Embed Size (px)

Citation preview

United States AgriculturalExport Yearbook

2020

Foreign Agricultural ServiceU.S. DEPARTMENT OF AGRICULTURE

The 2020 U.S. Agricultural Export Yearbook provides a statistical summary of U.S. agricultural commodity exports to the world. This summary lists only the United States’ primary trading partners. The Yearbook is produced by the U.S. Department of Agriculture’s (USDA) Foreign Agricultural Service (FAS) using trade data published by the U.S. Census Bureau of the U.S. Department of Commerce. Foreign country export data was sourced from the reporting countries’ national statistical agencies as reported through Trade Data Monitor (TDM).

The 2020 U.S. Agricultural Export Yearbook consists of two sections: (1) top U.S. commodity exports and (2) top destinations for U.S. exports. The Yearbook utilizes FAS Product Groups that can be found at FAS’ Global Agricultural Trade System (GATS) located at https://apps.fas.usda.gov/gats/. The product groups are defined using the Harmonized Tariff Schedule (HTS) at the 10-digit level and aggregated into classifications that include the primary commodity and its derivatives. FAS has titled these product groups as “BICO (HS-10).” BICO is an FAS designation that stands for Bulk, Intermediate & Consumer Oriented goods. The bulk commodity groups, such as corn, wheat, and rice, are aggregations of very few HTS codes. For example, the soybeans product group includes only 2 HTS codes; and cotton includes only 5 codes; while the Beef and Beef Product category incorporates 26 HTS lines; Dairy Products includes 46 HTS lines; and Fresh Vegetables includes 70 HTS codes.

The 16 product groups or commodity aggregations, displayed in the Yearbook, are based on the United States’ largest export categories. Ethanol is not considered an agricultural product according to the USDA definition of agriculture, and its export value is not included in the total value of U.S. agricultural exports ($145.7 billion).1 However, a Yearbook page on ethanol has been included in this publication because of the large value of its exports and its importance to the agricultural community and rural America. The top 15 export product groups (not including ethanol) accounts for nearly 72 percent of total U.S. agricultural products exported in 2020.

The country Yearbook pages include the United States’ top 15 export destinations as well as a page for the United Kingdom (UK). The European Union (EU27+UK), a customs union comprised of 28 member states, is included as a single trading partner. The only exception is that the UK has its own yearbook page given the importance of its withdrawal from the EU-28. The top 14 export markets represent 80 percent of total U.S. agricultural exports in 2020.

Questions or comments about The 2020 U.S. Agricultural Export Yearbook can be directed to USDA’s Foreign Agricultural Service ([email protected]) (202-720-1335).

1 The USDA changed its definition of “agricultural products” in March 2021 to conform to World Trade Organization standards. The new definition includes ethanol.

INTRODUCTION

Commodities

Overview ............................................................................................................................ 1 Beef & Beef Products .................................................................................................... 3 Corn ...................................................................................................................................... 5Cotton .................................................................................................................................. 7Dairy Products ................................................................................................................. 9 Ethanol ............................................................................................................................. 12Fresh Fruits & Vegetables ......................................................................................... 15Pork & Pork Products ................................................................................................. 17Poultry Meat & Products .......................................................................................... 20Prepared Food ............................................................................................................... 23Rice .................................................................................................................................... 25Soybeans .......................................................................................................................... 27Tree Nuts ......................................................................................................................... 29Wheat ............................................................................................................................... 32

Countries

Overview ......................................................................................................................... 34Canada .............................................................................................................................. 36China ................................................................................................................................. 39Colombia .......................................................................................................................... 41Egypt ................................................................................................................................. 44EU27+UK ........................................................................................................................ 47Hong Kong ...................................................................................................................... 50Indonesia ......................................................................................................................... 52Japan ................................................................................................................................. 54Mexico .............................................................................................................................. 56Philippines ....................................................................................................................... 59South Korea .................................................................................................................... 61Taiwan ............................................................................................................................... 63Thailand............................................................................................................................ 65United Kingdom ............................................................................................................ 68Vietnam ............................................................................................................................ 71

TABLE OF CONTENTS

Commodity 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Soybeans 22,839 21,456 17,058 18,663 25,683 38% 21,140

Corn 9,879 9,131 12,462 7,651 9,210 20% 9,667

Tree Nuts 7,902 8,479 8,515 9,076 8,402 -7% 8,475

Pork & Pork Products 5,936 6,485 6,403 6,952 7,715 11% 6,698

Beef & Beef Products 6,360 7,263 8,357 8,094 7,649 -6% 7,545

Prepared Food 6,118 5,938 6,245 6,731 6,733 -- 6,353

Dairy Products 4,698 5,377 5,493 5,924 6,453 9% 5,589

Wheat 5,346 6,058 5,387 6,232 6,298 1% 5,864

Cotton 3,967 5,845 6,562 6,148 5,976 -3% 5,700

Soybean Meal 4,073 3,881 5,073 4,365 4,758 9% 4,430

Fresh Fruit 4,564 4,752 4,676 4,384 4,325 -1% 4,540

Poultry Meat & Products 3,879 4,267 4,274 4,243 4,244 -- 4,181

Fresh Vegetables 2,446 2,513 2,577 2,672 2,564 -4% 2,554

Processed Vegetables 2,695 2,691 2,613 2,703 2,376 -12% 2,616

Ethanol (non-beverage) 2,042 2,412 2,663 2,349 2,333 -1% 2,360

Rice 1,784 1,709 1,678 1,850 1,877 1% 1,780

All Others 42,190 42,338 42,173 40,962 41,419 1% 41,816

Total exported 134,678 138,183 139,544 136,650 145,683 7% 138,948

Overview

Total U.S. agricultural exports in 2020 were nearly $146 billion, up almost 7 percent from 2019, and the second highest level on record (after Calendar Year 2014). The primary factor for this surge in exports was increased shipments of soybeans, corn, and pork to China.

Soybeans continued to be the United States’ No.1 agricultural export, increasing 38 percent to a record $25.7 billion in 2020 and accounting for nearly 18 percent of total U.S. agricultural exports. In 2020, soybean shipments to China accounted for 55 percent of total soybean exports, returning to levels prior to China’s imposition of

Top U.S. Agricultural Exports* (Values in millions of dollars)

EXPORT OVERVIEW

Source: U.S. Census Bureau Trade Data - BICO HS-10*Ethanol is not counted as an agricultural good in the USDA definition of agriculture

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 1

Section 232 and 301 retaliatory tariffs, when China accounted for at least 50 percent of total bean export value since 2009.

Corn exports to the world rose 20 percent to $9.2 billion, led primarily by a $1.1 billion increase in sales to China. Increased competitiveness due to production shortages in Argentina and Ukraine contributed to this sharp increase. Mexico and Japan continued to be the top two markets for U.S. exports, while high domestic prices in China led to the largest value of U.S. exports to China since 2013.

Pork exports was the other major contributor in 2020, rising by 11 percent. This rise was led by a 75- percent increase in exports to China and a 7-percent increase to Japan, the No. 2 market. Exports to China were buoyed by increased demand for imports following significant reduction of the Chinese herd due to African swine fever (ASF).

While tree nut exports to the world were down 7 percent in 2020 due to lower sales to Hong Kong and the EU, they remained the No. 3 export commodity for U.S. farmers and ranchers. Exports of processed vegetables fell by $326 million in 2020. Sixty-seven percent of this decline is attributable to lower exports of french fries, as the quick-service restaurant industry lost customers around the world due to stay-at-home edicts.

Other notable developments in 2020 included a 3-percent decrease in cotton exports to $6 billion, as sales were hit hard during the second quarter due to a reduction in demand and mill use arising from the coronavirus (COVID-19) pandemic. Overall bulk commodity exports increased $9.5 billion (22 percent) with sorghum performing well with a 160-percent ($837 million) leap from the previous year. Dairy product exports were up $529 million (9 percent) from a year ago, led by strong performance of skim milk powder to Southeast Asia. Total livestock, poultry, and dairy exports were up $765 million, a 2-percent increase from last year, as lower beef, hides & skins, and poultry exports partially offset the gains in pork and dairy.

Outlook

The year 2021 is a difficult year to forecast in terms of agricultural trade. While global economic growth is expected following the COVID-induced recession of 2020, the speed of recovery is uncertain due to differences in how individual countries will manage economic response and recovery.

The United States starts the year in a solid position with high global commodity prices and reduced competition for several major commodities, most notably soybeans from Brazil and corn from Ukraine. Strong demand from China is expected to continue to drive U.S. corn and soybean exports. China is expected to remain the top U.S. export destination as the post-ASF recovery of the swine heard will continue to require large volumes of soy and corn imports. China’s continued implementation of the U.S-China Phase One Agreement should also contribute to strong overall demand for U.S. goods throughout the year.

The United States expects an increase in exports from recently signed and upgraded trade agreements with Canada, Mexico, and Japan.

2 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Japan 1,510 1,889 2,102 1,950 1,944 0% 1,879

South Korea 1,071 1,220 1,746 1,843 1,722 -7% 1,520

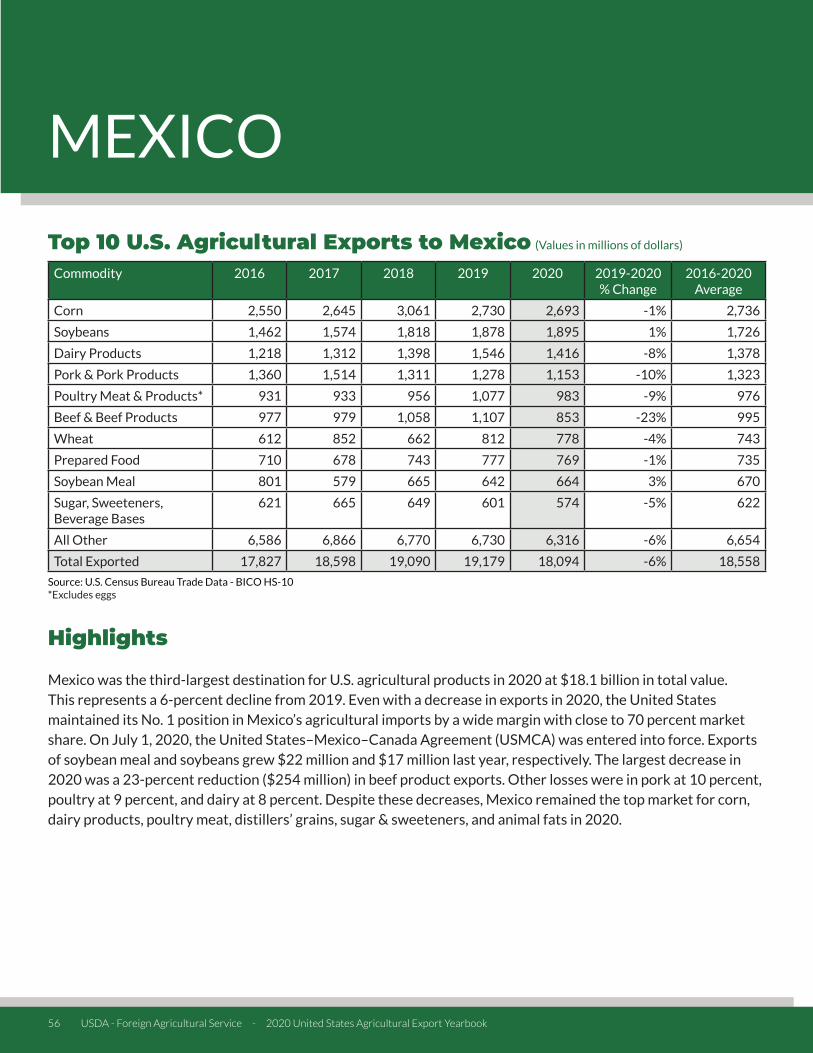

Mexico 977 979 1,058 1,107 853 -23% 995

Canada 758 791 745 654 728 11% 735

Hong Kong 684 884 964 746 666 -11% 789

Taiwan 363 409 552 568 552 -3% 489

China 4 31 61 86 310 260% 98

EU27+UK 247 252 231 193 153 -21% 215

Indonesia 39 54 62 85 72 -16% 62

Philippines 55 62 87 88 62 -29% 71

All Others 579 660 760 736 694 -6% 686

Total Exported 6,360 7,263 8,357 8,095 7,649 -6% 7,545

Highlights

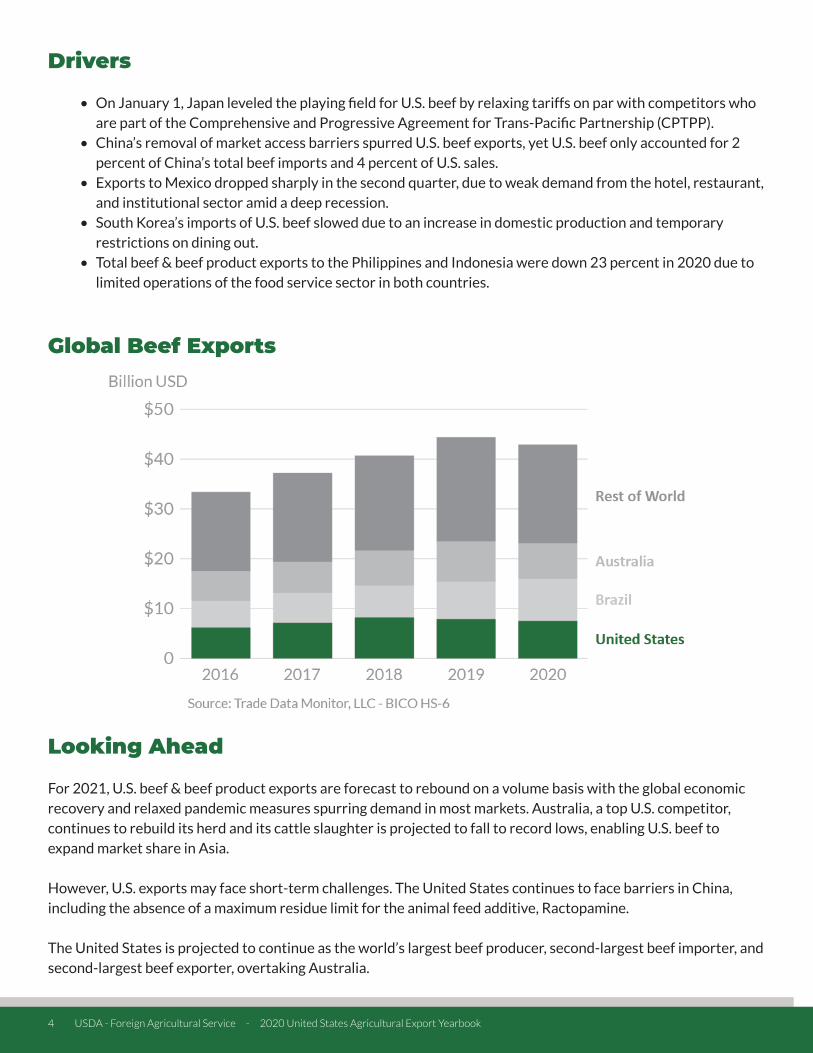

In 2020, the value of U.S. beef & beef product exports contracted 5.5 percent year-over-year, largely due to supply chain constraints and foodservice struggles in the wake of the COVID-19 pandemic. Japan at $1.9 billion, South Korea at $1.7 billion, and Mexico at $853 million accounted for 59 percent of total U.S. sales. Mexico’s beef imports from the United States decreased due to its economic slowdown and an unfavorable exchange rate relative to the U.S. dollar. U.S. exports to Japan, the No. 1 market, remained flat from the previous year. The effects of additional exports to Japan early in 2020 were negated by a drastic decline in the second quarter after COVID-19 became more widespread. Exports of U.S. beef to China increased due to China’s removal of market access barriers pursuant to the Phase One Agreement and strong meat demand in China due to reduced domestic pork supplies. Overall, exports accounted for 11 percent of U.S. domestic production. The United States was the world’s largest beef producer, second-largest importer, and third-largest exporter by volume.

Top 10 Export Markets for U.S. Beef (Values in millions of dollars)

BEEF & BEEF PRODUCTS

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 3

Drivers

• On January 1, Japan leveled the playing field for U.S. beef by relaxing tariffs on par with competitors who are part of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP).

• China’s removal of market access barriers spurred U.S. beef exports, yet U.S. beef only accounted for 2 percent of China’s total beef imports and 4 percent of U.S. sales.

• Exports to Mexico dropped sharply in the second quarter, due to weak demand from the hotel, restaurant, and institutional sector amid a deep recession.

• South Korea’s imports of U.S. beef slowed due to an increase in domestic production and temporary restrictions on dining out.

• Total beef & beef product exports to the Philippines and Indonesia were down 23 percent in 2020 due to limited operations of the food service sector in both countries.

Global Beef Exports

Looking Ahead

For 2021, U.S. beef & beef product exports are forecast to rebound on a volume basis with the global economic recovery and relaxed pandemic measures spurring demand in most markets. Australia, a top U.S. competitor, continues to rebuild its herd and its cattle slaughter is projected to fall to record lows, enabling U.S. beef to expand market share in Asia.

However, U.S. exports may face short-term challenges. The United States continues to face barriers in China, including the absence of a maximum residue limit for the animal feed additive, Ractopamine.

The United States is projected to continue as the world’s largest beef producer, second-largest beef importer, and second-largest beef exporter, overtaking Australia.

4 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Mexico 2,550 2,646 3,061 2,730 2,693 -1% 2,736

Japan 2,091 2,163 2,813 2,001 1,846 -8% 2,183

China 40 142 50 56 1,205 2072% 299

Colombia 771 785 927 683 876 28% 808

South Korea 865 705 1,356 359 548 53% 766

Canada 147 131 309 349 272 -22% 241

Guatemala 174 145 196 177 219 23% 182

Taiwan 460 395 593 228 179 -22% 371

Costa Rica 115 138 143 145 151 4% 138

Saudi Arabia 343 266 297 110 151 37% 233

All Others 2,324 1,615 2,718 814 1,072 32% 1709

Total Exported 9,879 9,131 12,462 7,651 9,210 20% 9,667

Highlights

U.S. corn exports were up $1.6 billion (20 percent) from a year ago to $9.2 billion in 2020. Strong feed demand in China contributed to this sharp increase, as did China’s implementation of the Phase One Agreement. Exports to China totaled $1.2 billion, the largest since 2012. China became the third largest destination for U.S. corn in 2020 after Mexico and Japan. The top three markets accounted for 62 percent of total U.S. corn exports. The sum total of U.S. corn exports to Colombia, South Korea, and Guatemala, three U.S. free trade partners, was up $424 million over 2019.

Drivers

• Exports to China were strong during the latter half of 2020 and ultimately exceeded the Phase One quota for 2020, as the recovery in China’s swine sector from the outbreaks of African swine fever (ASF) fueled demand for competitively priced feedstuffs.

Top 10 Export Markets for U.S. Corn (Values in millions of dollars)

CORN

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 5

• U.S. prices were competitive in global markets supported by abundant exportable supplies and weak domestic demand in the fuel ethanol sector amidst COVID-19.

• The depreciation of the U.S. dollar against a basket of currencies also boosted the competitiveness of U.S. corn overseas.

Global Corn Exports

Looking Ahead

U.S. corn is expected to remain competitive, with ample supplies and reduced competition from Ukraine, Argentina, and Brazil. Ukraine’s exports are forecast to be smaller (-17 percent) than the previous year due to a smaller crop. Corn prices in the South American countries remain elevated, reflecting tight stocks and strong domestic feed demand for animal production and meat exports. Moreover, Brazil’s corn is expected to come onto the market later than usual due to slow planting in the Center-West impacted by delays in the soybean harvest.

U.S. corn exports to China are expected to be stronger. At the end of January 2021, sales to China for delivery in 2021 stood at a record 11.6 million tons. China’s demand for competitively priced feedstuff should remain strong as its swine sector continues to rebound from ASF. High corn prices in China, which were nearly double those of U.S. corn at the end of January, are also expected to stimulate demand for imports.

With reduced competition, U.S. corn is expected to expand its market share in traditional markets in Asia and the Western Hemisphere, while rebuilding market share to countries in North Africa. In fact, U.S. sales and shipments to North African countries are off to a good start. At the end of January 2021, they totaled 750,000 tons compared to none a year ago.

6 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

China 551 973 920 705 1,821 158% 994

Vietnam 788 1,056 1,312 1,429 1,163 -19% 1,150

Pakistan 202 297 615 628 788 25% 506

Turkey 495 730 682 648 577 -11% 626

Bangladesh 95 284 387 388 330 -15% 297

Indonesia 346 498 600 416 264 -37% 425

Mexico 339 404 372 288 178 -38% 316

India 251 435 333 587 148 -75% 351

Thailand 164 213 272 215 119 -44% 197

South Korea 165 248 231 167 111 -34% 184

All Others 564 689 826 671 470 -30% 644

Total Exported 3,959 5,827 6,550 6,141 5,968 -3% 5,689

Highlights

U.S. exports of cotton declined 3 percent in 2020 to $6 billion but remained the fifth-highest export value on record. Exports to China surged by more than 150 percent to reach a 7-year high. Exports to Pakistan realized their fifth consecutive record. Exports to other markets were largely down, with 15 of the top 20 markets down by more than 30 percent. Much of the increase to China was destined for the State Reserve (SR), which limited supplies available for other markets. Brazil, which saw its third consecutive record crop, increased its market share relative to the United States in 20 of the top 25 import markets.

Global consumption in 2020 was dramatically affected by COVID-19 as consumer demand shrank and mill use fell by nearly 20 percent. Trade volume was reduced by nearly 10 percent. World and U.S. prices fell sharply in the first quarter of 2020 due to concerns over the impact of COVID-19 and large global stocks. However, prices rallied mid-year, supported by increasing prices for other commodities, and ended the year at a 2-year high.

Top 10 Export Markets for U.S. Cotton (Values in millions of dollars)

COTTON

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 7

Drivers

• Global impact of COVID-19 sharply decreased demand for cotton/textiles.• China State Reserve purchases of U.S. cotton limited availability of high-grade cotton to other markets.• Increased competition dampened U.S. exports as Brazil expanded export capacity and shipped record

volumes year-round, including during typically slow export months.

Global Cotton Exports

Looking Ahead

U.S. cotton exports are forecast unchanged at 15.5 million bales for the marketing year ending July 2022. Global trade volume is also expected stable.

SR purchases of U.S. cotton fueled shipments to China, and these types of purchases in 2021 are expected to shift back to domestic cotton, limiting U.S. sales.

Strong competition from key competitors such as Brazil is also expected to dampen U.S. exports. Brazil’s projected crop in the coming months is only down slightly from last year’s third consecutive record crop.

8 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Mexico 1,218 1,312 1,398 1,546 1,416 -8% 1,378

Canada 630 637 641 667 676 1% 650

China 386 576 498 373 539 45% 474

Philippines 227 243 246 273 410 50% 280

South Korea 231 279 290 330 371 12% 300

Indonesia 158 132 165 239 352 47% 209

Japan 206 291 269 282 322 14% 274

Vietnam 120 112 145 170 185 9% 146

Australia 109 185 153 148 170 15% 153

Malaysia 87 90 101 109 157 45% 109

All Others 1,327 1,520 1,586 1,788 1,856 4% 1,615

Total Exported 4,698 5,377 5,493 5,924 6,453 9% 5,589

Highlights

U.S. dairy product exports grew by 9 percent to reach $6.5 billion in 2020 despite significant challenges posed by the COVID-19 pandemic and ongoing trade policy issues with Canada and China. While still below the record level in 2014, this was the fourth year in a row that the value of U.S. dairy product exports expanded, registering an average annual growth rate of 8 percent over this period.

Mexico, Canada, and China were the top three markets, accounting for about 45 percent of sales. Sales to Mexico were down 8 percent due to the COVID-19 pandemic leading to slower economic growth and reduced consumer spending. Southeast Asia remains a critical region for growth, with the value of dairy shipments up an impressive 25 percent from 2019 to reach $2.7 billion. There were notable increases in exports of whey & whey products to China, and skimmed milk powder (SMP) to the Philippines and Indonesia.

Top 10 Export Markets for U.S. Dairy (Values in millions of dollars)

DAIRY PRODUCTS

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 9

Drivers

• China started to rebuild its pig herd and demand for pig feeds led to growth in imports of U.S. whey & whey products.

• Global demand for dairy products was surprisingly strong in 2020 while the availability of exportable stocks was lower than in 2019. This was particularly true for SMP as EU27+UK surplus intervention stocks were completely drawn down. As a result, U.S. exporters made strong gains in Asian markets, particularly Indonesia and the Philippines.

• The low value of the U.S. dollar plus the availability of ample stocks meant that U.S. dairy products were competitive on major global markets.

• Mexican imports of U.S. dairy products declined due to a deteriorating macroeconomic situation resulting from low oil prices, a deep recession, a weak currency, and COVID-19 pandemic measures.

Global Dairy Exports

Looking Ahead

Despite ongoing trade policy challenges, the outlook for U.S. dairy exports in 2021 is positive. The global economy is expected to improve, and import demand is expected to remain robust. U.S. milk production is forecast to grow by nearly 2 percent while milk output from competitors, including New Zealand and the EU27+UK, is expected to be more moderate, growing by less than 1 percent. Early in 2021, international prices for several key dairy products are rising, underscoring some tightness in exportable supplies among competitors. The U.S. dairy industry is well positioned with competitive prices and ample exportable supplies of key products including milk powder, cheese, butter, and whey & whey products.

10 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Most of the growth in U.S. exports is expected to be in Mexico and Asia where import demand for dairy products is being driven by higher per capita incomes and an expanding middle class. In China, there is the additional factor of rebuilding the swine herd which already boosted imports of U.S. whey & whey products in late 2020. For the year, U.S. exports of dairy products on a fat-basis are forecasted to grow by 8 percent, primarily due to higher volumes of butter. On a skim-solid milk equivalent basis, exports are forecasted to grow by 3 percent due to increased shipments of SMP and whey & whey products. On a skimmed milk equivalent basis, this will mean that approximately 22 percent of U.S. milk production will be exported.

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 11

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Canada 593 621 590 573 594 4% 594

Brazil 458 736 761 493 317 -36% 553

India 176 281 258 298 312 4% 265

EU27+UK 21 101 167 185 288 56% 152

South Korea 71 91 134 196 172 -12% 133

Colombia 10 56 76 116 121 4% 76

Mexico 58 56 51 52 119 128% 67

Peru 76 72 69 79 69 -13% 73

Philippines 103 101 125 94 67 -29% 98

Nigeria 34 45 33 33 58 74% 41

All Others 442 251 400 229 217 -5% 308

Total Exported 2,042 2,412 2,663 2,349 2,333 -1% 2,360

Highlights

In 2020, U.S. ethanol exports totaled 1.3 billion gallons valued at $2.3 billion. This volume was 9 percent lower than 2019 due to reduced demand for fuel use, and 20 percent below the record 1.7 billion gallons shipped in 2018. Year-over-year value fell only 1 percent due to higher prices for fuel ethanol and increased shipments of higher-value, medical-grade ethanol.

U.S. fuel ethanol to Brazil saw the largest absolute decline in 2020, due to Brazil’s COVID-19 impacted fuel market and a 40-percent depreciation in Brazil’s currency. Brazil’s 20 percent import duty continued to impact the market. Export volumes were also lower than expected to other fuel markets in 2020, most notably the Philippines, Colombia, and Peru. Sales to Canada held mostly steady as U.S. suppliers backfilled Canada’s increased sales to Europe. By contrast, U.S. fuel ethanol sales to mainland China rose from zero to 21.2 million gallons. Sales to Hong Kong added 10.5 million gallons.

Top 10 Export Markets for U.S. Ethanol (Values in millions of dollars)

ETHANOL

Source: U.S. Census Bureau Trade Data - BICO HS-10

12 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Differing from fuel ethanol markets and driven by demand for hand sanitizer, U.S. exports of other industrial and consumer ethanol rose, most notably to Mexico (up $67 million) and Nigeria (up $25 million). For the remaining top 10 markets, ethanol sales rose to the EU27+UK on strong demand for hand sanitizer and high local fuel ethanol prices, industrial ethanol sales to India inched higher to a record $312 million, and industrial ethanol sales to South Korea dropped as China covered South Korea’s demand for medical-grade product.

Drivers

• Regulations, limited infrastructure, and oil company resistance limit growth of ethanol blends above 10 percent in the U.S. market, thus raising the importance of export growth. Limited growth for higher blends and mostly static fuel demand also limit U.S. domestic market expansion.

• U.S. ethanol exports are mostly impacted by fuel markets since most is used as transport fuel. Sales are also impacted by markets for ethanol used as an industrial chemical and in consumer products, including hand sanitizers, with 20-25 percent of U.S. exports typically used for these non-fuel applications.

• In 2020, COVID-19 and reduced mobility severely impacted global gasoline markets and thus fuel ethanol demand. The impact on U.S. ethanol exports was sharp and swift with lower sales of fuel ethanol from March onward supporting a rise in the non-fuel portion of U.S. exports to an unprecedented 40 percent.

• Canada and Brazil remain the top markets for U.S. ethanol. Canada’s fuel ethanol imports are stable with no trade restrictions on U.S. suppliers who consistently cover about 40 percent of Canada’s consumption. U.S. suppliers also cover virtually all of Brazil’s fuel ethanol imports, but trade is impacted by several factors including sugar and oil prices and a volatile exchange rate.

• The United States has free trade agreements with four of the top 10 ethanol export destinations, which help reduce barriers to U.S. ethanol.

Global Ethanol Exports

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 13

Looking Ahead

As the spread of COVID-19 slows and vaccines are distributed in 2021, global demand for gasoline and ethanol will start recovering. Beyond 2021, with the world emerging from the pandemic, gasoline and ethanol markets will further recover, although the pace and degree will vary by country.

Pre-pandemic, the United States supplied half of the world’s ethanol exports, but its market share dropped to an estimated 43 percent in 2020 as fuel demand collapsed and some countries (notably China and Brazil) captured more of the trade in medical-grade product. Markets should mostly rebalance in the coming 1-2 years, permitting U.S. market share to rise as the pandemic recedes and fuel ethanol reasserts its dominance in trade.

Demand for mobility grows as population and incomes grow, but ethanol-blended gasoline is only one of several means to meeting increased demand for mobility while lowering greenhouse gas emissions. Increased mass transit, improved fuel efficiency, lifestyle changes including telework, and alternative drive trains like electric motors are all factors affecting transport demand, with which ethanol must compete. Antidumping and countervailing duties placed by China, Brazil, the EU27+UK, and others, and licensing restrictions or import bans imposed by Argentina, Thailand, India, and the Philippines, all limit (or threaten to limit) the United States’ ability to export fuel ethanol, while markets for ethanol used as an industrial chemical and in consumer products are relatively barrier-free.

14 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Canada 3,440 3,487 3,487 3,471 3,471 0% 3,471

Mexico 602 704 760 803 772 -4% 728

South Korea 401 508 512 419 480 15% 464

Japan 481 413 427 401 373 -7% 419

Taiwan 317 292 278 323 263 -19% 295

EU27+UK 234 246 247 216 199 -8% 228

Hong Kong 292 302 248 205 190 -7% 247

Vietnam 67 72 103 140 138 -1% 104

China 188 226 177 119 112 -6% 164

Australia 117 118 118 112 104 -7% 114

All Others 869 896 965 848 788 -7% 873

Total Exported 7,010 7,265 7,252 7,056 6,889 -2% 7,094

Highlights

In 2020, the value of U.S. fresh fruit and vegetable exports to the world reached $6.9 billion, a 2- percent decline from the prior year. Due to geographic proximity and climate, Canada remained the top U.S. market, accounting for 49 percent of total exports, or $3.5 billion. Mexico came in a distant second with 10 percent of U.S. exports while no other markets had more than 7 percent share of exports.

U.S. apple exports experienced the greatest drop, down $105 million from 2019 and accounting for more than half of the overall decline, with the largest losses in Taiwan, India, and Canada. U.S. orange exports had the largest growth, up $48 million on higher exports to South Korea and Canada. Fruit and vegetable exports to China declined for the third year in a row. However, South Korea saw a significant gain of $61 million. Apples, pears, peaches, citrus, table grapes, and cherries continue to make up nearly half of total U.S. fresh fruit and vegetable exports.

Top 10 Export Markets for U.S. Fresh Fruits and Vegetables (Values in millions of dollars)

FRESH FRUITS & VEGETABLES

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 15

Drivers

• Top fresh fruit export commodities included apples, grapes, oranges, and cherries, which accounted for a combined $2.6 billion, with top markets including Canada, Mexico, Japan, South Korea, and Taiwan.

• Top fresh vegetable export commodities included lettuce, potatoes, sweet potatoes, onions, and cauliflower, which accounted for a combined $1.2 billion, with top markets including Canada, the EU27+UK, and Mexico.

• India imposed an additional 20 percent tariff on U.S. apples in June 2019, bringing the total tariff rate to 70 percent.

• Regulatory requirements, including pesticide maximum residue levels (MRLs) on U.S. fruits and vegetables that differ from those of the United States, continued to challenge exporters selling to the EU27+UK and South Korea. The United States continues to adopt science-based standards.

Global Fresh Fruit and Vegetable Exports

Looking Ahead

U.S. apple production is forecast to decline due to weather-damaged crops in Washington and Michigan. Reduced supplies are expected to pressure exports lower. U.S. table grape production is forecast up more than 100,000 tons to 1 million. Despite good quality supplies, lower demand from Mexico is expected to reduce exports. U.S. orange production is forecast down more than 10 percent with production in Florida forecast to drop 20 percent due to above average droppage. Exports are forecast to be down with the drop in production. Cherry exports are projected to decline for the third straight year, reflecting lower supplies but also China’s retaliatory Section 232 tariffs. New growth markets for fresh fruit and vegetables include the Dominican Republic, Kuwait, and Peru. During the last 10 years, the growth rate for fresh vegetables has been trending up on the strength of shipments to Canada, the EU27+UK, and Mexico, while fresh fruit exports continue to decline from their 2013 peak, primarily due to lower table grape, apple, and orange shipments.

16 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

China 713 662 571 1,300 2,280 75% 1,105

Japan 1,553 1,626 1,631 1,523 1,626 7% 1,592

Mexico 1,360 1,514 1,311 1,278 1,153 -10% 1,323

Canada 798 793 765 802 853 6% 802

South Korea 364 475 670 593 453 -24% 511

Australia 178 208 227 302 253 -16% 234

Colombia 105 163 215 222 147 -34% 170

Chile 54 85 91 123 136 11% 97

Philippines 79 98 116 93 115 23% 100

Hong Kong 360 415 282 154 91 -41% 260

All Others 373 446 524 562 608 8% 503

Total Exported 5,936 6,485 6,403 6,952 7,715 11% 6,698

Highlights

In 2020, the value of U.S. pork & pork product exports to the world reached a record $7.7 billion, up 11 percent from the prior year. The top three markets, accounting for 66 percent of exports, were China at $2.3 billion, Japan at $1.6 billion, and Mexico at $1.2 billion. China overtook Japan as the top market for U.S. pork as African swine fever (ASF) continued to limit China’s domestic pork supplies and buoy demand for imports. However, exports to Japan also rebounded with implementation of lower tariffs under the U.S.-Japan Trade Agreement and major U.S. competitors increasingly focused on the Chinese market. Meanwhile, U.S. exports to Mexico struggled in 2020 as a depreciating peso and weak economy stifled import demand.

Drivers

• China became the largest market for U.S. pork in 2020, generating an additional $1 billion in exports over the previous year, due to decreased Chinese production resulting from ASF.

Top 10 Export Markets for U.S. Pork (Values in millions of dollars)

PORK & PORK PRODUCTS

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 17

• Exports to Japan increased $100 million as the tariffs faced by U.S. pork were reduced as part of the U.S.-Japan Trade Agreement.

• Import demand in the Philippines and Vietnam rose as those countries attempt to manage ASF outbreaks, leading to an additional $60 million in U.S. exports.

• A weak Hotel, Restaurant, and Institutional sector in South Korea depressed U.S. exports to that market by $140 million in 2020.

• A difficult economic environment and devalued peso limited Mexican buying power and led U.S. exports to decline by more than $100 million.

• Exports of pork to Colombia dropped 34 percent in 2020 because of strict COVID-19 lockdowns that lowered demand in the food service sector.

• Decreased transshipment of products to China is primarily responsible for a $63 million reduction in pork exports to Hong Kong last year.

Global Pork Exports

Looking Ahead

While Chinese pork prices remain high and import demand will continue to be considerably higher than the pre-ASF era, China imports are expected to contract year-over-year as their hog sector recovers. Increased competition in the Chinese market will cause U.S. pork export volumes to ease from the 2020 record. Lower exports to China will be partially offset as improving economic conditions promote growth in traditional markets such as Mexico and South Korea. Additionally, the Philippines and Vietnam are poised for robust import demand as these countries continue to rebound from ASF.

18 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

In addition to impacting global import demand, ASF has the potential to reshuffle global trade flows as major exporters cope with the disease. Towards the end of 2020, the discovery of ASF in Germany in feral swine effectively restricted German pork exports to key Asian markets. Ultimately, the ability to shift supply chains on the continent, with other member states picking up the slack, prevented total EU27+UK exports from severe impacts.

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 19

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Mexico 932 933 956 1,077 983 -9% 976

China 34 36 47 10 762 7277% 178

Canada 510 459 405 354 349 -1% 416

Taiwan 127 152 189 187 224 20% 176

Cuba 105 165 155 190 144 -25% 152

Vietnam 79 76 110 140 128 -9% 107

Guatemala 104 118 123 132 111 -15% 118

Hong Kong 426 469 431 353 107 -70% 357

Colombia 66 70 82 114 93 -18% 85

Angola 86 156 184 150 82 -45% 131

All Others 1,411 1,632 1,590 1,536 1,261 -10% 1,486

Total Exported 3,879 4,267 4,274 4,243 4,244 0% 4,181

Highlights

In 2020, the value of U.S. poultry & poultry product exports to the world reached $4.2 billion, unchanged from 2019 and thus failing to return to the pre-2015 highly pathogenic avian influenza (HPAI) outbreak levels. The top three markets, accounting for 49 percent of sales, were Mexico at $983 million, China at $762 million, and Canada at $349 million. The reopening of the Chinese market, the continuation of generally positive trade conditions, and modest growth in global demand as consumers viewed poultry meat as a low-cost animal protein supported sales in 2020. With shipments to many major markets lower in 2020, the key positive development was the reopening of the Chinese market, which buoyed total exports. U.S. exports of poultry & poultry products are primarily comprised of broiler meat (about 74 percent) to mostly developing country markets. Consequently, economic growth and rising incomes in low-and middle-income countries will bode well for growing exports.

Top 10 Export Markets for U.S. Poultry Products* (Values in millions of dollars)

POULTRY MEAT & PRODUCTS

Source: U.S. Census Bureau Trade Data - BICO HS-10 *Excluding eggs

20 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Drivers

• Exports fell to all major markets except for Taiwan and China, the reopening of which was critical to supporting total U.S. shipments. Sixty-one percent ($461 million) of shipments to China were chicken paws, a product for which there is virtually no other significant market. As a result, total exports of U.S. chicken paws reached a historic $958 million in 2020.

• The United States continued to face market access issues in South Korea, South Africa, Indonesia, Saudi Arabia, and India due to non-tariff barriers and purported sanitary issues.

• Strong competition from Brazilian exports has elevated the competitive environment along with shipments from rising poultry suppliers including Turkey, Ukraine, Argentina, and Russia.

• The United States continues to emphasize to the global trading community that the use of risk-based analysis and sound science are the best ways to approach long-standing challenges such as Highly Pathogenic Avian Influenza regionalization and establishment of veterinary drug standards.

Global Poultry Exports

Looking Ahead

The volume of U.S. poultry meat (excluding paws) exports is forecast flat in 2021 and prices are expected to decline which will negatively impact the total value of shipments. Exportable supplies of U.S. poultry meat will be constrained as forecasted higher feed prices will stymie U.S. production, forecast to rise less than 1 percent.

While global poultry meat consumption has been relatively resilient as a low-cost versatile animal protein amid the COVID-19 economic downturn, global economic recovery will yield limited gains in short-term demand. However, the USDA Long-Term Projections reflect a positive outlook and forecast U.S. poultry meat exports to grow nearly 25 percent during the next 10 years.

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 21

The United States is expected to maintain its position as the second-largest exporter of poultry meat behind Brazil, but U.S. market share of global trade will decline slightly. During the coming decade, growing population and rising incomes, particularly in low- and middle-income countries, will spur increased meat consumption, fostering demand for competitively priced chicken meat.

22 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Canada 1,889 1,908 1,931 2,048 2,178 6% 1,991

Mexico 710 678 743 777 769 -1% 735

EU27+UK 579 567 555 551 613 11% 573

South Korea 365 324 355 509 460 -10% 403

China 126 139 183 240 254 6% 188

Japan 233 275 265 233 234 0% 248

Hong Kong 232 169 228 191 186 -3% 201

Taiwan 162 149 154 149 141 -5% 151

Australia 146 136 151 130 131 1% 139

Thailand 125 131 133 137 129 -6% 131

All Others 1,551 1,462 1,547 1,766 1,638 -7% 1,593

Total Exported 6,118 5,938 6,245 6,731 6,733 0% 6,353

Highlights

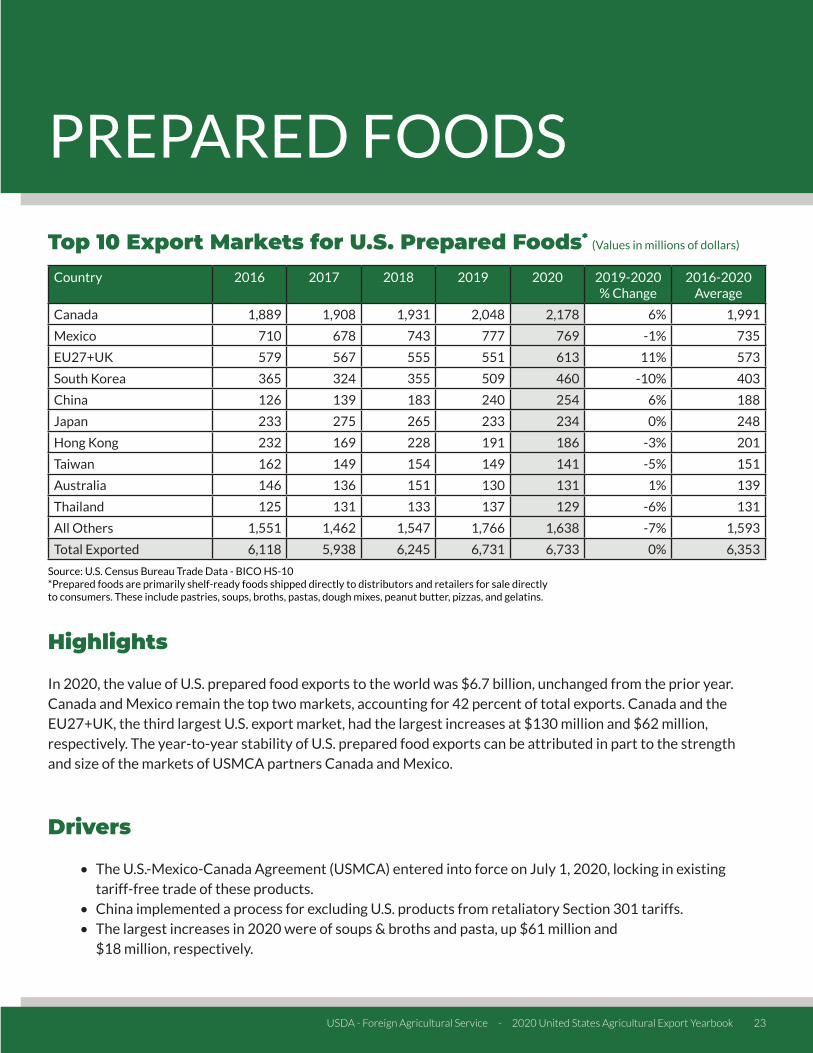

In 2020, the value of U.S. prepared food exports to the world was $6.7 billion, unchanged from the prior year. Canada and Mexico remain the top two markets, accounting for 42 percent of total exports. Canada and the EU27+UK, the third largest U.S. export market, had the largest increases at $130 million and $62 million, respectively. The year-to-year stability of U.S. prepared food exports can be attributed in part to the strength and size of the markets of USMCA partners Canada and Mexico.

Drivers

• The U.S.-Mexico-Canada Agreement (USMCA) entered into force on July 1, 2020, locking in existing tariff-free trade of these products.

• China implemented a process for excluding U.S. products from retaliatory Section 301 tariffs.• The largest increases in 2020 were of soups & broths and pasta, up $61 million and

$18 million, respectively.

Top 10 Export Markets for U.S. Prepared Foods* (Values in millions of dollars)

PREPARED FOODS

Source: U.S. Census Bureau Trade Data - BICO HS-10 *Prepared foods are primarily shelf-ready foods shipped directly to distributors and retailers for sale directly to consumers. These include pastries, soups, broths, pastas, dough mixes, peanut butter, pizzas, and gelatins.

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 23

Looking Ahead

The global trade of prepared foods has nearly doubled in the last decade. Demand is driven in large part by income growth and urbanization, both generally leading to increased consumer desire for convenient, shelf-ready packaged foods. Imported prepared foods provide variety for consumers, and often supply producers in domestic processed food sectors. Asian markets, especially China, have been the fastest growing for prepared foods in recent years, reflecting the effect of income growth on consumption habits. These trends are expected to continue and will likely provide strong markets for U.S. prepared food exports into the future.

However, there are many trade barriers facing prepared foods, including front-of-package labeling (FOPL), marketing and advertising restrictions, and penalties on foods that exceed certain thresholds of nutrients like sugar, fat, saturated fat, and sodium. In October 2020, Mexico implemented its new FOPL warning style labels. U.S. exports of about $3.4 billion are expected to be impacted. Mexico also implemented bans in two states in October, prohibiting the sale of products that carry warning labels to people under the age of 18. A Federal level ban is under consideration, as are proposals for nearly all other states.

In November 2020, Colombia established maximum sodium limits for foods that will be implemented in phases during the next 3 years. Products that exceed these limits will be subject to sanctions. This will impact about $54 million of U.S. exports each year. Latin American countries are expected to consider more regulations for prepared foods in 2021, driven largely by the recommendations of the World Health Organization and Pan-American Health Organization.

The COVID-19 pandemic did not have a significant impact on U.S. exports of prepared foods in 2020, likely because these products are most frequently purchased directly from supermarkets for preparation at home rather than at restaurants. Decreases in global income levels may affect consumer capacity to purchase packaged food, but it is unlikely that this effect will be long term.

In 2020, 63 percent of total U.S. exports of prepared foods were to free trade agreement partner countries. Negotiations with future free trade agreement partners like Kenya provide opportunities to address existing tariff and non-tariff barriers and create a pathway to new customers in regions of the world where income and demand are rising.

24 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Japan 234 190 232 275 261 -5% 238

Mexico 266 292 268 278 245 -12% 270

Haiti 190 237 206 206 245 19% 217

Canada 148 148 175 194 194 0% 172

South Korea 105 85 89 120 162 34% 112

Saudi Arabia 92 88 73 98 105 7% 91

Jordan 73 90 66 73 77 5% 76

Colombia 58 51 54 49 65 33% 55

Honduras 71 45 61 47 45 -4% 54

Brazil 1 0 1 0 38 21172% 8

All Others 546 483 453 510 440 -14% 486

Total Exported 1,784 1,709 1,678 1,850 1,877 2% 1780

Highlights

In 2020, the value of U.S. rice exports to the world was $1.9 billion, up 1.5 percent from the prior year. The top three markets, accounting for 40 percent of exports, were Japan at $261 million, Mexico at $245 million, and Haiti at $245 million. U.S. exports to Mexico declined as South American suppliers expanded market share in that primarily paddy market. Countries where the United States has free trade agreements remained significant markets, particularly in the Western Hemisphere.

Drivers

• U.S. rice export value rose 1.5 percent based on higher unit values, despite lower volumes.• Commercial exports to Haiti expanded, both in terms of volume and unit value.• Exports to Brazil were the highest since 2003, due to Brazil’s tightening supplies prompting

increased imports.

Top 10 Export Markets for U.S. Rice (Values in millions of dollars)

RICE

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 25

• Larger medium grain exports to South Korea more than offset lower exports to Japan.• Exports to Colombia rose with larger paddy rice volumes, benefiting from the free trade agreement with

the United States.• While Mexico remains the top U.S. market, export volumes declined in 2020 amid a smaller U.S. crop in

2019-2020 and increased competition from South America. These factors also led to declining exports to some Central American countries.

Global Rice Exports

Looking Ahead

Looking ahead to 2021, exports are forecast higher despite smaller production forecasts for 2021-2022. Demand for U.S. rice is expected to remain strong in core markets such as Mexico and Haiti. The outlook is favorable for maintaining a strong market presence in countries with free trade agreements such as Colombia, Central America, and the Dominican Republic. Exports for U.S. medium-grain rice, especially to East Asian markets such as Japan and South Korea, are forecast to remain steady. U.S. prices remain high relative to Asian prices, making it challenging to compete in price-sensitive markets including Africa and Southeast Asia. Thai and Vietnamese export prices are expected to decline amid the new harvest, while Indian export prices remain very low in comparison to other suppliers.

26 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

China 14,203 12,224 3,119 8,005 14,159 77% 10,342

EU27+UK 1,899 1,637 3,078 1,953 1,940 -1% 2,101

Mexico 1,462 1,574 1,818 1,878 1,895 1% 1,726

Egypt 100 364 1,164 995 1,475 48% 820

Japan 1,000 973 927 971 1,063 10% 987

Indonesia 988 922 998 864 884 2% 931

Taiwan 579 586 854 685 604 -12% 662

Thailand 362 467 593 524 568 8% 503

Bangladesh 228 391 434 388 481 24% 384

Vietnam 341 288 469 262 420 60% 356

All Others 1,678 2,029 3,603 2,138 2,192 3% 2,328

Total Exported 22,839 21,456 17,058 18,663 25,683 38% 21,140

Highlights

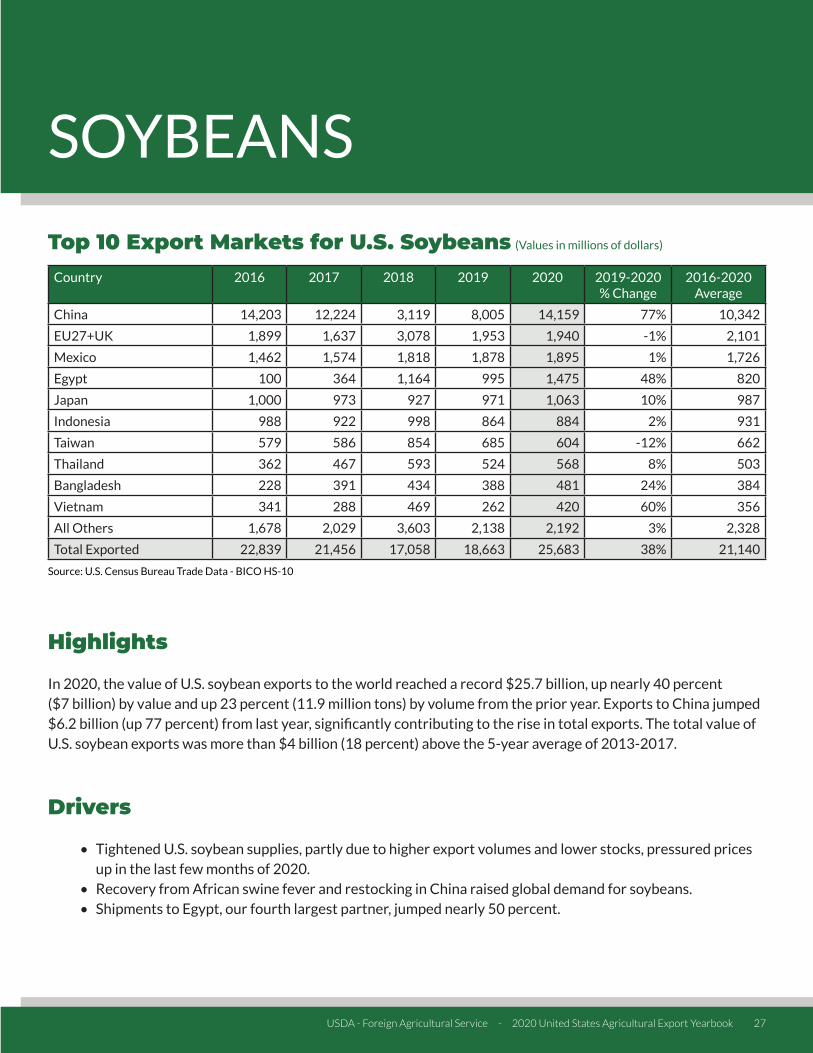

In 2020, the value of U.S. soybean exports to the world reached a record $25.7 billion, up nearly 40 percent ($7 billion) by value and up 23 percent (11.9 million tons) by volume from the prior year. Exports to China jumped $6.2 billion (up 77 percent) from last year, significantly contributing to the rise in total exports. The total value of U.S. soybean exports was more than $4 billion (18 percent) above the 5-year average of 2013-2017.

Drivers

• Tightened U.S. soybean supplies, partly due to higher export volumes and lower stocks, pressured prices up in the last few months of 2020.

• Recovery from African swine fever and restocking in China raised global demand for soybeans. • Shipments to Egypt, our fourth largest partner, jumped nearly 50 percent.

Top 10 Export Markets for U.S. Soybeans (Values in millions of dollars)

SOYBEANS

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 27

Global Soybean Exports

Looking Ahead

U.S. soybean exports are forecast at record levels for the marketing year ending in August (2020-2021). Soybean shipments are back on trend this MY with large sales being shipped out in late 2020 and early 2021. Sales are expected to drop during the normal South American shipping season. Surging demand from China as it rebuilds its stocks and the swine sector recovers from ASF have led to record shipments early in 2020-2021 compared to the same time period in prior years. As of early February 2021, 33.9 million tons have been shipped to China and another 1.9 million have been sold awaiting shipment. The United States will continue to face competition from Brazil, the largest exporter of soybeans. Exports to the EU27+UK are expected to remain steady as total commitments are at similar levels to last year, while exports to Mexico are expected to rise as total commitments are up 25 percent.

28 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

EU27+UK 2,585 2,707 2,769 3,115 2,879 -8% 2,811

India 521 738 663 823 914 11% 732

China 182 243 328 606 746 23% 421

Canada 598 643 696 697 737 6% 674

Japan 374 398 434 416 386 -7% 402

Mexico 253 256 371 343 329 -4% 310

United Arab Emirates 310 301 304 439 308 -30% 332

South Korea 296 306 290 291 295 2% 295

Hong Kong 1,156 1,251 1,052 692 271 -61% 884

Turkey 365 308 279 340 250 -27% 309

All Others 1,261 1,329 1,331 1,313 1,286 -2% 1,304

Total Exported 7,902 8,479 8,515 9,076 8,402 -7% 8,475

Highlights

In 2020, the value of U.S. tree nut exports to the world was $8.4 billion, a 7 percent decrease from 2019. The top three markets, accounting for 54 percent of sales, were the European Union (EU27+UK) at $2.9 billion, India at $914 million, and China at $746 million. While tree nut exports were up to India (11 percent), China (23 percent), and Canada (6 percent) in 2020, this was more than offset by lower sales to Hong Kong, the EU27+UK, and the United Arab Emirates. Record harvests put downward pressure on unit values, particularly for almonds. U.S. exports continue to dominate the global almond, pistachio, and walnut markets despite disruptions due to retaliatory tariffs and restrictive phytosanitary requirements. The breakout of 2020 tree nut exports was 55 percent almonds ($4.7 billion), 20 percent pistachios ($1.7 billion), 15 percent walnuts ($1.2 billion), 5 percent pecans ($432 million), 4 percent ‘mixed & other nuts’ ($296 million), and 1 percent hazelnuts ($97 million).

Top 10 Export Markets for U.S. Tree Nuts (Values in millions of dollars)

TREE NUTS

Source: U.S. Census Bureau Trade Data - BICO HS-10

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 29

Drivers

• Exports to Hong Kong declined $422 million due to China’s tightening of import controls on product passing through Hong Kong, which was only partially offset by $140 million in additional direct sales to China.

• The unit value of almonds dropped nearly 20 percent, which contributed to tree nut exports to the EU27+UK declining $236 million and the United Arab Emirates falling $131 million.

• Exports to India continue to expand on strong consumer demand for almonds, and to a lesser extent, walnuts.

Global Tree Nut Exports

Looking Ahead

Moving forward, the United States is likely to maintain its 80 percent share of world almond production and nearly 90 percent share of trade, with limited competition from Australia. The U.S. walnut industry commands half of world trade, with modest competition from China, Chile, and Ukraine. Although China produces more than 40 percent of the world’s walnuts, its exports only account for about 15 percent of world trade due to variety preferences and strong domestic demand. The U.S. pistachio industry will likely remain in close competition with Iran to be the world’s leading producer and exporter, often trading places depending on yield conditions.

New market opportunities for U.S. tree nut exports include countries in Central and South America. The United States has competitive advantages in tree nut production and exports, with 10-year growth averaging 7 percent annually and is well-positioned to maintain its global dominance.

30 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Some issues affecting future sales include compliance with pesticide maximum residue levels (MRLs) which has increasingly presented exporters with challenges selling to the European Union. The United States continues to advocate for countries to adopt science-based standards. U.S. tree nut producers also face concern over Japan’s stringent enforcement and testing protocol for aflatoxins which lead to 100 percent monitoring on U.S. shipments. The speed at which the global economy recovers from the COVID pandemic will impact the recovery in tree nut exports.

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 31

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Philippines 592 555 642 708 826 17% 665

Mexico 612 852 662 812 778 -4% 743

Japan 604 714 717 609 635 4% 656

China 205 351 106 56 570 926% 258

South Korea 248 328 363 300 340 13% 316

Nigeria 265 372 193 473 312 -34% 323

Taiwan 257 295 267 324 311 -4% 291

Indonesia 192 298 177 282 275 -3% 245

EU27+UK 165 153 210 210 246 17% 197

Yemen 92 84 103 168 195 16% 128

All Others 2,113 2,055 1,946 2,290 1,810 -21% 2,043

Total Exported 5,346 6,058 5,387 6,232 6,298 1% 5,864

Highlights

In 2020, the value of U.S. wheat exports to the world reached $6.3 billion, up 1 percent from 2019 due to increased demand from China. The top three markets, accounting for 36 percent of sales, were the Philippines at $826 million, Mexico at $778 million, and Japan at $635 million. Increased demand from China offset stronger competition from Russia and Canada in key markets including Nigeria.

Drivers

• Mexico, the Philippines, Japan, and South Korea continue as consistent buyers of U.S. wheat, accounting for 41 percent of total U.S. wheat exports.

• China was the largest growth market for U.S. wheat in 2020. U.S. wheat exports to China shrunk to $56 million in 2019 but surged to $570 million in 2020, a ten-fold increase.

• The extension of Brazil’s wheat tariff rate quota (TRQ) for non-Mercosur countries, along with reduced competition from Argentina, allowed U.S. wheat to expand its market share in Brazil. U.S. wheat exports to Brazil were $159 million in 2020, up 84 percent from 2019.

Top 10 Export Markets for U.S. Wheat (Values in millions of dollars)

WHEAT

Source: U.S. Census Bureau Trade Data - BICO HS-10

32 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

• A major challenge for U.S. wheat was competition from major exporting countries in price-sensitive markets in Africa and the Middle East.

Global Wheat Exports

Looking Ahead

Global trade in wheat is expected to grow in years to come, with major competitors to the United States being Russia, Canada, Australia, Ukraine, and the European Union. The United States is likely to continue as a major supplier of wheat to much of Latin America and East & Southeast Asia, with Mexico, the Philippines, and Japan expected to be strong, reliable markets for U.S. wheat.

U.S. competitiveness in core markets during 2021 is likely to remain strong based on continued demand from China and export restrictions in Russia. The Russian government will implement an indefinite floating export tax on wheat that may limit the country’s production and exports. This could offer an opportunity for U.S. wheat to expand its exports to markets where Russia has maintained a price advantage. However, the European Union is expected to have abundant exportable supplies amid a larger crop. Considering this competition, U.S. exports to Africa and the Middle East may face challenges in 2021. China is expected to have strong demand for imported wheat in 2021, and the United States will likely continue expanding exports there. Brazil’s 750,000-ton TRQ was recently extended for another year, offering additional export opportunities for U.S. wheat in South America.

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 33

Country 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

China 21,394 19,476 9,145 13,860 26,434 91% 18,062

Canada 20,307 20,608 20,867 20,886 20,992 1% 20,732

Mexico 17,827 18,598 19,090 19,179 18,094 -6% 18,558

Japan 11,030 11,915 12,925 11,740 11,487 -2% 11,819

EU27+UK 11,523 11,438 13,502 11,761 11,234 -4% 11,892

South Korea 6,183 6,872 8,313 7,524 7,530 0% 7,285

Vietnam 2,656 2,532 3,991 3,480 3,348 -4% 3,201

Taiwan 3,226 3,317 3,949 3,565 3,262 -9% 3,464

Philippines 2,573 2,581 2,954 2,898 3,151 9% 2,831

Indonesia 2,678 2,892 3,094 2,858 2,832 -1% 2,871

Colombia 2,383 2,528 2,904 2,667 2,740 3% 2,644

Hong Kong 3,832 4,213 3,959 2,992 2,018 -33% 3,403

Egypt 741 770 1,914 1,558 1,930 24% 1,383

Thailand 1,594 1,839 2,121 1,825 1,775 -3% 1,831

United Kingdom 1,906 1,702 1,823 1,649 1,603 -3% 1,737

All Others 26,731 28,603 30,816 29,858 28,854 -3% 28,972

World Total 134,678 138,183 139,544 136,650 145,683 7% 138,948

Highlights

U.S. agricultural exports rebounded in 2020 with a 7-percent ($9 billion) increase from the previous year. Record exports of $26.4 billion to China were a $12.6 billion increase from 2019, which offset a $3.5 billion decrease in exports to the rest of the world.

In 2020, China established a process for importers to seek exclusions from retaliatory Section 301 tariffs on U.S. products, including agricultural products. China also removed certain structural barriers to trade, expanding market access for a variety of U.S. agricultural exports in the world’s largest food import market. Simultaneously, increased U.S. competitiveness, due to production issues with foreign competitors and increased grain and oilseed prices in China, led to a surge in demand for U.S. exports.

Top U.S. Agricultural Export Markets (Values in millions of dollars)

COUNTRY OVERVIEW

Source: U.S. Census Bureau Trade Data *UK is counted in the EU-27+UK, but also reported as a separate market given its withdrawal from the EU customs union.

34 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Amongst the other top 15 markets, U.S. exports declined to 10 of those destinations. While the COVID-19 pandemic had a limited impact on the overall value of global trade of agricultural goods, there were impacts on some specific commodities, especially those used in manufacturing, such as cotton and hides, and high-value products such as beef and tree nuts.

The economic slowdown and public health restrictions, including on the hospitality sector, were more pronounced in some countries than others. Mexico experienced a deep recession contributing to a 6-percent decline in imports from the United States.

North American trading partners and the advanced economies of Japan, the European Union, and South Korea remained in the top 6 importing nations of U.S. goods. The emerging economies of Southeast Asia continued to be strong importers with Vietnam, the Philippines, Indonesia, and Thailand all remaining in the top 15. The Philippines was a success story in 2020, increasing imports by 9 percent, led by greater values of dairy products and soybean meal. Egypt increased imports from the United States by 24 percent led by greater purchases of soybeans, dairy products, and tree nuts.

Other than Mexico, U.S. exports fell sharply to the EU27+UK, Taiwan, and Hong Kong. The largest decreases to the EU27+UK were in tree nuts, beef, and wine. Taiwan imported less soybeans, corn, and cotton, and Hong Kong reduced their imports of U.S. tree nuts, poultry, beef, and fresh fruit.

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 35

Commodity 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Prepared Food 1,889 1,908 1,931 2,048 2,178 6% 1,991

Fresh Vegetables 1,807 1,878 1,884 1,986 1,891 -5% 1,889

Fresh Fruit 1,633 1,608 1,533 1,485 1,580 6% 1,568

Snack Foods 1,315 1,355 1,407 1,393 1,335 -4% 1,361

Non-Alcoholic Beverages* 1,156 1,087 1,069 1,041 1,013 -3% 1,073

Pork & Pork Products 798 793 765 802 853 6% 802

Dog & Cat Food 597 640 645 751 842 12% 695

Chocolate & Cocoa Products

749 748 713 713 753 6% 735

Tree Nuts 598 643 696 697 737 6% 674

Beef & Beef Products 758 791 745 654 728 11% 735

All Other 9,007 9,157 9,480 9,317 9,082 -3% 9,208

Total Exported 20,307 20,608 20,867 20,886 20,992 1% 20,732

Highlights

In 2020, Canada was the second largest market for U.S. agricultural exports, totaling $21 billion. This represents a 1-percent increase from 2019. On July 1, 2020, the United States–Mexico–Canada Agreement (USMCA) entered into force, expanding U.S. access to Canada for certain dairy, poultry, and egg products. The United States maintained the No. 1 position in Canada’s agricultural market with a 57-percent market share. The largest percentage export growth to Canada was in dog & cat food, increasing 12 percent, followed closely by beef & beef products at 11 percent. Exports of fresh fruit, pork & pork products, and prepared foods all increased 6 percent last year. The top 3 largest decreases in exports to Canada in 2020 were in fresh vegetables ($95 million), snack foods ($57 million), and non-alcoholic beverages ($28 million), losing 5 percent, 4 percent, and 3 percent, respectively. Despite these decreases, Canada remained the top market in 2020 for U.S. prepared food, fresh fruit, feeds & fodders, fresh vegetables, snack foods, and processed vegetables.

Top 10 U.S. Agricultural Exports to Canada (Values in millions of dollars)

CANADA

Source: U.S. Census Bureau Trade Data - BICO HS-10 *Excludes juices

36 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Drivers

• Processed foods such as prepared foods, snack foods, and beverages, as well as fresh fruits and vegetables, continue to be the top exports to Canada. Climatic conditions and geographic proximity provide the United States with a strong competitive advantage in supplying fresh goods to Canada while highly integrated supply chains and logistical advantages ensure the timely delivery of processed foods and retail-ready goods.

• U.S. exports of dog & cat food were up by $91 million, a 12-percent increase by value from 2019 and representative of a 91-percent market share. In 2020, Canadian dog & cat food imports from the world also increased 12 percent by value.

• U.S. exports of beef & beef products increased $73 million from 2019 but remained below 2015-2018 levels. Overall Canadian beef imports from the world increased 22 percent by value, with the United States capturing 63 percent market share by value and 56 percent by volume.

• U.S. dairy product exports reached a record high, climbing 1 percent to more than $675 million, with increases in milk-based drinks (up 7 percent to $88 million) and various cheeses (up 24 percent to $69 million) offsetting declines in exports of butter (down 16 percent), whey protein (down 12 percent), and other products.

Canada’s Agricultural Suppliers

Looking Ahead

On July 1, 2020, USMCA entered into force, strengthening the long-standing North American free trade relationship. USMCA maintains the zero tariffs between the three countries that were in place under NAFTA,

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 37

as well as provides new market access for a wide range of U.S. dairy products through tariff-rate quotas (TRQs). The Agreement also requires Canada to eliminate its milk classes 6 and 7, which allowed unfairly low-priced Canadian dairy products to undersell U.S. products in Canada and in third country markets.

Canada’s global chicken and chicken product imports before USMCA entered into force were constrained by (i) Canada’s WTO TRQ or by (ii) a regulation that calculated as a percentage of Canadian chicken production in the preceding calendar year, whichever was larger. USMCA provides a country-specific TRQ for poultry for the United States, preserving a portion of the market for U.S. exporters, even as the Canadian market evolves and becomes more competitive and open to other partners. The United States still has access to Canada’s WTO TRQ.

The USMCA contains new and enforceable rules to ensure that sanitary and phytosanitary measures (SPS) are science-based and developed and implemented in a transparent and non-discriminatory manner. The USMCA obligates Canada to eliminate discrimination in grading of U.S. wheat and the requirement for a country-of-origin statement on quality grade certificates for U.S. wheat.

The Distilled Spirits, Wine, Beer, and Other Alcohol Beverages Annex of the USMCA Agriculture Chapter contains non-discrimination and transparency commitments regarding sale and distribution of alcoholic beverages. Also, the Parties agreed to labeling and certification provisions to help prevent technical barriers to trade in wine and distilled spirits.

In a USMCA side letter with the United States, Canada committed to ensure that British Columbia eliminate measures governing grocery store wine sales that discriminate against U.S. wine, no later than November 1, 2019.

Canada has implemented free trade agreements with other agricultural exporting blocs: the 11-nation Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and the Comprehensive Economic and Trade Agreement (CETA) with the European Union. Canada is in the process of implementing a Canada-United Kingdom Trade Continuity Agreement following the United Kingdom’s exit from the European Union. Though Canada is a mature market with modest economic growth and low population growth, there remains significant export growth potential in Quebec, a regional economy the size of the Philippines, where U.S. products are underrepresented.

38 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Commodity 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Soybeans 14,203 12,224 3,119 8,005 14,160 77% 10,342

Pork & Pork Products 713 662 571 1,300 2,280 75% 1,105

Cotton 554 978 925 707 1,826 158% 998

Corn 40 142 50 56 1,205 2052% 299

Coarse Grains* 1,030 838 521 191 1,153 504% 747

Poultry Meat & Products**

34 36 47 10 762 7520% 178

Tree Nuts 182 243 328 606 746 23% 421

Wheat 205 351 106 56 570 918% 258

Dairy Products 386 576 498 373 539 45% 474

Hay 355 341 272 291 413 42% 334

All Other 3,693 3,086 2,709 2,267 2,781 23% 2,907

Total Exported 21,395 19,476 9,145 13,860 26,435 91% 18,062

Highlights

In 2020, U.S. agricultural exports to China totaled $26.4 billion, up $12.6 billion from 2019. China was the largest market for U.S. agricultural exports, a position it last held in 2016. Brazil (22 percent market share) and the United States (15 percent) were the top suppliers of agricultural goods to China, followed by the European Union with 14 percent. In 2020, China established a process for importers to seek exclusions for retaliatory Section 301 tariffs on U.S. products, including agricultural products. China also removed certain structural barriers to trade, expanding market access for a variety of U.S. agricultural exports in the world’s largest food import market. Exports of all top 10 commodity groups increased in 2020, with the largest increases for soybeans, corn, and cotton which were up $6.2 billion, $1.2 billion, and $1.1 billion, respectively. In addition, U.S. exports of pork & pork products, coarse grains (excluding corn), and poultry meat & products (excluding eggs) were up $980 million, $962 million, and $752 million, respectively. While exports for most commodity groups were up, a few including processed vegetables, hides & skins, and wine & beer were down $29 million, $23 million, and $18 million, respectively.

Top 10 U.S. Agricultural Exports to China (Values in millions of dollars)

CHINA

Source: U.S. Census Bureau Trade Data - BICO HS-10 *Excludes corn **Excludes eggs

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 39

Drivers

• The Chinese Government created an exclusion process for retaliatory Section 301 tariffs on a wide range of products; imports of these products have risen significantly since this process was granted.

• China’s economic recovery from COVID-19 led to strong demand for U.S. agricultural products, including cotton, soybeans, wheat, and corn.

• African swine fever significantly reduced China’s swine herd, which led to increases in demand for U.S. pork & pork products. In addition, Chinese demand for U.S. soybeans and feed products grew, as China worked to rebuild its swine population.

China’s Agricultural Suppliers

Looking Ahead

China committed to purchases nearly $40 billion per year of U.S. agricultural products for the first 2 years (2020 and 2021) of the Phase One Agreement. Due in part to the COVID-19 pandemic and related impacts on global demand, China missed its commitment by about 30 percent. Under the agreement, China removed specified structural barriers to U.S. agricultural products with 50 of these 57 commitments implemented on time. China also implemented a program to exempt retaliatory tariffs which improves the competitiveness of U.S. goods.

China’s strong demand for U.S. agricultural products is expected to continue. China recovered from COVID-19 more quickly than most of the world and is increasing purchases of U.S. agricultural products, including corn, soybeans, and other animal feeds needed to replenish its growing swine heard. Continued economic growth and an expanding middle-class also bodes well for increased exports of poultry, fruits and vegetables, and other higher-valued consumer- oriented goods.

40 USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook

Commodity 2016 2017 2018 2019 2020 2019-2020 % Change

2016-2020 Average

Corn 771 785 927 682 876 28% 808

Soybean Meal 259 340 481 412 485 18% 395

Soybeans 195 212 256 223 191 -14% 215

Pork & Pork Products 105 163 215 221 147 -34% 170

Wheat 181 173 88 137 133 -3% 142

Dairy Products 88 65 72 145 128 -12% 100

Poultry Meat & Products* 66 70 82 114 93 -18% 85

Feeds & Fodders 76 80 98 81 84 4% 84

Soybean Oil 62 73 100 57 77 36% 74

Rice 58 51 54 49 65 33% 56

All Other 522 516 531 546 461 -16% 515

Total Exported 2,383 2,528 2,904 2,667 2,740 3% 2,644

Highlights

In 2020, Colombia was the 11th largest destination for U.S. agricultural exports, totaling $2.7 billion. This represents a 3-percent increase from 2019. The United States is Colombia’s top supplier of agricultural goods by a wide margin, representing 48 percent of the total import market. The EU27+UK is Colombia’s second-largest supplier with only 8 percent market share. The U.S.-Colombia Trade Promotion Agreement (CTPA) has expanded export opportunities for many U.S. agricultural products. The largest year-to-year export increase was seen in corn, up 28 percent to $876 million in 2020. Exports of soybean meal, soybean oil, and rice also rose last year, up $73 million, $20 million, and $16 million, respectively. Exports of pork & pork products plummeted $74 million, while soybeans and poultry dropped $32 million and $21 million, respectively. In 2020, Colombia was the fourth-largest market for U.S. corn exports, third- largest market for U.S. soybean meal, and seventh-largest market for U.S. pork.

Top 10 U.S. Agricultural Exports to Colombia (Values in millions of dollars)

COLOMBIA

Source: U.S. Census Bureau Trade Data - BICO HS-10 *Excludes eggs

USDA - Foreign Agricultural Service - 2020 United States Agricultural Export Yearbook 41

Drivers

• In 2020, the economic slowdown associated with COVID-19 led to decreased food and agricultural exports to Colombia across many product categories. Increases in bulk and intermediate product sales narrowly made up for strong decreases in consumer-oriented product exports. In 2020, U.S. food and agricultural exports to Colombia grew 2.7 percent, reaching $2.9 billion.