Embed Size (px)

Citation preview

Education • Examination • Experience • Ethics

JOURNAL4EKKDN PP 11977/05/2011 (029485) Vol. 11, No. 1, 1Q 2011

T h e o f f i c i a l p u b l i c a t i o n o f t h e F i n a n c i a l P l a n n i n g A s s o c i a t i o n o f M a l a y s i a

Senator Datuk Seri Idris JalaMinister in the Prime Minister’s Department & CEO,Performance Management and Delivery Unit (PEMANDU)

Science, Behaviour, Art and ‘Nudges’

Competent Financial Planners: The Way Towards Professional Acceptance

Three Questions to Help Your Clients Shift Their Retirement Funding Capacity into Overdrive!

www.fpam.org.my

&Towards High-Income

Sustainability

p 18

INDUSTRY

Science, Behaviour, Art and ‘Nudges’

Competent Financial Planners: The Way Towards Professional Acceptance

Three Questions to Help Your Clients Shift Their Retirement Funding Capacity into Overdrive!

ISLAMIC FINANCE

Realising Maqasid Al-Shariah in Islamic Financial Planning

ECONOMY

The Tunisian Effect: Hike in Oil Price Revisited

NEWS IN BRIEF

Making Public Awareness a Top Priority

Public Bank’s new fund to invest in mid-to large-cap stocks in Asia Pacific

CFP CERTIFICATION GLOBAL UPDATESCHAPTER ACTIVITIESCE COURSES

Towards High-Income& Sustainability

“Malaysia has no time to lose,” said Senator Datuk Seri Idris Jala, Minister in the Prime Minister’s Department and chief executive officer of PEMANDU (Performance Management and Delivery Unit). “We need a complete, radical economic transformation. The days of depending on traditional growth engines are over.”

COVER STORY

5

9

25

13

28

33

343639

In this Issue

Copyright 2011 © Financial Planning Association of Malaysia. All rights reserved. (KKDN PP 11977/05/2011) No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the written permission of the publisher. All information provided in this publication are for the purpose of education and keeping the members of the Financial Planning Association of Malaysia and the general public informed of news, developments and direction in the financial planning industry. No article published here is exhaustive on the respective subject it covers and is not intended to be a substitute for legal and financial advice or diminish any duty, statutory or otherwise imposed on persons by existing laws.

CONTENTS

January - March 2011

, CERTIFIED FINANCIAL PLANNER® and are certification marks owned outside the U.S. by Financial Planning Standards Board Ltd. Financial Planning Association of Malaysia is the marks licensing authority for the CFP marks in Malaysia, through agreement with FPSB.

EDITORIAL

PublisherFinancial Planning Association of Malaysia

EditorDennis Tan

Managing Editor Steven K C Poh

AdvisorSteve L H Teoh

Editorial PanelTan Beng Wah

K P Bose DasanKong Kim Heng

Maznita Mokhtar

Administration & AdvertisingV. Murugiah

Consulting Produceri2Media Sdn Bhd (493346-K)

Suite 10-01, 10th Floor, Block A,Damansara Intan,

No.1, Jalan SS20/27,47400 Petaling Jaya,

Selangor Darul Ehsan.

PrinterMr Print Sdn Bhd (577080-H)

Lot 21, Jalan 4/32A, Off Batu 6 1/2,Mukim Batu, Jalan Kepong,

52100 Kuala Lumpur.

The 4E Journal is published quarterly by the Financial Planning Association of Malaysia. Opinions and views expressed in the 4E Journal are solely the writers’ and do not necessarily reflect those of the Financial Planning Association of Malaysia. The publisher accepts no responsibility for unsolicited manuscripts, illustrations or photographs. All manuscripts and enquiries should be addressed to:

The Editor, 4E Journal, c/o Financial Planning Association of Malaysia, Unit 1109, Block A,Pusat Dagangan Phileo Damansara II,No.15, Jln 16/11, Off Jalan Damansara,46350 Petaling Jaya, Selangor. Phone: +60-3-7954 9500 Fax: +60-3-7954 9400

Editorial Board

www.fpam.org.my

Planning to Live LifeDear Members,

The Financial Planning Association of Malaysia (FPAM) would be having its 11th annual general meeting (AGM) this year at the Bukit Kiara Equestrian & Country Resort on May 21. In addition to the routine matters, there would also be an election of the Board of Governors for the coming term.

By now you would have all received the notice of the AGM as well as the letter inviting nominations for the various positions on the Board of Governors. I hope all of you would make it a point to attend the AGM, and in the process vote for your preferred candidate to the Board.

On that same day, we would also be organising a graduation ceremony for all the members who have obtained their ‘Certified’ status in 2010. This is scheduled to take place before the AGM so that the newly Certified members can attend both events. Our congratulations to all the graduating Certified members for having successfully complete the rigorous exams and meeting all the necessary requirements on ethics and experience as well.

Our cover story features Senator Datuk Seri Idris Jala, Minister in the Prime Minister’s Department and CEO of Performance Management and Delivery Unit (PEMANDU). As the man entrusted with ensuring that the government’s socio-economic transformation programmes (both the Government Transformation Programme and the Economic Transformation Programme) achieve the desired results, his views and insights are particularly pertinent especially as they relate to the financial services sector of which we are all part of. Check out the discourse … you won’t want to miss it!

To facilitate forward planning, members would be pleased to know that the 2011 continuing education (CE) course calendar has been finalised till year end. We would be adding on new programmes as we go along, and the details would be published quarterly in the 4E Journal and our website.

I am also proud to announce a new addition to the FPAM family – First Sovereign Advisory Sdn Bhd – who joined us recently as a Corporate member. We welcome FSA on board and hope it will lead to a long and mutually beneficial relationship.

I am also pleased to once again welcome U Chen Hock to the Board of Governors and Ong Eu Jin to the Board of Certification and Standards.

In the first quarter of the year, the world has witnessed some dramatic developments. The upheaval in the Middle East and the natural disasters in Australia, China, New Zealand and Italy and lately, of epic proportion, in Japan will no doubt have an economic impact that will have a bearing on us as financial planners to our clients. There is much to do, planning-wise, for our clients, especially when there is so much volatility and uncertainty.

On a personal level, I would like to extend our deepest sympathies (on behalf of FPAM) to those who have been tragically affected by these disasters. FPAM, as part of the Financial Planning Standards Board (FPSB) fraternity is linked to a worldwide network of national affiliates including a number of whom are in the affected countries. Our heartfelt sympathies are with them and we wish them a speedy recovery.

Life’s so frail, live it now!

Wong Boon Choy, [email protected]

TM

The 4E Journal 5

Science, Behaviour,Art and ‘Nudges’By Jonathan Guyton, CFP®

Lately, I’ve found myself thinking about the powerful opportunities we have as financial planners for

our specific advice — and the manner in which we deliver it — to have a significant behavioural influence on the quality of our clients’ lives.

Going beyond the left-brain analytics of traditional financial planning to facilitate such an outcome is no easy task. To do so requires us to meet clients at the place of their past experiences, viewpoints, values, and, yes, biases. To expect them to see things as we do is to create a gap between us into which even the best financial planning science can fall, unimplemented.

Among other things, this means we must be in tune with the key aspects of our client’s history and relationship with money. We must advocate for those future scenarios that will most honour their values and are least likely to trigger the fears and self-sabotaging behaviours that can violate them. Both style and substance matter.

Clients’ past experiences create the “stories” they tell themselves that in turn become the prisms through which present events are framed — often in highly unhealthy ways. And the rigidity of this framing can lead to more stories about the future that can have the potential to violate their most precious values, a sure recipe for an unhealthy situation at many levels.

Fortunately, occasional moments present themselves in nearly every advisory relationship when this all comes together and breakthroughs can occur … if we are alert and have the skills to see such

moments for what they are. In the words of Thaler and Sunstein1, such moments are ripe for a “nudge.”

Scarcity

One of the most harmful of these “stories” involves the notion of scarcity. This can take many forms, but it frequently shows up as a (perceived) scarcity of financial resources or as a scarcity of time. A fear that there won’t be enough.

This most often occurs as a fear that life will either end too late or too soon. The former is a fear of outliving one’s money; the latter is a fear that the ability to live a worthwhile life will be cut short. And, as most of us know, the presence of both fears in a couple can be an insidious combination because each spouse feels justified in his or her fears and it sets up the poisonous proposition that one spouse’s concerns can only be addressed at the

expense of the other’s. Of course, this is all in their framing, but this framing is their reality. Unless some movement can be sparked and their framing expanded, here they are likely to remain.

Stuck.

Just like Cass and Becky are. Our sample couple’s lives have transitioned to include more flexibility to travel and be with their grandchildren living around the country now that Cass has wound down his consulting business. Despite this new freedom, Becky is worried. “My grandmother had to sell her house after my grandfather died when her pension and Social Security got cut in half,” she said. “And my parents didn’t save enough; they’re well on their way to foolishly spending through their principal. I don’t want that to be us.”

Things look different to Cass. “My side of the family usually sees a significant health decline by their early 70s. If we don’t live for today while we can, opportunities will pass us by.” Is it any wonder that Becky’s

INDUSTRYJanuary - March 2011

1 Thaler, Richard H. and Cass R. Sunstein. 2008. Nudge: Improving Decisions About Health, Wealth, and Happiness. New Haven: Yale University Press. The authors also have a blog at http://nudges.org.

6 The 4E Journal

family financial history colours her sense of long-term financial security and links it to “prudent” spending decisions in retirement, while Cass keeps wanting to tap their nest egg for extra distributions

“while we still can”? Scarcity fears seem firmly entrenched.

What is our role as planners when we encounter views of life thus framed by scarcity? First of all, both spouses are right: Becky’s conviction that spending policies play a significant role in the long-term level of financial security is supported by financial planning theory, and Cass’s sense that the failure to pursue dreams is a sure formula for regret resonates as well. The fears at the foundation of these views fester and spill over into their relationship and quality of life. As planners, we might soon see ourselves as either an arbitrator in a dispute or the bad cop in a zero-sum game. Unless we can change the rules.

Appreciative Inquiry

Clearly both Becky and Cass deserve to be honoured for their experiences and the life-views they have created, even if they cannot (yet) do so for each other. And this must happen before any alternative re-framing or solutions are offered. I might say to them, “You are both right. I completely understand why you feel the way you do. How could you not based on what you know? Cass fears the regret from not enough quality of life, and Becky fears the stress and consequences from too much quantity of life. That’s a tough one, and it happens with couples more often than you’d think.

If only one of you had paid me off before the meeting, I could now take your side and tell your beloved they are wrong.” (Believe it or not, sometimes the humour of the absurd can illuminate the “stuck” tension just enough to create an opening for clients to break free from their self-sabotaging storytelling.)

However, far more important than anything we can say, couples need to talk to each other. Appreciative inquiry can be a powerful approach in such

circumstances. We can ask them to reflect on their own life experiences to find an appreciation for the other’s framing. Perhaps Becky has felt the pang of regret over a missed opportunity. Maybe Cass has felt the gut-wrenching of having to choose between various necessities of life. If so, or at least if they can empathise with each other, the opportunity to honour their respective life-views via a reframed planning strategy now has the potential to also reach more deeply into their lives.

Core and Discretionary Portfolios

In this situation, we often rebrand clients’ overall investment portfolio into two distinct components, “core” and “discretionary” (or, as one of our clients delights in calling it, slush). Each component has its own purpose, policies, and underlying portfolio allocation. One of our retired clients has called this approach, “The best advice you’ve given us in our 10 years of working together.”

Along with any pension, Social Security, or other on-going reliable income, the core portfolio’s purpose is to fund on-going living expenses, including travel and entertainment, for the rest of the clients’ lives in an inflation-adjusted manner that is safe and sustainable. It has its own underlying withdrawal policies, ideally laid out in a withdrawal policy statement such as I wrote about in this Journal last June and spoke about at FPA’s annual conference last fall.

These withdrawal/spending policies need to be specific and disciplined; past research has shown that such disciplined withdrawal policies are the ones with the bullet-proof probabilities of success. Taking additional distributions outside

these policies can quickly put chinks in the armour of financial security and diminish a retirement plan’s security. Typically, the core portfolio consists of 85 percent to 95 percent of total investment assets, obviously depending on the after-tax cash flow it needs to fund. In a nutshell, this addresses Becky’s concerns.

The discretionary portfolio’s purpose supports Cass’s viewpoint. These funds are to be used both spontaneously and by design for expenditures beyond core needs for which the clients deem it worthwhile to tap these assets. That is the key: for which they deem it worthwhile. Moreover, it shifts the question, “Is it okay to take this extra one-time withdrawal?” from the planner (who can’t know because details about future “one-time” withdrawals are unknowable) to the client (who is empowered to make this choice based on priorities, timing, and values).

Now, with their core lifestyle securely funded by other resources, a freeing conversation can ensue as to how these resources might be deployed to enhance their quality of life. Dreams, values, and bucket lists can drive decisions rather than fear, guilt, or manipulation. Policies and plans for these assets can emerge. We are free to watch what clients do and to support their emerging choices without worry about what they might do next. The rules of the game have changed!

“However, far more important than anything we can say, couples need

to talk to each other. Appreciative inquiry can

be a powerful approach in such circumstances. “

“Past research has shown that disciplined withdrawal policies are the ones with the bullet-proof probabilities of success. “

Couples need to talk to each other.

The 4E Journal 7

Strategically, the discretionary portfolio is ideally funded at least in part with non-qualified or Roth IRA assets, though this is not essential. It is important for clients to know that this fund should only be replenished with unused withdrawals from the core portfolio or unanticipated inflows of capital such as an inheritance. Asset allocation should be determined through conversations, with higher anticipated withdrawals in the next three to five years prescribing a higher portion of fixed-income holdings.

support needed to foster healthy family relationships. His father had not done so, and that experience left its mark.

For her part, it mattered deeply to Lauren that Kerry would be able to retire at an age that would still allow them to pursue their bucket-list items, including extended periods of travel. Accelerating payments to eliminate the mortgage in 10 years was congruent with their values. And their planning was in good shape to sustain their future mortgage-free lifestyle from that point on.

plans to pay for it. Kerry stated that if he felt confident in their plan to pay the mortgage, he could see himself retiring before it was paid off.

With their values affirmed and now reframed in light of their circumstances, we proposed a seemingly unconventional strategy: lock in a modest on-going cash flow requirement by refinancing the remaining US$155,000 balance to a 30-year mortgage and continue to make aggressive pre-payments as their incomes allowed. Their slightly lower interest rate paled in comparison to the pressure relieved by the nearly US$1,100 reduction in their required payment. Kerry came to see that this US$785 obligation would not over-burden their retirement years, and Lauren liked the potential for reduced financial stress and the honouring of their original retirement time frame.

From a left-brain perspective, this is not rocket science, and it is a fair question why they didn’t refinance with a 15-year loan. The key, though, was the conversations in the six months between our initially addressing this situation and when Kerry embraced the new strategy. In fact, it was Kerry’s momentary hesitation at the US$350 higher 15-year payment that tipped the scale in terms of which approach would most honour their values and accomplish their goals.

“Asset allocation should be determined through

conversations, with higher anticipated withdrawals in the next three to five years

prescribing a higher portion of fixed-income holdings. “

“It is often in the slight pause or the furrowed brow or the sigh of acknowledgement when the art and science of our craft come together. “

One of Kerry’s primary values was to provide a mortgage-free home for himself and his beloved when

they retired.

Back in 2005, making the US$2,700 monthly payment necessary to accomplish this looked quite feasible. For the next few years, they stayed true to their plan. Then Lauren changed jobs to a more-satisfying but lower-paying position and Kerry’s income declined in the depressed housing market in which he worked. Cash flow was tight, and by early 2008 they could no longer make the extra mortgage payments; they needed both incomes to afford the US$1,850 required payment of the 15-year loan that was now unlikely to be paid off until 2019 when Kerry would be 75. Life stress rose sharply as their new financial reality frayed the fabric of their core values.

Our response was to initiate a conversation with Kerry and Lauren about what really mattered to them in this unanticipated situation. Lauren shared that Kerry’s increased stress was worrying her and that her paramount concern was for the quality of their life together. Both agreed that they wanted to continue living in their house, even if it meant revising their

This solution hinges on turning an “either/or” scarcity-based confrontation into a collaborative “both/and” approach. Surely, the core/discretionary bifurcation could have been presented without the preceding dialogue I described, but then it might have only minimised the tension rather than shifted the dynamic to a new plane.

A Values Focus

Sometimes, however, a series of events produces material and behavioural changes in circumstances that can put a key aspect of even the most conscientiously designed plan at risk. Even in times like these, with skill, grace, and good fortune, that moment of transformation may also appear.

Take the case of Kerry and Lauren. Though 11 years apart in age, Kerry and Lauren met as single parents while regularly attending their sons’ athletic events. They fell in love, began creating a wonderful life together, eventually married, and bought a new home, financed with a 30-year mortgage. In 2005, with interest rates having fallen, they refinanced to a 15-year loan. At that time, they were 61 and 50.

One of Kerry’s primary values was to provide a mortgage-free home for himself and his beloved when they retired in about nine years. I knew how important this was to him from prior conversations that revealed how closely he linked such financial responsibilities with the care and

For me, this was a key reminder. It is often in the slight pause or the furrowed brow or the sigh of acknowledgement when the art and science of our craft come together to make the whole so much greater than the sum of its parts.

Cue the “nudge.”

The author is principal of Cornerstone Wealth Advisers Inc., a holistic financial planning and wealth management firm in Edina, Minnesota. He is a researcher, mentor, author, and frequent national speaker on retirement planning and asset distribution strategies, and a former winner of the Journal of Financial Planning’s Call for Papers competition. Reprinted with permission from the February 2011 issue of the Journal of Financial Planning.

The Way Banking Should Be

The Way Banking Should Be

Certified to ISO 9001:2000Cert. No. : AR 1350

SIRIM

Certified to ISO 9001:2000Cert. No. : AR 1350

SIRIM

Certified to ISO 9001:2008Cert. No. : AR 1350

Certified to ISO 9001:2008Cert. No. : AR 1350

FPAM launch ad @ 4E journal_FA(o).indd 1 11/12/10 4:11 PM

The 4E Journal 9

Competent Financial Planners:The Way Towards Professional Acceptance

We live in exciting times but it is getting every bit challenging. And the profession of financial

planning is trying to fit in – into various scenarios in the financial services environment. Financial services have always been there but the traditional approaches are changing by the minute. The problem arises when individuals and institutions try to hold on to their old ways and turfs and try very hard to thwart the progress of new ideas and processes. It will be difficult to present an organised, methodical, and empirical analysis of the situation especially since it is a very demanding task and secondly I must confess, I do not possess the intellectual might to present such a comprehensive analysis.

Management gurus will try to find a chart or diagram like a triangle or circle

to present their approach and say this is the situation and this is the way out. I have no such tool, but financial planners can always start with the client.

And speaking of clients, what does the client actually want?

He perhaps wants to know, “are you the right person to talk to about his personal finances.” Let us say we successfully crossed that hurdle and the professional CFP certification had helped. He was curious as to whether there was a license involved to practise financial planning. Bang! We are thrown into some murky waters. The Securities Commission has through its 2007 Capital Markets Services Act made financial planning a regulated, licensed activity. Thus I had to show my client my CMS Representative License from the Securities Commission. As a CMSRL representative, I had to also let him know my principal company through which I am licensed.

He was duly assured that I was not just another agent selling insurance or unit trusts. The client was happy there was a differentiation. He now has the hope and expectation that I can deliver a deeper and more meaningful or perhaps comprehensive solutions to assist him in his personal financial matters. I had to quickly ask him if he was just looking

to buy insurance or unit trusts. He said perhaps, but he wants his situation analysed first and wants to know what is appropriate for him. This is the first match between the financial planner and the client.

Clients are generally aware that they need insurance or that they need to put some money into a good performing unit trust. But they may not be looking for a comprehensive financial planner. But this client wanted his financial position analysed first and also wanted to know what would be the most appropriate products for him to achieve some of his personal financial goals. He was also hoping that I could advise him on better ways to manage his personal finance and to find ways to improve his cash flow. He also slipped in the question if I was an independent financial planner with a wide array of financial products to choose from.

I gasped as to how to answer him. Yes, as an independent financial planning firm, my company has a variety of products from various vendors and manufacturers to choose from. It even has some prominent market players in insurance and investments, but not all of them are represented. But I assured him that we had a fairly wide range of products to choose from. My honesty appealed to him.

INDUSTRYJanuary - March 2011

By K P Bose Dasan, CFP®

“The problem arises when individuals and

institutions try to hold on to their old ways and

turfs and try very hard to thwart the progress of new ideas and processes.”

The Way Banking Should Be

The Way Banking Should Be

Certified to ISO 9001:2000Cert. No. : AR 1350

SIRIM

Certified to ISO 9001:2000Cert. No. : AR 1350

SIRIM

Certified to ISO 9001:2008Cert. No. : AR 1350

Certified to ISO 9001:2008Cert. No. : AR 1350

FPAM launch ad @ 4E journal_FA(o).indd 1 11/12/10 4:11 PM

10 The 4E Journal

But here’s an issue that has been around since financial planning came to Malaysian shores: are agents correctly distinguished from licensed financial planners? All insurance and unit trust agents sit for an exam to pre-qualify them to handle insurance or investment products. That is the depth of their academic requirement, but it must be said in all honesty that the financial institutions have good training programmes and have a system of nurturing agents through their multi-level agency supervision.

Some institutions equip their agents with materials and software to help them present their products in the best light to their clients. Therefore, tens of thousands of agents are out there handling the proprietary products of these financial institutions. They interest their clients in a variety of ways, but principally they appeal to their clients’ need to insure or invest for some general goal or objective. So the question now is: how different is this approach to that of a financial planner? To make matters even more serious, there are only a few hundred licensed financial planners in the marketplace when compared with the tens of thousands of agents out there.

In this context, it would be good to look at the definition under the CMSA 2007 with regard to financial planning. As per CMSA 2007, Schedule 2, Part 2: “financial planning” means analysing the financial circumstances of another person and providing a plan to meet that other person’s financial needs and objectives, including any investment plan in securities, whether or not a fee is charged in relation thereto.”

This definition implies that to analyse the financial circumstances of another person and to come up with a plan you need an SC license. It does not matter if you charge a fee or not. Therefore a clear distinction between a financial planner and an agent is that the financial planner makes it a point to analyse the financial circumstances of a client and propose a plan, written or otherwise, to help client achieve his financial need or objective.

An agent can be assumed to be only interested in representing his company’s product and perhaps go straight into the product presentation without analysing his client’s financial circumstances. It can be assumed that the product meets a general need like risk or investment and there is no attempt to provide a plan.

This is where it hits a snag. Good agents who want to do a good job want to analyse the client’s financial circumstances before offering an investment plan albeit with their company’s proprietary products. Are these agents then in the CMSA territory? Such is the confusion in the marketplace. It is perhaps good that the Securities Commission has not hauled up anybody for violating the CMSA provisions, which I believe it can if it wants to truly enforce this definition. The penalty for violating this provision is RM5 million or five years in prison or both.

That being the case, you can now understand my humble apology that I do not have the intellectual might to decipher what ails in our current legal situation and what can be done to simplify things. To make matters more interesting, there are many agents who have the globally

recognised professional certification – CFP – and who are still tied to a particular company. Then there are those who are qualified CFPs who are just keen to promote products without analysing the financial circumstances of the client and coming out with a written plan. There are also many CFP qualified relationship managers who work for banks and provide private banking services under the auspices of the bank and perhaps outside the ambit of the CMSA. In other words, there are many things that need to be ironed out before we can actually see a clear passage for financial planners.

To add a spanner to the works the insurance fraternity has coined the professional term “financial adviser” as their own and now you need a license to call yourself a financial adviser.

“Financial advisory business” in the insurance industry means any or all of the following services:

• analysing the financial planning needs of a person relating to insurance products

• recommending the appropriate insurance products

• sourcing insurance products from a licensed insurer

• arranging of contracts in respect of insurance products

• other financial services as prescribed by the Central Bank.

• You can now imagine the plight of a financial planning practitioner. To handle multiple insurance products, you need this financial adviser’s license. Fortunately both regulatory agencies have made things easier by coordinating the requirements for both licenses. However, the fact remains that you need two licenses and compliance with two regulatory agencies to practice financial planning. To me, this is a magnificent example of “Malaysia Boleh.”

A social economist might be interested to find out what is going on in the Malaysian financial services environment given

“The client only wants a good job done for him, effectively see his debt paid off or watch his money grow. He needs to be impressed by what the planner can do for him.”

The 4E Journal 11

personal financial objectives. He wants the financial planner to monitor the performance of his strategies and see that he is on track to achieving his goals.

Therefore there is a public face to all the things being discussed here. The public does not want to be confused. They can, with some certainty, identify a doctor or a lawyer but he needs to be sure about his financial planner or adviser who is going to handle his personal finance and add value to his wealth. Perhaps it is worth noting that doctors and lawyers go through a period of post qualification training called internship or chambering. The financial planning profession does not have this structure. The time has come, perhaps to thrash out the bigger picture and take the industry firmly forward towards 2020 to meet the government’s economic transformation initiative and achieve high-income and developed country status.

While the laws are being straightened out, the licensed financial planners can start the ball rolling by improving their competency level. By achieving higher competency, they can win the client’s trust and patronage. Their efficacy and efficiency will spiral a word of mouth promotional blitz and in the future it can be assumed that most affluent clients will only want to talk to qualified and licensed financial planners.

In this regard, I urge all planners and advisers to read the document prepared

this dichotomy between insurance and investment, and the attempt to license the less than a thousand financial planners but to allow the freedom to the tens of thousands of agents to ply their trade.

What is the big picture and what is the goal of the regulators? I suppose financial institutions do wield some clout. We may have to let things evolve or decay as no one has a clue as to where the law and practice of financial planning is going and what the final outcome is going to be.

The new initiatives by the Economic Planning Unit (EPU) under the leadership of the Prime Minister have drawn plans to build wealth management as one of the key areas for the new Economic Transformation Programme (ETP). Who will promote wealth management and its human capital development? We can’t even come to terms with whether a wealth manager is free of any restriction from being licensed as a financial planner or financial adviser. Do wealth managers need a license?

Of course, the client is not interested in the trail of discussion that I have taken the reader through. He only wants a good job done for him, effectively see his debt paid off or watch his money grow. He needs to be impressed by what the planner can do for him. He wants the assurance that all or any product recommended will do its stated job and help him achieve his

“The new initiatives by the Economic Planning Unit (EPU) under the leadership of the Prime Minister have drawn plans to build wealth management as one of the key areas for the new Economic Transformation Programme (ETP).”

by the Financial Planning Standards Board (FPSB) with regard to the accepted competency levels and the practical knowledge and skill sets expected of a CFP professional. Passing the exams is only one of the four pillars. Experience, ethics and continuing education are important prerequisites to remain relevant to the financial planning industry. Let us rise to the challenge of bringing economic transformation through expert wealth management by CFP professionals.

The author is a tax consultant and a certified financial planner licensed as an investment adviser (financial planning) representative with Standard Financial Planner Sdn Bhd.

12 The 4E Journal

PlanPlus for Students is used by University Financial Planning programs around the world. In Malaysia, KMDC, the Malaysian market leader in CFP® education has adopted the software for use in its CFP program.

Transition your business from a product to advice based model with award winning training like the Advice Transition Program

PlanPlus Planit Community Edition provides free Goal Based planning

for advisors worldwide.

PlanPlus is a supporter of www.planipedia.org

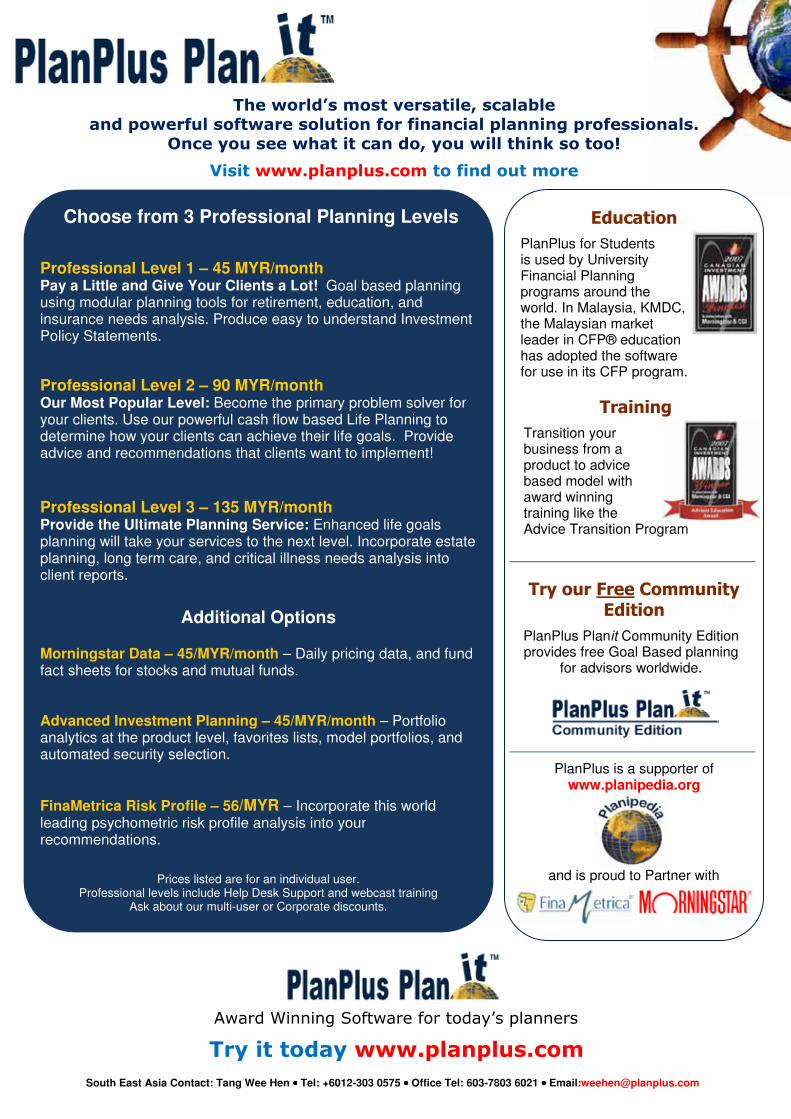

Choose from 3 Professional Planning Levels

Professional Level 1 – 45 MYR/month Pay a Little and Give Your Clients a Lot! Goal based planning using modular planning tools for retirement, education, and insurance needs analysis. Produce easy to understand Investment Policy Statements.

Professional Level 2 – 90 MYR/month Our Most Popular Level: Become the primary problem solver for your clients. Use our powerful cash flow based Life Planning to determine how your clients can achieve their life goals. Provide advice and recommendations that clients want to implement!

Professional Level 3 – 135 MYR/month Provide the Ultimate Planning Service: Enhanced life goals planning will take your services to the next level. Incorporate estate planning, long term care, and critical illness needs analysis into client reports.

Additional Options Morningstar Data – 45/MYR/month – Daily pricing data, and fund fact sheets for stocks and mutual funds. Advanced Investment Planning – 45/MYR/month – Portfolio analytics at the product level, favorites lists, model portfolios, and automated security selection.

FinaMetrica Risk Profile – 56/MYR – Incorporate this world leading psychometric risk profile analysis into your recommendations.

Prices listed are for an individual user. Professional levels include Help Desk Support and webcast training

Ask about our multi-user or Corporate discounts.

South East Asia Contact: Tang Wee Hen •••• Tel: +6012-303 0575 •••• Office Tel: 603-7803 6021 •••• Email:[email protected]

and is proud to Partner with

The 4E Journal 13

ISLAMIC FINANCE

January - March 2011

Realising Maqasid Al-Shariah in Islamic Financial Planning

Maqasid Al-Shariah is the guiding principle of determining any Islamic law that is widely used

in areas revolving around the Muslim way of life. And the objective of Shariah is to ultimately achieve maslahah and to uphold the interest of the public at large in this world and the hereafter. It deals with the prioritisation in Islam to safeguard the purity of the religion, mental, life, property and offspring of mankind.

In facing or solving current issues either directly or indirectly touching the social, economic, political and financial spheres, the application of Maqasid Al-Shariah is an important element that needs to be incorporated by all Muslims in their lives.

This article attempts to define the Maqasid Al-Shariah and examine the ways of realising the noble objectives of Shariah in all aspects of Islamic wealth planning – wealth creation, wealth generation, wealth purification, wealth protection and wealth distribution. It also looks at the implementation of these scopes of work in Malaysia. This exercise is not to determine what is halal or haram, but to ultimately achieve al-falah – to be successful in this life and the hereafter.

The Objectives of Maqasid Al-Shariah

The concept of compassion and guidance are part of Shariah’s objectives which are declared in the Quran, “We have not sent you but a mercy to the world”- (21:107) and “A healing to the (spiritual) ailment

of the hearts, guidance and mercy for the believers (and mankind)” – (10:57). It seeks to establish justice, eliminate prejudice and alleviate hardship. It promotes cooperation and mutual support within the family and society at large. This ensures the preservation of public interest (maslahah) as the objective of the Shariah which Islamic scholars have considered for all intents and purposes synonymous with compassion. Shariah identifies three areas, which constitute the component part of Rahman, namely promoting maslahah to the people, educating individuals1 and establishing justice.

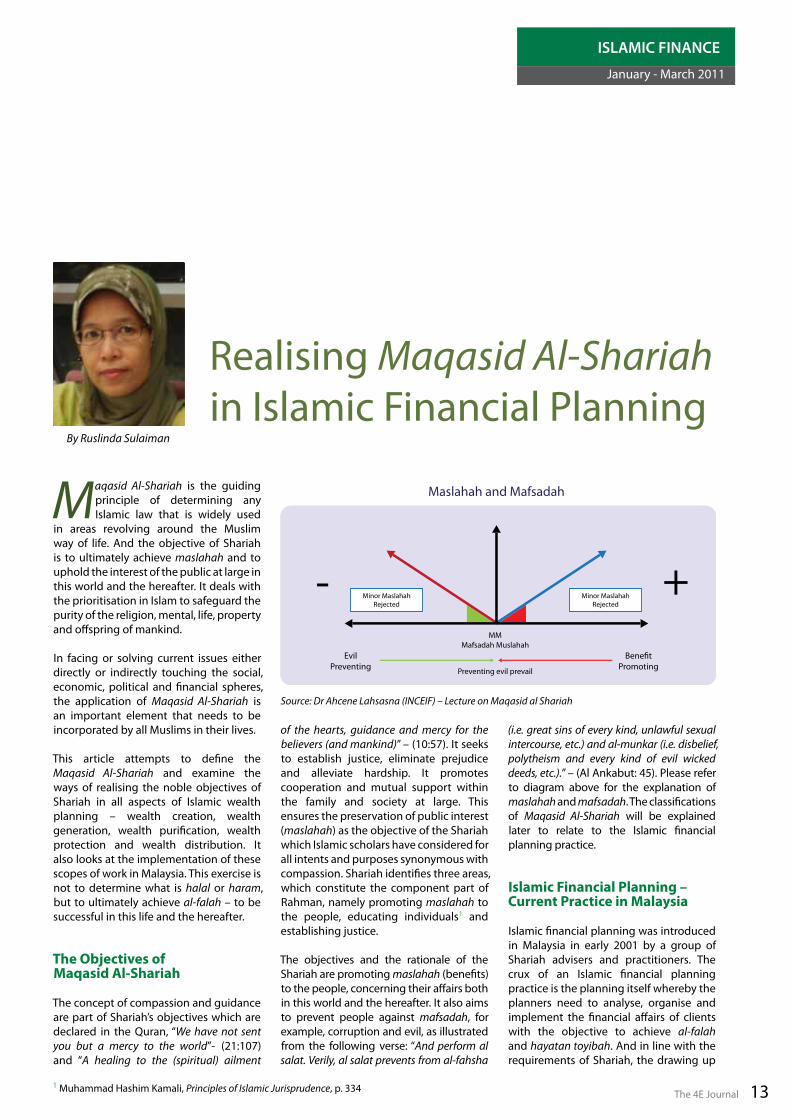

The objectives and the rationale of the Shariah are promoting maslahah (benefits) to the people, concerning their affairs both in this world and the hereafter. It also aims to prevent people against mafsadah, for example, corruption and evil, as illustrated from the following verse: “And perform al salat. Verily, al salat prevents from al-fahsha

(i.e. great sins of every kind, unlawful sexual intercourse, etc.) and al-munkar (i.e. disbelief, polytheism and every kind of evil wicked deeds, etc.).” – (Al Ankabut: 45). Please refer to diagram above for the explanation of maslahah and mafsadah. The classifications of Maqasid Al-Shariah will be explained later to relate to the Islamic financial planning practice.

Islamic Financial Planning – Current Practice in Malaysia

Islamic financial planning was introduced in Malaysia in early 2001 by a group of Shariah advisers and practitioners. The crux of an Islamic financial planning practice is the planning itself whereby the planners need to analyse, organise and implement the financial affairs of clients with the objective to achieve al-falah and hayatan toyibah. And in line with the requirements of Shariah, the drawing up

1 Muhammad Hashim Kamali, Principles of Islamic Jurisprudence, p. 334

Minor MaslahahRejected

Minor MaslahahRejected

EvilPreventing

MMMafsadah Muslahah

Preventing evil prevail

Bene�tPromoting

Maslahah and Mafsadah

Source: Dr Ahcene Lahsasna (INCEIF) – Lecture on Maqasid al Shariah

By Ruslinda Sulaiman

14 The 4E Journal

of the financial plan should be embedded with Islamic values and principles.

Planning for one’s life, whether for material gains or spiritual, is considered as an ibadah in Islam. In the story of Yusof, the Quran relates a 15-year economic plan that was put into action to thwart a disaster, “Ye shall sow seven years as usual, but that which ye reap, leave it in the ear, all save a little which ye eat. Then after that will come seven hard years which will devour all that ye have prepared for them, save a little of that which ye have stored. Then, after that, will come a year when the people will have plenteous crops and when they will press (wine and oil).”

It was the planning and storage of wheat and the keeping of fine seeds and good stalks of wheat that kept the country going during the seven-year drought leading to the abundant harvest in the fifteenth year. The keeping of good ‘stalks’ of wheat can be likened to the keeping of good ‘stocks’ with strong fundamentals. The ‘value’ seeds and stalks were preserved in the first and second seven-year cycle and re-invested to generate the abundant returns in the fifteenth year. This ayat shows that we need to work in order to earn, to spend wisely what has been earned and finally to save some for future.

Planning is a continuous and life-long process and not an ad hoc affair. Muslims are encouraged to plan for their life and achieve their goals by their own efforts. The final stage is tawakal (accept the result as destiny bestowed by Allah).

In Islam, financial planning is not merely a process of acquisition and accumulation of wealth. It has a broader definition and is related to the concept of vicegerency (khalifah). Allah has given His bounties to all mankind, and as a trustee, man has to administer this trust properly. Earning and spending should be in compliance with His covenants. Allah affirms: “For Allah is He Who Gives (all) sustenance …” (Al-Dhariyat 51:58).

The concept of Allah’s bounty is considered very important in Islam as a good Muslim is required to have a proper balance between the fulfillment of his spiritual and worldly obligations.

As the Prophet put it: “A Muslim should prepare himself for the next world as if he is going to die tomorrow, but at the same time work hard to improve all his worldly comforts as if he is going to live forever.” (Narrated by Al-Dailami)

The financial planning dimension in Islam covers five areas. They are: wealth creation, wealth generation, wealth purification, wealth protection and wealth distribution.

Wealth Creation

Wealth in Islam is rizq that connotes subsistence or means of living. This means of living is not necessarily an outcome of man’s effort. It is an endowment from Allah because He is the one who sustains mankind’s life. The effort of mankind is considered as a process, which will consequently lead to either positive or negative results. Everything on earth has been created for mankind. In the Quran, we are told time and again, that God is the real owner.

“… and God has made for you in your homes and abode and has made for you tents out of the hides of cattle for dwelling which you find so light and handy when you travel and when you stay; and of their wool, fur and hair furnishings and articles of convenience and comfort.”

The above verses show us that the creation of wealth is not due to our effort but that God is the one that has made it possible. Upon the availability of resources available, Muslims are encouraged to earn their living through halal income and with this income, they should be able to provide not only the basic necessities of their life but also things that would make their life in this world more comfortable.

Wealth Generation

In conventional financial planning, the word “accumulation” is widely used

to describe the creation of additional wealth. In Islam, the word accumulation is replaced with the word “generation” as it is more akin to the Islamic concept that implies that wealth is already there and its utilisation would bring more wealth.

The Quran says, “They who accumulate gold and silver and spend it not in the way of God, unto them give tidings of a painful doom. On the day when it will (all) be heated in the fire of hell, and their foreheads and their flanks and their backs will be branded therewith (and it will be said unto them): Here is that which ye accumulated for yourselves. Now taste of what ye used to accumulate.”

Wealth generation is very much encouraged by Islam. Among others, the Quran says, “Give not unto the foolish (what is in) your (keeping of their) wealth, which Allah hath given you to maintain; but feed and clothe them from it, and speak kindly unto them.”

This verse was revealed to remind those who are the guardians of orphans to manage the assets of their wards properly and efficiently.

Wealth should be lawfully generated and lawfully spent. In the hadith, the Prophet mentioned the use of wealth before poverty. The use of wealth before poverty means to use one’s wealth to generate enough income (through investments) to face uncertain and hard times ahead.

Wealth, in Islam, must not be kept idle, but should be invested. The hoarding of money is not allowed in Islam. For example, if gold is kept idle, one must pay zakat on the idle gold. In the hadith, the Prophet said, “Whoever develops an idle land, it belongs to him.” (Sahih Bukhari). Islam has laid down clear injunctions on how Muslims should generate their wealth through Shariah-compliant products where riba, maisir and gharar are to be avoided at all times.

Wealth Purification

Wealth needs to be purified for two reasons:

• to cleanse it from illegal income one may have unknowingly earned

• to give part of one’s wealth to others (8 asnafs)

In Islamic terms this is called zakat or compulsory alms. The Quran says, “Take alms of their wealth, wherewith thou

WealthCreation

WealthGeneration

WealthPuri�cation

WealthProtection

WealthDistribution

“Planning is a continuous and life-long process

and not an ad hoc affair. Muslims are encouraged to plan for their life and

achieve their goals by their own efforts.”

The 4E Journal 15

mayst purify them and mayst make them grow, and pray for them. Lo! thy prayer is an assuagement for them. Allah is Nearer, Knower.”

Wealth purification is very important in the overall financial planning process as the Prophet had said, “Whoever is made wealthy by Allah and does not pay the Zakat of his wealth, then on the Day of Resurrection his wealth will be made like a bald-headed poisonous male snake with two black spots over the eyes. The snake will encircle his neck and bite his cheeks and say,

‘I am your wealth, I am your treasure.’”

The payment of zakat is the third pillar of Islam and it is considered an obligatory charity for the Muslim. It is often said the return given by Allah SWT (SWT is from Arabic meaning subhanahu wa ta’ala which translates as ‘glorified and exalted’) for giving zakat is huge indeed, a 70,000 percent return on one’s investment.

In this respect, the Quran has this to say, “The likeness of those who spend their wealth

in the way of God, is as the likeness of a grain of corn; it grows seven ears, and each ear has a hundred grains. God gives manifold increase to whom He wills.”

Zakat helps the poor and the needy to live and it is useful for the development of the economy. The sharing of wealth with others will create harmony, love and unity in the Muslim society.

Wealth Protection

In conventional practice, wealth protection relates to mitigating risk through insurance, whilst in the Islamic practice, it is done through takaful participation. Takaful is a way to reduce the financial risk of loss due to accident and misfortunes. Takaful literally means mutual guarantee and solidarity – participants cooperating to guarantee each other against a defined loss. Risk, in this case is shared, not transferred.

Managing risk is encouraged in Islam especially in trying to reduce risk against loss and calamities, as illustrated in a hadith related by Tirmidhi: One day the Prophet Muhammad SAW noticed a Bedouin leaving his camel without tying the animal. He asked the Bedouin,

“Why don’t you tie down your camel?” The Bedouin answered, “I put my trust in Allah SWT.” The Prophet SAW (Sal Allaahu Alayhi wa Sallam) then said to the Bedouin, “Tie your camel first, then put your trust in Allah.” Tying the camel is an act to reduce the risk of the camel running away. The urging of the Prophet for the Bedouin to tie

down the camel clearly demonstrates the Islamic position on risk management.

Wealth Distribution

Wealth distribution deals with what a Muslim leaves behind upon death and how he should plan his estate according to Shariah. Proper planning will help a Muslim to distribute his wealth according to his wishes. One-third of his estate can be distributed according to his wishes while the other two-thirds would have to be distributed according to hukum faraid. Wealth distribution in Islam has its own rules that must be followed. The law is obligatory to be followed, especially by the heirs of the deceased Muslim.

The salient features of the Islamic law of distribution are2:

• A son’s share is equal to that of two daughters.

• The following Quranic heirs are entitled to the following shares.

It was mentioned in the hadith that it is not right for a Muslim who has properties to bequest that he should pass two nights

without having his will written down. Having a will is highly recommended for Muslims due to the complexity of estate administration laws in Malaysia. The process is very time consuming and this can be burdensome to the dependents

– especially if it involves infants, elderly parents or disabled child. Estate distribution for a Muslim will involve the settlement of all funeral expenses, debts, any claims of matrimonial assets and disposition of one-third of the assets to non-heirs. Only upon completion of these settlements, can the division of the residuary estate in accordance to the faraid principle be done. Proper planning will eliminate hardship and ensure the continuity of the dependants’ livelihood without any disruption.

Application of the Maqasid Al-Shariah in Financial Needs Analysis

One of the most important aspect/process in developing a holistic financial plan is the financial needs analysis (FNA) process. In classifying and prioritising the needs of a Muslim in his financial plan, the concept of Maqasid Al-Shariah must be upheld at all times. These needs should not

2 Azman Ismail, Islamic Financial Planning - Module 5

Quranic Heir

Husband

Wife

Daughter(s)

Mother

Father

Condition

If the wife does not leave childrenIf the wife leaves children

If the husband does not leave childrenIf the husband leaves children

If she is the only childIf there are two or more daughters and no sons

If the parents are the only survivorIf there are spouse and children

If the parents are the only survivorsIf there are spouse and children

Share

1/21/4

1/41/8

1/22/3

1/31/6

1/31/6

“Tie your camel first, then put your trust in Allah.”

16 The 4E Journal

transgress the dictates of Islam. They must adhere to the teachings of the Quran and the Sunnah in order to gain God’s blessing and barakah as mentioned in the Quran

“… and we revealed to thee from the Quran as a form of healing and mercy to mankind in all facets of their lives ….”

All Muslim regard life on earth as temporary and life in the hereafter as everlasting. A good Muslim is, therefore, required to have a proper balance between the fulfillment of his spiritual and worldly needs. Nevertheless, whilst we are here on earth, the need to be able to provide for one’s financial needs is a responsibility for all Muslims, especially so for Muslim men/husbands and fathers. In deciding what is important and what needs to be fulfilled, the level of necessities provided by the Maqasid Al-Shariah has to be observed at all times.

The objectives of Shariah can be divided into three levels of necessities:

The Essentials (Al Daruriyyat)

The most fundamental necessities – vital for the physical and spiritual well-being of an individual and his family – basic needs like food, clothing, shelter and education. Hence, when deciding which financial needs to be realised, these five values need to be considered and to be prioritised accordingly:

The protection of the five values are essential to ensure normal order in society as well as to the physical and spiritual well-being of individuals, so much so that necessary measures are needed to remove all the obstacles that would obstruct the realisation of these values.

• Protection of Religion (Al-Din)A Muslim has to strengthen his faith in Allah by observing different kind of needs in ibadah to increase his iman. For example, the paying of zakat is much more divine than giving sadaqah or the need to perform the haj is more desirable than performing umrah or to go for vacation elsewhere. Also, debt settlement is critical because a debt, if not paid back in full, will result in the debtor’s soul hanging in the hereafter and will not be accepted by God. And all non-Shariah-compliant products (conventional banking/insurance) are to be avoided at all times.

• Protection of Life (Al-Nafs)Diseases and illnesses can directly affect human well-being and in some cases the presence of life itself. They are, therefore, considered threats to life and it is of great importance to a Muslim to take care of his welfare by leading a healthy lifestyle. The need for takaful coverage for dreadful diseases and hospitalisation is indeed desirable so as to receive the best medical care if one has to face a deadly disease.

• Protection of Dignity or Lineage (Al-Ird)When you have found a suitable life partner, it is obligatory for you to proceed with the marriage over the purchase of a house or a car. This is to prevent any immoral activities and to preserve the dignity of the individual. Islam encourages marriage to allow the fulfillment of mankind’s basic need to pro-create. It also helps in curbing social problems that would jeopardise the Muslim society.

• Protection of the Intellect or Mind (Al-Aql)Islam also regards the quest for knowledge as one of the top priorities for all Muslims. If one is to decide between the need to save for retirement or to save for his children’s education, the latter should prevail. Providing a good education to his children is more encouraged because education is the pillar to ensure success and a good life in this world and the hereafter.

The Prophet SAW once said, “Any one who wants this worldly life, he should have knowledge, and any one who wants the life of the hereafter, he should have knowledge, and who wants both this life and next hereafter, he should also have knowledge.” Furthermore when the prophet’s son-

Essentials (Daruriyyat)

Complementary (Hajiyyat)

Embellishment (Tahsiniyyat)

“A good Muslim is, therefore, required to have a proper balance

between the fulfillment of his spiritual and

worldly needs.”

The 4E Journal 17

The Embellishment (Al-Tahsiniyyat)

The embellishment refers to interests which provide improvement in the society

– leading to a better life.

However, without these luxuries, the society will still function and the normal life process will not be interrupted. The examples in this category are: voluntary (sadaqah) and ethical as well as moral rules.

Conclusion

Maqasid Al-Shariah entails the commitment of individuals to achieve hayatan toyibah and al-falah by promoting brotherhood, justice and social welfare.

The concept focuses on fulfilling three levels of necessities – the essentials, complementary and embellishment. They are vital to ensure normal order in society as well as the survival of individuals.

In developing a holistic financial plan for a Muslim, the needs have to be analysed carefully to determine the suitability according to Shariah’s objectives.

Consideration has to be given in terms of preserving the five important values

– religion, life, lineage, intellect and property. Once these needs are met, the benefit to be received is not only during the lifetime but also for the hereafter.

The author is the principal consultant of RH Planners & Services, a personal financial planning services company. She is currently pursuing a PhD in Islamic Finance at the International Centre for Education in Islamic Finance (INCEIF).

in-law, Ali bin Abi Thalib compared the two dimensions of wealth, he said, “knowledge will take care of you while you protect your property.”

• Protection of Property (Al-Mal)Acquiring property is one of the necessities of mankind. It can be done through trade and investment. However, the acquisition has to be legitimate and does not contradict any Islamic laws. In order to ensure that the property is halal, one has to make sure that the transaction activity in generating wealth is in accordance with the Shariah principle. Prohibition of riba has to be observed at all times. Another way to protect the property is by taking a takaful scheme as a protective measure in case of theft or damage to property caused by fire or other calamities. Takaful can create an instant indemnity to the damaged property.

A Muslim can have a variety of needs at different life stages, but focusing on the needs that follow the objectives of Shariah is highly desirable. These needs not only give benefits during this lifetime but will also receive blessings from Allah SWT to live in the hereafter.

Upon completing the essential needs, man can now look at fulfilling his complementary as well as embellishment needs. Muslims are allowed to enjoy the fruits of their labour subject to moderation and compliance to the Shariah principle at all times.

The Complementary (Al-Hajjiyat)

In Islam, removing severity and hardship of individuals and community are considered as the aims of Shariah.

References

1. Al-Shatibi, Abu Ishaq (2003), Al-Muwafaqat fi Usul ash-Shariah, ed. Abdullah Diraz, Cairo: al-Maktabah al-Tawfiqiyyah.

2. Al-Alwani Taha Jabir (2001), Maqasid Al-Sahriah, 1 Ed. Beirut: IIIT and Dar al Hadi.

3. Azman Ismail (2005), Kuala Lumpur, Islamic Financial Planning (Module 1-6).

4. Dasuki, A W & Abozaid, A., A Critical Appraisal on the Challenges of Realising Maqasid Al Shariah in Islamic Banking and Finance, IIUM Journal of Economics and Management.

5. Ibn Ashur (1366 A. H.) Maqasid Al-Sahriah. Tunisia: Maktabat al-Istiqamah.

6. Ibn Ashur, Mohammad Al-Tahir (2006) (a) Ibn Ashur-Treatise on Maqasid Al-Shariah, trans. Mohamed El-Tahir El-Mesawi, Vol. 1, London-Washington: International Institute of Islamic Thought.

7. ___, (b) Maqasid Al-Shariah Al-Islamiyah, Ed. Mohamed El-Tahir El-Mesawi, Kuala Lumpur: Al-Fajr, 1999.

8. ___, (c) Usul Al-Nizam Al-Ijtimai Fil Islam, Ed. Mohamed El-Tahir Mesawi, Amman: Dar al-Nafais, 2001.

9. Kamali, M H (2009), Principles of Islamic Jurisprudence, Ilmiah Publishers, 2nd Revised Edition.

10. Laldin, M.A (2008), Introduction to Shariah & Islamic Jurisprudence, Kuala Lumpur, CERT Publications Sdn Bhd, 2nd Edition.

11. Nik Mohamad Affandi Nik Yusoff (2001), Islam and Wealth, Pelanduk Publications.

12. Rosly S.A (2005), USA, Critical Issues on Islamic Banking and Financial Markets, Authorhouse.

18 The 4E Journal

COVER STORY

January - March 2011

It was unprecedented – a bold, no-nonsense and ambitious initiative – to take the nation’s economy to the next

level of development. It was a project none has seen before in Malaysia – one with clear and measurable targets that are aimed at ensuring that the country achieves high-income status by the year 2020.

The brainchild of Prime Minister Datuk Seri Najib Razak, the Economic Transformation Programme (ETP) seeks to almost triple the country’s gross national income (GNI) from RM660 billion (US$188 billion) in 2009 to close to RM1.7 trillion (US$523

billion) in 2020. To achieve this, the country is expected to grow its GNI at 6 percent between 2011 and 2020 to hit the target.

And in line with its aspiration to bring about big results fast, 131 entry point projects (EPPs) and 60 business opportunities spread across 12 National Key Economic Areas (NKEAs) have been identified in the 10th Malaysia Plan – Oil, Gas & Energy, Palm Oil, Financial Services, Tourism, Business Services, Electrical & Electronics, Wholesale & Retail, Education, Healthcare, Communications Content & Infrastructure, Agriculture and Greater

Kuala Lumpur. Of the 12 NKEAs, 11 are industry sectors and one – Greater Kuala Lumpur – is a geographical location.

An NKEA is a driver of economic activity that has the potential to directly and materially contribute to a quantifiable amount of economic growth.

The ETP is also forecasted to create an incremental 3.3 million jobs, of which 63 percent will be in the middle- and high-income segments compared with the current 43 percent. The overall effect will be a significant growth in the job market,

&High-IncomeTowards

Sustainability

18 The 4E Journal

The 4E Journal 19

The Economic Transformation Programme (ETP) is, by far, Malaysia’s most ambitious economic programme. How is the ETP fundamentally different from say the New Economic Model and all the previous Malaysia Plans?

The ETP is a programme, not a plan. This simply means it has specified projects, targets, projection owners, timelines and action items. It is action-oriented and anchored on key performance indicators (KPIs) namely income and job generation.

On the other hand, plans tend to be strategic in nature and provide blueprint, which generally do not have precise roadmaps. The ETP is different in that it also prescribes a clear focus on 12 National Key Economic Areas (NKEAs) that the country is most competitive in and will channel disproportionate amount of financial and human capital as well as attention from the government.

This focus is validated by the forecast that 73 percent of the country’s gross national income (GNI) in 2020 will come from 11 NKEAs (excluding Greater Kuala Lumpur/Klang Valley due to potential income duplication). The implementation of the

131 entry point projects (EPPs) under the ETP will be closely monitored. They will also receive the necessary administrative facilitation and fiscal support to ensure optimal delivery.

What were the key findings that have come out from the various labs that have helped set the focus on achieving the various goals of the ETP?

In our aspiration to transition from middle-income to high-income, we must be focused and think out of the box. The need to really focus came with the realisation that we cannot excel in every economic sector, either due to loss of cost advantages or lack of competitiveness.

This is the reason why the 1,000-person workshop comprising participants from both the private and public sectors recommended that the country only focuses on the 12 NKEAs. After the focus on the 12 NKEAs was determined, the NKEAs labs of more than 500 members from the private and public sectors were set a few goals: take the per capita GNI from US$6,700 to US$15,000 by 2020, identify the projects to do so and create higher paying jobs in the process.

a shift towards higher paid jobs and a strengthening of skills base.

“Malaysia has no time to lose,” said Senator Datuk Seri Idris Jala, Minister in the Prime Minister’s Department and chief executive officer of PEMANDU (Performance Management and Delivery Unit). “We need a complete, radical economic transformation. The days of depending on traditional growth engines are over. If we continue on the current economic model, we risk getting stuck in middle-income trap and continue to lose out on talent necessary to support a high-income economy.”

“The ETP is essentially the economic roadmap for Malaysia, one that is co-created by the private sector and the government. It marks a fundamental departure in the approach towards economic planning in order to achieve developed nation status in 2020. It is also action-oriented and performance-focused, with well-developed and specific deliverables to grow each NKEA. It is the way forward,” Idris said matter-of-factly.

And this is where more transformational opportunities lie. The way forward also means creating a financially literate society in order that the wealth acquired may be duly and appropriately preserved for the long-term. As such, the government’s strategic intent of driving Malaysia towards becoming a high-income nation has to be delicately balanced with increasing financial literacy amongst the Rakyat to ensure sustainability. Both objectives must be given equal weightage and attention. The ETP has specifically addressed this need as well. With high-income comes the need for the populace to make better-informed financial choices and discipline in their personal finance. An increase in income clearly does not auger well if there is a corresponding increase in bankruptcies as both are not mutually exclusive. Unquestionably, financial literacy is critical to our prosperity as individuals as well as a nation.

To be better acquainted with the ETP, and specifically to find out more about the initiatives that the financial services NKEA has mapped out, the 4E Journal managing editor Steven K C Poh emailed Idris a list of questions, which he graciously and incisively answered. Plans are underway to integrate financial literacy into the Malaysian school curriculum and opportunities abound for financial planners to make their impact in the financial life of their clients. Check out the interview. The following are excerpts ….

Oil, Gas & Energy

Financial Services

Business Services

Wholesale & Retail

Healthcare

Content& Infrastructure

Palm Oil

Tourism

Electrical& Electronics

Education

Communications

GreaterKuala Lumpur

The 12 National Key Economic Areasof the Economic Transformation Programme

20 The 4E Journal

These targets are not easy to achieve but they are deliberately set high to force lab members out of their comfort zone and think out of the box. The message is that incremental improvement is not sufficient. Business as usual can no longer be the way forward. The result was an innovative, action-oriented way of doing things. The lab members not only told the government where to go but also who, how, when and what it takes to get there. The 131 EPPs identified clearly state the where, who, how, when and what to achieve the ambitious high-income nation targets.

How are efforts to realise the 12 NKEAs progressing so far? Can you share with us some of the early wins and what can be expected to be realised in 2011?

Since our launch on October 25, 2010, we have made good progress in all the 12 NKEAs. We have had four rounds of progress updates, where the Prime Minister announced new projects under the ETP. To date, we have announced 60 projects within 46 EPPs, which means 35 percent of the EPPs have taken off.

These projects have secured over RM95

billion in committed investments from a mix of domestic and multinational companies, a GNI impact of over RM137 billion, and will create 224,358 jobs by 2020. We have recently concluded the base load investment exercise where we contacted 5,835 companies in Malaysia, asking for projected investment in 2011.

Over 30 percent responded and we have also determined that private companies in Malaysia over the course of this year will invest RM50.6 billion. Coupled with the RM76 billion we expect to be invested through the EPPs, the best case scenario would be for a total investment of over RM127 billion in 2011. This gives us the confidence that the investment target of RM76 billion set for this year is achievable.

What are some of the key challenges PEMANDU, and in particular, the ETP, has faced in the last few months in terms of initiating change in the massive government machinery and what is currently being done to address the civil service mindset considering that it is an important, if not integral component of the transformation process (i.e. ensuring that the ETP is successfully implemented and achieve the desired results)?

For the ETP to succeed, implementation is key. We have always been long on planning but short on implementation. Not only must we set in motion the momentum to achieve our end target in 2020, we must also get big results fast to inspire confidence.

PEMANDU cannot do this on its own. We must form a winning coalition with the entire civil service to create an unstoppable movement that will not only generate results but also transform processes and culture. To do this, we must hold fast to the rigour of Discipline of Action.

Every project has an owner who will be held responsible for ensuring outcomes. PEMANDU’s role as a facilitator means ensuring collaboration and leverage both vertically and horizontally across the civil service.

At our monthly Steering Committee meetings chaired by the respective lead ministers, all relevant agencies, ministries and private sector project owners are present, to ensure action are agreed on and problems judiciously resolved. In this manner, we will ensure transparency and accountability and continued discipline of action will create a new culture of result-oriented performance.

From a national financial planning perspective, some quarters think a systemic change is required to efficiently manage the government’s revenue and expenditure in order that the objective to make Malaysia a high-income nation (a per capita income of US$15,000) by 2020 is achieved. Is this being addressed? How so and in what way?

The ETP is about systemic change in several ways. The unsustainable dependence on oil and gas as a gross domestic product

“In our aspiration to transition from middle-income to high-income,

we must be focused and think out of the box. “

The 4E Journal 21

(GDP) contributor has to be moderated from 22 percent to 14 percent in 2020. The services sector will reach 63 percent of the GDP, in line with the characteristics of developed economies, supporting contribution from commodities and manufacturing, among others. The economy can no longer rely on the government as the engine of growth. This task has to be returned to its rightful owner – the private sector.

The government will play the role of a facilitator. This way, the country’s fiscal position can be strengthened to ensure we are better positioned to deal with unexpected external global vagaries. The ETP, with its focus and precise implementation roadmap, provides the way to achieve all these goals.

How does the ETP complement or dovetail into the Government Transformation Programme (GTP)? Or

are the ETP and GTP mutually exclusive in their respective objectives?

The ETP and GTP are complementary programmes. The ETP focuses on increasing the wealth of the country by raising the GNI per capita and increasing wages, in an inclusive and sustainable way.

The GTP focuses on the social aspects of transformation, ensuring the distribution of wealth and increasing the quality of life for the Rakyat, especially for the bottom 40 percent that require assistance. Income generated from the ETP will be spent on the GTP. For example, revenue earned from increased tax arising from heightened profitability will be channeled and spent

on improving rural basic infrastructure, helping low-income households and improving education outcomes.

In this regard, education is especially key. Resources will be invested to ensure the bottom 40 percent received quality education that will help their children exit the vicious poverty cycle. Equipped with better skills, they will become more employable and create a pipeline of skilled workforce required by a higher income economy.

Some analysts have postulated that a high-income economy will also lead to high cost of living, which may basically mean that in the end we may not have a tenable quality of life. How is this issue mitigated and addressed in the ETP?

Malaysia is stuck in what we term the ‘middle-income trap.’ To meet our target of becoming a high-income nation by 2020, we must ensure that real wages go up. This means increasing wages faster than inflation. We can see this effect in a recent survey by Robert Walters, an international recruiting agency. Their findings predicted a rise of up to 30 percent in professional salaries. If we can keep this up through to 2020, we can ensure that the cost of living will be proportionally lower than what it is today.

In the nation’s quest to achieve a high-income status by the year 2020, where do you see the bottom 40 percent of the population in terms of their economic standing? There are concerns from various quarters that instead of bridging the income gap it may actually widen it. Your comment please.

Based on the lab analysis, it is expected that more jobs will be created in the upper income level and this will shift the bottom 40 percent of the population into a better income bracket.

“NGOs can greatly assist them by working hand in hand to address common misconceptions and provide the public with the required fundamental knowledge in financial planning. “

“Human capital is a very critical enabler in the financial services sector and to meet short-term demands for talent. “

22 The 4E Journal

The financial services sector has been positioned in the ETP as the bedrock of our high-income economy aspirations. Why financial services and not one of the other 11 NKEAs, say oil, gas & energy or perhaps Greater KL?

The financial services sector forms the bedrock of any economy. This is largely due to the fact that in any project, in this case, EPPs and business opportunities (BOs), would require capital for development and operations. All large successful economies require strong banks, vibrant capital markets and well-functioning financial infrastructure, which is the focus of this particular NKEA.

It is important that our financial services sector be sound and is ready to support the expected growth in the economy. Apart from being an industry on its own, growth in other sectors will need access to the capital market which will provide the required capital, be it from the bond market or the equity market.

Malaysia’s young wealth management industry is currently focused only on the affluent market. What will the government do, via the ETP, to ensure that the ‘wealth’ (whatever each citizen has) of the average Rakyat is effectively and efficiently managed to ensure long-term sustainability?

As mentioned earlier, the ETP aims to raise the GNI per capita to US$15, 000 per annum from the current US$7,600. Over the next 10 years, we will create significant wealth, and it is our intention that it is in a manner that would be sustainable for a long period of time.

This goes hand in hand with increased financial literacy. EPP 7, which addresses wealth management, intends to carefully liberalise and increase the number of wealth management products available to the general public, slowly introducing the concept of wealth management to the Rakyat at all income levels. To ensure the success of this EPP, the government will work with the private sector to bring in and nurture wealth managers and product specialists who are best able to cater not just to the affluent few, but to the general public as well.

One of the challenges of the Malaysian financial services sector is the low levels of financial literacy. What is the government doing to ensure that the Rakyat better manage their personal finances in line with its move to a high-income economy? Also will the government be proposing a tax

incentive for the citizenry to engage in financial and retirement planning? If so, when will this happen? Surely if tax incentives can be given to foreign companies to invest in Malaysia, they can be given to the Rakyat to be actively engaged in financial and retirement planning to significantly lessen the government’s financial burden in the provision of social welfare services.

Malaysia’s tax base is relatively narrow with approximately one million taxpayers, making a tax incentive scheme unfeasible. The Ministry of Finance is currently studying ways to increase this tax base to create avenues for the government to provide incentives for the Rakyat to undertake financial and retirement planning.

We realise that while economic growth is fueled by consumer spending and the

availability of credit enables consumers to spend more in the market, it is crucial that the Malaysian public is provided with at least a basic understanding of financial literacy to manage their personal finance. To this end, organisations such as Bank Negara Malaysia, the Securities Commission and Bursa Malaysia have begun initiatives to educate the public on this matter.

Specifically, what can a non-governmental organisation (NGO) like the Financial Planning Association of Malaysia (FPAM) do to assist the

“The financial services sector forms the bedrock of any economy.“

The 4E Journal 23