Embed Size (px)

DESCRIPTION

2nd IG Meeting – Region South-South East 5th July 2007, Krakow, Poland. Agenda. Implementation Task Forces. Gas Regional Initiative South-South East Contribution by TSOs. Milano Tasks. 5 July 2007, Krakow, Poland. Contribution by TSOs. Participating TSOs. Geoplin Plinovodi - PowerPoint PPT Presentation

Citation preview

2nd IG Meeting – Region South-South East5th July 2007, Krakow, Poland

2

Agenda

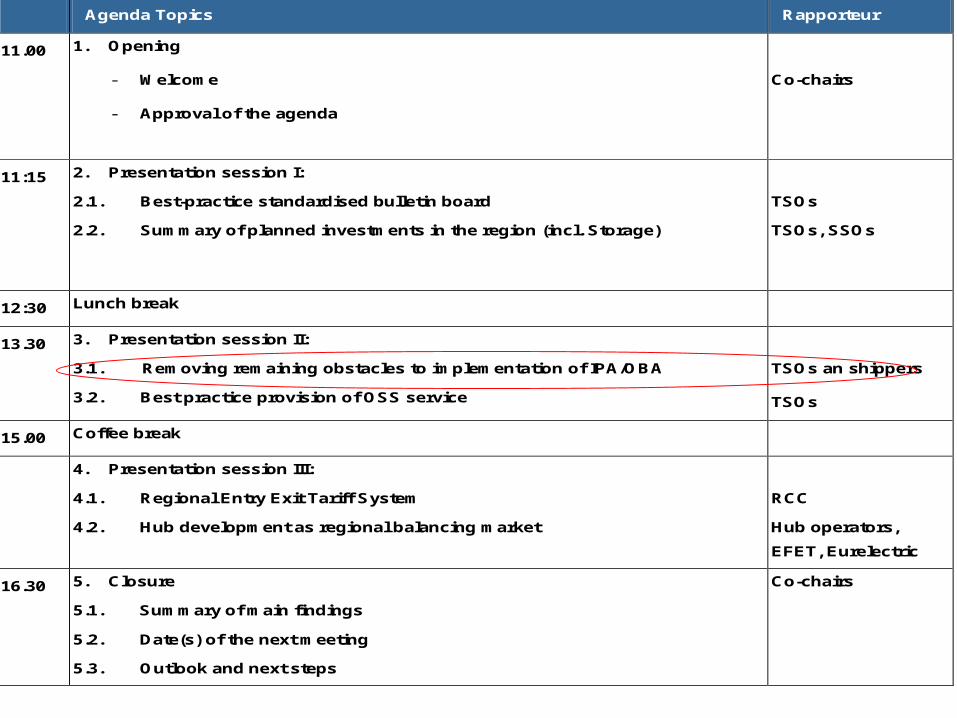

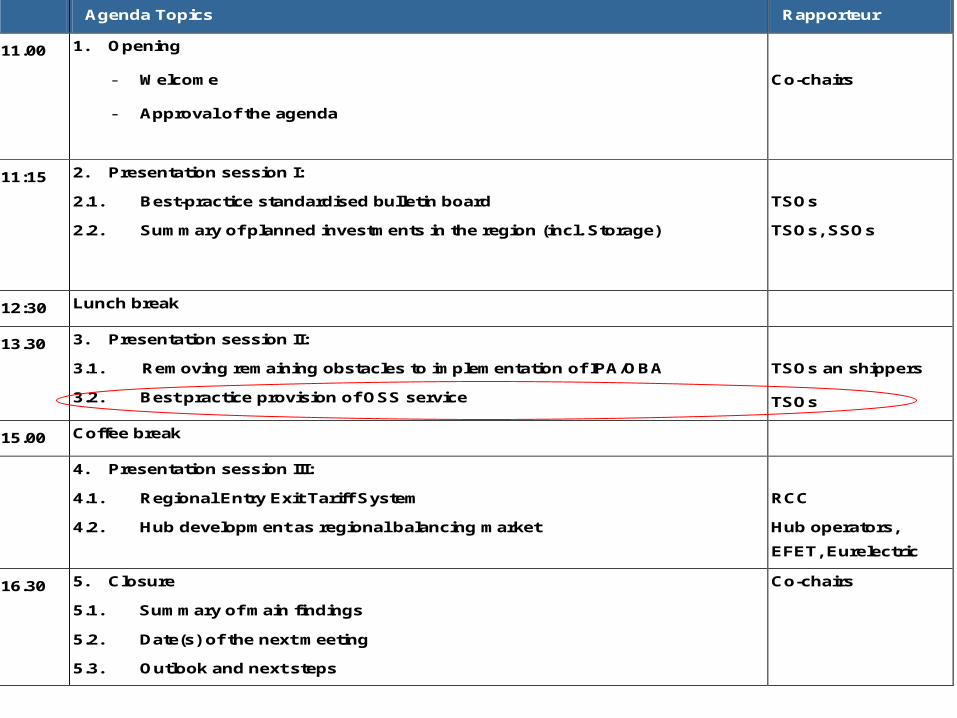

Agenda Topics Rapporteur

11.00 1. Opening

- Welcome

- Approval of the agenda

Co-chairs

11:15 2. Presentation session I:

2.1. Best-practice standardised bulletin board

2.2. Summary of planned investments in the region (incl. Storage)

TSOs

TSOs, SSOs

12:30 Lunch break

13.30 3. Presentation session II:

3.1. Removing remaining obstacles to implementation of IPA/OBA

3.2. Best practice provision of OSS service

TSOs an shippers

TSOs

15.00 Coffee break

4. Presentation session III:

4.1. Regional Entry Exit Tariff System

4.2. Hub development as regional balancing market

RCC

Hub operators,

EFET, Eurelectric

16.30 5. Closure

5.1. Summary of main findings

5.2. Date(s) of the next meeting

5.3. Outlook and next steps

Co-chairs

3

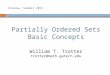

Implementation Task Forces

Implementation TF Responsible Result until

Best-practice standardised bulletin board - RCC: TOR- TSOs- Next steps

End June/ beginning of July

Summary of planned investments in the region (incl. Storage)

- RCC: TOR- ECG: Survey results- TSOs & SSOs- Next steps

End June/ beginning of July

Removing remaining obstacles to implementation of IPA/OBA

- RCC: TOR- TSOs - Next steps

End June/ beginning of July

Best practice provision of OSS service- RCC : TOR- TSOs- Next steps

End June/ beginning of July

REETS- RCC : TOR- AEEG- Next steps

End June/ beginning of July

Hub development as regional balancing market

- RCC TOR- CEGH, PSV - EFET, Eurelectric- Next steps

End June/ beginning of July

Gas Regional Initiative

South-South EastContribution by TSOs

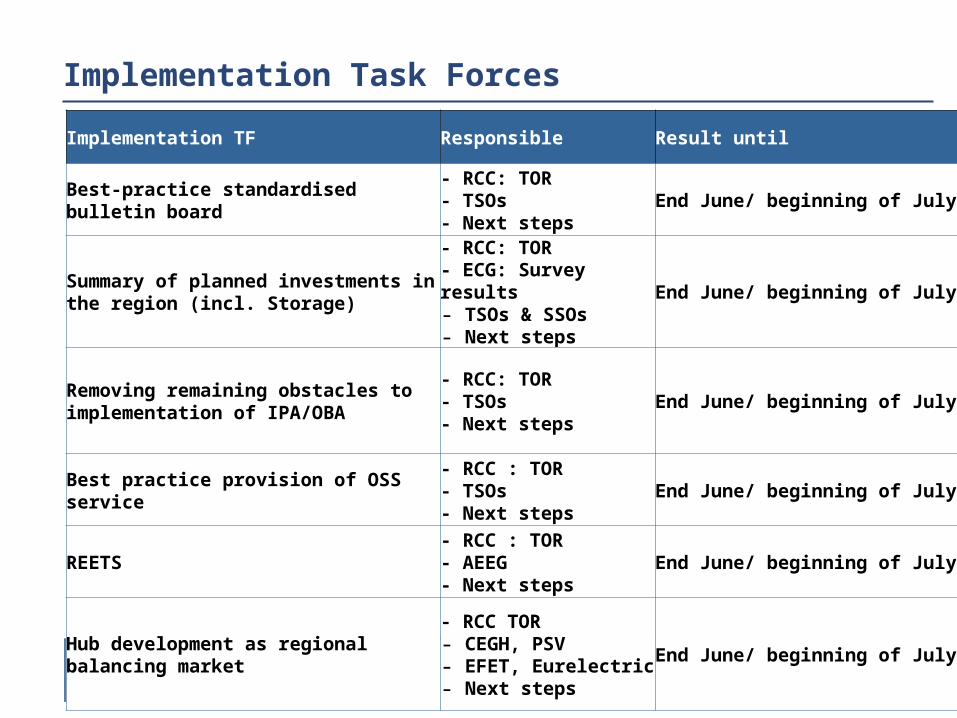

Milano Tasks

5 July 2007, Krakow, Poland

Contribution by TSOs

Participating TSOs

Geoplin Plinovodi OMV Gas GmbH RWE Transgas Net Snam Rete Gas SPP-preprava Trans Austria Gasleitung GmbH

Best practice: Standardised bulletin board

Summary of planned investments in the region (excl. storage)

Planned investments regarding storage should be presented by SSOs as TSOs may not be aware of them

Removing remaining obstacles to implementation of IPA/OBA

Best practice: Provision of one-stop-shop (OSS) service

Milano Tasks - Contribution by TSOs

TSOs discussed all topics identified as areas for further work

TSOs Met on 18 May in Prague

TSOs’ understanding of the Milano tasks was very different from the contents given in the

Terms of Reference sent on 23 May by Mr. Rieser /on 24 May by REM SSE Co-Chairs

The given Terms of Reference seem to go well beyond what was said in Milano

9

Agenda

Agenda Topics Rapporteur

11.00 1. Opening

- Welcome

- Approval of the agenda

Co-chairs

11:15 2. Presentation session I:

2.1. Best-practice standardised bulletin board

2.2. Summary of planned investments in the region (incl. Storage)

TSOs

TSOs, SSOs

12:30 Lunch break

13.30 3. Presentation session II:

3.1. Removing remaining obstacles to implementation of IPA/OBA

3.2. Best practice provision of OSS service

TSOs an shippers

TSOs

15.00 Coffee break

4. Presentation session III:

4.1. Regional Entry Exit Tariff System

4.2. Hub development as regional balancing market

RCC

Hub operators,

EFET, Eurelectric

16.30 5. Closure

5.1. Summary of main findings

5.2. Date(s) of the next meeting

5.3. Outlook and next steps

Co-chairs

10

Best-practice standardised bulletin board

Why necessary Regulation 1775/2005/EC Art. 8:

“Each transmission system operator shall take reasonable stepsto allow capacity rights to be freely tradable and to facilitatesuch trade.”

Quote from Explanatory Notes (Reg. 1775/2005/EC)“TSOs should be obliged to publish the offer of secondary capacity when requested by the seller. The TSOs should be urged to organise a bulletin board where this is not organised in another market place.“

RCC’s background paper:TSOs should cooperate in setting up a central bulletin board as a trading platform for secondary market capacities for transmission pipelines in the region SEE

11

Best-practice standardised bulletin board

What is expected: Implementation of an online, user-friendly, and secure trading

platform.

Step 1: a best practice online-based trading platform for secondary market capacities in the SSE regional energy market shall be identified

Step 2: implementation of an online platform using a harmonised standard for transmission capacity on all major transit systems of the region SEE

12

Example to be used for all Austrian transit capacities

TSOs’ understanding: creation of a harmonised user-friendly bulletin board by EACH TSO (no joint platform)

Bulletin Board is no true trading platform only an information board made available by the TSOs to make it easier for interested parties to find each other; the TSOs are not involved in the transaction until the parties that have traded/want to trade capacity send them notice thereof

Harmonised Bulletin Board (1)

Approach taken: operational rules for running the bulletin boards were checked and pros and cons of their functioning were discussed

TSOs agreed to use standard contents for presenting the information on the capacity bid/offer received in whatever form from the shippers

The contents (format) used by TAG has been chosen as the best practice

Harmonised Bulletin Board (2)

The TSOs would like to note that shippers have made very little use of the bulletin boards so far

TAG Bulletin Board

Harmonised Bulletin Board (3)

*

* Optional information may be in the form of an attachment or as directly published text

16

Action POINT 1 - Best-practice standardised bulletin board

Suggested next steps

Coordinator: TSOs Next steps:

TSOs agreed to use standard contents for presenting the information on the capacity bid/offer received in whatever form from the shippers

The contents (format) used by TAG has been chosen as the best practice

Timing: Implementation of the standard content till September

17

Agenda

Agenda Topics Rapporteur

11.00 1. Opening

- Welcome

- Approval of the agenda

Co-chairs

11:15 2. Presentation session I:

2.1. Best-practice standardised bulletin board

2.2. Summary of planned investments in the region (incl. Storage)

TSOs

TSOs, SSOs

12:30 Lunch break

13.30 3. Presentation session II:

3.1. Removing remaining obstacles to implementation of IPA/OBA

3.2. Best practice provision of OSS service

TSOs an shippers

TSOs

15.00 Coffee break

4. Presentation session III:

4.1. Regional Entry Exit Tariff System

4.2. Hub development as regional balancing market

RCC

Hub operators,

EFET, Eurelectric

16.30 5. Closure

5.1. Summary of main findings

5.2. Date(s) of the next meeting

5.3. Outlook and next steps

Co-chairs

18

Route Assessment in SSE

1

2

4

3

Gas Regional Initiative – Region: South-South East, Assessment on selected Transportation Routes

19

Available firm capacitySPP

Preprava

SK

RTN

CZ

BOG

A

TAG

A

OMV

A

Geoplinplinovodi

SI

SRG

I

GAZ System

PL

route 1UK-SK-CZ-GER

yes yes

route 2UK-SK-A-SI-I

no no yes no

route 3UK-SK-A-I

no no

route 4UK-SK-A-GER

no no

route 5BE-PL-GER

no

route 6AL-I-A-SK

no yes

20

Short term congestion managementSPP

Preprava

SK

RTN

CZ

BOG

A

TAG

A

OMV

A

Geoplinplinovodi

SI

SRG

I

GAZ System

PL

route 1UK-SK-CZ-GER

noneinterr. UIOLI,

bulletin board

route 2UK-SK-A-SI-I

noneinterr. UIOLI,

bulletin board

interr. UIOLI, bulletin board

none

route 3UK-SK-A-I

noneinterr. UIOLI,

bulletin board

route 4UK-SK-A-GER

noneinterr. UIOLI,

bulletin board

route 5BE-PL-GER

interr. UIOLI

route 6AL-I-A-SK

interr. UIOLI, bulletin board

bulletin board

21

Capacity expansionSPP

Preprava

SK

RTN

CZ

BOG

A

TAG

A

OMV

A

Geoplinplinovodi

SI

SRG

I

GAZ System

PL

route 1UK-SK-CZ-GER

no plans no plans

route 2UK-SK-A-SI-I

no plansplanned -

not enough

no plans planned

route 3UK-SK-A-I

no plansplanned -

not enough

route 4UK-SK-A-GER

no plansopen

season

route 5BE-PL-GER

no plans

route 6AL-I-A-SK

backhaul planned

22

Congestion Management – Obligation of TSOs

Why necessary Regulation 1775/2005/EC Art. 5:

“In the event that physical congestion exists, non discriminatory, transparent capacity allocation mechanisms shall be applied by the transmission system operator or, as appropriate, the regulatory authorities.“

Quote from Explanatory Notes (Reg. 1775/2005/EC)In the case of new investments in transportation capacity (which includes significant expansion of existing capacity), the TSOs' responsibility to ensure the long term ability of the system by meeting reasonable demands would make it appropriate to organise an open season or open subscription period before allocating capacity, in order to determine more precisely the required capacity expansion.

RCC’s route assessment:Congestion management measures are missing

23

Summary of planned investments in gas infrastructure

What is expected: Deliverable 1: Survey of the future gas demand and capacity

need by country (10 years ahead) Deliverable 2: Survey of planned and actual investments in

transmission pipelines and storage facilities, by country and TSO/SSO

Deliverable 3: Analysis of concrete obstacles to investment, be it regulatory, legal, political or other reasons

24

Summary of planned expansions in SEE (incl. Storage)

Presentation/report Report by RCC Early findings from questionnaire Review by country

Austria Bulgaria Czech Republic Greece Hungary Italy Poland Romania Slovakia Slovenia

In the light of the obligation imposed by Regulation (EC) 1775/2003 to publish regular long-term forecasts of available capacities for up to 10 years for all relevant points, in case the TSOs have the obligation under the national law to publish an investment forecast, they mostly interpret planned investments as investments that will be realised (i.e. no investment plans in pre-feasibility and feasibility stage)

Summary of Investment Forecasts

The TSOs would like to underline that it is not the investments as such but the associated increase

in transmission capacity that is of interest to shippers

SPP - preprava

Decisions on investments currently under preparation according to the demand of the network users.

Developments Length [km] Notes

Olbernhau-Waidhaus (link to the Nordstream/OPAL)

3 alternatives Market Survey OngoingThe new capacity should come on stream gradually between 2011-2015

RWE Transgas Net (1)

RWE Transgas Net (2)

Investments Volume Increase

Planned entry into operation

Notes

Compressor Station Eggendorf (Region Lower Austria)

3.2 bcm/y 1 October 2008 Capacity allocated through long-term allocation procedure on a pro-rata basis

Compressor Station Weitendorf (Region Styria)

3.3 bcm/y Capacity to be allocated in the near future

Total capacity to be made available through the new investments amounts to 6.5 bcm/y.

Further information will be published on TAG’s web site in due time.

Trans Austria Gas Leitung (1)

Trans Austria Gas Leitung (2)

Planned investments into the transit system

Volume Increase

Planned entry into operation

Notes

Compressor Station at Oberkappel (Penta West) including extension of PW transfer metering station at Überackern

1.75 bcm/y 1 November 2011 Under construction, capacity nearly sold

Planned investments into the Austrian domestic system should be looked up under the Long-term Planning Process of AGGM (www.aggm.at)

OMV Gas (1)

OMV Gas (2)

Developments Length [km]

Diameter [mm] Pressure [bar] Notes

M2/1 Rogatec – Rogaška Slatina

8.1 800 70 Under construction

R25D Šentrupert – Šoštanj

17 400 70 Under construction

M1/1 Kidričevo – Rogatec M1/1 Ceršak – Kidričevo M2/1 Rog. Slatina – Trojane M2/1 Trojane – Vodice M3/1 Vodice – Šempeter M3B/1 Šempeter – Miren M5 Vodice – Jarše

M5 Jarše – Novo mesto M6 Ajdovščina – Lucija M8/1 Jelšane – Kalce M8/2 Brod na Kolpi – Ljubljana (alternative) M8/3 Vinica – Ljubljana (alternative) R25A Trojane – Hrastnik R45 N. mesto – B. krajina R38 Kalce – Godovič

Planned developments -- different stages:

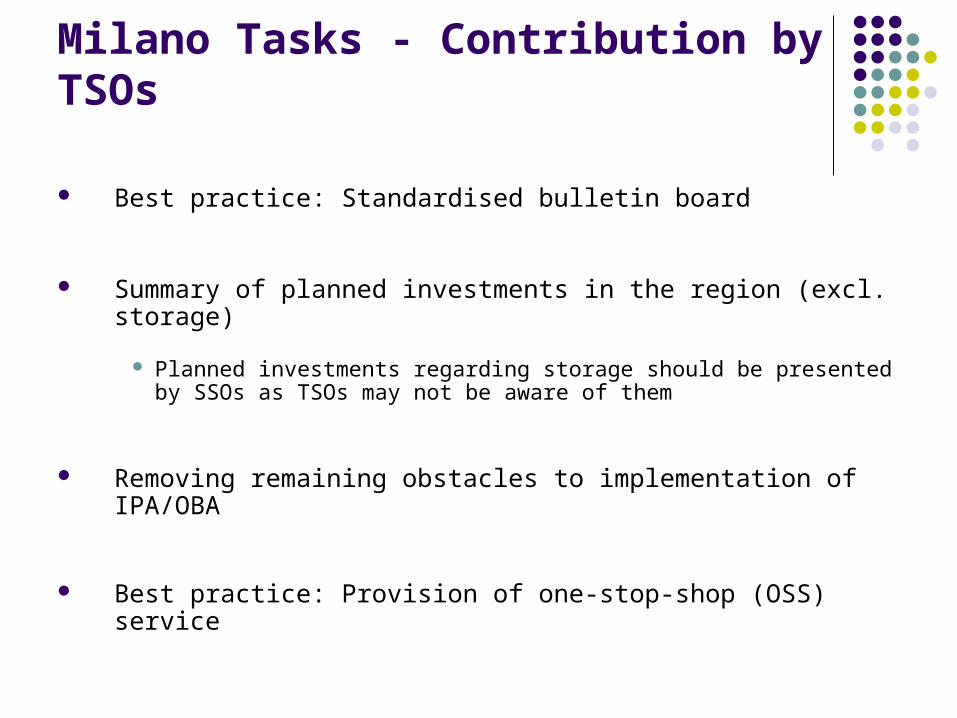

Geoplin Plinovodi (1)

Geoplin Plinovodi (2)

Developments Length [km]

Diameter [mm] Compressor Station [MW]

Notes

Reinforcement of infrastructure in Sicily

160 1200 25 Under construction

Reinforcement of infrastructure in North-West of Italy

45 750 - Under construction

Reinforcement of infrastructure in North-East of Italy

- - 100 Planned

Reinforcement of infrastructure in South Italy 1300 800/1200 88 PlannedAdriatica

Tirrenica

Development of Entry point of Panigaglia

150 900 - Planned

Information on respective increases in transmission capacity is available on Snam Rete Gas’ web site

Snam Rete Gas (1)

Entry PointNorth-Est Italy

Entry PointPanigaglia

Entry PointPasso Gries

Entry PointSouth Italy

Entry PointMazara del Vallo

Snam Rete Gas (2)

37

Presentation of the GSE website with all actual expansion projects in storage

38

39

Details for Austria and Poland

40

Gas Demand forecast in Austria

41

Congestion in the Domestic Transmission system

42

Plant power stations (4.000 MW till 2015?)

KW

KW

KW

KW

KW

KW

KW

Geplant bis 2010

Geplant bis 2015

Geplant bis 2020

KW

KW

angedacht

Zeltweg

Mellach

KW

Peisching

KW

KW

KW

KW

Riedersbach

Timelkam

KW

Ennshofen

Theiß II

Dürnrohr

400

400

400

4001000

650150

800

800

400

800

43

Feasibility Study to increase domestic capacity

44

WAG

TAGI + II

SOL

PENTAWest

HAG

BaumgartenOberkappel

Arnoldstein

Murfeld

Burghausen

SLO HR

H

CZ

SKD

I

Capacity expansions in gas transit

Existing pipelines

planned expansions

TGL(2010)

Nabucco(2012)17-20 bcm/y

new compressor stations

Weitendorf(2008)3.2 bcm/y

Eggendorff(2008)3.3 bcm/y

Rainbach(2011)1.4 bcm/y

45

Storage projects in Austria

Haag

Storage site Puchkirchenwgv 850 mcmWithdrawal rate 400.000 cm/h

Storage site Thannwgv 250 mcmWithdrawal rate 130.000 cm/h

Storage site Schönkirchenwgv 1.570 bcmWithdrawal rate 770.000 cm/h

Storage site Tallesbrunn wgv 300 mcmWithdrawal rate 160.000 cm/h

Tallesbrunn

Expansion project „Schönkirchen Tief“Wgv minimum 1 bcm,High withdrawal rateCompletion expected 2011

Expansion project „Puchkirchen/Haag“wgv 400 mcmWithdrawal rate 160.000 cm/hCompleted 2010

Expansion project „Haidach“First expension phase wgv 1.2 bcm

Completion wgv 2.4 bcmCommissioning 2007

RAG

OMV Gas

OMV Gas

Storage site Haidach 5WGV 13.5 mcm

Withdrawal rate 20.000 cm/h

Existing storage facilities

Storage projects

RAG

Piotr SekleckiPiotr SekleckiChief Expert Chief Expert Department of European Integration and Department of European Integration and Comparative StudiesComparative StudiesEnergy Regulatory OfficeEnergy Regulatory Office

e–mail: [email protected]. (+48 22) 6616 318, fax (+48 22) 6616

321

Address:: Chłodna 64, 00–872 Warsaw

InvestmentInvestmentss and Planning and Planning

2nd Implementation Group Meeting of the Gas Regional 2nd Implementation Group Meeting of the Gas Regional Initiative for the South-South East RegionInitiative for the South-South East Region

The structure of gas supplies in 2006 The structure of gas supplies in 2006 (in mcm)(in mcm)

20-242 -474 74

4318 4277

63

40

68

40

33

50

31

89

2005 2006 2005 2006 2005 2006 2005 2006

mln

m3

The Yamal contract

Other import

domestic production

import PGNiG SA. change in stock other domestic suppliers

The structure of gas supplies in near The structure of gas supplies in near future future

POGC is now importing gas within the POGC is now importing gas within the frames:frames:• a long – term contract for the supplies of a long – term contract for the supplies of the Russian gas of 25th September 1996, the Russian gas of 25th September 1996, with Gazexport, valid until 2022,with Gazexport, valid until 2022,• the contract between PGNiG and VNG the contract between PGNiG and VNG AG on 17 August 2006 and valid until AG on 17 August 2006 and valid until 2016 (for annual gas supply volume 2016 (for annual gas supply volume ranging from 400 to 500 million m³) and ranging from 400 to 500 million m³) and • the contract of 17 November 2006 the contract of 17 November 2006 concluded with RosUkrEnergo AG until concluded with RosUkrEnergo AG until 2009 (for purchase of 2.5 billion m³ of gas 2009 (for purchase of 2.5 billion m³ of gas per annum) with an extension option for per annum) with an extension option for further 2 years.)further 2 years.)

LNG Terminal in Świnoujście LNG Terminal in Świnoujście

The first deliveries of LNG to the terminal The first deliveries of LNG to the terminal are planned for the year 2011. The are planned for the year 2011. The regasification capacity of the terminal will regasification capacity of the terminal will be developed by stages to reach the be developed by stages to reach the target capability of receiving up to 7.5 target capability of receiving up to 7.5 bcm of natural gas per year from the bcm of natural gas per year from the terminal by the year 2020. PGNiG set up a terminal by the year 2020. PGNiG set up a company - Polskie LNG (PLNG)- to build company - Polskie LNG (PLNG)- to build the terminal and, subsequently, to the terminal and, subsequently, to provide the regasification service. The provide the regasification service. The company is based in Świnoujście and company is based in Świnoujście and controlled by PGNiG.controlled by PGNiG.

The domestic production (1996 – The domestic production (1996 – 2006)2006)

3,7 3,73,6

3,8

4 44,1

4,3 4,3 4,3

3,6

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

bcm

Expansion of storage capExpansion of storage capaacitycity

InvestmentInvestmentss planned by the TSO planned by the TSO

53

Action POINT 2 – Overview capacity expansions in SEE

Suggested next steps Coordinator: RCC/E-Control Next steps:

inclusion of received information (TSOs and GSE) on expansion projects (Transmission&Storage) into the survey

Timing: present the results at the next IG meeting

54

Agenda

Agenda Topics Rapporteur

11.00 1. Opening

- Welcome

- Approval of the agenda

Co-chairs

11:15 2. Presentation session I:

2.1. Best-practice standardised bulletin board

2.2. Summary of planned investments in the region (incl. Storage)

TSOs

TSOs, SSOs

12:30 Lunch break

13.30 3. Presentation session II:

3.1. Removing remaining obstacles to implementation of IPA/OBA

3.2. Best practice provision of OSS service

TSOs an shippers

TSOs

15.00 Coffee break

4. Presentation session III:

4.1. Regional Entry Exit Tariff System

4.2. Hub development as regional balancing market

RCC

Hub operators,

EFET, Eurelectric

16.30 5. Closure

5.1. Summary of main findings

5.2. Date(s) of the next meeting

5.3. Outlook and next steps

Co-chairs

55

Further improvment since March 07 ?SPP

Preprava

SK

RTN

CZ

BOG

A

TAG

A

OMV

A

Geoplinplinovodi

SI

SRG

I

GAZ System

PL

route 1UK-SK-CZ-GER

under negotiation

under negotiation

route 2UK-SK-A-SI-I

in testing phase

in testing phase

in testing phase

in testing phase

route 3UK-SK-A-I

in testing phase

in testing phase

route 4UK-SK-A-GER

in testing phase

in testing phase

route 5BE-PL-GER

no

route 6AL-I-A-SK

under negotiation

under negotiation

56

Removing remaining obstacles to implementation of IPA/OBA

Region Number of IPs(GTE map)

number of OBAs at IPs

in %

NNW 55 33 60%

S 17 12 70%

SSE 29 8 28%

57

Removing remaining obstacles to implementation of IPA/OBA

Interconnection point (GTE map)

affected TSOs reported status actual implementation?

Lanzot (54) RTNSPP

under negotiation

Hora Svate Kateriny (22b) RTNWINGAS

in place OK

Waidhaus(24) RTNEON GT, GDF DT

under negotiation

Oberkappel (25) BOGEON GT, GDF DT

under negotiation

Velke Kapusany (55) NAFTOGAZSPP

in place OK

Tarvisio (49) TAGSRG

in place OK

Murfeld (51) OMVGEOPLIN

under negotiation mid 2007?

Gorizia (48) GEOPLINSRG

under negotiation mid 2007?

Baumgarten (55) SPPOMV, TAG, BOG

under negotiation mid 2007?

TAGc

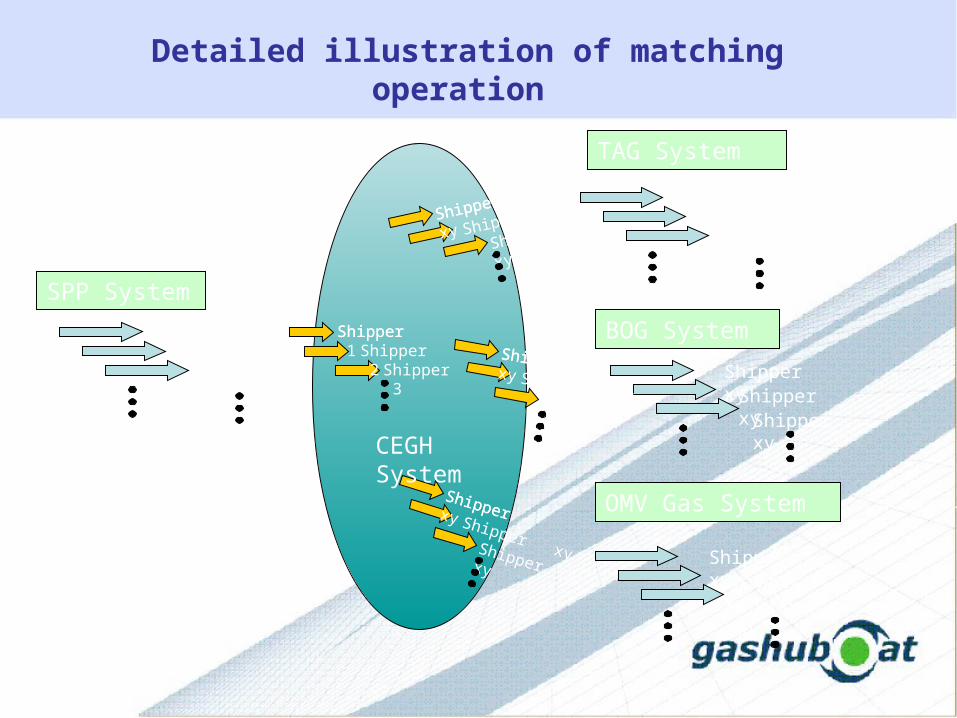

HUB central matching station in between Transportation Systems one step towards harmonization

c c

c

c

c

WAG

Regulatory Zone Austria

HAGMABStorage

SPP

Baumgarten March 2007

Graphical illustration of hub trade in Baumgarten

SPP System

BOG System

OMV Gas System

TAG System

SPP System

SPP System

Technical ICP Agreements

Bilaterally conclusion

Business ICP

Common agreementSPP System

CEGH System

BOG System TAG System

OMV Gas System

OBA: Contractual structure

Integration of CEGH in OBA

Carrier SPP

Carrier OMV

Carrier TAG

Carrier BOG

Operator

SPP

Operator

OMV

OBA CEGH

Shipper

upstream

Shipper

downstream

Trader

Operator

OMV

CEGH

SPP System

BOG System OMV Gas System

TAG System

TradingShipper CEGH

Shipper CEGH

Shipper CEGH

Shipper OMV GASShipper WAG

Shipper TAG

TradingShipper CEGH

Systems of Austrian Side

Systems of Slovakian Side

Shipper SPP

SPP System

BOG System

OMV Gas System

TAG System

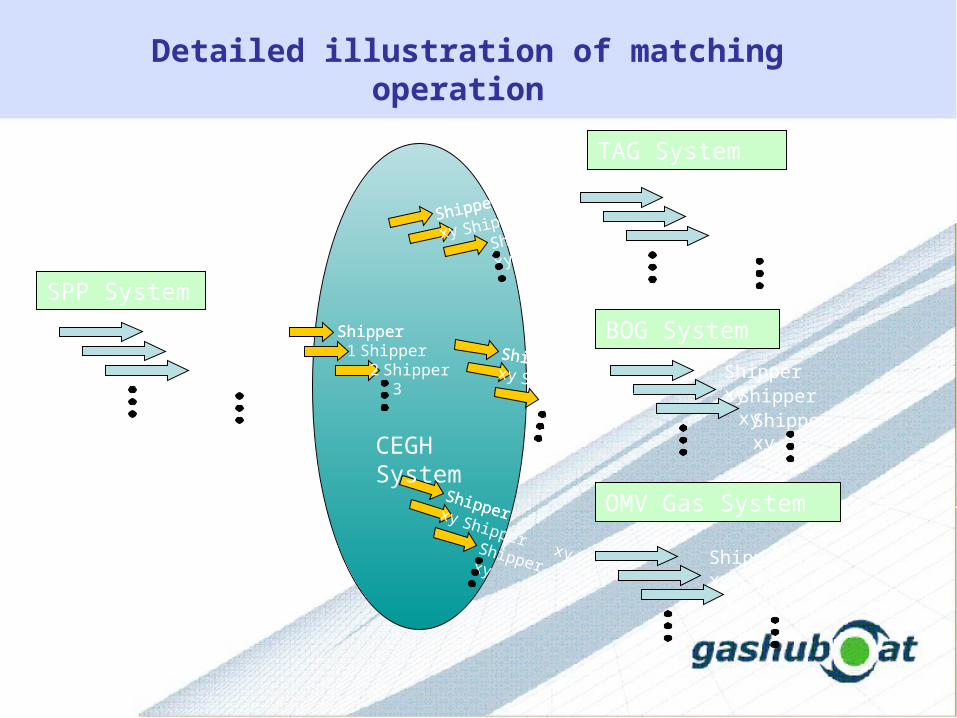

Shipper 1Shipper 2

Shipper 3

Shipper xyShipper xy

Shipper xy

Shipper xyShipper xy

Shipper xy

Shipper xyShipper xy

Shipper xy

ShipperShipper 1Shipper 2

Shipper 3

ShipperShipper xy

Shipper xy

Shipper xy

ShipperShipper xyShipper xyShipper xy

ShipperShipper xyShipper xy

Shipper xy

CEGH System

Detailed illustration of matching operation

64

Action Point 3: Removing remaining obstacles to implementation of IPA/OBA

Suggested next steps Affected TSOs: Next steps:

further update on implementation: TSOs will focus on concluding IPAs where these are not yet in place; Implementation of an OBA regime is dependent on certain prerequisites and will always be conditional; Shippers must be equally involved in the implementation process by complying with the nomination rules set up by the TSOs

Baumgarten: all involved stakeholders work on a solution within the next 3 months incl. a list of remaining obstacles

Timing: CEGH will coordinate a solution for Baumgarten within the next

3 months and present the results at the next IG meeting

65

Agenda

Agenda Topics Rapporteur

11.00 1. Opening

- Welcome

- Approval of the agenda

Co-chairs

11:15 2. Presentation session I:

2.1. Best-practice standardised bulletin board

2.2. Summary of planned investments in the region (incl. Storage)

TSOs

TSOs, SSOs

12:30 Lunch break

13.30 3. Presentation session II:

3.1. Removing remaining obstacles to implementation of IPA/OBA

3.2. Best practice provision of OSS service

TSOs an shippers

TSOs

15.00 Coffee break

4. Presentation session III:

4.1. Regional Entry Exit Tariff System

4.2. Hub development as regional balancing market

RCC

Hub operators,

EFET, Eurelectric

16.30 5. Closure

5.1. Summary of main findings

5.2. Date(s) of the next meeting

5.3. Outlook and next steps

Co-chairs

66

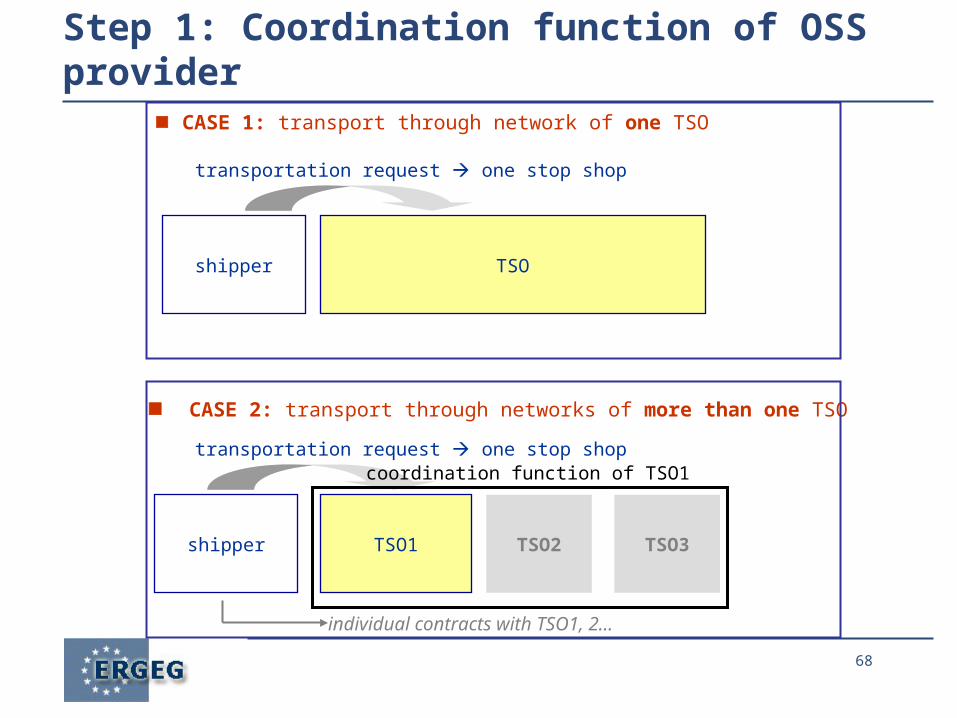

Best practice provision of OSS service

What is expected: Practical implementation of a voluntary one-stop-shop (OSS)

service based on the recommendations of the OSS study Information requirements

Capacity information Cumulative transportation tariff for the requested route Contract information to be signed with different parties Service fee for the OSS service

67

Regional one-stop-shop service provider

Step 1 – no new legal basis: requirements on a regional OSS provider

capacity information tariff information contract information service fee Standardized secondary market trading platform

(Step 2 – enhanced inter-TSO-cooperation) establishment of a regional entity set up by TSOs (RGM) main tasks of a RGM

Grid access and Capacity Management Gas Flow Control & Optimizing Investment (regional long-term planning)

68

Step 1: Coordination function of OSS provider

TSOshipper

transportation request one stop shop

TSO2

CASE 1: transport through network of one TSO

CASE 2: transport through networks of more than one TSO

shipper TSO1 TSO3

transportation request one stop shop

individual contracts with TSO1, 2...

coordination function of TSO1

69

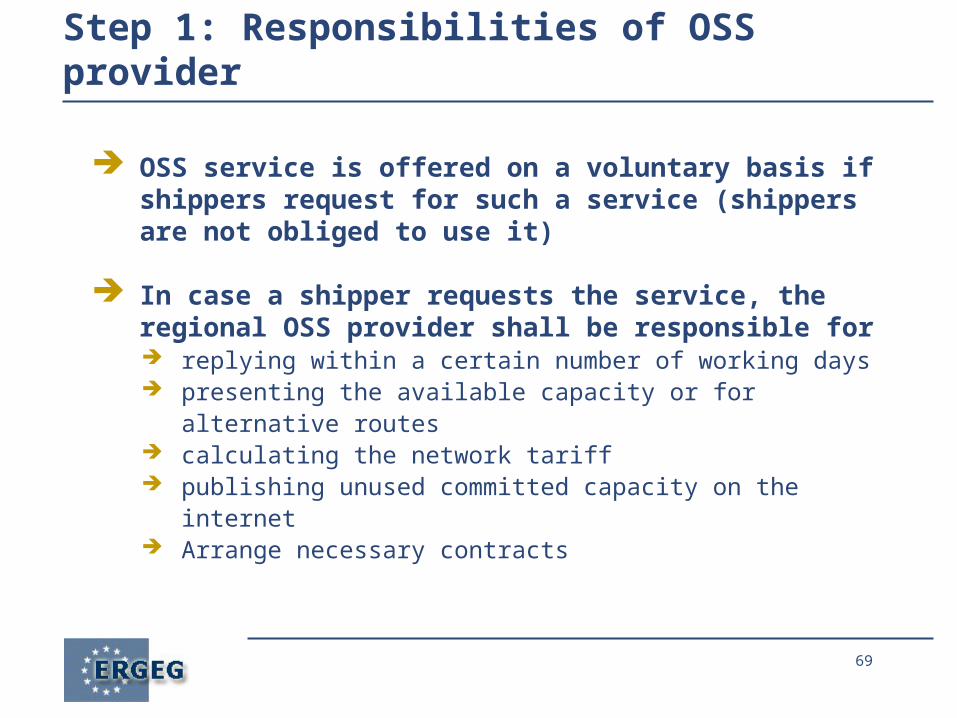

Step 1: Responsibilities of OSS provider

OSS service is offered on a voluntary basis if shippers request for such a service (shippers are not obliged to use it)

In case a shipper requests the service, the regional OSS provider shall be responsible for replying within a certain number of working days presenting the available capacity or for alternative routes calculating the network tariff publishing unused committed capacity on the internet Arrange necessary contracts

70

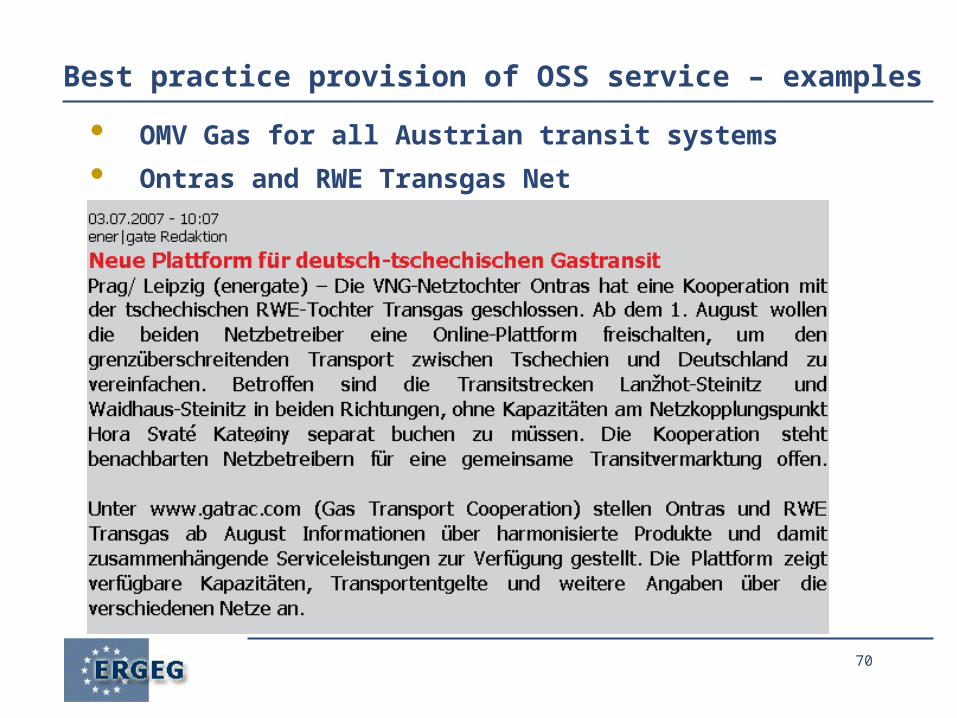

Best practice provision of OSS service – examples

OMV Gas for all Austrian transit systems

Ontras and RWE Transgas Net

One-Stop Shop Provider

TSOs see the first stage of a process that may in the end lead to a one-stop shop provider in creating one common webpage where all relevant information concerning capacity would be available

Action has been taken by TSOs at the European level within the framework of GTE, independent action at the regional level would therefore be superfluous and possibly distortive. In case of delay in the process, appropriate actions at regional level could be taken

One-Stop Shop Provider

TSOs will make every effort to contribute to the creation of a European-wide Transparency

Platform

Obstacles to Implementation of

IPAs/OBA

Process-related obstacles Determination of norms and units to be used for

communication between the relevant TSOs* in connection with the operation of the respective delivery/redelivery station(s) and metering

Determination of the counter-party (e.g. at interface btw Slovakia-Austria)

Obstacles to Implementation of IPAs

* The units agreed are then to be used by Shippers entering and exiting the system at the respective points

Process-related obstacles To be able to ensure allocation equalling nomination, TSOs need to be

able to steer the flows at IPs accordingly. This is only possible if 1) matching of nominations may be executed with the neighbouring TSO, 2) nominations are given sufficiently in advance of the relevant Gas Day, 3) these nominations do not significantly differ from any renominations later on, esp. during the relevant Gas Day (“yo-yo flows” would lead to a very inefficient operation of the system)

Risk-related obstacles Some TSOs may not have access to any other flexibility but linepack.

Additional flexibilities exceeding linepack might generate additional costs. In any way TSOs may not take on unlimited risks and therefore the OBA will remain limited. In case of extraordinary events, in particular unplanned breakdowns on the (upstream) system or unexpected cuts in supply by the producers, the TSOs will need to revert to pro-rata allocation regime.

Obstacles to Implementation of OBA

Obstacles to Implementation of IPAs/OBA

TSOs would like to note that primarily it is necessary to conclude IPAs as such. Their

existence is already a significant contribution to ensuring non-discriminatory, transparent and objective third-party access conditions to gas

grids. Implementation of an OBA regime is dependent on certain prerequisites and will

always be conditional. Shippers must be equally involved in the implementation process by

complying with the nomination rules set up by the TSOs.

77

Action Point 4: Best practice provision of OSS service

Suggested next steps Coordinator: TSOs Next steps:

Transparency platform (GTE pilot project) TSOs offer OSS service to shippers who request the service Best practice OSS (OMV Gas, www.gatrac.com)

Timing: update next meeting

78

Agenda

Agenda Topics Rapporteur

11.00 1. Opening

- Welcome

- Approval of the agenda

Co-chairs

11:15 2. Presentation session I:

2.1. Best-practice standardised bulletin board

2.2. Summary of planned investments in the region (incl. Storage)

TSOs

TSOs, SSOs

12:30 Lunch break

13.30 3. Presentation session II:

3.1. Removing remaining obstacles to implementation of IPA/OBA

3.2. Best practice provision of OSS service

TSOs an shippers

TSOs

15.00 Coffee break

4. Presentation session III:

4.1. Regional Entry Exit Tariff System

4.2. Hub development as regional balancing market

RCC

Hub operators,

EFET, Eurelectric

16.30 5. Closure

5.1. Summary of main findings

5.2. Date(s) of the next meeting

5.3. Outlook and next steps

Co-chairs

79

Regional Entry Exit Tariff System (REETS)

Expected Deliverables: Theoretical considerations on the stepwise introduction of a

REETS in the regional energy market SSE

80

Work plan of REETS study

Will deal with main transportation routes

Following and completing analysis of the routes undertaken in Vienna Workshop and Milan Stakeholder Group meeting

Benchmarking of current tariffs

Simulation of alternative approach (REETS)

Simulation and comparison with today will show feasibility, benefits, and costs of REETS

81

Scope of the study: existing routes

Routes already considered in the GRI for SSE:

1. UKR-SK-CZ-GER (Vel'ké Kapušany - Waidhaus or Hora S. Kateriny)

2. UKR-SK-A-SI-I (Vel'ké Kapušany – Baumgarten – Murfeld - Šempeter/Gorizia)

3. UKR-SK-A-I (Vel'ké Kapušany - Baumgarten - Tarvisio)

4. UKR-SK-A-GER (Vel'ké Kapušany – Baumgarten - Oberkappel)

5. BELARUS-PL-GER-CZ (Kondratki – Mallnow - HSK)

6. ALGERIA-I-(SI)-A-SK (- CZ, -H) (Mazara-Tarvisio (Gorizia–SI) - Baumgarten – Slovakia/Czech Rep./Hungary)

82

Scope of the study: other routes

Routes to be added7. UKR–H-Austria (Beregdaroć-Mosonmagyarovar-Baumgarten)

8. CH-I-A/SI (Griespass-Minerbio-Route 6)

9. Italian LNG terminal connection (Panigaglia-Minerbio-Route 6)

10. UKR-RO-BG-GR (Isaccea–Negru Voda-Kula-Revithoussa)

11. UKR–H-Serbia (Beregdaroć-Szeged)

12. UKR-PL (Drozdowice-Mallnow)

Future Routes ●- TR-BG-RO-H-A (Nabucco)●- TR-GR-I (IGI)●- New LNG terminals in Italy, Croatia and related pipelines

83

Scope of the study: entry and exit points

Entry points➢ SSE import-export points (Kondratki, Vel'ké Kapušany,

Beregdaroć, Griespass, Panigaglia, Mazara, Gela, Isaccea, Negru Voda, Kula, Revithoussa, Oberkappel, Szeged)

➢ Main domestic production and storage areas (Baumgarten area, N. Adriatic, Po Valley, Central - S. Romania, S. Hungary, Silesia...)

Exit points ➢ SSE import-export points

➢ Representative consumption points close to the routes (Warsaw, Krakow, Poznan, Bratislava, Košice, Brno, Prague, Vienna, Linz, Klagenfurt, Milan, Bologna, Rome, Messina, Ljubljana, Budapest, Szeged, Bucharest, Constanta, Sofia, Thessaloniki, Athens)

84

Main transportation profiles

● Standard profiles to be defined for current tariff benchmarking and REETS simulation

● Current tariffs to be calculated for all entry-exit pairs, for standard transportation profiles

● Based on ongoing CEER benchmarking study

➢ performed for B, F, DK, H, NL, forthcoming

➢ Balancing regimes and charges included in the study

➢ Volumes: 5 Gm3, 500 Mm3, 50 Mm3

➢ Load factors 0.88, 0.71, 0.57, 0.34 (on hourly basis)

85

Current average tariffs for main routes/TSO

Unit \ Line TAG GmbH BOG GmbH OMV Gas GmbH

Entry Baumgarten Baumgarten Mazara

Exit Baumgarten

102,2 29 10,6 180 81,6 108 301 7,1

Exit capacity Mcm/d 88,3 17 10,6 142 NA 100,8 260 2,6

Km 380 245 26 390 1720 684 470 235

Tariff methodology Cost-based Cost-based Cost-based Benchmarking Cost-based Cost-based Benchmarking Cost-based

EUR/(m3/h)/(km/a) 0,125 0,241 0,875 0,170 0,052 0,148 0,187 0,410

RWE Transgas NET, s.r.o

Snam Rete Gas S.p.A.GAZ-SYSTEM

S.A.SPP - preprava,

a.s.Geoplin Plinovodi

d.o.o.

Weitendorf Lanžhot Kondratki Velke Kapušany Ceršak

Arnoldstein/Tarvisio Oberkappel Ceršak Waidhaus Tarvisio/Arnoldstein Mallnow Šempeter

Entry capacity Mcm/d

86

REETS simulation: allowed revenues

Calculation of revenue requirements for each route and TSO

➢ Based on allowed revenue approved by National Regulator

for each TSO

➢ Based on current balance sheets

➢ After benchmarking and harmonisation of revenue

calculation criteria

87

REETS simulation: tariff structure● Simulation of common entry-exit system with interlinks between balancing zones

● Identification of bottlenecks & balancing zones

➢ where present red lights at TSO border

● Simulation of entry and exit tariffs within each balancing zone

➢ average cost vs. long run marginal cost

● Regulated interlinks between zones

● Single zone may be simulated assuming current bottlenecks are removed

88

REETS simulation: new investment

● Based on investment plans delivered by TSOs

● Including investment required for bottleneck removal

● Simulation of the new major infrastructure impact (Nabucco, Greece-Italy, Algeria-Sardinia-Italy, new LNG terminals), possibly subject to partial TPA exemption

● TPA exemption enhances sponsor/TSO responsibility, reduces impact on EE tariffs

89

Action Point 5: Regional Entry Exit Tariff System (REETS)

Suggested next steps Coordination: RCC/AEEG Next steps:

presentation of benchmarking results simulation of implementation REETS

Timing: update next meeting

90

Agenda

Agenda Topics Rapporteur

11.00 1. Opening

- Welcome

- Approval of the agenda

Co-chairs

11:15 2. Presentation session I:

2.1. Best-practice standardised bulletin board

2.2. Summary of planned investments in the region (incl. Storage)

TSOs

TSOs, SSOs

12:30 Lunch break

13.30 3. Presentation session II:

3.1. Removing remaining obstacles to implementation of IPA/OBA

3.2. Best practice provision of OSS service

TSOs an shippers

TSOs

15.00 Coffee break

4. Presentation session III:

4.1. Regional Entry Exit Tariff System

4.2. Hub development as regional balancing market

RCC

Hub operators,

EFET, Eurelectric

16.30 5. Closure

5.1. Summary of main findings

5.2. Date(s) of the next meeting

5.3. Outlook and next steps

Co-chairs

91

Punto

Scambio

V irtuale

Baumgarten

PL

A

I

SLO

H

SK

CZ

GR

Hub development as regional balancing market (I)

What is expected Step 1: Plan for development the Hubs in the region as a

regional balancing point Step 2: Suggestions for practical implementation of the

concepts developed under step 1

92

Hub development as regional balancing market (II)

16 February 2007Gas Committee – CEGH Working Group

Timeline

Feb 07 Oct 2008Oct 07

? For Bulletin Board the decision on Market Maker (volume? spread? period? rights and responsibilities?)

? Back-up/-down services? Customer focus

?OBAs?physical nomination < 1 day

lead time (now 5 days)?Web based nomination

? Workshop CEGH with EFET on products

Mar 07 May 2007

? systematic offering of structured products (week ahead, month ahead) anonymous

? standardised agreements (EFETs)

? (Super-) firm market place

? CEGH takes counterpart risk and makes clearing

? International balancing via CEGH

? online intraday balancing market

? derivative trading with physical hedge/forwards

? gas exchange

? Meeting CEGH with EFET CEGH Working Group (Ressl)

Jan 2009

? Derivative trading? Regional

balancing market

Mar/Apr 07 Jan 2008

? Meeting CEGH with EFET CEGH Working Group (after 20.03)

? day ahead products? intraday products? physical nomination

< 1 day possible? web based

nomination possible

Jul 07

? Operational Market Maker

? Back up/down service

? completion of contractual specifications

CEGH

SPP System

BOG System OMV Gas System

TAG System

TradingShipper CEGH

Shipper CEGH

Shipper CEGH

Shipper OMV GASShipper WAG

Shipper TAG

TradingShipper CEGH

Systems of Austrian Side

Systems of Slovakian Side

Shipper SPP

SPP System

BOG System

OMV Gas System

TAG System

Shipper 1Shipper 2

Shipper 3

Shipper xyShipper xy

Shipper xy

Shipper xyShipper xy

Shipper xy

Shipper xyShipper xy

Shipper xy

ShipperShipper 1Shipper 2

Shipper 3

ShipperShipper xy

Shipper xy

Shipper xy

ShipperShipper xyShipper xyShipper xy

ShipperShipper xyShipper xy

Shipper xy

CEGH System

Detailed illustration of matching operation

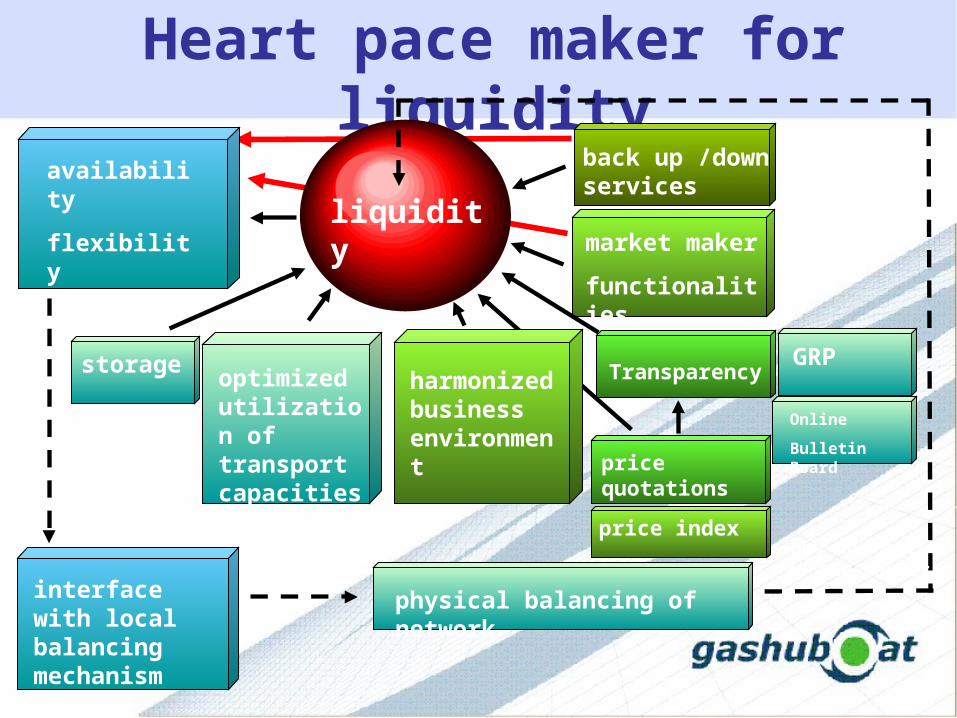

Heart pace maker for liquidity

optimized utilization of transport capacities

harmonized business environment

storage

price quotations

back up /down services

market maker

functionalities

availability

flexibility

of gas

interface with local balancing mechanism

physical balancing of network

liquidity

buy and sell to the market

TransparencyGRP

Online

Bulletin Board

price index

AGCSProvider 4

Provider 3

Provider 2

Provider 130€

25€ 20€

15€

Merit

Order

list

Provider 1

Provider 2

Provider 3

Provider 4

Balancing Energy Market

Back UP/DownMarket

Merit

Order

list

CEGH27€

23€

18€

13€

Shipper

1

Shipper

2

Shipper

3

Shipper

4

Shipper

5

Shipper

6

Shipper

7

Shipper

8

Shipper 9Shipper 10Shipper 11Shipper 12Shipper 13Shipper 14Shipper 9Shipper 10Shipper 11Shipper 12Shipper 13Shipper 14

Shipper 15

Shipper 16

Shipper 17

Shipper

1

Shipper

2

Shipper

3

Shipper

4

Shipper

5

Shipper 1

Shipper 2

Shipper 3

Shipper 4

Shipper 5

HUB

Control area

WAG

TAG

SPP

HAG

MAB

storage

Shi

pper

Shi

pper

Ship

per

Ship

per

Ship

per 9

Ship

per 1

0S

hip

per 1

1S

hip

per 1

2S

hip

per 1

3S

hip

per 1

4

Ship

per

9S

hip

per

10

Ship

per

11

Ship

per

12

Ship

per

13

Ship

per

14

ShipperShipper

13€

15€

18€

20€23€

25€

27€

30€

Combined Merit

Order

list

EFET – PLAN next steps back up back down services

Hub as Balancing Point

OBA

ERGEG - Issues

Back up/down Service

provision

Back up/down Service

Request for tender

Contract with providers

Contract with OTC - customers

Prepared for discussion with EFET

16 February 2007Gas Committee – CEGH Working Group

Timeline

Feb 07 Oct 2008Oct 07

? For Bulletin Board the decision on Market Maker (volume? spread? period? rights and responsibilities?)

? Back-up/-down services? Customer focus

?OBAs?physical nomination < 1 day

lead time (now 5 days)?Web based nomination

? Workshop CEGH with EFET on products

Mar 07 May 2007

? systematic offering of structured products (week ahead, month ahead) anonymous

? standardised agreements (EFETs)

? (Super-) firm market place

? CEGH takes counterpart risk and makes clearing

? International balancing via CEGH

? online intraday balancing market

? derivative trading with physical hedge/forwards

? gas exchange

? Meeting CEGH with EFET CEGH Working Group (Ressl)

Jan 2009

? Derivative trading? Regional

balancing market

Mar/Apr 07 Jan 2008

? Meeting CEGH with EFET CEGH Working Group (after 20.03)

? day ahead products? intraday products? physical nomination

< 1 day possible? web based

nomination possible

Jul 07

? Operational Market Maker

? Back up/down service

? completion of contractual specifications

100

Action Point 6: Hub development as regional balancing market (I)

Suggested next steps Lead: PSV/EFET and CEGH/EFET Next steps:

Separate workstreams and update on implementation of next steps according schedule

Timing:

16 February 2007Gas Committee – CEGH Working Group

Timeline

Feb 07 Oct 2008Oct 07

? For Bulletin Board the decision on Market Maker (volume? spread? period? rights and responsibilities?)

? Back-up/-down services? Customer focus

? OBAs? physical nomination < 1 day

lead time (now 5 days)? Web based nomination

? Workshop CEGH with EFET on products

Mar 07 May 2007

? systematic offering of structured products (week ahead, month ahead) anonymous

? standardised agreements (EFETs)

? (Super-) firm market place

? CEGH takes counterpart risk and makes clearing

? International balancing via CEGH

? online intraday balancing market

? derivative trading with physical hedge/forwards

? gas exchange

? Meeting CEGH with EFET CEGH Working Group (Ressl)

Jan 2009

? Derivative trading? Regional

balancing market

Mar/Apr 07 Jan 2008

? Meeting CEGH with EFET CEGH Working Group (after 20.03)

? day ahead products? intraday products? physical nomination

< 1 day possible? web based

nomination possible

Jul 07

? Operational Market Maker

? Back up/down service

? completion of contractual specifications

Gas Regional Initiative Regional Energy Market South-

South East

Hub development as a regional balancing market

PSV implementation TF

Hub development as regional balancing points:

TF considerations

The TF shares the ERGEG objective of developing the hubs as balancing points Market based balancing more effective and positive for liberalisation than fixed penalties Helps to increase the liquidity at the hubs in SSE Reduces the risk of exposure for traders

In principle the TF also shares the objective of setting regional balancing points

Hub development as regional balancing points:

TF considerations

In practice the SSE regional market lacks:

harmonized business environment (contractual conditions, operational procedures, balancing mechanism and procedures etc…)

well meshed gas grid. For instance there is no interconnection between Poland and the southern SSE countries

available capacities: gas flows throughout the whole region limited by physical/contractual congestion on the interconnection routes

Hub development as regional balancing points:

Balancing points in the SSE Region

As a first immediate step the TF suggests the development of two/three hubs in the region acting as balancing points for their reference area.

In the longer term the local balancing points could evolve to a regional dimension.

PSV Implementation Task Force

The way forward

Set users priorities for the development of PSV as a balancing point

Meet with other stakeholders (hub operator, regulators, other interested parties)

Plan for the development of PSV as balancing point

106

Agenda

Agenda Topics Rapporteur

11.00 1. Opening

- Welcome

- Approval of the agenda

Co-chairs

11:15 2. Presentation session I:

2.1. Best-practice standardised bulletin board

2.2. Summary of planned investments in the region (incl. Storage)

TSOs

TSOs, SSOs

12:30 Lunch break

13.30 3. Presentation session II:

3.1. Removing remaining obstacles to implementation of IPA/OBA

3.2. Best practice provision of OSS service

TSOs an shippers

TSOs

15.00 Coffee break

4. Presentation session III:

4.1. Regional Entry Exit Tariff System

4.2. Hub development as regional balancing market

RCC

Hub operators,

EFET, Eurelectric

16.30 5. Closure

5.1. Summary of main findings

5.2. Date(s) of the next meeting

5.3. Outlook and next steps

Co-chairs

107

Action Points 1-3

Implementation TF ActionsResponsible/Result until

Best-practice standardised bulletin board - harmonized content for individual TSO platforms accordnig TAG and OMV best practice

TSOspresentation at next IG meeting

Summary of planned investments in the region (incl. Storage)

- inclusion of information on expansion projects (Transmission&Storage) into the survey

RCCpresentation at next IG meeting

Removing remaining obstacles to implementation of IPA/OBA

- further update on implementation :TSOs will focus on concluding IPAs where these are not yet in place; Implementation of an OBA regime is dependent on certain prerequisites and will always be conditional; Shippers must be equally involved in the implementation process by complying with the nomination rules set up by the TSOs

- Baumgarten: all involved stakeholders work on a solution within the next 3 months incl. a list of remaining ostacles

TSOs, Shippers

CEGHpresentation at next IG meeting

108

Action Points 4-6

Implementation TF ActionsResponsible/Result until

Best-practice standardised bulletin board - harmonized contentaccordnig TAG and OMV best practice

TSOspresentation at next IG meeting

Summary of planned investments in the region (incl. Storage)

- inclusion of information on investments into survey

RCCpresentation at next IG meeting

Removing remaining obstacles to implementation of IPA/OBA

- further update on implementation and- Baumgarten: all involved stakeholders work on a solution within the next 3 months incl. a list of remaining ostacles

CEGHpresentation at next IG meeting

Best practice provision of OSS service

- Transparency platform (GTE pilot project)- TSOs offer OSS service to shippers who request it- best practice OSS (OMV, www.gatrac.com)

TSOs presentation at next IG meeting

REETS

- presentation of benchmarking results- simulation of introduction of REETS

RCCpresentation at next IG meeting

Hub development as regional balancing market

- update on implementation of next steps according schedule

CEGH/EFETPSV/EFETpresentation at next IG meeting

109

Any other business-AOB

Proposed date of next meeting

Suggestion: Next meeting (Stakeholder Group Meeting) end of

September in Maribor proposal

Key: Progress report by implementation group members

Regulators only to facilitate the process

Context of regional activities

Next Madrid Forum on 16th/17th October 2007

ERGEG to report on progress

Update on issues regarding transparency (Outcome of recent

survey)