Embed Size (px)

Citation preview

www.moodys.com

Corporate FinanceMoody’s Global

Special Comment

Table of Contents: Summary 1

I. Data and Methodology 3 II. Metrics by Rating Category Aggregated Across All Industries 3 III. Industry Study 4

EBITA / Average Assets 5 EBITA / Interest Expense 6 EBITA Margin 7 Operating Margin 7 (FFO + Interest Expense) / Interest Expense 8 FFO / Debt 9 Retained Cash Flow / Net Debt 9 Debt / EBITDA 10 Debt / Book Capitalization 11 CAPEX / Depreciation 12 Revenue Volatility 13

IV. Discussion 13 Appendix A: Detailed Distributions by Credit Metric 16 Appendix B: Definition of Credit Ratios 28 Appendix C: Definition of Industry Aggregates 29 Moody’s Related Research 30

Analyst Contacts:

New York 1.212.553.1653

Qidong (Tony) Zhang Associate Analyst

Jennifer Tennant Assistant Vice President – Analyst

Albert Metz Senior Vice President

December 2009

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009 Summary

This paper outlines key financial ratios across industries for each broad rating category for global non-financial non-utility corporations. The global category includes EMEA, Asia and the Americas and the ratios are based on the most recent fiscal year-end data. In addition to presenting these ratios by each rating and industry combination, we also focus on the Baa-rated issuers to deepen our analysis.

The underlying data are taken from Moody’s Financial Metrics™, a data and analytics platform that provides as-reported and adjusted financial data, ratios, models and interactive rating methodologies. The adjustments are described in detail in Moody’s Approach to Global Standard Adjustments in the Analysis of Financial Statements for Non-Financial Corporations - Parts I, II and III.

For more information, see Moody’s Financial Metrics homepage, www.MoodysFM.com.

The metrics presented are:

EBITA / Average Assets

EBITA / Interest Expense

EBITA Margin

(FFO + Interest Expense) / Interest Expense

FFO / Debt

RCF / Net Debt

Debt / EBITDA

Debt / Book Capitalization

Operating Margin

CAPEX / Depreciation Expense

Revenue Volatility

2 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

These eleven ratios provide a useful and foundational set of metrics for comparative analysis, with broad applications both across regions and, pertinent to this study, across industries. Combinations of these ratios, sometimes further modified by non-public data, are used in our rating methodologies in conjunction with industry-specific measures and subjective judgments. The definitions of the ratios are presented in Appendix B.

A companion spreadsheet containing the data presented in this report is available on the Moody’s Financial Metrics homepage, www.MoodysFM.com. (Click here to view file).

We stress however that this report is not intended to describe Moody’s rating process. Ratio analysis is but one part of Moody’s analytical process. Qualitative and forward-looking considerations are also important. Interested readers are referred to Moody’s rating methodologies for detailed discussions of our analytical approach and core ratios for each industry. When Moody’s does analyze financial ratios, it uses a multivariate approach. As a result, a simple monotonic relationship between ratings and any single ratio should not generally be expected at the industry level.

Section I of the report describes details of the data and methodology. Section II presents a brief review of the distribution of these metrics in the aggregate by rating category – that is, without regard to industry classification. Results for all Baa rated issuers by industry are presented in Section III, with subsections devoted to each of the eleven metrics. Section IV contains some brief discussion and analysis.

Each exhibit in Appendix A focuses on a single financial metric and shows how its median values vary across industries and across rating categories. Definitions of the ratios are provided in Appendix B, while descriptions of the industry aggregates are presented in Appendix C.

Our analysis shows the following:

In the aggregate, there exists a strong monotonic relationship between these metrics and ratings.

(FFO + Interest Expense) / Interest Expense monotonically increases with ratings, as expected. Debt / Book Capitalization monotonically decreases.

The median FFO / Debt, EBITA / Average Assets, EBITA / Interest Expense, EBITA Margin, Operating Margin and RCF / Net Debt are somewhat lower for Aa than A issuers; this may again be an artifact of the small Aa sample.

Industries with consistently better-than-average metrics for Baa rated issuers include:

Metals & Mining,

Energy & Environment, and

Healthcare

Industries with consistently weaker-than-average metrics for Baa issuers include:

Transportation,

Automotive, and

Retail & Distribution

The evidence suggests that more intrinsically risky industries are required to achieve better credit ratios to obtain a given rating. Put simply, those industries with more volatile revenues tend to be the same as

those with otherwise better credit metrics. This result is consistent with prior research.1

Table A.12 in Appendix A shows changes between the 2008 medians and latest available medians for Baa-rated issuers by industry. We plan to publish a new Special Comment that studies the percentage change in credit metrics at the end of first quarter in 2010.

1 See, for example, “The Distribution of Common Financial Ratios by Rating and Industry for North American Non-Financial Corporations,” Moody’s Special

Comment, July 2006.

3 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

d .

I. Data and Methodology

Financial data for this study are taken from the most recently available fiscal year-end filings in Moody’s Financial Metrics™. The metrics that we study include measures of coverage, leverage, cash flow-to-debt, profitability and revenue stability. Please consult Appendix B and the references for a detailed discussion and definitions.

All the issuers in the sample are rated by Moody’s. The reported ratings refer specifically to the issuer’s senior unsecured rating or, in the absence of such a rating, its estimated senior unsecured rating as of reporting

date.2 Government-Related Issuers (GRIs) are excluded from the sample.

Moody's Financial Metrics™ has expanded greatly recently. Therefore, our comparison of medians in Table A.12 is compared with the 2008 numbers from the current FM, not simply a comparison with the formerly published numbers. This paper, and its companion pieces, describes the latest available numbers for FM Issuers as of December 2009. So, December 2008 might be the most recent fiscal year end for some issuers.3 Please note that this is the change of median numbers of financial metrics for each industry. It is also desirable to see the changes for a matched sample of Baa issuers. For this purpose, we are planning a new study on the more extensive change in credit metrics for each industry, which is expected to be publisheat the end of first quarter in 2010

Industry classifications are based on proprietary Moody’s sector assignments. For descriptions, please see Appendix C.

II. Metrics by Rating Category Aggregated Across All Industries

In this section we examine some of the properties of these metrics in the aggregate, that is, without regard to industrial classification. In all cases, the statistics we report are medians. We consider the distribution of these metrics by broad rating category.

Exhibit 1 summarizes our findings. We make the following observations:

Two metrics are strictly monotonic with ratings:

(FFO + Interest Expense) / Interest Expense monotonically increases with ratings, as expected. Debt / Book Capitalization monotonically decreases.

Most metrics are very nearly monotonic with ratings:

Median FFO / Debt, EBITA / Interest Expense, and RCF / Debt are each less for Aa than A issuers, though this may be an artifact of the small Aa sample. EBITA / Average Assets, EBITA Margin and Operating Margin have Aa and Baa lower than Ba. Otherwise, these metrics behave as expected.

Only two metrics have weak relationships to ratings:

Revenue Volatility is higher for Aaa issuers than Aa issuers, which of course is a small sample, and is not strictly increasing across speculative-grade ratings. CAPEX / DepExp is not strictly monotonic either.

2 Please see “Moody’s Senior Ratings Algorithm & Estimated Senior Ratings,” Feb 2009 for a discussion of estimated senior unsecured ratings. 3 Limiting the sample to 2009 numbers, rather than the latest available, would cut down the sample too much.

4 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit 1

Aggregate Metrics by Rating Category

EBITA / Average

Assets Operating

Margin EBITA

Margin EBITA / Interest

Expense (FFO + IntExp) /

IntExp

Aaa 22.0% 18.6% 21.9% 18.6 17.8

Aa 7.4% 9.7% 11.2% 5.5 10.1

A 11.3% 13.4% 14.0% 6.6 8.9

Baa 9.5% 11.0% 12.2% 4.4 5.8

Ba 9.6% 11.3% 12.9% 3.2 4.6

B 6.9% 7.8% 9.1% 1.4 2.4

C 2.3% 1.7% 2.5% 0.3 1.2

Debt / EBITDA Debt / Book

Capitalization FFO / Debt

Retained Cash Flow / Net Debt

CAPEX / Depreciation

Revenue Volatility

Aaa 0.9 30.2% 87.5% 164.0% 1.3 13.0

Aa 2.1 43.4% 35.5% 23.1% 1.1 11.5

A 2.0 44.7% 37.6% 26.7% 1.3 15.0

Baa 2.8 50.6% 25.4% 22.9% 1.3 16.0

Ba 3.2 54.3% 22.3% 21.1% 1.2 22.0

B 5.3 74.9% 10.9% 10.5% 1.0 17.0

C 7.7 103.9% 2.3% 2.3% 0.8 15.0

Source: Moody’s Financial Metrics™

III. Industry Study

In this section, we study these financial metrics by industry. We compare ratios for Baa-rated issuers only. We do this not only to make the presentation tractable, but also because not all industries are represented in all rating categories. For instance, only five industries are represented in the Aaa category, and only nine in the Aa. The Baa category is the best represented investment-grade rating category.

Exhibit 2 lists the industries covered in this report and the number of Baa rated issuers in each. For descriptions of these industry classifications, please see Appendix C.

5 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit 2

Industry Coverage Industry Count of Baa issuers

Aerospace & Defense 10

Automotive 15

Chemicals 32

Consumer Products 68

Energy & Environment 76

Healthcare 11

Manufacturing 60

Media 25

Metals & Mining 23

Retail & Distribution 34

Services 7

Telecommunications 58

Transportation 23

Source: Moody’s Financial Metrics™

EBITA / Average Assets

Exhibit 3 sorts the industries by their median Baa EBITA / Average Assets ratio. The complete distribution is presented in Appendix A. The median aggregate ratios at different rating categories are highlighted for comparison.

Exhibit 3

0% 5% 10% 15% 20% 25%

Aggregate AaaEnergy & Environment

Metals & MiningAggregate A

Aerospace & DefenseServices

TelecommunicationsConsumer Products

HealthcareAggregate Ba Aggregate Baa

MediaManufacturing

Retail & DistributionChemicals

Aggregate Aa Aggregate B

TransportationAutomotive

Aggregate Caa-C

Source: Moody’s Financial Metrics™

Median Baa EBITA / Average Assets

6 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

From Exhibit 3 we see that for Baa rated issuers, median EBITA / Average Assets is highest for the Energy & Environment and Metals & Mining industries, exceeding that of the aggregate A rated issuer set. At the other extreme, the median Baa ratio is lowest for the Automotive industry, ranking just above the aggregate Caa-C rated issuer set.

While this ratio is nearly increasing across ratings in the aggregate up to A, this ratio is fully monotonic for only one industry.

EBITA / Interest Expense

Exhibit 4 presents median Baa EBITA / Interest Expense ratios by industry. Again, detailed distributions are reported in the Appendix. Aggregate ratios are monotonic except Aa, and that holds true for four industries.

Exhibit 4

0 2 4 6 8 10 12 14 16 18 2

Aggregate AaaMetals & Mining

HealthcareAggregate A

Aggregate Aa Services

Energy & EnvironmentManufacturing

Aerospace & DefenseAggregate Baa

MediaConsumer ProductsTelecommunicationsRetail & Distribution

ChemicalsAggregate Ba Transportation

AutomotiveAggregate B

Aggregate Caa-C

0

Source: Moody’s Financial Metrics™

Median Baa EBITA / Interest Expense

Metals & Mining and Healthcare have the largest metrics, exceeding that of the aggregate Aa cohort. Automotive and Transportation have the lowest median EBITA / Interest Expense Ratio, falling slightly above the aggregate B issuer pool.

7 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

EBITA Margin

Median Baa EBITA Margins are presented in Exhibit 5. This metric is strictly monotonic only in one industry.

This metric is highest for the Energy & Environment, Media and Telecommunications industries and lowest for the Automotive and Retail & Distribution.

Exhibit 5

0% 5% 10% 15% 20% 25%

Aggregate AaaEnergy & Environment

Media

TelecommunicationsHealthcare

Aggregate A

Metals & MiningAggregate Ba Aggregate Baa

Aerospace & DefenseConsumer Products

Aggregate Aa Manufacturing

Aggregate B

ChemicalsTransportation

Services

Retail & DistributionAutomotive

Aggregate Caa-C

Source: Moody’s Financial Metrics™

Median Baa EBITA Margin

Operating Margin

Median Baa Operating Margins are presented in Exhibit 6. This metric is strictly monotonic for only one industry.

Just as was the case with median EBITA Margin, the Energy & Environment, Telecommunications and Media industries have the greatest median Baa Operating Margins. Automotive and Retail & Distribution are on the lower end.

8 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit 6

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Aggregate AaaEnergy & Environment

TelecommunicationsMedia

Aggregate AMetals & Mining

HealthcareConsumer Products

Aggregate Ba Aggregate Baa

Aerospace & DefenseAggregate Aa Manufacturing

ChemicalsServices

Aggregate BTransportation

Retail & DistributionAutomotive

Aggregate Caa-C

Source: Moody’s Financial Metrics™

Median Baa Operating Margin

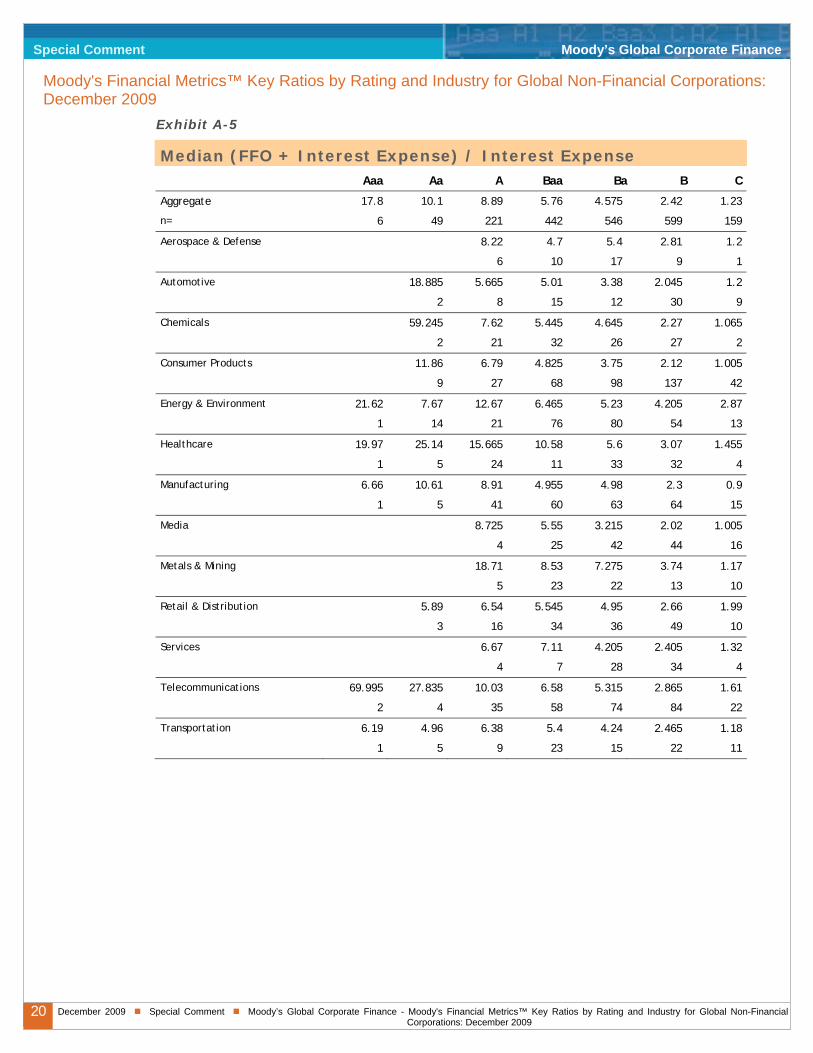

(FFO + Interest Expense) / Interest Expense

Exhibit 7 presents the median Baa (FFO + Interest Expense) / Interest Expense ratios by industry. In the aggregate, this metric strictly increases monotonically. That holds true for six industries as well.

The Healthcare industry has median ratios that exceed the Aa aggregate. On the other hand, the Aerospace & Defense industry has median metrics just above that of the aggregate Ba cohort.

Exhibit 7

0 2 4 6 8 10 12 14 16

Aggregate AaaHealthcare

Aggregate Aa Aggregate A

Metals & MiningServices

TelecommunicationsEnergy & Environment

Aggregate BaaMedia

Retail & DistributionChemicals

TransportationAutomotive

ManufacturingConsumer Products

Aerospace & DefenseAggregate Ba

Aggregate BAggregate Caa-C

18

Source: Moody’s Financial Metrics™

Median Baa (FFO + Interest Expense) / Interest Expense

9 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

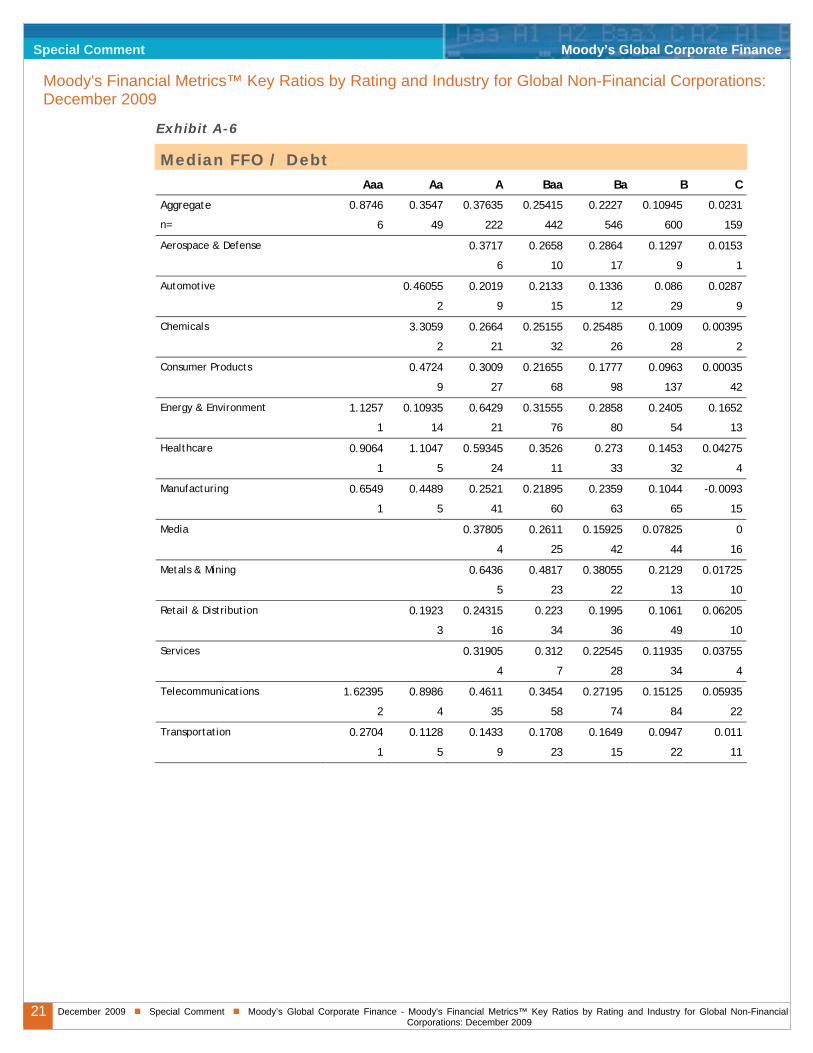

FFO / Debt

Median Baa FFO / Debt ratios are presented in Exhibit 8. In the aggregate, this metric increases monotonically with ratings except for Aa. That continues to hold true for five industries.

The Metals & Mining industry has median ratios exceeding that of the aggregate Aa cohort. The Transportation sector has the lowest median FFO / Debt ratio, slightly above that of the aggregate B issuer pool.

Exhibit 8

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Aggregate AaaMetals & Mining

Aggregate AAggregate Aa

HealthcareTelecommunications

Energy & EnvironmentServices

Aerospace & DefenseMedia

Aggregate BaaChemicals

Retail & DistributionAggregate Ba Manufacturing

Consumer ProductsAutomotive

TransportationAggregate B

Aggregate Caa-C

Source: Moody’s Financial Metrics™

Median Baa FFO / Debt

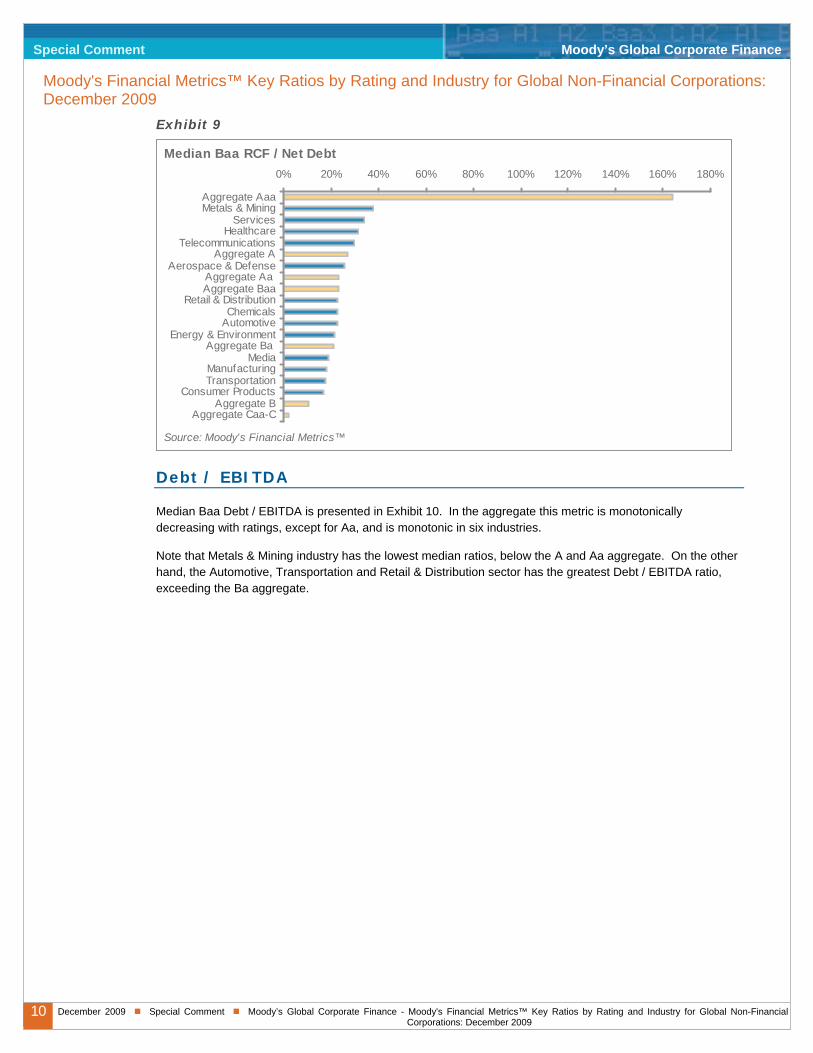

Retained Cash Flow / Net Debt

Median Baa RCF / Net Debt ratios are presented in Exhibit 9. This metric monotonically increase with ratings in the aggregate except for Aa and is monotonic in two industry sectors.

Metals & Mining and Services have median ratios in excess of the aggregate Aa pool. The Consumer Products, Transportation, Manufacturing and Media industries have RCF / Net Debt ratios below the aggregate Ba set.

10 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit 9

0% 20% 40% 60% 80% 100% 120% 140% 160% 180%

Aggregate AaaMetals & Mining

ServicesHealthcare

TelecommunicationsAggregate A

Aerospace & DefenseAggregate Aa Aggregate Baa

Retail & DistributionChemicals

AutomotiveEnergy & Environment

Aggregate Ba Media

ManufacturingTransportation

Consumer ProductsAggregate B

Aggregate Caa-C

Source: Moody’s Financial Metrics™

Median Baa RCF / Net Debt

Debt / EBITDA

Median Baa Debt / EBITDA is presented in Exhibit 10. In the aggregate this metric is monotonically decreasing with ratings, except for Aa, and is monotonic in six industries.

Note that Metals & Mining industry has the lowest median ratios, below the A and Aa aggregate. On the other hand, the Automotive, Transportation and Retail & Distribution sector has the greatest Debt / EBITDA ratio, exceeding the Ba aggregate.

11 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit 10

0 1 2 3 4 5 6 7

Aggregate AaaMetals & Mining

Aggregate AAggregate Aa

Energy & Environment

HealthcareTelecommunications

ServicesChemicals

Aerospace & Defense

Aggregate BaaManufacturing

MediaConsumer Products

Aggregate Ba

Retail & DistributionTransportation

AutomotiveAggregate B

Aggregate Caa-C

8

Source: Moody’s Financial Metrics™

Median Baa Debt / EBITDA

Debt / Book Capitalization

Median Baa Debt / Book Capitalization is presented in Exhibit 11. This decreases with ratings in the aggregate, and seven industry groups are completely monotonic.

The ordering of industries resembles that given by Debt / EBITDA ratios. The sectors with the least Debt / Book Cap metrics are Healthcare and Metals & Mining. The Transportation, Media, Retail & Distribution and services industries have the greatest Debt / Book Cap ratio, exceeding the Ba aggregate.

12 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit 11

0% 20% 40% 60% 80% 100% 120%

Aggregate AaaHealthcare

Metals & MiningAggregate Aa

Energy & EnvironmentAggregate A

ManufacturingChemicals

Aerospace & DefenseAggregate Baa

TelecommunicationsConsumer Products

AutomotiveAggregate Ba

ServicesRetail & Distribution

MediaTransportation

Aggregate BAggregate Caa-C

Source: Moody’s Financial Metrics™

Median Baa Debt / Book Capitalization

CAPEX / Depreciation

Exhibit 12 presents median CAPEX / Depreciation ratios for Baa rated issuers. This metric does not strictly increase across ratings in the aggregate, but does so for three industries.

Energy & Environment and Metals & Mining are among the strongest industry sectors, while Services is the weakest.

Exhibit 12

0.0 0.5 1.0 1.5 2.0 2.5

Energy & EnvironmentMetals & Mining

Retail & DistributionHealthcare

TransportationAerospace &Aggregate A

Aggregate AaaAggregate BaaManufacturing

Consumer ProductsAutomotiveChemicals

Aggregate Ba Telecommunications

MediaAggregate Aa

ServicesAggregate B

Aggregate Caa-C

Source: Moody’s Financial Metrics™

Median Baa CAPEX / Depreciation

13 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Revenue Volatility

Exhibit 13 presents median revenue volatility metrics for Baa rated issuers by industry. As discussed, this metric does not correlate well with ratings in the aggregate. And no industry exhibits the expected monotonic relationship.

The Automotive industry has the least volatile revenues among Baa rated issuers. Other leading sectors include Consumer Products, Retail & Distribution and Chemicals, all with revenues less volatile than the Aaa-rated aggregate. On the other hand, revenue volatility for two industries exceed that of the Ba-rated aggregate. These include Metals & Mining and Energy & Environment.

Exhibit 13

0 5 10 15 20 25 30

AutomotiveAggregate Aa

Consumer ProductsRetail & Distribution

ChemicalsMedia

TransportationAggregate Aaa

ServicesTelecommunications

Aggregate AAggregate Caa-C

HealthcareAggregate Baa

Aggregate BManufacturing

Aerospace & DefenseAggregate Ba

Metals & MiningEnergy & Environment

Source: Moody’s Financial Metrics™

Median Baa Revenue Volatility

IV. Discussion

Exhibit 14 summarizes the results presented above. For each metric, we report its standardized (mean 100,

standard deviation 1) value and sort the industries by their average score.4 The Metals & Mining, Healthcare

and Energy & Environment industries have the highest average score, while the Automotive, Transportation and Retail & Distribution sectors have the lowest.

What are we to make of these results? Recall that these results are conditioned on ratings: Baa-rated issuers in the Metals & Mining industry generally have stronger (sometimes substantially stronger) metrics than do Baa rated issuers in the Retail & Distribution industry.

One interpretation is that observing different values is evidence of different methods or standards in assigning ratings: we observe better metrics in Metals & Mining than Retail & Distribution because we hold the former to a higher standard than we do the latter, perhaps because one industry is intrinsically riskier than the other. Consistent with previous research, we find evidence to suggest that this is true.

Using “revenue volatility” as a proxy for intrinsic risk, the hypothesis is that we should observe better credit ratios associated with greater volatility within a rating category. In other words, we should observe a negative correlation between the standardized credit ratios and standardized revenue volatility.

4 The average is taken with respect to all metrics except revenue volatility. Adjustments are made for those metrics (e.g. Debt / EBITDA) for which greater

values are less desirable.

14 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

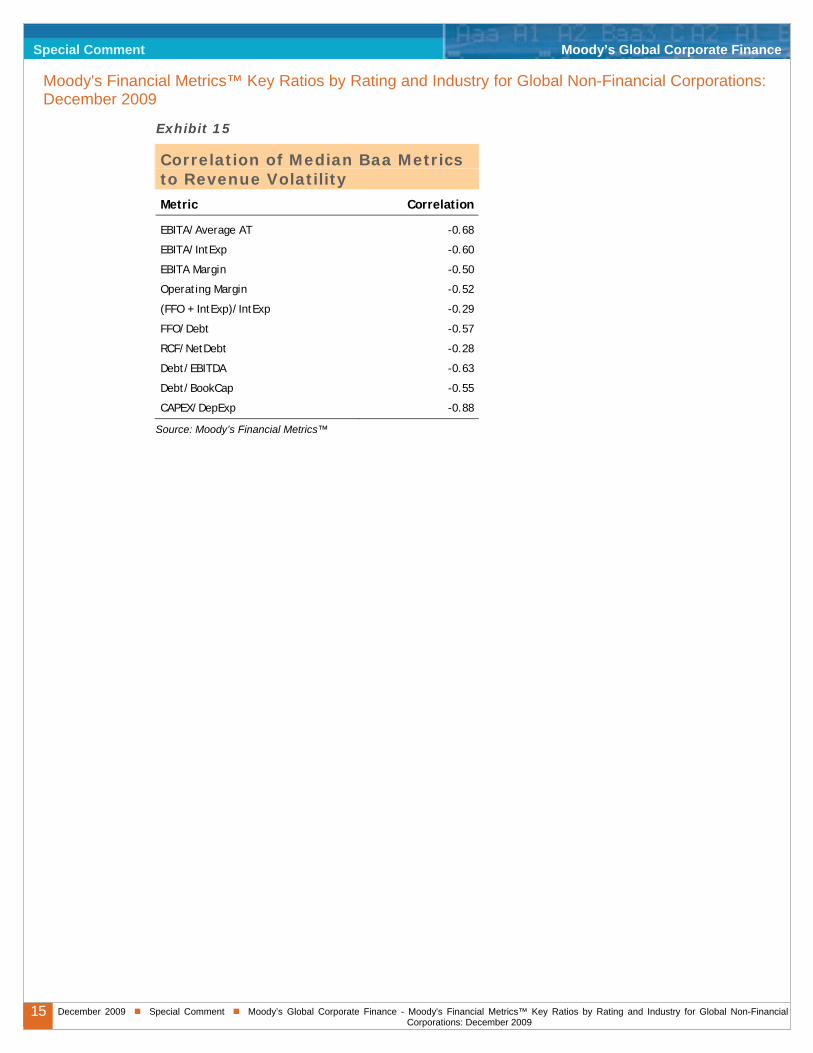

Exhibit 15 reports the correlation of the standardized values of each metric to revenue volatility. As expected, we obtain negative correlations for all metrics. The most significant correlations are with CAPEX / DepExp (-0.88), EBITA / Average AT (-0.68) and Debt / EBITDA (-0.63).

While purely suggestive, the results indicate that industries with more volatile revenues are required to achieve stronger credit metrics in order to obtain the Baa rating.

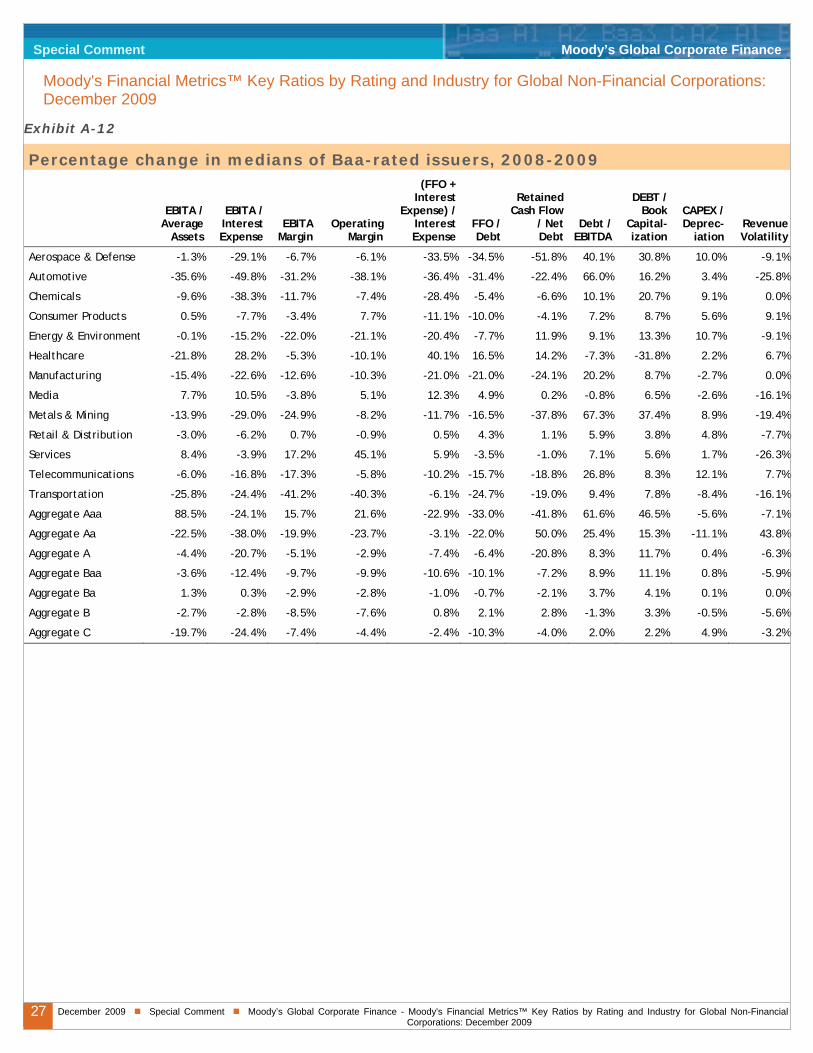

Exhibit A-12 shows the percentage change in medians of Baa-rated issuers from 2008 to 2009. Many industries exhibit big decline in these key metrics, whereas last year there was only modest change, if any. For example, Automotive industry has significant decline in most of the metrics, underscoring its turmoil in the current environment. Aggregated Aaa issuers also show big metrics change.

Exhibit 14

Summary of Standardized Baa Metrics

Average

score EBITA / Average

Assets EBITA / IntExp

EBITA Margin

Operating Margin

(FFO + IntExp) / IntExp

Metals & Mining 101.2 101.1 102.2 100.3 100.5 101.4

Healthcare 100.9 100.2 101.4 100.9 100.3 102.6

Energy & Environment 100.6 101.3 100.5 101.5 101.5 100.2

Telecommunications 100.4 100.5 99.7 101.1 101.4 100.2

Services 100.1 100.7 100.5 99.0 99.3 100.5

Media 100.0 99.8 99.8 101.4 101.3 99.6

Aerospace & Defense 99.9 100.9 99.9 100.0 100.0 99.1

Chemicals 99.7 99.5 99.6 99.4 99.5 99.6

Consumer Products 99.7 100.2 99.7 100.0 100.1 99.2

Manufacturing 99.6 99.8 99.9 99.8 99.7 99.3

Retail & Distribution 99.5 99.7 99.6 98.7 98.7 99.6

Transportation 99.1 98.4 98.7 99.2 99.2 99.5

Automotive 99.1 97.9 98.4 98.5 98.4 99.3

Average

score FFO / Debt RCF /

NetDebt Debt /

EBITDA Debt /

BookCap CAPEX / DepExp

Rev Vol

Metals & Mining 101.2 102.5 102.0 101.6 101.5 101.7 98.5

Healthcare 100.9 100.9 101.0 100.9 102.1 100.0 100.0

Energy & Environment 100.6 100.4 99.5 101.0 100.6 102.6 97.6

Telecommunications 100.4 100.8 100.8 100.8 99.9 99.3 100.4

Services 100.1 100.4 101.4 100.5 99.6 99.1 100.4

Media 100.0 99.8 99.2 99.8 99.1 99.2 100.6

Aerospace & Defense 99.9 99.8 100.1 100.1 100.0 99.8 99.3

Chemicals 99.7 99.7 99.7 100.2 100.0 99.5 100.6

Consumer Products 99.7 99.2 98.8 99.6 99.9 99.6 100.8

Manufacturing 99.6 99.3 99.1 99.8 100.1 99.6 99.7

Retail & Distribution 99.5 99.3 99.7 99.4 99.2 100.1 100.8

Transportation 99.1 98.7 99.0 98.3 98.3 100.0 100.6

Automotive 99.1 99.2 99.7 98.1 99.6 99.6 100.8

Source: Moody’s Financial Metrics™

15 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit 15

Correlation of Median Baa Metrics to Revenue Volatility Metric Correlation

EBITA/Average AT -0.68

EBITA/IntExp -0.60

EBITA Margin -0.50

Operating Margin -0.52

(FFO + IntExp)/IntExp -0.29

FFO/Debt -0.57

RCF/NetDebt -0.28

Debt/EBITDA -0.63

Debt/BookCap -0.55

CAPEX/DepExp -0.88

Source: Moody’s Financial Metrics™

16 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Appendix A: Detailed Distributions by Credit Metric

Source: Moody’s Financial Metrics™

Exhibit A-1

Median EBITA / Average Assets Aaa Aa A Baa Ba B C

Aggregate 0.2198 0.0736 0.11325 0.0946 0.0959 0.0687 0.0233

n= 6 49 222 442 546 601 159

Aerospace & Defense 0.1242 0.11295 0.1094 0.087 0.0541

6 10 17 9 1

Automotive -0.01385 0.0253 0.0502 0.05595 0.05235 0.009

2 9 15 12 30 9

Chemicals 0.13675 0.0924 0.08315 0.1098 0.06265 -0.17445

2 21 32 26 28 2

Consumer Products 0.1309 0.146 0.09865 0.08225 0.0627 0.03585

9 27 68 98 137 42

Energy & Environment 0.2686 0.02795 0.1479 0.1213 0.10355 0.0906 0.0148

1 14 21 76 80 54 13

Healthcare 0.2218 0.1768 0.184 0.0986 0.1013 0.07405 0.0318

1 5 24 11 33 32 4

Manufacturing 0.1048 0.0345 0.1021 0.08895 0.089 0.0727 -0.0196

1 5 41 60 63 65 15

Media 0.1245 0.0897 0.09625 0.0748 -0.002

4 25 42 44 16

Metals & Mining 0.1804 0.1177 0.1271 0.0464 0.00225

5 23 22 13 10

Retail & Distribution 0.0704 0.09385 0.0882 0.0951 0.068 0.02555

3 16 34 36 49 10

Services 0.0865 0.1082 0.11875 0.0804 0.042

4 7 28 34 4

Telecommunications 0.2437 0.1102 0.1346 0.10365 0.09765 0.0594 0.0224

2 4 35 58 74 84 22

Transportation 0.119 0.0674 0.0637 0.0617 0.0974 0.0458 0.0133

1 5 9 23 15 22 11

17 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-2

Median EBITA / Interest Expense Aaa Aa A Baa Ba B C

Aggregate 18.59 5.52 6.64 4.37 3.215 1.37 0.31

n= 6 49 221 442 546 599 159

Aerospace & Defense 6.875 4.375 4.4 1.98 0.79

6 10 17 9 1

Automotive -3.29 2.95 2.28 1.785 1.295 0.14

2 8 15 12 30 9

Chemicals 50.555 5.76 4.035 4.06 1.21 -1.615

2 21 32 26 27 2

Consumer Products 13.74 5.81 4.18 2.34 1.16 0.505

9 27 68 98 137 42

Energy & Environment 26.54 2.21 6.4 5.28 3.515 2.475 0.45

1 14 21 76 80 54 13

Healthcare 21.15 24.34 16.505 6.64 3.67 1.71 0.39

1 5 24 11 33 32 4

Manufacturing 6.22 10.28 7.29 4.425 3.12 1.35 -0.56

1 5 41 60 63 64 15

Media 8.1 4.36 2.21 1.31 0.11

4 25 42 44 16

Metals & Mining 21.05 7.76 5.465 1.37 0.16

5 23 22 13 10

Retail & Distribution 3.93 4.65 4.07 3.035 1.54 0.53

3 16 34 36 49 10

Services 5.135 5.34 3.815 1.485 0.505

4 7 28 34 4

Telecommunications 74.015 18.43 6.64 4.14 3.595 1.2 0.325

2 4 35 58 74 84 22

Transportation 3.49 2.68 6.01 2.72 2.68 0.935 0.19

1 5 9 23 15 22 11

18 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-3

Median EBITA Margin Aaa Aa A Baa Ba B C

Aggregate 0.21905 0.1124 0.14025 0.1216 0.1292 0.0913 0.0249

n= 6 49 222 441 546 599 157

Aerospace & Defense 0.12285 0.12135 0.1068 0.109 0.0591

6 10 17 9 1

Automotive -0.01345 0.0376 0.0452 0.05565 0.0407 0.0064

2 9 15 12 30 9

Chemicals 0.15715 0.1004 0.09095 0.09775 0.0815 -0.11675

2 21 32 26 27 2

Consumer Products 0.1882 0.1473 0.1209 0.1104 0.07545 0.0346

9 27 68 98 136 41

Energy & Environment 0.193 0.07205 0.1972 0.1933 0.1975 0.1875 0.117

1 14 21 75 80 54 13

Healthcare 0.2818 0.3269 0.27935 0.166 0.1402 0.112 0.05095

1 5 24 11 33 32 4

Manufacturing 0.1449 0.0429 0.0935 0.10695 0.0932 0.0918 -0.03285

1 5 41 60 63 65 14

Media 0.16535 0.1891 0.20195 0.1978 -0.0103

4 25 42 44 16

Metals & Mining 0.1846 0.1342 0.1818 0.0583 0.002

5 23 22 13 10

Retail & Distribution 0.0583 0.0631 0.056 0.0548 0.0643 0.0157

3 16 34 36 49 10

Services 0.15175 0.0711 0.17515 0.1129 0.02935

4 7 28 34 4

Telecommunications 0.3014 0.17265 0.2092 0.17475 0.2136 0.09315 0.03875

2 4 35 58 74 84 22

Transportation 0.1606 0.1907 0.1159 0.0795 0.1515 0.0543 0.0211

1 5 9 23 15 22 11

19 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-4

Median Operating Margin Aaa Aa A Baa Ba B C

Aggregate 0.1855 0.0972 0.13365 0.11 0.1126 0.078 0.0173

n= 6 49 222 441 546 599 157

Aerospace & Defense 0.1149 0.10645 0.0997 0.1086 0.0395

6 10 17 9 1

Automotive -0.01465 0.0323 0.0386 0.0529 0.0358 -0.0027

2 9 15 12 30 9

Chemicals 0.14225 0.0864 0.08585 0.0911 0.0685 -0.1246

2 21 32 26 27 2

Consumer Products 0.1772 0.1428 0.11285 0.09435 0.0685 0.0353

9 27 68 98 136 41

Energy & Environment 0.155 0.0614 0.2091 0.1743 0.1963 0.1686 0.0027

1 14 21 75 80 54 13

Healthcare 0.2538 0.2609 0.2176 0.1216 0.1273 0.1029 0.02695

1 5 24 11 33 32 4

Manufacturing 0.1386 0.0364 0.0946 0.09695 0.084 0.0734 -0.0357

1 5 41 60 63 65 14

Media 0.1637 0.1674 0.1617 0.1613 0.08895

4 25 42 44 16

Metals & Mining 0.1724 0.1319 0.14885 0.0497 -0.0021

5 23 22 13 10

Retail & Distribution 0.0576 0.05835 0.05135 0.0484 0.0614 0.01045

3 16 34 36 49 10

Services 0.1297 0.079 0.16025 0.0995 0.0238

4 7 28 34 4

Telecommunications 0.2864 0.15675 0.1756 0.1711 0.14055 0.0647 0.027

2 4 35 58 74 84 22

Transportation 0.1185 0.1844 0.1131 0.075 0.1465 0.0409 0.0063

1 5 9 23 15 22 11

20 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-5

Median (FFO + Interest Expense) / Interest Expense Aaa Aa A Baa Ba B C

Aggregate 17.8 10.1 8.89 5.76 4.575 2.42 1.23

n= 6 49 221 442 546 599 159

Aerospace & Defense 8.22 4.7 5.4 2.81 1.2

6 10 17 9 1

Automotive 18.885 5.665 5.01 3.38 2.045 1.2

2 8 15 12 30 9

Chemicals 59.245 7.62 5.445 4.645 2.27 1.065

2 21 32 26 27 2

Consumer Products 11.86 6.79 4.825 3.75 2.12 1.005

9 27 68 98 137 42

Energy & Environment 21.62 7.67 12.67 6.465 5.23 4.205 2.87

1 14 21 76 80 54 13

Healthcare 19.97 25.14 15.665 10.58 5.6 3.07 1.455

1 5 24 11 33 32 4

Manufacturing 6.66 10.61 8.91 4.955 4.98 2.3 0.9

1 5 41 60 63 64 15

Media 8.725 5.55 3.215 2.02 1.005

4 25 42 44 16

Metals & Mining 18.71 8.53 7.275 3.74 1.17

5 23 22 13 10

Retail & Distribution 5.89 6.54 5.545 4.95 2.66 1.99

3 16 34 36 49 10

Services 6.67 7.11 4.205 2.405 1.32

4 7 28 34 4

Telecommunications 69.995 27.835 10.03 6.58 5.315 2.865 1.61

2 4 35 58 74 84 22

Transportation 6.19 4.96 6.38 5.4 4.24 2.465 1.18

1 5 9 23 15 22 11

21 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-6

Median FFO / Debt Aaa Aa A Baa Ba B C

Aggregate 0.8746 0.3547 0.37635 0.25415 0.2227 0.10945 0.0231

n= 6 49 222 442 546 600 159

Aerospace & Defense 0.3717 0.2658 0.2864 0.1297 0.0153

6 10 17 9 1

Automotive 0.46055 0.2019 0.2133 0.1336 0.086 0.0287

2 9 15 12 29 9

Chemicals 3.3059 0.2664 0.25155 0.25485 0.1009 0.00395

2 21 32 26 28 2

Consumer Products 0.4724 0.3009 0.21655 0.1777 0.0963 0.00035

9 27 68 98 137 42

Energy & Environment 1.1257 0.10935 0.6429 0.31555 0.2858 0.2405 0.1652

1 14 21 76 80 54 13

Healthcare 0.9064 1.1047 0.59345 0.3526 0.273 0.1453 0.04275

1 5 24 11 33 32 4

Manufacturing 0.6549 0.4489 0.2521 0.21895 0.2359 0.1044 -0.0093

1 5 41 60 63 65 15

Media 0.37805 0.2611 0.15925 0.07825 0

4 25 42 44 16

Metals & Mining 0.6436 0.4817 0.38055 0.2129 0.01725

5 23 22 13 10

Retail & Distribution 0.1923 0.24315 0.223 0.1995 0.1061 0.06205

3 16 34 36 49 10

Services 0.31905 0.312 0.22545 0.11935 0.03755

4 7 28 34 4

Telecommunications 1.62395 0.8986 0.4611 0.3454 0.27195 0.15125 0.05935

2 4 35 58 74 84 22

Transportation 0.2704 0.1128 0.1433 0.1708 0.1649 0.0947 0.011

1 5 9 23 15 22 11

22 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-7

Median Retained Cash Flow / Net Debt Aaa Aa A Baa Ba B C

Aggregate 1.64005 0.2313 0.26715 0.22925 0.21065 0.1053 0.0226

n= 6 49 222 442 546 601 159

Aerospace & Defense 0.31005 0.25615 0.3012 0.1395 0.0157

6 10 17 9 1

Automotive -2.4264 0.2143 0.2256 0.1522 0.08655 0.0415

2 9 15 12 30 9

Chemicals -0.5958 0.2288 0.2275 0.17565 0.0967 0.0128

2 21 32 26 28 2

Consumer Products 0.3971 0.2395 0.1681 0.1712 0.0947 -0.0001

9 27 68 98 137 42

Energy & Environment 2.1972 0.1061 0.5775 0.21475 0.26525 0.226 0.1712

1 14 21 76 80 54 13

Healthcare 1.0829 0.3593 0.4384 0.314 0.2506 0.13425 0.04385

1 5 24 11 33 32 4

Manufacturing 0.2405 0.3964 0.2505 0.1828 0.2113 0.1039 -0.01

1 5 41 60 63 65 15

Media 0.36895 0.1898 0.14845 0.0729 0.0013

4 25 42 44 16

Metals & Mining 0.9088 0.3794 0.3529 0.0343 0.01945

5 23 22 13 10

Retail & Distribution 0.2313 0.23615 0.229 0.18985 0.1052 0.06475

3 16 34 36 49 10

Services 0.253 0.3422 0.24655 0.09825 0.0287

4 7 28 34 4

Telecommunications 11.3673 0.43465 0.3471 0.2969 0.3149 0.15355 0.06745

2 4 35 58 74 84 22

Transportation 0.3108 0.1093 0.1088 0.177 0.1512 0.08415 0.0123

1 5 9 23 15 22 11

23 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-8

Median Debt / EBITDA Aaa Aa A Baa Ba B C

Aggregate 0.905 2.05 2.015 2.825 3.23 5.26 7.7

n= 6 49 222 442 546 600 159

Aerospace & Defense 2.22 2.81 2.89 4.23 10.79

6 10 17 9 1

Automotive 2.09 3.14 4.2 5.415 5.615 7.24

2 9 15 12 30 9

Chemicals 1.005 2.86 2.775 2.61 5.59 3.215

2 21 32 26 27 2

Consumer Products 1.57 2.47 3.195 3.83 5.87 9.09

9 27 68 98 137 42

Energy & Environment 0.57 8.31 1.17 2.215 2.685 2.72 3.5

1 14 21 76 80 54 13

Healthcare 0.88 0.84 1.14 2.29 3.29 5.055 7.745

1 5 24 11 33 32 4

Manufacturing 1.26 1.61 2.36 3.03 2.73 4.47 5.04

1 5 41 60 63 65 15

Media 1.84 3.04 4.53 6.46 9.12

4 25 42 44 16

Metals & Mining 1.2 1.79 1.995 3.42 6.67

5 23 22 13 10

Retail & Distribution 3.55 3.04 3.335 3.745 5.99 10.34

3 16 34 36 49 10

Services 2.895 2.55 2.885 5.395 7.025

4 7 28 34 4

Telecommunications 0.64 1.13 1.74 2.295 2.93 4.685 6.595

2 4 35 58 74 84 22

Transportation 3.26 5.82 4.46 4.08 4.48 6.715 10.54

1 5 9 23 15 22 11

24 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-9

Median Debt / Book Capitalization Aaa Aa A Baa Ba B C

Aggregate 0.30165 0.4335 0.4472 0.50635 0.54265 0.7494 1.0386

n= 6 49 222 442 546 601 159

Aerospace & Defense 0.5092 0.50435 0.4955 0.549 1.1191

6 10 17 9 1

Automotive 0.1999 0.4633 0.5426 0.6986 0.8216 0.8705

2 9 15 12 30 9

Chemicals 0.2496 0.4575 0.5031 0.60155 0.8016 1.3829

2 21 32 26 28 2

Consumer Products 0.3733 0.6181 0.5165 0.59765 0.7629 1.21855

9 27 68 98 137 42

Energy & Environment 0.2471 0.72925 0.3354 0.4466 0.47995 0.537 0.7319

1 14 21 76 80 54 13

Healthcare 0.308 0.1592 0.27945 0.3063 0.4928 0.6591 1.62895

1 5 24 11 33 32 4

Manufacturing 0.2953 0.3043 0.4258 0.4919 0.4715 0.6414 0.8347

1 5 41 60 63 65 15

Media 0.35685 0.5836 0.75775 0.891 1.436

4 25 42 44 16

Metals & Mining 0.3002 0.3609 0.4845 0.5949 0.86185

5 23 22 13 10

Retail & Distribution 0.4971 0.55335 0.57905 0.65105 0.7829 1.01345

3 16 34 36 49 10

Services 0.40625 0.5434 0.55915 0.73965 1.14455

4 7 28 34 4

Telecommunications 0.24195 0.26385 0.4384 0.51475 0.56075 0.7467 1.32725

2 4 35 58 74 84 22

Transportation 1.0486 0.7744 0.5698 0.6641 0.694 0.86715 1.0171

1 5 9 23 15 22 11

25 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-10

Median CAPEX / Depreciation Aaa Aa A Baa Ba B C

Aggregate 1.3332 1.1236 1.3497 1.32985 1.2377 1.01955 0.8041

n= 6 49 222 440 543 598 156

Aerospace & Defense 1.3712 1.35915 1.2662 1.0392 0.946

6 10 17 9 1

Automotive 1.0323 1.408 1.2709 1.19835 0.94395 0.8018

2 9 15 12 30 9

Chemicals 1.30485 1.327 1.26055 1.12805 0.9336 0.44305

2 21 32 26 26 2

Consumer Products 1.299 1.2013 1.278 1.20345 0.9765 0.7583

9 27 68 98 137 41

Energy & Environment 1.2342 1.20235 1.8928 2.32245 2.0834 1.6752 1.6602

1 14 21 74 80 53 13

Healthcare 1.3889 0.8822 1.18415 1.4166 1.2797 1.1449 0.83365

1 5 24 11 33 32 4

Manufacturing 2.1923 0.9722 1.3532 1.2989 1.16585 0.8977 0.70355

1 5 41 60 62 65 14

Media 0.9857 1.1347 1.0485 0.9329 0.74955

4 25 41 44 16

Metals & Mining 2.1043 2.008 1.7032 1.6638 0.9397

5 23 22 13 9

Retail & Distribution 1.1236 1.4738 1.45715 1.143 1.0174 0.8902

3 16 34 36 49 10

Services 1.22015 1.1188 1.1429 1.07185 0.9442

4 7 28 34 4

Telecommunications 1.38965 1.2274 1.2162 1.1627 1.105 0.9704 0.67475

2 4 35 58 73 84 22

Transportation 0.9614 1.069 2.2467 1.4072 1.3336 1.20155 1.2341

1 5 9 23 15 22 11

26 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-11

Median Revenue Volatility Aaa Aa A Baa Ba B C

Aggregate 13.0 11.5 15.0 16.0 22.0 17.0 15.0

n= 5 46 205 399 455 471 127

Aerospace & Defense 17.5 20.0 26.5 16.5 40.0

6 9 12 6 1

Automotive 11.5 13.5 11.5 10.0 13.0 8.0

2 8 14 9 25 7

Chemicals 19.5 15.0 13.0 22.0 20.0 8.0

2 19 31 25 20 1

Consumer Products 15.0 12.0 12.0 17.0 13.5 12.0

8 26 60 85 110 31

Energy & Environment 17.0 10.5 23.5 30.0 37.5 38.5 22.5

1 14 20 70 66 46 10

Healthcare 13.0 14.0 16.5 16.0 19.0 27.0 14.0

1 5 20 9 23 27 4

Manufacturing 12.0 10.0 15.0 18.0 28.0 21.0 17.0

1 5 39 56 57 53 12

Media 9.0 13.0 20.5 14.0 11.0

3 21 34 35 15

Metals & Mining 24.0 25.0 42.0 26.5 24.0

5 17 17 10 6

Retail & Distribution 18.0 14.5 12.0 18.5 13.0 6.0

2 16 30 30 35 9

Services 16.0 14.0 28.0 17.0 10.5

4 5 23 29 4

Telecommunications 13.5 4.0 12.5 14.0 19.0 16.0 16.5

2 3 32 56 61 59 18

Transportation 9.0 17.0 13.0 21.0 19.0 20.0

5 7 21 13 16 9

27 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Exhibit A-12

Percentage change in medians of Baa-rated issuers, 2008-2009

EBITA / Average

Assets

EBITA / Interest Expense

EBITA Margin

Operating Margin

(FFO + Interest

Expense) / Interest Expense

FFO / Debt

Retained Cash Flow

/ Net Debt

Debt / EBITDA

DEBT / Book

Capital-ization

CAPEX / Deprec-

iation Revenue Volatility

Aerospace & Defense -1.3% -29.1% -6.7% -6.1% -33.5% -34.5% -51.8% 40.1% 30.8% 10.0% -9.1%

Automotive -35.6% -49.8% -31.2% -38.1% -36.4% -31.4% -22.4% 66.0% 16.2% 3.4% -25.8%

Chemicals -9.6% -38.3% -11.7% -7.4% -28.4% -5.4% -6.6% 10.1% 20.7% 9.1% 0.0%

Consumer Products 0.5% -7.7% -3.4% 7.7% -11.1% -10.0% -4.1% 7.2% 8.7% 5.6% 9.1%

Energy & Environment -0.1% -15.2% -22.0% -21.1% -20.4% -7.7% 11.9% 9.1% 13.3% 10.7% -9.1%

Healthcare -21.8% 28.2% -5.3% -10.1% 40.1% 16.5% 14.2% -7.3% -31.8% 2.2% 6.7%

Manufacturing -15.4% -22.6% -12.6% -10.3% -21.0% -21.0% -24.1% 20.2% 8.7% -2.7% 0.0%

Media 7.7% 10.5% -3.8% 5.1% 12.3% 4.9% 0.2% -0.8% 6.5% -2.6% -16.1%

Metals & Mining -13.9% -29.0% -24.9% -8.2% -11.7% -16.5% -37.8% 67.3% 37.4% 8.9% -19.4%

Retail & Distribution -3.0% -6.2% 0.7% -0.9% 0.5% 4.3% 1.1% 5.9% 3.8% 4.8% -7.7%

Services 8.4% -3.9% 17.2% 45.1% 5.9% -3.5% -1.0% 7.1% 5.6% 1.7% -26.3%

Telecommunications -6.0% -16.8% -17.3% -5.8% -10.2% -15.7% -18.8% 26.8% 8.3% 12.1% 7.7%

Transportation -25.8% -24.4% -41.2% -40.3% -6.1% -24.7% -19.0% 9.4% 7.8% -8.4% -16.1%

Aggregate Aaa 88.5% -24.1% 15.7% 21.6% -22.9% -33.0% -41.8% 61.6% 46.5% -5.6% -7.1%

Aggregate Aa -22.5% -38.0% -19.9% -23.7% -3.1% -22.0% 50.0% 25.4% 15.3% -11.1% 43.8%

Aggregate A -4.4% -20.7% -5.1% -2.9% -7.4% -6.4% -20.8% 8.3% 11.7% 0.4% -6.3%

Aggregate Baa -3.6% -12.4% -9.7% -9.9% -10.6% -10.1% -7.2% 8.9% 11.1% 0.8% -5.9%

Aggregate Ba 1.3% 0.3% -2.9% -2.8% -1.0% -0.7% -2.1% 3.7% 4.1% 0.1% 0.0%

Aggregate B -2.7% -2.8% -8.5% -7.6% 0.8% 2.1% 2.8% -1.3% 3.3% -0.5% -5.6%

Aggregate C -19.7% -24.4% -7.4% -4.4% -2.4% -10.3% -4.0% 2.0% 2.2% 4.9% -3.2%

28 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

(FFO – Preferred Dividends – Common Dividends – Minority Dividends) / (Short-Term Debt + Long-Term

(Short-Term Debt + Long-Term Debt) / EBITDA

zation

erm Debt + Long-Term Debt + Deferred Taxes + Minority

Revenue

railing Five Years of Net Revenue Growth

Appendix B: Definition of Credit Ratios

Below we define the ratios presented in this study. Please note that these definitions are applied to adjusted financial numbers. For a detailed discussion of Moody’s global adjustments, please consult the references.

EBITA / Average Assets

EBITA / Average of Current and Previous Year Assets

EBITA / Interest Expense

EBITA / Interest Expense

EBITA Margin

EBITA / Net Revenue

(FFO + Interest Expense) / Interest Expense

(Funds From Operations + Interest Expense) / Interest Expense

FFO / Debt

Funds From Operations / (Short-Term Debt + Long-Term Debt)

RCF / Debt

Debt)

Debt / EBITDA

Debt / Book Capitali

(Short-Term Debt + Long-Term Debt) / (Short-TInterest + Book Equity)

Operating Margin

Operating Profit / Net

CAPEX / Depreciation Expense

CAPEX / Depreciation Expense

Revenue Volatility

Standard Deviation of T

29 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

, building materials, (low technology) component equipment, (non-consumer) finished

Media

d newspaper publishing, broadcast and subscription radio and television, and diversified media.

ng, aluminum and steel production and recycling.

s, department stores, general and specialty merchandise retailers, and various

services, consumer services, technology services, and defense services.

are, component equipment, consumer electronics, semiconductor and contract

Appendix C: Definition of Industry Aggregates

In this report we study the distribution of financial ratios across 13 industry aggregates. These aggregates are based on proprietary Moody’s coding of broad and specific industry categories. They may generally be described as follows:

Aerospace & Defense

Aircraft, aerospace and defense equipment and parts manufacturers.

Automotive

Commercial and passenger automotive and parts manufacturers.

Chemicals

Agricultural, commodity and specialty chemicals producers.

Consumer Products

Packaged food and beverage, household and personal care products, apparel and shoes, textiles and durable consumer products. Casinos, lodging, restaurants and general amusements. Pulp and (non-packaging) paper, wood products, agriculture, protein and tobacco processors. Paper, glass, metal and plastic packaging.

Energy & Environment

Oil & gas exploration and production, refining and marketing, and integrated oil companies. (Non-utility) electricity production, merchant energy, oil service and pipeline operators, environmental services and waste management.

Healthcare

Hospitals, long-term care facilities, outpatient facilities, medical device manufacturers and medical service providers. General and specialty pharmaceuticals.

Manufacturing

Heavy machinery

products, and transportation equipment manufacturers. Commercial and residential construction, homebuilding.

Book an

Metals & Mining

Coal and metal mini

Retail & Distribution

Grocery stores, drug storewholesale distributors.

Services

Business

Telecommunications Computer hardware, softw

manufacturers. Wireless, wireline, towers, satellite equipment and services, equipment manufacturers and integrated telecommunications companies.

30 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Transportation

Equipment leasing, airlines, air freight, railroad and maritime shipping, commuter transportation.

Moody’s Related Research

Special Comment:

Moody's Financial Metrics™ Key Ratios By Rating and Industry For Global Non-Financial Corporations: 2008, January 2009 (113940)

Moody's Financial MetricsTM Key Ratios By Rating And Industry For European, Middle Eastern And African Non-Financial Corporations: 2008, January 2009 (113942)

Moody’s Financial MetricsTM Key Ratios by Rating and Industry for North American Non-Financial Corporations: 2008, January 2009 (113941)

The Distribution of Common Financial Ratios by Rating and Industry for North American Non-Financial Corporations: 2008, July 2006 (98551)

Moody’s Senior Ratings Algorithm & Estimated Senior Ratings, February 2009 (114614)

Rating Methodology:

Moody's Approach to Global Standard Adjustments in the Analysis of Financial Statements for Non-Financial Corporations - Part I, February 2006 (96760)

Moody’s Approach to Global Standard Adjustments in the Analysis of Financial Statements for Non-Financial Corporations - Part II, February 2006 (96729)

Moody’s Approach to Global Standard Adjustments in the Analysis of Financial Statements for Non-Financial Corporations - Part III , September 2006 (98842)

Special Report:

Moody’s Basic Definitions for Credit Statistics, June 2007 (78480)

To access any of these reports, click on the entry above. Note that these references are current as of the date of publication of this report and that more recent reports may be available. All research may not be available to all clients.

31 December 2009 Special Comment Moody’s Global Corporate Finance - Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

Special Comment Moody’s Global Corporate Finance

Moody's Financial Metrics™ Key Ratios by Rating and Industry for Global Non-Financial Corporations: December 2009

CREDIT RATINGS ARE MOODY'S INVESTORS SERVICE, INC.'S (MIS) CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MIS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS DO NOT CONSTITUTE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS ARE NOT RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. CREDIT RATINGS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MIS ISSUES ITS CREDIT RATINGS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE. © Copyright 2009, Moody’s Investors Service, Inc., and/or its licensors and affiliates (together, "MOODY'S”). All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT. All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, such information is provided “as is” without warranty of any kind and MOODY’S, in particular, makes no representation or warranty, express or implied, as to the accuracy, timeliness, completeness, merchantability or fitness for any particular purpose of any such information. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The credit ratings and financial reporting analysis observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER. Each rating or other opinion must be weighed solely as one factor in any investment decision made by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security and of each issuer and guarantor of, and each provider of credit support for, each security that it may consider purchasing, holding or selling. MOODY’S hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MOODY’S have, prior to assignment of any rating, agreed to pay to MOODY’S for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,400,000. Moody’s Corporation (MCO) and its wholly-owned credit rating agency subsidiary, Moody’s Investors Service (MIS), also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually on Moody’s website at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Report Number: 121772

Authors Senior Production Associate

Jennifer Tennant

Albert Metz

Wing Chan

![[XLS]dev.eiopa.europa.eu · Web view2 6 6 7/7/2014 8 7/7/2014 1 7 7 7/7/2014 9 7/7/2014 1 8 8 7/7/2014 10 7/7/2014 1 9 9 7/7/2014 11 7/7/2014 1 10 10 7/7/2014 12 7/7/2014 1 11 11](https://img.pdfslide.net/doc/110x75/5ae5800d7f8b9a8b2b8bf1f3/xlsdeveiopa-view2-6-6-772014-8-772014-1-7-7-772014-9-772014-1-8-8-772014.jpg)

![December 21, 2015 - Wisconsin Supreme Court · RB-1 (2015) [?\^]`_ acbedgfhbeij[ ahik[ l 1. mon#p qsrHt`rvuxwnzye{E|}ux~)r 'p n#w )rv|}ux~x 7 7 7 7 7 7 7 7 7 7 7 7 7 7 7 7 7 7 7 7](https://img.pdfslide.net/doc/110x75/5fb3422fccf05f68ab3a22e4/december-21-2015-wisconsin-supreme-court-rb-1-2015-acbedgfhbeij-ahik.jpg)