Embed Size (px)

Citation preview

AYCHT 27/7/2019

1

2019 reviewSuccession & Probate

Au‐Yeung Cheng Ho Tin solicitors – CPD

28 July 2019

Tak Wong

1

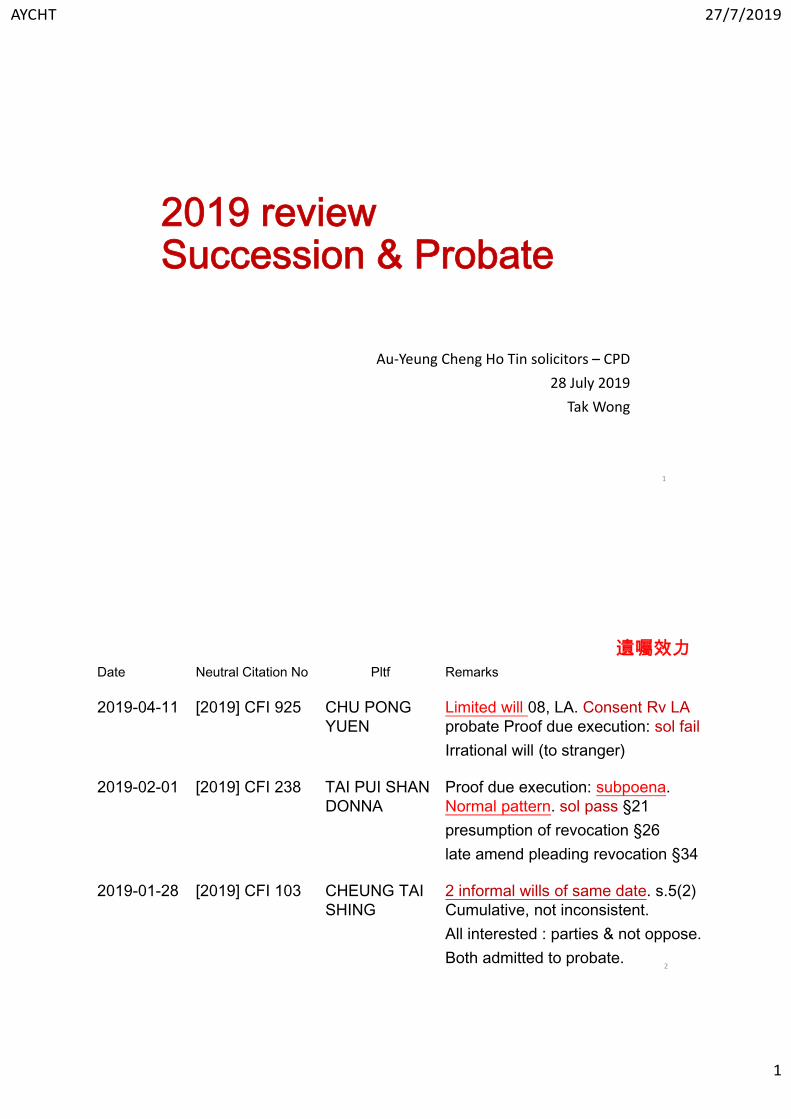

遺囑效力

2

Date Neutral Citation No Pltf Remarks

2019-04-11 [2019] CFI 925 CHU PONG YUEN

Limited will 08, LA. Consent Rv LA probate Proof due execution: sol failIrrational will (to stranger)

2019-02-01 [2019] CFI 238 TAI PUI SHAN DONNA

Proof due execution: subpoena. Normal pattern. sol pass §21 presumption of revocation §26late amend pleading revocation §34

2019-01-28 [2019] CFI 103 CHEUNG TAI SHING

2 informal wills of same date. s.5(2) Cumulative, not inconsistent.All interested : parties & not oppose.Both admitted to probate.

AYCHT 27/7/2019

2

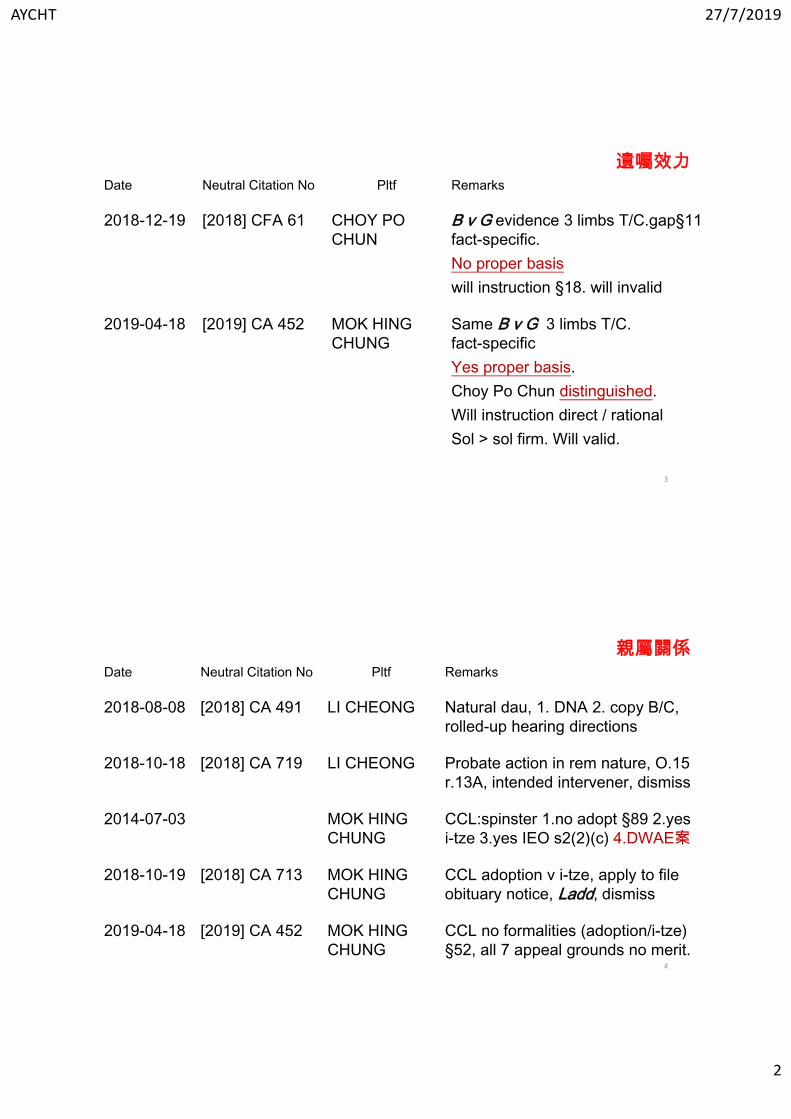

遺囑效力

3

Date Neutral Citation No Pltf Remarks

2018-12-19 [2018] CFA 61 CHOY PO CHUN

B v G evidence 3 limbs T/C.gap§11 fact-specific. No proper basis will instruction §18. will invalid

2019-04-18 [2019] CA 452 MOK HING CHUNG

Same B v G 3 limbs T/C. fact-specificYes proper basis. Choy Po Chun distinguished. Will instruction direct / rationalSol > sol firm. Will valid.

親屬關係

4

Date Neutral Citation No Pltf Remarks

2018-08-08 [2018] CA 491 LI CHEONG Natural dau, 1. DNA 2. copy B/C, rolled-up hearing directions

2018-10-18 [2018] CA 719 LI CHEONG Probate action in rem nature, O.15 r.13A, intended intervener, dismiss

2014-07-03 MOK HING CHUNG

CCL:spinster 1.no adopt §89 2.yes i-tze 3.yes IEO s2(2)(c) 4.DWAE案

2018-10-19 [2018] CA 713 MOK HING CHUNG

CCL adoption v i-tze, apply to file obituary notice, Ladd, dismiss

2019-04-18 [2019] CA 452 MOK HING CHUNG

CCL no formalities (adoption/i-tze)§52, all 7 appeal grounds no merit.

AYCHT 27/7/2019

3

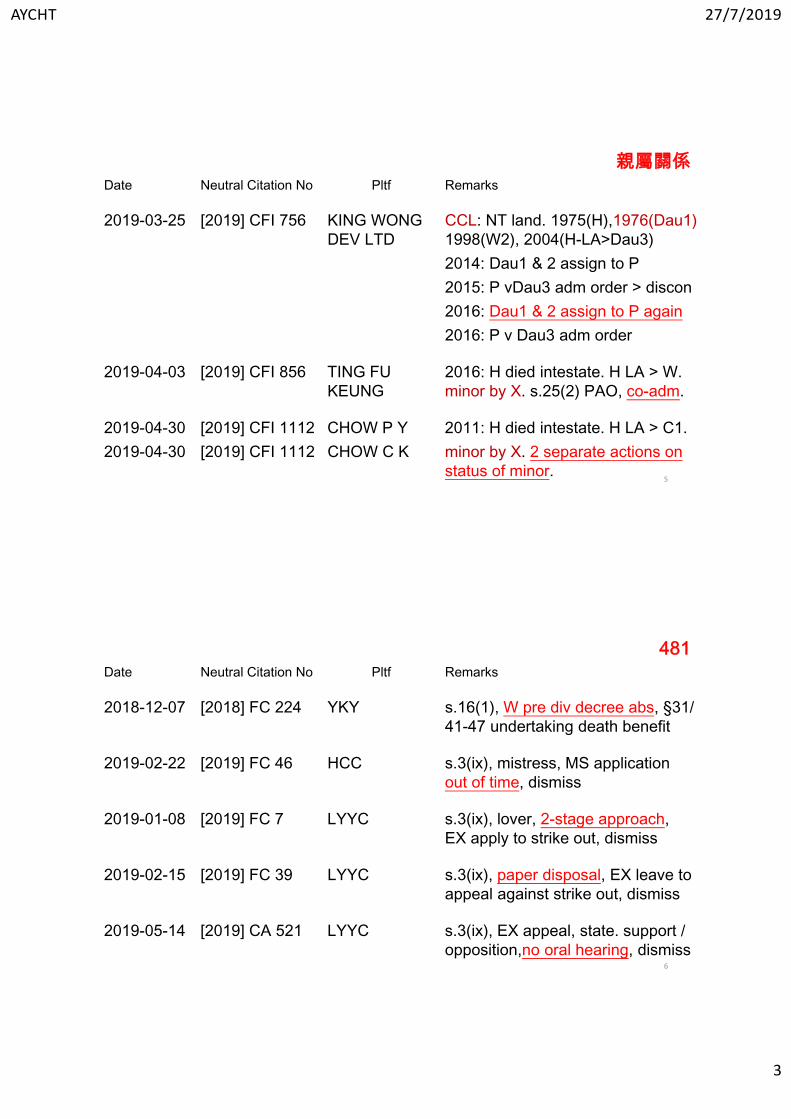

親屬關係

5

Date Neutral Citation No Pltf Remarks

2019-03-25 [2019] CFI 756 KING WONG DEV LTD

CCL: NT land. 1975(H),1976(Dau1) 1998(W2), 2004(H-LA>Dau3)2014: Dau1 & 2 assign to P2015: P vDau3 adm order > discon2016: Dau1 & 2 assign to P again2016: P v Dau3 adm order

2019-04-03 [2019] CFI 856 TING FU KEUNG

2016: H died intestate. H LA > W. minor by X. s.25(2) PAO, co-adm.

2019-04-30 [2019] CFI 1112 CHOW P Y 2011: H died intestate. H LA > C1.2019-04-30 [2019] CFI 1112 CHOW C K minor by X. 2 separate actions on

status of minor.

481

6

Date Neutral Citation No Pltf Remarks

2018-12-07 [2018] FC 224 YKY s.16(1), W pre div decree abs, §31/ 41-47 undertaking death benefit

2019-02-22 [2019] FC 46 HCC s.3(ix), mistress, MS application out of time, dismiss

2019-01-08 [2019] FC 7 LYYC s.3(ix), lover, 2-stage approach,EX apply to strike out, dismiss

2019-02-15 [2019] FC 39 LYYC s.3(ix), paper disposal, EX leave to appeal against strike out, dismiss

2019-05-14 [2019] CA 521 LYYC s.3(ix), EX appeal, state. support / opposition,no oral hearing, dismiss

AYCHT 27/7/2019

4

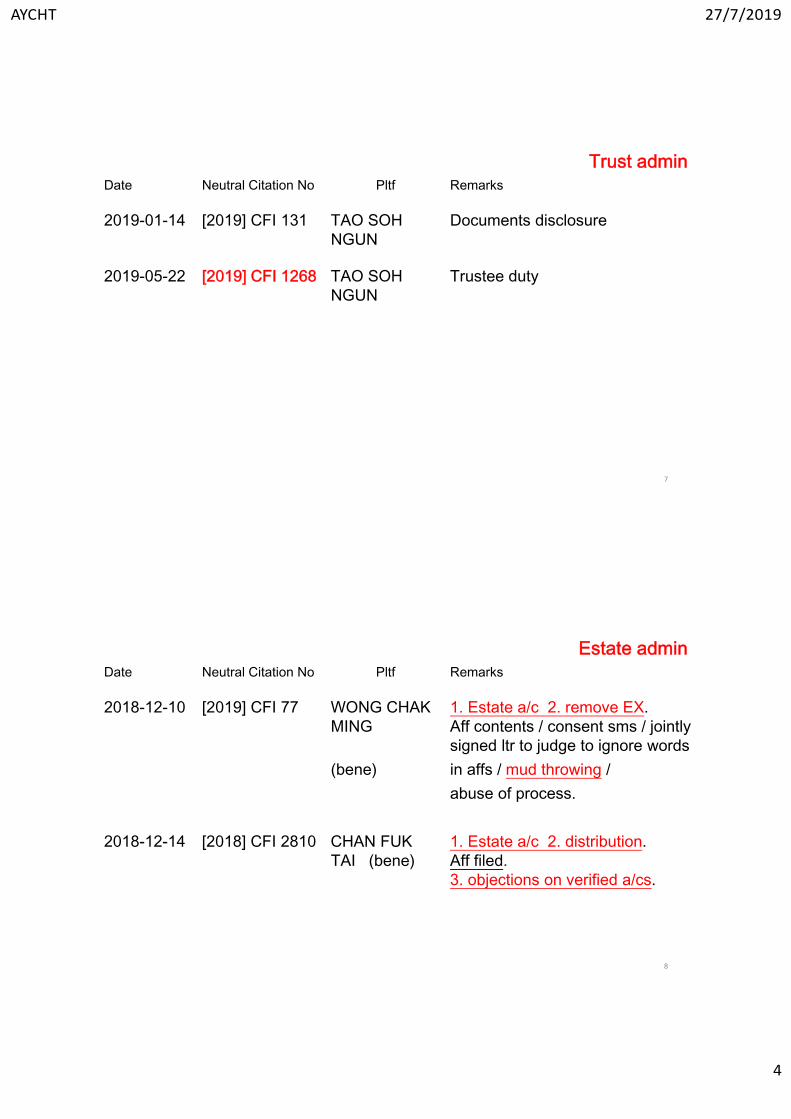

Trust admin

7

Date Neutral Citation No Pltf Remarks

2019-01-14 [2019] CFI 131 TAO SOH NGUN

Documents disclosure

2019-05-22 [2019] CFI 1268 TAO SOH NGUN

Trustee duty

Estate admin

8

Date Neutral Citation No Pltf Remarks

2018-12-10 [2019] CFI 77 WONG CHAK MING

1. Estate a/c 2. remove EX. Aff contents / consent sms / jointly signed ltr to judge to ignore words

(bene) in affs / mud throwing /abuse of process.

2018-12-14 [2018] CFI 2810 CHAN FUK TAI (bene)

1. Estate a/c 2. distribution. Aff filed. 3. objections on verified a/cs.

AYCHT 27/7/2019

5

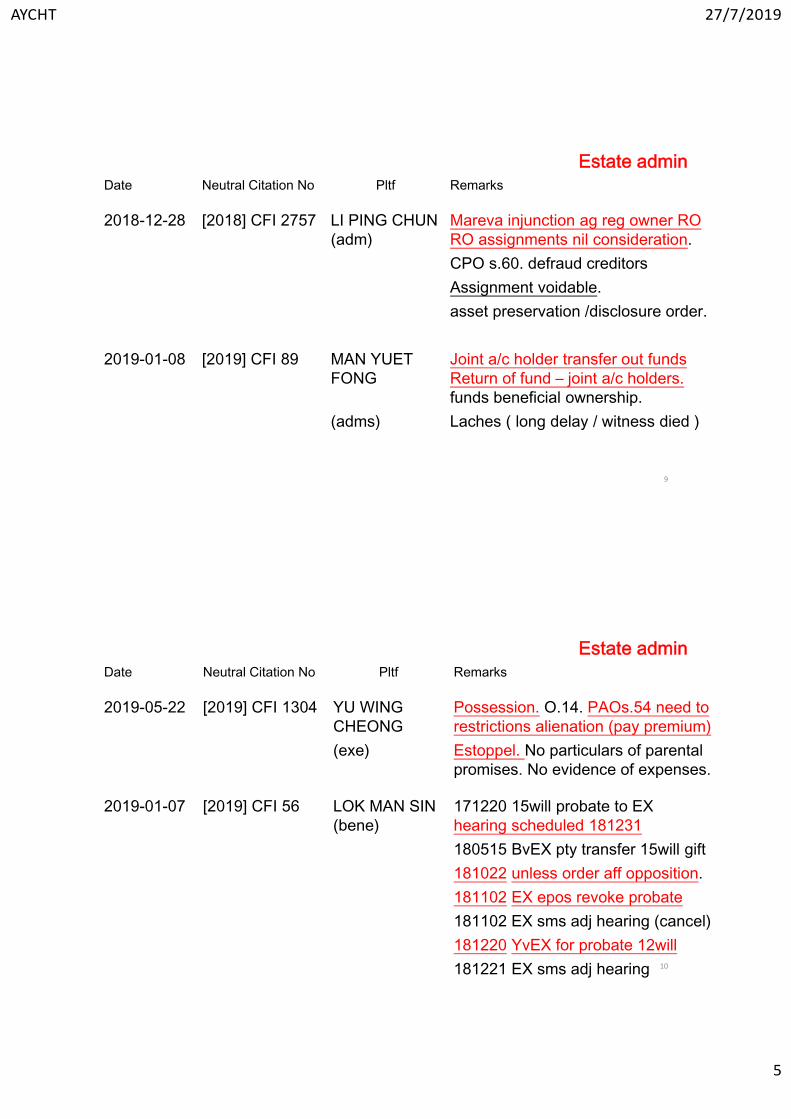

Estate admin

9

Date Neutral Citation No Pltf Remarks

2018-12-28 [2018] CFI 2757 LI PING CHUN (adm)

Mareva injunction ag reg owner RO RO assignments nil consideration. CPO s.60. defraud creditorsAssignment voidable. asset preservation /disclosure order.

2019-01-08 [2019] CFI 89 MAN YUET FONG

Joint a/c holder transfer out funds Return of fund – joint a/c holders. funds beneficial ownership.

(adms) Laches ( long delay / witness died )

Estate admin

10

Date Neutral Citation No Pltf Remarks

2019-05-22 [2019] CFI 1304 YU WING CHEONG

Possession. O.14. PAOs.54 need to restrictions alienation (pay premium)

(exe) Estoppel. No particulars of parental promises. No evidence of expenses.

2019-01-07 [2019] CFI 56 LOK MAN SIN (bene)

171220 15will probate to EX hearing scheduled 181231180515 BvEX pty transfer 15will gift181022 unless order aff opposition.181102 EX epos revoke probate181102 EX sms adj hearing (cancel)181220 YvEX for probate 12will 181221 EX sms adj hearing

AYCHT 27/7/2019

6

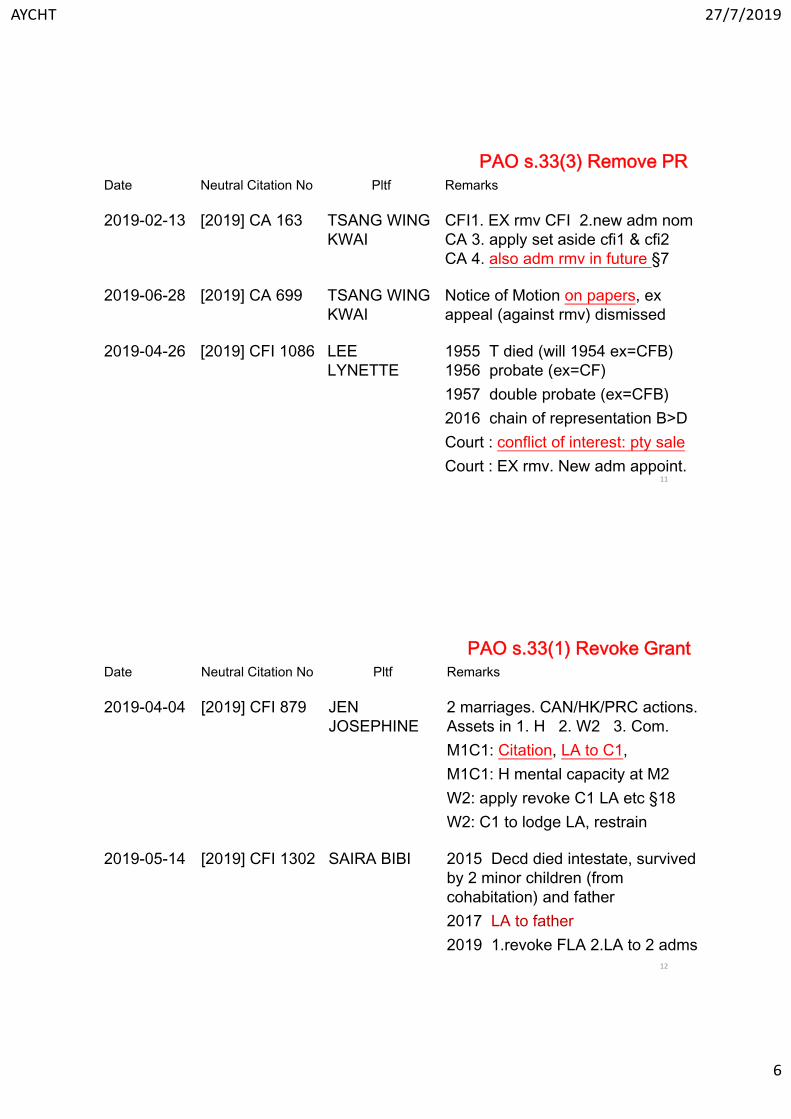

PAO s.33(3) Remove PR

11

Date Neutral Citation No Pltf Remarks

2019-02-13 [2019] CA 163 TSANG WING KWAI

CFI1. EX rmv CFI 2.new adm nom CA 3. apply set aside cfi1 & cfi2 CA 4. also adm rmv in future §7

2019-06-28 [2019] CA 699 TSANG WING KWAI

Notice of Motion on papers, exappeal (against rmv) dismissed

2019-04-26 [2019] CFI 1086 LEE LYNETTE

1955 T died (will 1954 ex=CFB)1956 probate (ex=CF) 1957 double probate (ex=CFB)2016 chain of representation B>D Court : conflict of interest: pty saleCourt : EX rmv. New adm appoint.

PAO s.33(1) Revoke Grant

12

Date Neutral Citation No Pltf Remarks

2019-04-04 [2019] CFI 879 JEN JOSEPHINE

2 marriages. CAN/HK/PRC actions. Assets in 1. H 2. W2 3. Com. M1C1: Citation, LA to C1, M1C1: H mental capacity at M2W2: apply revoke C1 LA etc §18W2: C1 to lodge LA, restrain

2019-05-14 [2019] CFI 1302 SAIRA BIBI 2015 Decd died intestate, survived by 2 minor children (from cohabitation) and father 2017 LA to father 2019 1.revoke FLA 2.LA to 2 adms

AYCHT 27/7/2019

7

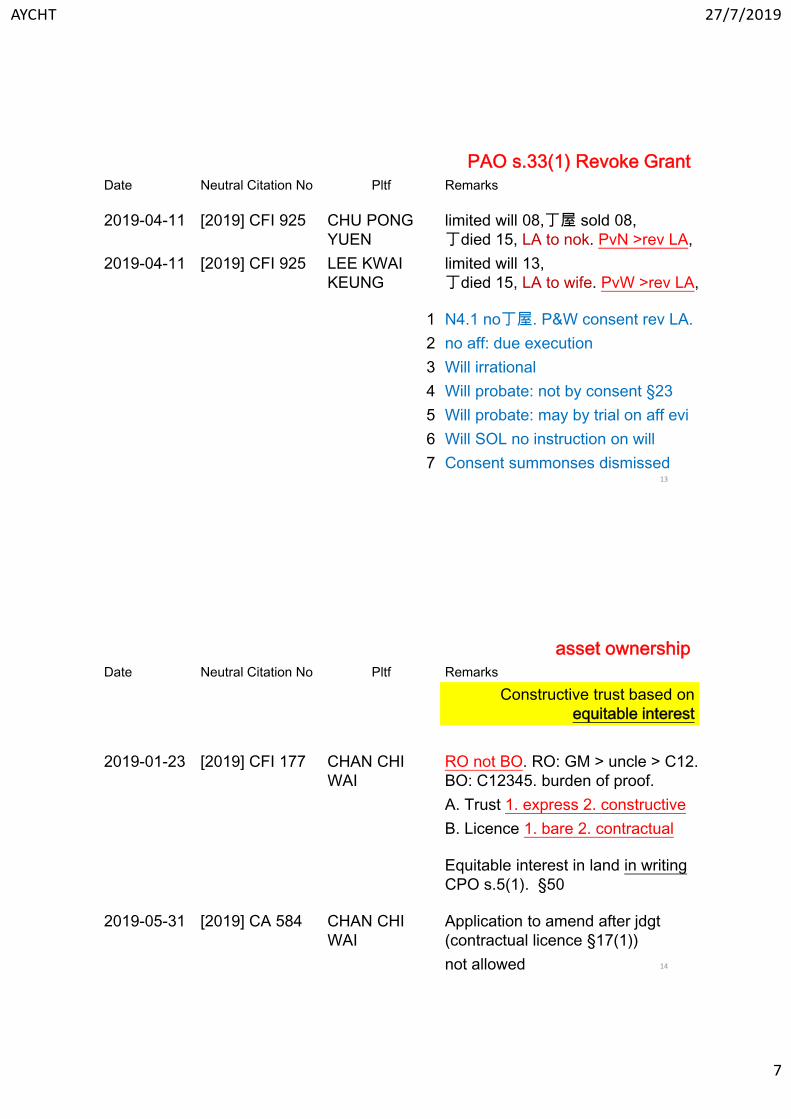

PAO s.33(1) Revoke Grant

13

Date Neutral Citation No Pltf Remarks

2019-04-11 [2019] CFI 925 CHU PONG YUEN

limited will 08,丁屋 sold 08, 丁died 15, LA to nok. PvN >rev LA,

2019-04-11 [2019] CFI 925 LEE KWAI KEUNG

limited will 13, 丁died 15, LA to wife. PvW >rev LA,

1 N4.1 no丁屋. P&W consent rev LA. 2 no aff: due execution3 Will irrational 4 Will probate: not by consent §235 Will probate: may by trial on aff evi6 Will SOL no instruction on will7 Consent summonses dismissed

asset ownership

14

Date Neutral Citation No Pltf RemarksConstructive trust based on

equitable interest

2019-01-23 [2019] CFI 177 CHAN CHI WAI

RO not BO. RO: GM > uncle > C12. BO: C12345. burden of proof. A. Trust 1. express 2. constructive B. Licence 1. bare 2. contractual

Equitable interest in land in writingCPO s.5(1). §50

2019-05-31 [2019] CA 584 CHAN CHI WAI

Application to amend after jdgt(contractual licence §17(1))not allowed

AYCHT 27/7/2019

8

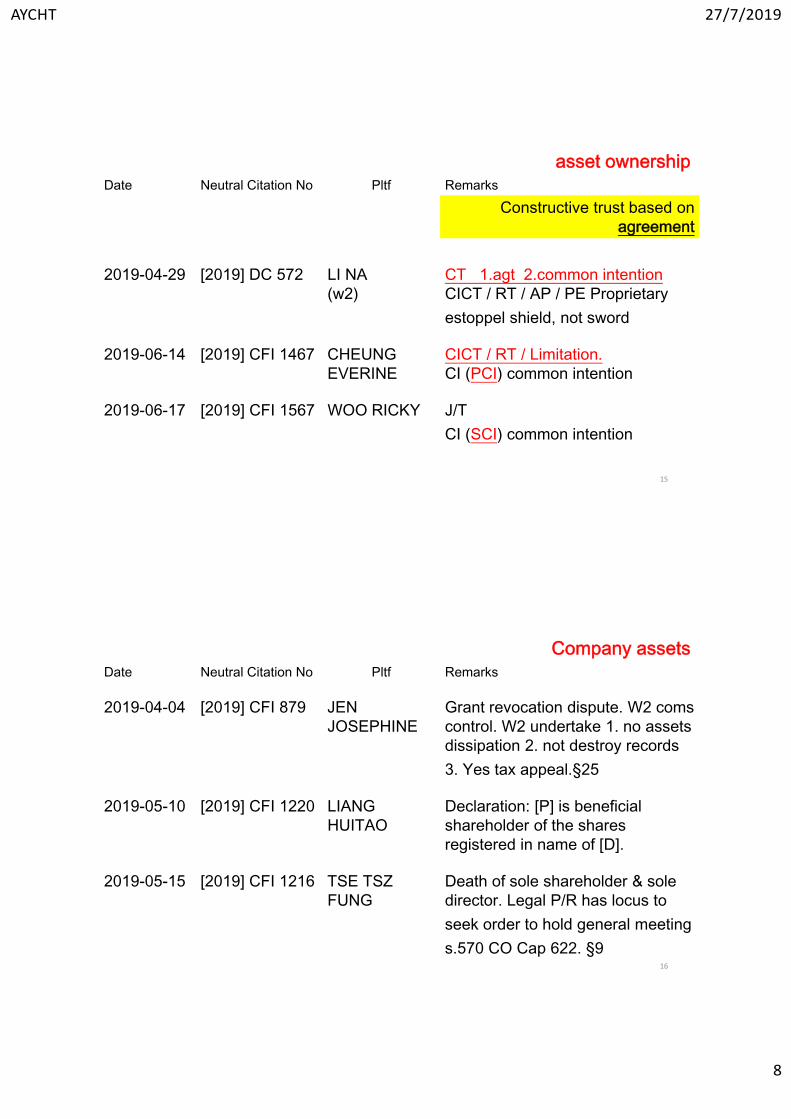

asset ownership

15

Date Neutral Citation No Pltf RemarksConstructive trust based on

agreement

2019-04-29 [2019] DC 572 LI NA (w2)

CT 1.agt 2.common intention CICT / RT / AP / PE Proprietaryestoppel shield, not sword

2019-06-14 [2019] CFI 1467 CHEUNG EVERINE

CICT / RT / Limitation. CI (PCI) common intention

2019-06-17 [2019] CFI 1567 WOO RICKY J/TCI (SCI) common intention

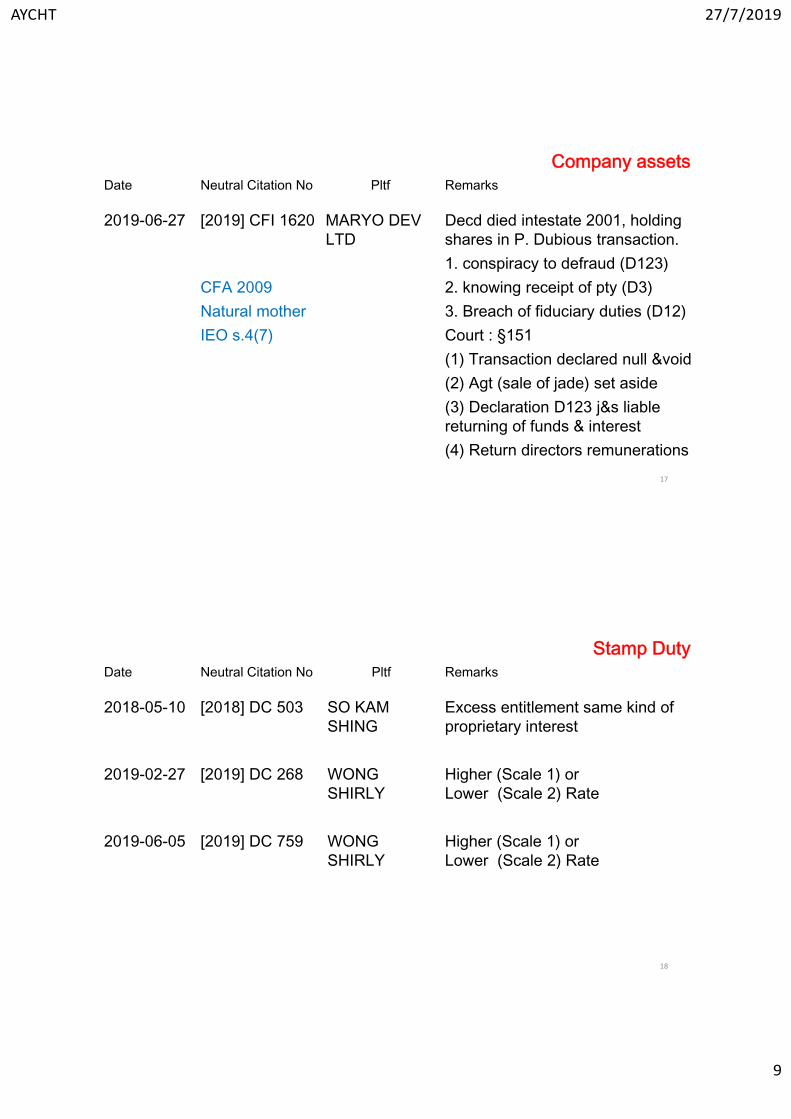

Company assets

16

Date Neutral Citation No Pltf Remarks

2019-04-04 [2019] CFI 879 JEN JOSEPHINE

Grant revocation dispute. W2 coms control. W2 undertake 1. no assets dissipation 2. not destroy records 3. Yes tax appeal.§25

2019-05-10 [2019] CFI 1220 LIANG HUITAO

Declaration: [P] is beneficial shareholder of the shares registered in name of [D].

2019-05-15 [2019] CFI 1216 TSE TSZ FUNG

Death of sole shareholder & sole director. Legal P/R has locus to seek order to hold general meetings.570 CO Cap 622. §9

AYCHT 27/7/2019

9

Company assets

17

Date Neutral Citation No Pltf Remarks

2019-06-27 [2019] CFI 1620 MARYO DEVLTD

Decd died intestate 2001, holding shares in P. Dubious transaction.1. conspiracy to defraud (D123)

CFA 2009 2. knowing receipt of pty (D3)Natural mother 3. Breach of fiduciary duties (D12)IEO s.4(7) Court : §151

(1) Transaction declared null &void(2) Agt (sale of jade) set aside(3) Declaration D123 j&s liable returning of funds & interest(4) Return directors remunerations

Stamp Duty

18

Date Neutral Citation No Pltf Remarks

2018-05-10 [2018] DC 503 SO KAM SHING

Excess entitlement same kind of proprietary interest

2019-02-27 [2019] DC 268 WONG SHIRLY

Higher (Scale 1) or Lower (Scale 2) Rate

2019-06-05 [2019] DC 759 WONG SHIRLY

Higher (Scale 1) or Lower (Scale 2) Rate

AYCHT 27/7/2019

10

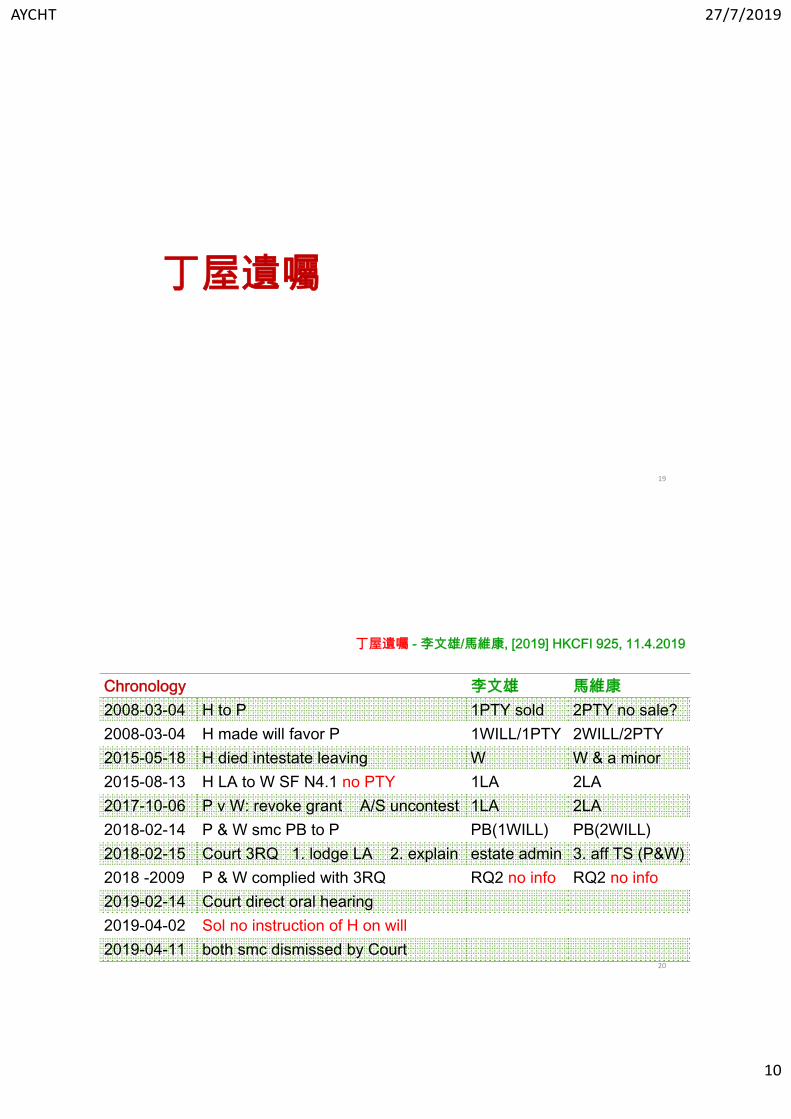

丁屋遺囑

19

丁屋遺囑 - 李文雄/馬維康, [2019] HKCFI 925, 11.4.2019

20

Chronology 李文雄 馬維康2008-03-04 H to P 1PTY sold 2PTY no sale?2008-03-04 H made will favor P 1WILL/1PTY 2WILL/2PTY2015-05-18 H died intestate leaving W W & a minor2015-08-13 H LA to W SF N4.1 no PTY 1LA 2LA2017-10-06 P v W: revoke grant A/S uncontest 1LA 2LA2018-02-14 P & W smc PB to P PB(1WILL) PB(2WILL)2018-02-15 Court 3RQ 1. lodge LA 2. explain estate admin 3. aff TS (P&W)2018 -2009 P & W complied with 3RQ RQ2 no info RQ2 no info2019-02-14 Court direct oral hearing2019-04-02 Sol no instruction of H on will2019-04-11 both smc dismissed by Court

AYCHT 27/7/2019

11

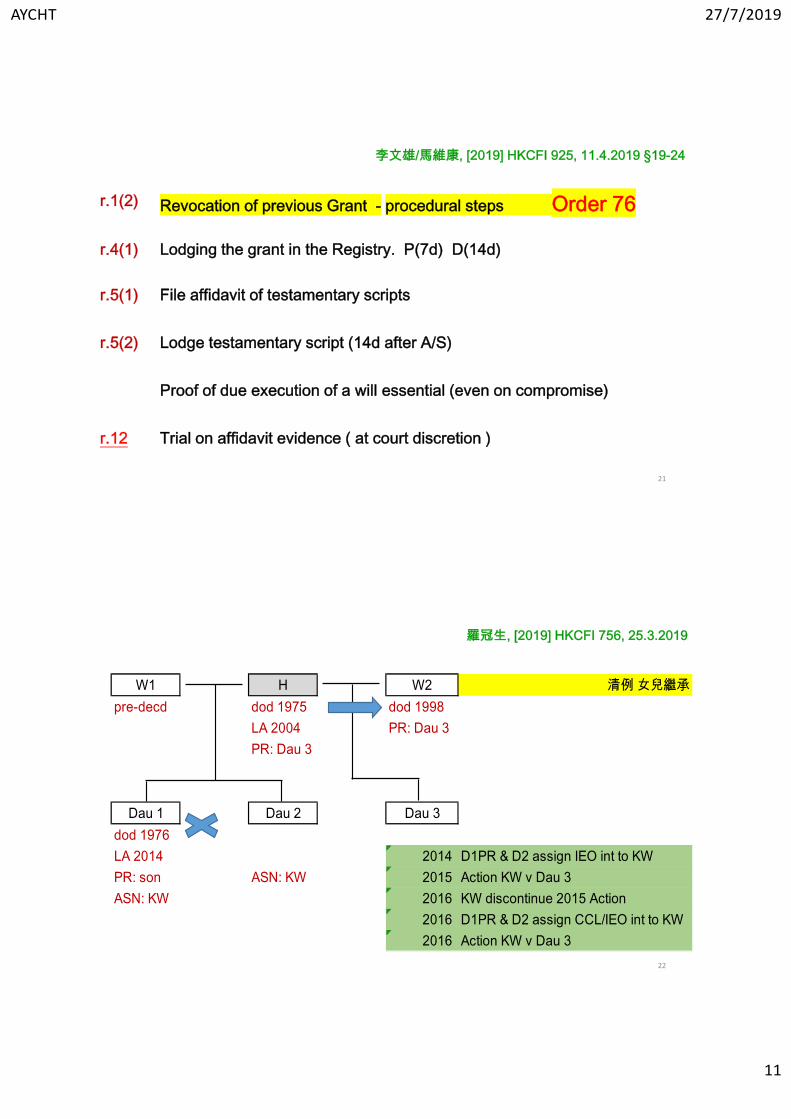

21

r.1(2) Revocation of previous Grant - procedural steps Order 76

r.4(1) Lodging the grant in the Registry. P(7d) D(14d)

r.5(1) File affidavit of testamentary scripts

r.5(2) Lodge testamentary script (14d after A/S)

Proof of due execution of a will essential (even on compromise)

r.12 Trial on affidavit evidence ( at court discretion )

李文雄/馬維康, [2019] HKCFI 925, 11.4.2019 §19-24

羅冠生, [2019] HKCFI 756, 25.3.2019

W1 H W2 清例 女兒繼承pre-decd dod 1975 dod 1998

LA 2004 PR: Dau 3PR: Dau 3

Dau 1 Dau 2 Dau 3dod 1976LA 2014 2014 D1PR & D2 assign IEO int to KWPR: son ASN: KW 2015 Action KW v Dau 3ASN: KW 2016 KW discontinue 2015 Action

2016 D1PR & D2 assign CCL/IEO int to KW2016 Action KW v Dau 3

22

AYCHT 27/7/2019

12

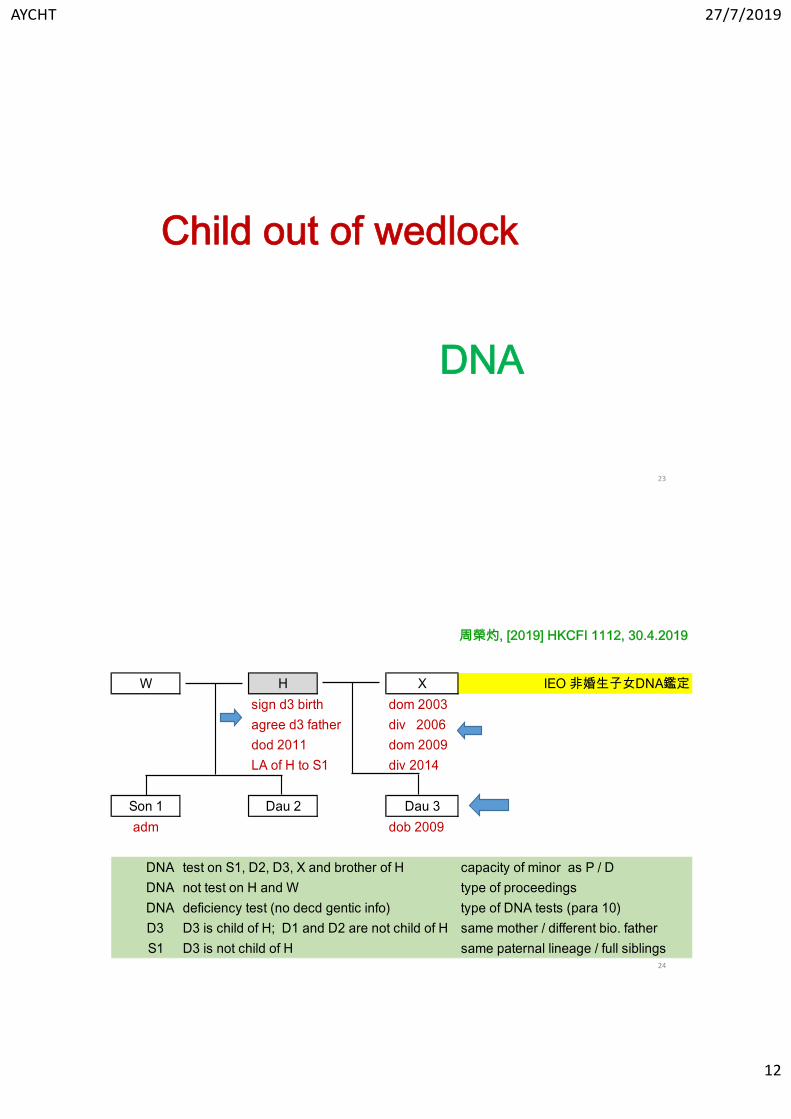

Child out of wedlock

DNA

23

周榮灼, [2019] HKCFI 1112, 30.4.2019

W H X IEO 非婚生子女DNA鑑定sign d3 birth dom 2003agree d3 father div 2006dod 2011 dom 2009LA of H to S1 div 2014

Son 1 Dau 2 Dau 3adm dob 2009

DNA test on S1, D2, D3, X and brother of H capacity of minor as P / DDNA not test on H and W type of proceedingsDNA deficiency test (no decd gentic info) type of DNA tests (para 10)D3 D3 is child of H; D1 and D2 are not child of H same mother / different bio. fatherS1 D3 is not child of H same paternal lineage / full siblings

24

AYCHT 27/7/2019

13

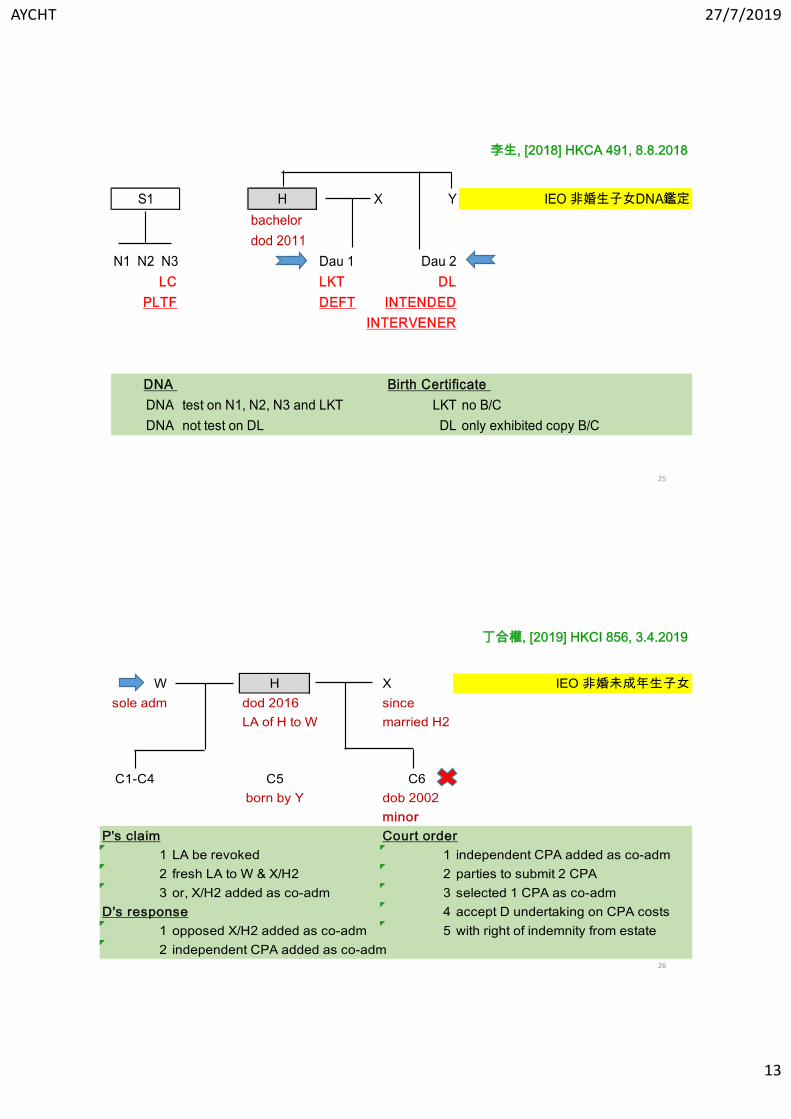

李生, [2018] HKCA 491, 8.8.2018

S1 H X Y IEO 非婚生子女DNA鑑定bachelordod 2011

N1 N2 N3 Dau 1 Dau 2LC LKT DL

PLTF DEFT INTENDEDINTERVENER

DNA Birth Certificate DNA test on N1, N2, N3 and LKT LKT no B/CDNA not test on DL DL only exhibited copy B/C

25

丁合權, [2019] HKCI 856, 3.4.2019

W H X IEO 非婚未成年生子女sole adm dod 2016 since

LA of H to W married H2

C1-C4 C5 C6born by Y dob 2002

minorP's claim Court order

1 LA be revoked 1 independent CPA added as co-adm2 fresh LA to W & X/H2 2 parties to submit 2 CPA3 or, X/H2 added as co-adm 3 selected 1 CPA as co-adm

D's response 4 accept D undertaking on CPA costs1 opposed X/H2 added as co-adm 5 with right of indemnity from estate2 independent CPA added as co-adm

26

AYCHT 27/7/2019

14

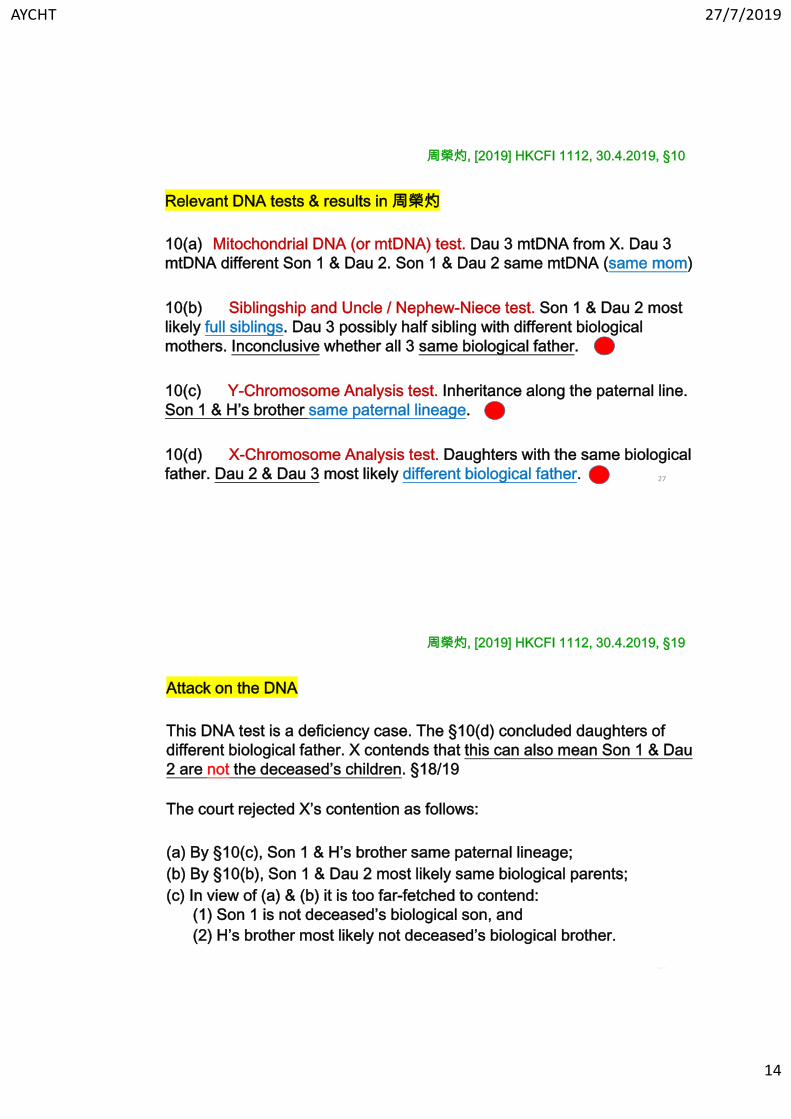

周榮灼, [2019] HKCFI 1112, 30.4.2019, §10

27

Relevant DNA tests & results in 周榮灼

10(a) Mitochondrial DNA (or mtDNA) test. Dau 3 mtDNA from X. Dau 3 mtDNA different Son 1 & Dau 2. Son 1 & Dau 2 same mtDNA (same mom)

10(b) Siblingship and Uncle / Nephew-Niece test. Son 1 & Dau 2 most likely full siblings. Dau 3 possibly half sibling with different biological mothers. Inconclusive whether all 3 same biological father.

10(c) Y-Chromosome Analysis test. Inheritance along the paternal line. Son 1 & H’s brother same paternal lineage.

10(d) X-Chromosome Analysis test. Daughters with the same biological father. Dau 2 & Dau 3 most likely different biological father.

周榮灼, [2019] HKCFI 1112, 30.4.2019, §19

28

Attack on the DNA

This DNA test is a deficiency case. The §10(d) concluded daughters of different biological father. X contends that this can also mean Son 1 & Dau2 are not the deceased’s children. §18/19

The court rejected X’s contention as follows:

(a) By §10(c), Son 1 & H’s brother same paternal lineage;(b) By §10(b), Son 1 & Dau 2 most likely same biological parents;(c) In view of (a) & (b) it is too far-fetched to contend:

(1) Son 1 is not deceased’s biological son, and(2) H’s brother most likely not deceased’s biological brother.

AYCHT 27/7/2019

15

周榮灼, [2019] HKCFI 1112, 30.4.2019, §10

29

Reliability of DNA

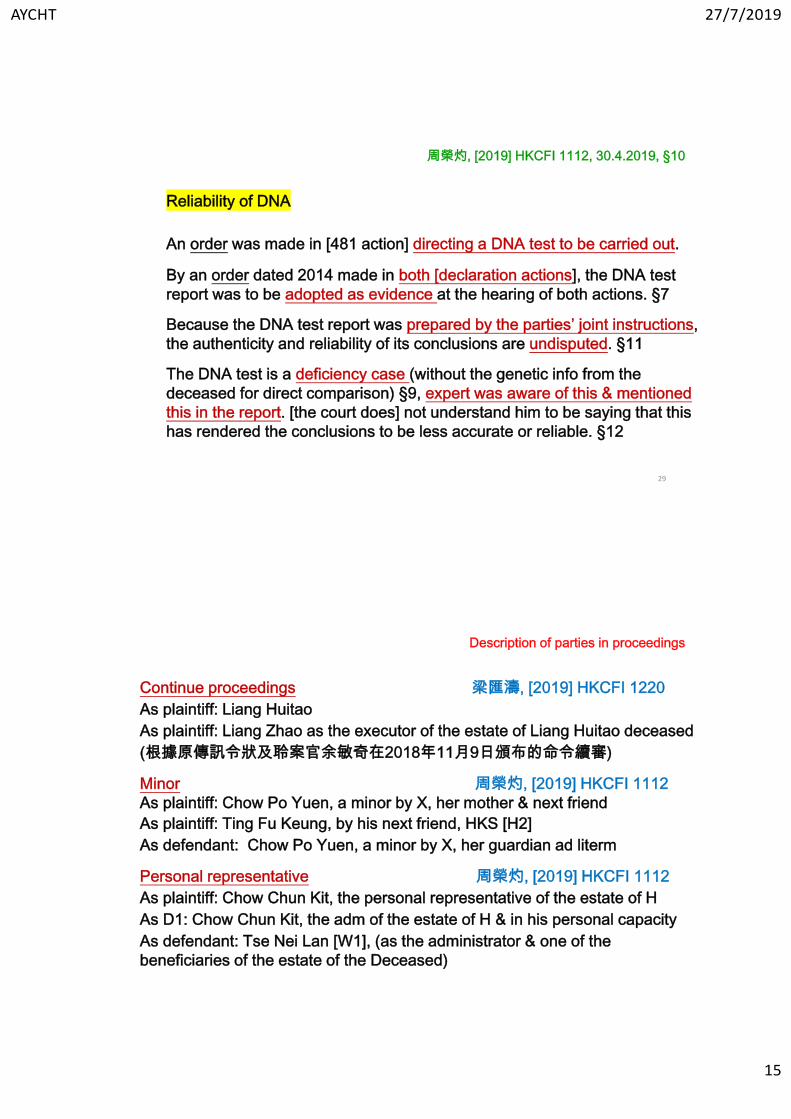

An order was made in [481 action] directing a DNA test to be carried out.

By an order dated 2014 made in both [declaration actions], the DNA test report was to be adopted as evidence at the hearing of both actions. §7

Because the DNA test report was prepared by the parties’ joint instructions, the authenticity and reliability of its conclusions are undisputed. §11

The DNA test is a deficiency case (without the genetic info from the deceased for direct comparison) §9, expert was aware of this & mentioned this in the report. [the court does] not understand him to be saying that this has rendered the conclusions to be less accurate or reliable. §12

Description of parties in proceedings

30

Continue proceedings 梁匯濤, [2019] HKCFI 1220As plaintiff: Liang HuitaoAs plaintiff: Liang Zhao as the executor of the estate of Liang Huitao deceased(根據原傳訊令狀及聆案官余敏奇在2018年11月9日頒布的命令續審)

Minor 周榮灼, [2019] HKCFI 1112As plaintiff: Chow Po Yuen, a minor by X, her mother & next friendAs plaintiff: Ting Fu Keung, by his next friend, HKS [H2] As defendant: Chow Po Yuen, a minor by X, her guardian ad literm

Personal representative 周榮灼, [2019] HKCFI 1112As plaintiff: Chow Chun Kit, the personal representative of the estate of HAs D1: Chow Chun Kit, the adm of the estate of H & in his personal capacityAs defendant: Tse Nei Lan [W1], (as the administrator & one of the beneficiaries of the estate of the Deceased)

AYCHT 27/7/2019

16

Stamp Duty

FAQ

31

32

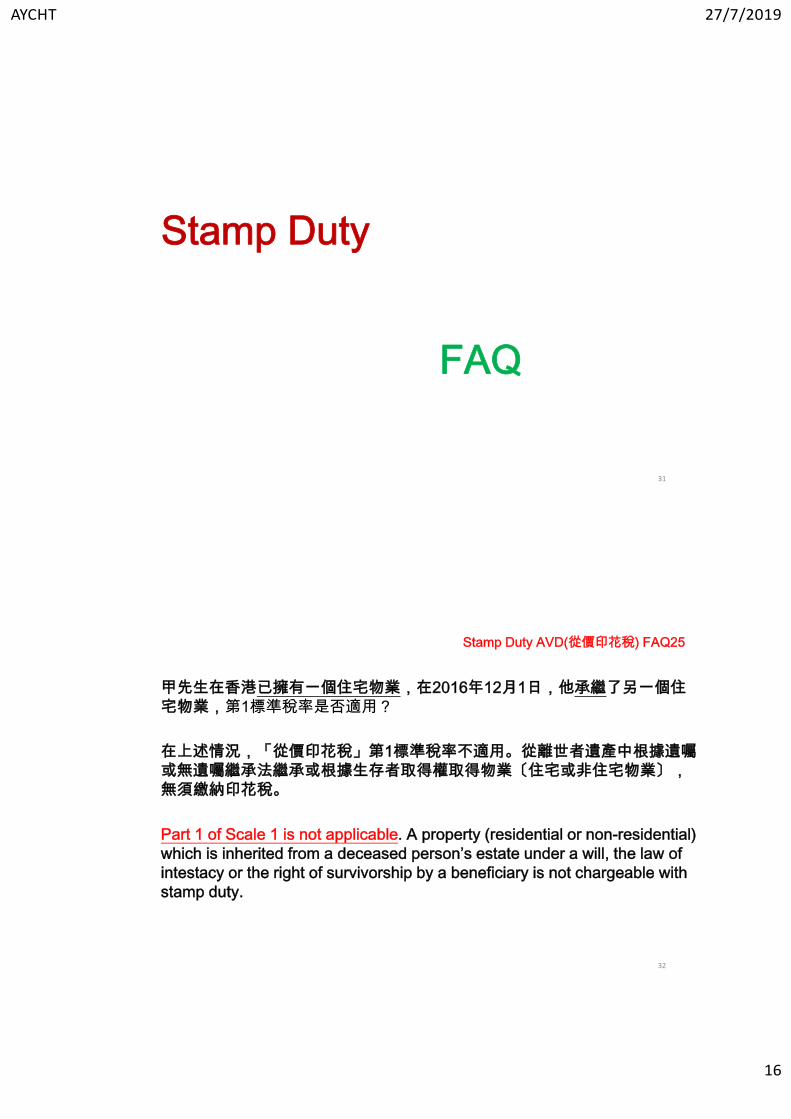

甲先生在香港已擁有一個住宅物業,在2016年12月1日,他承繼了另一個住宅物業,第1標準稅率是否適用?

在上述情況,「從價印花稅」第1標準稅率不適用。從離世者遺產中根據遺囑或無遺囑繼承法繼承或根據生存者取得權取得物業〔住宅或非住宅物業〕,無須繳納印花稅。

Part 1 of Scale 1 is not applicable. A property (residential or non-residential) which is inherited from a deceased person’s estate under a will, the law of intestacy or the right of survivorship by a beneficiary is not chargeable with stamp duty.

Stamp Duty AVD(從價印花稅) FAQ25

AYCHT 27/7/2019

17

33

乙先生由一位已故人士承繼了位於香港的住宅物業X,他現打算購入另一住宅物業Y,第1標準第一部稅率是否適用?

由於在購買物業Y時,乙先生在香港已擁有另一個住宅物業,第1標準第1部稅率將適用於購買住宅物業Y的買賣協議/轉易契,這與乙先生以何種方式取得物業X無關。

Part 1 of Scale 1 will apply to the agreement for sale/conveyance on sale in respect of Property Y since at the time of its acquisition, Mr B already owned another residential property in Hong Kong, i.e. Property X. How MrB became owner of Property X is not relevant.

Stamp Duty AVD(從價印花稅) FAQ26

34

如果一位非香港永久性居民在2012年10月27日或以後由一位已故人士承繼一個住宅物業,他是否須繳納「買家印花稅」?

該名非香港永久性居民無須繳納「買家印花稅」。根據遺囑或無遺囑繼承法律從離世者遺產中繼承或根據生存者取得權取得住宅物業無須繳納印花稅。根據《印花稅條例》(第117章),「印花稅」包括「從價印花稅」、「額外印花稅」和「買家印花稅」。

The non-HKPR is not liable to BSD as the residential property which is inherited from a deceased person's estate under a will or the law of intestacy or right of survivorship by a beneficiary is exempted from stamp duty. "Stamp duty" is defined under the SDO (Cap.117) to include ad valorem stamp duty, special stamp duty and BSD.

Stamp Duty BSD(買家印花稅) FAQ16

AYCHT 27/7/2019

18

35

如果我於2010後繼承已離世者的住宅物業,並於24或36個月或以內將之轉售或轉讓與他人,我是否須就有關交易繳納「額外印花稅」?

遺產受益人出售或轉讓其繼承自離世者遺產,就是根據遺囑、無遺囑繼承法律或生存者取得權而取得的住宅物業,可豁免繳納「額外印花稅」。因此,假如你在繼承住宅物業後24或36個月或以內將該物業轉售或轉讓予他人,也無須就有關交易繳納「額外印花稅」。

Sale or transfer of a residential property which is inherited from a deceased person's estate under a will, the law of intestacy or right of survivorship by a beneficiary is exempted from SSD. Therefore, SSD will NOT apply to the disposal of the inherited property even if it is disposed of within 24 months (if the property was acquired between 20.11.2010 and 26.10.2012) or 36 months (if the property was acquired on or after 27.10.2012) from the date of inheritance.

Stamp Duty SSD(額外印花稅) FAQ11

Stamp Duty on DFA / Assent

[2018] HKDC 503 So Kam Shing

36

AYCHT 27/7/2019

19

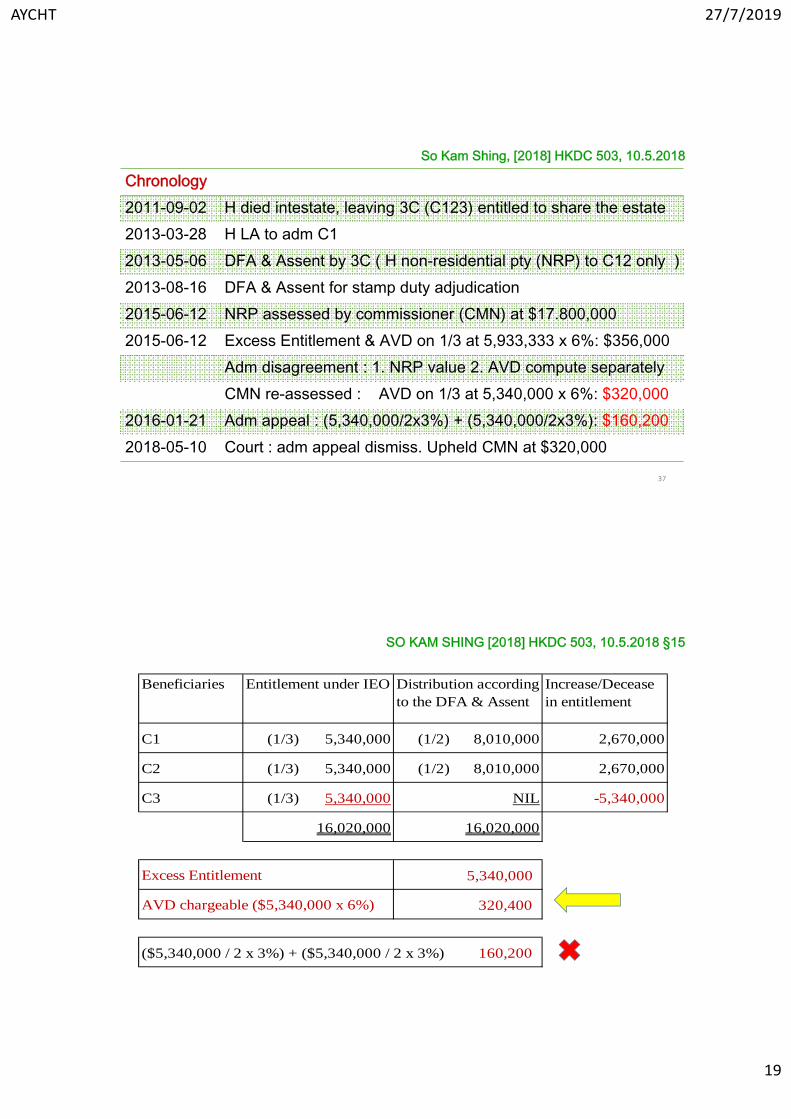

So Kam Shing, [2018] HKDC 503, 10.5.2018

37

Chronology2011-09-02 H died intestate, leaving 3C (C123) entitled to share the estate2013-03-28 H LA to adm C12013-05-06 DFA & Assent by 3C ( H non-residential pty (NRP) to C12 only )2013-08-16 DFA & Assent for stamp duty adjudication2015-06-12 NRP assessed by commissioner (CMN) at $17.800,0002015-06-12 Excess Entitlement & AVD on 1/3 at 5,933,333 x 6%: $356,000

Adm disagreement : 1. NRP value 2. AVD compute separatelyCMN re-assessed : AVD on 1/3 at 5,340,000 x 6%: $320,000

2016-01-21 Adm appeal : (5,340,000/2x3%) + (5,340,000/2x3%): $160,2002018-05-10 Court : adm appeal dismiss. Upheld CMN at $320,000

38

SO KAM SHING [2018] HKDC 503, 10.5.2018 §15

Beneficiaries Increase/Deceasein entitlement

C1 (1/3) 5,340,000 (1/2) 8,010,000 2,670,000

C2 (1/3) 5,340,000 (1/2) 8,010,000 2,670,000

C3 (1/3) 5,340,000 NIL -5,340,000

16,020,000 16,020,000

5,340,000

320,400

($5,340,000 / 2 x 3%) + ($5,340,000 / 2 x 3%) 160,200

Entitlement under IEO Distribution accordingto the DFA & Assent

AVD chargeable ($5,340,000 x 6%)

Excess Entitlement

AYCHT 27/7/2019

20

39

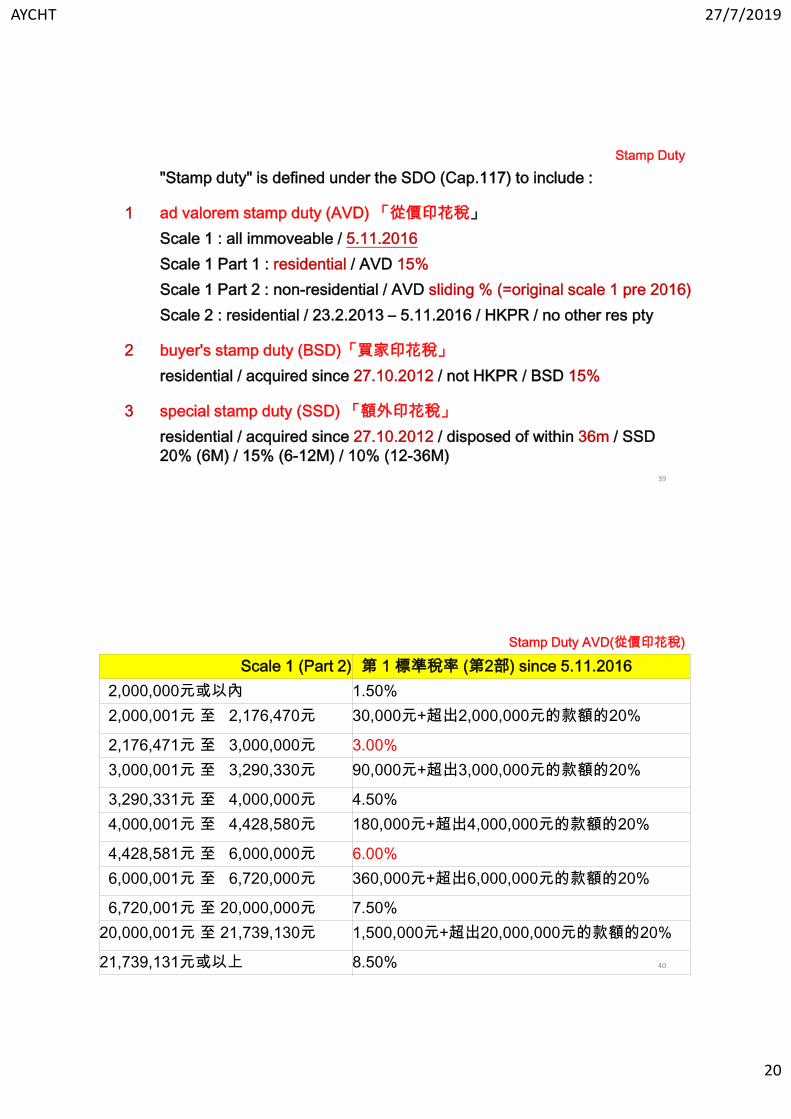

"Stamp duty" is defined under the SDO (Cap.117) to include :

1 ad valorem stamp duty (AVD) 「從價印花稅」Scale 1 : all immoveable / 5.11.2016Scale 1 Part 1 : residential / AVD 15%Scale 1 Part 2 : non-residential / AVD sliding % (=original scale 1 pre 2016)Scale 2 : residential / 23.2.2013 – 5.11.2016 / HKPR / no other res pty

2 buyer's stamp duty (BSD)「買家印花稅」residential / acquired since 27.10.2012 / not HKPR / BSD 15%

3 special stamp duty (SSD) 「額外印花稅」residential / acquired since 27.10.2012 / disposed of within 36m / SSD 20% (6M) / 15% (6-12M) / 10% (12-36M)

Stamp Duty

40

Stamp Duty AVD(從價印花稅)

Scale 1 (Part 2) 第 1 標準稅率 (第2部) since 5.11.20162,000,000元或以內 1.50%2,000,001元 至 2,176,470元 30,000元+超出2,000,000元的款額的20%

2,176,471元 至 3,000,000元 3.00%3,000,001元 至 3,290,330元 90,000元+超出3,000,000元的款額的20%

3,290,331元 至 4,000,000元 4.50%4,000,001元 至 4,428,580元 180,000元+超出4,000,000元的款額的20%

4,428,581元 至 6,000,000元 6.00%6,000,001元 至 6,720,000元 360,000元+超出6,000,000元的款額的20%

6,720,001元 至 20,000,000元 7.50%20,000,001元 至 21,739,130元 1,500,000元+超出20,000,000元的款額的20%

21,739,131元或以上 8.50%

AYCHT 27/7/2019

21

41

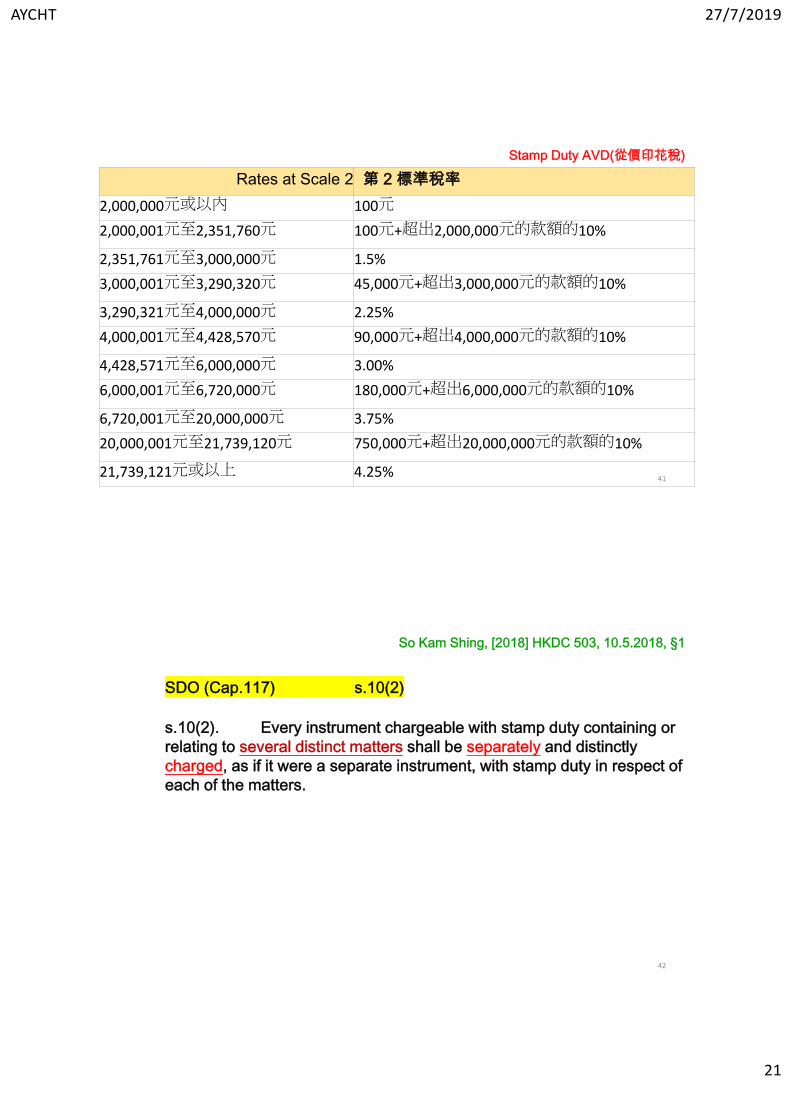

Stamp Duty AVD(從價印花稅)

Rates at Scale 2 第 2 標準稅率2,000,000元或以內 100元

2,000,001元至2,351,760元 100元+超出2,000,000元的款額的10%

2,351,761元至3,000,000元 1.5%

3,000,001元至3,290,320元 45,000元+超出3,000,000元的款額的10%

3,290,321元至4,000,000元 2.25%

4,000,001元至4,428,570元 90,000元+超出4,000,000元的款額的10%

4,428,571元至6,000,000元 3.00%

6,000,001元至6,720,000元 180,000元+超出6,000,000元的款額的10%

6,720,001元至20,000,000元 3.75%

20,000,001元至21,739,120元 750,000元+超出20,000,000元的款額的10%

21,739,121元或以上 4.25%

So Kam Shing, [2018] HKDC 503, 10.5.2018, §1

42

SDO (Cap.117) s.10(2)

s.10(2). Every instrument chargeable with stamp duty containing or relating to several distinct matters shall be separately and distinctly charged, as if it were a separate instrument, with stamp duty in respect of each of the matters.

AYCHT 27/7/2019

22

43

It is not [C3] transferring her 1/3 proprietary interest in the Property to C12 in equal shares, but the [adm] with [C3]’s consent indicated in the DFA transferring the 1/3 proprietary interest in the Property to C12 by executing the Asset.

The crux is whether that transfer is 1 matter or 2 separate distinct matters.

Court : “distinct matters” in SDO s.10(2) are different classes of property being transferred in 1 instrument. The Excessive Entitlement transferred to [C12] by the Deeds is the same kind of proprietary interest. SDO s.10(2) not of assistance.

So Kam Shing, [2018] HKDC 503, 10.5.2018, §30/33

44

Held, dismissing the appeal, that

1. By operation of the DFA and the Assent, Ts had inherited a share in X's estate which was in excess of the interest to which they were entitled under intestacy law.

The Deeds were therefore deemed to be a conveyance of transfer operating as a voluntary disposition inter vivos under s.27(4) of [SDO] and chargeable with AVD. §23

(Baker v IRC [1924] AC 270, Tan Kay Thye v CSD [1991] 3 MLJ 150 applied).

So Kam Shing, [2018] HKDC 503, 10.5.2018, §23

AYCHT 27/7/2019

23

45

2. As a matter of law, S never had any proprietary interest in the shop, since benes of an estate did not have any proprietary interest in any asset of the estate until the execution of an assent by the [P/R].

It was not S, but the administrator with S's consent under the DFA, who transferred S's one-third interest in the shop to T1-2 by executing the Assent. §29-30

(CSD (Queensland) v Livingston [1965] AC 694 applied).

So Kam Shing, [2018] HKDC 503, 10.5.2018, §29-30

46

3. "Distinct matters" under s.10(2) were different classes of property being transferred in the same document.

The Excessive Entitlement transferred to Ts under the Deeds were the same kind of proprietary interest so that there was only 1 matter, not 2 separate matters. Accordingly, the AVD chargeable was $320,400. §31-34

(Ansell v CIR [1929] applied).

So Kam Shing, [2018] HKDC 503, 10.5.2018, §31-34

AYCHT 27/7/2019

24

Stamp Duty on DFA / Assent

[2019] HKDC 268 Wong Suet Foon Shirly

47

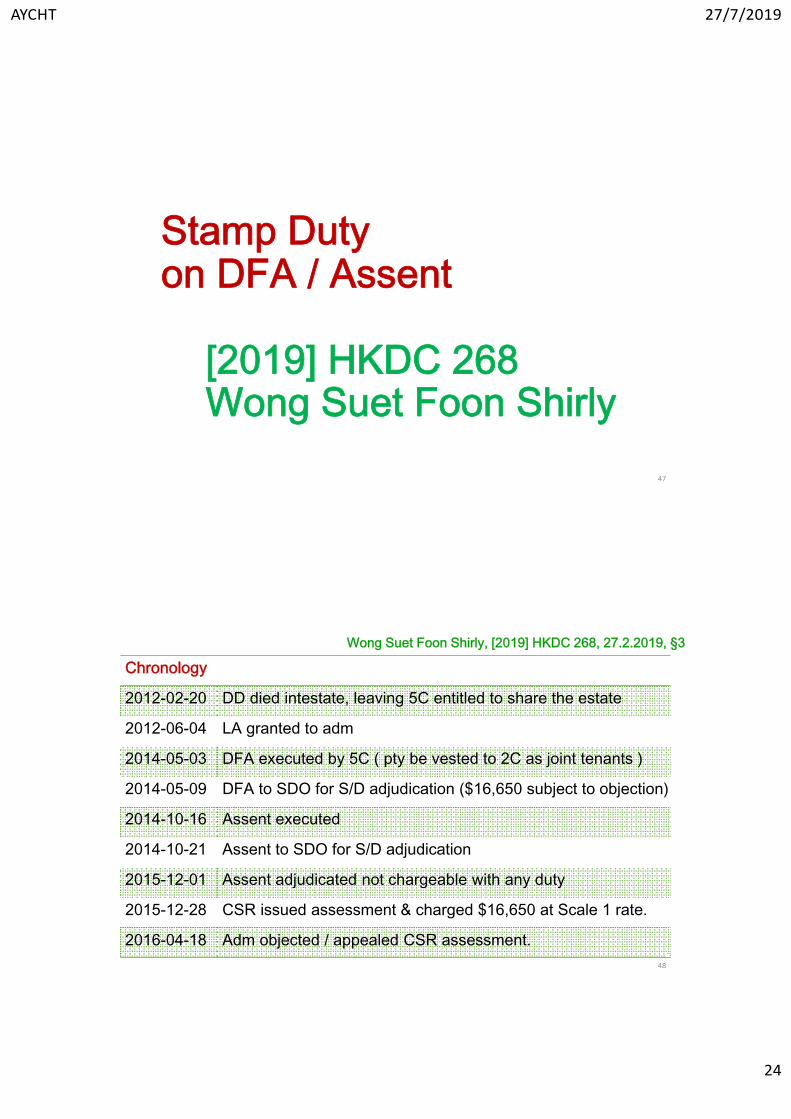

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §3

48

Chronology

2012-02-20 DD died intestate, leaving 5C entitled to share the estate

2012-06-04 LA granted to adm

2014-05-03 DFA executed by 5C ( pty be vested to 2C as joint tenants )

2014-05-09 DFA to SDO for S/D adjudication ($16,650 subject to objection)

2014-10-16 Assent executed

2014-10-21 Assent to SDO for S/D adjudication

2015-12-01 Assent adjudicated not chargeable with any duty

2015-12-28 CSR issued assessment & charged $16,650 at Scale 1 rate.

2016-04-18 Adm objected / appealed CSR assessment.

AYCHT 27/7/2019

25

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §14

49

L20151228 IRD

CSR issued the assessment and charged the stamp duty of HK$16,650 on the Deed (and on the Assent) on the grounds that the Deed and the Assent “operate as a voluntary disposition inter vivos” and therefore were chargeable with stamp duty under s.27(1) SDO.

The vesting of the said Property by the … administratrix of the said Deceased in [2C] was not a transfer of residential property between close relatives, and Scale 2 rates were not applicable thereto”.

As a result, the Higher Scale 1 rates were charged.

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §16

50

Issues for the Court’s determination listed in Case Stated

(1) Whether the Deed and the Assent (collectively as “the Deeds”) are chargeable with ad valorem stamp duty; and

(2) If so, with what amount of stamp duty they are chargeable ?

AYCHT 27/7/2019

26

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §18

51

Issues for the Court’s determination) per the Appellant

(1) Whether or not under the Deed and/or the Assent, the abandoned, disclaimed or renounced “shares” and/or “interest” of the alleged “60%” of the Property were “voluntary dispositions inter vivos” by [3 of 5 intestate benes] disclaiming to [2 of the other benes] thereby attracting stamp duty;

(2) If they were or any of them was, whether Scale 1 (higher) rates or Scale 2 (lower) rates should be so chargeable and charged by reason of any (close) relationship or at all ?

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §17

52

Stance of CSR ( represented by DOJ ) on Q1

1. Whether or not under the Deed and/or the Assent, the abandoned, disclaimed or renounced “shares” and/or “interest” of the alleged “60%” of the Property were “voluntary dispositions inter vivos” by [3 of 5 intestate benes] disclaiming to [2 of the other benes] thereby attracting stamp duty

本上訴的《印花稅評稅及繳款通知書》[T9/52] 提及署長就《家庭協議契據》及《允許書》兩份文件徵收印花稅的說法並不正確,正確的分析應為只有《允許書》需要繳付印花稅The statement of the Collector charging stamp duty on the 2 docs, [DFA] and [Assent] as mentioned in “the Stamp Duty Assessment and Demand for Payment” (T9/52) in this Appeal was incorrect, the correct analysis is that ONLY “the Assent” was required to pay the stamp duty.

AYCHT 27/7/2019

27

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §24

53

Stance of CSR ( represented by DOJ )

The Assent constituted a conveyance of immovable property operating as a voluntary disposition inter vivos to [2C] within the meaning of section 27(1) of [SDO] to the extent in excess of their entitlement under the applicable intestacy law, ie 60% (as opposed to 40% in aggregate),

and as such ad valorem stamp duty under Scale 1 of Head 1(1) in the First Schedule of [SDO] was chargeable on the Assent.

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §25

54

Stance of CSR ( represented by DOJ )

Scale 2 rates, ie the lower rates, were not applicable given the vesting of the Property pursuant to the Assent was not a transfer of residential property between close relatives such that section 29AL of [SDO] was not applicable.

AYCHT 27/7/2019

28

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §15

55

L20160418/ L20171114 adm initial grounds of objection to CSR

1. Confinement of 2 successors by reason of any alienation restriction (as per HKHA advice) in taking the Property was caused by the Govt.

2. Any transfer was in any event made between close relatives and therefore should only be chargeable with Scale 2 rates.

3. The transfer of [Deceased Property] unto the 2 benes under the intestacy should … not be chargeable with, any stamp duty; and

4. Inappropriate for CSR to [charge] the Scale 1 rates stamp duty for the transfer of [Deceased Property] unto the 2 benes succeeding.

56

Disclaiming bene never had any proprietary interest in Pty. 18DC 268 §29

Benes of the estate of a deceased do not have any proprietary interest in any particular asset in the estate before the execution of an assent by the executor or administrator. 18DC 268 §29.

Williams, Mortimer & Sunnucks (20ed) §81-03 :-Until assent or conveyance, a person interested under the will or intestacy has an inchoate transmissible to his own representation. It is a chose inaction capable of itself being settled or transmitted. …

Benes have no beneficial interest in the estate (including the Pty) until the administration of the estate by the adm by an assent: 19DC 268 §36.

So Kam Shing, [2018] HKDC 503 §29 / WONG SHIRLY, [2019] HKDC 268 §36

AYCHT 27/7/2019

29

57

Written assent is required to effect the passing of a legal estate, even if the P/R and the beneficiary are the same person. Wong Mei Sin v Ng Wai Kin, HCMP2/2011, 5.7.2011.

An assent to the vesting of a legal estate shall be in writing, signed by the P/R, & shall name the person in whose favour it is given, and shall operate to vest in that person the legal estate to which it relates : PAO s.66(3).

It is the assent which operates to vest an immovable property onto a bene under a will. 19DC 268 §39 The assent shall operate to vest in that person the estate to which the assent relates : PAO s.66(2).

WONG SUET FOON SHIRLY, [2019] HKDC 268, 27.2.2019 §32

58

An assent is deemed to be a conveyance operating as a voluntary disposition inter vivos insofar as the share in the estate inherited was in excess of the interest that one may inherit under the intestacy laws: §47.

By … [the DFA and Assent], [benes] have inherited a share in the Decd’sestate … in excess of the interest that they may inherit under the intestacy law. … the Deeds are deemed to be a conveyance or transfer operating as a voluntary disposition inter vivos under SDO s 27(4). The Deeds are therefore chargeable with ad valorem stamp duty. 18HKDC 503 §23.

The test on whether a substantial benefit has been conferred on the transferee is an objective test & … intention of the parties is irrelevant: §48 .

WONG SUET FOON SHIRLY, [2019] HKDC 268, 27.2.2019 §47

AYCHT 27/7/2019

30

59

I also find the comments made by Viscount Cave LC in Baker v Commissioner of Inland Revenue [1924] AC 270 at p 275 helpful: §49.

…a conveyance, although for value, comes within the sec-tion if it confers upon the grantee a substantial benefit beyond what that grantee gives, or (in other words) if it is in substance a gift to the person taking under it after allowing for any consideration which he brings in. In such cases the conveyance does confer a benefit – that is a gift – on the person to whom the conveyance is made, and to that extent is to be treated a as a voluntary disposition.

WONG SUET FOON SHIRLY, [2019] HKDC 268, 27.2.2019 §49

60

Whether s.29AL of SDO applies ?

s.29AL such a “conveyance on sale” is chargeable with the stamp duty at Scale 2 rates (the lower rates) if, among others, the property concerned is residential property and the transferee, or each of the transferees is closely related to the transferor, or to each of the transferors.

Who is/are the transferor(s) ?

WONG SUET FOON SHIRLY, [2019] HKDC 268, 27.2.2019 §51

AYCHT 27/7/2019

31

61

The transferor could not be the 3 renouncing beneficiaries. … by executing the [DFA], they had merely renounced their rights to inherit the Property. I find that at no time did they have any beneficial interest in the Property which was capable of being transferred to the [transferee benes]. §53

[Adm] acting in her capacity as administratrix in executing the Assent did not hold any interest over the estate of the Deceased which she could in her personal capacity transfer to herself and the [other transferee benes]. §534

WONG SUET FOON SHIRLY, [2019] HKDC 268, 27.2.2019 §53

62

Williams, Mortimer & Sunnucks (21ed) §35-09 :-

The interests vesting in the [P/R] do not vest in him beneficially.

Although he is not necessarily a trustee he is said to hold “in auter droit” (in right of another) so that his interest is different from the absolute and ordinary interest which a person would have in his own property.

It has been said that he has his estate merely as the minister and dispenser of the goods of the dead.

WONG SUET FOON SHIRLY, [2019] HKDC 268, 27.2.2019 §54

AYCHT 27/7/2019

32

Wong Suet Foon Shirly, [2019] HKDC 268, 27.2.2019, §55

63

Court’s decision

(1) Whether the Deed and the Assent are chargeable with ad valorem stamp duty ?

Yes. On the Assent but not the DFA.

(2) If so, with what amount of stamp duty they are chargeable ?

$16,650 ( charged at Scale at Head 1(1) First Schedule SDO of 15% )

Stamp Duty on DFA / Assent

[2019] HKDC 759Wong Suet Foon Shirly

64

AYCHT 27/7/2019

33

Wong Suet Foon Shirly, [2019] HKDC 759, 5.6.2019, §7

65

Adm grounds on appeal to DC (3 個理由作為申請上訴)

(1) 上訴人兩姊妺獲得物業的全部業權。屬無遺產繼承之下的繼承,不能視作業權的轉讓。

(2) 《家庭協議契據》3位受益人放棄了繼承物業的權利,只餘下2位為合法繼承人。

(3) 《允許書》獲得業權是繼承的程序,所以印花稅應予豁免。故判決書中第33段所裁定 《允許書》需予徵收印花稅及稅款金額港幣 $16,650 均不正確。

Wong Suet Foon Shirly, [2019] HKDC 759, 5.6.2019, §17

66

Court Decision on 上訴理由 (1)

(1) [兩人] 獲物業的全部業權, 屬無遺產繼承…, 不能視作業權的轉讓。

本法院就本案的事實背景, 及適用的法律條文(即《印花稅條例》第27(1)及(4)條), 及有約束性的案例中,如 So Kam Shing [2018] HKDC 503 (§§21-26);Tan Kay Thye [1991] 3 MLJ 150 (§§156-157) 及 Baker v CIR [1924] AC (§§274-276)

就本案爭議點,本案《允許書》是否可予徵收從價印花稅,已作出裁決。

AYCHT 27/7/2019

34

Wong Suet Foon Shirly, [2019] HKDC 759, 5.6.2019, §22

67

Court Decision on 上訴理由 (2)

(2) 《家庭協議契據》3受益人放棄繼承物業權利,只餘下2位合法繼承人。

原判決書中的 §§7,18(1)及41-49 詳細考慮並駁回此項上訴之理據。

[兩人]確是本案單位合法繼承人,但這點對本案《允許書》是否須要繳交從價印花稅並沒有實質關連,亦不能構成《允許書》不須繳交從價印花稅的因由。

Wong Suet Foon Shirly, [2019] HKDC 759, 5.6.2019, §27

68

Court Decision on 上訴理由 (3)

(2) 《允許書》獲得業權是繼承的程序,所以印花稅應予豁免。

原判決書中 (見§§26-50)已列出《允許書》是否可予徵收從價印花稅所考慮的各項因素及法庭原則,及裁定可予徵收從價印花稅的原因。

AYCHT 27/7/2019

35

Wong Suet Foon Shirly, [2019] HKDC 759, 5.6.2019, §33

69

樓宇補價的問題

上訴人並指稱涉及本案單位價值以估值港幣$1,850,000計算,須先償還有關責任包括補價($1,344,083)。

即使有補價的債項…,該補價已應在簽訂《家庭協議契據》及《允許書》前被解除,故不應構成本案單位的債項。

Wong Suet Foon Shirly, [2019] HKDC 759, 5.6.2019, §38

70

印花稅金額之計算

上訴人認為按《遺囑認證及遺產管理條例》第64條,附有責任的財產須先作為償還有關責任之用。根據此說法,上訴人認為她們所應繳付從價印花稅之金額應為港幣$1,549。

根據《印花稅條例》第27(1)條,印花稅是按物業的價值予以徵收,而並非按物業在扣除所有債項後的價值予以徵收。因此,上訴人在此方面的說法,[法院]認爲是沒有任何可爭議的地方。

AYCHT 27/7/2019

36

Wong Suet Foon Shirly, [2019] HKDC 759, 5.6.2019, §43

71

已表明相反意願 ( IEO s.5(1)(c) – hotchpot rule )

上訴人認為他們的三兄弟以《家庭協議契據》放棄其權利,已符合《無遺囑者遺產條例》第5(1)條的「已表明相反意願」要求。

該5(1)(c)條是指無遺囑者藉預付財產辦法而已付給或在其子女成婚時已付給該子女的任何金錢或財產,該已付給子女的預付財產或金錢,須視作為全數或局部償付該子女應承受的份額,或用作全數或局部償付該無遺囑者去世時仍活着的每位子女可承受的份額,除非有人表明任何相反意願。

該5(1)(c)條是指無遺產者若在身故前將財產或金錢預先付給子女,該財產或金錢須視為用全數或局部償付給子女應承受的份額,除非有人表明任何相反意願。明顯地,該條款是與本案的案情截然不同,亦不適用於本上訴案之中。

IEO Cap 73 s5(1)c)

72

Statutory trusts in favour of issue and other classes of relatives of intestate

5(1)(c) where the property held on the statutory trusts for the issue is divisible into shares, then any money or property which, by way of advancement or on the marriage of a child of the intestate, has been paid to such child by the intestate or settled by the intestate for the benefit of such child … shall, subject to any contrary intention expressed or appearing from the circumstances of the case, be taken as being so paid or settled in or towards satisfaction of the share of such child or the share which each child would have taken if living at the death of the intestate, and shall be brought into account…

AYCHT 27/7/2019

37

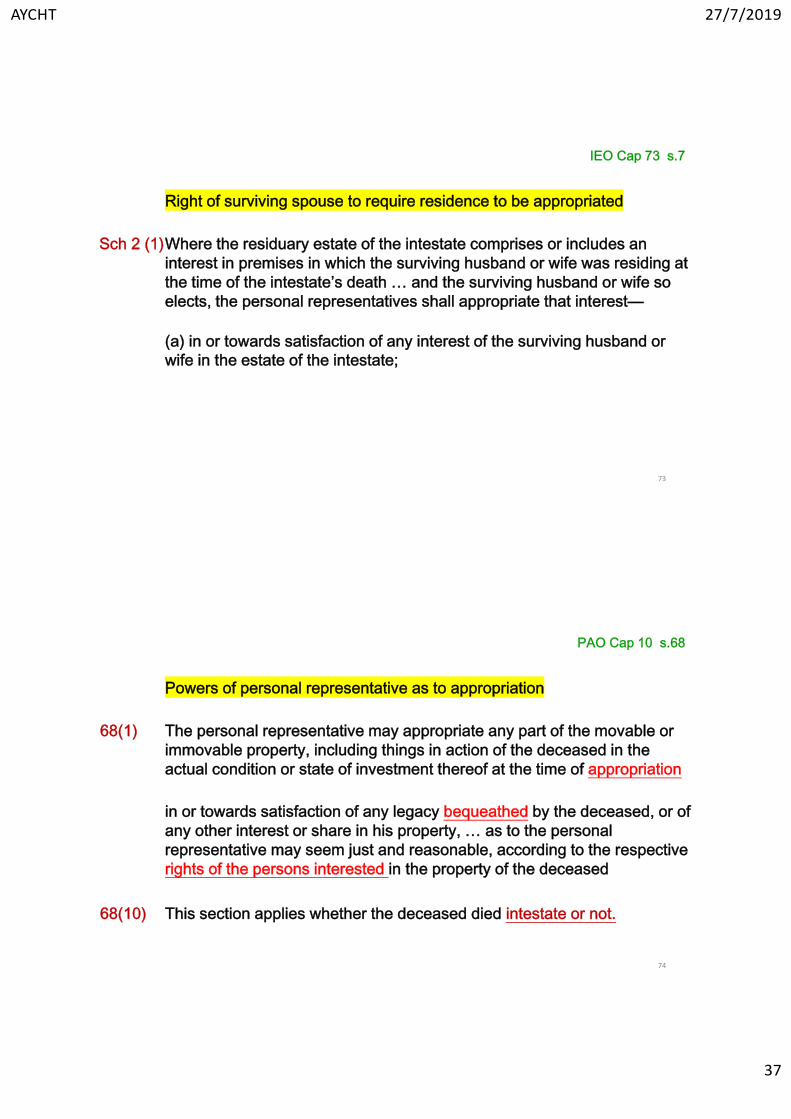

IEO Cap 73 s.7

73

Right of surviving spouse to require residence to be appropriated

Sch 2 (1)Where the residuary estate of the intestate comprises or includes an interest in premises in which the surviving husband or wife was residing at the time of the intestate’s death … and the surviving husband or wife so elects, the personal representatives shall appropriate that interest—

(a) in or towards satisfaction of any interest of the surviving husband or wife in the estate of the intestate;

PAO Cap 10 s.68

74

Powers of personal representative as to appropriation

68(1) The personal representative may appropriate any part of the movable or immovable property, including things in action of the deceased in the actual condition or state of investment thereof at the time of appropriation

in or towards satisfaction of any legacy bequeathed by the deceased, or of any other interest or share in his property, … as to the personal representative may seem just and reasonable, according to the respective rights of the persons interested in the property of the deceased

68(10) This section applies whether the deceased died intestate or not.

AYCHT 27/7/2019

38

75

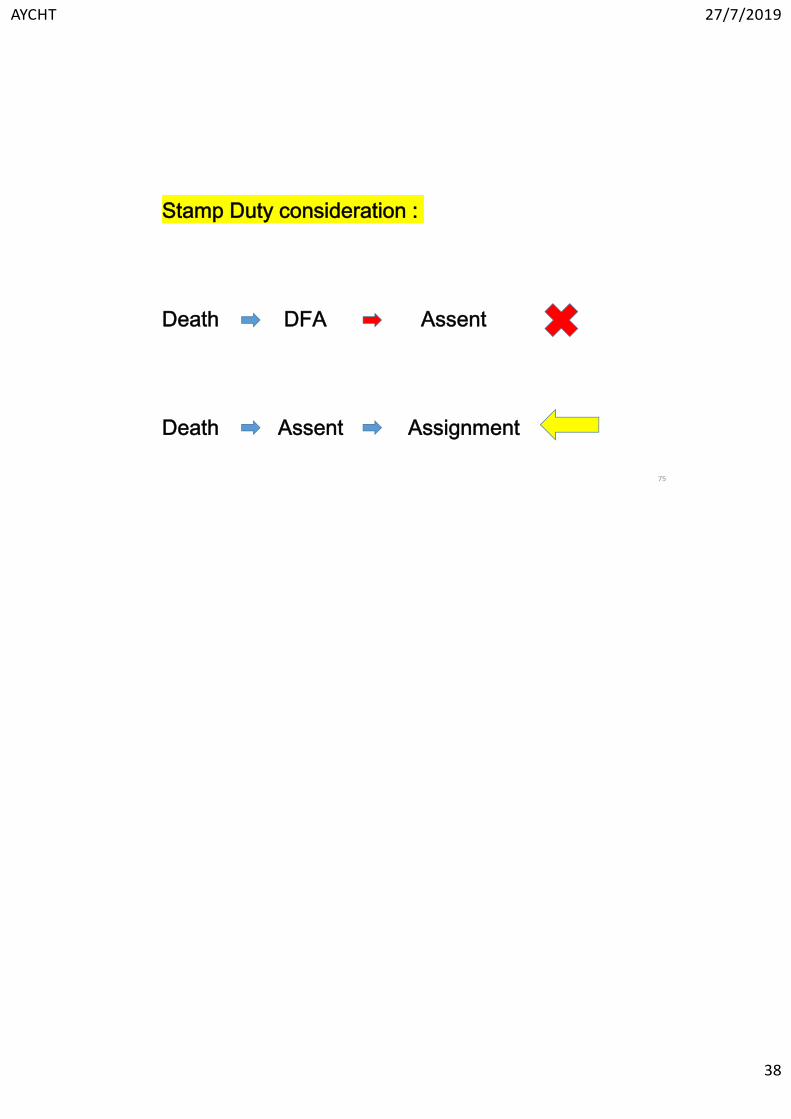

Stamp Duty consideration :

Death DFA Assent

Death Assent Assignment