Embed Size (px)

Citation preview

1

21st century steel2008-2009 Update

Alonso Ancira Altos Hornos de México

Rafael Naranjo OlmedoAcerinox

Chang Sae-Joo Dongkuk Steel Mill

Hajime Bada JFE Steel

Zhang Xiaogang Anshan Steel

Antonio Gozzi Duferco

Shen Wenrong (Bill) Jiangsu Shagang Group

Lakshmi N. Mittal ArcelorMittal

Sajjan Jindal JSW Steel

Carolin Kramer Badische Stahlwerke

Prashant Ruia Essar Steel

Xu Leijang Baosteel Group

worldsteel Board of directors 2008-2009

Masatoshi Ozawa Daido Steel

Raul Gutierrez Deacero

Park Seung-Ha Hyundai Steel Company

Ahmadali Harati Nik IMIDRO

Vinod Mittal Ispat Industries

Hideo Suzuki Nisshin Steel

Alexei Mordashov Severstal

John P. Surma United States Steel

Vladimir Lisin Novolipetsk Steel

Zhu Jimin Shougang Group

Marco Antonio Castello Branco Usiminas

Daniel R. DiMicco Nucor

Miguel Álvarez Cádiz SIDOR

Pradip K. Bishnoi Vizag Steel

Geoff Plummer OneSteel

Olof Faxander SSAB

Jarmo T. Tonteri Ovako

Sushil Kumar Roongta Steel Authority of India (SAIL)

Lee Ku-Taek POSCO

Hiroshi Tomono Sumitomo Metal Industries

Continued on inside back cover

ğM. Aydin Müderrisoglu Eregli Iron and Steel Works

contents

Cover: Tokyo International Forum © Tom McLaughlan. This publication is printed on MultiDesign paper. MultiDesign is certified by the Forestry Stewardship Council as environmentally-responsible paper.

foreword 5

economic sustainability 6

People and safety 10

environment 14

Market development 18

competition and trade 22

the future 26

worldsteel affiliated members and associate member companies 30

Continued on inside back cover

our vision

the steel industry should be profitable over the complete

business cycle. it rewards shareholders and re-invests

in new products and processes. Steel companies minimise their environmental footprint and conduct their operations in a sustainable way. the steel industry has strong growth potential in developing

and industrialised countries. The world steel industry must be free of government involvement that distorts the market and prevents fair competition. steel is a high-tech industry with skilled people working in a

safe environment. it attracts bright people to follow a career

in steel. it aims to be an accident-free industry. Steel is the most innovative, recyclable and sustainable material of the 21st century.

A sustainable steel industry in a sustainable world.

Steelisauniquelyversatilematerial.Itisinvolvedinvirtuallyeveryphaseofourlivesfromhousing,foodsupplyandtransporttoenergydelivery,machineryandhealthcare.Infact,itissoversatilethatprettywelleverythingpeopleuseeverydayiseithermadefromsteelorisprovidedbysteel.

Steelhasfacilitatedourqualityoflife,underpinnedhumankind’sdevelopmentandevenhelpedustounderstandourplanetandtheeco-systemsitsupports.

Withoutbeingawareofit,societynowdependsonsteel.Humankind’sfuturesuccessinmeetingchallengessuchasclimatechange,poverty,populationgrowth,waterdistributionandenergylimitedbyalowercarbonworlddependsonapplicationsofsteel.

Steel’sclaimtoberightforthesetimesisnotsolelybasedonitsclaimasthemostversatileman-madematerial.Recyclabilityisanotherofitskeyperformancecharacteristics.Steelcanberecycledagainandagainwithoutlossofquality.Thisdifferentiatessteelfrommanyothermaterialswherethereisalossinperformanceateachrecycling.

Infiniterecyclingmeansthatsteelisperfectlyalignedtomeetthecontinuingandincreasinglydemandingrequirementsofthe21stcentury.

Theindustrycandrawonalongheritageofcontinuoustechnologicaldevelopment,ofprocessrefinementandproductinnovation,tohelpitspreadbestpracticeandevolvetoworksuccessfullyonnewchallenges.

InOctober2008,after41yearsastheInternationalIronandSteelInstitute,wechangedournametoWorldSteelAssociation(worldsteel).Theworldforsteelhadchangedsubstantiallysince1967andsohadweasanorganisation.

Wearenowatrulyglobalorganisation,representing130oftheworld’sleadingsteelcompanies,includingsevenofthetop10producersinChina.

Ournewnameprovidesasimpledescriptionofourroleandclaritytoourpurpose.

worldsteelistherepresentativebodyofanessentialindustrythattakesaleadershiprolethroughenvironmental,socialandeconomicprogrammes.

Ouractivitiesarefocusedonhelpingtheindustrymeetsociety’srequirements.Werunlifecycleassessmentprogrammestohelpcustomersfactorindifferentsteels’performanceindifferentapplications(p.19).Wecoordinateresearchintonewsteelproductsandprocesses(p.27)becauseithasstronggrowthpotentialbothindevelopingandinindustrialisedcountries.

AndtohelptheindustrymakethemostimmediateimpactonCO

2emissionswithexistingtechnology,we

runaworldwideprogrammethatenablescompaniestoreferencetheirperformanceagainstthebestinclass(p.16).

Steelcompanieswillsucceedinthistechnologically-drivenenvironmentwheretheyhavetheskilledpeopleworkinginasafeenvironment(p.12)andthatisattractivetobrightyoungpeople(p.11).

Tomeetincreaseddemand,minimisesteel’senvironmentalfootprintandcontinueconductingoperationsinasustainablewaywillrequireamassiveinvestmentbytheindustryandnationalgovernments.Thecurrentfinancialcrisishasdonenothingtohelp.Yet,investmentwillhavetobesustainedifprogressistofollow(p.9).Thebestwaytoensurethatthishappensistoencouragedynamiccompetitioninopenandfairmarkets,sothatallproducersandmarketsaresubjecttosharedglobalpressuresthatwillencouragesharedsolutions(p.23).

IanChristmasDirectorGeneral

foreword

6

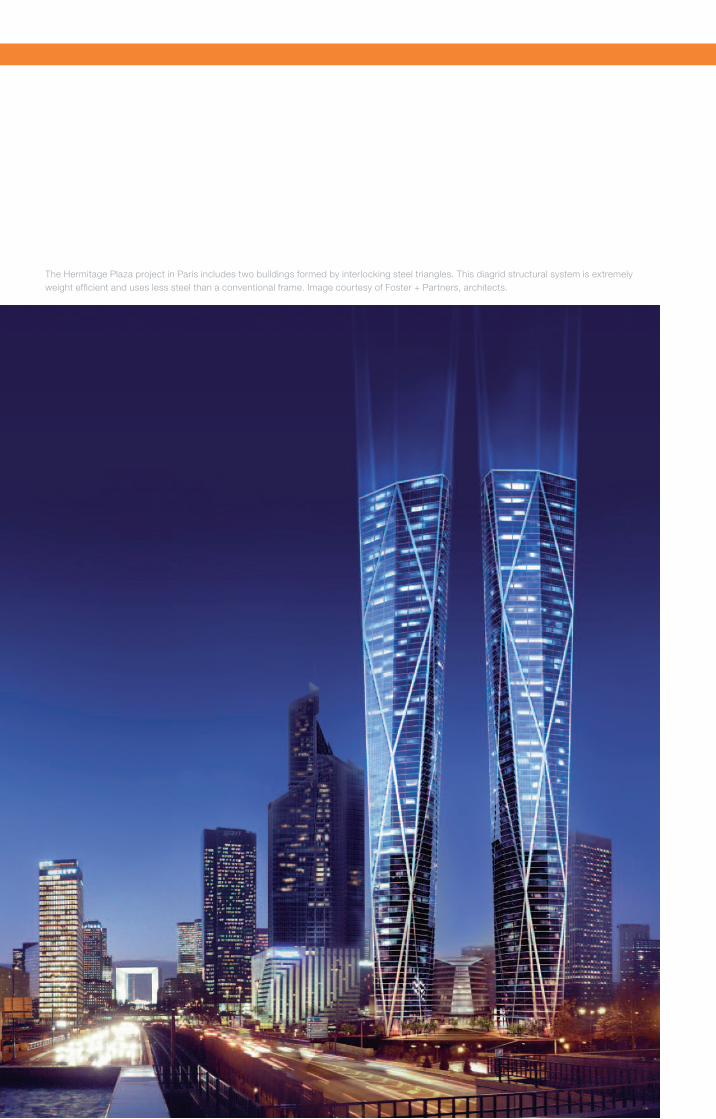

The Hermitage Plaza project in Paris includes two buildings formed by interlocking steel triangles. This diagrid structural system is extremely weight efficient and uses less steel than a conventional frame. Image courtesy of Foster + Partners, architects.

7

econoMic sustainaBility

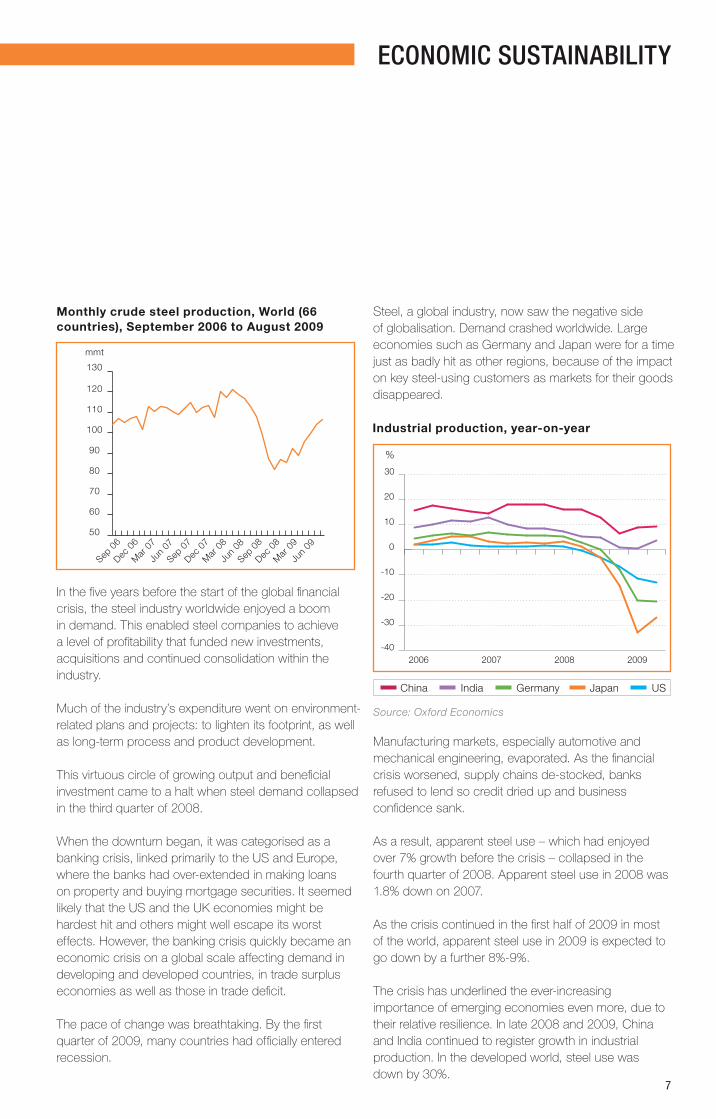

Inthefiveyearsbeforethestartoftheglobalfinancialcrisis,thesteelindustryworldwideenjoyedaboomindemand.Thisenabledsteelcompaniestoachievealevelofprofitabilitythatfundednewinvestments,acquisitionsandcontinuedconsolidationwithintheindustry.

Muchoftheindustry’sexpenditurewentonenvironment-relatedplansandprojects:tolightenitsfootprint,aswellaslong-termprocessandproductdevelopment.

Thisvirtuouscircleofgrowingoutputandbeneficialinvestmentcametoahaltwhensteeldemandcollapsedinthethirdquarterof2008.

Whenthedownturnbegan,itwascategorisedasabankingcrisis,linkedprimarilytotheUSandEurope,wherethebankshadover-extendedinmakingloansonpropertyandbuyingmortgagesecurities.ItseemedlikelythattheUSandtheUKeconomiesmightbehardesthitandothersmightwellescapeitsworsteffects.However,thebankingcrisisquicklybecameaneconomiccrisisonaglobalscaleaffectingdemandindevelopinganddevelopedcountries,intradesurpluseconomiesaswellasthoseintradedeficit.

Thepaceofchangewasbreathtaking.Bythefirstquarterof2009,manycountrieshadofficiallyenteredrecession.

Steel,aglobalindustry,nowsawthenegativesideofglobalisation.Demandcrashedworldwide.LargeeconomiessuchasGermanyandJapanwereforatimejustasbadlyhitasotherregions,becauseoftheimpactonkeysteel-usingcustomersasmarketsfortheirgoodsdisappeared.

Monthly crude steel production, World (66 countries), September 2006 to August 2009

50

60

70

80

90

100

110

120

130

mmt

Sep 0

6

Dec 0

6

Mar

07

Jun

07

Sep 0

7

Dec 0

7

Mar

08

Jun

08

Sep 0

8

Dec 0

8

Mar

09

Jun

09

Manufacturingmarkets,especiallyautomotiveandmechanicalengineering,evaporated.Asthefinancialcrisisworsened,supplychainsde-stocked,banksrefusedtolendsocreditdriedupandbusinessconfidencesank.

Asaresult,apparentsteeluse–whichhadenjoyedover7%growthbeforethecrisis–collapsedinthefourthquarterof2008.Apparentsteelusein2008was1.8%downon2007.

Asthecrisiscontinuedinthefirsthalfof2009inmostoftheworld,apparentsteelusein2009isexpectedtogodownbyafurther8%-9%.

Thecrisishasunderlinedtheever-increasingimportanceofemergingeconomiesevenmore,duetotheirrelativeresilience.Inlate2008and2009,ChinaandIndiacontinuedtoregistergrowthinindustrialproduction.Inthedevelopedworld,steelusewasdownby30%.

Industrial production, year-on-year

China India Germany Japan US

-40

-30

-20

-10

0

10

20

30

%

2006 2007 2008 2009

Source: Oxford Economics

8

World steel capacity development

1062 1062

CAGR 3.3%

CAGR 7.9%

10951170

12451356

14531583

1713

2000 2001 2002 2003 2004 2005 2006 2007 20080

500

1000

1500

2000

mmt

0%

5%

10%

15%

20%

World steel capacity utilisation

50

60

70

80

90

100

%

May

08

88.0%84.4%

70.4%

57.5%

62.3%

61.1%

70.3%

71.7%

Jun

08

Jul 0

8

Aug 0

8

Sep 0

8

Oct 0

8

Nov 0

8

Dec 0

8

Jan

09

Feb

09

Mar

09

Avr 0

9

May

09

Jun

09

Jul 0

9

Aug 0

9

capacity

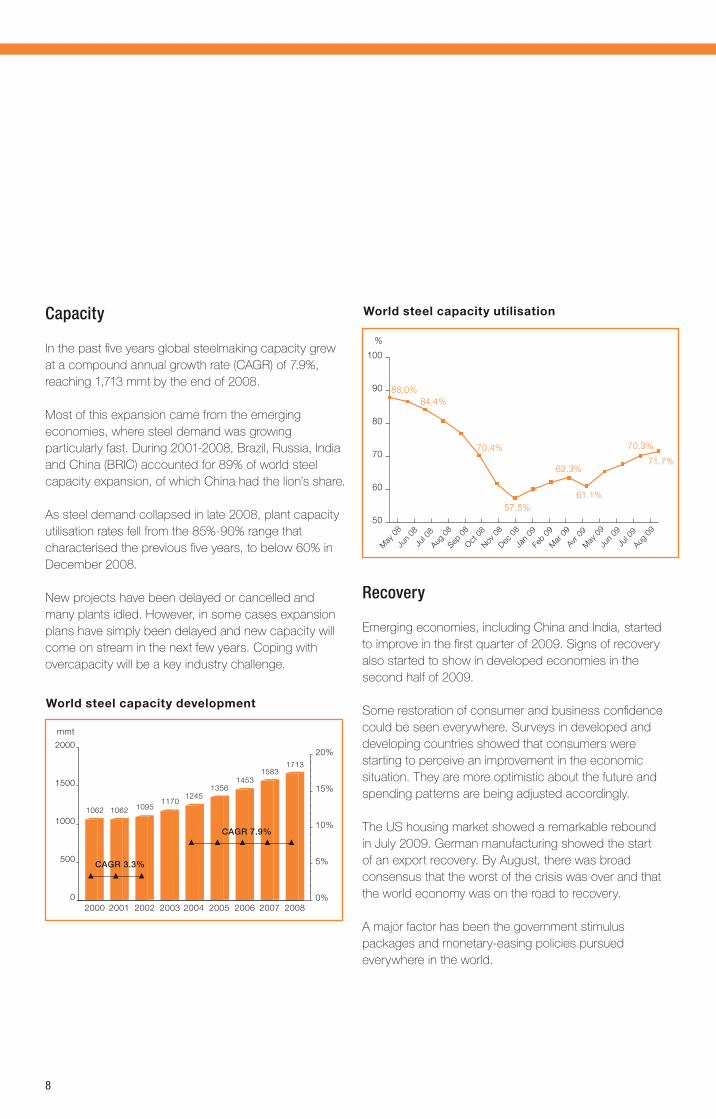

Inthepastfiveyearsglobalsteelmakingcapacitygrewatacompoundannualgrowthrate(CAGR)of7.9%,reaching1,713mmtbytheendof2008.

Mostofthisexpansioncamefromtheemergingeconomies,wheresteeldemandwasgrowingparticularlyfast.During2001-2008,Brazil,Russia,IndiaandChina(BRIC)accountedfor89%ofworldsteelcapacityexpansion,ofwhichChinahadthelion’sshare.

Assteeldemandcollapsedinlate2008,plantcapacityutilisationratesfellfromthe85%-90%rangethatcharacterisedthepreviousfiveyears,tobelow60%inDecember2008.

Newprojectshavebeendelayedorcancelledandmanyplantsidled.However,insomecasesexpansionplanshavesimplybeendelayedandnewcapacitywillcomeonstreaminthenextfewyears.Copingwithovercapacitywillbeakeyindustrychallenge.

recovery

Emergingeconomies,includingChinaandIndia,startedtoimproveinthefirstquarterof2009.Signsofrecoveryalsostartedtoshowindevelopedeconomiesinthesecondhalfof2009.

Somerestorationofconsumerandbusinessconfidencecouldbeseeneverywhere.Surveysindevelopedanddevelopingcountriesshowedthatconsumerswerestartingtoperceiveanimprovementintheeconomicsituation.Theyaremoreoptimisticaboutthefutureandspendingpatternsarebeingadjustedaccordingly.

TheUShousingmarketshowedaremarkablereboundinJuly2009.Germanmanufacturingshowedthestartofanexportrecovery.ByAugust,therewasbroadconsensusthattheworstofthecrisiswasoverandthattheworldeconomywasontheroadtorecovery.

Amajorfactorhasbeenthegovernmentstimuluspackagesandmonetary-easingpoliciespursuedeverywhereintheworld.

9

NAFTA

India

AfricaandMiddleEast

EU(27)

Asiaex.China&India

CIS

China

OtherAmerica

economic sustainability

the china effect

Duringtheeconomiccrisis,ChinaimpressedtheworldwithitsGDPgrowthof7.1%inthefirsthalfof2009andover8%GDPgrowthexpectedfor2009.TheincreaseddemandfromChinahelpedrecoveryinotherAsianeconomies,includingSouthKoreaandTaiwan,China.

ThisreboundwaslargelyattributabletothesuccessoftheUS$586billiondomesticstimuluspackageannouncedattheendof2008tooffsettheslumpinexternaldemandforChinesegoods.However,thejumpstartfromtheChinesegovernmentstimuluspoliciescannotbemaintainedforever.Withnostrongrecoveryinthedevelopedeconomiesforecast,akeychallengewillbehowtomaintaingrowthwithoutthesupportofavibrantexportmarket.

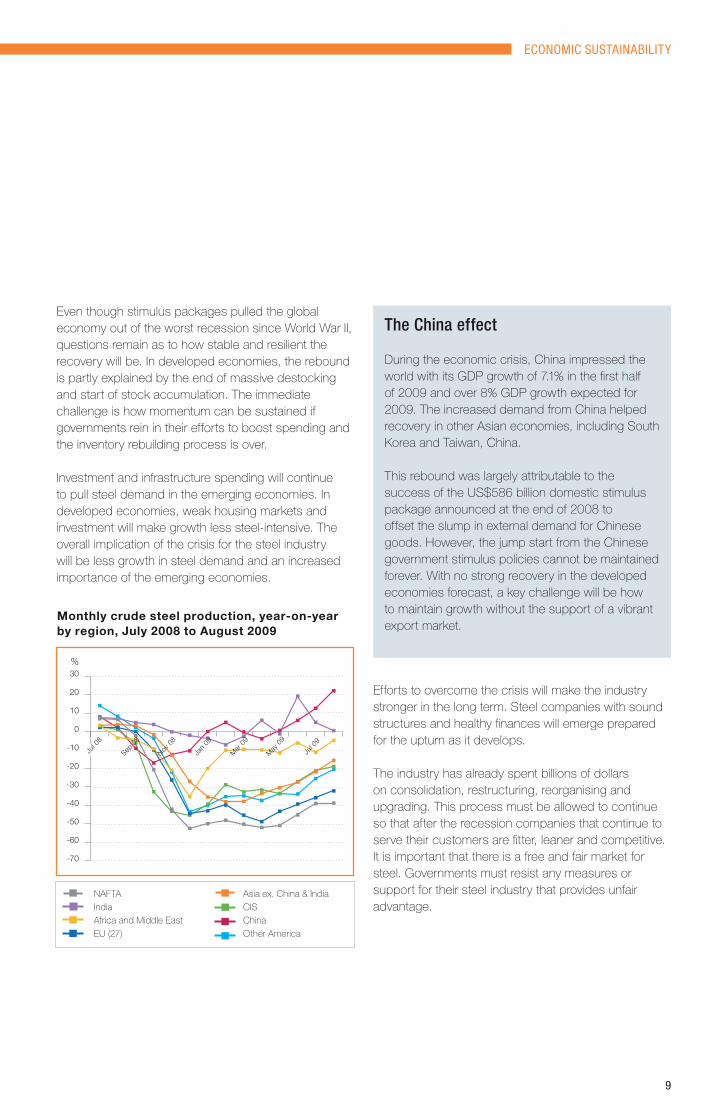

EventhoughstimuluspackagespulledtheglobaleconomyoutoftheworstrecessionsinceWorldWarII,questionsremainastohowstableandresilienttherecoverywillbe.Indevelopedeconomies,thereboundispartlyexplainedbytheendofmassivedestockingandstartofstockaccumulation.Theimmediatechallengeishowmomentumcanbesustainedifgovernmentsreinintheireffortstoboostspendingandtheinventoryrebuildingprocessisover.

Investmentandinfrastructurespendingwillcontinuetopullsteeldemandintheemergingeconomies.Indevelopedeconomies,weakhousingmarketsandinvestmentwillmakegrowthlesssteel-intensive.Theoverallimplicationofthecrisisforthesteelindustrywillbelessgrowthinsteeldemandandanincreasedimportanceoftheemergingeconomies.

Effortstoovercomethecrisiswillmaketheindustrystrongerinthelongterm.Steelcompanieswithsoundstructuresandhealthyfinanceswillemergepreparedfortheupturnasitdevelops.

Theindustryhasalreadyspentbillionsofdollarsonconsolidation,restructuring,reorganisingandupgrading.Thisprocessmustbeallowedtocontinuesothataftertherecessioncompaniesthatcontinuetoservetheircustomersarefitter,leanerandcompetitive.Itisimportantthatthereisafreeandfairmarketforsteel.Governmentsmustresistanymeasuresorsupportfortheirsteelindustrythatprovidesunfairadvantage.

Monthly crude steel production, year-on-year by region, July 2008 to August 2009

-70

-60

-50

-40

-30

-20

-10

0

10

20

30%

Jul 0

8

Sep 0

8

Nov 0

8

Jan

09

Mar

09

May

09

Jul 0

9

10

11

PeoPle and safety

Successfulorganisationsarethosethatdeveloptheirmostimportantresource:thepeopletheyemploy.Onewaytodothisisbyadoptinginnovativetraininganddevelopmentpracticesthathaveameasurableimpactonperformance.

Inthesteelindustry,thereisconstantpressuretoinnovateandimplementadvancesinproductionprocesses.Steelcompaniesmustalsoensurethatemployeeshavetheskillstoexploittheseimprovements.Thisiscrucialtoproductivity,jobsatisfactionandemployeeretention.

Thegrowthofthesteelindustryalsoincreasestheneedtodevelopthenextgenerationofsteelindustryprofessionals.Theindustryrecognisesthatitisimportanttomanageknowledgeofmetallurgyandsteelmaking,particularlywhenmoreprofessorsandexpertsareretiringthanarejoiningtheindustry.

Promoting industry knowledge

Althoughthesteelindustryemployspeoplewithdiverseskillsandcapabilities,steelcompaniesaroundtheworldfaceashortageoftalentinmetallurgy,materialsscience,physics,chemistry,engineeringandmathematics.Asaresult,theindustryhastosecureitsworkforcefromanincreasinglysmallerpoolofpotentialrecruits.

Recognisingthistrend,theindustryhasintroducedmanyinitiativestoattract,developandretaintalentedpeopleaswellasimprovetheindustry’simage.Onesuchinitiative,steeluniversity.org,playsanimportantrole.

steeluniversity.orgisafreeon-lineinitiativedevelopedbyworldsteel.Withfinancialandtechnicalsupportfromworldsteelmembercompanies,itprovideshighlyinteractivee-learningresourcesonsteeltechnologies.Theycoverallaspectsoftheironandsteelmakingprocessesthroughtosteelproducts,theirapplicationsandrecycling.

steeluniversity.orggivesstudentstheopportunitytostudyandapplythebasicscientific,metallurgicalandengineeringprinciples,thatunderpintheproductionanduseofsteel.Atitsheartisaseriesofrealistic,game-likesimulationsofthemainsteelmakingoperations.Studentscaneventestwhattheyhavelearnedastheyprogressthroughthemodules.

Theresourcesareintendedforusebyundergraduatestudents,theirteachers,lecturersandprofessorsandalsobyemployeesandtheirtrainersinsteelcompanies.

extract from the electric arc furnace steelmaking module

Theelectricarcfurnace(EAF)isthemajorproductionrouteforrecyclingsteelscrap,oftenintohigherqualitysteel.Thestepsintheprocessinvolve:

• Selecttheappropriatetypeofscrapandquantitiesforproductionorder

• Dividethescrapintomixedbatches• Chargethescrapintothefurnacewhereitis

meltedusingahighvoltageelectriccurrent• Refinetheproductwiththeinjectionof

appropriateelementsandalloys• Deliverthemoltensteeltotheladle.

Studentlearningoutcomesforthismoduleinclude:

• UnderstandthefunctionofanEAF• Identifythebroadrangeofsteelscrap• Describethechemicalreactionsthattakeplace

duringtherefiningprocess• Understandthedifferentstrategiesfor

maximisingyield.

12

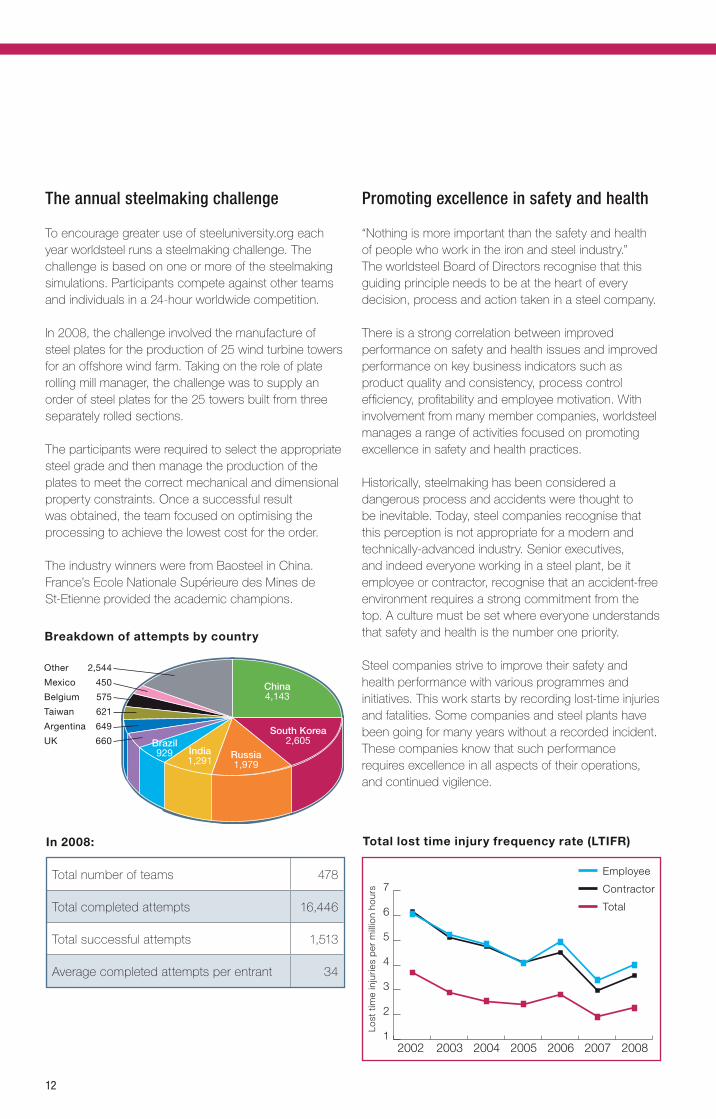

the annual steelmaking challenge

Toencouragegreateruseofsteeluniversity.orgeachyearworldsteelrunsasteelmakingchallenge.Thechallengeisbasedononeormoreofthesteelmakingsimulations.Participantscompeteagainstotherteamsandindividualsina24-hourworldwidecompetition.

In2008,thechallengeinvolvedthemanufactureofsteelplatesfortheproductionof25windturbinetowersforanoffshorewindfarm.Takingontheroleofplaterollingmillmanager,thechallengewastosupplyanorderofsteelplatesforthe25towersbuiltfromthreeseparatelyrolledsections.

Theparticipantswererequiredtoselecttheappropriatesteelgradeandthenmanagetheproductionoftheplatestomeetthecorrectmechanicalanddimensionalpropertyconstraints.Onceasuccessfulresultwasobtained,theteamfocusedonoptimisingtheprocessingtoachievethelowestcostfortheorder.

TheindustrywinnerswerefromBaosteelinChina.France’sEcoleNationaleSupérieuredesMinesdeSt-Etienneprovidedtheacademicchampions.

In 2008:

Totalnumberofteams 478

Totalcompletedattempts 16,446

Totalsuccessfulattempts 1,513

Averagecompletedattemptsperentrant 34

Breakdown of attempts by country

China4,143

South Korea2,605

Russia1,979

India1,291

Brazil929

India1,291

Other 2,544

Mexico 450

Belgium 575

Taiwan 621

Argentina 649

UK 660

Promoting excellence in safety and health

“Nothingismoreimportantthanthesafetyandhealthofpeoplewhoworkintheironandsteelindustry.”TheworldsteelBoardofDirectorsrecognisethatthisguidingprincipleneedstobeattheheartofeverydecision,processandactiontakeninasteelcompany.

Thereisastrongcorrelationbetweenimprovedperformanceonsafetyandhealthissuesandimprovedperformanceonkeybusinessindicatorssuchasproductqualityandconsistency,processcontrolefficiency,profitabilityandemployeemotivation.Withinvolvementfrommanymembercompanies,worldsteelmanagesarangeofactivitiesfocusedonpromotingexcellenceinsafetyandhealthpractices.

Historically,steelmakinghasbeenconsideredadangerousprocessandaccidentswerethoughttobeinevitable.Today,steelcompaniesrecognisethatthisperceptionisnotappropriateforamodernandtechnically-advancedindustry.Seniorexecutives,andindeedeveryoneworkinginasteelplant,beitemployeeorcontractor,recognisethatanaccident-freeenvironmentrequiresastrongcommitmentfromthetop.Aculturemustbesetwhereeveryoneunderstandsthatsafetyandhealthisthenumberonepriority.

Steelcompaniesstrivetoimprovetheirsafetyandhealthperformancewithvariousprogrammesandinitiatives.Thisworkstartsbyrecordinglost-timeinjuriesandfatalities.Somecompaniesandsteelplantshavebeengoingformanyyearswithoutarecordedincident.Thesecompaniesknowthatsuchperformancerequiresexcellenceinallaspectsoftheiroperations,andcontinuedvigilence.

12002 2003 2004 2005 2006 2007 2008

2

3

4

5

6

7

Total lost time injury frequency rate (LTIFR)

Lost

tim

e in

jurie

s p

er m

illio

n ho

urs

Employee

Contractor

Total

13

sharing experience and good practice

In1999,worldsteeldevelopedAccident-FreeSteel,aninitiativethatbroughttogethersafetyspecialistsandlinemanagersfromworldsteelmembercompanies.Throughaseriesofregionalseminars,membersexchangedideas,shareinformationandstatistics,anddevelopedprogrammestodemonstratehowtohaveanaccident-freeenvironmentinasteelplant.

Thisinitiativecontinuestoday.Onceayear,seniorsafetyandhealthmanagersfrommembercompaniesmeettodiscusswaystoimprovesafetyandhealthperformanceandtoexchangeexperiencesonseriousaccidentsandfatalities.

worldsteel safety and health principles

worldsteelrecentlypublishedguidelinestohelpcompaniesimplementsixprinciplesforimprovedsafetyperformance.Adoptingtheseprinciplesatthehighestlevel,membercompaniesdemonstratetheircommitmenttoaninjury-freeandhealthyworkplace.

Theguidelinesarechallengingandrequiresignificantefforttoimplement.The24-pagepublicationhasbeentranslatedintomorethan10languageswiththousandsofcopiesdistributedtomembercompanyemployees.

people and safety

Belowaresomeexamplesoftheimplicationsoftheprinciplesandhoweachemployeecanbeinvolvedintheiradoptionandimplementation.

Onprinciple2–managementresponsibility

• Ifleadersdonotvisiblychange,nothingwill.• Includesafetyandhealthresultsinperformance

assessmentsandothercareeradvancementdecisions.

Onprinciple4–workingsafelyisaconditionofemployment

• Everyemployeeisempoweredtostopanyworkorprocessiftheybelieveittobeunsafeorunhealthy.

excellence recognition award

TheworldsteelSafetyandHealthRecognitionAwardgivesmembercompaniestheopportunitytoshowcasespecificeffortstheyhavemadetoeliminateincidentsandinjuries,andtosharethemwithothercompanies.

In2008fivemembercompaniesreceivedrecognitionfortheireffortsinaddressingthreekeycriteria:

• Howthepracticeorprogrammedemonstratedandappliedtheworldsteelsafetyandhealthprinciples.

• Howtheprojectwasabletodemonstratemeasurableimprovementandquantifytheimprovement.

• Howtheprogrammewasabletodemonstrateitsrelevanceandapplicabilitytoothermembercompanies.

six fundamental principles

• Allinjuriesandwork-relatedillnessescanandmustbeprevented.

• Managementisresponsibleandaccountableforsafetyandhealthperformance.

• Employeeengagementandtrainingisessential.• Workingsafelyisaconditionofemployment.• Excellenceinsafetyandhealthsupports

excellentbusinessresults.• Safetyandhealthmustbeintegratedintoall

businessmanagementprocesses.

14

Detail from the masterplan study of a North Sea ring of offshore wind farms, Zeekracht. Image courtesy of OMA (Office for Metropolitan Architecture).

15

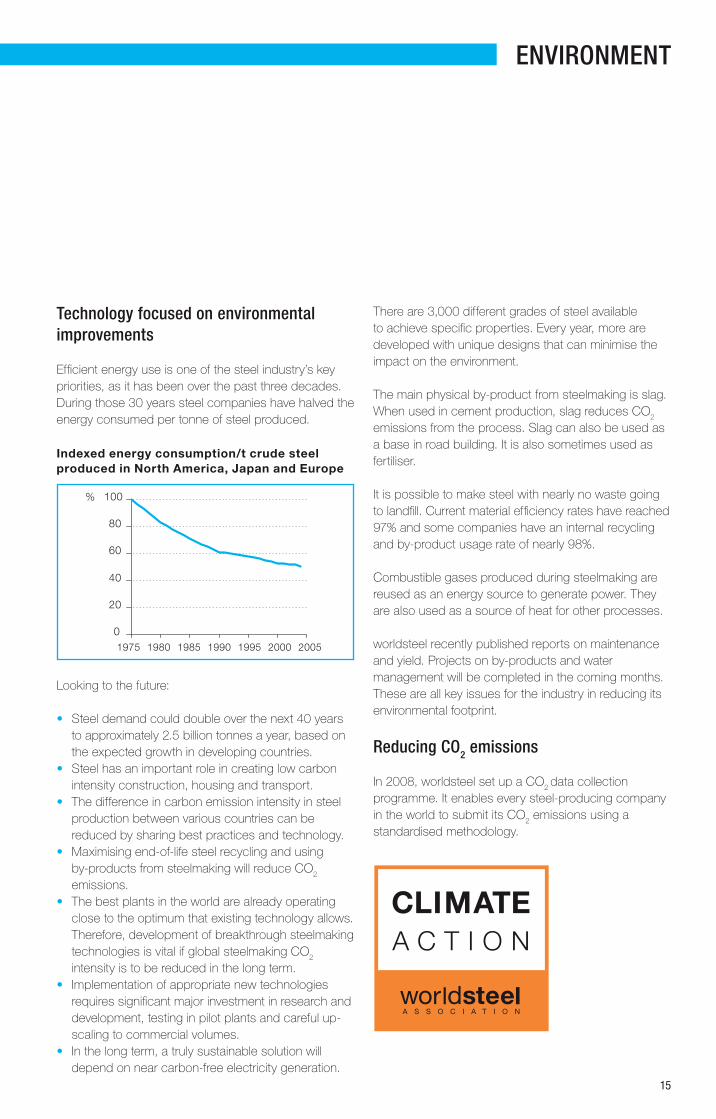

environMent

technology focused on environmental improvements

Efficientenergyuseisoneofthesteelindustry’skeypriorities,asithasbeenoverthepastthreedecades.Duringthose30yearssteelcompanieshavehalvedtheenergyconsumedpertonneofsteelproduced.

Lookingtothefuture:

• Steeldemandcoulddoubleoverthenext40yearstoapproximately2.5billiontonnesayear,basedontheexpectedgrowthindevelopingcountries.

• Steelhasanimportantroleincreatinglowcarbonintensityconstruction,housingandtransport.

• Thedifferenceincarbonemissionintensityinsteelproductionbetweenvariouscountriescanbereducedbysharingbestpracticesandtechnology.

• Maximisingend-of-lifesteelrecyclingandusingby-productsfromsteelmakingwillreduceCO2

emissions.

• Thebestplantsintheworldarealreadyoperatingclosetotheoptimumthatexistingtechnologyallows.Therefore,developmentofbreakthroughsteelmakingtechnologiesisvitalifglobalsteelmakingCO2

intensityistobereducedinthelongterm.

• Implementationofappropriatenewtechnologiesrequiressignificantmajorinvestmentinresearchanddevelopment,testinginpilotplantsandcarefulup-scalingtocommercialvolumes.

• Inthelongterm,atrulysustainablesolutionwilldependonnearcarbon-freeelectricitygeneration.

Thereare3,000differentgradesofsteelavailabletoachievespecificproperties.Everyyear,morearedevelopedwithuniquedesignsthatcanminimisetheimpactontheenvironment.

Themainphysicalby-productfromsteelmakingisslag.Whenusedincementproduction,slagreducesCO2

emissionsfromtheprocess.Slagcanalsobeusedasabaseinroadbuilding.Itisalsosometimesusedasfertiliser.

Itispossibletomakesteelwithnearlynowastegoingtolandfill.Currentmaterialefficiencyrateshavereached97%andsomecompanieshaveaninternalrecyclingandby-productusagerateofnearly98%.

Combustiblegasesproducedduringsteelmakingarereusedasanenergysourcetogeneratepower.Theyarealsousedasasourceofheatforotherprocesses.

worldsteelrecentlypublishedreportsonmaintenanceandyield.Projectsonby-productsandwatermanagementwillbecompletedinthecomingmonths.Theseareallkeyissuesfortheindustryinreducingitsenvironmentalfootprint.

reducing co2 emissions

In2008,worldsteelsetupaCO2datacollection

programme.Itenableseverysteel-producingcompanyintheworldtosubmititsCO2

emissionsusingastandardisedmethodology.

0

20

40

60

80

100%

1975 1980 1985 1990 1995 2000 2005

Indexed energy consumption/t crude steel produced in North America, Japan and Europe

16

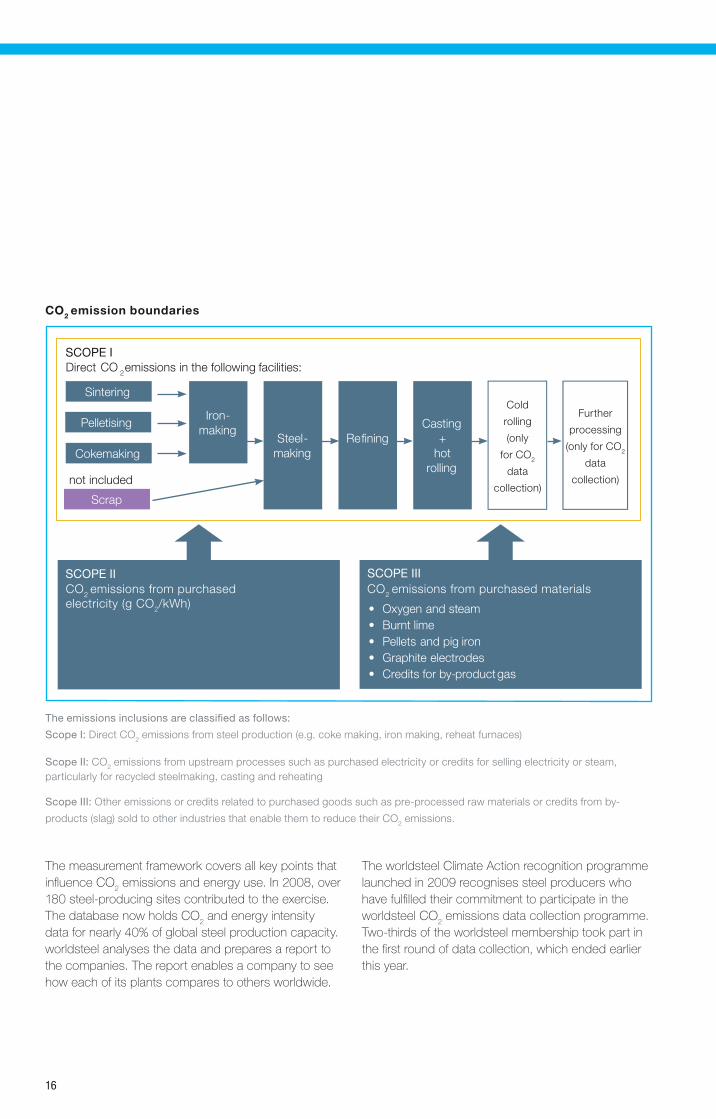

Theemissionsinclusionsareclassifiedasfollows:

ScopeI: Direct CO2 emissions from steel production (e.g. coke making, iron making, reheat furnaces)

ScopeII:CO2 emissions from upstream processes such as purchased electricity or credits for selling electricity or steam, particularly for recycled steelmaking, casting and reheating

ScopeIII: Other emissions or credits related to purchased goods such as pre-processed raw materials or credits from by-

products (slag) sold to other industries that enable them to reduce their CO2 emissions.

ThemeasurementframeworkcoversallkeypointsthatinfluenceCO

2emissionsandenergyuse.In2008,over

180steel-producingsitescontributedtotheexercise.ThedatabasenowholdsCO2

andenergyintensitydatafornearly40%ofglobalsteelproductioncapacity.worldsteelanalysesthedataandpreparesareporttothecompanies.Thereportenablesacompanytoseehoweachofitsplantscomparestoothersworldwide.

TheworldsteelClimateActionrecognitionprogrammelaunchedin2009recognisessteelproducerswhohavefulfilledtheircommitmenttoparticipateintheworldsteelCO2

emissionsdatacollectionprogramme.Two-thirdsoftheworldsteelmembershiptookpartinthefirstroundofdatacollection,whichendedearlierthisyear.

CO2 emission boundaries

SCOPE IDirect CO 2emissions in the following facilities:

Sintering

Cokemaking

Iron-making

Steel-making

RefiningCasting

+ hot

rolling

Pelletising

SCOPE II SCOPE III

• Oxygen and steam• Burnt lime• Pellets and pig iron• Graphite electrodes• Credits for by-productgas

Cold rolling(only

for CO 2

datacollec-tion)

Furtherpro-

cessing(only

for CO 2

datacollec-tion)Scrap

not included

CO2 emissions from purchased electricity (g CO2/kWh)

CO2 emissions from purchased materials

Further

processing

(only for CO2

data

collection)

Cold

rolling

(only

for CO2

data

collection)

17

TheClimateActionprogrammeisopentoallsteelproducers,membersandnon-membersofworldsteelalike.Recognitioncanbeobtainedatacorporateleveloratasitelevel,aslongasCO2

emissionsdataformorethan90%ofthecrudesteelproductionofthecompanyorthesiteissubmitted.Therecognitionisvalidfortwoyears.

ThemodernsteelindustryhaspushedsteelproductionprocessesveryclosetotheirtheoreticalminimumCO2

intensitypertonneofsteeloutput.Someminorgainscanbemadethroughtheincreaseduseofscrapinprimaryproduction.However,scrapavailabilityitselfisalimitingfactor.

worldsteelestimatesthat,basedoncurrentprocesstechnologiesandwithmorescrapavailable,theEAFshareofproductioncouldreach43%ofglobalsteeloutputby2050,upfrom35%today.Alongwithsomeotherchanges,theincreaseinscraprecoverycouldleadtoareductionof200milliontonnesofCO2

.

Production efficiency

Everysteelcompanyandeverysteel-producingcountryisatadifferentpointofmaturityanddevelopment.worldsteel’svisionistohelpsteelmakersachievebest-in-classperformancebyeffectiveandefficientuseoftheirassets.

However,thisisstillnotenoughtomeettheefficiencyimprovementtargetstheindustryneedstomake,giventheprobabledoublingindemandforsteelproductsoverthenext40years.

worldsteelencouragescompaniesandgovernmentstodevelop,testandintroducethenextgenerationofsteelmakingusingbreakthroughtechnologiesforasustainablefuture(seep.27).

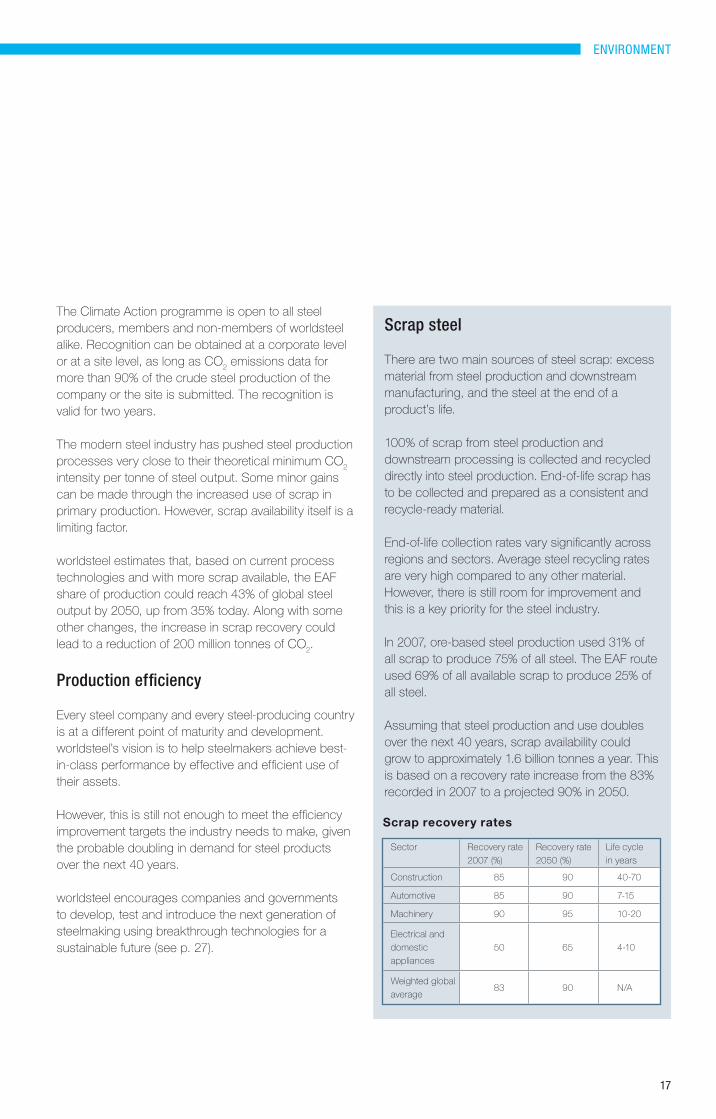

scrap steel

Therearetwomainsourcesofsteelscrap:excessmaterialfromsteelproductionanddownstreammanufacturing,andthesteelattheendofaproduct’slife.

100%ofscrapfromsteelproductionanddownstreamprocessingiscollectedandrecycleddirectlyintosteelproduction.End-of-lifescraphastobecollectedandpreparedasaconsistentandrecycle-readymaterial.

End-of-lifecollectionratesvarysignificantlyacrossregionsandsectors.Averagesteelrecyclingratesareveryhighcomparedtoanyothermaterial.However,thereisstillroomforimprovementandthisisakeypriorityforthesteelindustry.

In2007,ore-basedsteelproductionused31%ofallscraptoproduce75%ofallsteel.TheEAFrouteused69%ofallavailablescraptoproduce25%ofallsteel.

Assumingthatsteelproductionandusedoublesoverthenext40years,scrapavailabilitycouldgrowtoapproximately1.6billiontonnesayear.Thisisbasedonarecoveryrateincreasefromthe83%recordedin2007toaprojected90%in2050.

Sector Recoveryrate

2007(%)

Recoveryrate

2050(%)

Lifecycle

inyears

Construction 85 90 40-70

Automotive 85 90 7-15

Machinery 90 95 10-20

Electricaland

domestic

appliances

50 65 4-10

Weightedglobal

average83 90 N/A

Scrap recovery rates

environment

18

The Future Steel Vehicle will combine alternative powertrains and advanced high-strength steels to reduce the vehicle’s life cycle footprint.

19

Market develoPMent

developing sustainable products

Tenyearsago,thesocialandenvironmentalfootprintofacorporationanditsproductswereafterthoughtstotherealbusinessofcompetingforpositioninthemarketplace.Economicimpactwasoftenonlymeasuredbythebalancesheetandshareprice.

Buttheworldhaschanged.Today,lifecycleassessment(LCA)andcorporateresponsibilityranknearthetopofissuesthatallcompaniesmustaddress.Aplethoraofregulations,standardsandassessmentscreatethepotentialforaddedcosts.Corporatesocialandenvironmentalperformanceisincreasinglydrivingpurchasedecisionsbybusinesscustomerswhoseektoensurethattheirsuppliers’performancealignswiththeirowngoals.

Consequently,steel-usingcustomersareincreasinglydemandinginformationaboutthesustainabilityperformanceofsteelandthecompaniesthatmakesteel.

Fornearly15years,worldsteelhasplayedaleadingroleindefiningtheindustry’sprogresstowardsustainability.CoreactivitiesincludethedevelopmentoftheauthoritativeglobalLCIforsteel,thebi-annualSustainabilityReportthattrackstheindustry’sperformanceagainst11social,economicandenvironmentalindicators,andinitiativesthatproduceindustryconsensusandactionontrendsandissues.

Inthisway,worldsteelhelpsmembercompaniesto:

• ensurethatsteelisaccuratelyandpositivelyrepresentedinLCA-basedstudies

• makemoreinformeddecisionsintheidentificationofmarketopportunities,andthedevelopmentandmarketingofproducts

• respondtocustomerswhoneedLCAdatafortheirownoperating,complianceandmarketingactivities

• supporttechnologyassessmentandthedevelopmentofprocessandenvironmentalimprovementprogrammes

• increasepublicawarenessofsteelasanecessaryandpositivecontributortothegrowthofeconomiesaroundtheworld.

lca: enabling informed decisions

Anaccurateunderstandingoftheimpactamaterialhasongreenhousegas(GHG)emissionsandtheenvironmentisbasedonthetotalemissionsthroughoutallphasesoftheproductlife,includingproduction,useandend-of-life(recyclingordisposal).

Thisapproachisbasedonaninternationallystandardisedmethodology(ISO14040series).Itprovidessystematicbenchmarkingandanalysisoftheknownenvironmentalburdensofindustrialprocesses,suchastotallifetimeGHGemissions,energyconsumptionandwaterconsumption.

TheLCAforsteelisbasedontheworldsteellifecycleinventory(LCI)thatrepresentstheglobalenvironmentalprofileofsteel.

ThethirdroundofLCIdatacollectionwillbecompletedin2009,enablingthedevelopmentofanup-to-dateglobalprofilefor14steelproducts.ThisuniquedatabaseservesasthebasisforLCAstudiesofproductsthatusesteel.

Inaseriesofenvironmentalcasestudies,worldsteeldemonstratesthebenefitsoftoday’shigh-performancesteels.Todate,worldsteelhaspublishedcasestudiesonwindenergy,bridges,automotivesteels,foodcansandnaturalgaspipelines.Thesecasestudiesareavailableonworldsteel.org.

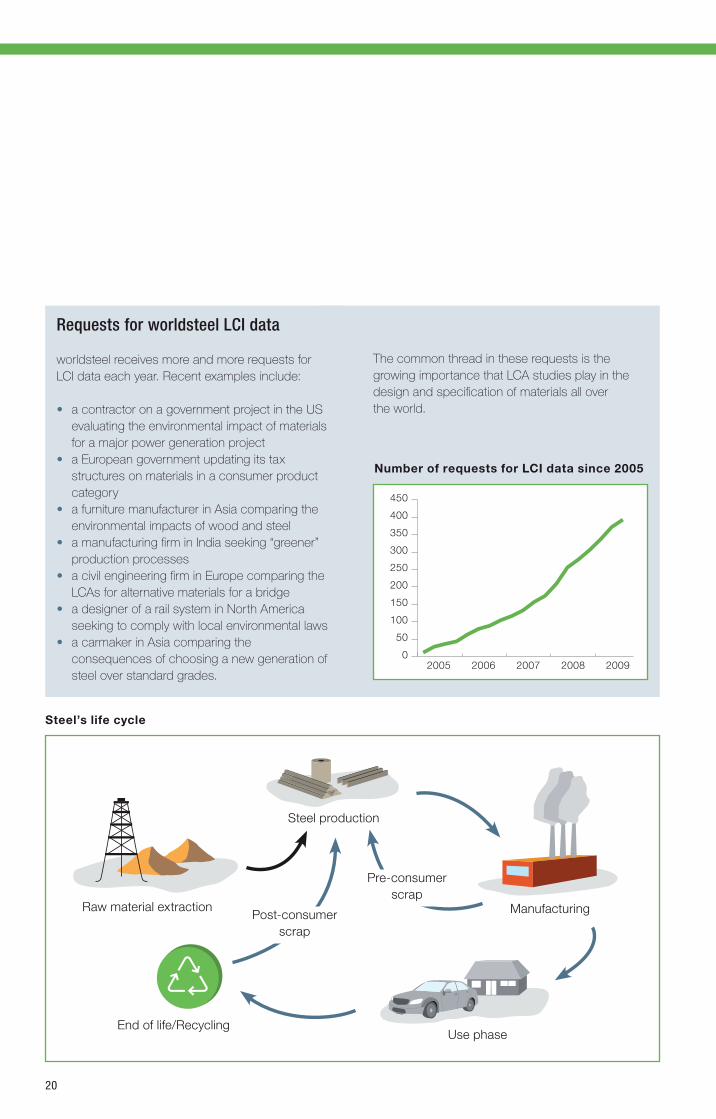

20

Raw material extraction

Steel production

Manufacturing

Use phase End of life/Recycling

Pre-consumer scrap

Post-consumer scrap

Steel’s life cycle

requests for worldsteel lci data

worldsteelreceivesmoreandmorerequestsforLCIdataeachyear.Recentexamplesinclude:

• acontractoronagovernmentprojectintheUSevaluatingtheenvironmentalimpactofmaterialsforamajorpowergenerationproject

• aEuropeangovernmentupdatingitstaxstructuresonmaterialsinaconsumerproductcategory

• afurnituremanufacturerinAsiacomparingtheenvironmentalimpactsofwoodandsteel

• amanufacturingfirminIndiaseeking“greener”productionprocesses

• acivilengineeringfirminEuropecomparingtheLCAsforalternativematerialsforabridge

• adesignerofarailsysteminNorthAmericaseekingtocomplywithlocalenvironmentallaws

• acarmakerinAsiacomparingtheconsequencesofchoosinganewgenerationofsteeloverstandardgrades.

ThecommonthreadintheserequestsisthegrowingimportancethatLCAstudiesplayinthedesignandspecificationofmaterialsallovertheworld.

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009

Number of requests for LCI data since 2005

21

market development

living steel’s third international architecture competition

TheLivingSteelinternationalcompetitionforsustainablehousingstimulatesinnovationinconstruction.Nowinitsthirdyear,thecompetitionaddressestheeconomic,environmentalandsocialaspirationsofagrowingworldpopulation.

Forthe2008competition,architectswereaskedtocreateenergyefficient,single-familydetachedhomesforemployeesofSeverstalinCherepovets,Russia.TheconstructionhadtominimiseGHGemissionsandbeabletowithstandtemperaturesrangingfrom-49°Cto39°C.Thehomesalsohadtobeaffordabletobuildandbuy.

PeterStutchburyArchitectswonfirstprizeinthe2008competition.AnotherAustralianfirm,BlighVollerNieldArchitecture,andCanadianarchitectsRVTRToronto,receivedhonourablementionsfromthejury.

Thewinningfirmreceivesa€50,000prizeandwillbeginworkingwithSeverstalandalocalRussianarchitecttodefinethedesignforconstructioninCherepovets.LivingSteelplanstoshowcaseademonstrationbuildinginlate2009.

The12finalistswerechosenoutof246proposalsfrom52countries.

Manufacturing

advanced steels in housing and automotive designs

Sustainabilityplaysanimportantroleinworldsteel’sotherindustrymarketdevelopmentprogrammes.WorldAutoSteelusesLCAtodemonstratethatadvancedhigh-strengthsteelsandoptimisedvehicledesigncanreducetotallifecycleGHGemissionswhilemaintainingsafetyandaffordability.

WorldAutoSteelhaslaunchedPhase2ofitsFutureSteelVehicle(FSV)programme.Itisaimedatcreatinglightweight,environmentally-friendlysteeldesignsforfuturebatteryelectric,plug-inhybrid,andfuelcellvehicles.Itwillusetheneweststeelgradesandtechnologiesavailable.

Internationalcompetitionsmanagedbyworldsteel’sconstructionprogramme,LivingSteel,demonstratehowsteelcanbeusedininnovativehousingdesigntoproduceunique,environmentallyefficientandaffordablehousing.

Rendering of the winning project for Cherepovets (see box).

22

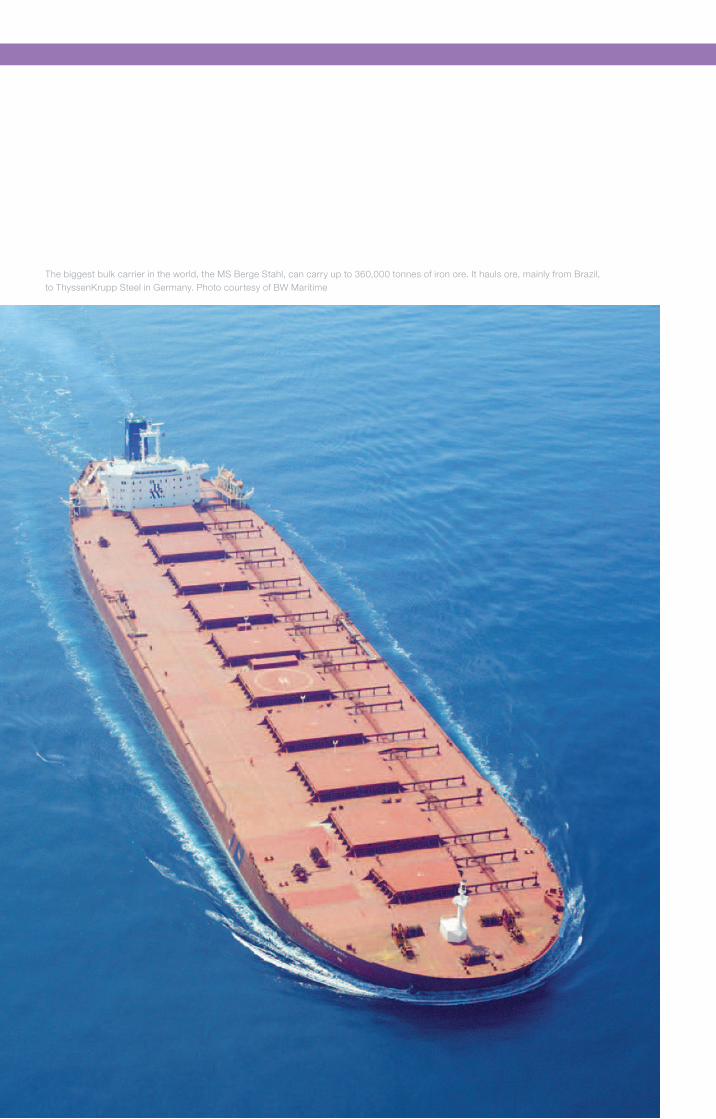

The biggest bulk carrier in the world, the MS Berge Stahl, can carry up to 360,000 tonnes of iron ore. It hauls ore, mainly from Brazil, to ThyssenKrupp Steel in Germany. Photo courtesy of BW Maritime

23

coMPetition and trade

a competitive steel industry worldwide

Oneoftheindustry’sdefiningtrendsoverthelast20orsoyearshasbeenthedeclineinstateownershiparoundtheworld,exceptinChina.Governmentaftergovernmenthassoldoffitsinterestentirelyoropenedupmarketstocompetition.

Themovetoamoremarket-drivenstructureinmanycountrieshascoincidedwithsomeothersignificanttrends.Theseincludeglobalisationandafourfoldincreaseinsteeltradedinternationally.

Thereisalsoamuchstrongerfocusondeliveringcustomer-specifiedsolutions,whichrequiressteelsupplierstoworkcloselywiththeircustomers.

Today,40%oftheworld’ssteelistradedinternationally.Thedangerremainsthatgovernmentswillseektosupportthedomesticindustryinawaythatisanti-competitive.worldsteelhasalong-standingandwell-supportedpositiononbehalfofitsmembersinpromotingfreeandfairtrade.

TheWTOhasconsistentlywarnedthattradebarriersusedbycountriestoprotecttheirindustriesriskdoingmoreharmthangood.

SomeactionsarepermittedunderWTOrules.Theseincludecountervailingactionsagainstunfairtradepracticeswhicharenecessarytomaintainfaircompetition.However,tit-for-tatpoliciesaredangerous,astheGreatDepressionofthe1930sshowed,becausetheyexacerbatethedownwardspiralininternationaltrade.Ifgovernmentsseektoprotectinefficientoperatorsovertheshort-term,theiractionswillinevitablyputcustomercompaniesatalong-termdisadvantage.

worldsteelisanactiveparticipantonplatformswheretheseissuesarediscussed,promotingsteel’smessagesonsustainabilityandfreeandfairtrade.

oecd steel committee

TheOECDSteelCommitteeisthemaingovernmentforumforthediscussionofglobalissuesfacingthesteelindustry.Allthemajorsteel-producingcountriesincludingBRICarerepresentedasmembersorobserversofthecommittee.

TheOECDGoverningCouncildecidedsomeyearsagotoreducetheactivitiesoftheorganisationinindividualindustrialsectorsandasaresulthasreducedthelevelofresourcesavailabletotheSteelCommittee.

Tofillthisgap,worldsteelnowprovidestheexpertreportsthatwereformerlypreparedbytheOECDSecretariat.Twiceayear,worldsteelproducesanoverviewoftheoutlookforsteeldemandbasedonthemostrecentshortrangeoutlooktogetherwithareportonrawmaterialtrendsandareportonsteelmakingcapacitydevelopmentsandutilisation.ItmakesthesereportsavailabletotheOECDSteelCommittee.

TheOECDSteelCommitteefulfilsanimportantrolebutitisworthreiteratingthatitisaforumfordiscussionandincreasedunderstandingratherthanfornegotiationonparticulartopics.

raw materials

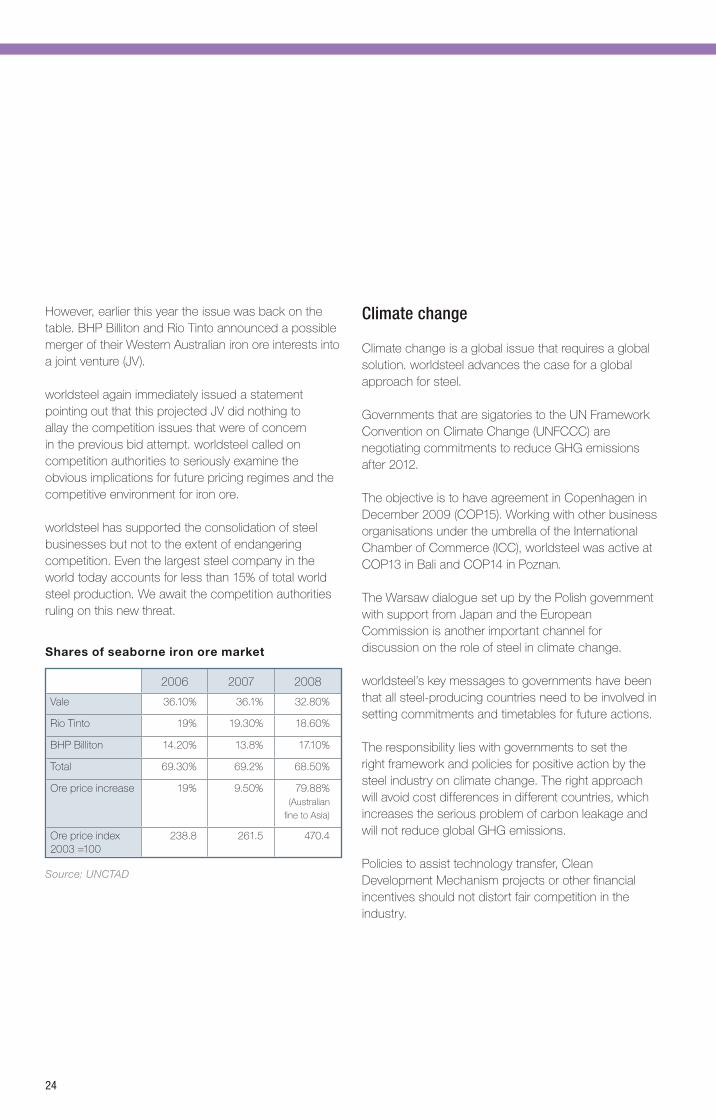

Thelasttwoyearshavebeenarollercoaterridefortheindustryasironore,cokingcoalandscrappriceswentthroughtheroofandthenfellastherecessiontookhold.Atthesametime,thesteelindustrywatchedwithconsiderableconcernasBHPBillitonattemptedtotakeoverRioTinto.Amergeroftwoofthethreecompanieswhodominatemorethan75%oftheworldmarketforseaborneironorecouldonlyhaveledtoanunacceptableconcentrationandcontrolofthemarket.

Thesteelindustryrespondedvigorously.Asaresult,theEuropeanCommissionissuedastatementofobjectionswhichheavilyinfluencedBHPBillitonintowithdrawingitsbid.

24

However,earlierthisyeartheissuewasbackonthetable.BHPBillitonandRioTintoannouncedapossiblemergeroftheirWesternAustralianironoreinterestsintoajointventure(JV).

worldsteelagainimmediatelyissuedastatementpointingoutthatthisprojectedJVdidnothingtoallaythecompetitionissuesthatwereofconcerninthepreviousbidattempt.worldsteelcalledoncompetitionauthoritiestoseriouslyexaminetheobviousimplicationsforfuturepricingregimesandthecompetitiveenvironmentforironore.

worldsteelhassupportedtheconsolidationofsteelbusinessesbutnottotheextentofendangeringcompetition.Eventhelargeststeelcompanyintheworldtodayaccountsforlessthan15%oftotalworldsteelproduction.Weawaitthecompetitionauthoritiesrulingonthisnewthreat.

Shares of seaborne iron ore market

2006 2007 2008

Vale 36.10% 36.1% 32.80%

RioTinto 19% 19.30% 18.60%

BHPBilliton 14.20% 13.8% 17.10%

Total 69.30% 69.2% 68.50%

Orepriceincrease 19% 9.50% 79.88%(Australian

finetoAsia)

Orepriceindex2003=100

238.8 261.5 470.4

Source: UNCTAD

climate change

Climatechangeisaglobalissuethatrequiresaglobalsolution.worldsteeladvancesthecaseforaglobalapproachforsteel.

GovernmentsthataresigatoriestotheUNFrameworkConventiononClimateChange(UNFCCC)arenegotiatingcommitmentstoreduceGHGemissionsafter2012.

TheobjectiveistohaveagreementinCopenhageninDecember2009(COP15).WorkingwithotherbusinessorganisationsundertheumbrellaoftheInternationalChamberofCommerce(ICC),worldsteelwasactiveatCOP13inBaliandCOP14inPoznan.

TheWarsawdialoguesetupbythePolishgovernmentwithsupportfromJapanandtheEuropeanCommissionisanotherimportantchannelfordiscussionontheroleofsteelinclimatechange.

worldsteel’skeymessagestogovernmentshavebeenthatallsteel-producingcountriesneedtobeinvolvedinsettingcommitmentsandtimetablesforfutureactions.

Theresponsibilitylieswithgovernmentstosettherightframeworkandpoliciesforpositiveactionbythesteelindustryonclimatechange.Therightapproachwillavoidcostdifferencesindifferentcountries,whichincreasestheseriousproblemofcarbonleakageandwillnotreduceglobalGHGemissions.

Policiestoassisttechnologytransfer,CleanDevelopmentMechanismprojectsorotherfinancialincentivesshouldnotdistortfaircompetitionintheindustry.

25

Governmentsmustsupportresearchanddevelopmentofbreakthroughtechnologies.Themajorexpenditurerequiredcannotcomefromindustryalone.Governmentfundingneedstobeavailableintermsofprimaryresearchandinthemoresignificantsumsforpilotplants,toprovethetechnicalandeconomicalfeasibilityofnewtechnologies.Already,majorgovernmentalsupportisinplaceintheEUandJapan.Moresupportandnewinitiativesbyothergovernmentsareneeded.

worldsteelhasworkedwiththeInternationalEnergyAgencyonpapersfortheG8onopportunitiesforCO

2reduction.worldsteel’sinputhasbeentoprovide

knowledgeaboutsteelatatechnicallevel.

TheWorldBusinessCouncilforSustainableDevelopmenthasagreedtoamemorandumofunderstandingwithworldsteel.Itpermitsworldsteeltoworkwiththecouncilonclimatechangeissueseventhoughmembershipisrestrictedtocompanies.

Finally,ontechnologytransfer,emissionsreductionandbreakthroughtechnology,worldsteelworkswiththeAsiaPacificPartnershipthroughitsmembercompanies.

asia-Pacific Partnership on clean development and climate

TheAsia-PacificPartnershiponCleanDevelopmentandClimateaimstoacceleratethedevelopmentanddeploymentofcleanenergytechnologies.

ThepartnercountriesareAustralia,Canada,China,India,Japan,KoreaandtheUS.Theyhaveagreedtoworktogetherandwithprivatesectorpartnerstomeetgoalsforenergysecurity,nationalairpollutionreductionandclimatechangeinwaysthatpromotesustainableeconomicgrowthandpovertyreduction.

Thepartnershipfocusesonexpandinginvestmentandtradeincleanerenergytechnologies,goodsandservicesinkeymarketsectors.Itsmembershaveapprovedeightpublic-privatesectortaskforces,includingoneforsteel.

Thesteeltaskforce’sobjectivesareto:

• developsector-relevantbenchmarkandperformanceindicators

• facilitatethedeploymentofbestpracticesteeltechnologies

• increasecollaborationbetweenrelevantpartnershipcountrygovernment,researchandindustrysteel-relatedinstitutions

• developprocessestoreduceenergyusage,airpollutionandGHGemissionsfromsteelproduction

• increaserecyclingacrossthepartnership.

Actionwillfocusonsecuringimprovedbenchmarkingandreporting,energyandmaterialefficienciesandtechnologydevelopmentanddeployment.

competition and trade

26

Design for a new high speed train station in Florence, Italy. Image courtesy of Foster + Partners, architects.

27

working for the future

Invirtuallyeveryphaseofourlives,steelplaysanessentialrole.Therails,roadsandvehiclesthatmakeupourtransportsystemsusesteel.Steelprovidesastrongframeworkandconnectionsinthebuildingswherewework,learnandlive.Itprotectsanddeliversourwaterandfoodsupply.Itisabasiccomponentintechnologiesthatgenerateandtransmitenergy.

Steelplaysacriticalrolesimplybecausenoothermaterialhasthesameuniquecombinationofstrength,formabilityandversatility.Consequently,asnationsaroundtheworldseektoimprovetheirstandardsoflivingandliftpopulationsoutofpoverty,itisinevitablethatthedemandforsteelwillincrease.

Evenasitaddressestheneedsandchallengesoftoday’seconomicenvironment,thesteelindustryislookingaheadatthechallengesthatarejustoverthehorizon.Materialsthatarestrongerandmeethigherenvironmentalstandardswillbeneeded.

Newgenerationsofsteelcontinuetobedevelopedthatmakeitpossibleformanufacturersandbuilderstoimplementdurable,lightweightdesigns.Furthermore,steelcanbeendlesslyrecycledwithoutlossofstrength,durabilityoranyofitsotherdistinctiveproperties.

Thesteelindustryisworkingondeliveringlong-termsolutions,whilecontinuingtomeetitscustomers’requirementsoftoday.worldsteel’sfourbuildingblocksunderpintheindustry’sdirectionforthefuture.Theyareto:

• reduceCO2intensitypertonneofsteel

• spreadbestpracticeacrosstheindustry• researchanddevelopbreakthroughtechnologiesfor

steelmaking• usesteelordevelopnewsteelproductsin

applicationsmakingahighimpactonendproductlifecycleperformanceandsustainability.

ThefirststeptowardsreducingCO2emissions

hasbeentoestablishacommonmethodologyformeasuringCO2

intensity.Seepages15-16formoreaboutthemeasurementframework.

Breakthrough technologies

TomakeasignificantdifferenceinCO2intensity,

newsteelmakingtechniquesareneeded.In2003,worldsteellaunchedtheCO2

BreakthroughCoordinationProgrammetoexchangeinformationonnewtechnologiesthatcanberesearchedanddevelopedinagloballycoordinatedway.Theprogrammereflectsthecommitmentofthesteelindustrytorespondtothechallengeofclimatechange.

Ore-basedsteelmakingusingblastfurnaceshashighercarbonintensitypertonneofsteelproducedthantheEAFroute,sothefocusisontheblastfurnaceroutefirst.

ThisisthebiggestcollaborativeR&Dprojectcoordinationeverundertakenbythesteelindustry.

Researchistakingplacein:

• theEU(ultra-lowCO2steelmaking,orULCOS,

supportedby48EUcompaniesand15EUgovernments)

• theUS(theAmericanIronandSteelInstitute)• Canada(theCanadianSteelProducersAssociation)• SouthAmerica(ArcelorMittalBrazil)• Japan(JapaneseIronandSteelFederation)• Korea(POSCO)• China(Baosteel)andTaiwan(ChinaSteel)and• Australia(BluescopeSteel/OneSteelandCSIRO

coordination).

Thevariousprogrammescallonarangeofindustrialexpertisefromsteelproducers,energygenerators,plantdesignersandequipmentmanufacturers.Theyalsocallonscientificexpertisefromgovernment-fundedmaterialsresearchandacademicinstitutions.

the future

28

TheprogrammeshaveidentifiedthemostpromisingsteelmakingtechnologiesthatpotentiallyreduceCO2

emissionstoatmospherebymorethan50%.Researchisnowfocusedonfeasibilityatvariouslevelsofproduction,fromlaboratoryworktopilotplantdevelopmentandeventuallycommercialimplementation.

AsignificantamountofCO2willstillbeproducedif

carbonisusedasthereducingagentforironore.Onetechniquefordealingwiththegasistocaptureitandstoreit.Thisiscalledcarboncaptureandstorage(CCS).

Thiswillrequiretechnicalsolutionsforcleaningthegasandtransportingitthroughpipesintostoragesites.Thesearenotalwaysconvenientlylocatednearproductionfacilities.Storageoptionsincludeexhaustedgasfields,oldcoalminesorsalineaquifers.CCSwillrequireinter-governmentalcooperationonpoliciesandregulationstoallowtransferofthegastosuitablesites.

Coal-basedironmakingtechnologiesassociatedwithCCSarethemostlikelycandidatesfordevelopment.Hydrogenandelectrolysisarefurtherintothefuture,asthesetechnologieswillrequirere-engineeringofsteelproductionandthedevelopmentofnewprocessesfromfirstprinciples(seebox).

technologies of the future

TopgasrecyclingincombinationwithCCSBlastfurnacetopgasrecyclingreliesonseparationoftheoffgasessothattheusefulcomponentscanberecycledintothefurnaceasareducingagent.TheCO2

hastobecaptured,transportedandstored.

Smeltingreduction(HISARNA)incombinationwithCCSHISARNAisbasedonbath-smelting.Itcombinescoalpreheatingandpartialpyrolysisinareactor,ameltingcyclonefororemeltingandasmeltervesselforfinalorereductionandironproduction.CCSisalsoakeyrequirementforthisprocess.

NewdirectreductionincombinationwithCCSTherewouldbeasinglesourceofCO2

fromthedirectreductionfurnace.Theoff-gaseswouldbestoredusingCCS.

AlkalineelectrolysisofironoreElectrolysisiscommonlyusedtoproducemetalsotherthansteel.Forsteelmaking,largeamountsofelectricitywouldbeneeded.TheprocesswoulddependonaCO2

-leanelectricitysourcesuchashydroornuclearpower.

MoltenoxideelectrolysisMoltenoxideelectrolysisworksbypassinganelectriccurrentthroughmoltenslagfedwithironoxide.Theironoxidebreaksdownintoliquidironandoxygengas.Nocarbondioxideisproduced.ThisprocesswoulddependonaCO2

-leanelectricitysource.

HydrogenflashsmeltingIronisreducedfromironoreathightemperatures(above1,300°C)andwithveryshortreactiontimes.NoCO2

isemittedbutproducinghydrogenrequireslargeamountsofCO

2-leanelectricity.

29

the future

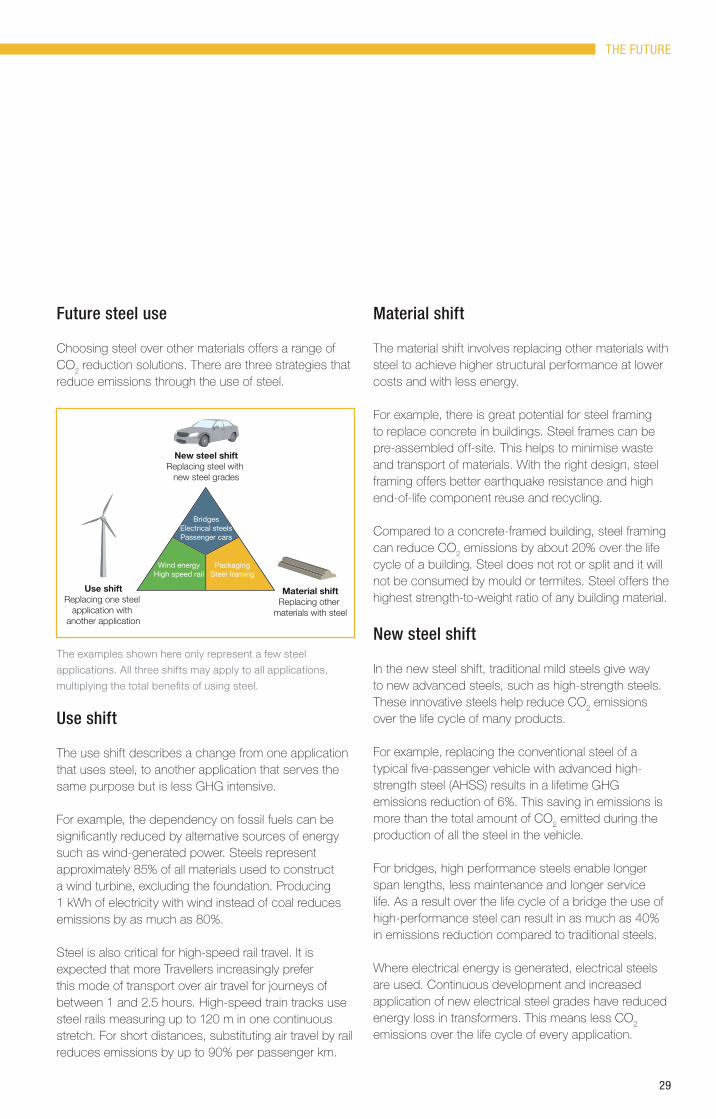

Material shift

Thematerialshiftinvolvesreplacingothermaterialswithsteeltoachievehigherstructuralperformanceatlowercostsandwithlessenergy.

Forexample,thereisgreatpotentialforsteelframingtoreplaceconcreteinbuildings.Steelframescanbepre-assembledoff-site.Thishelpstominimisewasteandtransportofmaterials.Withtherightdesign,steelframingoffersbetterearthquakeresistanceandhighend-of-lifecomponentreuseandrecycling.

Comparedtoaconcrete-framedbuilding,steelframingcanreduceCO2

emissionsbyabout20%overthelifecycleofabuilding.Steeldoesnotrotorsplitanditwillnotbeconsumedbymouldortermites.Steeloffersthehigheststrength-to-weightratioofanybuildingmaterial.

new steel shift

Inthenewsteelshift,traditionalmildsteelsgivewaytonewadvancedsteels,suchashigh-strengthsteels.TheseinnovativesteelshelpreduceCO2

emissionsoverthelifecycleofmanyproducts.

Forexample,replacingtheconventionalsteelofatypicalfive-passengervehiclewithadvancedhigh-strengthsteel(AHSS)resultsinalifetimeGHGemissionsreductionof6%.ThissavinginemissionsismorethanthetotalamountofCO2

emittedduringtheproductionofallthesteelinthevehicle.

Forbridges,highperformancesteelsenablelongerspanlengths,lessmaintenanceandlongerservicelife.Asaresultoverthelifecycleofabridgetheuseofhigh-performancesteelcanresultinasmuchas40%inemissionsreductioncomparedtotraditionalsteels.

Whereelectricalenergyisgenerated,electricalsteelsareused.Continuousdevelopmentandincreasedapplicationofnewelectricalsteelgradeshavereducedenergylossintransformers.ThismeanslessCO2

emissionsoverthelifecycleofeveryapplication.

use shift

Theuseshiftdescribesachangefromoneapplicationthatusessteel,toanotherapplicationthatservesthesamepurposebutislessGHGintensive.

Forexample,thedependencyonfossilfuelscanbesignificantlyreducedbyalternativesourcesofenergysuchaswind-generatedpower.Steelsrepresentapproximately85%ofallmaterialsusedtoconstructawindturbine,excludingthefoundation.Producing1kWhofelectricitywithwindinsteadofcoalreducesemissionsbyasmuchas80%.

Steelisalsocriticalforhigh-speedrailtravel.ItisexpectedthatmoreTravellersincreasinglypreferthismodeoftransportoverairtravelforjourneysofbetween1and2.5hours.High-speedtraintracksusesteelrailsmeasuringupto120minonecontinuousstretch.Forshortdistances,substitutingairtravelbyrailreducesemissionsbyupto90%perpassengerkm.

BridgesElectrical steelsPassenger cars

New steel shiftReplacing steel with

new steel grades

Use shiftReplacing one steel

application with another application

Material shiftReplacing other

materials with steel

PackagingSteel framing

Wind energyHigh speed rail

The examples shown here only represent a few steel

applications. All three shifts may apply to all applications,

multiplying the total benefits of using steel.

future steel use

ChoosingsteeloverothermaterialsoffersarangeofCO

2reductionsolutions.Therearethreestrategiesthat

reduceemissionsthroughtheuseofsteel.

30

worldsteel affiliated MeMBers and associate MeMBer coMPanies

affiliated members

ABM-AssociaçãoBrasileiradeMetalurgiaeMateriais

AmericanIronandSteelInstitute(AISI)

APEAL

TheAfricanIronandSteelAssociation

ArabIronandSteelUnion

ArcelorMittalResearch

ArgentineSteelProducersAssociation

(CIS-CentrodeIndustrialesSiderurgicos)

ASMET,TheAustrianSocietyforMetallurgy&Materials

AssociationforIron&SteelTechnology(AIST)

AssociationofFinnishSteelandMetalProducers

AssociationoftheHungarianIronandSteelIndustry

(MagyarVas-ésAcélipariEgyesülés-MVAE)

AustralianSteelInstitute

CANACERO

CanadianSteelProducersAssociation(CSPA)

CentredeRecherchesMétallurgiques(CRM)

CentroNacionaldeInvestigacionesMetalúrgicas(CENIM)

CentroSviluppoMaterialiSpA(CSM)

ChinaChamberofCommerceforMetallurgyIndustry

ChinaIron&SteelAssociation(CISA)

TheChineseSocietyforMetals(CSM)

EUROFER

FEDERACCIAI

FédérationFrançaisedel’Acier(F.F.A.)

GroupementdelaSidérurgie/StaalindustrieVerbond(GSV)

HutniczaIzbaPrzemysłowo-HandlowaHIPH

(PolishSteelAssociation)

TheIndianInstituteofMetals

TheInstituteofMaterials,Minerals&Mining

InstitutoAçoBrasil(BrazilianSteelInstitute)

InstitutoLatinoamericanodelFierroyelAcero(ILAFA)

InternationalMetallurgistsUnion

IronandSteelFederationSMN

TheIronandSteelInstituteofJapan

IronandSteelInstituteofThailand

TheJapanIronandSteelFederation(JISF)

Jernkontoret

KoreaIronandSteelAssociation(KOSA)

MalaysianIron&SteelIndustryFederation(MISIF)

RomanianSteelProducers’Union-UniRomSider

SouthAfricanIronandSteelInstitute(SAISI)

SouthEastAsiaIronandSteelInstitute(SEAISI)

Staalinfocentrum/CentreInformationAcier

StahlinstitutVDEh(SteelInstituteVDEh)

TheSteelFederation(Hutnictvíželeza,a.s.-HZ)

SteelManufacturersAssociation(SMA)

SwereaMEFOS

TaiwanSteelandIronIndustriesAssociation

TurkishIronandSteelProducersAssociation(TISPA)

UKSteel

UnióndeEmpresasSiderúrgicas(UNESID)

WirtschaftsvereinigungStahl

associate member companies

AcciaieriaArvedi

AcciaierieBertoliSafau

ACERINOX

AichiSteelCorporation

AsilÇelikA.S.

BaoshanIron&SteelCo.,Ltd.StainlessSteelBusinessUnit

BentelerSteel/Tube

BÖHLERUDDEHOLM

CapeGate

CapeTownIron&SteelWorks(CISCO)

CogneAcciaiSpeciali

ColumbusStainless

DaidoSteel

DeutscheEdelstahlwerke(DEW)

DillingerHüttenwerke

DufercoBelgium

Electrotherm

ERAMET

GeorgsmarienhütteHolding

GerdauAçosEspeciaisPiratini

HalyvourgikiInc.

JindalSteelandPower

JSL

LatrobeSpecialtySteelCompany

NakayamaSteelWorks

NatSteelHoldings

Nedstaal

NipponKinzoku

NipponMetalIndustry

NipponYakinKogyo

NorthAmericanStainless(NAS)

OsakaSteel

Outokumpu

PanchmahalSteel

QatarSteelCompany

SanyoSpecialSteel

SIDETUR

SIJSlovenianSteelGroup

TangEngIronWorks

ThainoxStainless

TheTimkenCompany

UGITECH

VirajGroup

WalsinLihwaCorp.,YenshueiPlant

YiehUnitedSteelCorporation(YUSCO)

ZhangjiagangPohangStainlessSteel(ZPSS)

worldsteel affiliated MeMBers and associate MeMBer coMPanies

Jorge Johannpeter Gerdau

Jürgen R. Großmann Georgsmarienhütte Holding

Andrey Varichev Metalloinvest Management Company

Wang Yifang Handan Iron and Steel Group

Igor Syry Metinvest Holding

Herbert Eichelkraut Hüttenwerke Krupp Mannesmann

Shoji Muneoka Nippon Steel

Hiroshi Sato Kobe Steel

Alexander Frolov Evraz Group

Song Lanxiang Laiwu Steel Group

Paul O’Malley BlueScope Steel

Ahmed Abdel Aziz Ezz EZZ Steel

Victor F. Rashnikov Magnitogorsk Iron & Steel Works

Francisco Rubiralta CELSA Group

Chang Chia-Juch China Steel

Murray McClean Commercial Metals Company

Benjamin Steinbruch Companhia Siderúrgica Nacional

Kirby Adams Corus Group

Sakari Tamminen Rautaruukki

B. Muthuraman Tata Steel

Fabio Riva Riva Fire

Paolo Rocca Techint Group

Klaus Harste Saarstahl

Daniel Novegil Ternium Hylsa

Wolfgang Leese Salzgitter

Karl-Ulrich KöhlerThyssenKrupp

Hassan Al-Ghannam Al-Buainain Saudi Basic Ind. Corp. (HADEED)

Dmitry Pumpyanskiy TMK

Benedikt Niemeyer Schmolz + Bickenbach Group

Jiri Cienciala Třinecké železárny

worldsteel Board of directors 2008-2009

Ian Christmas World Steel Association

Wolfgang Eder voestalpine

Deng Qiling Wuhan Steel Group

32

WorldSteelAssociation

RueColonelBourg120

B-1140Brussels

Belgium

T:+32(0)27028900

F:+32(0)27028899

C413OfficeBuilding

BeijingLufthansaCenter

50LiangmaqiaoRoad

ChaoyangDistrict

Beijing100125

China

T:+861064646733

F:+861064646744

worldsteel.org