Embed Size (px)

Citation preview

7 - 1Copyright 2003 Pearson Education Canada Inc.

CHAPTER 7Audit Planning

and Documentation

7 - 2Copyright 2003 Pearson Education Canada Inc.

What are the What are the main reasonsmain reasons for audit for audit planningplanning??

7 - 3Copyright 2003 Pearson Education Canada Inc.

What are the What are the main reasonsmain reasons for audit for audit planningplanning??

- to enable the auditor to obtain suffi- cient appropriate evidence

$

7 - 4Copyright 2003 Pearson Education Canada Inc.

What are the What are the main reasonsmain reasons for audit for audit planningplanning??

- to enable the auditor to obtain suffi- cient appropriate evidence- to help keep audit costs reasonable

7 - 5Copyright 2003 Pearson Education Canada Inc.

What are the What are the main reasonsmain reasons for audit for audit planningplanning??

- to enable the auditor to obtain suffi- cient appropriate evidence- to help keep audit costs reasonable- to avoid misunderstandings with the client

7 - 6Copyright 2003 Pearson Education Canada Inc.

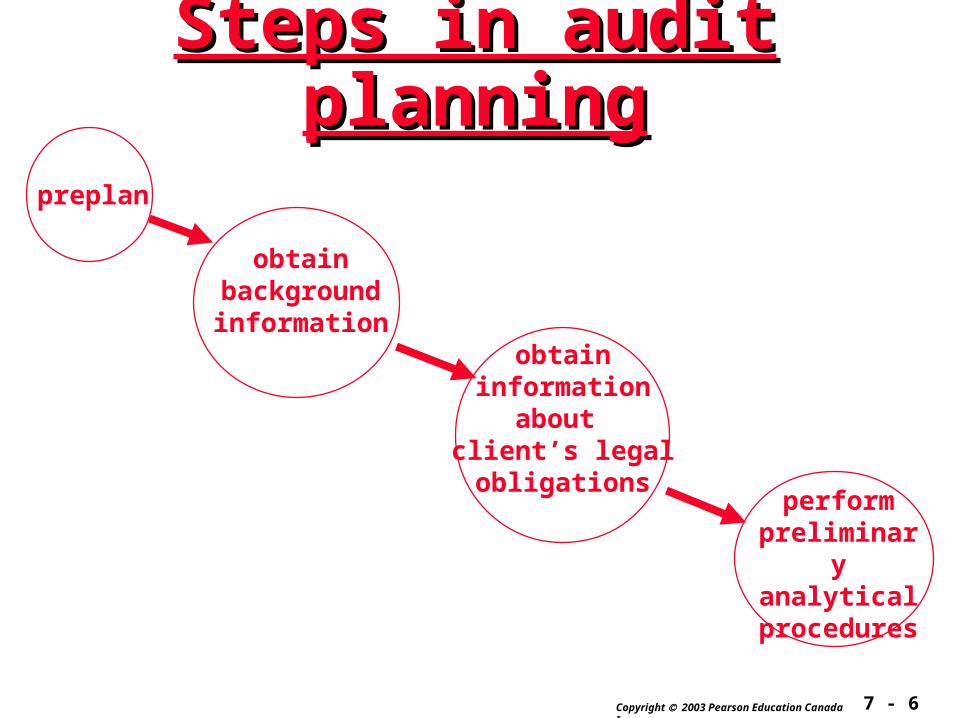

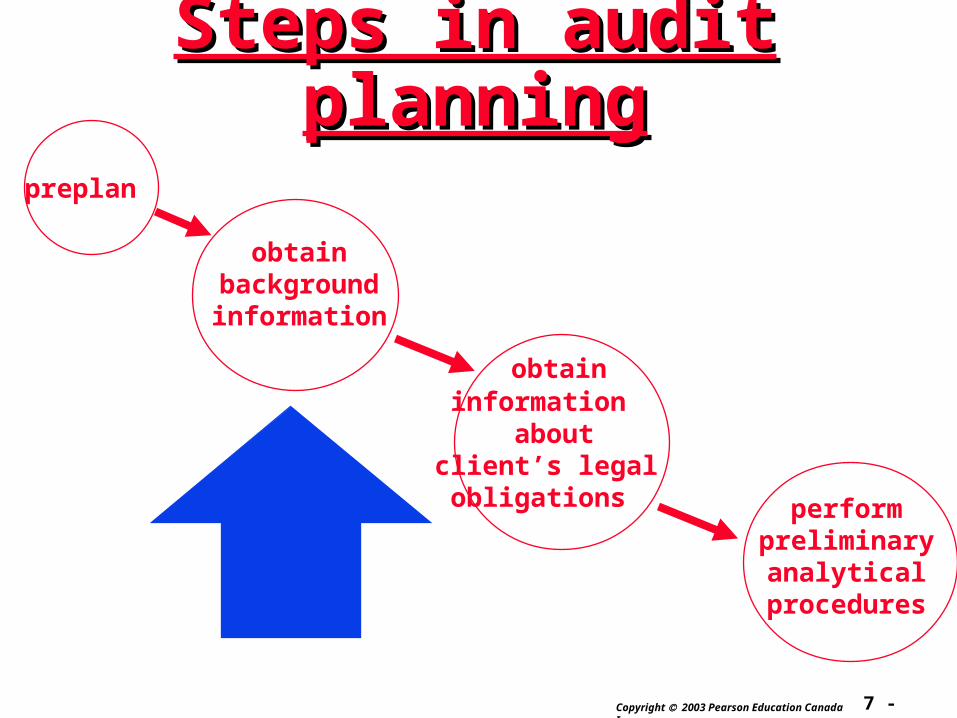

Steps in audit planningSteps in audit planning

obtaininformation

about client’s legalobligations

performpreliminaryanalytical

procedures

preplan

obtainbackgroundinformation

7 - 7Copyright 2003 Pearson Education Canada Inc.

early brainstormingearly brainstormingabout the audit about the audit

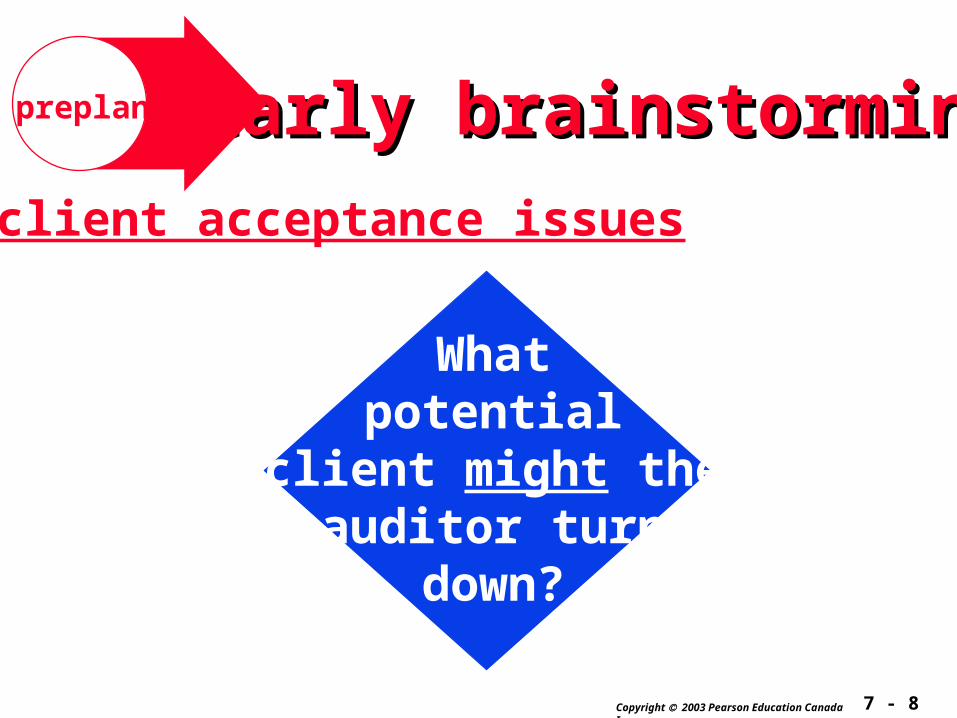

preplan

7 - 8Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues

Whatpotential

client might theauditor turn

down?

early brainstormingearly brainstormingpreplan

7 - 9Copyright 2003 Pearson Education Canada Inc.

- client lacking integrity- financially unstable client- client unable to pay audit fees

- client acceptance issues

Whatpotential

client might theauditor turn

down?

early brainstormingearly brainstormingpreplan

7 - 10Copyright 2003 Pearson Education Canada Inc.

Predecessor and Successor AuditorsPredecessor and Successor Auditors

- Rules of Professional Conduct require the successor auditor to communicate

with the predecessor.

WHY?WHY?

7 - 11Copyright 2003 Pearson Education Canada Inc.

- Rules of Professional Conduct require the successor auditor to communicate

with the predecessor

WHY?WHY?

Predecessor and Successor AuditorsPredecessor and Successor Auditors

to facilitate the successor auditor’sclient acceptance decision

7 - 12Copyright 2003 Pearson Education Canada Inc.

Predecessor and Successor AuditorsPredecessor and Successor Auditors

- Rules of Professional Conduct require the successor auditor to communicate with the predecessor- the client must give permission for the communication

7 - 13Copyright 2003 Pearson Education Canada Inc.

- Rules of Professional Conduct require the successor auditor to communicate with the predecessor- the client must give permission for the communication- the successor is required to initiate the communication

Predecessor and Successor AuditorsPredecessor and Successor Auditors

7 - 14Copyright 2003 Pearson Education Canada Inc.

Predecessor and Successor AuditorsPredecessor and Successor Auditors

- Rules of Professional Conduct require the successor auditor to communicate with the predecessor- the client must give permission for the communication- the successor is required to initiate the communication- the predecessor is required to respond

7 - 15Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues If a prospective client has not been audited before, the auditor may base client acceptance on discussions with:- lawyers- banks- other businesses

BANK

early brainstormingearly brainstormingpreplan

7 - 16Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues

- identify client’s reasons for an audit

WHY?WHY?

early brainstormingearly brainstormingpreplan

7 - 17Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit

WHY?WHY? The client’s motivation for the

audit is one of the major factors affecting audit risk.

early brainstormingearly brainstormingpreplan

7 - 18Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit

For a large business,For a large business,what is the what is the probableprobablereason for an audit?reason for an audit?

early brainstormingearly brainstormingpreplan

7 - 19Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit

For a large business, what is the For a large business, what is the probable probable reason for an audit?reason for an audit?

Companies subject to securities commission regulation are required to have annual audits.

early brainstormingearly brainstormingpreplan

7 - 20Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit

Because of Because of audit riskaudit risk, an auditor will, an auditor willtypically gather typically gather more evidencemore evidence for: for:

??

early brainstormingearly brainstormingpreplan

7 - 21Copyright 2003 Pearson Education Canada Inc.

- publicly held clients- clients with extensive indebtedness- clients changing ownership- newly formed, rapidly growing businesses

Because of Because of audit riskaudit risk, an auditor will, an auditor willtypically gather typically gather more evidencemore evidence for: for:

- client acceptance issues - identify client’s reasons for an audit

early brainstormingearly brainstormingpreplan

7 - 22Copyright 2003 Pearson Education Canada Inc.

What is an engage-ment letter and why

is it necessary?

- client acceptance issues - identify client’s reasons for an audit- obtain an engagement letter

early brainstormingearly brainstormingpreplan

7 - 23Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit- obtain an engagement letter

The intent is todocument terms of the

audit and minimizemisunderstandings.

early brainstormingearly brainstormingpreplan

7 - 24Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit- obtain an engagement letter

The letter iswritten by the auditor tothe client, then signed

by both.

early brainstormingearly brainstormingpreplan

7 - 25Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit - obtain an engagement letter

The morespecific, the better -

including:

early brainstormingearly brainstormingpreplan

7 - 26Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit - obtain an engagement letter

The morespecific, the better -

including: fees

schedules

use of clientpersonnel

early brainstormingearly brainstormingpreplan

7 - 27Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit - obtain an engagement letter

When should theletter be prepared

and signed?

early brainstormingearly brainstormingpreplan

7 - 28Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit- obtain an engagement letter

When should theletter be prepared

and signed?

in advance of any audit procedures

early brainstormingearly brainstormingpreplan

7 - 29Copyright 2003 Pearson Education Canada Inc.

- client acceptance issues - identify client’s reasons for an audit- obtain an engagement letter- select audit team

Considerations?Considerations?

early brainstormingearly brainstormingpreplan

7 - 30Copyright 2003 Pearson Education Canada Inc.

- select audit team

Considerations?Considerations?- training and overall experience

early brainstormingearly brainstormingpreplan

7 - 31Copyright 2003 Pearson Education Canada Inc.

- select audit team

Considerations?Considerations?- training and overall experience- industry and client experience

early brainstormingearly brainstormingpreplan

7 - 32Copyright 2003 Pearson Education Canada Inc.

- select audit team

Considerations?Considerations?- training and overall experience- industry and client experience- supervision

early brainstormingearly brainstormingpreplan

7 - 33Copyright 2003 Pearson Education Canada Inc.

- select audit team

Considerations?Considerations?- training and overall experience- industry and client experience- supervision- need for specialists

early brainstormingearly brainstormingpreplan

7 - 34Copyright 2003 Pearson Education Canada Inc.

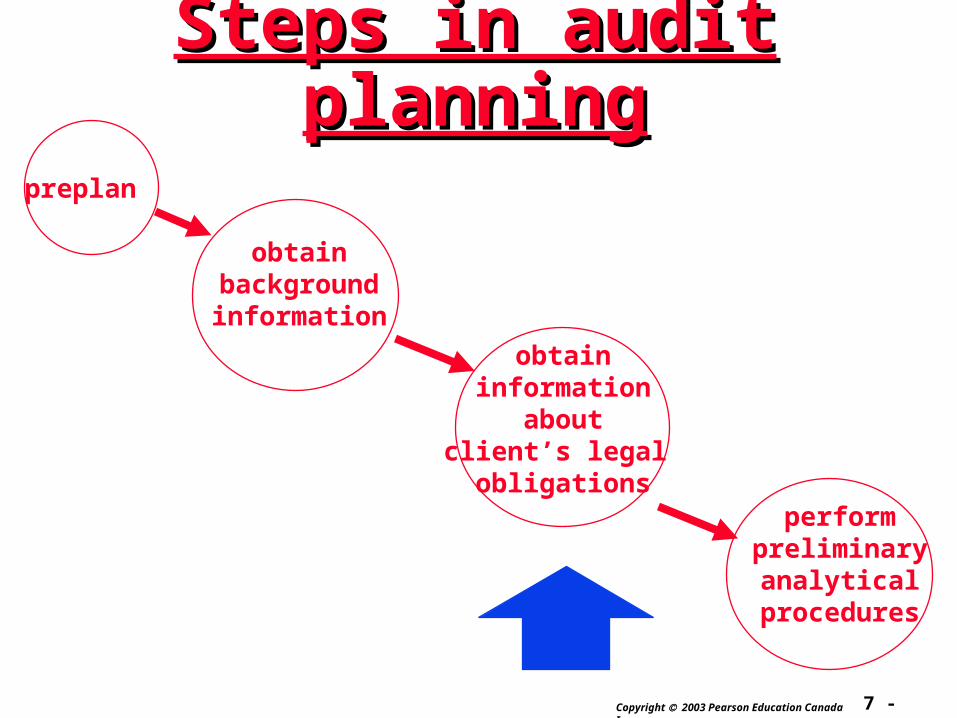

preplan

Steps in audit planningSteps in audit planning

obtain information about client’s legal obligations perform

preliminaryanalytical

procedures

obtainbackgroundinformation

7 - 35Copyright 2003 Pearson Education Canada Inc.

obtainbackgroundinformation

Why should the auditorWhy should the auditorobtain backgroundobtain background

information?information?

7 - 36Copyright 2003 Pearson Education Canada Inc.

- to identify the need for outside specialists

obtainbackgroundinformation

Why should the auditorWhy should the auditorobtain backgroundobtain background

information?information?

7 - 37Copyright 2003 Pearson Education Canada Inc.

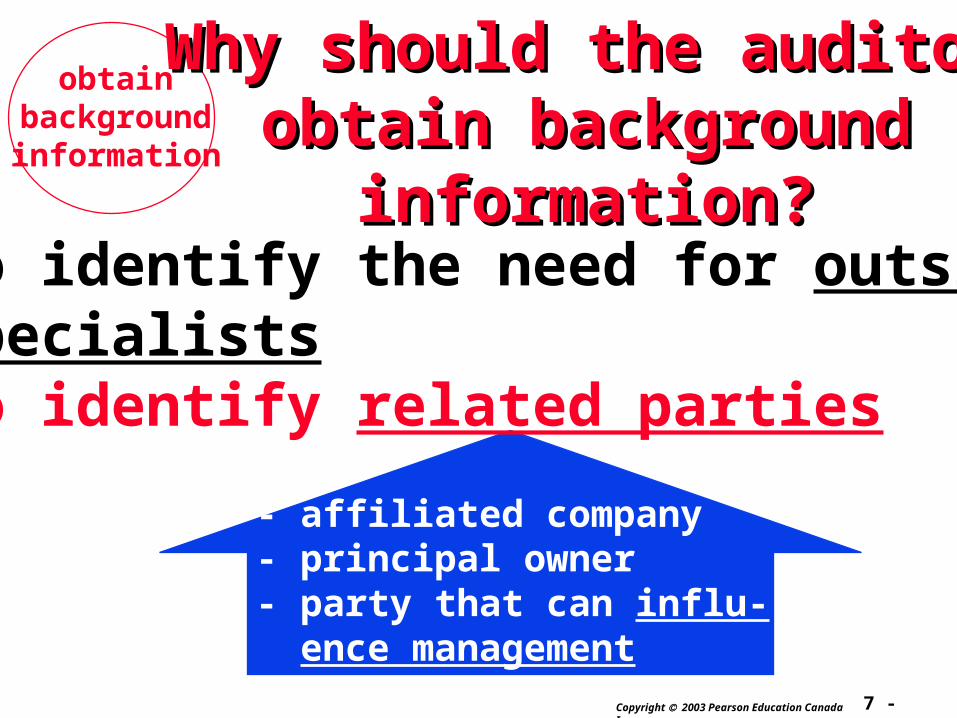

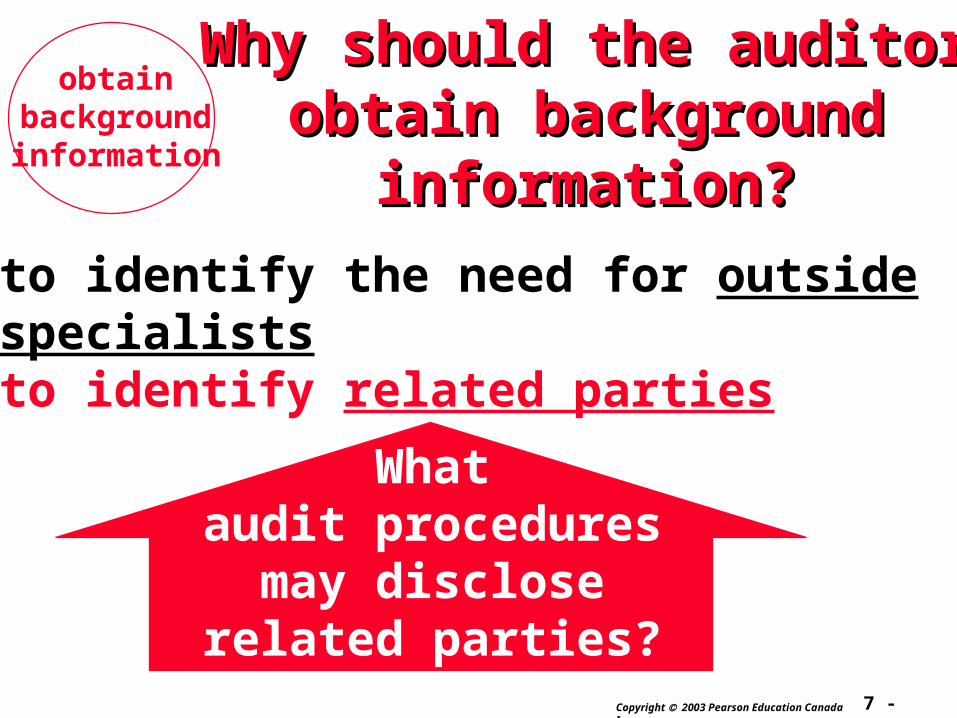

- to identify the need for outside specialists- to identify related parties

?

obtainbackgroundinformation

Why should the auditorWhy should the auditorobtain backgroundobtain background

information?information?

7 - 38Copyright 2003 Pearson Education Canada Inc.

obtainbackgroundinformation

Why should the auditorWhy should the auditorobtain backgroundobtain background

information?information?

- affiliated company- principal owner- party that can influ- ence management

- to identify the need for outside specialists- to identify related parties

7 - 39Copyright 2003 Pearson Education Canada Inc.

obtainbackgroundinformation

Why should the auditorWhy should the auditorobtain backgroundobtain background

information?information?- to identify the need for outside specialists- to identify related parties

GAAPrequires disclosure of

related partytransactions.

7 - 40Copyright 2003 Pearson Education Canada Inc.

obtainbackgroundinformation

Why should the auditorWhy should the auditorobtain backgroundobtain background

information?information?

- to identify the need for outside specialists- to identify related parties

Whataudit procedures

may discloserelated parties?

7 - 41Copyright 2003 Pearson Education Canada Inc.

obtainbackgroundinformation

Why should the auditorWhy should the auditorobtain backgroundobtain background

information?information?- to identify the need for outside specialists- to identify related parties

- inquire of management- review shareholder records for principal shareholders

7 - 42Copyright 2003 Pearson Education Canada Inc.

GAAS requires an extensiveGAAS requires an extensiveknowledge of the client’sknowledge of the client’sbusiness, industry and business, industry and

operations.operations.

obtainbackgroundinformation

7 - 43Copyright 2003 Pearson Education Canada Inc.

obtainbackgroundinformation

Why understand theWhy understand theclient’s business, client’s business,

industry or operations?industry or operations?

7 - 44Copyright 2003 Pearson Education Canada Inc.

- to determine if any unique accounting requirements exist

Why understand theWhy understand theclient’s business, client’s business,

industry or operations?industry or operations?

obtainbackgroundinformation

7 - 45Copyright 2003 Pearson Education Canada Inc.

- to determine if any unique accounting requirements exist- to identify industry risks for setting acceptable audit risk

Why understand theWhy understand theclient’s business, client’s business,

industry or operations?industry or operations?

obtainbackgroundinformation

7 - 46Copyright 2003 Pearson Education Canada Inc.

- to determine if any unique accounting requirements exist- to identify industry risks for setting acceptable audit risk- to identify industry risks for setting inherent risk

Why understand theWhy understand theclient’s business, client’s business,

industry or operations?industry or operations?

obtainbackgroundinformation

7 - 47Copyright 2003 Pearson Education Canada Inc.

- Also helps in:- determining materiality- understanding internal control- identifying sources and nature of available audit

evidence- understanding substance of transactions- assessing whether sufficient appropriate evidence

is available- assessing appropriateness of accounting policies- evaluating overall financial statement presentation

Why understand theWhy understand theclient’s business, client’s business,

industry or operations?industry or operations?

obtainbackgroundinformation

7 - 48Copyright 2003 Pearson Education Canada Inc.

obtainbackgroundinformation

What are the auditor’s What are the auditor’s sources of industry sources of industry

information?information?

7 - 49Copyright 2003 Pearson Education Canada Inc.

- prior auditors - firm industry experts- CICA research studies, audit technique studies and other publications- industry journals and other literature- discussions with management- plant and office tour- review of policies and procedures

What are the auditor’s What are the auditor’s sources of industry sources of industry

information?information?

obtainbackgroundinformation

7 - 50Copyright 2003 Pearson Education Canada Inc.

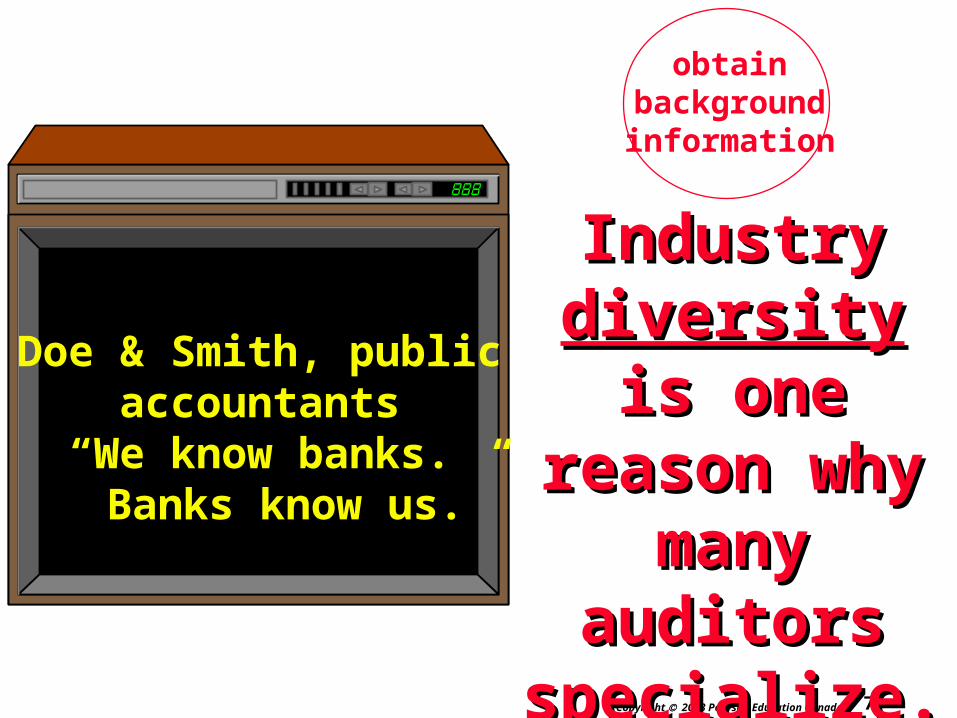

Industry Industry diversitydiversity

is one reason is one reason why many why many auditorsauditors

specializespecialize..

obtainbackgroundinformation

Doe & Smith, publicaccountants

“We know banks. Banks know us.”

7 - 51Copyright 2003 Pearson Education Canada Inc.

preplan

Steps in audit planningSteps in audit planning

performpreliminaryanalytical

procedures

obtainbackgroundinformation

obtaininformation

aboutclient’s legal obligations

7 - 52Copyright 2003 Pearson Education Canada Inc.

obtaininformation

aboutclient’s legal obligations

how?

7 - 53Copyright 2003 Pearson Education Canada Inc.

- study articles of incorporation & bylaws

obtaininformation

aboutclient’s legal obligations

how?

Articles of Incorporation

7 - 54Copyright 2003 Pearson Education Canada Inc.

- study articles of incorporation & bylaws- study minutes of board and share- holder meetings Minutes of

Board of DirectorsMeetings

Ace Company

obtaininformation

aboutclient’s legal obligations

how?

7 - 55Copyright 2003 Pearson Education Canada Inc.

- study articles of incorporation & bylaws- study minutes of board and share- holder meetings- study existing contracts

obtaininformation

aboutclient’s legal obligations how?

...it’s a deal!!

7 - 56Copyright 2003 Pearson Education Canada Inc.

Why is this part of audit planning?

obtaininformation

aboutclient’s legal obligations

7 - 57Copyright 2003 Pearson Education Canada Inc.

Throughout the engage-ment, auditors will be

observing evidence thatmay relate to these items

and their disclosure.

Why is this part of audit planning?

obtaininformation

aboutclient’s legal obligations

7 - 58Copyright 2003 Pearson Education Canada Inc.

preplan

Steps in audit planningSteps in audit planning

performpreliminaryanalytical

procedures

obtainbackgroundinformation

obtaininformation

aboutclient’s legal obligations

7 - 59Copyright 2003 Pearson Education Canada Inc.

What is thepurpose of preliminary

analyticalprocedures?

7 - 60Copyright 2003 Pearson Education Canada Inc.

What is thepurpose of preliminary analytical

procedures?

- understanding the client’s industry- assessing going concern issues- indicating possible misstatements- reducing detailed tests

7 - 61Copyright 2003 Pearson Education Canada Inc.

What are What are working papersworking papers??

7 - 62Copyright 2003 Pearson Education Canada Inc.

What are What are working papersworking papers??

auditor records of:auditor records of:

proceduresapplied

7 - 63Copyright 2003 Pearson Education Canada Inc.

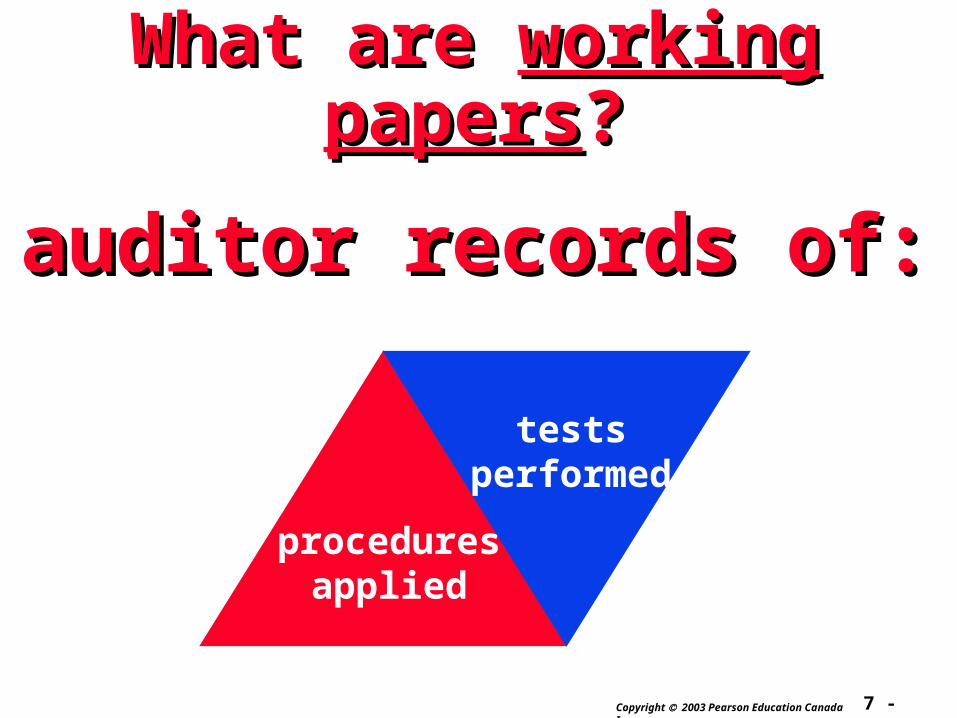

What are What are working papersworking papers??

proceduresapplied

testsperformed

auditor records of:auditor records of:

7 - 64Copyright 2003 Pearson Education Canada Inc.

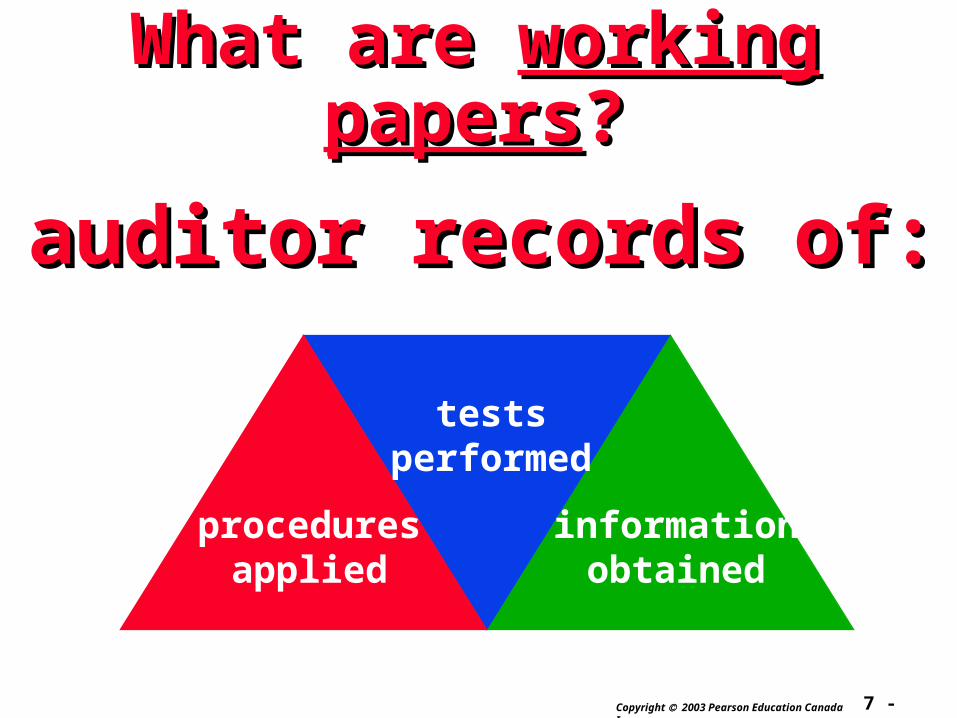

What are What are working papersworking papers??

proceduresapplied

testsperformed

informationobtained

auditor records of:auditor records of:

7 - 65Copyright 2003 Pearson Education Canada Inc.

What are What are working papersworking papers??

proceduresapplied

informationobtained

conclusionsreached

testsperformed

auditor records of:auditor records of:

7 - 66Copyright 2003 Pearson Education Canada Inc.

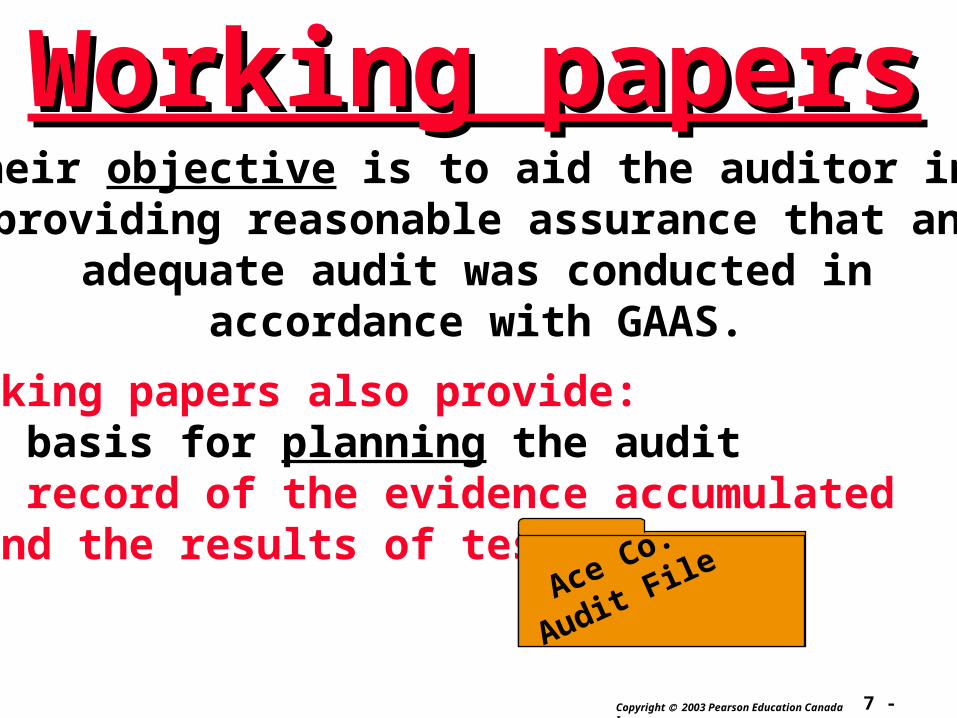

Working papersWorking papersTheir objective is to aid the auditor in

providing reasonable assurance that anadequate audit was conducted in

accordance with GAAS.

7 - 67Copyright 2003 Pearson Education Canada Inc.

Working papersWorking papers

Working papers also provide:- a basis for planning the audit

Their objective is to aid the auditor in providing reasonable assurance that an

adequate audit was conducted inaccordance with GAAS.

January

7 - 68Copyright 2003 Pearson Education Canada Inc.

Working papersWorking papers

Working papers also provide:- a basis for planning the audit- a record of the evidence accumulated and the results of tests

Their objective is to aid the auditor in providing reasonable assurance that an

adequate audit was conducted inaccordance with GAAS.

Ace Co.

Audit File

7 - 69Copyright 2003 Pearson Education Canada Inc.

Working papersWorking papers

Working papers also provide:- a basis for planning the audit- a record of the evidence accumulated and the results of tests- data supporting the audit report

Their objective is to aid the auditor in providing reasonable assurance that an

adequate audit was conducted inaccordance with GAAS.

7 - 70Copyright 2003 Pearson Education Canada Inc.

Working papersWorking papers

Working papers also provide:- a basis for planning the audit- a record of the evidence accumulated and the results of tests- data supporting the audit report- a basis for supervisor/partner review

Their objective is to aid the auditor in providing reasonable assurance that an

adequate audit was conducted inaccordance with GAAS.

7 - 71Copyright 2003 Pearson Education Canada Inc.

Working papersWorking papersWorking papers include

current files andpermanent files.

?

7 - 72Copyright 2003 Pearson Education Canada Inc.

Permanent filesPermanent files contain data of a contain data of a historical naturehistorical nature of of continuingcontinuing relevance relevance

to current and future engagements.to current and future engagements.

PERMANENT

7 - 73Copyright 2003 Pearson Education Canada Inc.

CONTRACTCONTRACT

Permanent files contain data of a Permanent files contain data of a historical naturehistorical nature of of continuingcontinuing relevance relevance

to current and future engagements.to current and future engagements.

INCLUDE:- copies of client documents of continu- ing importance (e.g., articles of incor- poration, bylaws, contracts)

Articles of Incorporation

7 - 74Copyright 2003 Pearson Education Canada Inc.

Permanent files contain data of a Permanent files contain data of a historical naturehistorical nature of of continuingcontinuing relevance relevance to current and future engagements.to current and future engagements.

INCLUDE:-copies of client documents of

continuing importance

- analyses from prior audits that have continuing importance (e.g., bond premium amortization, depreciation)

7 - 75Copyright 2003 Pearson Education Canada Inc.

Permanent files contain data of a Permanent files contain data of a historical naturehistorical nature of of continuingcontinuing relevance relevance to current and future engagements.to current and future engagements.

INCLUDE:-copies of client documents of

continuing importance - analyses from prior audits that have continuing importance - internal control information (flow- charts, descriptions of transaction cycles)

7 - 76Copyright 2003 Pearson Education Canada Inc.

Permanent files contain data of a Permanent files contain data of a historical naturehistorical nature of of continuingcontinuing relevance relevance

to current and future engagements.to current and future engagements.

INCLUDE:-copies of client documents of

continuing importance- analyses from prior audits that have continuing importance - internal control information - results of prior audit analytical procedures

7 - 77Copyright 2003 Pearson Education Canada Inc.

Does an audit client haveDoes an audit client havea legal right to audit a legal right to audit working papers?working papers?

7 - 78Copyright 2003 Pearson Education Canada Inc.

Does an audit client have a Does an audit client have a legal right to audit working legal right to audit working

papers?papers?

NO!NO!

7 - 79Copyright 2003 Pearson Education Canada Inc.

audit working papersaudit working papers

How does theprovincial CA

institutes’ Rules of Professional

Conduct apply?

7 - 80Copyright 2003 Pearson Education Canada Inc.

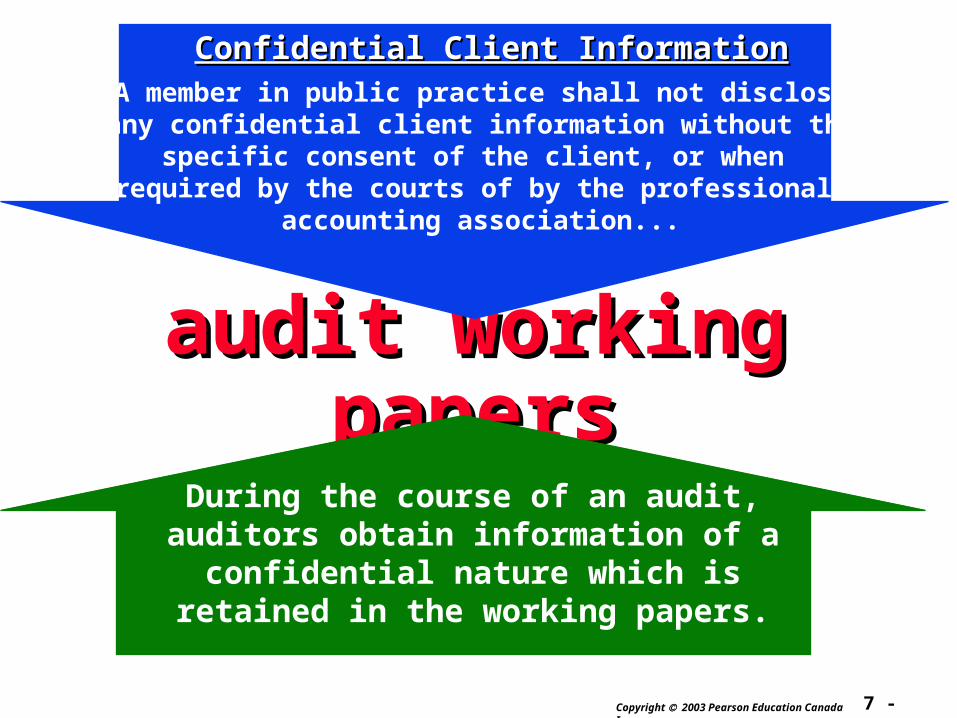

audit working papersaudit working papers

Confidential Client InformationConfidential Client InformationA member in public practice shall not discloseany confidential client information without the

specific consent of the client, or when required by the courts of by the professional

accounting association...

During the course of an audit,auditors obtain information of a

confidential nature which isretained in the working papers.

7 - 81Copyright 2003 Pearson Education Canada Inc.

What are working paper What are working paper tick markstick marks??

~ ! @ # ^ & * “ < >

7 - 82Copyright 2003 Pearson Education Canada Inc.

What are working paper What are working paper tick tick marksmarks??

symbols of audit work completed

~ ! @ # ^ & * “ < >