’s Putin, as noted, dreams of resurrecting Soviet imperialism. Egypt. Syria. Venezuela’s socialism is sinking into a King Lear madness. A phenomenon spreading with the ease of ink dropped into a glass of water. Last but not least is North Korea; we often refer to George Orwell’s book 1984, whose futurology is proving to have been the work of a visionary genius.

Mass Psychology ripples through the work we will leave behind, which could be interpreted as our utter rejection of Keynesian economics, that features irresponsible excess debt and deficits. Sometimes we ponder whether Keynesian economics is the cause or effect of Mass Psychology. The chicken and the egg conundrum.

The worldwide acceptance of Keynesian economics by governments, hatched during the agony of what we call the “First” Great Depression, perhaps echoes to what we call “The Second Great Depression” – palliatively described these days as “The Great Recession of 2008.” We see the refusal to use the “depression” word as denial, therefore concealing a truth.

We have struggled for decades to decipher the secrets of Mass Psychology’s impact on the stock market, and we share with you our latest update to TPG (TDL’S Political Gamut) on page 22. We often include TPG in our predicting, a type of Rosetta Stone you yourself could use in the future.

TDL’S LATEST ON TPG (THE POLITICAL GAMUT)

What Does Brand-New Northward Trend Mean?

If there had been any formidable body of cannibals in the country he would have promised to provide them with free missionaries, fattened at taxpayers’ expense. H L Mencken

January 4, 2017, Page 22 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

Advice and Information for Traders and Investors January 4, 2017, Page 23

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

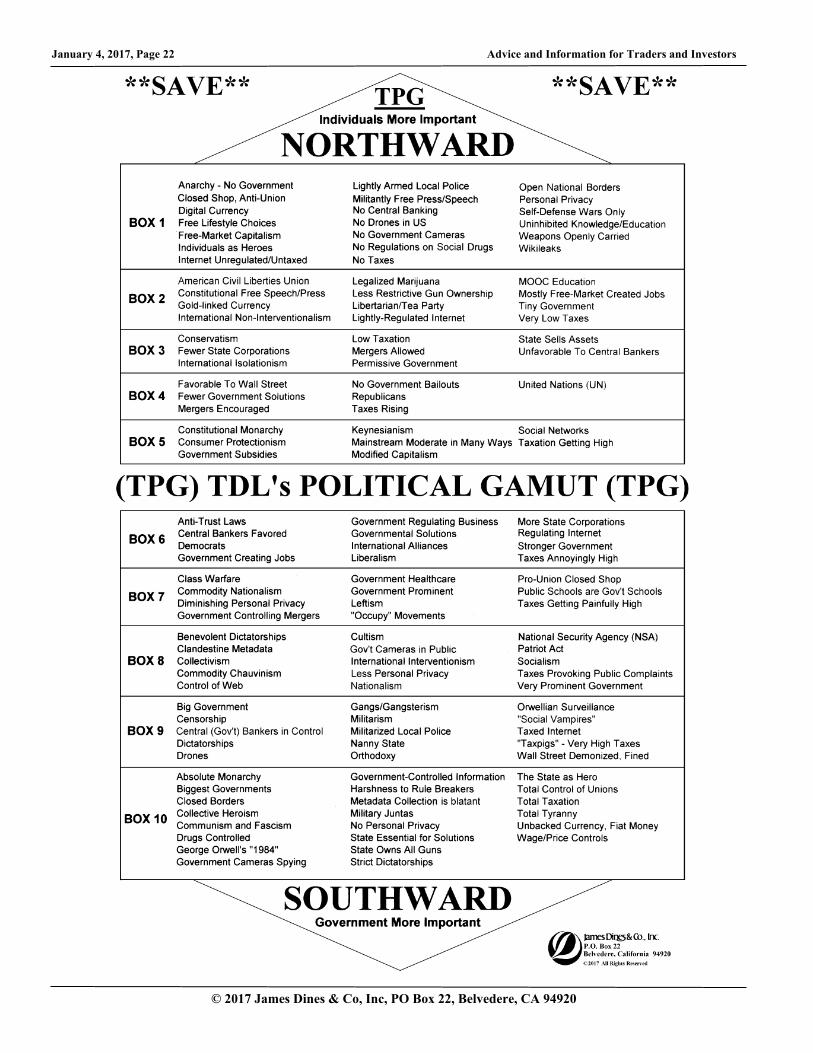

The accompanying graphic is quite simple: the box on top is very little government, descending in stages to total government in the bottom box. That’s it.

There is nothing to agree or disagree with, as the chart is as neutral as an alphabet, a measuring stick, or a vertical piano keyboard. Everybody could find the box somewhere on TPG with which they most. Please find the box that is closest to your views.

Fascinatingly, the Gamut is one of our key predicting tools, first shared with the world in detail in our Mass Psychology book (page 111). Let us demonstrate how TPG might be useful to you now. It can be used as a gauge for where America’s politics currently sits, near the top or bottom of TPG. The key insight: At either antipode one could anticipate directional change in the Mass Mind beginning to express itself. In other words, a r ise toward 1-3 or a decline toward 8-10, should result in a surprise turn!

COULD TPG PREDICT PROSPERITY

AND WARS? Could TPG help us predict war, or prosperity?

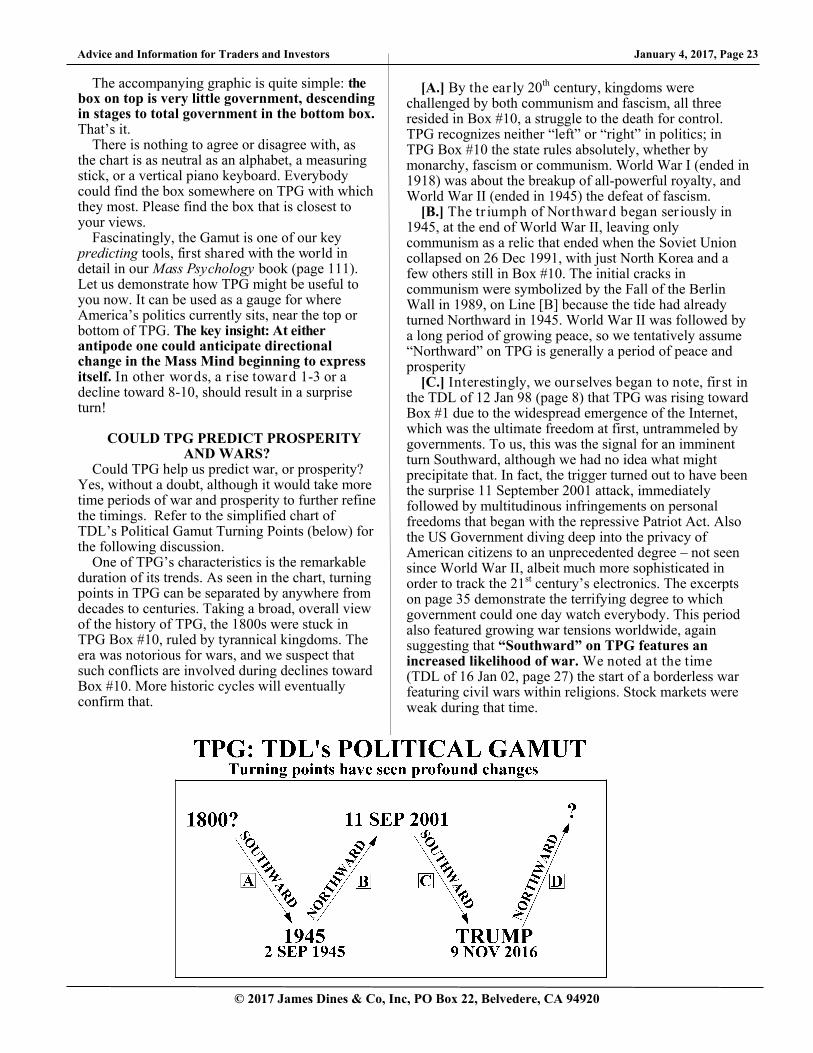

Yes, without a doubt, although it would take more time periods of war and prosperity to further refine the timings. Refer to the simplified chart of TDL’s Political Gamut Turning Points (below) for the following discussion.

One of TPG’s characteristics is the remarkable duration of its trends. As seen in the chart, turning points in TPG can be separated by anywhere from decades to centuries. Taking a broad, overall view of the history of TPG, the 1800s were stuck in TPG Box #10, ruled by tyrannical kingdoms. The era was notorious for wars, and we suspect that such conflicts are involved during declines toward Box #10. More historic cycles will eventually confirm that.

[A.] By the ear ly 20th century, kingdoms were challenged by both communism and fascism, all three resided in Box #10, a struggle to the death for control. TPG recognizes neither “left” or “right” in politics; in TPG Box #10 the state rules absolutely, whether by monarchy, fascism or communism. World War I (ended in 1918) was about the breakup of all-powerful royalty, and World War II (ended in 1945) the defeat of fascism.

[B.] The tr iumph of Nor thward began ser iously in 1945, at the end of World War II, leaving only communism as a relic that ended when the Soviet Union collapsed on 26 Dec 1991, with just North Korea and a few others still in Box #10. The initial cracks in communism were symbolized by the Fall of the Berlin Wall in 1989, on Line [B] because the tide had already turned Northward in 1945. World War II was followed by a long period of growing peace, so we tentatively assume “Northward” on TPG is generally a period of peace and prosperity

[C.] Interestingly, we ourselves began to note, fir st in the TDL of 12 Jan 98 (page 8) that TPG was rising toward Box #1 due to the widespread emergence of the Internet, which was the ultimate freedom at first, untrammeled by governments. To us, this was the signal for an imminent turn Southward, although we had no idea what might precipitate that. In fact, the trigger turned out to have been the surprise 11 September 2001 attack, immediately followed by multitudinous infringements on personal freedoms that began with the repressive Patriot Act. Also the US Government diving deep into the privacy of American citizens to an unprecedented degree – not seen since World War II, albeit much more sophisticated in order to track the 21st century’s electronics. The excerpts on page 35 demonstrate the terrifying degree to which government could one day watch everybody. This period also featured growing war tensions worldwide, again suggesting that “Southward” on TPG features an increased likelihood of war. We noted at the time (TDL of 16 Jan 02, page 27) the start of a borderless war featuring civil wars within religions. Stock markets were weak during that time.

January 4, 2017, Page 24 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

[D.] We repeatedly looked for the onset of a reversal to Northward because society was way heavily Southward, where reversals tend to occur.* Understanding Mass Psychology correctly, we took note of a remarkably popular socialist presidential candidate, Bernie Sanders, in TPG Box #8. TPG indicated to us that change was very near. As we study more turns on TPG, we hope one day to understand it well enough to also anticipate the actual reversal triggers.

Still, we pondered, would the world continue to shift further Southward toward war under Trump - and even stronger leaders emerging in other countries? It might seem that way to many, but if our TPG theory is correct this time we are somehow headed for peace and prosperity, as improbable as it might seem, what with nations worldwide in an arms race that usually precedes wars.

Personally, we believe a new rising trend [D] began with the election of President Donald Trump. Despite his reputation as a strong leader, TPG suggests in a strictly neutral TDL that he would somehow end up as flexible, free-market pro-capitalist, which could shock many. The turn on TPG is why his election caught the world largely off guard. While we don’t know how Northward his other policies get, and how long [D] will last, we hope we will all be able to predict the next reversal as TPG rises toward the top of the chart on page 22.

NEW DISCOVERY!

Something we have recently discerned: Mass Psychology can also corral other nations worldwide in a new trend because all national Masses are from the same source. Being human! We had long suspected that TPG itself would be amenable to international corroboration, by DIWPAT.**

We noticed how so many strong and populist (mass rejection of ruling elites, as noted) governments are emerging in the world these days, although others are still heading Southward - TPG’s prediction is that they will likewise rise Northward soon, following America, believe the unbelievable or not! If that prediction works, it would reaffirm not only that TPG works, but it might be the first tool ever discovered to actually map Mass Psychology!

Finally, is there a way to forecast stock market movements using TPG? We have long been very intrigued by this Long-Wave Theory, and one result of our research so far is that TPG could be used as a guide to predict the amount of control the rulers would exert over the various parts of their country, including the economy. Depending on the breadth of such, we could ascertain whether

companies might benefit from such policies as subsidies, tax breaks, and export controls affecting their profitability and competitiveness in domestic and international markets. Historically, Northward means governments interfere less with the operations of companies. We tentatively interpret that as grounds for stock market optimism in the coming period!

Trump is a builder by profession and, as noted, promises massive new construction in America, already possibly confirmed by uptrends in industrial metals. Dare we therefore hope that a huge new upleg in the stock market lies somewhere ahead, a ray of optimism? All will be revealed by the whispers of time. Net, net. TDLrs are advised to keep an open mind and remain hopeful*** for a period of peace and prosperity.

* 9 Jan 14 (page 17), 27 Jun 14 (pages 5, 8 & 13), 29 Aug 14 (page 8), 4 Jan 16 (page 31), 5 Feb 16 (page 6) and 4 Mar 16 (page 9). ** (Dinesism #10, The Dines Wolfpack Theory). When a few stocks of an economically related group move in a certain direction, the rest of the group will tend to follow that direction as “Confirmation.” *** TDL’s serious students of “High States” would recognize

this as DIHOPE rather than DIFOPE.

A. TERRORISM WILL HAUNT RUSSIA Summary: TDL Predicts “Moscow will bleed”

resulting from its past aggression against Chechnya, on Crimean Tatars, and now Islamists fighting Syria’s Assad.

After Russia’s failed incursion in Afghanistan, Russia reignited its conflict with Muslim fundamentalists in Chechnya. In its invasion of Crimea, Russia sent Crimean Tatars, a Turkic ethnic tribe, back into exile. In 2015 Russia joined Assad and the Shiite Iranians against Syrian rebels and Islamists (mostly Sunnis), embroiling itself in a new religious war, with deadly consequences – as predicted earlier.

Here are TDL's Predictions: 1) (The Dines Letter, 7 Jul 00, Page 10): An

Islamic uprising throughout Russia’s southern tier could threaten a centrifugalistic disintegration of Russia – losing a wide swath of territory to Iran or Turkey. Islamic fundamentalists have already added Russia to their list of enemies, along with the US, India, and Israel, so the outlines of the coming battles begin to emerge.

NOSTRADINESUS

To you, Baldrick, the Renaissance was just something that happened to other people, wasn’t it? Richard Curtis, Blackadder II (TV Ser ies)

Advice and Information for Traders and Investors January 4, 2017, Page 25

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

2) (The Dines Letter, 28 Mar 14, Page 3): The Tatars returned to Crimea after the Soviet Union imploded. It dawns on us that the media is not focusing on revenge-seeking Muslim states all across Russia’s southern border, from Turkey all the way to Tajikistan.

3) (The Dines Letter, 9 Oct 15, Page 8): Russia

is a nation whose national pastime is chess, and Putin has apparently decided to shift the attack to the south. His imperialism frustrated at Russia’s west by NATO, he moved his knight on the chessboard skipping over Turkey and plopped it into the seething cauldron of Syria. Putin could not care less if his current bombing in Syria drives the Sunnis out in favor of the Shias. But Putin’s plot has at least one strategic weakness. Jihadis worldwide have had bad blood with Russia since it invaded Afghanistan in 1979 – a disaster that created bin Laden himself. We have long-predicted the Muslim southern border of Russia, its "soft underbelly" (as Churchill described the invasion of Italy during World War II), is in danger of rising up, especially Dagestan in the Caucusus. Putin should grasp that his actions might trigger a jihadi uprising along the Stans.

4) (The Dines Letter, 6 Nov 15, Page 8): Of

great importance is the emergence of America as backers of the Sunnis, and Russia of the Shias, the two main externals in Islam’s civil war. Thus, Islam’s war has the added complexity of a proxy war between America and Russia. We suspect that the Russo-Shia alliance will eventually outrage Russia’s own Sunni Muslim population, igniting terrorism. Last month al Qaeda in Syria called on its followers for revenge by attacking Russia for having rescued Assad. The leader of the Al-Nusra Front even called for terror attacks to be launched from Russia’s North Caucasus. Moscow will bleed. This will spread the inferno metastasizing toward southern Russia, and it will go on from there.

5) (Interim Warning Bulletin, 10 Dec 15): An

angry Turkey was also upset that Russians had bombed its allied Turkmen battling Assad instead of ISIS.

6) (The Dines Letter, 4 Jan 16, Page 12): Russia

wants to dismember Syria, maintaining Assad as a puppet. Putin’s bombings have focused on Assad’s enemies instead of ISIS. As clever as Putin’s thrust into Syria might appear, we believe it incorporates a fatal flaw in that most of the Muslims in Russia are Sunnis, and he is blatantly taking sides with the Shiites in Iran, a blunder comparable with America having sided with Sunnis in the previous century.

This creates a greater risk of terrorism emerging from Putin’s North Caucasus region. Worse, Putin truly fears all the thousands of jihadis that have gone to fight and train with ISIS, who will soon return to wreak havoc in Russia.

7) (The Dines Letter, 2 Sep 16, Page 7): Putin’s new

axis includes both Shiites and Sunnis under the same umbrella. If we have been right that World War III would be dominated by a civil war within Islam, between Shiites and Sunnis – not even considering the fringe terrorist groups – the Axis should begin to suffer from an internal explosion based on the conflicts within that group possibly detonating a regional war. Terrorism will soon visit Russia.

Early Results 1) (Washington Post, 19 Dec 16): A Turkish police

officer who angrily denounced the bloodshed in Syria killed the Russian ambassador to Turkey in Ankara on Monday, shooting the diplomat in front of a room full of horrified spectators at an art gallery in an assassination captured on video and quickly shared around the world. As the ambassador, Andrei Karlov, lay on the floor, the assailant, 22-year-old Mevlut Mert Altintas, still waving his gun, screamed, “Don’t forget Aleppo! Don’t forget Syria!” The shooting was among the most brazen retaliatory attacks yet on Russia since Moscow entered the war in Syria on the side of President Bashar al-Assad, and unleashed a bombardment on Aleppo that has drawn international condemnation for what observers on the ground have called indiscriminate attacks on civilians. Some in Moscow suggested that the West was to blame for its support of moderate rebel factions in Syria.

B. TDL PREDICTS

“THE COMING PENSION FUND CRISIS” Summary: As the Federal Reserve stepped up its

quantitative easing and interest rate suppression, TDL declared “The Coming Pension Fund Crisis” in 10 Jan 2011 and has consistently warned of its worsening implications.

TDL Predictions 1) (The Dines Letter, Annual Forecast Issue, 10 Jan 11,

Page 24): America’s pension funds could be the next crisis. One Alabama city ran out of money in its pension fund in 2009 and stopped sending checks to its retired workers; it has tried to file for bankruptcy but the state won’t allow it, even though some residents are without electricity and running water. Maybe some of the money America is spending overseas should help Americans first,

January 4, 2017, Page 26 Advice and Information for Traders and Investors

© 2017 James Dines & Co, Inc, PO Box 22, Belvedere, CA 94920

as charity begins at home. Other states are in trouble, for example Michigan, Illinois and Pennsylvania, and what will happen when their payments to retirees stop? More borrowing from the Federal government? The Government bond market is another nightmare, and we have repeatedly steered TDLrs away from it. It is important to pay off and redeem debts with variable interest rates first; actually we prefer you get out of all debts. One of the unfortunate predictions in this TDL is "The Coming Wave of Bankruptcies in Muni Bonds." Illinois’ spending is double its income. The bottom line is that American states are bankrupt.

2) (The Dines Letter, 11 Nov 11, Page 4):

Investors are desperate for income precisely because of governments holding interest rates artificially lower so that they themselves could borrow cheaply and cheat income seekers of normal interest payments. By having distorted the free marketplace, it’s not just individuals who are having trouble earning money on their bank accounts or bonds, but insurance companies and banks that manage pension funds and other actuarial institutions that make assumptions based on long-term average interest rates who are making almost no money on their capital. TDL has been bitterly against what is being done because it is not free-enterprise capitalism, which will nevertheless be blamed for the consequences. That will not emerge into the public debate until pension funds become increasingly unable to pay benefits and wretched recipients finally demand to know, "What happened?"

3) (The Dines Letter, 19 Oct 12, Page 8): We