Embed Size (px)

Citation preview

2018 Cattle Market Situation and Outlook - August 9, 2018

Josh Maples - Assistant ProfessorLivestock Extension Economist

Overview

• Market Conditions• Beef Cattle Market Fundamentals

-Supply and Demand• Beef Demand & Consumption• International Trade• Questions/Discussion

Market Conditions

C-P-4910/10/17

90

110

130

150

170

190

210

JAN APR JUL OCT

$ Per Cwt.

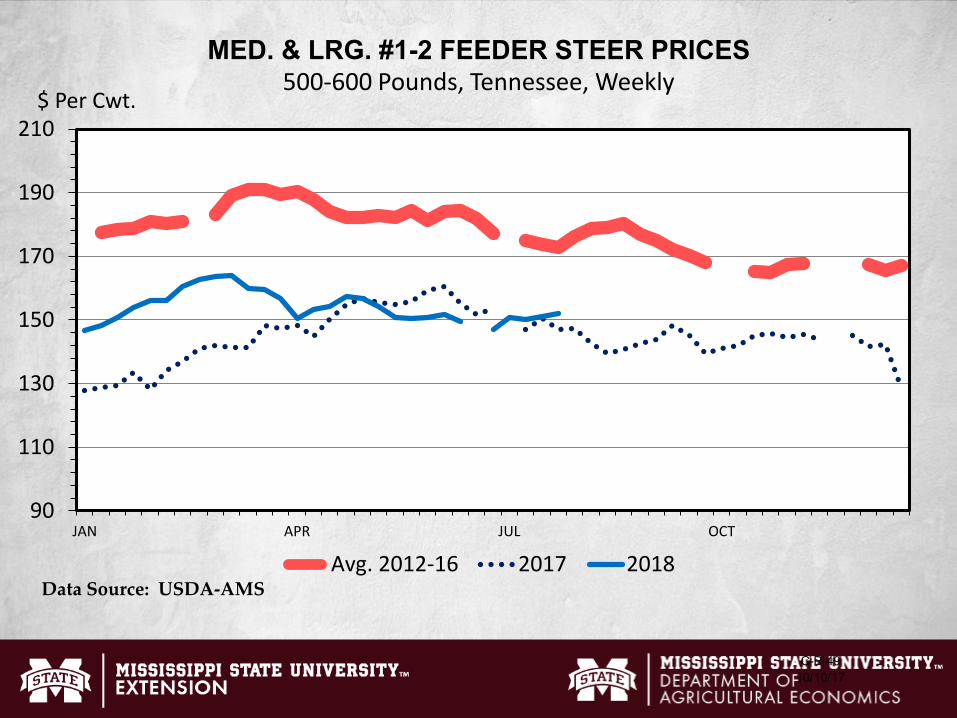

MED. & LRG. #1-2 FEEDER STEER PRICES500-600 Pounds, Tennessee, Weekly

Avg. 2012-16 2017 2018Data Source: USDA-AMS

C-P-4910/10/17

90

100

110

120

130

140

150

160

170

JAN APR JUL OCT

$ Per Cwt.

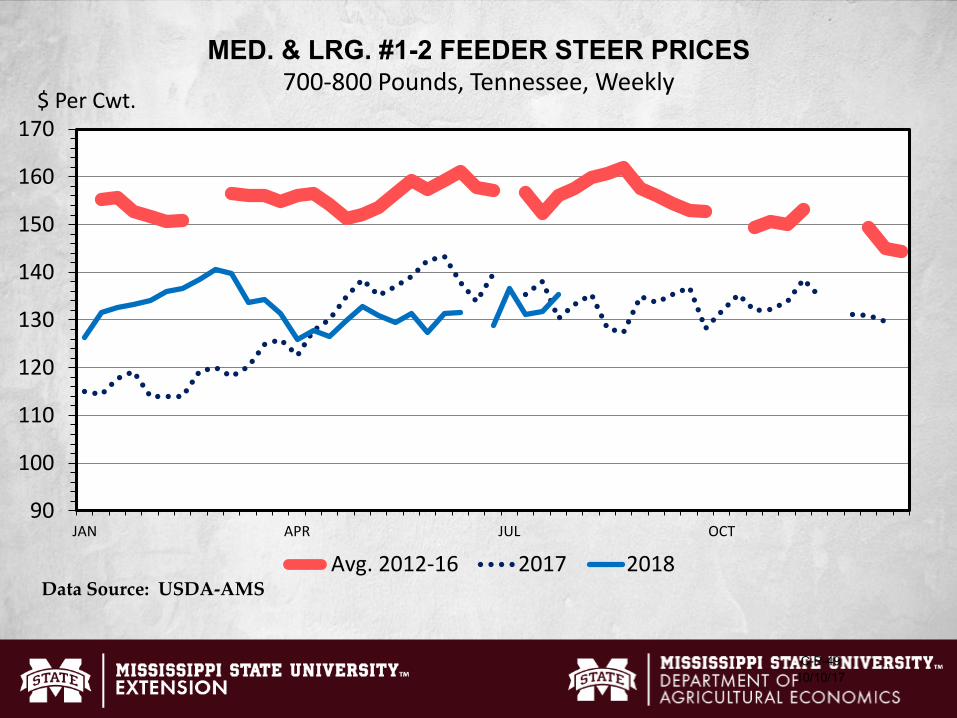

MED. & LRG. #1-2 FEEDER STEER PRICES700-800 Pounds, Tennessee, Weekly

Avg. 2012-16 2017 2018Data Source: USDA-AMS

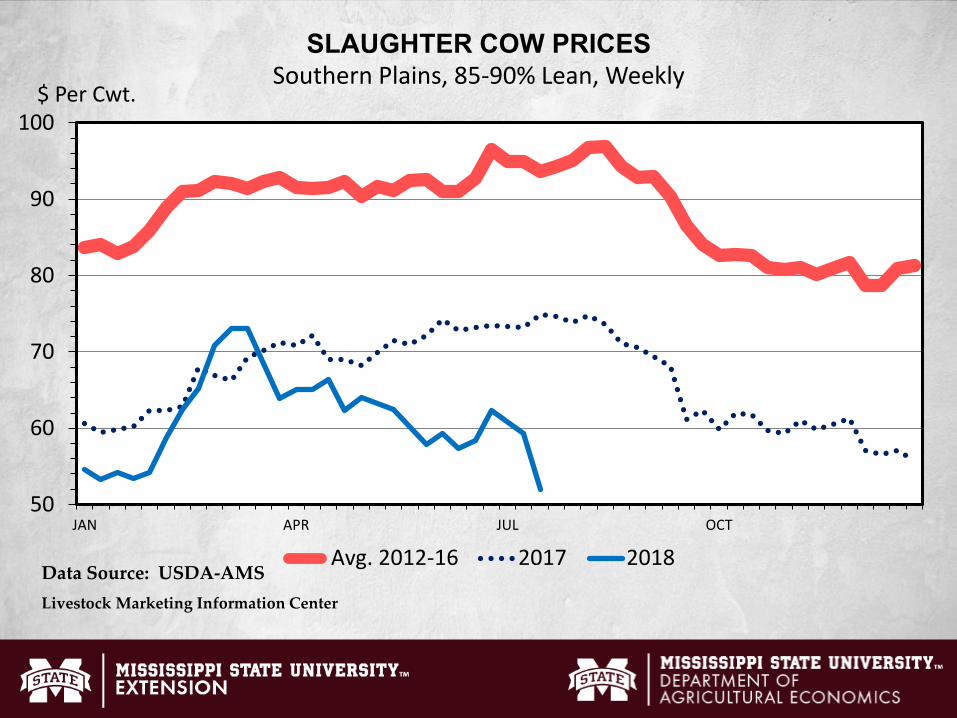

50

60

70

80

90

100

JAN APR JUL OCT

$ Per Cwt.

SLAUGHTER COW PRICESSouthern Plains, 85-90% Lean, Weekly

Avg. 2012-16 2017 2018Data Source: USDA-AMSLivestock Marketing Information Center

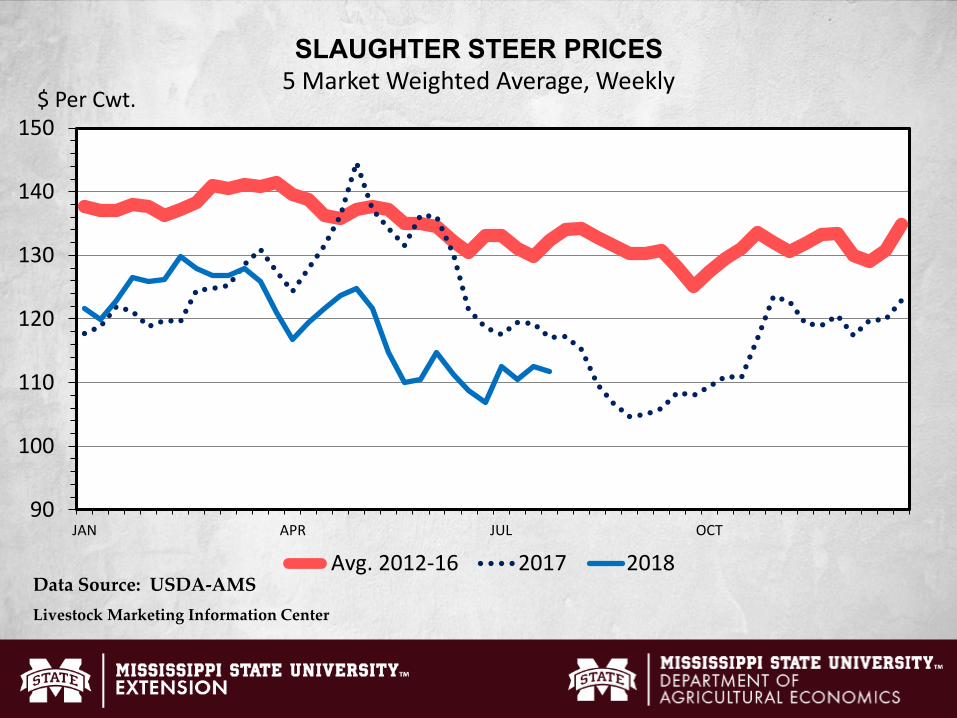

90

100

110

120

130

140

150

JAN APR JUL OCT

$ Per Cwt.

SLAUGHTER STEER PRICES5 Market Weighted Average, Weekly

Avg. 2012-16 2017 2018Data Source: USDA-AMSLivestock Marketing Information Center

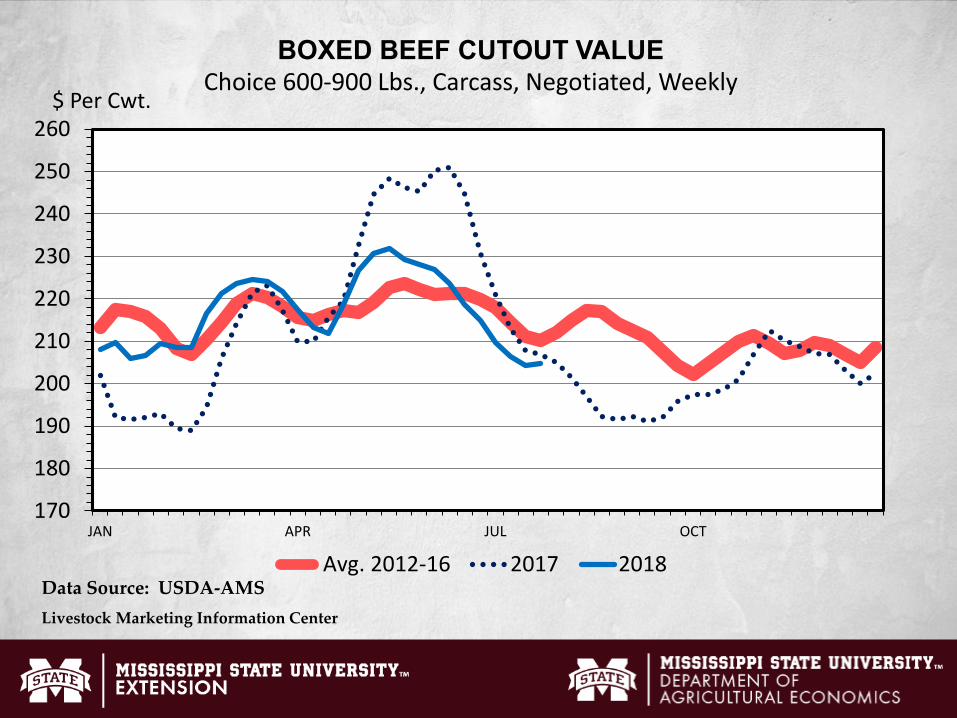

170

180

190

200

210

220

230

240

250

260

JAN APR JUL OCT

$ Per Cwt.

BOXED BEEF CUTOUT VALUEChoice 600-900 Lbs., Carcass, Negotiated, Weekly

Avg. 2012-16 2017 2018Data Source: USDA-AMSLivestock Marketing Information Center

Supply

80

85

90

95

100

105

1988 1993 1998 2003 2008 2013 2018

Mil. Head

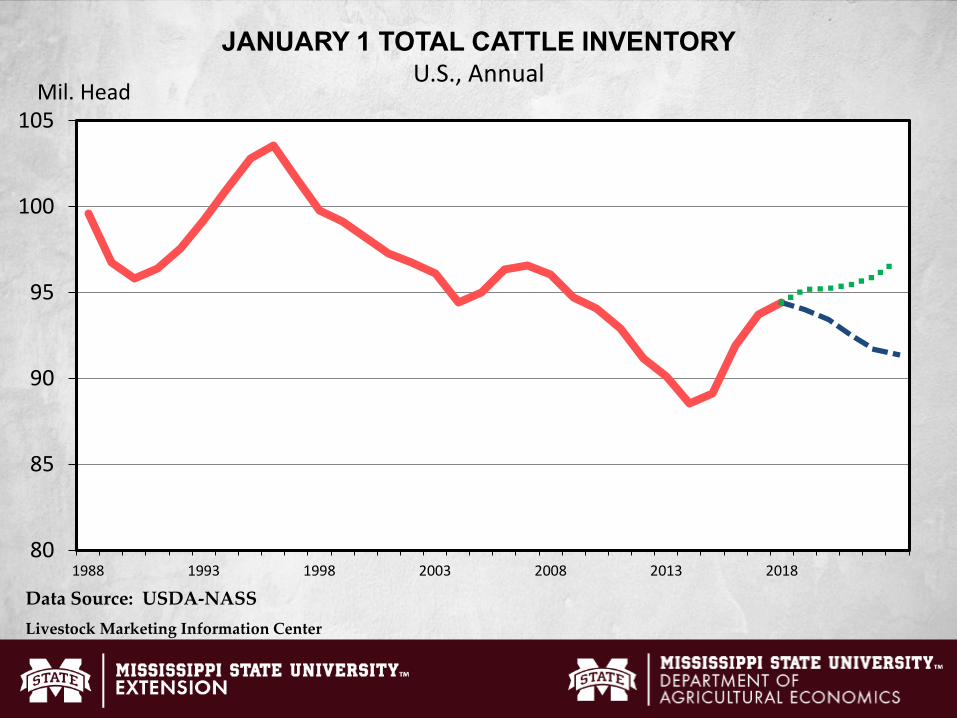

JANUARY 1 TOTAL CATTLE INVENTORYU.S., Annual

Data Source: USDA-NASSLivestock Marketing Information Center

37

38

39

40

41

42

43

44

45

46

1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018 2021

Mil. Head

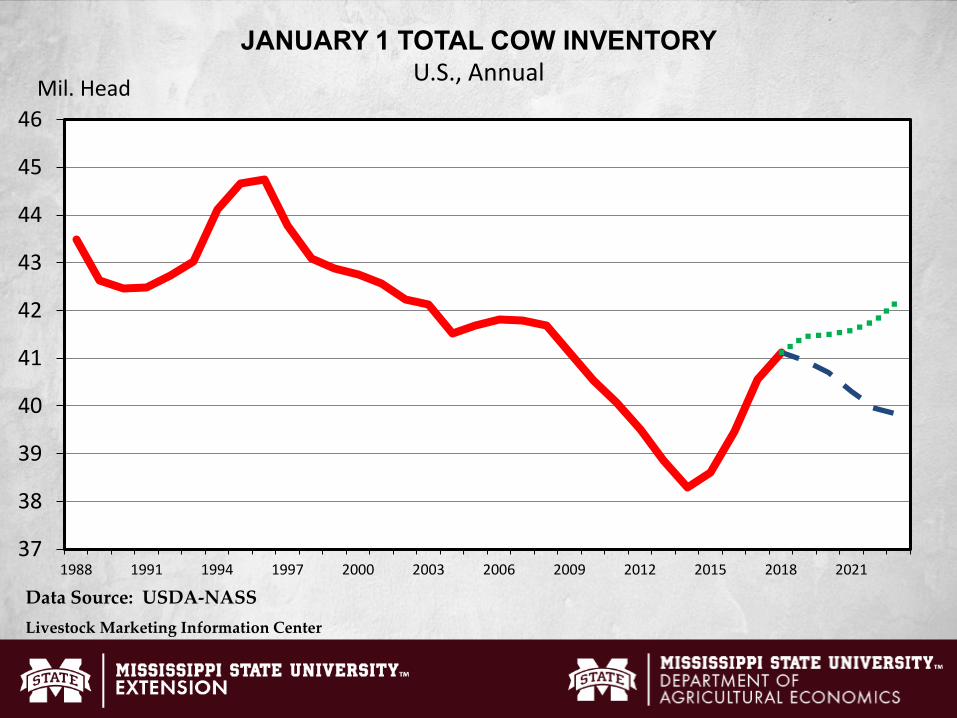

JANUARY 1 TOTAL COW INVENTORYU.S., Annual

Data Source: USDA-NASSLivestock Marketing Information Center

33

34

35

36

37

38

39

40

41

1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

Mil. Head

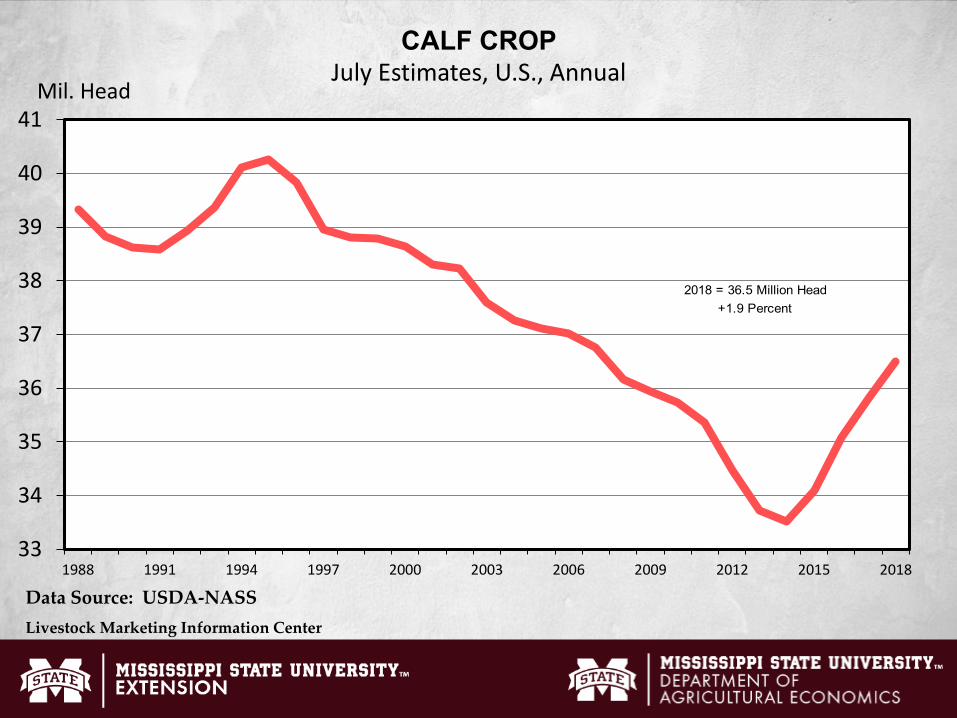

CALF CROPJuly Estimates, U.S., Annual

Data Source: USDA-NASSLivestock Marketing Information Center

+1.9 Percent2018 = 36.5 Million Head

9.7

10.0

10.3

10.6

10.9

11.2

11.5

11.8

12.1

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Mil. Head

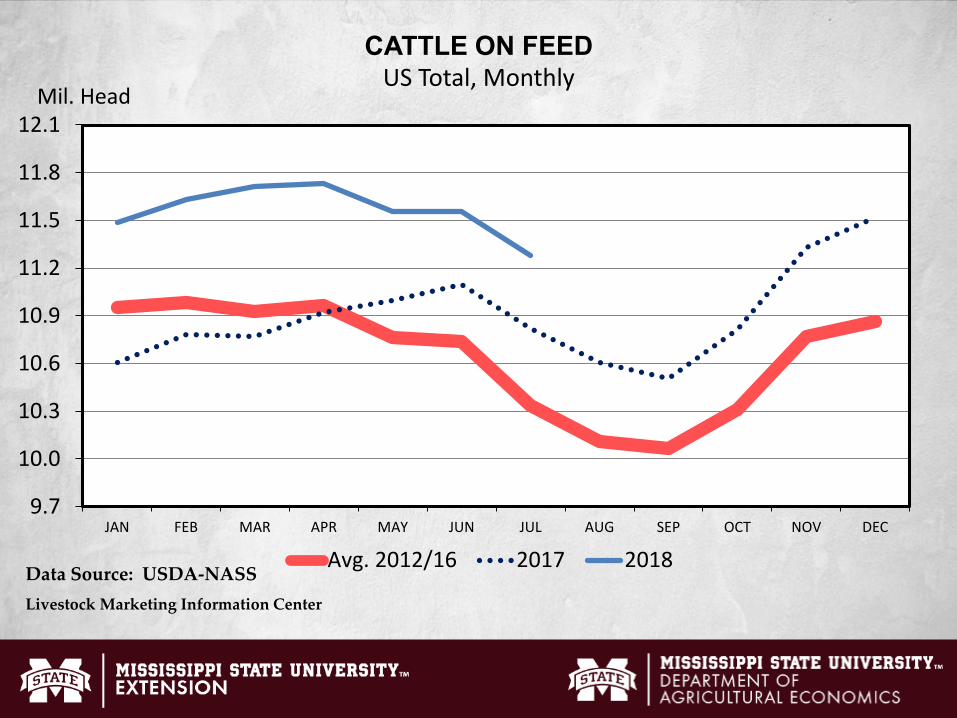

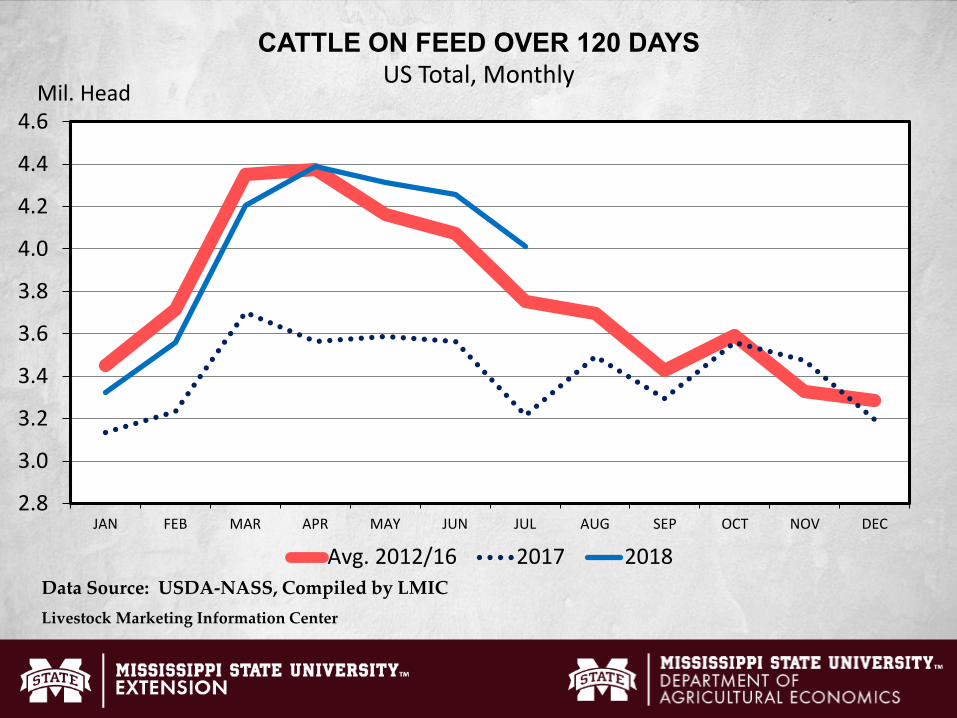

CATTLE ON FEEDUS Total, Monthly

Avg. 2012/16 2017 2018Data Source: USDA-NASSLivestock Marketing Information Center

2.8

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Mil. Head

CATTLE ON FEED OVER 120 DAYSUS Total, Monthly

Avg. 2012/16 2017 2018Data Source: USDA-NASS, Compiled by LMICLivestock Marketing Information Center

820

830

840

850

860

870

880

890

900

910

920

JAN APR JUL OCT

Pounds

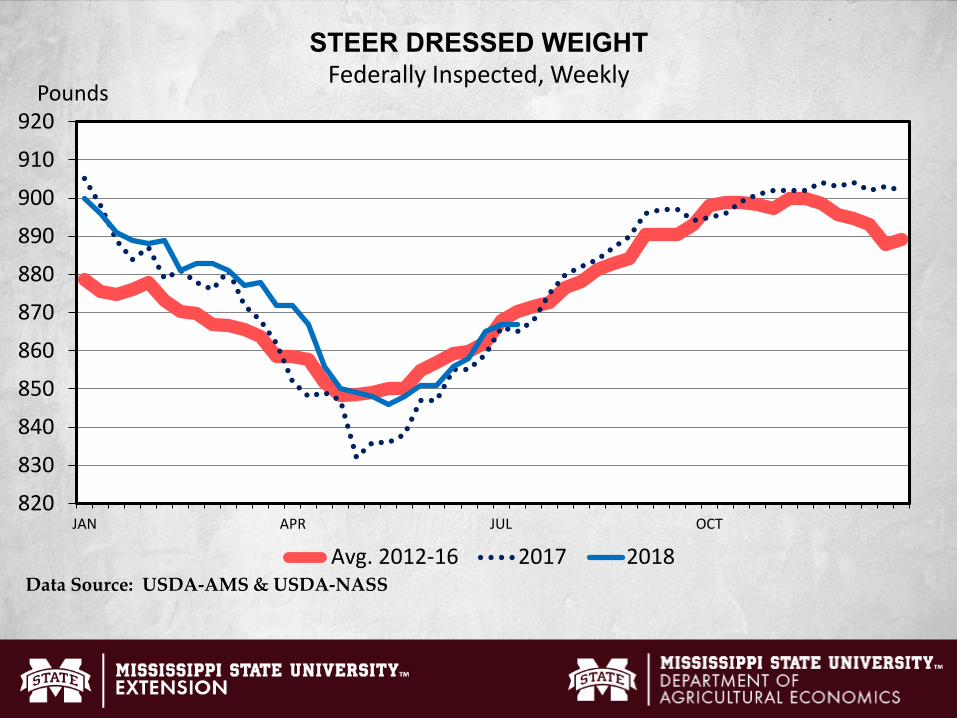

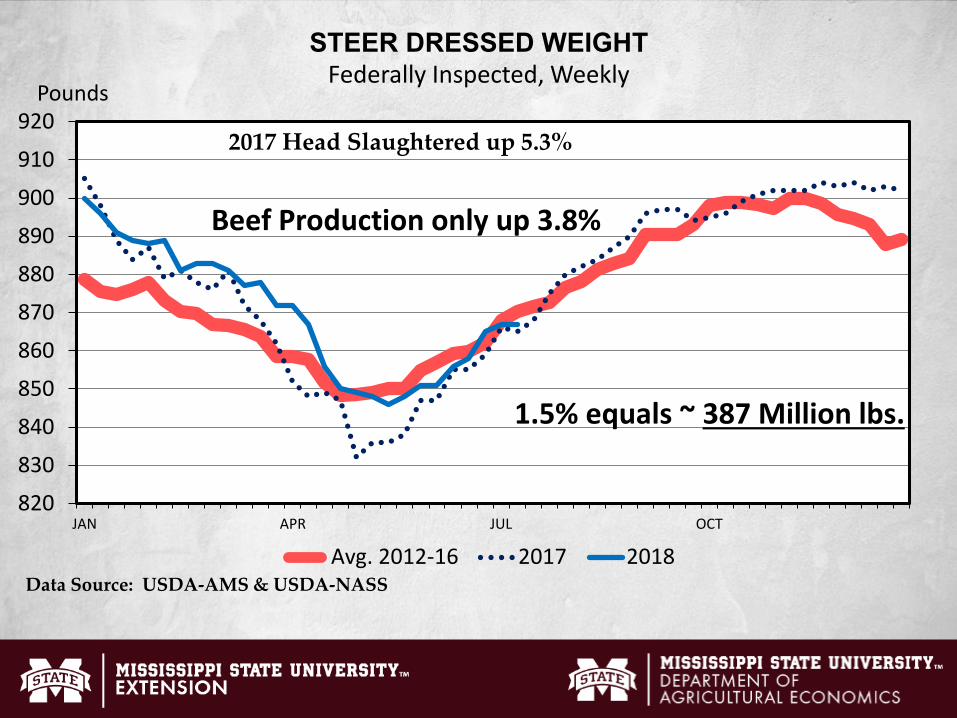

STEER DRESSED WEIGHTFederally Inspected, Weekly

Avg. 2012-16 2017 2018Data Source: USDA-AMS & USDA-NASS

820

830

840

850

860

870

880

890

900

910

920

JAN APR JUL OCT

Pounds

STEER DRESSED WEIGHTFederally Inspected, Weekly

Avg. 2012-16 2017 2018

1.5% equals ~ 387 Million lbs.

Data Source: USDA-AMS & USDA-NASS

2017 Head Slaughtered up 5.3%

Beef Production only up 3.8%

10

15

20

25

30

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Bil. Pounds

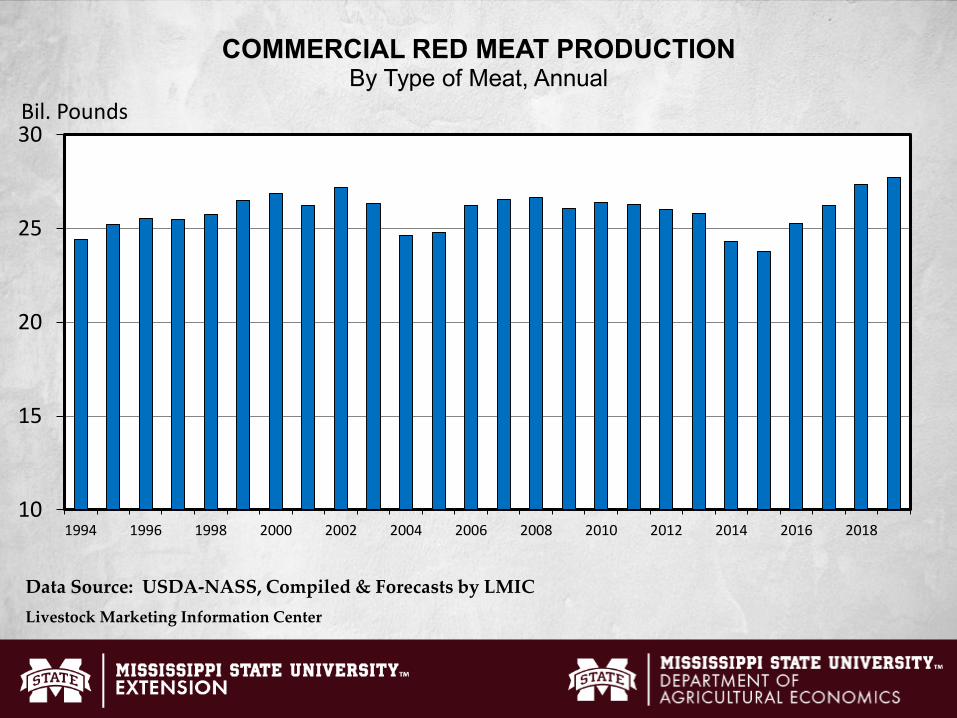

COMMERCIAL RED MEAT PRODUCTIONBy Type of Meat, Annual

Data Source: USDA-NASS, Compiled & Forecasts by LMICLivestock Marketing Information Center

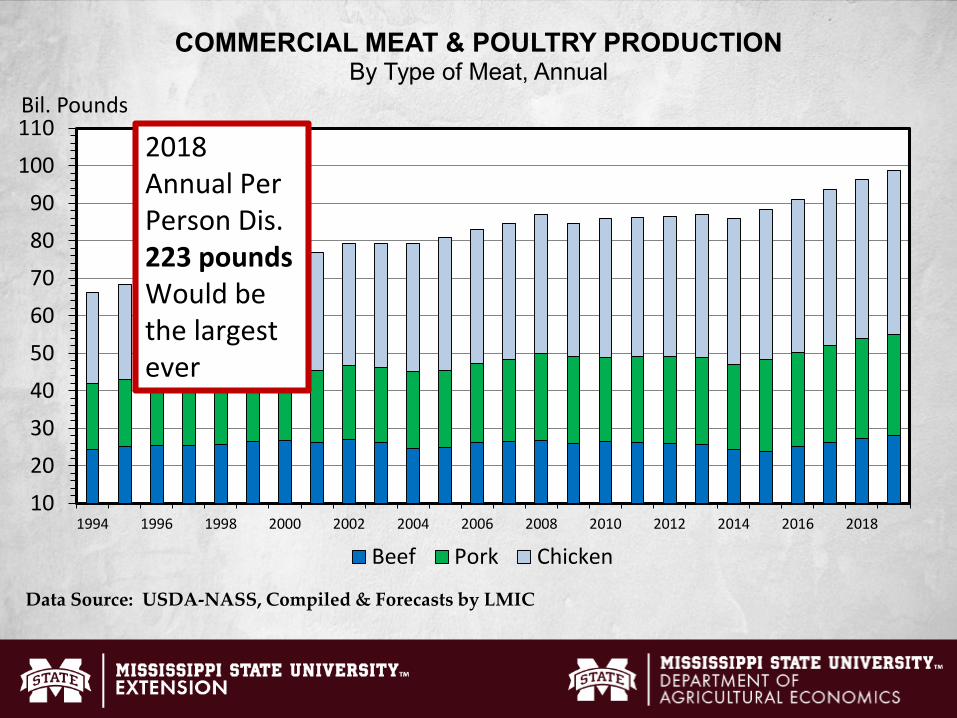

102030405060708090

100110

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Bil. Pounds

COMMERCIAL MEAT & POULTRY PRODUCTIONBy Type of Meat, Annual

Beef Pork Chicken

2018 Annual Per Person Dis. 223 poundsWould be the largest ever

Data Source: USDA-NASS, Compiled & Forecasts by LMIC

The Cattle Cycle

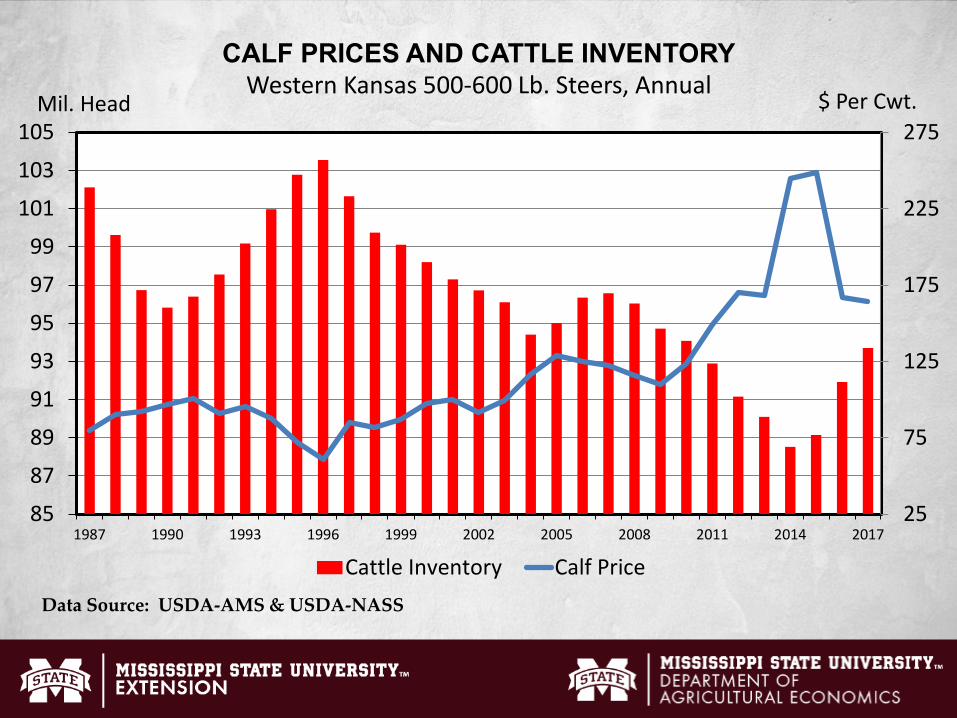

25

75

125

175

225

275

85

87

89

91

93

95

97

99

101

103

105

1987 1990 1993 1996 1999 2002 2005 2008 2011 2014 2017

$ Per Cwt.Mil. Head

CALF PRICES AND CATTLE INVENTORYWestern Kansas 500-600 Lb. Steers, Annual

Cattle Inventory Calf PriceData Source: USDA-AMS & USDA-NASS

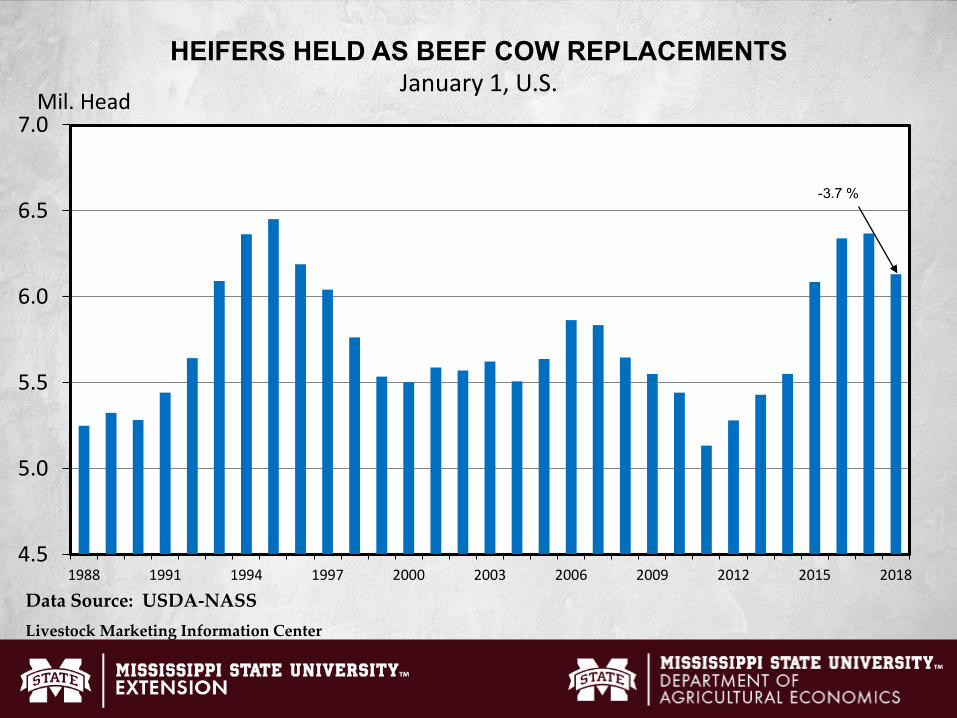

4.5

5.0

5.5

6.0

6.5

7.0

1988 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018

Mil. Head

HEIFERS HELD AS BEEF COW REPLACEMENTSJanuary 1, U.S.

-3.7 %

Data Source: USDA-NASSLivestock Marketing Information Center

60

70

80

90

100

110

120

130

140

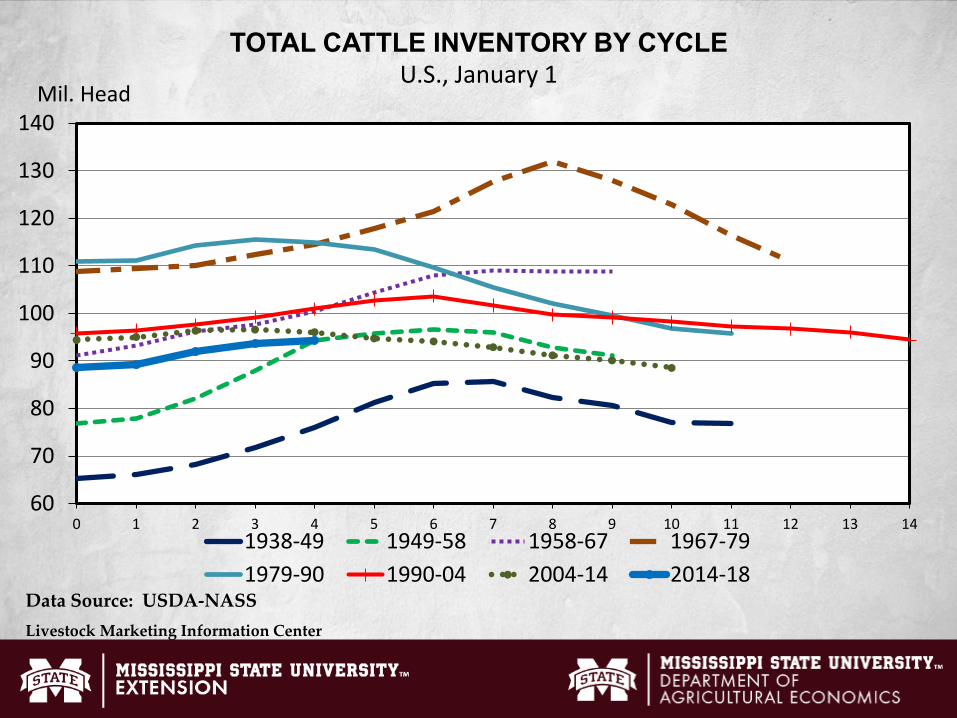

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14

Mil. Head

TOTAL CATTLE INVENTORY BY CYCLEU.S., January 1

1938-49 1949-58 1958-67 1967-791979-90 1990-04 2004-14 2014-18

Data Source: USDA-NASSLivestock Marketing Information Center

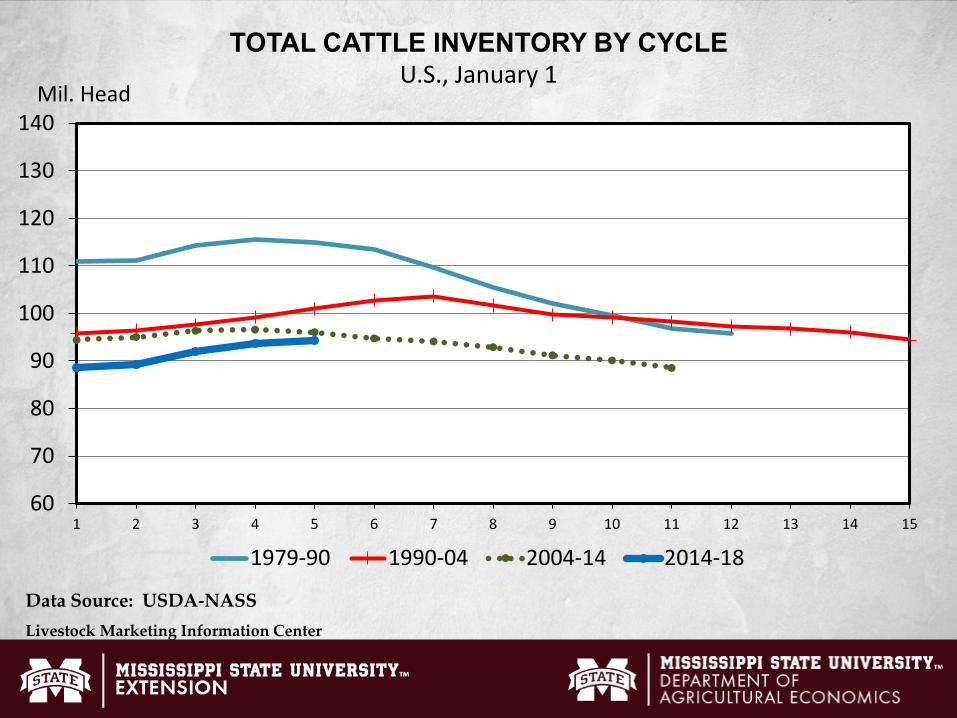

60

70

80

90

100

110

120

130

140

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Mil. Head

TOTAL CATTLE INVENTORY BY CYCLEU.S., January 1

1979-90 1990-04 2004-14 2014-18

Data Source: USDA-NASSLivestock Marketing Information Center

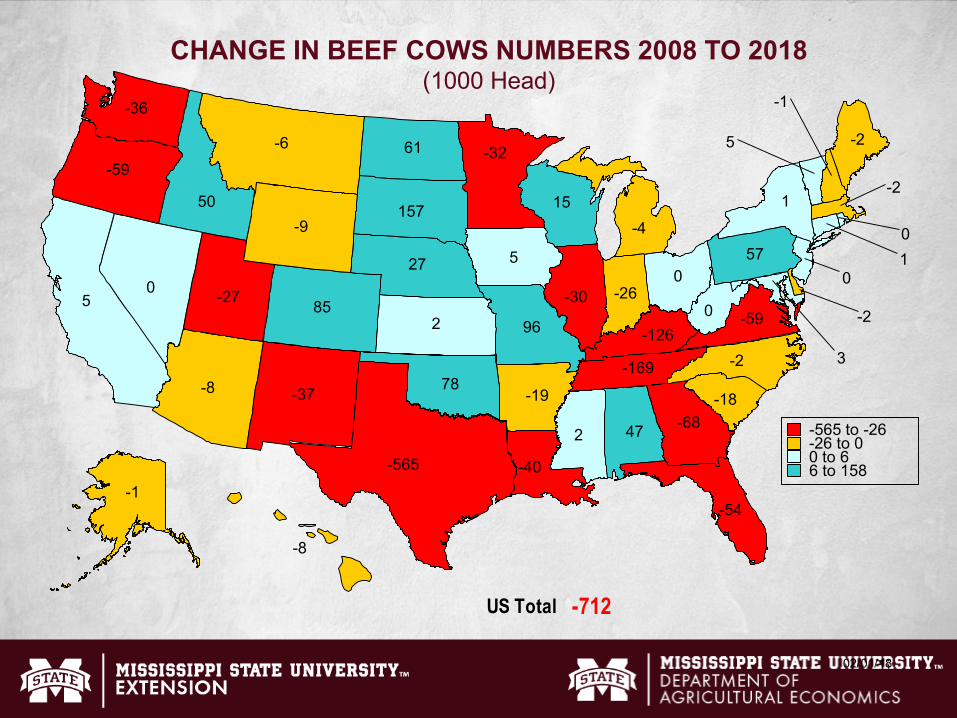

CHANGE IN BEEF COWS NUMBERS 2008 TO 2018(1000 Head)

US Total -712

02/01/18

-565

-169

-126

-68

-59

-59

-54

-40

-37

-36

-32

-30-27 -26

-19 -18

-9

-8

-8

-6

-4

-2

-2

-2

-2

-1

-1

000

0

01

1

2

2

3

5

5

5

15

27

47

50

57

61

78

8596

157

-565 to -26-26 to 00 to 66 to 158

The Supply Story• Long-term

• We expanded during 2017 – slower pace• I expect 2018 to be very close to flat <1% • The stage is already set for larger calf crops in 2018 and probably 2019

•2020 is looking like the inventory peak• The supply market pressure is currently

negative, but signs of a slowdown

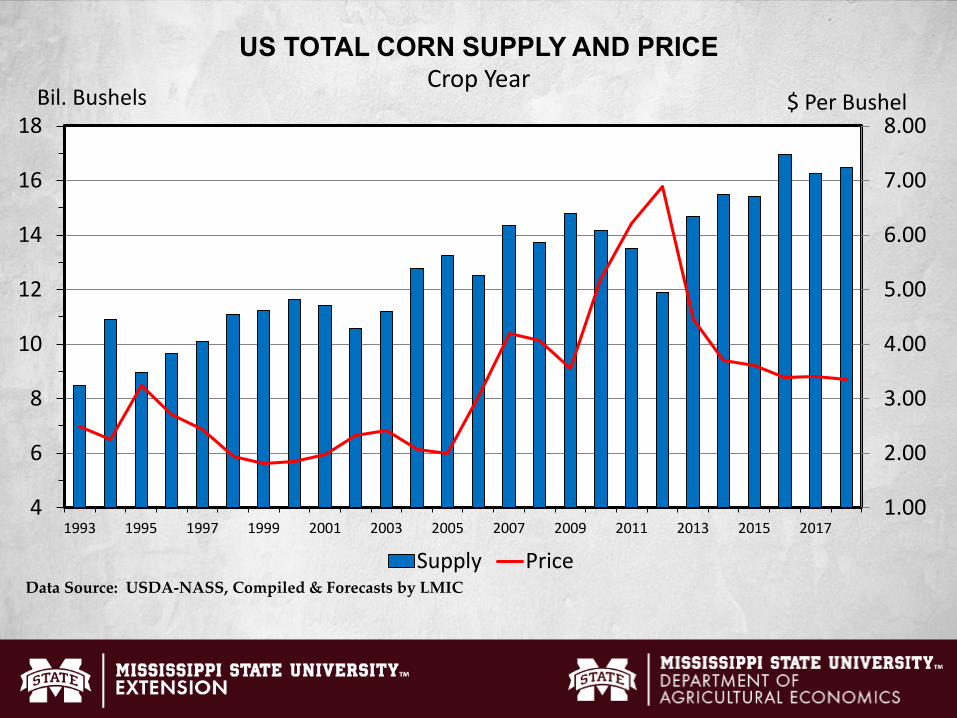

Feedstuffs

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

4

6

8

10

12

14

16

18

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

$ Per BushelBil. Bushels

US TOTAL CORN SUPPLY AND PRICECrop Year

Supply PriceData Source: USDA-NASS, Compiled & Forecasts by LMIC

DemandPart 1: Domestic

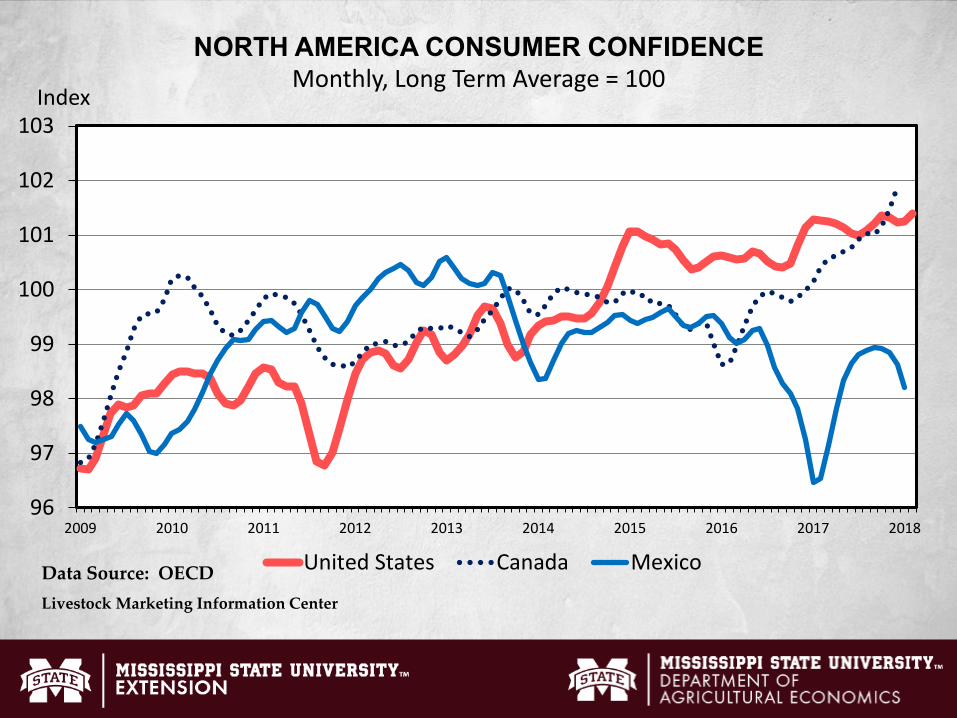

96

97

98

99

100

101

102

103

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Index

NORTH AMERICA CONSUMER CONFIDENCE Monthly, Long Term Average = 100

United States Canada MexicoData Source: OECDLivestock Marketing Information Center

50

55

60

65

70

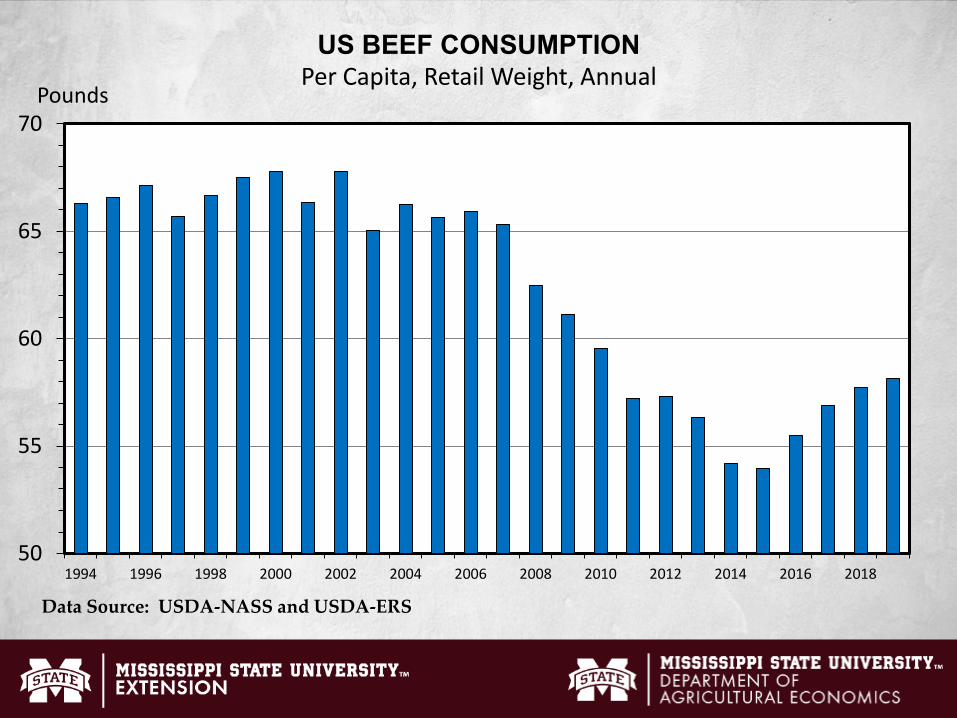

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Pounds

US BEEF CONSUMPTIONPer Capita, Retail Weight, Annual

Data Source: USDA-NASS and USDA-ERS

200

250

300

350

400

450

500

550

600

650

700

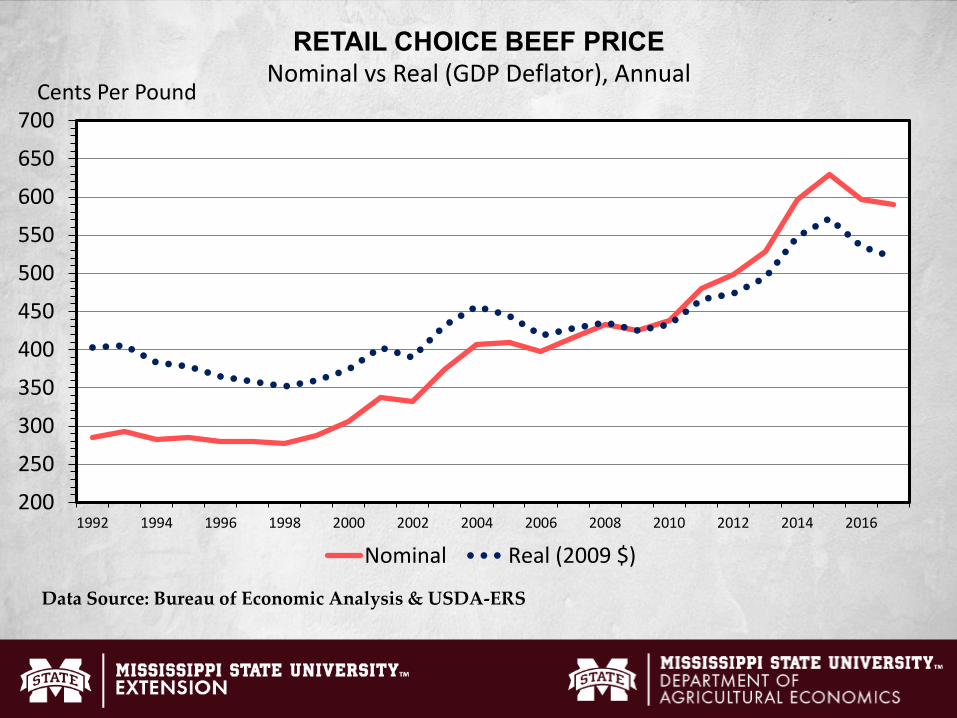

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Cents Per Pound

RETAIL CHOICE BEEF PRICENominal vs Real (GDP Deflator), Annual

Nominal Real (2009 $)

Data Source: Bureau of Economic Analysis & USDA-ERS

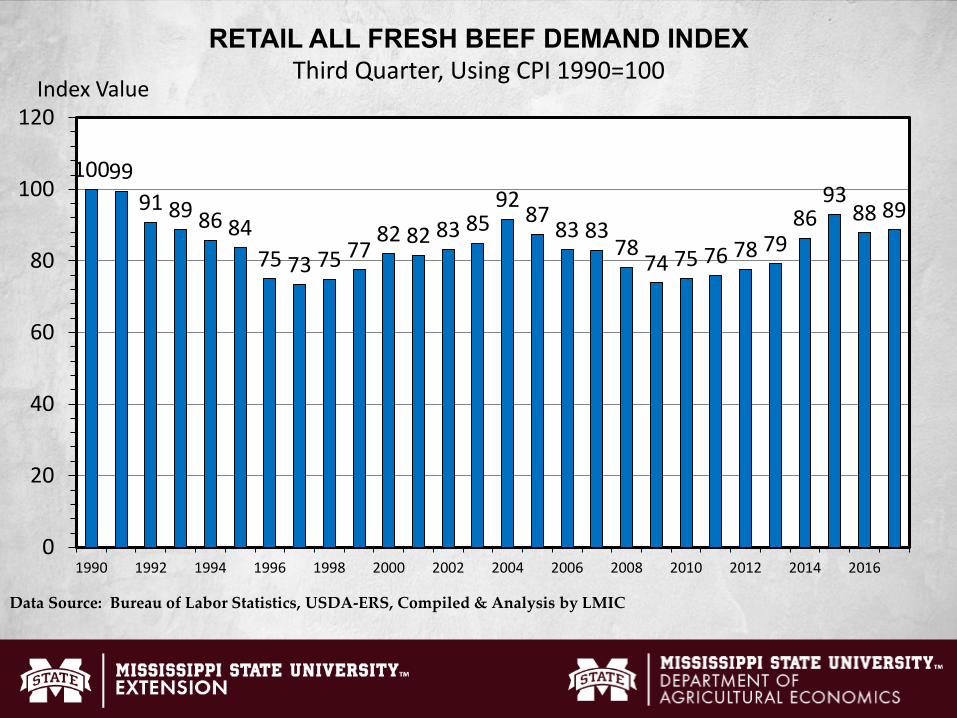

1009991 89 86 84

75 73 75 7782 82 83 85

92 8783 83

7874 75 76 78 79

8693

88 89

0

20

40

60

80

100

120

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Index Value

RETAIL ALL FRESH BEEF DEMAND INDEXThird Quarter, Using CPI 1990=100

Data Source: Bureau of Labor Statistics, USDA-ERS, Compiled & Analysis by LMIC

Changing Retail Landscape• Domestic beef demand is strong• How/where will consumers buy their beef

in the future?• Increased online sales of other products• Meat brings consumers in the door &

retailers are using beef to attract customers

DemandPart 2: International Trade

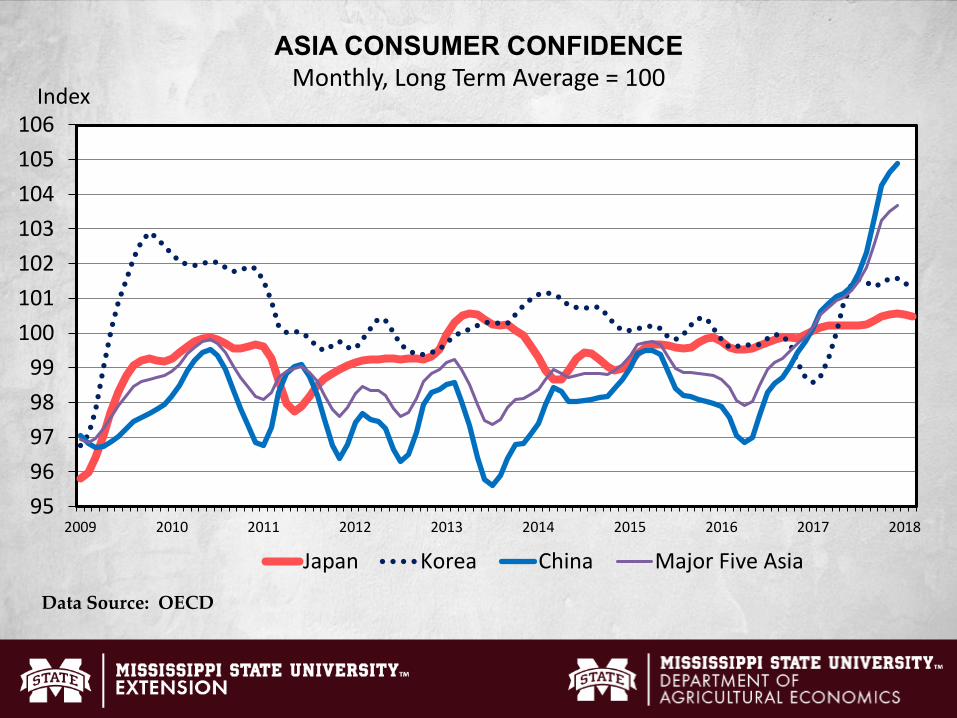

9596979899

100101102103104105106

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Index

ASIA CONSUMER CONFIDENCE Monthly, Long Term Average = 100

Japan Korea China Major Five Asia

Data Source: OECD

150

170

190

210

230

250

270

290

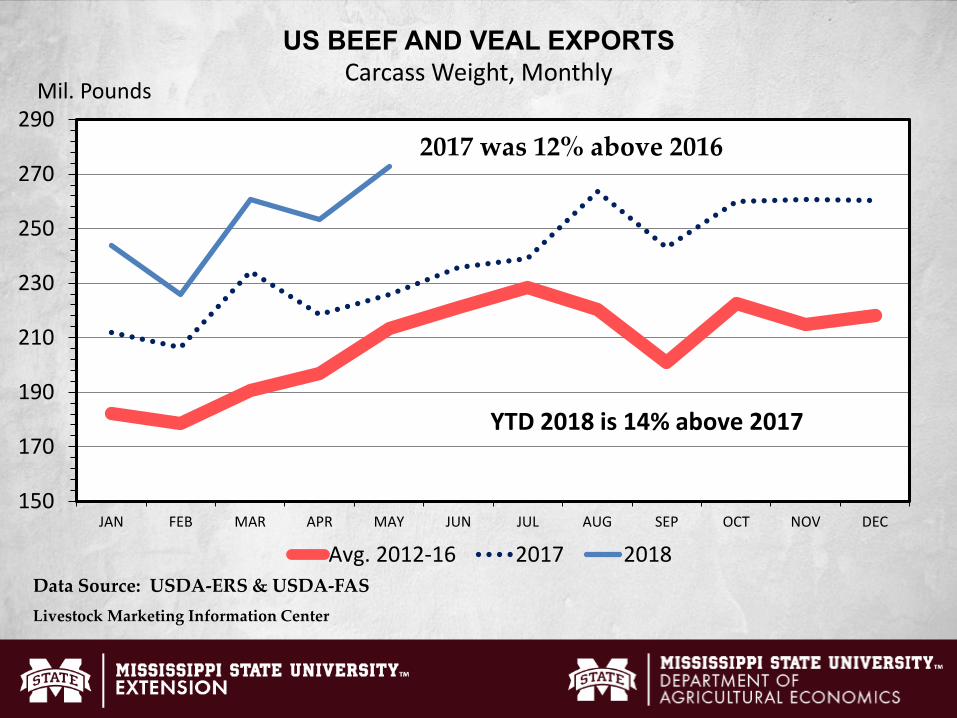

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Mil. Pounds

US BEEF AND VEAL EXPORTSCarcass Weight, Monthly

Avg. 2012-16 2017 2018

YTD 2018 is 14% above 2017

Data Source: USDA-ERS & USDA-FASLivestock Marketing Information Center

2017 was 12% above 2016

I-N-0602/07/18

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

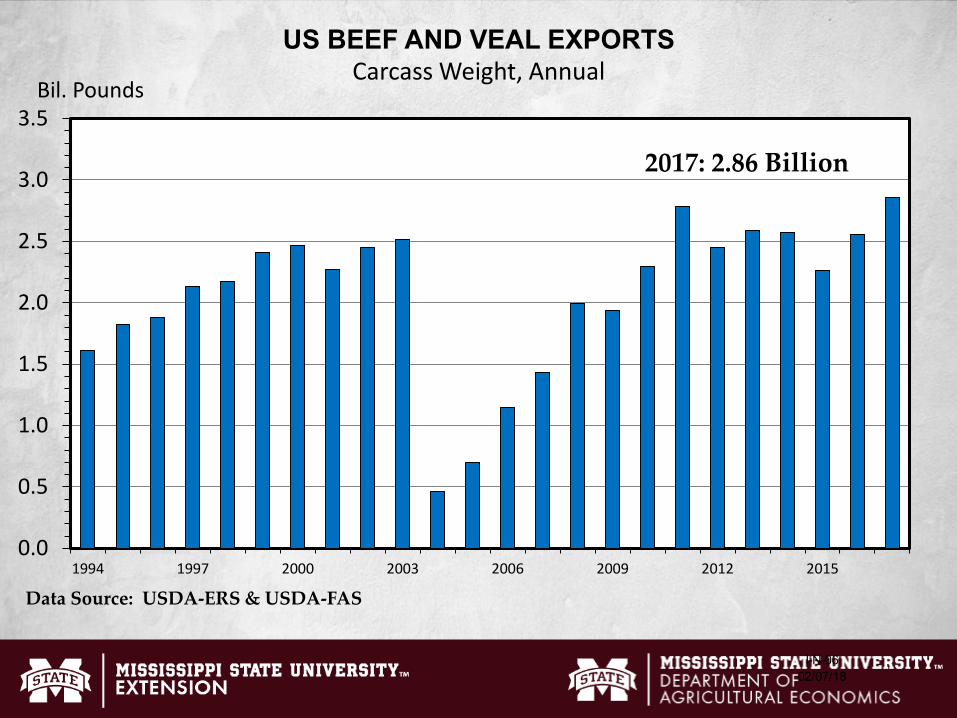

1994 1997 2000 2003 2006 2009 2012 2015

Bil. Pounds

US BEEF AND VEAL EXPORTSCarcass Weight, Annual

Data Source: USDA-ERS & USDA-FAS

2017: 2.86 Billion

I-N-1802/07/18

0

100

200

300

400

500

600

700

800

900

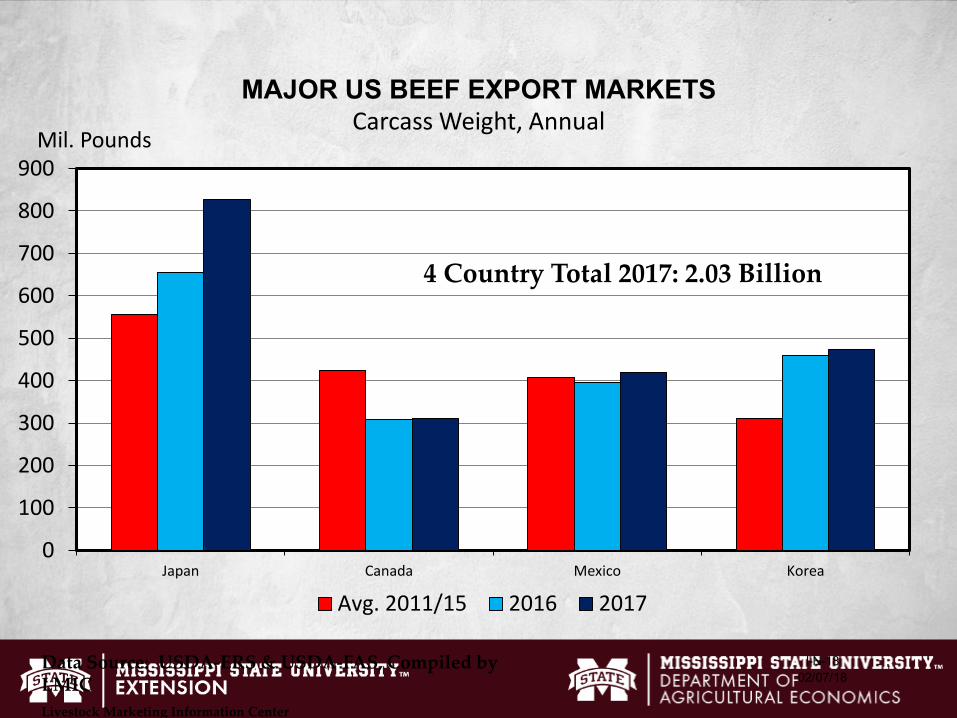

Japan Canada Mexico Korea

Mil. Pounds

MAJOR US BEEF EXPORT MARKETSCarcass Weight, Annual

Avg. 2011/15 2016 2017

Data Source: USDA-ERS & USDA-FAS, Compiled by LMICLivestock Marketing Information Center

4 Country Total 2017: 2.03 Billion

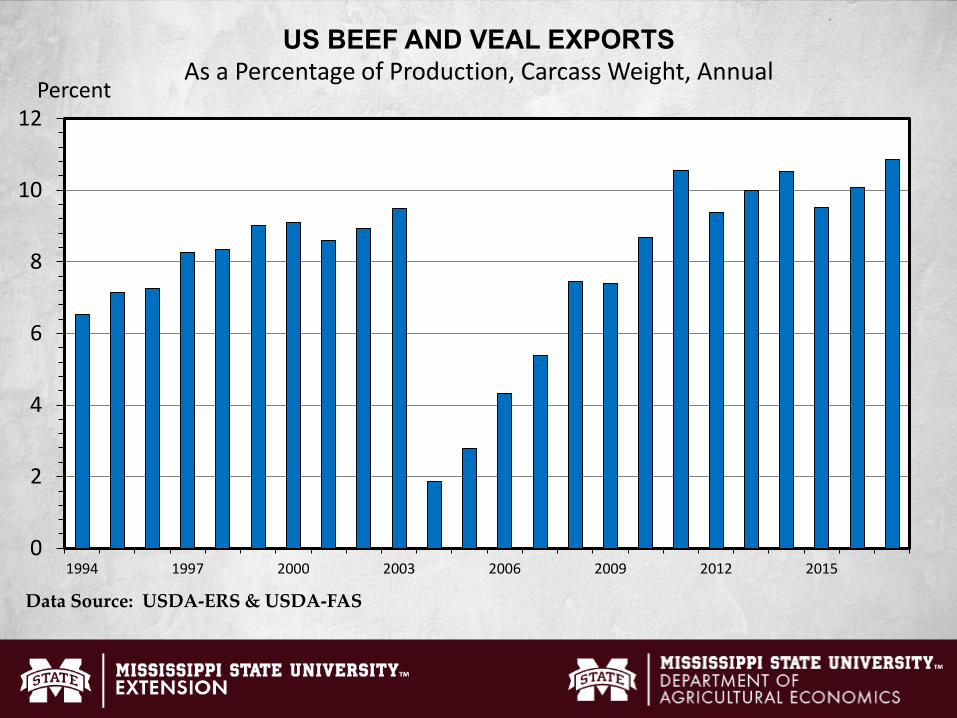

0

2

4

6

8

10

12

1994 1997 2000 2003 2006 2009 2012 2015

Percent

US BEEF AND VEAL EXPORTSAs a Percentage of Production, Carcass Weight, Annual

Data Source: USDA-ERS & USDA-FAS

The Demand Story• Strong International Demand is

supporting U.S. cattle prices in 2018• Can the sharp increases continue?• Forecasts this time last year were for 3%

growth – we hit 12%• Plenty of outside uncertainty• The demand-side pressure is positive on

prices

Forecasts

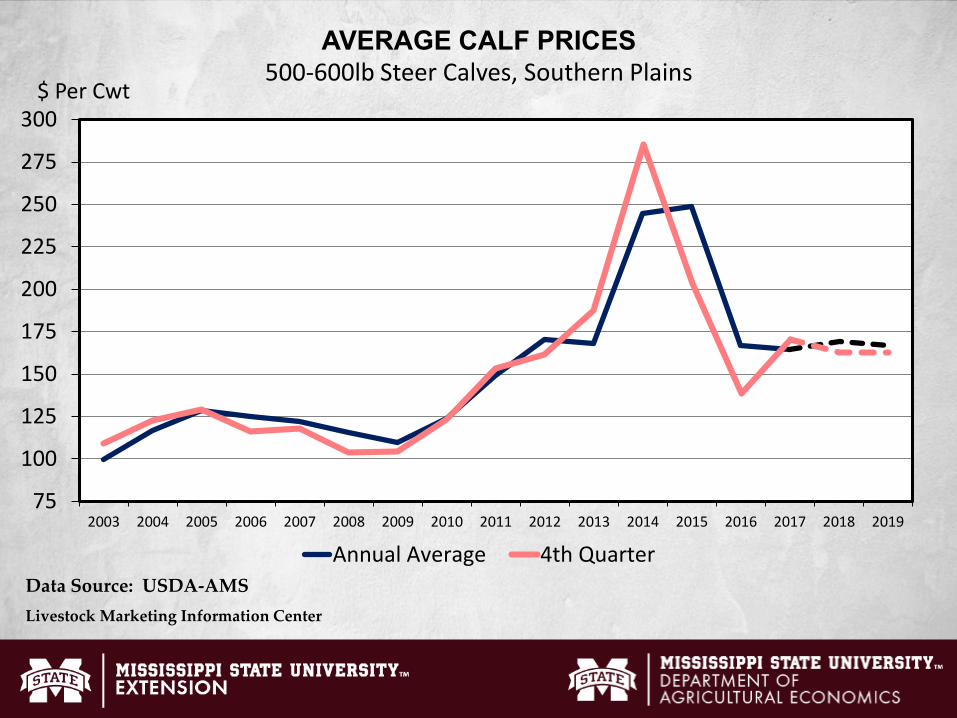

75

100

125

150

175

200

225

250

275

300

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

$ Per Cwt

AVERAGE CALF PRICES500-600lb Steer Calves, Southern Plains

Annual Average 4th QuarterData Source: USDA-AMSLivestock Marketing Information Center

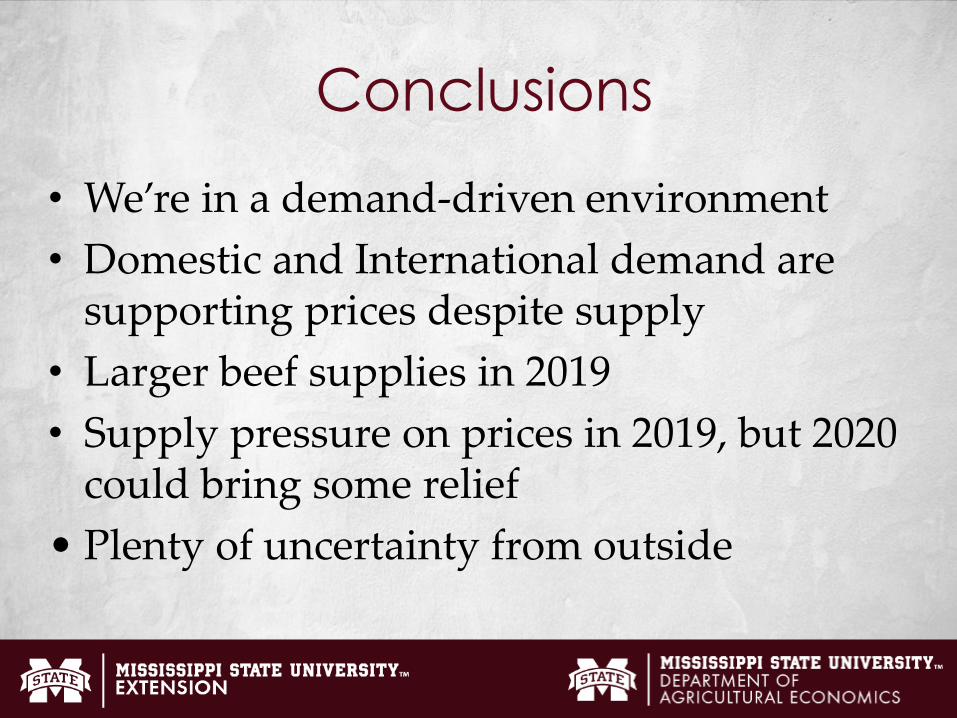

Conclusions

• We’re in a demand-driven environment • Domestic and International demand are

supporting prices despite supply• Larger beef supplies in 2019• Supply pressure on prices in 2019, but 2020

could bring some relief• Plenty of uncertainty from outside