Embed Size (px)

Citation preview

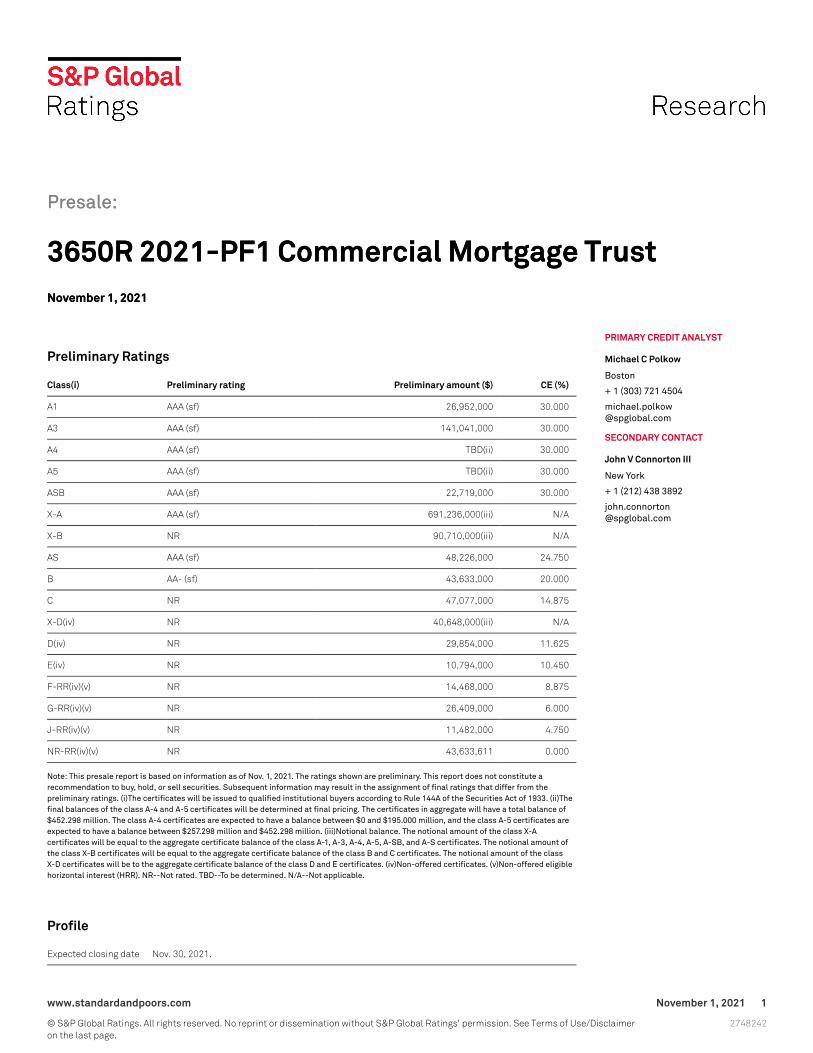

Presale:

3650R 2021-PF1 Commercial Mortgage TrustNovember 1, 2021

Preliminary Ratings

Class(i) Preliminary rating Preliminary amount ($) CE (%)

A1 AAA (sf) 26,952,000 30.000

A3 AAA (sf) 141,041,000 30.000

A4 AAA (sf) TBD(ii) 30.000

A5 AAA (sf) TBD(ii) 30.000

ASB AAA (sf) 22,719,000 30.000

X-A AAA (sf) 691,236,000(iii) N/A

X-B NR 90,710,000(iii) N/A

AS AAA (sf) 48,226,000 24.750

B AA- (sf) 43,633,000 20.000

C NR 47,077,000 14.875

X-D(iv) NR 40,648,000(iii) N/A

D(iv) NR 29,854,000 11.625

E(iv) NR 10,794,000 10.450

F-RR(iv)(v) NR 14,468,000 8.875

G-RR(iv)(v) NR 26,409,000 6.000

J-RR(iv)(v) NR 11,482,000 4.750

NR-RR(iv)(v) NR 43,633,611 0.000

Note: This presale report is based on information as of Nov. 1, 2021. The ratings shown are preliminary. This report does not constitute arecommendation to buy, hold, or sell securities. Subsequent information may result in the assignment of final ratings that differ from thepreliminary ratings. (i)The certificates will be issued to qualified institutional buyers according to Rule 144A of the Securities Act of 1933. (ii)Thefinal balances of the class A-4 and A-5 certificates will be determined at final pricing. The certificates in aggregate will have a total balance of$452.298 million. The class A-4 certificates are expected to have a balance between $0 and $195.000 million, and the class A-5 certificates areexpected to have a balance between $257.298 million and $452.298 million. (iii)Notional balance. The notional amount of the class X-Acertificates will be equal to the aggregate certificate balance of the class A-1, A-3, A-4, A-5, A-SB, and A-S certificates. The notional amount ofthe class X-B certificates will be equal to the aggregate certificate balance of the class B and C certificates. The notional amount of the classX-D certificates will be to the aggregate certificate balance of the class D and E certificates. (iv)Non-offered certificates. (v)Non-offered eligiblehorizontal interest (HRR). NR--Not rated. TBD--To be determined. N/A--Not applicable.

Profile

Expected closing date Nov. 30, 2021.

Presale:

3650R 2021-PF1 Commercial Mortgage TrustNovember 1, 2021

PRIMARY CREDIT ANALYST

Michael C Polkow

Boston

+ 1 (303) 721 4504

SECONDARY CONTACT

John V Connorton III

New York

+ 1 (212) 438 3892

www.standardandpoors.com November 1, 2021 1

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Profile (cont.)

Collateral Thirty-five commercial mortgage loans with an aggregate principal balance of $918.587 million(approximately $781.946 million of offered certificates), secured by the fee and leasehold interestsin 42 properties across 17 states.

S&P Global Ratingspooled trust LTV

102.2% (based on S&P Global Ratings' NCF and weighted average capitalization rate of 7.52%).

S&P Global Ratingspooled trust DSC

2.10x (based on S&P Global Ratings' NCF and the actual debt service payable on the mortgageloans and, for the partial-term interest-only loans, the debt service due when the interest-onlyperiod expires).

S&P Global Ratingspooled trust debt yield

7.79% (based on S&P Global Ratings' NCF and the loan balances for the mortgage loans).

Payment structure The transaction is structured to comply with risk retention requirements by way of an eligiblehorizontal risk retention structure, which includes the class F-RR, G-RR, J-RR, and NR-RRcertificates, collectively the HRR certificates. The total required credit risk retention percentage forthis transaction is 5.0%. On each distribution date, interest accrued for each class of certificates atthe applicable pass-through rate will be distributed in the following priority, if funds are available:to the class A-1, A-3, A-4, A-5, A-SB, X-A, X-B, and X-D certificates, pro rata, based on theirrespective entitlements to interest for that distribution date, and sequentially to the class A-S, B,C, D, E, F-RR, G-RR, and H-RR certificates, in that order, until interest payable to each class is paidin full. Principal payments on the certificates will be distributed to the class A-SB certificates untilthe balance is reduced to the planned principal balance for that distribution date, and thensequentially to the class A-1, A-3, A-4, A-5, A-SB, A-S, B, C, D, E, F-RR, G-RR, and J-RR certificatesuntil each class' balance is reduced to zero. If the class A-S through J-RR certificates' total balancehas been reduced to zero, principal payments on the certificates will be distributed to the classA-1, A-3, A-4, A-5, and A-SB certificates, pro rata, based on each class' certificate balance. Losseswill be allocated to each class of certificates in reverse alphabetical order starting with the classJ-RR certificates through and including the class A-S certificates, and then to the class A-1, A-3,A-4, A-5, and A-SB certificates, pro rata, based on each class' certificate balance.

Depositor 3650 REIT Commercial Mortgage Securities II LLC.

Mortgage loan sellersand sponsors

3650 Real Estate Investment Trust 2 LLC, Citi Real Estate Funding Inc., and German AmericanCapital Corp.

Master servicer Midland Loan Services, a Division of PNC Bank N.A.

Special servicer 3650 REIT Loan Servicing LLC.

Trustee and certificateadministrator

Wells Fargo Bank N.A.

LTV--Loan-to-value ratio, which is based on S&P Global Ratings' values. DSC--Debt service coverage. NCF--Net cash flow. TBD--To bedetermined.

Rationale

The preliminary ratings assigned to the 3650R 2021-PF1 Commercial Mortgage Trust'scommercial mortgage pass-through certificates reflect the credit support provided by thetransaction's structure, our view of the underlying collateral's economics, the trustee-providedliquidity, the collateral pool's relative diversity, and our overall qualitative assessment of thetransaction. S&P Global Ratings determined that the collateral pool has, on a weighted averagebasis, debt service coverage (DSC) of 2.10x and beginning and ending loan-to-value (LTV) ratios of102.2% and 98.7%, respectively, based on our values.

www.standardandpoors.com November 1, 2021 2

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Environmental, Social, And Governance (ESG) Factors

Our rating analysis considers a transaction's potential exposure to ESG credit factors. For CMBS,we view the exposure to environmental credit factors as above average, social credit factors asaverage, and governance credit factors as average (see "ESG Industry Report Card: CommercialMortgage-Backed Securities," published March 31, 2021). The sector's above-average exposure toenvironmental credit factors reflect environmental risks, such as physical climate and pollution.These risks can have serious and material effects on the value of the underlying commercial realestate backing the rated certificates--especially since CMBS pools are generally moreconcentrated than other highly diversified asset classes in structured finance.

The transaction's exposure to environmental credit factors is in line with our sector benchmark, inour view. Our analysis of the underlying real estate we examined in the loan pool included a reviewof third-party appraisal(s), environmental site, property condition, and seismic risk assessments(when located in a high hazard earthquake zone). We also reviewed the underlying loandocumentation or a sample of the largest loans in the loan pool in conduit transactions. Inparticular, we looked at the property insurance requirements, the loan covenants requiringborrower(s) to maintain the real estate in good condition and appropriately address any exposureto environmental conditions, and any other available loan features we deemed relevant (e.g.,environmental indemnity, third-party environmental guarantee, and specific cash reserve). Wealso reviewed the disclosed exceptions to the seller's representations and warranties to identifyany other significant unmitigated environmental credit factors present in the smaller loans, ifapplicable.

Our review concluded that environmental credit factors are not key rating drivers in thistransaction because these risks were adequately addressed. While the progressivedecarbonization of the real estate sector by 2050 is expected to influence market values over time,we believe our current approach to evaluating stressed long-term recovery values indirectlyaccounts for the potential materialization of that pricing differentiation over the expected life ofthe transaction. In addition, our analysis does not give credit to any future actions that landlordsand tenants may take to reduce their carbon footprint to support a healthier environment andpreserve property value. As a result, we have not separately identified this as a material ESG creditfactor in our analysis.

The transaction's exposure to social and governance credit factors is in line with our sectorbenchmark, in our view.

Transaction Overview

The chart shows an overview of the transaction's structure, cash flows, and other considerations.

www.standardandpoors.com November 1, 2021 3

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Strengths

The transaction exhibits the following strengths:

- The transaction has a strong weighted average S&P Global Ratings' DSC of 2.10x based onactual debt service and, for the partial-term interest-only loans, the debt service due when theinterest-only period expires. Nevertheless, the prevailing low interest rate environmentinfluences this DSC, and any increase in interest rates could affect the loans' ability torefinance at maturity. Our DSCs for the pool range from 1.15x-7.12x.

- The pool is geographically diverse, with 42 properties spread across 17 states. The largestconcentration is in California (nine properties, 30.9% of the pooled trust balance), followed byNew York (eight properties, 21.2%) and Massachusetts (one properties, 8.5%). No other stateaccounts for more than 5.4% of the pooled trust balance.

www.standardandpoors.com November 1, 2021 4

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

- The transaction has a strong concentration of properties in primary markets, specifically withinrelatively strong metropolitan statistical areas (MSAs), including Los Angeles, New York, andSan Jose, Calfi.. Of the pooled trust balance, 68.8% is located in primary markets (as defined byS&P Global Ratings) and 15.7% in secondary markets. The remaining 15.6% of the pool islocated in tertiary markets.

- The loan pool has a relatively diverse mix of property types, as categorized by S&P GlobalRatings. Of the pooled trust balance, 26.7% is backed by office properties, 23% by multifamilyproperties, 21.8% by retail properties, 16.9% by mixed-use properties, 8.6% by industrialproperties, 2.2% by other properties, and 0.9% by self-storage properties. There are no lodgingproperties in the pool.

- All of the pool's loan borrowers are structured as special-purpose entities (SPEs). Thirty-two ofthe loans (94.7%) provided lenders with non-consolidation opinions, including all of the top 10loans. Thirty-three loans (96.9%) have borrowers that are structured with at least oneindependent director.

- Twenty-seven of the loans (79.8% of the pooled trust balance) have some form of lockbox: 15loans (58.3%) are structured with a hard lockbox, 10 loans (16.7%) with springing lockboxes,and two loans (4.8%) have a hard in-place lockbox for commercial tenants and a soft in-placelockbox for residential tenants. Four loans (12.3%) have in-place cash management whiletwenty-three loans (67.5%) are structured with springing cash management. Eight loans(20.2%) have no cash management, and the same eight loans have no lockbox provisions.

- Eight loans (22.4% of the pooled trust balance) represent acquisition oracquisition/recapitalization financing. Although some of these loans have limited operatingdata due to their recent acquisition, these loans benefit from the recent equity contribution bytheir sponsors. The weighted average LTV ratio for these loans, based on the appraiser's "as is"value, was 52.8%, reflecting average equity contribution of 47.2% for these loans.

- Two loans (7.3% of the pooled trust balance) are secured by multiple properties, ranging fromthree to six properties, which may lessen their net cash flow (NCF) volatility. However, both ofthese loan portfolios include properties located within the same city or state, which limits theirgeographic diversification. Additionally, one of the loans (1.9%) allows for property releases,subject to various conditions, which may further reduce the benefit of the initial diversity.

Risk Considerations

We considered these risks when analyzing this transaction:

- While still elevated, U.S. CMBS delinquencies have declined in recent months after increasingin 2020 due to the economic slowdown resulting from the COVID-19 pandemic and theassociated containment efforts, including social distancing, restrictions on travel, andgovernment-mandated closures of certain businesses. Many lodging assets were closed oroperating at low occupancy levels, and certain tenants within retail assets stopped paying rentor requested rent relief due to closure or demand reductions. However, we note that there areno lodging assets in this pool. The COVID-19 pandemic and the responses to it have led to anincrease in unemployment levels and a reduction in consumer spending, which may alsoadversely impact multifamily, office, self-storage, and industrial properties. Multifamily andself-storage properties may be negatively affected if unemployment rates rise and disposableincome levels fall, or if there is a moratorium on evictions. Office properties may experiencefluctuations in occupancy as businesses adjust their plans in response to government actions

www.standardandpoors.com November 1, 2021 5

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

or if employers permit enhanced flexible work arrangements. The trust's exposure to retail isthrough 6 loans (23.9% of the pooled trust balance) that we discuss further below. According tothe issuer, all of the loans in the transaction whose first payment date has already occurred arecurrent on their debt service obligations. In some cases, borrowers may be in discussions withtenants that have requested lease modifications or rent relief. We selectively increased ourvacancy rate and/or capitalization rate assumptions on certain properties that we deemed tohave a higher risk for cash flow disruption.

- The transaction has high leverage, with a weighted average LTV ratio of 102.2% based on S&PGlobal Ratings' values. The LTV was one of the primary factors in S&P Global Ratings' derivationof credit enhancement levels for this transaction.

- The transaction is moderately diversified by loan balance, with an effective loan count (asmeasured by the Herfindahl-Hirschman Index) of 24.5. The 10 largest loans represent 53.5% ofthe pooled trust balance. More diversified transactions can be less susceptible to volatility indefault and loss rates due to their reduced exposure to loan-related event risk, such as leaserollover, tenant bankruptcy, or changes in local market conditions. The effective loan count wasone of the key factors in our derivation of credit enhancement for this transaction.

- Twenty-six loans (80.7% of the pooled trust balance) are interest-only for their entire loanterms, including eight of the top 10 loans (44.5%). The interest-only loans have a high weightedaverage S&P Global Ratings LTV ratio of 101.2%, and 13 loans (35.4% of the pooled trustbalance) have LTV ratios over 100%. Four loans (5.7%) have a partial interest-only period,including zero of the top 10 loans, and five loans in the pool (13.7%) are structured asamortizing loans. The transaction is scheduled to amortize 5.5% through maturity. S&P GlobalRatings considered loan amortization characteristics when assigning credit enhancementlevels to the individual loans and the transaction.

- Six loans (23.9% of the pooled trust balance) are secured by retail assets. Four of these loans(16.9%) are anchored retail properties that are either grocery-anchored or shadow anchored bystrong retailers or grocers. One loan (4.90%) is anchored by a super-regional mall inWestchester, NY, and one loan (2.2%) is secured by a single tenant property leased to Cabelas.The U.S. retail sector has been facing numerous challenges over the past several years giventhe continued growth of e-commerce, increasing consumer price sensitivity due to stagnatingwage growth, and changing consumer tastes. These trends have resulted in declining sales,store closures, and smaller average store sizes for many national retailers. However,brick-and-mortar retail stores in well-situated class-A malls and within shopping centers, aswell as freestanding properties that are located in infill locations near major transportationnodes and in areas with strong demographic profiles, continue to prosper. Low supply growth inrecent years may help keep vacancy levels at their currently low levels and boost rent growth.Five of the six retail loans (21.7%) are secured by properties located in primary locations. Wevisited Plaza La Cienaga (5.4%; a mixed-use retail and medical office property in West LosAngeles), Venice Crossroads (4.9%; a grocery-anchored retail center in Los Angeles), TheWestchester (4.9%; a super-regional, luxury-oriented mall in White Plains, NY), and MarinaPacifica, a multi-tenant shopping center in Long Beach, Calif.). One retail loan (2.2% of thepooled trust balance) is secured by a property located in a tertiary location.

- Eight properties (29.7% of the pooled trust balance) are leased to a single tenant. Theseproperties can be susceptible to cash flow disruption if the tenant's business operations areadversely impacted or if the tenant fails to renew its lease. The largest of these is CX - 350 &450 Water Street (8.5%; Boston; office/lab/R&D properties that are 100% leased to Sanofi[AA/Stable/A-1+] through Nov. 30, 2036). Five of the single-tenant properties (25.1%) havelease terms that extend beyond the loan maturity date, while the leases for the remaining three

www.standardandpoors.com November 1, 2021 6

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

properties (4.6%) expire before loan maturity. Three of the properties (11.4%) are leased totenants that have investment-grade ratings ('BBB-' and above) from S&P Global Ratings.

- Eleven loans (47.3% of the pooled trust balance) do not have warm-body carve-out guarantors.In our view, this limitation generally lessens the disincentive provided by a typical nonrecoursecarve-out related to "bad boy" acts or voluntary bankruptcy.

- Eleven loans in the pool (45.5% of the pooled trust balance) have a pari passu component; threeloans, CX – 350 & 450 Water Street (8.5%), The Westchester (4.9%), and One SoHo Square(2.7%) have a subordinate first-mortgage loan component in addition to their senior trust andpari passu loan components (which were securitized in separate stand-alone transactions).Three loans (8.5%) have mezzanine debt. Our S&P Global Ratings loan-level recoverythresholds account for the presence of additional subordinate debt related to mezzanine debt,B-notes, and preferred equity, where applicable.

- The transaction documents include provisions for the transaction parties to seek rating agencyconfirmation (RAC) that certain actions will not result in a downgrade or withdrawal of thethen-current ratings on the securities. The definition of RAC in the transaction documentsincludes an option for the transaction parties to deem their RAC request satisfied if, afterhaving delivered a RAC request, the transaction parties have not received a response to therequest within a certain period of time. We believe it is possible for a situation to arise where anaction subject to a RAC request would cause us to downgrade the securities according to ourratings methodology, even though a RAC request is deemed to be satisfied pursuant to thisoption.

Pool Characteristics

Collateral description

The pool contains 35 loans that are secured by either a first-mortgage lien on the fee interest (32properties, 75.2% of the pooled trust balance), a leasehold interest (seven properties, 10.9%), or afee/leasehold interest (three properties, 13.9%). The top five and 10 loan concentrationsrepresent 31.5% and 53.5% of the pooled trust balance, respectively (see table 9 for a detaileddescription of the 10 largest loans in the pool).

Property type distribution

The top two property types in the pool are office assets, which account for 26.7% of the pooledtrust balance, and multifamily, which accounts for 23.0% (see table 1).

Table 1

Property Type Composition

Type(i)No. ofloans

Pooled trustbalance (mil. $)

% of pooled trustbalance

Weighted averageS&P LTV (%)

Weighted averageS&P DSC (x)

Multifamily 13 211.0 23.0 100.2 1.97

Office 6 193.5 21.1 106.6 2.08

Mixed-use 6 155.0 16.9 100.5 2.29

Retail anchored 4 155.0 16.9 92.6 2.20

www.standardandpoors.com November 1, 2021 7

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Table 1

Property Type Composition (cont.)

Type(i)No. ofloans

Pooled trustbalance (mil. $)

% of pooled trustbalance

Weighted averageS&P LTV (%)

Weighted averageS&P DSC (x)

Industrial 2 78.7 8.6 102.0 2.14

Medical office 1 52.0 5.7 130.8 1.91

Mall 1 45.0 4.9 105.8 1.93

Single tenant - nonIG

1 20.0 2.2 89.2 2.25

Self-storage 1 8.4 0.9 97.7 1.46

Total 35 918.6 100.0 102.2 2.10

(i)Based on S&P Global Ratings' classification. IG--Investment-grade.

Geographic distribution

The pool consists of properties that are located in 17 states. Of these properties, 60.5% (by pooledtrust balance) are located in three states: California, New York, and Massachusetts. The top fivestates represent 71.3% of the pooled trust balance.

As part of our property analysis, we classify the MSA in which each property is located as primary,secondary, or tertiary. Generally, primary markets have higher barriers to entry than secondaryand tertiary markets. The nature of each market type affects capitalization rates and valuationdynamics and can influence the timing and amount of liquidation proceeds if a mortgage loan isforeclosed. (See table 2 for the pool's distribution by state and market type.)

Table 2

Geographic Concentrations

Market type (%)

State Pooled trust balance (mil. $) No. of properties Primary Secondary Tertiary

California 283.7 9 89.4 6.9 3.6

New York 194.4 8 93.5 - 6.5

Massachusetts 77.9 1 100.0 - -

Alabama 49.8 6 - - 100.0

Florida 49.0 3 49.0 - 51.0

Louisiana 30.0 1 - 100.0 -

South Carolina 30.0 1 - 100.0 -

Texas 30.0 2 100.0 - -

Georgia 27.5 2 100.0 - -

Virginia 27.0 1 - 100.0 -

Other states - seven 119.4 8 30.8 31.1 38.1

Total 918.6 42 68.8 15.7 15.6

www.standardandpoors.com November 1, 2021 8

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Borrower concentration

The largest borrower sponsors in the pool are DivcoWest (Divco), California State Teachers'Retirement System, and Teacher Retirement System of Texas (co-sponsoring CX -350 & 450 WaterStreet; 8.5% of the pooled trust balance) and New Mountain Net Lease Corp. (50 Horseblock;6.4%).

Three groups of loans have related borrower-sponsors:

- Michael Pashaie, one of four sponsors for Rox San, which accounts for 5.7% of the pooled trustbalance, is also the sole sponsor for 477 Rodeo (1.5%) for a combined exposure of 7.2%.

- Gideon D. Levy is the sponsor for 93 East Apartments and PeachTree Plaza Apartments, whichaccount for 3.0% of the pooled trust balance combined.

- Dan M. Stauss, Lynn Stauss, and Scott Stauss are the sponsors for Carrington CourtApartments and Times Square Apartments, which account for 2.3% of the pooled trust balancecombined.

Single-tenant properties

There are eight properties across eight loans (29.7% of the pooled trust balance) that are leased toa single tenant. Five of these tenants associated with properties representing 25.1% of the pooledtrust balance have lease terms that exceed the loan maturity date. The remainder of theproperties have leases that expire before the loan matures (see table 3).

Table 3

Single-Tenant Properties

Property TenantTenant S&Prating

Pooled trustbalance (mil.

$)

% of pooledtrust

balance

Loanexpiration

date

Leaseexpiration

date

CX - 350 & 450Water Street

Sanofi AA/Stable 77.9 8.5 11/6/2031 11/30/2036

50 Horseblock Amneal PharmaceuticalsLLC

B/Stable 59.0 6.4 06/05/2031 6/30/2043

520 Almanor Nokia Corp. BB+/Stable 50.0 5.4 11/06/2031 6/30/2034

PetSmart HQ PetSmart Home OfficeInc.

B/Stable 23.0 2.5 04/05/2028 3/31/2032

Cabelas Cabela's NR 20.0 2.2 11/05/2031 5/31/2044

CAL OESPortfolio

California Governor'sOffice of EmergencyServices

AA-/Positive 19.7 2.1 10/06/2031 6/30/2029

Centene Centene NR 15.6 1.7 05/05/2031 11/30/2030

301 VoyagerWay

Northrop GrummanSystems Corp.

BBB+/Stable 7.3 0.8 08/06/2031 02/28/2023

Total - - 272.5 29.7 -

(i)Owner occupied space. NR--Not rated.

www.standardandpoors.com November 1, 2021 9

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Loan Characteristics

Loan type, origination date, term, and amortization

All of the loans in the pool pay a fixed interest rate and were originated between January 2020 andOctober 2021. The weighted average loan interest rate is 3.41%.

The original loan terms range from 84 to 120 months, with a weighted average original loan term of113.7 months. The weighted average remaining loan term is 110.2 months.

Twenty-six Loans (80.7% of the pooled trust balance) are interest only for the entire term and, ofthese, three loans (16.1%) are interest-only followed by an anticipated repayment date (ARD).Four loans (5.7% of pooled trust balance) are structured with partial interest-only periodsfollowed by a 360-month amortization scheduled. The partial interest-only loans have initialinterest-only periods ranging from 12 months to 60 months. Five loans (13.7%) have nointerest-only periods, and four (10.1%) of them amortize on a 360-month schedule while theremaining loan (Marina Pacifica, 3.6%) amortizes on a 120-month schedule. S&P Global Ratingsadjusted its analysis to reflect the various amortization terms and loan structures (see table 4).

Table 4

Loan Amortization

Loan typeNo. ofloans

% of poolbalance

S&P Global Ratings'DSC (x)

S&P Global Ratings' weighted averageLTV ratio (x)

Interest-only 26 80.7 2.28 101.20

Partial interest-only 4 5.7 1.28 107.00

Amortizing balloon 5 13.7 1.32 106.10

Fully amortizing - - - -

LTV--Loan to value. ARD--Anticipated repayment date. N/A--Not applicable.

Subordinated debt

Eleven loans in the pool (45.5% of the pooled trust balance) have a pari passu component (seetable 5); three loans, CX – 350 & 450 Water Street (8.5%), The Westchester (4.9%), and One SoHoSquare (2.7%) have a subordinate first-mortgage loan component in addition to their senior trustand pari passu loan components (which were securitized in separate stand-alone transactions).Three loans (8.5%) have mezzanine debt. Our S&P Global Ratings loan-level recovery thresholdsaccount for the presence of additional subordinate debt related to mezzanine debt, B-notes, andpreferred equity.

www.standardandpoors.com November 1, 2021 10

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Table 5

Loans With Existing Additional Debt

Property

Pooled trustbalance

(mil. $)

% of pooledtrust

balance

Paripassu

debt (mil.$)

Juniortrust note

(mil. $)(i)

B-notebalance

(mil. $)Mezzanine

balance (mil. $)

Totaldebt (mil.

$)

CX - 350 & 450 WaterStreet

77.9 8.5 736.1 411.0 - - 1225.0

520 Almanor 50.0 5.4 51.6 - - - 101.6

Plaza La Cienega 50.0 5.4 40.0 - - - 90.0

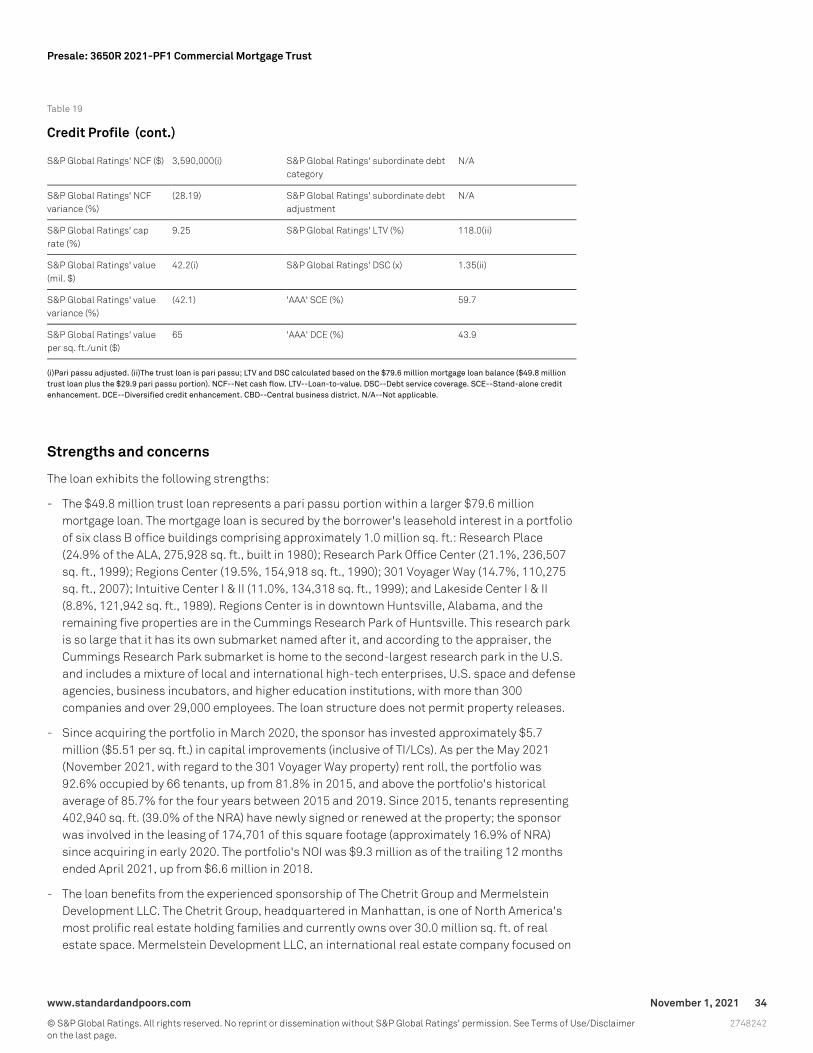

Huntsville OfficePortfolio

49.8 5.4 29.9 - - - 79.6

The Westchester 45.0 4.9 298.0 57.0 - - 400.0

Patewood CorporateCenter

30.0 3.3 38.5 - - 10.0 78.5

2 Washington 26.5 2.9 105.0 - - - 131.5

One SoHo Square 25.2 2.7 444.8 315.0 - 120.0 905.0

Icon One Daytona 25.0 2.7 25.0 - - - 50.0

PetSmart HQ 23.0 2.5 45.0 - - 12.0 80.0

Centene 15.6 1.7 31.2 - - - 46.8

(i)Securitized in separatestand-alonetransactions heldoutside of the trust.

Cross-collateralized and portfolio loans

Two loans (7.3% of the pooled trust balance) are secured by portfolios with multiple properties:the Huntsville Office Portfolio (5.4%; five multi-tenanted office properties and one single-tenantoffice property) and the Farrell Hampton Portfolio (1.9%; one mixed-use industrial/multifamilyproperty, one medical office property, and one office property). There are no cross-collateralizedand cross-defaulted loans in the pool.

Third-Party Review

We reviewed appraisal, environmental, engineering, and seismic reports on the properties weanalyzed, where applicable. All of these reports were completed within the past 12 months (seetable 6).

Ten properties (33.1% of the pooled trust balance) are located in seismic zones 3 or 4. None of theloans had an overall probable maximum loss (PML) percentage over 17%, a level below 20% PMLthreshold at which our criteria would require earthquake insurance to be in place.

www.standardandpoors.com November 1, 2021 11

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Table 6

Third-Party Review

Third-party reports No. of properties% of pooled trust

balance

Appraisal review within the past 12 months 42 100.0

Environmental review within the past 12 months 41(i) 95.1

Engineering review within the past 12 months 41(i) 95.1

Seismic review for properties in zones 3 or 4 10 33.1

(i)The only loan that did not receive an environmental or engineering review in thepast 12 months is The Westchester, which was previously securitized in severaltransactions in early 2020.

Structural Review

We reviewed structural matters that we believe are relevant to our analysis, as well as the majortransaction documents, including the prospectus, pooling and servicing agreement, and otherrelevant documents and opinions, to understand the transaction's mechanics and its consistencywith applicable criteria. We also conducted a focused structural review of the 10 largest loans inthe pool, as well as for loans with a non-trust pari passu balance over $20.0 million. We note thestructural matters, if any, that we factored into our analyses of these loans in the Top 10 Loanssection below.

S&P Global Ratings' Credit Evaluation

Our analysis of the pool included the following:

- We derived an S&P Global Ratings NCF for 27 of the 35 loans in the pool (91.4% of the pooledtrust balance). For the remaining loans, we extrapolated NCF haircuts according to propertytype and selected capitalization rates for each property. We excluded certain outlier loans fromour extrapolation calculation. (See Appendix I for S&P Global Ratings' NCF variance applied toeach loan in the transaction.)

- We conducted site inspections for nine properties across nine loans (43.6% of the pooled trustbalance).

- We analyzed the property-level operating statements, rent rolls, and third-party appraisal,environmental, engineering, and, if applicable, seismic reports, for each loan that we reviewedin the pool.

- We reviewed structural matters that we considered relevant to the analysis of the loans and thetransaction, and we performed a loan-level structural analysis for the 10 largest loans in thepool, as well as for loans with a non-trust pari passu balance over $20.0 million.

S&P Global Ratings' NCF variance

S&P Global Ratings' property-level cash flow analysis derives what it believes to be a property'slong-term sustainable NCF. In our analysis, we considered issuer-provided projections, historicaland projected operating statements, third-party appraisal reports, relevant market data, and

www.standardandpoors.com November 1, 2021 12

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

assessments of the various properties' competitive positions. On a pool-wide basis, our weightedaverage NCF was 19.6% lower than the issuer's underwritten NCF. (See Appendix I for S&P GlobalRatings' NCF variance for each loan.)

S&P Global Ratings' DSC

We calculated the pool's 2.10x DSC using the respective loans' contract interest rate and the S&PGlobal Ratings NCF (see table 7).

Table 7

S&P Global Ratings' DSC Range

DSC range (x) No. of loans Loan balance (mil. $) % of pooled trust balance

Less than 1.00 - - -

1.00–1.10 - - -

1.10–1.20 2 23.9 2.6

1.20–1.30 2 47.2 5.1

1.30–1.40 3 87.1 9.5

1.40–1.50 2 19.3 2.1

1.50–1.60 1 25.0 2.7

1.60–1.70 1 21.0 2.3

1.70–1.80 4 95.6 10.4

1.80–1.90 2 16.0 1.7

1.90–2.00 5 163.7 17.8

Greater than 2.00 13 419.8 45.7

DSC--Debt service coverage.

S&P Global Ratings' LTV

Based on our analysis, S&P Global Ratings' weighted average beginning LTV ratio is 102.2% andits ending LTV ratio is 98.7%, which reflects the 7.52% weighted average S&P Global Ratingscapitalization rate (see table 8).

Table 8

S&P Global Ratings' LTV Ratios(i)

LTV ratio range (%) No. of loans Loan balance (mil. $) % of pooled trust balance

Less than 50 1 10.0 1.1

50–55 - - -

55–60 - - -

60–65 - - -

65–70 - - -

70–75 - - -

75–80 - - -

www.standardandpoors.com November 1, 2021 13

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Table 8

S&P Global Ratings' LTV Ratios(i) (cont.)

LTV ratio range (%) No. of loans Loan balance (mil. $) % of pooled trust balance

80–85 2 70.3 7.7

85–90 4 117.1 12.7

90–95 2 88.4 9.6

95–100 7 182.8 19.9

100–105 7 117.7 12.8

105–110 3 78.6 8.6

Greater than 110 9 253.7 27.6

LTV--Loan to value.

S&P Global Ratings' credit assessment by property type

Table 9 summarizes S&P Global Ratings' NCF and valuation assessment by property type.

Table 9

Cash Flow Analysis And Valuation

Property type

% of pooledtrust

balance

S&P GlobalRatings' DSC

(x)(i)% NCFdiff.(ii)

S&P GlobalRatings' cap

rate (%)

S&P GlobalRatings' weightedaverage LTV ratio

(%)

S&P GlobalRatings' valueper unit/sq. ft.

($)

Multifamily 23.0 1.97 (16.2) 7.07 100.2 148,716

Office 21.1 2.08 (31.2) 7.91 106.6 296

Mixed-use 16.9 2.29 (19.7) 7.81 100.5 706

Retail anchored 16.9 2.20 (8.4) 7.18 92.6 287

Industrial 8.6 2.14 (12.7) 7.82 102.0 122

Medical office 5.7 1.91 (16.1) 7.75 130.8 690

Mall 4.9 1.93 (46.5) 6.75 105.8 400

Single tenant - non IG 2.2 2.25 (10.7) 8.50 89.2 174

Self-storage 0.9 1.46 (5.3) 8.00 97.7 136

Total/weightedaverage

100.0 2.10 (19.6) 7.52 102.2 -

(i)Calculated based on S&P Global Ratings' NCF and the fixed loan interest rate. (ii)The difference between S&P Global Ratings' estimated NCFand the underwriter's estimated NCF as a percentage of the underwriter's estimated NCF. DSC--Debt service coverage. NCF--Net cash flow.LTV--Loan to value. IG--Investment grade.

S&P Global Ratings' credit assessment of the top 10 loans

Table 10 summarizes S&P Global Ratings' NCF and valuation assessment of the top 10 loans. Weprovide individual analyses of these loans in the Top 10 Loans section below.

www.standardandpoors.com November 1, 2021 14

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Table 10

Top 10 Loans

PropertyPropertytype

% ofpooled

trustbalance

S&P GlobalRatings'

trust DSC(x)(i)

% NCFdiff.(ii)

S&P GlobalRatings' cap

rate (%)

S&P GlobalRatings'LTV (%)

S&P GlobalRatings'

value perunit/sq. ft.

($)

CX - 350 & 450 WaterStreet

Mixed-use 8.5 2.65 (24.3) 7.50 90.3 985

50 Horseblock Industrial 6.4 2.40 (11.1) 7.75 99.3 126

Rox San Medicaloffice

5.7 1.91 (16.1) 7.75 130.8 690

520 Almanor Office 5.4 2.71 (45.8) 7.25 89.6 490

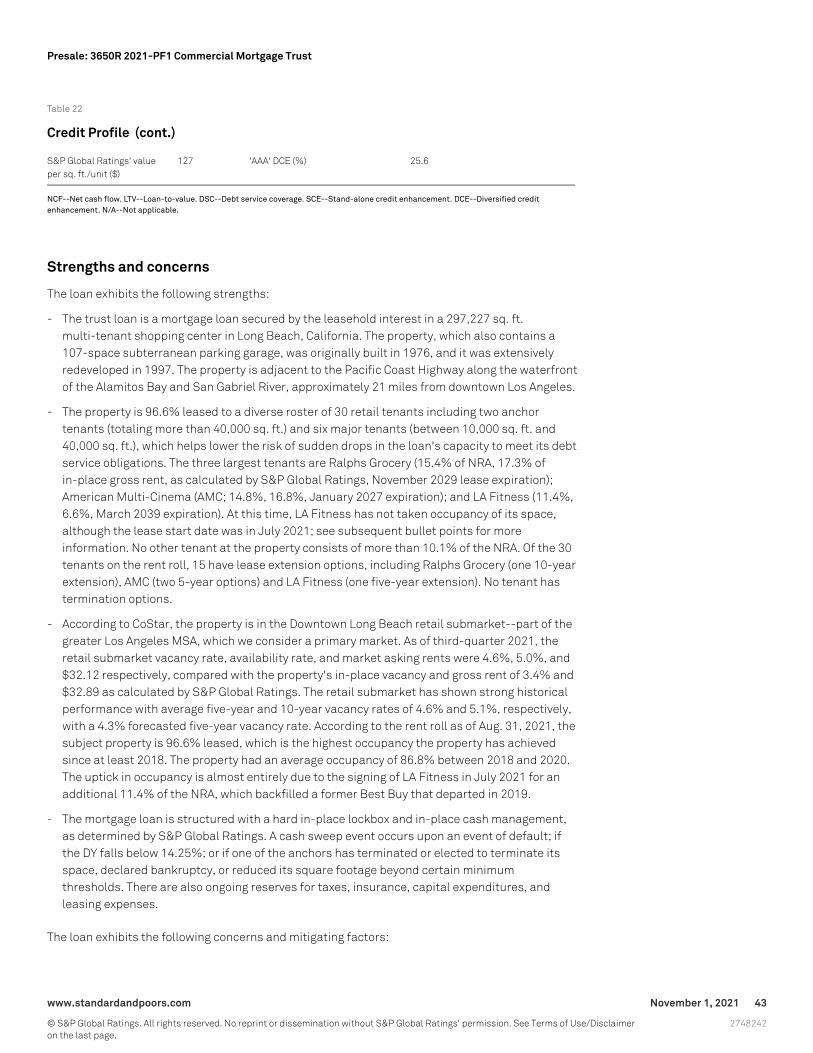

Plaza La Cienega RetailAnchored

5.4 2.22 (6.4) 7.25 99.2 297

Huntsville OfficePortfolio

Office 5.4 1.35 (28.2) 9.25 118.0 65

Venice Crossroads Retailanchored

4.9 2.95 (4.7) 7.00 81.9 349

The Westchester Mall 4.9 1.93 (46.5) 6.75 105.8 400

Marina Pacifica Retailanchored

3.6 1.27 (14.8) 7.25 87.7 127

Patewood CorporateCenter

Office 3.3 1.79 (15.4) 8.00 116.6 131

Total/weightedaverage

- 53.5 2.19 (21.7) 7.58 101.4 -

(i)Calculated based on S&P Global Ratings' NCF and the fixed loan interest rate. (ii)The difference between S&P Global Ratings' estimated NCFand the underwriter's estimated NCF as a percentage of the underwriter's estimated NCF only. For pari passu loans, S&P Global Ratings' DSCand LTV are based on the trust and pari passu balance. DSC--Debt service coverage. NCF--Net cash flow. LTV--Loan to value.

Table 11 summarizes S&P Global Ratings' NCF and valuation assessment of loans 11-20. Forthese loans, our weighted average NCF is 19.1% lower than the issuer's underwritten NCF. S&PGlobal Ratings' weighted average beginning LTV ratio is 104.6% for these loans, and we calculateda 2.00x DSC using the respective loans' contract interest rates and S&P Global Ratings' NCF.Factors that contributed to NCF variances over 7.0%, positive NCF variances, or high S&P GlobalRatings LTV ratios over 90.0% are outlined in table 11. (See Appendix I for S&P Global Ratings' NCFvariance, LTV ratio, and DSC ratio for all of the loans in the transaction.)

Table 11

Loans 11-20

PropertyPropertytype

% ofpooled

trustbalance

S&PGlobal

Ratings'trust DSC

(x)(i)% NCFdiff.(ii)

S&PGlobal

Ratings'cap rate

(%)

S&PGlobal

Ratings'LTV (%)

S&PGlobal

Ratings'value per

unit/sq.ft. ($)

NCFvariance/high

S&P GlobalRatings' LTV

drivers

TanglewoodApartments

Multifamily 3.3 1.93 (14.4) 7.50 100.2 78,002 Vacancy, otherincome, and

R&M expense

www.standardandpoors.com November 1, 2021 15

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Table 11

Loans 11-20 (cont.)

PropertyPropertytype

% ofpooled

trustbalance

S&PGlobal

Ratings'trust DSC

(x)(i)% NCFdiff.(ii)

S&PGlobal

Ratings'cap rate

(%)

S&PGlobal

Ratings'LTV (%)

S&PGlobal

Ratings'value per

unit/sq.ft. ($)

NCFvariance/high

S&P GlobalRatings' LTV

drivers

Axis Apartmentsand Lofts

Multifamily 2.9 1.78 (9.8) 6.75 97.2 144,613 Vacancy andother income

Shops of Wisconsin Retailanchored

2.9 2.03 (10.6) 7.25 104.5 360 Vacancy,managementfee, and TI/LC

2 Washington Multifamily 2.9 1.91 (32.1) 6.83 102.0 373,510 Marked in-placelease to market,

vacancy, andreal estate taxes

One SoHo Square Office 2.7 3.18 (34.7) 6.50 83.1 718 Vacancy, realestate taxes,

and TI/LCs

Icon One Daytona Multifamily 2.7 1.53 (23.2) 7.25 126.9 139,691 Vacancy,concessions,

and otherincome

PetSmart HQ Office 2.5 1.74 (23.1) 8.00 115.2 161 GPR, vacancy,and TI/LC

747 AmsterdamAvenue

Mixed-use 2.3 2.06 (21.7) 8.71 132.2 487 Vacancy, realestate taxes,

andmanagement

fees

93 East Apartments Multifamily 2.3 1.62 (9.0) 6.75 97.9 109,995 Vacancy, otherincome, real

estate taxes,and

managementfees

Cabelas Singletenant - nonIG

2.2 2.25 (10.7) 8.50 89.2 174 Vacancy andTI/LC

Total/weightedaverage

- 26.7 2.00 (19.1) 7.36 104.6 -

(i)Calculated based on S&P Global Ratings' NCF and the fixed loan interest rate. (ii)The difference between S&P Global Ratings' estimated NCFand the underwriter's estimated NCF as a percentage of the underwriter's estimated NCF only. For pari passu loans, S&P Global Ratings' DSCand LTV are based on the trust and pari passu balance. DSC--Debt service coverage. NCF--Net cash flow. LTV--Loan to value. CapEx--Capitalexpenditure. TI/LC--Tenant improvements and leasing commissions. GPI—Gross potential income. N/A--Not applicable.

Loan-level credit enhancement

We used each loan's S&P Global Ratings DSC and LTV to calculate its respective stand-alonecredit enhancement (SCE) and diversified credit enhancement (DCE) at the various ratingcategories. These calculations included adjustments to reflect the various loans' amortization

www.standardandpoors.com November 1, 2021 16

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

terms and the presence of any subordinated additional debt (See Appendix II for a list of eachloan's SCE and DCE).

Pool diversity

Overall transaction credit enhancement levels at each rating category are directly affected by theloan pool's diversity, a function of the transaction's effective loan count. The effective loan count,which is measured by the Herfindahl-Hirschman Index, accounts for the relative size of the loansin the pool by normalizing a transaction's loan count to account for unevenly sized loans. Thistransaction has an effective loan count of 24.5, which we consider to be moderately diversified,resulting in a concentration coefficient of 61.4%.

We also considered the loan pool's geographic makeup in our overall transaction-level analysis.This loan pool is geographically diverse and is located primarily within primary markets (68.8%)and secondary markets (15.7%).

Transaction-level credit enhancement

We establish transaction-level credit enhancement levels using the concentration coefficient (afunction of a pool's effective loan count) to interpolate between the weighted average SCE andDCE at each rating category, subject to applicable floors and any adjustment for overalltransaction-level considerations.

We believe this transaction's high percentage of full-term, interest-only loans warranted anadditional negative qualitative adjustment beyond that produced from our loan-level analysis andmodel results.

Scenario Analysis

We performed several 'AAA' stress scenario analyses to determine how sensitive the certificatesare to a downgrade over the loan term.

Effect of declining NCF

A decline in NCF may constrain cash flows available for debt service. A decline in cash flows mayoccur due to falling rental rates and occupancy levels, changes to operating expenses, or otherfactors that may decrease a property's net income. To analyze the effect of a decline in cash flowson our ratings, we have developed scenarios whereby the NCF from the portfolio decreases by10%-40% from our current cash flow, which is 19.6% lower than the issuer's underwritten NCF.(See table 13 for the potential effect on S&P Global Ratings' 'AAA' rating under these scenarios,holding constant S&P Global Ratings' overall capitalization rate of 7.52%.)

Table 13

Effect Of Declining NCF On S&P Global Ratings

Decline in S&P Global Ratings' NCF (%) 0 -10 -20 -30 -40

Potential 'AAA' rating migration AAA A+ B- CCC- CCC-

Note: Per the Credit Stability Criteria, dated May 2010, the 'AAA' rating should not move below 'A+' within one year, and should not move below'CCC-' within three years. Per the table below, a NCF decline of more than 10% would be required to breach the one-year tolerance, and a NCFdecline of more than 30% would be required to breach the three-year tolerance. NCF--Net cash flow.

www.standardandpoors.com November 1, 2021 17

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Top 10 Loans

1. CX - 350 & 450 Water Street

Table 14

Credit Profile

Loan no. 1 Property type Mixed-use

Loan name CX - 350 & 450 WaterStreet

Subproperty type Various

Pooled trust loanbalance ($)

77,900,000 Property sq. ft./no. of units 915,233

% of total pooledtrust balance (%)

8.5 Year built 2021

City Cambridge Sponsors Divco West Real Estate Services, LLC,California State Teachers' RetirementSystem, and Teachers Retirement System ofTexas

State Mass. S&P Global Ratings'amortization category

Interest only

S&P Global Ratings'market type

Primary S&P Global Ratings'amortization adjustment (%)

(2.50)

S&P Global Ratings'NCF ($)

5,840,000(i) S&P Global Ratings'subordinate debt category

N/A

S&P Global Ratings'NCF variance (%)

(24.28) S&P Global Ratings'subordinate debtadjustment

N/A

S&P Global Ratings'cap rate (%)

7.50 S&P Global Ratings' LTVratio (%)

90.3(ii)

S&P Global Ratings'value (mil. $)

86.2(i) S&P Global Ratings' DSC (x) 2.65(ii)

S&P Global Ratings'value variance (%)

(53.4) 'AAA' SCE (%) 50.2

S&P Global Ratings'value per sq. ft./unit($)

985 'AAA' DCE (%) 12.0

(i)Pari passu adjusted. (ii)The trust loan is pari passu; LTV ratio and DSC are calculated based on the $736.1 million pari passu companion loanand the $77.9 million pooled trust loan balance (collectively, the senior loan component). NCF--Net cash flow. LTV--Loan-to-value. DSC--Debtservice coverage. SCE--Stand-alone credit enhancement. DCE--Diversified credit enhancement. N/A--Not applicable.

Strengths and concerns

The loan exhibits the following strengths:

- The $77.9 million pooled trust loan, along with the $736.1 million pari passu portion heldoutside the trust, represents an $814.0 million senior loan component of a $1.225 billion wholeloan. The whole loan is secured by the borrower's fee simple interest in Cambridge Crossing –350 Water Street and 450 Water Street, a two-building, class A office/R&D/laboratory complex

www.standardandpoors.com November 1, 2021 18

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

totaling 915,233 sq. ft. in Cambridge, Mass. The two adjacent buildings are part of the 45-acre,4.2 million sq. ft. science, technology, residential, and retail Cambridge Bridge master-planneddevelopment that is close to MIT, Harvard University, and Massachusetts General Hospital. Thecollateral includes a 12-story, 511,157-sq.-ft. R&D/laboratory building located at 350 WaterStreet with three below-grade stories of parking totaling 361 spaces; and an adjacentnine-story, 404,076-sq.-ft. office building located at 450 Water Street, with five levels ofparking totaling 456 spaces, two of which are below-grade. Both buildings are targeting aLEED-Gold certification.

- The senior loan component has a strong DSC of 2.65x, calculated using the loan's fixed interestrate and our in-place NCF for the property, which is 24.3% lower than the issuer's NCF. Thecash flow variance is primarily driven by our higher vacancy rate and tenant improvement andleasing commission (TI/LC) assumptions and exclusion of straight-line rent income. Weconsidered future investment-grade tenant rent steps in our analysis via an addition to ourcapitalized value. Including the non-trust subordinate component, our DSC decreases to 1.76xfor the whole loan.

- Both buildings are 100% leased to a single tenant according to two, triple net 15-year leasesthat are guaranteed by the tenant's publicly traded investment-grade rated parent. AventisInc., a subsidiary of the French multinational pharmaceutical firm Sanofi (AA/Stable/A-1+)executed the two leases in late 2018 with the lease on the 350 Water Street R&D/laboratorybuilding commencing in July 2021. The lease on the 450 Water Street office building that isestimated to start in November 2021. Both leases expire in 2036, five years after the loan'sinitial maturity date. Aventis has begun paying rent on the 350 Water Street building and isexpected to start paying rent on the other building in November 2021, subject to the sponsorcompleting certain base building and tenant improvement work (discussed below). However,the loan is structured with upfront reserves of $10.7 million (roughly equivalent to five monthsof rent) to mitigate the risk that rental payments on the 450 Water Street building may bedelayed due to construction.

- The properties will be mission critical for Aventis and act as its North American researchheadquarters and are expected to have 3,000 employees that are consolidated from severalsmaller offices in the Boston area. Along with housing traditional business operations, thislocation will house a "Center of Excellence" dedicated to mRNA vaccine research.

- The property is located in a strong office and life science submarket within the Boston MSA,which we consider a primary market. According to CoStar, the East Cambridge/Kendall Squareoffice submarket, where the properties are located, had a vacancy rate and base asking rent of3.4% and $88.83 per sq. ft., respectively, as of third-quarter 2021. According to the appraiser,the East Cambridge submarket is largely concentrated with life science, pharmaceutical, andtechnology companies and continues to exhibit one of the tightest vacancy rates for laboratoryspace at 1.3%, with asking base rent of $105.81 per sq. ft. as of second-quarter 2021. Inaddition, the appraiser concluded an office submarket vacancy rate and asking base rent of7.2% and $82.60 per sq. ft., respectively. This compares to an in-place base rent of $75.90 persq. ft. on the R&D/laboratory space (350 Water Street building) and $66.00 per sq. ft. on theoffice space (450 Water Street building). The leases include contractual rent escalations ofapproximately 2.5% annually. The submarket's historical five- and 10-year average officevacancy rates were 2.2% and 4.8%, respectively, with a 4.2% five-year forecasted vacancy rate,according to CoStar.

- The Boston-Cambridge market is the largest life science cluster in the U.S. and 18 out of the 20largest pharmaceutical companies have a presence in the market, according to CoStar. Drivingthe submarket's performance is its access to a deep talent pool from the adjacent MIT campus

www.standardandpoors.com November 1, 2021 19

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

and nearby universities, such as Harvard, Boston University, and Tufts. The submarket also hasa large presence of venture capital firms, biotech, and technology firms, which all benefit fromthe outflow of university talent. Given the strong submarket fundamentals, below market rentspaid by Aventis, and a strong credit parent guaranteeing the long-term leases, we utilized a3.0% vacancy factor to derive our sustainable NCF on the property.

- The whole loan benefits from the institutional and experienced joint venture sponsorship ofDivco, CalSTRS and TRS. Divco is a developer, owner, and operator of real estate that manages$12.9 billion in assets as of December 2020 throughout the U.S. Divco has invested in andmanaged over 22 commercial properties in the Boston area and was one of the firstinstitutional investors in the Kendall Square/East Cambridge submarket. CalSTRS, establishedin 1913, is the second-largest public pension fund with a market value of approximately $306.7billion (12.1% or $37.2 billion is allocated toward real estate investments) as of May 31, 2021.TRS, established in 1937, is the largest public retirement system in Texas and the sixth-largestpublic pension fund in America. It provides retirement and related benefits for those employedby the public schools, colleges and universities and manages a $180.0 billion trust fund.

- We visited the property on Oct. 13, 2021, accompanied by a sponsor representative and twoconstruction crew members. The collateral property is part of the Cambridge Crossingmaster-planned development which will include over 10 acres of public space. We observedthat the two buildings were not completed yet and in various stages of construction. Theexterior of the two buildings, parking garages, mechanical, and engineering were nearcompletion. We toured each building's lobby, mezzanine levels, parking garage, engineeringroom, and office or laboratory space. The 350 Water Street building infrastructure includeslobby and laboratory spaces on the first floor. The lobby is designed with floor to ceilingwindows that open to the outdoors. The laboratory space will have 15-foot ceilings and isexpected to be open for public viewing, allowing visitors to observe the laboratory operations.The 450 Water Street building is outfitted for office use with a bike storage room as part ofCambridge's greater biking initiative. During the tour, the sponsor representative pointed outthat the tenant requested to have the two buildings connected by two bridges after the externalfinishes were completed. The sponsor representative was not able to provide a date as to whenthe buildings would be substantially completed, but expects the tenant to partly occupy the twobuildings in mid- to late-2022.

- The mortgage loan is structured with a hard in-place lockbox and springing cash management,which allows the borrower to control funds until an event of default has occurred, a DSC ratio of1.75x is breached for two consecutive quarters, the ARD in November 2031, or either one of theAventis leases has terminated or elected to terminate its space, declared bankruptcy, orreduced its square footage beyond certain minimum thresholds. At that point, the borrower willbe required to maintain monthly tax and insurance escrows, and TI/LC deposits. During atrigger period, all excess cash flow will be deposited into a lender-controlled account.

The loan exhibits the following concerns and mitigating factors:

- The senior loan component has high leverage, with an S&P Global Ratings' LTV ratio of 90.3%,based on our valuation. The LTV ratio based on the appraiser's as-is valuation is 42.0%. Ourestimate of the long-term sustainable value is 53.4% lower than the appraiser's as-isvaluation. The variance is primarily driven by our capitalization rate of 7.5%, versus theappraiser's capitalization rate of 3.7%.

- In addition to the senior loan component of $835.0 million, there is also a $411.0 million juniornon-trust note, which is the controlling piece of the whole loan. Based on the whole loan, ourLTV ratio increases to 136.3% from 90.3%. The LTV ratio based on the appraiser's as-is

www.standardandpoors.com November 1, 2021 20

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

valuation is 67.7%.

- The loan is interest-only for its entire initial 10-year term, and there will be no scheduledamortization through the ARD. The initial maturity of the loan is November 2031. After the ARD,excess cash will be used to hyper-amortize the loan for five years. To account for the lack ofamortization during the initial term, we applied negative LTV threshold adjustments across thecapital structure.

- Both buildings are still in various phases of construction with the base building work not 100%completed yet. According to the issuer, the base building work for both 350 and 450 WaterStreet are approximately 90% complete. The property does not have temporary certificates ofoccupancy. According to the issuer, the certificates are expected to be issued once thebuildings are substantially completed in fourth-quarter 2021 for 450 Water Street andsecond-quarter 2022 for 350 Water Street. The sponsor projects total costs to construct andbuild out the two buildings at about $1.1 billion, of which approximately $213.0 million has yetto be spent. To mitigate the construction risk, the loan is structured with upfront reserves($96.0 million for hard costs, $18.0 million for soft costs, and $99.0 million for outstanding TIs)held by the lender for the remaining estimated construction cost amount. The appraiserdeducted $156.4 million for remaining development cost and profit to arrive at its as-isvaluation. We accounted for the construction risk by using a higher capitalization rate in ouranalysis.

- The property lacks operating performance history since it is still under construction and isexposed to single-tenant risk. In addition, the tenant has the right to terminate its leases oneyear prior to the 2036 lease expiration date. These concerns are partly mitigated because theleases are guaranteed by a high investment-grade rated parent and the property will serve asthe tenant's North American research headquarters housing about 3,000 employees. Inaddition, Aventis is expected to spend about $181.7 million ($198 per sq ft) to build out its ownspace not including furniture, fixtures, and equipment. The loan is structured with lease andcash flow sweeps generally triggered by the sole tenant not renewing or extending its leasesand a DSC below 1.75x, respectively.

- The 350 Water Street building is outfitted for specialized uses, primarily R&D and laboratory.Repurposing these spaces to traditional office or alternative uses would be costly, and it ispossible office or alternatively used space would garner lower rent than the property's in-placerent. We accounted for this risk by utilizing a higher capitalization rate for the non-office spacecompared to the appraiser's capitalization rate.

- The tenant has not commenced paying rent on the 450 Water Street building yet. The lease isestimated to start in November 2021, subject to the sponsors completing certain base buildingand tenant work. To mitigate the risk that rental payments may be delayed, the lender reserved$8.9 million upfront for gap rent, which equals about four months of rent. Additionally, wecalculated that the DSC would be above 1.00x on the whole loan, excluding the rent on the 450Water Street building, and assuming the gap rent reserve is depleted.

- The whole loan is a refinancing and the loan proceeds paid off a $617.8 million constructionloan, funded $149.4 million of upfront gap rent, hard costs, soft costs, and TI reserves, coveredapproximately $5.8 million of closing costs, and returned approximately $451.9 million (36.9%of the financing) to the sponsor. The sponsor acquired the land in August 2015 and is currentlydeveloping the two buildings for an estimated cost of $1.1 billion.

- The loan permits individual property releases, subject to a release premium equal to 110% ofthe allocated loan amount (ALA) for the 350 Water Street building and 105% of the ALA for the450 Water Street building. Each release is subject to a DSC test, whereby the DSC after release

www.standardandpoors.com November 1, 2021 21

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

is at least the greater of the DSC at closing and the aggregate DSC immediately prior to thatrelease.

- During alterations to the property, the loan documents leave to the servicer's discretion thedecision whether to require collateral for alterations whose cost exceeds a certain threshold. Inaddition, this collateral, if required, may not be rated by S&P Global Ratings. This structurepotentially exposes the transaction to risks associated with additional leverage beyond a deminimis amount and additional liens, such as mechanic's liens, some of which may havepriority over the mortgage lien.

- The loan does not have any entity named as a carve-out guarantor. In our view, this limitationgenerally lessens the disincentive provided by a full nonrecourse carve-out related to "badacts" or voluntary bankruptcy.

2. 50 Horseblock

Table 15

Credit Profile

Loan no. 2 Property type Industrial

Loan name 50Horseblock

Subproperty type Flex

Pooled trust loan balance($)

59,000,000 Property sq. ft./no. of units 472,278

% of total pooled trustbalance (%)

6.4 Year built/renovated 1986

City Yaphank Sponsor New Mountain Net Lease Corp. and NewMountain Net Lease Partners Corp.

State NY S&P Global Ratings' amortizationcategory

Interest Only

S&P Global Ratings'market type

Primary S&P Global Ratings' amortizationadjustment (%)

(2.50)

S&P Global Ratings' NCF($)

4,600,000 S&P Global Ratings' subordinatedebt category

N/A

S&P Global Ratings' NCFvariance (%)

(11.07) S&P Global Ratings' subordinatedebt adjustment

N/A

S&P Global Ratings' caprate (%)

7.75 S&P Global Ratings' LTV (%) 99.3

S&P Global Ratings' value(mil. $)

59.4 S&P Global Ratings' DSC (x) 2.40

S&P Global Ratings' valuevariance (%)

(34.9) 'AAA' SCE (%) 55.2

S&P Global Ratings' valueper sq. ft./unit ($)

126 'AAA' DCE (%) 14.7

NCF--Net cash flow. LTV--Loan-to-value. DSC--Debt service coverage. SCE--Stand-alone credit enhancement. DCE--Diversified creditenhancement. N/A--Not applicable.

www.standardandpoors.com November 1, 2021 22

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Strengths and concerns

The loan exhibits the following strengths:

- The trust loan is a mortgage loan secured by the fee-simple interest in a 472,278 sq.-ft.industrial property located in Yaphank, New York. The property is located approximately 1.5miles from the Long Island Expressway, the major highway serving the community and the restof Long Island. The property, which is 100% leased to Amneal Pharmaceuticals LLC (Amneal,'B/stable'), contains a mix of research and development, manufacturing, warehouse, and officespace.

- The trust loan has a strong DSC of 2.40x, calculated using the loan's fixed interest rate and ourin-place NCF for the property, which is 13.9% lower than the issuer's NCF. Our lower NCF isprimarily driven by our higher vacancy, real estate taxes, and TI/LC assumptions.

- The property is 100% leased to Amneal under a triple-net lease through June 2043. The leaseexpires approximately 12 years after the loan's maturity in June 2031. The lease contains two10-year renewal options and no termination options. According to the issuer, Amneal is one ofthe five largest producers of generic drugs in the U.S. by prescription volume. This property isAmneal's primary generic pharmaceutical manufacturing facility in the U.S. Amneal had ownedand occupied this property since its 2008 acquisition of Interpharm Holdings. Following its2008 purchase of the property, Amneal invested over $160.0 million on the expansion andmodernization of the property by increasing its footprint to 472,278 sq. ft. from 124,200 sq. ft.Approximately $135.1 million went toward building costs, with the remaining $28.3 milliontoward facility equipment. The facility is temperature controlled and has 28-foot ceiling heightsand 12 loading docks.

- The property is in the primary market of New York City. According to CoStar, the property is inthe South-Central Suffolk industrial submarket. As of third-quarter 2021, the submarket'svacancy rate and gross rent were 1.4% and $12.98 per sq. ft., compared with a base rent of$12.26 per sq. ft. at the property. Although the property is 100% leased to Amneal through June2043, we applied a 10.0% vacancy rate in our analysis to account for the single-tenant risk.

- The mortgage loan benefits from New Mountain Net Lease Corporation and New Mountain NetLease Partners Corporation's experienced sponsorship, both of which are subsidiaries of NewMountain Finance Corporation. New Mountain is an investment company that specializes inprivate equity, public, equity, credit and net lease investments. The company has over $20billion assets under management.

- The mortgage loan is structured with a hard in-place lockbox and in-place cash management,as determined by S&P Global Ratings. A cash sweep event occurs upon an event of default, ifthe debt yield falls below 7.75%, or the major tenant has terminated or elected to terminate itsspace, declared bankruptcy, defaulted, failed to timely renew, been downgraded below certainminimum thresholds of 'CCC', or reduced its square footage by 50%. There are also ongoingreserves for taxes and insurance.

The loan exhibits the following concerns and mitigating factors:

- The trust loan has high leverage with a 99.3% LTV ratio, based on S&P Global Ratings'valuation. Our long-term sustainable value estimate is 35.0% lower than the appraiser'svaluation, primarily driven by our higher vacancy assumptions as well as a higher capitalizationrate assumption of 7.75%, compared to the appraiser's capitalization rate of 6.00%. Theappraiser also concluded a dark value on the property of $52,700,000, which is 12.7% lower

www.standardandpoors.com November 1, 2021 23

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

than our S&P Global Ratings' valuation.

- The trust loan is interest-only for its entire 10-year term, and there will be no scheduledamortization during the loan term. We reduced our LTV recovery thresholds across the capitalstructure to account for the higher refinancing risk at loan maturity.

- The mortgage loan is a recapitalization and the loan proceeds returned $57.9 million (98.3% ofthe financing) of equity to the sponsor. However, the sponsor purchased the property in anall-cash transaction in March 2021 for $89.3 million. Based on the purchase price of $89.3million, the sponsor will have $31.4 million of cash equity remaining in the property.Furthermore, based on the appraisal value of $91.3 million as of April 2021, the sponsor has$32.3 million of implied equity in the property.

- The property exhibits single-tenant concentration risk because it is 100% leased to Amneal.Furthermore, the property was also historically occupied by a single tenant. Following itsconstruction in 1986, it was occupied by Arrow Electronics and then Interpharm Holdings.Therefore, if Amneal vacates the property, the ability to re-tenant the property for multi-tenantuse may require a significant amount of capital expenditure. This risk is partially mitigated bythe in-place cash sweep provisions of the cash management structure noted above. We alsoaccounted for this risk by applying a 10% vacancy rate in our analysis.

- The property currently benefits from a payment in lieu of taxes (PILOT) program with a specificpayment schedule set up by the Suffolk County and the town of Brookhaven. The PILOT programincentivizes companies to create jobs in the local community. The current PILOT extendsthrough 2027, whereafter the borrower is expected to pay full taxes on the property. Theexpiration of the PILOT program will result in a significant increase in real estate tax at theproperty. However, the lease with Amneal is triple-net, and the increase in real estate tax isexpected to be reimbursed by Amneal. However, the increase in real estate tax may result in thegross rent being paid by Amneal to be above market rents. Therefore, in our analysis, weassumed an unabated tax figure, which is fully recovered in the form of expensereimbursement, to derive our S&P value on the property. Since the increase in real estate taxwill increase the gross rent being paid by Amneal, we also applied our assumed vacancy factoron the expense reimbursement.

- The loan agreement only requires a coverage of 12-month business interruption insurance ifAmneal's lease is in effect. This is less than the 18-month business interruption we typicallysee for loans of this size, exclusive of extensions and regardless of the leasing status of theproperty. We reduced our LTV recovery thresholds across the capital structure to account forthis business interruption risk.

- The loan does not have a warm body carve-out guarantor. In our view, this limitation generallylessens the disincentive provided by a full nonrecourse carve-out related to "bad acts" orvoluntary bankruptcy.

- Although the borrower must provide the lender with annual financial statements, they are notrequired to be audited. We believe audited financial statements are more conclusive andreliable than unaudited statements. Additionally, unaudited quarterly financial statements arenot required if a single-tenant triple-net lease is in effect.

3. Rox San

www.standardandpoors.com November 1, 2021 24

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

Table 16

Credit Profile

Loan no. 3 Property type Office

Loan name Rox San Subproperty type Medical

Pooled trust loan balance($)

52,000,000 Property sq. ft./no. of units 57,666

% of total pooled trustbalance (%)

5.7 Year built/renovated 1963

City Beverly Hills Sponsor David Taban, Manouchehr Illoulian, MichaelPashaie, and K. Joseph Shabani

State CA S&P Global Ratings' amortizationcategory

Interest Only

S&P Global Ratings'market type

Primary S&P Global Ratings' amortizationadjustment (%)

(2.50)

S&P Global Ratings' NCF($)

3,320,000 S&P Global Ratings' subordinatedebt category

N/A

S&P Global Ratings' NCFvariance (%)

(16.12) S&P Global Ratings' subordinatedebt adjustment

N/A

S&P Global Ratings' caprate (%)

7.75 S&P Global Ratings' LTV Ratio(%)

130.8

S&P Global Ratings' value(mil. $)

39.8 S&P Global Ratings' DSC (x) 1.91

S&P Global Ratings' valuevariance (%)

(50.3) 'AAA' SCE (%) 67.1

S&P Global Ratings' valueper sq. ft./unit ($)

690 'AAA' DCE (%) 30.8

NCF--Net cash flow. LTV--Loan-to-value. DSC--Debt service coverage. SCE--Stand-alone credit enhancement. DCE--Diversified creditenhancement. N/A--Not applicable.

Strengths and concerns

The loan exhibits the following strengths:

- The trust loan is secured by the fee-simple interest in an 11-story, class A medical officebuilding totaling 57,666 sq. ft. built in 1963 in the Golden Triangle area of Beverly Hills, Calif.The sponsor purchased the property in 2008 and invested approximately $17.5 million inrenovations ($303 per sq. ft.) over the past 13 years including an architectural façade andexterior upgrade, lobby and common area renovations, a new heating, ventilation, and airconditioning (HVAC) system, and new elevators. According to the sponsor, the tenancy isconcentrated in the cosmetic enhancement sector, with tenants such as plastic surgeons,prosthodontists, endocrinologists, and dermatologists. The property offers 218 subterraneanparking spaces, an attractive amenity in the infill location.

- The trust loan has a moderately high DSC of 1.94x, calculated using the loan's fixed interestrate and our in-place NCF for the property, which is 16.1% lower than the issuer's NCF, avariance mainly driven by our 17.0% submarket vacancy assumption compared with theissuer's estimate of 3.0%.

- Despite the COVID-19 pandemic, the property has maintained strong occupancy rates. Since

www.standardandpoors.com November 1, 2021 25

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2748242

Presale: 3650R 2021-PF1 Commercial Mortgage Trust

2018, the property's occupancy has averaged 98.9%, and approximately 55% of the NRA hasbeen at the property since 2011. The property's occupancy rate has not dipped below 95.5%since 2011, and according to the rent roll as of June 15, 2021, the property is 97.9% occupied by22 tenants. The property also had a positive-trending NOI between 2018 and 2019, rising to$3.7 million from $3.1 million, an increase of 18.4%, mostly attributed to higher gross rents.However, the property's NOI peaked in 2019, and it has declined slightly as of March 2021 to$3.3 million (a 10.6% decline) due to loss of revenue from parking income and rent abatementsdue to the pandemic.

- The property benefits from its location and high barrier to entry in the downtown Beverly Hillsarea of Los Angeles. Currently, there is an ordinance that prohibits expansion or relocation ofbuildings with medical uses. Specifically, any new building greater than 6,000 sq. ft. isprohibited without registration with the City of Beverley Hills. Due to this, we believe theproperty may be able to attain lower vacancy rates than the submarket and higher rents.

- The property benefits from a diverse roster of 22 tenants, which helps lower the risk of suddendrops in the loan's capacity to meet its debt obligations. According to the June 2021 rent roll,the three largest tenants are Radnet Management Inc. (10.6% of the NRA, 11.8% of the grossrents, lease expiration of June 2023), Dermatology Association (9.2%, 9.2%, March 2022), andCalvert Ent (7.8%, 8.1%, September 2030).

- The mortgage loan benefits from the experienced sponsorship of David Taban, Jerry Illoulian,Michael Pashaie, and Joseph Shabani. The sponsors own more than $1.97 billion of commercialreal estate, and their combined net worth is over $621.9 million.

- We visited the property on Sept. 15, 2021, and we found that the property warranted the class Adesignation. The property is several stories taller than adjacent buildings with prominentsignage and is accessed primarily through a parking garage where clients valet their cars. Giventhe building height, several offices have nice views of the surrounding area, and a few haveoutdoor patios. The parking garage was fairly busy on the day of the visit, and tenant spacesseemed to all have at least a few clients inside. The building is 100% occupied withapproximately 22 tenants, including the ground floor space currently being built out for a dentaltenant. An overwhelming majority of tenants are involved in cosmetic surgery or relatedbusinesses. No tenants vacated during COVID-19, and all tenants are current onCOVID-19-related rent deferrals.

The loan exhibits the following concerns and mitigating factors:

- The trust loan has high leverage with a 130.8% LTV ratio, based on S&P Global Ratings'valuation. Our long-term sustainable value estimate is 50.3% lower than the appraiser'svaluation. The variance is due to our cap rate of 7.75% compared with the appraiser's cap of4.25%, and our 17.0% sustainable vacancy assumption

- The loan is interest-only for its entire seven-year term, and there will be no scheduledamortization during the loan term. We reduced our LTV recovery thresholds across the capitalstructure to account for the higher refinancing at loan maturity.

- The mortgage loan is a refinancing, and the loan proceeds returned approximately $8.8 million(16.7% of the financing) of equity to the sponsor. Based on the sponsor's cost basis of $54.5million, $3.5 million of cash equity will remain in the portfolio at closing. The sponsor acquiredthe property for approximately $37.0 million ($641 per sq. ft.) in 2008.