Embed Size (px)

Citation preview

3-1

ADJUSTMENTS FOR FINANCIAL REPORTING

CHAPTER 3CHAPTER 3

3-2

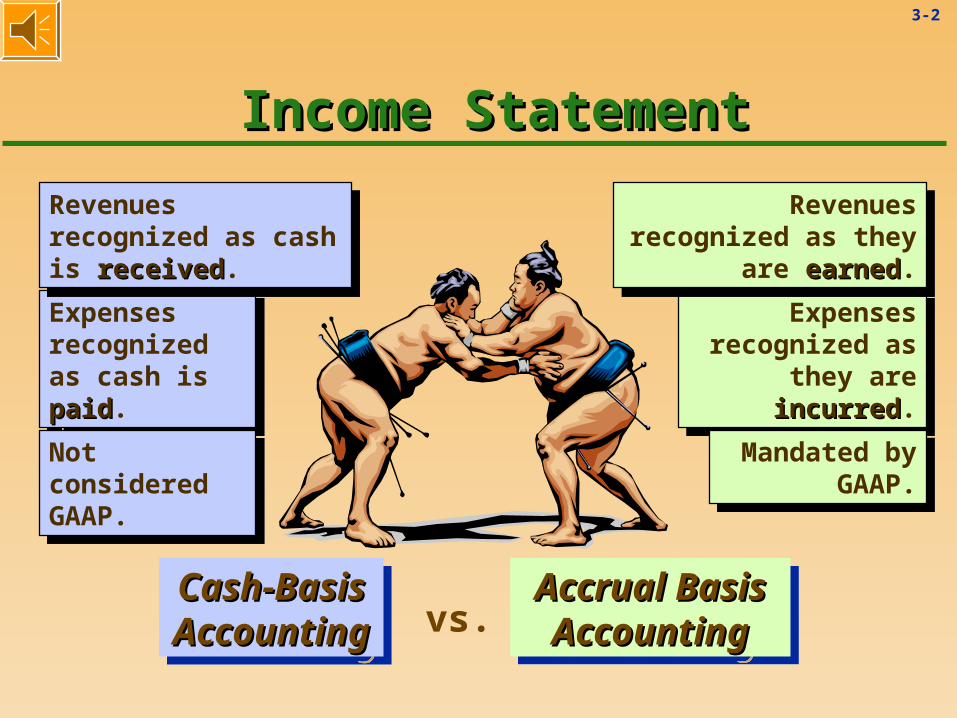

Cash-Basis Cash-Basis AccountingAccountingCash-Basis Cash-Basis AccountingAccounting

Accrual Basis Accrual Basis AccountingAccounting

Accrual Basis Accrual Basis AccountingAccountingvs.

Income StatementIncome Statement

Expenses recognized as cash is paidpaid.

Expenses recognized as cash is paidpaid.

Revenues recognized as cash is receivedreceived.

Revenues recognized as cash is receivedreceived.

Not considered GAAP.

Not considered GAAP.

Expenses recognized as

they are incurredincurred.

Expenses recognized as

they are incurredincurred.

Revenues recognized as they are earnedearned.

Revenues recognized as they are earnedearned.

Mandated by GAAP.

Mandated by GAAP.

3-3

Matching PrincipleMatching Principle

Expenses should be recognized in the same accounting period as are the revenues they generated. (i.e., match revenues and expenses.)

Matching - The Most Important Matching - The Most Important Accounting PrincipleAccounting Principle

3-4

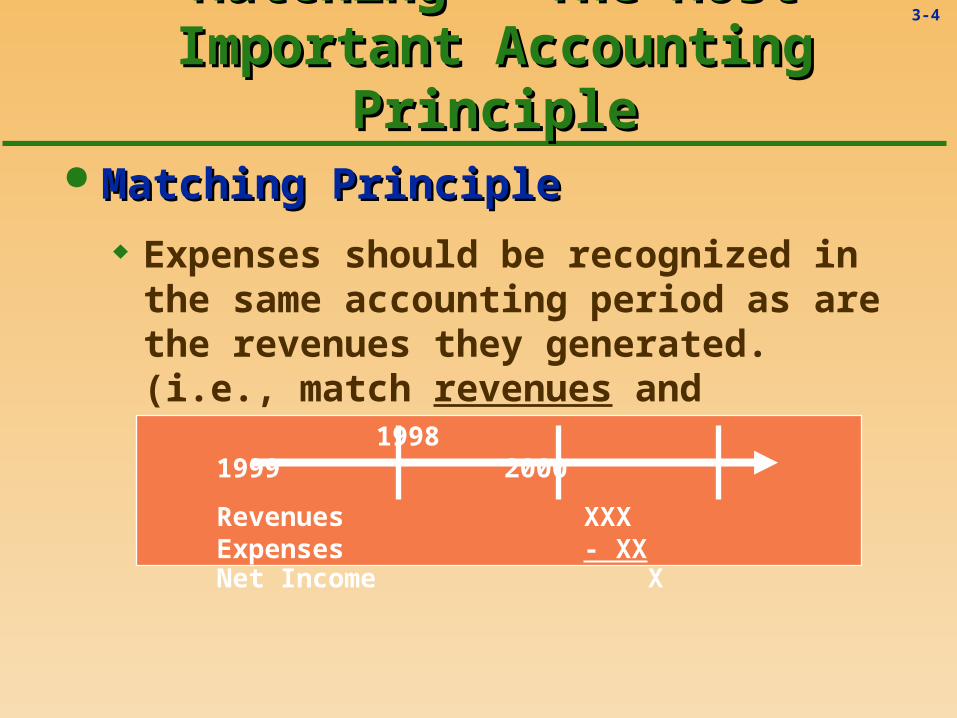

Matching PrincipleMatching Principle

Expenses should be recognized in the same accounting period as are the revenues they generated. (i.e., match revenues and expenses.)

1998 1999 2000

Revenues XXXExpenses - XXNet Income X

Matching - The Most Important Matching - The Most Important Accounting PrincipleAccounting Principle

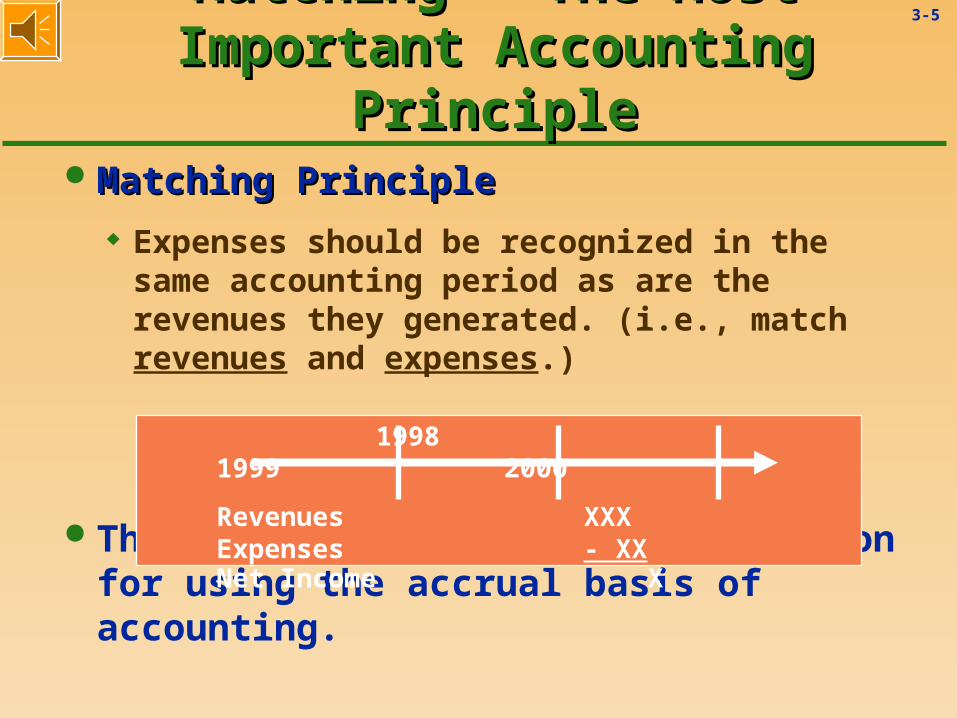

3-5

Matching PrincipleMatching Principle

Expenses should be recognized in the same accounting period as are the revenues they generated. (i.e., match revenues and expenses.)

The Matching Principle Matching Principle is the reason for using the accrual basis of accounting.

1998 1999 2000

Revenues XXXExpenses - XXNet Income X

Matching - The Most Important Matching - The Most Important Accounting PrincipleAccounting Principle

3-6

Journal entries are made at the end of each accounting period to bring about a proper matchingmatching of revenues and expenses

Economic events (i.e., transactions) have been ongoing but never recorded. Why not?

The Need for Adjusting EntriesThe Need for Adjusting Entries

3-7

Journal entries are made at the end of each accounting period to bring about a proper matchingmatching of revenues and expenses

Economic events (i.e., transactions) have been ongoing but never recorded. Why not?

Examples?

The Need for Adjusting EntriesThe Need for Adjusting Entries

3-8

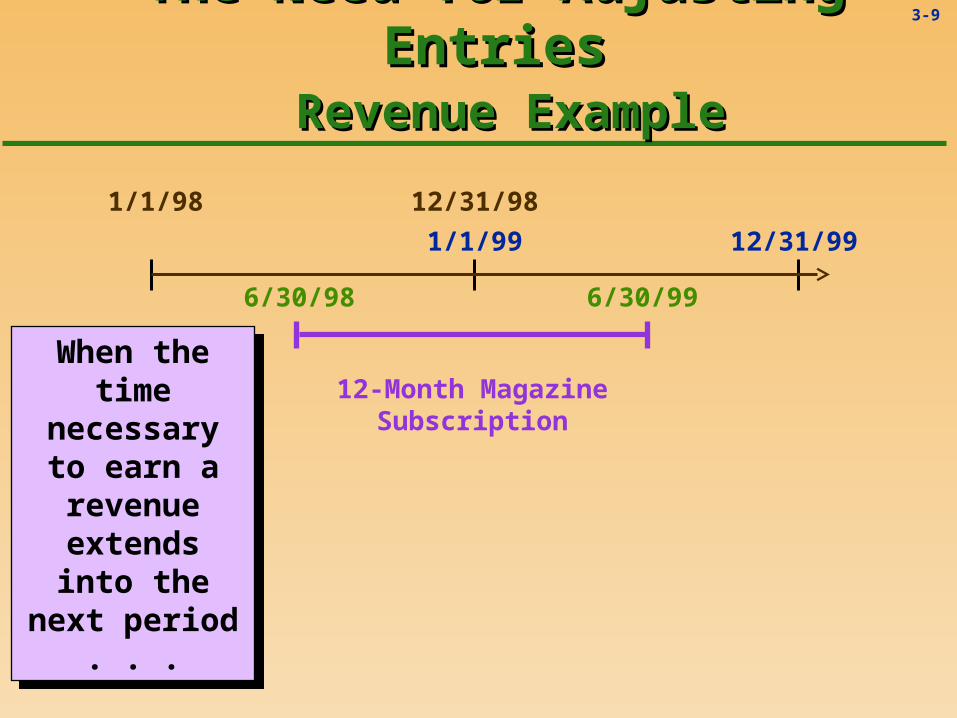

The Need for Adjusting EntriesThe Need for Adjusting Entries Revenue ExampleRevenue Example

3-9

12-Month Magazine Subscription

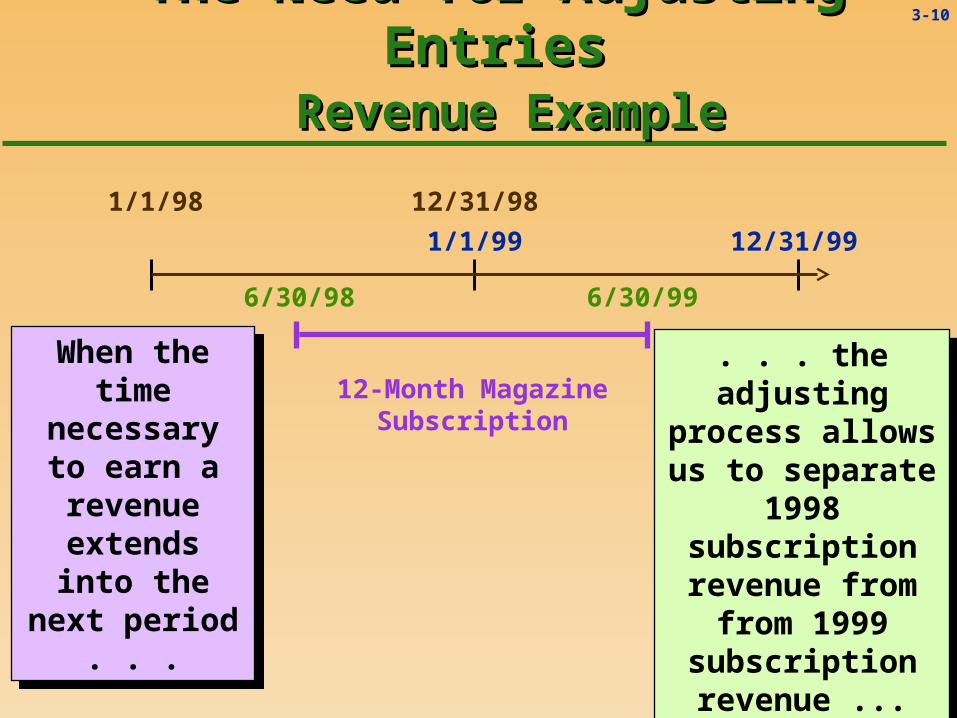

The Need for Adjusting EntriesThe Need for Adjusting Entries Revenue ExampleRevenue Example

1/1/98 12/31/98

1/1/99 12/31/99

6/30/98 6/30/99

When the time necessary to

earn a revenue

extends into the next

period . . .

When the time necessary to

earn a revenue

extends into the next

period . . .

3-10

. . . the adjusting process allows us to separate 1998

subscription revenue from

from 1999 subscription revenue ...

. . . the adjusting process allows us to separate 1998

subscription revenue from

from 1999 subscription revenue ...

When the time necessary to

earn a revenue

extends into the next

period . . .

When the time necessary to

earn a revenue

extends into the next

period . . .

12-Month Magazine Subscription

1/1/98 12/31/98

1/1/99 12/31/99

6/30/98 6/30/99

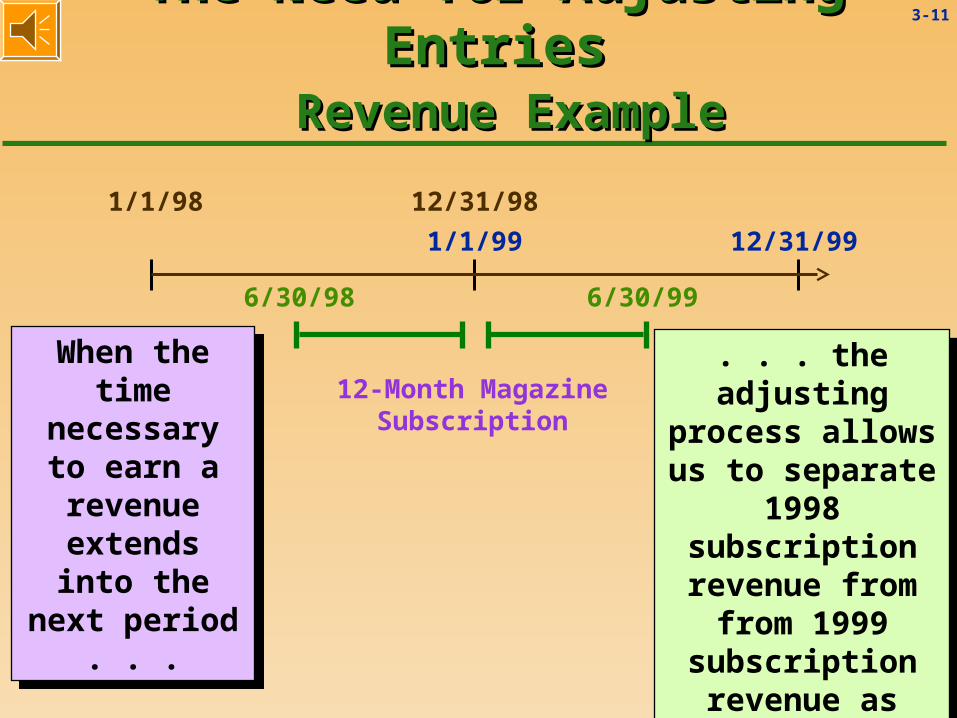

The Need for Adjusting EntriesThe Need for Adjusting Entries Revenue ExampleRevenue Example

3-11

. . . the adjusting process allows us to separate 1998

subscription revenue from

from 1999 subscription revenue as

shown.

. . . the adjusting process allows us to separate 1998

subscription revenue from

from 1999 subscription revenue as

shown.

When the time necessary to

earn a revenue

extends into the next

period . . .

When the time necessary to

earn a revenue

extends into the next

period . . .

12-Month Magazine Subscription

1/1/98 12/31/98

1/1/99 12/31/99

6/30/98 6/30/99

The Need for Adjusting EntriesThe Need for Adjusting Entries Revenue ExampleRevenue Example

3-12

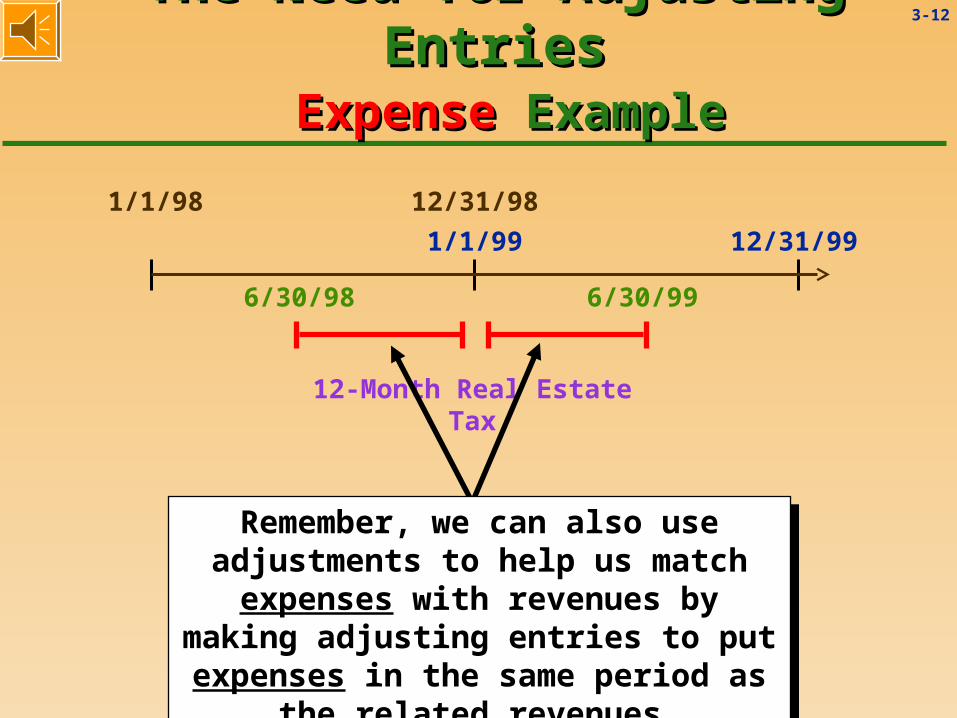

12-Month Real Estate Tax

Remember, we can also use adjustments to help us match

expenses with revenues by making adjusting entries to put expenses in the

same period as the related revenues.

Remember, we can also use adjustments to help us match

expenses with revenues by making adjusting entries to put expenses in the

same period as the related revenues.

1/1/98 12/31/98

1/1/99 12/31/99

6/30/98 6/30/99

The Need for Adjusting EntriesThe Need for Adjusting Entries ExpenseExpense Example Example

3-13

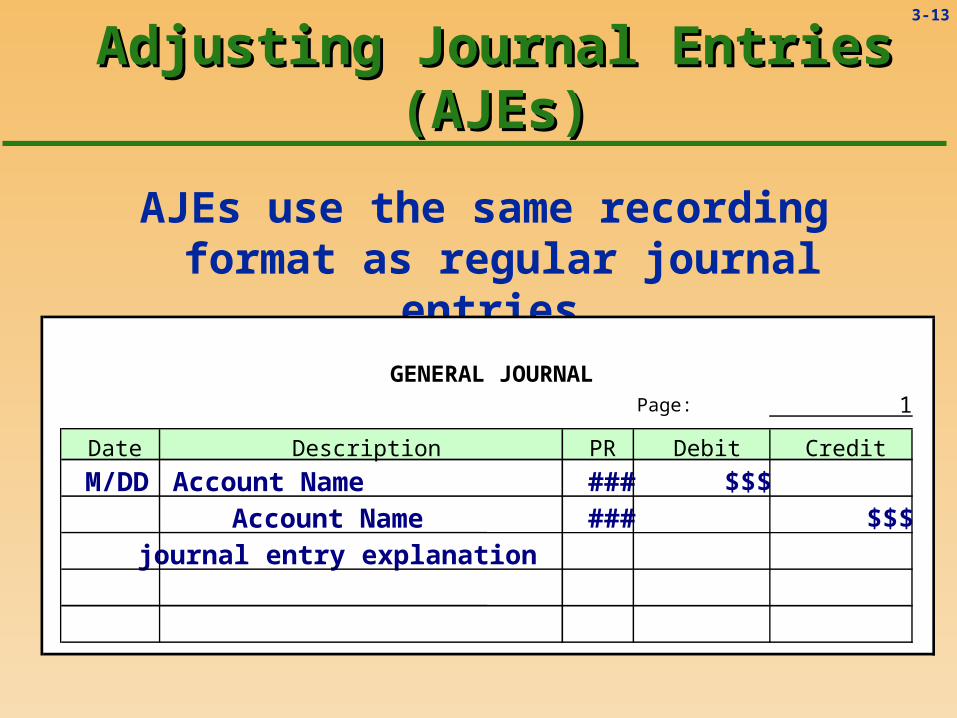

Adjusting Journal Entries (AJEs)Adjusting Journal Entries (AJEs)

AJEs use the same recording format as regular journal entries.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

M/DDAccount Name ### $$$ Account Name ### $$$

journal entry explanation

3-14

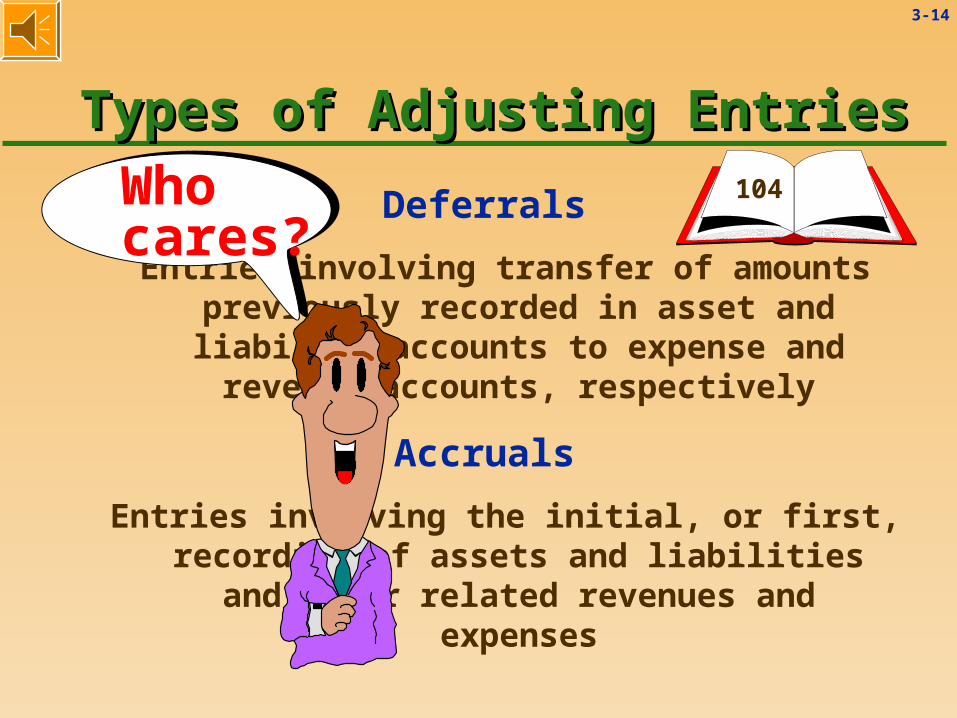

Types of Adjusting EntriesTypes of Adjusting Entries

Deferrals

Entries involving transfer of amounts previously recorded in asset and liability

accounts to expense and revenue accounts, respectively

Accruals

Entries involving the initial, or first, recording of assets and liabilities and their

related revenues and expenses

104Who cares?

3-15

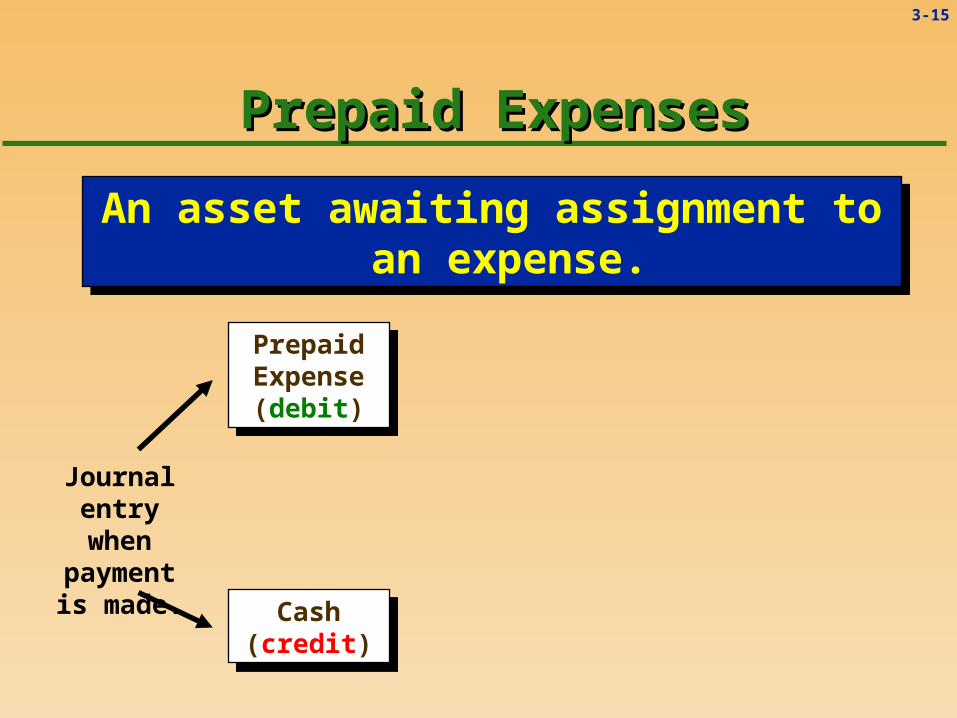

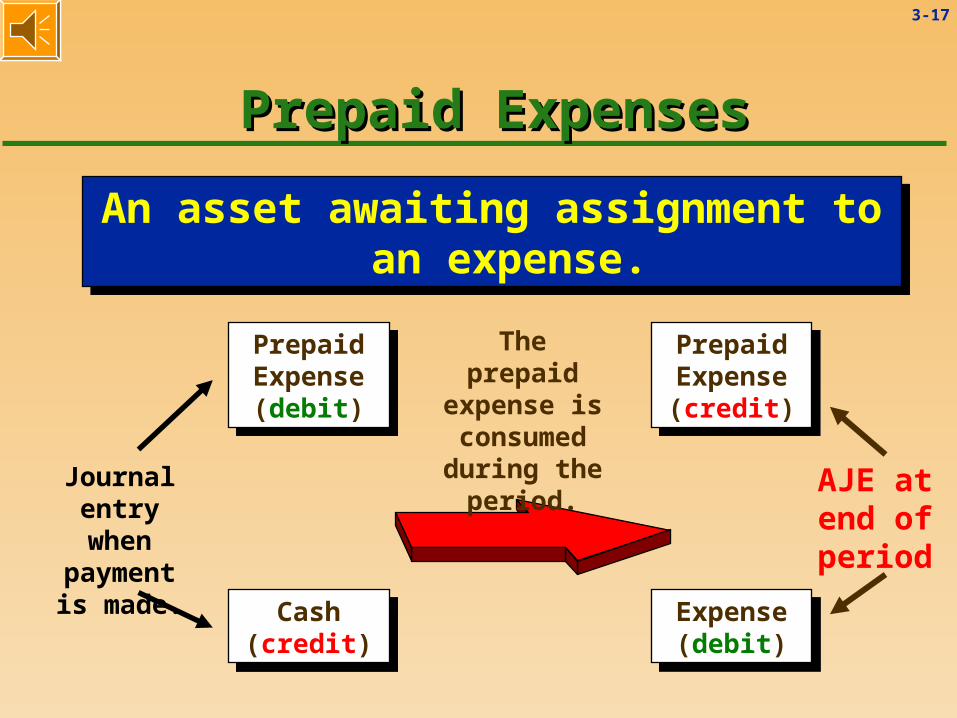

Prepaid ExpensesPrepaid Expenses

An asset awaiting assignment to an expense.

An asset awaiting assignment to an expense.

Cash (credit)

Cash (credit)

Prepaid Expense (debit)

Prepaid Expense (debit)

Journal entry when payment is

made.

3-16

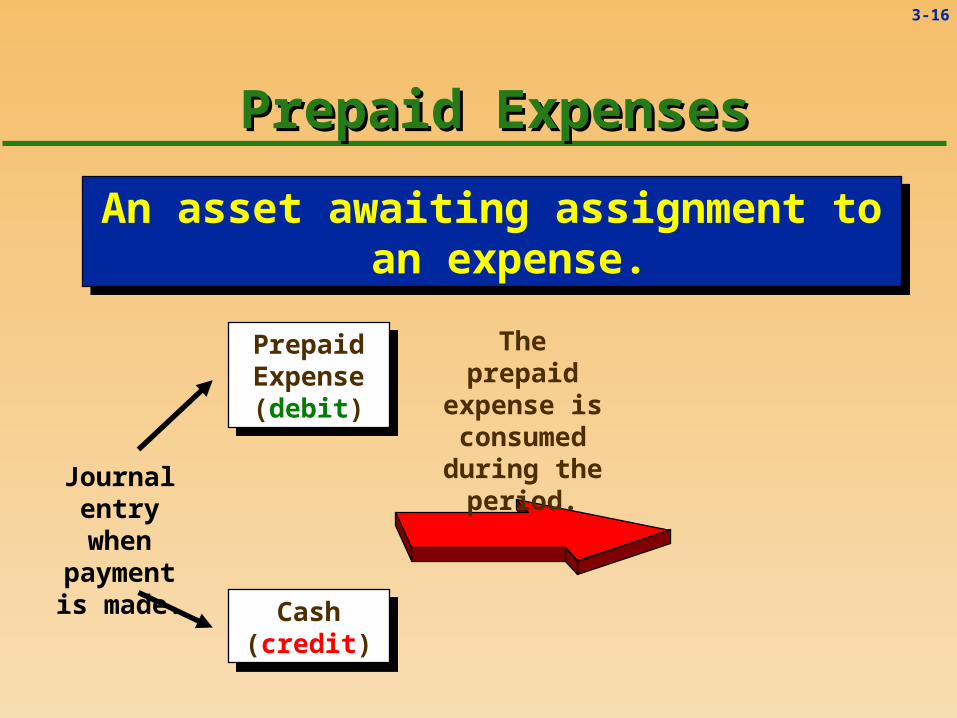

Prepaid ExpensesPrepaid Expenses

An asset awaiting assignment to an expense.

An asset awaiting assignment to an expense.

The prepaid expense is consumed during the

period.

Cash (credit)

Cash (credit)

Prepaid Expense (debit)

Prepaid Expense (debit)

Journal entry when payment is

made.

3-17

Prepaid ExpensesPrepaid Expenses

An asset awaiting assignment to an expense.

An asset awaiting assignment to an expense.

Expense (debit)

Expense (debit)

Prepaid Expense (credit)

Prepaid Expense (credit)

The prepaid expense is consumed during the

period.

Cash (credit)

Cash (credit)

Prepaid Expense (debit)

Prepaid Expense (debit)

Journal entry when payment is

made.

AJE at end of period

3-18

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

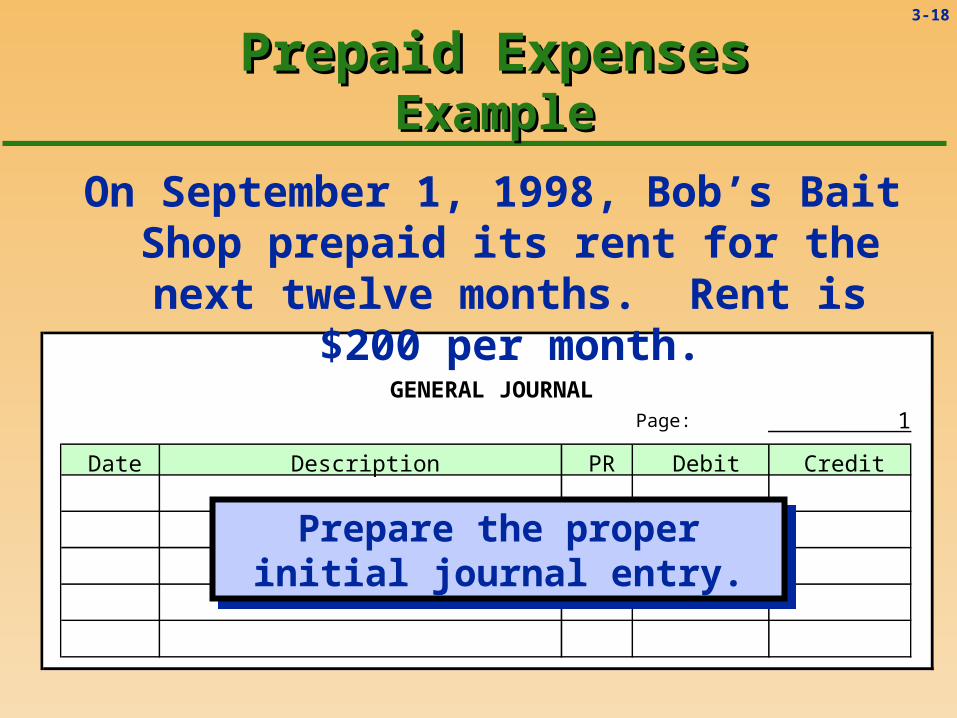

Prepaid ExpensesPrepaid ExpensesExampleExample

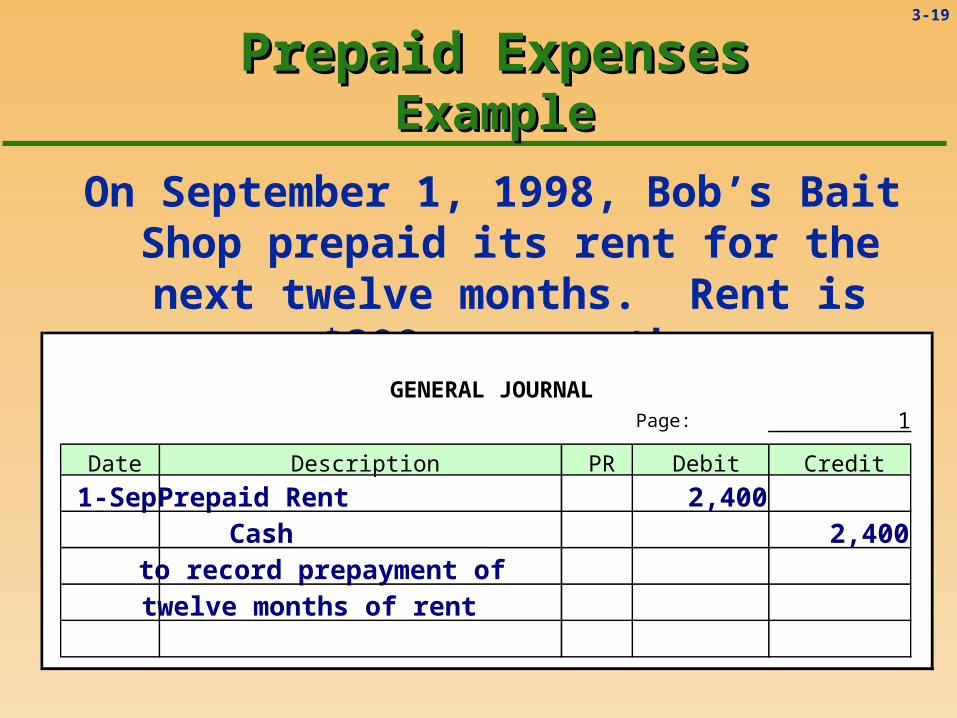

On September 1, 1998, Bob’s Bait Shop prepaid its rent for the next twelve months. Rent is $200 per month.

Prepare the proper initial journal entry.

Prepare the proper initial journal entry.

3-19

On September 1, 1998, Bob’s Bait Shop prepaid its rent for the next twelve months. Rent is $200 per month.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

1-Sep Prepaid Rent 2,400 Cash 2,400to record prepayment of twelve months of rent

Prepaid ExpensesPrepaid ExpensesExampleExample

3-20

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

Prepaid ExpensesPrepaid ExpensesExampleExample

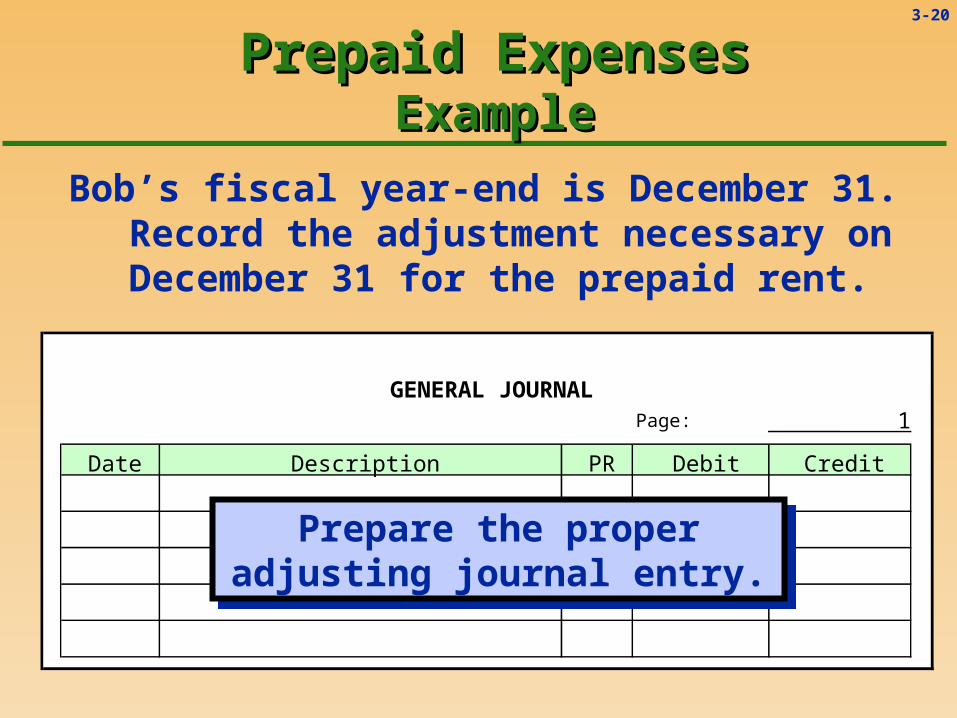

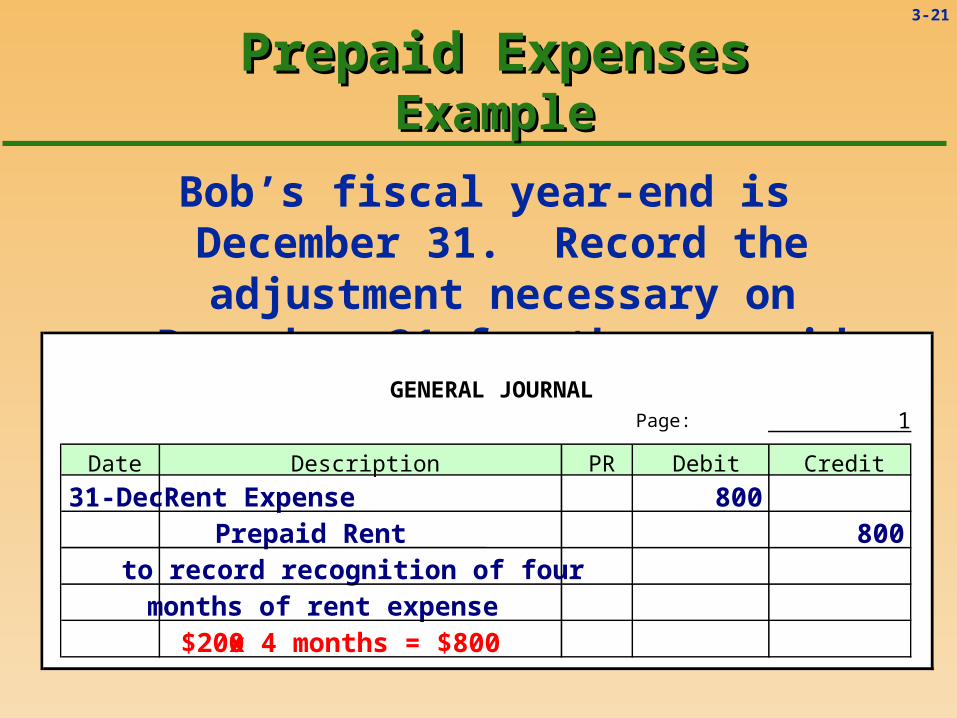

Bob’s fiscal year-end is December 31. Record the adjustment necessary on

December 31 for the prepaid rent.

Prepare the proper adjusting journal entry.

Prepare the proper adjusting journal entry.

3-21

Bob’s fiscal year-end is December 31. Record the adjustment necessary on

December 31 for the prepaid rent.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

31-Dec Rent Expense 800 Prepaid Rent 800to record recognition of fourmonths of rent expense $200x 4 months = $800

Prepaid ExpensesPrepaid ExpensesExampleExample

3-22

Prepaid ExpensesPrepaid ExpensesOther ExamplesOther Examples

Prepaid Insurance Premiums are paid in advance.

Prepaid Subscriptions Magazine and newspaper

subscriptions are always paid in advance.

Supplies on Hand Supplies are “charged” to

expense periodically.

3-23

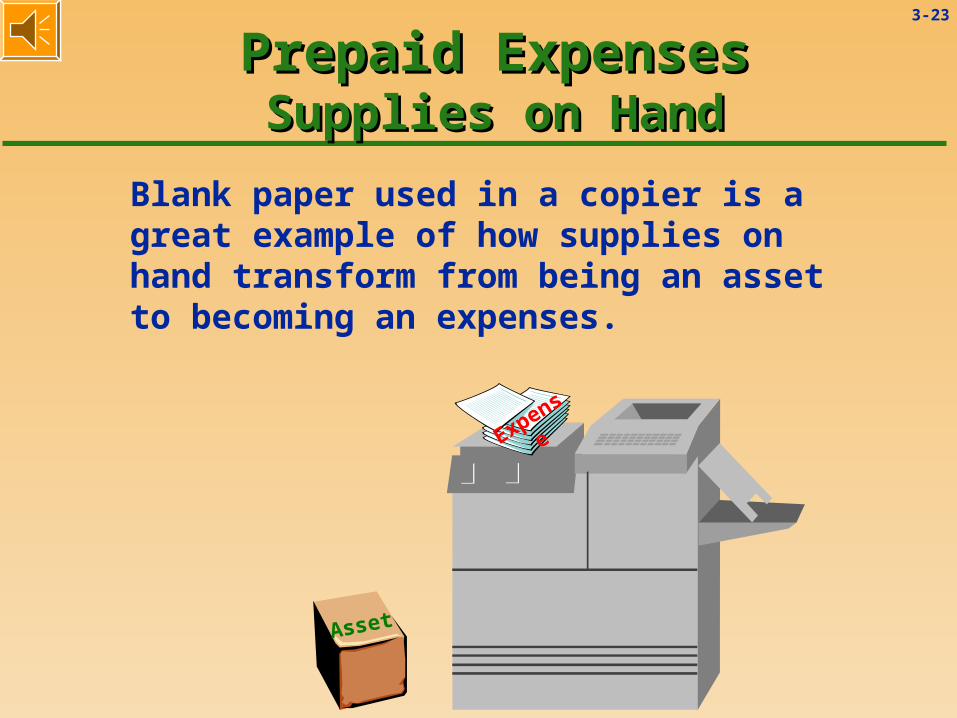

Prepaid ExpensesPrepaid ExpensesSupplies on HandSupplies on Hand

Blank paper used in a copier is a great example of how supplies on hand transform from being an asset to becoming an expenses.

Asset

Expense

3-24

Accounting EstimatesAccounting Estimates

Some assets are not fully used up in a single fiscal period. A truck may last five years, but its value

as a resource declines with time and usage.

3-25

Accounting EstimatesAccounting Estimates

Some assets are not fully used up in a single fiscal period. A truck may last five years, but its value as

a resource declines with time and usage.

Assets that benefit more than one year are called long-tlong-terermm or “fixed”“fixed” assets.

3-26

Accounting EstimatesAccounting Estimates

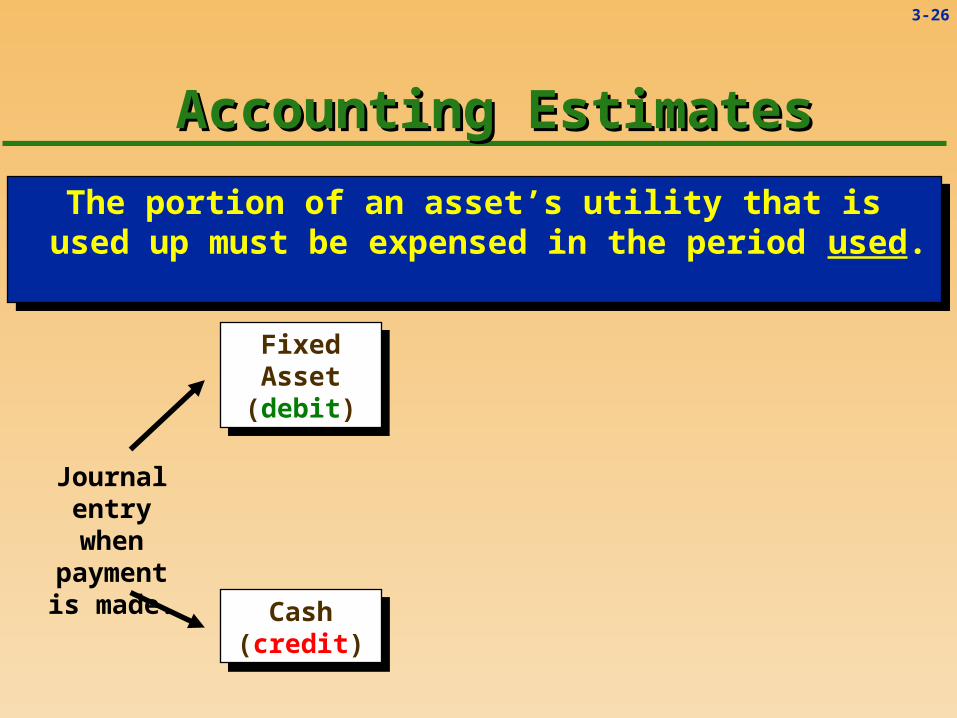

The portion of an asset’s utility that is used up must be expensed in the period used.

The portion of an asset’s utility that is used up must be expensed in the period used.

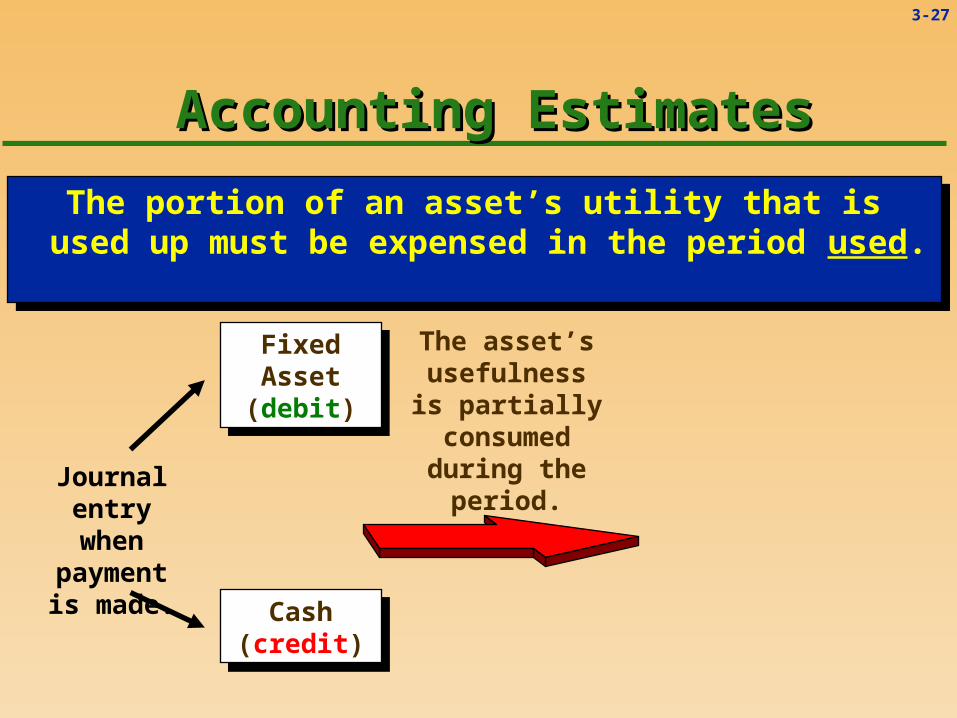

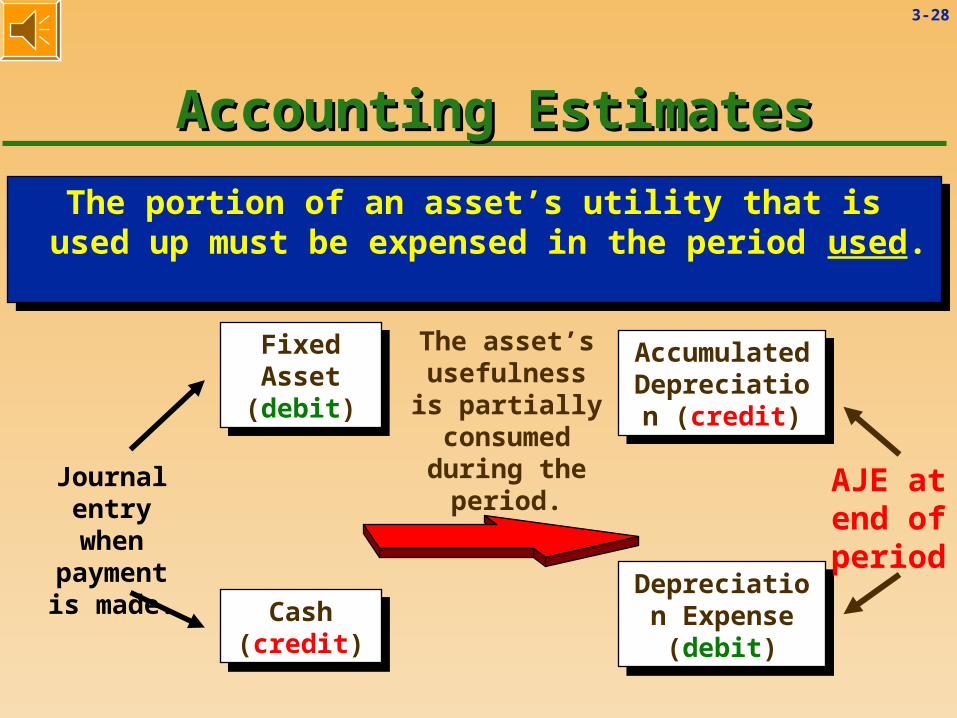

Cash (credit)

Cash (credit)

Fixed Asset (debit)

Fixed Asset (debit)

Journal entry when payment is

made.

3-27

Accounting EstimatesAccounting Estimates

Cash (credit)

Cash (credit)

Fixed Asset (debit)

Fixed Asset (debit)

Journal entry when payment is

made.

The asset’s usefulness is

partially consumed during the

period.

The portion of an asset’s utility that is used up must be expensed in the period used.

The portion of an asset’s utility that is used up must be expensed in the period used.

3-28

Accounting EstimatesAccounting Estimates

Accumulated Depreciation

(credit)

Accumulated Depreciation

(credit)

Depreciation Expense (debit)

Depreciation Expense (debit)

Cash (credit)

Cash (credit)

Fixed Asset (debit)

Fixed Asset (debit)

Journal entry when payment is

made.

The asset’s usefulness is

partially consumed during the

period.

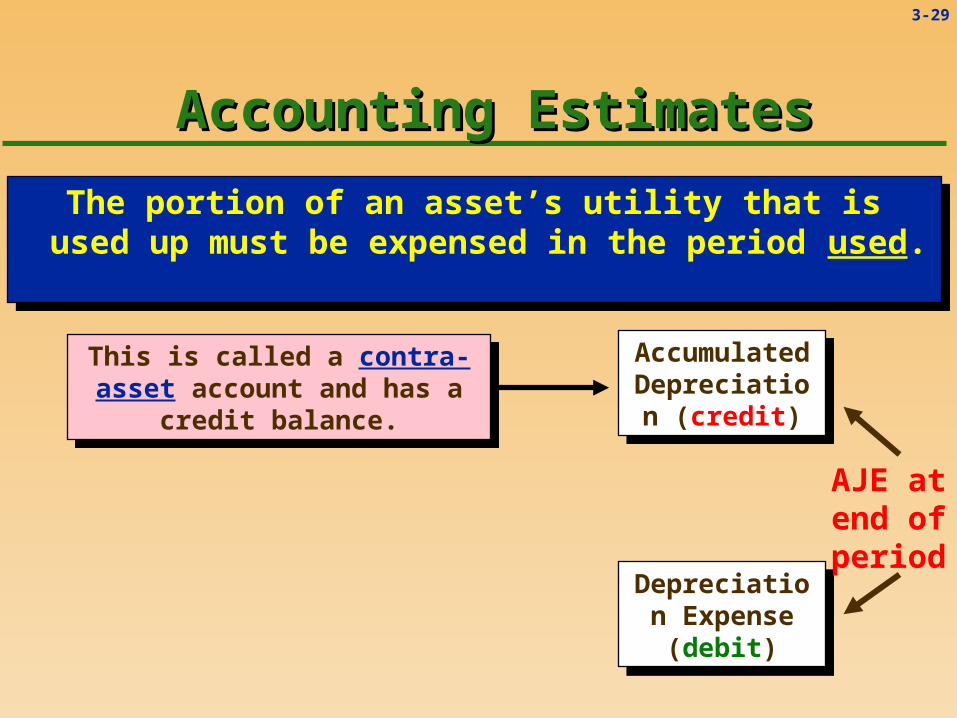

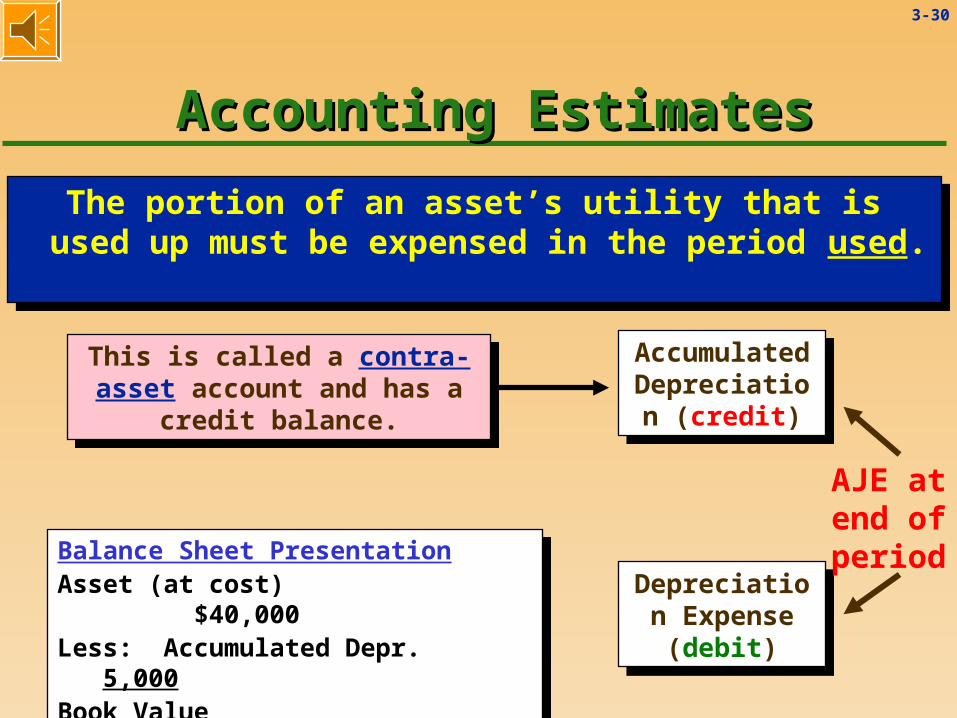

The portion of an asset’s utility that is used up must be expensed in the period used.

The portion of an asset’s utility that is used up must be expensed in the period used.

AJE at end of period

3-29

Accounting EstimatesAccounting Estimates

Accumulated Depreciation

(credit)

Accumulated Depreciation

(credit)

Depreciation Expense (debit)

Depreciation Expense (debit)

This is called a contra-asset account and has a credit

balance.

This is called a contra-asset account and has a credit

balance.

The portion of an asset’s utility that is used up must be expensed in the period used.

The portion of an asset’s utility that is used up must be expensed in the period used.

AJE at end of period

3-30

Accounting EstimatesAccounting Estimates

Accumulated Depreciation

(credit)

Accumulated Depreciation

(credit)

Depreciation Expense (debit)

Depreciation Expense (debit)

This is called a contra-asset account and has a credit

balance.

This is called a contra-asset account and has a credit

balance.

The portion of an asset’s utility that is used up must be expensed in the period used.

The portion of an asset’s utility that is used up must be expensed in the period used.

AJE at end of periodBalance Sheet Presentation

Asset (at cost) $40,000Less: Accumulated Depr. 5,000Book Value $35,000

Balance Sheet Presentation Asset (at cost) $40,000Less: Accumulated Depr. 5,000Book Value $35,000

3-31

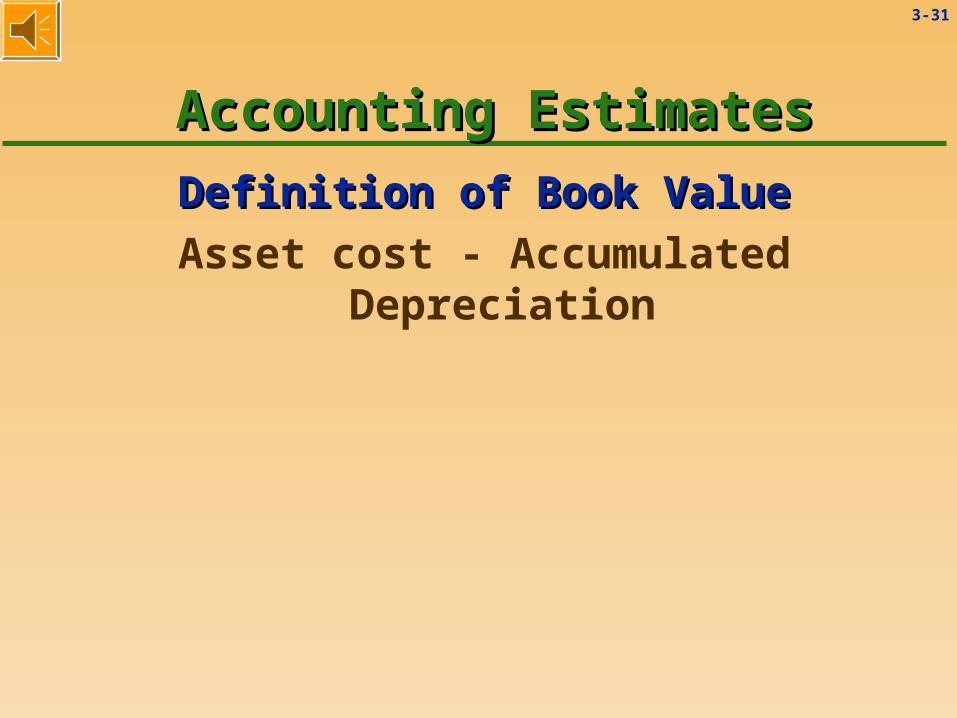

Definition of Book ValueDefinition of Book Value

Asset cost - Accumulated Depreciation

Accounting EstimatesAccounting Estimates

3-32

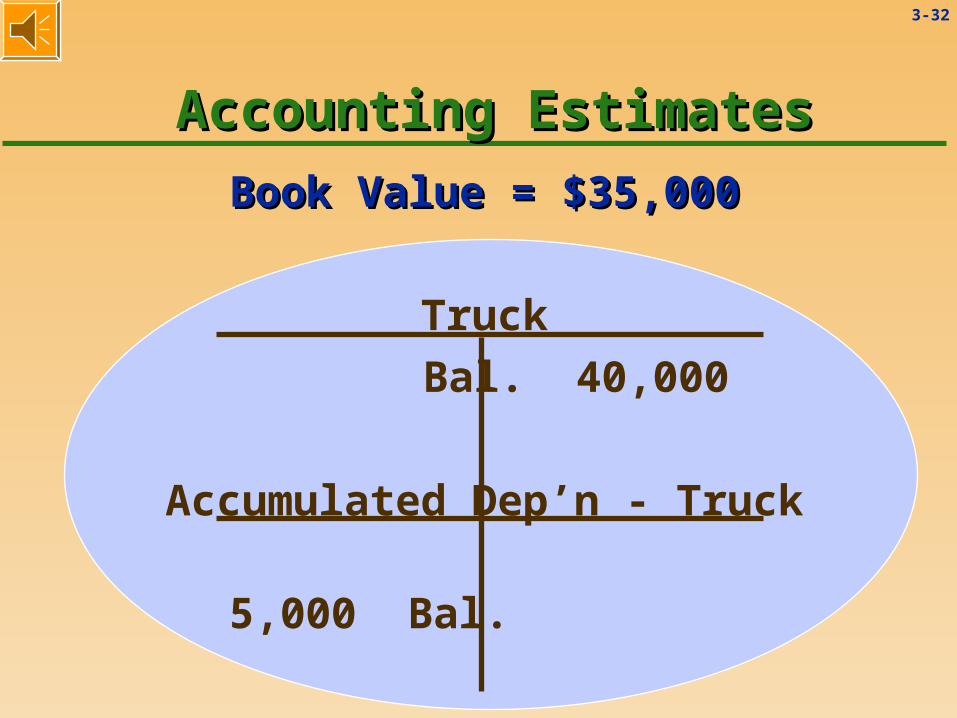

Book Value = $35,000Book Value = $35,000

Truck

Bal. 40,000

Accumulated Dep’n - Truck

5,000 Bal.

Accounting EstimatesAccounting Estimates

3-33

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

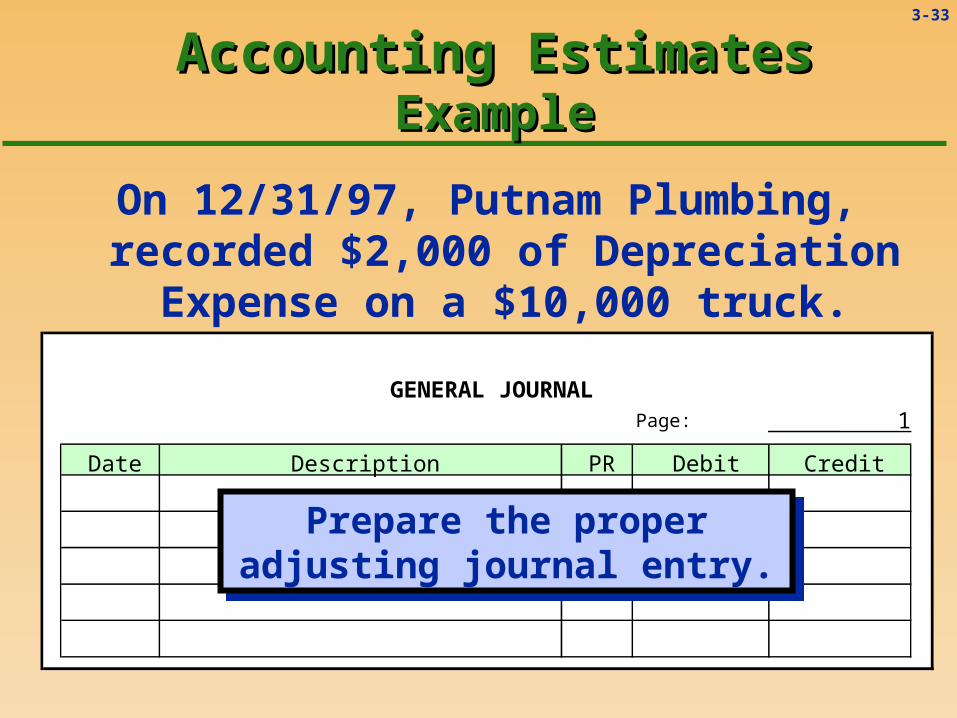

Accounting EstimatesAccounting EstimatesExampleExample

On 12/31/97, Putnam Plumbing, recorded $2,000 of Depreciation Expense on a

$10,000 truck.

Prepare the proper adjusting journal entry.

Prepare the proper adjusting journal entry.

3-34

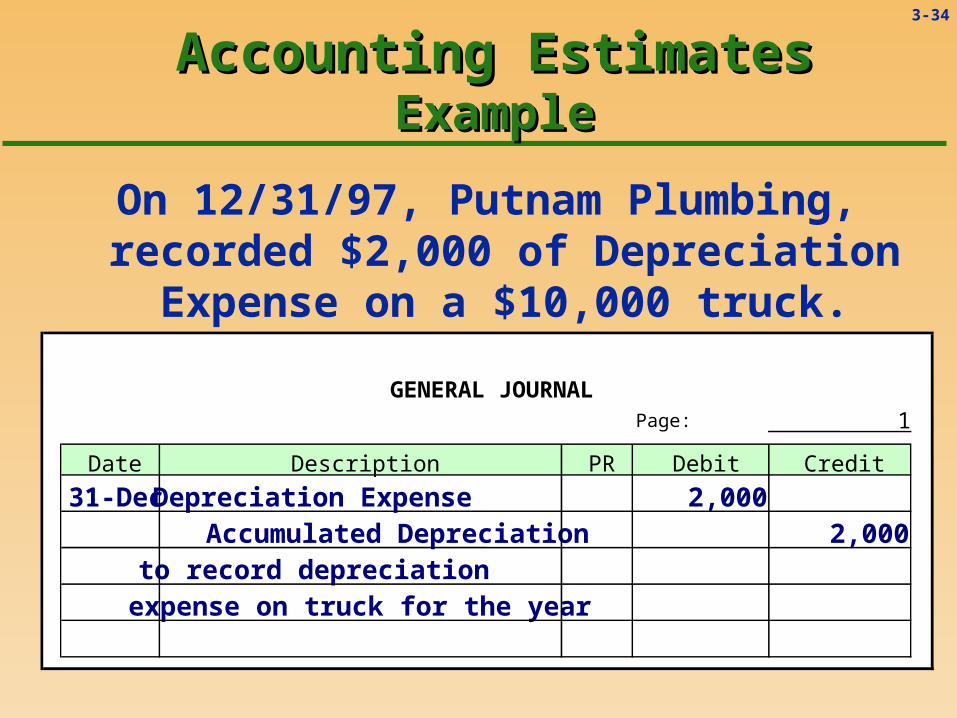

On 12/31/97, Putnam Plumbing, recorded $2,000 of Depreciation Expense on a

$10,000 truck.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

31-Dec Depreciation Expense 2,000 Accumulated Depreciation 2,000to record depreciationexpense on truck for the year

Accounting EstimatesAccounting EstimatesExampleExample

3-35

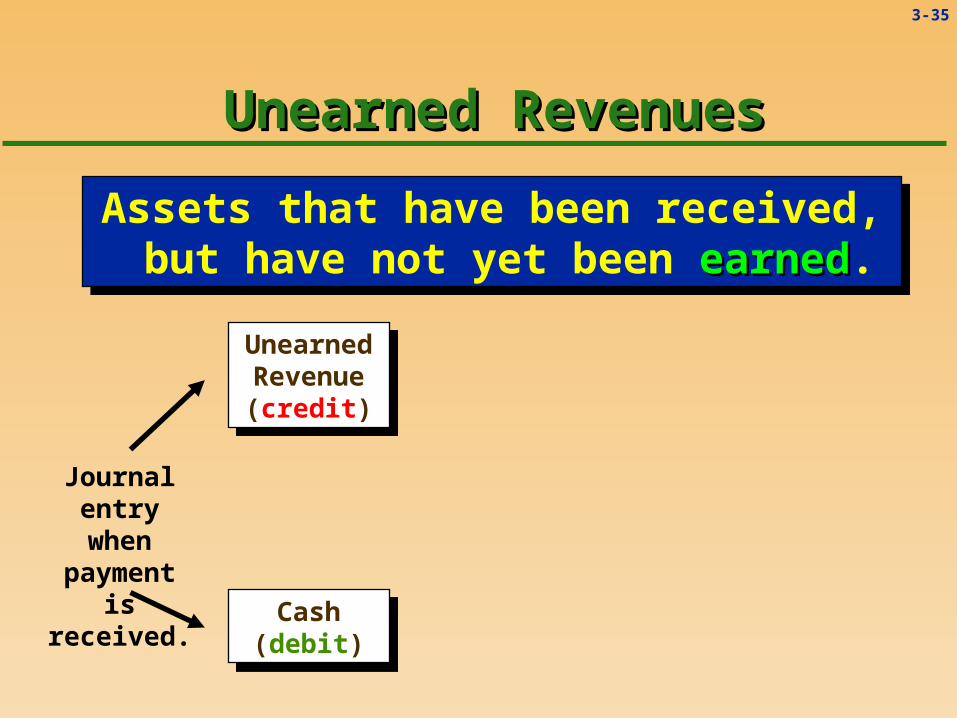

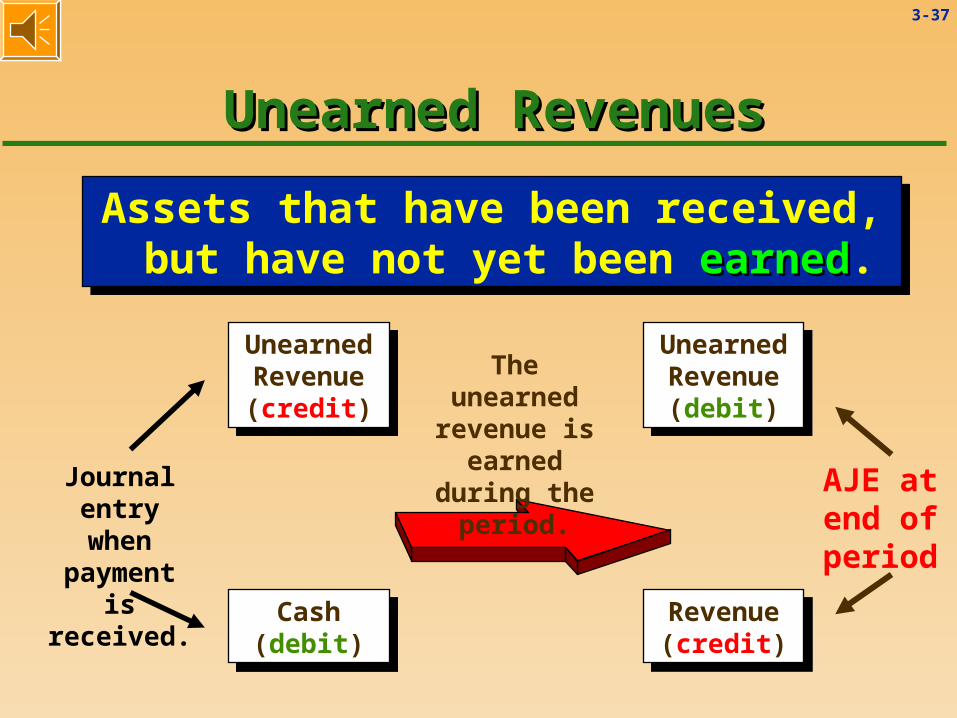

Unearned RevenuesUnearned Revenues

Cash (debit)

Cash (debit)

Unearned Revenue (credit)

Unearned Revenue (credit)

Journal entry when payment is received.

Assets that have been received, but have not yet been earnedearned.

Assets that have been received, but have not yet been earnedearned.

3-36

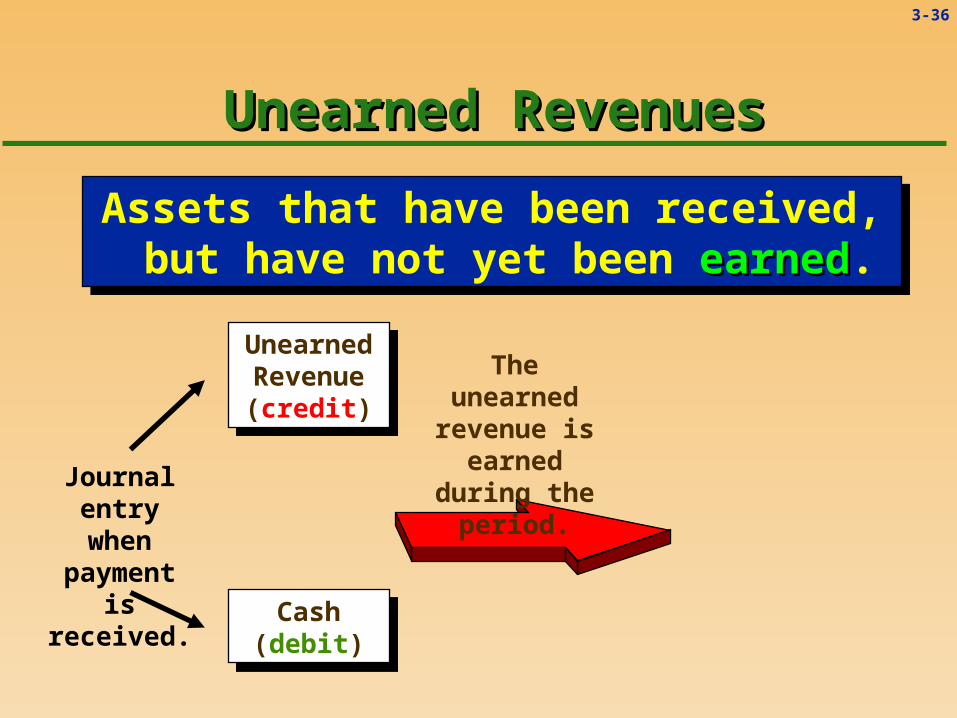

Unearned RevenuesUnearned Revenues

Cash (debit)

Cash (debit)

Unearned Revenue (credit)

Unearned Revenue (credit)

Assets that have been received, but have not yet been earnedearned.

Assets that have been received, but have not yet been earnedearned.

The unearned revenue is

earned during the period.

Journal entry when payment is received.

3-37

Revenue (credit)

Revenue (credit)

Unearned Revenue

(debit)

Unearned Revenue

(debit)

Unearned RevenuesUnearned Revenues

Cash (debit)

Cash (debit)

Unearned Revenue (credit)

Unearned Revenue (credit)

Assets that have been received, but have not yet been earnedearned.

Assets that have been received, but have not yet been earnedearned.

The unearned revenue is

earned during the period.

AJE at end of period

Journal entry when payment is received.

3-38

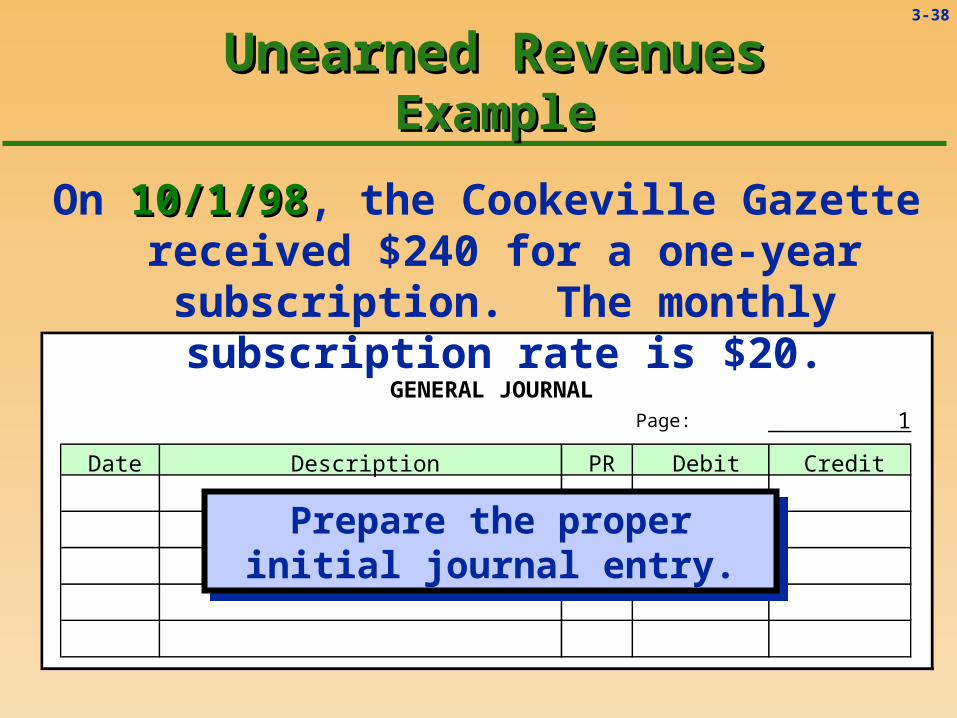

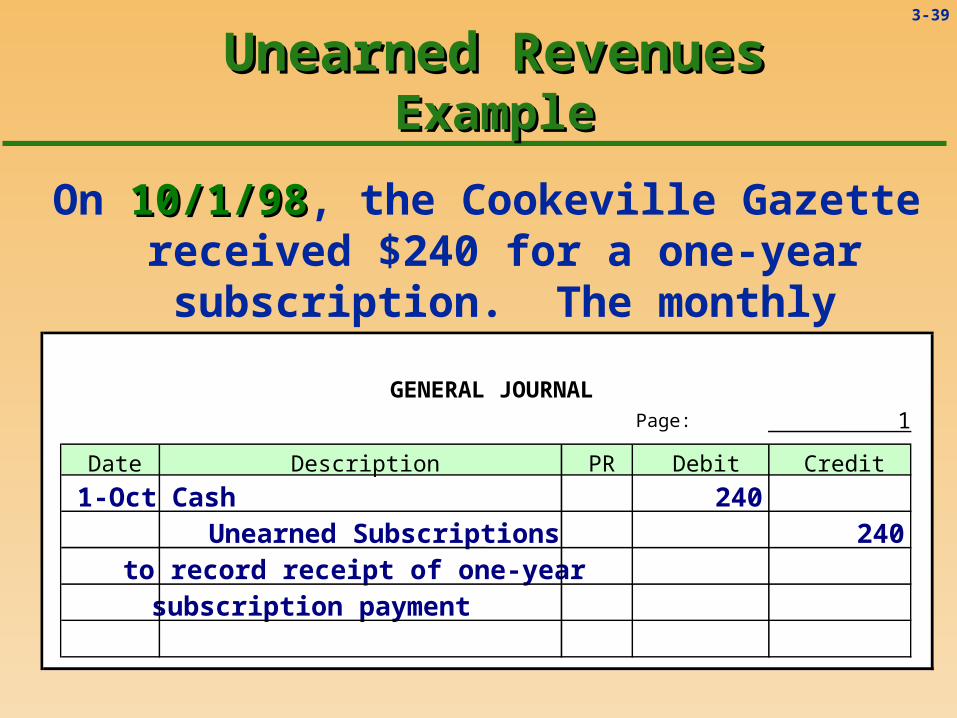

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

Unearned RevenuesUnearned RevenuesExampleExample

On 10/1/9810/1/98, the Cookeville Gazette received $240 for a one-year subscription. The

monthly subscription rate is $20.

Prepare the proper initial journal entry.

Prepare the proper initial journal entry.

3-39

On 10/1/9810/1/98, the Cookeville Gazette received $240 for a one-year subscription. The

monthly subscription rate is $20.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

1-Oct Cash 240 Unearned Subscriptions 240to record receipt of one-yearsubscription payment

Unearned RevenuesUnearned RevenuesExampleExample

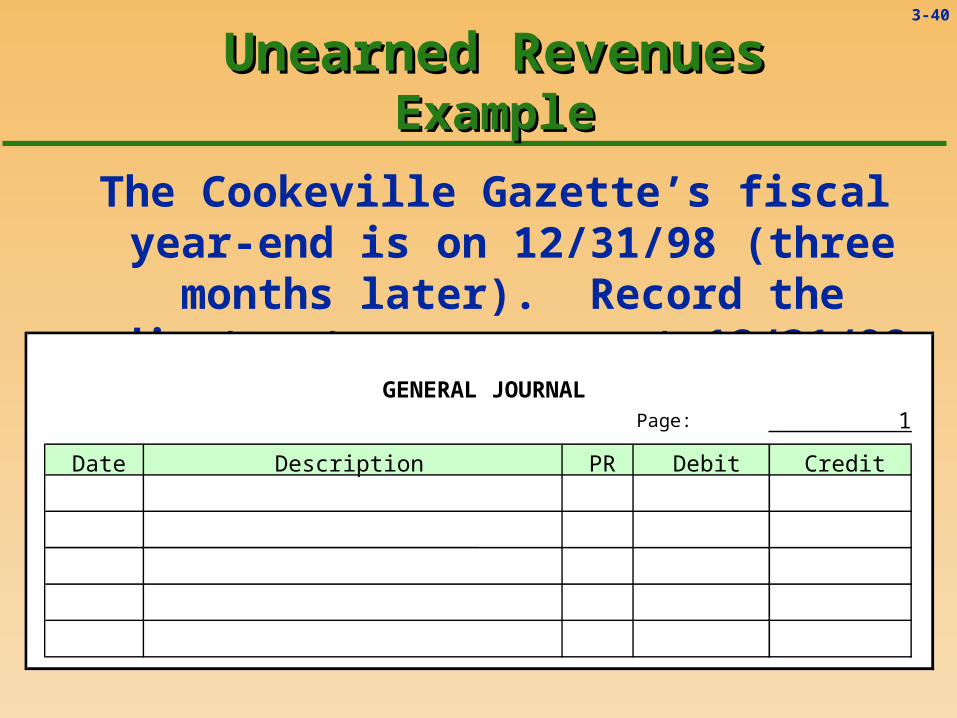

3-40

The Cookeville Gazette’s fiscal year-end is on 12/31/98 (three months later). Record

the adjustment necessary at 12/31/98.

Prepare the proper adjusting journal entry.

Prepare the proper adjusting journal entry.

Unearned RevenuesUnearned RevenuesExampleExample

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

3-41

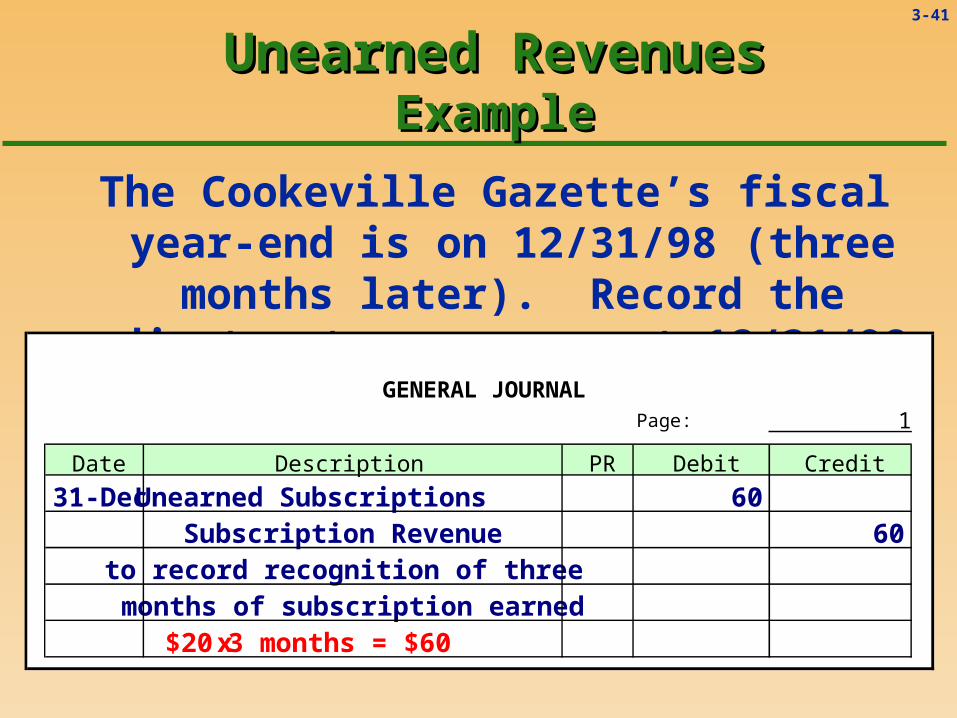

The Cookeville Gazette’s fiscal year-end is on 12/31/98 (three months later). Record

the adjustment necessary at 12/31/98.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

31-Dec Unearned Subscriptions 60 Subscription Revenue 60to record recognition of threemonths of subscription earned $20x3 months = $60

Unearned RevenuesUnearned RevenuesExampleExample

3-42

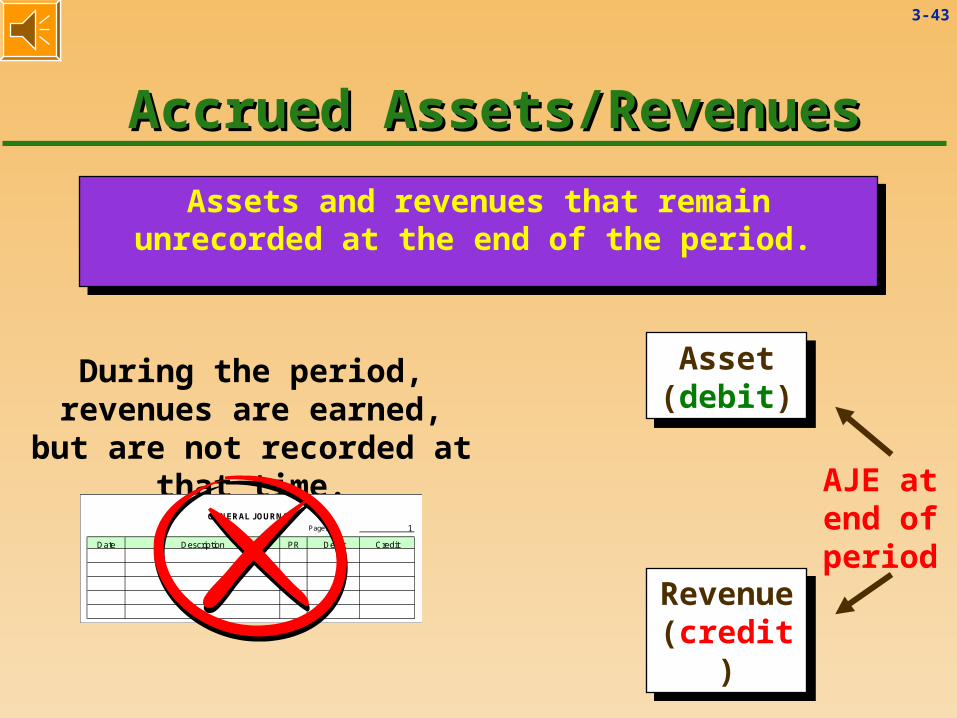

Accrued Assets/RevenuesAccrued Assets/Revenues

Assets and revenues that remain unrecorded at the end of the period. Assets and revenues that remain

unrecorded at the end of the period.

During the period, revenues are earned, but are not recorded at that time.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

3-43

Accrued Assets/RevenuesAccrued Assets/Revenues

Revenue (credit)

Revenue (credit)

Asset (debit)

Asset (debit)

During the period, revenues are earned, but are not recorded at that time.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

AJE at end of period

Assets and revenues that remain unrecorded at the end of the period. Assets and revenues that remain

unrecorded at the end of the period.

3-44

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

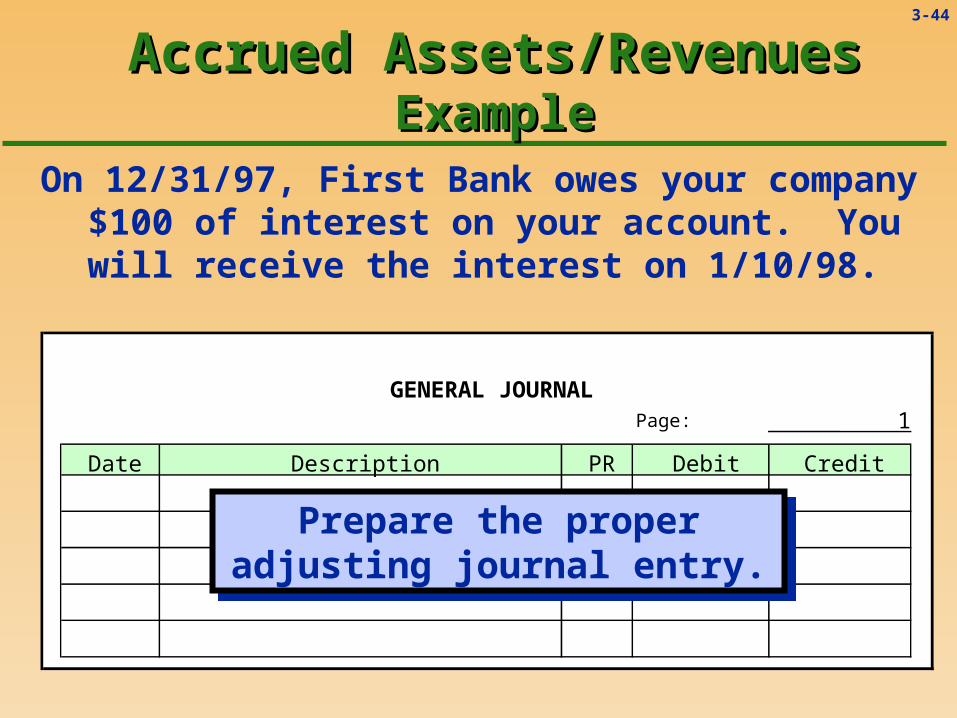

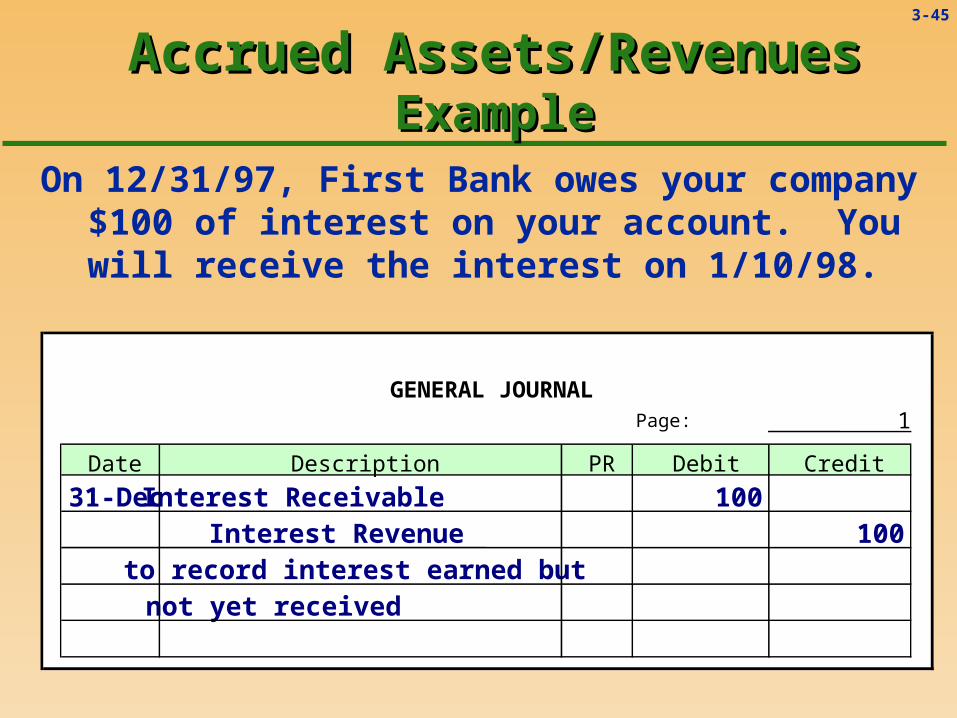

Accrued Assets/RevenuesAccrued Assets/RevenuesExampleExample

On 12/31/97, First Bank owes your company $100 of interest on your account. You will

receive the interest on 1/10/98.

Prepare the proper adjusting journal entry.

Prepare the proper adjusting journal entry.

3-45

Accrued Assets/RevenuesAccrued Assets/RevenuesExampleExample

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

31-Dec Interest Receivable 100 Interest Revenue 100to record interest earned butnot yet received

On 12/31/97, First Bank owes your company $100 of interest on your account. You will

receive the interest on 1/10/98.

3-46

Accrued Liabilities/ExpensesAccrued Liabilities/Expenses

Liabilities and expenses that remain unrecorded at the end of the period.

Liabilities and expenses that remain unrecorded at the end of the period.

During the period, expenses are incurred, but are not

recorded at that time.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

3-47

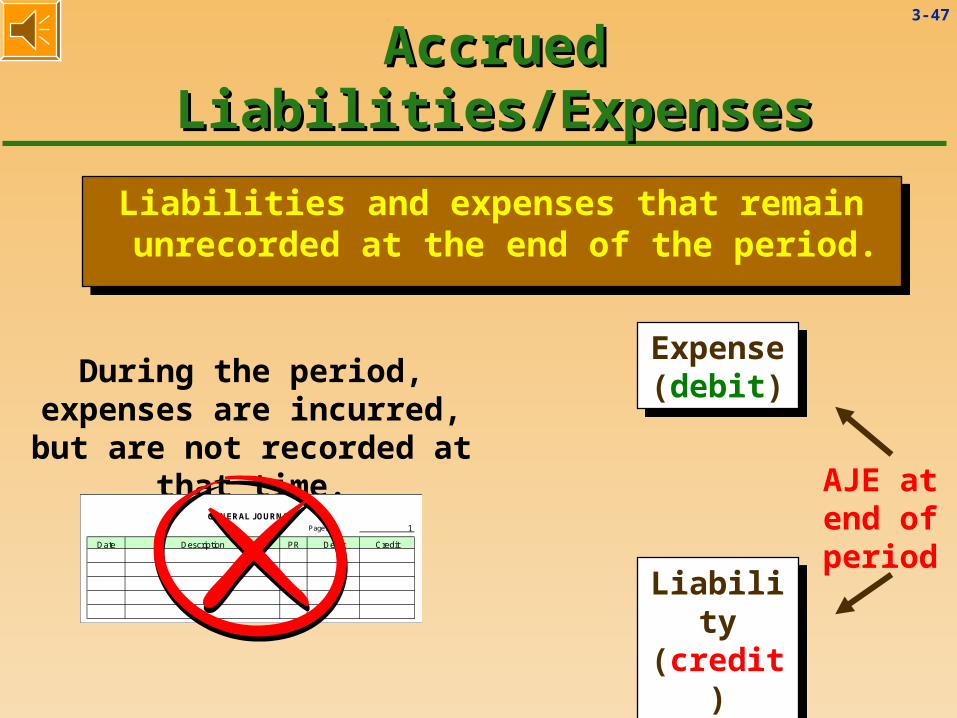

Accrued Liabilities/ExpensesAccrued Liabilities/Expenses

Liabilities and expenses that remain unrecorded at the end of the period.

Liabilities and expenses that remain unrecorded at the end of the period.

Liability (credit)

Liability (credit)

Expense(debit)

Expense(debit)During the period, expenses

are incurred, but are not recorded at that time.

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

AJE at end of period

3-48

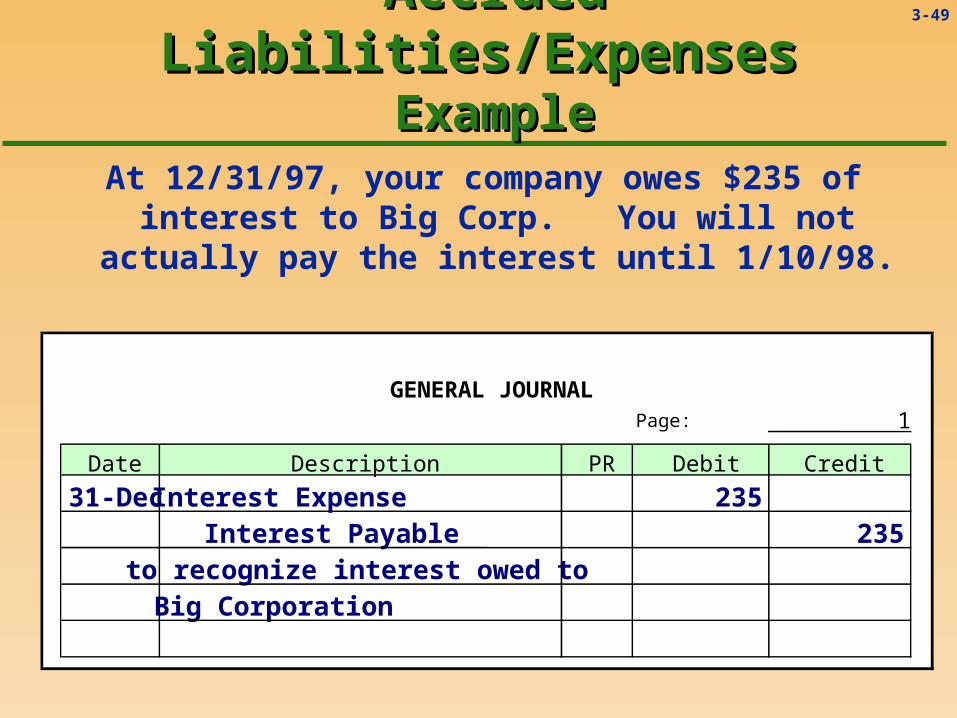

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

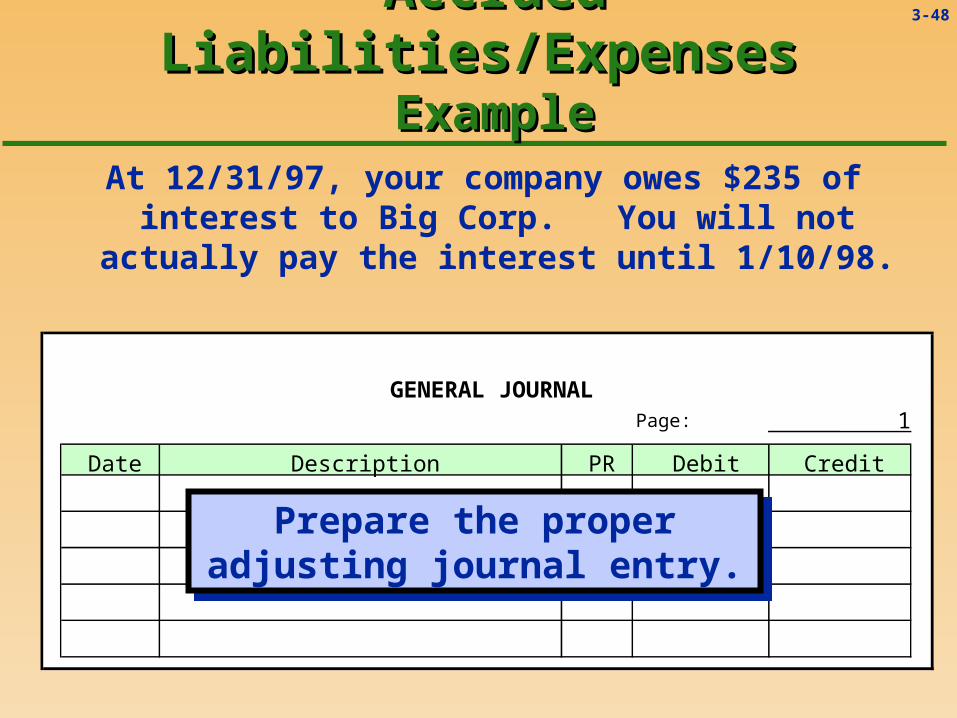

Accrued Liabilities/Expenses Accrued Liabilities/Expenses ExampleExample

At 12/31/97, your company owes $235 of interest to Big Corp. You will not

actually pay the interest until 1/10/98.

Prepare the proper adjusting journal entry.

Prepare the proper adjusting journal entry.

3-49

Accrued Liabilities/Expenses Accrued Liabilities/Expenses ExampleExample

GENERAL JOURNALPage: 1

Date Description PR Debit Credit

31-Dec Interest Expense 235 Interest Payable 235to recognize interest owed toBig Corporation

At 12/31/97, your company owes $235 of interest to Big Corp. You will not

actually pay the interest until 1/10/98.

3-50

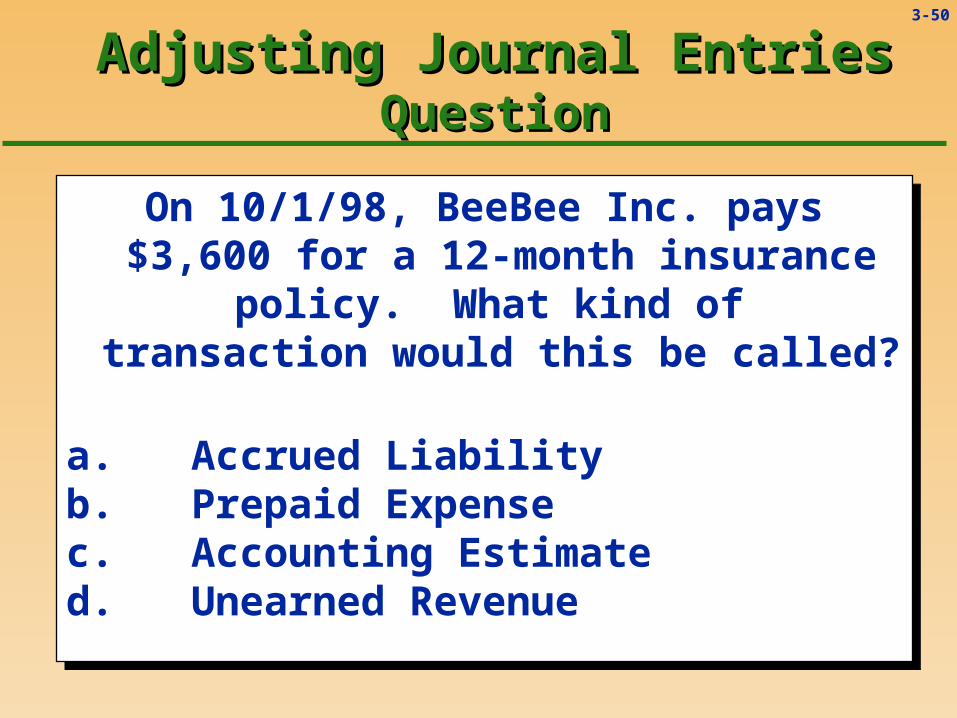

Adjusting Journal EntriesAdjusting Journal EntriesQuestionQuestion

On 10/1/98, BeeBee Inc. pays $3,600 for a 12-month insurance policy. What kind of transaction would this be called?

a. Accrued Liabilityb. Prepaid Expensec. Accounting Estimated. Unearned Revenue

On 10/1/98, BeeBee Inc. pays $3,600 for a 12-month insurance policy. What kind of transaction would this be called?

a. Accrued Liabilityb. Prepaid Expensec. Accounting Estimated. Unearned Revenue

3-51

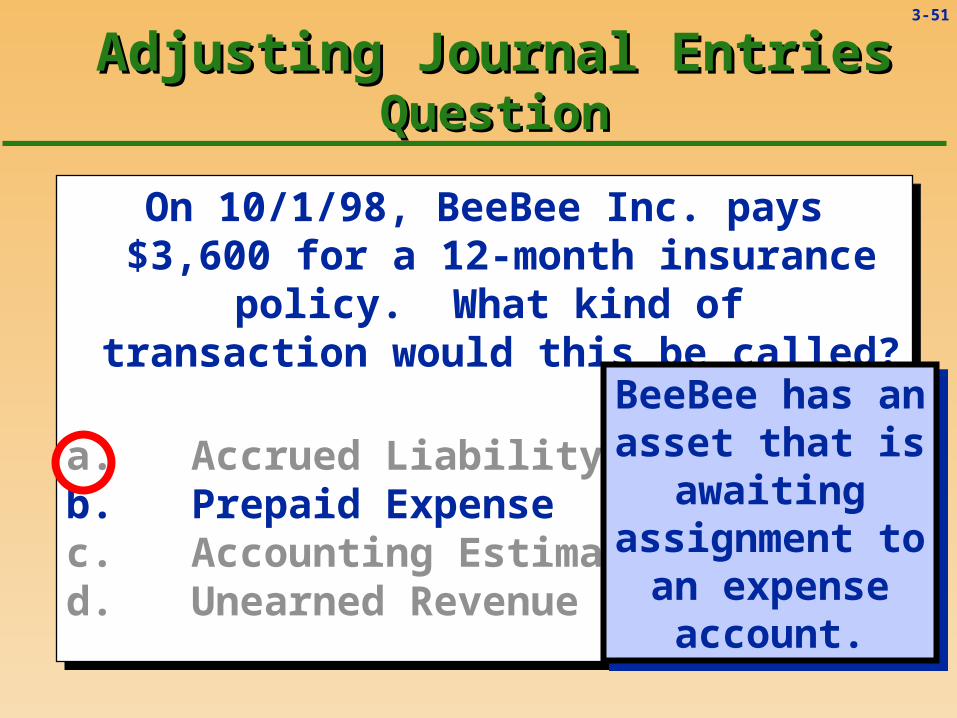

Adjusting Journal EntriesAdjusting Journal EntriesQuestionQuestion

On 10/1/98, BeeBee Inc. pays $3,600 for a 12-month insurance policy. What kind of transaction would this be called?

a. Accrued Liabilityb. Prepaid Expensec. Accounting Estimated. Unearned Revenue

On 10/1/98, BeeBee Inc. pays $3,600 for a 12-month insurance policy. What kind of transaction would this be called?

a. Accrued Liabilityb. Prepaid Expensec. Accounting Estimated. Unearned Revenue

BeeBee has an asset that is

awaiting assignment to

an expense account.

BeeBee has an asset that is

awaiting assignment to

an expense account.

3-52

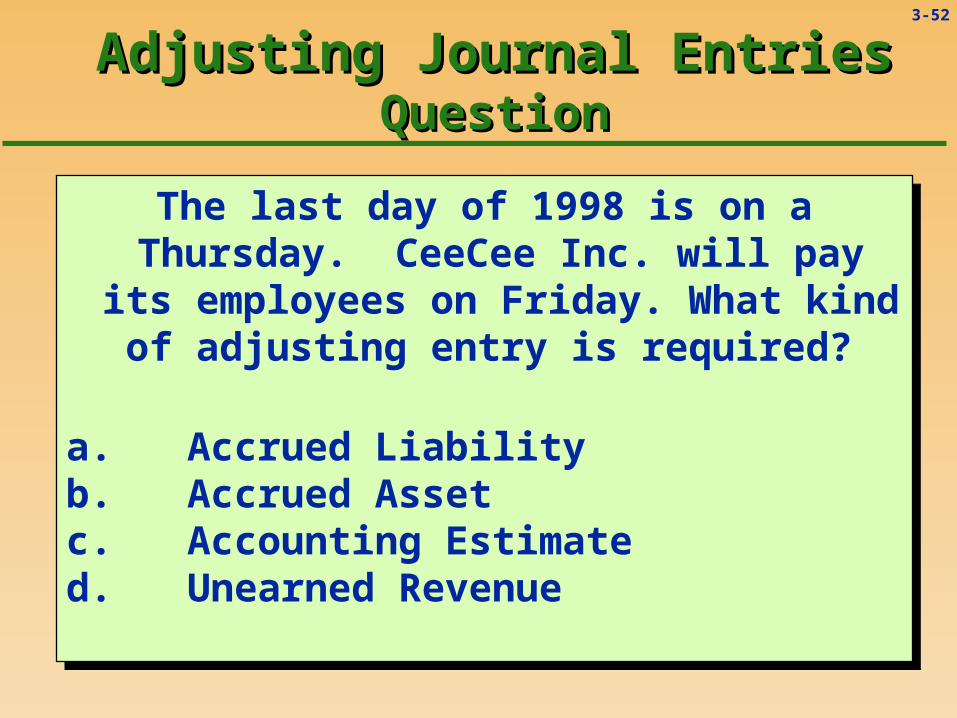

Adjusting Journal EntriesAdjusting Journal EntriesQuestionQuestion

The last day of 1998 is on a Thursday. CeeCee Inc. will pay its employees on Friday. What kind of adjusting entry is

required?

a. Accrued Liabilityb. Accrued Assetc. Accounting Estimated. Unearned Revenue

The last day of 1998 is on a Thursday. CeeCee Inc. will pay its employees on Friday. What kind of adjusting entry is

required?

a. Accrued Liabilityb. Accrued Assetc. Accounting Estimated. Unearned Revenue

3-53

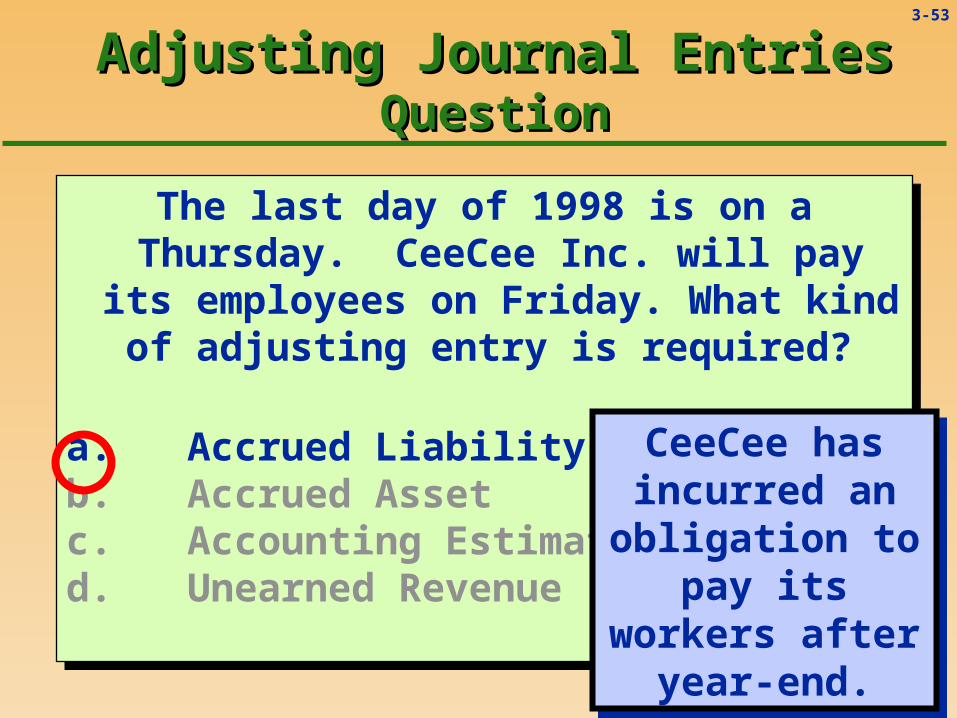

Adjusting Journal EntriesAdjusting Journal EntriesQuestionQuestion

The last day of 1998 is on a Thursday. CeeCee Inc. will pay its employees on Friday. What kind of adjusting entry is

required?

a. Accrued Liabilityb. Accrued Assetc. Accounting Estimated. Unearned Revenue

The last day of 1998 is on a Thursday. CeeCee Inc. will pay its employees on Friday. What kind of adjusting entry is

required?

a. Accrued Liabilityb. Accrued Assetc. Accounting Estimated. Unearned Revenue

CeeCee has incurred an

obligation to pay its workers after

year-end.

CeeCee has incurred an

obligation to pay its workers after

year-end.

3-54

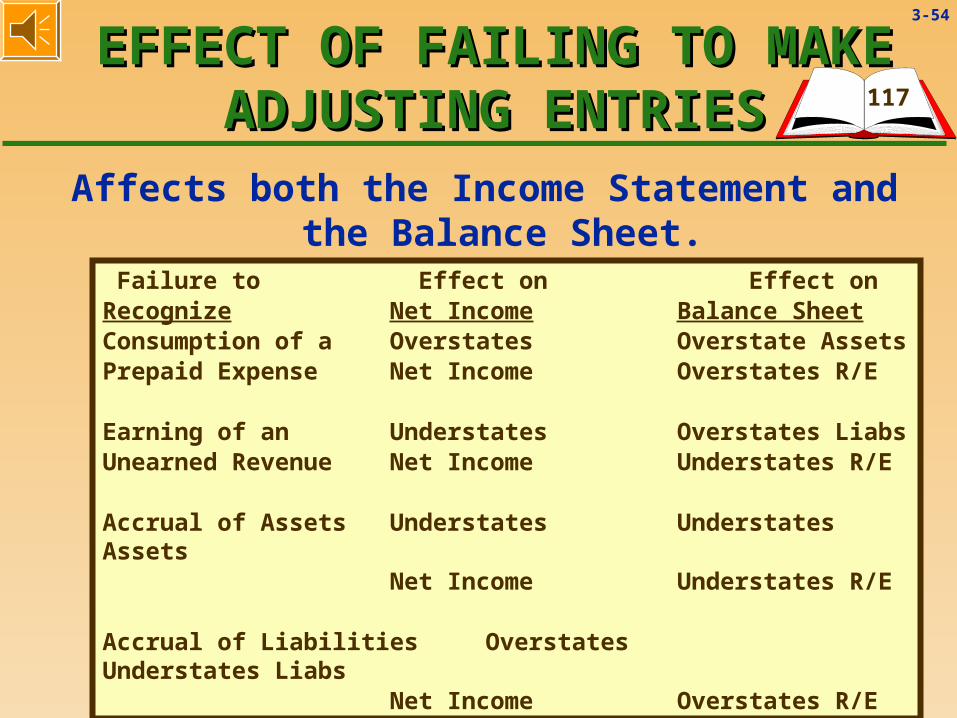

EFFECT OF FAILING TO MAKE EFFECT OF FAILING TO MAKE ADJUSTING ENTRIESADJUSTING ENTRIES

Affects both the Income Statement and the Balance Sheet.

Failure to Effect on Effect onRecognize Net Income Balance SheetConsumption of a Overstates Overstate Assets Prepaid Expense Net Income Overstates R/E

Earning of an Understates Overstates LiabsUnearned Revenue Net Income Understates R/E

Accrual of Assets Understates Understates AssetsNet Income Understates R/E

Accrual of Liabilities Overstates Understates LiabsNet Income Overstates R/E

117

3-55

ROLL ‘EM !ROLL ‘EM !

Video #1(Approx. 8 min.)

Video #2(Approx. 6 min.)

Video #3(Approx. 8 min.)

Video #4(Approx. 6 min.)

3-56

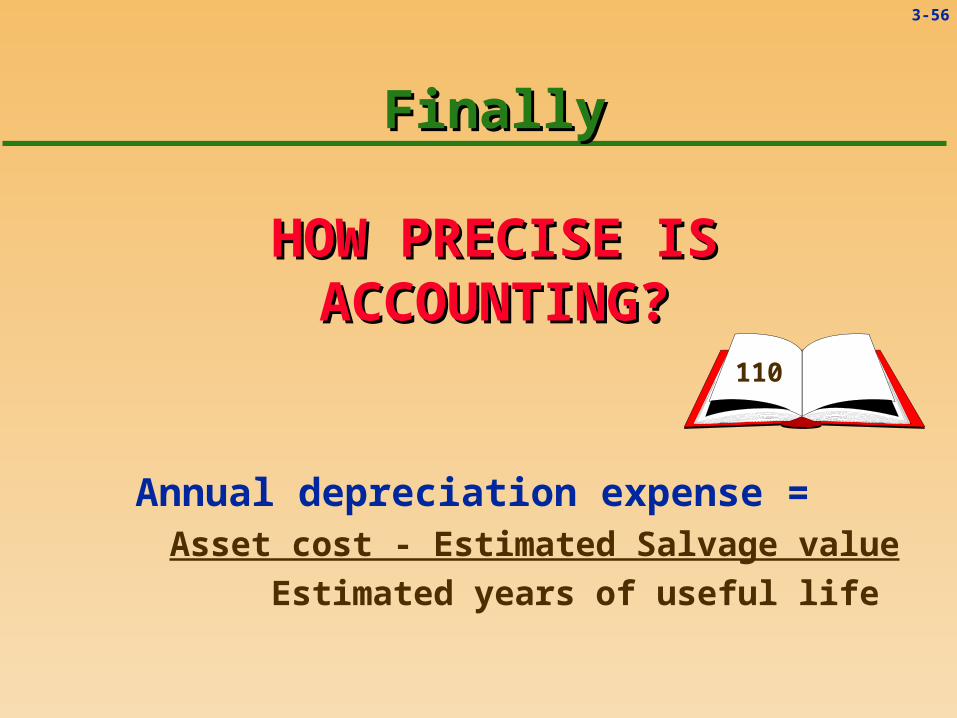

FinallyFinally

110

Annual depreciation expense = Asset cost - Estimated Salvage value

Estimated years of useful life

HOW PRECISE IS HOW PRECISE IS ACCOUNTING?ACCOUNTING?

3-57

FinallyFinally

110

EstimatedEstimated^ Annual depreciation expense =

Asset cost - EstimatedEstimated Salvage value

EstimatedEstimated years of useful life

HOW PRECISE IS HOW PRECISE IS ACCOUNTING?ACCOUNTING?

3-58

Why would anyone want to make a CRUDE journal entry?

Crude Attempt at HumorCrude Attempt at Humor