Embed Size (px)

Citation preview

3/26/2018

1

NEW MEXICO STATE AUDITOR

AUDIT RULE 2018

WAYNE A. JOHNSONState Auditor

NEW MEXICO GOVERNMENT AGENCIESAgency Type # Agency Type #

State Agencies (exc. PED) 92 Housing Authorities* 45

Public Education Department • State-Chartered Charter Schools

158

Regional Housing Authorities 3

Municipalities* 107 Soil & Water Districts 47

Counties 33 Special Districts 57

Schools and School Districts • District Charter Schools

9239

Mutual Domestic Water Association 220

Higher Education • Component Units of Higher Ed.

1723

Regional Educational Co-ops* 11

District Attorneys 15 Workforce Dev. Boards 5

District Courts 14 Public Improvement Districts 13

Hospitals & Special Hospital Dist.* 9 Tax Increment Development Districts* 8

Councils of Governments* 7 Land Grants 23

Acequias and Ditches 442

Total Entities = 1,381 (*includes component units)

Entity Count in 2015 was ~ 980

ORGANIZATIONAL CHARTExecutive Management

State Auditor, Wayne Johnson

Deputy State Auditor, Jack Emmons, CPA,

CFE

Chief of Staff, Bobbie Shearer

Deputy Chief of Staff, Enrique Knell

Chief Government Accountability Officer and General Counsel, Barbara Bruin, JD

3/26/2018

2

ORGANIZATIONAL CHARTFinancial Audit Division

Deputy State Auditor, Jack Emmons, CPA, CFE

Financial Audit Director, Lynette Kennard, CPA,

CGFM

Audit Manager, Elise Mignardot, CPA

Audit Manager, Vacant

Supervision per job basis

Audit Supervisor, VacantAudit Supervisor, Kevin

ChavezAudit Supervisor, Vacant

Supervision per job basis

Senior Auditor, Ralen Randel, CGFM, MACCT,

MBA, MASenior Auditor, Vacant

Supervision per job basis

Staff Auditor, Anne Kelbley

Staff Auditor, Vacant

Senior Auditor, Antonio Baca, CPA

Audit Supervisor, Lisa Jennings, MBA

Audit Supervisor, Jessica Lucero

Audit Manager, Shannon Sanders, CPA, CFE

ORGANIZATIONAL CHARTSpecial Investigations

Deputy State Auditor, Jack Emmons, CPA,

CFE

Special Investigations Director, Vacant

Audit Supervisor, Hamish Thomson,

CPA/CFF, CFE

Senior Auditor, Cindy Padilla

Staff Auditor, Guadalupe Jaramillo

Audit Supervisor, Chelsea Martin, CPA, CFE, CICA,

CRFAC

Senior Auditor, Terry Becenti, CFE

Staff Auditor, Brendan Miller

ORGANIZATIONAL CHARTAdministrative Services

Chief of Staff, Bobbie Shearer

IT Director, Arthur Baca

Budget & Finance Director, Antonio Medina

Human Resource

Manager, Lori Johnson

Operations Administrator,

Vacant

Exec. Sec. Adm., Amanda Herrera

3/26/2018

3

ORGANIZATIONAL CHARTGovernment Accountability Office, Compliance and Regulation Division

Chief Government Accountability Officer and General Counsel, Barbara Bruin, JD

Government Accountability Office

Senior Analyst, Joe Johnson

Compliance and Regulation Division

Compliance and Quality Control Director, Vacant

Records Custodian, Bernadet Martinez

Contracts Admin, Frank Valdez

AUDIT FEE HISTORY

PERIOD AUDITS TOTAL

CONTRACT AMOUNT HOURS AVERAGE

PER AUDIT AVERAGE PER HOUR

TOTAL IPA’s

REC'D CONT

PERCONT/ IPA

30-Jun-14 566 $19,616,231.20 169,969 $34,657.65 $115.41 82 67 8.45Fee Increase $916,007.94

30-Jun-15 612 $20,170,205.15 174,962 $32,957.85 $115.28 80 66 9.27Fee Increase $553,973.95

30-Jun-16 641 $20,290,486.09 148,140 $31,654.42 $136.97 76 63 10.17

Fee Increase $120,280.94

30-Jun-17 586 $19,054,474.00 150,438 $32,516.17 $126.66 74 61 9.61

Fee Decrease ($1,236,012.09)

NEW MEXICO STATE AUDITOR

Helping government work better by combatingfraud, waste and abuse.

• Annual audit accountability and finding reduction

• Accessible and responsive to agencies and IPAs

• Support for At Risk entities and Small Political Subdivisions

• Robust investigative efforts and case load reduction

STATE AUDITOR VISION

3/26/2018

4

WHAT WE SEE IN THE FUTURE

Possible audits of public financing

The future of CAFR preparation- Senate Bill 316- Joint task force CPA society and state officials- CAFR is the latest in the country- Timely CAFR should increase our bond rating thus lower interest rate.

Performance Audits- Internal control and compliance part of current audits- Revenues should be same or more for all firms

Honor Roll

• Accounting & Financial Solutions, LLC

• CliftonLarsonAllen, LLP

• Hinkle + Landers, PC

• Integrity Accounting & Consulting, LLC

• Kriegel/Gray/Shaw & Co., PC

• Kubiak, Melton, & Associates, LLC

• Manning Accounting and Consulting Services, LLC

• Precision Accounting, LLC

Honor Roll ‐ Criteria

• More than ten audits

• No significant deficiencies

• No late reports

• Pass peer review

3/26/2018

5

CONTRACTING

AUDIT RULE 2018

BASIC OVERVIEW OF THE AUDIT PROCESS

1. Submission of firm profiles2. Develop the list of approved audit firms3. State Auditor’s Office will select which audits we will perform4. Finalize Audit Rule, Audit Rule trainings & update financial compliance

audit contracts5. Send notification letters to Agencies/IPAs6. Agencies must submit draft contract by due date listed in Audit Rule7. IPAs conduct financial audits8. Progress payments9. Delivery and review of audit reports10. Report release and final payments

CONTRACTING 101

• Agency selects IPA

• Agency submits draft contract to OSA through OSA‐Connect

• OSA reviews draft contract

• OSA sends a letter of approval to Agency

– If OSA rejects contract, Agency can correct technical errors and resubmit, or request reconsideration

• Agency obtains necessary signatures and third‐party approvals (PED, HED, DFA)

• Agency sends PDF version of final agreement with all signatures to OSA

3/26/2018

6

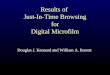

SELECTING AN AUDITOR

• Agency must receive written notification from the State Auditor before beginning the selection process (sent 2/27)

– You can request an exception BEFORE you start the RFP process

– You can perform interim work before this time

• Available at www.osanm.org:

– 2018 Audit Rule

– List of approved audit firms

– Past contract information

SELECTING AN AUDITOR FOR HIGHER ED

• Use OSA‐Connect to prepare draft contract

• Submit Contract to HED for review and approval

• HED issues each Institution an IPA Contract approval letter

• Institutions submit draft IPA Contract to the OSA via the OSA‐Connect website

• OSA reviews and approves draft IPA Contract based upon review and communicates approval via letter

• Institution obtains required contract signatures and submits final contract to OSA by email

CONTRACTING IS STILL ON OSA‐CONNECT

• WWW.OSA‐APP.ORG

• Don’t forget to update the contact persons for your agency.

• Contact Frank Valdez ([email protected]) for assistance.

• Make sure to review ALL information for your agency, even if it is pre‐filled in OSA‐Connect.

• Tier System‐ don’t forget to go to Agency Profile and confirm the tier for your agency for this fiscal year.

3/26/2018

7

WHERE TO FIND CONTRACTING INSTRUCTIONS

AUDIT AND AUP CONTRACTS

Fewer audit contract forms:– State Agencies with DFA Approval– Statewide CAFR– PERA and ERB– Higher Education– All Others

Scope of work section refers to Audit Rule.

Deadline section refers to Audit Rule. If you want to have the exact deadline stated in your contract, use “Other”.

CONTRACTS and OSA‐CONNECT

• “Intellisense” will auto-fill the name of your audit firm after you start typing.

• AUP contracts include the procedures as an exhibit (same as last year).

3/26/2018

8

PLEASE READ YOUR CONTRACT!

• Late notification required as soon as IPA becomes aware that the audit may be late.

• Subcontracting – requires State Auditor approval

• Conflict of interest – Contractor and Agency both certify that you are complying with Governmental Conduct Act.

• Pay Equity Reporting – are you (IPA) required to do it and are you?

– Applies to companies with 10 or more New Mexico employees OR 8 or more employees in the same job classification .

OSA CONNECT COMMON QUESTIONS & ERRORS

• Issues with the multi‐year proposal – this information is very important to get right.

OSA‐CONNECT COMMON ERRORS

• Don’t forget to press “submit.” Saving and printing are not the same as submitting contracts to OSA.

3/26/2018

9

AMENDMENTS TO CONTRACTS

• Contracts expire one year after the latest signature (or DFA approval for state agencies requiring DFA approval). After that you need to submit a NEW CONTRACT, you can no longer amend.

• Amendments are subject to review by the OSA. Increases in price must be justified by an increase in scope.

• Amendments to change the tier (up or down) of an AUP need to include the procedures for the new tier.

• Change from audit to AUP or vice versa requires new contract.

• Consider price changes in all amendments.

AMENDMENTS TO CONTRACTS

• The OSA has several forms of amendment – pick the one most appropriate for your situation

KEY AUDIT RULE CHANGES

AUDIT RULE 2018

3/26/2018

10

KEY AUDIT RULE CHANGES

• 2.2.2.8.G ‐ Rotation rule‐ remove expired exception language for multi‐year proposals.

• 2.2.2.10.H ‐ Expanded the referrals section to include "risk advisories", explaining where they are posted and the requirement for the IPA to consider in performing the annual financial and compliance audit. New requirement that the IPA provide a response to the "risk advisory" at least 14 days prior to the draft report.

KEY AUDIT RULE CHANGES

• 2.2.2.10.L ‐ Requirements of the summary of prior years findings only finding number, title, and status (resolved, repeated or repeated and modified).

• 2.2.2.10.L ‐ Corrective plan of action for federal findings must be in a separate document from auditor's findings and must be on the audited agency's letterhead.

TOP TEN FINDINGS

1. Lack of policies, procedures and internal controls

2. State Law compliance (Anti‐donation, open meetings)

3. Budgetary compliance

4. Financial reporting

5. Cash & investments (Stale checks, no reconciliation)

6. Payroll & related liabilities (W/H, pay rates, I‐9)

7. Grant compliance

8. Capital assets (No inventory)

9. Improper Procurement

10. Revenue & receivables (Deposit 24 Hr., Cut‐off)

3/26/2018

11

KEY AUDIT RULE CHANGES

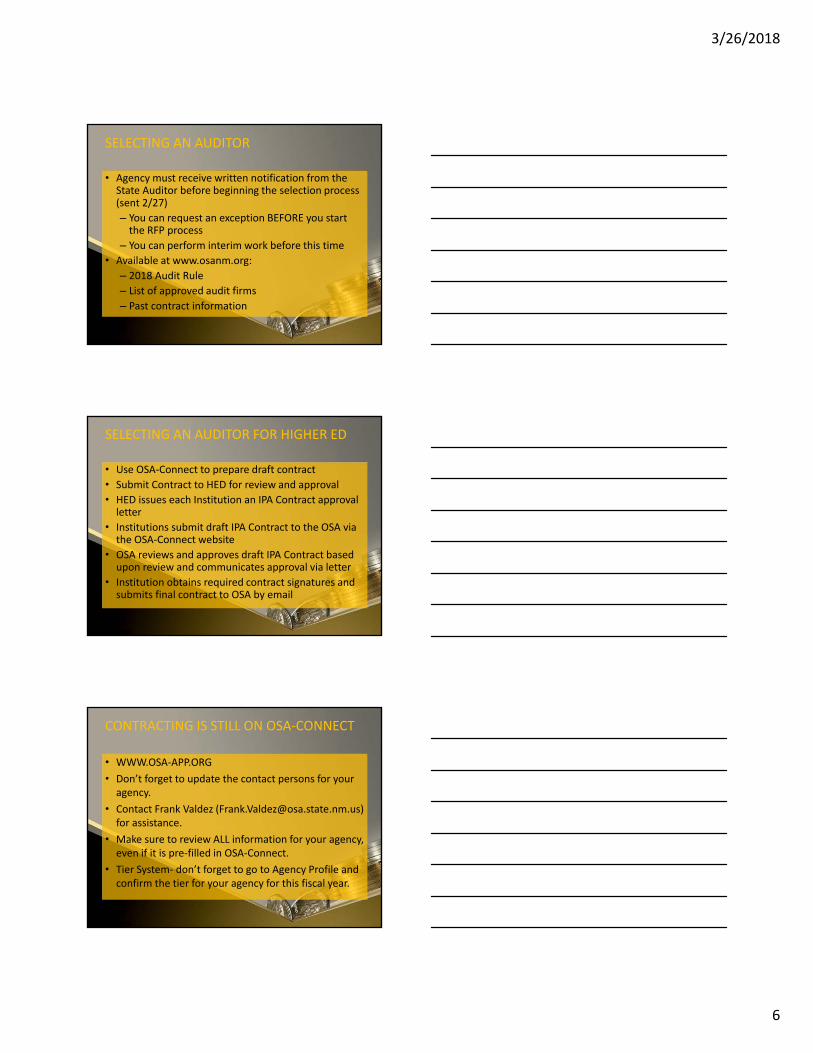

• 2.2.2.10.M ‐ Exit conference‐ requirements for what must be available at exit conference scaled back from full report to draft including the following: independent auditor's report, basic financial statements, findings, schedule of prior year findings, internal control report, and single audit compliance report.

• 2.2.2.10.W ‐ Capital asset inventory‐ eliminated the requirement to keep old assets capitalized under historical thresholds (under $5,000) on inventory listing.

KEY AUDIT RULE CHANGES

• 2.2.2.10.Z and DD ‐ GASB Schedules 68 and 75 schedules of employer allocation of PERA, ERB, and RHCA‐new requirement that IPA give in‐relation‐to opinion on supplementary information schedules included in schedule of employer allocations report, new required note disclosures for plans.

• 2.2.2.10.BB ‐ Tax abatement disclosure requirements modified to align with GASB 77 by allowing aggregation and the use of a quantitative threshold for determining individual disclosure.

KEY AUDIT RULE CHANGES

• 2.2.2.10.CC ‐ New standards‐updated for new standards effective for FY 18 GASB 75 PEB is the most significant.

• 2.2.2.12.F ‐ Indigent care reporting requirements for Hospitals‐clarified requirements to present schedules in audit report as supplementary information and to submit electronic version of schedules to OSA.

3/26/2018

12

KEY AUDIT RULE CHANGES

• 2.2.2.10.M.4 ‐ Once the audit report is released to the agency by the State Auditor and five days have passed or unless waived, the audit report shall be presented by the IPA to a quorum of the governing authority at an open meeting.

KEY AUDIT RULE CHANGES

• 2.2.2.12.G ‐ Schedule of asset management costs‐investing agencies (STO, PERA, ERB, and SIC).

• 2.2.2.15.A ‐ Fraud, waste and abuse reported to OSA‐new requirement that agencies respond to OSA‐SID fact‐finding inquiries within 21 calendar days of receipt. IPAs required to test compliance and report noncompliance as a finding.

ENHANCED ACCOUNTABILITY ‐ LATE AUDIT LIST

3/26/2018

13

ENHANCED ACCOUNTABILITY ‐ LATE AUDIT LIST CONT.

ENHANCED ACCOUNTABILITY –ADVERSE or DISCLAIMED OPIONIONS LIST

PAST RULES CAUSING PROBLEMS

Cash vs Accrual

• 2.2.2.10.D.1 – The financial statements presented in audit report shall be prepared from the agency’s books of record.

• 2.2.2.10.D.2 – The financial statements are the responsibility of the agency.

• 2.2.2.8.L – IPA shall maintain independence in accordance with governmental auditing standards.

3/26/2018

14

PAST RULES CAUSING PROBLEMS

Late Reports

• 2.2.2.9.A.5 – As soon as the auditor is aware that the audit will be late, a letter must notify the State Auditor with a copy to the oversight agency (DFA, PED, LGD). Letter shall contain specific explanation regarding why the report will be late. Must be signed by the IPA and a representative of the agency.

COMBATING WASTE, FRAUD & ABUSE

AUDIT RULE 2018

FRAUD – AUDIT RULE NMAC 2.2.2.15.A.1

• FINANCIAL REPORTING

‐ Intentional misstatements or omissions of amounts or disclosures.

• MISUSE OF PUBLIC FUNDS PROHIBITED BY LAW

• MISAPPROPRIATION

• EMBEZZLEMENT

• CORRUPTION (bribery and other illegal acts) etc.

3/26/2018

15

WASTE AND ABUSE – AUDIT RULE

• “… MAY IMPACT THE ACHIEVEMENT OF DEFINED OBJECTIVES”

• NMAC 2.2.2.15.A.2 and GAO‐14‐704G federal internal control standards paragraph 8.02

• Waste is the act of using or expending resources carelessly, extravagantly, or to no purpose.

• Abuse involves behavior that is deficient or improper when compared with behavior that a prudent person would consider reasonable and necessary operational practice given the facts and circumstances.

WHAT WE SEE AND WHAT WE DO

• About 300 tips per year– Time theft, ethics, procurement, embezzlement, misuse of

resources

• Log, prioritize, assign and discuss

• Fact finding– Review laws, policies, public information, media

• Determine course of action– Special audit/ risk review– Forward to internal audit/inspector general – Forward to other oversight body– Forward to management/governing body– Refer to IPA for financial audit– Close

NOTIFICATION OF CRIMINAL VIOLATIONS

• NMSA 1978, § 12‐6‐6 (Criminal violations)

– An agency or independent auditor shall report a violation of a criminal statute in connection with financial affairs immediately to the state auditor.

• NMAC 2.2.2.10.N.2 (Audit Rule)

–Must be in writing

– Include an estimate of dollar amount involved

– Detailed description of the violation, including names of persons involved and any action taken or planned

3/26/2018

16

OSA REFERRALS TO IPAS

• Purpose

– Alert IPA to issues potentially affecting planning and risk assessment, or non‐compliance with state law

• Responsibilities of IPA

– Consider issues and perform procedures as necessary

– Consider confidentiality of referral

– Respond in writing prior to audit submission

• Responsibilities of Agency

– Cooperate with IPA to ensure timely and adequate response

SPECIAL ENGAGEMENTS

• NMSA 1978, § 12‐6‐3 (C) states, “In addition to the annual audit, the state auditor may cause the financial affairs and transactions of an agency to be audited in whole or in part.”

• NMAC 2.2.2.15 (Special Audits, Attestation Engagements, Performance Audits and Forensic Audits)

• OSA designated• Agency‐initiated

SPECIAL ENGAGEMENTS

• NMAC 2.2.2.15.B.9 (Required Reporting). Reports must state the applicable standards and findings should include condition, criteria, cause, effect, recommendation, and management response with corrective action plan.

• NMAC 2.2.2.15.C (Agency‐initiated). With exception of agencies authorized by statute to conduct performance and forensic audits, contracts relating to financial fraud, waste or abuse must be approved by the OSA.

3/26/2018

17

SPECIAL INVESTIGATIONS DIVISION ‐ FY18

UPDATES FROM FISCAL YEAR 2017 AND EARLIER

• La Promesa Charter School

• Southwest Secondary/Primary Learning Centers

• Office of the Superintendent of Insurance

• City of Jal

• Dora Consolidated Schools

• Developmental Disabilities Planning Council

• Northern New Mexico College

• Hanover Mutual Domestic Water Utility Authority

• Procurement Study

SPECIAL INVESTIGATIONS DIVISION ‐ FY18

OTHER CASES IN THE LAST YEAR:

• Town of Silver City

• Albuquerque Public Schools

• University of New Mexico

• City of Las Vegas

• Otis Mutual Domestic Water Utility Authority

• Martin Luther King Commission

THANK YOU!

Website: www.saonm.org

Fraud Hotline: 1‐866‐OSA‐FRAUD

Main Phone: 505‐476‐3800

3/26/2018

18

Government Finance Experts Conference

May21,22,23,2018SandiaResort&CasinoAlbuquerque