Embed Size (px)

Citation preview

4 OCTOBER 2012

MIDF EQUITY BEAT Thursday, 04 October 2012

2

MIDF Research Team | 603-2772 1650 | [email protected]

OIL & GAS SECTOR Sustained Growth in Local O&G Awards MAINTAIN POSITIVE

We reiterate our POSITIVE stance on the sector based on favourable oil price movement, sustained local oil

and gas activities and uptick in global exploration activities. For Jan-Sep12, the West Texas Intermediate (WTI)

crude averaged USD96.2pb. We upgrade our WTI price forecast for 2012 from USD90pb to USD94pb (+4.4%),

expecting WTI to trade at an average of USD90pb in 4Q12. We maintain our forecast of average WTI price in

2013 at USD90pb.

Our BUYS are SapuraKencana, WahSeong, Dialog and Gas Malaysia.

OIL PRICES

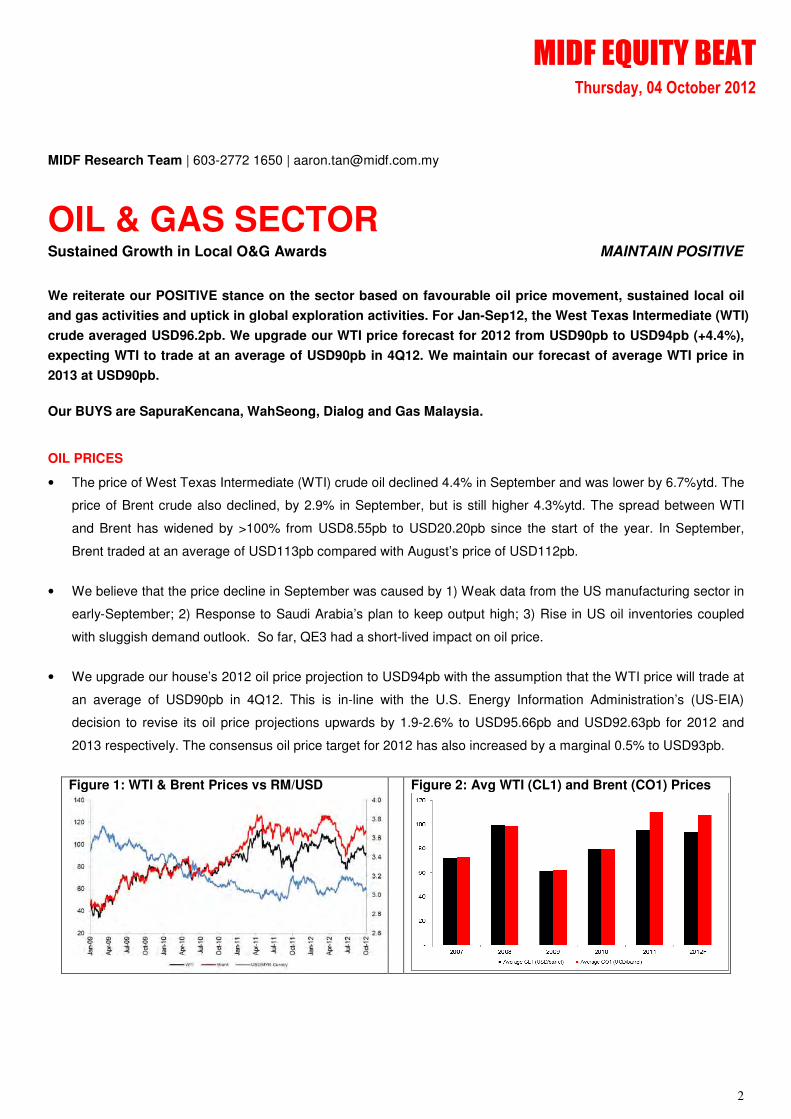

• The price of West Texas Intermediate (WTI) crude oil declined 4.4% in September and was lower by 6.7%ytd. The

price of Brent crude also declined, by 2.9% in September, but is still higher 4.3%ytd. The spread between WTI

and Brent has widened by >100% from USD8.55pb to USD20.20pb since the start of the year. In September,

Brent traded at an average of USD113pb compared with August’s price of USD112pb.

• We believe that the price decline in September was caused by 1) Weak data from the US manufacturing sector in

early-September; 2) Response to Saudi Arabia’s plan to keep output high; 3) Rise in US oil inventories coupled

with sluggish demand outlook. So far, QE3 had a short-lived impact on oil price.

• We upgrade our house’s 2012 oil price projection to USD94pb with the assumption that the WTI price will trade at

an average of USD90pb in 4Q12. This is in-line with the U.S. Energy Information Administration’s (US-EIA)

decision to revise its oil price projections upwards by 1.9-2.6% to USD95.66pb and USD92.63pb for 2012 and

2013 respectively. The consensus oil price target for 2012 has also increased by a marginal 0.5% to USD93pb.

Figure 1: WTI & Brent Prices vs RM/USD

Figure 2: Avg WTI (CL1) and Brent (CO1) Prices

MIDF EQUITY BEAT Thursday, 04 October 2012

3

Table 1: Crude Oil Price Forecasts CY12 (USDpb)

Average WTI (USDpb) Latest Previous Revision (%) YoY (%)

2012F 2013F 2012F 2013F 2012F 2013F 2012F 2013F

US EIA 95.66 92.63 93.90 90.25 1.9% 2.6% 0.8% -3.2%

Consensus 93.00 96.00 92.50 96.40 0.5% -0.4% -2.0% 3.2%

MIDFR 94.00 90.00 90.00 90.00 4.4% 0.0% -5.1% 0.0%

Sources: US EIA, Bloomberg, MIDFR

Table 2: Historical Crude Oil WTI Prices (USDpb)

Month-

end Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12

USDpb 98.48 107.07 103.02 104.87 86.53 84.96 88.06 96.47 92.19

MoM -0.4% 8.7% -3.8% 1.8% -17.5% -1.8% 3.6% 9.6% -4.4%

YoY 6.8% 10.4% -3.5% -8.0% -15.7% -11.0% -8.0% 8.6% 16.4%

Sources: US EIA, Bloomberg, MIDFR

WORLD CRUDE OIL DEMAND (CONSUMPTION) – JULY12

• The International Energy Agency (IEA) finally increased (after a series of downward revisions) its 2012 global oil

demand outlook to 89.8mbpd from 89.6mbpd previously. However, this slight upgrade is mainly due to revisions in

absolute demand by 100kbpd for both 2012 and 2013. The IEA expects demand to grow at a steady rate of

around 0.8mbpd in both 2012 and 2013 on the back of a global GDP growth of 3.3% and 3.6% for 2012 and 2013

respectively. World demand is expected to hit 90.6mbpd in 2013.

• The IEA noted that the pace of oil demand growth is expected to remain relatively steady over the next eighteen

month with annual gains of 0.8mbpd for both 2012 and 2013. This modest growth rate stems from the sluggish

global economic activity, historically elevated oil price and global improvements in energy efficiency.

• It is worth noting that despite the sedate headline growth, changes in consumption varied greatly by product.

Gasoil demand is forecast to expand more rapidly than oil as a whole, with gains of 1.1% in 2012 to 26.4mbpd

and 1.4% in 2013 to 26.8mbpd. Push factors include industrial growth, power generation and shift in transportation

fuel to diesel.

• The US-EIA is of the view that global oil consumption for 2012 and 2013 will be 89.09mbpd (from 88.83mbpd

previously) and 90.10mbpd (from 89.70mbpd previously) respectively, still marginally lower than the IEA’s forecast

for the same period by 0.5-0.7mbpd.

MIDF EQUITY BEAT Thursday, 04 October 2012

4

WORLD CRUDE OIL SUPPLY (PRODUCTION) – AUGUST12

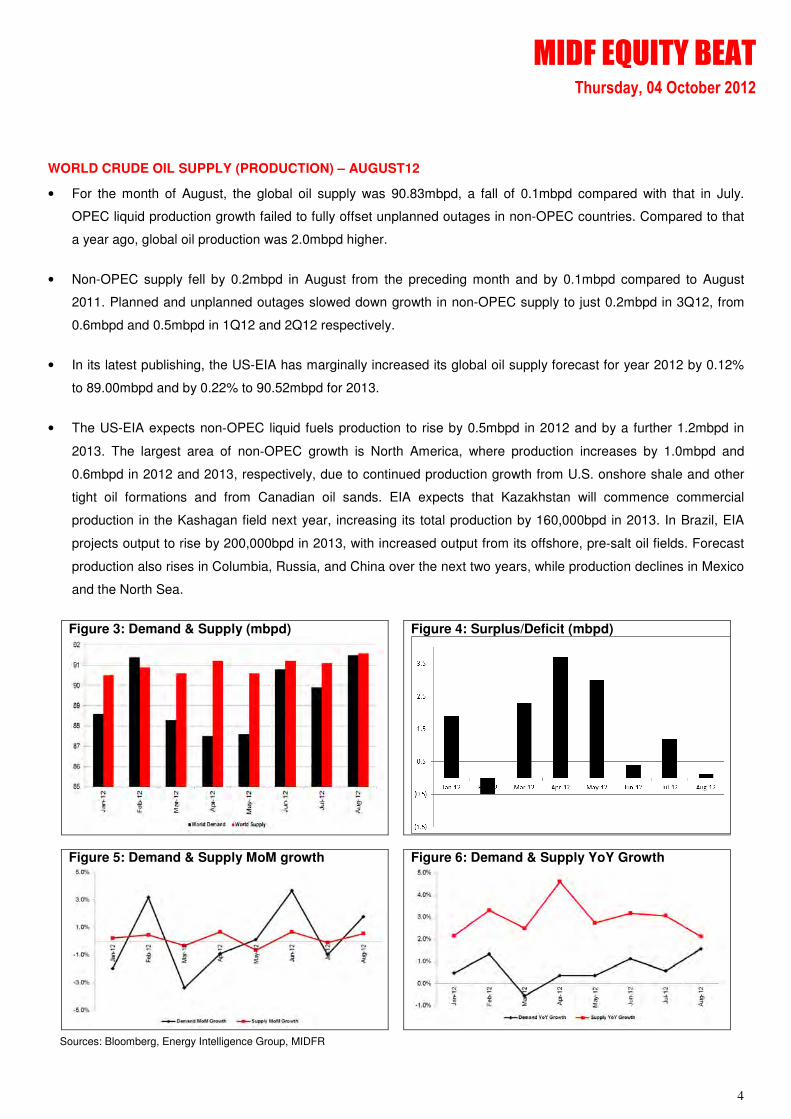

• For the month of August, the global oil supply was 90.83mbpd, a fall of 0.1mbpd compared with that in July.

OPEC liquid production growth failed to fully offset unplanned outages in non-OPEC countries. Compared to that

a year ago, global oil production was 2.0mbpd higher.

• Non-OPEC supply fell by 0.2mbpd in August from the preceding month and by 0.1mbpd compared to August

2011. Planned and unplanned outages slowed down growth in non-OPEC supply to just 0.2mbpd in 3Q12, from

0.6mbpd and 0.5mbpd in 1Q12 and 2Q12 respectively.

• In its latest publishing, the US-EIA has marginally increased its global oil supply forecast for year 2012 by 0.12%

to 89.00mbpd and by 0.22% to 90.52mbpd for 2013.

• The US-EIA expects non‐OPEC liquid fuels production to rise by 0.5mbpd in 2012 and by a further 1.2mbpd in

2013. The largest area of non‐OPEC growth is North America, where production increases by 1.0mbpd and

0.6mbpd in 2012 and 2013, respectively, due to continued production growth from U.S. onshore shale and other

tight oil formations and from Canadian oil sands. EIA expects that Kazakhstan will commence commercial

production in the Kashagan field next year, increasing its total production by 160,000bpd in 2013. In Brazil, EIA

projects output to rise by 200,000bpd in 2013, with increased output from its offshore, pre‐salt oil fields. Forecast

production also rises in Columbia, Russia, and China over the next two years, while production declines in Mexico

and the North Sea.

Figure 3: Demand & Supply (mbpd)

Figure 4: Surplus/Deficit (mbpd)

Figure 5: Demand & Supply MoM growth Figure 6: Demand & Supply YoY Growth

Sources: Bloomberg, Energy Intelligence Group, MIDFR

MIDF EQUITY BEAT Thursday, 04 October 2012

5

Table 3: Global Oil Demand Forecasts (mil barrels/day)

2011E 2012F 2012F growth OECD

Non-OECD

Total +/-* OECD Non-

OECD Total +/-*

IEA 46.6 42.4 89.0 0.20 46.2 43.5 89.7 0.10 0.79%

OPEC 45.7 42.2 87.9 0.10 45.6 43.2 88.7 0.04 0.96%

US EIA 46.6 42.4 89.0 0.90 46.2 43.5 89.7 -0.20 0.79%

Average 88.6 0.43 89.4 -0.02 0.84%

Sources: US EIA, IEA, OPEC, MIDFR *Compared with the forecasts in previous month

Table 4: Global Oil Supply Forecasts (mil barrels/day)

2011E 2012F 2012F growth OECD

Non-OECD

Non-OPEC

Total +/-* OECD Non-

OECD Non-

OPEC Total +/-*

IEA 18.9 29.9 52.8 88.4 88.4 19.8 29.4 53.2 nm na nm

OPEC 20.1 32.4 35.1 87.6 87.6 20.9 32.3 - nm na nm

US EIA 21.6 68.5 51.6 87.1 87.1 22.4 66.6 52.5 89.0 89.0 2.19%

Average 87.7 na 89.0 na

Sources: US EIA, MIDFR *Compared with the forecasts in previous month

LIST OF MAJOR CONTRACTS AWARDED IN 2012 FOR COMPANIES LISTED ON BURSA MALAYSIA

• Year-to-date, about to RM7.7b worth of contracts have been awarded to our local listed O&G players. For the

month of September, about RM663.9m worth of new jobs were awarded, up by more than 14.8%mom; namely to

SapuraKencana (BUY; TP: RM2.74), Handal Resources (Not Rated), Coastal Contracts (Not Rated), Favelle

Favco (Not Rated) and Muhibbah Engineering (Not Rated).

• In terms of number of contracts, 2H12 is turning out to be more exciting than 1H12. For the remaining part of the

year, we can expect a possible Floating, Production, Storage and Offloading (FPSO) contract to be awarded,

numerous local hook-up and commissioning (HUC) jobs and vessel sale/chartering contracts.

• We believe that the PAN Malaysia HUC works which was called for tender in July this year will further excite the

industry. The umbrella project, worth about RM10b, is made up of nine contracts which will benefit many local

HUC players. Key beneficiaries include Dayang (unrated; FV: RM2.32), SapuraKencana (BUY; TP: RM2.74) and

Petra Energy (unrated). We believe that awards will likely be in 4Q12 or early 1Q13.

• In addition to that, the North Malay Basin, which has seen a commitment of RM16.4b from Petronas and Hess, is

likely to see some jobs being awarded. Further north of that region is the Thai-Malaysia Joint Development Area,

another potential source of job awards. Sources indicate that tenders for pipe manufacturing for the North Malay

Basin has been called for and tenders for pipe coating will follow soon after. Potential local beneficiaries for this

include Malaysia Marine and Heavy Engineering (HOLD; TP: RM5.06) and Wah Seong Corp (BUY @ RM2.13)

MIDF EQUITY BEAT Thursday, 04 October 2012

6

• The FPSO segment of the value chain will also see more excitement this 2H12. We gather that there are up to

four FPSOs which could be up for grabs in the immediate term. Fields which require FPSOs are Belud, Kamelia,

Balai, Dahlia & Teratai and Shell’s E6 field. The potential beneficiary is Bumi Armada (NEUTRAL; TP: RM3.64)

• Figure 7 shows the total number and value of contracts awarded to O&G companies listed on Bursa Malaysia.

YTD, RM2b worth of contracts were awarded by Petronas’ subsidiaries and RM5.7b worth of jobs awarded by

foreign-owned companies. For the month of September, all the projects tracked were awarded by non-Petronas

entities. For the third month running, this supports our notion that our local players do not depend solely and

heavily on Petronas which mitigates the risk of contract dependency on a single entity. We have not included

news that Petra Energy Bhd (Not rated) has been chosen as the local partner for Coastal Energy to develop the

Kapal, Banang and Meranti marginal fields as no formal announcement and no contract value have been

disclosed. Market speculation is that the value of the contract could be USD0.5-1b.

• The latest major news reported was that a new oil and gas storage and refining facility, dubbed the Sabah Oil

Terminal is being planned in Sipitang Sabah, at an estimated cost of RM8.5b.

Figure 7: 9M12 Contracts awarded by Petronas and non-Petronas

Source: MIDFR, Bursa Malaysia

MIDF EQUITY BEAT Thursday, 04 October 2012

7

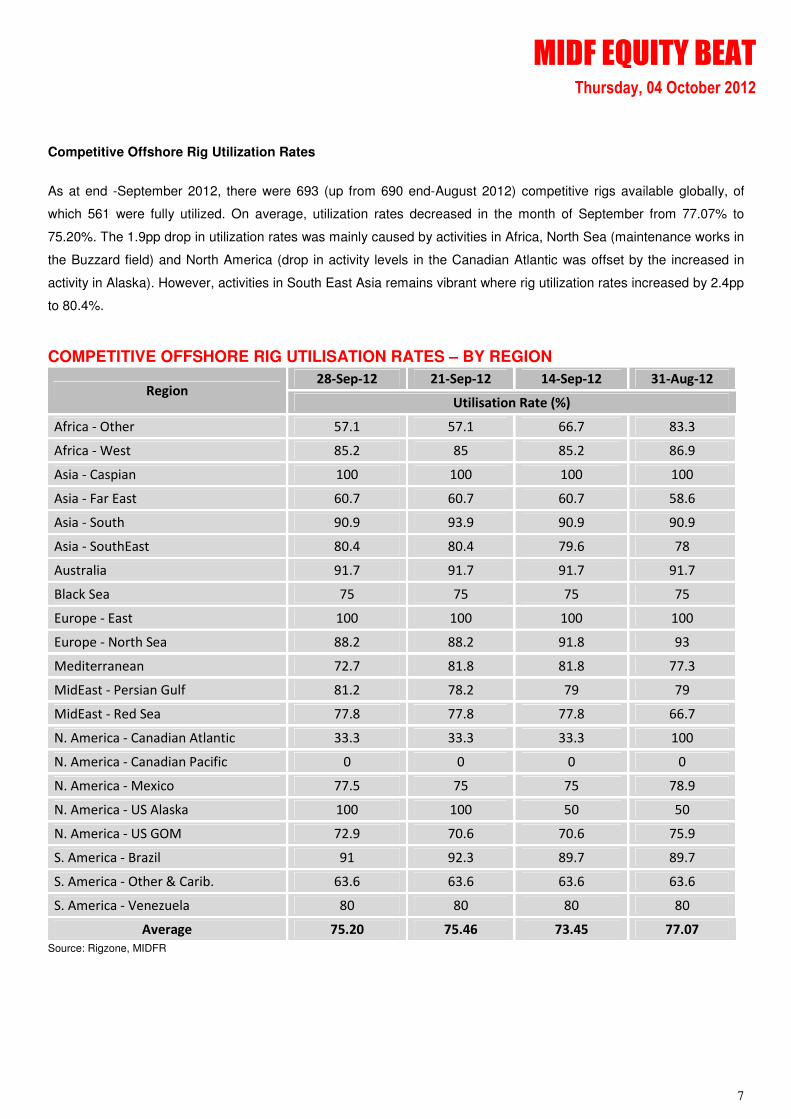

Competitive Offshore Rig Utilization Rates

As at end -September 2012, there were 693 (up from 690 end-August 2012) competitive rigs available globally, of

which 561 were fully utilized. On average, utilization rates decreased in the month of September from 77.07% to

75.20%. The 1.9pp drop in utilization rates was mainly caused by activities in Africa, North Sea (maintenance works in

the Buzzard field) and North America (drop in activity levels in the Canadian Atlantic was offset by the increased in

activity in Alaska). However, activities in South East Asia remains vibrant where rig utilization rates increased by 2.4pp

to 80.4%.

COMPETITIVE OFFSHORE RIG UTILISATION RATES – BY REGION

Region 28-Sep-12 21-Sep-12 14-Sep-12 31-Aug-12

Utilisation Rate (%)

Africa - Other 57.1 57.1 66.7 83.3

Africa - West 85.2 85 85.2 86.9

Asia - Caspian 100 100 100 100

Asia - Far East 60.7 60.7 60.7 58.6

Asia - South 90.9 93.9 90.9 90.9

Asia - SouthEast 80.4 80.4 79.6 78

Australia 91.7 91.7 91.7 91.7

Black Sea 75 75 75 75

Europe - East 100 100 100 100

Europe - North Sea 88.2 88.2 91.8 93

Mediterranean 72.7 81.8 81.8 77.3

MidEast - Persian Gulf 81.2 78.2 79 79

MidEast - Red Sea 77.8 77.8 77.8 66.7

N. America - Canadian Atlantic 33.3 33.3 33.3 100

N. America - Canadian Pacific 0 0 0 0

N. America - Mexico 77.5 75 75 78.9

N. America - US Alaska 100 100 50 50

N. America - US GOM 72.9 70.6 70.6 75.9

S. America - Brazil 91 92.3 89.7 89.7

S. America - Other & Carib. 63.6 63.6 63.6 63.6

S. America - Venezuela 80 80 80 80

Average 75.20 75.46 73.45 77.07

Source: Rigzone, MIDFR

MIDF EQUITY BEAT Thursday, 04 October 2012

8

CORPORATE & INDUSTRY DEVELOPMENT IN SEPT12

Date Company(s) Event(s)

28-Sep UMW & Petronas Carigali UMW Group's unit won a contract from Petronas Carigali to supply a main power generation package for the Diyarbekir Oil Dev Project

25-Sep Petronas & GE Oil & Gas GE Oil and Gas entered into an agreement with Petronas to supply gas turbine-driven compressor train technology for a floating liquefied natural gas (FLNG) facility being developed off the coast of Sarawak, Malaysia.

21-Sep Petra Energy Petra Energy reported to have become the local partner to Coastal Energy on the Kapal, Banang and Meranti marginal fields Risk Service Contract

21-Sep Petronas Carigali

Eurasia Drilling Company Ltd (EDC), the leading onshore and offshore drilling service provider in the Commonwealth of Independent States, has been awarded a multi-year contract extension with Petronas Carigali (Turkmenistan) Sdn Bhd for drilling offshore Turkmenistan in the Caspian Sea

19-Sep Petronas

Petroliam Nasional Bhd (Petronas) has decided to sell all its assets in Thailand to Susco Plc. The transfer of assets is expected to be finalized by November. Susco plans to allocate about THB50m a year for facelifts for the 100 petrol stations in Thailand.

13-Sep Dialog The consortium comprising of Dialog Group Bhd, the Johor Government and Royal Vopak will invest RM4.08b to develop the Pengerang LNG terminal project.

12-Sep Petronas Carigali Petronas Carigali Sdn Bhd, a subsidary of Petronas, has signed a technology collaboration agreement with MIT Innovation Sdn Bhd for the development of a cost-saver drilling tool.

7-Sep Petronas

Petroliam Nasional Bhd (Petronas), which posted a 30% drop in earnings to RM15.22b in the second quarter ended June 30, 2012, will struggle to match last year's performance due to production issues, low oil prices and anticipated increase in gas subsidy.

6-Sep KNM Group

KNM Group Bhd has proposed to list its unit Borsig Beteiligungsverwaltungsgesellschaft mb on the Main Board of the Singapore Exchange. It expected the proposed listing to be launched in 2013 with an indicative valuation for Borsig of between RM1.8b and RM1.9b.

Sources: Company, Media, MIDFR

VALUATION AND RECOMMENDATION

We maintain our POSITIVE conviction on the local oil & gas sector on the continuous contract awards announced.

With the support from Petronas’ capex commitment along with jobs in the global arena, we believe that the local O&G

players will likely see more action in the coming months.

We favour Wah Seong Corp for its undemanding valuation coupled with good visibility, Dialog Group for its strong

engineering arm with good support from its Centralised Tankage Facilities, Gas Malaysia for its stable earnings and

as a dividend play stock and SapuraKencana for its strong orderbook with its market leading ability as an EPC player.

MIDF EQUITY BEAT Thursday, 04 October 2012

9

Summary of O&G Stocks under MIDFR’s Coverage

Company Last Price (RM)

TP (RM) Upside

(%) Call

EPS (sen) PER (x) ROA ROE

FY12F FY13F FY12F FY13F (%) (%)

Dialog 2.34 2.80 19.7 BUY 7.6 9 36.8 31.1 14.1 24.6

KNM 0.68 0.56 -17.6 SELL 10.5 6.6 5.3 8.5 na na

SapuraKencana 2.42 2.74 13.2 BUY 11.6 12.8 23.6 21.4 5.8 61.1

Petronas Chemicals

6.44 6.10 -5.3 NEUTRAL 43.7 47.7 14.0 12.8 12.3 16.9

MMHE 4.90 5.06 3.3 NEUTRAL 19 22.5 26.6 22.5 6.8 14.5

Petronas Gas 19.74 17.72 -10.2 NEUTRAL 79.5 84.4 22.3 21.0 12.8 15.8

Wah Seong 1.76 2.13 21.0 BUY 11.9 16.9 17.9 12.6 4.8 10.1

Bumi Armada 3.69 3.64 -1.4 NEUTRAL 14.5 17.3 25.1 21.0 5.2 10.2

Gas Malaysia 2.63 2.84 8.0 BUY 10.9 12.8 26.1 22.2 15.5 22.7

Source: MIDFR estimates

WTI Price Chart

Source: Bloomberg, MIDFR

MIDF EQUITY BEAT Thursday, 04 October 2012

10

APPENDIX: YTD 2012 List of Contracts Awarded to Bursa-listed O&G Companies

Company Projects Clients Date

(2012) Value (RMm)

Perisai Petroleum Charter of Intan Group’s 8 offshore support vessels

Emas Offshore 18 Sept 120

Provision of topside general maintenance

Talisman 14-Feb 125

Bumi Armada Provision of DP2 Accomodation Workboat

Tecnologías Relacionadas con Energía y Servicios Especializados

7-May 202

Provision of Platform Supply Vessel

Petrobras 21-Mar 115

Provision of AHTS Petrobras 16-Jan 155

15km Pipe laying - Caspian Sea

Lukoil 16-Apr 620

SapuraKencana PCI for Manora Field Pearl Oil (Thailand) 25-Sep 78

Charter of Sapura 3000 vessel Construcciones Maritimas Mexicanas S.A. de C.V

10-Sep 140

EPCC Platform & Accomodation

Murphy Sarawak 26-Jul 250-300

HUC at Montara Development Project

PTTEP Australasia 3-Aug 50

HUC for Kebabangan Field Kebabangan 9-Aug 106

Scomi Group Provision of drilling fluids & Engineering services

Qatar Petroleum 23-Aug 130

Favelle Favco Provision of offshore cranes

Consortium of P.T. Pal Indonesia Offshore Oil Engineering and Technip France

4-Sep 89.6

Muhibbah Engineering

Sale of 2 units AHTS na 26-Sep 240.6

MIDF EQUITY BEAT Thursday, 04 October 2012

11

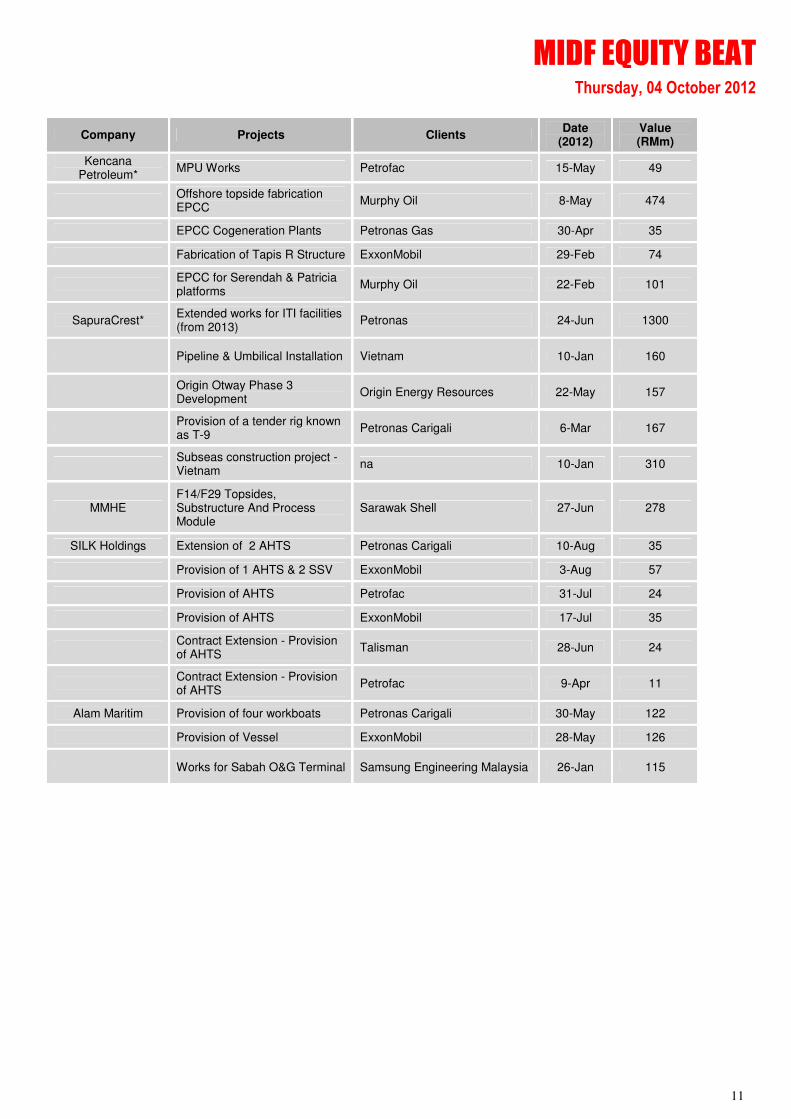

Company Projects Clients Date

(2012) Value (RMm)

Kencana Petroleum*

MPU Works Petrofac 15-May 49

Offshore topside fabrication EPCC

Murphy Oil 8-May 474

EPCC Cogeneration Plants Petronas Gas 30-Apr 35

Fabrication of Tapis R Structure ExxonMobil 29-Feb 74

EPCC for Serendah & Patricia platforms

Murphy Oil 22-Feb 101

SapuraCrest* Extended works for ITI facilities (from 2013)

Petronas 24-Jun 1300

Pipeline & Umbilical Installation Vietnam 10-Jan 160

Origin Otway Phase 3 Development

Origin Energy Resources 22-May 157

Provision of a tender rig known as T-9

Petronas Carigali 6-Mar 167

Subseas construction project - Vietnam

na 10-Jan 310

MMHE F14/F29 Topsides, Substructure And Process Module

Sarawak Shell 27-Jun 278

SILK Holdings Extension of 2 AHTS Petronas Carigali 10-Aug 35

Provision of 1 AHTS & 2 SSV ExxonMobil 3-Aug 57

Provision of AHTS Petrofac 31-Jul 24

Provision of AHTS ExxonMobil 17-Jul 35

Contract Extension - Provision of AHTS

Talisman 28-Jun 24

Contract Extension - Provision of AHTS

Petrofac 9-Apr 11

Alam Maritim Provision of four workboats Petronas Carigali 30-May 122

Provision of Vessel ExxonMobil 28-May 126

Works for Sabah O&G Terminal Samsung Engineering Malaysia 26-Jan 115

MIDF EQUITY BEAT Thursday, 04 October 2012

12

Company Projects Clients Date

(2012) Value (RMm)

Dayang Provision of topside general maintenance

Talisman 14-Feb 125

Extension of time charter for Dayang Zamrud

Nautika (for Brunei Shell Petroleum)

16-Jan 85

Handal Resources Provision of crane maintenance services

Newfield Peninsula Malaysia 3-Sep 4.7

Provision of crane long term service

Carigali-Hess 15-Aug 11

Provision of integrated cranes ExxonMobil 25-Jun 150

Provision of integrated cranes Petronas Carigali 11-Jun 120

Supply of offshore pedestal cranes

PT Guna Tesuma Internasional 7-Mar 3

Supply of offshore pedestal cranes

Kencana HL 22-Feb 7

Crane service and maintenance Petrofac 24-May na

Uzma Provision of Production and Integrity Chemicals.

ExxonMobil 27-Aug 27.5

Supply of Chemical & Related Services

Talisman 8-Aug 62

Provision of Water Injection Studies

Petronas Carigali 11-Jun 36

Provision of well testing equipments

Petronas Carigali 16-Feb 350

Tanjung Offshore Provision of gas generator packages

Havayar Trading 13-Jul 80

TH Heavy Engineering

Fabrication of Substructure and Topside

Sarawak Shell 14-Jun 178

Fabrication of wellhead support structure

Aquaterra Energy 13-Mar 24

TAS Offshore Sale of AHTS na 14-Jun 49

Sale of AHTS na 18-May 98

Perdana Petroleum Supply of AHTS Murphy Oil 28-Jun 86

Coastal Contracts Sale of AHTS, Subsea support vessel

na 20-Sep 111

Sale of AHTS na 13-Aug 141

Source: Bursa Malaysia, Companies, MIDFR

MIDF EQUITY BEAT Thursday, 04 October 2012

13

MIDF RESEARCH is part of MIDF Amanah Investment Bank Berhad (23878 - X).

(Bank Pelaburan)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

DISCLOSURES AND DISCLAIMER

This report has been prepared by MIDF AMANAH INVESTMENT BANK BERHAD (23878-X). It is for

distribution only under such circumstances as may be permitted by applicable law.

Readers should be fully aware that this report is for information purposes only. The opinions contained

in this report are based on information obtained or derived from sources that we believe are reliable.

MIDF AMANAH INVESTMENT BANK BERHAD makes no representation or warranty, expressed or

implied, as to the accuracy, completeness or reliability of the information contained therein and it should

not be relied upon as such.

This report is not, and should not be construed as, an offer to buy or sell any securities or other financial

instruments. The analysis contained herein is based on numerous assumptions. Different assumptions

could result in materially different results. All opinions and estimates are subject to change without

notice. The research analysts will initiate, update and cease coverage solely at the discretion of MIDF

AMANAH INVESTMENT BANK BERHAD.

The directors, employees and representatives of MIDF AMANAH INVESTMENT BANK BERHAD may

have interest in any of the securities mentioned and may benefit from the information herein. Members

of the MIDF Group and their affiliates may provide services to any company and affiliates of such

companies whose securities are mentioned herein This document may not be reproduced, distributed or

published in any form or for any purpose.

MIDF AMANAH INVESTMENT BANK : GUIDE TO RECOMMENDATIONS

STOCK RECOMMENDATIONS

BUY Total return is expected to be >15% over the next 12 months.

TRADING BUY Stock price is expected to rise by >15% within 3-months after a Trading Buy rating has been assigned due to positive newsflow.

NEUTRAL Total return is expected to be between -15% and +15% over the next 12 months.

SELL Total return is expected to be <-15% over the next 12 months.

TRADING SELL Stock price is expected to fall by >15% within 3-months after a Trading Sell rating has been assigned due to negative newsflow.

SECTOR RECOMMENDATIONS

POSITIVE The sector is expected to outperform the overall market over the next 12 months.

NEUTRAL The sector is to perform in line with the overall market over the next 12 months.

NEGATIVE The sector is expected to underperform the overall market over the next 12 months.