Embed Size (px)

Citation preview

1

3E/N Assignment Questions Trading, Profit and Loss

1. The following balances were taken from the ledger of Jacintha, a retailer, on 31 December 2010.

$ Sales 63 000 Purchases 26 500 Carriage inwards 900 Carriage outwards 1 350 Insurance expense 3 000 Sales returns 550 Purchases returns 475 Rent expense 1 100 Salaries 5 225 Utilities 2 400 Commission received 15 000 Motor expenses 1 700 Motor vehicle 163 225 Bank 8 750 Debtors 18 000 Creditors 10 475 Loan from Bank 132 500 Interest expense 750 Drawings 9 000 Capital 81 000 Stock at 1 January 2010 60 000 Stock at 31 December 2010 46 500

Required: (a) Prepare the Trading and Profit and Loss Account for the year ended

31 December 2010. [20]

(b) Prepare the Balance Sheet as at 31 December 2010. [10]

2

2 The following balances were extracted from the books of Tom on 30 April 2011:

$ Capital as at 1 May 2010 156 000 Drawings 1 000 Furniture 30 000 Motor vehicles 70 000 Premises 140 000 Stock as at 1 May 2010 7 500 Bank overdraft 6 000 Cash in hand 5 000 Debtors 15 000 Creditors 20 000 Mortgage on premises 90 000 Purchases 63 000 Sales 80 000 Returns inwards 5 000 Returns outwards 8 000 Custom duty 1 500 Carriage inwards 4 500 Carriage outwards 5 500 General expenses 850 Rent received 3 000 Interest paid 300 Stationery 900 Salaries and wages 9 000 Discount allowed 200 Discount received 750 Insurance 4 500

The following additional information is available:

(i) Cost of stock on 30 April 2011 was $11 000. The net realizable value of the stock on 30 April 2011 was 10 000.

(ii) It was estimated that one-third (1/3) of the total salaries and wages had been used to prepare the goods for resale.

REQUIRED:

Prepare the following: (a) Trading, Profit and Loss Accounts for the year ended 30 April 2011. [11] (b) Balance Sheet as at 30 April 2011. [9]

3

3 The following Trial Balance is extracted from the books of Bryan Co on 31 December 2010.

$

Sales 55,000

Purchases 36,200

Sales returns 500

Purchases returns 400

Stock 8,000

Carriage inwards 700

Carriage outwards 750

Duty on purchases 300

Discount received 800

Commission received 1,200

Rent 6,000

Utilities 2,200

Wages 2,800

Discount allowed 1,000

Interest expense 450

Capital 21,300

Drawings 800

Office Equipment 3,000

Motor Vehicle 21,500

Debtors 5,200

Bank loan (payable in 2015) 5,000

Creditors 4,500

Bank overdraft 1,200

Additional information:

(i) Stock at 31 December 2010 is $7,200. (ii) Owner withdrew $200 worth of stock for own use. This has not been recorded in both the

drawings and purchases accounts.

REQUIRED (a) Prepare the Trading, Profit and Loss and Appropriation Accounts for the year ended 31 December 2010. [12] (b) Prepare the Balance Sheet as at 31 December 2010. [8]

4

4. Dean runs a small business dealing with second hand computers. On 30 April 2011, he had the following balances shown in his Trial Balance:

Dr Cr

$ $

Purchases / Sales 51 250 87 500

Stock, 1 May 2010 8 700

Returns 200 450

Discount Allowed 720

Premises 20 000

Motor Vehicles 15 000

Debtors / Creditors 6 570 5 840

Cash at Bank 2 500

Cash in Hand 860

Commission 770

Salaries 8 400

Capital, 1 May 2010 15 000

Drawings 1 580

Carriage on Purchases 600

Carriage on Sales 1 270

Rental Expense 3 800

Advertising 2 200

Bank Loan (due 31 May 2015) 10 000

General Expense 910

124 110 124 110 The following additional information was made available on 30 April 2011:

1 Stock at 30 April 2011 was valued at $7 800 at cost but has a net realisable value of $7 250.

2 Dean took stock worth $350 for his own use. No record was made in the books. 3 One-quarter (¼) of the salaries was paid to workers for sorting and packing goods for resale

purposes. 4 An amount of $210 paid for Dean‟s personal utility bill was recorded as General Expenses. 5 On 1 May 2010, Dean paid half (½) the Bank Loan using a personal cheque. This was not

recorded in the books. 6 Loan interest of 5% per annum was deducted from the bank account on 30 April 2011 but this

was not reflected in the books.

5

REQUIRED

(a) Prepare the Trading and Profit and Loss Account for the year ended 30 April 2011. [14]

(b) Prepare the Balance Sheet as at 30 April 2011. [10] (c) Explain the term “net realisable value”. [2] (d) How is closing stock valued in the books? Explain your answers with the support of a relevant

accounting concept. [2] (e) During the year, Dean purchased some computers for his office staff to use and recorded them

as purchase of stock.

(i) Do you agree with his treatment of the transaction? Explain your answer. [1]

(ii) What is the effect on profit when Dean recorded the computers as purchase of stock? [1]

[Total: 30] Gross Profit/ Net Profit

5 Prepare a table in the format shown below to show the amount by which transactions

itemised (b) to (g) would increase or decrease the gross profit or net profit of a business.

Treat each item separately and if you think that a transaction has no effect on gross profit or

net profit, write „no effect‟ in the relevant „increase‟ or „decrease‟ columns. Item (a) has been

done as an example.

Item Gross Profit Net Profit

Increase ($) Decrease ($) Increase ($) Decrease ($)

(a)

No effect

400

(b)

(c)

(d)

(e)

(f)

(g)

6

(a) Payment of advertising expenses $400.

(b) Payment of carriage on purchases $200.

(c) Discount received of $70 from creditor.

(d) Owner invested additional cash of $6 000 in the business.

(e) Returned goods to supplier $100.

(f) Interest paid on bank overdraft $80.

(g) Interest of $50 received on loan to employee Alvin.

[Total: 12]

Ledger/ Books of Prime Entry

6 The accounts below were prepared by Muthu, the owner of a provision store.

Thila

2011 $ 2011 $

Mar 5 Goods (i) 5 000 Mar 10 Returns (ii) 700

16 Cheque (iii) 2 000

Raja

2011 $ 2011 $

Mar 6 Returns (v) 450 Mar 3 Goods (iv) 2 500

10 Cheque (vi) 1 600

REQUIRED:

(a) Is Thila a debtor or a creditor? [1]

(b) Is Raja a debtor or a creditor? [1]

(c) Describe each transaction represented by each of the entries (ii) to (vi) in the above account. The

first item has been completed as an example.

(i) Sold goods worth $5 000 on credit to Thila. [10]

(d) What is the net amount of goods purchased and sold during the month of March?

[2]

(e) Rewrite Thila‟s account showing the appropriate account names and balance the account on 31

March 2011. [2]

(f) Rewrite Raja‟s account showing the appropriate account names and balance the account on 31

March 2011. [2]

[Total: 18]

7

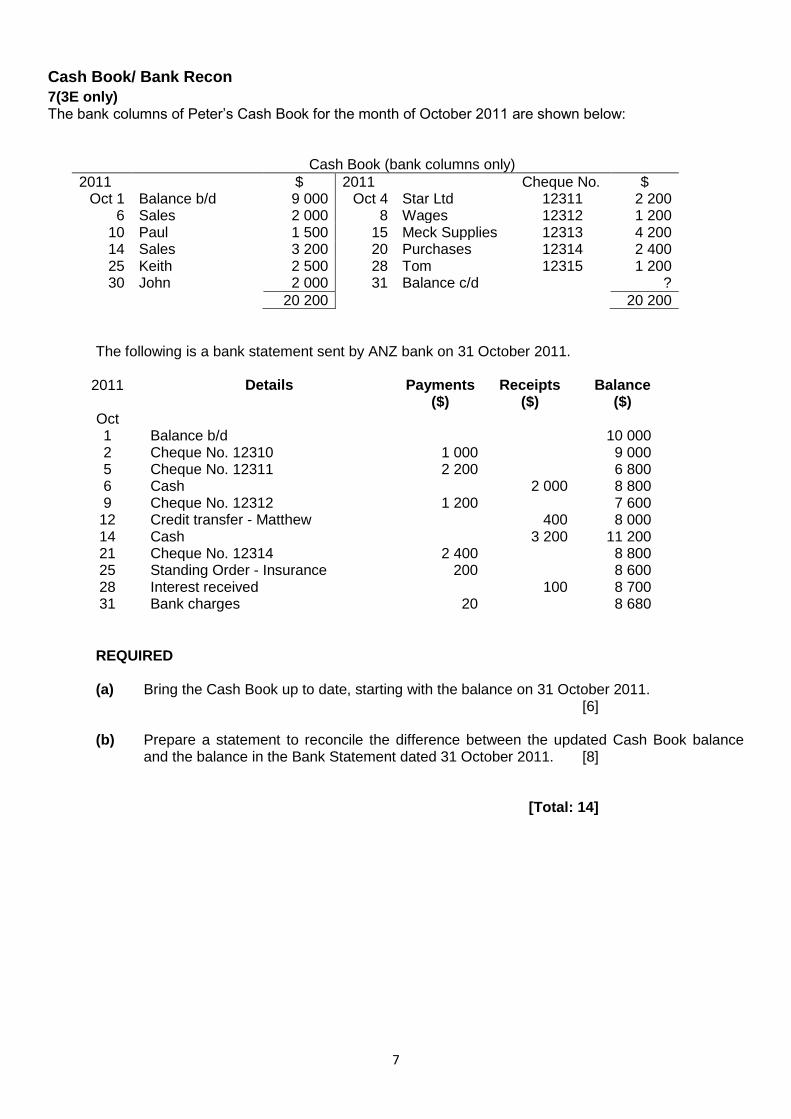

Cash Book/ Bank Recon

7(3E only) The bank columns of Peter‟s Cash Book for the month of October 2011 are shown below:

Cash Book (bank columns only)

2011 $ 2011 Cheque No. $ Oct 1 Balance b/d 9 000 Oct 4 Star Ltd 12311 2 200

6 Sales 2 000 8 Wages 12312 1 200 10 Paul 1 500 15 Meck Supplies 12313 4 200 14 Sales 3 200 20 Purchases 12314 2 400 25 Keith 2 500 28 Tom 12315 1 200 30 John 2 000 31 Balance c/d ?

20 200 20 200

The following is a bank statement sent by ANZ bank on 31 October 2011.

2011 Details Payments

($) Receipts

($) Balance

($) Oct 1 Balance b/d 10 000 2 Cheque No. 12310 1 000 9 000 5 Cheque No. 12311 2 200 6 800 6 Cash 2 000 8 800 9 Cheque No. 12312 1 200 7 600

12 Credit transfer - Matthew 400 8 000 14 Cash 3 200 11 200 21 Cheque No. 12314 2 400 8 800 25 Standing Order - Insurance 200 8 600 28 Interest received 100 8 700 31 Bank charges 20 8 680

REQUIRED

(a) Bring the Cash Book up to date, starting with the balance on 31 October 2011. [6]

(b) Prepare a statement to reconcile the difference between the updated Cash Book balance

and the balance in the Bank Statement dated 31 October 2011. [8] [Total: 14]

8

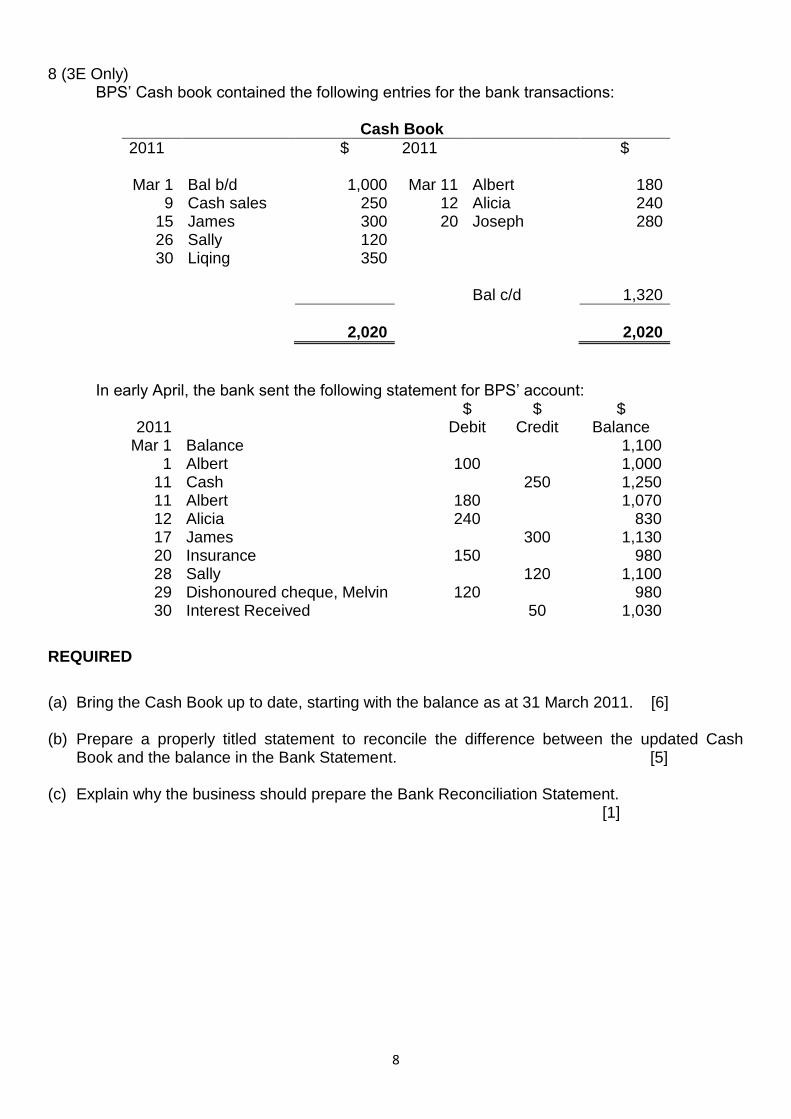

8 (3E Only)

BPS‟ Cash book contained the following entries for the bank transactions:

Cash Book

2011 $ 2011 $

Mar 1 Bal b/d

1,000 Mar 11 Albert 180 9 Cash sales 250 12 Alicia 240

15 James 300 20 Joseph 280 26 Sally 120 30 Liqing 350

Bal c/d

1,320

2,020

2,020

In early April, the bank sent the following statement for BPS‟ account:

REQUIRED

(a) Bring the Cash Book up to date, starting with the balance as at 31 March 2011. [6] (b) Prepare a properly titled statement to reconcile the difference between the updated Cash

Book and the balance in the Bank Statement. [5] (c) Explain why the business should prepare the Bank Reconciliation Statement. [1]

2011 $

Debit $

Credit $

Balance Mar 1 Balance 1,100

1 Albert 100 1,000 11 Cash 250 1,250 11 Albert 180 1,070 12 Alicia 240 830 17 James 300 1,130 20 Insurance 150 980 28 Sally 120 1,100 29 Dishonoured cheque, Melvin 120 980 30 Interest Received 50 1,030

9

8.

The following transactions took place in Jupiter Trading‟s Book in the month of April 2011.

2011 $ Apr 1 Bank balance 7 080

1 Cash balance 3 540 3 Cash sales 2 990 5 Transferred cash from the bank to office 1 020

10 Received cheque of $1 500 from Mars Trading in full settlement of its debt of $1 600

12 Received commission in cash 800 14 Sold goods on credit to Venus Trading 5 000 15 Paid rent by cash 6 000 17 Owner took cash to finance his own holiday 3 200 19 Received bank interest 240 22 Received payment in cash from Venus Trading for

goods sold on April 14 after giving a 5% cash discount

23 Mars Trading‟s cheque on April 10 was bounced 25 Transferred cash from the office to the bank 1 100 27 Jupiter Trading paid for advertising expense using a

cheque 2 600

29 Paid wages in cash 500 30 Deposited all cash, except for $300, into the bank. 30 Closed off the accounts

REQUIRED

(a) Prepare a Three-Column Cash Book for Jupiter Trading for the month of April 2011. [12] (b) Give a reason why a cash discount is given to Venus Trading. [1]

(c) Suggest a reason why Mars Trading‟s cheque bounced. [1]

[Total: 14]

10

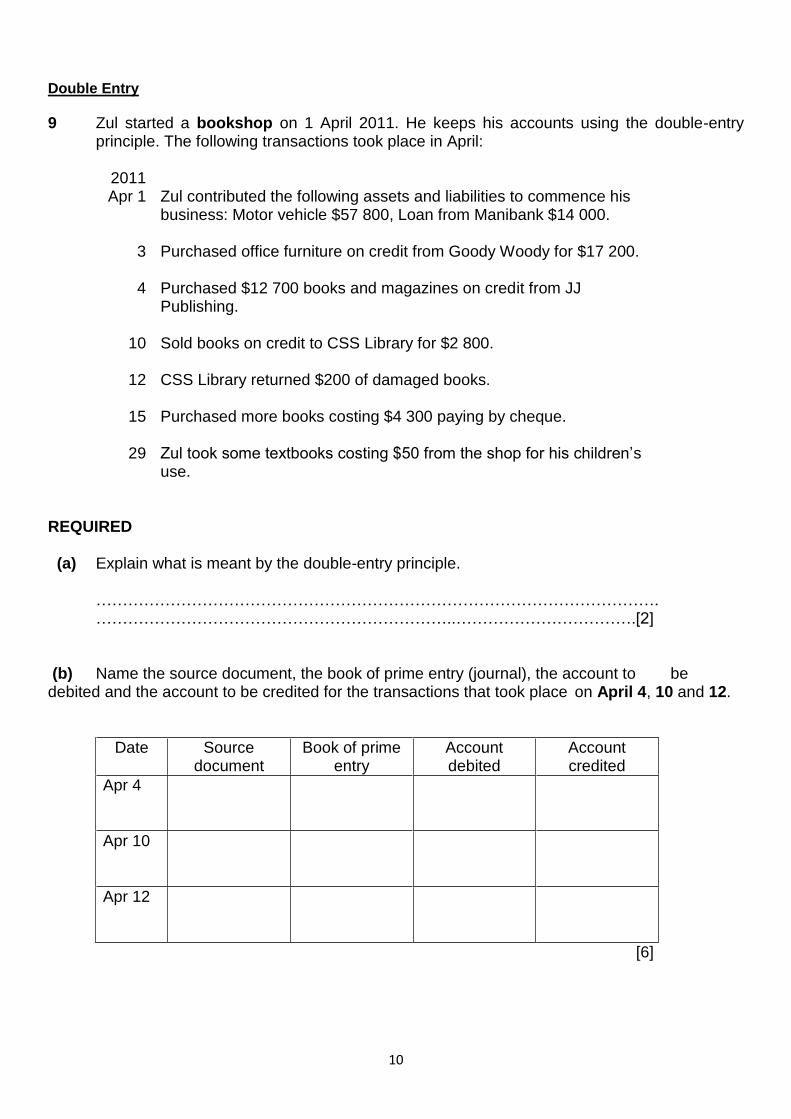

Double Entry

9 Zul started a bookshop on 1 April 2011. He keeps his accounts using the double-entry principle. The following transactions took place in April:

2011 Apr 1 Zul contributed the following assets and liabilities to commence his

business: Motor vehicle $57 800, Loan from Manibank $14 000.

3 Purchased office furniture on credit from Goody Woody for $17 200.

4 Purchased $12 700 books and magazines on credit from JJ Publishing.

10 Sold books on credit to CSS Library for $2 800.

12 CSS Library returned $200 of damaged books.

15 Purchased more books costing $4 300 paying by cheque.

29 Zul took some textbooks costing $50 from the shop for his children‟s use.

REQUIRED (a) Explain what is meant by the double-entry principle.

……………………………………………………………………………………………. …………………………………………………………..…………………………….[2] (b) Name the source document, the book of prime entry (journal), the account to be debited and the account to be credited for the transactions that took place on April 4, 10 and 12.

Date Source document

Book of prime entry

Account debited

Account credited

Apr 4

Apr 10

Apr 12

[6]

11

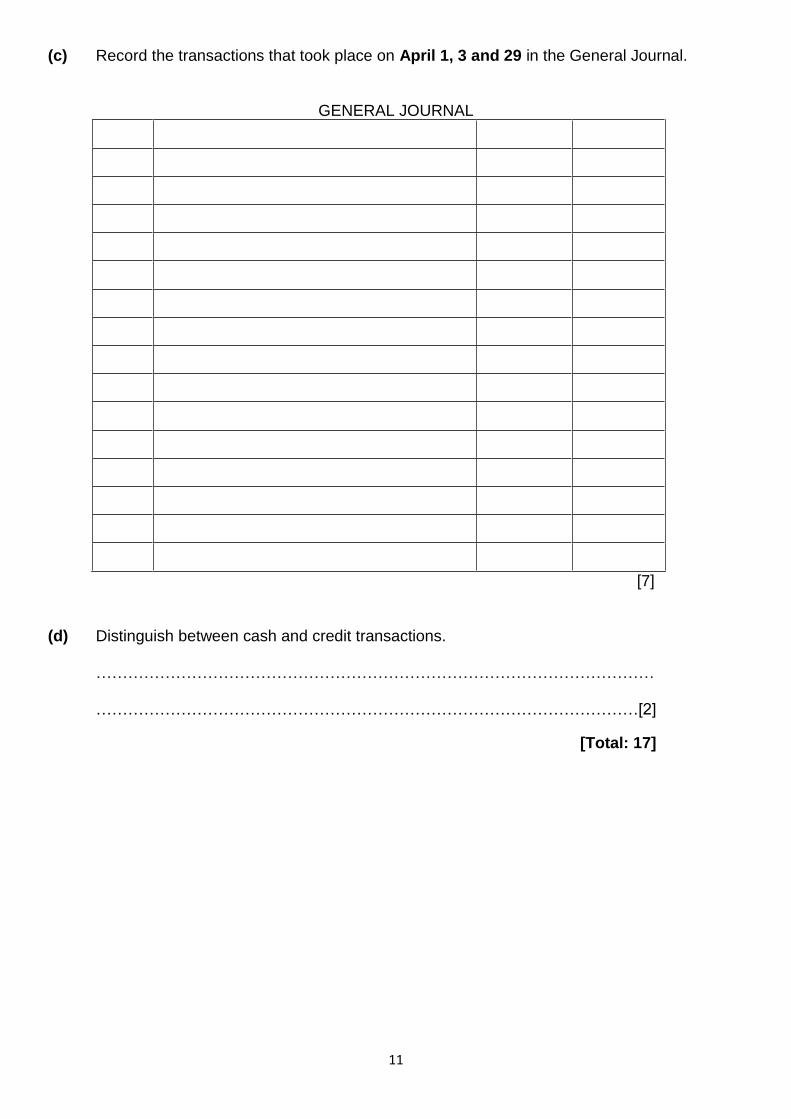

(c) Record the transactions that took place on April 1, 3 and 29 in the General Journal.

GENERAL JOURNAL

[7] (d) Distinguish between cash and credit transactions. …………………………………………………………………………………………… …………………………………………………………………………………………[2]

[Total: 17]

12

10 (a) Prepare the Journal to record the transactions of James in the month of June. Narratives are not

required. [9]

Date Transactions

(i) 5 June 2010 Brought in his personal delivery van worth $4,000 into the business

(ii) 19 June 2010 Received a cheque $1,800 in settlement for $2,000 from Robin.

(iii) 23 June 2010 Paid for utilities $200 by cheque

(iv) 30 June 2010 Deposited $1,000 into the bank, from money withdrawn from the cash box in office

Date Particulars Debit Credit

$ $

(i)

(ii)

(iii)

(iv)

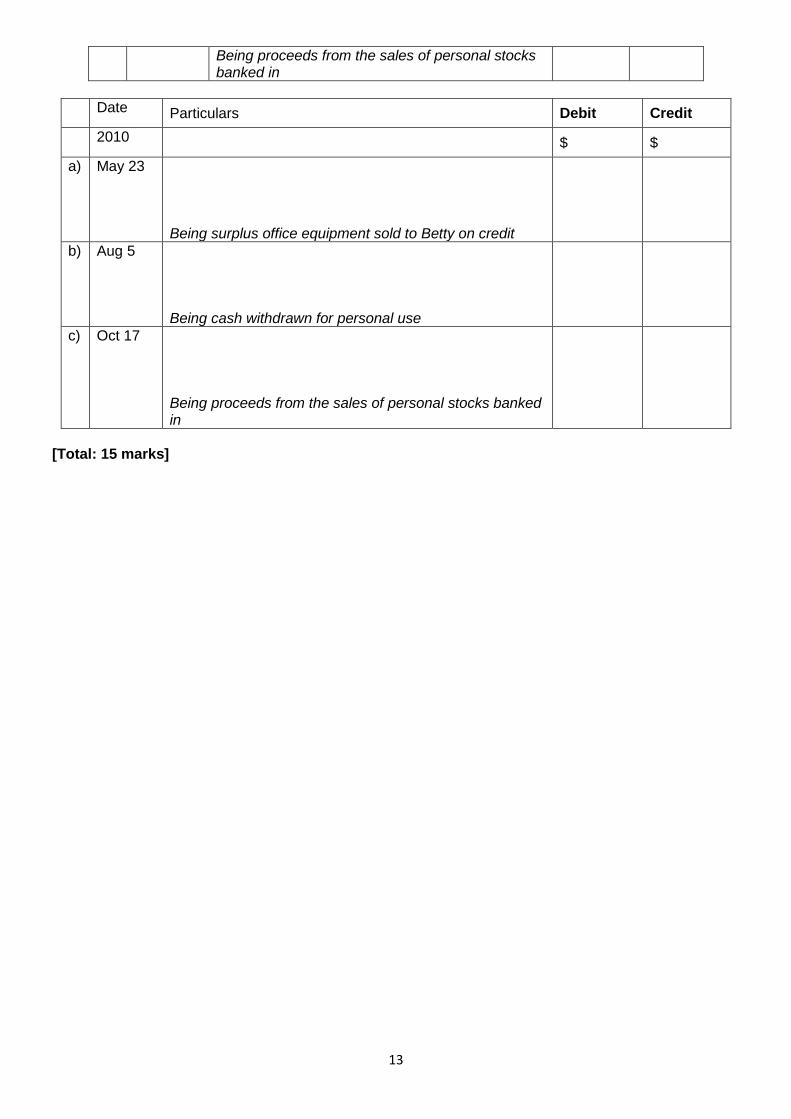

b) Below are some transactions found in James‟ General Journal. The narrations given for each transaction are correct. However, some of the entries are wrong. Correct the entries in the table provided. [6]

Date Particulars Debit Credit

2010

$ $

(i) May 23 Dr Cash Cr Debtor Betty Being surplus office equipment sold to Betty on credit

800 800

(ii) Aug 5

Dr Drawings Cr Capital Being cash withdrawn for personal use

300 300

(iii) Oct 17

Dr Stocks Cr Bank

1,500 1,500

13

Being proceeds from the sales of personal stocks banked in

Date Particulars Debit Credit

2010

$ $

a) May 23 Being surplus office equipment sold to Betty on credit

b) Aug 5

Being cash withdrawn for personal use

c) Oct 17

Being proceeds from the sales of personal stocks banked in

[Total: 15 marks]

14

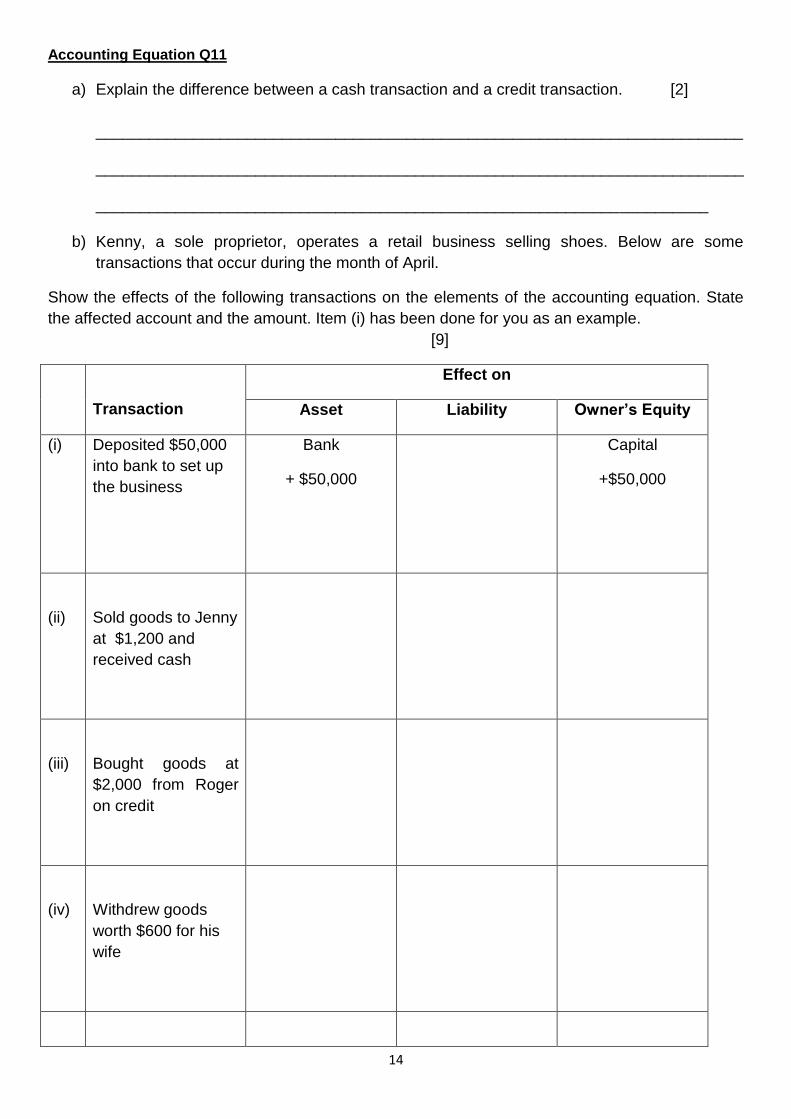

Accounting Equation Q11

a) Explain the difference between a cash transaction and a credit transaction. [2]

_________________________________________________________________________

_________________________________________________________________________

_____________________________________________________________________

b) Kenny, a sole proprietor, operates a retail business selling shoes. Below are some

transactions that occur during the month of April.

Show the effects of the following transactions on the elements of the accounting equation. State

the affected account and the amount. Item (i) has been done for you as an example.

[9]

Transaction

Effect on

Asset Liability Owner’s Equity

(i) Deposited $50,000

into bank to set up

the business

Bank

+ $50,000

Capital

+$50,000

(ii)

Sold goods to Jenny

at $1,200 and

received cash

(iii)

Bought goods at

$2,000 from Roger

on credit

(iv)

Withdrew goods

worth $600 for his

wife

15

(v) Accepted debt

settlement from

Cass - a computer

worth $500 and the

remaining $700

received in cash

12. State the books of original entry and source documents for the following transactions:

(a) Credit Sales $2000

(b) Purchases Returns $500

(c) Purchase of furniture $3000 on credit

(d) Received $1000 cheque from debtor

(e) Payment of postage $3

(f) Cash Purchases $650

Copy and complete the table below on your answer paper. [12]

Transaction Book of Original Entry Source Document

(a)

(b)

(c)

(d)

(e)

(f)

16

13. The following errors were discovered in the book of Mary:

i) $1200 paid for repairs of motor vehicles had been debited to motor vehicle account

ii) A payment of $500 for Rent had been omitted from the books.

iii) Interest received $430, had been debited in the Interest Received account and credited in the Bank account.

iv) A credit note for $240 received from Mavis had been entered in the books as $420.

v) A credit sale to Michelle had been treated as credit purchase from Mitchel.

You are required to:

(a) show the journal entries to correct the above errors. Narrations are not required. [12]

(b) name the type of errors committed in item (i) to (iv). [4]

17

14)

Jenny‟s Cash Book (Bank columns only) for the month of September 2006 was as follows:

Cash Book (Bank columns)

2006 $ 2006 Cheque No. $

Sep 1 Bal b/d 850 Sep 4 Utilities 9010 700

2 Alice 100 8 Audrey 9011 100

15 Andy 130 12 John 9012 140

30 Sales 590 19 Jessie 9013 50

21 Advertising 9014 410

The following Bank Statement was received in early October 2006:

Date Particulars Payments Receipts Balance

2006 $ $ $

Sep 1 Balance b/d 1520

2 Cash 1800 3320

4 Cheque 9010 700 2620

6 Cheque 9009 670 1950

11 Cheque 9011 1100 850

15 Deposit 130 980

20 Standing order –Insurance 108 872

21 Cheque 9014 410 462

26 Cheque 9013 50 412

30 Dividends 400 812

30 Bank charges 9 803

Required: (a) Bring the Cash Book up to date. [6] (There is no need to copy down the whole Cash Book as shown above.) (b) Prepare a statement, under its proper title, to reconcile the difference between your

amended Cash Book balance and the balance in the Bank Statement on 30 September 2006. [4]

(c) Under which sub-heading would the bank balance appear in Jenny‟s Balance Sheet?

Also, state the amount of this bank balance. [2]

18

15

Michael was in business as a merchant and the following balances were extracted from his books on 30 June 2005:

$ Stock (1 January 2005) 7000 Fixtures and fittings 8000 Premises 50000 Motor vehicles 14000 Purchases 41800 Sales 64500 Carriage outwards 1400 Duty on purchases 400 Sales returns 300 Interest received 1500 Cash 300 Stationery 700 Office expenses 2000 Commission revenue 1800 Wages 4200 Mortgage on premises 15000 Debtors 5100 Creditors 6900 Bank overdraft 2300 Drawings 1000 Capital 44200

Stock on 30 June 2005 was valued at $9000 at cost and $11000 at net realisable value. REQUIRED

(a) Prepare the Trading and Profit and Loss Accounts for the half year ended 30 June 2005. [9] (b) Prepare the Balance Sheet as at 30 June 2005. [12] [Total : 21]

19

16. Meyer Bros had the following balances in its books on 1 September 2007:

Debtor, Aliston $4 340 Dr

Creditor, Kang AH $1 900 Cr The following relevant transactions in September were extracted from Meyer Bros‟ books:

Sep 5 Received a cheque, $1 000 from Aliston

9 Paid Kang AH the amount owing on 1 Sep, less 5% discount

12 Aliston bought goods on credit at $2 600 less 25% trade discount

16 Received defective goods from Aliston, list price being $300

21 Meyer Bros. purchased goods on credit, $1 200 from Kang AH

23 Received part-payment from Aliston, $2 340 to settle a debt of $2 500

29 Received a debit note for $180 from Kang AH for goods undercharged

Required

Write up the ledger accounts for Debtor, Aliston and Creditor, Kang AH in the books of Meyer Bros. from the information above. Balance off both accounts on 30 Sep 2007. Dates and details must be shown. [12]

Debtor, Aliston

Date Particulars $ Date Particulars $

Creditor, Kang AH

Date Particulars $ Date Particulars $

20

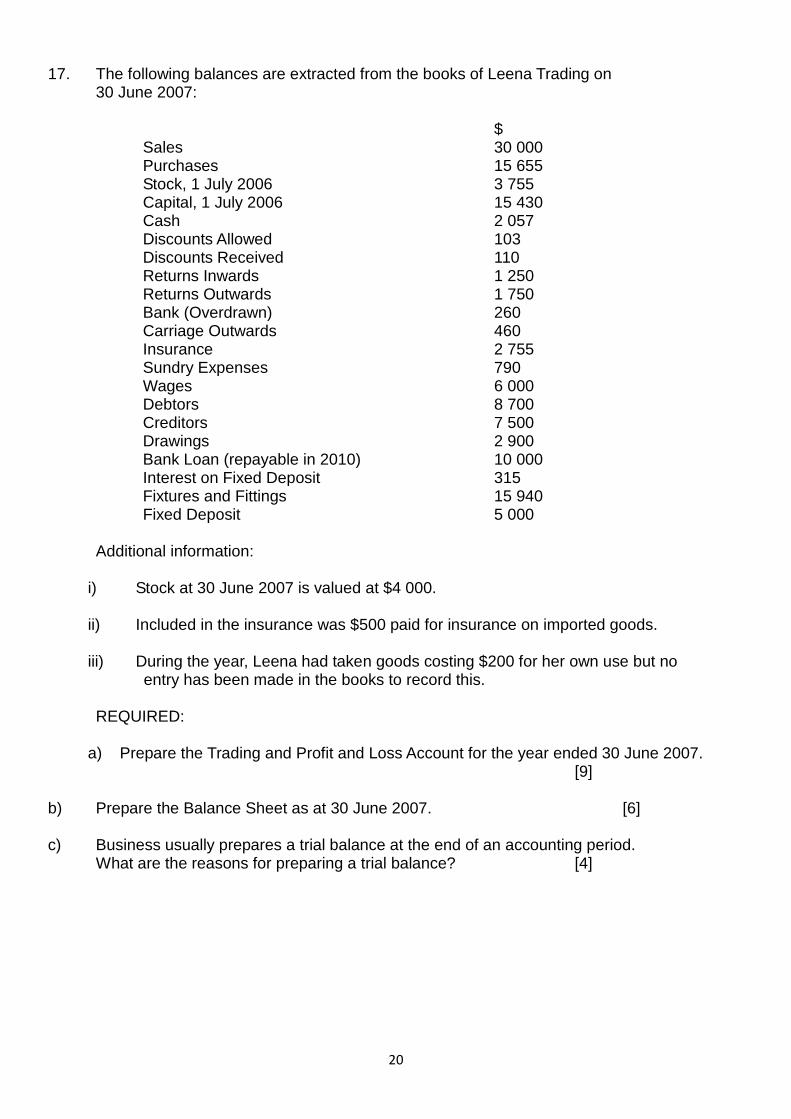

17. The following balances are extracted from the books of Leena Trading on 30 June 2007:

$ Sales 30 000 Purchases 15 655 Stock, 1 July 2006 3 755 Capital, 1 July 2006 15 430 Cash 2 057 Discounts Allowed 103 Discounts Received 110 Returns Inwards 1 250 Returns Outwards 1 750 Bank (Overdrawn) 260 Carriage Outwards 460 Insurance 2 755 Sundry Expenses 790 Wages 6 000 Debtors 8 700 Creditors 7 500 Drawings 2 900 Bank Loan (repayable in 2010) 10 000 Interest on Fixed Deposit 315 Fixtures and Fittings 15 940 Fixed Deposit 5 000

Additional information:

i) Stock at 30 June 2007 is valued at $4 000.

ii) Included in the insurance was $500 paid for insurance on imported goods.

iii) During the year, Leena had taken goods costing $200 for her own use but no entry has been made in the books to record this. REQUIRED:

a) Prepare the Trading and Profit and Loss Account for the year ended 30 June 2007. [9] b) Prepare the Balance Sheet as at 30 June 2007. [6] c) Business usually prepares a trial balance at the end of an accounting period. What are the reasons for preparing a trial balance? [4]