Embed Size (px)

Citation preview

5 Tax Topics for 2017Pearl P. BalsaraRandy Garcia

Huselton, Morgan & Maultsby, P.C.June 20, 2017

1

Disclaimer

LEGAL, INVESTMENT AND TAX NOTICE

These materials do not constitute tax or legal advice, and cannot be reliedupon for purposes of avoiding penalties under the Internal Revenue Code.These materials may omit discussion of exceptions, qualifications,definitions, effective dates, jurisdictional differences, and other relevantauthorities and considerations. In no event should a reader rely on thesematerials in planning a specific transaction or litigation. Non-lawyers shouldnot attempt to provide legal services or legal advice in circumstanceswhere that would violate laws against the unauthorized practice of law.HM&M will not be responsible for any error, omission, or inaccuracy inthese materials.

2June 20, 2017 Huselton, Morgan & Maultsby, Confidential

Key Takeaways …

● The American Health Care Act Vs Affordable Care Act

● R&D Tax Credit

● Partnership Audit Rules

● Tax Reform

● 2017 Updates

3June 20, 2017 Huselton, Morgan & Maultsby, Confidential

The American Health Care Act (AHCA)

● The House voted on May 4 to approve the AHCA – a plan/proposal to repeal & replace the ACA

● AHCA now has moved to the Senate & its fate is in their hands!

4June 20, 2017 Huselton, Morgan & Maultsby, Confidential

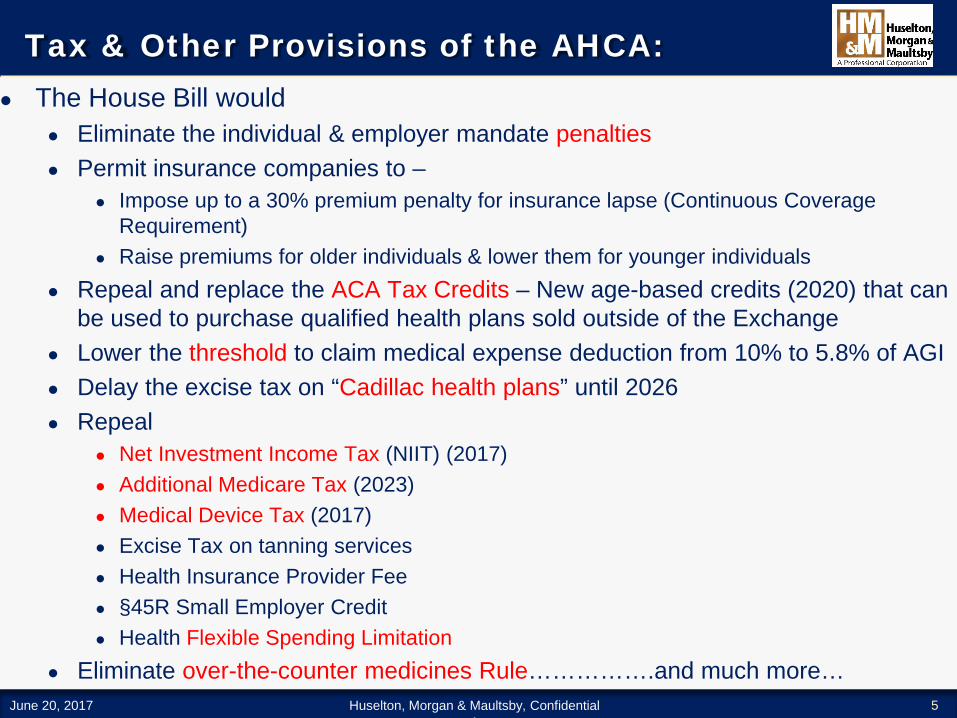

Tax & Other Provisions of the AHCA:● The House Bill would

● Eliminate the individual & employer mandate penalties● Permit insurance companies to –

● Impose up to a 30% premium penalty for insurance lapse (Continuous Coverage Requirement)

● Raise premiums for older individuals & lower them for younger individuals● Repeal and replace the ACA Tax Credits – New age-based credits (2020) that can

be used to purchase qualified health plans sold outside of the Exchange● Lower the threshold to claim medical expense deduction from 10% to 5.8% of AGI● Delay the excise tax on “Cadillac health plans” until 2026● Repeal

● Net Investment Income Tax (NIIT) (2017)● Additional Medicare Tax (2023) ● Medical Device Tax (2017)● Excise Tax on tanning services● Health Insurance Provider Fee● §45R Small Employer Credit● Health Flexible Spending Limitation

● Eliminate over-the-counter medicines Rule…………….and much more…5June 20, 2017 Huselton, Morgan & Maultsby, Confidential

l

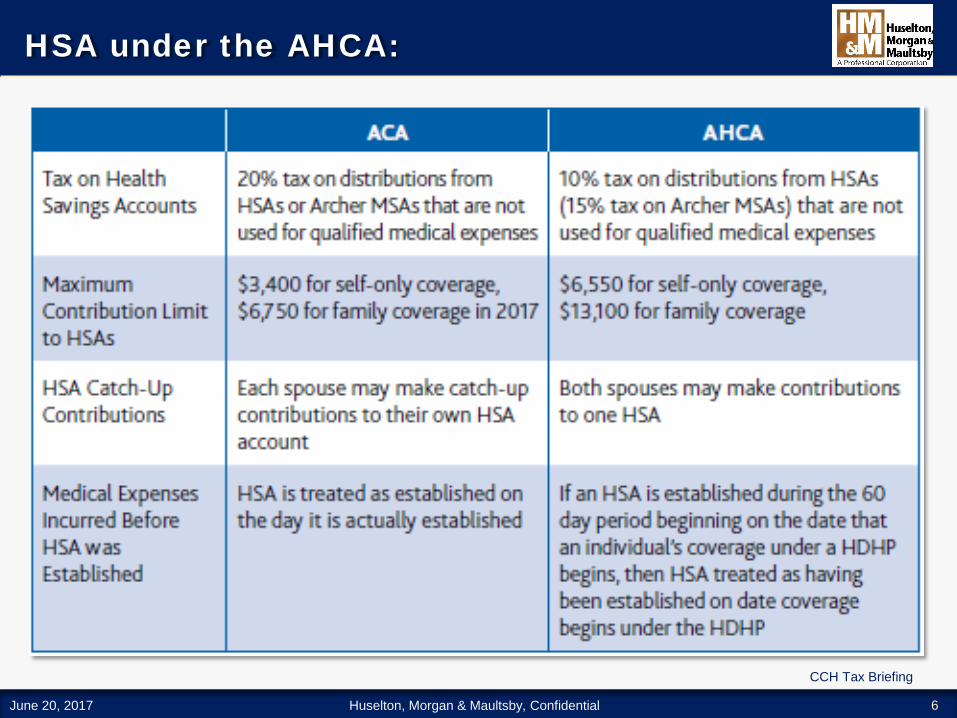

HSA under the AHCA:

6

CCH Tax Briefing

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

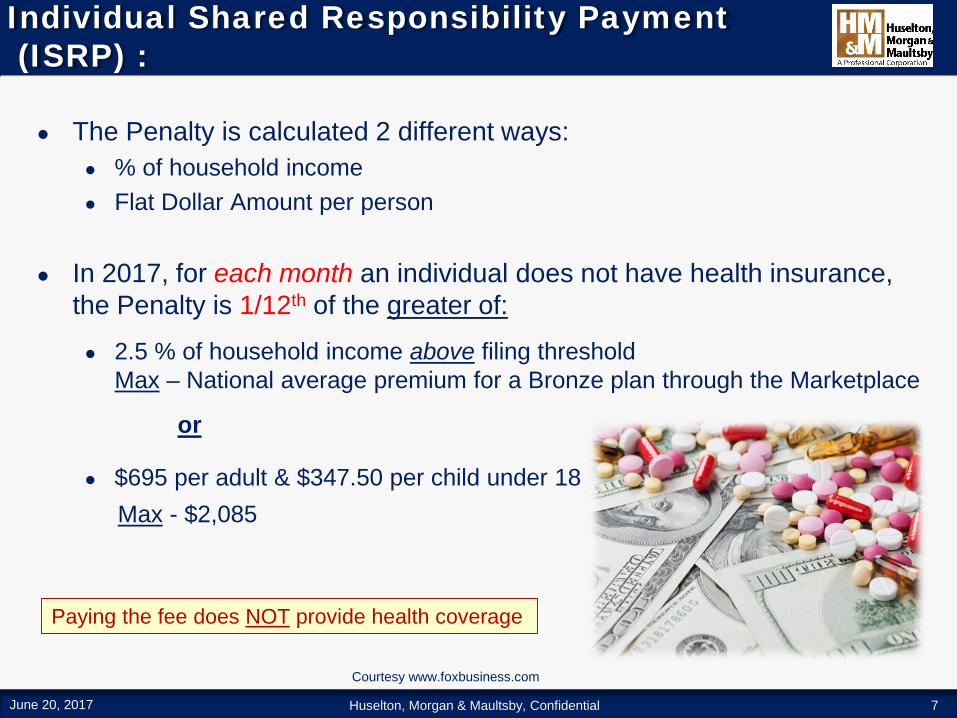

Individual Shared Responsibility Payment(ISRP) :

● The Penalty is calculated 2 different ways:● % of household income ● Flat Dollar Amount per person

● In 2017, for each month an individual does not have health insurance, the Penalty is 1/12th of the greater of:

● 2.5 % of household income above filing threshold Max – National average premium for a Bronze plan through the Marketplace

or

● $695 per adult & $347.50 per child under 18 Max - $2,085

7

Courtesy www.foxbusiness.com

Paying the fee does NOT provide health coverage

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

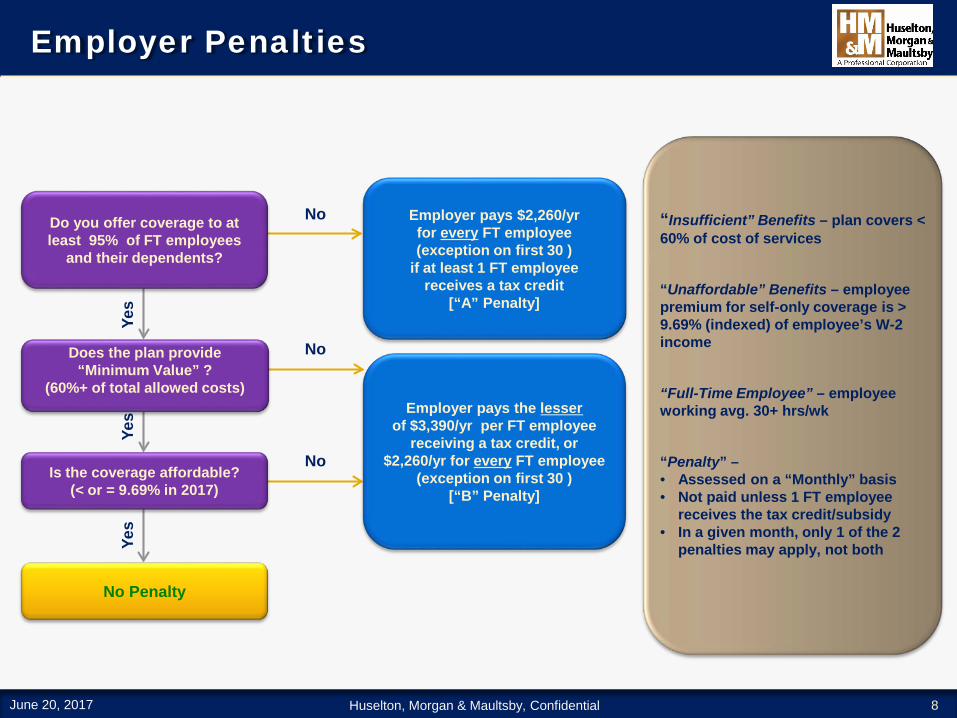

Employer Penalties

8

Yes

Yes

Yes

Do you offer coverage to at least 95% of FT employees

and their dependents?

Does the plan provide “Minimum Value” ?

(60%+ of total allowed costs)

Is the coverage affordable?(< or = 9.69% in 2017)

No Penalty

Employer pays the lesserof $3,390/yr per FT employee

receiving a tax credit, or $2,260/yr for every FT employee

(exception on first 30 )[“B” Penalty]

Employer pays $2,260/yrfor every FT employee (exception on first 30 )

if at least 1 FT employee receives a tax credit

[“A” Penalty]

No

No

No

“Insufficient” Benefits – plan covers < 60% of cost of services

“Unaffordable” Benefits – employee premium for self-only coverage is > 9.69% (indexed) of employee’s W-2 income

“Full-Time Employee” – employee working avg. 30+ hrs/wk

“Penalty” –• Assessed on a “Monthly” basis • Not paid unless 1 FT employee

receives the tax credit/subsidy• In a given month, only 1 of the 2

penalties may apply, not both

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

R&D Tax Credit

9

Courtesy : minnesotabusiness.com

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

R&D Tax Credit (§41 Credit)

Under the “Protecting Americans From Tax Hikes Act of 2015” (the “PATH Act”) …

● R&D Tax Credit is permanently extended

● Eligible/Qualifying Small Businesses may use the credit to offset –● both Regular tax and AMT liabilities (AMT Benefit)● Payroll taxes (PT Benefit)

10June 20, 2017 Huselton, Morgan & Maultsby, Confidential

R&D Tax Credit Benefits

The Potential Benefits of the R&D Tax Credit can include:

● Dollar-for-dollar reduction in your federal and state income tax liability● Increase in earnings-per-share● Reduction of your effective tax rate● Improved cash flow● Credit carried forward up to 20 years● Recent regulatory developments make claiming the R&D tax credit for

companies much more feasible● Look back studies can recognize unclaimed

credits for open tax years (generally 3-4 years)● In certain cases, credits from closed tax

years are also eligible

11

Picture courtesy momentumgroupni.com

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

R&D Tax Credit – Qualifying Activities & Industries

● Some common qualified research activities:● Developing or designing new products, processes or formulas● Developing a new manufacturing process● Developing prototypes or models● Developing internal software solutions● Developing or improving software technologies● Testing new materials or concepts ● And many more…….

● Some of the industries that typically have eligible activities:● Aerospace● Agriculture● Architecture● Breweries/Wineries● Commercial Bakeries● Electronics● Furniture makers● O&G Refineries……and many more

12

Picture courtesy robertsnathan.com

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

R&D Tax Credit – The Four-Part Test

An activity that meets the following 4 tests may qualify for R&D Tax Credits:

● Elimination of Uncertainty about the development or improvement of a product or process

● Process of Experimentation to eliminate or resolve a technical uncertainty

● Technological in Nature – process of experimentation must rely on hard sciences, such as engineering, physics, chemistry etc

● Qualified Purpose – to create a new or improved product or process

13

“Documentation” is KEY to strengthening the R&D Tax Credit claimed

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

R&D Tax Credit – Qualifying Research Expenses

Expenses that may qualify for R&D Tax Credits can be broadly categorized as:

● Salaries

● Supplies

● Contract Research

14

https://www.merieuxnutrisciences.com/us/services/food-safety-and-quality/contract-research http://www.regentchemicals.com/

http://www.sundaynews.co.zw/no-more-delays-for-civil-servants-salaries/

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

R&D Tax Credit – Annual Considerations

● 2 key considerations each year:● Which credit method to use

● Regular Credit (“Old & Cold” Method) – 20% x QREs over Base Amount● Alternative Simplified Credit (ASC) – 14% x QREs over Base Amount

● Whether to make the §280C Reduced Credit Election

● §280C Reduced Credit Election:● Annual Election● 35% reduction to CY calculated credit amount● Avoids reduction to CY QREs deducted by amount of the credit● No “double benefit”● Generally will make the §280C election if subject to tax● Preserves election if taxpayer amends return to claim R&D credit

15June 20, 2017 Huselton, Morgan & Maultsby, Confidential

Partnership Audit Rules

● Bipartisan Budget Act of 2015 (P.L. 114-74) signed into law on November 2nd, 2015. To date, no Regulations (kind of)

● Eliminates the TEFRA unifiedpartnership audit rules, the smallpartnership audit rules and theelecting large partnership rules

● Implements streamlinedpartnership audit rules

● Effective for tax years beginning after December 31, 2017

16Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

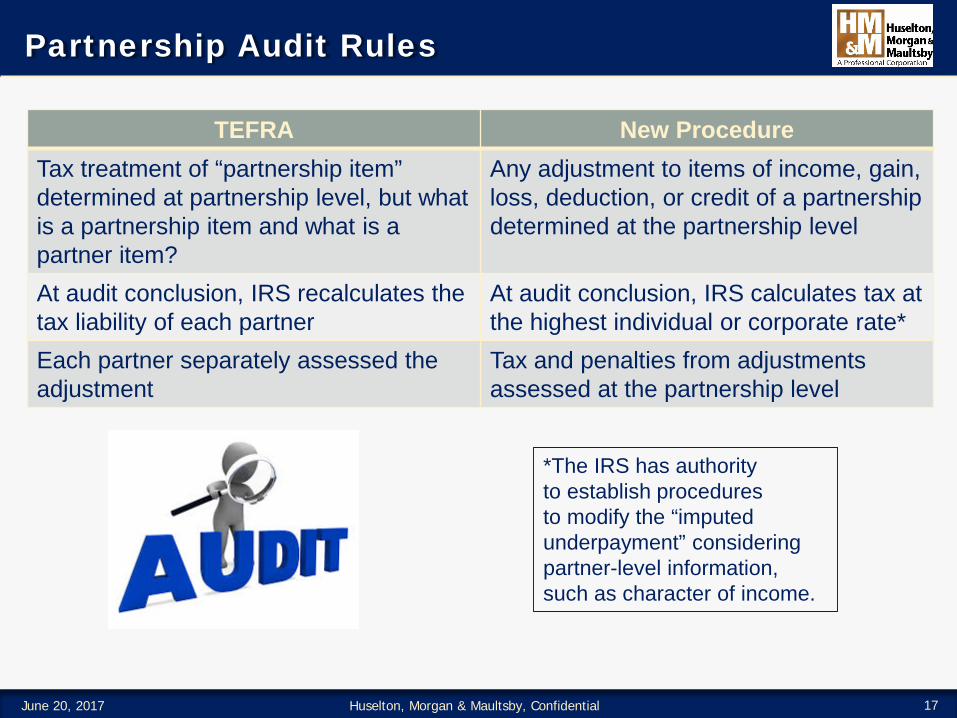

Partnership Audit Rules

TEFRA New ProcedureTax treatment of “partnership item” determined at partnership level, but what is a partnership item and what is a partner item?

Any adjustment to items of income, gain, loss, deduction, or credit of a partnership determined at the partnership level

At audit conclusion, IRS recalculates the tax liability of each partner

At audit conclusion, IRS calculates tax at the highest individual or corporate rate*

Each partner separately assessed the adjustment

Tax and penalties from adjustments assessed at the partnership level

17Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

*The IRS has authorityto establish proceduresto modify the “imputedunderpayment” consideringpartner-level information,such as character of income.

Partnership Audit Rules

● Electing out of the new rules● Year by year election● Election included on a timely filed return for the respective tax

year and discloses the name and TIN or each partner● Partnership must notify partners of the election● Eligible partnerships may only issue 100 or fewer K-1s

● What if the same partner receives a K-1 for multiple classes of interest?

● What about transfers of interest causing two or more K-1s?

18Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

Partnership Audit Rules

● Electing out of the new rules● Eligible partnerships may only have partners that are

● Individuals● C Corporations● Foreign entities that would be C Corps if they were domestic● An estate of a deceased partner● S Corporations

● K-1s issued by the S Corporation count towards the 100 K-1 limit● Missing? Partnerships and Trusts (including Grantor).

● If elected out:● Subject to the general rules for the assessment and collection

of tax deficiencies applicable to individual taxpayers● TEFRA and the old regime is gone.

19Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

Partnership Audit Rules

● Election for partner-level adjustment● Elected no later than 45 days after receiving notice of final

partnership adjustment● Partnership issues adjusted information returns (K-1s) to the

reviewed year partners● Simplified amended-return process for partners to report

adjustments and pay tax● “Surcharge”

● Underpayment rate for partners is 2 percentage points higher than the general rate on underpayments

● Later-year tax attributes must be adjusted by the partners● NOLs, tax basis, PALs, etc.

20Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

Partnership Audit Rules

● Partnership Representative – need not be a partner● Person with “substantial presence in the United States”● More powerful than the Tax Matters Partner

● Sole authority to act on behalf of the partnership● May bind the partnership and partners in IRS audits and in court● IRS only needs to provide notices to the PR

● If partnership representative has not been designated, the IRS may select any person as the partnership representative

21Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

Partnership Audit Rules

● These new rules are the law and they are coming fast

● What do to now – changes to Partnership Agreements● Designate a partnership representative or determine rules for

selecting one. Will the PR act independently or should the PR be guided by other partners?

● Consider indemnification clauses

● Consider whether your partnership qualifiesto elect out and whether it is a good idea

● New partners: Do proper diligence on possible exposure

22Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

Tax Reform Update

23Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

Tax Reform Update

● Important considerations● Simplification

● Revenue neutrality

● Permanence

● “There is no perfect way to tax, but there are proven ways to grow our economy” – Rep. Brady, opening remarks on hearing May 18th, 2017.

24Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

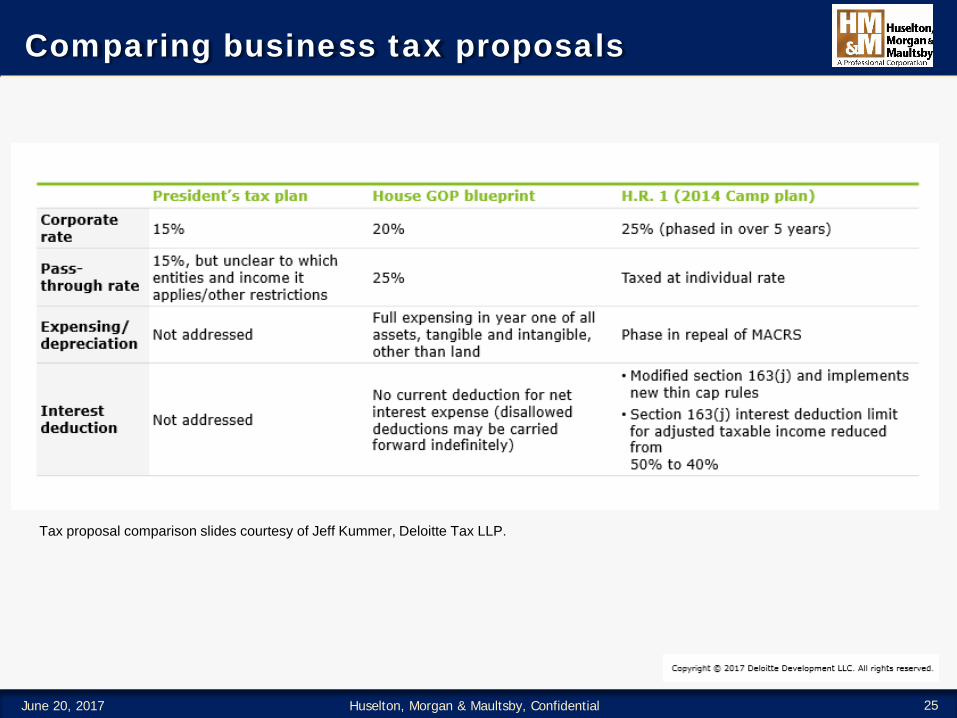

Comparing business tax proposals

Tax proposal comparison slides courtesy of Jeff Kummer, Deloitte Tax LLP.

June 20, 2017 Huselton, Morgan & Maultsby, Confidential 25

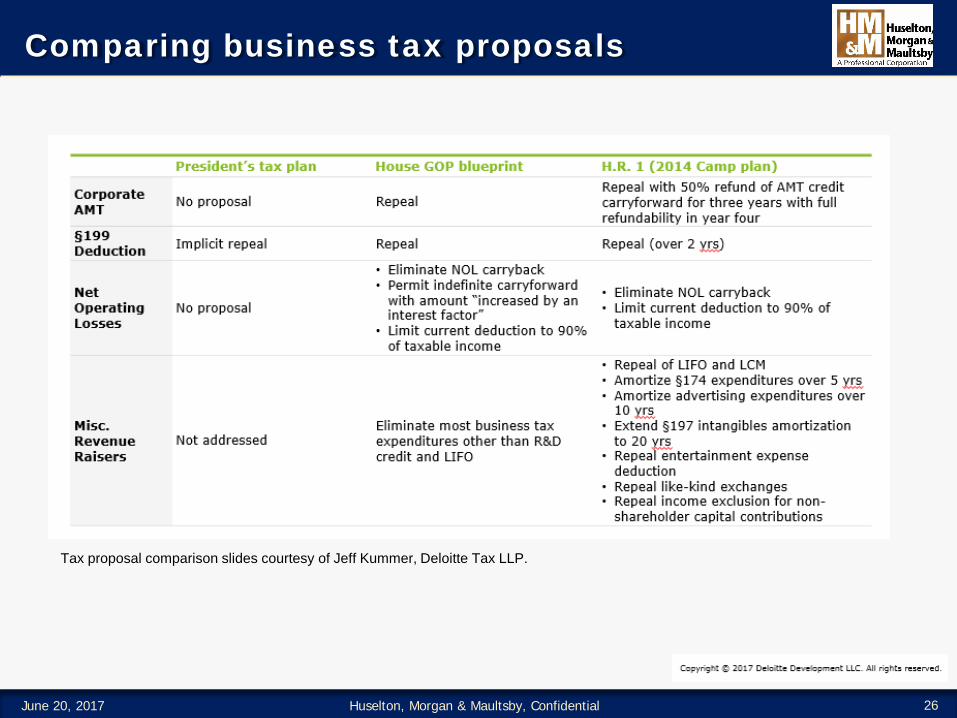

Comparing business tax proposals

Tax proposal comparison slides courtesy of Jeff Kummer, Deloitte Tax LLP.

June 20, 2017 Huselton, Morgan & Maultsby, Confidential 26

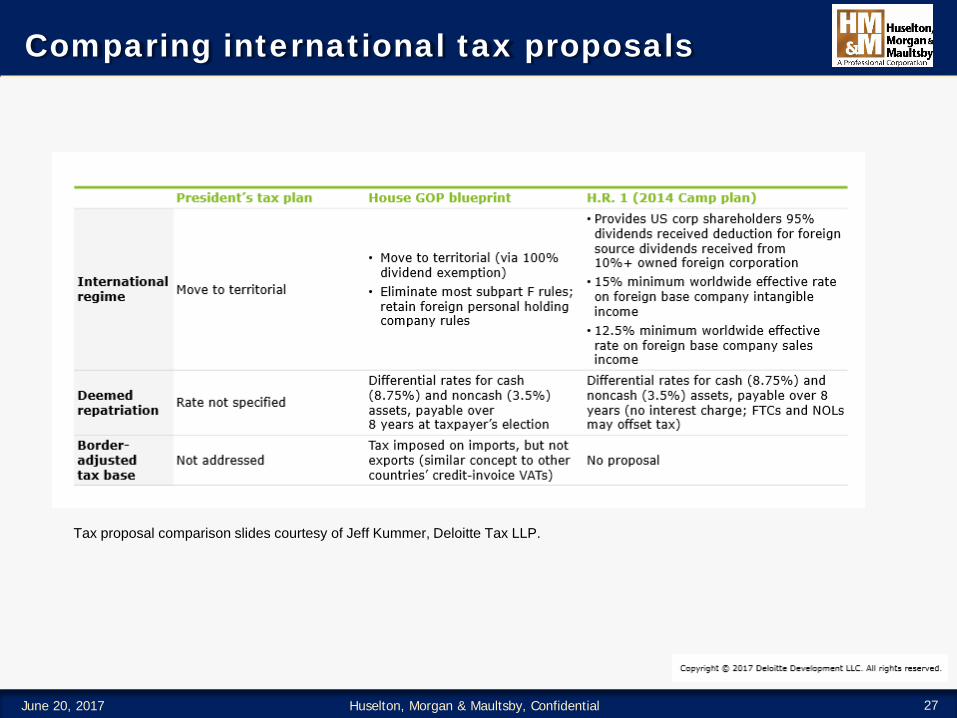

Comparing international tax proposals

Tax proposal comparison slides courtesy of Jeff Kummer, Deloitte Tax LLP.

June 20, 2017 Huselton, Morgan & Maultsby, Confidential 27

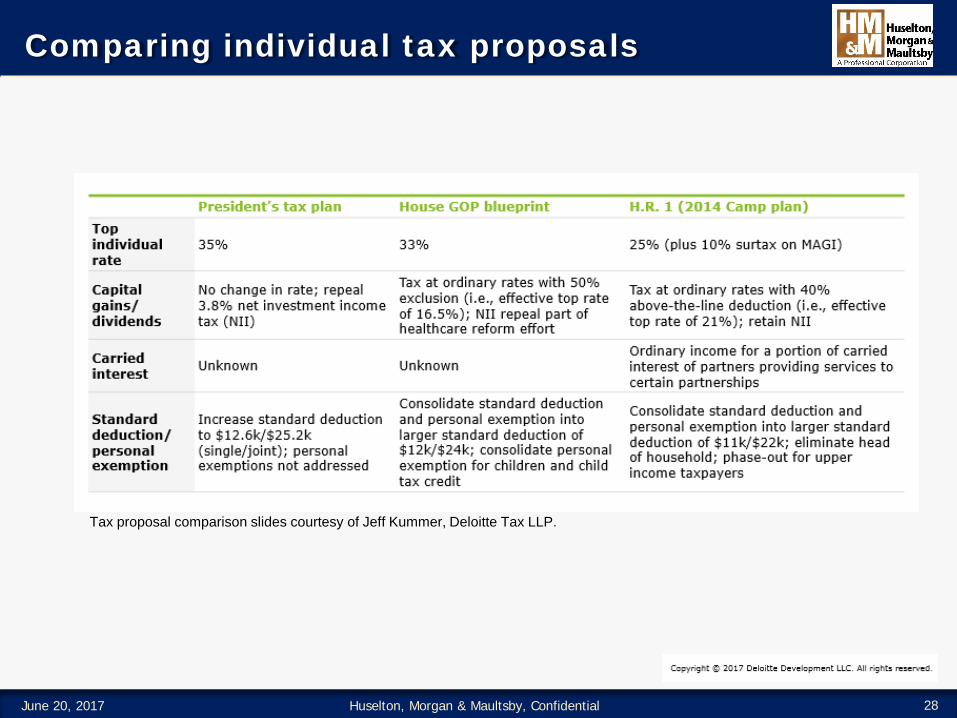

Comparing individual tax proposals

Tax proposal comparison slides courtesy of Jeff Kummer, Deloitte Tax LLP.

June 20, 2017 Huselton, Morgan & Maultsby, Confidential 28

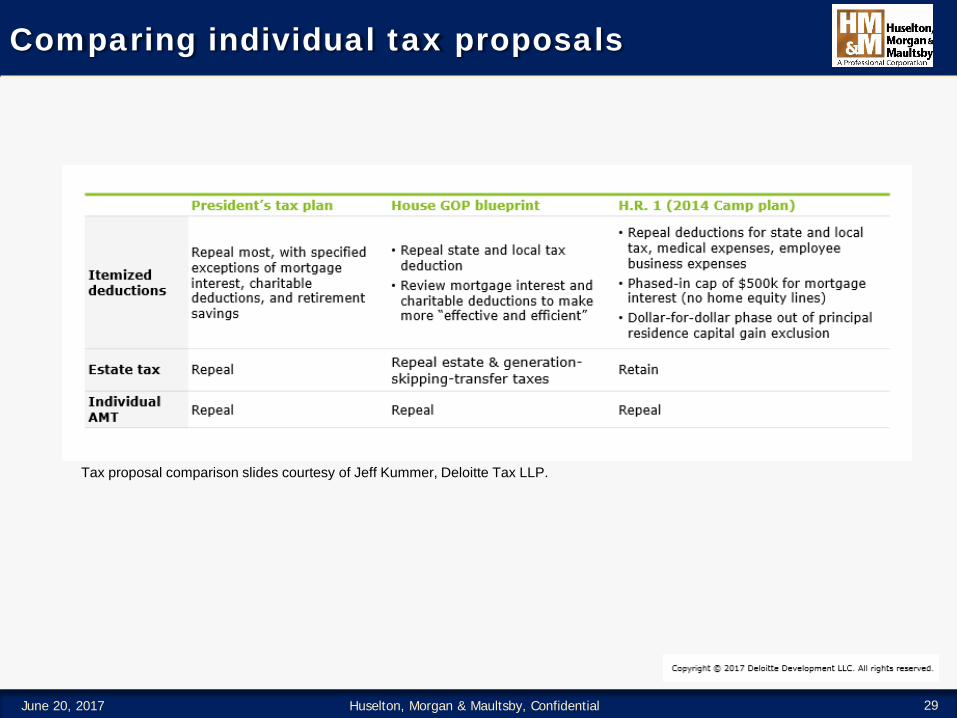

Comparing individual tax proposals

Tax proposal comparison slides courtesy of Jeff Kummer, Deloitte Tax LLP.

June 20, 2017 Huselton, Morgan & Maultsby, Confidential 29

Tax Reform Update

30Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

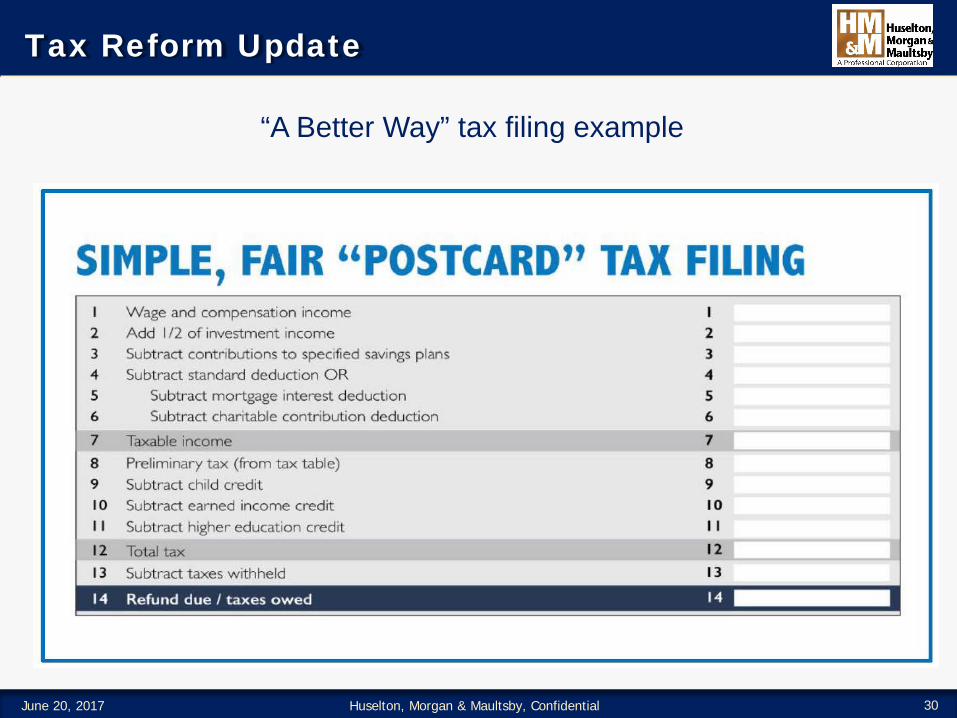

“A Better Way” tax filing example

Tax Reform Update

● Dates of recent events● June 24th, 2016: “A Better Way” released

● April 26th, 2017: Trump one page tax plan released

● May 18th, 2017: House Ways and Means Committee first hearing during this session of Congress

● June 13th, 2017: Rep. Brady proposes phase-in of BAT

31Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017

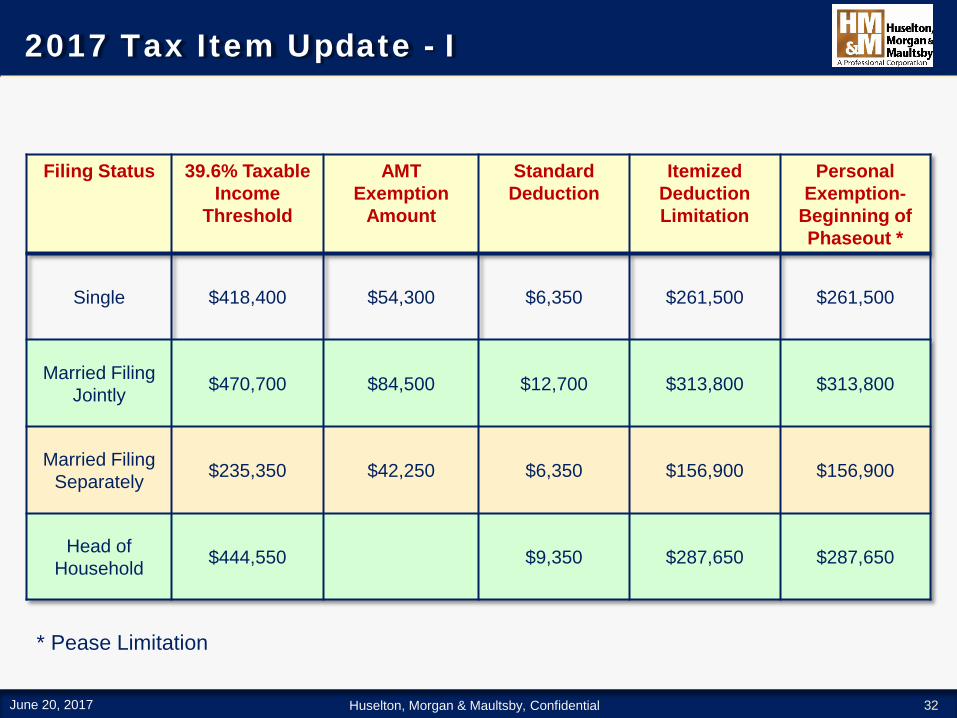

2017 Tax Item Update - I

32

Filing Status 39.6% Taxable Income

Threshold

AMT Exemption

Amount

Standard Deduction

Itemized DeductionLimitation

Personal Exemption-

Beginning of Phaseout *

Single $418,400 $54,300 $6,350 $261,500 $261,500

Married Filing Jointly $470,700 $84,500 $12,700 $313,800 $313,800

Married Filing Separately $235,350 $42,250 $6,350 $156,900 $156,900

Head of Household $444,550 $9,350 $287,650 $287,650

* Pease Limitation

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

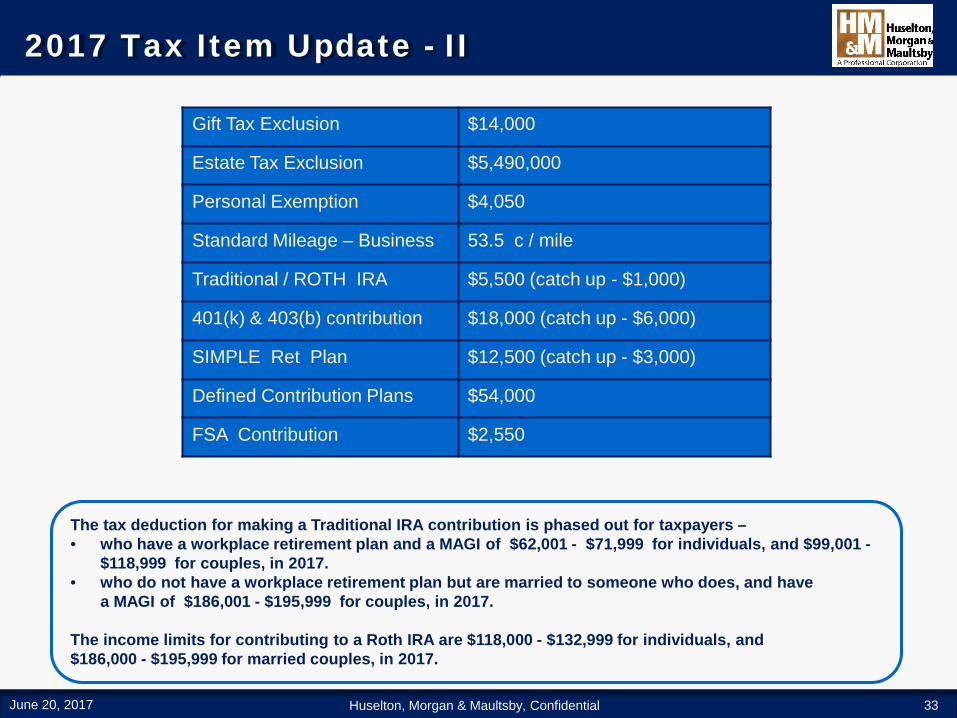

2017 Tax Item Update - II

33

Gift Tax Exclusion $14,000

Estate Tax Exclusion $5,490,000

Personal Exemption $4,050

Standard Mileage – Business 53.5 c / mile

Traditional / ROTH IRA $5,500 (catch up - $1,000)

401(k) & 403(b) contribution $18,000 (catch up - $6,000)

SIMPLE Ret Plan $12,500 (catch up - $3,000)

Defined Contribution Plans $54,000

FSA Contribution $2,550

The tax deduction for making a Traditional IRA contribution is phased out for taxpayers –• who have a workplace retirement plan and a MAGI of $62,001 - $71,999 for individuals, and $99,001 -

$118,999 for couples, in 2017.• who do not have a workplace retirement plan but are married to someone who does, and have

a MAGI of $186,001 - $195,999 for couples, in 2017.

The income limits for contributing to a Roth IRA are $118,000 - $132,999 for individuals, and $186,000 - $195,999 for married couples, in 2017.

June 20, 2017 Huselton, Morgan & Maultsby, Confidential

Tax Extenders through 2016 only

● For Individuals● 7.5% AGI floor for medical expense deduction for 65 & above● Qualified tuition & fees for post-secondary education● Cancellation of Mortgage Debt● Mortgage Insurance Premiums

34June 20, 2017 Huselton, Morgan & Maultsby, Confidential

Tax Extenders through 2016 only

● For Businesses:● Bonus Depreciation

● 50% thru 2017● 40% in 2018● 30% in 2019

● Empowerment zones incentives● Film/television expensing● §25C Residential Energy Property Credit● Energy-efficient Commercial buildings● Credit for

● 2-wheel plug-in electric vehicles● 2nd generation biofuel producer credit etc

● ….to name a few

35June 20, 2017 Huselton, Morgan & Maultsby, Confidential

Questions

36Huselton, Morgan & Maultsby, ConfidentialJune 20, 2017