Embed Size (px)

Citation preview

LOGO

A Better Regulatory Measure:

Introduction to the Stress TestPresent By: Minghui Lu Econ 439

LOGOContents

1. Introduction

2. Two Measures of Capital Adequacy

3. 2014 DFAST and CCAR Implementations

4. 2014 CCAR Requirement and Result Tables

LOGOIntroduction

Why the banks needed to be regulated? Banks issued subprime mortgages led to massive

default on mortgages Invented of derivatives to cover up toxic assets

Federal Reserve’s supervisory tools The Basel Models: Is it enough? New instruments: Comprehensive Capital Analysis

Review (CCAR) and Dodd-Frank Act Stress Test (DFAST)

LOGOTwo Measures of Capital Adequacy

The Basel Accords

The first regulatory method adopted by developed countries to measure bank holding companies’ (BHCs) capital ratios

Have been modified through time: Basel I, II, and III

LOGOThe Basel Accords

Basel I: Separated assets based on risk levels and divided the total capital – AKA Tier 1 Common Capital Ratio

• Banks needed to meet a standard of 4%• Set foundation for later models• Had weaknesses

Basel II: Revision on Basel I to cover loopholes

• Added in extra factors• 3 pillars: Minimum capital requirements;

Supervisory review; Market discipline.Basel III: Enhanced risk coverage, review

capital types and expanded risk coverage

LOGOTwo Measures of Capital Adequacy

The CCAR and DFAST

Financial institutions started to run internal stress tests since 1990’s • provided hypothetical adverse scenarios and see

if banks could remain insolvency The Fed Initiated Supervisory Capital

Assessment Program (SCAP) in 2009• 19 largest BHCs run mandatory stress tests under

supervisions of the Fed, OCC, and FDIC• Required to increase capital buffer if fail the test• Macroprudential supervision: government could

evaluate risk to the society as a whole

LOGOThe CCAR and DFAST (cont.)

Building on the SCAP, the Fed also ran annual stress tests as a complementary part of CCAR 3 economic scenarios (baseline, adverse, severely

adverse) Large BHCs also conducted semiannual stress tests

using own supplied scenarios Need to meet tier 1 common capital ratio of 5%

Submission of the proposed capital distribution plans Qualitative measure to ensure safe practices

Ability to meet Basel III requirements

LOGOThe CCAR and DFAST (cont.)

If BHCs fail to meet CCAR standards, the Fed would reject plan for capital distribution Shares Buying-back Issuance of dividends

Stress tests conducted in CCAR are different from DFAST!! DFAST includes mid-size BHCs ($10-50 billion

assets); while CCAR only included large BHCs DFAST use a standardized set of capital action

assumptions CCAR adjust capital level according to change of

common stock and dividend level

LOGOWhy is Stress Test Better?

The Basel models use historical data Under moderate growth assumption, even high level

of confidence would not help Stress test creates hypothetical scenarios

Basel models are static Use data on the balance sheets Stress test has longer time horizon

Other reasons Intentional reduction of portfolio Data mismeasurements

LOGOThe 2014 DFAST Result

All BHCs with total asset values over $10 billion had to participate

3 sets of scenarios (baseline, adverse, severely adverse)

A total of 28 variables: Interest rate, inflation, GDP growth, etc.

A time horizon of 9 quarters

LOGOThe 2014 DFAST Result (cont.)

Key changes: The Fed independently projected risk-weight assets

for each BHCs. Added in new capital ratios; changed risk levels in

each asset categories Disclose result under severely adverse scenarios

Results suggested a dramatic decrease of capital level under severely adverse scenario

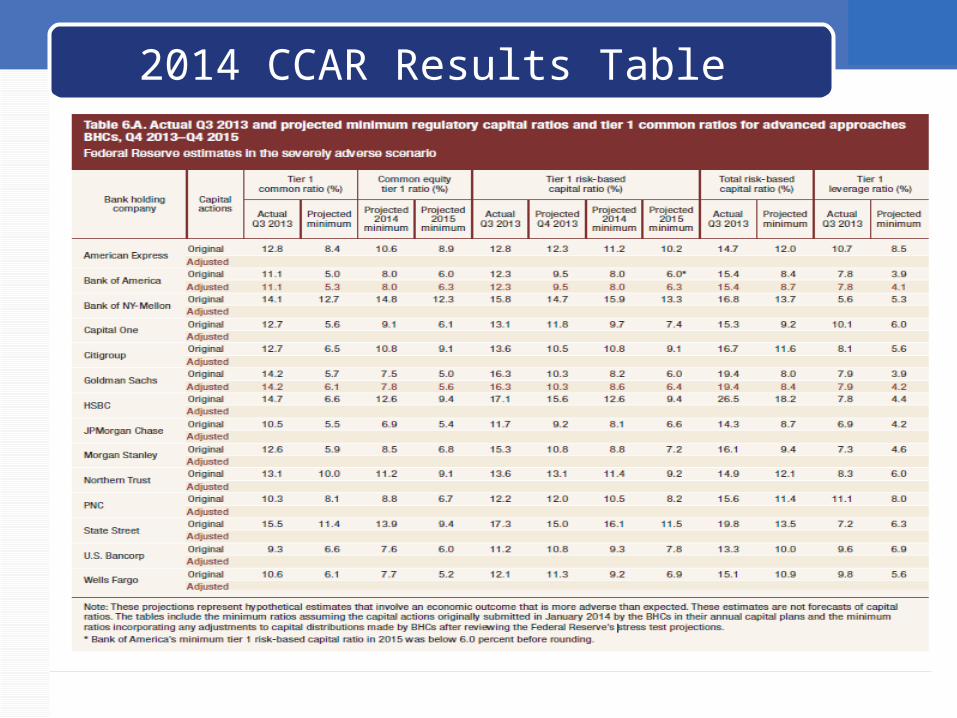

LOGOThe 2014 CCAR Results

Covered 30 BHCs with assets over $50 billions

Quantitative and Qualitative Measures Rejected 5 capital plans; 3 of them were new to the

CCAR exercise 3 of the BHCs failed to meet capital requirement in

the stress test; needed to resubmit their capital action

The result revealed that the Fed consists high expectation and standard BHCs responded to increase capital buffer; capital

ratio doubled from 2009 to 2013

LOGO2014 CCAR Capital Requirements

LOGO2014 CCAR Results Table

LOGO