Embed Size (px)

Citation preview

Automotive transactions and trendsGlobal automotive mergers and acquisitions review3Q 2014 (July–September)

2 | Automotive transactions and trends 3Q 2014

Mark ShortGlobal Automotive and Transportation Industry Leader, Transaction Advisory Services

“ The automotive sector is the leading industry sector for driving future transactions. Optimism in the sector has never been higher. Stronger balance sheets, combined with continued debt financing opportunities, are positioning automotive companies to embark on a new wave of transactional initiatives. Middle-market transactions, those valued up to US$250 million, will comprise the bulk of deals in the sector. Continued focus on expanding core product opportunities, coupled with increasing the mix of new products and services, are key criteria for driving M&A activity.”

M&A momentum in the auto sector to be driven by middle-market transactions

Executive summaryRecord deal activity achieved in the automotive sector in 3Q14 driven by the supplier sub-sector and developed markets

Sub-segment insights Regional scenario

Share of suppliers in deal values, highest in last two years

84%Share of US (top target market) in deal values

79%

Growth in fleet and leasing deal values y-o-y

2xShare of Germany (top acquiring market) in deal values

2/3

Growth in deal values y-o-y and a 48% increase q-o-q (second highest in last eight quarters)

Rise in deal volumes y-o-y, indicating a sharp rise in average deal size y-o-y

3X 8%Deal activity

3Automotive transactions and trends 3Q 2014 |

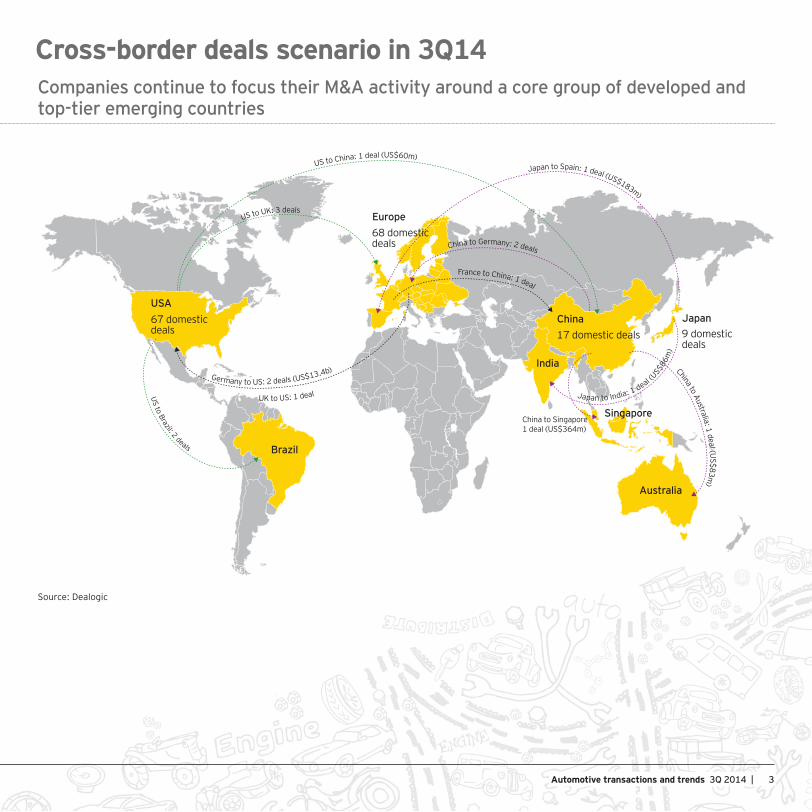

Cross-border deals scenario in 3Q14Companies continue to focus their M&A activity around a core group of developed and top-tier emerging countries

USA

Brazil

Europe

India

Singapore

Australia

US to China: 1 deal (US$60m)

UK to US: 1 deal

Germany to US: 2 deals (US$13.4b)

Japan to Spain: 1 deal (US$183m)

68 domestic deals

China17 domestic deals 9 domestic

deals

67 domestic deals

US to Brazil: 2 deals

US to UK: 3 deals

China to Germany: 2 deals

France to China: 1 deal

China to Australia: 1 deal (US$83m)

Japan to India: 1 deal (US$

86m

)

China to Singapore1 deal (US$364m)

Japan

Source: Dealogic

4 | Automotive transactions and trends 3Q 2014

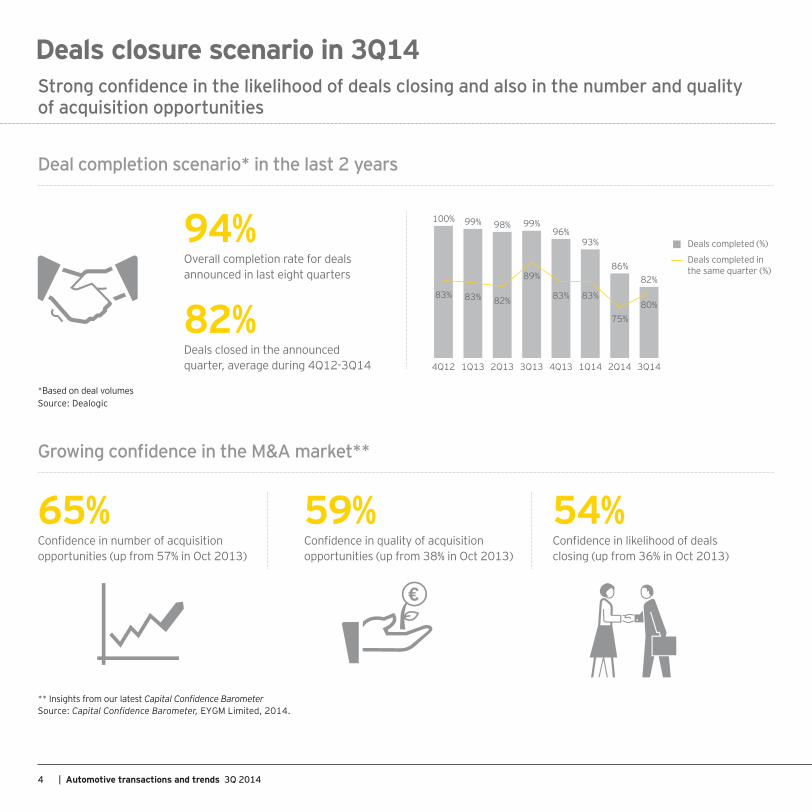

Strong confidence in the likelihood of deals closing and also in the number and quality of acquisition opportunities

Deals closure scenario in 3Q14

Source: Dealogic

100% 99% 98% 99%96%

93%

86%82%

83% 83% 82%

89%

83% 83%

75%80%

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14

Deals completed (%)

Deals completed in the same quarter (%)

Overall completion rate for deals announced in last eight quarters

94%

Deals closed in the announced quarter, average during 4Q12-3Q14

82% *Based on deal volumes

Deal completion scenario* in the last 2 years

Growing confidence in the M&A market**

** Insights from our latest Capital Confidence BarometerSource: Capital Confidence Barometer, EYGM Limited, 2014.

Confidence in number of acquisition opportunities (up from 57% in Oct 2013)

65%Confidence in likelihood of deals closing (up from 36% in Oct 2013)

54%Confidence in quality of acquisition opportunities (up from 38% in Oct 2013)

59%

5Automotive transactions and trends 3Q 2014 |

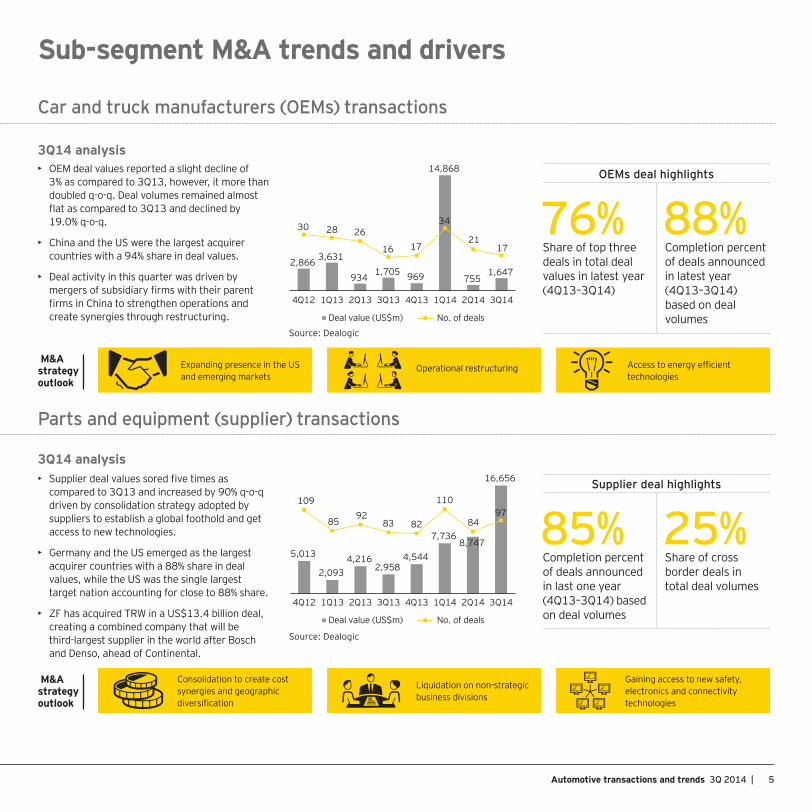

Parts and equipment (supplier) transactions

Sub-segment M&A trends and drivers

Car and truck manufacturers (OEMs) transactions

3Q14 analysis

3Q14 analysis

• OEM deal values reported a slight decline of 3% as compared to 3Q13, however, it more than doubled q-o-q. Deal volumes remained almost flat as compared to 3Q13 and declined by 19.0% q-o-q.

• China and the US were the largest acquirer countries with a 94% share in deal values.

• Deal activity in this quarter was driven by mergers of subsidiary firms with their parent firms in China to strengthen operations and create synergies through restructuring.

• Supplier deal values sored five times as compared to 3Q13 and increased by 90% q-o-q driven by consolidation strategy adopted by suppliers to establish a global foothold and get access to new technologies.

• Germany and the US emerged as the largest acquirer countries with a 88% share in deal values, while the US was the single largest target nation accounting for close to 88% share.

• ZF has acquired TRW in a US$13.4 billion deal, creating a combined company that will be third-largest supplier in the world after Bosch and Denso, ahead of Continental.

Source: Dealogic

Source: Dealogic

76%

85%

Share of top three deals in total deal values in latest year (4Q13–3Q14)

Completion percent of deals announced in last one year (4Q13–3Q14) based on deal volumes

88%

25%

Completion percent of deals announced in latest year (4Q13–3Q14) based on deal volumes

Share of cross border deals in total deal volumes

OEMs deal highlights

Supplier deal highlights

2,866 3,631

934 1,705 969

14,868

755 1,647

30 28 26

16 17

34

2117

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14

Deal value (US$m) No. of deals

5,013

2,093 4,216

2,958 4,544

7,736 8,747

16,656

109

8592

83 82

110

8497

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14

Deal value (US$m) No. of deals

M&A strategy outlook

Expanding presence in the US and emerging markets

Operational restructuring Access to energy efficient technologies

M&A strategy outlook

Consolidation to create cost synergies and geographic diversification

Gaining access to new safety, electronics and connectivity technologies

Liquidation on non-strategic business divisions

6 | Automotive transactions and trends 3Q 2014

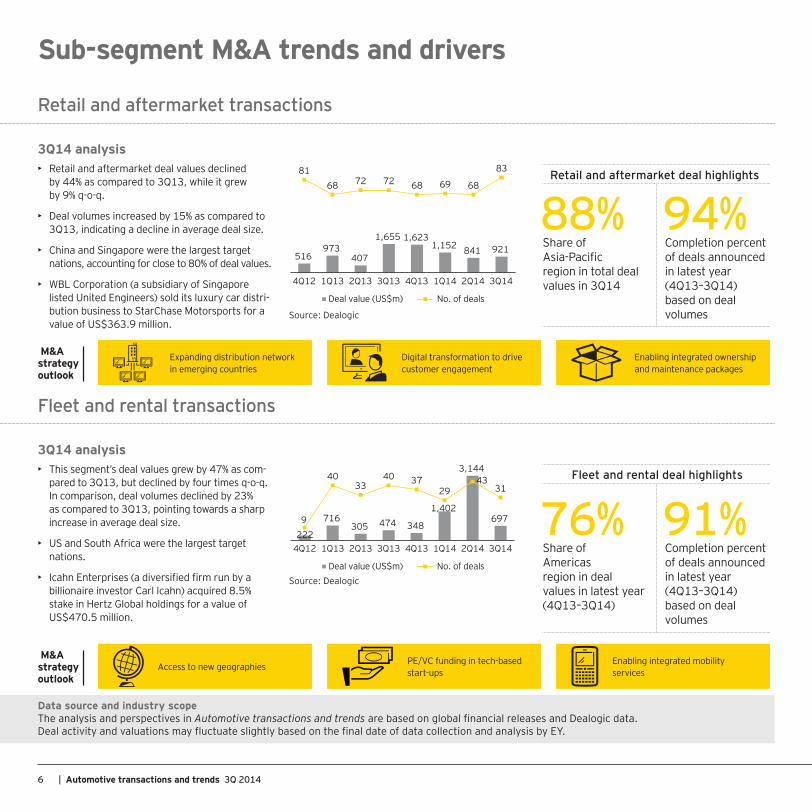

Fleet and rental transactions

3Q14 analysis• This segment’s deal values grew by 47% as com-

pared to 3Q13, but declined by four times q-o-q. In comparison, deal volumes declined by 23% as compared to 3Q13, pointing towards a sharp increase in average deal size.

• US and South Africa were the largest target nations.

• Icahn Enterprises (a diversified firm run by a billionaire investor Carl Icahn) acquired 8.5% stake in Hertz Global holdings for a value of US$470.5 million.

Source: Dealogic

76%Share of Americasregion in deal values in latest year (4Q13–3Q14)

91%Completion percent of deals announced in latest year (4Q13–3Q14) based on deal volumes

Fleet and rental deal highlights

Deal value (US$m) No. of deals

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14222

716 305 474 348

1,402

3,144

697 9

4033

40 3729

4331

3Q14 analysis• Retail and aftermarket deal values declined

by 44% as compared to 3Q13, while it grew by 9% q-o-q.

• Deal volumes increased by 15% as compared to 3Q13, indicating a decline in average deal size.

• China and Singapore were the largest target nations, accounting for close to 80% of deal values.

• WBL Corporation (a subsidiary of Singapore listed United Engineers) sold its luxury car distri-bution business to StarChase Motorsports for a value of US$363.9 million.

Source: Dealogic

88%Share of Asia-Pacificregion in total deal values in 3Q14

94%Completion percent of deals announced in latest year (4Q13–3Q14) based on deal volumes

Retail and aftermarket deal highlights

4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14

516 973

407

1,655 1,623 1,152 841 921

8168 72 72 68 69 68

83

Deal value (US$m) No. of deals

Data source and industry scopeThe analysis and perspectives in Automotive transactions and trends are based on global financial releases and Dealogic data.Deal activity and valuations may fluctuate slightly based on the final date of data collection and analysis by EY.

Retail and aftermarket transactions

Sub-segment M&A trends and drivers

Expanding distribution network in emerging countries

Digital transformation to drive customer engagement

Enabling integrated ownership and maintenance packages

M&A strategy outlook

Access to new geographies PE/VC funding in tech-based start-ups

Enabling integrated mobility services

M&A strategy outlook

7Automotive transactions and trends 3Q 2014 |

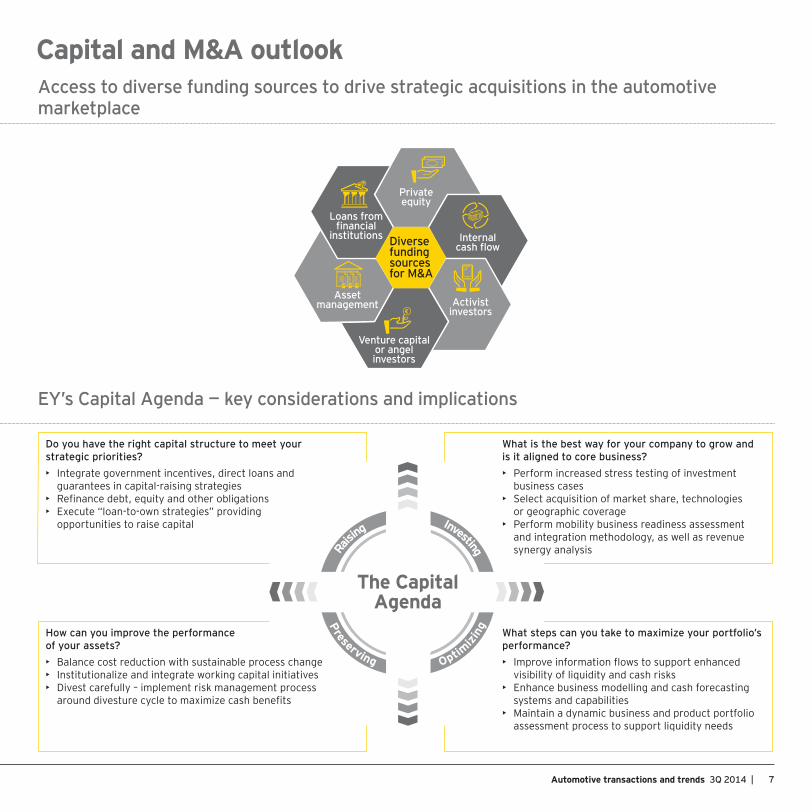

The CapitalAgenda

Raisin

g Investing

Preserving Optim

izing

Do you have the right capital structure to meet your strategic priorities?• Integrate government incentives, direct loans and

guarantees in capital-raising strategies• Refinance debt, equity and other obligations• Execute “loan-to-own strategies” providing

opportunities to raise capital

What is the best way for your company to grow and is it aligned to core business?• Perform increased stress testing of investment

business cases• Select acquisition of market share, technologies

or geographic coverage• Perform mobility business readiness assessment

and integration methodology, as well as revenue synergy analysis

How can you improve the performance of your assets?• Balance cost reduction with sustainable process change• Institutionalize and integrate working capital initiatives• Divest carefully – implement risk management process

around divesture cycle to maximize cash benefits

What steps can you take to maximize your portfolio’s performance?• Improve information flows to support enhanced

visibility of liquidity and cash risks• Enhance business modelling and cash forecasting

systems and capabilities• Maintain a dynamic business and product portfolio

assessment process to support liquidity needs

Capital and M&A outlook

EY’s Capital Agenda — key considerations and implications

Diverse funding sources for M&A

Internal cash flow

Private equity

Loans from financial

institutions

Asset management

Venture capital or angel investors

Activist investors

Access to diverse funding sources to drive strategic acquisitions in the automotive marketplace

For a conversation about your capital strategy, please contact us:

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2014 EYGM Limited.All Rights Reserved.

EYG no. ED0131CSG/GSC2014/1526011ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/automotive

Acknowledgments

Special thanks to EY Knowledge automotive analysts Abhishek Gupta and Bhaskar Mazumdar for the analysis and compilation of this study.

Randall MillerGlobal Automotive and Transportation Industry Leader +1 313 628 8642 [email protected]

Mark ShortGlobal Automotive and Transportation Industry Leader Transaction Advisory Services +1 313 628 8760 [email protected]

Jim CarterAmericas Automotive and Transportation Industry Leader Transaction Advisory Services +1 313 628 8690 [email protected]

Stephan HellmannPartner, Transaction Advisory Services + 49 6196 996 25030 [email protected]

Tony TsangFar East and Oceania Automotive Industry Leader Transaction Advisory Services +86 21 2228 2358 [email protected]

Peter WespPartner, Transaction Advisory Services +49 6196 996 27282 [email protected]

Anil ValsanGlobal Automotive and Transportation Lead Analyst +44 20 7951 6879 [email protected]

Regan GrantGlobal Automotive and Transportation Marketing Leader +1 313 628 8974 [email protected]