Embed Size (px)

Citation preview

2021Buyer insight reportAnalyzing the digital purchase paths of over 3,000 auto shoppers.

“COVID continues to cause commotion in the auto industry, from plant and retail shutdowns to production. Meanwhile, consumers are especially eager to buy cars due to an influx in stimulus and concerns over shared mobility. Both factors have resulted in a unique phenomenon: extraordinarily high demand and low supply.”

“The pandemic forced people to change their routines and habits. Over a year into it, many shoppers tell us that these changes are here to stay. Those include increased personal vehicle use and handling more of the car-buying process online. While this past year has been challenging for buyers and sellers alike, it’s caused people to have a greater appreciation for their vehicles and the new, more convenient shopping options available.”

Madison Edwards Director of Consumer Insights

Kevin Roberts Director of Industry Analytics

STATE OF THE MARKET

It goes without saying that the automotive market has changed significantly over the past 12–24 months. This report—which features findings from our fourth annual path-to-purchase study in partnership with GfK—aims to help you adapt your business model to this new normal. Using cur-rent insights on consumers’ mindsets and behaviors, we’ll point out the most effective strategies for success in the auto industry.

Buyer mindset

Buyer behavior

Why they buy

What they face

How they feel

Who they consider

5

6

7

8

10

11

12

13

14

15

16

4

9

The sites they browse

The social media they use

The time they spend

The devices they prefer

The criteria they look for

They ways they make contact

The CarGurus consumer

Buyer predictions

Conclusion

18

19

20

21

22

23

17

22

The rise of digital retail

The role of the store

Electric and self-driving cars

Mobility trends

Key takeaways

Background & methodology

Table of contents

BUYER MINDSETShopping for a car can be both exciting and stressful. By anticipating buyers’ attitudes and preconceptions, dealers and OEMS can ease consumers’ anxieties.

2021 Buyer Insight Report Report | 4

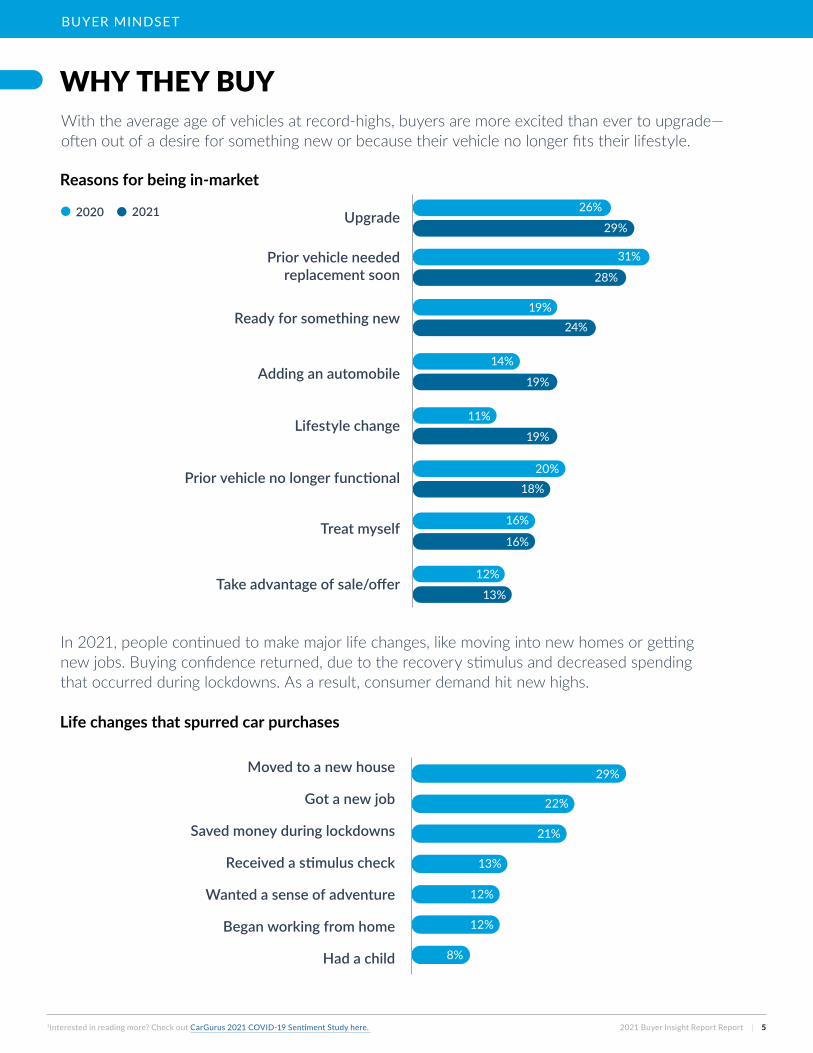

WHY THEY BUY

In 2021, people continued to make major life changes, like moving into new homes or getting new jobs. Buying confidence returned, due to the recovery stimulus and decreased spending that occurred during lockdowns. As a result, consumer demand hit new highs.

With the average age of vehicles at record-highs, buyers are more excited than ever to upgrade—often out of a desire for something new or because their vehicle no longer fits their lifestyle.

BUYER MINDSET

Reasons for being in-market

Upgrade2020 2021

Prior vehicle needed replacement soon

Ready for something new

Adding an automobile

Lifestyle change

Prior vehicle no longer functional

Treat myself

Take advantage of sale/offer

1Interested in reading more? Check out CarGurus 2021 COVID-19 Sentiment Study here. 2021 Buyer Insight Report Report | 5

26%

29%

31%

28%

19%

14%

19%

11%

19%

20%18%

16%

16%

12%

13%

24%

Life changes that spurred car purchases

Moved to a new house

Got a new job

Saved money during lockdowns

Received a stimulus check

Wanted a sense of adventure

Began working from home

Had a child

29%

22%

21%

13%

12%

12%

8%

Prices seem higher than typical

Selection seems worse than typical

Shopper perceptions of price and inventory

of recent buyers say a vehicle they were planning to see in-person was sold before they got there

of current shoppers say they delayed or pushed off shopping for a vehicle because prices were/are so high.

30%

31%

58% 47%

33% 25%24% 24%

“There’s more demand now than before. It makes me

wonder if it’s even a good time to purchase.”

– CarGurus user, July 2021

WH AT S H O PPER S A R E SAY I N G

WHAT THEY FACEDealers and manufacturers are struggling to keep up with demand, and shoppers have taken notice. Now more than ever, shoppers are aware that prices are high and inventory is low, particularly in the US. These inventory issues have negatively impacted many buyers’ experiences.

1Interested in reading more? Check out CarGurus 2021 COVID-19 Sentiment Study here.

BUYER MINDSET

Nov-20 Jul-21

2021 Buyer Insight Report Report | 6

“We’re likely to see tightened inventory into the second half of 2022 as supply chain issues persist.”

- Kevin Roberts, Director of Industry Analytics

26%

32%

58%

47%

HOW THEY FEELWhile the pandemic and inventory shortages have presented car buyers with new challenges, delayed purchases have resulted in a lot of pent-up demand. Furthermore, dealers have quickly adapted, providing a streamlined experience that shoppers are enjoying more than ever.

59%

59%

78%

54%

27%

76%

“Car shopping is fun.”

“Using online tools and resources makes me a smarter shopper.”

“The car someone drives says a lot about

them.”

“Cars don’t excite me.”

up from 49% in 2018

down from 63% in 2018

down from 32% in 2020

up from 51% in 2018

Buyers are accustomed to solving challenges online, and that applies to car buying, too.

BUYER MINDSET

“Car shopping is stressful.”

“I research and compare cars exhaustively

before making my final

purchase.”

2021 Buyer Insight Report Report | 7

While most people start their car-buying journey unsure of which seller to buy their car from, buyers are selective about who they contact and visit.

Shoppers’ uncertainty on initial decisions

dealers contacted, on average

dealers visited, on average

of shoppers visited only one dealer before buying3 2 42%

WHO THEY CONSIDERCompared to shoppers in years past, today’s consumers are even more undecided on major decisions like whether to finance, trade-in, and buy new or used. Over 50% of car buyers begin their shopping journey unsure of which make and model they want.

BUYER MINDSET

Seller

Model

Make

What to do with a prior vehicle

Approximate price willing to pay

Body style

Whether to finance

New or used

Purchase or lease

indicates a 5ppt increase vs. 2018**‘whether to finance’ is compared vs. 2019 when it was added

63%

55%

52%

44%

42%

38%

36%

33%

31%

53%switch body styles (i.e., sedan to SUV)

switch makes switch models

69% 86%

2021 Buyer Insight Report Report | 8

BUYER BEHAVIORUnderstanding how people navigate a car purchase—specifically the sources they trust, devices they prefer, and ways they contact sellers—is helpful when determining how to communicate with them.

2021 Buyer Insight Report Report | 9

BUYER BEHAVIOR

THE SITES THEY BROWSEShoppers often tell us a vehicle purchase feels like a high-stakes decision, so they need to check a range of sites. Auto-shopping sites, however, are their favorite. They attract nearly all car shoppers and earn 2x more visits than dealer or OEM sites on average.

Site type Share of shoppers visitingAverage # of visits per user

Auto-shopping sites 13

9

6

6

5

3

Auto-information sites

Parts, service, or repair sites

OEM sites

Dealership sites

Industry press sites

2021 Buyer Insight Report Report | 10

Among auto-shopping sites, CarGurus is the most popular. CarGurus is nearly 3X more likely to be the final auto-shopping site buyers visit before purchasing.³

D I D YO U K N OW ?

3Compared to competitive average of Autotrader, Cars.com, Carfax, Edmunds, KBB and TrueCar

94%

77%

75%

63%

61%

34%

unique sites used by the average buyer,

up from 13 in 2019

17

THE SOCIAL MEDIA THEY USEIn addition to auto-shopping sites, social-media sites are popular destinations for consumers to actively research, crowd-source recommendations, and engage with dealers and brands.

YouTube and Facebook are people’s most-used social media channels for recreational and car-shopping purposes.

YouTubeFacebook Instagram Twitter Snapchat Pinterest TikTok Reddit

of online car shopperschecked social media during a car-shopping session.

say social media directly informed their car

purchase, up from 19% a year ago.

say they used social media to assist with car shopping in some way.

95%26% 68%

BUYER BEHAVIOR

Social Media Use

Use regularly Use for car shopping

76%

44%

74%

45% 44%

18%

31% 29% 27%

21%11% 11%10% 9%

57%

26%

2021 Buyer Insight Report Report | 11

of online car shopperschecked social media during a car-shopping session.

95%

BUYER BEHAVIOR

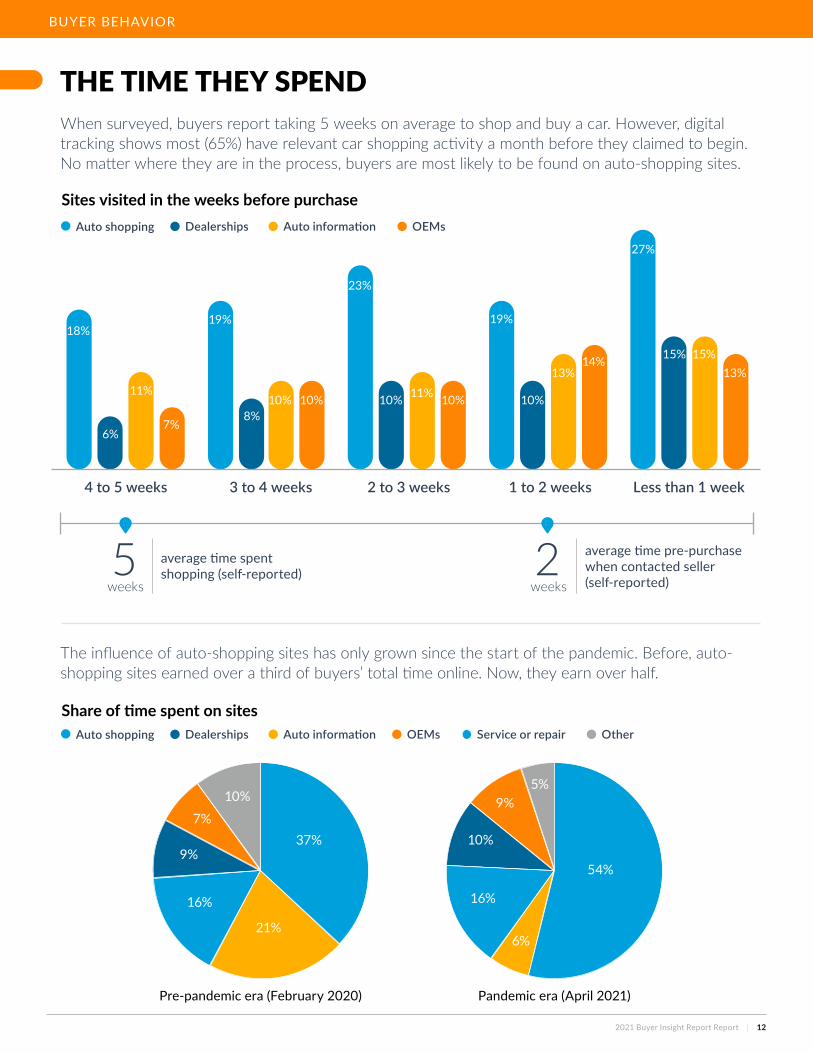

THE TIME THEY SPENDWhen surveyed, buyers report taking 5 weeks on average to shop and buy a car. However, digital tracking shows most (65%) have relevant car shopping activity a month before they claimed to begin. No matter where they are in the process, buyers are most likely to be found on auto-shopping sites.

The influence of auto-shopping sites has only grown since the start of the pandemic. Before, auto-shopping sites earned over a third of buyers’ total time online. Now, they earn over half.

Sites visited in the weeks before purchase

Share of time spent on sites

Pre-pandemic era (February 2020) Pandemic era (April 2021)

Auto shopping

Auto shopping

Dealerships

Dealerships

Auto information

Auto information

OEMs

OEMs Service or repair Other

18%

6%

11%

7%

19%

8%10% 10% 10% 10% 10%

13% 13%14%

27%

15% 15%

19%

23%

11%

4 to 5 weeks 3 to 4 weeks 2 to 3 weeks 1 to 2 weeks Less than 1 week

average time spent shopping (self-reported)

average time pre-purchase when contacted seller (self-reported)

2021 Buyer Insight Report Report | 12

37%

54%

6%21%

16% 16%

10%

9%5%

9%

7%

10%

5 2weeks weeks

THE DEVICES THEY PREFERBuyers use a combination of devices when car shopping. Most shoppers in the discovery and comparison phases prefer desktop. Desktop sessions draw a higher degree of engagement compared to smartphone sessions, especially in the week before purchase. Mobile, however, is most frequently used—including for last minute reassurance.

Choose specific vehicle to purchase

Learn what’s on the market

Compare makes, models, and trims

Decide what body style to look for

Sell or trade in a vehicle

Get financing

Find dealership/seller

Prepare to visit the seller or negotiate

BUYER BEHAVIOR

Preferred device for activity

Time spent on device (in minutes)

Desktop

Desktop

Mobile devices

Mobile devices

Tablet

53%

50%

50% 36%

36%

38%

38%

43%

44%

50%

48%

47%

44%

40%

2219 20

16

21

14

43

17

32%

36% 14%

14%

14%

15%

15%

13%

16%

16%

2021 Buyer Insight Report Report | 13

3 to 4 weeks 2 to 3 weeks 1 to 2 weeks Less than 1 week

Top reasons for choosing a vehicle

Top reasons for choosing a dealership

2 Interested in reading more? Check out CarGurus 2021 Reliability Survey here

THE CRITERIA THEY LOOK FORShoppers care most about finding a car that’s reliable and fits their budget.

BUYER BEHAVIOR

Budget

Prices

Reliability

Available inventory

Driving feel

Location of the seller

Make

Financing availability/offers

Safety ratings

Confidence that I would get treated fairly

Expected ownership costs

Vehicle servicing availability/reputation

Fuel type/powertrain

Past experience with seller

37%

53%

35%

30%

26%

22%

20%

20%

36%

24%

24%

20%

18%

16%

2021 Buyer Insight Report Report | 14

“Reliability is always a top concern for buyers, but many struggle to assess it, particularly when buying used. Only half of used-car buyers say they can easily judge a vehicle’s reliability vs. over two-thirds of new-car buyers.” ²

- Madison Edwards, Director of Consumer Insights

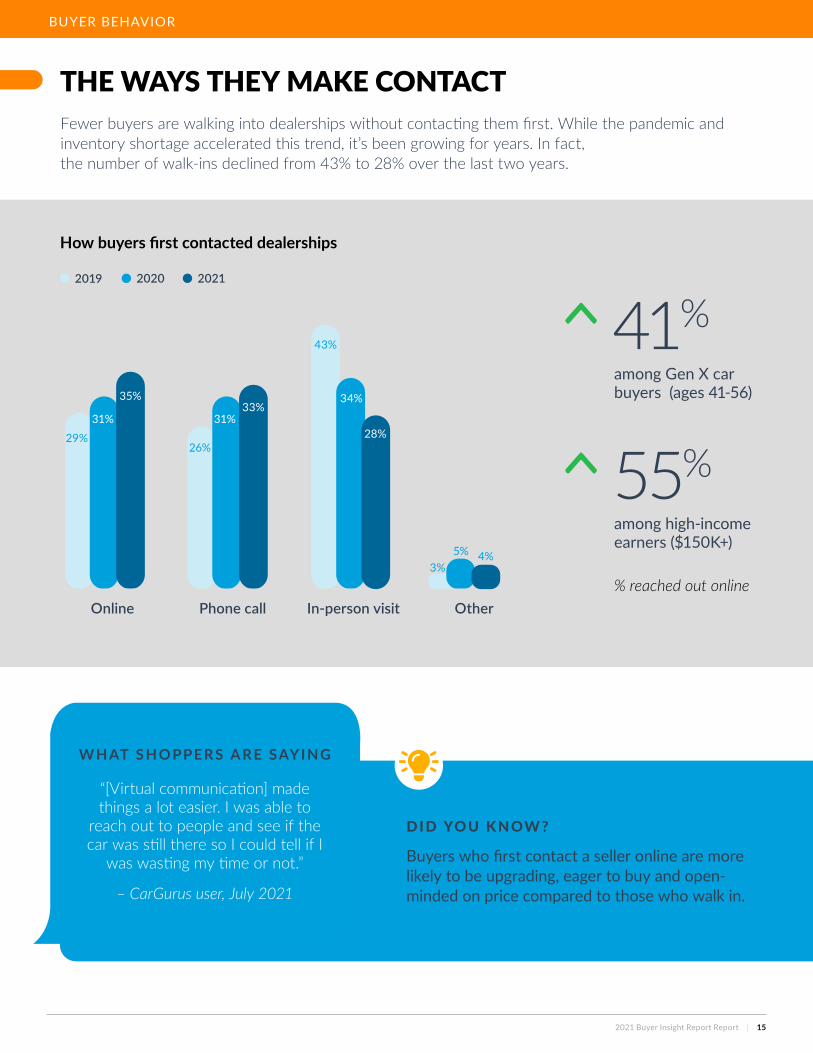

THE WAYS THEY MAKE CONTACTFewer buyers are walking into dealerships without contacting them first. While the pandemic and inventory shortage accelerated this trend, it’s been growing for years. In fact, the number of walk-ins declined from 43% to 28% over the last two years.

How buyers first contacted dealerships

% reached out onlineOnline Phone call In-person visit Other

among Gen X car buyers (ages 41-56)

among high-income earners ($150K+)

41%

55%

BUYER BEHAVIOR

2019 2020 2021

Buyers who first contact a seller online are more likely to be upgrading, eager to buy and open-minded on price compared to those who walk in.

“[Virtual communication] made things a lot easier. I was able to

reach out to people and see if the car was still there so I could tell if I

was wasting my time or not.”

– CarGurus user, July 2021

29%26%

43%

3%5% 4%

31% 31%

34%

28%

35%33%

WH AT S H O PPER S A R E SAY I N G

D I D YO U K N OW ?

2021 Buyer Insight Report Report | 15

THE CARGURUS CONSUMERCarGurus attracts the most down-funnel and ready-to-buy shoppers. They put in the time to compare options, find a great deal, and prepare for their dealer visit. CarGurus’ products and features empower them to get the job done.

CarGurus users are more likely to report engaging with the site than competitors’ users, on average.³

CarGurus users are more likely than average to prefer an omnichannel approach to shopping.

47%

31%

30%

28%

27%

15%

more likely to sign up for alerts that notify them when there are new listings that match their search

more likely to download the app

more likely to view photos of specific cars on site

more likely to review vehicle listings on site

more likely to save a listing so they can review it later

more likely to research whether a vehicle is a good deal

CarGurus is nearly 3X more likely to be the final auto-shopping site buyers visit before purchasing.³

are open to buying online, but most still prefer an in-person test drive

more likely to prefer online financing

more likely to prefer an online trade-in valuation

80%

22%

21%

3Compared to competitive average of Autotrader, Cars.com, Carfax, Edmunds, KBB and TrueCar

BUYER BEHAVIOR

2021 Buyer Insight Report Report | 16

of CarGurus users say their purchase is very or

extremely urgentvs. 25% on average.

of CarGurus users say they research and compare exhaustively before buying

vs. 76% on average

34% 84%

BUYER PREDICTIONSWith the advent of digital retail, consumers foresee changes in car-shopping. They’re also very excited by the latest automotive innovations. In this section, we’ll explore how buyers envision their next car purchase, their opinions on electric and autonomous vehicles, and our predictions for the future of car ownership.

2021 Buyer Insight Report Report | 17

THE RISE OF DIGITAL RETAILConsumers’ openness to buying online spiked during the pandemic. For now, the test drive remains the biggest deterrent to a completely digital purchase. However, people want to get their car shopping done quickly. For that reason, they love the idea of handling more of the purchase process from home and online, specifically financing, negotiation, and trade-in valuation.

of auto shoppers say they’d prefer to do more of the car-buying process from home for their next purchase

60%

Preference for handling a car-shopping activity online

Finance Price negotiation Trade-in valuation Test drive (via VR or 360° videos)

1Interested in reading more? Check out CarGurus 2021 COVID-19 Sentiment Study here.

BUYER PREDICTIONS

2020 (pre-pandemic)

2021

2021 Buyer Insight Report Report | 18

“During the pandemic, more shoppers learned about the ways they can jump-start their car-buying process from home. Now that they know there are options, they have even higher expectations for their next purchase.”

- Madison Edwards, Director of Consumer Insights

36%

51%

25%

45%

34%36%

9% 18%

BUYER MINDSETBUYER MINDSET

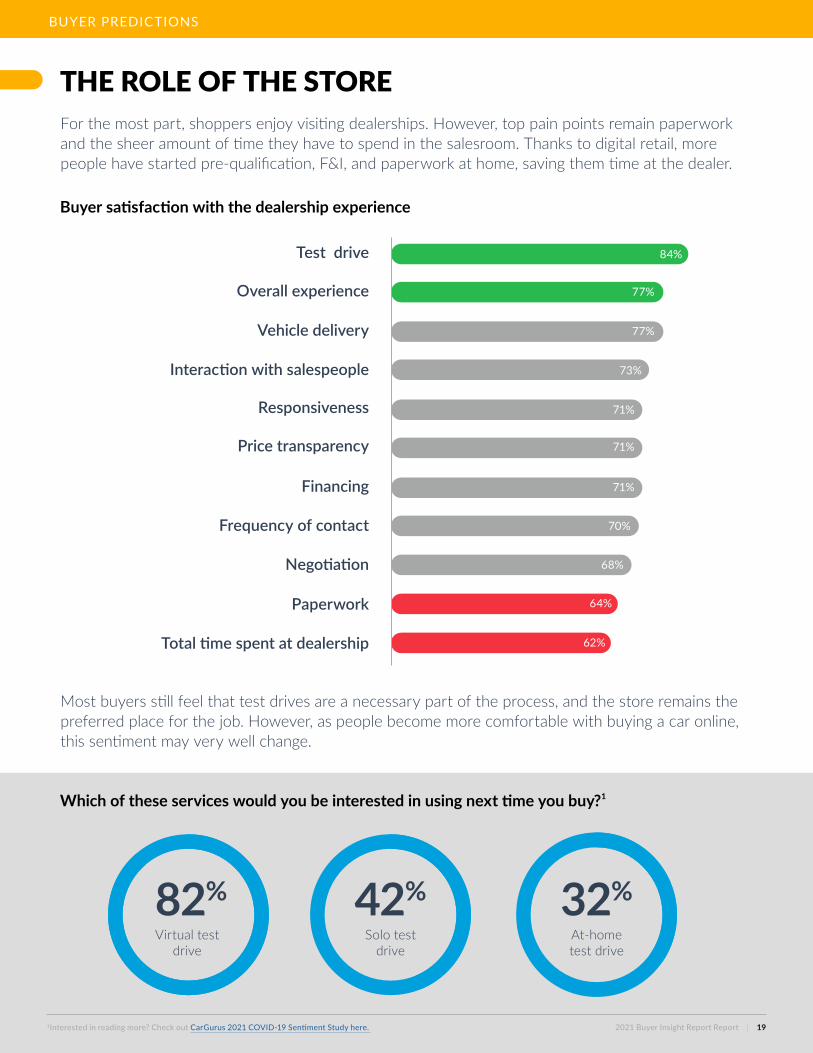

THE ROLE OF THE STOREFor the most part, shoppers enjoy visiting dealerships. However, top pain points remain paperwork and the sheer amount of time they have to spend in the salesroom. Thanks to digital retail, more people have started pre-qualification, F&I, and paperwork at home, saving them time at the dealer.

Most buyers still feel that test drives are a necessary part of the process, and the store remains the preferred place for the job. However, as people become more comfortable with buying a car online, this sentiment may very well change.

Test drive

Overall experience

Vehicle delivery

Interaction with salespeople

Responsiveness

Price transparency

Financing

Frequency of contact

Negotiation

Paperwork

Total time spent at dealership

Buyer satisfaction with the dealership experience

Which of these services would you be interested in using next time you buy?¹

1Interested in reading more? Check out CarGurus 2021 COVID-19 Sentiment Study here.

BUYER PREDICTIONS

84%

77%

77%

73%

71%

71%

71%

70%

68%

64%

62%

82% 42% 32%Virtual test

driveSolo test

driveAt-home test drive

2021 Buyer Insight Report Report | 19

TOP BRANDS CONSIDERED AMONG SHOPPERS INTERESTED IN EVS

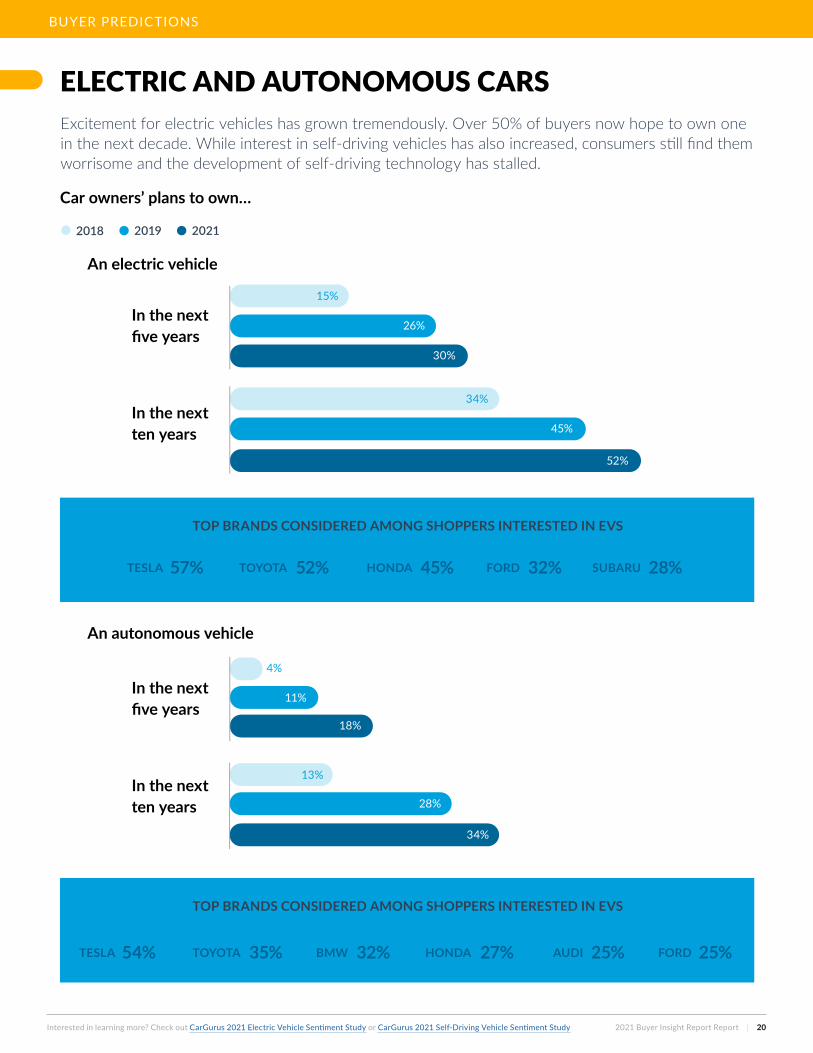

ELECTRIC AND AUTONOMOUS CARSExcitement for electric vehicles has grown tremendously. Over 50% of buyers now hope to own one in the next decade. While interest in self-driving vehicles has also increased, consumers still find them worrisome and the development of self-driving technology has stalled.

Car owners’ plans to own…

TESLA

TESLA

TOYOTA

TOYOTA

HONDA

BMW

FORD

HONDA

SUBARU

AUDI FORD

57%

54%

52%

35%

45%

32%

32%

27%

28%

25% 25%

An electric vehicle

TOP BRANDS CONSIDERED AMONG SHOPPERS INTERESTED IN EVS

In the next five years

In the next five years

In the next ten years

In the next ten years

An autonomous vehicle

Interested in learning more? Check out CarGurus 2021 Electric Vehicle Sentiment Study or CarGurus 2021 Self-Driving Vehicle Sentiment Study

BUYER PREDICTIONS

2018 2019 2021

15%

4%

13%

34%

26%

11%

18%

28%

34%

45%

52%

30%

2021 Buyer Insight Report Report | 20

BUYER MINDSETBUYER MINDSET

MOBILITY TRENDSConsumers have stopped or reduced their use of shared transportation during the pandemic, and many are not eager to resume, even in the long-term. People have become reliant on personal vehicles to replace these services, and to offer an escape and sense of joy during the pandemic. Looking forward, it’s clear that personal vehicle ownership is here to stay.

Share of people planning to resume pre-pandemic activity

Plans for vehicle ownership in the next 5–10 years

Ride-sharing and taxis (e.g., Uber)

Public transportation

CarGurus 2021 COVID-19 Sentiment Study, US (n = 600)

BUYER PREDICTIONS

Increase Keep same Decrease

54%

47%

42% 54% 4%

53%

59%

among millennials (ages 24–33) 56%

2021 Buyer Insight Report Report | 21

“As a result of the pandemic, people are relying on their cars more than ever before. This, in part, explains why demand for vehicles has hit record highs. ”

In the next year In the long-term

- Kevin Roberts, Director of Industry Analytics

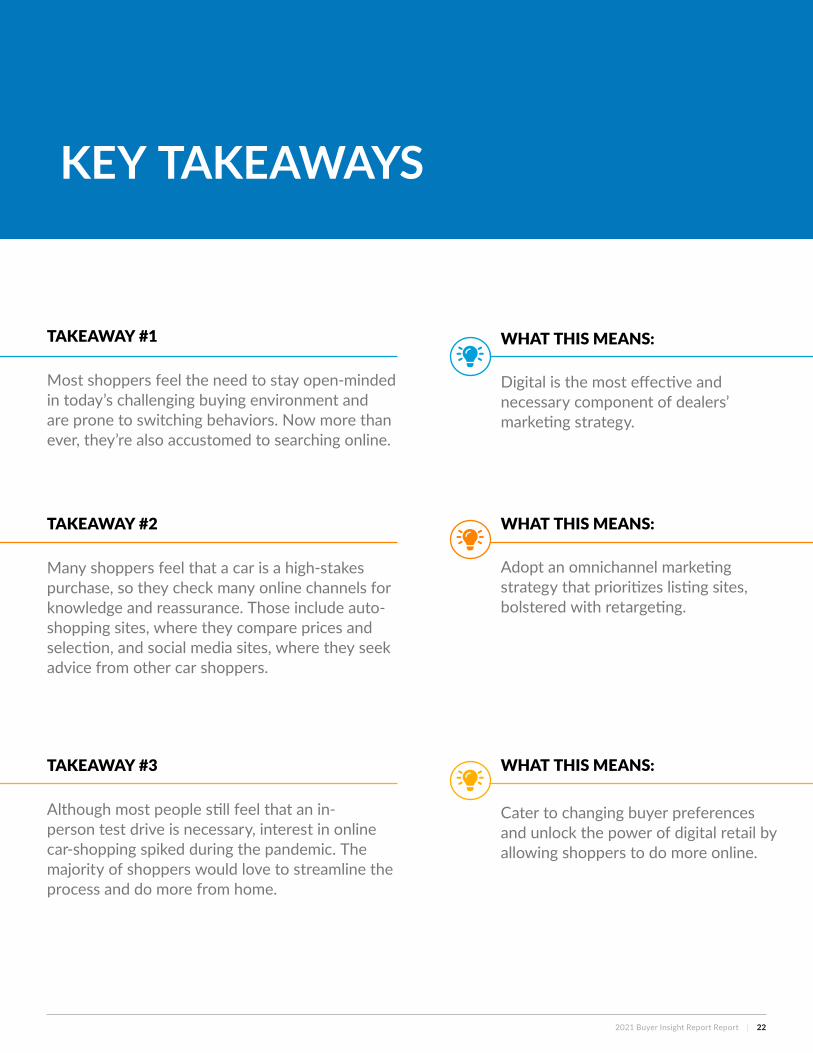

TAKEAWAY #1

Most shoppers feel the need to stay open-minded in today’s challenging buying environment and are prone to switching behaviors. Now more than ever, they’re also accustomed to searching online.

TAKEAWAY #2

Many shoppers feel that a car is a high-stakes purchase, so they check many online channels for knowledge and reassurance. Those include auto-shopping sites, where they compare prices and selection, and social media sites, where they seek advice from other car shoppers.

TAKEAWAY #3

Although most people still feel that an in-person test drive is necessary, interest in online car-shopping spiked during the pandemic. The majority of shoppers would love to streamline the process and do more from home.

Digital is the most effective and necessary component of dealers’ marketing strategy.

Adopt an omnichannel marketing strategy that prioritizes listing sites, bolstered with retargeting.

Cater to changing buyer preferences and unlock the power of digital retail by allowing shoppers to do more online.

WHAT THIS MEANS:

WHAT THIS MEANS:

WHAT THIS MEANS:

2021 Buyer Insight Report Report | 22

KEY TAKEAWAYS

Methodology

Data is primarily sourced from an April 2021 study conducted by CarGurus and GfK, a leading market research firm. The study included (1) a survey of 3,031 recent auto purchasers—including new and used—and (2) an analysis of the relevant digital behaviors of 355 car purchasers, tracked passively across devices in the weeks before purchase. Additional data is sourced from CarGurus 2021 COVID-19 Sentiment Study, CarGurus 2021 Reliability Survey, CarGurus 2021 Electric Vehicle Sentiment Study, and CarGurus 2021 Self-Driving Sentiment Study. Please see those reports for detailed methodology.

About CarGurus

CarGurus (Nasdaq: CARG) is a multinational, online automotive platform for buying and selling vehicles that is building upon its industry-leading listings marketplace with both digital retail solutions and the CarOffer online wholesale platform. The CarGurus marketplace gives consumers the confidence to purchase or sell a vehicle either online or in-person; and gives dealerships the power to accurately price, effectively market, instantly acquire and quickly sell vehicles, all with a nationwide reach. The company uses proprietary technology, search algorithms, and data analytics to bring trust, transparency, and competitive pricing to the automotive shopping experience. CarGurus is the most visited automotive shopping site in the U.S. (source: Comscore Media Metrix® Multi-Platform, Automotive – Information/Resources, Total Audience, Q2 2021, U.S.).CarGurus also operates online marketplaces under the CarGurus brand in Canada and the United Kingdom. In the United States and the United Kingdom, CarGurus operates the Autolist and PistonHeads online marketplaces, as independent brands. To learn more about CarGurus, visit www.cargurus.com. For more information on CarOffer visit www.caroffer.com.

CarGurus® is a registered trademark of CarGurus, Inc., and CarOffer® is a registered trademark of CarOffer, LLC. All other product names, trademarks, and registered trademarks are property of their respective owners.© 2021 CarGurus, Inc., All Rights Reserved.

BACKGROUND & METHODOLOGY

2021 Buyer Insight Report Report | 23