Embed Size (px)

Citation preview

29 September 2013Jesse Redding | Cameron Kirby | Sam

Johnson

Thesis

Large growth opportunity in

ecigs

Solid core business with room for

expansion

Fundamental Undervaluation

Undervalued share price

Valuation

Revenue = $530mmP/S = 3

Equity Value = $1.59 bn

EBIT = $2.033bnEV/EBIT = 12EV = $24.4 bn

Equity Value = $1.59 bn + $24.4 bn - $3.1bn= $23 bn (35% upside)

E-Cigarettes Traditional

Opportunity in E-Cigs

Value Proposition• eCigarettes offer to the consumer:– Freedom to smoke whenever and

wherever one chooses to–No smell– Decreased social stigma– Significantly reduced health risks

Addressable Market• Almost 100% of ecig customers were

or are smokers.• Total cigarette industry: ~$80b

retail revenue, ~$30b manufacturer revenue

• Total Volume of 290b cigarettes/year• 2012 ecig industry: ~$1b retail

revenue

How we Quantified Market Growth

2012 Cigarettes sold: 290b

4% Annual Volume Decrease

~8.5b fewer cigarettes sold in 2013

~8.5b fewer cigarettes sold in 2013

30% of volume moves to ecigs

ecig market grows by ~2.55b cigarette equivalents

Competitors• eCigarette industry is

large and highly fragmented

• Currently, Blu commands ~40% market share followed by NJOY which has ~30% market share

• Quickly changing industry with recent entry of Reynolds and Altria

E-Cig Economics

Razor/BladE ModelRazor Blade

$35

Margins

Low Margins on Starter Packs

High Margins on Cartridges

Margin Expansion as product matures

Distribution Channels

Lorillard

Retailers

Customers

E-Cig Regulation

Regulation• Currently, eCigarette regulation is state by

state with the only restrictions being on sales to minors

• FDA has them listed as tobacco products, and they are thus subject to fewer regulations

• Since eCigarettes are under laxer FDA regulations, they can be advertised on television and radio

• Due to the appeal of flavors to children, many have called for the ban of the different flavors of eCigarette cartridge

Valuation

Valuation of Blu

(Revenue) $530 mm * (P/S) 3

Equity Value = $1.59 bn

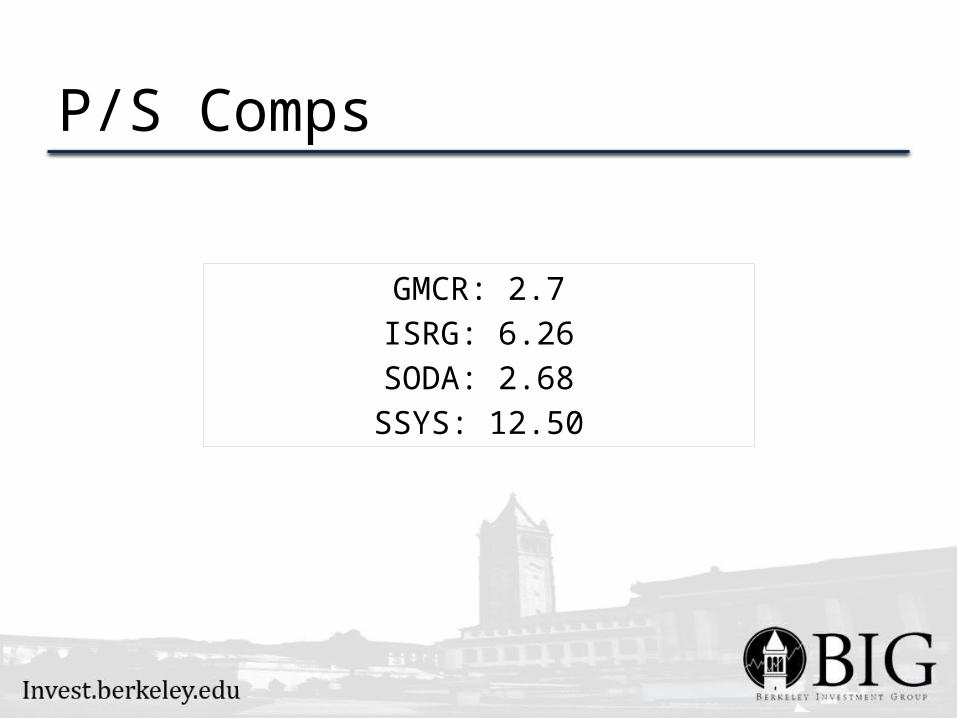

P/S Comps

GMCR: 2.7ISRG: 6.26SODA: 2.68SSYS: 12.50

Legacy Business

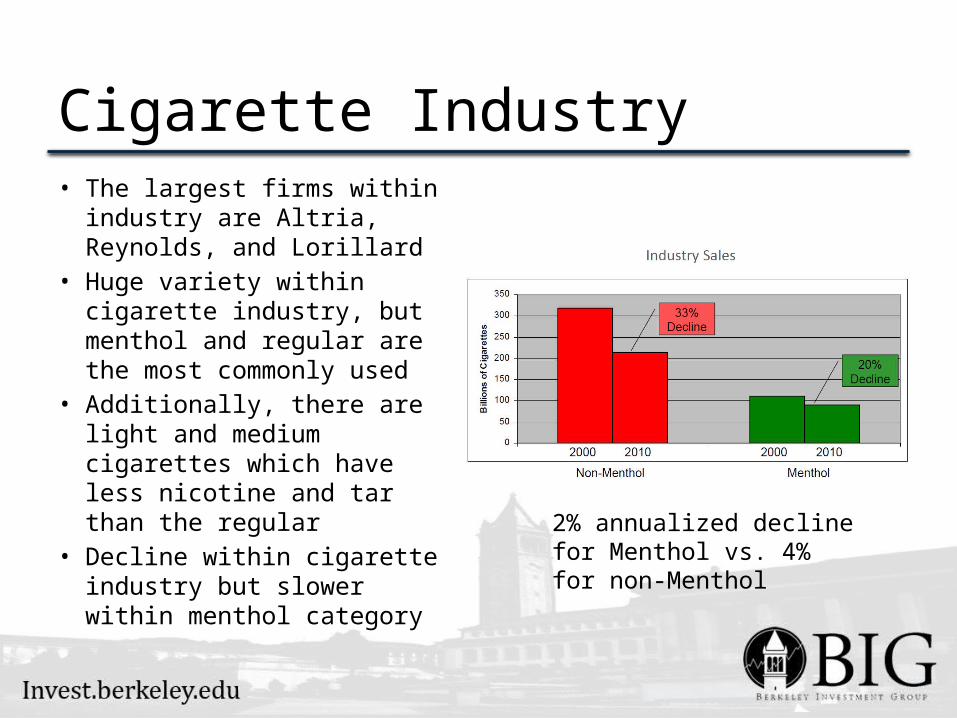

Cigarette Industry• The largest firms within

industry are Altria, Reynolds, and Lorillard

• Huge variety within cigarette industry, but menthol and regular are the most commonly used

• Additionally, there are light and medium cigarettes which have less nicotine and tar than the regular

• Decline within cigarette industry but slower within menthol category

2% annualized decline for Menthol vs. 4% for non-Menthol

Lorillard is Menthol

• Newports are the menthol brand

• Sustained dominance without discounting

Menthol is Resistant• Menthol caters to a

lower socio-economic demographic

• More deeply embedded smoking habits

• Little crossover between flavors

• Minimal cannibalization from shift to ecigs

Expansion into Non-Menthol• No existing presence means easy market share

gains• Small upfront costs mitigate risk• Much larger non-menthol market means small

gains are profitable

Regulation• Menthol-specific regulation has been

tossed around for a long time• Current efforts remain stalled• Science does not appear to support

difference in damage between menthol and non-menthol

• clearing of overhang would help stock

Segment Projections

Proven ability to increase prices

Flat volume due to new markets

~1-2% annual revenue growth

Segment Valuation• Currently Trades at 10.6 EV/EBITDA• MO10.4 EV/EBITDA, RAI 11.9• We believe a fair valuation is 12x

Valuation

Variant Perception• Market sees E-Cigs as too small• This segment should be valued at a

premium to the rest of the business

Traditional Metrics• Other tobacco companies are

trading at:– P/E (industry average): 14– P/CF (industry average): 16

• On these metrics, LO should trade for:– $54 based on P/E (20% upside)– $58 based on P/CF (28% upside)

Optionalities• Lorillard can expand into:–Non-Menthol Non-Full Flavor–Non-Menthol Full Flavor

Valuation

Revenue = $530mmP/S = 3

Equity Value = $1.59 bn

EBIT = $2.033bnEV/EBIT = 12EV = $24.4 bn

Equity Value = $1.59 bn + $24.4 bn - $3.1bn= $23 bn (35% upside)

E-Cigarettes Traditional

Recommendation• BIG should take a 5% position on

Wednesday morning