Embed Size (px)

Citation preview

Treasury Operations Basics 1

BAS-BN202

Treasury Operations Basics

Treasury Operations Basics 2

Table of Contents

Basic – Treasury Operations.................................................................................................. 4 1. Introduction to Treasury Operations .................................................................................. 4

1.1 Understanding Treasury Operations .................................................................................. 4

1.2 Structure and Functions of Treasury Management ........................................................... 8

1.3 Role and Functions of Front, Mid and Back Office of Integrated Treasury Department . 9

1.4 Treasury Control Framework ........................................................................................... 12

2. Macroeconomic Policy ...................................................................................................... 17

2.1 GDP / GNP ......................................................................................................................... 17

2.2 Inflation ............................................................................................................................. 18

2.3 Interest Rates .................................................................................................................... 19

2.4 Exchange Rate: .................................................................................................................. 20

2.5 Macroeconomic Policies – Monetary and Fiscal Policies ................................................ 20

2.6 Monetary and Fiscal Policies ............................................................................................ 22

2.7 Monetary policy and interest rates.................................................................................. 24

3. Treasury markets and instruments ................................................................................... 26

3.1 Money Market Instruments ............................................................................................. 26

3.2 Coupon Bearing Instruments ............................................................................................ 27

3.3 Discount Instruments ....................................................................................................... 27

3.4 Fixed income instruments ................................................................................................ 28

3.5 Participants in fixed income markets .............................................................................. 29

3.6 Government Securities ..................................................................................................... 30

3.7 Corporate Debt Markets ................................................................................................... 31

3.8 Credit Rating and its importance ..................................................................................... 31

3.9 Trading in fixed income securities ................................................................................... 33

3.10 Bond Mathematics – Yield, Duration, Convexity, Bond Prices and Interest Rates ........ 33

3.11 Cost of Funds ..................................................................................................................... 48

3.12 Managing Investment Portfolio and Trading Portfolio ................................................... 49

3.13 Derivatives in Fixed Income Markets – Forwards, Futures, Options and Swaps ........... 50

4. Foreign Exchange Markets – Introduction ........................................................................ 59

4.1 Overview of Global Forex Markets .................................................................................. 59

4.2 Products and Participants in Foreign Exchange Markets ................................................ 60

Treasury Operations Basics 3

4.3 Spot and forward markets................................................................................................ 61

4.4 Foreign Exchange Arithmetic – Rate Computations ........................................................ 65

4.5 Factors affecting Foreign Exchange Market ..................................................................... 69

5. Asset Liability Management – Overview ........................................................................... 71

5.1 Product Pricing and Performance Management, Interest Rate Risk for Asset Liability

Management ..................................................................................................................... 71

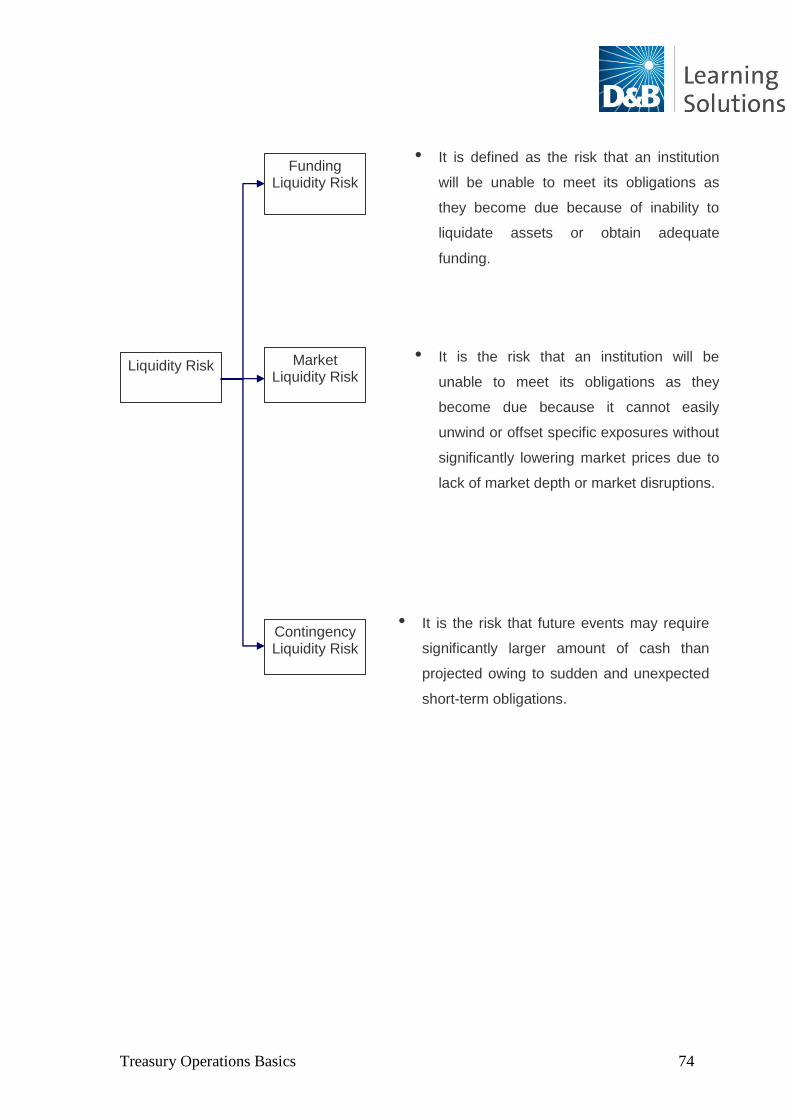

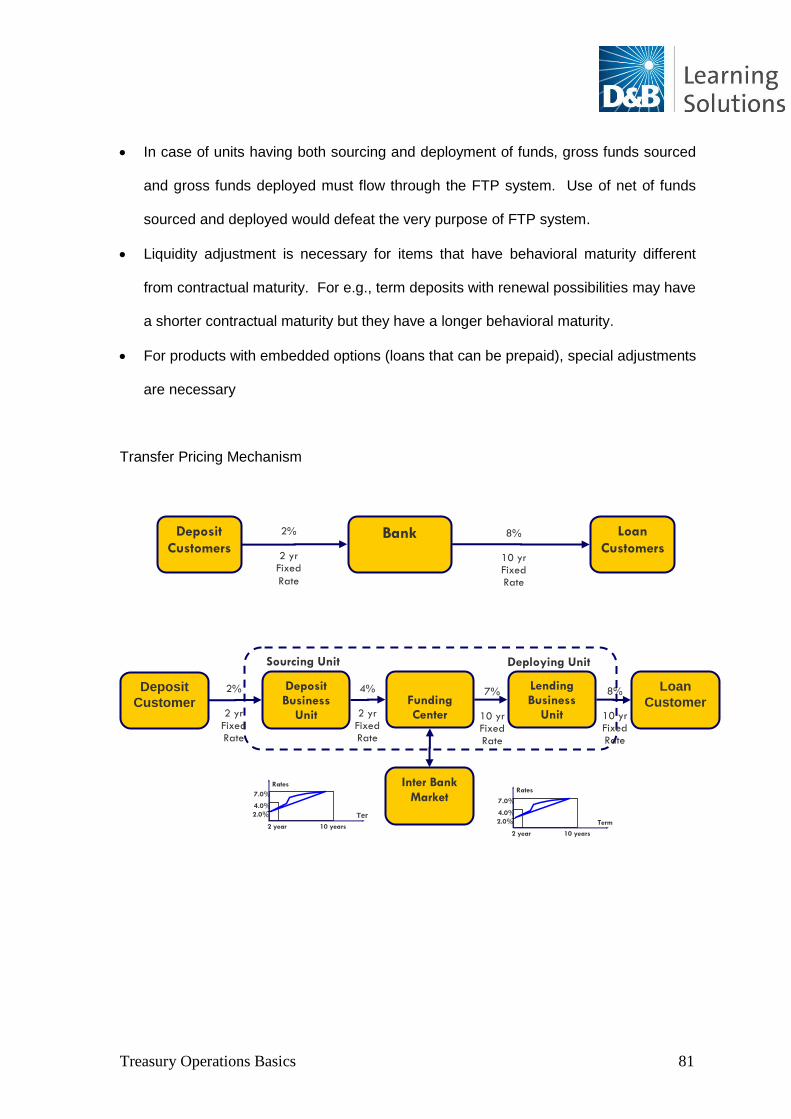

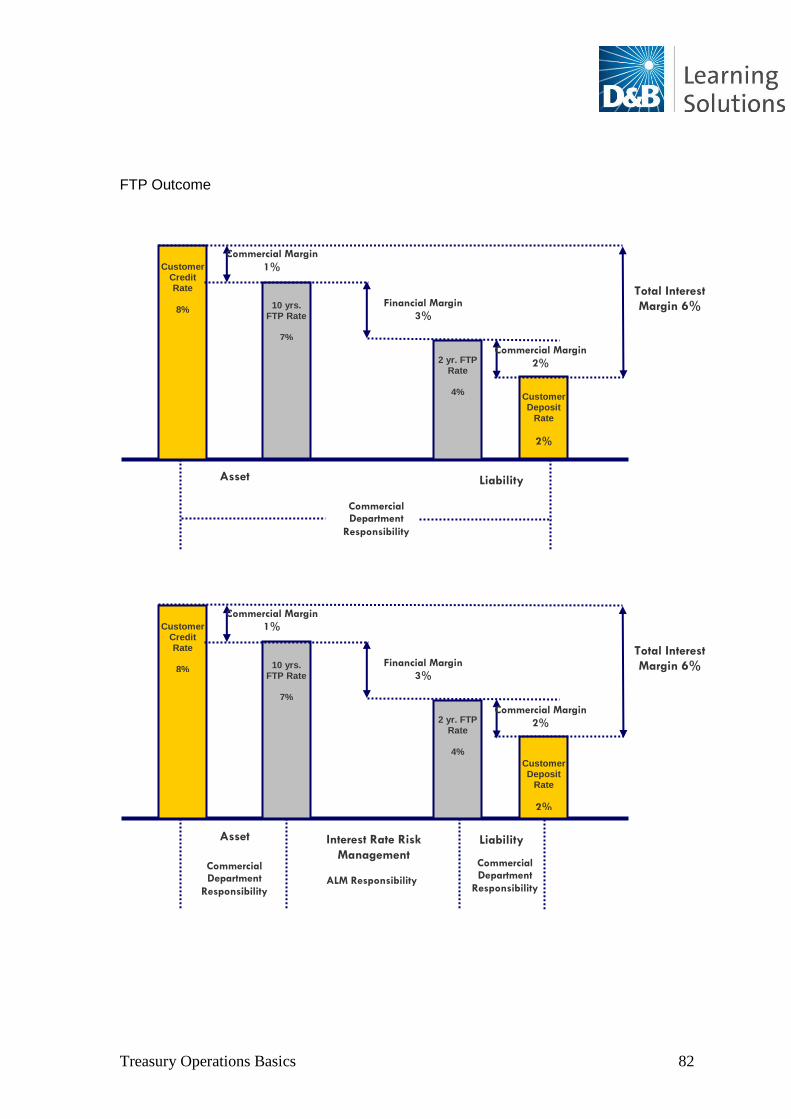

5.2 Liquidity Risk in Asset Liability Management, Transfer Pricing ...................................... 73

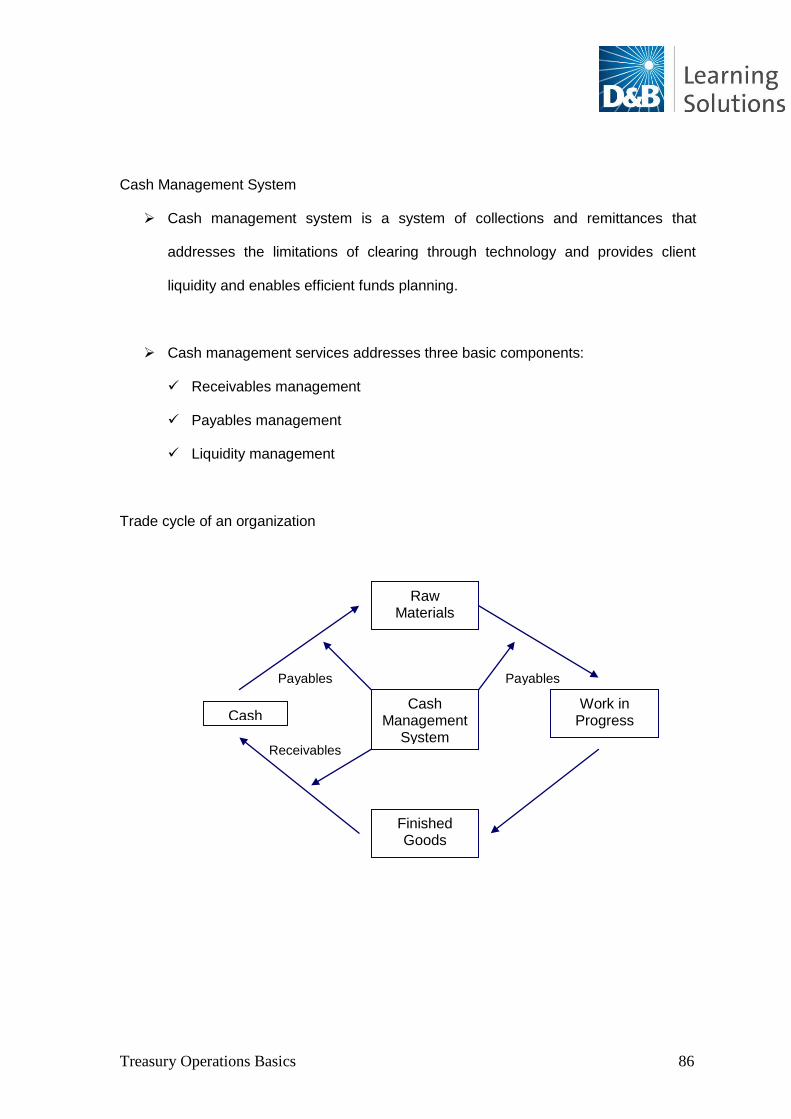

6. Cash Management............................................................................................................. 84

6.1 Cash Flow Dynamics, Forecasting and Valuation ............................................................ 85

6.2 Short-Term Funding Investments ..................................................................................... 87

6.3 Cash Management Techniques ........................................................................................ 88

6.4 Sales Cash Conversion Cycle (SCCC) ................................................................................. 89

6.5 Cash Budget ...................................................................................................................... 89

Treasury Operations Basics 4

Basic – Treasury Operations

1. Introduction to Treasury Operations

Chapter objectives:

1. To introduce the concept of treasury operations

2. To understand the structure and functions of treasury management

3. To comprehend the role and functions of front, mid and back office of integrated

treasury department

4. To understand the framework of treasury control

Treasury operations refer to all activities related to management of cash inflows and

outflows of all organizations. Treasury is a special term within a compass of the broader

term finance. The basis of treasury operations is money and near-money assets such as

money market instruments, derivatives, bonds and securities. The money in terms of

foreign currencies is traded in the forex or foreign exchange market.

1.1 Understanding Treasury Operations

Treasury operations include management of an organization‟s investible surpluses,

which in turn include trading in bonds, currencies, derivatives and associated risk

management. Treasury operations are prevalent across all types of organizations, e.g.,

corporations, banks, financial institutions, insurance companies, asset management

companies, etc. Typically, in a bank or financial institutions, the person in charge of the

treasury is called Treasurer and in a non-financial organization or corporations, the Chief

Financial Officer or Director – Finance is typically in charge of the treasury and he/she

also manages the finance department.

Treasury Operations Basics 5

In a bank, treasury operations typically comprise the following business lines:

Proprietary Trading – Proprietary trading comprises trading in financial instruments

such as equities, bonds, currencies and the derivatives thereof for the bank‟s own

portfolio within regulatory restrictions.

Balance Sheet Management – Balance sheet management comprises trading and

investments in financial instruments keeping in mind the objective of asset liability

management for the bank, i.e., managing the interest rate and liquidity risks.

Corporate Sales – Corporate sales, as the name suggests, comprises all the treasury

financial transactions, e.g., buying and selling of currencies, bonds and derivatives

with the bank‟s institutional clients (typically corporations), based on their specific

trade, commerce and treasury requirements.

Inter-Bank dealings – Inter-Bank dealings are typically dealings with banks and

financial institutions with the main objective of trading or hedging corporate sales

transactions either back-to-back or otherwise.

Treasury Operations Basics 6

In a corporation, treasury operations would typically comprise the following business

lines:

Banking and Cash Management – Banking and cash management includes

management of bank accounts including account administration and user

authorization, negotiation of contracts for various products and services based on the

corporation‟s industry and ongoing monitoring of activity to ensure optimal pricing

and consistent service levels. It also includes review and validation of daily bank

transactions, initiation of wire transfers and transactions as necessary and long-term

and daily cash forecasting, including daily evaluation of cash positions to ensure

appropriate investment of funds.

Investments – Managing and monitoring investments of surplus investible funds

based on working capital requirement or operating funds based on short-term,

medium-term and long-term objectives. Investments to comply with all policies

adopted by the board and all other regulatory compliances. They also need to adhere

to all generally accepted accounting principles.

Debt servicing – Debt servicing includes managing or monitoring servicing of all

existing or future debts of the corporation including managing or monitoring all

registration, payment and transfer activities.

Treasury Operations Basics 7

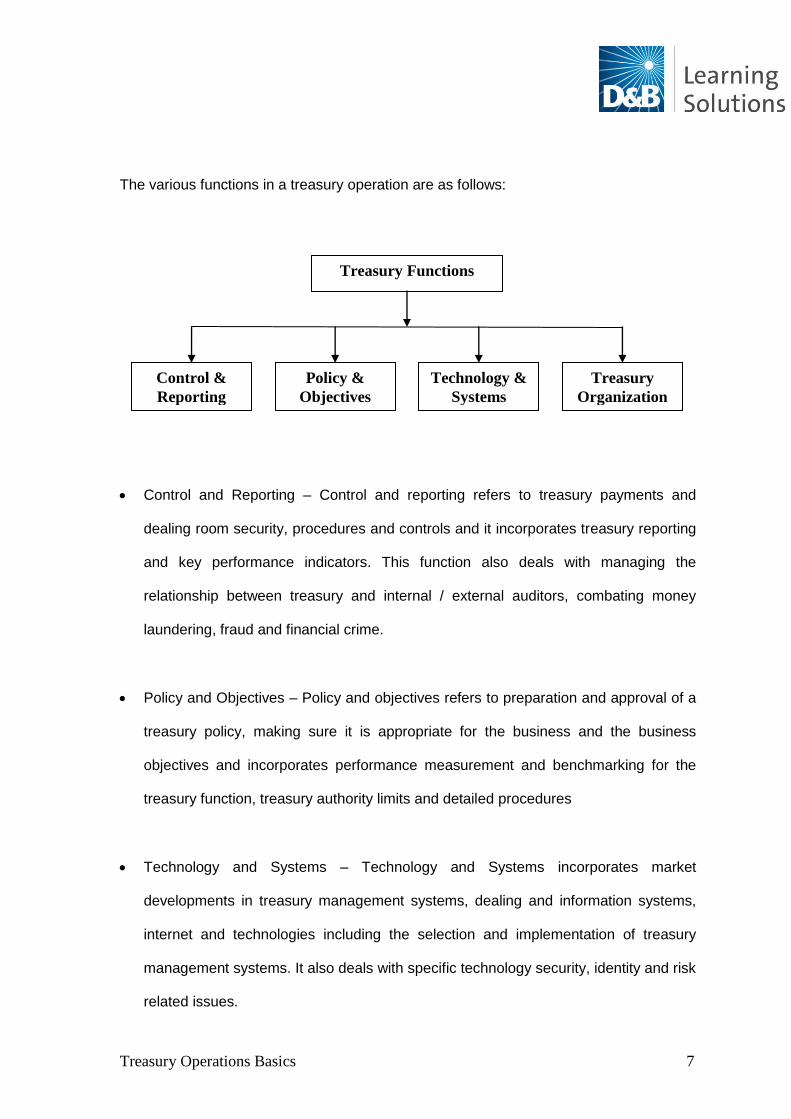

The various functions in a treasury operation are as follows:

Control and Reporting – Control and reporting refers to treasury payments and

dealing room security, procedures and controls and it incorporates treasury reporting

and key performance indicators. This function also deals with managing the

relationship between treasury and internal / external auditors, combating money

laundering, fraud and financial crime.

Policy and Objectives – Policy and objectives refers to preparation and approval of a

treasury policy, making sure it is appropriate for the business and the business

objectives and incorporates performance measurement and benchmarking for the

treasury function, treasury authority limits and detailed procedures

Technology and Systems – Technology and Systems incorporates market

developments in treasury management systems, dealing and information systems,

internet and technologies including the selection and implementation of treasury

management systems. It also deals with specific technology security, identity and risk

related issues.

Treasury Functions

Control &

Reporting

Policy &

Objectives

Technology &

Systems

Treasury

Organization

Treasury Operations Basics 8

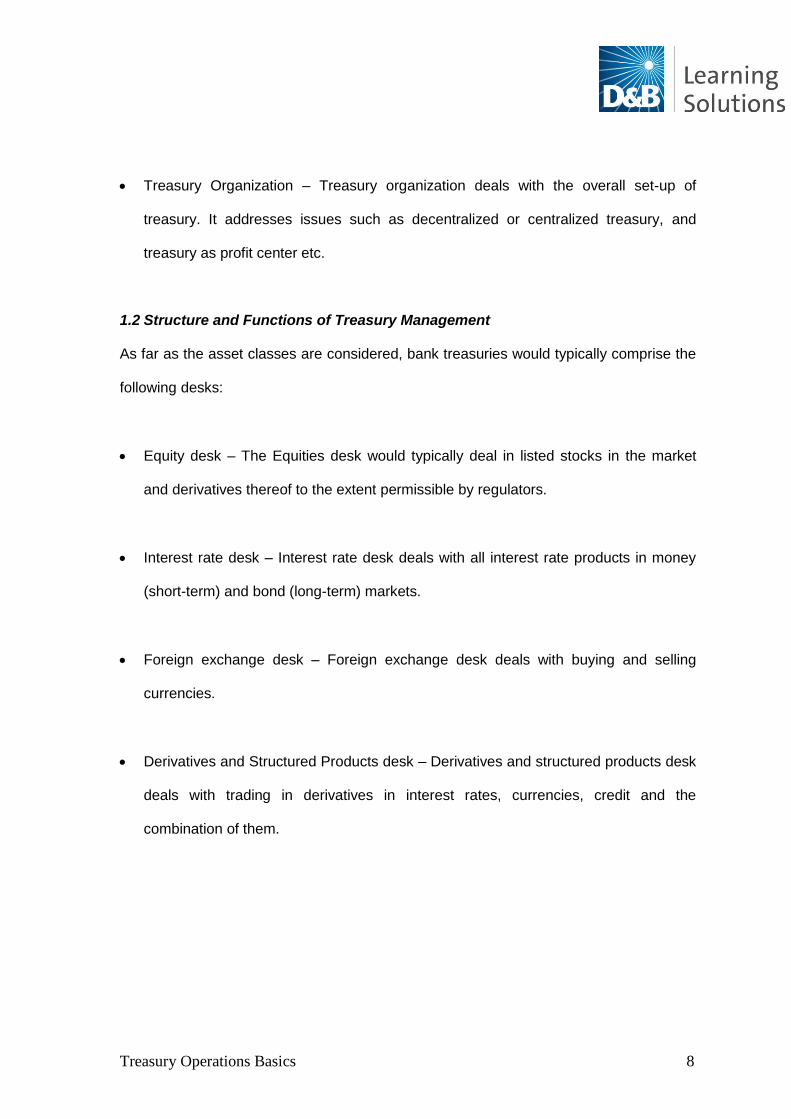

Treasury Organization – Treasury organization deals with the overall set-up of

treasury. It addresses issues such as decentralized or centralized treasury, and

treasury as profit center etc.

1.2 Structure and Functions of Treasury Management

As far as the asset classes are considered, bank treasuries would typically comprise the

following desks:

Equity desk – The Equities desk would typically deal in listed stocks in the market

and derivatives thereof to the extent permissible by regulators.

Interest rate desk – Interest rate desk deals with all interest rate products in money

(short-term) and bond (long-term) markets.

Foreign exchange desk – Foreign exchange desk deals with buying and selling

currencies.

Derivatives and Structured Products desk – Derivatives and structured products desk

deals with trading in derivatives in interest rates, currencies, credit and the

combination of them.

Treasury Operations Basics 9

1.3 Role and Functions of Front, Mid and Back Office of Integrated Treasury

Department

Front Office

Front office department in an integrated treasury function is essentially the group that

initiates a financial transaction. Front office undertakes hedging and financing, which

includes investments, position management, trading and arbitrage.

Some of the important functions of the front office are:

Sales and trading – The primary function of the front office is buying and selling

products on behalf of the organization or its clients. Traders buy and sell financial

products in the market with the goal of earning profit on each trade. The

salesperson‟s job is to suggest trading ideas to the clients and take orders on their

behalf.

Corporate finance – This function involves helping customers raise funds in capital

markets. This division is generally divided into industry coverage and product

coverage groups. Industry coverage groups focus on a specific industry whereas

product coverage groups focus on various types of financial products.

Treasury Desks

Equity

Interest Rates

Foreign

Exchange

Derivatives &

Structured

Products

Treasury Operations Basics 10

Research – This function involves reviewing companies and writing reports about

their prospects with recommendations. This group has also been involved in

research for specific financial markets like equity, interest rates, forex, and credit. It

assists the traders in trading, the sales force in suggesting ideas to customers and

helps the corporate finance people by covering their clients.

Mid Office

Mid office department in an integrated treasury function is essentially the group that is

responsible for control, compliance and risk management for the treasury. The functions

involve valuations and collateral management of the treasury portfolio of the

organization. Mid office also ensures compliance of the organization‟s treasury and risk

policies. It essentially ensures control and processing of transactions.

Some of the important functions of the mid office are:

Financial control – This function tracks and analyzes the capital flows of the firm,

acting as the principal adviser to senior management on areas like controlling the

firm‟s global risk exposure and profitability of the various lines of business. Valuation

and collateral management, including margining, is a sub-function of financial control.

Front Office

Sales & Trading Corporate

Finance

Research

Treasury Operations Basics 11

Compliance and Asset Liability Management – This function is responsible for the

organization‟s daily operations compliance with regulations, both external and

internal and is also responsible for monitoring asset liability management for the

organization.

Risk Management – This function involves analyzing market, credit and operational

risks that sales and trading are taking onto the balance sheet, setting limits on the

amount of capital that they are able to trade and ensuring that all economic risks are

captured accurately, correctly and on time.

Back Office

The back office department in an integrated treasury function is essentially the group that

monitors post-trade processing of transactions. It is responsible for confirmation,

payment, settlement and accounting of all treasury transactions of the organization,

whether banking or corporate. It also ensures the treasury regulatory compliance

required by regulators. Further, it is responsible for managing all ancillary functions such

as reconciliations and documentations for the treasury function.

Mid Office

Financial Control Compliance and

Asset Liability

Management

Risk

Management

Treasury Operations Basics 12

Some of the important functions of the back office are:

Operations – This function involves validating trades that have been executed,

ensuring that they are not erroneous and transacting the required transfers.

Operations include various sub-functions like reconciliations, confirmation, payment,

settlement, documentation and accounting.

Technology – This function manages all the information technology requirements of

the treasury, including management of in-house software with technical support.

1.4 Treasury Control Framework

The treasury front office executives take large positions across asset classes, including

leveraged products such as derivatives. Hence, managements are highly sensitive to

treasury risks as they make significant impact on the organization. The risk of losing

capital is much higher than in the credit business. The conventional control and

supervisory measures, mostly in the nature of preventive steps, may be divided into the

following parts:

Back Office

Operations Technology

Treasury Operations Basics 13

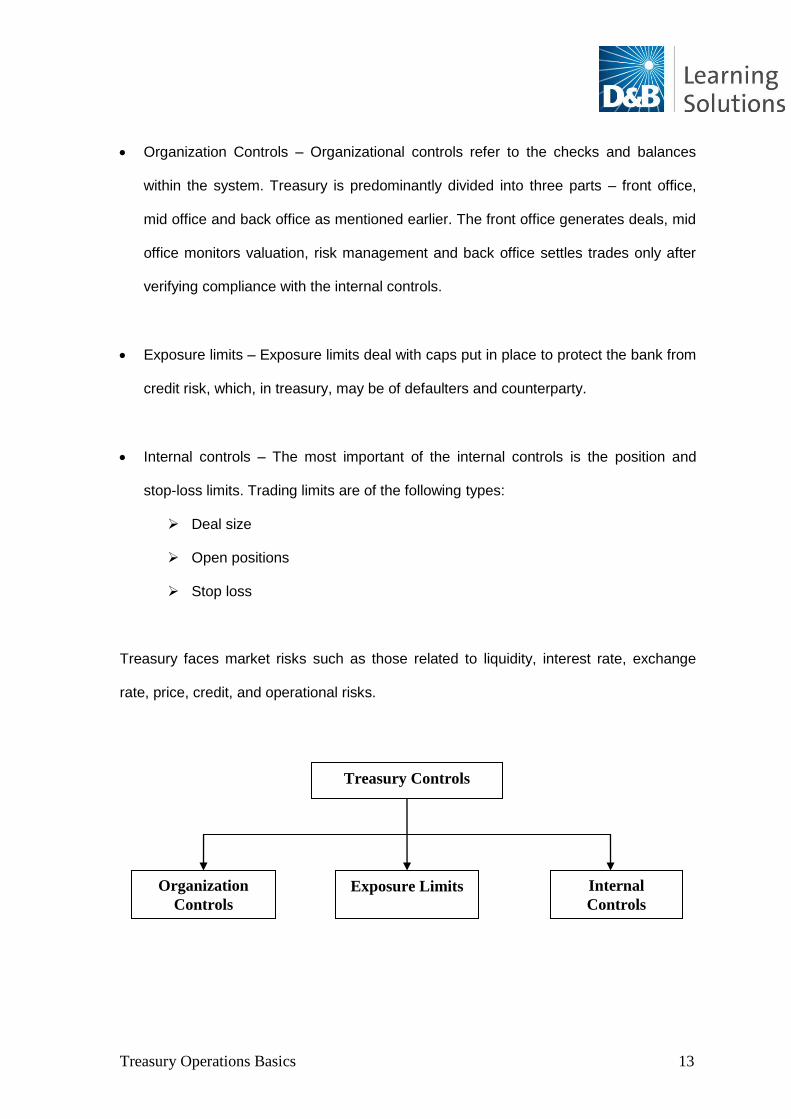

Organization Controls – Organizational controls refer to the checks and balances

within the system. Treasury is predominantly divided into three parts – front office,

mid office and back office as mentioned earlier. The front office generates deals, mid

office monitors valuation, risk management and back office settles trades only after

verifying compliance with the internal controls.

Exposure limits – Exposure limits deal with caps put in place to protect the bank from

credit risk, which, in treasury, may be of defaulters and counterparty.

Internal controls – The most important of the internal controls is the position and

stop-loss limits. Trading limits are of the following types:

Deal size

Open positions

Stop loss

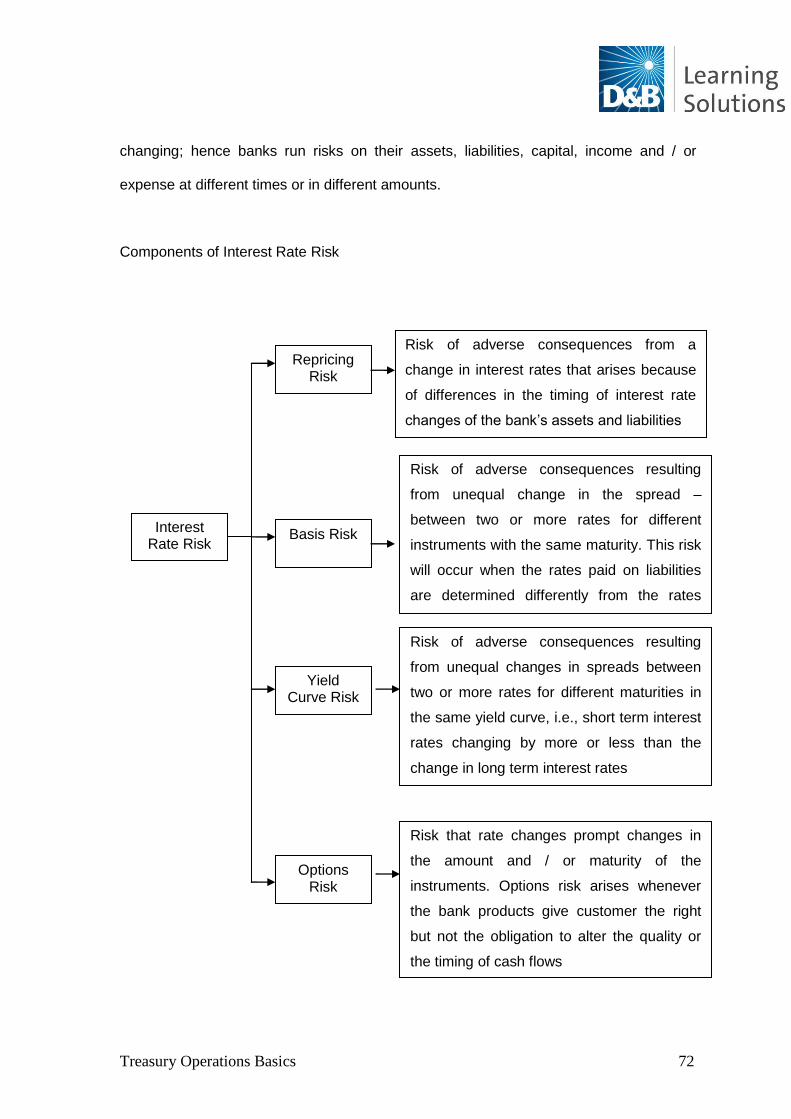

Treasury faces market risks such as those related to liquidity, interest rate, exchange

rate, price, credit, and operational risks.

Treasury Controls

Organization

Controls

Exposure Limits Internal

Controls

Treasury Operations Basics 14

Salient features of the treasury control framework are:

Risk Appetite – An organization‟s risk appetite needs to be decided before designing

an efficient treasury control framework. A tighter control framework is expected to be

around a business that runs a profit centre treasury to make returns rather than a

simpler transaction-based treasury. Differentiation needs to be also made for a

treasury that runs a more manual process compared with a greater level of straight-

through processing.

Governance – The ultimate responsibility for ensuring that an adequate system of

internal controls is established and maintained lies with the board of directors. The

risks the business is facing needs to be understood by senior management. Policies

and procedures need to be developed that reflect that position, articulating the risk

appetite. A policy covering identification, measurement, management, monitoring and

control of financial risk should be approved by the board.

Operating Controls – Following are some of the operating controls that are ideal for

an efficient treasury control function:

o Segregation of duties - Segregation of duties pertaining to front, mid, and back

office is a key element for proper treasury controls. Some of the key duties that

should be properly segregated in a treasury are:

Identification of opportunities and trades

Deal authorization

Confirmations

Settlement authorization

Settlement release

Accounting

Treasury Operations Basics 15

o Dealing - Competitive quotes should be sought in a dealing function. Records of

banks contacted and rates quoted need to be maintained. No one bank or broker

is favored over another and it needs to be ensured that the best returns are being

achieved. The dealer should immediately input deal details into the treasury

management system as soon a deal is struck.

o Access to the front office - Physical access to the dealing room within a treasury

environment is debatable. In a banking environment, it is common to have staff

from the front and back offices physically separated.

o System security - Regular checking of passwords for systems and locking of

computers of unattended personnel is essential. Time-out locks should be

installed, which flag alerts if a machine is not touched for a period of time.

o Confirmations - Back office has the responsibility of confirming details of all

treasury transactions before the settlement is made, to minimize the risk of error

or fraud. An exception report should ideally generate, to show transactions not

being confirmed.

Treasury Operations Basics 16

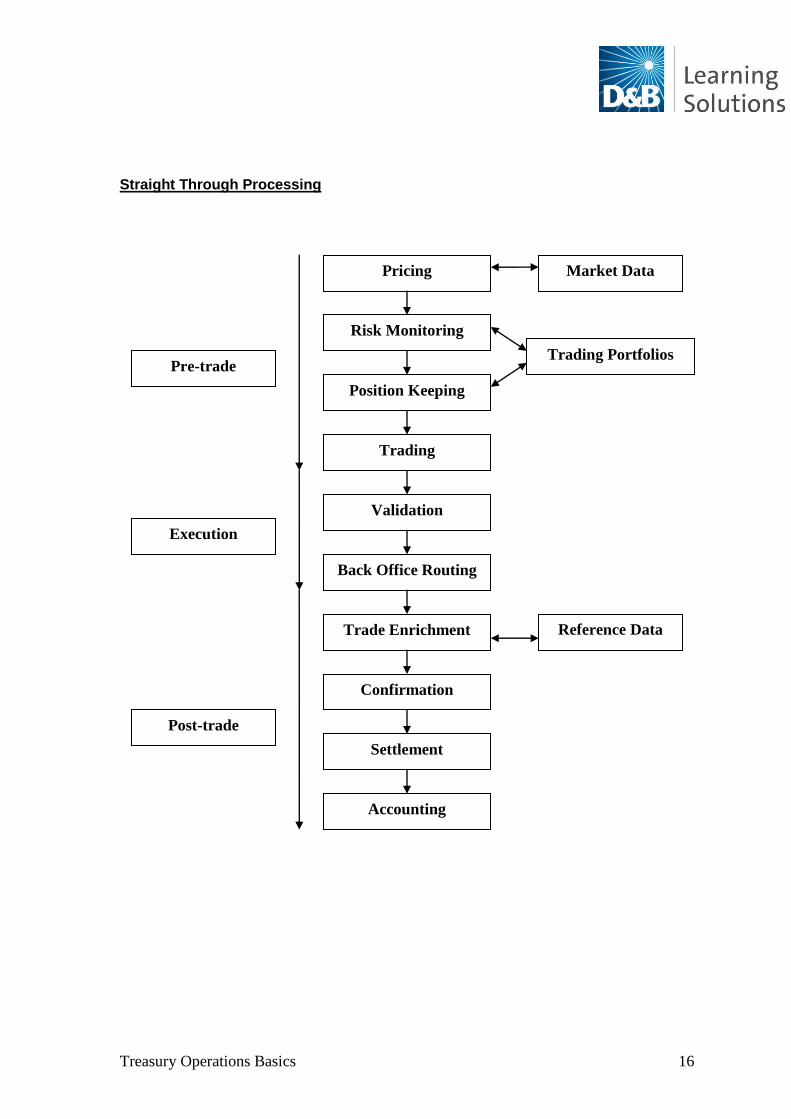

Straight Through Processing

Confirmation

Post-trade

Pre-trade

Position Keeping

Trading

Validation

Back Office Routing

Trade Enrichment

Risk Monitoring

Pricing

Settlement

Accounting

Execution

Market Data

Trading Portfolios

Reference Data

Treasury Operations Basics 17

2. Macroeconomic Policy

Chapter Objective:

1. To understand macroeconomic aggregates

2. To identify the various monetary and fiscal policies

3. To comprehend the macroeconomics and treasury operations

2.1 GDP / GNP

Gross Domestic Product (GDP) is the money value of all final goods and services

produced in a country during a given time period, generally during a year. In estimating

the GDP, we do not differentiate between production carried out by nationals of a given

economy and those of foreign nationals/ firms having manufacturing facilities and service

organizations operating in a country.

Nominal and Real GDP: GDP measured in current market prices is called Nominal GDP.

Real GDP refers to nominal GDP minus inflation rate. In other words, the real GDP

measure provides the quantity of goods and services produced and valued at prices in

the base year rather than current market prices. Real GDP measures actual physical

volume of production.

Gross National Product (GNP) measures the value of output that can be attributed to the

nationals of an economy. It is estimated by deducting the value of the output produced

by foreign firms in that country from the GDP. To this, we add the value of the output the

local firms produced during the same time period in the rest of the world. Such

Treasury Operations Basics 18

information is continuously obtained by the government departments from major

countries of the world.

2.2 Inflation

Inflation basically refers to a rise in general price level. In other words, if the price of one

of the items we are purchasing goes up sharply, we cannot say that there is inflation

present in the economy. We need to, therefore, differentiate between price rise in

individual good and rise in price level of an identified basket of important goods. There

could also be some goods whose prices may be on the decline.

Inflation is sensitive to day-to-day changes that take place in the economy. All changes

would invariably have to be classified into factors that either affect cost of production or

influence demand. The part of inflation resulting from changes that influence cost of

production is known as cost-push inflation. Examples include:

Rise in fuel cost

Increase in input tax rate

Upward revision in duties

Rise in wages/ salaries

Increase in lending rates charged by banks

Increase in transportation costs

Increase in power tariffs and, rentals for office premises etc.

Demand pull inflation is due to the following factors:

Rise in money supply

Spurt in spending on infrastructure

Increase in Foreign Direct Investment

Treasury Operations Basics 19

Rise in income levels of individuals

Panic buying

Artificial supply bottlenecks

Anticipated shortage of essential goods

Deflation: Deflation is a situation in which prices of most goods and services fall over

time so that inflation is negative.

2.3 Interest Rates

Interest rates decide the level of investment activity in the country. Nominal

interest rate is the contractual rate of interest when a business firm/ individual

borrows money from a bank or financial institution. Real interest rate is the

inflation adjusted interest rate (real interest rate = nominal interest rate - inflation).

As the Indian firms are made to compete with the global players as part of our

globalization exercise, interest rates in India need to be lowered in line with cost

of funds for firms abroad.

Investment is of two types: autonomous and induced. Autonomous investment is

interest-independent and income-independent. This type of investment takes

places largely as public investment. Induced investment, on the other hand, is

interest-sensitive investment that rises when there is a decline in interest rate

(lending rate) and vice versa.

Treasury Operations Basics 20

2.4 Exchange Rate:

Price of one currency expressed in terms of another currency. It depends on the trade

and investment flows between countries.

Balance of Payments

Balance of payments is a systematic record of transactions made by one country

with the rest of the world during a given time period, normally a year. This record

helps us understand the value of merchandise exports and imports and the

services transacted as well as the long-term capital-related transactions taking

place.

The balance of payments has two accounts: the current account and the capital

account. When we talk about the position of the balance of payments, we are

taking into account the cumulative value of the two accounts. It may give us a

negative or positive value as the “overall value”. It has to be offset by an

equivalent amount to have neither a surplus nor a deficit. In other words, balance

of payments should always remain balanced.

2.5 Macroeconomic Policies – Monetary and Fiscal Policies

The goal of macroeconomic policy is to achieve high and stable growth rate of the

economy with low and stable inflation. It is to be noted that monetary, fiscal and external

trade policies play a critical role in the management of an economy. Monetary policy

aims at influencing the performance of an economy in terms of price stability, output

growth, and employment. Depending on the phase of the business cycle an economy is

undergoing, it tries to affect consumption and, spending decisions of firms and

individuals. Monetary policy is a much better stabilization tool. Using monetary policy,

Treasury Operations Basics 21

unlike most government actions (tax and expenditure policies), interest rates can be

changed literally overnight. Fiscal policy focuses on building solid foundations for long-

term growth. Stabilizing prices requires estimates of sustainable or potential growth rate

of the economy. The potential output depends on three factors: growth in labor force,

capital investment and technological progress. External policy focuses on exchange rate

movements and their impact on capital inflows and outflows, tariffs to be imposed on

imports, and issues relating to the country‟s balance of payments situation.

Fluctuations in real economic growth measured by real GDP over a long period can be

analyzed in terms of business cycle. Business cycle has four phases. These phases are:

Expansion or boom

Recession

Depression

Recovery

The business cycle is the periodic but irregular up-and-down movements in economic

activity, measured by fluctuations in real GDP and other macroeconomic variables. A

business cycle is not a regular, predictable, or repeating phenomenon like the swing of

the pendulum of a clock. Its timing is random and, to a large extent, unpredictable.

Currently, policymakers worldwide are seriously involved in formulating and fine-tuning

macroeconomic policies to address issues relating to the recent 2008 financial crisis. If

we look keenly into their efforts, we can see that all these policy makers are trying to

revive economic growth rate, stabilize inflation, and handle large scale unemployment

that had resulted due to the financial crisis. By inducing liquidity into the system and

Treasury Operations Basics 22

reducing interest rates, policy makers are trying for the recovery in their respective

economies.

2.6 Monetary and Fiscal Policies

Monetary Policy

Monetary Policy is formulated by the respective central banks of the countries. Its

objective is to determine money supply and assess its impact on output, inflation,

unemployment. It has various policy tools like quantitative and qualitative measures that

help fine-tune policy making as per the situation warranted.

In the US context, the Federal Reserve is the central bank that formulates US monetary

policies and is the authority to affect changes in policy interest rates. It uses open market

operations, changes in reserve requirements, and Fed fund rate as policy instruments to

affect money supply, credit availability and liquidity in the system.

Money Supply measures

In the US, the following two money supply measures are used:

M1 - Currency, demand deposits, other checkable deposits and travelers checks

M2 - M1 plus savings deposits, small denominated time deposits and money market

mutual funds

Treasury Operations Basics 23

Monetary policy and business cycles

During the boom time a contractionary monetary policy is used to cool down the

economy from overheating. During recessions, an expansionary monetary policy is used

to bring back the economy on to the growth path.

To tighten or ease credit availability, central banks generally influence short-term interest

rates. These changes are gradually transmitted to longer-term rates. Central banks

influence rates largely by buying and selling government securities in the market, an

activity referred to as open market operations. Buying and selling activity influences bank

reserves and lending power. For example, monetary ease is achieved by buying

government securities and expanding bank reserves. Monetary restraint is achieved

through sale of government securities. To a large extent, the central banks can affect

interest rates by adjusting the level of reserves required to back bank deposits (reserve

requirements) and adjusting the rate at which it will lend money to banks (discount rate).

Monetary policy and inflation – In the long run, rate of growth of money supply and rate

of growth of inflation are closely related. A larger money supply in circulation will cause

people to increase prices of existing goods and services. Velocity of money supply refers

to the relation between money supply prices and output.

Monetary Policy and exchange rates: In a flexible exchange rate regime, monetary policy

(by raising real interest rate) increases demand for currency and causes it to appreciate.

The stronger currency reinforces the effects of tight monetary policy on aggregate

demand by reducing net exports. Easy monetary policy, on the other hand, lowers real

interest rates and weakens the currency, which stimulates exports.

Treasury Operations Basics 24

2.7 Monetary policy and interest rates

A central bank operates Monetary Policy by controlling money supply, media and

financial markets focus on the central bank‟s announcements on interest rates. The

central bank‟s ability to control money supply is the source of its ability to control interest

rates. Nominal money supply is determined by demand and supply forces. Demand for

money is determined by comparison of costs and benefits of holding money. The

nominal interest rate measures the opportunity cost of holding money. Increases in GDP,

price level, and volume of transactions, result in increased demand for money. The

central bank determines supply of money through use of open market operations,

changes in reserve ratios, and changes in short-term policy rates.

Fiscal Policies

Levying and collection of various types of taxes, purchase of goods and services, and

spending on transfer payments, constitute major functions of the government. The

policies that govern these aspects are termed Fiscal Policies. The government uses

different tools to influence economic activity.

Taxes and expenditure are the two major components of fiscal policies. Charges of

public goods/services are other aspect of public finance. Taxes are levied on incomes

(personal, corporate) and goods and services (customs, excise). These taxes provide

resources to the government to carry out its functions of national security and public

expenditure. It reduces the disposable incomes of individuals and companies by levying

taxes on their earned income. The tax system is also used to give a direction to

economic activities. For instance, tax incentives encourage investments into certain

Treasury Operations Basics 25

productive activities (housing loan incentives) and high level of taxes discourages certain

activities like smoking of cigarettes.

Expenditure is made on public goods such as roads, education, public protection along

with the social security (pensions, public healthcare subsidies, unemployment doles,

relief and ex-gratia payments are termed as transfer payments) by the government to

individuals. These help in building infrastructure of a country and in improving quality of

life of individuals.

The concept of fiscal deficit refers to the overall borrowing requirement of the

government; it is the gap between aggregate expenditure (revenue and capital) and

aggregate receipts (net of non-debt receipts).

The higher the fiscal deficit, the greater is the pressure on interest rates to rise. This is

because the government is now raising loans from the market. Thus, given limited

availability of funds at the disposal of institutions, a rise in demand for credit would make

interest rates rise, discouraging the private sector from borrowing at rising interest rates.

Government policies have a strong effect on the performance of industries and other

sectors of the economy. Business firms can represent their concerns to the appropriate

department/ ministry to influence public policies in their favor, although public policies are

considered to be exogenous or something beyond the control of firms. Removal of

restrictions on the movement of some goods between states or regions, fix prices (e.g.

statutory minimum price), retrenchment of workers, tax-related policies and subsidies,

etc., go a long way in deciding the overall performance of firms.

Treasury Operations Basics 26

3. Treasury markets and instruments

Chapter objectives:

1. To understand the various money market and fixed income market instruments

2. To identify the participants of fixed income markets

3. To understand the role of credit rating

4. To comprehend various concepts of bond mathematics

5. To identify the derivatives instruments used in fixed income markets

6. To analyze the cost of funds and manage investment and trading portfolio

The entire treasury desk is basically divided into two groups: Forex market desk, and

home currency desk and ALM. Details about forex market desk and ALM are taken in

chapter 4 and 5 and this chapter deals with home currency desk operations.

Treasury markets on the home currency desk can be classified into money market and

bond market, depending on the maturity of instruments that are traded in these markets.

The money market is where short-term instruments for borrowing and lending (less than

one year of original maturity) are traded. The bond market, on the other hand, is the

financial market where participants buy and sell long-term debt securities.

3.1 Money Market Instruments

Inter Bank Markets It is a market where banks borrow and lend to each other for

short-term purposes such as meeting reserve requirements.

Term Money It is an inter-bank borrowing and lending money for short period of

Treasury Operations Basics 27

time, usually up to one year.

Repo Repo or repurchase agreement is a transaction where one party

buys securities from another party, only to sell it back to the same

party after a short period of time. Repo is used by central banks as

a liquidity management tool.

Banker‟s

Acceptance

Banker‟s acceptance is a short-term money market instrument

where a bank guarantees payment to a counterparty if the buyer

defaults on a trade transaction.

Euro Dollar

Deposits

Euro dollars are short-term (up to one year) USD denominated

institutional deposits held with banks outside the US

3.2 Coupon Bearing Instruments

Treasury notes and bonds –Treasury notes and bonds are issued by various

governments. These instruments have longer maturities (greater than one year)

and they pay coupon periodically.

Corporate bonds – Corporate bonds are long-term instruments used to borrow

funds by corporations.

3.3 Discount Instruments

Treasury bills – Treasury bills are short-term (up to one year) discount papers

issued by governments to meet short-term borrowing requirements. They are

issued at less than face value and redeemed at face value on maturity.

Treasury Bills are usually issued at regular intervals for a particular issue size and

may have multiple maturities, e.g., fortnight, month, 3-month, 6-month, and 1

year. These bills are liquid instruments and banks, financial institutions and

investment funds are the major traders, investors in these instruments. They are

Treasury Operations Basics 28

considered risk free securities since they are issued by governments and hence

are believed to have no default risk.

Commercial papers – Commercial papers are short-term (up to one year)

discount papers issued by corporations to meet their short-term financing

requirements. They are issued at less than face value and redeemed at face

value on maturity.

Treasury markets and instruments and fixed income markets

3.4 Fixed income instruments

Capital can be raised in two forms: equity and debt. Equity capital is contributed by

owners (i.e., shareholders) of the company and represents owned funds. Debt capital is

raised from outside lenders such as banks and hence constitutes borrowed funds.

Financial market instruments that are used to raise borrowed funds are typically called

debt or fixed income instruments. As already mentioned, the debt market is divided into

money market and bond market. Some of the bond market instruments are government

securities and corporate bonds.

Bonds can also be differentiated based on:

Taxability : Taxable and tax-free bonds

Issuers: Banks, Financial Institutions, Agencies, Corporates, Special Purpose

Entities

Convertibility: Fully, partially, and non-convertible

Apart from debt instruments that are cash market instruments, we also have fixed

income derivative instruments. Some of the interest rate derivative instruments are

Treasury Operations Basics 29

forward rate agreements, interest rate futures, interest rate swaps, currency swaps, and

interest rate options and swaptions.

3.5 Participants in fixed income markets

Some of the participants in the fixed income markets are:

Governments – Governments are typically the largest players in the fixed income

markets since they borrow large quantum of funds in a year to meet their

budgetary requirements. Short-term borrowings of the government are through

treasury bills while long-term borrowings by governments are through

government securities.

Regulators – The central bank of a country is the banker to the government and

typically regulates the banking industry and as a result, it predominantly regulates

the fixed income markets. Apart from central banks, other regulators (regulating

the capital markets or insurance sector etc.) may regulate certain aspects of fixed

income markets.

Banks –. Banks participate in various capacities such as issuers, dealers,

investors and brokers.

Financial Institutions – Apart from banks, financial institutions are also important

players in fixed income markets. These institutions raise substantial capital in the

form of debt. Many of these are active investors in debt instruments.

Primary dealers – Primary Dealers are a special type of fixed income market

participants who act as underwriters for government security issuances by

Treasury Operations Basics 30

accepting underwriting commission from the government. They have a

responsibility towards development of this market by readily providing two-way

quotes for securities being traded in the market. As a result, they provide the

required liquidity to the market.

Corporations – Corporations take part in the fixed income market as issuers or

investors. Large amount of funds are raised in the form of debt and corporates

also invest surplus funds in debt instruments.

Asset Management Companies – Asset Management Companies manage

mutual funds which pool investors‟ money. These mutual funds invest the

proceeds in debt and fixed income markets.

Insurance companies – Insurance companies, both life and non-life, invest in the

fixed income markets to provide returns to the policy holders. Maturity profiles of

insurance companies are typically much longer than other investors.

Broker dealers – Broker dealers predominantly act as intermediaries in the fixed

income markets and as facilitators to major players in the market. They do so by

acting as a bridge between the buyer and seller. Many a times, however, they

invest or trade for their own proprietary portfolio positions in the market.

3.6 Government Securities

As mentioned earlier, government securities are instruments through which governments

raise funds for longer tenors to meet their budgetary requirements. A government pays

periodic coupon payments, usually semi-annually, to the holder of the bonds until

Treasury Operations Basics 31

maturity of the bonds. Maturity of the bonds can be as long as 50 years. Rather than

paying regular fixed coupons, government may even pay floating rate coupons to bond

holders and link it to any industry approved benchmarks, which would be reset at regular

intervals, typically during periodic cash flow dates.

3.7 Corporate Debt Markets

As mentioned earlier, corporate debt markets are the market for corporations to raise

funds, both short-term and long-term. Commercial papers are short-term money market

instruments with maturity of up to one year are used by corporations to raise short-term

funds to meet their working capital requirements. Corporate bonds are long-term bond

market instruments for maturity beyond a year and are used by corporations to raise

funds to meet their demands for long-term capital for business, expansions,

infrastructure funding etc.

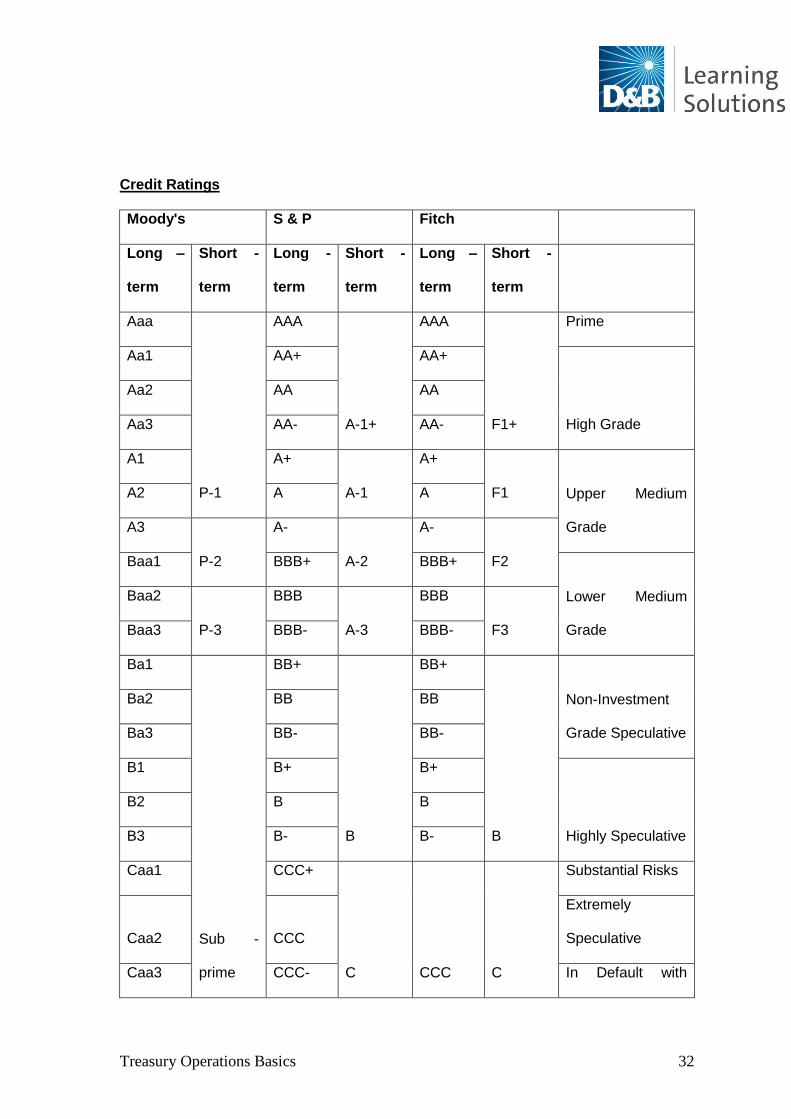

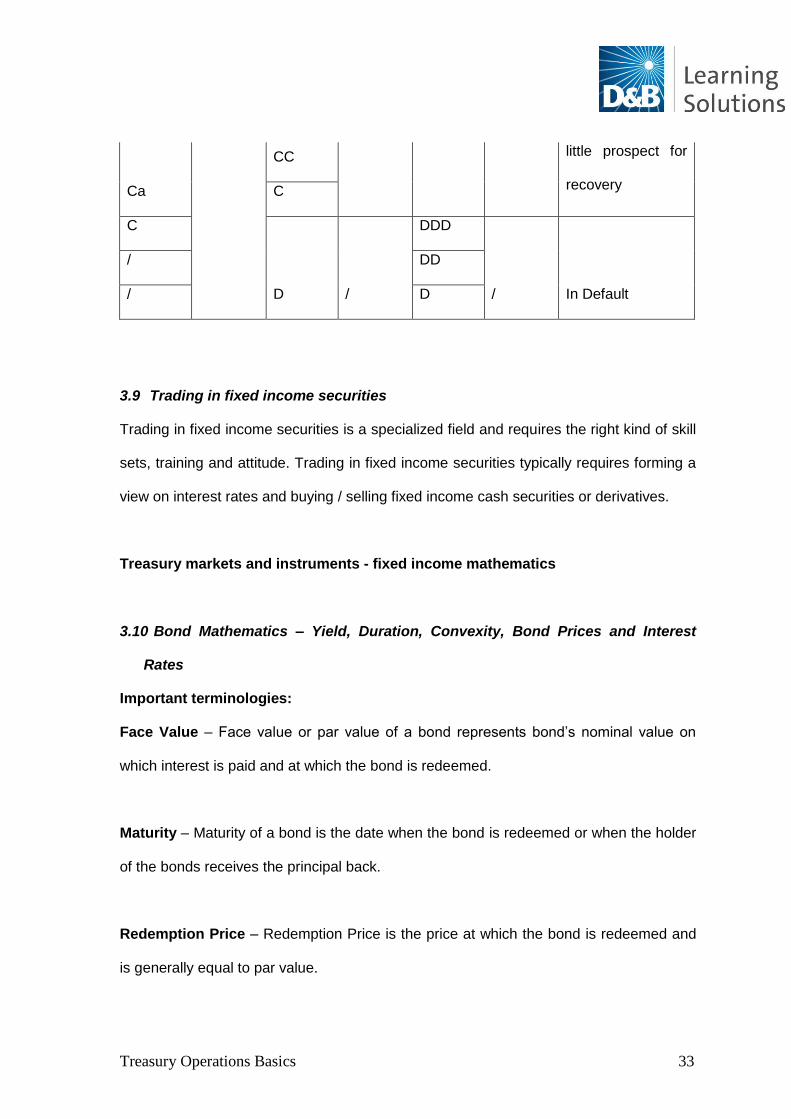

3.8 Credit Rating and its importance

Credit rating is a mechanism by which issuers and issuances with different credit-

worthiness are differentiated from each other both for short-term and long-term. There

are specialized global credit rating agencies such as Moody‟s, S&P and Fitch, which

provide credit ratings to organizations, issuances and even countries, based on their

past performance and projected cash flows. Most credit worthy organizations and

issuances are awarded the highest credit rating, viz., Aaa from Moody‟s, AAA from S&P

and Fitch and D is generally a default rating. Investment grade ratings are typically

higher than and up to Baa3 from Moody‟s and BBB from S&P and Fitch.

Treasury Operations Basics 32

Credit Ratings

Moody's S & P Fitch

Long –

term

Short -

term

Long -

term

Short -

term

Long –

term

Short -

term

Aaa

P-1

AAA

A-1+

AAA

F1+

Prime

Aa1 AA+ AA+

High Grade

Aa2 AA AA

Aa3 AA- AA-

A1 A+

A-1

A+

F1 Upper Medium

Grade

A2 A A

A3

P-2

A-

A-2

A-

F2 Baa1 BBB+ BBB+

Lower Medium

Grade

Baa2

P-3

BBB

A-3

BBB

F3 Baa3 BBB- BBB-

Ba1

Sub -

prime

BB+

B

BB+

B

Non-Investment

Grade Speculative

Ba2 BB BB

Ba3 BB- BB-

B1 B+ B+

Highly Speculative

B2 B B

B3 B- B-

Caa1 CCC+

C CCC C

Substantial Risks

Caa2 CCC

Extremely

Speculative

Caa3 CCC- In Default with

Treasury Operations Basics 33

Ca

CC little prospect for

recovery C

C

D /

DDD

/ In Default

/ DD

/ D

3.9 Trading in fixed income securities

Trading in fixed income securities is a specialized field and requires the right kind of skill

sets, training and attitude. Trading in fixed income securities typically requires forming a

view on interest rates and buying / selling fixed income cash securities or derivatives.

Treasury markets and instruments - fixed income mathematics

3.10 Bond Mathematics – Yield, Duration, Convexity, Bond Prices and Interest

Rates

Important terminologies:

Face Value – Face value or par value of a bond represents bond‟s nominal value on

which interest is paid and at which the bond is redeemed.

Maturity – Maturity of a bond is the date when the bond is redeemed or when the holder

of the bonds receives the principal back.

Redemption Price – Redemption Price is the price at which the bond is redeemed and

is generally equal to par value.

Treasury Operations Basics 34

Coupon frequency – Coupon Frequency refers to the number of times in a year coupon

is received by the holder of the bond.

Coupon on bond – It is the rate at which interest is paid to bond holders.

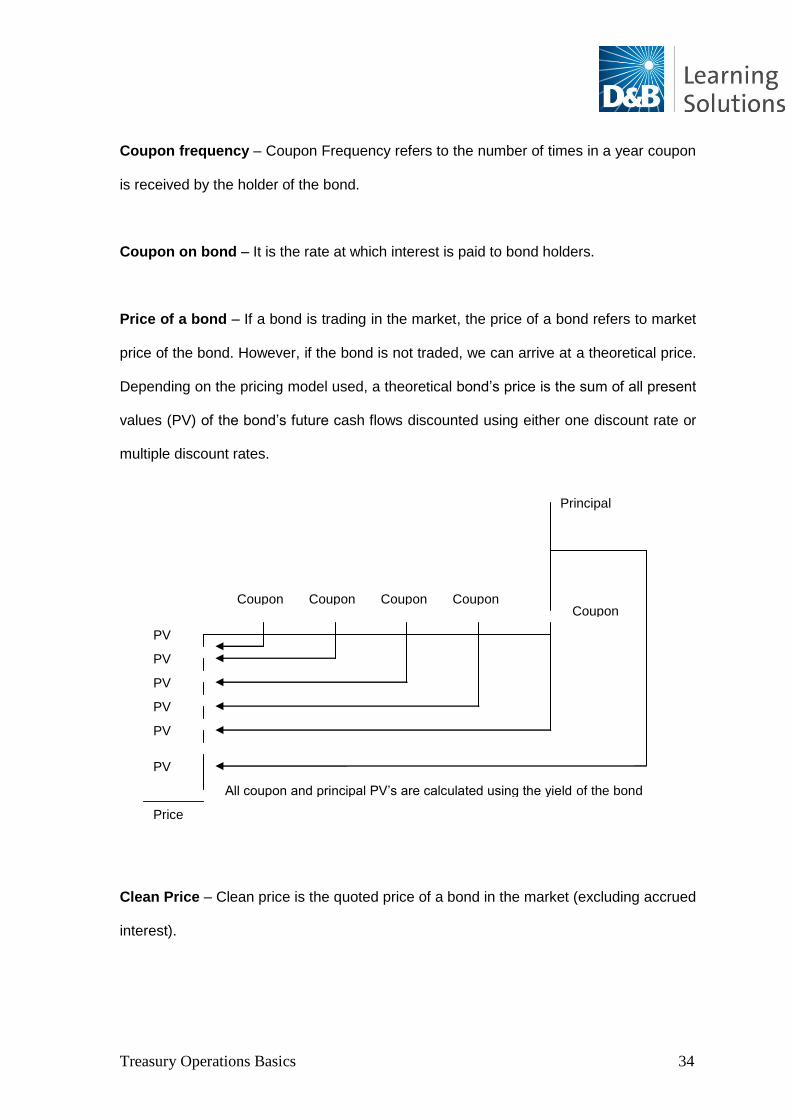

Price of a bond – If a bond is trading in the market, the price of a bond refers to market

price of the bond. However, if the bond is not traded, we can arrive at a theoretical price.

Depending on the pricing model used, a theoretical bond‟s price is the sum of all present

values (PV) of the bond‟s future cash flows discounted using either one discount rate or

multiple discount rates.

Clean Price – Clean price is the quoted price of a bond in the market (excluding accrued

interest).

Principal

Coupon Coupon Coupon Coupon Coupon

PV

PV

PV

PV

PV

PV

Price

All coupon and principal PV‟s are calculated using the yield of the bond

Treasury Operations Basics 35

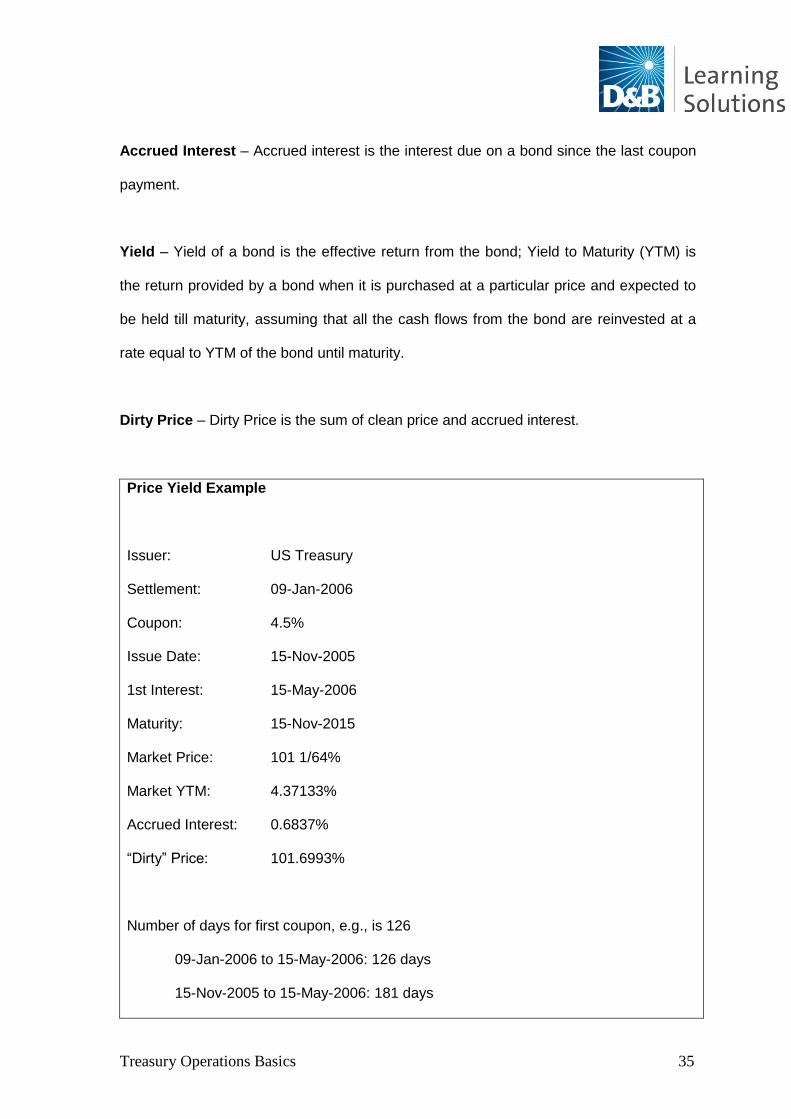

Accrued Interest – Accrued interest is the interest due on a bond since the last coupon

payment.

Yield – Yield of a bond is the effective return from the bond; Yield to Maturity (YTM) is

the return provided by a bond when it is purchased at a particular price and expected to

be held till maturity, assuming that all the cash flows from the bond are reinvested at a

rate equal to YTM of the bond until maturity.

Dirty Price – Dirty Price is the sum of clean price and accrued interest.

Price Yield Example

Issuer: US Treasury

Settlement: 09-Jan-2006

Coupon: 4.5%

Issue Date: 15-Nov-2005

1st Interest: 15-May-2006

Maturity: 15-Nov-2015

Market Price: 101 1/64%

Market YTM: 4.37133%

Accrued Interest: 0.6837%

“Dirty” Price: 101.6993%

Number of days for first coupon, e.g., is 126

09-Jan-2006 to 15-May-2006: 126 days

15-Nov-2005 to 15-May-2006: 181 days

Treasury Operations Basics 36

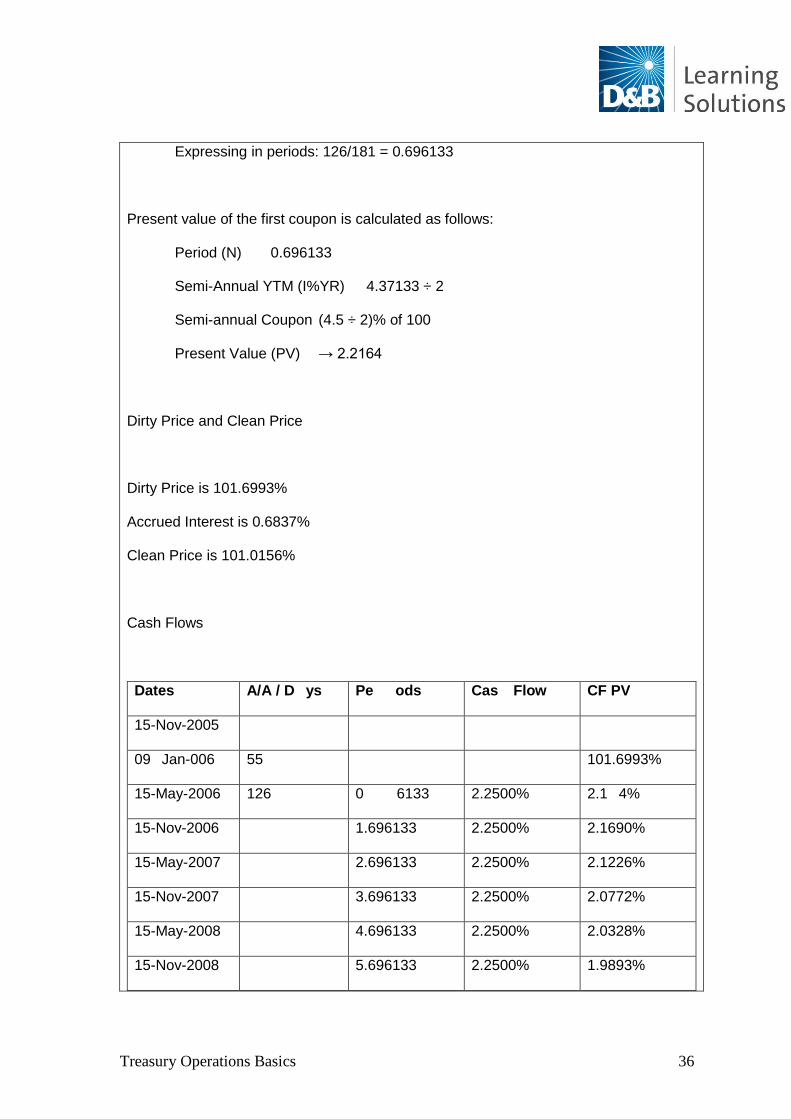

Expressing in periods: 126/181 = 0.696133

Present value of the first coupon is calculated as follows:

Period (N) 0.696133

Semi-Annual YTM (I%YR) 4.37133 ÷ 2

Semi-annual Coupon (4.5 ÷ 2)% of 100

Present Value (PV) → 2.2164

Dirty Price and Clean Price

Dirty Price is 101.6993%

Accrued Interest is 0.6837%

Clean Price is 101.0156%

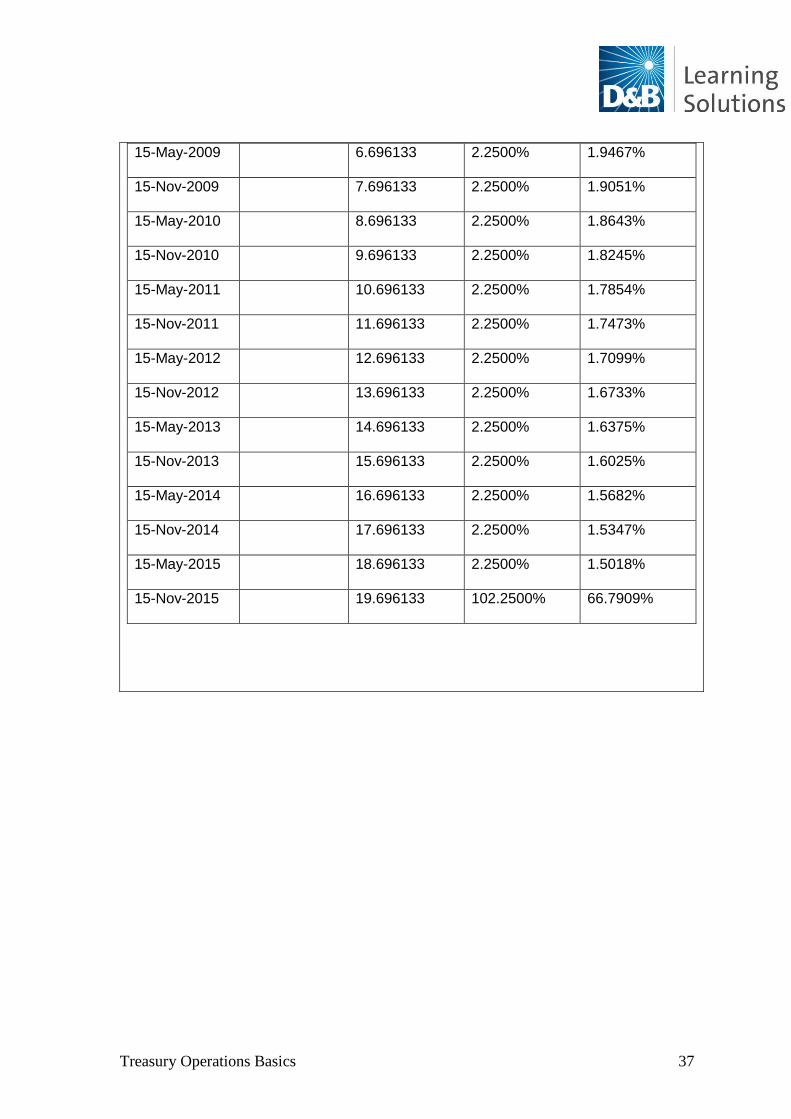

Cash Flows

Dates A/A / D ys Pe ods Cas Flow CF PV

15-Nov-2005

09 Jan-006 55 101.6993%

15-May-2006 126 0 6133 2.2500% 2.1 4%

15-Nov-2006 1.696133 2.2500% 2.1690%

15-May-2007 2.696133 2.2500% 2.1226%

15-Nov-2007 3.696133 2.2500% 2.0772%

15-May-2008 4.696133 2.2500% 2.0328%

15-Nov-2008 5.696133 2.2500% 1.9893%

Treasury Operations Basics 37

15-May-2009 6.696133 2.2500% 1.9467%

15-Nov-2009 7.696133 2.2500% 1.9051%

15-May-2010 8.696133 2.2500% 1.8643%

15-Nov-2010 9.696133 2.2500% 1.8245%

15-May-2011 10.696133 2.2500% 1.7854%

15-Nov-2011 11.696133 2.2500% 1.7473%

15-May-2012 12.696133 2.2500% 1.7099%

15-Nov-2012 13.696133 2.2500% 1.6733%

15-May-2013 14.696133 2.2500% 1.6375%

15-Nov-2013 15.696133 2.2500% 1.6025%

15-May-2014 16.696133 2.2500% 1.5682%

15-Nov-2014 17.696133 2.2500% 1.5347%

15-May-2015 18.696133 2.2500% 1.5018%

15-Nov-2015 19.696133 102.2500% 66.7909%

Treasury Operations Basics 38

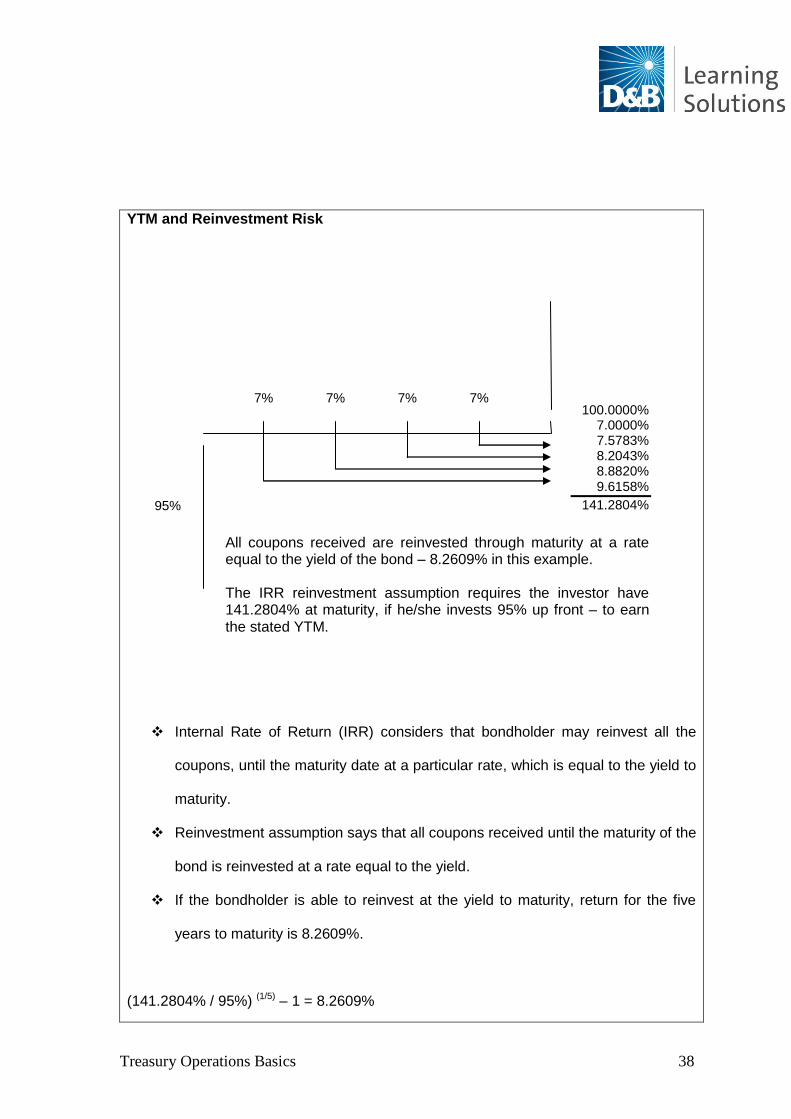

YTM and Reinvestment Risk

Internal Rate of Return (IRR) considers that bondholder may reinvest all the

coupons, until the maturity date at a particular rate, which is equal to the yield to

maturity.

Reinvestment assumption says that all coupons received until the maturity of the

bond is reinvested at a rate equal to the yield.

If the bondholder is able to reinvest at the yield to maturity, return for the five

years to maturity is 8.2609%.

(141.2804% / 95%) (1/5) – 1 = 8.2609%

100.0000% 7.0000% 7.5783% 8.2043% 8.8820% 9.6158%

141.2804%

7% 7% 7% 7%

95%

All coupons received are reinvested through maturity at a rate equal to the yield of the bond – 8.2609% in this example. The IRR reinvestment assumption requires the investor have 141.2804% at maturity, if he/she invests 95% up front – to earn the stated YTM.

Treasury Operations Basics 39

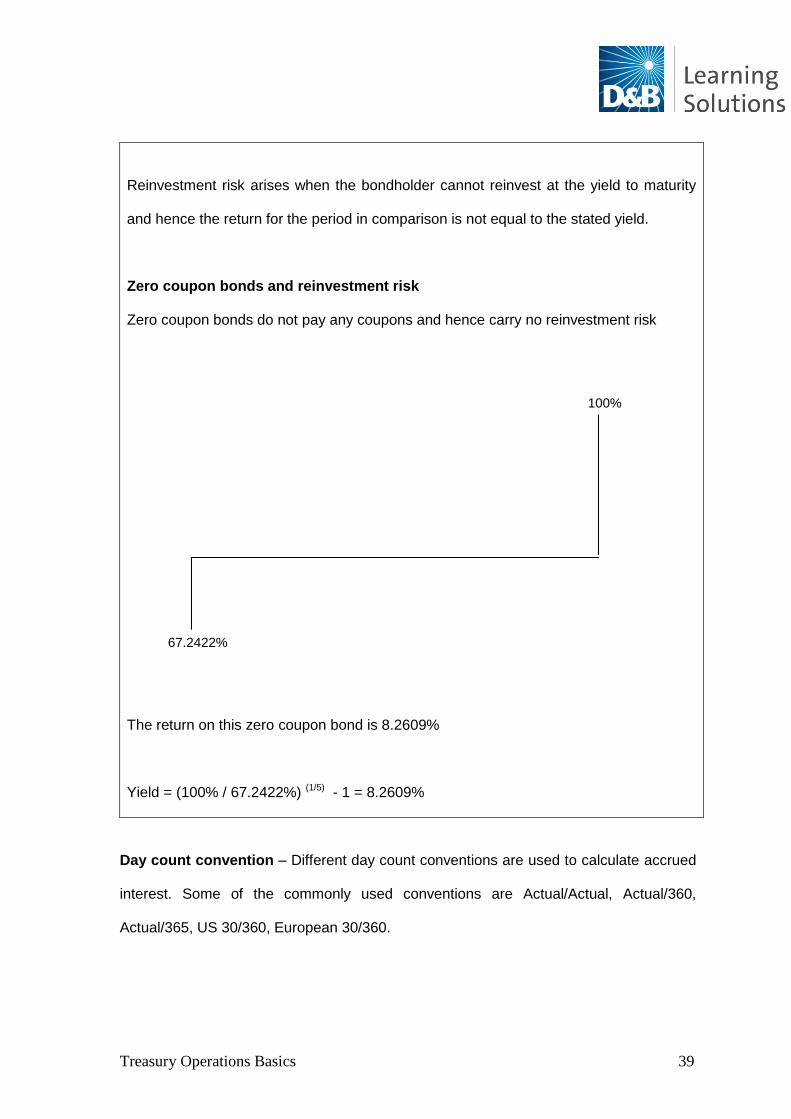

Reinvestment risk arises when the bondholder cannot reinvest at the yield to maturity

and hence the return for the period in comparison is not equal to the stated yield.

Zero coupon bonds and reinvestment risk

Zero coupon bonds do not pay any coupons and hence carry no reinvestment risk

The return on this zero coupon bond is 8.2609%

Yield = (100% / 67.2422%) (1/5) - 1 = 8.2609%

Day count convention – Different day count conventions are used to calculate accrued

interest. Some of the commonly used conventions are Actual/Actual, Actual/360,

Actual/365, US 30/360, European 30/360.

100%

67.2422%

Treasury Operations Basics 40

Valuation of bonds using Zero Coupon Yield Curve

As explained earlier, bonds can be valued using YTM as the discounting factor.

However, YTM suffers from reinvestment rate assumption. Hence bonds can be valued

using alternate methodology i.e. by deriving zero coupon yield curve. A zero coupon

yield applicable to particular maturity is called a spot rate.

Determining Spot Rates

Spot rates are used to discount a single cash flow to be received at some specific

date in the future.

Hence all cash flows received at t=1 must be discounted at the same rate,

assuming that the issuer for all bonds is same.

The one-year zero coupon bond has only one cash flow, we can use its YTM as

the discount factor for other t=1 cash flows (again assuming same issuer or same

credit quality of issuer), i.e. use the YTM as the one-year spot rate Z1.

The approach that we are employing to create a theoretical spot rate curve is

called bootstrapping.

Zero Coupon Cash Flow Approach

To avoid the problems of comparability caused by differing cash flow patterns among on-

the-run Treasuries, we can realize that each coupon bond is really a package of single

payment bonds.

Treasury Operations Basics 41

For example, a 2-year 10% coupon bond is really a package of five single-payment

bonds:

four for the semi-annual coupon payments and

one for the repayment of the corpus

Zeroes

A single-payment bond is called a “zero”

A coupon bond can be thought of as a package of zeroes,

one for each of the coupon payments and

one for the principal

In principle, any coupon bond can be “stripped” or “unbundled” into its constituent

zeroes. STRIPS are unbundled coupon bonds.

Spot Yields

A “spot yield” is the current YTM on a zero coupon bond.

For example, the one-year spot yield is the yield to maturity on a one-year zero.

The price of an n-year zero is related to the n-year spot rate by the formula:

0Pn = 1 / (1 + in/2)2n

0Pn = Price of n-year zero

in = n-year spot rate

Treasury Operations Basics 42

Forward Rates

These are used for valuing, borrowing, or lending, which can happen at some future

date. The spot rate for a six-month tenor, one-year from now is known as the “six-month

forward rate one-year from now”. This rate will be applicable on a sum of money

borrowed for a period between 1-year and 1.5 years from now. This rate can be derived

from the zero-coupon spot rate curve as follows. A spot bond is issued at $ 100 on date

0 and gets repaid on date t2 (say after 2 years). In a forward contract, one agrees on

date 0 to lend $ 100 on date t1 (say after 1 year) and gets repaid on date t2. As with all

forward contracts, there is no optionality, and it is a locked-in contract. The interest rate

rt2 (contracted at time 0 for a period between t1 to t2) is known as “a forward interest rate”.

The spot yield curve directly shows all the rt values.

Case 1: When one buys a bond for $100, it yields 100(1+r02)2 after two years.

Case 2: When one buys a one–year bond and enters into a following one–year forward

contract, we get the following:

100 (1+r0

2)2 = 100(1+r0

1)(1+r1

2)

(1+r1

2) = (1+r0

2)2

(1+r0

1)

Measuring bond price sensitivity

An investor in fixed income is worried about bond price fluctuations. Since bond prices

fluctuate mainly in response to change in interest rates an interesting question to be

answered is how sensitive are bond prices to changes in interest rates? The concept of

duration helps us to arrive at approximate changes in bond prices due to changes in

interest rates as follows.

Treasury Operations Basics 43

Duration

Duration is the weighted average maturity of a bond, where the present values of

cash flows are used as weights.

In computing duration, we consider both the timing and magnitude of all cash

flows associated with the security.

Duration is a measure of the price volatility of a bond.

The concept of duration is used for a single asset, a portfolio of assets, or the

entire balance sheet.

(Macaulay) Duration Formula

D = Σ(t x PV(t)) / ΣPV(t)

D = Duration

t = Period

PV (t) = Present Value of Cash Flow in Period t

Modified duration:

It is a price sensitivity measure. It measures the change in market value of a bond

resulting from a small change in interest rates.

Modified duration = Duration / (1 + YTM)

YTM = Yield to Maturity

Treasury Operations Basics 44

Percent change in bond price = - Modified duration x Change in yield

Steps in Computing Duration

1. Calculate the timing and magnitude of cash flows associated with the instrument.

2. Find the present value of each cash flow.

3. Find the total of all PVs.

4. Find the time-weighted PV of each cash flow.

5. Find the total of all time-weighted PVs.

6. Duration: Divide the total in Step 5 by the total in Step 3.

7. Find the modified duration as Duration / (1 + Yield).

Duration and modified duration

Problem 1: 5-year 12% Coupon Bond selling at Rs.100 par

Problem 2: 5-year 10% Coupon Bond selling at Rs.100 par

Problem 3: 5-year 6% Coupon Bond selling at Rs.100 par

Problem 4: 10-year 10% Coupon Bond selling at Rs.100 par

Treasury Operations Basics 45

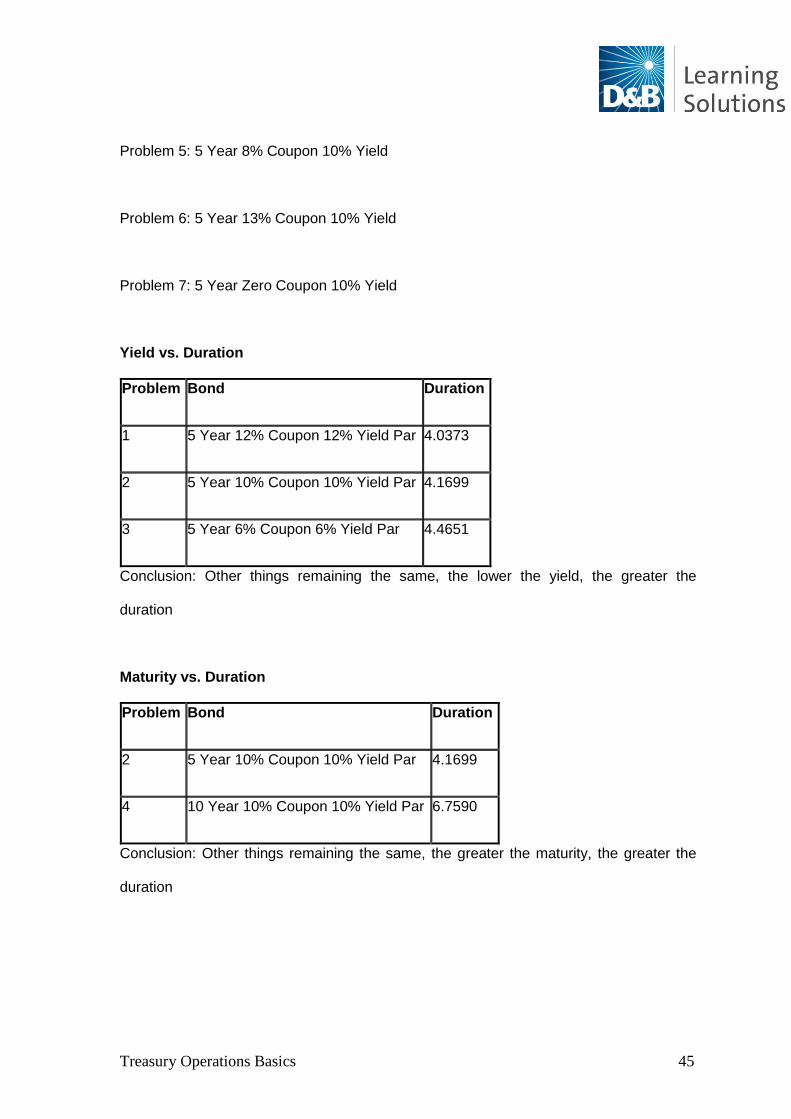

Problem 5: 5 Year 8% Coupon 10% Yield

Problem 6: 5 Year 13% Coupon 10% Yield

Problem 7: 5 Year Zero Coupon 10% Yield

Yield vs. Duration

Problem Bond Duration

1 5 Year 12% Coupon 12% Yield Par 4.0373

2 5 Year 10% Coupon 10% Yield Par 4.1699

3 5 Year 6% Coupon 6% Yield Par 4.4651

Conclusion: Other things remaining the same, the lower the yield, the greater the

duration

Maturity vs. Duration

Problem Bond Duration

2 5 Year 10% Coupon 10% Yield Par 4.1699

4 10 Year 10% Coupon 10% Yield Par 6.7590

Conclusion: Other things remaining the same, the greater the maturity, the greater the

duration

Treasury Operations Basics 46

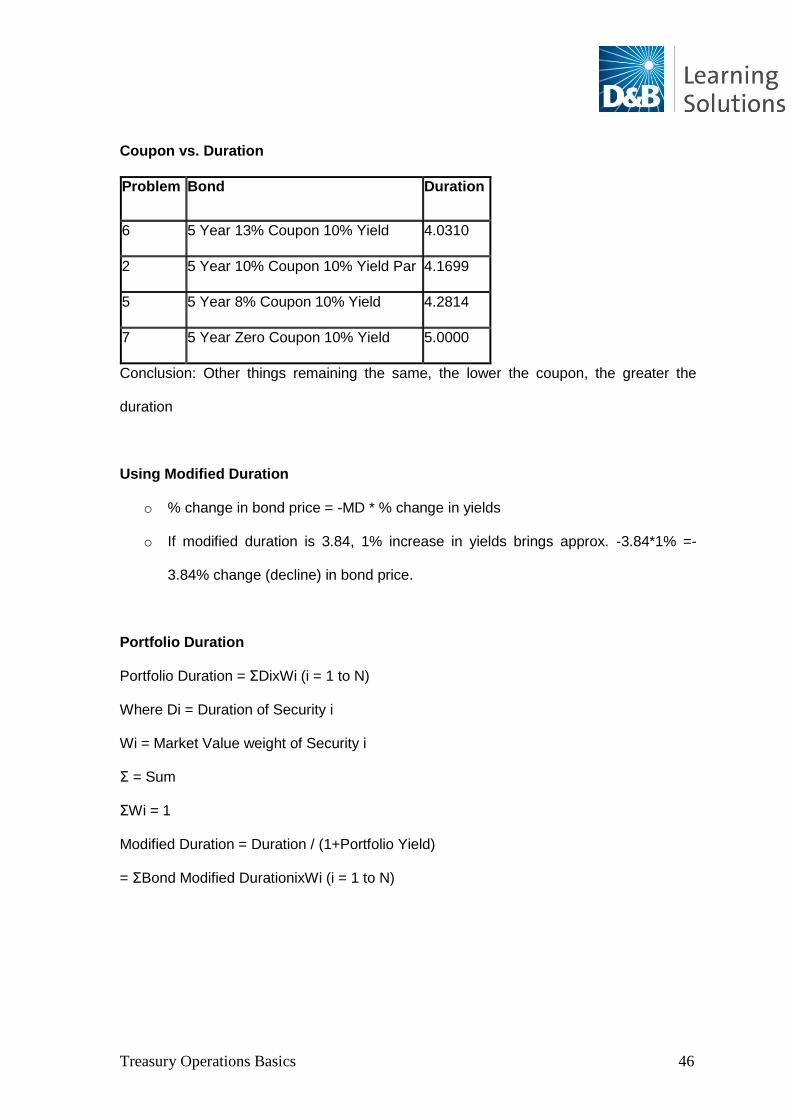

Coupon vs. Duration

Problem Bond Duration

6 5 Year 13% Coupon 10% Yield 4.0310

2 5 Year 10% Coupon 10% Yield Par 4.1699

5 5 Year 8% Coupon 10% Yield 4.2814

7 5 Year Zero Coupon 10% Yield 5.0000

Conclusion: Other things remaining the same, the lower the coupon, the greater the

duration

Using Modified Duration

o % change in bond price = -MD * % change in yields

o If modified duration is 3.84, 1% increase in yields brings approx. -3.84*1% =-

3.84% change (decline) in bond price.

Portfolio Duration

Portfolio Duration = ΣDixWi (i = 1 to N)

Where Di = Duration of Security i

Wi = Market Value weight of Security i

Σ = Sum

ΣWi = 1

Modified Duration = Duration / (1+Portfolio Yield)

= ΣBond Modified DurationixWi (i = 1 to N)

Treasury Operations Basics 47

Properties of Duration

Duration of a zero coupon bond equals its maturity.

Duration of a coupon paying bond is less than its maturity.

Duration of a floating rate bond selling at par equals its repricing maturity.

Greater the coupon, lower the duration

Greater the yield, lower the duration

Greater the maturity, greater the duration

Greater the frequency of coupon payments, lower the duration

Duration of a coupon paying bond decreases slower than time

Duration works well for small changes in yield, for large changes in yields we

have to use duration as well as convexity to judge the change in bond price

Convexity

Convexity is the rate of change of duration.

Duration is the first derivative (of bond price with respect to interest rates).

Convexity is the second derivative (of bond price with respect to interest rates).

Convexity can be positive, negative or zero.

A non-callable bond has positive convexity.

Treasury Operations Basics 48

Coupon vs. Convexity

Higher convexity implies greater price volatility.

Security with lower coupon has higher convexity.

Option embedded debt contract / security has negative convexity, e.g., callable

bond, home mortgage / mortgage backed security. This happens because when

interest rates fall, bond may be called and mortgage may be repaid. Thus, the

rate of increase in the bond‟s price (due to fall in interest rates) will be less

compared with a non-callable bond.

Using Convexity

% change in price as indicated by Convexity is as follows:

= C* ½ * %change in yields 2

Thus, total % change in bond‟s price is approximately equal to

i) % change indicated by modified duration (=-MD * % change in yields)

ii) % change indicated by convexity (= C* ½ * %change in yields2)

3.11 Cost of Funds

The interest rate paid on an outstanding loan is referred to as cost of funds. Thus, it is

the cost of borrowing money by any entity, either the government, a bank, financial

institution or a corporation. Cost of funds is low during a benign interest rate regime

whereas it is quite steep in a hardened interest rate regime.

Treasury Operations Basics 49

3.12 Managing Investment Portfolio and Trading Portfolio

Portfolios are of different types. Typically, a portfolio in a bank is classified as a trading

portfolio, an available-for-sale portfolio, and a held-to-maturity portfolio. The trading

portfolio is the portfolio where securities are traded very frequently to make profits; an

available–for-sale portfolio is one where securities are bought and sold for a

comparatively longer period of time and a held-to-maturity portfolio is one where

securities are bought to be held until maturity of the security.

Different strategies are used for management of trading portfolio and investment

portfolios. Bullet, barbell and ladder strategies (mentioned below) are some of the

strategies used for trading portfolios. Investment strategies include immunization, cash

flow matching, horizon matching, yield curve strategies and yield spread strategies.

Bond Portfolio Management (Trading) Strategies

Bullet Strategy – the portfolio is constructed so that maturity of securities in the

portfolio is highly concentrated at one point on the yield curve.

Barbell Strategy – the maturity of securities included in portfolio is concentrated at

two extreme maturities.

Ladder Strategy – the portfolio is constructed to have approximately equal

amounts of each maturity.

Bond Portfolio Management (Investment) Strategies

Immunization – This strategy involves matching the duration of assets with the

investment horizon of the institution. This immunizes the portfolio from interest

rate risks.

Treasury Operations Basics 50

Cash flow matching – This strategy involves matching of cash flow arising from

bond investment to liabilities. For example, if a liability is maturing after five years,

we can match the cash outflow (since the liability is to be repaid) with cash inflow

from a bond that matures after five years.

Horizon matching – This is a combination of the above two strategies. In this

case, cash flow matching is done for next few years and duration matching is

done for rest of the years.

Yield curve strategies – These are based on interest rate anticipation. For

example, if interest rates are expected to fall, portfolio duration can be increased

and vice versa.

Yield spread analysis – In this case, portfolio management strategies are

designed by taking into account expected yield curve changes.

3.13 Derivatives in Fixed Income Markets – Forwards, Futures, Options and Swaps

The meaning of the word “derivative” according to Chamber‟s dictionary is “derived from

something else, not original”. In the financial world also, derivatives are instruments,

which derive value from an underlying asset. Derivatives are used for trading, arbitrage

and hedging. The underlying assets from which derivatives derive their value are equity

prices, equity indices, interest rates, currencies, and commodities, etc.

Characteristics

Options, forwards, futures and swaps are derivative instruments. Forwards and swaps

are over-the-counter (OTC) instruments whereas futures are exchange-traded ones.

Options can both be exchange traded and OTC. OTC instruments refer to those

Treasury Operations Basics 51

instruments that are tailor-made as per the requirements of the parties to the contract.

These are not standardized products like exchange-traded instruments.

Applications of derivatives

Risk Transfer

Derivatives are used for hedging risks. For example, an investor who is worried about fall

in value of his investment portfolio may use derivatives for risk management. He/she will

be able to hedge the risk since the value of derivatives fluctuates directly or inversely

with the underlying and hence a suitable position in derivatives will ensure price risk is

hedged.

Leverage Effect

A position in the derivative instrument can be created at nil or fraction of cost of the

asset. For example, in case of forwards and swaps, no upfront cost needs to be incurred

while in case of options there is a premium to be paid, which generally is a fraction of the

asset cost. Hence, with the same amount of capital, a trader can take a large position in

derivatives compared with outright trading of an underlying asset. This creates a

leverage effect, magnifying the trader‟s gains as well as losses.

Liquidity

The tradability of derivatives raises the interest and number of market participants, which

in turn improves their liquidity. This means, large volumes can be traded at any time,

without influencing the prices.

Treasury Operations Basics 52

Derivative products

Forward Rate Agreements

A Forward Rate Agreement (FRA) is an agreement whereby the seller of the FRA agrees

to pay to the buyer the value of the difference between a pre-agreed interest rate and the

final settlement rate, based on an agreed Notional principal for a notional period. It is

basically to hedge the interest rate risk. The seller of the FRA will not take deposit or

make an advance to the Buyer of the FRA. The buyer of the FRA will either place a

deposit in the market or borrow from the market. If market rate is adverse in comparison

to the FRA rate, then the seller of the FRA will have to compensate the buyer of the

FRA. The difference of interest is calculated at the FRA contract rate and the market rate

and is payable at the start of the period at discounted interest rate i.e. at market rate. On

the other hand, if the market rate is favourable than the FRA contract rate, then the

buyer will have to pay the seller of the FRA the difference of interest calculated @ FRA

rate and the market rate. This is also payable at the start of the period and hence

discounted @ market rate of interest.

The settlement rate is determined by an agreed reference rate. Settlement is discounted

to the start of the period.

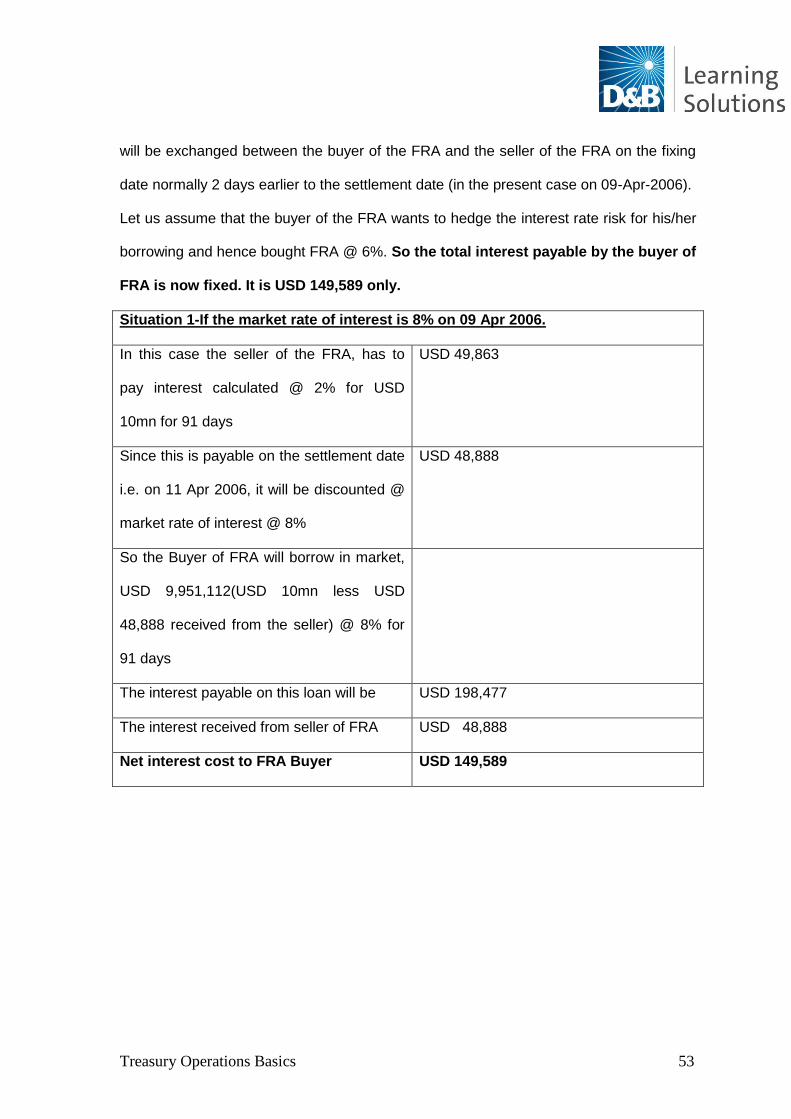

Example: On 11 Jan 2006, a customer asks for a quote from bank for USD 10mn for

3x6 months.The bank‟s quote will be: USD 10mn 3x6 5.90/6.00, which means bank is

ready to lend @ 6% or take deposit @ 5.90% , USD 10mn on 11-Apr-2006 for a period

of 3 months effectively 91 days period. The buyer of FRA will continue to place deposit/

borrow from the market only. The difference of interest for notional period (in the preset

example it is for 91 days) for a notional principal (in the present example it is USD 10mn)

Treasury Operations Basics 53

will be exchanged between the buyer of the FRA and the seller of the FRA on the fixing

date normally 2 days earlier to the settlement date (in the present case on 09-Apr-2006).

Let us assume that the buyer of the FRA wants to hedge the interest rate risk for his/her

borrowing and hence bought FRA @ 6%. So the total interest payable by the buyer of

FRA is now fixed. It is USD 149,589 only.

Situation 1-If the market rate of interest is 8% on 09 Apr 2006.

In this case the seller of the FRA, has to

pay interest calculated @ 2% for USD

10mn for 91 days

USD 49,863

Since this is payable on the settlement date

i.e. on 11 Apr 2006, it will be discounted @

market rate of interest @ 8%

USD 48,888

So the Buyer of FRA will borrow in market,

USD 9,951,112(USD 10mn less USD

48,888 received from the seller) @ 8% for

91 days

The interest payable on this loan will be USD 198,477

The interest received from seller of FRA USD 48,888

Net interest cost to FRA Buyer USD 149,589

Treasury Operations Basics 54

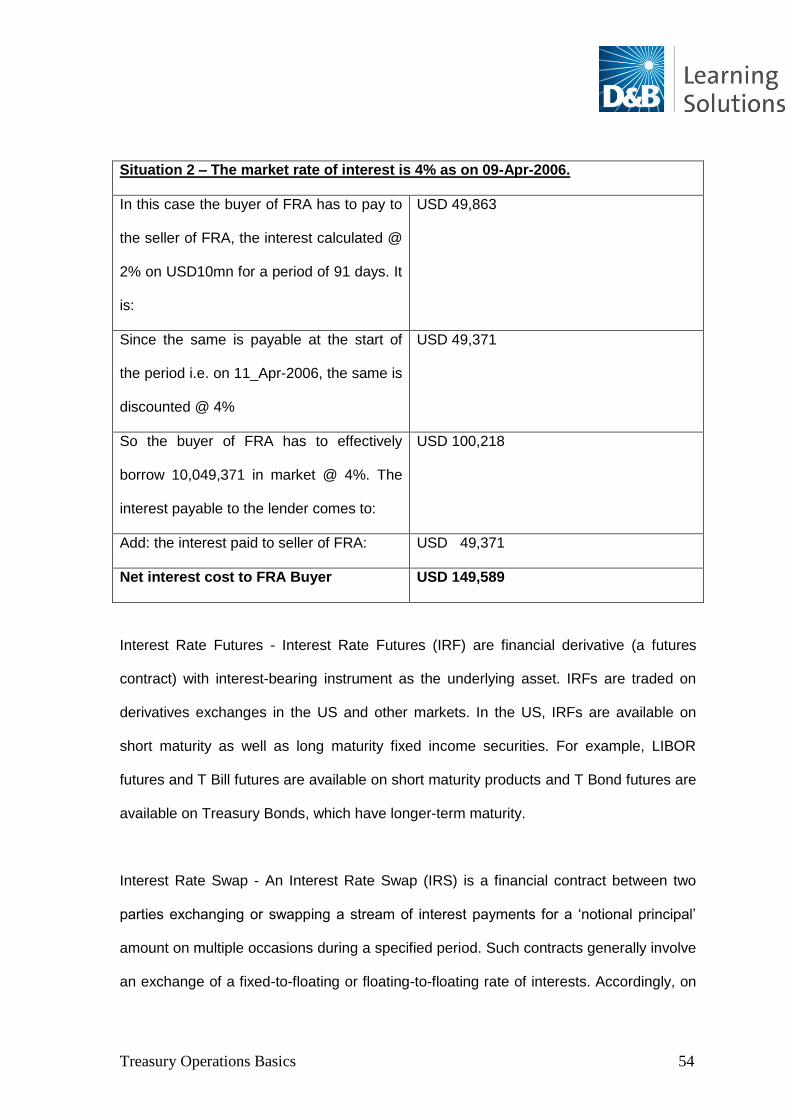

Situation 2 – The market rate of interest is 4% as on 09-Apr-2006.

In this case the buyer of FRA has to pay to

the seller of FRA, the interest calculated @

2% on USD10mn for a period of 91 days. It

is:

USD 49,863

Since the same is payable at the start of

the period i.e. on 11_Apr-2006, the same is

discounted @ 4%

USD 49,371

So the buyer of FRA has to effectively

borrow 10,049,371 in market @ 4%. The

interest payable to the lender comes to:

USD 100,218

Add: the interest paid to seller of FRA: USD 49,371

Net interest cost to FRA Buyer USD 149,589

Interest Rate Futures - Interest Rate Futures (IRF) are financial derivative (a futures

contract) with interest-bearing instrument as the underlying asset. IRFs are traded on

derivatives exchanges in the US and other markets. In the US, IRFs are available on

short maturity as well as long maturity fixed income securities. For example, LIBOR

futures and T Bill futures are available on short maturity products and T Bond futures are

available on Treasury Bonds, which have longer-term maturity.

Interest Rate Swap - An Interest Rate Swap (IRS) is a financial contract between two

parties exchanging or swapping a stream of interest payments for a „notional principal‟

amount on multiple occasions during a specified period. Such contracts generally involve

an exchange of a fixed-to-floating or floating-to-floating rate of interests. Accordingly, on

Treasury Operations Basics 55

each payment date that occurs during the swap period, parties make cash payments to

one another based on fixed/floating and floating rates.

Features of IRS

An IRS involves exchange of interest obligations between two parties at regular

intervals over the life of IRS.

Debt is denominated in the same currency.

There is no transfer of principal. It is only notional.

Typically floating/fixed swaps are done.

Suppose Company A and Company B wants to borrow $ 10mn for five years and have

been offered the following rates.

Fixed Floating

Company A 10% 6 m Libor + 0.3%

Company B 11.20% 6 m Libor + 1%

Spread 1.2% 0.7%

Difference in Spread 1.2% - 0.7% = 0.5%

Let us also assume that Company A wants to borrow on a floating basis and Company B

wants to borrow on a fixed basis. The following table summarizes their borrowing

obligations and comparative advantage in borrowing.

Desired borrowing

obligation

Comparative advantage in

borrowing

Company A Floating Fixed

Company B Fixed Floating

Treasury Operations Basics 56

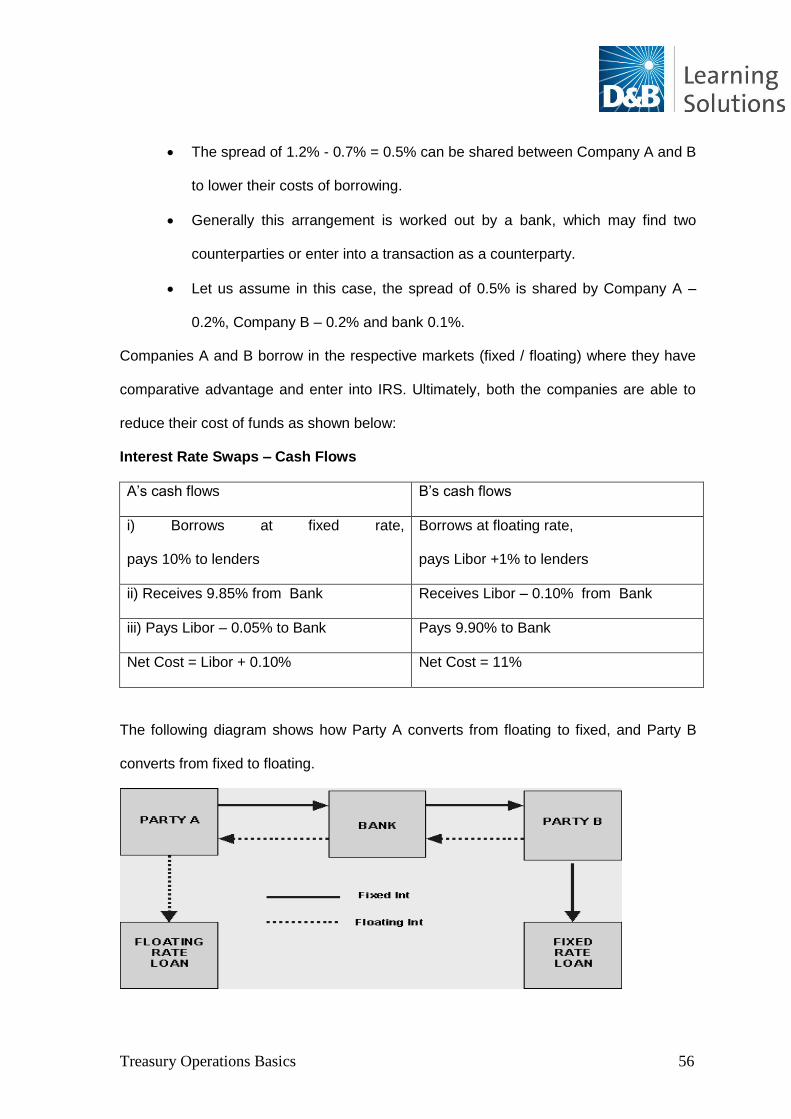

The spread of 1.2% - 0.7% = 0.5% can be shared between Company A and B

to lower their costs of borrowing.

Generally this arrangement is worked out by a bank, which may find two

counterparties or enter into a transaction as a counterparty.

Let us assume in this case, the spread of 0.5% is shared by Company A –

0.2%, Company B – 0.2% and bank 0.1%.

Companies A and B borrow in the respective markets (fixed / floating) where they have

comparative advantage and enter into IRS. Ultimately, both the companies are able to

reduce their cost of funds as shown below:

Interest Rate Swaps – Cash Flows

A‟s cash flows B‟s cash flows

i) Borrows at fixed rate,

pays 10% to lenders

Borrows at floating rate,

pays Libor +1% to lenders

ii) Receives 9.85% from Bank Receives Libor – 0.10% from Bank

iii) Pays Libor – 0.05% to Bank Pays 9.90% to Bank

Net Cost = Libor + 0.10% Net Cost = 11%

The following diagram shows how Party A converts from floating to fixed, and Party B

converts from fixed to floating.

Treasury Operations Basics 57

Another form of interest rate swap is the “Basis Swap” or floating-to-floating swap. Here,

two floating rate obligations are exchanged where the two obligations are based on

different benchmark rates. For example, the benchmark rate can be LIBOR or T-Bill rate.

Interest Rate Options

Interest rate options represent the right to make a fixed interest payment and receive a

floating interest payment or to make a floating interest payment and receive a fixed

interest payment. These interest rate options will have exercise rate or strike rate. They

are available for both European and American versions. Interest rate options are widely

used to hedge an interest rate exposure on a specific date.

Interest Rate Cap

An interest rate cap is defined as a combination of interest rate calls designed to protect

a borrower in a floating rate loan against increases in interest rates. Each component call

is referred to as a caplet. A combination of interest rate puts designed to protect a lender

in a floating rate loan against decreases in interest rate is known as interest rate floor.

Each component put is referred to as a floorlet. A combination of long cap and short floor

is known as an interest rate collar. This is most often used by a borrower and consists of

a long position in a cap, financed by selling a short position in a floor.

An interest rate cap, also known as a ceiling, is a call option on interest rates. It is a

contract that guarantees a maximum level of a floating rate benchmark. A Cap can serve

as a guarantee for one particular period, known as a Caplet. A series of Caplets or Caps

can extend for many years. The maximum loss on a Cap transaction is the premium paid

by the buyer.

Treasury Operations Basics 58

Interest Rate Floor

This is a put option on interest rates. Floors guarantee a maximum level of the fixed rate

benchmark, and they comprise a series of floorlets, each of which is a put option at a

given future date.

Interest Rate Floors are used typically by lenders in a floating rate loan when they wish

to counter falling rates. A floor contains a series of interest rate put options, each of

which is known as a floorlet.

An Interest Rate Collar

A collar is a combination of buying a cap and simultaneously selling a floor. The strike

levels are generally decided such that the net premia outflow is zero.

Collar = Cap - Floor

Swaptions

Swaptions are options on Interest Rate Swaps. The payer of a Swaption has an option

to enter into a payer swap (pay a Fixed Rate and receive a Floating Rate). The receiver

of a Swaption has the Option to enter into a receiver swap (receive a Fixed Rate and pay

a Floating Rate).

Treasury Operations Basics 59

4. Foreign Exchange Markets – Introduction

Chapter objectives:

1. To identify the products and participants of foreign exchange markets

2. To understand the important terminologies and mechanism of spot and derivative

markets

3. To recognize the factors that affect foreign exchange markets

4.1 Overview of Global Forex Markets

The market that facilitates exchange of currencies is the Foreign Exchange Market. The

world is emerging as a global economy because of flow of goods, services and capital.

For each transaction of goods and services, there is a corresponding currency

transaction, which forms a part of international network of payments. The foreign

exchange market is that in which currencies are bought and sold against each other.

The foreign exchange market is largely an OTC market. This means that there is no

single market place or an organized exchange, electronic or physical (like stock

exchange) where all trades are executed between exchange members. The traders sit in

the offices (foreign exchange dealing rooms) of major commercial banks around the

world and communicate with each other through telephones, telexes and other electronic

means of communication.

The market spans all time zones of the world and functions virtually round-the-clock,

enabling a trader to offset a position created in one market using another market. The

major market centers are London, New York and Tokyo. Other important centers are

Zurich, Frankfurt, Hong Kong and Singapore.

Treasury Operations Basics 60

4.2 Products and Participants in Foreign Exchange Markets

The participants in the foreign market can be classified under three broad categories:

Non-bank Entities who wish to exchange currencies to meet or hedge contractual

commitments (arising out of, for e.g., import or export contracts in foreign

currencies). Many multinational firms engage themselves in forward contracts to

protect the home currency values of foreign currency denominated assets and