Embed Size (px)

Citation preview

7(a) LOAN GUARANTY PROGRAMFlexible financing for your small business customers

1

7(a) LOAN APPLICATION PROCESS

AT THE LGPC

Igniting the Flames of SuccessOFO/OCA LENDER RELATIONS SPECIALISTS’ TRAINING

September 6, 2017

Presenters – Brendell Givens and Betty Hill

7A LGPC LOCATIONS

2

6501 Sylvan Road, Suite 122

Citrus Heights, CA 95610

Phone: (877) 475-2435

262 Black Gold Blvd

Hazard, KY 41701

Phone: (606) 436-0801

General Questions:Phone: (877) 475-2435

Loan Mods (prior to full disbursement): [email protected]

LGPC MISSION STATEMENT

3

The mission of the Center is to efficiently

process 7(a) loan guaranty applications

and to provide assistance and oversight,

as necessary, to lenders before and after

submission.

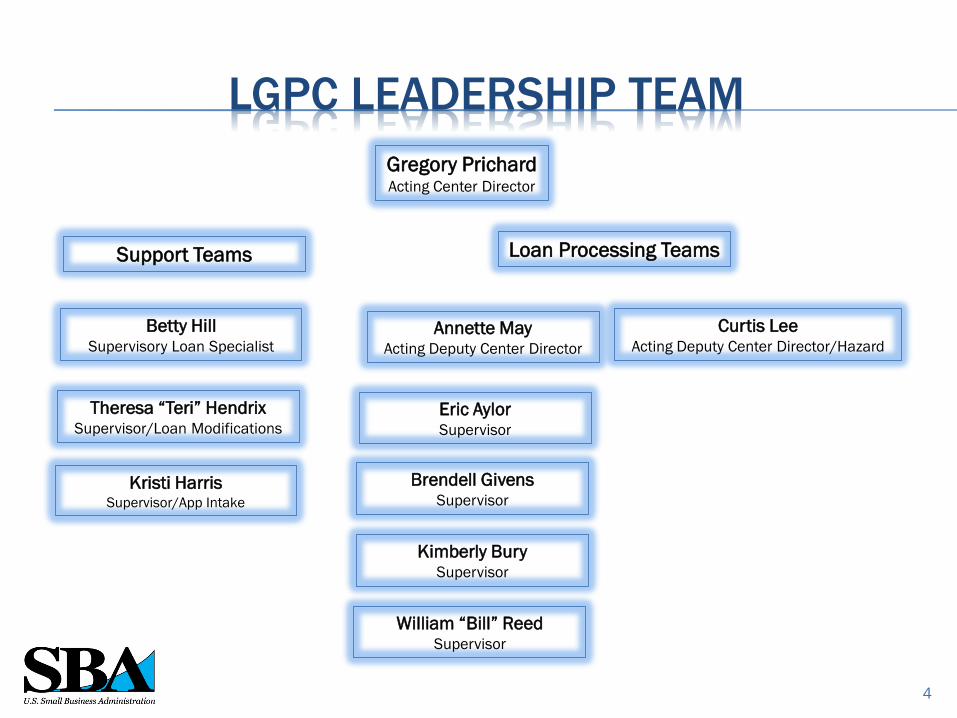

LGPC LEADERSHIP TEAM

Gregory PrichardActing Center Director

Annette MayActing Deputy Center Director

Betty HillSupervisory Loan Specialist

4

Brendell GivensSupervisor

William “Bill” ReedSupervisor

Kristi HarrisSupervisor/App Intake

Kimberly BurySupervisor

Eric AylorSupervisor

Loan Processing Teams

Curtis LeeActing Deputy Center Director/Hazard

Theresa “Teri” HendrixSupervisor/Loan Modifications

Support Teams

7(a) LOAN APPLICATION SUBMISSION PROCESS

5

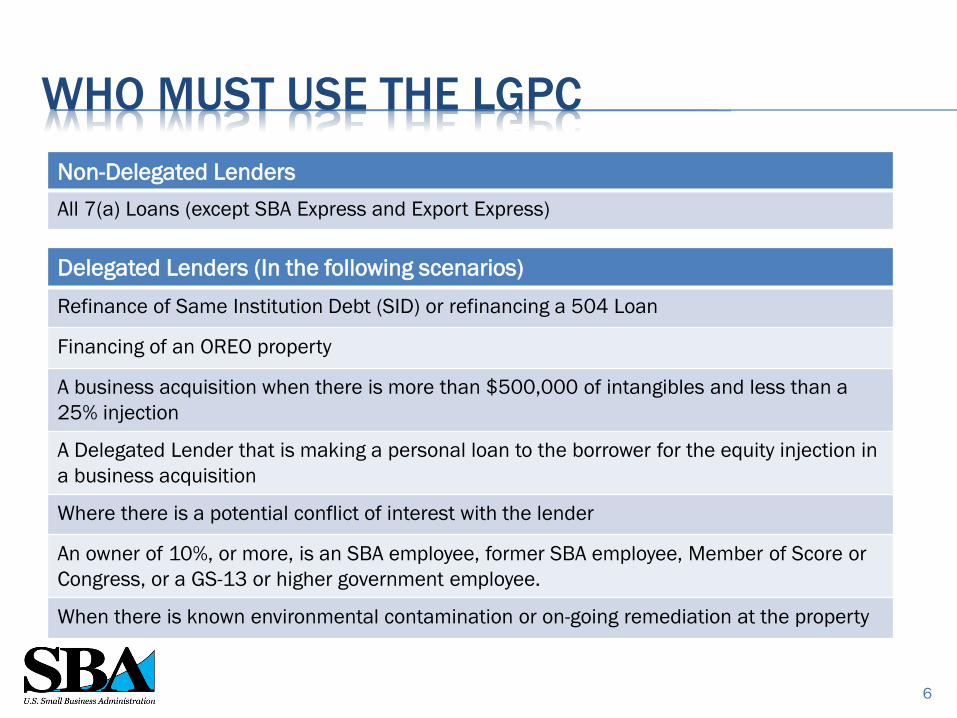

WHO MUST USE THE LGPC

Non-Delegated Lenders

All 7(a) Loans (except SBA Express and Export Express)

Delegated Lenders (In the following scenarios)

Refinance of Same Institution Debt (SID) or refinancing a 504 Loan

Financing of an OREO property

A business acquisition when there is more than $500,000 of intangibles and less than a

25% injection

A Delegated Lender that is making a personal loan to the borrower for the equity injection in

a business acquisition

Where there is a potential conflict of interest with the lender

An owner of 10%, or more, is an SBA employee, former SBA employee, Member of Score or

Congress, or a GS-13 or higher government employee.

When there is known environmental contamination or on-going remediation at the property

6

SUBMISSION METHODS

SBA One or E-TRAN Origination

1. Create an application

2. Answer required questions

3. Verify data

4. Attach documents

5. Submit

Status will change from “Application in Process” to “Review Reviewer 1”

If the status is anything other than “Review Reviewer 1” the file will not transmit

to the LGPC.

➢ For questions regarding SBA One, contact Colson’s SBA One support services at

[email protected] or 877-245-6159, Call Option 5

➢ For questions regarding E-TRAN, contact Ryan Gerald at [email protected] or Glenn

Hannon at [email protected]

➢ For general submission questions contact [email protected]

7

WHAT NEEDS TO BE INCLUDED?

For submissions to the Center Small & CA Loans Regular 7(a)

Form 1919 (complete Borrower Application) X X

Form 1920 (complete Lender Application) X X

Lender Credit Memorandum (see detail page) X X

Personal Financial Statements for all principals owning 20% or

greater

X

912s (where required) * X X

USCIS Verification (where required) * X X

Business Financials (Interim + 3 prior yrs.) including debt

schedule

X

Projections with reasonable assumptions for start-ups and

change of ownership

X

Affiliate Financials (Interim + 3 prior yrs.) X

Draft Authorization (CLP Submissions) X

8

* We suggest submitting the following forms to the appropriate Agencies as early in the application process as possible to avoid

any unnecessary delays in the application process: IRS Form 4506-T, Form 912 Statement of Personal History, and Form G-845

WHAT ELSE SHOULD BE INCLUDED?

For submissions to the Center Small Loan & CA Loans Regular 7a

Copies of all notes to be refinanced X X

Transcripts for Same Institution Debt (SID) X X

Copy of Business Purchase Agreement X X

Seller Financials signed by Seller (Interim + 3 prior yrs.) X

Lender Certification that Financials are verified against IRS

Transcripts *

X X

Internal or External Business Valuation per SOP guidelines X X

Real Estate Purchase Agreement OREO property only X

Real Estate Appraisal (OREO properties only) X X

Franchise Documents (see next page for detail) X X

9

* We suggest submitting the following forms to the appropriate Agencies as early in the application process as possible to avoid

any unnecessary delays in the application process: IRS Form 4506-T, Form 912 Statement of Personal History, and Form G-845

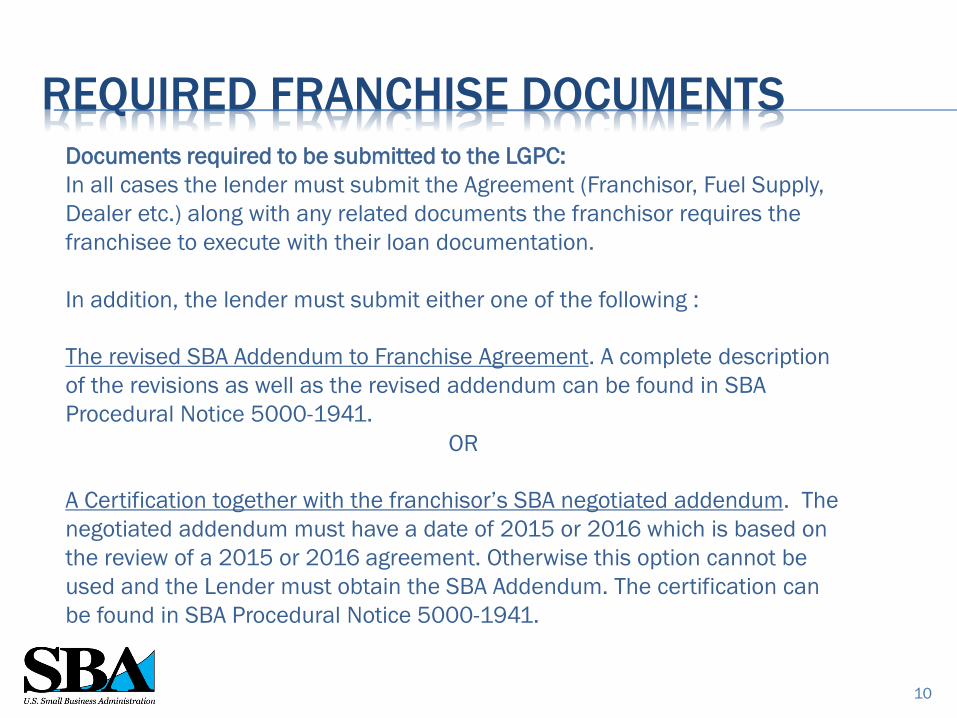

REQUIRED FRANCHISE DOCUMENTS

10

Documents required to be submitted to the LGPC:

In all cases the lender must submit the Agreement (Franchisor, Fuel Supply,

Dealer etc.) along with any related documents the franchisor requires the

franchisee to execute with their loan documentation.

In addition, the lender must submit either one of the following :

The revised SBA Addendum to Franchise Agreement. A complete description

of the revisions as well as the revised addendum can be found in SBA

Procedural Notice 5000-1941.

OR

A Certification together with the franchisor’s SBA negotiated addendum. The

negotiated addendum must have a date of 2015 or 2016 which is based on

the review of a 2015 or 2016 agreement. Otherwise this option cannot be

used and the Lender must obtain the SBA Addendum. The certification can

be found in SBA Procedural Notice 5000-1941.

WHO NEEDS TO COMPLETE THE FORM 1919?

For ALL Regular 7(a) Processing including Small & CA Loans

For a sole proprietorship, the sole proprietor

For a partnership, all general partners, and all limited partners owning 20% or more of the

equity of the firm, or any partner that is involved in management of the applicant business

For a corporation, all owners of 20% or more of the corporation and each officer and director

For limited liability companies (LLCs), all members owning 20% or more of the company and

each officer, director, and managing member

Any person hired by the business to manage day-to-day operations

11

Make sure that each 1919 is signed and dated.

WHAT SHOULD BE COVERED IN YOUR CREDIT MEMO?

Do the loan terms match the 1920 and your Draft Authorization?

Addressed financial analysis including repayment ability from operations?

Is the request for SBA funds clearly articulated?

Have you addressed Credit Elsewhere?

Have you clearly addressed the eligibility of each note to be refinanced? (e.g. unreasonable terms, 10% savings)

Have you addressed the specific collateral that will secure the proposed loan? If so, have you done a liquidation

value evaluation to determine whether the loan is fully secured?

Discussed business and management history?

How about the personal history, experience and credit history of the principals?

If repayment is based upon projections, have you addressed why they are reasonable?

Changes of Ownership – why is it good for the business? Experience of new owner, recent business trends,

seller financing standby terms?

If there is other financing involved, has it been addressed?

Injection and need for working capital

12

LGPC WORKFLOW

The completeness of the submission package will impact the efficiency of the

processing timeline.

13

PRIMARY SCREEN-OUT REASONS

14

THE TOP FIVE CATEGORIES

The top 5 categories account for 78% of the total Screen Outs Fiscal YTD

29%

26%10%

7%

6%

22% Credit Memo Incomplete

FinancialStatements/Projections

Debt Refinance

1919/1920Missing/Incompletee

Change of Ownership

Other

15

NUMBER ONE…

Credit Memo Incomplete

Collateral Shortfall not addressed

Life Insurance not addressed

Derogatory credit not addressed

including Delinquent Federal

Debt

Use of Proceeds Unclear

Need for Working Capital not

addressed

Schedule of Collateral Missing or

Incomplete

Certification that financial

information has been verified

against IRS Transcripts is missing

Shareholder debt not placed on

standby or not addressed

Draft Authorization conflicts with

Credit Memo

Notes to be refinanced not clearly

identified

Justification for refinance not

properly addressed (Benefit to the

Borrower)

Justification for Projections not

addressed

16

2ND ON THE LIST …

Financial Statements Missing/Incomplete

Affiliate financial statements missing/incomplete

Projections missing or assumptions not included

Borrower’s historical financial statements missing/incomplete

Personal Financial Statement Incomplete

Debt schedule missing/incomplete or doesn’t match balance sheet debt

Pro-forma Balance Sheet missing/incomplete

Seller financial statements missing/incomplete

Make sure that current YTD Business Financials are no older than 180 days from submission to SBA

Make sure the Personal Financial Statement is no older than 90 days from submission to SBA

17

3RD ON THE LIST…

Debt Refinance

Copy of Notes to be Refinanced Missing

Transcripts for Same Institution Debt Refinance Missing

Benefit to Business Not Stated

Loan to be Refinanced on Reasonable Terms Not Met

10% Improvement to Cash Flow Not Met

Same Collateral Position Required When Refinancing

Certification that Credit Card was Used for Business Purposes Missing

18

4TH ON THE LIST…

Forms 1919 and 1920

Forms are missing, incomplete or unsigned

Co-borrower ownership % is not reflected on form

Ownership identified does not total 100%

Other SBA loans are not identified on 1920

Use of Proceeds on 1920 is incomplete or doesn’t match credit memo

Trade Name (dba) left blank when applicable on 1920

Payment Amount and Rate Adjustment Frequency missed on 1920

19

5TH ON THE LIST…

Change of Ownership

Asset Purchase/Stock Purchase Agreement Missing

Third party Independent Business Valuation Missing/Unacceptable

Lender’s Internal Business Valuation Missing/Unacceptable

Change of Ownership Appears Ineligible

Payment to Associate

EPC partner buyout

Finance amount not supported by business valuation

20

7(a) LOAN MODIFICATION PROCESS

21

The lender may request modifications to the terms and

conditions of the Authorization at any time after approval.

Prior to final disbursement, LGPC modifications should be sent by e-mail to

[email protected] or by fax (202) 481-0861. A 2237 Form is not

required.

After final disbursement, LGPC modification requests must be sent to the

appropriate CLSC – Fresno or Little Rock.

*(For EWCP loans, submit the request to the appropriate USEAC.)

22Visit us at: www.sba.gov/CitrusHeightsLGPC

REQUESTING A LOAN MODIFICATION

For PLP processing, the lender may modify the authorization

under its delegated authority. The file must be documented with

a written explanation that includes justification for the change

and any supporting documentation.

Exceptions: The following actions require SBA approval:

Change in the guaranty % - If funds have been disbursed, rate is

locked.

Reinstatement - SOP 50 10 5 (I), Page 135.

Transfer of participation – the form MUST be signed by both

Lenders

Preference issues

23Visit us at: www.sba.gov/CitrusHeightsLGPC

PLP LOAN MODIFICATION PROCESS

Submit a written request to the LGPC (via e-mail ) that includes the name of the lender, name of the lending officer, phone number, fax number, name of the borrower, SBA Loan Number and the following information:

How it is now;

How it should be; and

Why (justification for the change and any supporting documentation must be included to process the request).

Please include the e-mail address you want the completed request returned to.

24Visit us at: www.sba.gov/CitrusHeightsLGPC

LOAN MODIFICATION FORMAT

LGPC UNILATERAL ACTIONS…

25

No SBA Approval is Required – Changes are made in E-Tran by the Lender

1. Lender can cancel the SBA Guaranty in E-Tran.

2. Lender can extend the Maturity Date (prior to the stated maturity expiring).

3. Lender can change the loan from a revolving to a non-revolving loan in E-Tran.

4. Lender can change the Borrower’s Name or Address in E-Tran.

5. Lender can process the Assumption of the loan without releasing an Obligor

(Adding a Borrower).

6. Lender can ADD a Guarantor (All SOP Requirements apply as in original

processing).

7. Lender will Classify the loan in “liquidation” status.

8. Lender can change the interest rate prior to the first disbursement.

9. Lender can extend the final disbursement date. 48 months is already stated

in the Loan Authorization which is the maximum number of months allowed.

10. Lender can change the name and the title of the individual signing the Loan

Authorization on behalf of the Lender.

LGPC UNILATERAL ACTIONS (CONT.)…

26

No SBA Approval is Required – Changes are made in E-Tran by the Lender

11. Lender can change “Furnish year end statement to Lender within _____ days

of fiscal year end” not to exceed 120 days of the fiscal year end.

12. Performance Bond Waiver – No modification required -SOP 50 10 5 (I), Page

179 (13 CFR 120.200)

SBA has granted a blanket waiver on the requirement of a performance bond when a 3rd

party in the business of construction management services controls the disbursement of

the loan proceeds.

13. Lender can change the monthly payment amount – the Loan Authorization

states the Lender should amortize at least annually.

14. Lender can change the adjustment period without a modification.

15. Lender can change from the Date of the Note to the Date of Initial

Disbursement without a modification.

16. Lender may establish the payment due date without submitting a

modification.

LENDER RESOURCES

27

SBA.GOV

28

SBA.GOV …FOR LENDERS

29

SBA.GOV …LGPC

30

THANK YOU FOR ATTENDING THIS BREAK OUT SESSION

31