Embed Size (px)

Citation preview

1

Understanding Agricultural Risks:

United States Department of AgricultureRisk Management Agency

Introduction to

Risk ManagementProductionMarketingFinancialLegalHuman Resources

Revised December 1997

2

CONTENTS

INTRODUCTION: IT’S A WHOLE NEW BALL GAME.......................................................... 3

UNDERSTANDING GOALS AND RISK TOLERANCE .......................................................... 4

UNDERSTANDING PRODUCTION RISKS ............................................................................. 6

Enterprise Diversification

Crop Insurance

Contract Production

Evaluating New Technologies

UNDERSTANDING MARKETING RISKS ............................................................................... 9

Personal Considerations in Marketing

Developing a Marketing Plan

Marketing Plan Discipline

Marketing Tools

UNDERSTANDING FINANCIAL RISK .................................................................................. 13

Farm Records and Financial Analysis

Interest Rate Risk

Liquidity and Meeting Cash Flow Requirements

Insurance

Family Living Costs

Legal Issues and Security

LEGAL ISSUES ASSOCIATED WITH AGRICULTURE ........................................................ 16

Structural Issues

Contract Arrangements

Statutory Obligations

Tort Liability

Environmental Liability

Summary

HUMAN RESOURCE ISSUES ................................................................................................. 18

Managing People

Estate Planning

3

It’s A WholeNew Ball Game

Risk has always been a part of agriculture. But, farming inAmerica is a ball game that has changed dramatically over thepast few years. Increasingly, farmers and ranchers are learningthat it is now a game with new rules, new stakes, and, most ofall, new risks.

The nation’s most successful farmers are now looking at adeliberate and knowledgeable approach to risk management as avital part of their game plan. For them, risk management meansfarming with confidence in a rapidly changing world. It is theability to deal with risks that come with new, attractive farmingopportunities.

This handbook is part of a campaign to improve the riskmanagement skills of American farmers and ranchers. Theurgent need for this campaign stems from many changes inproducers’ business environment. In this environment,opportunities have increased, but so have the risks. Some of themore important changes affecting producers’ risks include:

A changing governmental role. Increasingly, governmentpolicy makers are placing greater confidence in the abilityof producers to make sound business decisions. They havepassed market-oriented farm legislation and crop insurancereforms which allow producers to be more active inmanaging their profit opportunities and risks.

Outside forces. Many factors are forcing producers to makerisky, but potentially profitable, decisions regarding theirbusinesses. These factors include increased globalcompetition, rapid changes in the structure of productionagriculture, changes in the marketing of agriculturalproducts in the farm supply sector, new technology, andmore volatile weather patterns.

Risk connections. Increasingly, decisions in certain riskareas are affecting the riskiness and profitability of otheraspects of farming. For instance, more lenders are nowrequiring sound business plans before approving credit.Thus, good management of marketing risks can lowerborrowing costs and result in long-run financial stability. Asfarmers become more aware of the many such connectionsbetween their risks, the need for effective risk managementwill increase.

A broad array of established risk management tools arethere, ready to be used. At the same time, a growing interest in

agricultural risk management is encouraging the development ofexciting new tools and services. By learning about and usingthese tools, U.S. farmers and ranchers can build the confidencethey need to deal with both the risks and the excitingopportunities of the future.

How To Use This HandbookHow can you better manage risk? Well, for starters, you can

assess your risk management skills by conducting an annualRisk Management Checkup—one that identifies the interactionsbetween one source of risk and another and causes you to takeaction.

We have identified five primary sources of risk: Production,Marketing, Finance, Legal, and Human Resources.

Since risk management should be driven by your goals, thishandbook first reviews goal setting and risk tolerance.Succeeding chapters will then give you insights into the benefitsof improved risk management in each specific area. As youreview these chapters, look for instances of the connectionsbetween the various areas of risk. Also, consider questions to askyourself or the professionals whose help you may need.

Remember, you are not competing by yourself. You have awhole team of professional players prepared to help you win.Who are your teammates? They are grain elevator operators,commodity brokers, crop insurance agents, loan officers,extension educators, commodity organizations, cooperatives,lawyers, accountants, and the people in local USDA offices.

Your teammates are currently mastering new skills,identifying new opportunities, and learning how to play as ateam. Remember, it’s a new ball game for them, too. But, each ofthem has unique strengths, skills, and experiences. The mosteffective way for you to use them is to make them part of yourteam. Share your game plan with them. Then, use their strengthsto help your plan succeed.

Start now to think about risk management as a key elementof the new ball game of agriculture—a game that you can win.Learn the fundamentals, use your teammates, then act on whatyou learn. Make risk management an important part of yourgame plan!

3

4

UNDERSTANDING GOALS

While no two people share the samegoals in life, all of the people involvedin a family business must share somecommon goals. Identifying thoseshared goals, involving everyone in thegoal-setting process, and then acting to-gether to achieve those goals should bea serious effort that focuses both the in-dividual and the organization. After all,a family business cannot be successfulif it does not help fulfill the individualdreams of everyone involved.

Many times, the hardest thingabout setting risk management goals isreconciling different views about risk.People have different answers for thesame fundamental questions....What are my risks? What are our risks?What is an acceptable level of risk?What should we do about the risks?Recognizing and acting on opportuni-ties as well as trying to minimize lossescan help shape agreement on funda-mental risk management goals.

Benefits of Goal Setting:• Reflects your values, interests,

resources and capabilities. An honestgoal-setting session for yourself, yourfamily, and your business will causeyou to take inventory of those things.

• Provides a basis for your deci-sions and a focal point for everyoneinvolved. Well-understood organiza-tional goals allow every individual inthe organization to set realistic personalgoals.

• Establishes priorities for the allo-cation of scarce resources. What thingswill you do today and what things willyou do in the future? For example,what priorities have you established forusing net farm income? Buy land, payfor college, pay down debt?

• Provides a means for measuringprogress. Which decisions madeprogress toward your goals and whichdecisions need to be reevaluated?

What Is Your Risk Tolerance?Your risk tolerance is reflected in theways you choose to manage risks. Un-derstanding your choices andconsidering each of them may causeyou to change your management styleto more closely reflect your tolerancefor risk.

Risks can be handled in one of fiveways, or in certain combinations of thefive:

1. Retain (With no protection fromdownside risk, as in holding anunpriced commodity.)

2. Shift (A contractual arrangementwhere someone else takes on some ofthe chance of a negative occurrence inexchange for a premium. The more riskyou shift, the higher the cost.)

3. Reduce (Keeping fences in goodrepair to keep livestock off the highwayand a marketing plan that locks in somelevel of guaranteed return are examplesof reducing risk.)

Some Questions for Your RiskManagement Check-up:

• Are my goals written, rea-sonable, and measurable?

• Are my goals attainable inmy lifetime?

• Have I shared my goalswith everyone involved in thebusiness and have they sharedtheir goals with me?

5

4. Self-insure (Emergency reservesfunded from previous years’ profits.)

5. Avoid (Not selecting a particularenterprise...not pushing either end ofplanting windows...not increasing yourdebt-to-asset ratio beyond your comfortlevel.)

Any risk must be evaluated for itsfrequency of occurrence and its pos-sible negative consequences. As ageneral rule, formal insurance strate-gies are available for risks with lowoccurrences but with severe negativeconsequences. Examples include dis-ability insurance, health insurance, cropinsurance and life insurance.

Benefits of Identifying Your RiskTolerance and Assessing Your Risks:

• Allows you to identify and ex-clude those alternatives which exposeyou to unacceptable risks.

• Helps guide providers of riskmanagement services to the best op-tions for you.

• Ensure that your insurance dollarswill be spent wisely.

• Increases the likelihood that youwill select the best combination of riskmanagement strategies.

Some Questions for Your RiskManagement Check-up:

• Have I identified my riskmanagement tolerance?

• Have I communicated mytolerance for risk to the profes-sionals who provide me with riskmanagement services?

• Which risks can keep mefrom attaining my goals?

• Which risks am I comfort-able retaining and managing withmy own resources? Which riskswill I shift to others? Which will Iavoid?

• When was my last insurancecheck-up for health, life casualty,property, disability, long-termcare, Medicare/Medicaid and cropinsurance?

• Have I established a confi-dent relationship with my riskmanagement advisers, so that theycan help me assess my businessand personal risk exposure?

6

Agricultural production implies an ex-pected outcome or yield. Variability inoutcomes from those which are ex-pected poses risks to your ability toachieve financial goals.

The major sources of productionrisks are weather, pests, diseases, theinteraction of technology with otherfarm and management characteristics,genetics, machinery efficiency, and thequality of inputs. Following are somerisk management strategies you canconsider to lower production risks.

Enterprise DiversificationDiversification is an effective way ofreducing income variability. It is thecombining of different production pro-cesses. For instance, diversification caninclude different crops, combinationsof crops and livestock, different endpoints in the same production process(such as different selling weights), ordifferent types of the same crop (suchas yellow, white, waxy or high-proteincorns). Diversification can also beachieved through different incomesources, such as off-farm employmentfor smaller farms.

Effective diversification occurswhen low income from one enterpriseis simultaneously offset by satisfactoryor high incomes from other enterprises.It typically reduces large year-to-yearvariations in income. However, diversi-fication is becoming increasinglycostly, as capital investment require-ments become greater. Diversificationcan ensure adequate cash flow formeeting production costs, debt obliga-tions, and family living needs.

UNDERSTANDING PRODUCTION RISKS

Crop InsuranceManagement of yield or price riskthrough the purchase of crop insurancetransfers risk from you to others for aprice which is stated as an insurancepremium. Crop insurance is an exampleof a risk management tool that not onlyprotects against losses but also offersthe opportunity for more consistentgains. When used with a sound market-ing program, crop insurance canstabilize revenues and potentially in-crease average annual profits.

Crop insurance provides two im-portant benefits. It ensures a reliablelevel of cash flow and allows moreflexibility in your marketing plans; ifyou can insure some part of your ex-pected production, that level ofproduction can be forward-priced with

Some Questions for Your RiskManagement Check-up:

• What knowledge and man-agement capabilities do I needfor an additional enterprise? Arethey readily available? Do I havea serious commitment to a newenterprise?

• Which additional capital in-vestments would I need todiversify?

• What are the added laborneeds of a new enterprise?

• Where are new markets?

• What is the income relation-ship between a prospective newenterprise and my existingenterprise(s)? Will the new enter-prise provide effectivediversification?

greater certainty, creating a more pre-dictable level of revenue.

With the elimination of ad hoc di-saster payments and deficiencypayments, crop producers will nolonger receive government aid duringyears of crop disasters or price supportpayments during low price years. Cropinsurance provides partial replacementfor the Federal safety net.

Insurance companies offer a widevariety of crop insurance protection andcoverage levels. The basic Multiple-Peril Crop Insurance (MPCI) programprotects against yield shortfall by pro-viding coverage against most naturaldisasters. The level of protection can beselected as a percentage of your historicyield.

Crop Revenue Coverage (CRC)protects against both yield and pricelosses. It is currently offered for corn,soybeans, grain sorghum, cotton, andwheat in selected states and counties.Its combined price and yield feature as-sures producers that they will earn aminimum revenue. The yield guaranteeis set using each producer’s Actual Pro-duction History (APH), just as it is inMPCI policies.

Group Risk Protection (GRP) issimilar to the basic MPCI program, ex-cept that the yield guarantees andindemnity payments are based oncounty yields rather than on individualfarm yields. This program is attractiveto producers whose farm yields closelytrack county yields and where crop di-sasters, such as drought, affect a widearea.

Other programs are currently beingoffered on a pilot basis in limited geo-graphical areas. These include IncomeProtection (IP) and Revenue Assurance

7

(RA). These revenue programs offerprotection against those combinationsof yields and prices which result in rev-enues which are below a guaranteedminimum.

The premiums for all of these cropinsurance policies are subsidized by theFederal government. Subsidies tend tobenefit those producers most who in-vest in higher levels of coverage.

Examples of private, non-subsi-dized crop insurance programs includecrop-hail insurance, which offers pro-tection for one specific peril (hail), andvarious products which supplementfederally subsidized insurance.

all crop insurance policies are fullysubsidized by the Federal government,although most farmers will pay an ad-ministrative fee. Farmers with limitedresources may be eligible for a waiverof the fee for CAT coverage. Any cropinsurance agent can assist producers indetermining if they are eligible for a feewaiver.

Crop insurance is currently avail-able on over 60 crops. For those cropswhich are not insurable, or for whichinsurance is not available in an area,producers can apply for the NoninsuredAssistance Program (NAP). NAP pro-vides coverage roughly similar to theCAT level of crop insurance. AlthoughNAP requires no administrative fee, itmust be applied for prior to planting.Producers should file an annual acreageand production report with the localUSDA Farm Service Agency (FSA) of-fice.

Contract ProductionContract production is normally associ-ated with vertical integration, where anagribusiness firm coordinates all as-pects of a product from production tothe consumer’s table. Contract produc-tion is common in poultry and livestockproduction. The agribusiness firm pro-vides feed and other inputs to theproducer, who manages the grow-outprocess.

Through production contracts, theagribusiness firm commits the producerto deliver a specific quality and quan-tity of final product. The producer mustcomply with the firm’s quality specifi-cations and must manage yield riskwith insurance and sound managementpractices.

Before you agree to a productioncontract you need to consider thetradeoffs. A major advantage for theproducer is that a market for the outputand, very often, a favorable price isguaranteed. A disadvantage is that theproducer loses the opportunity of ben-efitting from upside price potential,since the sale of the product is fixed byconditions of the contract.

The loss of flexibility and profitopportunities is the cost of receiving apredictable cash flow. The challengeassociated with contract production isto find contracts that are consistent withthe producer’s goals and risk tolerance.

Some Questions for Your RiskManagement Check-up:

• How much coverage do Ineed for adequate cash flow?

• Which crop insurance prod-uct will best complement mymarketing plan?

• What are the implications ofa crop loss on my ability to meetmy debt obligations?

• What are the major sourcesof production risk and what typeof crop insurance coverage do Ineed to protect against thoserisks?

• What are the costs of thevarious types of coverage andwhich offers the best protectionfor the level of coverage I need?

Part of a crop damaged by hailmight be less than the deductible on anMPCI policy. In this instance, crop-hailinsurance can fill the coverage gap. AnMPCI policy protects against losses se-vere enough to significantly drop thewhole farm’s yield average. Crop-hailinsurance, on the other hand, givessupplemental, acre by acre protectionthat more accurately reflects the actualcash value of damage from hail.

Crop insurance is available onlythrough private crop insurance agents.Coverage for a crop must be arrangedbefore its sales closing date.

Catastrophic Risk Protection(CAT) is the lowest level of MPCI cov-erage. Premiums for the CAT portion of

8

Evaluating New TechnologiesThe challenge of evaluating new tech-nologies is best illustrated by the twonewest crop technologies: geneticallyaltered seeds and precision farming.

For instance, some seeds are beinggenetically altered to provide resistanceto specific herbicides, thereby permit-

Some Questions for Your RiskManagement Check-up:

• Which benefits will a pro-duction contract provide?

• What flexibility will I giveup?

• Do I understand the condi-tions of the contract? Do I needlegal advice?

Some Questions for Your RiskManagement Check-up:

• What are the economictradeoffs between more aggres-sive pest control and minimalcontrol?

• Are my pest managementstrategies consistent with mymanagement philosophy aboutenvironmental quality?

• Will more intensive moni-toring of pests be an economicalstrategy?

ting improved weed control. Otherseeds are being engineered to provideresistance to diseases or insects.

Precision farming controls the rateof application of crop inputs such asseed, fertilizer and pesticides on eachacre of a field. By contrast, the conven-tional approach applies the same rateacross an entire field. Precision farmingallows yields to be measured for eachacre so that output can be strictly mea-sured against crop inputs.

As with all new technologies,farmers who adopt these new innova-tions try to capture a range of potentialbenefits, including lower input costsand environmental quality. Benefits caninclude higher crop yields due to im-proved pest control and morecost-effective use of crop inputs.

• What is the economic benefitof adopting new technology?

You should compare each aspectof the new technology with thecurrent technology to determinethe desirability of adoption. Forexample, consider the evaluationof costs and benefits for corn seedthat is resistant to the Europeancorn borer. For this, you must esti-mate the probability of infestationby corn borers in a particular year,the cost and effectiveness ofchemical treatment for borers, andthe changes in field scouting costs.

Some Questions for Your RiskManagement Check-up:

These costs must be weighedagainst the additional $25 or $30per bushel for borer-resistant seedand any increase or decrease inyield associated with the new seed.

• Does the adoption of a newtechnology reduce my risk?

New technology can provide only anarrow “insurance policy” if it pro-tects against only one pest. Otherinsects, diseases, and weather con-ditions will influence yield too.

• Would it be more profitable tomanage risk by purchasing seed that

is resistant to a specific pest or bydiversifying production over sev-eral crops? For instance, woulddiversification encourage thespread of natural predators of thecorn borer?... Or would it give theborer sanctuary?

• Would it be a better risk strat-egy to simply buy crop insurance,regardless of the specific factorthat might cause a reduction inyield reduction, than to buy seedthat is resistant to a specific pest?

9

Marketing is that part of your businessthat transforms production activitiesinto financial success.

Unanticipated forces, such asweather or government action, can leadto dramatic changes in crop and live-stock prices. As agriculture movestowards a more global market, theseforces stem increasingly from worldfactors. Other farmers’ weather andother governments can affect yourprices. When these forces are under-stood, they can become importantconsiderations for the skilled marketer.

To be successful, you should takean informed and balanced approach tomaking marketing decisions. Focus onlong-term profitability, not short-termwindfalls. Academic studies indicatethat marketing strategies which dependon price chasing or speculation havenot been shown to be consistently prof-itable. Also, those strategies that do notconsider financial and production riskswill likely prove to be poor.

Personal Considerations in MarketingMarketing agricultural products in-

volves information, objectivity, attitudeand skill. You should develop market-ing plans and strategies that work foryou. Here are three important consider-ations in developing a marketing plan:

1. Know what level of risk you arecomfortable with.

Inability to control market forces anddifficulty in predicting those forcesmake marketing an inexact science. Abetter understanding of your financialsituation and the possible consequences

UNDERSTANDING MARKETING RISKS

of your decisions will remove some ofthe uncertainty from marketing deci-sions. Obviously, marketing involvesunderstanding your level of risk toler-ance. It also involves a goodunderstanding of your current financialposition.

2. Be willing to increase the num-ber of skills in your marketing toolbox.You may need to pay for professionalhelp in developing your marketingplan.

Successful marketers are continuallyupdating their abilities by learning newskills. Such efforts should be under-taken without the expectation of animmediate payoff. There are many pro-fessionals who can help you. Theseinclude futures brokers, elevator opera-tors, financial planners and farmconsultants.

3. Develop an integrated manage-ment approach to your business.

Marketing decisions should not bemade independent of other farm busi-ness decisions. They should be plannedaccording to the impact they will haveon the production, financial, legal andhuman resource aspects of your busi-ness. Marketing decisions often involvecontractual agreements that have im-portant legal consequences. Thesecontracts can significantly affect finan-cial plans.

Developing a Marketing PlanManaging market risk begins with amarketing plan. The goals and objec-tives of your business should drive themarketing plan.

An accurate understanding of pro-duction costs is a critical part of asound marketing plan. . . for you andfor professionals who work with you.There may be times when the marketprice fails to cover all of the costs asso-ciated with production. A break-even

Some Questions for Your RiskManagement Check-up:

• Am I financially able to“shoot for the top price” andwithstand the potential downsideconsequences of missing it?

• Can I afford to store a crop,hoping the price will increase, orare my cash flow needs such thatI must sell directly at harvest?

• Will my lender understandmy plan and help me achieve mygoals?

• When cattle prices are mov-ing downward, am I financiallyable to retain ownership of feedercalves and sell them at higherweights later?

• What are the potential costsand returns associated with alter-native strategies?

• Should I seek professionalmarketing services?

• Would a “marketing club”fit my need for current informa-tion and help in developing amarketing plan?

10

price should serve as an important ref-erence, even though it is usually notyour desired price.

An analysis of supply and demandis important in developing targets foryour marketing plan. Supply and de-mand projections are published by theU. S. Department of Agriculture and byprivate firms. Early in the growing sea-son, expectations are highly uncertain.However, commodity markets responddecisively to these projections, so youshould be aware of them.

You should also be aware of pricesreceived in your area and know the av-erage prices received in previous years.Again, you have a choice of learningthese skills and monitoring this infor-mation yourself, or hiring aprofessional to help you.

Financial considerations such ascash flow requirements, including fam-ily living needs, should be incorporatedin your marketing plan. Financial cir-cumstances and other personal factorshelp determine your ability and willing-ness to tolerate market risks. Marketingplans should be as unique as the finan-cial, production, and managementcharacteristics of each individual pro-ducer. What works well for a neighbormay not be appropriate for you andyour family.

Marketing Plan DisciplineMarketing involves emotion, science,discipline, and analysis. The best mar-keting plan will fail without theself-discipline to stay on track. Unfor-tunately, letting emotions rule is easywhen prices are moving. When pricesrise, it is hard to resist trying to squeezean extra few cents from the market.And, it is easy to panic when pricesfall. In marketing, NOT making a deci-sion IS a decision. A marketing plan isof little value if actual decisions deviatefrom the plan. Having a written market-ing plan will help ensure discipline.

Contingency plans, as part of thebasic marketing plan, will also help.What to do if the price doesn’t reachthe desired level and what to do if thecrop is not as large as expected are im-portant contingency actions when themarket does not develop according toyour general expectations.

Some Questions for Your RiskManagement Check-up:

• Does my marketing plancover the entire calendar or cropyear?

• Are all crop and livestockenterprises covered in my plan?

• Have I checked my market-ing plan against my financialplan to make sure that incomefrom marketing covers cash flowneeds?

• Have I calculated produc-tion costs and estimated my yieldto determine my breakevenprice?

Marketing ToolsLearning about the full range of pricerisk management tools will allow youto become a better marketer and riskmanager. Selecting the right tool to useat the right time will not only reducerisk, it could increase your profit. Fol-lowing are a basic overview of morecommonly used pricing strategies andguidelines for determining when to useeach.

Storage( with no protection).Storage is a way of avoiding seasonallylow prices. When prices are below thelevel anticipated in the marketing plan,storage may be justified, assuming thatyou have adequate financial resources.Storage may be warranted when thereis a realistic expectation of a marketprice increase. Historical data indicatethat the market is often willing to payyour storage costs. However, storedgrain can go out of condition and issubject to theft.

Cash Sale. When prices are favor-able and at levels anticipated in themarketing plan, a direct cash sale iswarranted.

Deferred Payment Contracts.Deferred payment contracts allow forthe current pricing and delivery of thecrop, but can delay the receipt of pay-ment. They are often used as an incomemanagement tool for tax planning pur-poses. A deferred payment contractmakes the seller an unsecured creditorof the elevator. This has implicationsboth for legal and for financial risk ex-posure.

Fixed Price Contract for DeferredDelivery. This contract allows produc-ers to establish a price for laterdelivery. A fixed price contract, alsoknown as a cash forward contract, may

11

allow you to schedule deliveries attimes of the year that better fit with la-bor, grain quality, and logistics. Havingan adequate amount of crop insuranceallows you to comfortably contract theinsured portion of your crop. Thesecontracts often work well when cropsare large, when storage is tight, orwhen the market price reaches the ob-jective in your marketing plan.

Basis Contract. Basis is the differ-ence between the local cash price and afutures contract price. Basis is typicallymore stable and predictable than eitherthe underlying futures contract or thelocal cash price. However, basis doeschange in response to local supply anddemand factors. A basis contract allowsyou to fix the basis, but allows the finalcash selling price to be determined at alater date by subtracting the fixed basisfrom the futures price. This strategyworks well when the basis is strong(cash prices are high relative to futures)and there is some potential for an in-crease in futures prices. MPCI orrevenue insurance can give you theconfidence to enter into basis contractswithout the concern of not having acrop to deliver.

Deferred or Delayed Price Con-tract. A deferred or delayed pricecontract transfers title of a crop to thebuyer at delivery, but allows the sellerto set the price later. It is commonlyused when storage is tight. At thesetimes, the local elevator wants to movemore grain into the marketing channel,but the seller may not be satisfied with

current prices. When producers havecrop insurance, they have a guaranteed,minimum production level. They can,therefore, safely use deferred price con-tracts early in the growing season.

Minimum Price Contract. A mini-mum price contract establishes a floorprice for the duration of the contract.The floor price is typically severalcents below the cash price at the begin-

ning of the contract. A producer couldnet less with a minimum price contractthan with a fixed price contract if pricesfall, but will benefit from a rise in mar-ket prices. This contract eliminatesmuch downside price risk.

Hedge-to-Arrive (HTA) Contract.This contract has risk managementproperties similar to a short futuresmarket position. It is the opposite of abasis contract. It permits the seller toset the futures price level by the deliv-ery date, but the basis is determinedlater. The seller is responsible for deliv-ering the contracted amount on thedelivery date.

Short Futures Hedge. Selling fu-tures contracts to protect the value ofgrain or livestock in inventory or thevalue of expected production is a shortfutures hedge. A short futures hedge re-duces downside price risk. On the otherhand, it also reduces the ability to cap-ture upside price movements.

Put Option Purchase. This tool issimilar to a minimum price contract. Itsets a floor on the crop or livestockprice throughout the life of the contract.If prices rise during the period, theseller can capture upside price gains.

Contracted Production. Manyvariations of this type of contractual ar-rangement exist. Historically,production contracts have been used forspecialty crops, poultry, and livestock.Purchasers have been willing to offersuch contracts to fulfill the need forhighly specific agricultural products.Recently, contracted production hasbeen offered on an increasingly broaderrange of crops and livestock. Contractproduction reduces flexibility and theopportunity to capture upside price po-tential. But, it assures a relativelyreliable cash flow.

Marketing Cooperatives. Formingand participating in marketing coopera-tives provides members the opportunityto benefit from volume sales or pur-chases. Benefits may be in the form ofenhanced prices received or reducedcosts. There has been an increased in-terest in marketing cooperatives forboth crops and livestock.

12

Direct Sales. For some producers,selling directly to final consumers is away to enhance profitability and reducerisk. Smaller farms near populationcenters may especially benefit from di-rect sales. Examples include the salesof fruits and vegetables through road-side stands and “you-pick” operations.Also, some producers can increaseprofits and reduce risk with specialtylivestock products, like “all natural”beef, which reach a specialized marketniche.

• Which marketing tools aremost familiar to me?

• How can I learn the basics ofunfamiliar marketing tools?

• Does the use of a particularmarketing tool preclude the use ofothers? If it does, have I weighedall the alternatives?

Some Questions for Your RiskManagement Check-up:

• Is the use of a particular mar-keting tool likely to enhanceincome, reduce risk, or both?

• Can my marketing plan beexecuted without undue influencefrom income tax and cash flow de-mands?

13

Financial risk has three basic compo-nents: 1) the cost and availability ofdebt capital, 2) the ability to meet cashflow needs in a timely manner, and 3)the ability to maintain and grow equity.Cash flows are especially important be-cause of the variety of ongoing farmobligations, such as cash input costs,cash lease payments, tax payments,debt repayment, and family living ex-penses.

Your objective should be to man-age this risk through sound planningand financial control. To do that, youshould continually monitor your abilityto bear financial risk.

Farm Records and Financial AnalysisA set of well-maintained financialrecords is an absolute necessity tomaintaining financial control of a farmor ranch. The flow of information iscritical in evaluating past performanceand in planning for future accomplish-ments. Financial risk management isnot achieved directly by maintainingcomprehensive records. However,records do provide much of the infor-mation needed to understand criticalfinancial risks.

Essential financial statements in-clude the balance sheet and statementof owner’s equity, income statement,and projected and actual cash flows.These records provide a history of yourbusiness and the data you need to cal-culate financial performance measures.Even small farms need a basic level ofrecord keeping.

As the size and complexity of anoperation grow, so does the need for fi-nancial records. Ratios such asdebt-to-asset, debt-to-equity, and asset

UNDERSTANDING FINANCIAL RISK

• What are my short-term andlong-term goals and how do theyaffect my financial planning?

• Was documented historicalinformation used in my financialprojections? Was it accurate?

• Which records do I need tomonitor the financial status of myoperation?

• Which records do I need todocument my borrowing requests?

• Which farm record and finan-cial analysis packages might helpme?

• What have been the trends inmy business’s key performance in-dicators?

• How do the ratios for my op-eration compare to those of similaroperations?

Some Questions for Your RiskManagement Check-up:

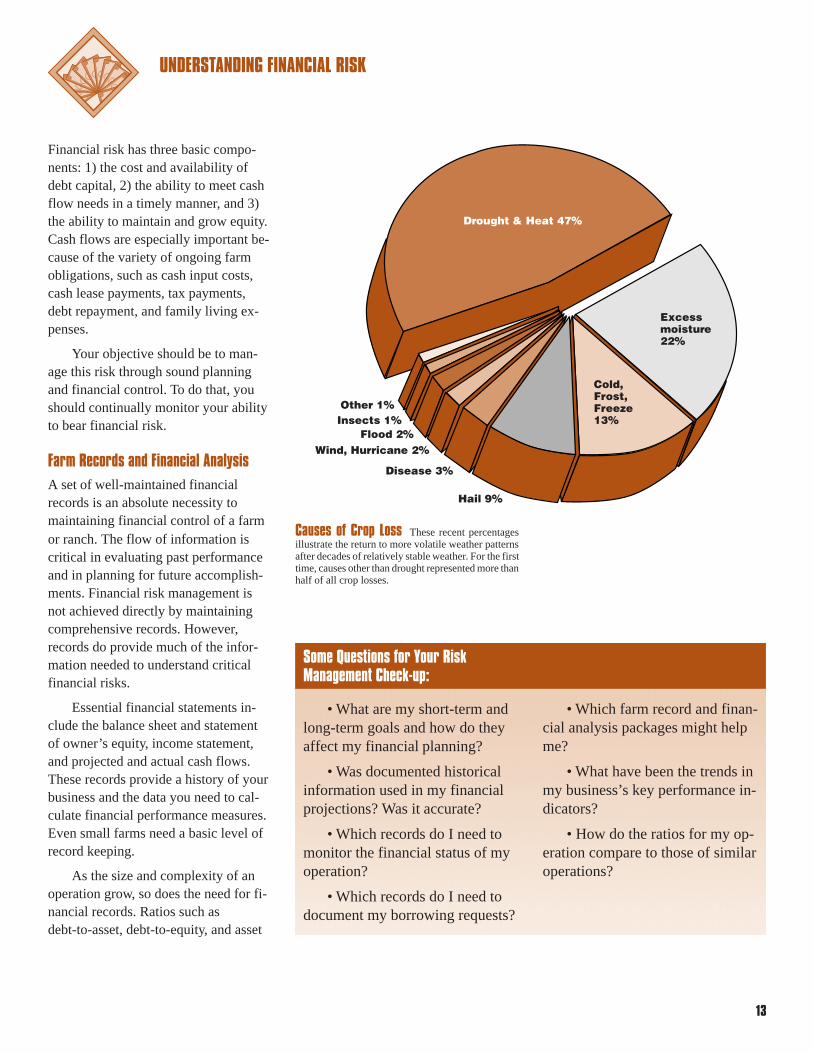

Drought & Heat 47%

Excessmoisture22%

Cold,Frost,Freeze13%

Hail 9%

Disease 3%

Wind, Hurricane 2%Flood 2%

Insects 1%Other 1%

Causes of Crop Loss These recent percentagesillustrate the return to more volatile weather patternsafter decades of relatively stable weather. For the firsttime, causes other than drought represented more thanhalf of all crop losses.

14

turnover are important in monitoringoverall financial performance. Othermeasures can be used to monitor the fi-nancial status of the business andprovide guidelines for future decisions.These examine liquidity, solvency,profitability, financial efficiency, andrepayment capacity of the business.

Interest Rate RiskInvestment decisions are based on as-sumptions about future borrowing costsor the opportunity cost of investedfunds. Borrowed capital can be a rea-sonable expense, especially if you areprudent in the financial leveraging ofyour business. After all, few operationsare in a position to use only equitycapital for new investments. Borrowingis a vital part of most farming busi-nesses.

Interest rate risk is mostly out ofyour control. However, you can some-times influence your interest rate bylowering your debt-to-asset ratio andthrough the use of crop insurancecoupled with a sound marketing plan.These actions by you reduce a lender’srisk exposure.

Liquidity and Meeting Cash FlowRequirementsEnsuring liquidity and adequate cashflow is the same as ensuring the farm’sability to survive shortfalls in net in-come relative to various cashobligations.

Assets classified as current on thebalance sheet are assets that can beconverted into cash within one operat-ing cycle of the farm business, usually12 months. Liquid assets include instru-ments that yield cash directly or thatcan be converted quickly to cash. Liq-uid assets include cash on hand,supplies, and crops and livestock to besold within the year.

Adequate liquidity is essential toensure a sufficient cash flow. Also, ad-equate liquid reserves can facilitatecontingency plans for production disas-ters or poor market conditions.

Some Questions for Your RiskManagement Check-up:

• What is the most effectiveway to monitor general financialconditions and expected changesin interest rates?

• What are alternative sourcesof financing and their terms andconditions?

• What can I do to reduce alender’s risk exposure andthereby ensure that I pay the low-est possible interest rate?

• Do I completely understandthe terms and conditions of myborrowing arrangements, includ-ing the calculation of interest?

Some Questions for Your RiskManagement Check-up:

• What alternative sources ofincome are available to me?

• What are my cash flow re-quirements for operating inputs,machinery, personnel, land costs,debt payments and farm over-head?

• What are some ways of re-ducing cash expenses?

• What are my tax obliga-tions?

• What types of personal andproperty insurance do I need?

• What are the cash flow im-plications of a crop failure or lowmarket prices?

• What is an effective contin-gency plan for meeting cash flowneeds after a crop failure or a pe-riod of low prices.

However, excess liquidity typicallygenerates lower rates of return thanfixed assets.

Timing is critical for ensuring ad-equate cash flows. With properplanning of expenses, cash flow needscan be known with reasonable cer-tainty. This allows you to planmarketing decisions in advance and totake advantage of attractive pricing op-portunities. Improving liquidity toensure adequate cash flows can includereducing family living expenditures,using resources efficiently, leasing as-sets, and utilizing appropriate insuranceprograms.

15

InsuranceThere is a lot more to risk manage-

ment than buying insurance. But,insurance can complement many otherrisk management tools. Knowing theseinteractions in risk can help you getmore value from your insurance dollar.

Benefits of insurance planning:An annual insurance review should as-sure proper coverages and protection.Just because many insurance policiesare automatically renewed is no reasonto neglect an annual examination ofyour insurance needs. A healthy “whatif” session with your insurance profes-sionals can help identify bothweaknesses and opportunities in yourcoverage.

Family Living CostsA significant component of financialrisk is controlling and meeting familyliving costs. Reducing family livingcosts may not be feasible. But, carefulscrutiny of your living costs should bean integral part of annual cash flowplanning.

In certain instances, off-farm em-ployment can be a risk managementstrategy. It can ensure that living costsare met and can increase the family’sstandard of living. It may also reducethe need to liquidate farm assets tomeet family living needs.

Questions for Your RiskManagement Check-up:

Life insurance:

• Have I compared costs andbenefits of different types of poli-cies?

• Is low-cost borrowingpower “hidden” in a long-heldlife insurance policy?

• Is my list of beneficiariesup-to-date?

• Do I need to include an in-vestment program in my lifeinsurance policy (whole life), oris pure life insurance (term) suffi-cient?

( See other sections for crop in-surance, liability insurance,health, etc.)

Legal Issues and SecurityImportant legal issues are involved inborrowing. The legal language incorpo-rated into loan contracts can beintimidating and puzzling. Neverthe-less, you should have sound knowledgeof the details and implications of all le-gal documents. You should seek theguidance of an attorney before you signimportant documents.

Some Questions for Your RiskManagement Check-up:

• Have family expenses fol-lowed projections?

• What alternative enterprisesor employment opportunities areavailable?

• Are all living expenses in-cluded in cash flow projections?

From a lender’s point of view, se-curity and repayment capacity areessential. Liens, credit life insurance,and crop insurance — coupled with asound marketing plan — can help tomake a loan more secure in the eyes ofthe lender.

From your perspective, you can en-sure continued access to debt capitalwhen you need it by maintaining accu-rate financial records and a consistentrecord of timely repayment of loans.

Some Questions for Your RiskManagement Check-up:

• Are certain contracts benefi-cial to me?

• Do I understand all the im-plications of a contract before Isign?

• When do I need to consultan attorney in regard to con-tracts?

16

Many of the day-to-day activities offarmers and ranchers involve commit-ments that have legal implications.Understanding these issues can lead tobetter risk management decisions.

Legal issues cut across other riskareas. For example, acquiring an oper-ating loan has legal implications if notrepaid in the specified manner. Produc-tion activities involving the use ofpesticides have legal implications if ap-propriate safety precautions are nottaken. Marketing of agricultural prod-ucts involves contract law. Humanresource issues associated with agricul-ture also have legal implications,ranging from employer/employee rulesand regulations, to inheritance laws.

The legal issues most commonlyassociated with agriculture fall intofour broad categories: appropriate legalbusiness structure and tax and estateplanning, contractual arrangements, tortliability, and statutory compliance, in-cluding environmental issues.

Structural IssuesThe first legal issue that many familyfarms encounter is the nature of the en-tity under which the business is to beoperated. Often, through lack of atten-tion, sole proprietorship isautomatically chosen. However, alter-natives entities exist includingpartnerships, limited partnerships, lim-ited-liability companies, andcorporations (both Subchapters C andS) as well as a wide variety of trust ar-rangements. In addition, many States,and the Federal Government, have spe-cial statutory provisions for farmsmeeting certain criteria, such as “familyfarm” provisions.

LEGAL ISSUES ASSOCIATED WITHAGRICULTURE

Income and property tax conse-quences at the local, State and Federallevel vary significantly, dependingupon the legal entity chosen. Somestructures lend themselves to the avoid-ance of estate tax and the ease ofadministration during probate. Liabilityto third parties is also a consideration instructural decisions, as is ease of opera-tion within the chosen structure.

Estate planning considerations mayarise in the course of making structuraldecisions. Estate planning mechanismsrange from simple wills to family farmcorporations with complex inheritanceprovisions. Trusts, both living and tes-tamentary, are often included in estateplanning.

Contract ArrangementsContractual arrangements in agriculturetake many forms. A contract is anyagreement (written or verbal) where theparties exchange mutual promises in re-turn for some sort of consideration orbenefit.

Contracts include financial ar-rangements, such as promissory notesand mortgages. Leases and crop sharearrangements are contracts. Many Stateand Federal farm programs are contrac-tual in nature, such as the ConservationReserve Program. Sale of agriculturalproducts is often accomplished by con-tracts for future performance. Cropinsurance coverage is also based on acontractual agreement. Even employ-ment arrangements, although often notwritten, are treated as contracts.

A basic legal issue pertaining tocontracts is their enforceability. For in-stance, many States have what isknown as “statutes of frauds,” whichrequire that certain types of agreements

be in writing before they can be en-forced. Examples of contracts whichoften must be in writing before they areconsidered valid include agreements forthe sale of real estate and agreementswhich cannot be performed within 1year.

Assuming a contract is legally en-forceable, a concern arises as tononperformance by a party to the con-tract. Obviously, nonperformance cancome from the farmer or rancher, orfrom the other party to the contract.

In many instances, contractsspecify what constitutes events of de-fault and the remedies of the variousparties in the event of default. If thecontract is unclear, the courts generallyemploy two types of relief for breach ofcontract: specific performance anddamages. In the case of specific perfor-mance, the breaching party is orderedto remedy the default and fulfill thecontract. If specific performance is notpossible or reasonable, damages areawarded to compensate the party not inbreach.

17

Contractual nonperformance canhave ramifications well beyond thescope of the contract itself. For in-stance, the inability to meet contractualfinancial obligations to your mortgagelender may result in foreclosure. Alter-natively, it may force you to seek otherlegal recourse, such as debt restructur-ing or liquidation in bankruptcy.

Statutory ObligationsA huge variety of statutory mandatesapply to farmers and ranchers. Theseinclude tax reporting and payment obli-gations, wage and hour and safetyrequirements, compliance with nondis-crimination statutes, termination ofemployees, use of pesticides and herbi-cides, participation in certain farmprograms, and many more. Althoughmany in agriculture are not fully awareof their legal obligations, failure tocomply may have serious consequencesin terms of fines, penalties and abate-ment.

Tort LiabilityTort liability arises from the negligentor intentional infliction of damage to aperson or to property. This type of li-ability is commonly insured under ageneral liability insurance policy.

The simplest type of tort ariseswhere someone is injured on a farm orranch property. In recent years, tort li-ability has broadened significantly, toinclude what may be classed as em-ployment torts, such as wrongfuldischarge. Another area of expansionhas been in the so-called “toxic tort”area in which adjacent landowners,public groups, or others assert liabilityfor damage to air and water quality onaccount of agricultural activity.

Environmental LiabilityPollution laws are a major concern forfarmers. The line between point andno-point pollution is being erased bythe courts. Many of the newer liabilitypolicies exclude coverage for pollutionclaims entirely, forcing farmers to pur-chase special pollution policies. Thepollution policies that are availablecontain unique characteristics that areunfamiliar to farmers. Managing liabil-ity risk begins with understandingliability insurance coverage.

Beyond having the proper liabilitycoverage as protection, farmers must beprepared to deal with possible criminalprosecutions by State and Federal agen-cies for environmental events. Liabilityinsurance affords no protection fromcriminal penalties assessed against afarmer by a regulatory agency. Farmerscan greatly reduce their criminal liabil-

ity exposure by formulating and fol-lowing environmental audit procedures.Many good farmers fail to keep recordsnecessary to prove compliance. Accu-rate records should be kept on theapplications of herbicides, pesticides,and fertilizers.

SummaryWhen entering into any contractual ar-rangement, either oral or written, youshould be concerned about what hap-pens if a disagreement between theparties arises. How will disputes behandled? What is the appropriate juris-diction if the contracting parties do notreside in the same county or State? Isone party liable for court costs andattorney’s fees?

When contacting an attorney, youshould ask for basic information aboutthe attorney’s familiarity with the lawfor particular situations. Attorneys arelike other professionals in that they of-ten specialize. For example, a goodcontract attorney may not have muchexpertise in estate planning. You shouldhave a good understanding of fee ar-rangements, billing cycles, expectedcosts, etc., for any matters that will in-volve your attorney.

It is a good practice to visit an at-torney prior to entering into a businesstransaction rather than after the transac-tion has gone bad. Preventive actionsare often cheaper and less time-con-suming.

Many States have publications onvarious legal topics available from theState Bar Associations. Some land-grant universities and State cooperativeextension services also have lay publi-cations about legal issues. However, forissues and concerns specific to your op-eration, contact a qualified attorney.

Some Questions for Your RiskManagement Check-up:

• Have I reviewed my prop-erty and liability insurancepolicies? Do they exclude areasthat concern me, such as pollu-tion or livestock?

• Am I covered in communityservice activities?

• What about leased buildingsor equipment?

• Are my recent acquisitionscovered, such as computers orantiques?

• Do I need to perform an en-vironmental audit? Am I aware ofand do I follow environmentalrecord keeping requirements?

18

Human resources are both a source ofrisk and an important part of the strat-egy for dealing with risk. At the core ofdealing with that risk, and that poten-tial, is your approach to managingpeople.

Managing PeopleMost families that successfully

work together have evolved a goodmanagement system, although theyusually don’t think about it as a man-agement system. Their system flowsfrom the interdynamics of lifetimesspent together, of giving and taking, oflistening to and respecting one another.But, even small family farms can ben-efit as much as large operations fromclearly defining how plans and deci-sions are to be made for the business.

Involving everyone, family andoutside employees, in the planning pro-cess can create a sense of groupownership of the goals of the organiza-tion. Workers who understand why andhow decisions are made, and exactlywhat their responsibilities are, will seeopportunities for the organization andfor themselves inside the organization.Formalizing planning and managementcan improve safety performance and re-duce legal risks arising from employeerelationships.

HUMAN RESOURCES ISSUES

Human resource management isbest viewed as a process. Seven func-tions describe that process:

1) Job analysis and job descrip-tions,

2) Hiring,

3) Orientation and training,

4) Employer/employee interaction,

5) Performance appraisal,

6) Compensation, and

7) Discipline.

You can learn more about these func-tions — what is expected from you andwhat you should expect from employ-ees — from your local library and fromyour State cooperative extension ser-vice.

Remember, hired labor is not theonly component of your human re-source team. Family, managers fromoutside the business, consultants, andexternal advisory committees can alsobe a part of your team. It is important

that everyone on your managementteam understands your risk manage-ment tools.

Human resource calamities canhamper even the most carefully madeand appropriate risk management deci-sions. Those calamities include divorce,chronic illness, and accidental death.Your risk management plans should an-ticipate the likelihood of humanresource calamities.

Remember, risk management strat-egies are implemented through people.Every manager’s job description shouldhave explicit risk management dutiesand delegations of power and authorityto manage risk.

Identifying risks and strategies formanaging those risks is an importantpart of business planning and can giveemployees confidence in their ownlong-term future with the organization.That is especially true of family mem-bers. For family members, businessplanning should inevitably lead to es-tate planning.

19

Benefits of formal planning andmanagement systems:

• Helps everyone focus on the rightpriorities.

• Allows the business to functionduring the illness or absence of a keyperson.

• Gives employees a better oppor-tunity to plan their own lives.

Estate PlanningEstate planning: the process of plan-ning for the final disposition of yourlife’s work. Will the distribution be fair,and according to your desires? Life willbe tough enough for your family andbusiness partners after your death with-out leaving tough decisions for them tomake. Estate planning is as much forthem as it is for your peace of mind.Who should have an estate plan? Any-one with business or personal assetsand with responsibility for children orparents should have an estate plan.

• Do I have a will? When did Ilast review it?

• Have I sought professionalhelp to guide me through this pro-cess?

• Can I find important docu-ments such as wills, titles toproperty, banking and investmentrecords? Is it possible for others tofind them?

Benefits of Estate Planning:• A reduction in estate tax liability,

where there is sufficient wealth to ex-ceed the legal life time limit, therebypreserving more assets for your family.

• Peace of mind for you and yourfamily.

• A distribution of assets which isaccording to your wishes.

• An assurance that your businesswill continue with the least amount ofdisruption.

Questions for Your Risk ManagementCheck-up:

• Does everyone understandour plans and decision makingstructure?

• Does everyone feel thatthey have a chance to contributeto the planning process?

• Do I understand the goals ofother family members and em-ployees?

• Do we have regularlyscheduled times for reviewinggoals and performance?

• Does everyone clearly un-derstand what has to be done tobe successful within the organi-zation?

Questions for Your RiskManagement Check-up:

• Have I explored combina-tions of ownership, trusts,disposition by will, and lifetimegifting as a way to transfer assetsto the next generation?

The United States Department of Agriculture (USDA) prohibits discrimination in its programs on the basis of race, color, nationalorigin, sex, religion, age, disability, political beliefs and marital or familial status. (Not all prohibited bases apply to all programs.)Persons with disabilities who require alternative means for communication of program information (Braille, large print, audiotape, etc.)should contact USDA’s TARGET Center at (202) 720-2600 (voice and TDD).

To file a complaint, write the Secretary of Agriculture, U.S. Department of Agriculture, Washington, D.C., 20250, or call 1-800-245-6340 (voice) or (202) 720 1127 (TDD). USDA is an equal opportunity employer.

Acknowledgements: Alan Baquet, Montana State University; Ruth Hambleton, University of Illinois; Doug Jose, University ofNebraska-LI; Jan Eliason, Ad Hoc Associates.