Embed Size (px)

Citation preview

28 February 2008

Sir Ian RobinsonChairman

28 February 2008

Brian WallaceGroup Finance Director

Summary of performanceYear to 31 December

Continuing operations

Operating profit(1)

Net finance costs(1)

Interest income on Hotels sale proceeds

Profit before tax(1)

Effective tax rate(1)

EBITDA(1)

EPS(1)

2007£m

420.0

(68.0)

-

352.0

15.6%

470.4

47.4p

2006£m

262.2

(44.6)

24.0

241.6

17.5%

304.4

21.7p

Variance B(W)%

60.2

(52.5)

(100.0)

45.7

54.5

118.4(1) Before non-trading items

Betting and GamingYear to 31 December

UK Retail

Ireland, Belgium & Italy

eGaming

Telephone Betting

Other (2)

Corporate Costs

Total

2007£m

739.3

103.1

156.5

280.1

7.4

-

1,286.4

2006£m

715.8

84.0

144.4

46.1

-

-

990.3

VarianceB(W)%

3.3

22.7

8.4

507.6

29.9

2007£m

187.8

21.7

55.0

183.6

(7.0)

(21.1)

420.0

2006(1)

£m

199.8

17.0

44.3

17.3

(1.6)

(14.6)

262.2

VarianceB(W)%

(6.0)

27.6

24.2

961.3

(337.5)

(44.5)

60.2

Operating ProfitGross Win

(1) Restated divisions operating profit. Total operating profit remains unchanged(2) Other is casino and international development operations

UK Retail – Results2007£m

490.9248.4 739.3(37.5)701.8

4.0(72.1)

(201.3)(93.9)(58.1)(92.6)

(445.9)187.8

2006(1)

£m

510.5205.3715.8(31.9)683.9

4.0(75.0)

(180.6)(89.1)(58.6)(84.8)

(413.1)199.8

OTC gross winMachines gross winTotal gross winAdjustments to gross win (2)

Net revenueAssociate incomeGross profits taxStaff costsProperty costs (3)

Content costs (4)

Other costs (inc. depn and FOBT tax) (5)

Operating costsOperating profit

VarianceB(W)%

(3.8)21.0

3.3

2.6

(11.5)(5.4)0.9

(9.2) (7.9) (6.0)

Year to 31 December

(1) Restated revenue, costs and operating profit(2) Fair value adjustments, VAT

(3) Rent, rates and utilities (4) Pictures, data, levy, Sky(5) Depreciation = £40.9m (2006: £34.7m), FOBT tax = £13.8m (2006:£5.6m)

UK Retail – KPIsYear to 31 December

2007

17.1%

(4.1)%

20.3%

2.9%

3%

6.1%

£8.24

8,147

£585

2006

16.9%

1.1%

0.1%

0.8%

4%

2.9%

£8.39

8,189

£481

Variance B(W)%

(1.8)

(0.5)

21.6

OTC margin

Like for like OTC gross win growth

Like for like machines gross win growth

Like for like total gross win growth

Like for like total costs (1) increase

Like for like shop staff costs increase

Stake per slip (2)

Average number of machines

Average weekly gross win per machine

(1) Excludes VAT, Gross profits tax and FOBT tax (2) Slips exclude machines

IrelandYear to 31 December 2007

£m

61.8

(0.4)

61.4

(4.4)

(36.9)

20.1

5.4%

215

2006(1)

£m

48.9

(0.4)

48.5

(5.1)

(29.4)

14.0

10.4%

195

VarianceB(W)%

26.4

(25.5)

43.6

10.3

Gross win

Fair value adjustments

Net revenue

Duty / Gross profits tax

Other costs

Operating profit

Like for like gross win increase

Shop numbers at the end of the period(1) Restated costs and operating profit

eGaming – Net revenueYear to 31 December

Sportsbook

Casino

Poker

Games

Net revenue

2007£m

52.2

43.1

31.0

17.2

143.5

2006(1)

£m

45.5

41.0

35.0

12.6

134.1

VarianceB(W)%

14.7

5.1

(11.4)

36.5

7.0

Gross win

Fair value adjustments (2)

Net revenue

Gross profits tax

Levy and licences

Staff costs

Software & geographical partners (3)

Marketing (inc. affiliates)

Banking and chargebacks

Other costs (inc. depn)

Operating costs

Operating profit

2007£m

156.5

(13.0)

143.5

(7.9)

(2.7)

(17.9)

(18.1)

(20.1)

(5.2)

(16.6)

(80.6)

55.0

%age of net revenue

5.5

1.9

12.5

12.6

14.0

3.6

11.6

56.2

38.3

2006(1)

£m

144.4

(10.3)

134.1

(6.9)

(2.1)

(12.6)

(29.0)

(17.3)

(7.8)

(14.1)

(82.9)

44.3

%age of net revenue

5.2

1.6

9.4

21.6

12.9

5.8

10.5

61.8

33.0

VarianceB(W)%

8.4

7.0

2.8

24.2

Year to 31 December

(1) Restated costs and operating profit(2) Adjustments for free bets, promotions and bonuses

(3) Payments to third party software and platform providers and geographical partners

eGaming – Results

eGaming – KPIsYear to 31 December

2007

601

307

£120

£86

2006

549

303

£91

£56

VarianceB(W)%

9.5

1.3

(31.9)

(53.6)

Unique active players (000s) (1)

Real money sign-ups (000s) (2)

Cost per acquisition (3)

Adjusted cost per acquisition (4)

(1) A player who contributed to rake and/or placed a wager during the period(2) A new player who has registered and deposited funds during the period(3) Total of all online and offline marketing spend (including promotions and bonuses netted from revenue) and all affiliate expenses relating to deals where affiliates are paid a one-off fee for each sign-up and all bonus costs (except those relating to sign-ups from revenue share affiliates) divided by the aggregate real money sign-ups from non-affiliate sources and the number of real money sign-ups through affiliates that are paid a one-off fee.(4) As per cost per acquisition, but excluding any marketing costs attributed to CRM activity.

Telephone Betting – Results

Gross win exc. High Rollers

Fair value adjustments

Net revenue exc. High Rollers

High Rollers’ net revenue

Net revenue

Gross profits tax

Levy

Staff costs

Direct operating costs (2)

Other costs (inc. marketing and depn)

Operating costs

Operating profit

2007£m

30.5

(0.3)

30.2

249.6

279.8

(37.2)

(15.9)

(9.5)

(3.3)

(30.3)

(59.0)

183.6

2006(1)

£m

33.9

(0.3)

33.6

12.2

45.8

(7.3)

(2.6)

(9.0)

(3.3)

(6.3)

(21.2)

17.3

%age of net revenue

excl High Rollers

31.4

10.9

%age of net revenue

excl High Rollers

26.8

9.8

VarianceB(W)%

(10.0)

(10.1)

1,945.9

510.9

(178.3)

961.3(1) Restated costs and operating profit (2) Direct operating costs include telephone, bandwidth and banking costs

Year to 31 December

Telephone Betting - KPIs (excl High Rollers)

Year to 31 December 2007

7,165

61p

7.1%

115.0

193

2006

7,832

59p

7.2%

124.4

209

VarianceB(W)%

(8.5)

(3.4)

(7.6)

(7.7)

No. of calls (000s) (1)

Agent cost per call

Gross win margin

Unique active players (000s) (2)

Average monthly active player days (000s)

(1) Number of calls (excluding customer service calls)(2) A player who has placed a wager during the period

Analysis of 2007 Capex

CapexUK development (1)

FOBTs and EPOSXtraIreland, Belgium and ItalyOther (including IT: £6.7m; 2006 - £8.0m)European RetaileGaming / Telephone BettingInternational development and casinoTotalStatutory and licence acquisitions (2) SponsioOther (Italy: £26.6m, Casino: £10.7m, Ireland: £7.6m, UK: £1.4m)

2007£m

18.815.2

-13.015.262.2

5.83.0

71.0

37.846.3

155.1

2006£m

38.815.7

6.34.5

17.082.3

5.1-

87.4

-32.4

119.8

(1) Development = relocations, extensions and refurbishments, (2) Excludes £3.7 million (2006: £nil) cash obtained through acquisition of subsidiaries

Year to 31 December

Cash generated by operationsInterest and taxPPE capital spend (1)

IntangiblesAcquired subsidiariesTotal capital spend (1)

Cash flow after interest, tax and capitalVernons/Hotels disposal proceedsDividends paidProceeds from issue of shares, convertibles and optionsShare buybacksExchange and other movementsNet borrowings movementOpening net borrowingsClosing net borrowingsNet debt to EBITDA ratio (1)

Net debt to EBITDA ratio (1) adjusted for high rollers

Year to 31 December

Cash Flow2007

£m

(62.4)

(31.8)(60.9)

2007£m

421.1(133.0)

(155.1)133.0

40.8(84.6)

7.6(70.4)

5.531.9

(948.9)(917.0)

1.93.1

2006£m

(84.8)(9.0)

(26.0)

2006£m264.7

(53.5)

(119.8)91.4

3,241.4(4,208.4)

344.5-

(19.9)(551.0)(397.9)(948.9)

3.1 3.2

(1) Continuing operations only

28 February 2008

Christopher BellChief Executive

2007 Overview• Record profits

• Improved performance from UK Retail towards year end

• Double digit profit growth from eGaming

• Strong Telephone High Rollers performance

• Established new business in Italy

UK Retail• Renewed 8,190 strong gaming

machine estate

• New machine content

• Winter evening opening

• Improved betting content

Euro 2008

UK Retail – Product Development• Leading edge technology

• Current testing:

Customer loyalty scheme

Self service terminals

Kiosk based shops

• Enhanced content and product range

• Active shop portfolio management

Kiosk and SST – Ladbrokes Retail Marketing

Ireland• Strong performance in 2007

• Acquisition of 54 shops in Northern Ireland during February

• Market leaders in Northern Ireland and Republic of Ireland

Italy• 26 shops trading

• 10 corners trading

• Focus on opening Bersani licences and ongoing shop acquisitions

• Ladbrokes.it launched Q4 2007

Spain• Sportium brand

• JV with Cirsa Slot

• Madrid operating licence

• 60 sportsbetting outlets expected to start trading in the months following licence award

• Further regional deregulation required

Other International Development• China

– Product development with AGTech

– Great Gate shops

• Vietnam

– Fixed odds football lottery bid

• Turkey

– Sportsbetting licence opportunity

Telephone Betting• Strong performance from High

Rollers

• Core business slightly down

• High quality service to all Telephone customers

eGaming• Continued double digit profit growth

in 2007

• Leveraging the brand

• Driving new customer acquisitions

• Jurisdictional prudence

• Management team strengthened

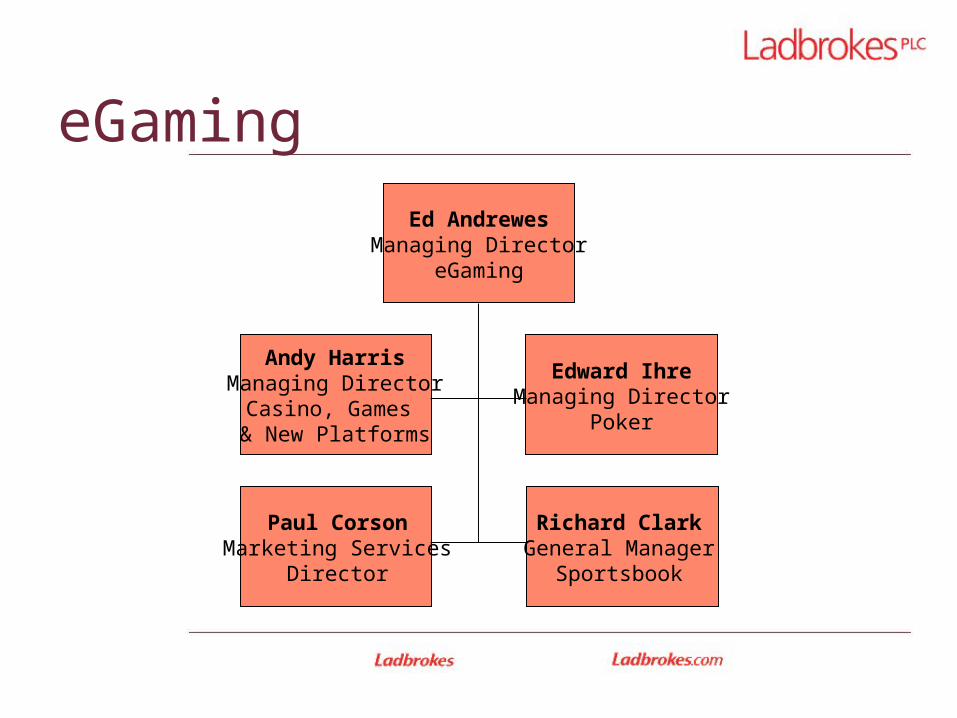

eGaming

Ed AndrewesManaging Director

eGaming

Andy HarrisManaging DirectorCasino, Games & New Platforms

Paul CorsonMarketing Services

Director

Edward IhreManaging Director

Poker

Richard ClarkGeneral Manager

Sportsbook

eGaming – Growth Acceleration• Increased investment in customer

acquisition • Targeted NGR growth through

– More aggressive Poker affiliates programme

– TV advertising for Casino and Bingo– Increased investment in Nordic

region• Flat operating profit in 2008• Profit growth in 2009 and 2010

UK Regulation• No longer pursuing new UK casino

opportunity

• Paddington Casino to be sold

• 2005 Gambling Act from 1 September 2007

Winter evening opening met expectations

TV advertising well received

• 47th levy scheme determination

Summary• Ongoing revenue and cost

opportunities in UK Retail

• Consolidation in Irish Retail

• Focused investments in eGaming

• High Rollers in Telephone Betting

• International progress, with focus on Italy and Spain

Outlook

Q&A

Appendix

eGaming – KPIsSportsbook Gross win margin 7.2% 6.4% Unique active players (000s) 421 398 5.8 Average monthly active player days (000s) 648 610 6.2 Yield per unique active player (£) (1) 124 114 8.8Casino Unique active players (000s) 105 90 16.7 Average monthly active player days (000s) 82 72 13.9 Yield per unique active player (£) (1) 411 455 (9.7)Poker Unique active players (000s) 151 154 (1.9) Average monthly active player days (000s) 409 461 (11.3) Yield per unique active player (£) (1) 205 227 (9.7)Games Unique active players (000s) 148 126 17.5 Average monthly active player days (000s) 142 99 43.4 Yield per unique active player (£) (1) 116 100 16.0

2007 2006 Variance% B(W)

(1) Revenue per unique active player for the period

Year to 31 December

European Retail

2007£m

739.3

61.8

34.8

6.5

842.4

2006£m

715.8

48.9

35.1

-

799.8

3.3

26.4

(0.9)

-

5.3

2007£m

187.8

20.1

3.2

(1.6)

209.5

2006(1)

£m

199.8

14.0

3.0

-

216.8

Operating ProfitGross Win

UK Retail

Ireland

Belgium

Italy

Total

(1) Restated divisions operating profit. Total operating profit remains unchanged

Variance B(W)%

Variance B(W)%

(6.0)

43.6

6.7

(3.4)

Year to 31 December

UK Retail

Ireland & Belgium

eGaming

Telephone Betting

Other (3)

Corporate Costs

Total

Reported£m

195.4

17.3

47.0

17.7

5.9

(15.2)

268.1

Adj (1)

£m

-

-

-

-

(5.9)

-

(5.9)

Adj (2)

£m

4.4

(0.3)

(2.7)

(0.4)

(1.6)

0.6

-

Restated operating profit

(1) Continuing operating profit restated for treatment of Vernons as discontinued(2) Restated divisions operating profit. Total operating profit remains unchanged(3) Other restated is casino and international development

Restated£m

199.8

17.0

44.3

17.3

(1.6)

(14.6)

262.2

Year to 31 December 2006