Embed Size (px)

Citation preview

25 - 1©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Activity-Based Costing

and Other CostManagement ToolsChapter

25

25 - 2©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

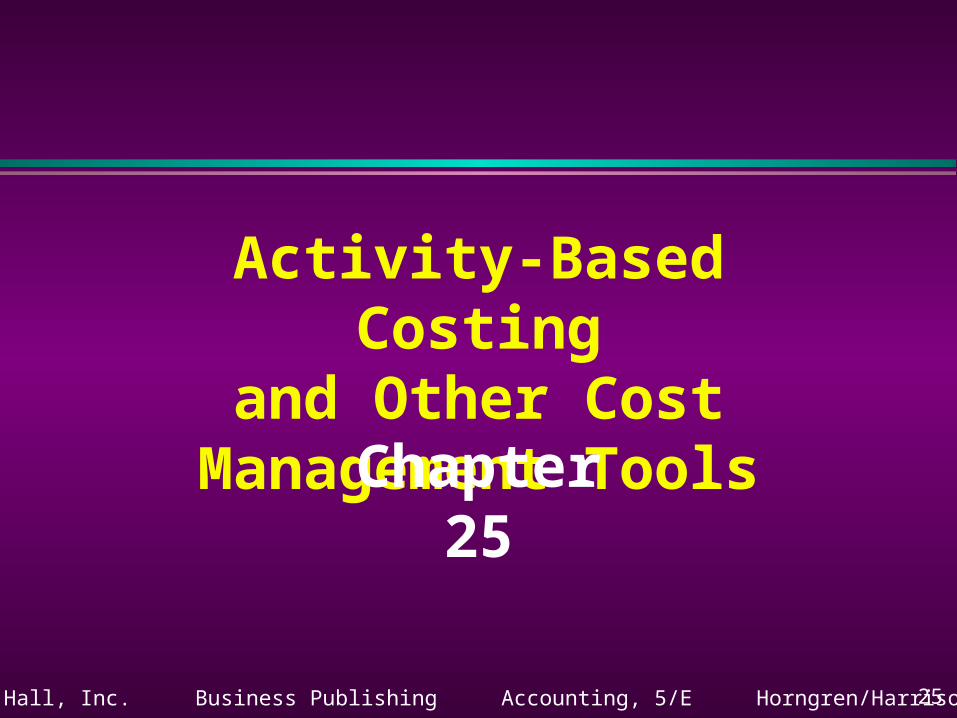

David, Matt, and Marc:Total expenses = $900

Cost allocated = $300 per person

Rent and Utilities $570Cable TV 50High speed Internet access 40Groceries 240Total $900

Refining Cost Systems

25 - 3©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

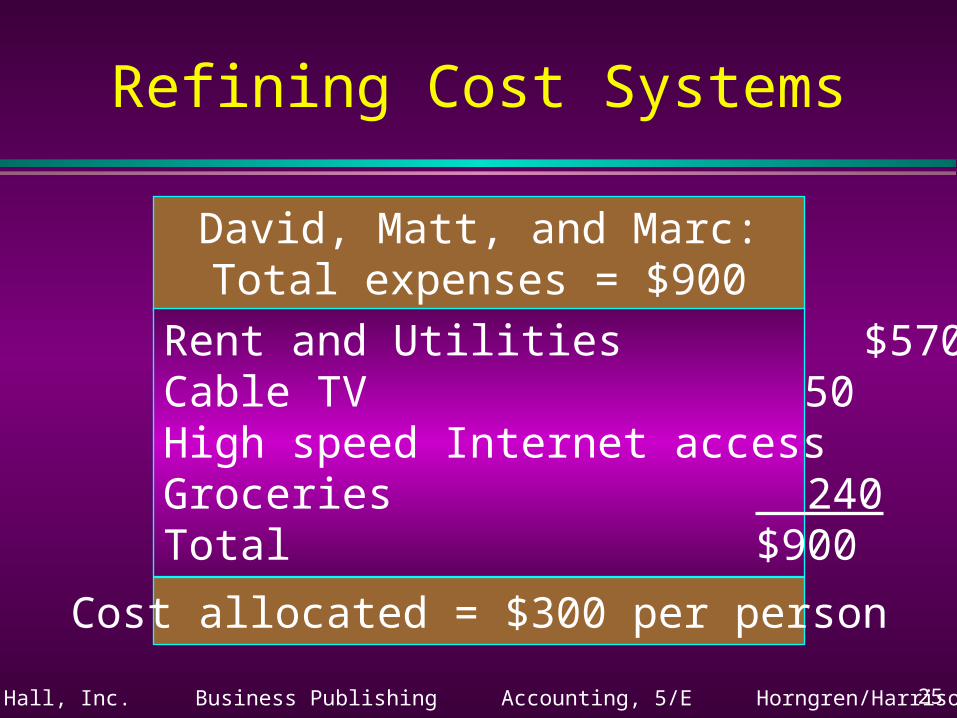

Refining Cost Systems

More Refined Allocation

David Matt Marc TotalRent and Utilities $190 $190 $190 $570Cable TV 25 – 25 50Internet access – 40 – 40Groceries – 80 160 240Total costs allocated $215 $310 $375 $900Original cost allocation 300 300 300 900Difference $(85) $ 10 $ 75 $ 0

25 - 4©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

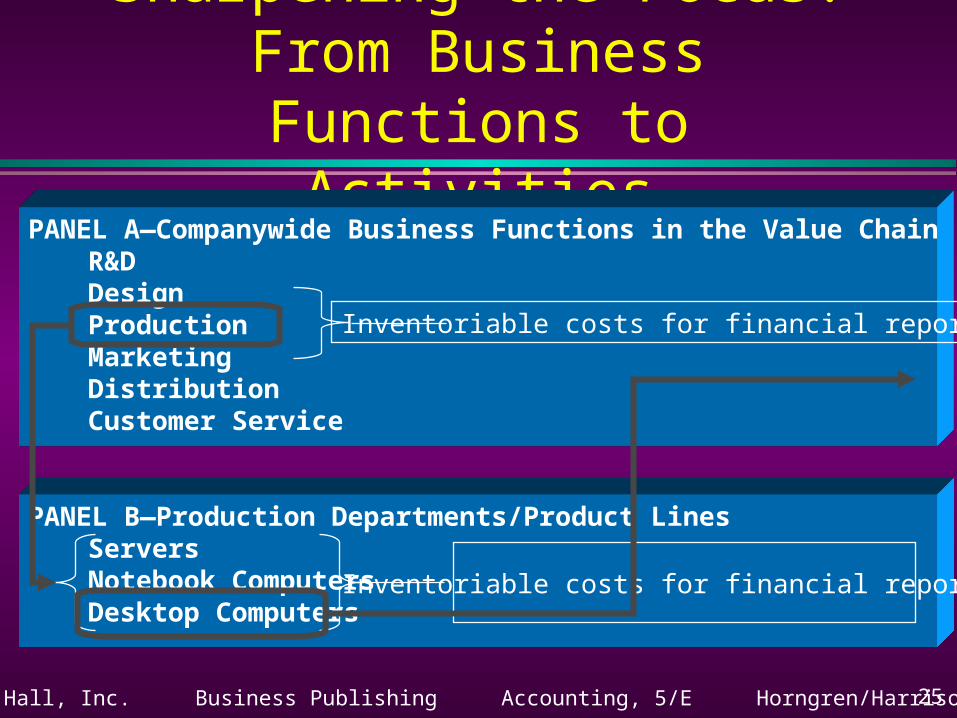

Sharpening the Focus: From Business Functions to Activities

PANEL A—Companywide Business Functions in the Value ChainR&DDesignProductionMarketingDistributionCustomer Service

PANEL B—Production Departments/Product LinesServersNotebook ComputersDesktop Computers

Inventoriable costs for financial reporting

Inventoriable costs for financial reporting

25 - 5©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

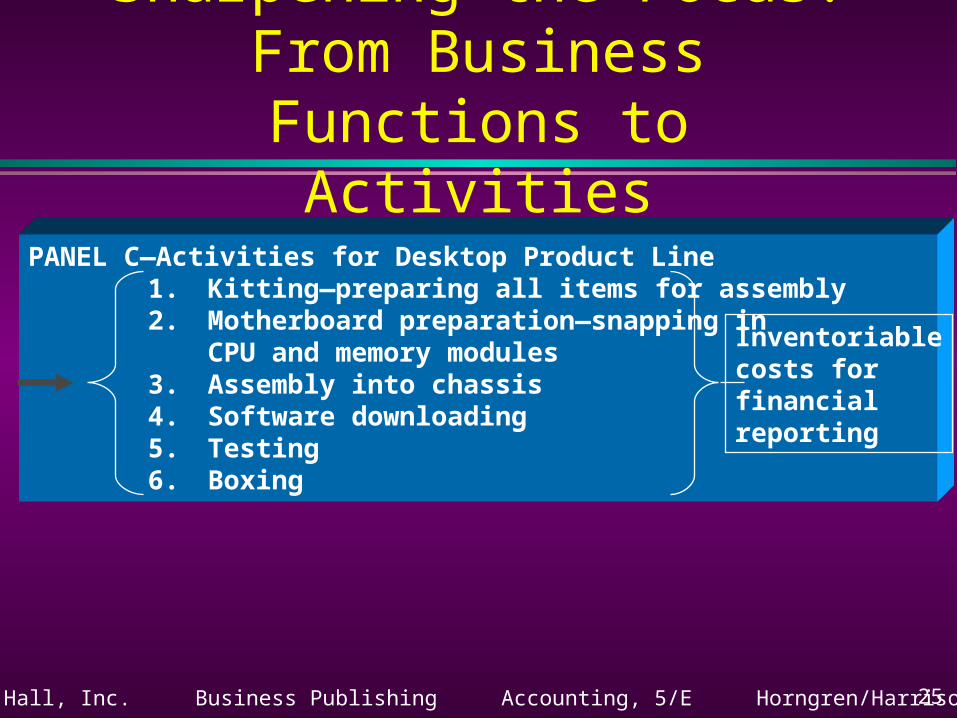

Sharpening the Focus: From Business Functions to Activities

PANEL C—Activities for Desktop Product Line1. Kitting—preparing all items for assembly2. Motherboard preparation—snapping in

CPU and memory modules3. Assembly into chassis4. Software downloading5. Testing6. Boxing

Inventoriablecosts forfinancialreporting

25 - 6©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Describe and developactivity-based costs

(ABC).

Objective 1

25 - 7©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

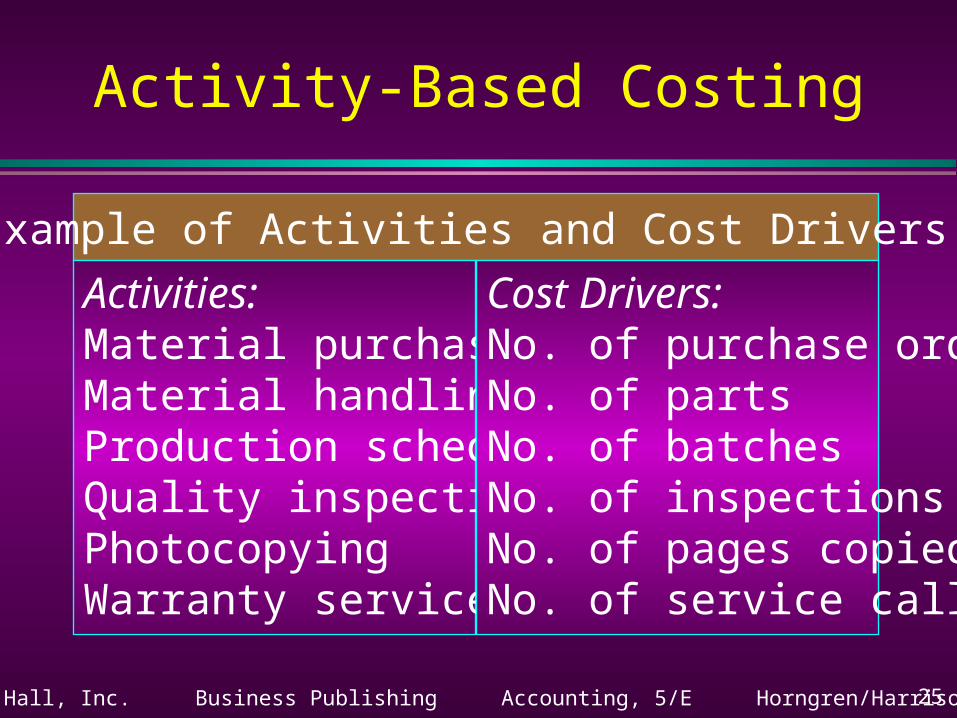

Example of Activities and Cost Drivers:

Activities:Material purchasingMaterial handlingProduction schedulingQuality inspectionsPhotocopyingWarranty service

Cost Drivers:No. of purchase ordersNo. of partsNo. of batchesNo. of inspectionsNo. of pages copiedNo. of service calls

Activity-Based Costing

25 - 8©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Traditional versus Activity-BasedCosting Systems

Chemtech produces large quantities of “commodity” chemicals.

It also manufactures small quantities of specialty chemicals.

In the past, Chemtech’s manufacturing department has used direct labor hours as its single allocation base at a 200% rate.

25 - 9©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Traditional versus Activity-BasedCosting Systems

Among its many products, the department produces Aldehyde (a commodity chemical used by producing plastics) and...

Phenylephrine Hydrochloride (PH), which is a specialty chemical.

A single customer uses PH in manufacturing blood-pressure medications.

25 - 10©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Traditional versus Activity-BasedCosting Systems

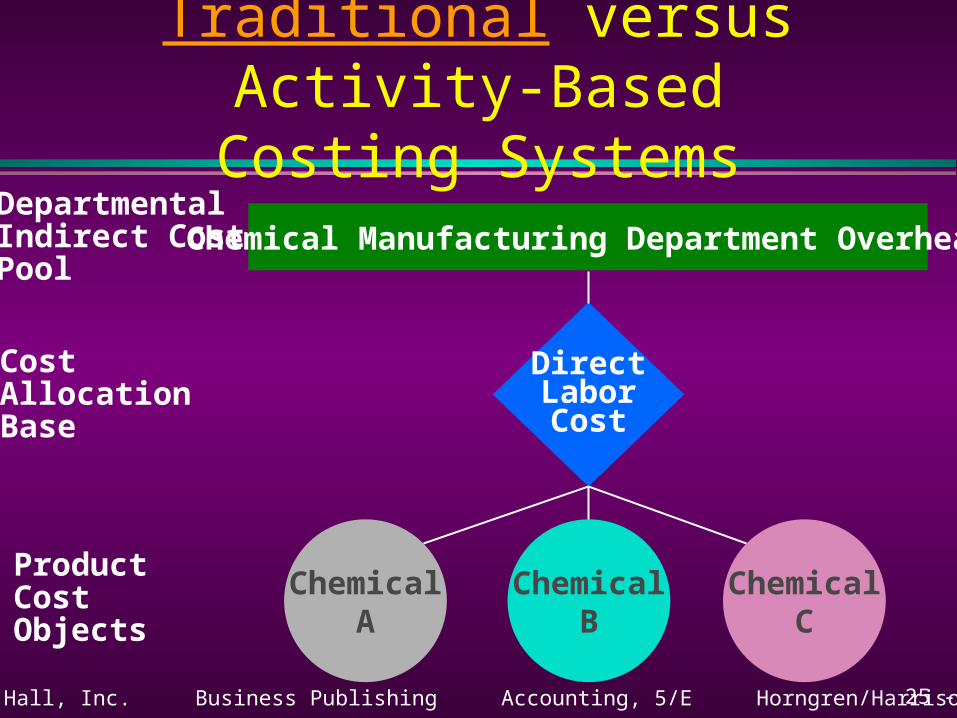

Chemical Manufacturing Department Overhead

DirectLaborCost

ChemicalA

ChemicalB

ChemicalC

DepartmentalIndirect CostPool

CostAllocationBase

ProductCostObjects

25 - 11©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Traditional versus Activity-BasedCosting Systems

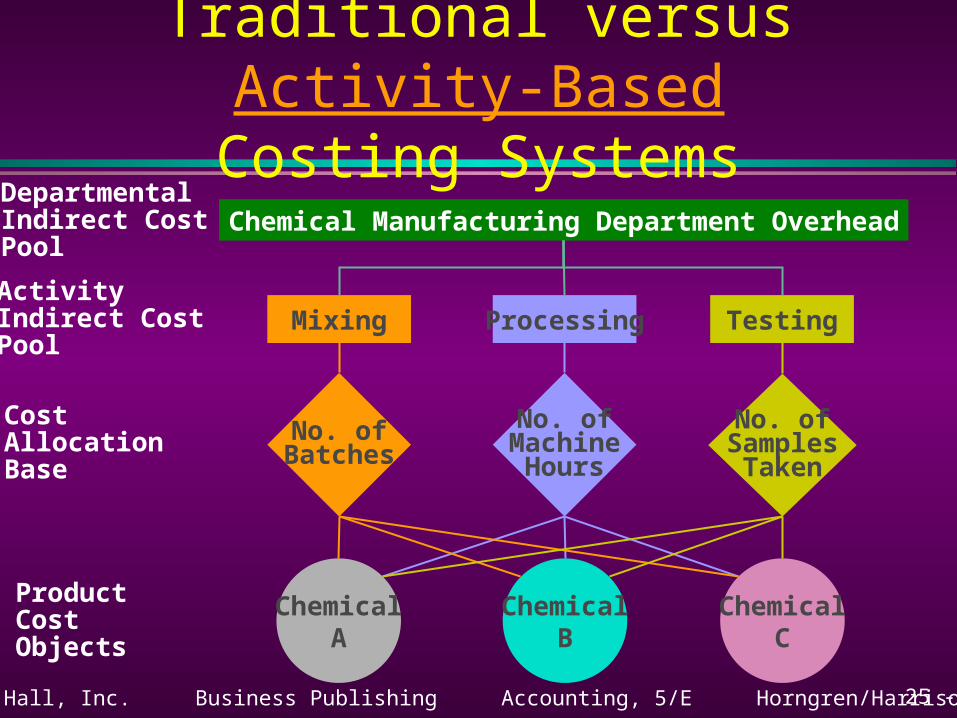

Chemical Manufacturing Department Overhead

No. ofMachine

Hours

ChemicalA

ChemicalB

ChemicalC

DepartmentalIndirect CostPool

CostAllocationBase

ProductCostObjects

No. ofSamplesTaken

No. ofBatches

ProcessingMixing TestingActivityIndirect CostPool

25 - 12©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

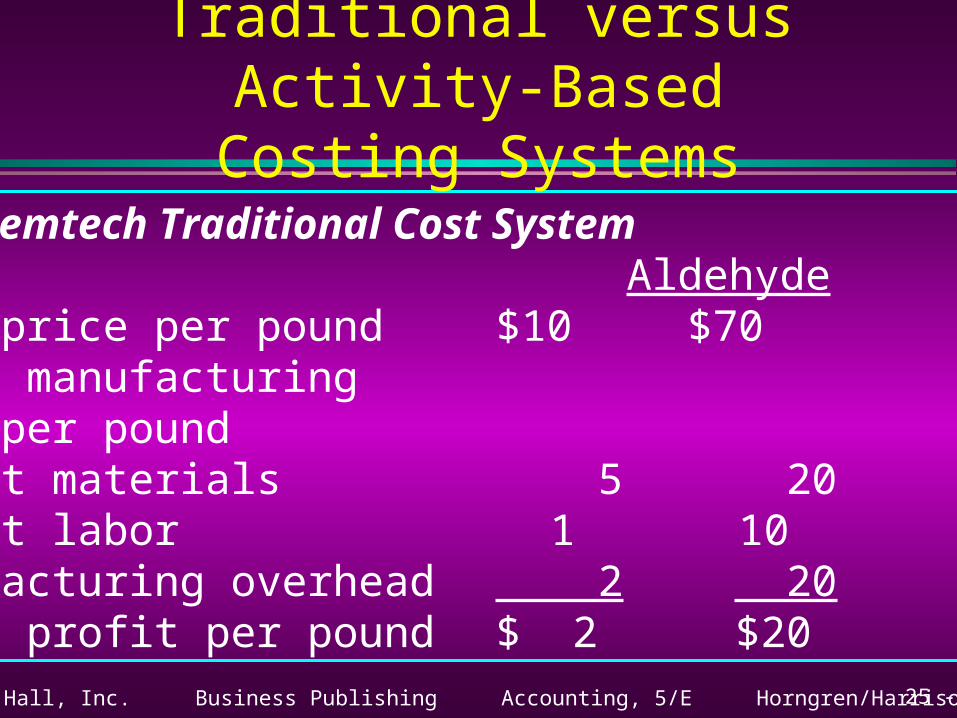

Chemtech Traditional Cost System Aldehyde PH

Sale price per pound $10 $70Less: manufacturingcost per poundDirect materials 5 20Direct labor 1 10Manufacturing overhead 2 20Gross profit per pound $ 2 $20

Traditional versus Activity-BasedCosting Systems

25 - 13©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Traditional versus Activity-BasedCosting Systems

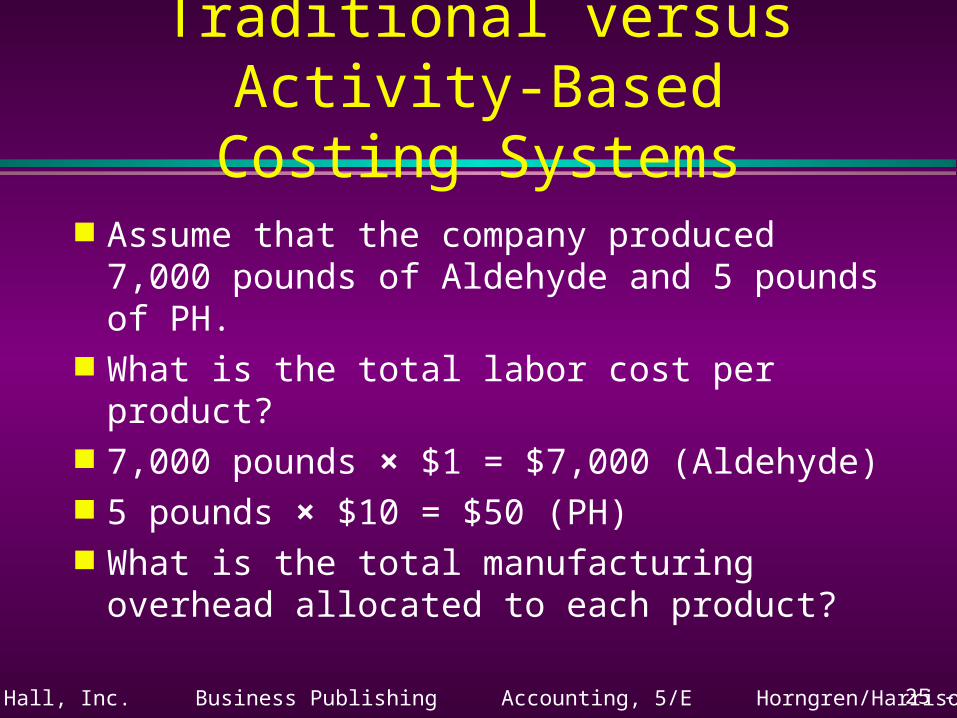

Assume that the company produced 7,000 pounds of Aldehyde and 5 pounds of PH.

What is the total labor cost per product? 7,000 pounds × $1 = $7,000 (Aldehyde) 5 pounds × $10 = $50 (PH) What is the total manufacturing overhead

allocated to each product?

25 - 14©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

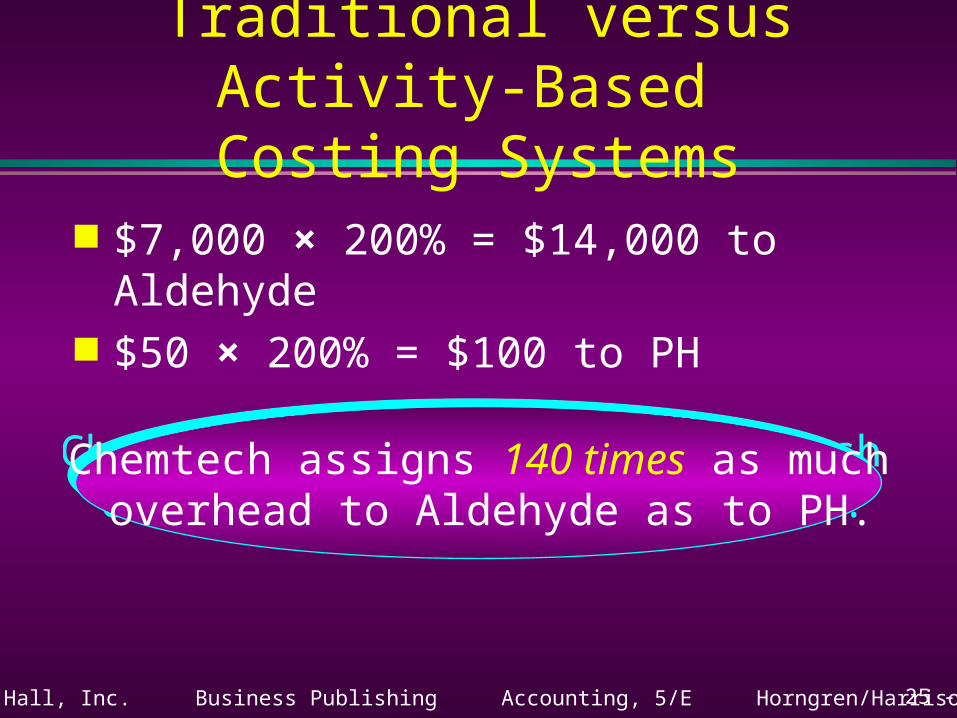

Chemtech assigns 140 times as much overhead to Aldehyde as to PH.

Chemtech assigns 140 times as much overhead to Aldehyde as to PH.

Traditional versus Activity-Based

Costing Systems $7,000 × 200% = $14,000 to Aldehyde $50 × 200% = $100 to PH

25 - 15©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Activity-Based Costing System

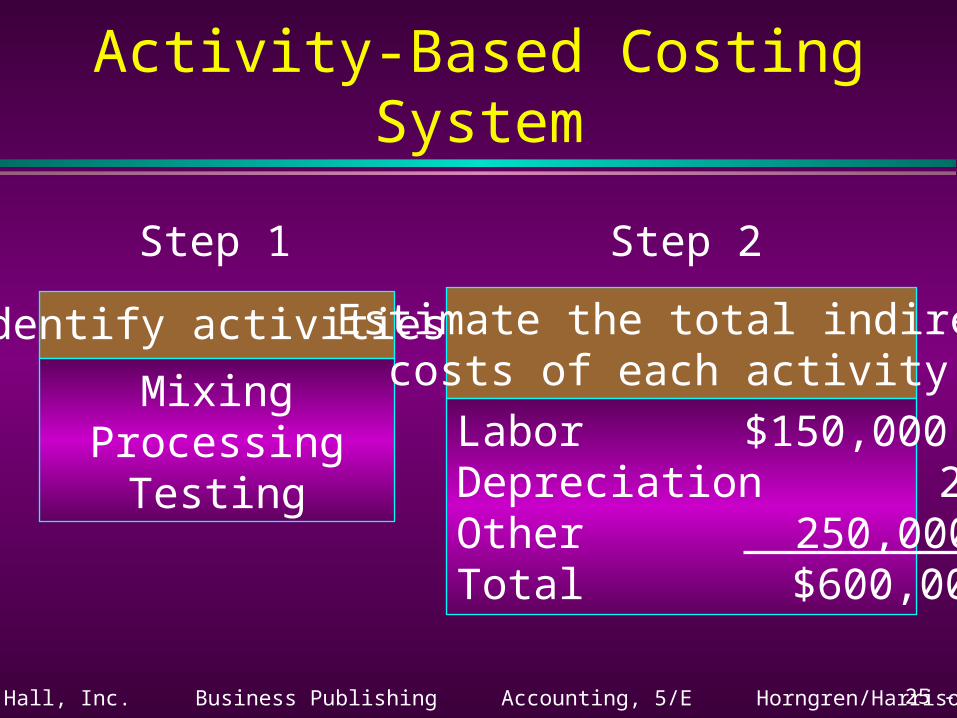

Identify activities.

MixingProcessing

Testing

Estimate the total indirectcosts of each activity.

Labor $150,000Depreciation 200,000Other 250,000Total $600,000

Step 1 Step 2

25 - 16©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

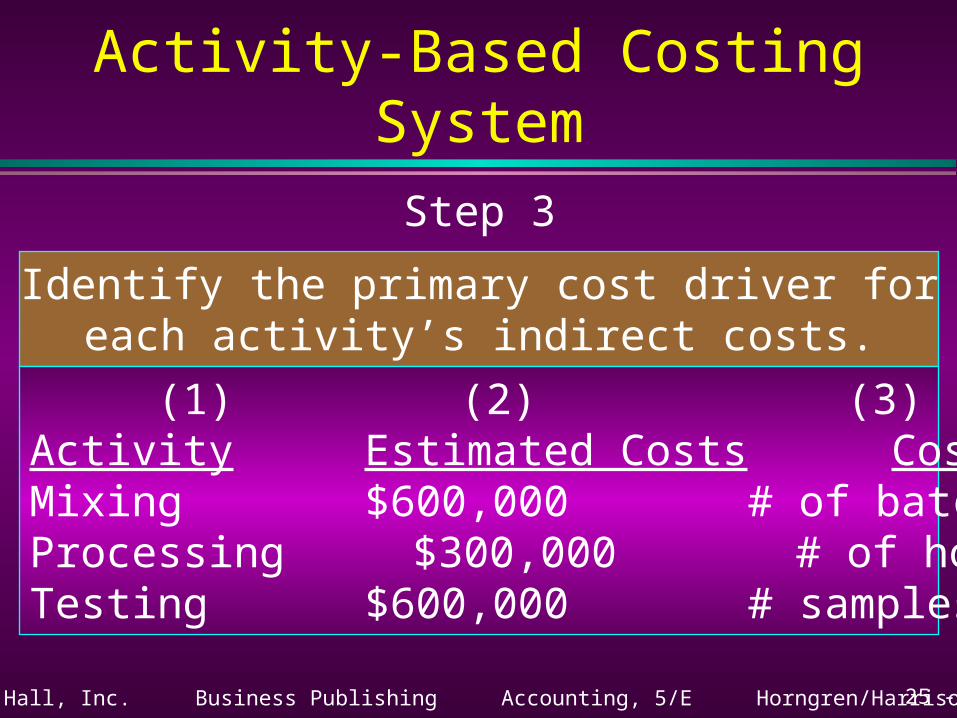

Activity-Based Costing System

Identify the primary cost driver foreach activity’s indirect costs.

(1) (2) (3)Activity Estimated Costs Cost DriverMixing $600,000 # of batchesProcessing $300,000 # of hours (MH)Testing $600,000 # samples

Step 3

25 - 17©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

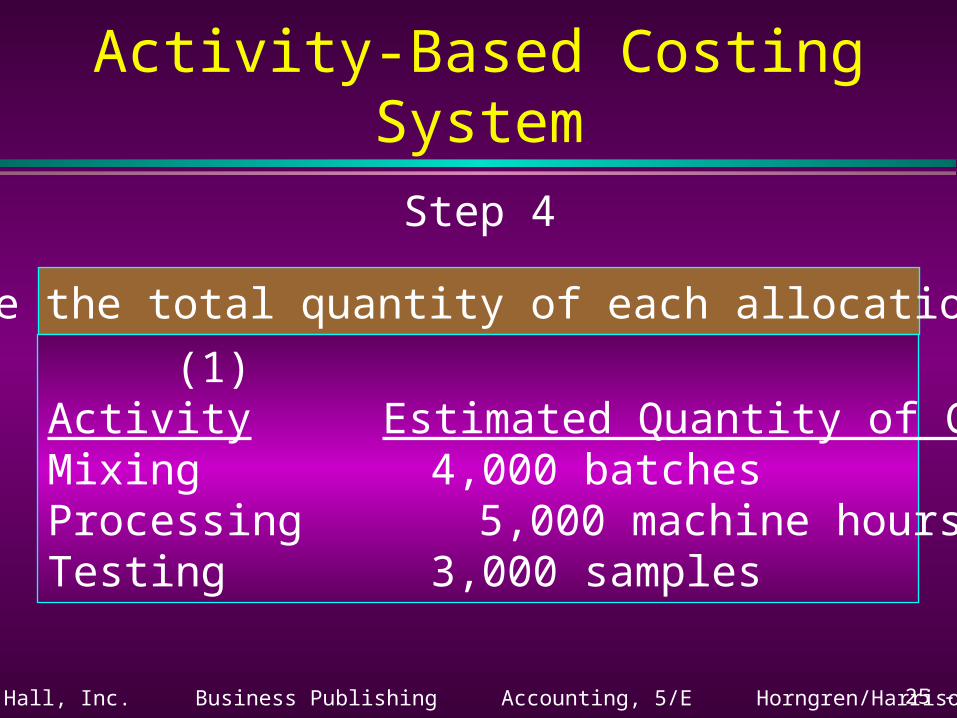

Activity-Based Costing System

Estimate the total quantity of each allocation base.

(1) (4)Activity Estimated Quantity of Cost DriverMixing 4,000 batchesProcessing 5,000 machine hours (MH)Testing 3,000 samples

Step 4

25 - 18©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

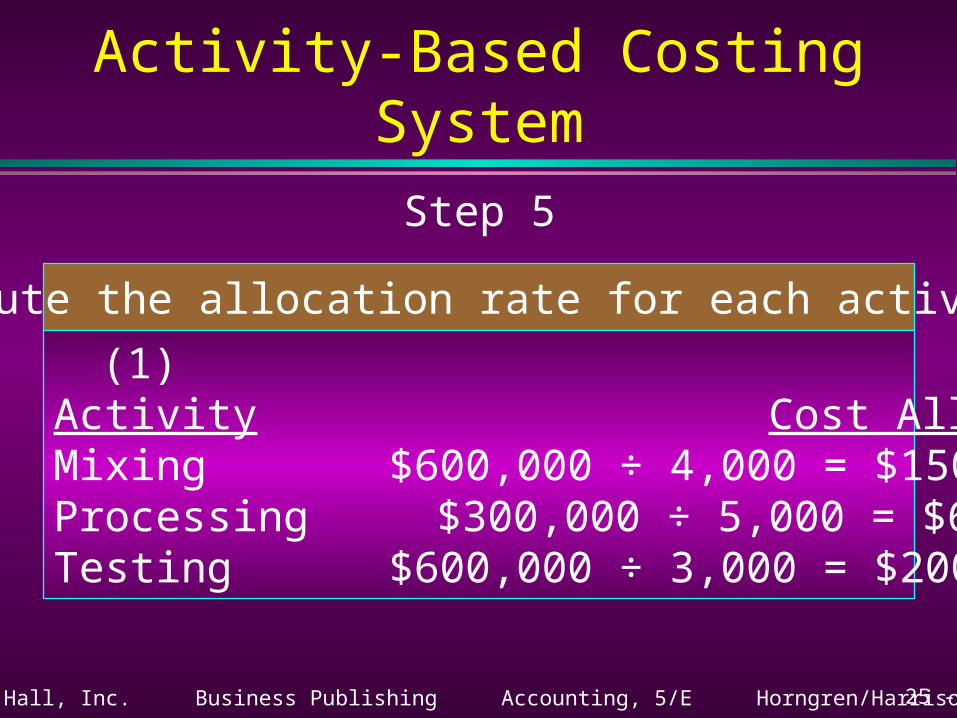

Activity-Based Costing System

Compute the allocation rate for each activity.

(1) (5)Activity Cost Allocation RateMixing $600,000 ÷ 4,000 = $150/batchProcessing $300,000 ÷ 5,000 = $60/MHTesting $600,000 ÷ 3,000 = $200/sample

Step 5

25 - 19©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

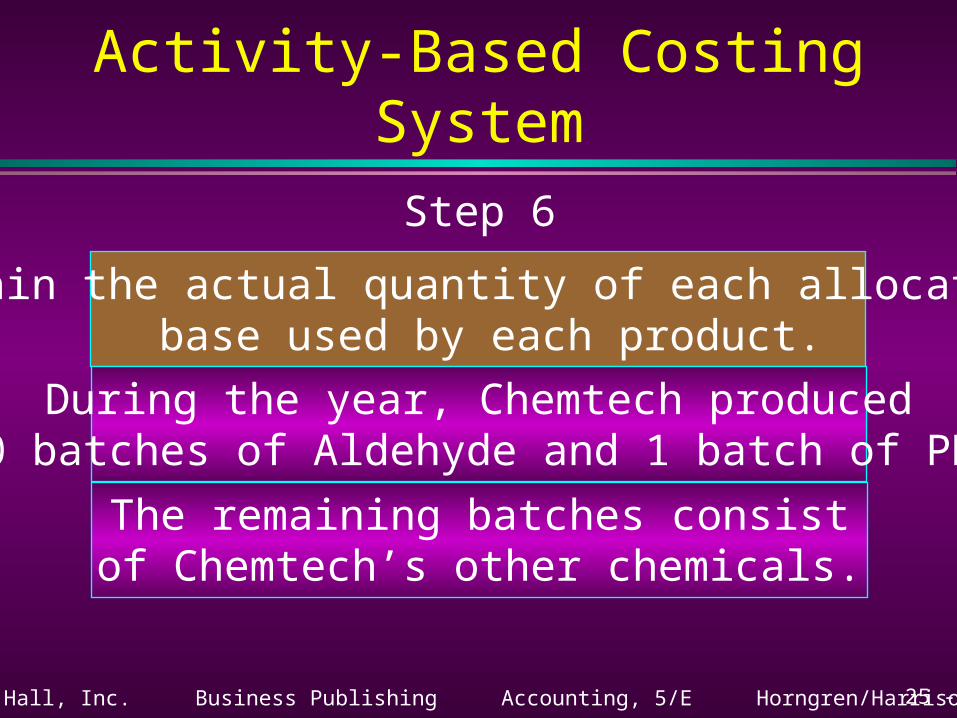

Activity-Based Costing System

Obtain the actual quantity of each allocation base used by each product.

During the year, Chemtech produced60 batches of Aldehyde and 1 batch of PH.

The remaining batches consistof Chemtech’s other chemicals.

Step 6

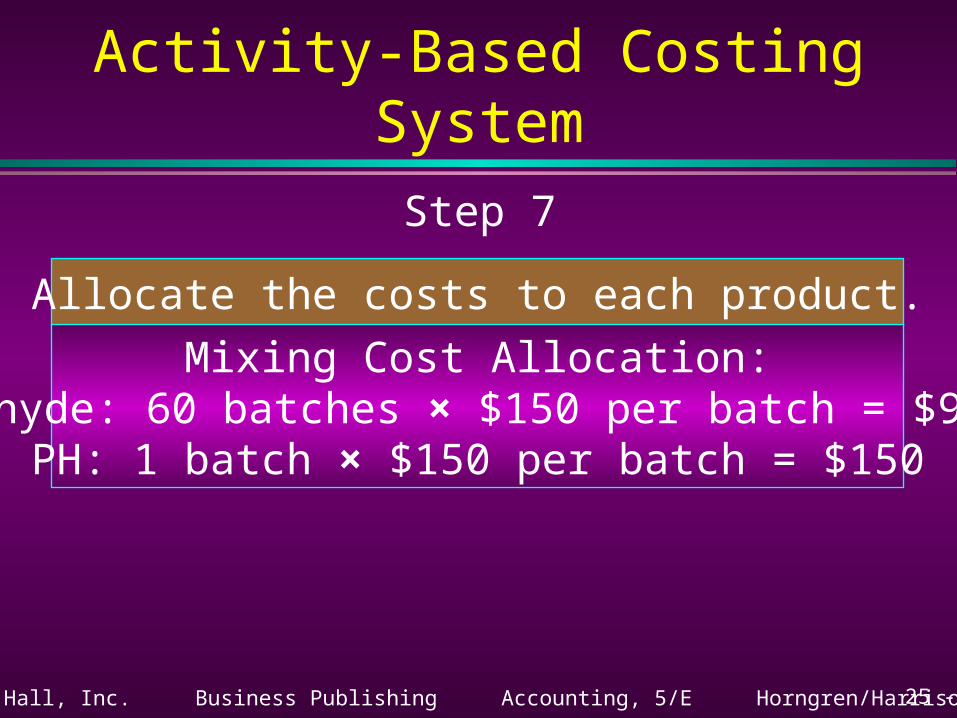

25 - 20©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Activity-Based Costing System

Allocate the costs to each product.

Mixing Cost Allocation:Aldehyde: 60 batches × $150 per batch = $9,000

PH: 1 batch × $150 per batch = $150

Step 7

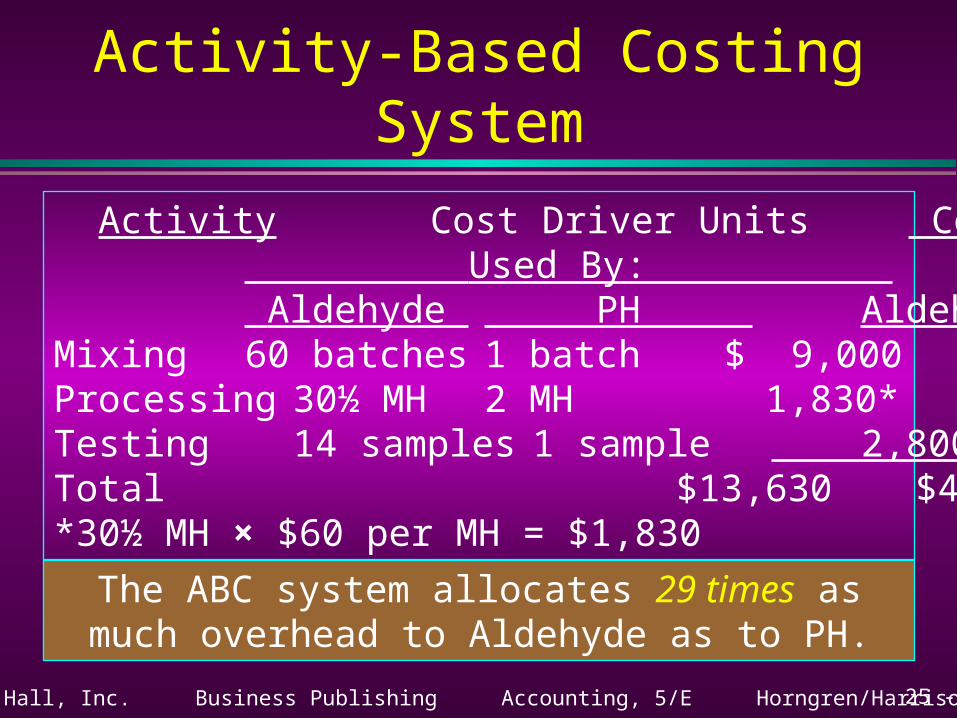

25 - 21©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Activity-Based Costing System

The ABC system allocates 29 times asmuch overhead to Aldehyde as to PH.

Activity Cost Driver Units Cost Allocated to: Used By: Aldehyde PH Aldehyde PH

Mixing 60 batches 1 batch $ 9,000 $150Processing 30½ MH 2 MH 1,830* 120Testing 14 samples 1 sample 2,800 200Total $13,630 $470*30½ MH × $60 per MH = $1,830

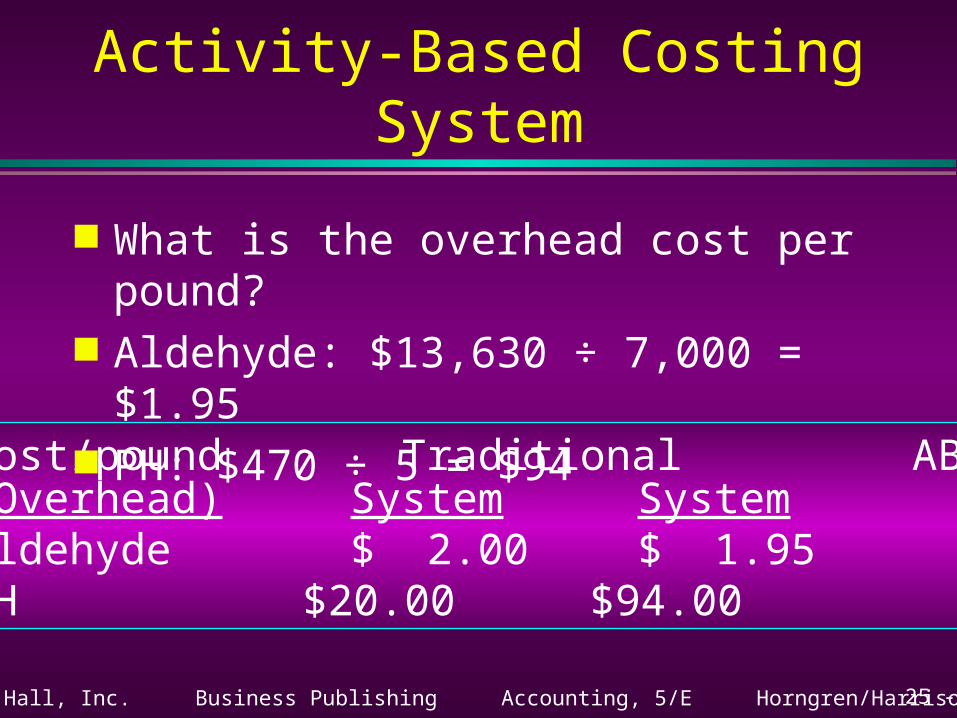

25 - 22©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Cost/pound Traditional ABC(Overhead) System SystemAldehyde $ 2.00 $ 1.95PH $20.00 $94.00

Activity-Based Costing System

What is the overhead cost per pound? Aldehyde: $13,630 ÷ 7,000 = $1.95 PH: $470 ÷ 5 = $94

25 - 23©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

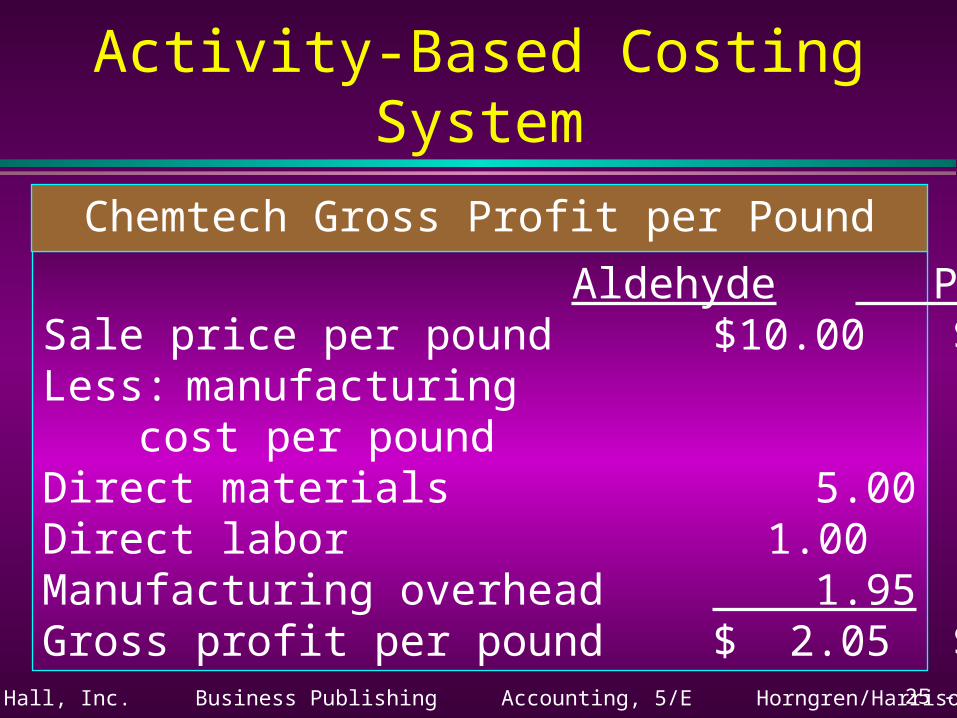

Aldehyde PH Sale price per pound $10.00 $ 70.00Less: manufacturing

cost per poundDirect materials 5.00 20.00Direct labor 1.00 10.00Manufacturing overhead 1.95 94.00 Gross profit per pound $ 2.05 $(54.00)

Activity-Based Costing System

Chemtech Gross Profit per Pound

25 - 24©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Use ABC data and activity-based

management (ABM) to makebusiness decisions.

Objective 2

25 - 25©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

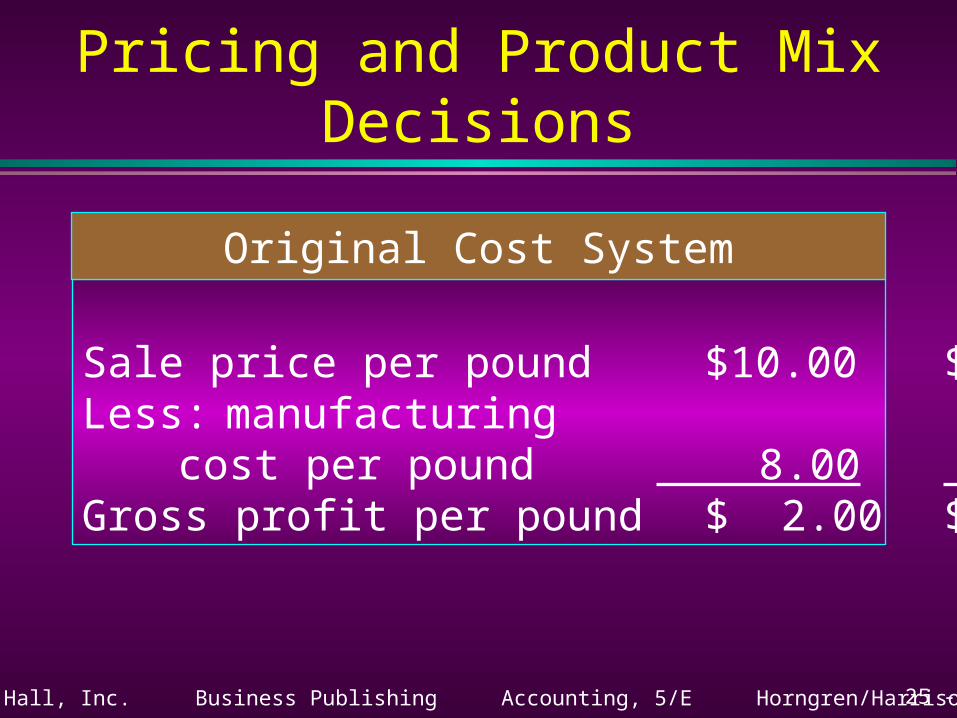

Pricing and Product Mix Decisions

Aldehyde PH Sale price per pound $10.00 $70.00Less: manufacturing

cost per pound 8.00 50.00Gross profit per pound $ 2.00 $20.00

Original Cost System

25 - 26©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

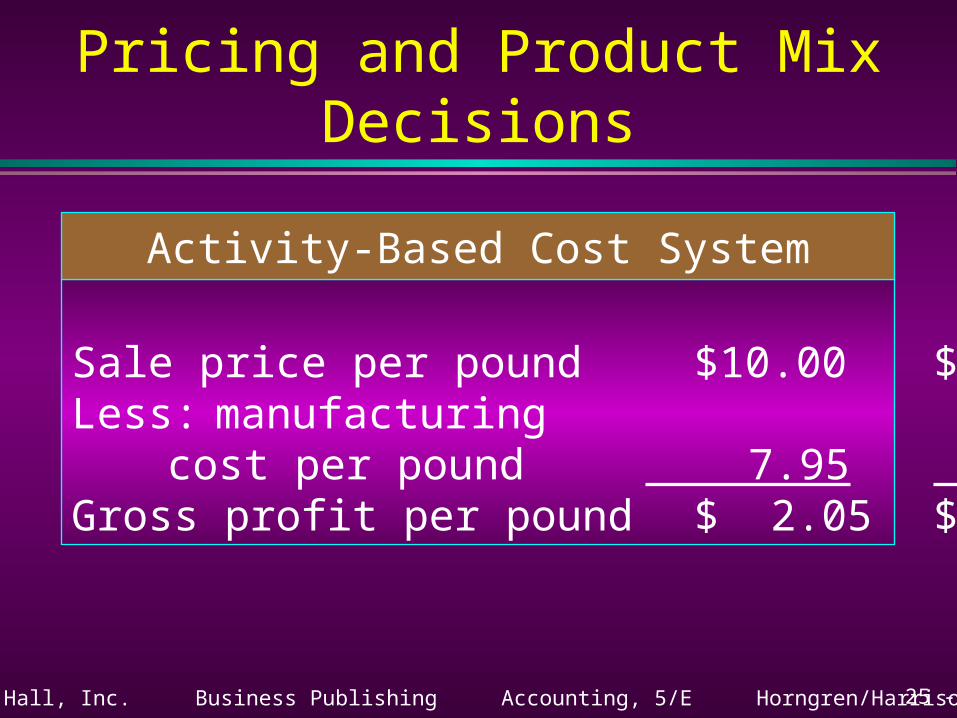

Pricing and Product Mix Decisions

Aldehyde PH Sale price per pound $10.00 $70.00Less: manufacturing

cost per pound 7.95 124.00Gross profit per pound $ 2.05 $(54.00)

Activity-Based Cost System

25 - 27©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

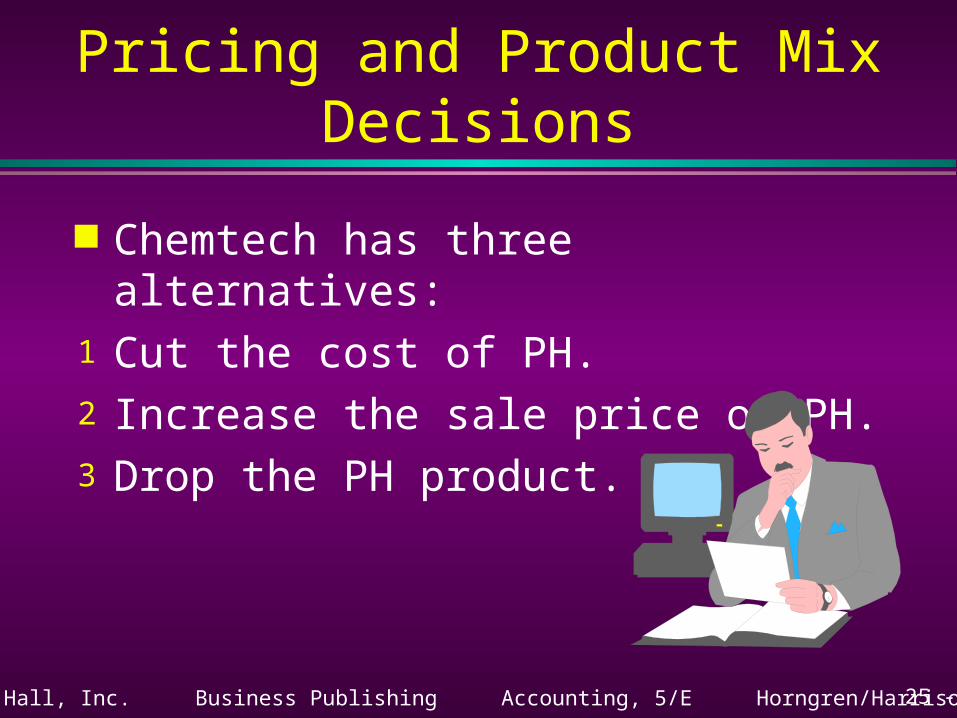

Pricing and Product Mix Decisions

Chemtech has three alternatives:1 Cut the cost of PH.2 Increase the sale price of PH.3 Drop the PH product.

25 - 28©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Use ABM and valueengineering to achievetarget costs for target

pricing.

Objective 3

25 - 29©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Cost Reduction Decisions

Value engineering means systematically evaluating activities in an effort to reduce costs while satisfying customer needs.

25 - 30©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

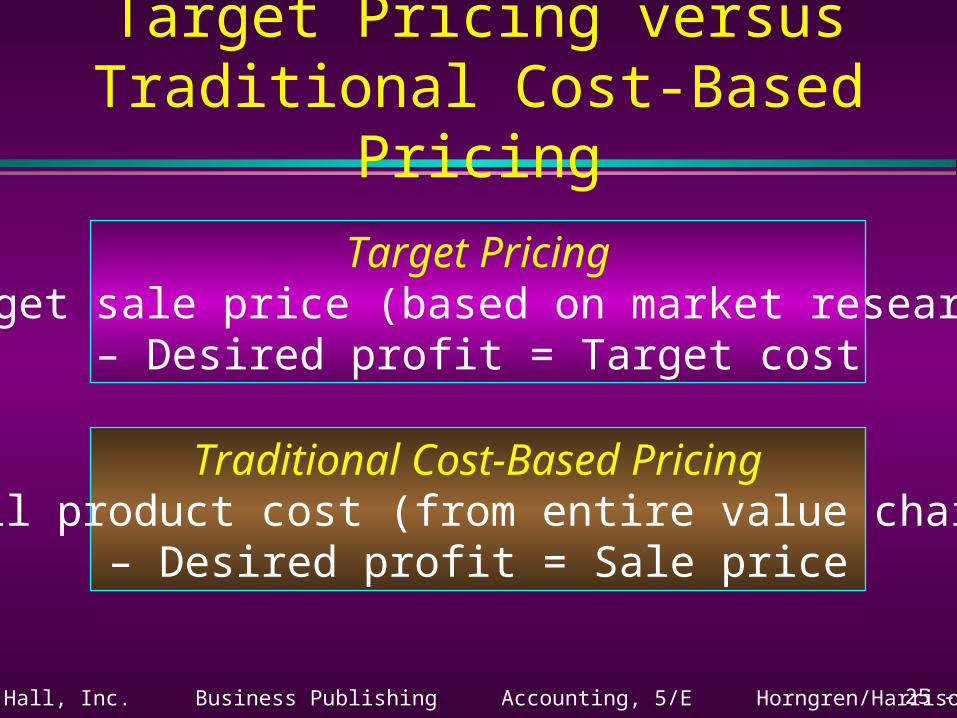

Target PricingTarget sale price (based on market research)

– Desired profit = Target cost

Traditional Cost-Based PricingFull product cost (from entire value chain)

– Desired profit = Sale price

Target Pricing versus Traditional Cost-Based Pricing

25 - 31©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

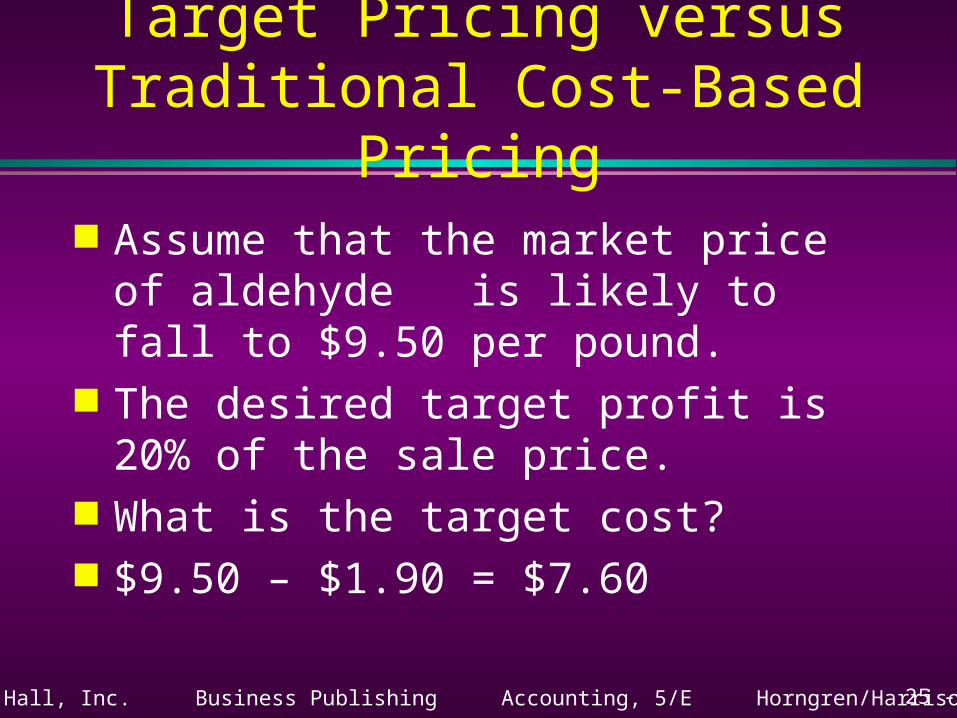

Target Pricing versus Traditional Cost-Based Pricing

Assume that the market price of aldehyde is likely to fall to $9.50 per pound.

The desired target profit is 20% of the sale price.

What is the target cost? $9.50 – $1.90 = $7.60

25 - 32©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

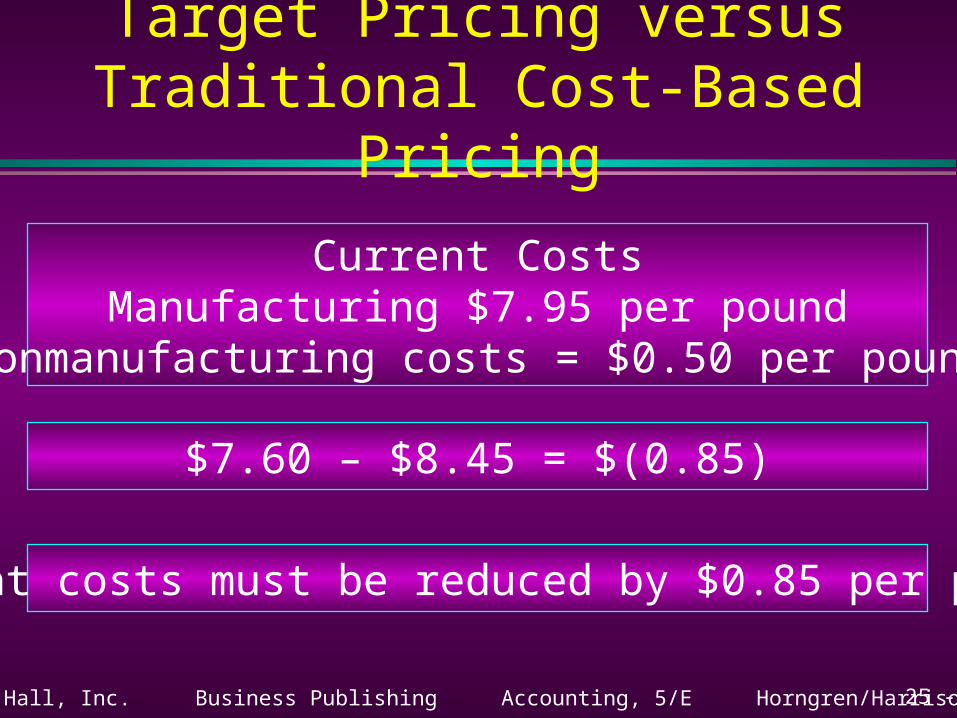

Target Pricing versus Traditional Cost-Based Pricing

Current CostsManufacturing $7.95 per pound

Nonmanufacturing costs = $0.50 per pound

$7.60 – $8.45 = $(0.85)

Current costs must be reduced by $0.85 per pound.

25 - 33©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Decide when ABC is most likely

to pass the cost-benefit test.

Objective 4

25 - 34©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

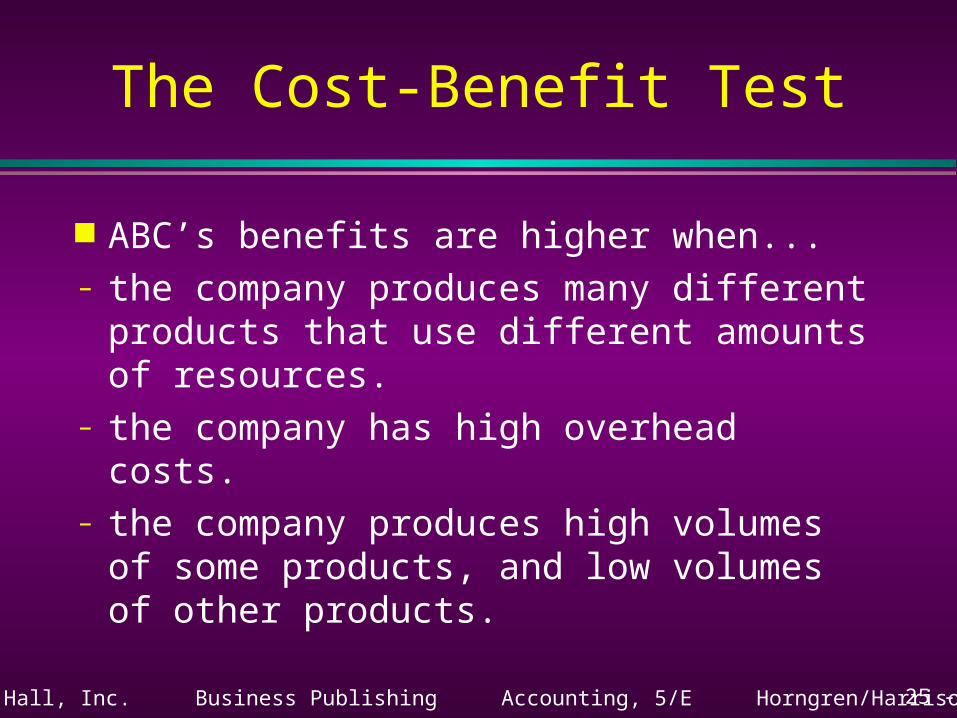

The Cost-Benefit Test

ABC’s benefits are higher when...– the company produces many different

products that use different amounts of resources.

– the company has high overhead costs.– the company produces high volumes of some

products, and low volumes of other products.

25 - 35©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

The Cost-Benefit Test

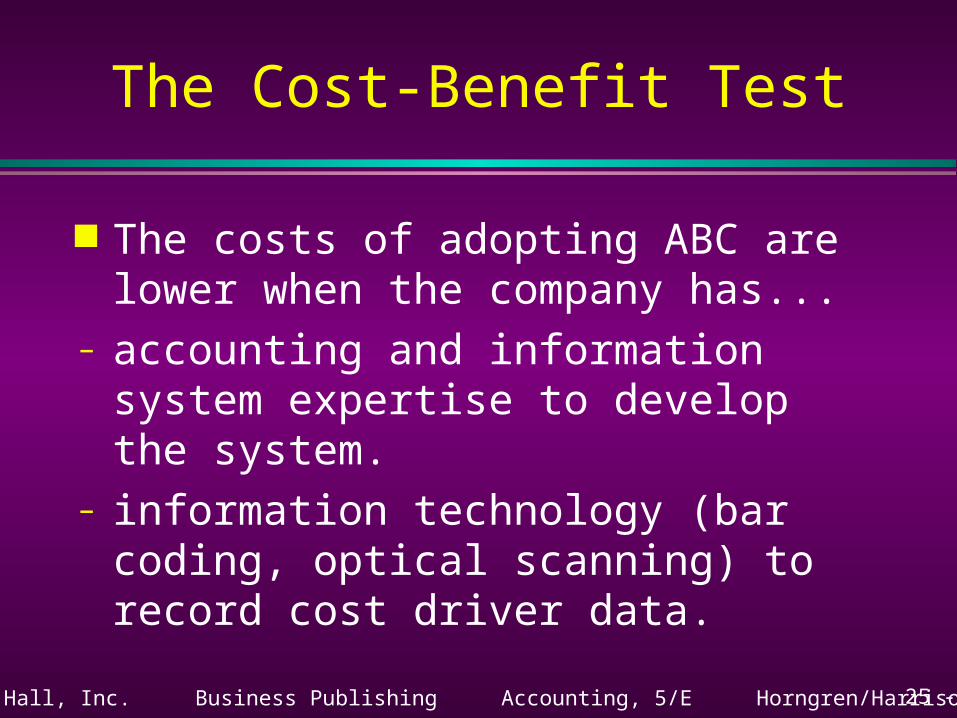

The costs of adopting ABC are lower when the company has...

– accounting and information system expertise to develop the system.

– information technology (bar coding, optical scanning) to record cost driver data.

25 - 36©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Managers don’t understand costs and profits.

The cost system is outdated.

Signs That the Cost SystemMay Be Broken

25 - 37©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Compare a traditional production

system to a just-in-time(JIT) production system.

Objective 5

25 - 38©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

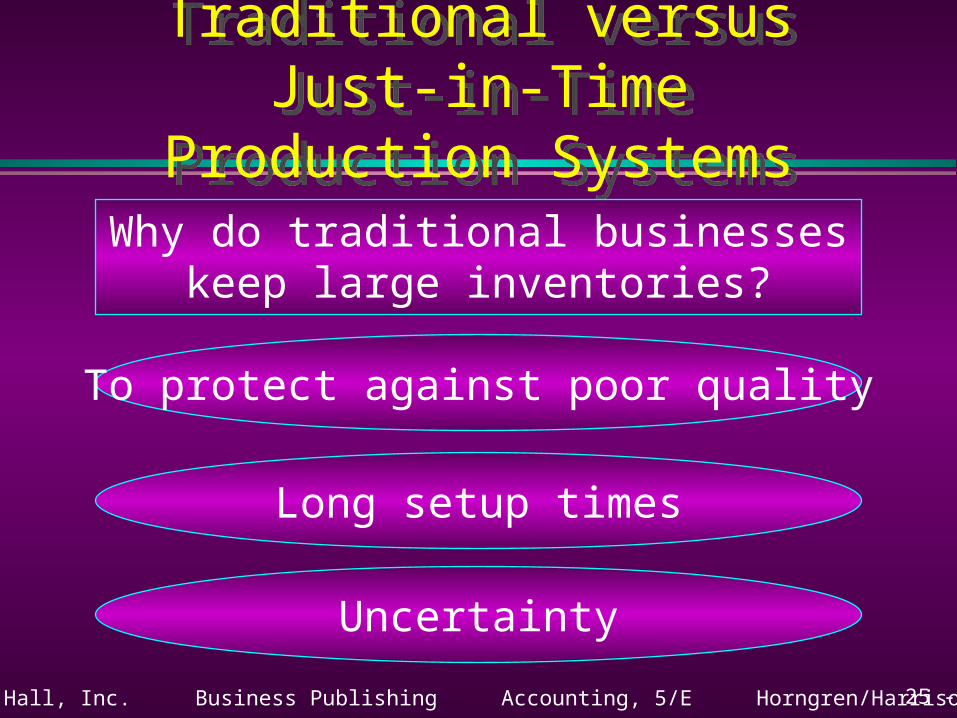

Traditional versus Just-in-Time Production Systems

Traditional versus Just-in-Time Production Systems

Why do traditional businesseskeep large inventories?

To protect against poor quality

Long setup times

Uncertainty

25 - 39©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

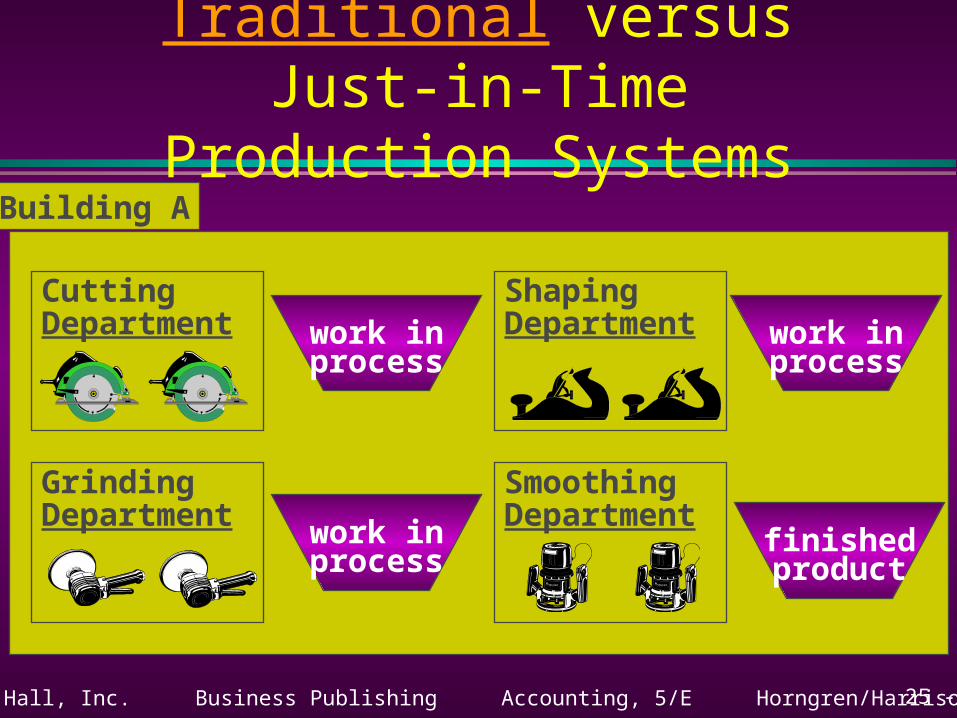

Traditional versus Just-in-Time Production Systems

Building A

CuttingDepartment work in

process

ShapingDepartment work in

process

GrindingDepartment work in

process

SmoothingDepartment

finishedproduct

25 - 40©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Traditional versus Just-in-Time Production Systems

Building A

cuttingmachine

shapingmachine

smoothingmachine

finishedproduct

grindingmachine

25 - 41©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Traditional versus Just-in-Time Production Systems

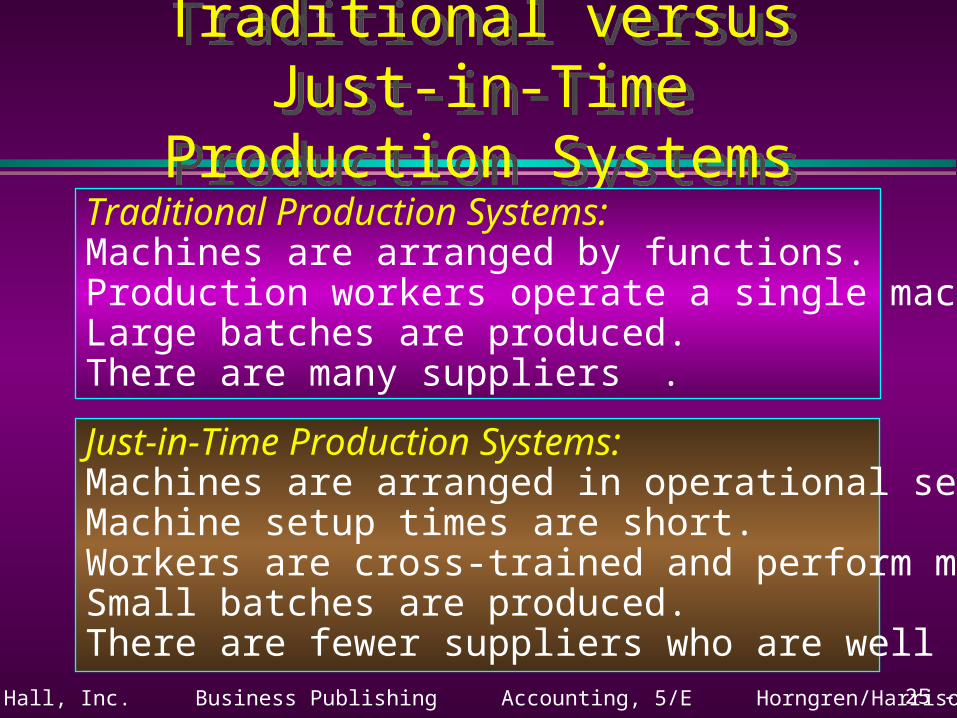

Traditional versus Just-in-Time Production Systems

Traditional Production Systems:Machines are arranged by functions.Production workers operate a single machine.Large batches are produced.There are many suppliers .

Just-in-Time Production Systems:Machines are arranged in operational sequence.Machine setup times are short.Workers are cross-trained and perform many tasks.Small batches are produced.There are fewer suppliers who are well coordinated.

25 - 42©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

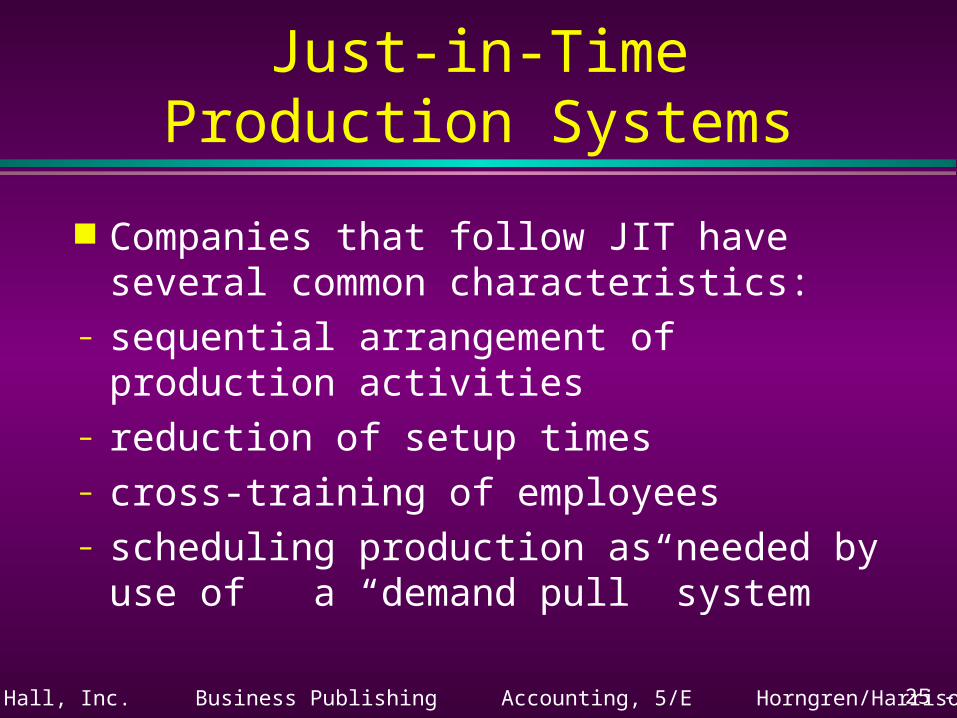

Just-in-Time Production Systems

Companies that follow JIT have several common characteristics:

– sequential arrangement of production activities

– reduction of setup times– cross-training of employees– scheduling production as needed by use of a

“demand pull” system

25 - 43©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Record manufacturing

costs for a just-in-timecosting system.

Objective 6

25 - 44©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

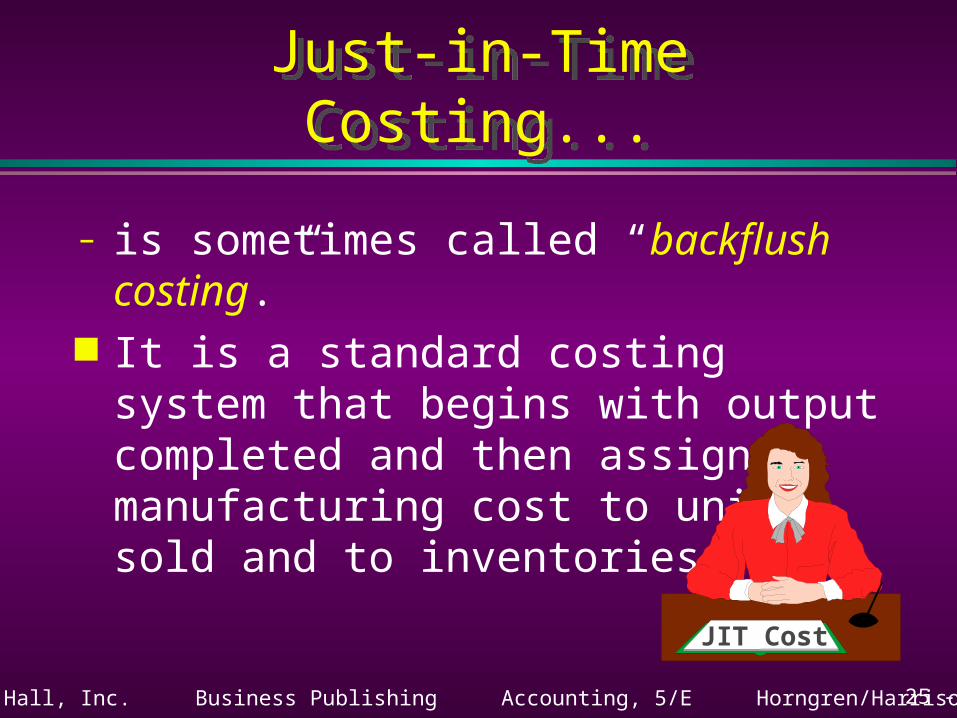

Just-in-Time Costing...Just-in-Time Costing...

– is sometimes called “backflush costing.” It is a standard costing system that begins

with output completed and then assigns manufacturing cost to units sold and to inventories.

JIT Cost

25 - 45©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

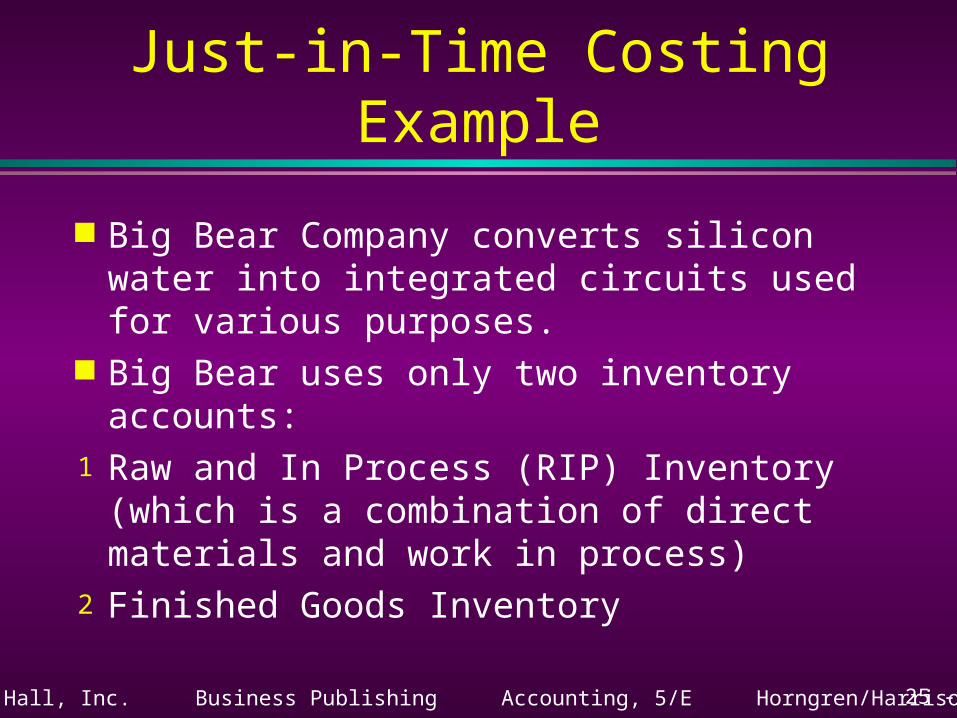

Just-in-Time Costing Example

Big Bear Company converts silicon water into integrated circuits used for various purposes.

Big Bear uses only two inventory accounts:1 Raw and In Process (RIP) Inventory (which

is a combination of direct materials and work in process)

2 Finished Goods Inventory

25 - 46©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

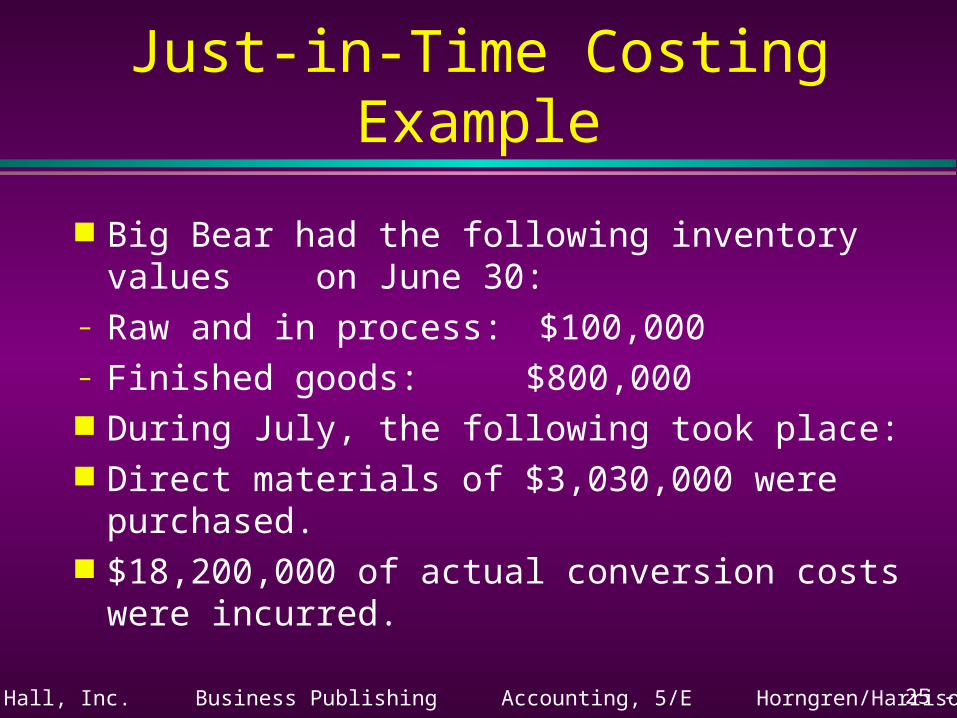

Just-in-Time Costing Example

Big Bear had the following inventory values on June 30:

– Raw and in process: $100,000– Finished goods: $800,000 During July, the following took place: Direct materials of $3,030,000 were purchased. $18,200,000 of actual conversion costs were

incurred.

25 - 47©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

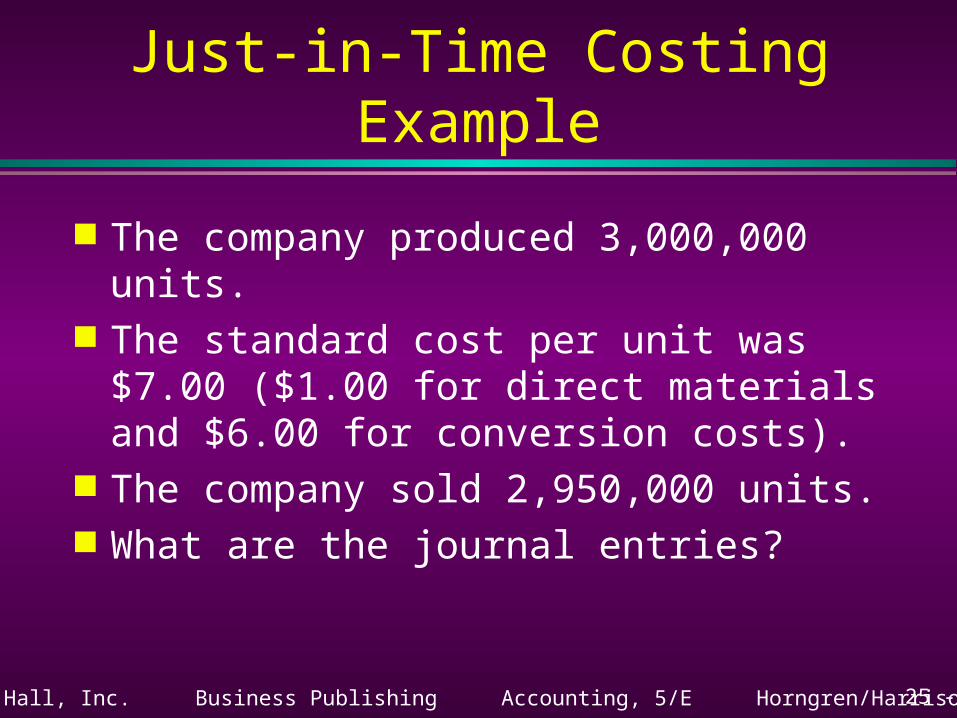

Just-in-Time Costing Example

The company produced 3,000,000 units. The standard cost per unit was $7.00 ($1.00

for direct materials and $6.00 for conversion costs).

The company sold 2,950,000 units. What are the journal entries?

25 - 48©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

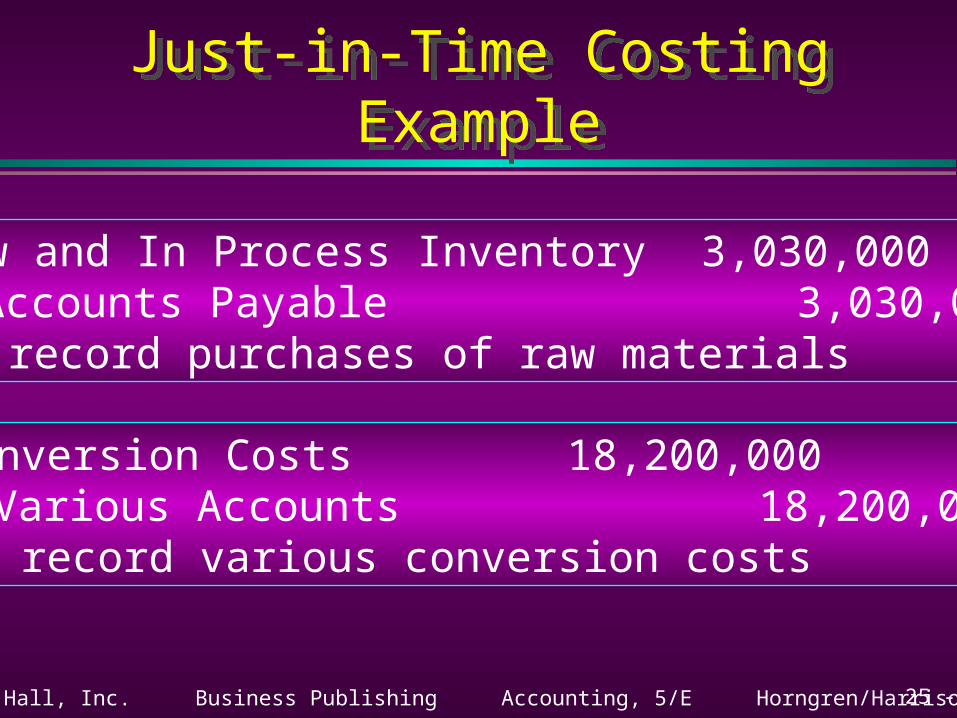

Just-in-Time Costing ExampleJust-in-Time Costing Example

Raw and In Process Inventory 3,030,000Accounts Payable 3,030,000

To record purchases of raw materials

Conversion Costs 18,200,000Various Accounts 18,200,000

To record various conversion costs

25 - 49©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Finished Goods Inventory 21,000,000RIP Inventory 3,000,000Conversion Costs 18,000,000

Completed units

Cost of Goods Sold 20,650,000Finished Goods Inventory 20,650,000

To record 2,950,000 units sold

Just-in-Time Costing Example

25 - 50©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

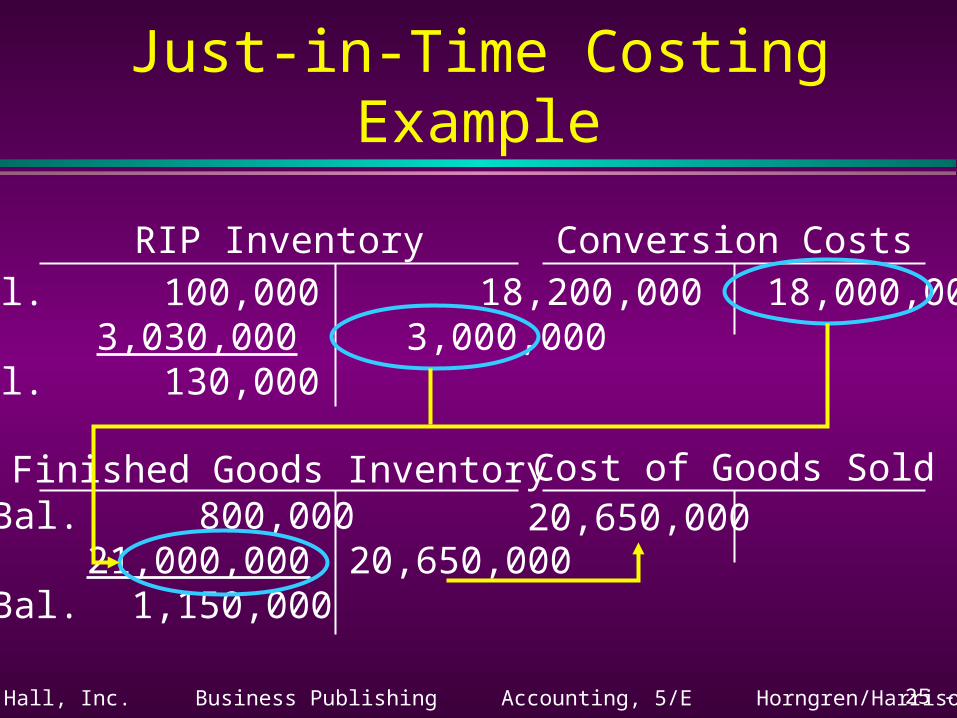

Just-in-Time Costing Example

RIP Inventory Conversion Costs

Finished Goods Inventory Cost of Goods Sold

Bal. 100,000 3,030,000 3,000,000

Bal. 130,000

18,200,000 18,000,000

Bal. 800,00021,000,000 20,650,000

Bal. 1,150,000

20,650,000

25 - 51©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Contrast the four types ofquality costs and use

thesecosts to make decisions.

Objective 7

25 - 52©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Total Quality Management

The goal of total quality management (TQM) is to provide customers with superior products and services.

Total quality management (TQM) describes the entire effort of improving quality throughout the organization’s value chain.

25 - 53©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Types of Quality Costs

Prevention costs are incurred to avoid inferior quality goods or services.

Training personnelEvaluating potential suppliers

Improved materialsPreventive maintenance

Improved equipment and processes

25 - 54©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Types of Quality Costs

Appraisal costs are incurred todetect inferior quality goods or services.

Inspection of incoming materialsInspection at various stages of production

Inspection of final products or servicesProduct testing

25 - 55©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Types of Quality Costs

Internal failure costs are incurred when the company detects and corrects inferior quality

goods or services before delivery to customers.

Production loss caused by downtimeReworkScrap

Rejected product unitsDisposal of rejected units

25 - 56©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

Types of Quality Costs

External failure costs are incurred wheninferior quality goods or services are notdetected until after delivery to customers.

Profit losses from lost customersWarranty costs

Service costs at customer sitesSales returns due to quality problems

Product liability claims

25 - 57©2002 Prentice Hall, Inc. Business Publishing Accounting, 5/E Horngren/Harrison/Bamber

End of Chapter 25