Embed Size (px)

Citation preview

ABN 78 087 649 929

46TH ANNUAL REPORT 2015

CAPE - Customer Owned Banking ABN 78 087 649 929

46th Annual Report 2015

A N N U A L R E P O R T

2015CONTENTS

CHAIRMAN’S REPORT 6

DIRECTORS’ REPORT 8

AUDITOR’S INDEPENDENCE DECLARATION 13

INDEPENDENT AUDITOR’S REPORT 14

DIRECTOR’S DECLARATION 16

STATEMENT OF PROFIT AND LOSS AND OTHER COMPREHENSIVE INCOME 17

STATEMENT OF CHANGES IN MEMBER EQUITY 18

STATEMENT OF FINANCIAL POSITION 19

STATEMENT OF CASH FLOWS 20

TABLE OF OTHER NOTES TO ACCOUNTS 21

NOTES TO ACCOUNTS 22

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES 22

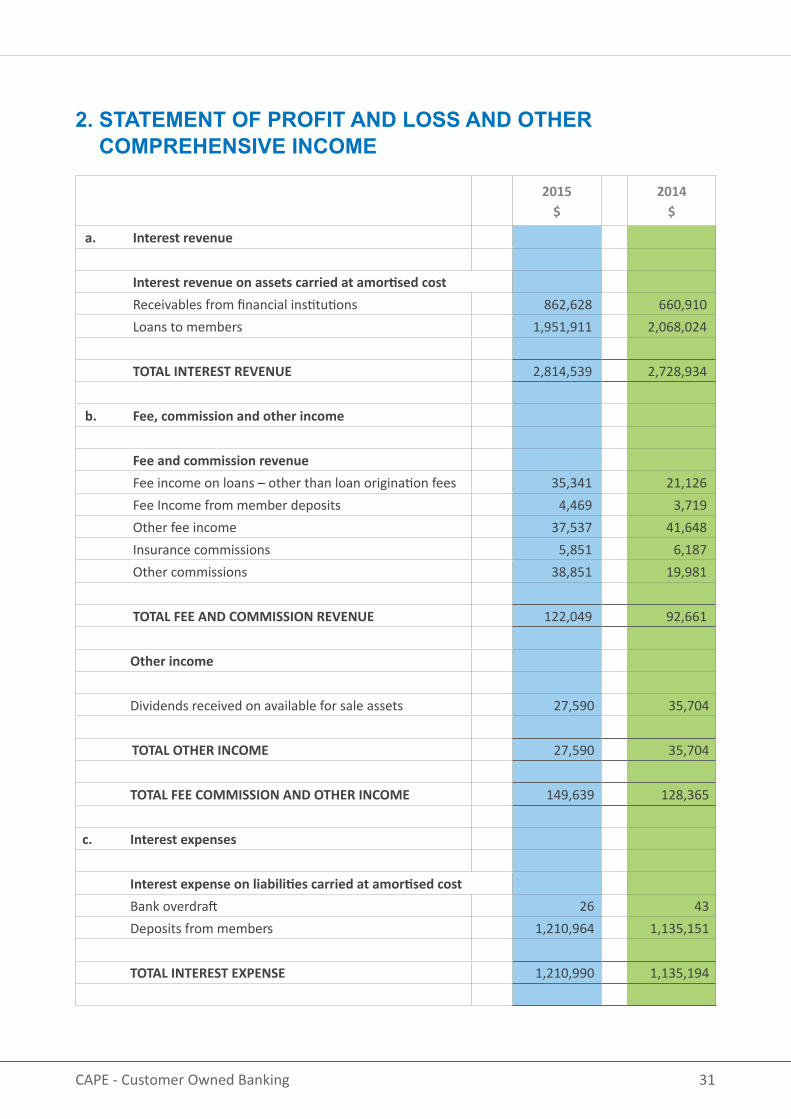

2. STATEMENT OF PROFIT AND LOSS AND OTHER COMPREHENSIVE INCOME 31

3. INCOME TAX EXPENSE 33

4. CASH AND CASH EQUIVALENTS 33

5. LIQUID INVESTMENTS 34

6. RECEIVABLES 34

7. LOANS TO MEMBERS 34

8. PROVISION ON IMPAIRED LOANS 36

9. AVAILABLE FOR SALE INVESTMENTS 38

10. PROPERTY, PLANT AND EQUIPMENT 38

11. TAXATION ASSETS 39

12. INTANGIBLE ASSETS 39

13. DEPOSITS FROM MEMBERS 40

14. CREDITOR ACCRUALS AND SETTLEMENT ACCOUNTS 41

15. TAXATION LIABILITIES 41

16. PROVISIONS 41

17. GENERAL RESERVE FOR CREDIT LOSSES 41

18. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES 42

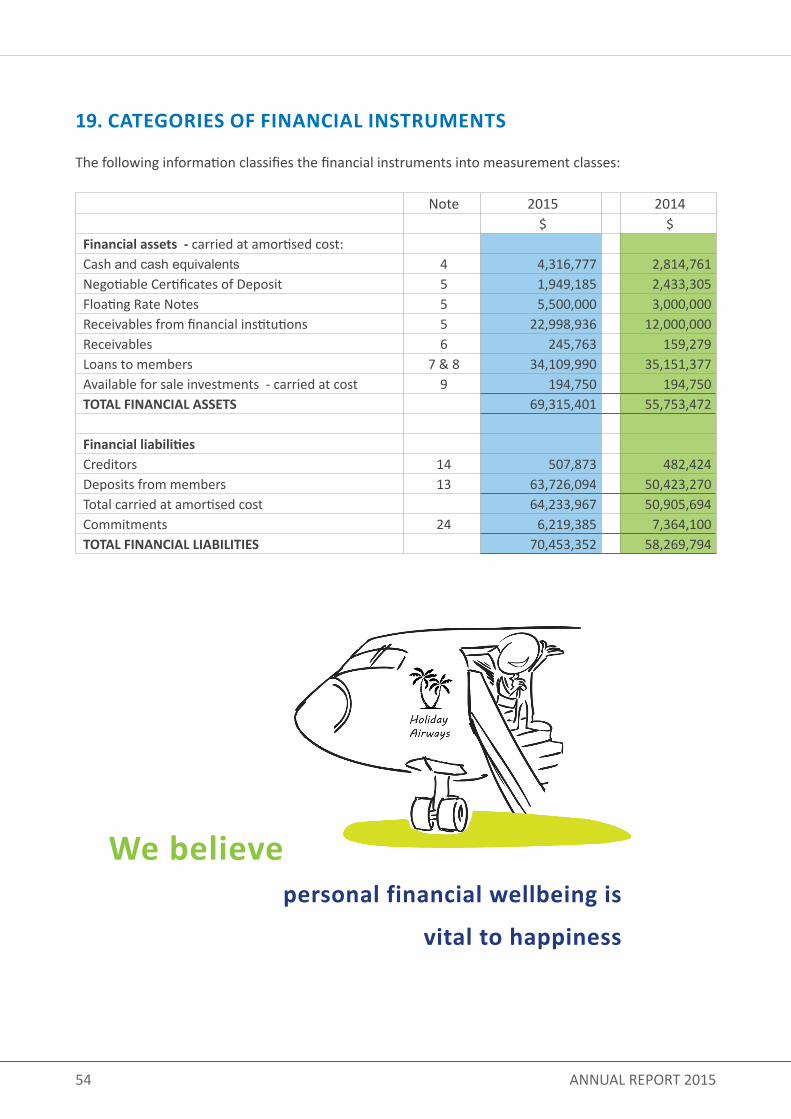

19. CATEGORIES OF FINANCIAL INSTRUMENTS 54

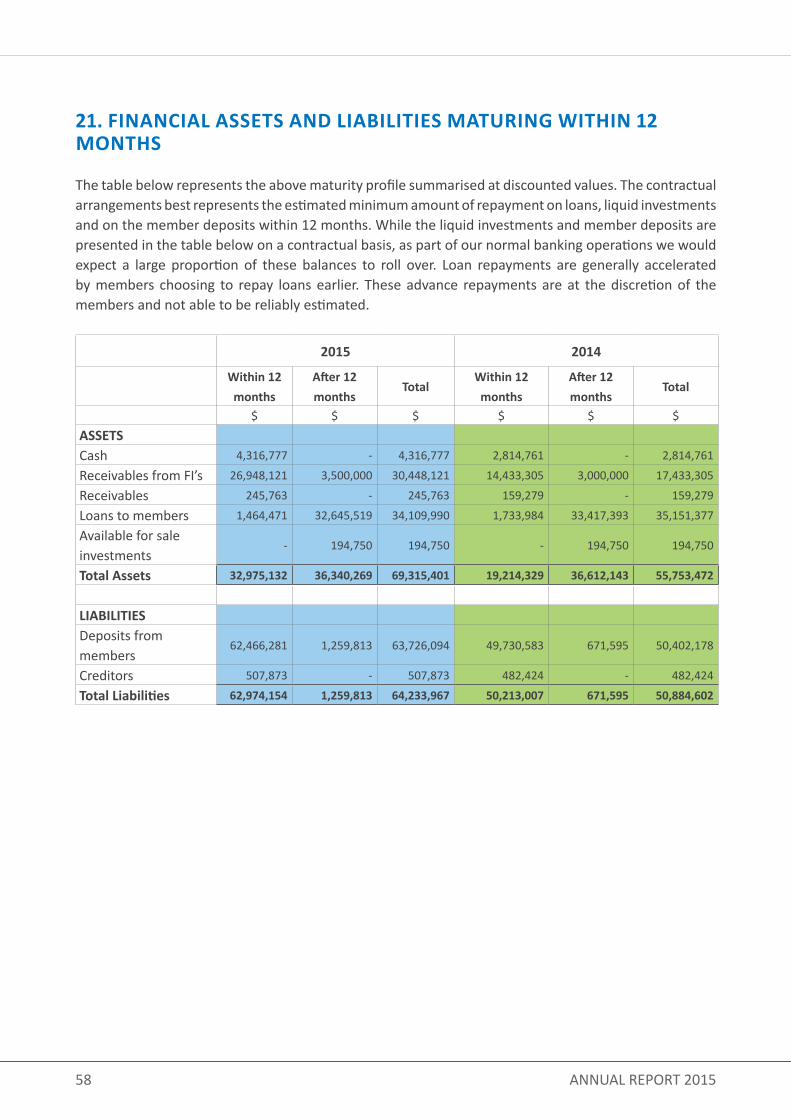

20. MATURITY PROFILE OF FINANCIAL ASSETS AND LIABILITIES 56

21. CURRENT AND NON-CURRENT DISSECTION OF FINANCIAL ASSETS AND LIABILITIES 58

22. INTEREST RATE CHANGE PROFILE OF FINANCIAL ASSETS AND LIABILITIES 60

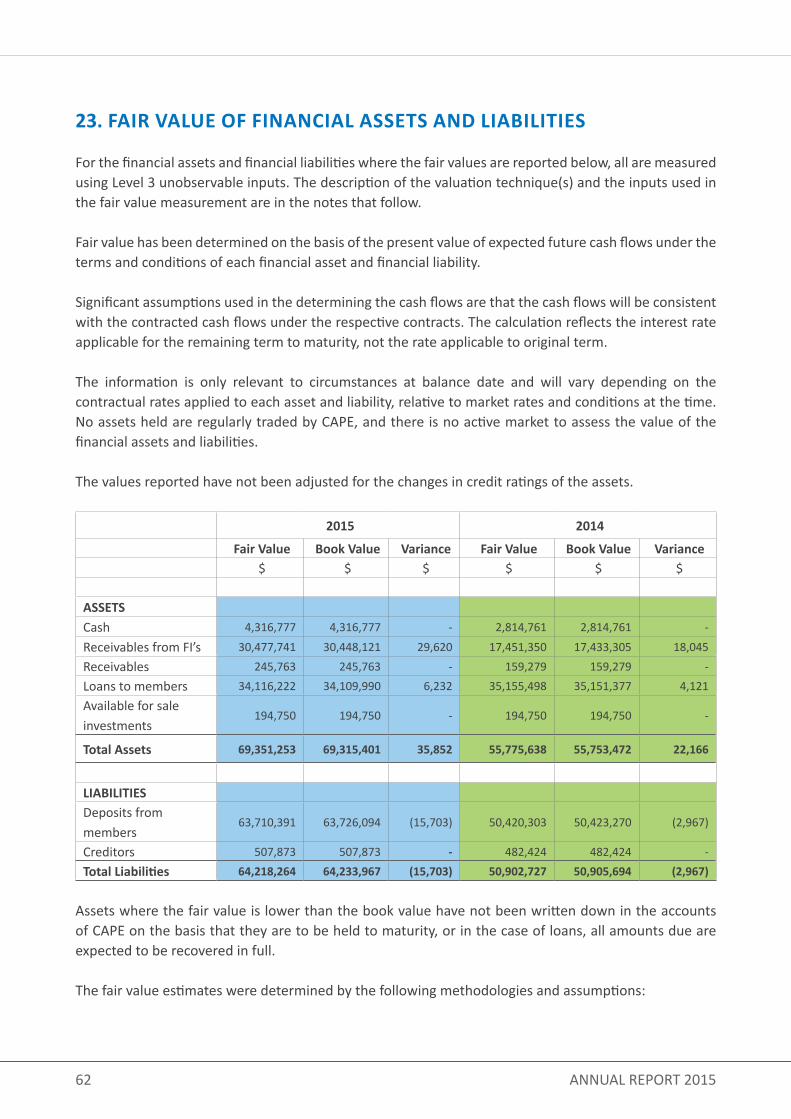

23. FAIR VALUE OF FINANCIAL ASSETS AND LIABILITIES 62

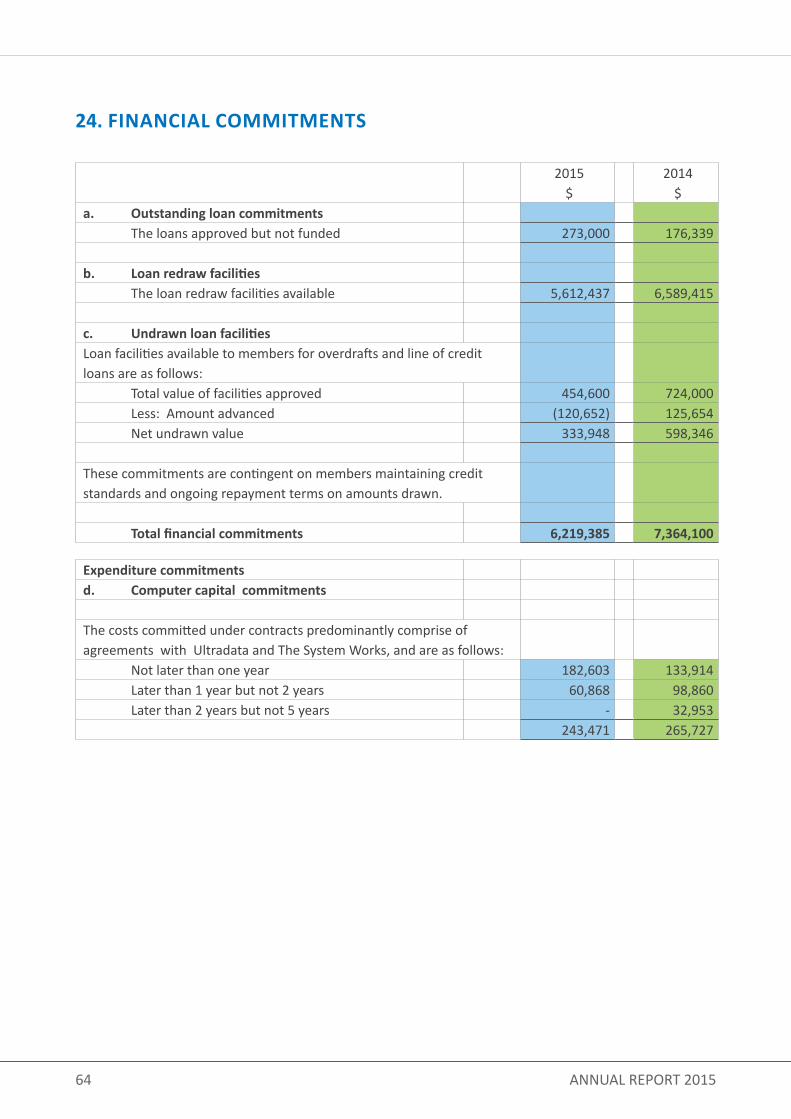

24. FINANCIAL COMMITMENTS 64

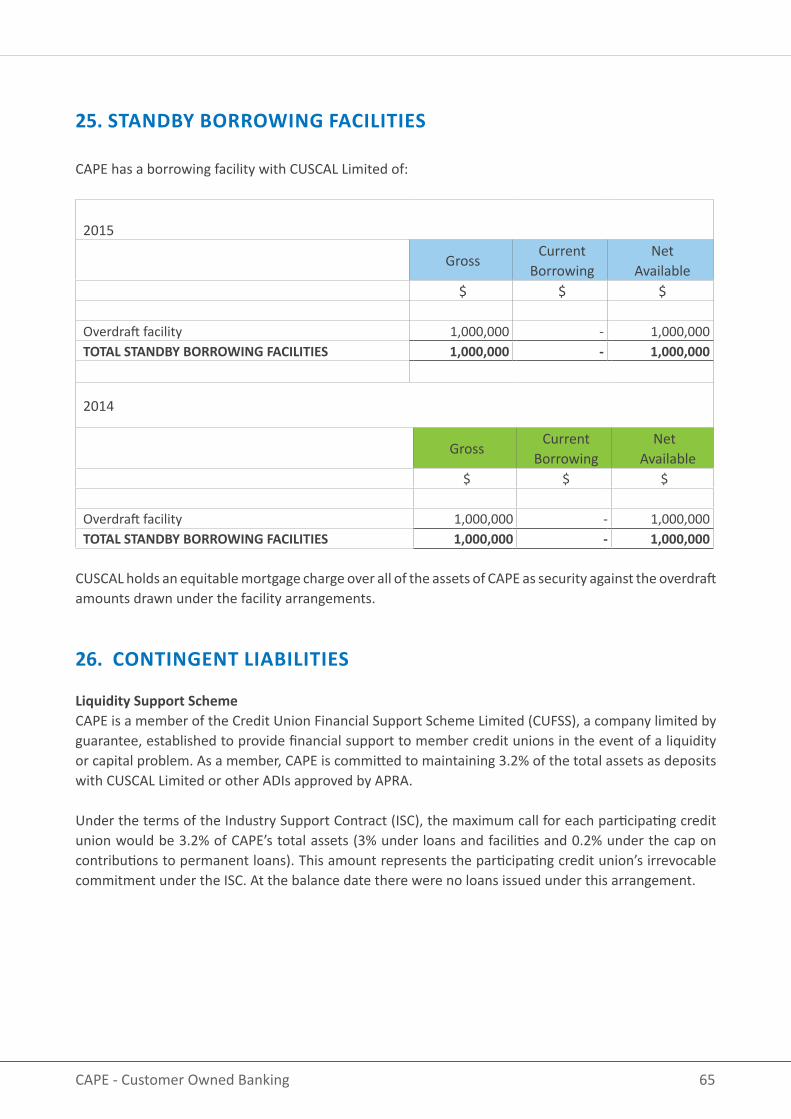

25. STANDBY BORROWING FACILITIES 65

26. CONTINGENT LIABILITIES 65

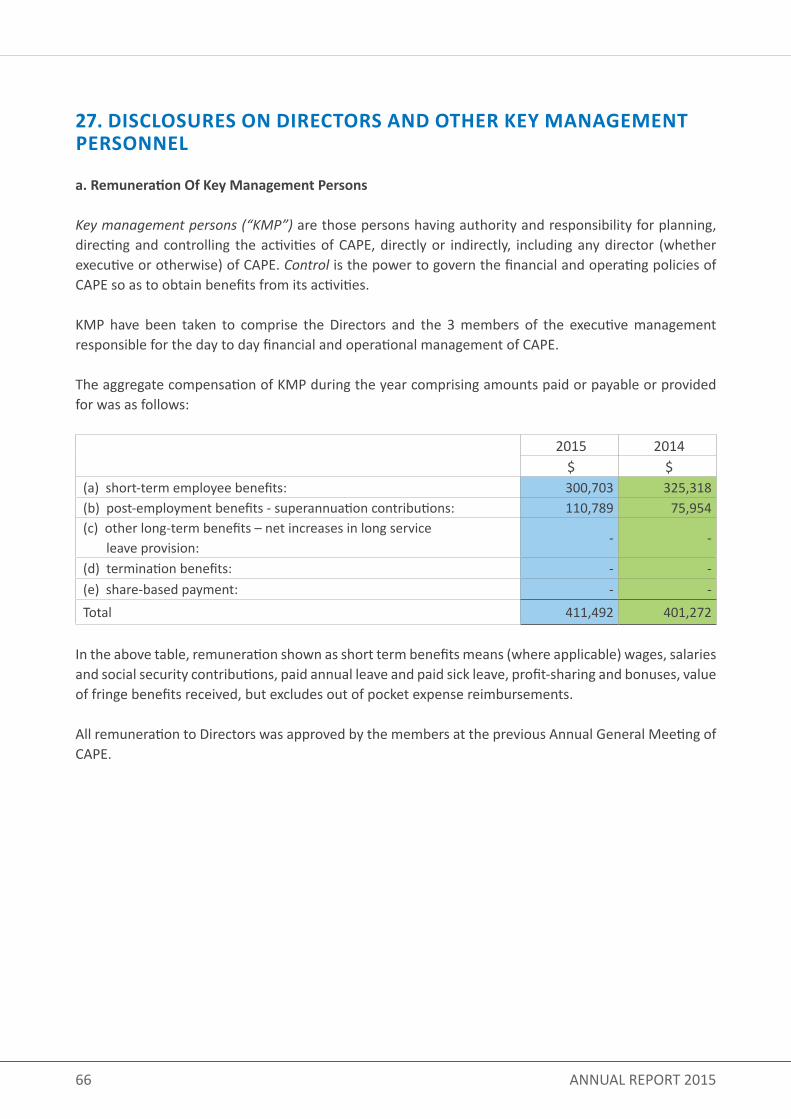

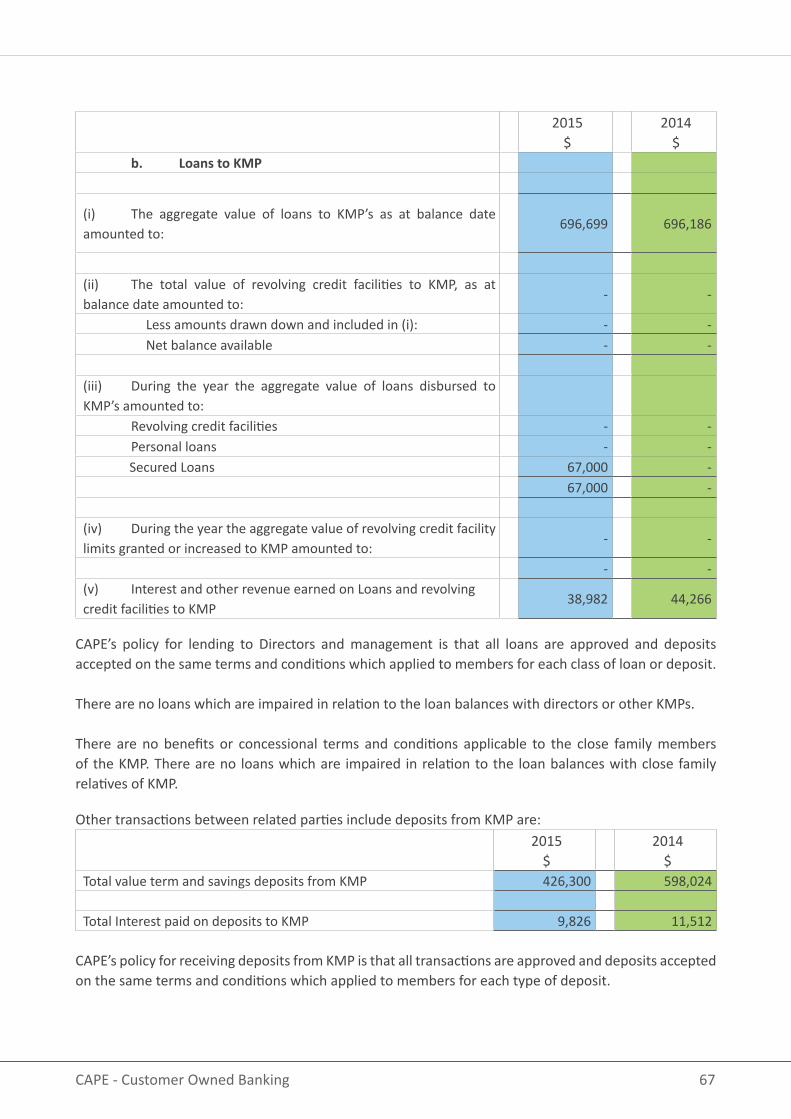

27. DISCLOSURES ON DIRECTORS AND OTHER KEY MANAGEMENT PERSONNEL 66

28. OUTSOURCING ARRANGEMENTS 68

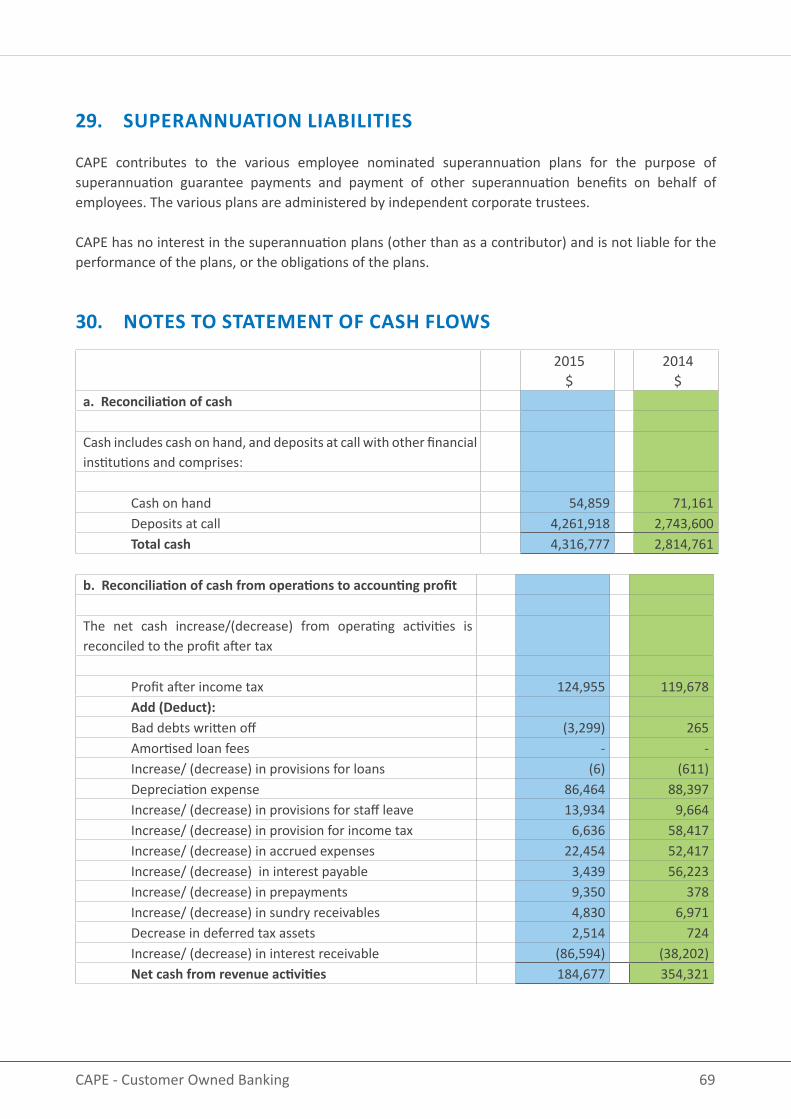

29. SUPERANNUATION LIABILITIES 69

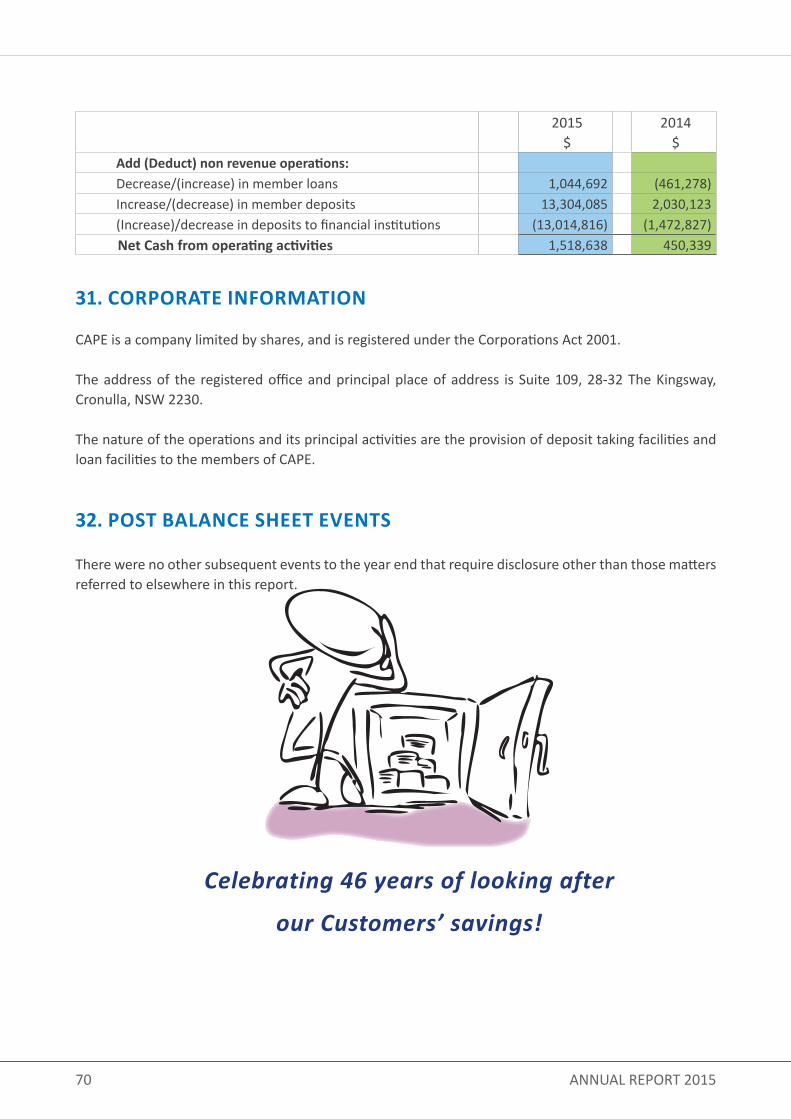

30. NOTES TO STATEMENT OF CASH FLOWS 69

31. CORPORATE INFORMATION 70

32. POST BALANCE SHEET EVENTS 70

ANNUAL GENERAL MEETING 71

6 ANNUAL REPORT 2015

I am pleased on behalf of the Board of Directors of CAPE Credit Union Limited (‘CAPE”) to present to you the 46th Annual report for the financial year ended 30 June 2015.

The 2014/15 financial year continued to be marked by subdued economic conditions though considerable escalation in property prices has been observed in some markets, particularly Sydney and Melbourne. We experienced further reductions in official interest rates during the year which presents your Board and Management with significant challenges as rates reduce, our investment yields reduce and our term deposit portfolio takes quite some time to subsequently reprice.

Earlier in 2014 the Board and Management established a goal to grow CAPE’s assets to $70m by 2016. We are pleased to report this milestone was achieved 12 months ahead of plan. During the 2014/15 year CAPE grew its total assets from $56.67m to $70.14m. Additionally we posted a 9.3% increase in profit before tax to $169,852.

The closure of the Caltex Kurnell Refinery was experienced during the year and CAPE played its role in supporting those Members impacted by the closure. The number of Members who benefited from detailed financial advice/retirement planning was significant and CAPE’s involvement in ensuring high quality financial planning was made available to affected Members was particularly pleasing.

The continuing caution shown by our Members in taking on new debt combined with some Refinery workers directing redundancy monies to debt retirement resulted in CAPE suffering a small 3% contraction on total loans outstanding. The level of our liquid investments increased by 75% to over $30m.

CAPE continues to adhere to its core strategic themes of: relevance to its members; capability; competitiveness.

In recent years CAPE has invested heavily into new products and services and its capability to meet Member needs has never been greater. The pleasing take up of our new Visa debit card which includes the latest chip technology, Pay Wave functionality, 24/7 fraud monitoring, online and telephone shopping indicates we are meeting the needs of a contemporary member.

CHAIRMAN’S REPORT

7CAPE - Customer Owned Banking

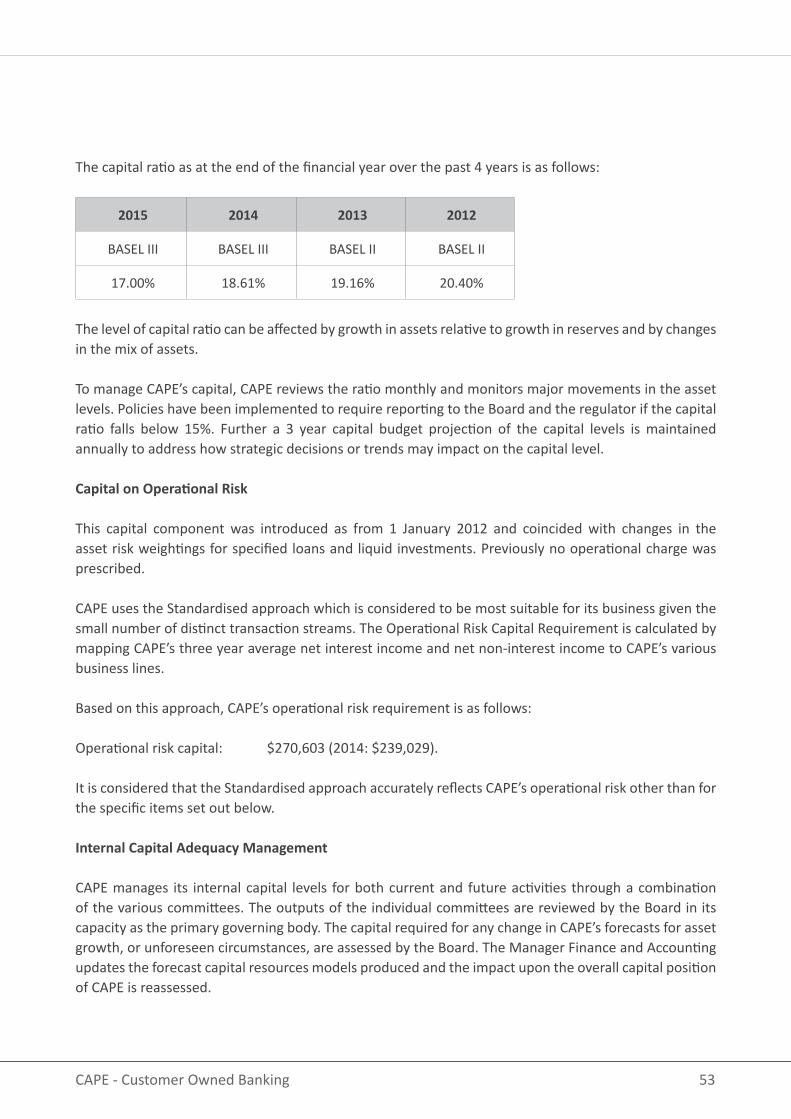

CAPE remains very well capitalised and enjoys a sound relationship with our regulator (The Australian Prudential Regulation Authority – “APRA”) and continues to comfortably meet all the prevailing prudential standards. Our Risk and Compliance framework is particularly robust and positions us effectively to address and deal will the challenges and risks that we continue to face.

We expect the coming year to again provide another challenging operating environment. However, the Board is confident that with our focus on organic growth, a strong team of people working with us and our effective risk management will see CAPE remain in a sound financial position.

During the year one of our long-serving directors and Deputy Chairman, Wayne Meredith, stood down for personal reasons. Wayne served on the CAPE Board for approximately 30 years which is an incredible feat. He was a dedicated servant to CAPE and its members. We acknowledge and thank Wayne for the significant contribution he made to our Credit Union.

Finally, I would like to thank my fellow directors, management and staff of CAPE for their hard work and commitment to ensuring we have a successful and viable Credit Union.

I would like to commend this report to members on behalf of the Board of Directors and thank every Member for their continuing patronage and support.

William RankineChairman

8 ANNUAL REPORT 2015

DIRECTORS’ REPORT

INFORMATION ON DIRECTORSYour Directors present their report on CAPE Credit Union Limited (CAPE) for the financial year ended 30 June 2015. CAPE is a company registered under the Corporations Act 2001. The names of the Directors in office at any time during or since the end of the year are:

BILL RANKINE - CHAIRMANQualifications: Member of Australasian Mutuals Institute. Master of Business Administration – Deakin University, Graduate Diploma of Business (Finance) – Edith Cowan University, Diploma in Corporate Management – Institute of Chartered Secretaries, Certificate in Accounting – TAFE.Experience: Formerly an employee of Caltex for 33 years, Member of Board of Directors since January 2007, current Member of the Executive, Audit, Risk, Nominations and Remuneration Committees.

Wayne Meredith - Deputy ChairmanExperience: Formerly IT Project Leader and employee of Caltex for 33 years, Member of Board of Directors since 1984, Member of Executive Committee and the Nominations and Remuneration Committee. Resigned 25 February 2015.

Gordon GoodacreExperience: 39 years experience within mutual Credit Unions holding senior roles at Landmark CU, Reliance CU and Gateway CU. Introduced to CAPE to fill vacant CEO position until fulltime replacement during 2008. Member of Board of Directors since 2008, current member of Nominations and Remuneration Committee. Past Chair of the Audit and Risk Committee.

Cecil Riley - Chairman Nominations and Remuneration CommitteeQualifications: Member of Australasian Mutuals Institute. Experience: Formerly supervisor and employee of Caltex for 40 years; Member of Board of Directors since 1980, current member of Executive Committee and past Board Chair.

Rebecca Murray - Chairperson of Strategic Planning CommitteeQualifications: Bachelor of Science (Hons) Australian National University, MBA Macquarie University, GAICD.Experience: Financial services executive and management consultant with 22 years experience. Senior financial services roles at Zurich, Ipac Securities, Colonial First State, Financial Planning Association and The Australian Retail Credit Association (ARCA). Member of Board of Directors since 2010.

9CAPE - Customer Owned Banking

John McNally - Chairman Audit Committee and Risk CommitteeQualifications: SPQ (Uni NSW), Grad Dip AppSc (Uni NSW), MAppSc (Uni NSW). Member of the Australasian Mutuals Institute.Experience: Principal and Director of LKR Consulting Pty Ltd. Formerly Operational Excellence Manager and employee of Caltex for 36 years. Member of the Board of Directors since 1993, past Board Chair, current Chair of the Audit Committee and Risk Committee, member of the Executive and Strategic Planning Committees.

Robert Norris Experience: Accountant Corporate Finance, employee of AGL/Jemena for 33 years. Director of First Gas Credit Union (AGL) from 1992 – 2003. Alternate Director since August 2003. Member of Board of Directors since 2005, current Member of the Audit Committee and Risk Committee.

Jeanette BrooksQualifications: Bachelor Business (Mgmt & Info Sys) CSU, Graduate Certificate Management UOW, Company Director Diploma, Australian Institute of Company DirectorsExperience: Director Learning Links, Regional General Manager at Australian Unity, formally Chief Executive The INS Group. Over 21 years’ experience in ICT development and operations. Member of Board of Directors since 2012, current Member of the Strategic Planning Committee.

Directors were in office from the beginning of the financial year, unless otherwise stated.

COMPANY SECRETARYThe following person held the position of company secretary during the financial year:

Richard NowakowskiQualifications: Member of Financial Services Institute of Australasia (Fellow), Accountancy Certificate, Six Sigma / TQM. Experience: Chief Risk Officer and Company Secretary at CAPE since January 2012 Previous - 37 years in the financial sector (Big 4 Bank) in Customer Interface; Operational Risk Management; Sales; Lending; Operations; Audit; Compliance; Change, Project & Knowledge Management: 25 years in Senior and National roles.

10 ANNUAL REPORT 2015

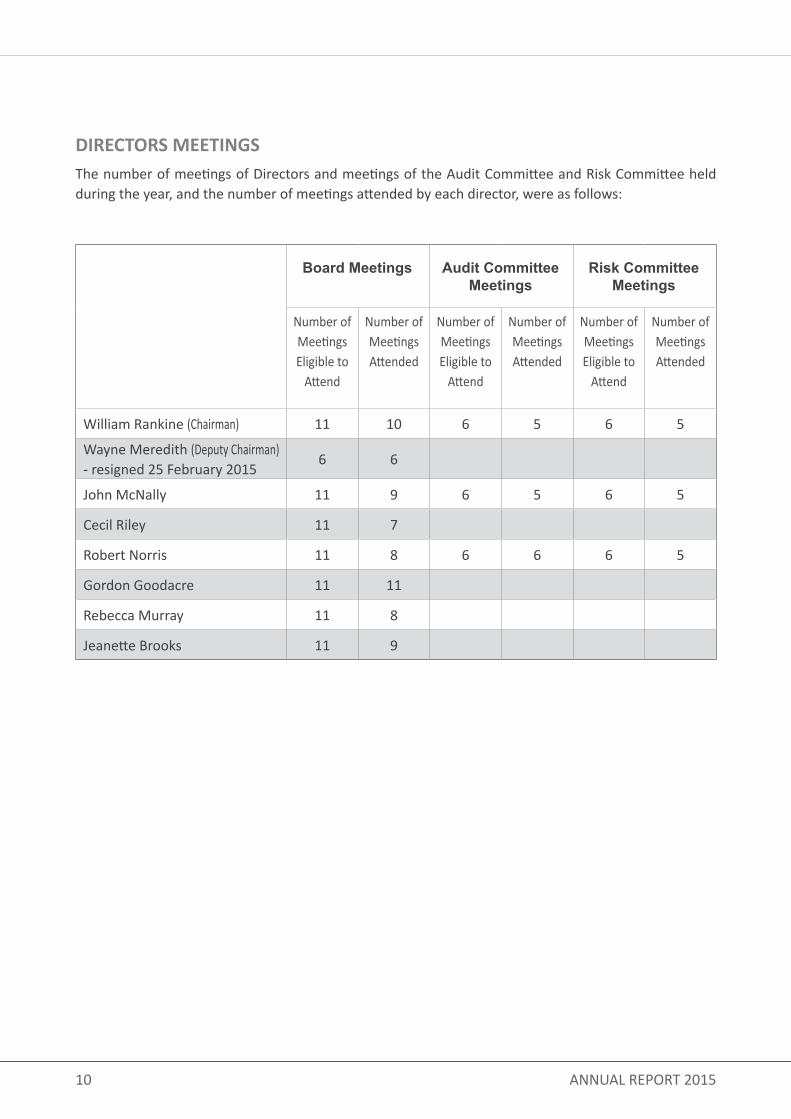

DIRECTORS MEETINGSThe number of meetings of Directors and meetings of the Audit Committee and Risk Committee held during the year, and the number of meetings attended by each director, were as follows:

Board Meetings Audit Committee Meetings

Risk Committee Meetings

Number of Meetings Eligible to

Attend

Number of Meetings Attended

Number of Meetings Eligible to

Attend

Number of Meetings Attended

Number of Meetings Eligible to

Attend

Number of Meetings Attended

William Rankine (Chairman) 11 10 6 5 6 5

Wayne Meredith (Deputy Chairman)- resigned 25 February 2015

6 6

John McNally 11 9 6 5 6 5

Cecil Riley 11 7

Robert Norris 11 8 6 6 6 5

Gordon Goodacre 11 11

Rebecca Murray 11 8

Jeanette Brooks 11 9

11CAPE - Customer Owned Banking

DIRECTORS’ BENEFITSOther than any benefit that may have been derived from loans and deposits provided by, and to, the Credit Union, no Directors have, during the financial year and the period to the date of this report, become entitled to receive any benefit by reason of a contract made by CAPE with:• a related entity with the director; or• a firm of which the director is a member; or• an entity in which the director has a substantial financial interest.

A total amount of $58,000 was paid to the Board of Directors for allocation amongst the individual Board members, at their discretion, as approved by the members at the 2014 Annual General Meeting.

No director has received or become entitled to receive during, or since the financial year, any other benefit because of a contract made by CAPE, controlled credit union, or a related body corporate with a director, a firm of which a director is a member or a credit union in which a director has a substantial financial interest, other than that disclosed in Note 27 of the financial report.

INDEMNIFYING OFFICER OR AUDITORInsurance premiums have been paid to insure each of the Directors and officers of CAPE against any costs and expenses incurred by them in defending any legal proceeding arising out of their conduct while acting in their capacity as an officer of CAPE. In accordance with normal commercial practice, disclosure of the premium amount and the nature of the insured liabilities is prohibited by a confidentiality clause in the contract.

No insurance cover has been provided for the benefit of the auditors of CAPE.

PRINCIPAL ACTIVITIESThe principal activities of CAPE during the year were the provision of retail financial services to members in the form of taking deposits and giving financial accommodation as prescribed by the Constitution.

No significant changes in the nature of these activities occurred during the year.

OPERATING RESULTSThe net profit of CAPE for the year after providing for income tax was $124,955, (2014 $119,678).

DIVIDENDSNo dividends have been paid or declared since the end of the financial year and no dividends have been recommended or provided for by the Directors of CAPE.

12 ANNUAL REPORT 2015

REVIEW OF OPERATIONSCAPE’s activities centre around the provision of financial services to its members. The results for the financial year 2014/15 were consistent with its normal activities and did not change significantly from the previous year.

SIGNIFICANT CHANGES IN STATE OF AFFAIRSThere were no significant changes in the state of the affairs of CAPE during the year.

EVENTS OCCURRING AFTER BALANCE DATE No other matters or circumstances have arisen since the end of the financial year which significantly affected or may significantly affect the operations, or state of affairs of CAPE in subsequent financial years.

LIKELY DEVELOPMENTS AND RESULTSNo other matter, circumstance or likely development in the operations has arisen since the end of the financial year that has significantly affected or may significantly affect:

(i) The operations of CAPE;(ii) The results of those operations; or(iii) The state of affairs of CAPE

In the financial years subsequent to this financial year.

AUDITORS’ INDEPENDENCEThe auditors have provided the declaration of independence to the Board as prescribed by the Corporations Act 2001 as set out on Page 13.

This report is made in accordance with a resolution of the Board of Directors and is signed for and on behalf of the Directors by:

13CAPE - Customer Owned Banking

14 ANNUAL REPORT 2015

15CAPE - Customer Owned Banking

16 ANNUAL REPORT 2015

DIRECTOR’S DECLARATION In the opinion of the directors of CAPE Credit Union Limited:a. The financial statements and accompanying notes, are in accordance with the Corporations Act 2001, including (i) giving a true and fair view of its financial position as at 30 June 2015 and of its performance for the financial year ended on that date; and (ii) complying with Australian Accounting Standards (including the Australian Accounting Interpretations) and the Corporations Regulations 2001; andb. There are reasonable grounds to believe that CAPE Credit Union Limited will be able to pay its debts as and when they become due and payable.c. The financial statements comply with International Financial Reporting Standards.

Signed in accordance with a resolution of the directors:

17CAPE - Customer Owned Banking

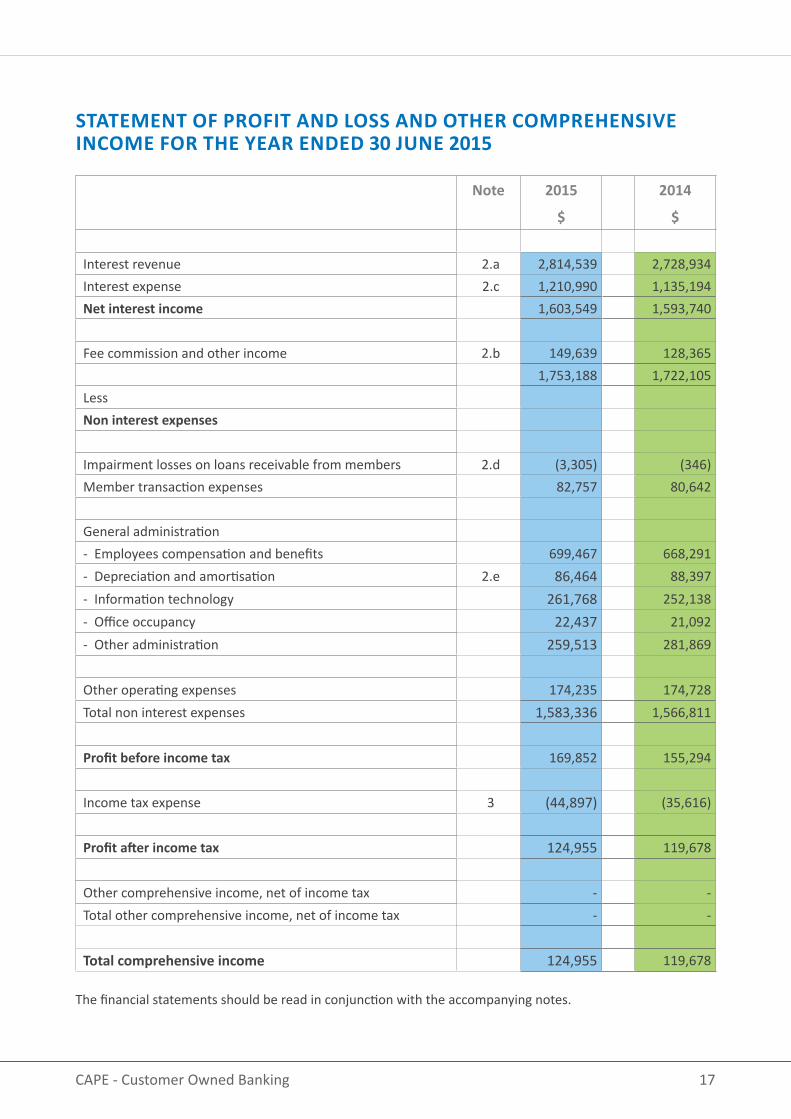

Note 2015

$

2014

$

Interest revenue 2.a 2,814,539 2,728,934Interest expense 2.c 1,210,990 1,135,194Net interest income 1,603,549 1,593,740

Fee commission and other income 2.b 149,639 128,365 1,753,188 1,722,105LessNon interest expenses

Impairment losses on loans receivable from members 2.d (3,305) (346)Member transaction expenses 82,757 80,642

General administration- Employees compensation and benefits 699,467 668,291- Depreciation and amortisation 2.e 86,464 88,397- Information technology 261,768 252,138- Office occupancy 22,437 21,092- Other administration 259,513 281,869

Other operating expenses 174,235 174,728Total non interest expenses 1,583,336 1,566,811

Profit before income tax 169,852 155,294

Income tax expense 3 (44,897) (35,616)

Profit after income tax 124,955 119,678

Other comprehensive income, net of income tax - -Total other comprehensive income, net of income tax - -

Total comprehensive income 124,955 119,678

STATEMENT OF PROFIT AND LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 JUNE 2015

The financial statements should be read in conjunction with the accompanying notes.

18 ANNUAL REPORT 2015

STATEMENT OF CHANGES IN MEMBER EQUITY FOR THE YEAR ENDED 30 JUNE 2015

Capital Reserve

General Reserve

for Credit Losses

Retained Earnings

Total

$ $ $ $Note 17Total at 30 June 2013 26,988 346,904 5,180,778 5,554,670

Profit for the year - - 119,678 119, 678Transfer to capital account 1,982 - (1, 982) -General Reserve for credit losses - 4,610 (4,610) -Total as at 30 June 2014 28,970 351,514 5,293,864 5,674,348

Profit for the year - - 124,955 124,955Transfer to capital account 1,970 - (1,970) -General Reserve for credit losses - (10,414) 10,414 -Total as at 30 June 2015 30,940 341,100 5,427,263 5,799,303

The financial statements should be read in conjunction with the accompanying notes.

We believe in an equal share and an equal vote for every customer

19CAPE - Customer Owned Banking

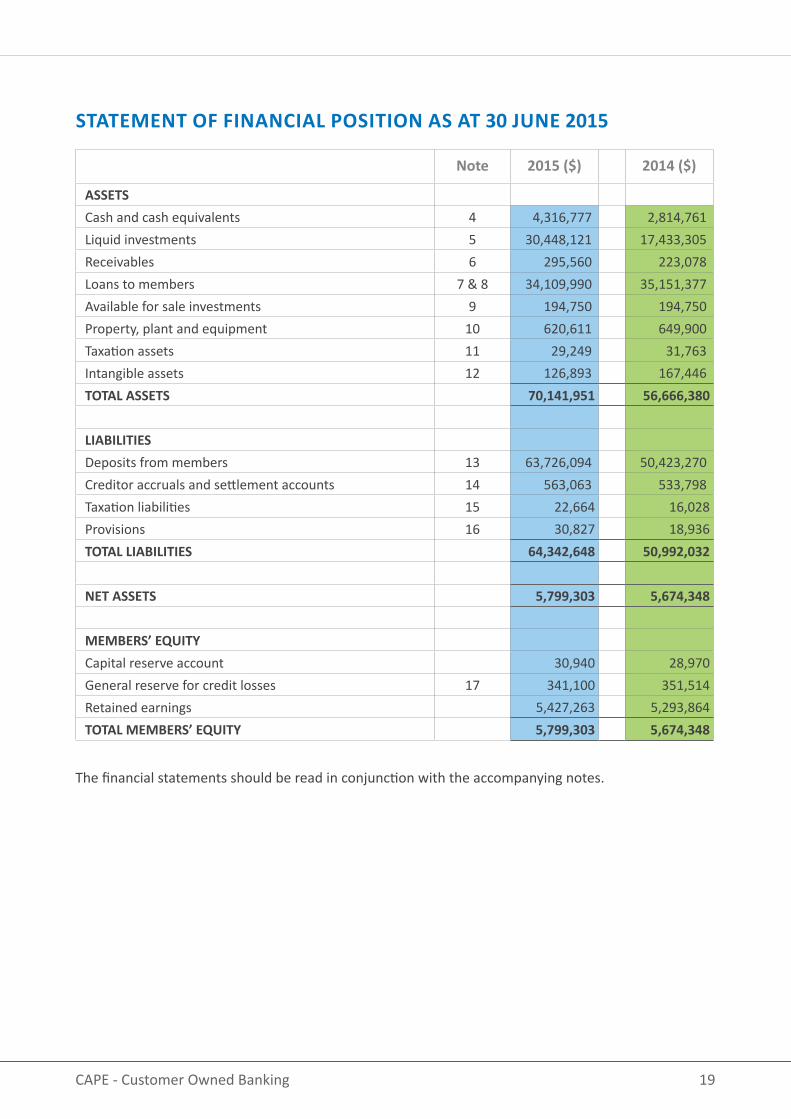

Note 2015 ($) 2014 ($)

ASSETSCash and cash equivalents 4 4,316,777 2,814,761Liquid investments 5 30,448,121 17,433,305Receivables 6 295,560 223,078Loans to members 7 & 8 34,109,990 35,151,377Available for sale investments 9 194,750 194,750Property, plant and equipment 10 620,611 649,900Taxation assets 11 29,249 31,763Intangible assets 12 126,893 167,446TOTAL ASSETS 70,141,951 56,666,380

LIABILITIESDeposits from members 13 63,726,094 50,423,270Creditor accruals and settlement accounts 14 563,063 533,798Taxation liabilities 15 22,664 16,028Provisions 16 30,827 18,936TOTAL LIABILITIES 64,342,648 50,992,032

NET ASSETS 5,799,303 5,674,348

MEMBERS’ EQUITYCapital reserve account 30,940 28,970General reserve for credit losses 17 341,100 351,514Retained earnings 5,427,263 5,293,864TOTAL MEMBERS’ EQUITY 5,799,303 5,674,348

The financial statements should be read in conjunction with the accompanying notes.

STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2015

20 ANNUAL REPORT 2015

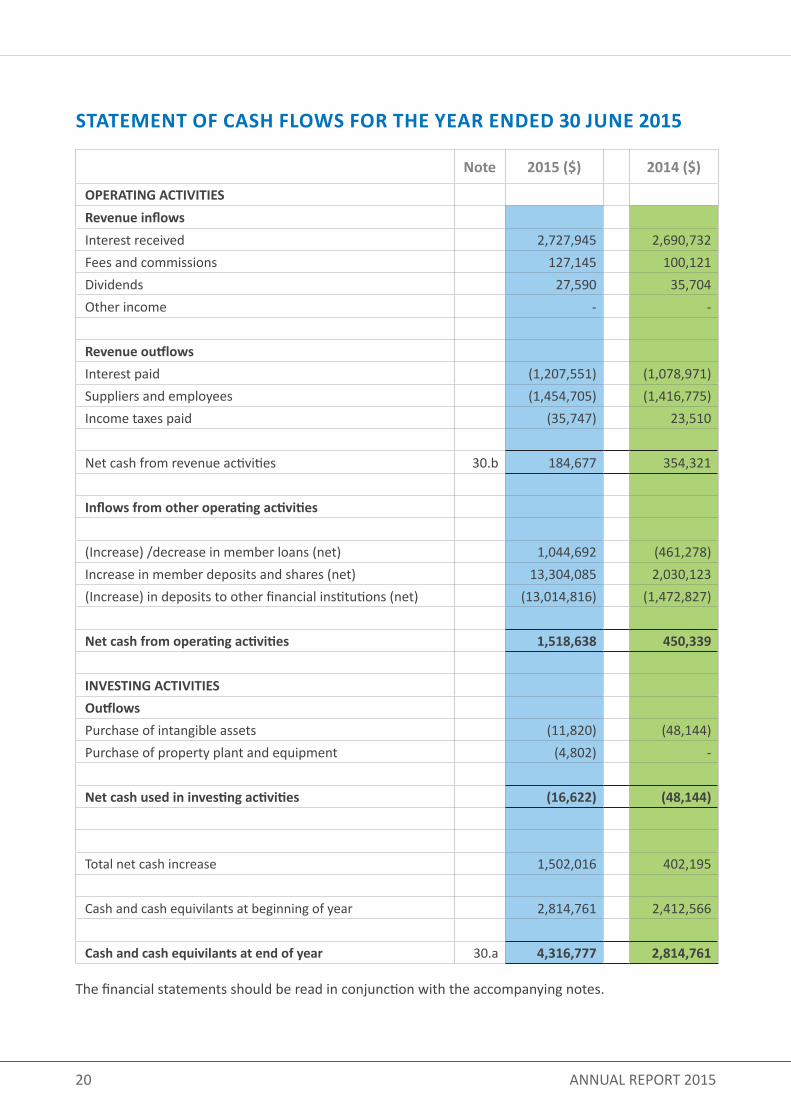

Note 2015 ($) 2014 ($)

OPERATING ACTIVITIESRevenue inflowsInterest received 2,727,945 2,690,732Fees and commissions 127,145 100,121Dividends 27,590 35,704Other income - -

Revenue outflowsInterest paid (1,207,551) (1,078,971)Suppliers and employees (1,454,705) (1,416,775)Income taxes paid (35,747) 23,510

Net cash from revenue activities 30.b 184,677 354,321

Inflows from other operating activities

(Increase) /decrease in member loans (net) 1,044,692 (461,278)Increase in member deposits and shares (net) 13,304,085 2,030,123(Increase) in deposits to other financial institutions (net) (13,014,816) (1,472,827)

Net cash from operating activities 1,518,638 450,339

INVESTING ACTIVITIESOutflowsPurchase of intangible assets (11,820) (48,144)Purchase of property plant and equipment (4,802) -

Net cash used in investing activities (16,622) (48,144)

Total net cash increase 1,502,016 402,195

Cash and cash equivilants at beginning of year 2,814,761 2,412,566

Cash and cash equivilants at end of year 30.a 4,316,777 2,814,761

The financial statements should be read in conjunction with the accompanying notes.

STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 30 JUNE 2015

21CAPE - Customer Owned Banking

TABLE OF OTHER NOTES TO ACCOUNTS

18 Financial risk management objectives and policies 19 Categories of financial instruments20 Maturity profile of financial assets and liabilities21 Current and non current dissection of financial assets and liabilities22 Interest rate change profile of financials assets and liabilities 23 Fair value of financial assets and liabilities24 Financial commitments25 Standby borrowing facilities26 Contingent liabilities27 Disclosures on Directors and other key management personnel28 Outsourcing Arrangements29 Superannuation liabilities30 Notes to statement of cash flows31 Corporate information32 Post balance sheet events

We believe in Principle before Profit

22 ANNUAL REPORT 2015

NOTES TO ACCOUNTS FOR THE YEAR ENDED 30 JUNE 2015

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES

This financial report is prepared for CAPE Credit Union Limited (CAPE) as a single credit union, for the year ended 30 June 2015. The report was authorised for issue on 30 September 2015 in accordance with a resolution of the Board of Directors. The financial report is presented in Australian dollars.

The financial report is a general purpose financial report which has been prepared in accordance with the requirements of the Corporations Act 2001, Australian Accounting Standards and other authoritative pronouncements of the Australian Accounting Standards Board. Compliance with Australian Accounting Standards ensures compliance with the International Financial Reporting Standards (IFRSs) as issued by the International Accounting Standards Board (IASB). CAPE is a for profit entity for the purpose of preparing the financial statements.

A. BASIS OF MEASUREMENTThe financial statements have been prepared on an accruals basis, and are based on historical costs, which do not take into account changing money values or current values of non current assets, except for available for sale investments which are stated at fair value. The accounting policies are consistent with the prior year unless otherwise stated.

B. CLASSIFICATION AND SUBSEQUENT MEASUREMENT OF FINANCIAL ASSETS AND FINANCIAL LIABILITIESFinancial assets and financial liabilities are recognised when CAPE becomes a party to the contractual provisions of the financial instrument, and are measured initially at fair value adjusted by transaction costs. Subsequent measurement of financial assets and financial liabilities are described below.

Financial assets are derecognised when the contractual rights to the cash flows from the financial assets expire, or when the financial asset and all substantial risks and rewards are transferred. A financial liability is derecognised when it is extinguished, discharged, cancelled or expires.

Classification And Subsequent Measurement Of Financial AssetsFor the purpose of subsequent measurement, financial assets are classified into the following categories upon initial recognition:

• loans and receivables• held-to-maturity (HTM) investments• available-for-sale (AFS) financial assets

The category determines subsequent measurement and whether any resulting income and expense is recognised in profit or loss or in other comprehensive income.All financial assets are subject to review for impairment at least at each reporting date to identify whether

23CAPE - Customer Owned Banking

there is any objective evidence that a financial asset or a group of financial assets is impaired. Different criteria to determine impairment are applied for each category of financial assets, which are described below.

All income and expenses relating to financial assets that are recognised in the Statement of Profit or Loss and Other Comprehensive Income are presented within net interest income, except for impairment of loans and receivables which are presented within non interest expenses.

Loans and ReceivablesLoans and receivables are non-derivative financial assets with fixed and determinable payments that are not quoted in an active market. After initial recognition, these are measured at amortised cost using the effective interest method, less provision for impairment. CAPE’s liquid investments, trade and most other receivables fall into this category of financial instruments.

Individually significant receivables are considered for impairment when they are past due or when other objective evidence is received that a specific counterparty will default. Receivables that are not considered to be individually impaired are reviewed for impairment and are determined by reference to the industry and region of a counterparty and other shared credit risk characteristics.

HTM InvestmentsHTM investments are non-derivative financial assets with fixed or determinable payments and fixed maturity other than loans and receivables. Investments are classified as HTM if CAPE has the intention and ability to hold them until maturity. CAPE currently holds Term Deposits, Negotiable Certificates of Deposit and Floating Rate Notes in this category. If more than an insignificant portion of these assets are sold or redeemed early then the asset class will be reclassified as Available for Sale financial assets.

HTM investments are measured subsequently at amortised cost using the effective interest method. If there is objective evidence that the investment is impaired, determined by reference to external credit ratings, the financial asset is measured at the present value of estimated future cash flows. Any changes to the carrying amount of the investment, including impairment losses, are recognised in profit and loss.

Available For Sale (AFS) Financial AssetsAFS financial assets are non-derivative financial assets that are either designated to this category or do not qualify for inclusion in any of the other categories of financial assets. CAPE’s AFS financial assets is the equity investment in Cuscal Limited.

The equity investment in Cuscal Limited is measured at cost less any impairment charges, as its fair value cannot currently be estimated reliably. Impairment charges are recognised in profit and loss.

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES continued

24 ANNUAL REPORT 2015

Classification And Subsequent Measurement Of Financial LiabilitiesCAPE’s financial liabilities include borrowings and trade and other payables. Financial liabilities are measured subsequently at amortised cost using the effective interest method.

C. LOAN TO MEMBERS(i) Basis of recognitionAll loans are initially recognised at fair value, net of loan origination fees and inclusive of transaction costs incurred. Loans are subsequently measured at amortised cost. Any difference between the proceeds and the redemption amount is recognised in the Statement of Profit or Loss and Other Comprehensive Income over the period of the loans using the effective interest method.

Loans to members are reported at their recoverable amount representing the aggregate amount of principal and unpaid interest owing to CAPE at balance date, less any allowance or provision against impairment for debts considered doubtful. A loan is classified as impaired where recovery of the debt is considered unlikely as determined by the Board of Directors.

(ii) Interest earnedTerm loans - interest is calculated on the basis of the daily balance outstanding and is charged in arrears to a members account on the last day of each month.

Overdrafts – interest is calculated initially on the basis of the daily balance outstanding and is charged in arrears to a members account on the last day of the month.

Non accrual loan interest – while still legally recoverable, interest is not brought to account as income where CAPE is informed that the member has deceased, or, where a loan is impaired.

(iii) Loan origination fees and discountsLoan establishment fees and discounts are initially deferred as part of the loan balance, and are brought to account as income over the expected life of the loan as interest revenue.

(iv) Transaction costsTransaction costs are expenses which are direct and incremental to the establishment of the loan. These costs are initially deferred as part of the loan balance, and are brought to account as a reduction to income over the expected life of the loan, and included as part of interest revenue.

(v) Fees on loansThe fees charged on loans after origination of the loan are recognised as income when the service is provided or costs are incurred.

(vi) Net gains and lossesNet gains and losses on loans to members to the extent that they arise from the partial transfer of

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES continued

25CAPE - Customer Owned Banking

business or on securitisation, do not include impairment write downs or reversals of impairment write downs.

D. LOAN IMPAIRMENT(i) Specific and collective provision for impairmentA provision for losses on impaired loans is recognised when there is objective evidence that the impairment of a loan has occurred. Estimated impairment losses are calculated on either a portfolio basis for loans of similar characteristics, or on an individual basis. The amount provided is determined by management and the Board to recognise the probability of loan amounts not being collected in accordance with terms of the loan agreement. The critical assumptions used in the calculation are as set out in Note 8. Note 18 details the credit risk management approach for loans.

The APRA Prudential Standards require a minimum provision to be maintained, based on specific percentages on the loan balance which are contingent upon the length of time the repayments are in arrears. This approach is used to assess the collective provisions for impairment.

An assessment is made at each statement of financial position date to determine whether there is objective evidence that a specific financial asset or a group of financial assets is impaired. Evidence of impairment may include indications that the borrower has defaulted, is experiencing significant financial difficulty, or where the debt has been restructured to reduce the burden to the borrower.

(ii) Reserve for credit lossesIn addition to the above specific provision, the Board has recognised the need to make an allocation from retained earnings to ensure there is adequate protection for members against the prospect that some members will experience loan repayment difficulties in the future. The reserve is based on estimation of potential risk in the loan portfolio based upon:• the level of security taken as collateral; and• the concentration of loans taken by employment type.

(iii) Renegotiated loansLoans which are subject to renegotiated terms which would have otherwise been impaired do not have the repayment arrears diminished and interest continues to accrue to income. Each renegotiated loan is retained at the full arrears position until the normal repayments are reinstated and brought up to date and maintained for a period of 6 months.

E. BAD DEBTS WRITTEN OFF (DIRECT REDUCTION IN LOAN BALANCE)Bad debts are written off from time to time as determined by management and the Board of Directors when it is reasonable to expect that the recovery of the debt is unlikely. Bad debts are written off against the provisions for impairment, if a provision for impairment had previously been recognised. If no provision had been recognised, the write offs are recognised as expenses in the profit and loss.

26 ANNUAL REPORT 2015

F. PROPERTY, PLANT AND EQUIPMENTLand and buildings are measured at cost less accumulated depreciation. Property, plant and equipment, with the exception of freehold land, are depreciated on a straight line basis so as to write off the net cost of each asset over its expected useful life to CAPE.

The useful lives are adjusted if appropriate at each reporting date. Estimated useful lives as at the balance date are as follows:• Buildings - 40 years• Plant and equipment - 3 to 7 years• Assets less than $300 are not capitalised

G. RECEIVABLES FROM OTHER FINANCIAL INSTITUTIONSTerm Deposits, Floating Rate Notes and Negotiable Certificates of Deposit with other financial institutions are unsecured and have a carrying amount equal to their principal amount. Interest on Term Deposits and Negotiable Certificates of Deposit is paid on the daily balance at maturity. Interest on Floating Rate Notes is paid quarterly. All deposits are in Australian currency.

The accrual for interest receivable is calculated on a proportional basis of the unexpired period of the term of the investment or interest rate reset term. Interest receivable is included in the amount of receivables in the statement of financial position.

H. EQUITY INVESTMENTS AND OTHER SECURITIESInvestments in sharesInvestments in shares are classified as available for sale financial assets where they do not qualify for classification as loans and receivables, or investments held for trading.

Investments in shares which do not have a ready market and are not capable of being reliably valued are recorded at the lower of cost or recoverable amount.

All investments are in Australian currency.

I. MEMBER DEPOSITSi) Basis for measurementMember savings and term investments are quoted at the aggregate amount of money owing to depositors.

(ii) Interest payableInterest on savings is calculated on the daily balance and posted to the accounts periodically, or on maturity of the term deposit. Interest on savings is brought to account on the amount of money owing to depositors on an accrual basis in accordance with the interest rate terms and conditions of each savings and term deposit account as varied from time to time. The amount of the accrual is shown as part of amounts payable.

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES continued

27CAPE - Customer Owned Banking

J. PROVISION FOR EMPLOYEE BENEFITSProvision is made for CAPE’s liability for employee benefits arising from services rendered by employees to balance date.

Short-term employee benefits expected to be settled within one year, have been measured at the undiscounted amount that CAPE expects to pay as a result of the unused entitlement.

Annual leave is discounted when calculating the leave liability when CAPE does not expect all annual leave for all employees to be used wholly within 12 months of the end of the reporting period. Annual leave liability is still presented as a current liability for presentation purposes under AASB101 Presentation of Financial Statements.

Other employee benefits payable later than one year have been measured at the present value of the estimated future cash outflows to be made for those benefits discounted using national government bond rates.

Provision for long service leave is on a pro-rata basis from commencement of employment with CAPE based on the present value of its estimated future cash flows.

Annual leave is accrued in respect of all employees on pro-rata entitlement for part years of service and leave entitlement due but not taken at balance date. Annual leave is reflected as part of the creditor accruals and settlement accounts.

Contributions are made by CAPE to an employee’s superannuation fund and are charged to profit and loss as incurred.

K. LEASEHOLD ON PREMISESLeases where the lessor retains substantially all the risks and rewards of ownership of the net asset are classified as operating leases. Payments made under operating leases (net of incentives received from the lessor) are charged to the Statement of Profit or Loss and Other Comprehensive Income on a straight-line basis over the period of the lease.

L. INCOME TAXThe income tax expense shown in the Statement of Profit or Loss and Other Comprehensive Income is based on the profit before income tax adjusted for any non tax deductible, or non assessable items between accounting profit and taxable income. Deferred tax assets and liabilities are recognised using the Statement of Financial Position liability method in respect of temporary differences arising between the tax bases of assets or liabilities and their carrying amounts in the financial statements. Current and deferred tax balances relating to amounts recognised directly in equity are also recognised directly in equity.

28 ANNUAL REPORT 2015

Deferred tax assets and liabilities are recognised for all temporary differences between carrying amounts of assets and liabilities for financial reporting purposes and their respective tax bases at the rate of income tax applicable to the period in which the benefit will be received or the liability will become payable. These differences are presently assessed at 30%.

Deferred tax assets are only brought to account if it is probable that future taxable amounts will be available to utilise those temporary differences. The recognition of these benefits is based on the assumption that no adverse change will occur in income tax legislation; and the anticipation that CAPE will derive sufficient future assessable income and comply with the conditions of deductibility imposed by the law to permit an income tax benefit to be obtained.

M. INTANGIBLE ASSETSItems of computer software which are not integral to the computer hardware owned by CAPE are classified as intangible assets. Computer software is amortised over the expected useful life of the software. These lives range from 2 to 5 years.

N. GOODS AND SERVICES TAXAs a financial institution CAPE is input taxed on all income except for income from commissions and some fees. An input taxed supply is not subject to GST collection, and similarly the GST paid on related or apportioned purchases cannot be recovered. As some income is charged GST, the GST on purchases are generally recovered on a proportionate basis. In addition certain prescribed purchases are subject to reduced input tax credits (RITC), of which 75% of the GST paid is recoverable.

Revenue, expenses and assets are recognised net of the amount of goods and services tax (GST). To the extent that the full amount of the GST incurred is not recoverable from the Australian Tax Office (ATO), the GST is recognised as part of the cost of acquisition of the asset or as part of an item of the expense.

Receivables and payables are stated with the amount of GST included. The net amount of GST recoverable from, or payable to, the ATO is included as a current asset or current liability in the statement of financial position. Cash flows are included in the cash flow statement on a gross basis. The GST components of cash flows arising from investing and financing activities which are recoverable from, or payable to, the Australian Taxation Office are classified as operating cash flows.

O. CASH AND CASH EQUIVALENTSCash comprises cash on hand and demand deposits. Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

P. IMPAIRMENT OF ASSETSAt each reporting date CAPE assesses whether there is any indication that individual assets are impaired. Where impairment indicators exist, recoverable amount is determined and impairment losses are

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICIES continued

29CAPE - Customer Owned Banking

recognised in the profit and loss where the asset’s carrying value exceeds its recoverable amount. Recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. For the purpose of assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. Where it is not possible to estimate recoverable amount for an individual asset, recoverable amount is determined for the cash-generating unit to which the asset belongs.

Q. ACCOUNTING ESTIMATES AND JUDGEMENTSManagement have made critical accounting estimates when applying CAPE’s accounting policies with respect to the impairment provisions for loans - refer Note 8.

R. NEW STANDARDS APPLICABLE FOR THE CURRENT YEARThere were no new or revised accounting standards applicable for the financial year commencing from 1 July 2014 that had any significant impact on the financial statements of CAPE.

S. NEW OR EMERGING STANDARDS NOT YET MANDATORYCertain new accounting standards and interpretations have been published that are not mandatory for 30 June 2015 reporting periods. CAPE’s assessment of the impact of these new standards and interpretations is set out below. Changes that are not likely to impact the financial report of CAPE have not been reported.

We believe we do banking differently

30 ANNUAL REPORT 2015

AASB Reference Nature of Change Application Date

Impact on Initial Application

AASB 9 Financial Instruments

(December 2014)

AASB 9 amends the requirements for classification and measurement of financial assets.

The following requirements have generally been carried forward unchanged from AASB 139 Financial Instruments: Recognition and Measurement into AASB 9. These include the requirements relating to: Classification and measurement of financial liabilities; and Derecognition requirements for financial assets and liabilities.

However, AASB 9 states that:(a) financial assets can be designated and measured at fair value through profit or loss at initial recognition if doing so eliminates or significantly reduces a measurement or recognition inconsistency that would arise from measuring assets or liabilities, or recognising the gains and losses on them, on different bases.

(b) Where the fair value option is used for financial liabilities the change in fair value is to be accounted for as follows:• The change attributable to changes

in credit risk are presented in other comprehensive income; and

• The remaining change is presented in profit and loss.

Periods beginning on or after 1 January 2018

CAPE has not yet assessed the full impact of AASB 9 as this standard does not apply mandatorily before 1 January 2018 and the revised Standard is not permitted to be early adopted until at least the year ended 30 June 2016.

However based upon a preliminary assessment, the Standard is not expected to have a material impact upon the transactions and balances recognised when it is first adopted.

AASB 15 Revenue from Contracts with Customers

Revenue from financial instruments is not covered by this new Standard, but AASB 15 establishes a new revenue recognition model for other types of revenue.

Periods beginning on or after 1 January 2017

CAPE is yet to make a detailed assessment of the impact of AASB 15. However, based upon a preliminary assessment, the Standard is not expected to have a material impact upon the transactions and balances recognised when it is first adopted.

31CAPE - Customer Owned Banking

2015$

2014$

a. Interest revenue

Interest revenue on assets carried at amortised cost Receivables from financial institutions 862,628 660,910 Loans to members 1,951,911 2,068,024

TOTAL INTEREST REVENUE 2,814,539 2,728,934

b. Fee, commission and other income

Fee and commission revenue Fee income on loans – other than loan origination fees 35,341 21,126 Fee Income from member deposits 4,469 3,719 Other fee income 37,537 41,648 Insurance commissions 5,851 6,187 Other commissions 38,851 19,981

TOTAL FEE AND COMMISSION REVENUE 122,049 92,661

Other income Dividends received on available for sale assets 27,590 35,704

TOTAL OTHER INCOME 27,590 35,704

TOTAL FEE COMMISSION AND OTHER INCOME 149,639 128,365

c. Interest expenses

Interest expense on liabilities carried at amortised cost Bank overdraft 26 43 Deposits from members 1,210,964 1,135,151

TOTAL INTEREST EXPENSE 1,210,990 1,135,194

2. STATEMENT OF PROFIT AND LOSS AND OTHER COMPREHENSIVE INCOME

32 ANNUAL REPORT 2015

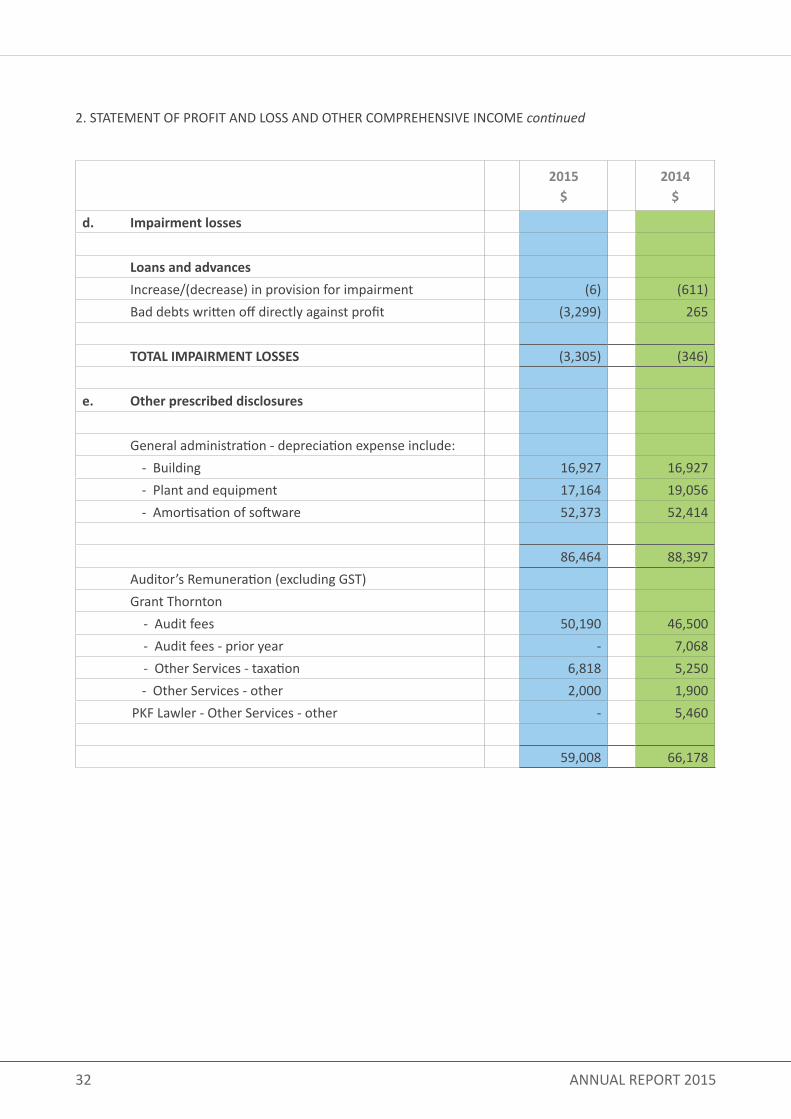

2015$

2014$

d. Impairment losses

Loans and advances Increase/(decrease) in provision for impairment (6) (611) Bad debts written off directly against profit (3,299) 265

TOTAL IMPAIRMENT LOSSES (3,305) (346)

e. Other prescribed disclosures

General administration - depreciation expense include: - Building 16,927 16,927 - Plant and equipment 17,164 19,056 - Amortisation of software 52,373 52,414

86,464 88,397 Auditor’s Remuneration (excluding GST) Grant Thornton - Audit fees 50,190 46,500 - Audit fees - prior year - 7,068 - Other Services - taxation 6,818 5,250 - Other Services - other 2,000 1,900 PKF Lawler - Other Services - other - 5,460

59,008 66,178

2. STATEMENT OF PROFIT AND LOSS AND OTHER COMPREHENSIVE INCOME continued

33CAPE - Customer Owned Banking

2015$

2014$

a. The income tax expense comprises amounts set aside as:-

Current tax charge 43,873 37,775 Deferred tax charge 2,515 (2,175) Adjustments for previous years (1,491) 16 Total income tax expense in income statement 44,897 35,616

b. The prima facie tax payable on profit is reconciled to the income tax expense in the accounts as follows: Profit 169,852 155,294

Prima facie tax payable on profit before income tax at 30% 50,956 46,588 Add tax effect of other assessable income 3,896 2,433 Non-deductible expenses 1,869 1,897

Less - Franking rebate (11,824) (15,302)

- Adjustment for transitional tax rate provision - -

Income tax expense attributable to current year profit 44,897 35,616

(c) Franking credits

Franking credits held by CAPE after adjusting for franking credits that will arise from the payment of income tax payable as at the end of the financial year is:

1,216,225 1,181,737

3. INCOME TAX EXPENSE

4. CASH AND CASH EQUIVALENTS2015

$2014

$

Cash on hand 54,859 71,161 Deposits at call 4,261,918 2,743,600

4,316,777 2,814,761

34 ANNUAL REPORT 2015

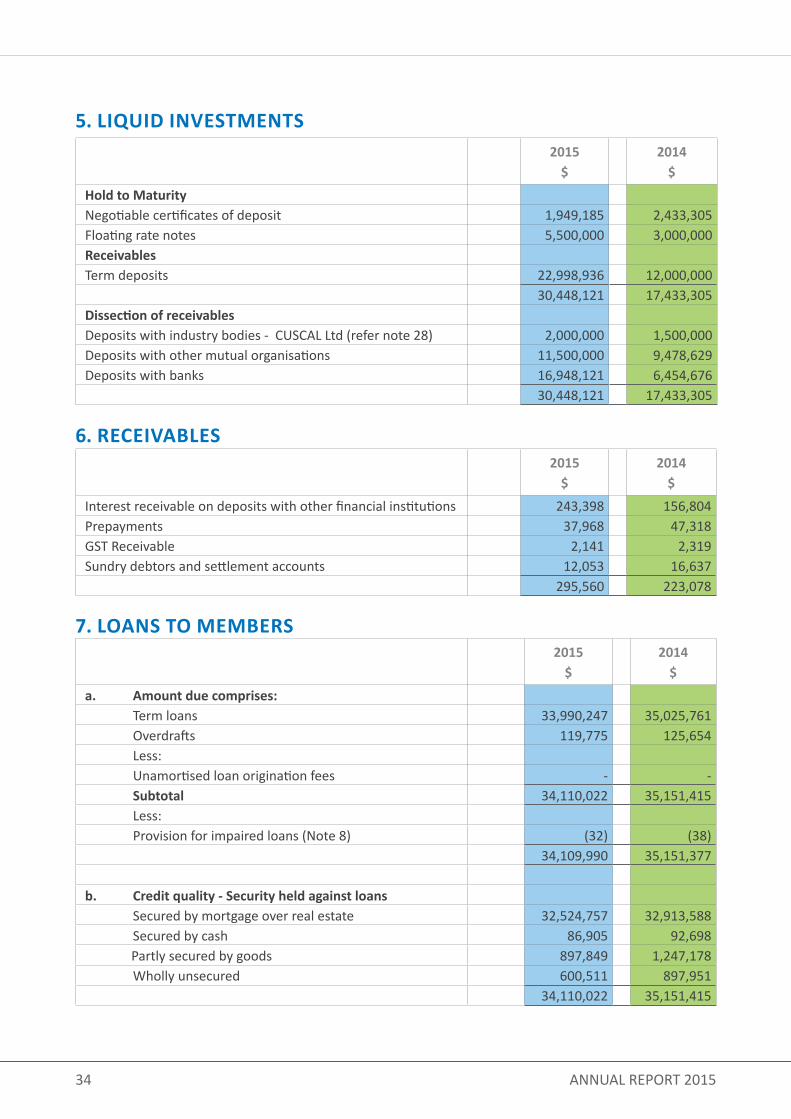

2015$

2014$

a. Amount due comprises: Term loans 33,990,247 35,025,761 Overdrafts 119,775 125,654 Less: Unamortised loan origination fees - - Subtotal 34,110,022 35,151,415 Less: Provision for impaired loans (Note 8) (32) (38) 34,109,990 35,151,377

b. Credit quality - Security held against loans Secured by mortgage over real estate 32,524,757 32,913,588 Secured by cash 86,905 92,698 Partly secured by goods 897,849 1,247,178 Wholly unsecured 600,511 897,951

34,110,022 35,151,415

5. LIQUID INVESTMENTS

6. RECEIVABLES

7. LOANS TO MEMBERS

2015$

2014$

Hold to MaturityNegotiable certificates of deposit 1,949,185 2,433,305Floating rate notes 5,500,000 3,000,000ReceivablesTerm deposits 22,998,936 12,000,000

30,448,121 17,433,305Dissection of receivablesDeposits with industry bodies - CUSCAL Ltd (refer note 28) 2,000,000 1,500,000Deposits with other mutual organisations 11,500,000 9,478,629Deposits with banks 16,948,121 6,454,676

30,448,121 17,433,305

2015$

2014$

Interest receivable on deposits with other financial institutions 243,398 156,804Prepayments 37,968 47,318GST Receivable 2,141 2,319Sundry debtors and settlement accounts 12,053 16,637

295,560 223,078

35CAPE - Customer Owned Banking

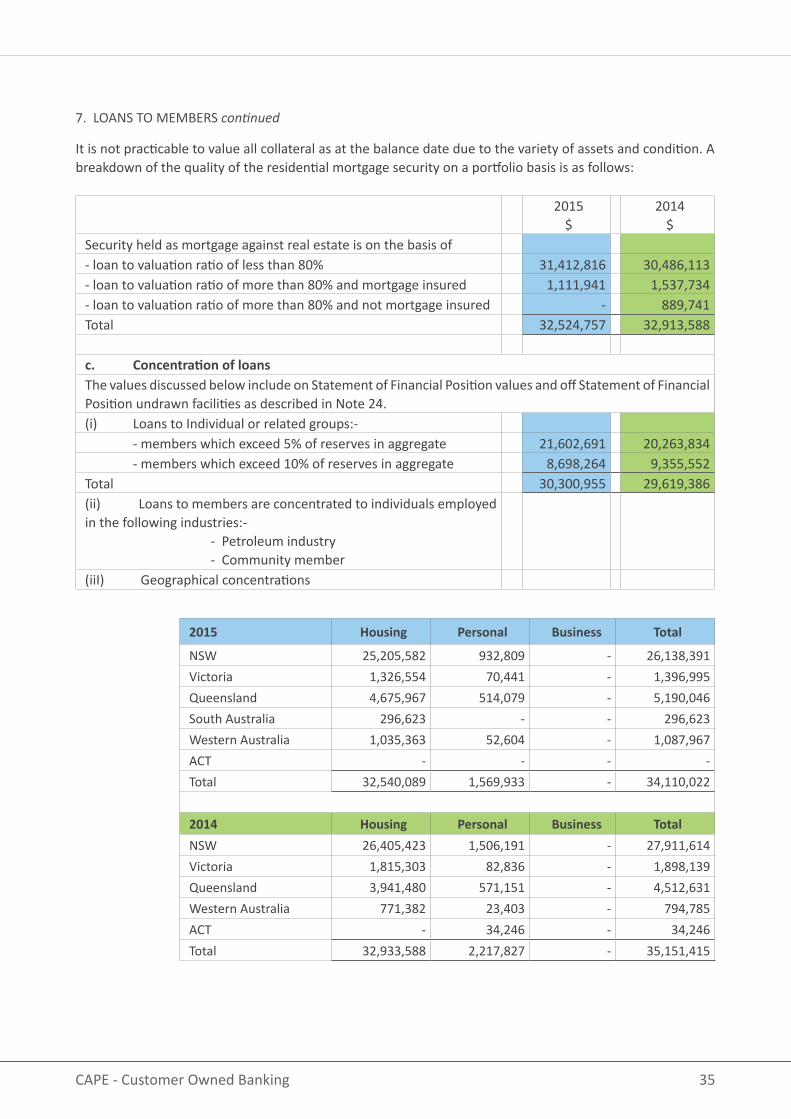

It is not practicable to value all collateral as at the balance date due to the variety of assets and condition. A breakdown of the quality of the residential mortgage security on a portfolio basis is as follows:

2015$

2014$

Security held as mortgage against real estate is on the basis of - loan to valuation ratio of less than 80% 31,412,816 30,486,113- loan to valuation ratio of more than 80% and mortgage insured 1,111,941 1,537,734- loan to valuation ratio of more than 80% and not mortgage insured - 889,741Total 32,524,757 32,913,588

c. Concentration of loans The values discussed below include on Statement of Financial Position values and off Statement of Financial Position undrawn facilities as described in Note 24.(i) Loans to Individual or related groups:- - members which exceed 5% of reserves in aggregate 21,602,691 20,263,834 - members which exceed 10% of reserves in aggregate 8,698,264 9,355,552Total 30,300,955 29,619,386(ii) Loans to members are concentrated to individuals employed in the following industries:- - Petroleum industry - Community member(iiI) Geographical concentrations

2015 Housing Personal Business Total

NSW 25,205,582 932,809 - 26,138,391Victoria 1,326,554 70,441 - 1,396,995Queensland 4,675,967 514,079 - 5,190,046South Australia 296,623 - - 296,623Western Australia 1,035,363 52,604 - 1,087,967ACT - - - -Total 32,540,089 1,569,933 - 34,110,022

2014 Housing Personal Business Total NSW 26,405,423 1,506,191 - 27,911,614Victoria 1,815,303 82,836 - 1,898,139Queensland 3,941,480 571,151 - 4,512,631Western Australia 771,382 23,403 - 794,785ACT - 34,246 - 34,246Total 32,933,588 2,217,827 - 35,151,415

7. LOANS TO MEMBERS continued

36 ANNUAL REPORT 2015

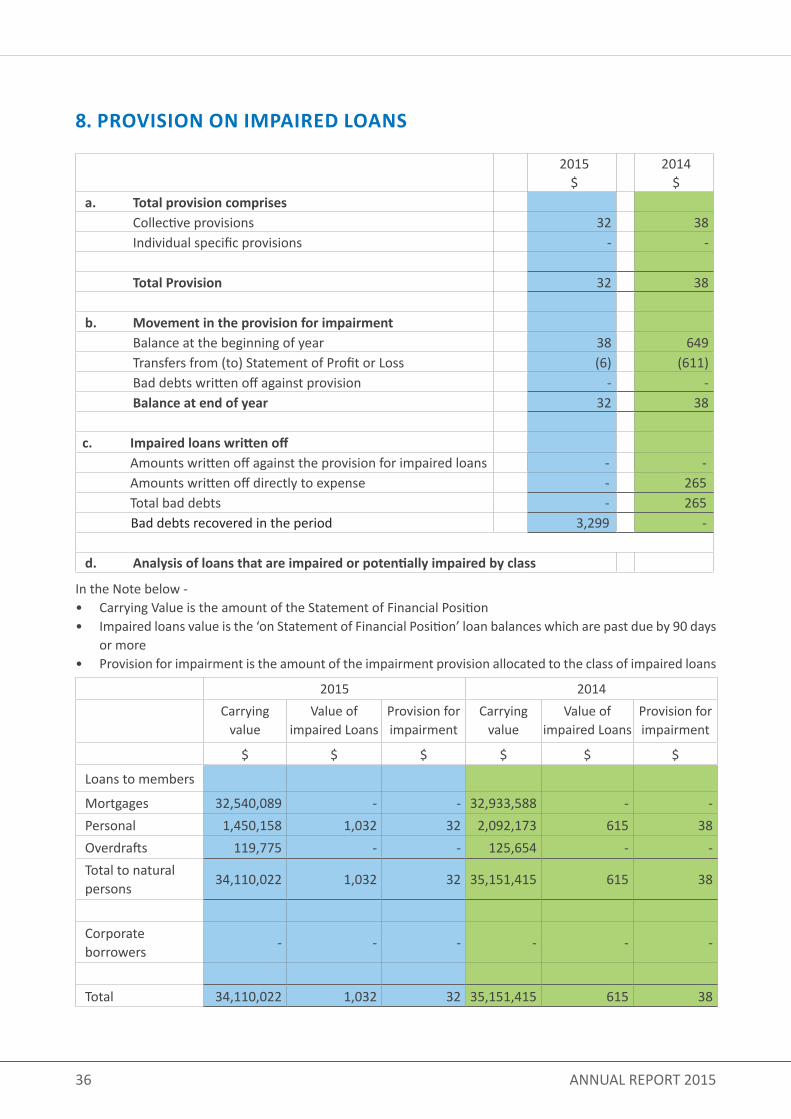

2015$

2014$

a. Total provision comprises Collective provisions 32 38 Individual specific provisions - -

Total Provision 32 38

b. Movement in the provision for impairment Balance at the beginning of year 38 649 Transfers from (to) Statement of Profit or Loss (6) (611) Bad debts written off against provision - - Balance at end of year 32 38

c. Impaired loans written off Amounts written off against the provision for impaired loans - - Amounts written off directly to expense - 265 Total bad debts - 265 Bad debts recovered in the period 3,299 -

d. Analysis of loans that are impaired or potentially impaired by class

2015 2014Carrying

valueValue of

impaired LoansProvision for impairment

Carrying value

Value of impaired Loans

Provision for impairment

$ $ $ $ $ $

Loans to members

Mortgages 32,540,089 - - 32,933,588 - -Personal 1,450,158 1,032 32 2,092,173 615 38Overdrafts 119,775 - - 125,654 - -Total to natural persons

34,110,022 1,032 32 35,151,415 615 38

Corporate borrowers

- - - - - -

Total 34,110,022 1,032 32 35,151,415 615 38

8. PROVISION ON IMPAIRED LOANS

In the Note below - • Carrying Value is the amount of the Statement of Financial Position • Impaired loans value is the ‘on Statement of Financial Position’ loan balances which are past due by 90 days

or more• Provision for impairment is the amount of the impairment provision allocated to the class of impaired loans

37CAPE - Customer Owned Banking

e. Analysis of loans that are impaired or potentially impaired based on age of repayments outstanding 2015 2014

Carrying Value

ProvisionCarrying

ValueProvision

Non impaired $ $ $ $up to 30 days in arrears - - 2,611,451 -30 to 90 days in arrears 217,241 - -Impaired -30 to 90 days in arrears 1,427 - - -90 to 180 days in arrears - - - -180 to 270 days in arrears - - - -270 to 365 days in arrears - - - -Over 365 days in arrears - - -

Overlimit facilities over 14 days 1,032 32 615 38Total in arrears 219,700 32 2,612,066 38Total loans not in arrears 33,890,322 - 32,539,349 -Total 34,110,022 32 35,151,415 38Loans with repayments past due but not impaired are not considered to be impaired as the value of related security over residential property is in excess of the loan due.

f. Loans renegotiatedThere were no loans that were previously past due or impaired which have been renegotiated by CAPE and are no longer regarded as impaired.

g. Key assumptions in determining the provision for impairmentIn the course of the preparation of the annual report CAPE has determined the likely impairment loss on loans which have not maintained the loan repayments in accordance with the loan contract, or where there is other evidence of potential impairment such as industrial restructuring, job losses or economic circumstances. In identifying the impairment likely from these events CAPE is required to estimate the potential impairment using the length of time the loan is in arrears and the historical losses arising in past years. Given the relatively small number of impairedloans, the circumstances may vary for each loan over time resulting in higher or lower impairment losses.

An estimate is based on the period of impairment as is shown in this table:

It is not practicable to determine the fair value of all collateral as at the balance date due to the variety of assets and conditions.

Period of impairment % of Balance

Up to 90 days 090 days to 181 days 40

181 days to 270 days 60270 days to 265 days 80

Over 365 days 100

38 ANNUAL REPORT 2015

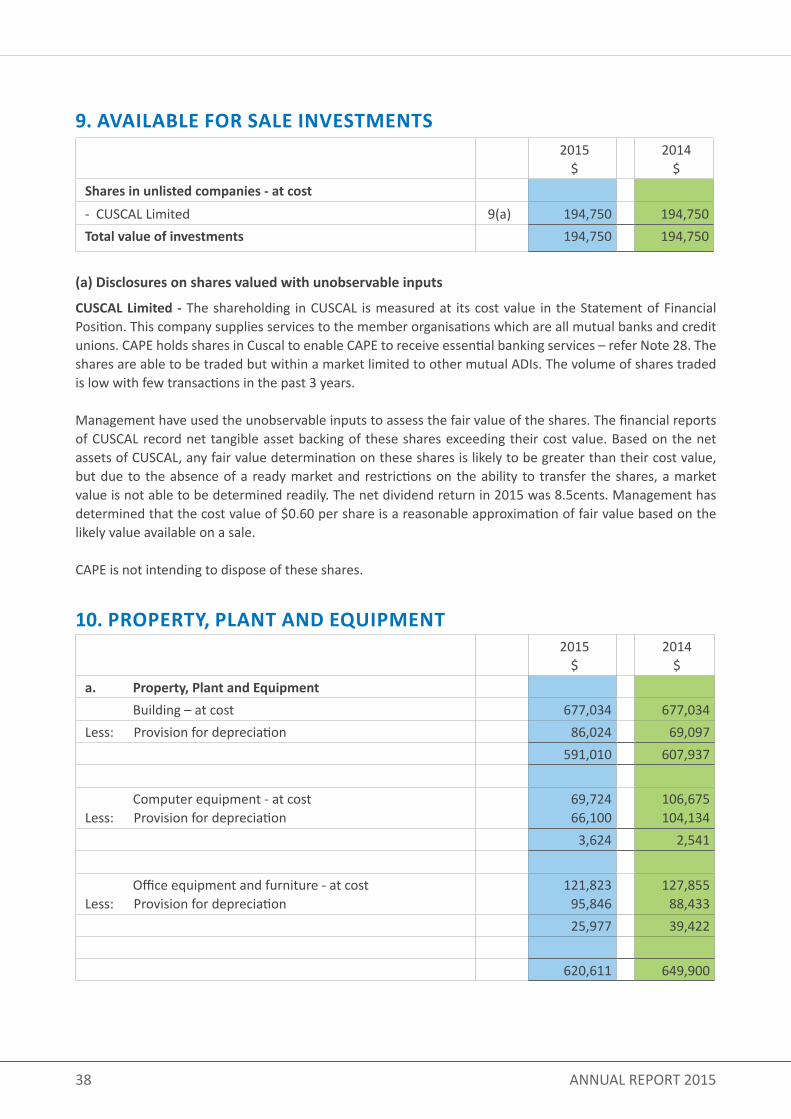

2015$

2014$

Shares in unlisted companies - at cost- CUSCAL Limited 9(a) 194,750 194,750Total value of investments 194,750 194,750

(a) Disclosures on shares valued with unobservable inputs

CUSCAL Limited - The shareholding in CUSCAL is measured at its cost value in the Statement of Financial Position. This company supplies services to the member organisations which are all mutual banks and credit unions. CAPE holds shares in Cuscal to enable CAPE to receive essential banking services – refer Note 28. The shares are able to be traded but within a market limited to other mutual ADIs. The volume of shares traded is low with few transactions in the past 3 years.

Management have used the unobservable inputs to assess the fair value of the shares. The financial reports of CUSCAL record net tangible asset backing of these shares exceeding their cost value. Based on the net assets of CUSCAL, any fair value determination on these shares is likely to be greater than their cost value, but due to the absence of a ready market and restrictions on the ability to transfer the shares, a market value is not able to be determined readily. The net dividend return in 2015 was 8.5cents. Management has determined that the cost value of $0.60 per share is a reasonable approximation of fair value based on the likely value available on a sale.

CAPE is not intending to dispose of these shares.

10. PROPERTY, PLANT AND EQUIPMENT2015

$2014

$a. Property, Plant and Equipment Building – at cost 677,034 677,034Less: Provision for depreciation 86,024 69,097

591,010 607,937

Computer equipment - at costLess: Provision for depreciation

69,72466,100

106,675104,134

3,624 2,541

Office equipment and furniture - at costLess: Provision for depreciation

121,82395,846

127,85588,433

25,977 39,422

620,611 649,900

9. AVAILABLE FOR SALE INVESTMENTS

39CAPE - Customer Owned Banking

2015$

2014$

Deferred Tax Assets 29,249 31,763

Deferred tax assets comprise: Provisions 22,327 18,152 Accrued expenses 27,003 21,548 Others (20,081) (7,937) 29,249 31,763

2015$

2014$

Computer software 375,258 363,439 Less provision for amortisation (248,365) (195,993)

126,893 167,446

Movement in the assets balances during the year were : Opening balance 167,446 171,716 Purchases 11,820 48,144 Less Amortisation charge (52,373) (52,414) Balance at the end of the year 126,893 167,446

11. TAXATION ASSETS

12. INTANGIBLE ASSETS

b. Movement in the assets balances during the year were :2015 2014

BuildingPlant and

EquipmentTotal Building

Plant and Equipment

Total

$ $ $ $ $ $

Opening Balance 607,937 41,963 649,900 624,864 61,019 685,883

Purchases in the year - 4,801 4,801 - - -LessNet Value of assets disposed - - - - - -Depreciation charge 16,927 17,164 34,090 16,927 19,056 35,983Balance at the end of the year 591,010 29,601 620,611 607,937 41,963 649,900

10. PROPERTY, PLANT AND EQUIPMENT continued

40 ANNUAL REPORT 2015

13. DEPOSITS FROM MEMBERS

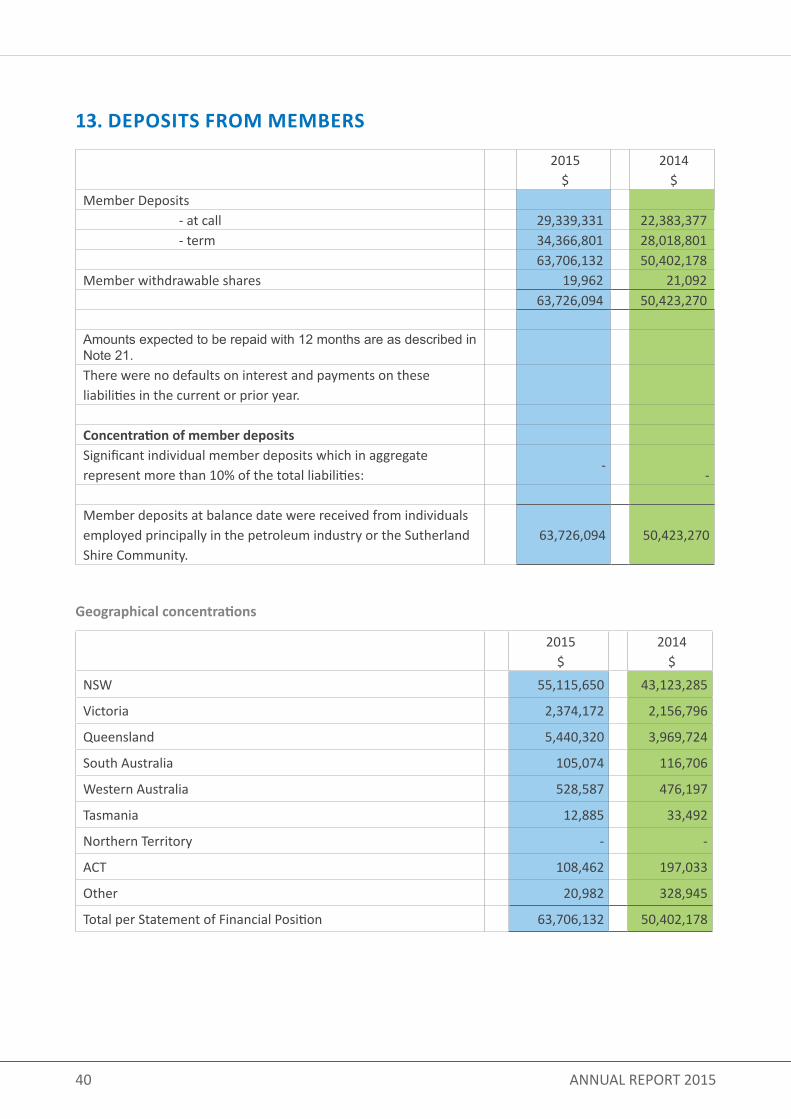

2015

$2014

$Member Deposits - at call 29,339,331 22,383,377 - term 34,366,801 28,018,801

63,706,132 50,402,178Member withdrawable shares 19,962 21,092 63,726,094 50,423,270

Amounts expected to be repaid with 12 months are as described in Note 21. There were no defaults on interest and payments on these liabilities in the current or prior year.

Concentration of member depositsSignificant individual member deposits which in aggregate represent more than 10% of the total liabilities:

--

Member deposits at balance date were received from individuals employed principally in the petroleum industry or the Sutherland Shire Community.

63,726,094 50,423,270

Geographical concentrations

2015$

2014$

NSW 55,115,650 43,123,285

Victoria 2,374,172 2,156,796

Queensland 5,440,320 3,969,724

South Australia 105,074 116,706

Western Australia 528,587 476,197

Tasmania 12,885 33,492

Northern Territory - -

ACT 108,462 197,033

Other 20,982 328,945

Total per Statement of Financial Position 63,706,132 50,402,178

41CAPE - Customer Owned Banking

14. CREDITOR ACCRUALS AND SETTLEMENT ACCOUNTS2015

$2014

$ Annual leave 43,577 41,534 Creditors and accruals 11,027 9,698 Interest payable 326,246 322,807 Accrual for other tax liabilities 586 142 Sundry creditors 181,627 159,617 563,063 533,798

15. TAXATION LIABILITIES2015

$2014

$ Current income tax liability / (asset) 22,664 16,028

Current income tax liability comprises: Balance – previous year 16,028 (42,389) Less refund/(paid) (14,537) 42,373 Over statement/(under statement) in prior year (1,491) 16 Carried forward from previous year - - Liability for income tax in current year 43,875 34,891 Less instalments paid in current year 21,211 18,863 Balance – current year 22,664 16,028

16. PROVISIONS2015

$2014

$

Long service leave 30,827 18,936

17. GENERAL RESERVE FOR CREDIT LOSSES2015

$2014

$

General reserve for credit losses 341,100 351,514

General reserve for credit losses

This reserve records amounts maintained to comply with the Prudential Standards set down by APRA Balance at beginning of year 351,514 346,904 Increase transferred from retained earnings (10,414) 4,610 Balance at end of year 341,100 351,514

42 ANNUAL REPORT 2015

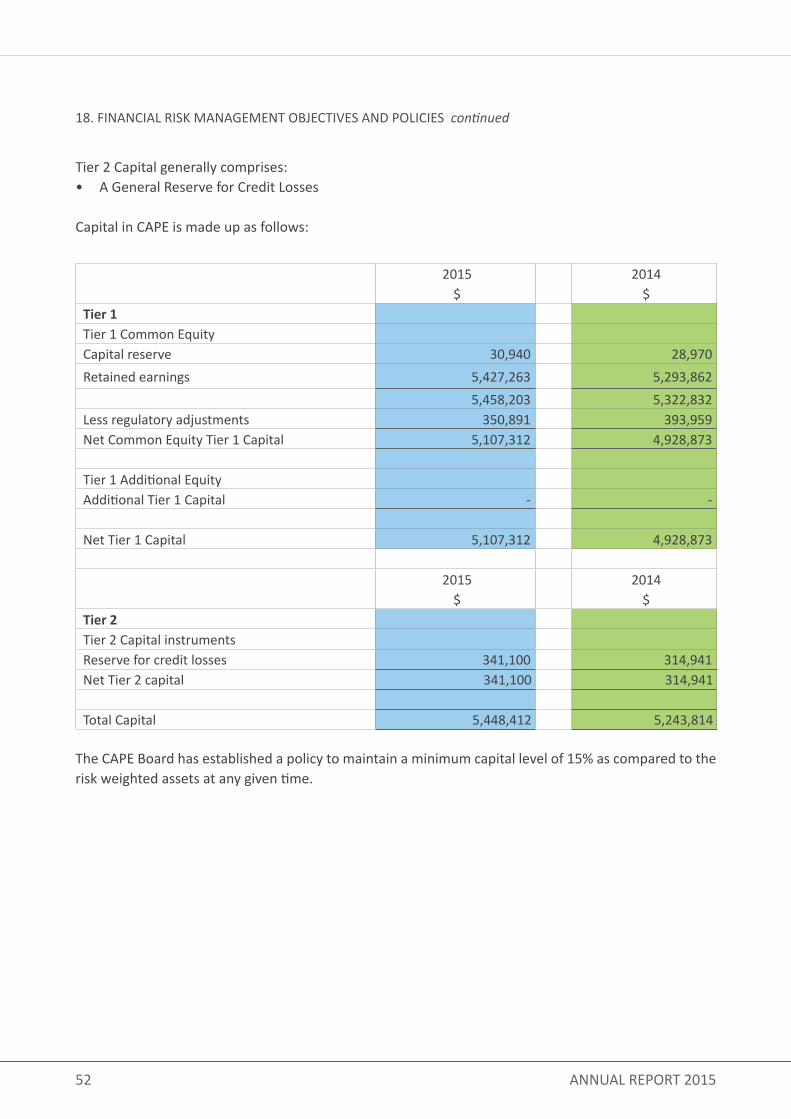

18. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES

IntroductionThe Board has endorsed a policy of compliance and risk management to support the risk profile of CAPE.

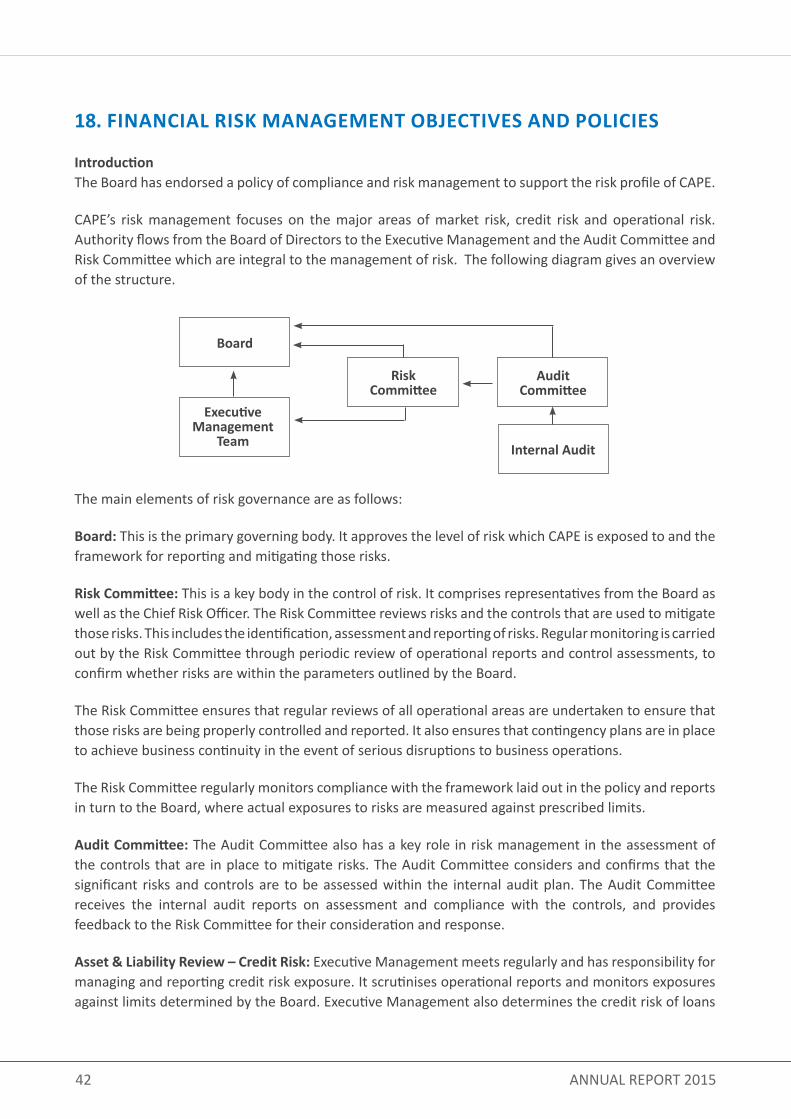

CAPE’s risk management focuses on the major areas of market risk, credit risk and operational risk. Authority flows from the Board of Directors to the Executive Management and the Audit Committee and Risk Committee which are integral to the management of risk. The following diagram gives an overview of the structure.

The main elements of risk governance are as follows:

Board: This is the primary governing body. It approves the level of risk which CAPE is exposed to and the framework for reporting and mitigating those risks.

Risk Committee: This is a key body in the control of risk. It comprises representatives from the Board as well as the Chief Risk Officer. The Risk Committee reviews risks and the controls that are used to mitigate those risks. This includes the identification, assessment and reporting of risks. Regular monitoring is carried out by the Risk Committee through periodic review of operational reports and control assessments, to confirm whether risks are within the parameters outlined by the Board.

The Risk Committee ensures that regular reviews of all operational areas are undertaken to ensure that those risks are being properly controlled and reported. It also ensures that contingency plans are in place to achieve business continuity in the event of serious disruptions to business operations.

The Risk Committee regularly monitors compliance with the framework laid out in the policy and reports in turn to the Board, where actual exposures to risks are measured against prescribed limits.

Audit Committee: The Audit Committee also has a key role in risk management in the assessment of the controls that are in place to mitigate risks. The Audit Committee considers and confirms that the significant risks and controls are to be assessed within the internal audit plan. The Audit Committee receives the internal audit reports on assessment and compliance with the controls, and provides feedback to the Risk Committee for their consideration and response.

Asset & Liability Review – Credit Risk: Executive Management meets regularly and has responsibility for managing and reporting credit risk exposure. It scrutinises operational reports and monitors exposures against limits determined by the Board. Executive Management also determines the credit risk of loans

Board

Executive Management

Team

Risk Committee

Internal Audit

Audit Committee

43CAPE - Customer Owned Banking

in the banking book, ensures provisioning is accurate and determines controls that need to be put in place regarding the authorisation of new loans.

Executive Management has responsibility for implementing policies to ensure that all large credit exposures are properly pre-approved, measured and controlled. Details concerning a prospective borrower are subject to a criteria-based decision-making process and strictly within the Delegations of Authority approved by the Board. Criteria used for this assessment include: credit references, loan-to-value ratio on security and borrower’s capacity to repay which vary according to the value of the loan or facility.

All large credit exposure facilities above policy limits are approved by the Board. All exposures are checked daily against approved limits.

All loans are managed weekly through the monitoring of the scheduled repayments. Accounts where the arrears are over 90 days or overdrawn/overlimit facilities over 14 days have collective provisions charged against them. Other provisions are taken up on accounts considered doubtful and the status of these loans is reported to the Board.

Arrears are strictly controlled. The size of the loan book is such that it is possible to monitor each individual exposure to evaluate whether specific provisions are necessary and adequate. The Officer responsible for credit control reports to the General Manager and implements CAPE’s credit risk policy. Additionally, a collective provision is held to cover any losses where there is objective evidence that losses are present in components of the loans and advances portfolio at the Statement of Financial Position date.

Asset and Liability Review - Market Risk: Executive Management meets regularly and has responsibility for managing interest rate risk exposures, and ensuring that the treasury and finance functions adhere to exposure limits as outlined in the policies for interest rate GAP. The weekly scrutiny of market risk reports is intended to prevent any exposure breaches prior to the monthly review by the Board.

Chief Risk Officer: has responsibility for both liaising with the operational function to ensure timely production of information for the Board and ensuring that instructions passed down from the Board via the Risk Committee are implemented.

Internal Audit: Internal audit has responsibility for implementing the controls testing and assessment as required by the Audit Committee.

CAPE’s risk management policies encompassed in the overall risk management framework include both core and non core risks including:

• Market and Interest rate risk • Liquidity management• Credit risk management• Operations risk management including data risk management

CAPE has undertaken the following strategies to minimise the risks arising from financial instruments.

44 ANNUAL REPORT 2015

A. MARKET RISK POLICYThe objective of CAPE’s market risk management is to manage and control market risk exposures in order to optimise and minimise risk.

Market risk is the risk that changes in interest rates, foreign exchange rates or other prices and volatilities will have an adverse effect on CAPE’s financial condition or results. CAPE is not exposed to currency risk, and other significant price risk. CAPE does not trade in the financial instruments it holds on its books. CAPE is exposed only to interest rate risk arising from changes in market interest rates.

The management of market risk is the responsibility of the Risk Committee, which reports directly to the Board.

(i) INTEREST RATE RISK

Interest rate risk is the risk of variability of the fair value or future cash flows arising from financial instruments due to the changes in interest rates.

Most banks are exposed to interest rate risk within its Treasury operations. CAPE does not have a treasury operation and does not trade in financial instruments.

Interest Rate Risk In The Banking BookCAPE is exposed to interest rate risk in its banking book due to mismatches between the repricing dates of assets and liabilities.

The interest rate risk on the banking book is monitored by the Manager Finance and Accounting and reported to the General Manager and reported to the Board monthly.

In the banking book the most common risk CAPE faces arises from fixed rate assets and liabilities. This exposes CAPE to the risk of sensitivity should interest rates change.

The level of mismatch on the banking book is set out in Note 22 below. The table set out at Note 22 displays the period that each asset and liability will reprice as at the balance date. This risk is not considered significant to warrant the use of derivatives to mitigate this risk.

Method Of Managing Risk CAPE manages its interest rate risk by the use of interest rate sensitivity analysis, the detail and assumptions used are set out below.

Interest Rate Sensitivity CAPE’s exposure to market risk is measured and monitored using interest rate sensitivity models. The policy of CAPE to manage the risk is to maintain a balanced ‘on book’ strategy by ensuring the net interest rate gaps between assets and liabilities are not excessive. The Gap is measured regularly to

18. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES continued

45CAPE - Customer Owned Banking

identify any large exposures to interest rate movements and to rectify the excess through targeted fixed rate interest products available through investment assets, and term deposit liabilities to rectify the imbalance to within acceptable levels. The policy of CAPE is not to undertake derivatives to match the interest rate risks. CAPE’s exposure to interest rate risk is set out in Note 22.

Based on the calculations as at 30 June 2015, the net profit impact for a 1% decrease movement in interest rates would be a reduction in net interest income of $174,579 (2014: $212,123). The net profit impact for a 1% increase movement in interest rates would be an improvement in net interest income of $174,579 (2014: $212,123).

CAPE performs a sensitivity analysis to measure market risk exposures.

The method used in determining the sensitivity was to evaluate the profit based on the timing of the interest repricing on the banking book of CAPE for the next 12 months. In doing the calculation the assumptions applied were that:

- the interest rate change would be applied equally over to the loan products, term deposits and investments; - the rate change would be as at the beginning of the 12 month period and no other rate changes would be effective during the period; - the term deposits would all reprice to the new interest rate at the term maturity, or be replaced by deposits with similar terms and rates applicable; - fixed rate loans would all reprice to the new interest rate at the contracted date and treated as variable loans from that point; - mortgage loans all reprice to the new interest rate within 28 days; - personal loans all reprice to the new interest rate within 28 days; - all loans would be repaid in accordance with the current average repayment rate (or contractual repayment terms); - the value and mix of call savings to term deposits will be unchanged; and - the value and mix of personal loans to mortgage loans will be unchanged.

There has been no change to CAPE’s exposure to market risk or the way CAPE manages and measures market risk in the reporting period.

B. LIQUIDITY RISKLiquidity risk is the risk that CAPE may encounter difficulties raising funds to meet commitments associated with financial instruments, e.g. borrowing repayments or member withdrawal demands. It is the policy of the Board of Directors that CAPE maintains adequate cash reserves and committed credit facilities so as to meet the member withdrawal demands when requested.

CAPE manages liquidity risk by:• Continuously monitoring actual daily cash flows and longer term forecasted cash flows;

46 ANNUAL REPORT 2015

• Monitoring the maturity profiles of financial assets and liabilities;• Maintaining adequate reserves, liquidity support facilities and reserve borrowing facilities; and• Monitoring the prudential liquidity ratio daily.

CAPE has a long standing arrangement with the industry liquidity support entity Credit Union Financial Support Services (CUFSS) which can access industry funds to provide support to CAPE should it be necessary at short notice.

CAPE is a member of the Austraclear “system” as an Associate participant. Austraclear provides clearing and settlement services in relation to security transactions entered into by CAPE. Additionally CAPE also now enjoys membership of the Reserve Bank Information and Transfer System (RITS) which is Australia’s high-value payments system, used by banks and other approved institutions to settle their payment obligations on a real-time gross settlement (RTGS) basis.

RITS membership also facilitates CAPE’s participation in the Reserve Bank’s domestic market operations whereby the Reserve Bank will purchase, if required, securities held by CAPE to assist in liquidity risk management.

CAPE is required to maintain at least 9% of total adjusted liabilities as liquid assets capable of being converted into cash within 24 hours under the APRA Prudential standards. CAPE policy is to ensure a minimum of 13% of total adjusted liabilities is held as liquid assets to maintain adequate funds for meeting member withdrawal requests. The ratio is checked daily. Should the liquidity ratio fall below this level the management and Board are to address the matter and ensure that the liquid funds are obtained from new deposits, or borrowing facilities available. Note 25 describes the borrowing facilities as at the balance date. These facilities are in addition to the support from CUFSS.

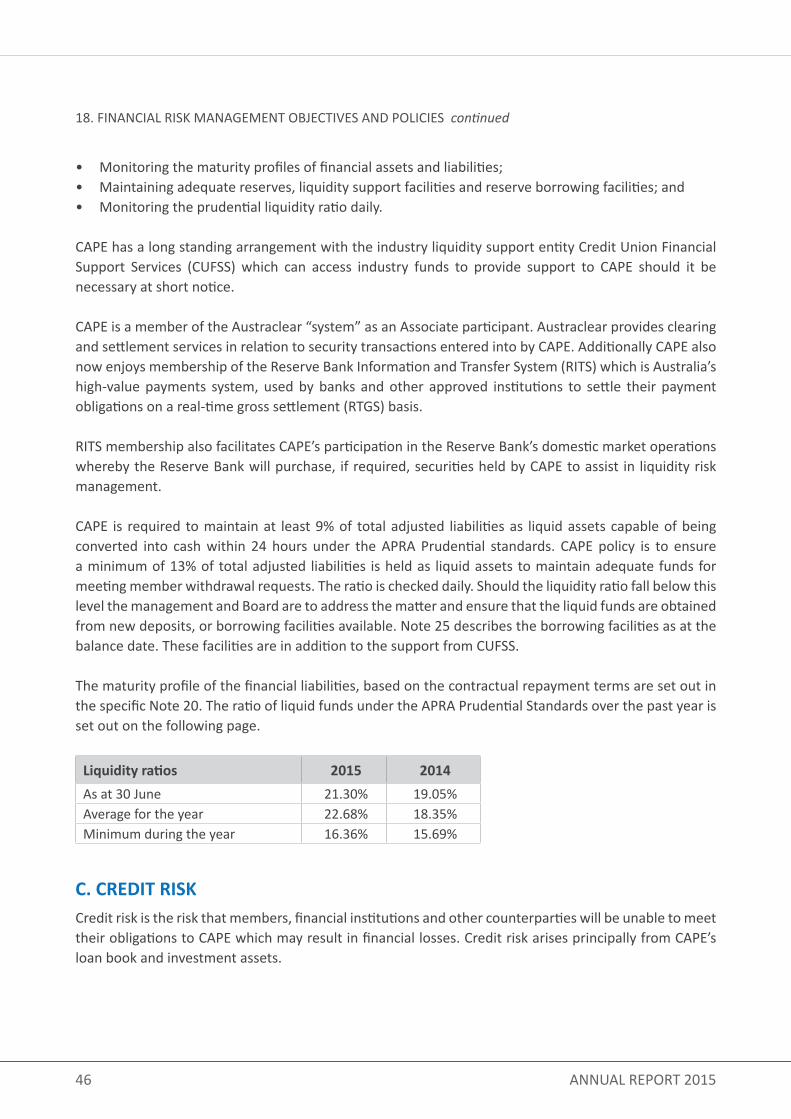

The maturity profile of the financial liabilities, based on the contractual repayment terms are set out in the specific Note 20. The ratio of liquid funds under the APRA Prudential Standards over the past year is set out on the following page.

Liquidity ratios 2015 2014As at 30 June 21.30% 19.05%Average for the year 22.68% 18.35%Minimum during the year 16.36% 15.69%

C. CREDIT RISKCredit risk is the risk that members, financial institutions and other counterparties will be unable to meet their obligations to CAPE which may result in financial losses. Credit risk arises principally from CAPE’s loan book and investment assets.

18. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES continued

47CAPE - Customer Owned Banking

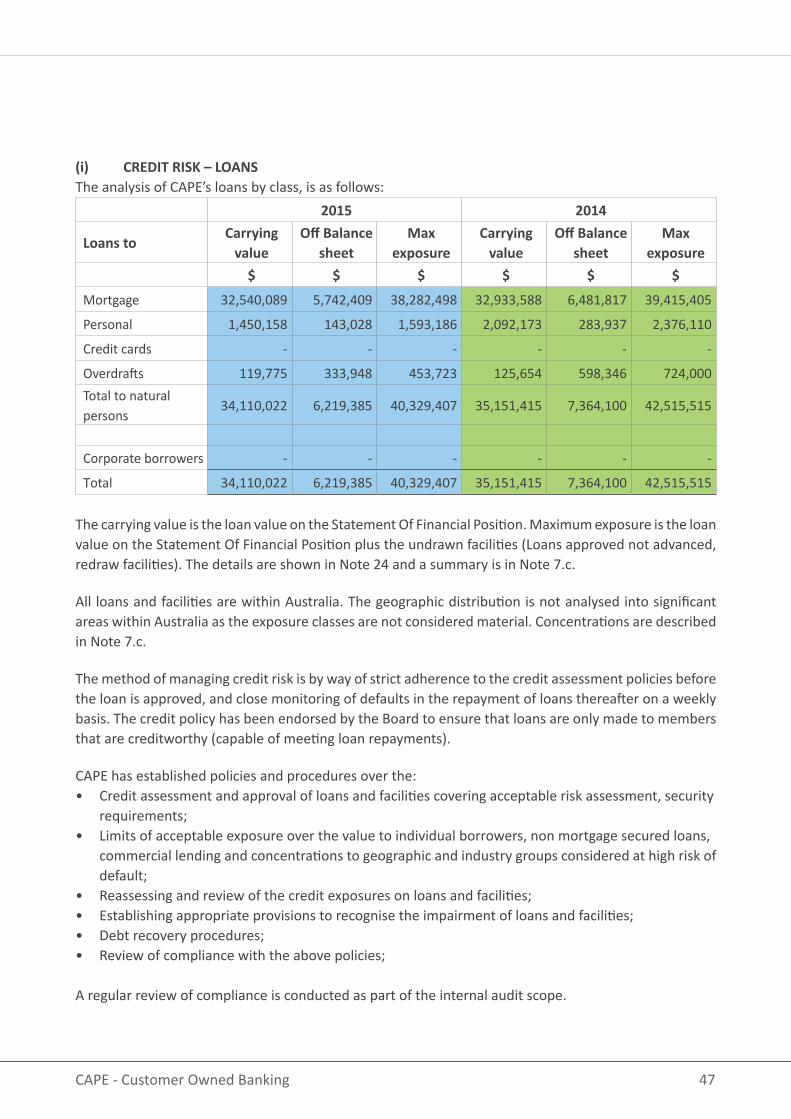

(i) CREDIT RISK – LOANSThe analysis of CAPE’s loans by class, is as follows:

2015 2014

Loans to Carrying

valueOff Balance

sheetMax

exposureCarrying

valueOff Balance

sheetMax

exposure$ $ $ $ $ $

Mortgage 32,540,089 5,742,409 38,282,498 32,933,588 6,481,817 39,415,405

Personal 1,450,158 143,028 1,593,186 2,092,173 283,937 2,376,110

Credit cards - - - - - -

Overdrafts 119,775 333,948 453,723 125,654 598,346 724,000Total to natural persons

34,110,022 6,219,385 40,329,407 35,151,415 7,364,100 42,515,515

Corporate borrowers - - - - - -

Total 34,110,022 6,219,385 40,329,407 35,151,415 7,364,100 42,515,515

The carrying value is the loan value on the Statement Of Financial Position. Maximum exposure is the loan value on the Statement Of Financial Position plus the undrawn facilities (Loans approved not advanced, redraw facilities). The details are shown in Note 24 and a summary is in Note 7.c.

All loans and facilities are within Australia. The geographic distribution is not analysed into significant areas within Australia as the exposure classes are not considered material. Concentrations are described in Note 7.c.

The method of managing credit risk is by way of strict adherence to the credit assessment policies before the loan is approved, and close monitoring of defaults in the repayment of loans thereafter on a weekly basis. The credit policy has been endorsed by the Board to ensure that loans are only made to members that are creditworthy (capable of meeting loan repayments).

CAPE has established policies and procedures over the:• Credit assessment and approval of loans and facilities covering acceptable risk assessment, security

requirements;• Limits of acceptable exposure over the value to individual borrowers, non mortgage secured loans,

commercial lending and concentrations to geographic and industry groups considered at high risk of default;

• Reassessing and review of the credit exposures on loans and facilities; • Establishing appropriate provisions to recognise the impairment of loans and facilities;• Debt recovery procedures;• Review of compliance with the above policies;

A regular review of compliance is conducted as part of the internal audit scope.

48 ANNUAL REPORT 2015

Past Due And Impaired

A financial asset is past due when the counterparty has failed to make a payment when contractually due. As an example, a member enters into a lending agreement with CAPE that requires interest and a portion of the principal to be paid every month. On the first day of the next month, if the agreed repayment amount has not been paid, the loan is past due. Past due does not mean that a counterparty will never pay, but it can trigger various actions such as renegotiation, enforcement of covenants, or legal proceedings. Once the past due exceeds 90 days the loan is regarded as impaired, unless other factors indicate the impairment should be recognised sooner.

Daily reports monitor the loan repayments to detect delays in repayments and recovery action is undertaken after 7 days. For loans where repayments are doubtful, external consultants may be engaged to conduct recovery action once the loan is over 90 days in arrears. The exposures to losses arise predominantly in the personal loans and facilities not secured by registered mortgages over real estate.

If such evidence exists, the estimated recoverable amount of that asset is determined and any impairment loss, based on the net present value of future anticipated cash flows, is recognised in the Statement of Profit or Loss. In estimating these cash flows, management makes judgements about a counterparty’s financial situation and the net realisable value of any underlying collateral.

In addition to specific provisions against individually significant financial assets, CAPE makes collective assessments for each financial asset portfolio segmented by similar risk characteristics.

Statement of Financial Position provisions are maintained at a level that management deems sufficient to absorb probable incurred losses in CAPE’s loan portfolio from homogenous portfolios of assets and individually identified loans.

A provision for incurred losses is established on all past due loans after a specified period of repayment default where it is probable that some of the capital will not be repaid or recovered. Specific loans and portfolios of assets are provided against depending on a number of factors including deterioration in the general economy, changes in a counterparties industry, and technological developments, as well as identified structural weaknesses or deterioration in cash flows.

The provisions for impaired and past due exposures relate to the loans to members. Past due value is the on Statement of Financial Position loan balances which are past due by 90 days or more. Details are as set out in Note 8.

Bad Debts

Amounts are written off when collection of the loan or advance is considered to be remote. All write offs are on a case by case basis, taking account of the exposure at the date of the write off.

18. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES continued

49CAPE - Customer Owned Banking

On secured loans, the write off takes place on ultimate realisation of collateral value, or from claims on any lenders mortgage insurance. A reconciliation in the movement of both past due and impaired exposure provisions is provided in Note 8.

Collateral Securing Loans

A sizeable portfolio of the loan book is secured by residential property in Australia. Therefore, CAPE is exposed to risks in the reduction of the Loan to Value (LVR) cover should the property market be subject to a decline. The risk of losses from the loans undertaken is primarily reduced by the nature and quality of the security taken.

Concentration Risk – Individuals

Concentration risk is a measurement of CAPE’s exposure to an individual counterparty (or group of related parties). If prudential limits are exceeded as a proportion of CAPE’s regulatory capital (10%) a large exposure is considered to exist. No capital is required to be held against these but APRA must be informed. APRA may impose additional capital requirements if it considers the aggregate exposure to all loans over the 10% capital benchmark, to be higher than acceptable.

The aggregate value of large exposure loans are set out in Note 7. Concentration exposures to counterparties are closely monitored with annual reviews being prepared for all exposures over 5% of the capital base.

Concentration Risk – Industry

There is no concentration of credit risk with respect to loans and receivables as CAPE has a large number of customers dispersed in areas of employment.

CAPE has a concentration in the retail lending for members who comprise employees and family in the petroleum industry. This concentration is considered acceptable on the basis that CAPE was formed to service these members, and the employment concentration is not exclusive. Should members leave the industry the loans continue and other employment opportunities are available to the members to facilitate the repayment of the loans. The details of the geographical and industry concentrations are set out in Note 7.

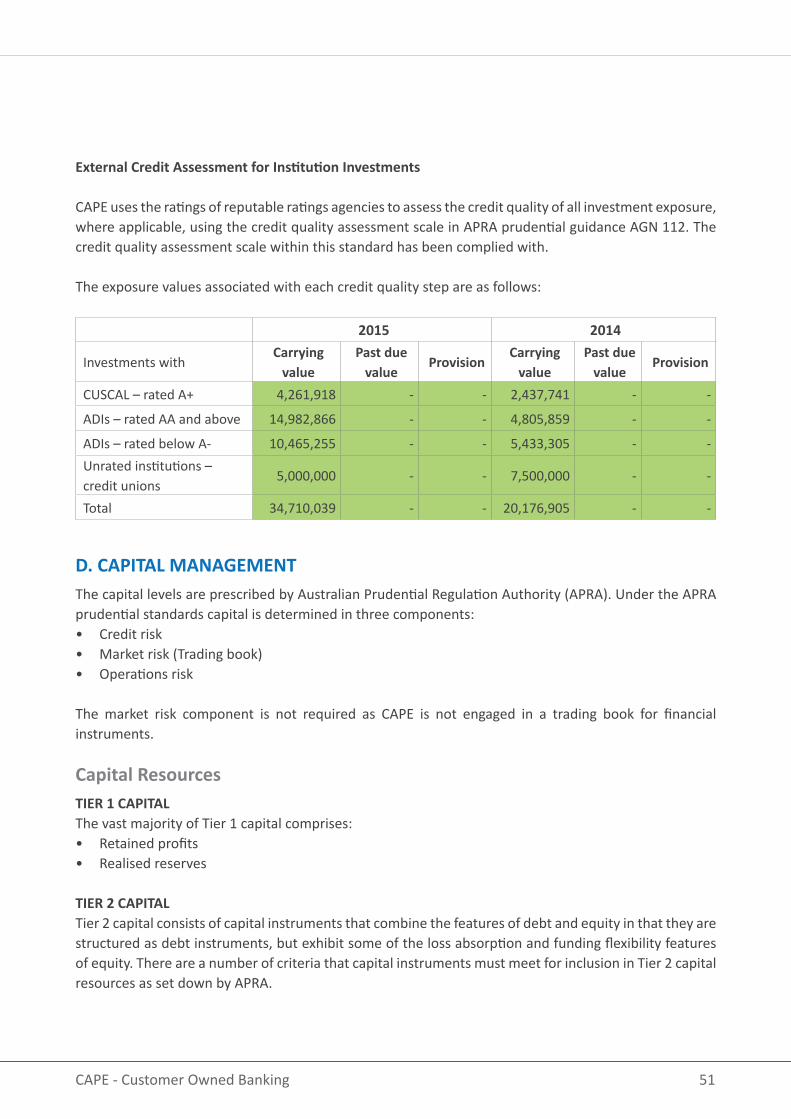

(ii) CREDIT RISK – LIQUID INVESTMENTS

Credit risk is the risk that the other party to a financial instrument will fail to discharge their obligation resulting in CAPE incurring a financial loss. This usually occurs when debtors fail to settle their obligations owing to CAPE.

50 ANNUAL REPORT 2015