Embed Size (px)

Citation preview

6 - 1©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Audit Audit ResponsibilitiesResponsibilitiesand Objectivesand Objectives

Chapter 6Chapter 6

6 - 2©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 1Learning Objective 1

Explain the objective ofExplain the objective of

conducting an audit ofconducting an audit of

financial statements andfinancial statements and

an audit of internal controls.an audit of internal controls.

6 - 3©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Objective of Conducting an Audit Objective of Conducting an Audit of Financial Statementsof Financial Statements

The objective of the ordinary audit of financialThe objective of the ordinary audit of financialstatements is the expression of an opinion ofstatements is the expression of an opinion ofthe fairness with which they present fairly, inthe fairness with which they present fairly, inall respects, financial position, result ofall respects, financial position, result ofoperations, and its cash flows inoperations, and its cash flows inconformity with GAAP.conformity with GAAP.

6 - 4©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

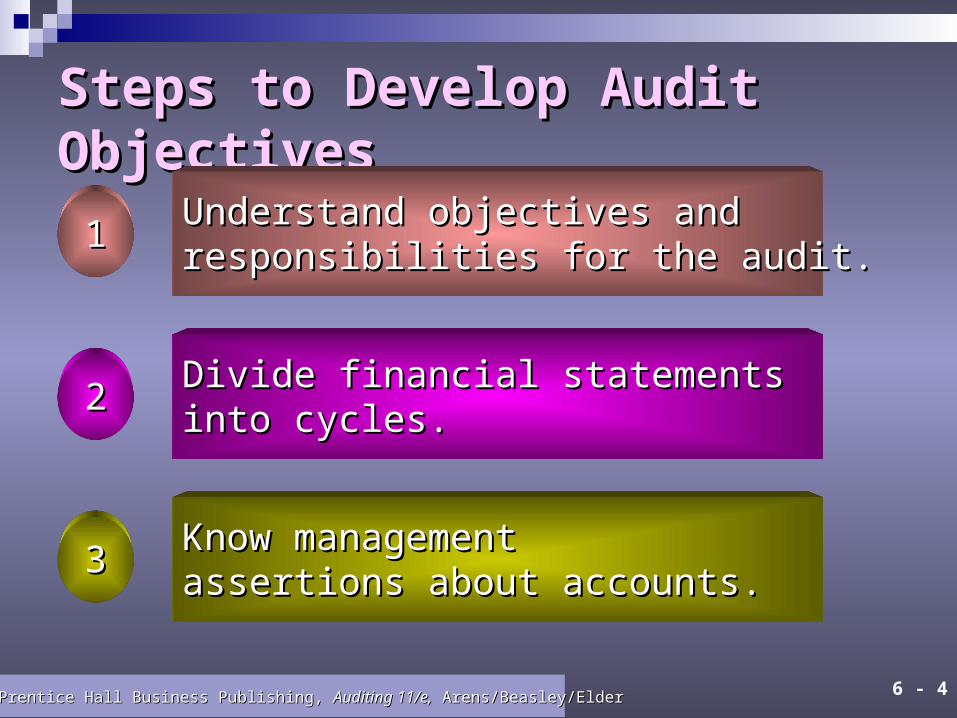

Steps to Develop Audit ObjectivesSteps to Develop Audit Objectives

Understand objectives andUnderstand objectives andresponsibilities for the audit.responsibilities for the audit.11

22Divide financial statementsDivide financial statementsinto cycles.into cycles.

33Know managementKnow managementassertions about accounts.assertions about accounts.

6 - 5©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

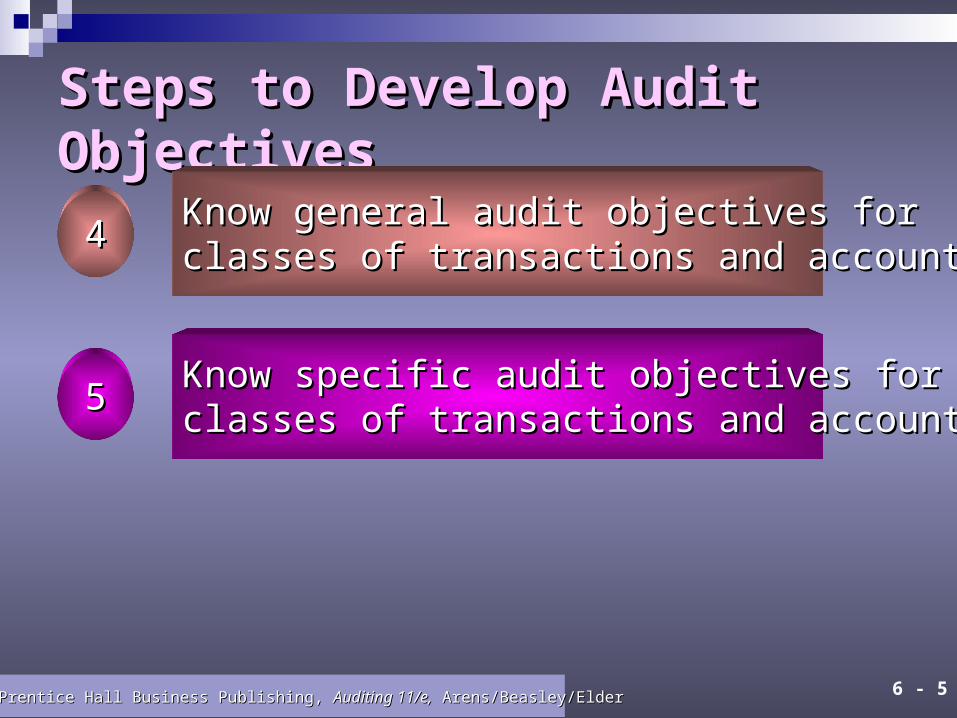

Steps to Develop Audit ObjectivesSteps to Develop Audit Objectives

Know general audit objectives forKnow general audit objectives forclasses of transactions and accounts.classes of transactions and accounts.44

55Know specific audit objectives forKnow specific audit objectives forclasses of transactions and accounts.classes of transactions and accounts.

6 - 6©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 2Learning Objective 2

Distinguish management’sDistinguish management’sresponsibility for the financialresponsibility for the financialstatements and internal controlstatements and internal controlfrom the auditor’s responsibilityfrom the auditor’s responsibilityfor verifying the financialfor verifying the financialstatements and effectivenessstatements and effectivenessof internal control.of internal control.

6 - 7©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Management’s ResponsibilitiesManagement’s Responsibilities

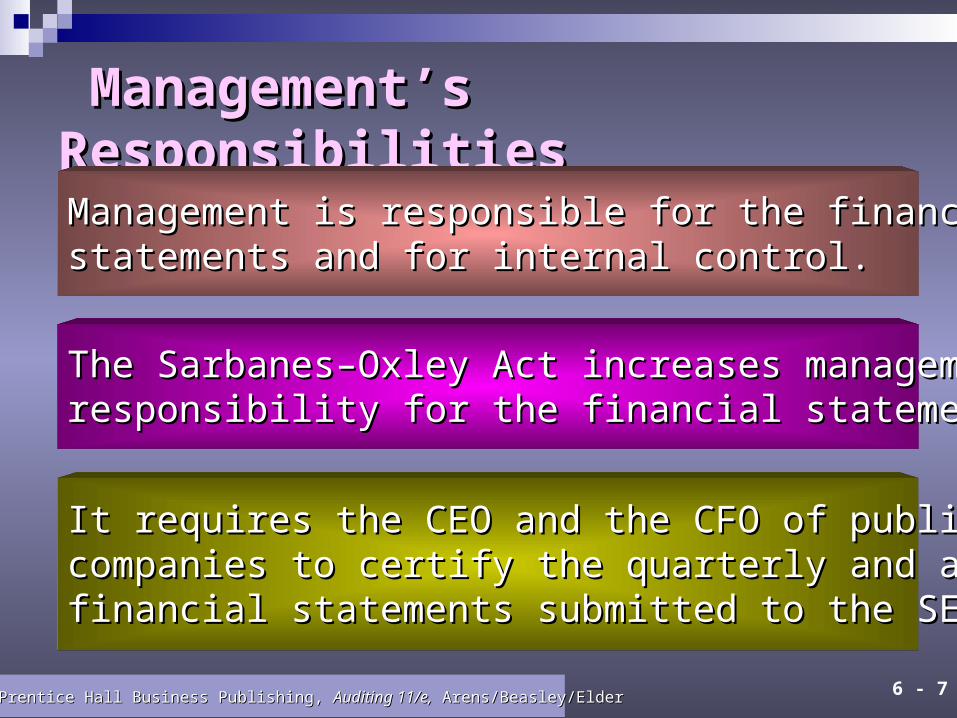

Management is responsible for the financialManagement is responsible for the financialstatements and for internal control.statements and for internal control.

The Sarbanes–Oxley Act increases management’sThe Sarbanes–Oxley Act increases management’sresponsibility for the financial statements.responsibility for the financial statements.

It requires the CEO and the CFO of publicIt requires the CEO and the CFO of publiccompanies to certify the quarterly and annualcompanies to certify the quarterly and annualfinancial statements submitted to the SEC.financial statements submitted to the SEC.

6 - 8©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Management’s ResponsibilitiesManagement’s Responsibilities

The Sarbanes-Oxley Act provides for criminalThe Sarbanes-Oxley Act provides for criminalpenalties for anyone who knowingly falselypenalties for anyone who knowingly falselycertifies the statements.certifies the statements.

6 - 9©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 3Learning Objective 3

Explain the auditor’sExplain the auditor’s

responsibility for discoveringresponsibility for discovering

material misstatements.material misstatements.

6 - 10©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Auditor’s ResponsibilitiesAuditor’s Responsibilities

–– Material versus immaterial misstatementsMaterial versus immaterial misstatements–– Reasonable assuranceReasonable assurance–– Errors versus fraudErrors versus fraud–– Professional skepticismProfessional skepticism–– Fraud resulting from fraudulent financialFraud resulting from fraudulent financial

reporting versus misappropriation of assetsreporting versus misappropriation of assets

6 - 11©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Auditor’s Responsibilities for Auditor’s Responsibilities for Discovering Illegal ActsDiscovering Illegal Acts

Direct-effect illegal actsDirect-effect illegal acts

Indirect-effect illegal actsIndirect-effect illegal acts

Evidence accumulation when there is no reasonEvidence accumulation when there is no reasonto believe indirect-effect illegal act existsto believe indirect-effect illegal act exists

6 - 12©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Auditor’s Responsibilities for Auditor’s Responsibilities for Discovering Illegal ActsDiscovering Illegal Acts

Evidence accumulation and other actionsEvidence accumulation and other actions when there is reason to believe direct- orwhen there is reason to believe direct- orindirect-effect illegal acts may existindirect-effect illegal acts may exist

Actions when the auditor knows of an illegal actActions when the auditor knows of an illegal act

6 - 13©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 4Learning Objective 4

Classify transactions and accountClassify transactions and account

balances into financial statementbalances into financial statement

cycles and identify benefits of acycles and identify benefits of a

cycle approach to segmentingcycle approach to segmenting

the audit.the audit.

6 - 14©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Financial Statements CyclesFinancial Statements Cycles

Audits are performed by dividing the financialAudits are performed by dividing the financialstatements into smaller segments or components.statements into smaller segments or components.

6 - 15©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

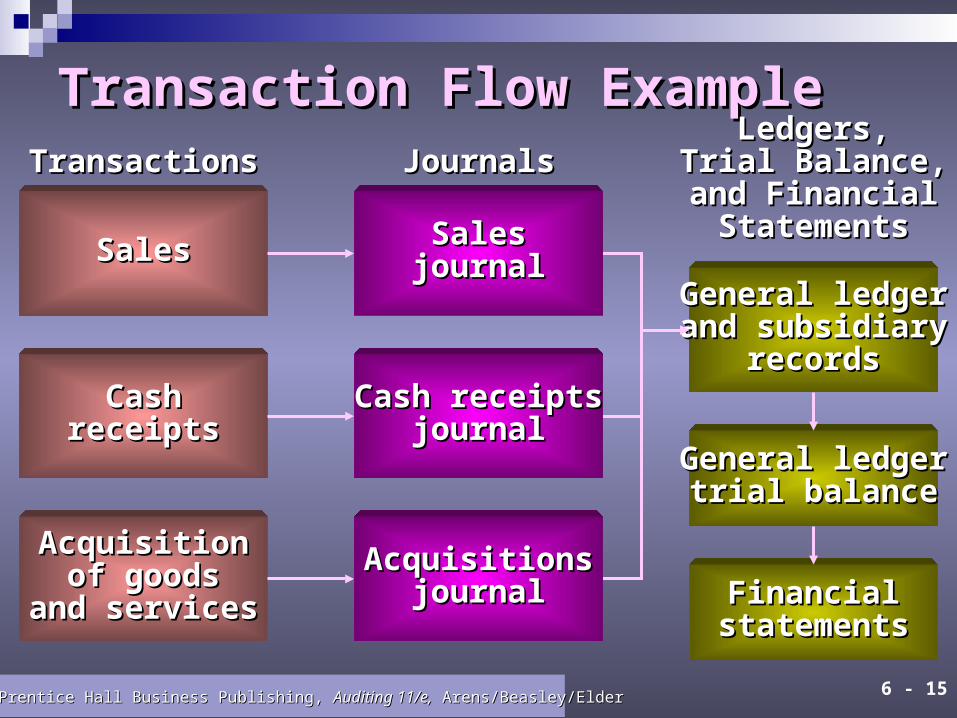

Transaction Flow ExampleTransaction Flow ExampleLedgers,Ledgers,

Trial Balance,Trial Balance,and Financialand FinancialStatementsStatements

General ledgerGeneral ledgerand subsidiaryand subsidiary

recordsrecords

General ledgerGeneral ledgertrial balancetrial balance

FinancialFinancialstatementsstatements

AcquisitionAcquisitionof goodsof goods

and servicesand services

SalesSales

CashCashreceiptsreceipts

TransactionsTransactions

Cash receiptsCash receiptsjournaljournal

SalesSalesjournaljournal

AcquisitionsAcquisitionsjournaljournal

JournalsJournals

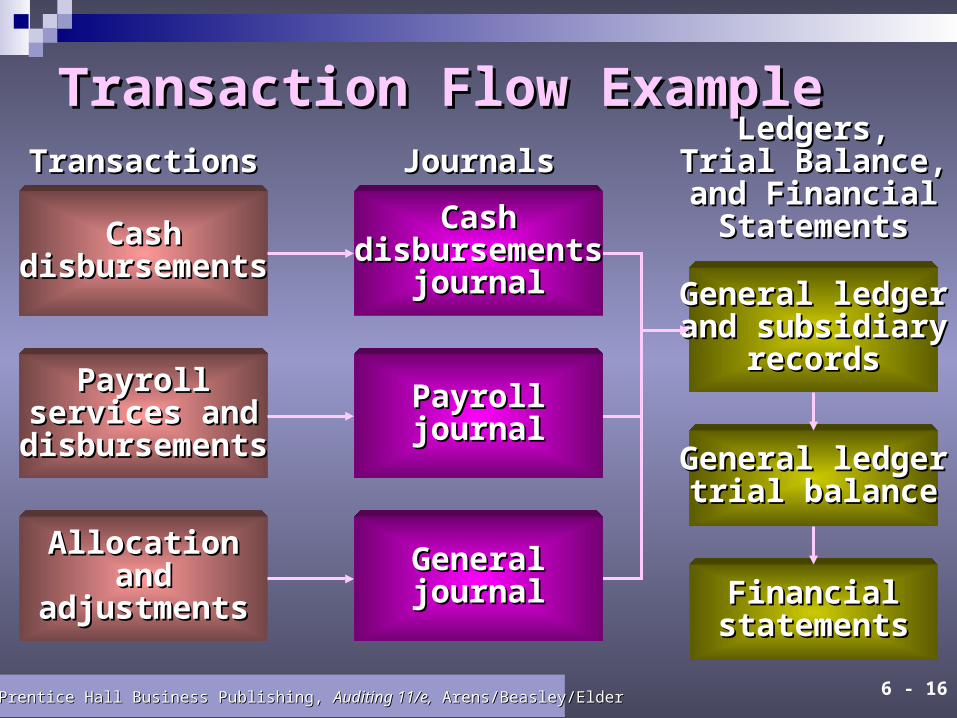

6 - 16©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Transaction Flow ExampleTransaction Flow Example

AllocationAllocationandand

adjustmentsadjustments

CashCashdisbursementsdisbursements

PayrollPayrollservices andservices and

disbursementsdisbursements

Ledgers,Ledgers,Trial Balance,Trial Balance,and Financialand FinancialStatementsStatements

General ledgerGeneral ledgerand subsidiaryand subsidiary

recordsrecords

General ledgerGeneral ledgertrial balancetrial balance

FinancialFinancialstatementsstatements

TransactionsTransactions

PayrollPayrolljournaljournal

CashCashdisbursementsdisbursements

journaljournal

GeneralGeneraljournaljournal

JournalsJournals

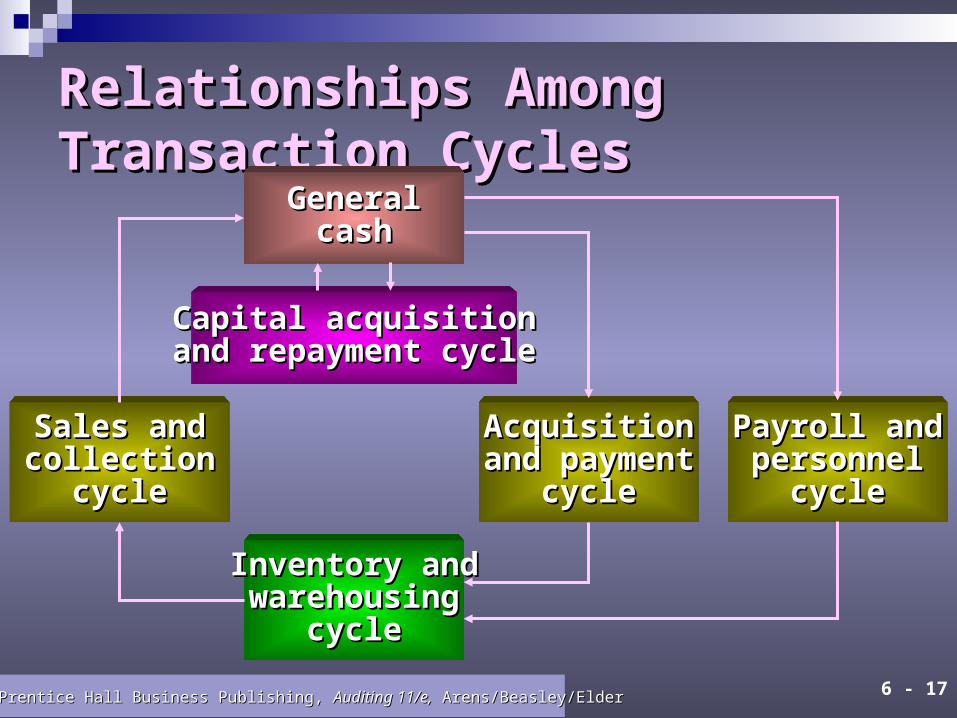

6 - 17©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Relationships Among Transaction Relationships Among Transaction CyclesCycles

GeneralGeneralcashcash

Capital acquisitionCapital acquisitionand repayment cycleand repayment cycle

Sales andSales andcollectioncollection

cyclecycle

AcquisitionAcquisitionand paymentand payment

cyclecycle

Payroll andPayroll andpersonnelpersonnel

cyclecycle

Inventory andInventory andwarehousingwarehousing

cyclecycle

6 - 18©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 5Learning Objective 5

Describe why the auditor obtainsDescribe why the auditor obtains

a combination of assurance bya combination of assurance by

auditing class of transactions andauditing class of transactions and

ending balances in accounts.ending balances in accounts.

6 - 19©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

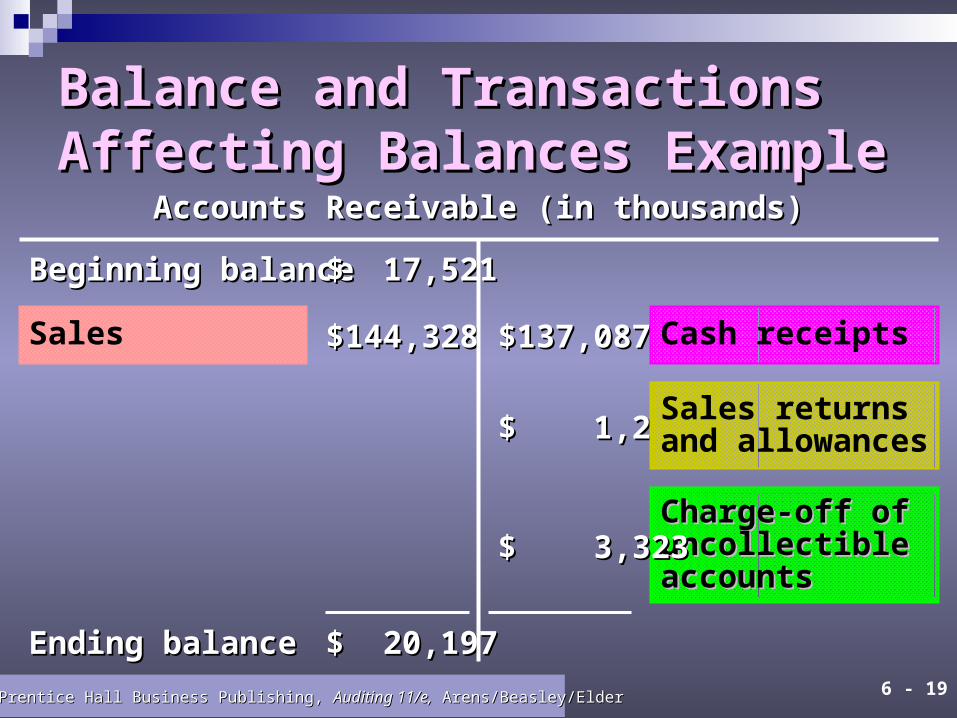

Balance and Transactions Balance and Transactions Affecting Balances ExampleAffecting Balances Example

Beginning balanceBeginning balance

Sales

$ 17,521$ 17,521

$144,328$144,328 $137,087$137,087 Cash receipts

$ 1,242$ 1,242Sales returnsand allowances

Charge-off ofCharge-off ofuncollectibleuncollectibleaccountsaccounts

Ending balanceEnding balance $ 20,197$ 20,197

$ 3,323$ 3,323

Accounts Receivable (in thousands)Accounts Receivable (in thousands)

6 - 20©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 6Learning Objective 6

Distinguish among the fiveDistinguish among the five

categories of managementcategories of management

assertions about financialassertions about financial

information.information.

6 - 21©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

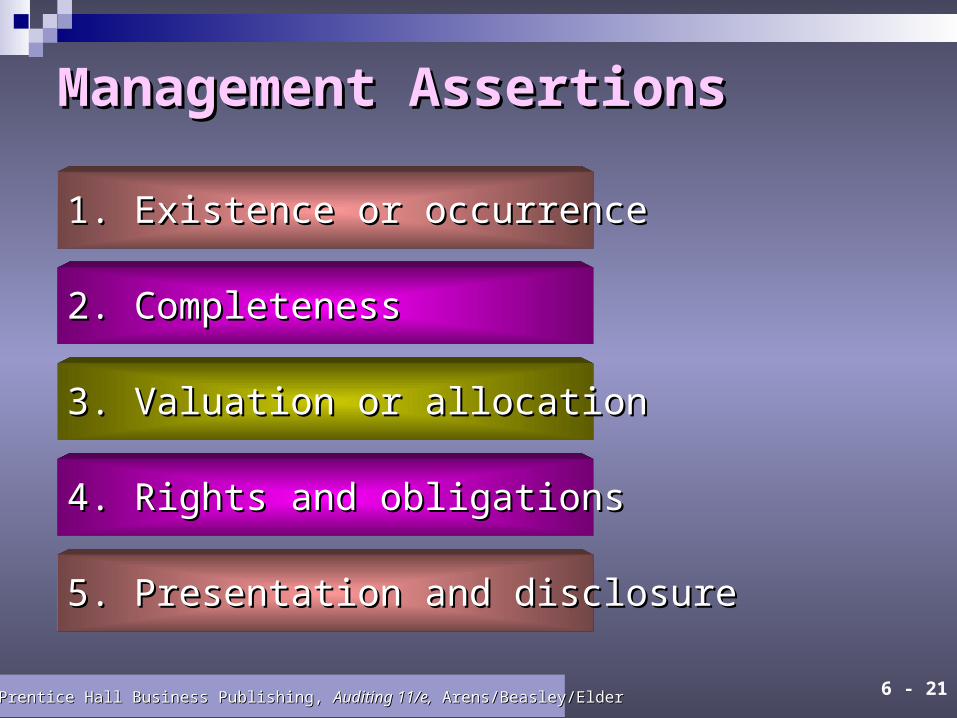

Management AssertionsManagement Assertions

1. Existence or occurrence1. Existence or occurrence

2. Completeness2. Completeness

3. Valuation or allocation3. Valuation or allocation

4. Rights and obligations4. Rights and obligations

5. Presentation and disclosure5. Presentation and disclosure

6 - 22©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 7Learning Objective 7

Link the six general transaction-Link the six general transaction-

related audit objectives to therelated audit objectives to the

five management assertions.five management assertions.

6 - 23©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

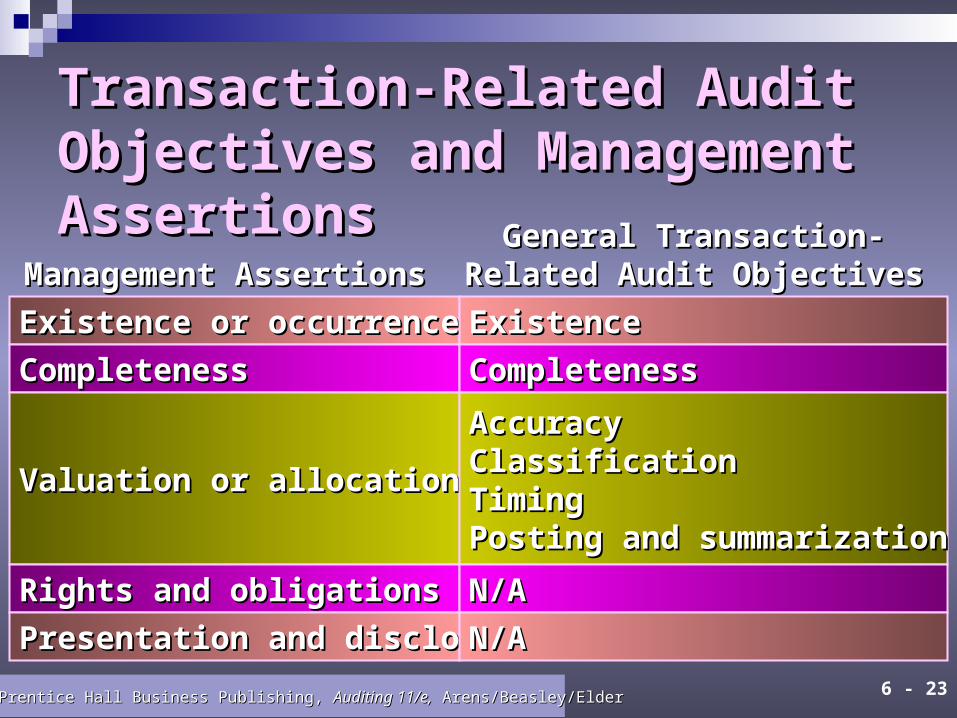

Transaction-Related Audit Transaction-Related Audit Objectives and Management Objectives and Management AssertionsAssertions

Management AssertionsManagement AssertionsGeneral Transaction-General Transaction-

Related Audit ObjectivesRelated Audit Objectives

Existence or occurrenceExistence or occurrence

CompletenessCompleteness

Valuation or allocationValuation or allocation

ExistenceExistence

CompletenessCompleteness

AccuracyAccuracyClassificationClassificationTimingTimingPosting and summarizationPosting and summarization

Rights and obligationsRights and obligations

Presentation and disclosurePresentation and disclosure

N/AN/A

N/AN/A

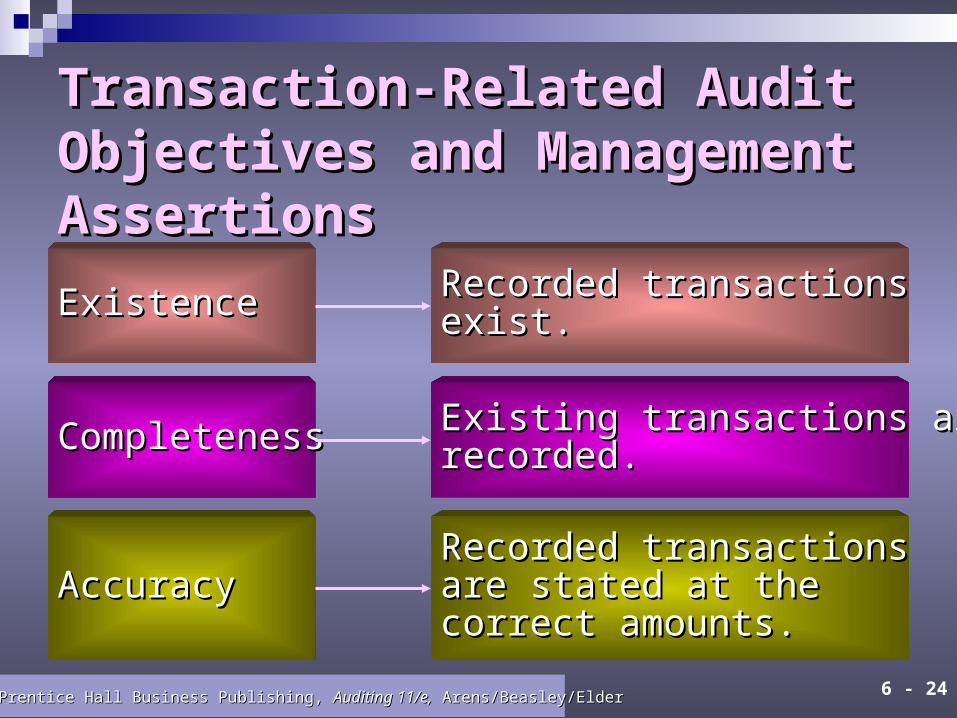

6 - 24©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

ExistenceExistence Recorded transactionsRecorded transactionsexist.exist.

CompletenessCompleteness Existing transactions areExisting transactions arerecorded.recorded.

AccuracyAccuracyRecorded transactionsRecorded transactionsare stated at theare stated at thecorrect amounts.correct amounts.

Transaction-Related Audit Transaction-Related Audit Objectives and Management Objectives and Management AssertionsAssertions

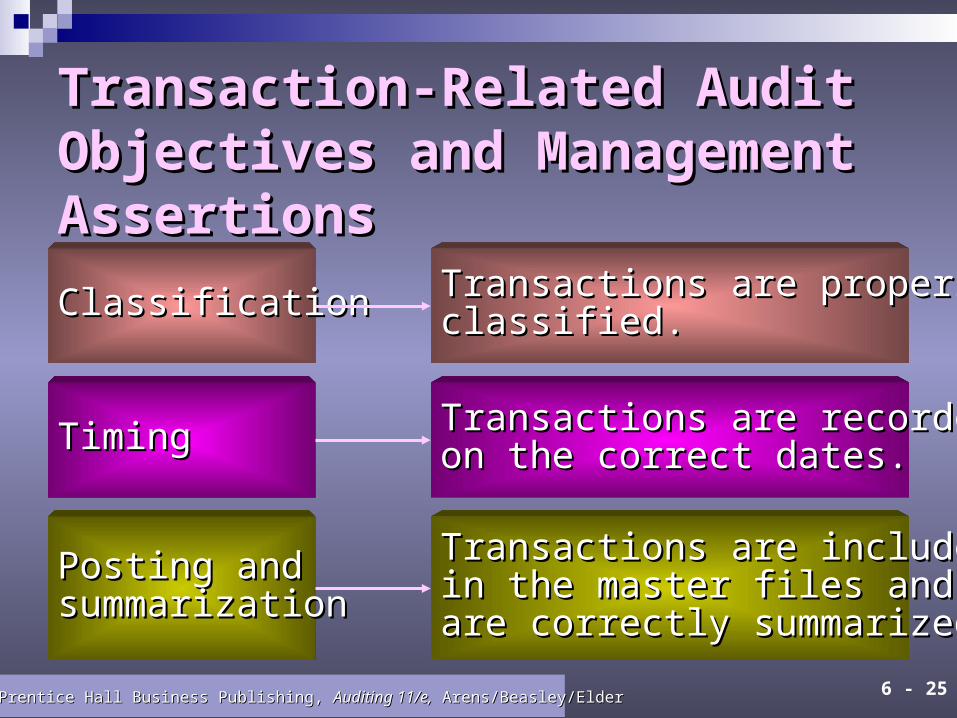

6 - 25©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

ClassificationClassification Transactions are properlyTransactions are properlyclassified.classified.

TimingTiming Transactions are recordedTransactions are recordedon the correct dates.on the correct dates.

Posting andPosting andsummarizationsummarization

Transactions are includedTransactions are includedin the master files andin the master files andare correctly summarized.are correctly summarized.

Transaction-Related Audit Transaction-Related Audit Objectives and Management Objectives and Management AssertionsAssertions

6 - 26©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 8Learning Objective 8

Link the nine general balance-Link the nine general balance-

related audit objectives to therelated audit objectives to the

five management assertions.five management assertions.

6 - 27©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

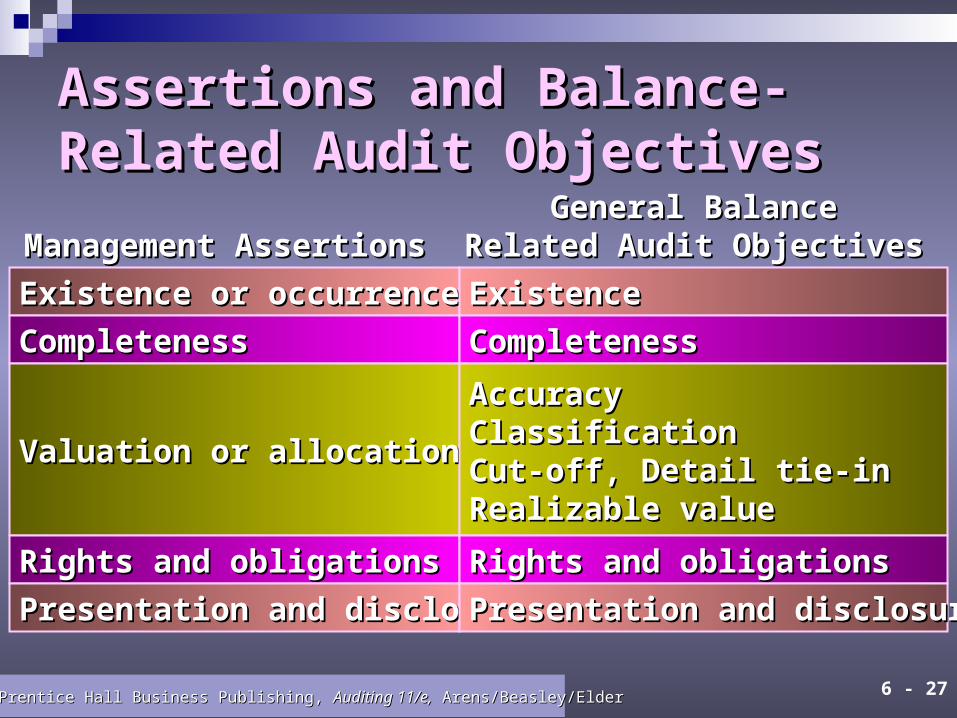

Assertions and Balance-Related Assertions and Balance-Related Audit ObjectivesAudit Objectives

Management AssertionsManagement AssertionsGeneral BalanceGeneral Balance

Related Audit ObjectivesRelated Audit Objectives

Existence or occurrenceExistence or occurrence

CompletenessCompleteness

Valuation or allocationValuation or allocation

ExistenceExistence

CompletenessCompleteness

AccuracyAccuracyClassificationClassificationCut-off, Detail tie-inCut-off, Detail tie-inRealizable valueRealizable value

Rights and obligationsRights and obligations

Presentation and disclosurePresentation and disclosure

Rights and obligationsRights and obligations

Presentation and disclosurePresentation and disclosure

6 - 28©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

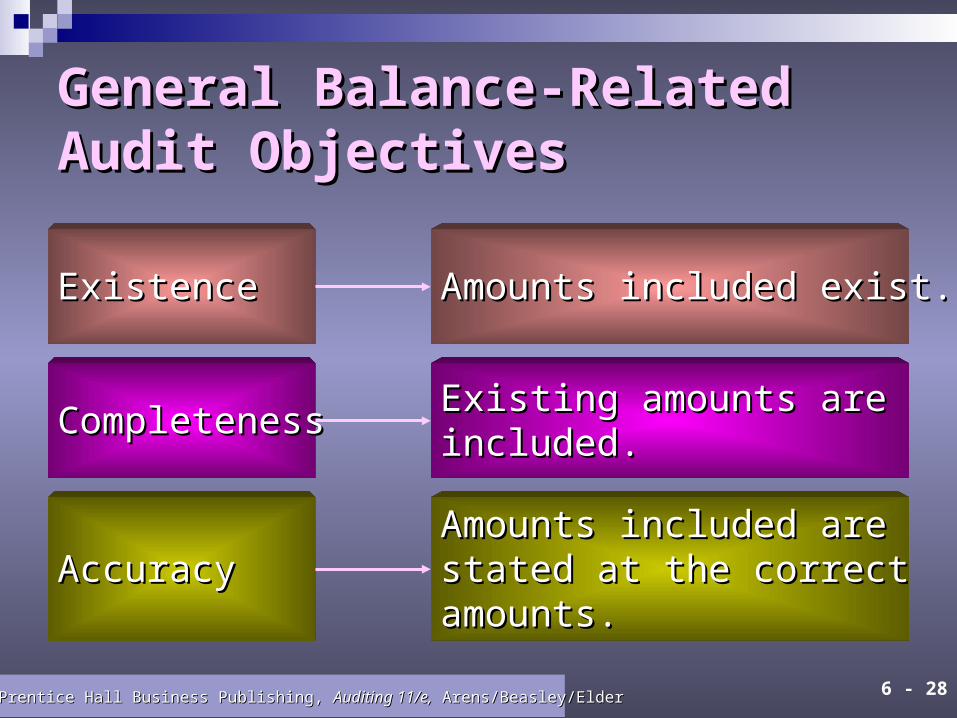

ExistenceExistence Amounts included exist.Amounts included exist.

CompletenessCompleteness Existing amounts areExisting amounts areincluded.included.

AccuracyAccuracyAmounts included areAmounts included arestated at the correctstated at the correctamounts.amounts.

General Balance-RelatedGeneral Balance-RelatedAudit ObjectivesAudit Objectives

6 - 29©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

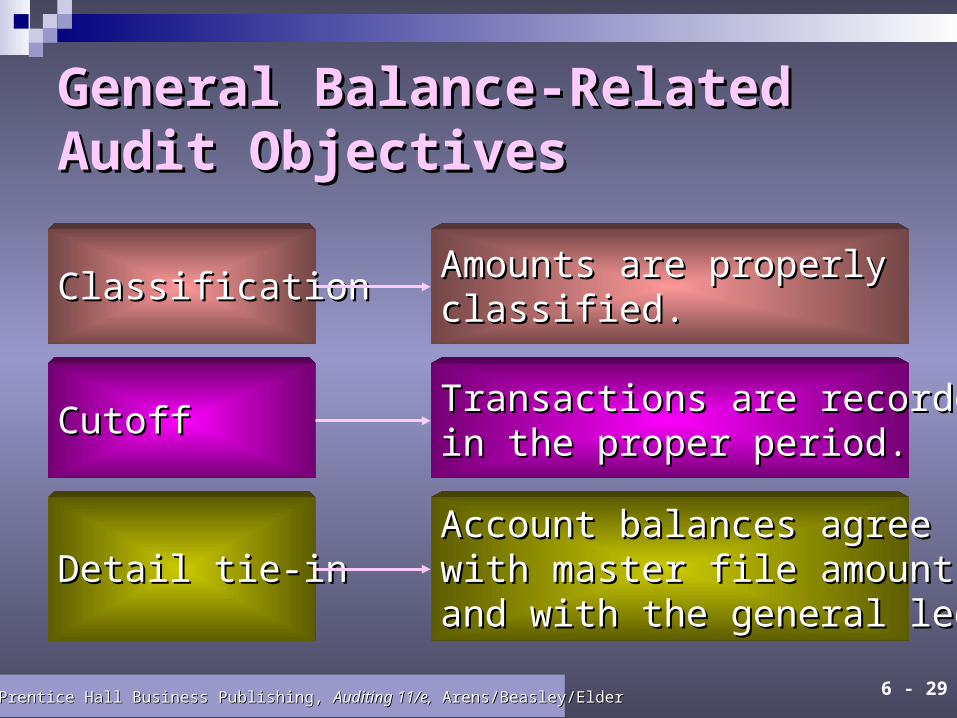

ClassificationClassification Amounts are properlyAmounts are properlyclassified.classified.

CutoffCutoff Transactions are recordedTransactions are recordedin the proper period.in the proper period.

Detail tie-inDetail tie-inAccount balances agreeAccount balances agreewith master file amounts,with master file amounts,and with the general ledger.and with the general ledger.

General Balance-RelatedGeneral Balance-RelatedAudit ObjectivesAudit Objectives

6 - 30©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

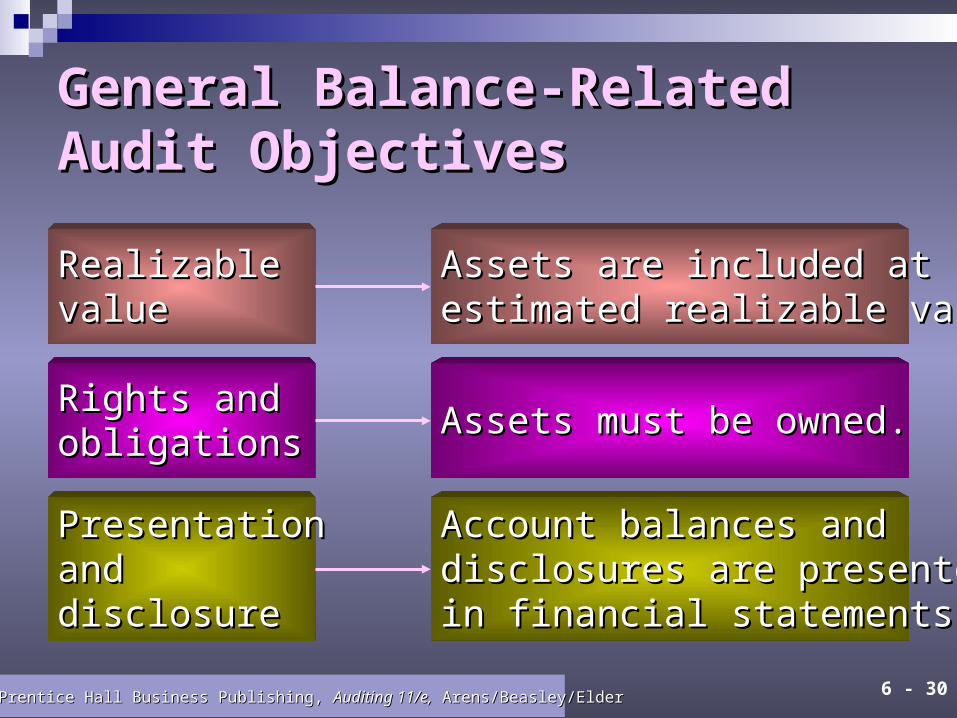

RealizableRealizablevaluevalue

Assets are included atAssets are included atestimated realizable value.estimated realizable value.

Rights andRights andobligationsobligations Assets must be owned.Assets must be owned.

PresentationPresentationandanddisclosuredisclosure

Account balances andAccount balances anddisclosures are presenteddisclosures are presentedin financial statements.in financial statements.

General Balance-RelatedGeneral Balance-RelatedAudit ObjectivesAudit Objectives

6 - 31©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

Learning Objective 9Learning Objective 9

Explain the relationship betweenExplain the relationship between

audit objectives and theaudit objectives and the

accumulation of audit evidence.accumulation of audit evidence.

6 - 32©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

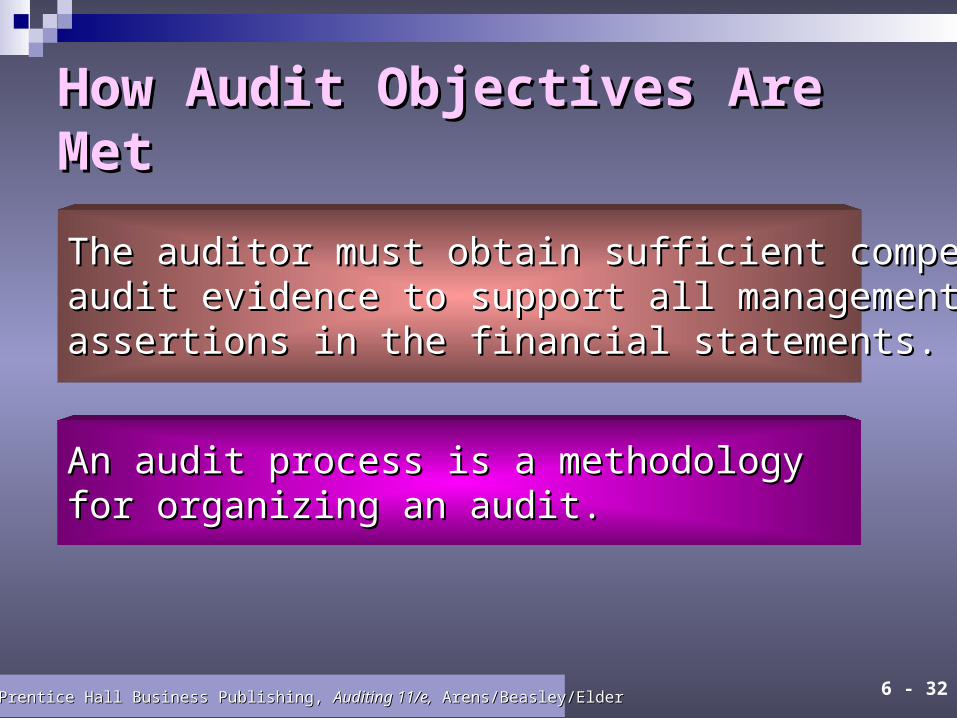

How Audit Objectives Are MetHow Audit Objectives Are Met

The auditor must obtain sufficient competentThe auditor must obtain sufficient competentaudit evidence to support all managementaudit evidence to support all managementassertions in the financial statements.assertions in the financial statements.

An audit process is a methodologyAn audit process is a methodologyfor organizing an audit.for organizing an audit.

6 - 33©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

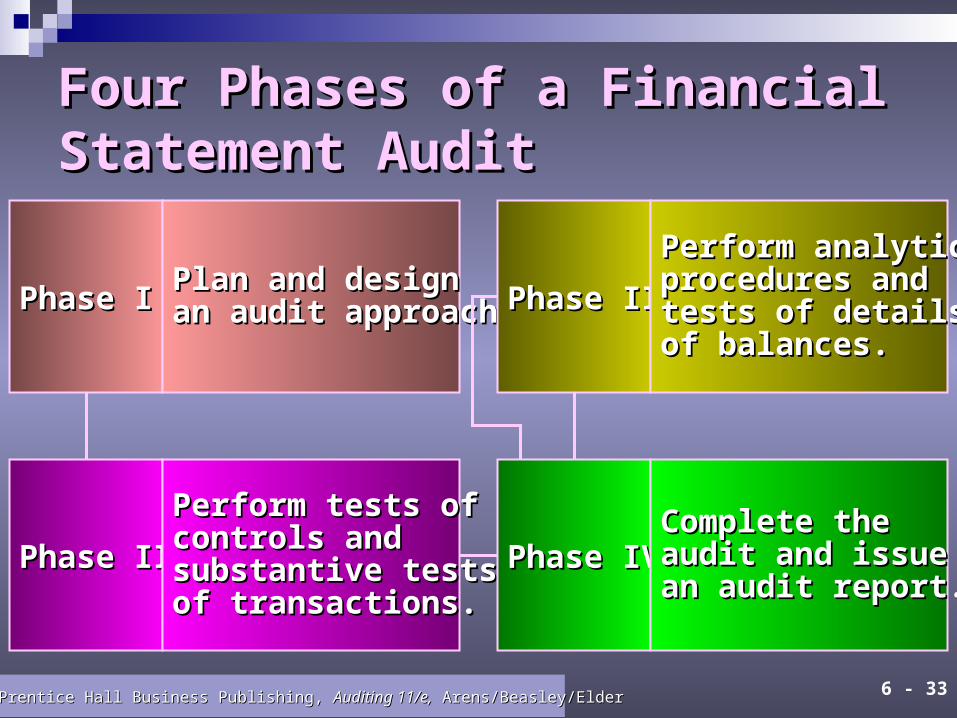

Four Phases of a Financial Four Phases of a Financial Statement AuditStatement Audit

Phase IPhase IPlan and designPlan and designan audit approach.an audit approach.

Phase IIPhase II

Perform tests ofPerform tests ofcontrols andcontrols andsubstantive testssubstantive testsof transactions.of transactions.

Phase IIIPhase III

Perform analyticalPerform analyticalprocedures andprocedures andtests of detailstests of detailsof balances.of balances.

Phase IVPhase IVComplete theComplete theaudit and issueaudit and issuean audit report.an audit report.

6 - 34©2006 Prentice Hall Business Publishing, ©2006 Prentice Hall Business Publishing, Auditing 11/e,Auditing 11/e, Arens/Beasley/Elder Arens/Beasley/Elder

End of Chapter 6End of Chapter 6