Embed Size (px)

Citation preview

8/25/04

Valerie Tardiff and Paul JensenOperations Research Models and Methods

Copyright 2004 - All rights reserved

Economic Decision Making

Decisions using Time Value of Money Models

2

Engineering Economic Analysis Recall the seven steps of

Engineering Economic Analysis

3

Why Do We Make Investments? Buy stock in return for dividends and a higher

stock price in the future. Invest in a machine in return for reduced

operating costs or greater sales in the future. Buy a bond in return for interest payments

and the return of principal in the future.

We give up money now in the hopes of receiving more money in the future.

How much return is enough?

4

Why Do We Borrow Money? We borrow money to buy a $100,000

house in return for paying $300,000 over the next 30 years.

We borrow $10,000 to buy a car and pay an extra $2,000 in interest.

We buy a new set of clothes and put the bill on our credit card.

We spend money now in return for paying more money in the future.

How much are we willing to pay?

5

Example Your brother borrows $200 from you. He will pay back in monthly payments of

$14.44 for the next 16 months. Is this an acceptable investment for you,

the lender (or investor)? Is this an acceptable loan for your brother,

the borrower?

6

Cash Flow for Lender

0

14.44

0 1 2 3 4 5 6 7 8 16

……

……

-200

For the investor

7

Is this an acceptable investment? What is the total summed over all cash

flows? -200 + $14.44 (16) = $31.04

Is this enough?

Say the lender requires a minimum return of 1% per month. Does this investment obtain the required return?

8

Selection Procedure Choose

a Minimum Acceptable Rate of Return (MARR) (for the lender) or

Evaluate the Equivalent Value of the Cash Flow using the MARR: Compute the Net Present Worth (NPW), compute the Future Worth (FW) , or compute the Net Annual Worth (NAW).

If the NPW, FW or NAW is ≥ 0, accept the investment or the loan. Otherwise, accept the do-nothing alternative. In other

words, reject the investment or the loan.

9

The NPW as a function of MARR

2.5

-15-10-505

101520253035

0 0.5 1 1.5 2

Net Present Worth

MARR (Percent)

Recall our Example,NPW = –200 + 14.44 (P/A, MARR, 16)

When MARR is 1%, NPW is > 0, so accept the investment.

10

Minimum Acceptable Rate of Return (MARR)

In theory, the minimum acceptable rate of return (MARR) is the interest rate that could be received if the funds were invested elsewhere.

It helps to think of it as the hurdle rate.

11

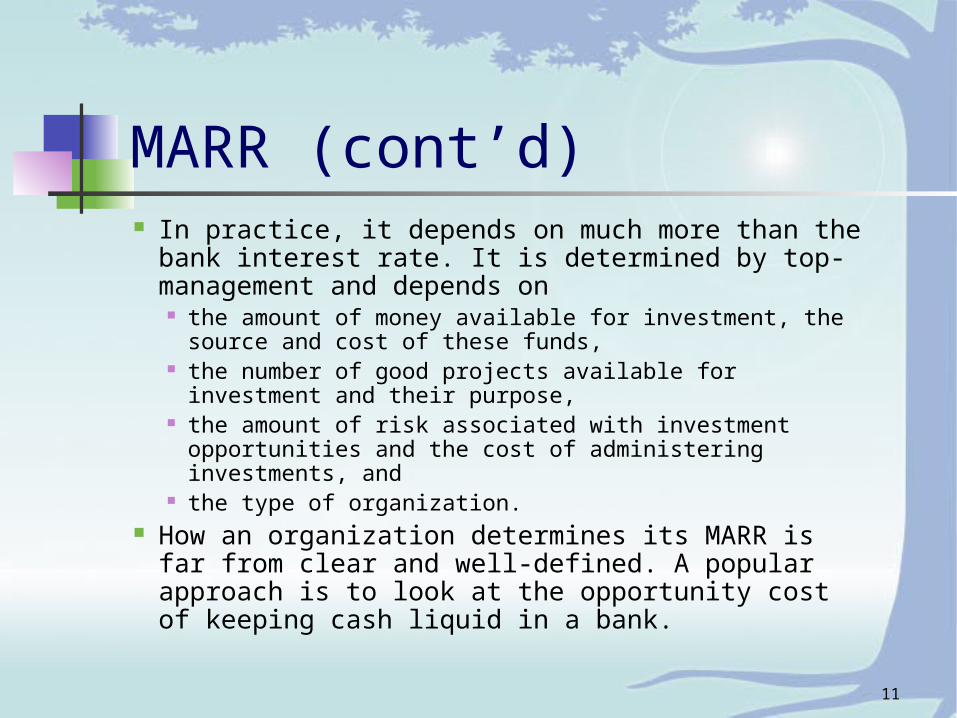

MARR (cont’d) In practice, it depends on much more than the bank

interest rate. It is determined by top-management and depends on the amount of money available for investment, the source

and cost of these funds, the number of good projects available for investment and

their purpose, the amount of risk associated with investment opportunities

and the cost of administering investments, and the type of organization.

How an organization determines its MARR is far from clear and well-defined. A popular approach is to look at the opportunity cost of keeping cash liquid in a bank.

12

Net Present Worth The Net Present Worth method, also called the Present Worth (PW), method compares all cash flows only after they have been measured at a common point in time determined to be the present date.

To find the NPW as a function of i%, we transform cash flow amounts to their equivalent in the present and add them.

NPW = CF0 + CF1 (P/F, i,1) + CF2 (P/F, i,2) + …. + CFN (P/F, i, N)

13

0

-14.44

0 1 2 3 4 5 6 7 8 16

……

……

200

For the borrower

Cash Flow for the Borrower

14

Is this an acceptable loan?

What is the total summed over all cash flows? 200 - $14.44 (16) = - $31.04

Is this reasonable?

Say the borrower wants a cost of borrowing no more than 2%. Does this loan cost more than the maximum acceptable rate for borrowing?

Compute the NPW using the MARB. If it is positive, accept the loan, otherwise reject.

15

2.5

-35-30-25-20-15-10-505

1015

0 0.5 1 1.5 2

Net Present Worth

MARB (Percent)

The NPW as a function of MARB Recall our example,

NPW = +200 - 14.44 (P/A, MARB, 16)

When MARB is 2%, NPW is > 0, so accept the loan.

16

Maximum Acceptable Rate of Borrowing (MARB)

The maximum acceptable rate of borrowing (MARB) is the interest rate that would be paid if the funds were borrowed elsewhere.

The interest rate charged by a bank is often the MARB used.

17

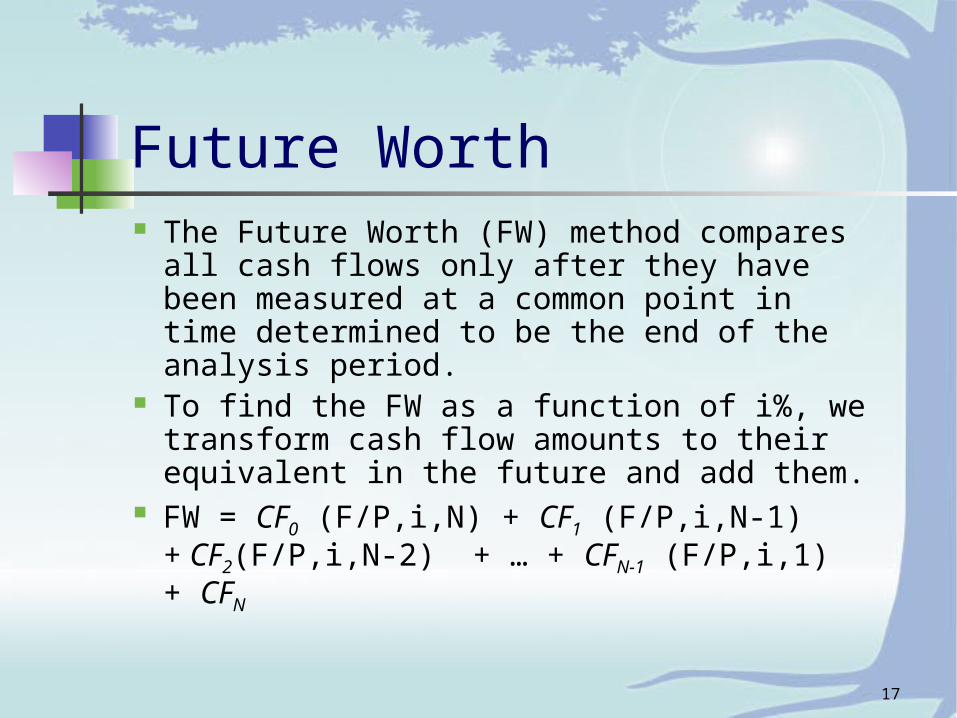

Future Worth The Future Worth (FW) method compares

all cash flows only after they have been measured at a common point in time determined to be the end of the analysis period.

To find the FW as a function of i%, we transform cash flow amounts to their equivalent in the future and add them.

FW = CF0 (F/P,i,N) + CF1 (F/P,i,N-1) + CF2(F/P,i,N-2) + … + CFN-1 (F/P,i,1) + CFN

18

Net Annual Worth The Net Annual Worth (NAW) method, also called the Annual Worth (AW), method compares all cash flows only after they have been transformed into time-equivalent annuities.

To find the NAW as a function of i%, we transform the cash flows over time as uniform payments over the length of the project period.

NAW = NPW (A/P, i, N) = FW(A/F, i, N)

19

Equivalence NPW, FW, and NAW all yield the same

decision since they are all the representations of the same cash flows at different points of time.

NAW = NPW (A/P, i, N) FW = NPW (F/P, i, N)

where i = MARR for the investor

i = MARB for the borrower

20

Capital Recovery Cost In most engineering situations, the capital cost has two components I, the investment expended at time 0, and S, the salvage value received at time N.

I

0

S

N

21

Capital Recovery Cost (cont’d) Capital Recovery (CR) Cost is the annual

equivalent of the capital cost. CR (i) = I (A/P, i, N) - S (A/F, i, N) Other Formulas

CR (i) = (I -S) (A/P, i, N) + i S and CR (i) = (I -S) (A/F, i, N) + i I

22

Example Your company is planning to manufacture a new product. The product requires a machine that the company does not now own. The cost of the machine is $10,000, its life is 4 years, and its salvage value (at the end of the 4th year) is $1,000. With this machine, the new profit from each product is $12. What annual production makes the investment worthwhile? The MARR is 10%.

23

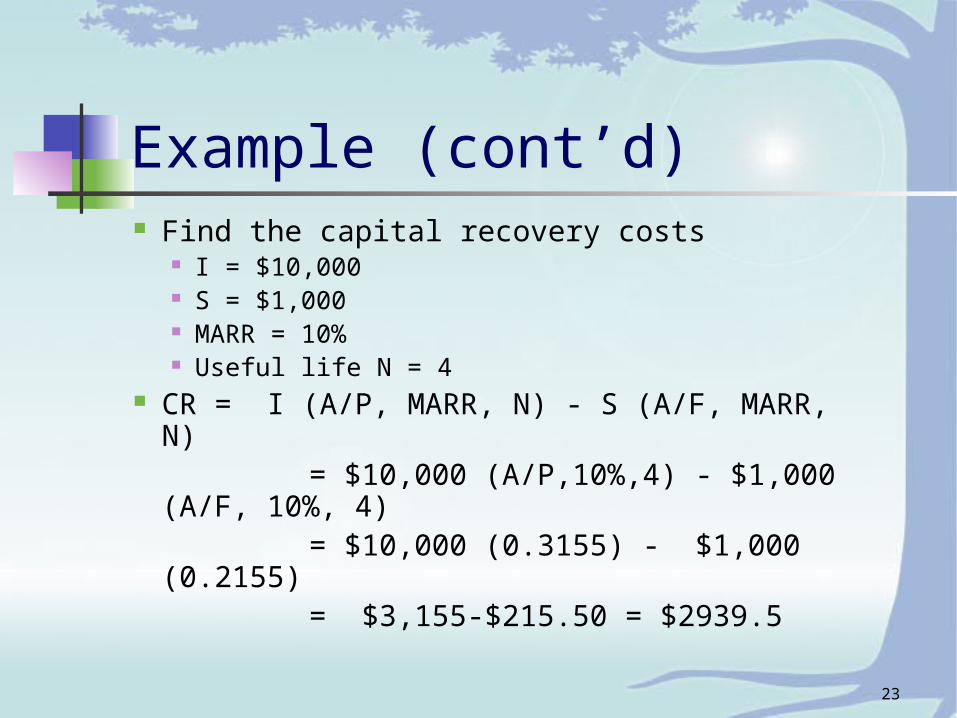

Example (cont’d) Find the capital recovery costs

I = $10,000 S = $1,000 MARR = 10% Useful life N = 4

CR = I (A/P, MARR, N) - S (A/F, MARR, N) = $10,000 (A/P,10%,4) - $1,000 (A/F, 10%,

4) = $10,000 (0.3155) - $1,000 (0.2155) = $3,155-$215.50 = $2939.5

24

Example (cont’d) Using the shortcuts,we get CR = (I-S) (A/P,10%,4) + (10%) S

= $9,000 (0.3155) + (0.1)$1,000

= $2,839.5 + $100 = $2939.5 CR = (I-S) (A/F,10%,4) + (10%) I

= $9,000 (0.2155) + (0.1)$10,000

= $1,939.5 + $1,000 = $2939.5

25

Example (cont’d) Capital recovery costs must equal or

exceed revenues to be profitable. CR = $2939.5 = $12x where x is the

number of products produced per year. Solving for x, we get x >= 250 units.