Embed Size (px)

Citation preview

23rd Annual CFO Roundtable and Tax Director Workshop

Las Vegas, NevadaSeptember 24-26, 2017

Page 2 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Disclaimer

► Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited located in the US.

► The Ernst & Young organization is divided into five geographic areas and firms may be members of the following entities: Ernst & Young Americas LLC, Ernst & Young EMEIA Limited, Ernst & Young Far East Limited and Ernst & Young Oceania Limited. These entities do not provide services to clients.

► This presentation is ©2015 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Any US tax advice contained herein was not intended or written to be used, and cannot be used for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

► The views expressed by speakers at this event are not necessarily those of Ernst & Young LLP.

Page 3 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

AgendaGlobal Mobility Workforce

Topic1. Disaster relief for employees

2. Employer provided meals and the Boston Bruins

3. State wage withholding and reporting

4. Reporting and withholding for US inbound and outbound employees

Employer Provided Disaster Relief

Page 5 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

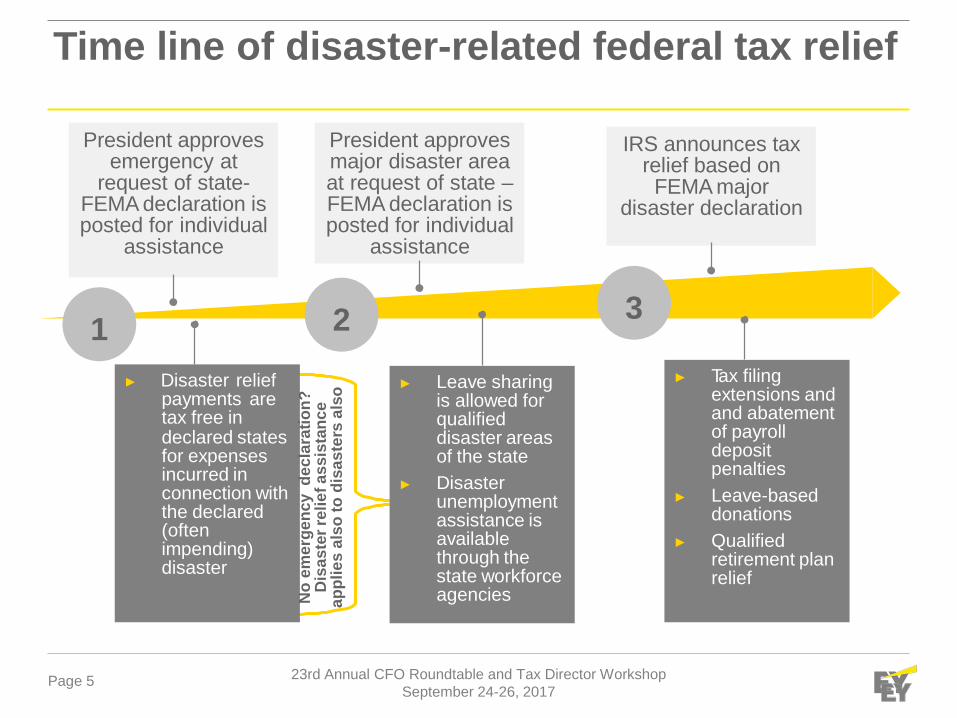

Time line of disaster-related federal tax relief

President approves emergency at

request of state-FEMA declaration is posted for individual

assistance

► Disaster reliefpayments aretax free indeclared states for expenses incurred in connection with the declared (often impending) disaster

1

President approves major disaster area at request of state –FEMA declaration is posted for individual

assistance

► Leave sharing is allowed for qualified disaster areas of the state

► Disaster unemployment assistance is available through the state workforce agencies

2

IRS announces taxrelief based on

FEMA major disaster declaration

3

► Tax filing extensions and and abatement of payroll deposit penalties

► Leave-based donations

► Qualified retirement plan relief

No

emer

genc

y de

clar

atio

n?

Dis

aste

rrel

iefa

ssis

tanc

e ap

plie

sal

soto

disa

ster

sal

so

Page 6 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

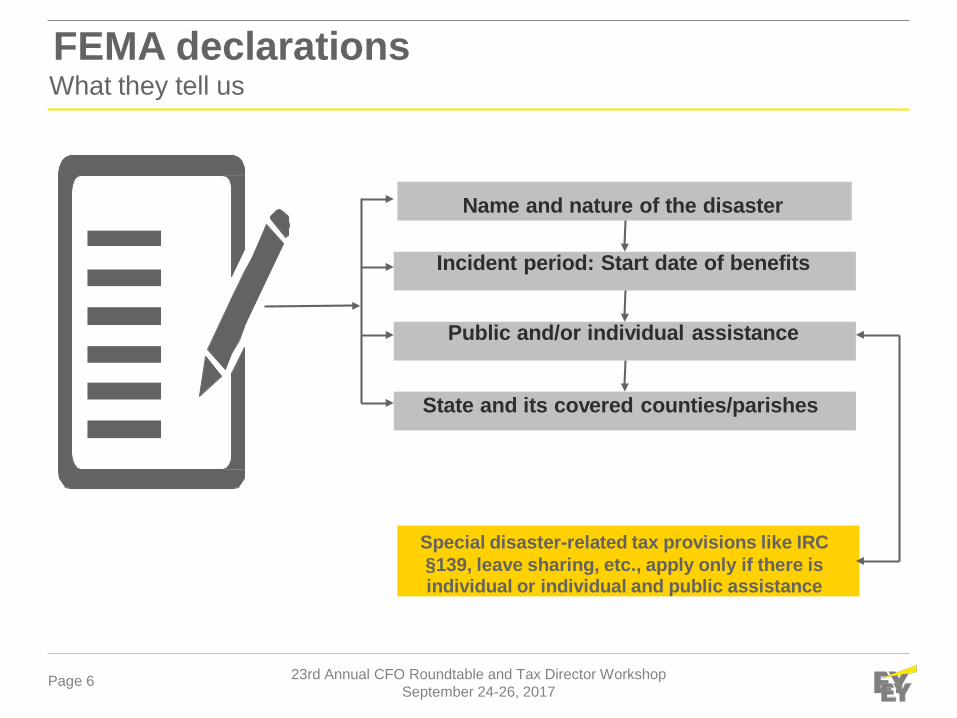

FEMA declarationsWhat they tell us

Name and nature of the disaster

Incident period: Start date of benefits

Public and/or individual assistance

State and its covered counties/parishes

Special disaster-related tax provisions like IRC§139, leave sharing, etc., apply only if there is individual or individual and public assistance

Page 7 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

How is state defined?

► Generally, (an exception applied, for instance, for Ebola andHaiti), tax-favored disaster relief provisions are available only to individuals in a presidentially-declared disaster areadefined in IRC §165(h)(3)(c)(i)

► As stated in the FEMA declaration process

A State also includes the District of Columbia, Puerto Rico, the Virgin Islands, Guam, American Samoa, and the Commonwealth of the Northern Mariana Islands.The Republic of Marshall Islands and the Federated States of Micronesia are alsoeligible to request a declaration and receive assistance through the Compacts ofFree Association

► Payments made to persons not meeting the state definition (i.e., a foreign person) are foreign-sourced wages not subject US reporting and withholding

Page 8 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

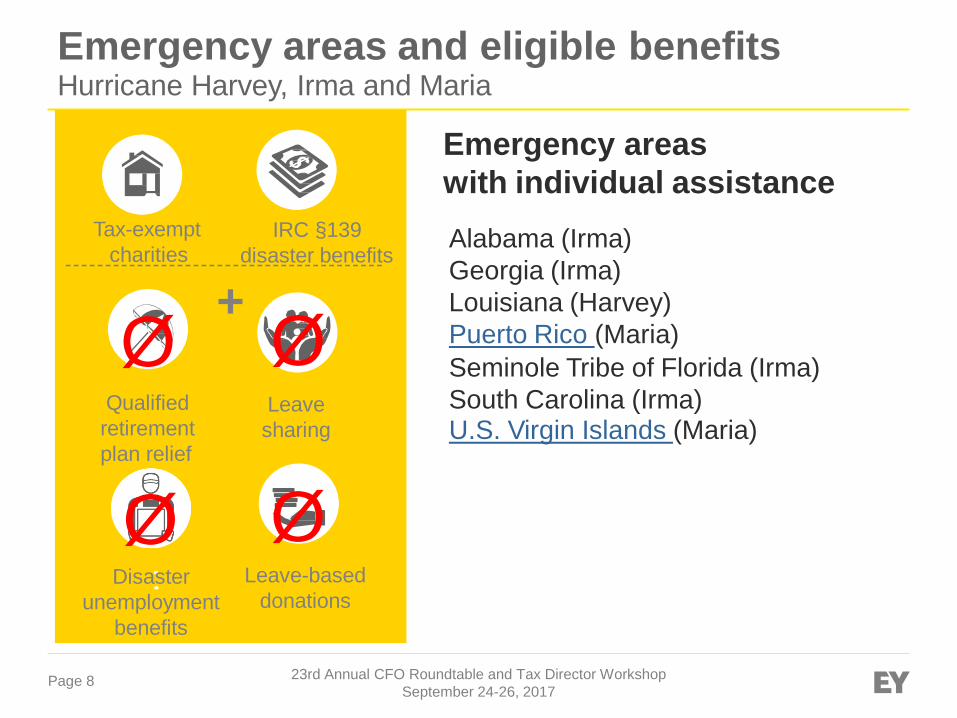

Emergency areas and eligible benefitsHurricane Harvey, Irma and Maria

Emergency areaswith individual assistanceAlabama (Irma) Georgia (Irma) Louisiana (Harvey) Puerto Rico (Maria)Seminole Tribe of Florida (Irma) South Carolina (Irma)U.S. Virgin Islands (Maria)

Tax-exempt IRC §139charities disaster benefits

ØLeave-based

donations

ØLeave

sharing

ØQualifiedretirementplan relief

ØDisaster

unemployment benefits

+

Page 9 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

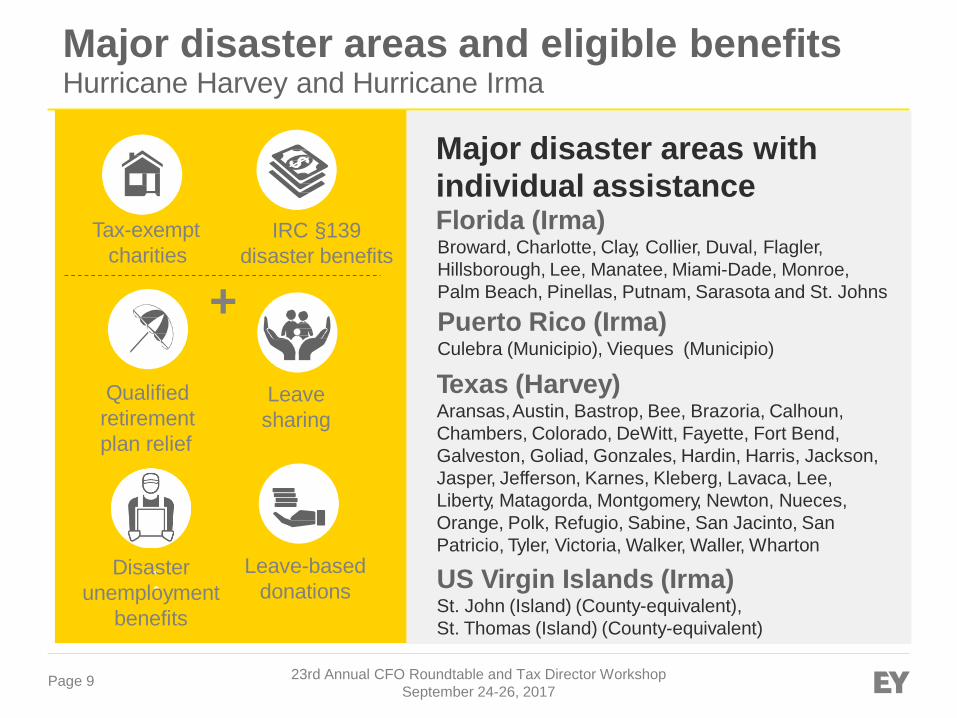

Major disaster areas and eligible benefitsHurricane Harvey and Hurricane Irma

Major disaster areas with individual assistance Florida (Irma)Broward, Charlotte, Clay, Collier, Duval, Flagler, Hillsborough, Lee, Manatee, Miami-Dade, Monroe, Palm Beach, Pinellas, Putnam, Sarasota and St. Johns

Puerto Rico (Irma)Culebra (Municipio), Vieques (Municipio)

Texas (Harvey)Aransas,Austin, Bastrop, Bee, Brazoria, Calhoun, Chambers, Colorado, DeWitt, Fayette, Fort Bend, Galveston, Goliad, Gonzales, Hardin, Harris, Jackson, Jasper, Jefferson, Karnes, Kleberg, Lavaca, Lee, Liberty, Matagorda, Montgomery, Newton, Nueces, Orange, Polk, Refugio, Sabine, San Jacinto, San Patricio, Tyler, Victoria, Walker, Waller, Wharton

US Virgin Islands (Irma)St. John (Island) (County-equivalent), St. Thomas (Island) (County-equivalent)

Tax-exemptcharities

Leave-based donations

Leavesharing

IRC §139disaster benefits

Qualifiedretirementplan relief

Disaster unemployment

benefits

+

Page 10 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

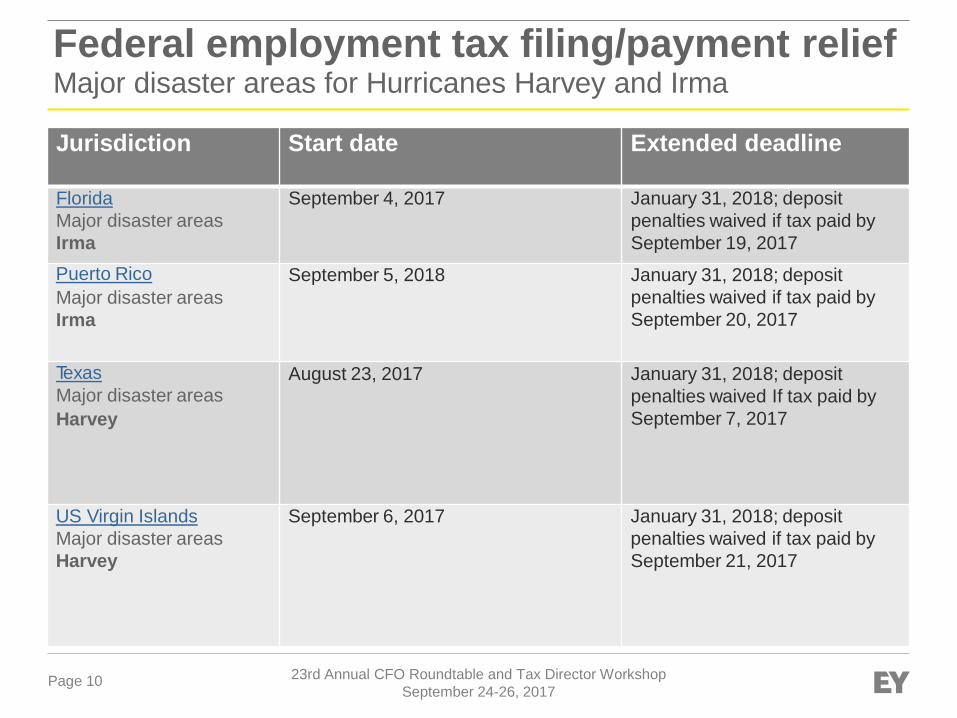

Federal employment tax filing/payment reliefMajor disaster areas for Hurricanes Harvey and Irma

Jurisdiction Start date Extended deadline

FloridaMajor disaster areasIrma

September 4, 2017 January 31, 2018; deposit penalties waived if tax paid by September 19, 2017

Puerto RicoMajor disaster areasIrma

September 5, 2018 January 31, 2018; deposit penalties waived if tax paid by September 20, 2017

TexasMajor disaster areasHarvey

August 23, 2017 January 31, 2018; deposit penalties waived If tax paid by September 7, 2017

US Virgin IslandsMajor disaster areas Harvey

September 6, 2017 January 31, 2018; deposit penalties waived if tax paid by September 21, 2017

Wage advances and loansDebby Salam

Page 12 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

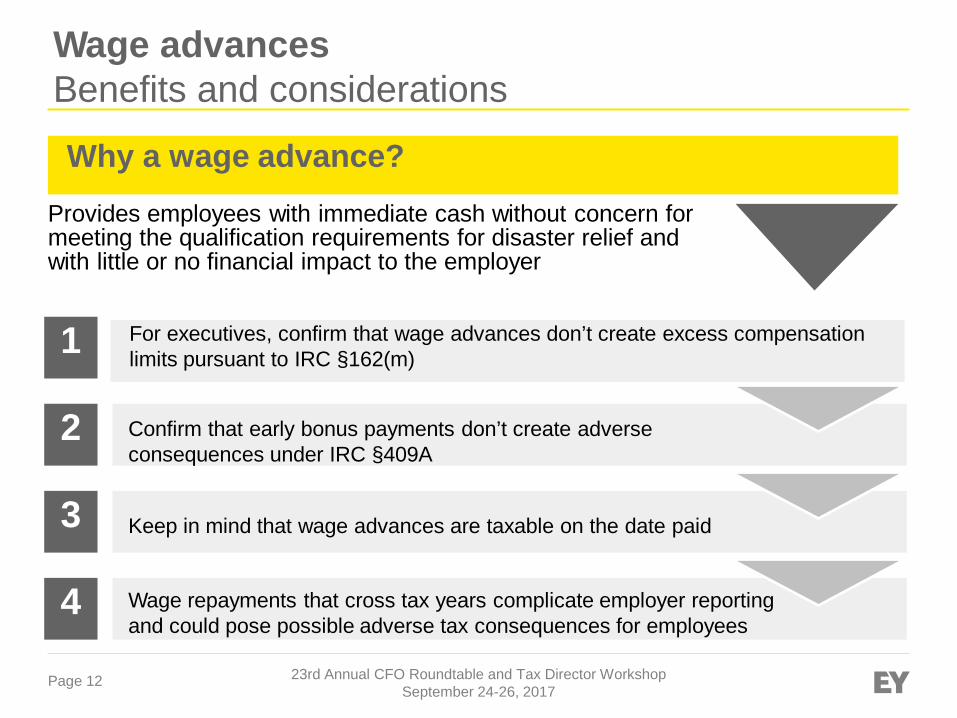

Wage advancesBenefits and considerations

Why a wage advance?Provides employees with immediate cash without concern for meeting the qualification requirements for disaster relief and with little or no financial impact to the employer

4

3

2

1 For executives, confirm that wage advances don’t create excess compensationlimits pursuant to IRC §162(m)

Confirm that early bonus payments don’t create adverseconsequences under IRC §409A

Keep in mind that wage advances are taxable on the date paid

Wage repayments that cross tax years complicate employer reporting and could pose possible adverse tax consequences for employees

Page 13 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Wage advances – claim-of-right doctrine

► When wage repayments are made in years subsequent to the advance, the IRS instructs employers in IRS Publication 15 that special rules govern the Form W-2c

► There may also be adverse consequences to the employee under the claim-of-right rule (IRS Publication 525, Taxable and Nontaxable Income)► The amount of the subsequent-year repayment is reported on Form W-2c

for the year of the advance, but only for the purpose of reducing Social Security (Form W-2, box 3) and Medicare (Form W-2, box 5) wages and related taxes

► The employer issues a FICA refund to the employee once employee completes requisite written statement

► Note that state rules governing wage repayments may vary

Page 14 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

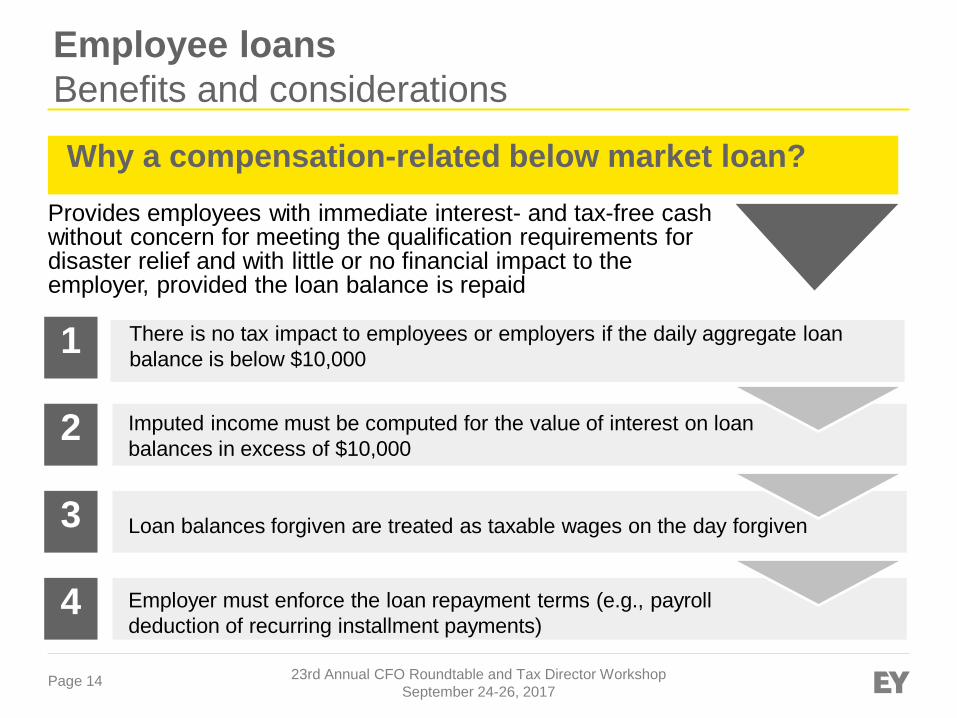

Employee loansBenefits and considerations

Why a compensation-related below market loan?Provides employees with immediate interest- and tax-free cash without concern for meeting the qualification requirements for disaster relief and with little or no financial impact to the employer, provided the loan balance is repaid

4

3

2

1 There is no tax impact to employees or employers if the daily aggregate loan balance is below $10,000

Imputed income must be computed for the value of interest on loan balances in excess of $10,000

Loan balances forgiven are treated as taxable wages on the day forgiven

Employer must enforce the loan repayment terms (e.g., payrolldeduction of recurring installment payments)

Tax-free employer-provided disaster relief

Page 16 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

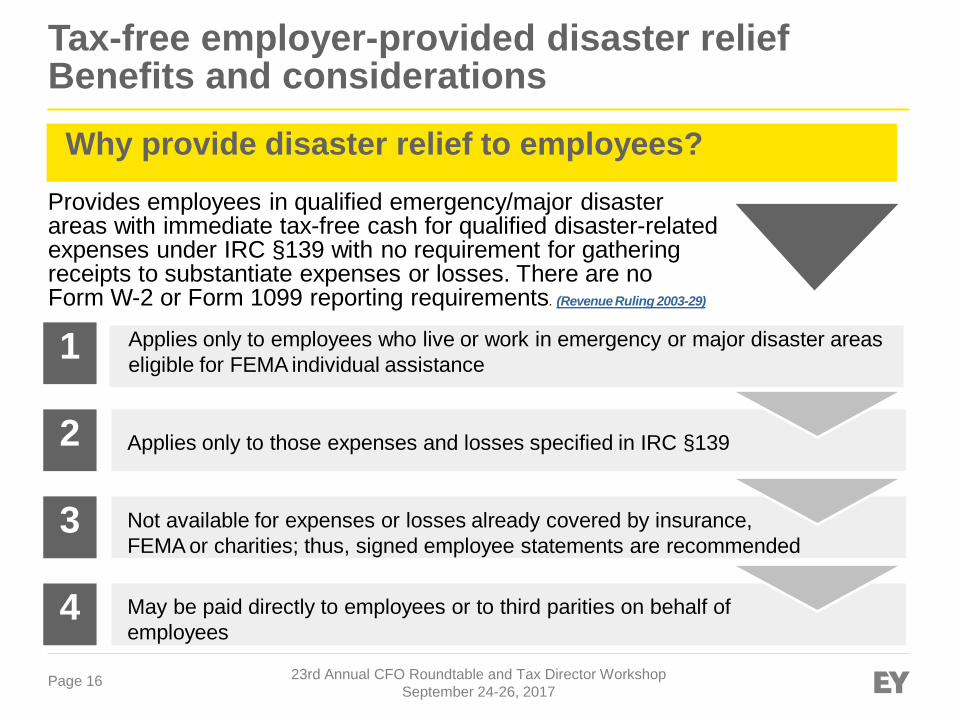

Tax-free employer-provided disaster reliefBenefits and considerationsWhy provide disaster relief to employees?

Provides employees in qualified emergency/major disaster areas with immediate tax-free cash for qualified disaster-related expenses under IRC §139 with no requirement for gathering receipts to substantiate expenses or losses. There are noForm W-2 or Form 1099 reporting requirements. (Revenue Ruling 2003-29)

4

3

2

1 Applies only to employees who live or work in emergency or major disaster areas eligible for FEMA individual assistance

Applies only to those expenses and losses specified in IRC §139

Not available for expenses or losses already covered by insurance,FEMA or charities; thus, signed employee statements are recommended

May be paid directly to employees or to third parities on behalf of employees

Page 17 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

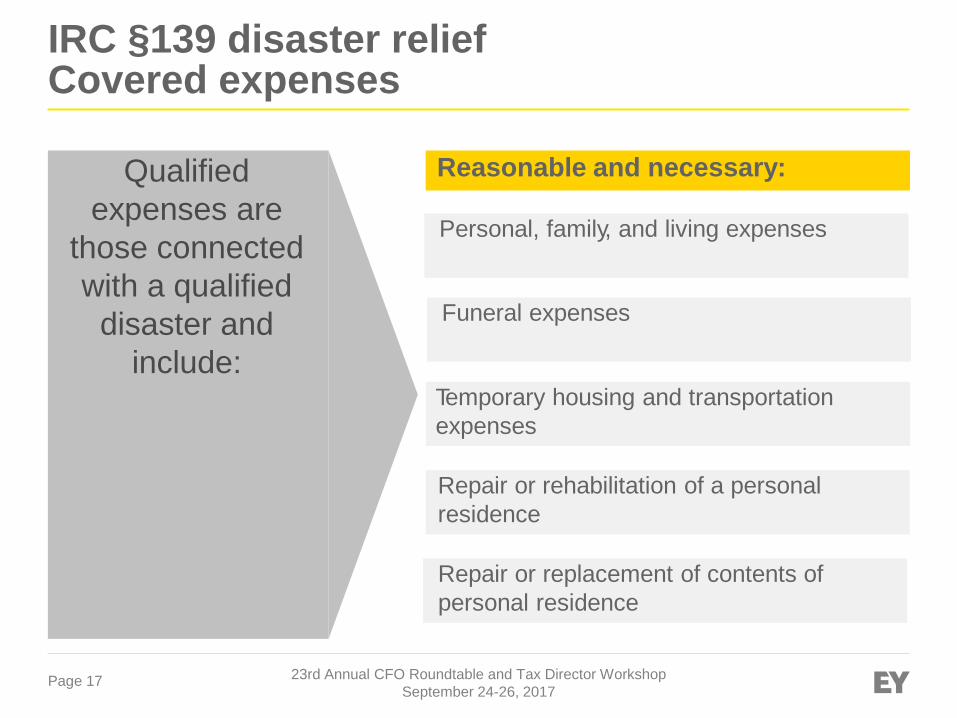

IRC §139 disaster reliefCovered expenses

Reasonable and necessary:Qualified expenses are

those connected with a qualified

disaster and include:

Personal, family, and living expenses

Funeral expenses

Temporary housing and transportation expenses

Repair or rehabilitation of a personal residence

Repair or replacement of contents of personal residence

Page 18 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

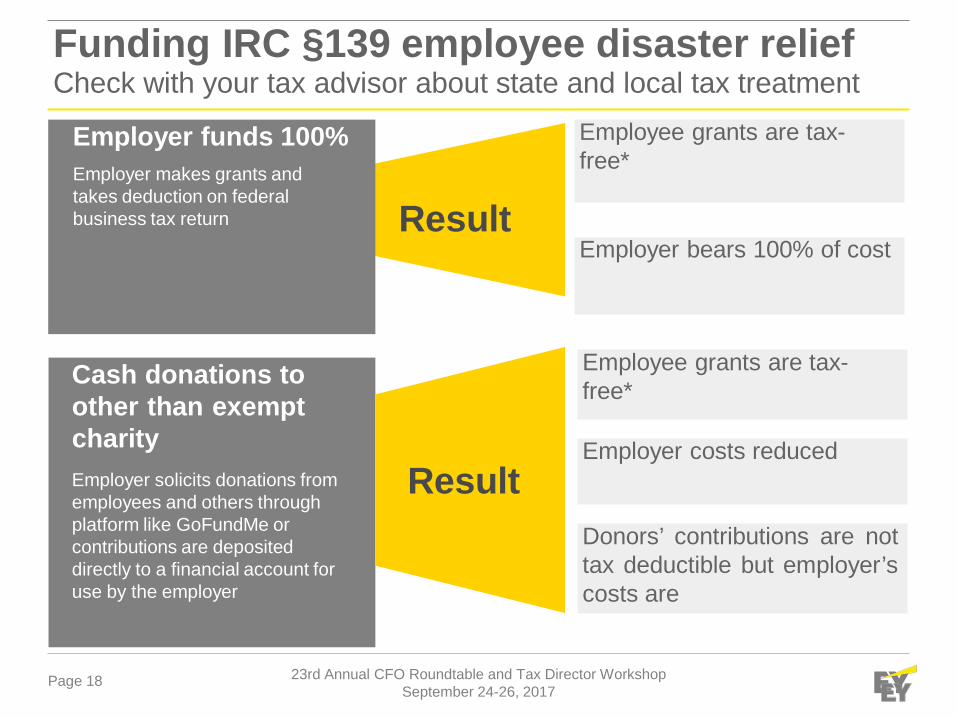

Funding IRC §139 employee disaster reliefCheck with your tax advisor about state and local tax treatment

Result

Employer funds 100%Employer makes grants and takes deduction on federal business tax return

Cash donations toother than exemptcharityEmployer solicits donations from employees and others through platform like GoFundMe or contributions are deposited directly to a financial account for use by the employer

Employee grants are tax-free*

Employer costs reduced

Donors’ contributions are nottax deductible but employer’scosts are

Result

Employee grants are tax-free*

Employer bears 100% of cost

Leave sharing and leave donations

Page 20 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

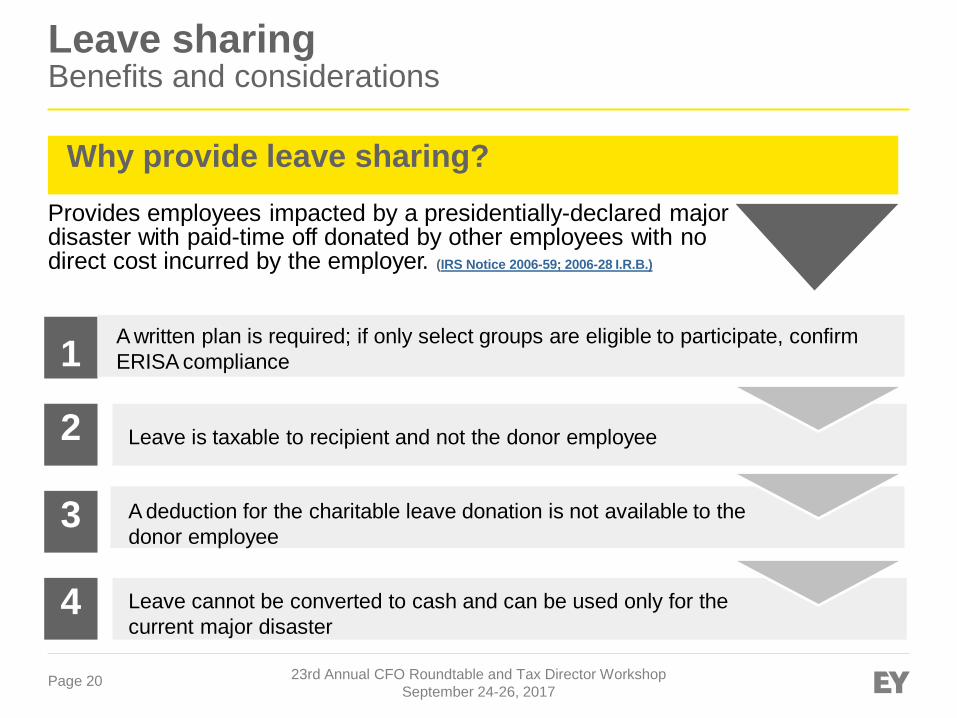

Leave sharingBenefits and considerations

Why provide leave sharing?Provides employees impacted by a presidentially-declared major disaster with paid-time off donated by other employees with no direct cost incurred by the employer. (IRS Notice 2006-59; 2006-28 I.R.B.)

4

3

2

1 A written plan is required; if only select groups are eligible to participate, confirmERISA compliance

Leave is taxable to recipient and not the donor employee

A deduction for the charitable leave donation is not available to the donor employee

Leave cannot be converted to cash and can be used only for thecurrent major disaster

Page 21 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

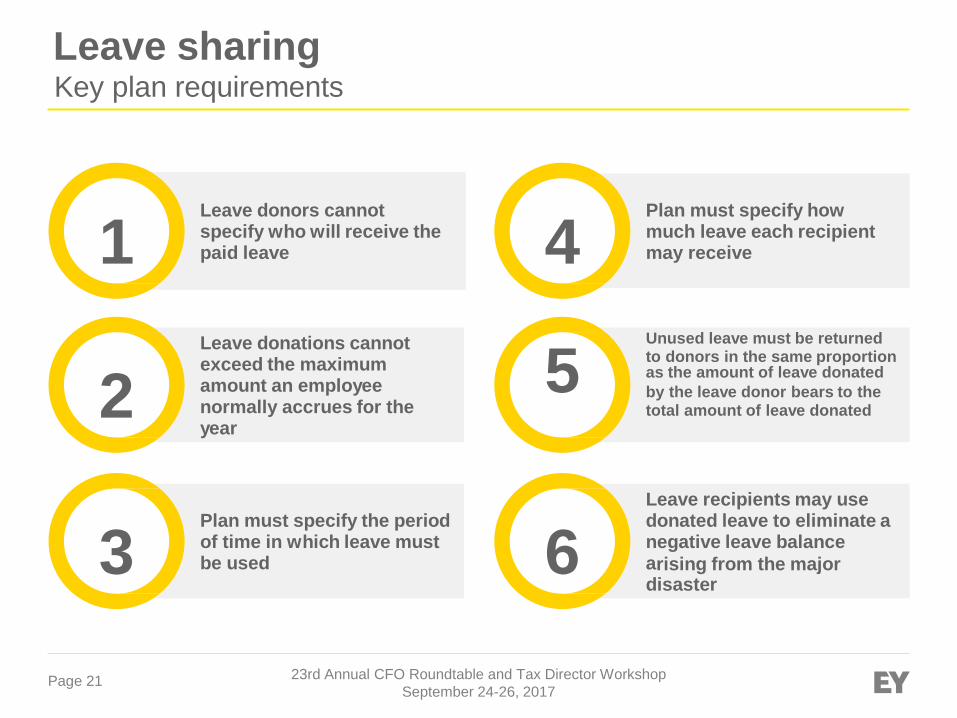

Leave sharingKey plan requirements

Leave donors cannot specify who will receive the paid leave1Leave donations cannot exceed the maximum amount an employee normally accrues for the year

2Plan must specify the period of time in which leave must be used3

Plan must specify how much leave each recipient may receive4Unused leave must be returned

5 to donors in the same proportionas the amount of leave donatedby the leave donor bears to the total amount of leave donated

Leave recipients may use donated leave to eliminate a negative leave balancea disasterrising from the major6

Page 22 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Leave-based donations to charitiesBenefits and considerations

Why provide leave-based donations to charities?When specifically allowed by IRS announcement pursuant to a major disaster area, employees can elect to have the employer donate the cash value of their paid leave to an IRC §170(c) charitable organization

4

3

2

1 The value of leave donated is excluded from employees’ wages subject to federalincome tax, federal income tax withholding and Social Security/Medicare

Because the donated leave is excluded from taxable wages,employees cannot also claim a deduction for the charitable donation

The employer can deduct the leave it donates to an IRC 170(c) organization under the rules of IRC §162

Leave-based donations meeting these requirements are not reported on Form W-2 in boxes 1, 3 or 5

Page 23 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

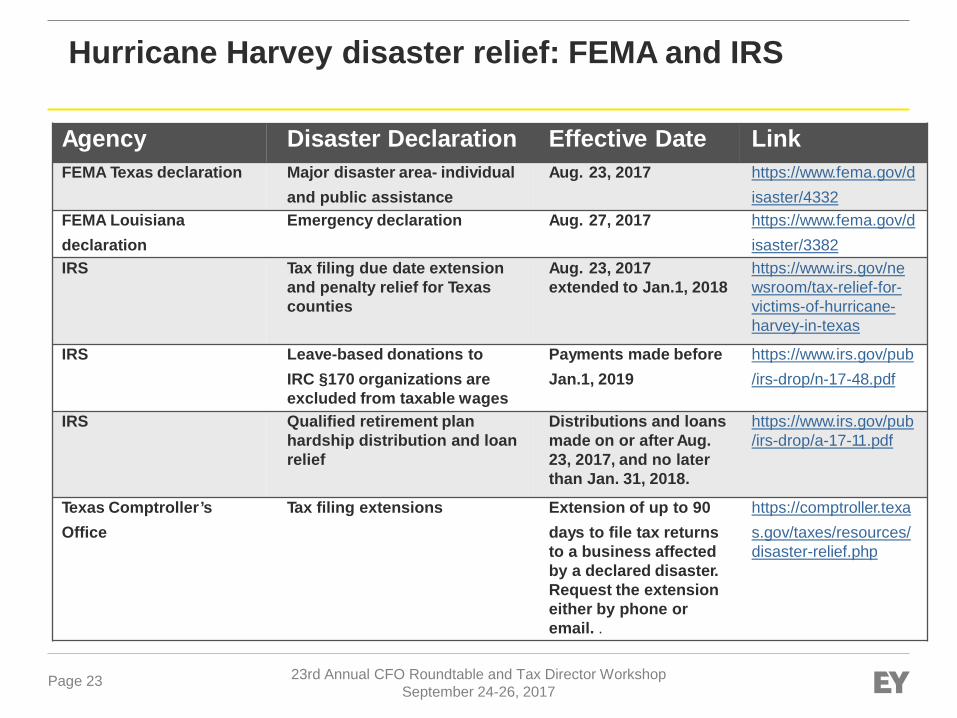

Hurricane Harvey disaster relief: FEMA and IRS

Agency Disaster Declaration Effective Date LinkFEMA Texas declaration Major disaster area- individual Aug. 23, 2017 https://www.fema.gov/d

and public assistance isaster/4332FEMA Louisiana Emergency declaration Aug. 27, 2017 https://www.fema.gov/ddeclaration isaster/3382IRS Tax filing due date extension

and penalty relief for Texas counties

Aug. 23, 2017extended to Jan.1, 2018

https://www.irs.gov/newsroom/tax-relief-for-victims-of-hurricane-harvey-in-texas

IRS Leave-based donations to Payments made before https://www.irs.gov/pubIRC §170 organizations are Jan.1, 2019 /irs-drop/n-17-48.pdfexcluded from taxable wages

IRS Qualified retirement plan hardship distribution and loan relief

Distributions and loans made on or after Aug.23, 2017, and no laterthan Jan. 31, 2018.

https://www.irs.gov/pub/irs-drop/a-17-11.pdf

Texas Comptroller’s Tax filing extensions Extension of up to 90 https://comptroller.texaOffice days to file tax returns s.gov/taxes/resources/

to a business affected disaster-relief.phpby a declared disaster.Request the extensioneither by phone oremail. .

Page 24 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

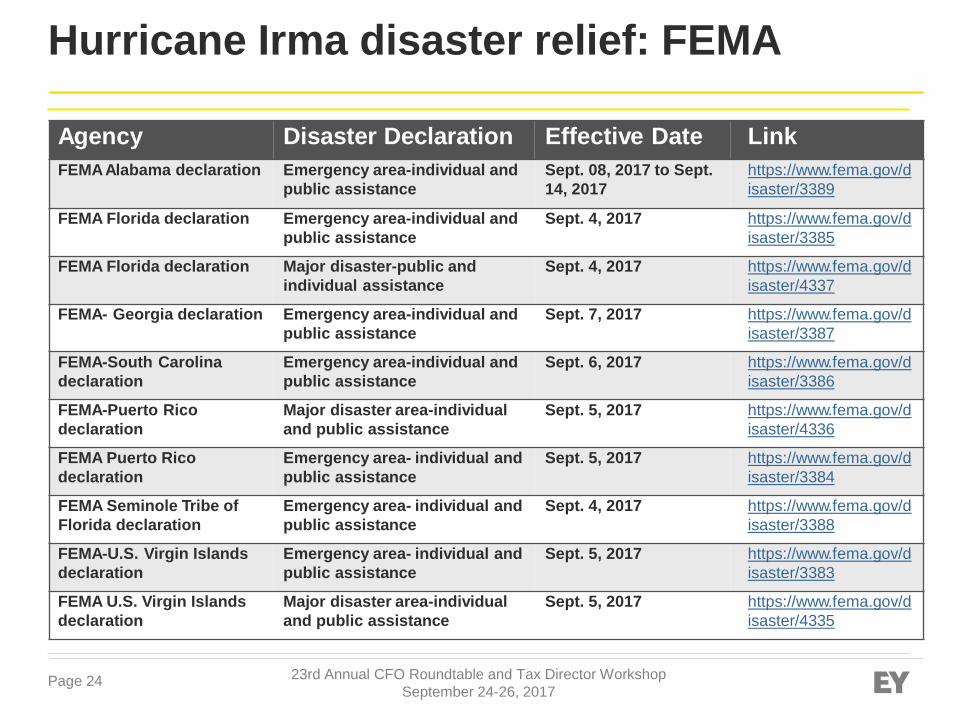

Hurricane Irma disaster relief: FEMA

Agency Disaster Declaration Effective Date LinkFEMAAlabama declaration Emergency area-individual and

public assistanceSept. 08, 2017 to Sept.14, 2017

https://www.fema.gov/disaster/3389

FEMA Florida declaration Emergency area-individual and public assistance

Sept. 4, 2017 https://www.fema.gov/disaster/3385

FEMA Florida declaration Major disaster-public and individual assistance

Sept. 4, 2017 https://www.fema.gov/disaster/4337

FEMA- Georgia declaration Emergency area-individual and public assistance

Sept. 7, 2017 https://www.fema.gov/disaster/3387

FEMA-South Carolina declaration

Emergency area-individual and public assistance

Sept. 6, 2017 https://www.fema.gov/disaster/3386

FEMA-Puerto Rico declaration

Major disaster area-individual and public assistance

Sept. 5, 2017 https://www.fema.gov/disaster/4336

FEMA Puerto Rico declaration

Emergency area- individual and public assistance

Sept. 5, 2017 https://www.fema.gov/disaster/3384

FEMA Seminole Tribe of Florida declaration

Emergency area- individual and public assistance

Sept. 4, 2017 https://www.fema.gov/disaster/3388

FEMA-U.S. Virgin Islands declaration

Emergency area- individual and public assistance

Sept. 5, 2017 https://www.fema.gov/disaster/3383

FEMA U.S. Virgin Islands declaration

Major disaster area-individual and public assistance

Sept. 5, 2017 https://www.fema.gov/disaster/4335

Page 25 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

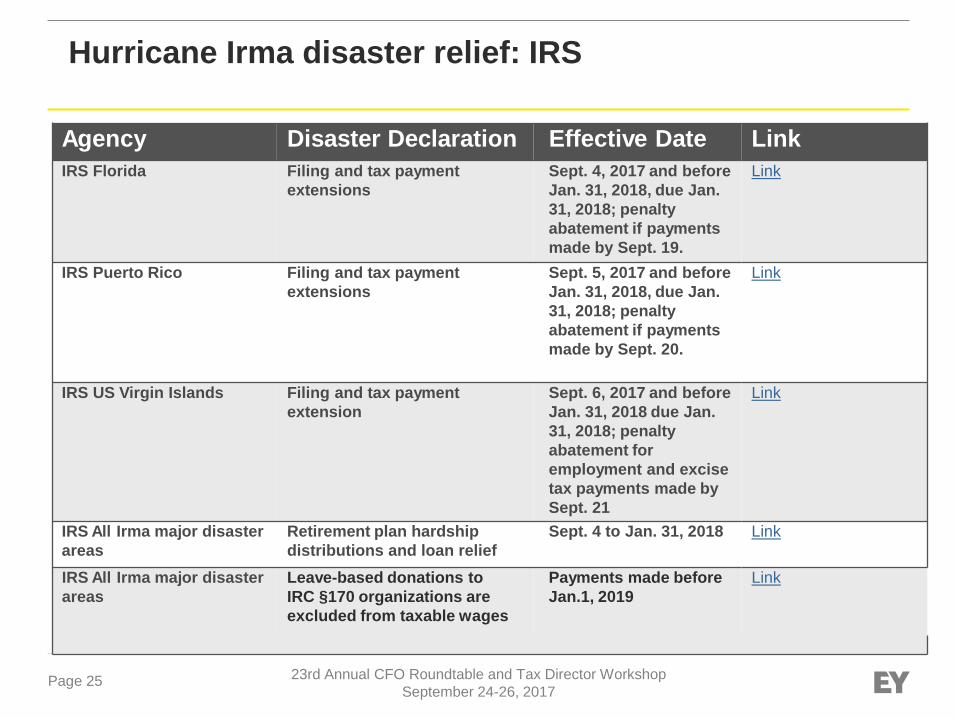

Hurricane Irma disaster relief: IRS

Agency Disaster Declaration Effective Date LinkIRS Florida Filing and tax payment

extensionsSept. 4, 2017 and beforeJan. 31, 2018, due Jan.31, 2018; penalty abatement if payments made by Sept. 19.

Link

IRS Puerto Rico Filing and tax payment extensions

Sept. 5, 2017 and beforeJan. 31, 2018, due Jan.31, 2018; penalty abatement if payments made by Sept. 20.

Link

IRS US Virgin Islands Filing and tax payment extension

Sept. 6, 2017 and beforeJan. 31, 2018 due Jan.31, 2018; penalty abatement for employment and excise tax payments made by Sept. 21

Link

IRS All Irma major disaster areas

Retirement plan hardship distributions and loan relief

Sept. 4 to Jan. 31, 2018 Link

IRS All Irma major disaster areas

Leave-based donations to IRC §170 organizations are excluded from taxable wages

Payments made before Jan.1, 2019

Link

Employer on Site Meals – Boston Bruins Case

Page 27 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Overview of “Bruins” Case

► Tax court ruled in Jeremy M. Jacobs et ux. v. Commissioner that pre-game meals provided to players and staff traveling with Boston Bruins were not taxable as de minimisfringe benefits under IRC 274(n)(2)(B). (Jacobs is owner of the Bruins)

► Ruling is significant because de minimis fringe benefit meals are not subject to the 50% limitation under 274(n)(1)

► In order to be considered de minimis fringe benefit meals the meals must be: at eating facility owned or leased by employer, operated by the employer, furnished before/during/after workhours, and revenue from facility must equal or exceed operating costs (as defined in IRC

132(e)

Additionally, the meals must be provided at or near the business premises of the employee.

► Court determined that “the right to use and occupy” hotel banquet facilities qualified as being “leased by the employer” as Bruins even though the agreement with the hotel did not identify the contract as a lease

Page 28 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Overview of “Bruins” Case

► Because the Bruins dictated the time, place, set up and specific meals to be served, the banquet room qualified as “being operated by the employer”.

► The court determined that because the Bruins travel significantly away from home and in away cities, the hotel in which the meals were served would be deemed as part of the Bruins’ business premises,

► The value of the meals are also excludible from employee income under IRC 119.

► Case is very fact specific and must be carefully analyzed to determine if Court’s position may be applied in other circumstances.

► Could potentially apply to employee “camps” for long term construction projects.

► If IRS files appeal, taxpayers may wish to consider filing protective refund claims as it may take several years to determine whether decision is upheld under appeal.

Page 29

State Wage Withholding and Reporting

Executive Tax Update 2016

Page 30 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

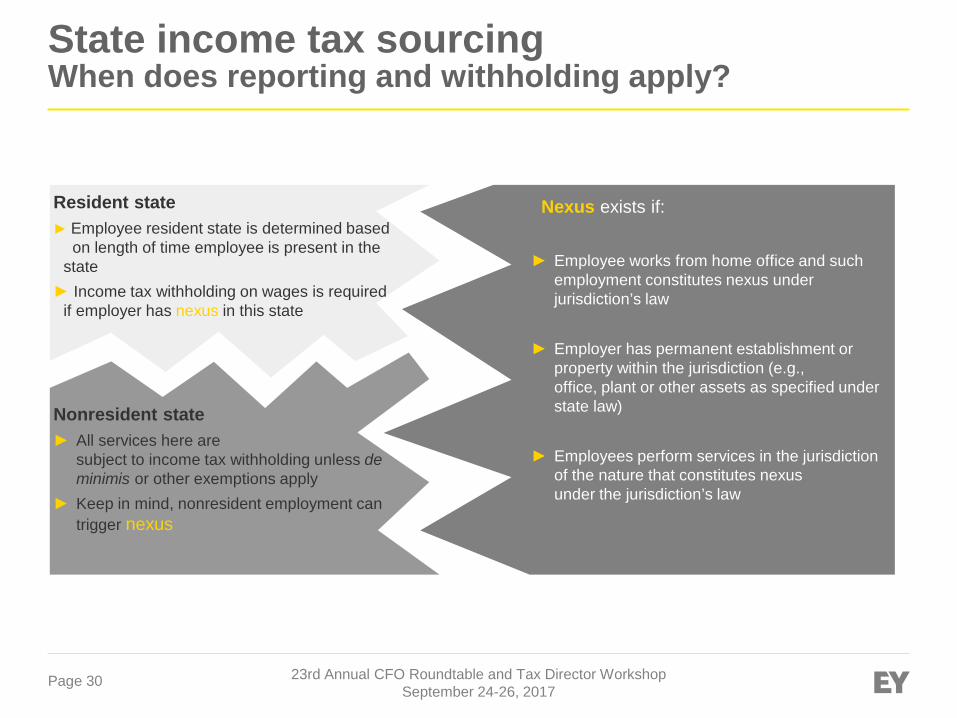

State income tax sourcingWhen does reporting and withholding apply?

Nonresident state► All services here are

subject to income tax withholding unless de minimis or other exemptions apply

► Keep in mind, nonresident employment can trigger nexus

Nexus exists if:

► Employee works from home office and such employment constitutes nexus under jurisdiction’s law

► Employer has permanent establishment or property within the jurisdiction (e.g., office, plant or other assets as specified under state law)

► Employees perform services in the jurisdiction of the nature that constitutes nexusunder the jurisdiction’s law

Resident state ► Employee resident state is determined based

on length of time employee is present in the state

► Income tax withholding on wages is required if employer has nexus in this state

Page 31 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

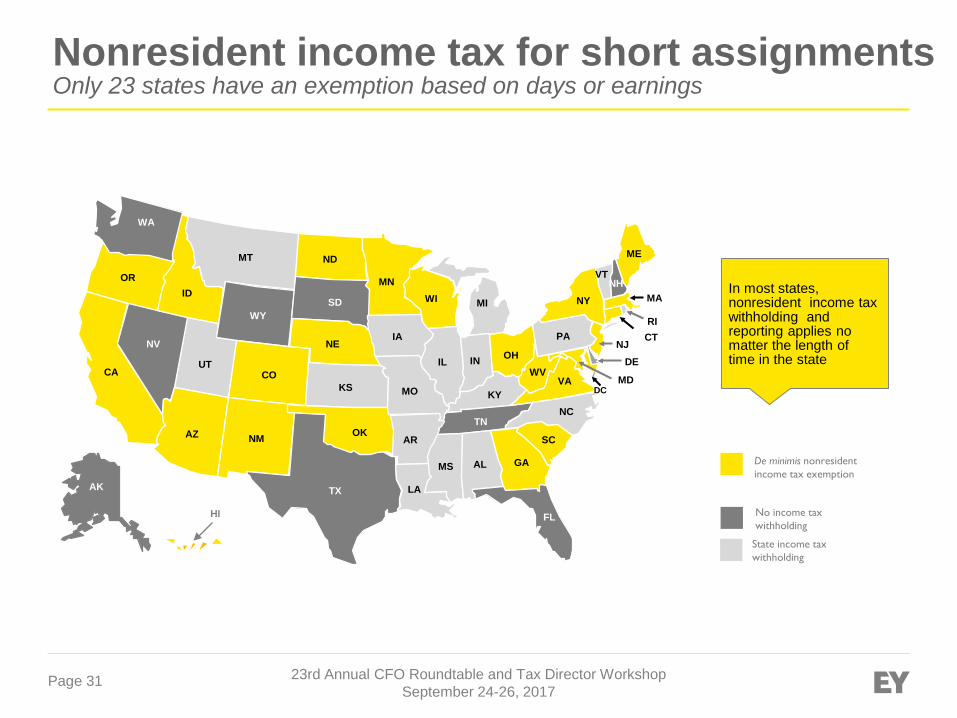

Nonresident income tax for short assignments Only 23 states have an exemption based on days or earnings

HI

ME

RI

VTNH

MANY

CTPANJ

DC

DEWV

SC

GA

IL OHIN

MIWI

KY

TN

ALMS

AR

LATX

OK

MOKS

IA

MN

ND

SD

NE

NMAZ

COUT

WY

MT

WA

ORID

NV

CAVA

MDMD

WA

De minimis nonresident income tax exemption

FL

NC

No income tax withholding

State income tax withholding

WA

AK

In most states, nonresident income tax withholding and reporting applies no matter the length of time in the state

Page 32 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

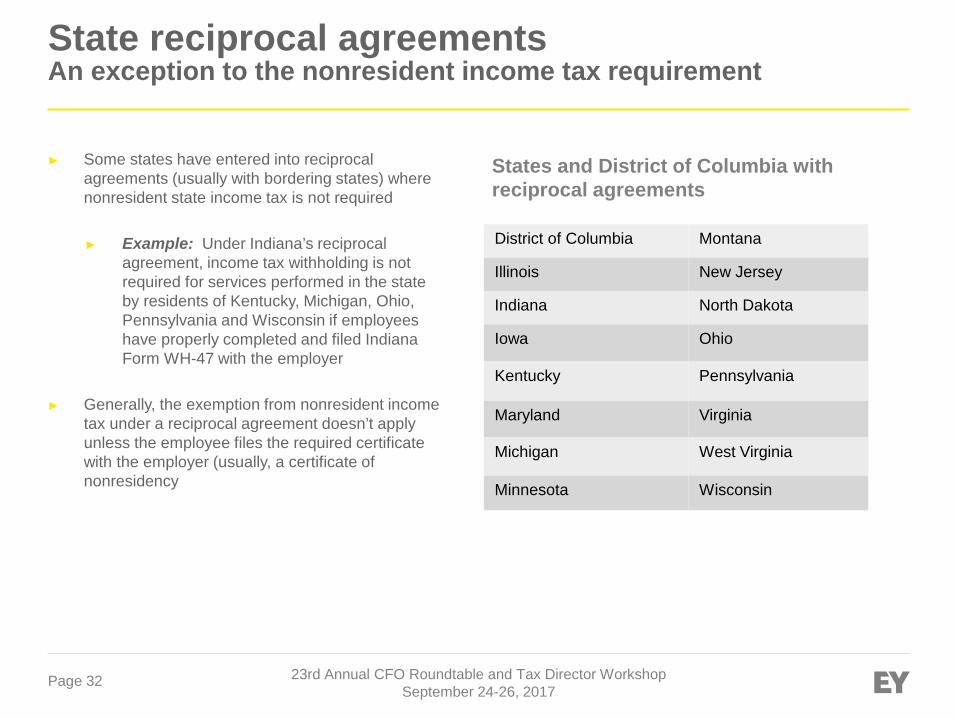

State reciprocal agreementsAn exception to the nonresident income tax requirement

► Some states have entered into reciprocal agreements (usually with bordering states) where nonresident state income tax is not required

► Example: Under Indiana’s reciprocal agreement, income tax withholding is not required for services performed in the state by residents of Kentucky, Michigan, Ohio, Pennsylvania and Wisconsin if employees have properly completed and filed Indiana Form WH-47 with the employer

► Generally, the exemption from nonresident income tax under a reciprocal agreement doesn’t apply unless the employee files the required certificate with the employer (usually, a certificate of nonresidency

States and District of Columbia with reciprocal agreements

District of Columbia Montana

Illinois New Jersey

Indiana North Dakota

Iowa Ohio

Kentucky Pennsylvania

Maryland Virginia

Michigan West Virginia

Minnesota Wisconsin

Page 33 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Telecommuter considerationsThe home office could be a local business office

► If employees regularly work from home, the home office could be treated as a work location of the employer in many states (and localities)

► If the home office is deemed an employer work location, the business can be subject to income tax withholding, unemployment insurance and other businesses taxes

► In a New Jersey case, it was determined that a foreign corporation with a principal place of business in Maryland was subject to New Jersey’s corporate income tax requirements because one of its employees was allowed to work on a full-time basis from her New Jersey home office (Telebright Corporation v. Director, N.J. Super. Ct. App. Div., Dkt. No. A-5096-09T2, 03/02/2012)

Page 34 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Telecommuter considerationsNonresident income tax may apply in the headquarters’ state

► Some states (e.g., New York) take the position that 100% of the wages paid to a nonresident are subject to New York income tax if the employee is working out of state for the employee’s own convenience

► The rule applies when an employee receives direction and control from a New York location and the employee works in New York for any period in the year

► To argue that work location is for the employer’s convenience, there must be a direct business benefit in having the employee work outside of New York

► The rule can result in double taxation (e.g., tax in both the resident state and New York)

► The US Supreme Court declined to hear a challenge concerning the constitutionality of this law (Zelinsky v. Tax Appeals Tribunal)

Page 35 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

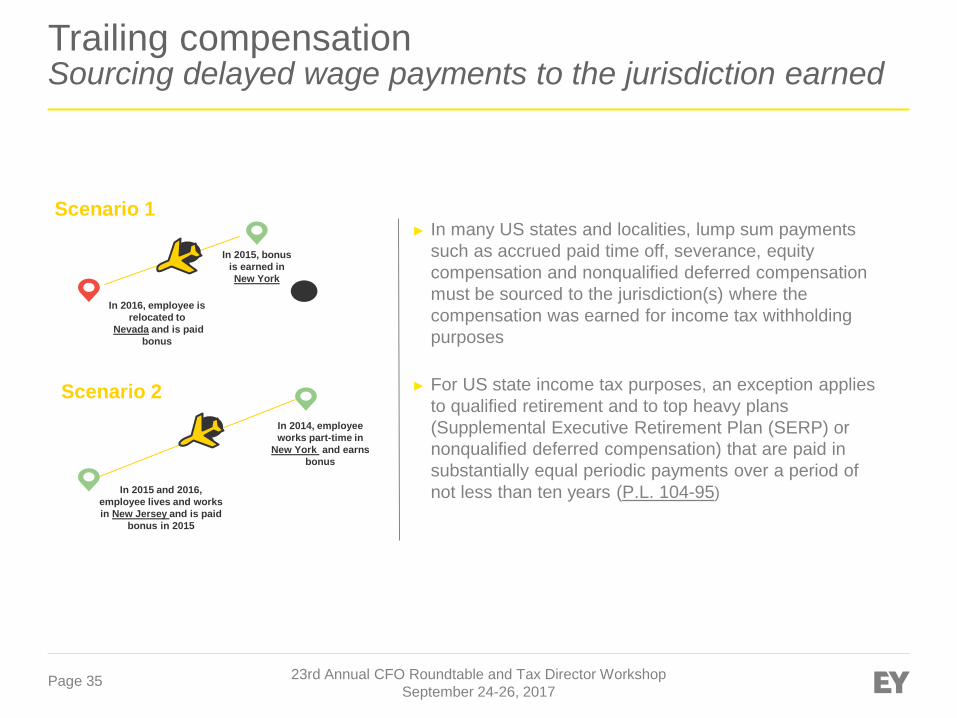

Trailing compensation Sourcing delayed wage payments to the jurisdiction earned

In 2016, employee is relocated to

Nevada and is paid bonus

In 2015, bonus is earned in New York

► In many US states and localities, lump sum payments such as accrued paid time off, severance, equity compensation and nonqualified deferred compensation must be sourced to the jurisdiction(s) where the compensation was earned for income tax withholding purposes

► For US state income tax purposes, an exception applies to qualified retirement and to top heavy plans (Supplemental Executive Retirement Plan (SERP) or nonqualified deferred compensation) that are paid in substantially equal periodic payments over a period of not less than ten years (P.L. 104-95) In 2015 and 2016,

employee lives and works in New Jersey and is paid

bonus in 2015

In 2014, employee works part-time in

New York and earns bonus

Scenario 1

Scenario 2

Page 36 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

The top most misunderstood factsCommon income tax withholding tax errors occur in these areas

1The New York 14-day rules don’t extend to employees’ personal income tax obligations.

2 Income tax exemptions under tax treaties and reciprocal agreements are not necessarily automatic.

3 Employers are responsible for knowing where their employees are working and the tax that applies.

4 Employee work at home may be considered a place of business for resident nexus purposes..

5 Employees working from home may owe tax in the corporate office state.

6A federal tax treaty exemption does not necessarily apply to state and local taxes.

7 Income tax may continue to apply to trailing compensation even after the employee transfers to another state.

8 Computation of resident income tax varies when employees work outside of the state.

9 Federal law prohibits nonresident income tax for certain industries and payments.

10 Short-term work assignments are not necessarily disregarded for nonresident income tax purposes.

Page 37 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

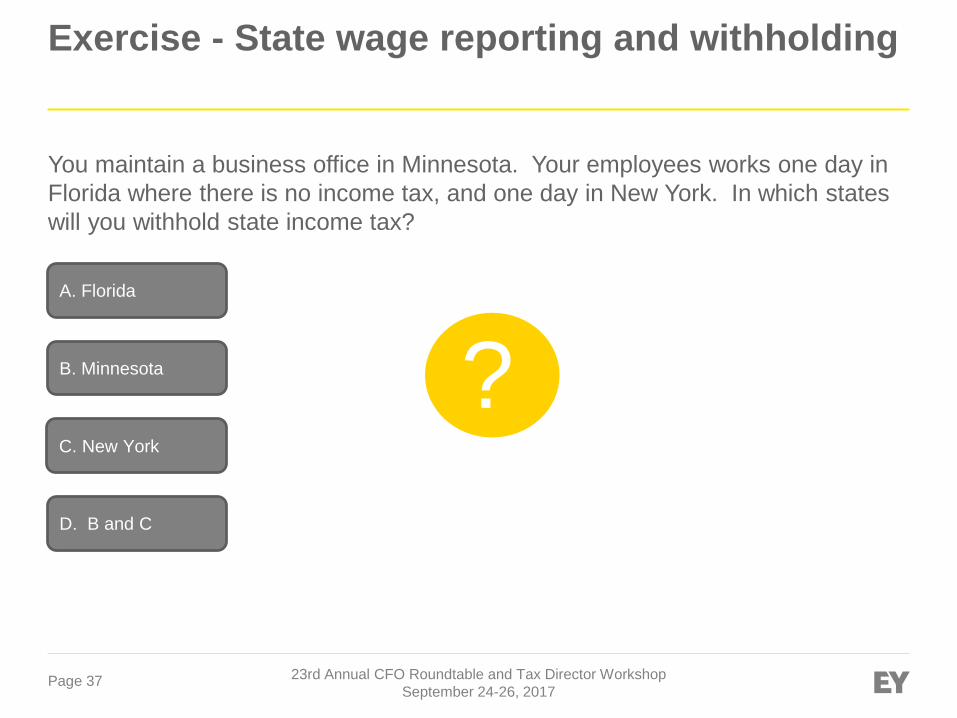

Exercise - State wage reporting and withholding

You maintain a business office in Minnesota. Your employees works one day in Florida where there is no income tax, and one day in New York. In which states will you withhold state income tax?

A. Florida

B. Minnesota

C. New York

D. B and C

?

Page 38 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

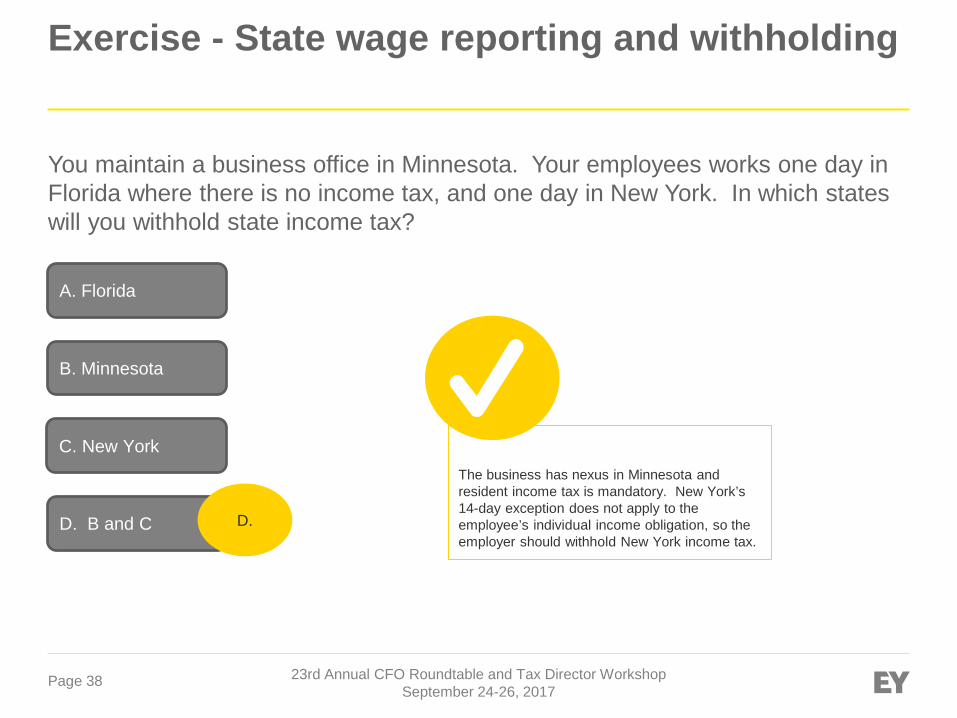

Exercise - State wage reporting and withholding

You maintain a business office in Minnesota. Your employees works one day in Florida where there is no income tax, and one day in New York. In which states will you withhold state income tax?

A. Florida

B. Minnesota

C. New York

D. B and C

The business has nexus in Minnesota and resident income tax is mandatory. New York’s 14-day exception does not apply to the employee’s individual income obligation, so the employer should withhold New York income tax.

D.

Page 39 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

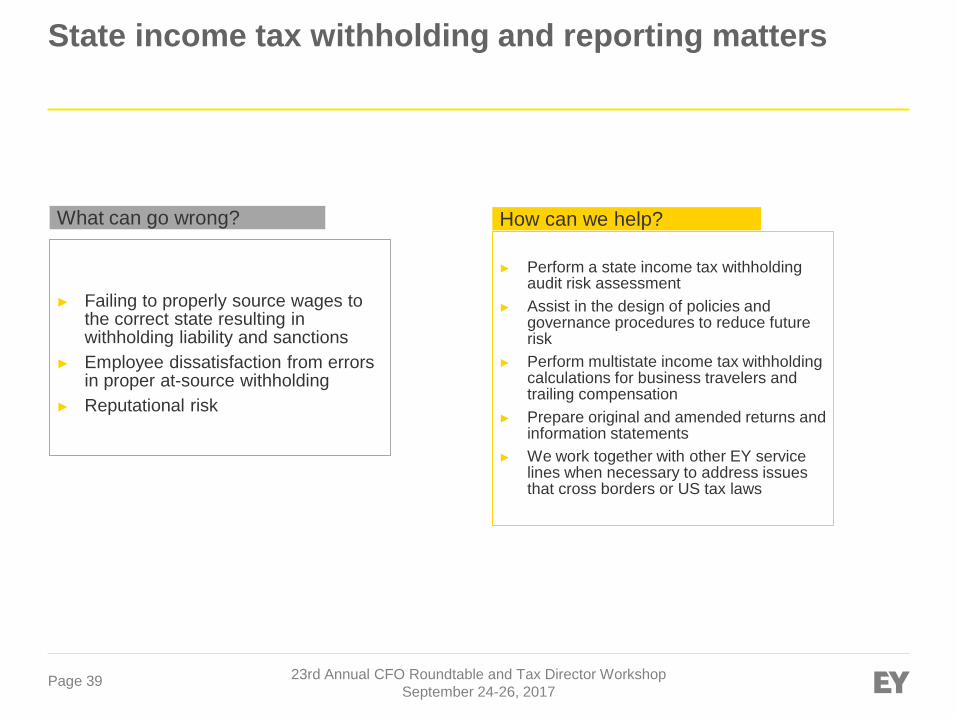

State income tax withholding and reporting matters

What can go wrong?

► Failing to properly source wages to the correct state resulting in withholding liability and sanctions

► Employee dissatisfaction from errors in proper at-source withholding

► Reputational risk

How can we help?

► Perform a state income tax withholding audit risk assessment

► Assist in the design of policies and governance procedures to reduce future risk

► Perform multistate income tax withholding calculations for business travelers and trailing compensation

► Prepare original and amended returns and information statements

► We work together with other EY service lines when necessary to address issues that cross borders or US tax laws

Page 40

Reporting and Withholding for US Inbound and Outbound Employees

Page 41 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

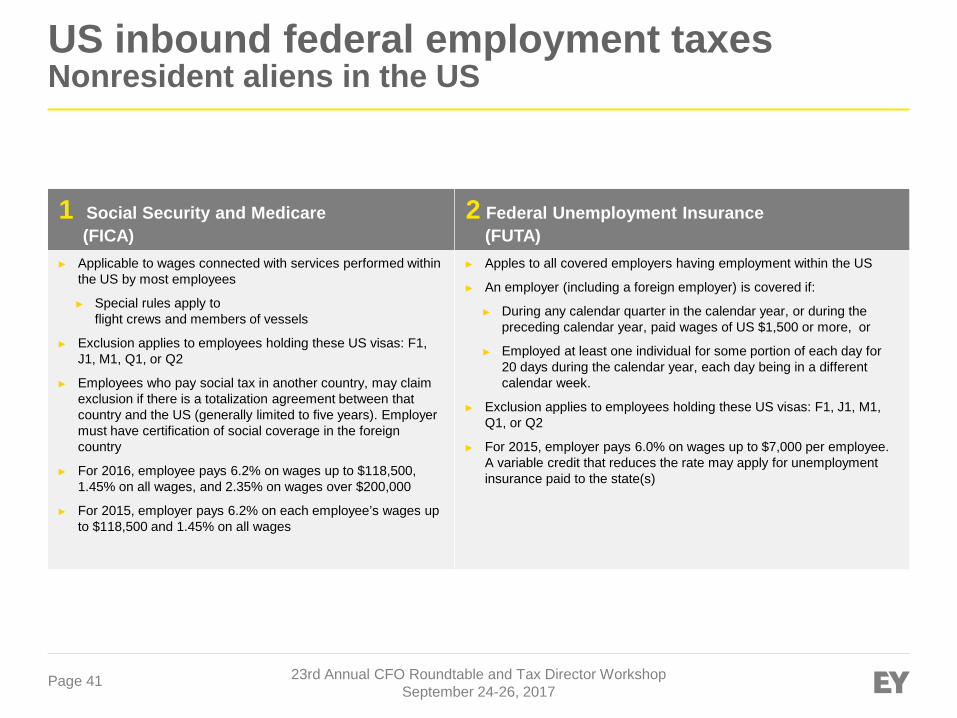

US inbound federal employment taxes Nonresident aliens in the US

1 Social Security and Medicare(FICA)

2 Federal Unemployment Insurance (FUTA)

► Applicable to wages connected with services performed within the US by most employees

► Special rules apply to flight crews and members of vessels

► Exclusion applies to employees holding these US visas: F1, J1, M1, Q1, or Q2

► Employees who pay social tax in another country, may claim exclusion if there is a totalization agreement between that country and the US (generally limited to five years). Employer must have certification of social coverage in the foreign country

► For 2016, employee pays 6.2% on wages up to $118,500, 1.45% on all wages, and 2.35% on wages over $200,000

► For 2015, employer pays 6.2% on each employee’s wages up to $118,500 and 1.45% on all wages

► Apples to all covered employers having employment within the US

► An employer (including a foreign employer) is covered if:

► During any calendar quarter in the calendar year, or during the preceding calendar year, paid wages of US $1,500 or more, or

► Employed at least one individual for some portion of each day for 20 days during the calendar year, each day being in a different calendar week.

► Exclusion applies to employees holding these US visas: F1, J1, M1, Q1, or Q2

► For 2015, employer pays 6.0% on wages up to $7,000 per employee. A variable credit that reduces the rate may apply for unemployment insurance paid to the state(s)

Page 42 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

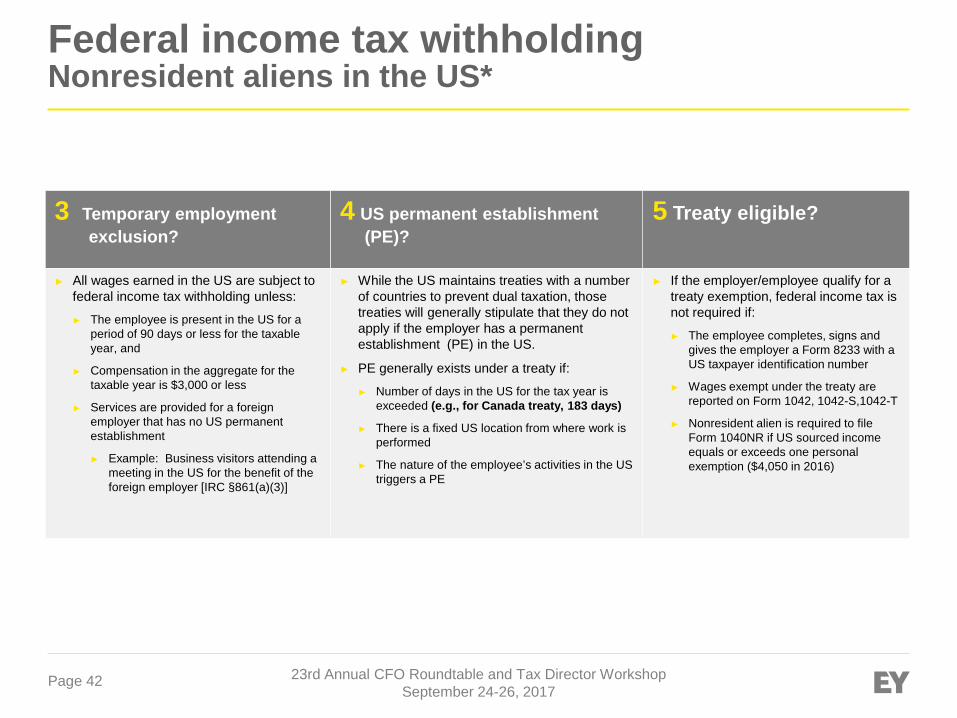

Federal income tax withholding Nonresident aliens in the US*

3 Temporary employment exclusion?

4 US permanent establishment (PE)?

5 Treaty eligible?

► All wages earned in the US are subject to federal income tax withholding unless:

► The employee is present in the US for a period of 90 days or less for the taxable year, and

► Compensation in the aggregate for the taxable year is $3,000 or less

► Services are provided for a foreign employer that has no US permanent establishment

► Example: Business visitors attending a meeting in the US for the benefit of the foreign employer [IRC §861(a)(3)]

► While the US maintains treaties with a number of countries to prevent dual taxation, those treaties will generally stipulate that they do not apply if the employer has a permanent establishment (PE) in the US.

► PE generally exists under a treaty if:

► Number of days in the US for the tax year is exceeded (e.g., for Canada treaty, 183 days)

► There is a fixed US location from where work is performed

► The nature of the employee’s activities in the US triggers a PE

► If the employer/employee qualify for a treaty exemption, federal income tax is not required if:

► The employee completes, signs and gives the employer a Form 8233 with a US taxpayer identification number

► Wages exempt under the treaty are reported on Form 1042, 1042-S,1042-T

► Nonresident alien is required to file Form 1040NR if US sourced income equals or exceeds one personal exemption ($4,050 in 2016)

Page 43 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Social Security totalization agreements

► Social security totalization agreements eliminate dual social tax when a worker is required to pay such tax on the same earnings in more than one country

► These agreements also fill gaps in benefit protection when workers have divided their careers between the US and another country

► The exemption under a totalization agreement applies for a limited period, generally, five years

► Employees must present a certificate of coverage from the foreign country to qualify for exemption from US Social Security and Medicare tax under the agreement

Australia France Poland

Austria Germany Portugal

Belgium Greece Slovak Republic New in 2014

Brazil (in process) Ireland South Korea

Canada Italy Spain

Chile Japan Sweden

Czech Republic Luxembourg Switzerland

Denmark Netherlands United Kingdom

Finland Norway

Countries with Social Security totalization agreements with the US

Page 44 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Common Visa Situations – F-1 or F-1/OPT

► F-1 Nonresident Visas► Statement from USCIS Website: Foreign students may be allowed to work in the

US under certain circumstance► Students may not be able to work off campus during the first academic year► Students on F-1 Visas will be issued a Form I-20 , Certificate of Eligibility for

Nonimmigrant Student Status

► Form I-20► Upon student acceptance into a student and exchange visitor program certified

school, the school official will issue the I-20 Form

► I-20 is for F-1 and M-1 visa status► Student and student dependent must have Form 1-20 to apply for visa, to enter the

US and apply for benefits► Form I-20 is needed when applying for US visa at local US embassy or consulate,

entering the US, applying for drivers license or Social Security number

Page 45 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Common Visa Situations – J-1

► J-1 Nonresident Visas (Exchange Visitors)

► Generally used for purposes of teaching, lecturing, studying, conducting research, to receive graduate education or training, etc.

► Statement from USCIS Website: Some J-1 Visa holders enter the US for employment while others do not. Employment is authorized only under the terms of the exchange program J-1-student (service grant) and J-1-researcher (non service grant)

► Visitors applying for a J-1 Visa are required to submit Form DS-2019, Certificate of Eligibility for Exchange Visitor Status. This form is provided by your sponsoring agency. DS-2019 should be reviewed to determine work status

Page 46 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

US employee outbound considerations

► The worldwide wages paid by a US employer to US employees who are US citizens and US residents is generally subject to federal income tax withholding, Social Security/Medicare and federal unemployment insurance

► An exemption from federal income tax withholding applies:► Only if the employee completes, signs and returns Form 673 to the employer, and

then:► On the portion of wages exempt under IRC §911 (foreign earned income and housing

exclusions) ► For US citizens only (and not residents), on the portion of wages subject to income tax

withholding in the foreign country [IRC Code §3401(a)(8)(A)(i)]

Page 47 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Exercise – Solution

A US nonresident alien exempt under a totalization agreement and who provides you with a certificate of coverage is exempt from which of these US taxes?

A. FICA

B. Federal incometax

C. FUTA

D. All of the above

?

Page 48 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

Exercise - US inbound and outbound reporting and withholding

A US nonresident alien exempt under a totalization agreement and who provides you with a certificate of coverage is exempt from which of these US taxes?

A. FICA

B. Federal incometax

C. FUTA

D. All of the above

A.

Exemption under a totalization agreement applies only to Social Security/Medicare. Federal income tax and federal unemployment insurance apply unless separate tests for exemption apply.

Page 49 23rd Annual CFO Roundtable and Tax Director WorkshopSeptember 24-26, 2017

What can go wrong?

► Employer liability for FICA and income tax it failed to withhold

► Failure to pay taxes required of the employer

► Failure to file returns and information statements

► Sanctions for reporting and tax payment errors

► Employee dissatisfaction from errors in proper at-source withholding

► Reputational risk

How can we help?

► Provide detailed federal, state and local filing and tax payment requirements for foreign employers

► Shadow payroll services for foreign employers with employment in the US

► Prepare original and amended returns and information statements

► File returns and make required tax payments

► We work together with other EY service lines when necessary to address issues that cross borders or US tax laws

US outbound income tax withholding and reporting matters

Add the EY Boilerplate text in this text box. You can always find the latest EY Boilerplate text here.