Embed Size (px)

Citation preview

ASEAN in the World’s Spotlight

ASEAN Business Intelligence Report

May 2012

เมื่อ 10 ประเทศสมาชิกอาเซียนรวมตัว แกนเศรษฐกจิ โลกเปลี่ยนทิศทางการหมนุ

ในปี 2011 อาเซียนมีผลิตผลมวลรวมหรือ GDP อยู่ที่ 2.72 ล้านล้านดอลล่าร์สหรัฐฯ คิดเป็น 3% ของผลผลิตมวลรวมของโลก และจะเพิ่มสูงขึ้นเป็น 25% ในปี 2050 ดังนั้น อาเซียนจึงเป็นโอกาสใหม่ของนักลงทุนทั่วโลก และปัจจัยหลักที่จะท าให้อาเซียนกลายเป็นศูนย์กลางการลงทุนของโลกแห่งใหม่ คือ ทรัพยากรธรรมชาติที่มีความพร้อมต่อการผลิต โดยเฉพาะอิ น โ ดนี เ ซี ย ซึ่ ง นั บ ว่ า เ ป็ นปร ะ เ ทศที่ มี ค ว ามพร้ อมด้ า นทรัพยากรธรรมชาติมากที่สุดในอาเซียน ในช่วง 10 ปีที่ผ่านมาอาเซียนมีน้ ามันส ารองเพิ่มขึ้นถึงร้อยละ 50 ในขณะที่ตะวันออกกลางเพิ่มขึ้นเพียงร้อยละ 14 ลาวและพม่าพร้อมที่จะเป็นแหล่งผลิตไฟฟ้าขนาดใหญ่ของเอเซีย (Battery of ASIA) เม็ดเงินลงทุนจ านวนมหาศาลจะเคลื่อนย้ายไปยังกลุ่มประเทศต่างๆ ที่เปิดบ้านต้อนรับนักลงทุนจากทั่วโลก ระบบขนส่งที่เปดิโอกาสตอ่การเขา้สูต่ลาดหลกัของโลกอยา่งจนีและอินเดีย เส้นทาง Asian Highway Routes ในอาเซียน 39 เส้นทาง ส่งผลให้กลุ่มประเทศอาเซียนมีความสะดวกและคล่องตัวในการเคลื่อนย้ายสินค้า บริการและแรงงาน ประเทศไทยมี Highway Routes มากที่สุดในอาเซียน ในขณะที่อินโดนีเซียและฟลิปปินส์ไม่มี Highway Route เช่ือมต่อกับประเทศในกลุ่มอาเซียนเลย การพัฒนาของฝีมือแรงงานและอัตราค่าจ้างแรงงาน หากมองย้อนเกือบ 10 ปีที่ผ่านมา จะพบว่า มีเม็ดเงินจ านวนกว่า 7 ล้านล้านดอลล่าร์สหรัฐฯ ที่ไหลเข้าสู่กลุ่มประเทศในอาเซียน เมื่อเงินทุนเคลื่อนย้าย กลุ่มแรงงานจึงมีการเคลื่อนย้ายตาม ทิศทางการลงทุนในอาเซียนด้วยเช่นกัน กลุ่มแรงงานทักษะพร้อมจะกระจายตัวเข้าสู่ประเทศที่มีศักยภาพการจ้างงาน และกลุ่มแรงงานไร้ทักษะพร้อมจะเคลื่อนย้ายกลับภูมิล าเนาของตัวเอง เพราะมีโอกาสในการประกอบอาชีพ ใน ASEAN Business Intelligence Report : May 2012 ฉบับนี้ จะพูดถึงแนวโน้มหรือเทรนด์ที่จะเกิดขึ้นในอนาคตอันใกล้ โดยเริ่มจากประเด็นแรงงานในอาเซียน เมื่อโลกทั้งโลกเฝ้าจับตากลุ่มอาเซียน (ASEAN in the world’s spotlight)

MEGA TREND 1

ASEAN in the world’s spotlight

MEGA TREND 2

Technology dominated, Anywhere & Anytime

MEGA TREND 3

Rising ASEAN Middle Class

MEGA TREND 4

World’s Aging Society

MEGA TREND 5

Faces of Future

MEGA TREND 6 Power of Women

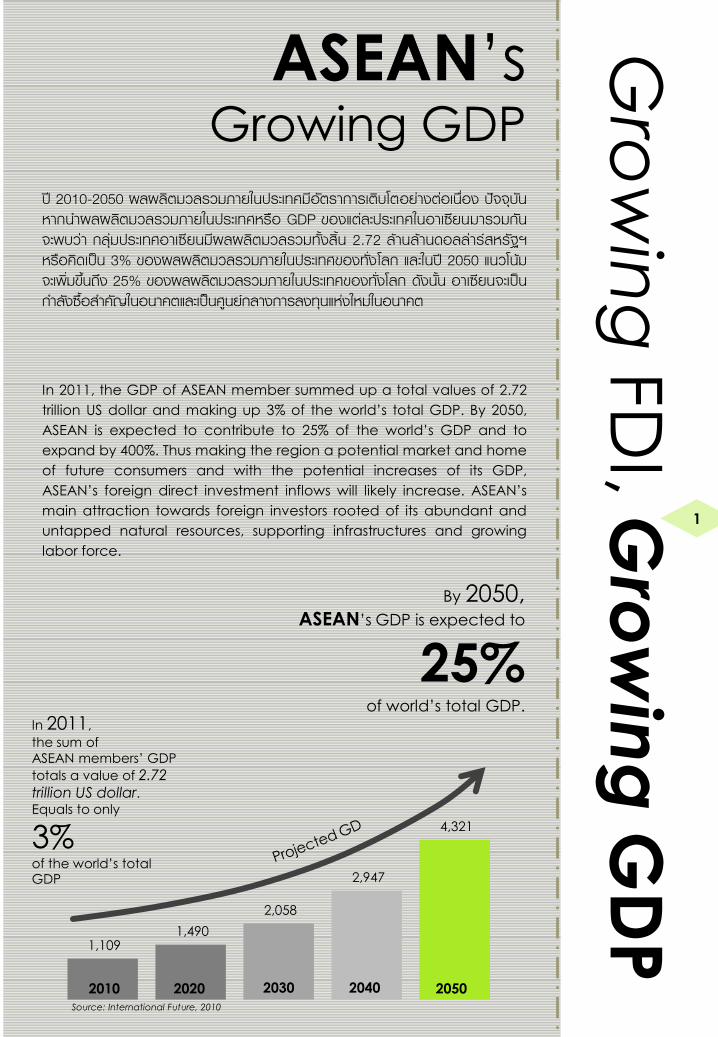

ปี 2010-2050 ผลผลิตมวลรวมภายในประเทศมีอัตราการเติบโตอย่างต่อเนื่อง ปัจจุบันหากน าผลผลิตมวลรวมภายในประเทศหรือ GDP ของแต่ละประเทศในอาเซียนมารวมกัน จะพบว่า กลุ่มประเทศอาเซียนมีผลผลิตมวลรวมทั้งสิ้น 2.72 ล้านล้านดอลล่าร์สหรัฐฯ หรือคิดเป็น 3% ของผลผลิตมวลรวมภายในประเทศของทั่งโลก และในปี 2050 แนวโน้มจะเพิ่มขึ้นถึง 25% ของผลผลิตมวลรวมภายในประเทศของทั่งโลก ดังนั้น อาเซียนจะเป็นก าลังซื้อส าคัญในอนาคตและเป็นศูนย์กลางการลงทุนแห่งใหม่ในอนาคต

By 2050, ASEAN’s GDP is expected to

25% of world’s total GDP.

1,109 1,490

2,058

2,947

4,321

2010 2020 2030 2040 2050 Source: International Future, 2010

In 2011, the GDP of ASEAN member summed up a total values of 2.72

trillion US dollar and making up 3% of the world’s total GDP. By 2050,

ASEAN is expected to contribute to 25% of the world’s GDP and to

expand by 400%. Thus making the region a potential market and home

of future consumers and with the potential increases of its GDP,

ASEAN’s foreign direct investment inflows will likely increase. ASEAN’s

main attraction towards foreign investors rooted of its abundant and

untapped natural resources, supporting infrastructures and growing

labor force.

In 2011,

the sum of

ASEAN members’ GDP

totals a value of 2.72 trillion US dollar. Equals to only

3% of the world’s total GDP

Gro

win

g F

DI, G

row

ing

GD

P

ASEAN’s Growing GDP

1

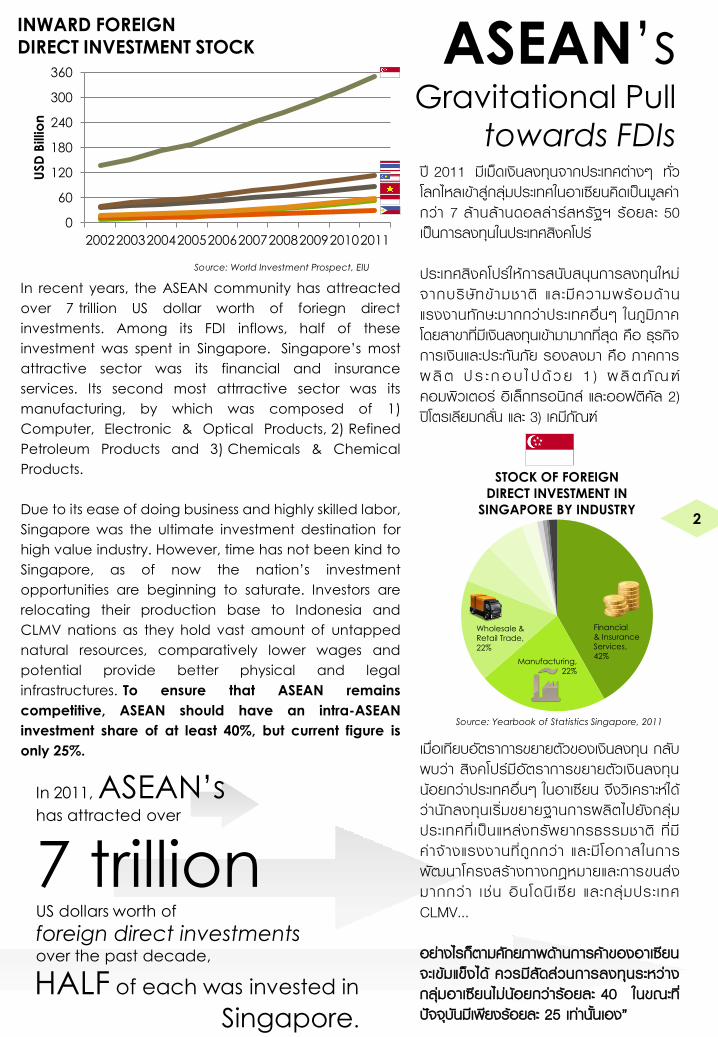

ปี 2011 มีเม็ดเงินลงทุนจากประเทศต่างๆ ทั่วโลกไหลเข้าสู่กลุ่มประเทศในอาเซียนคิดเป็นมูลค่ากว่า 7 ล้านล้านดอลล่าร์สหรัฐฯ ร้อยละ 50 เป็นการลงทุนในประเทศสิงคโปร์ ประเทศสิงคโปร์ให้การสนับสนุนการลงทุนใหม่จากบริษัทข้ามชาติ และมีความพร้อมด้านแรงงานทักษะมากกว่าประเทศอ่ืนๆ ในภูมิภาค โดยสาขาที่มีเงินลงทุนเข้ามามากที่สุด คือ ธุรกิจการเงินและประกันภัย รองลงมา คือ ภาคการผลิ ต ป ร ะ ก อ บ ไ ป ด้ ว ย 1 ) ผ ลิ ต ภัณ ฑ์คอมพิวเตอร์ อิเล็กทรอนิกส์ และออฟติคัล 2) ปิโตรเลียมกลั่น และ 3) เคมีภัณฑ์

ASEAN’s

Gravitational Pull

towards FDIs

STOCK OF FOREIGN

DIRECT INVESTMENT IN

SINGAPORE BY INDUSTRY

Financial

& Insurance

Services,

42% Manufacturing,

22%

Wholesale &

Retail Trade,

22%

Source: Yearbook of Statistics Singapore, 2011

In 2011, ASEAN’s has attracted over

7 trillion US dollars worth of

foreign direct investments over the past decade,

HALF of each was invested in

Singapore.

0

60

120

180

240

300

360

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

USD

Billio

n

Source: World Investment Prospect, EIU

INWARD FOREIGN

DIRECT INVESTMENT STOCK

เมื่อเทียบอัตราการขยายตัวของเงินลงทุน กลับพบว่า สิงคโปร์มีอัตราการขยายตัวเงินลงทุนน้อยกว่าประเทศอ่ืนๆ ในอาเซียน จึงวิเคราะห์ได้ว่านักลงทุนเริ่มขยายฐานการผลิตไปยังกลุ่มประเทศที่ เป็นแหล่งทรัพยากรธรรมชาติ ที่มีค่าจ้างแรงงานที่ถูกกว่า และมีโอกาสในการพัฒนาโครงสร้างทางกฎหมายและการขนส่งมากกว่า เ ช่น อินโดนี เซีย และกลุ่มประเทศ CLMV... อย่างไรก็ตามศักยภาพด้านการค้าของอาเซียนจะเข้มแข็งได้ ควรมีสัดส่วนการลงทุนระหว่างกลุ่มอาเซียนไม่น้อยกว่าร้อยละ 40 ในขณะที่ปัจจุบันมีเพียงร้อยละ 25 เท่านั้นเอง”

In recent years, the ASEAN community has attreacted

over 7 trillion US dollar worth of foriegn direct

investments. Among its FDI inflows, half of these

investment was spent in Singapore. Singapore’s most

attractive sector was its financial and insurance

services. Its second most attrractive sector was its

manufacturing, by which was composed of 1)

Computer, Electronic & Optical Products, 2) Refined

Petroleum Products and 3) Chemicals & Chemical

Products.

Due to its ease of doing business and highly skilled labor,

Singapore was the ultimate investment destination for

high value industry. However, time has not been kind to

Singapore, as of now the nation’s investment

opportunities are beginning to saturate. Investors are

relocating their production base to Indonesia and

CLMV nations as they hold vast amount of untapped

natural resources, comparatively lower wages and

potential provide better physical and legal

infrastructures. To ensure that ASEAN remains

competitive, ASEAN should have an intra-ASEAN

investment share of at least 40%, but current figure is

only 25%.

2

3

Shining the Spotlight on

“Foreign direct investments in

Indonesia grew 20% in 2010, with

total values of 175 trillion rupiah or

19.3 billion US dollars... At that rate,

Indonesia now appears to be

significantly outpacing many other

Asian countries that used to easily

surpass it in drawing foreign money,

one of which is Thailand.”

– Wall Street Journal –

x1

ASEAN GROWTH-GROWTH ANALYSIS (2002 – 2011)

X2 x3 x4 x5 x6 x7 x8

FDI Growth Rate (no. times)

Source: CIA World Factbook,

ASEAN Business Intelligence

ASEAN Average

3.6 folds 7

6

5

4

3

2

1

GD

P G

row

th R

ate

(%

)

Vietnam

Malaysi

a

Philippines

Thailand

Indonesia

While Thais are looking at Myanmar, the

eyes of the rest of the world is on Indonesia.

Over the past decade, Indonesia has

outpaced Signapore and the rest of the

ASEAN communicty with the highest GDP

and foreign direct investment growth.

Although Singapore has constantly been

receiving the highest amount to FDI inflows,

its acutal FDI growth was only 2.6 folds,

landing it in 4th place and below the ASEAN

average. Indonesia, however receive an

expectional growth of 7.6 folds. Within

Indonesia’s FDI inflow, its manufacturing

industry attracted the most foreign direct

investments, dominated other its other

sectors. As manufacturing base, raw material

are needed to support such production, thus

making mining its second most FDI attractive

industry.

ในช่วงทศวรรษที่ผ่านมา อินโดนีเซียได้ล ้าหน้าหลายๆ ประเทศในอาเซียนไปแล้ว ด้วยอัตราการขยายตัวของการลงทุนจากต่างชาติถึง 7.6 เท่า ในขณะที่สิงคโปร์มีอัตราการขยายตัวเพียง 2.6 เท่า เป็นอันดับที่สี่ของอาเซียนและน้อยกว่าอัตราการขยายตัวโดยรวมของอาเซียน กลุ่มอุตสาหกรรมที่ได้รับการสนใจจากนักลงทุนมากเป็นอันดับหนึ่ง คือ อุตสาหกรรมการผลิต รองลงมา คือ อุตสาหกรรมเหมืองแร ่การเข้ามาลงทุนอย่าง ต่อเนื่องในอินโดนีเซีย แสดงให้เห็นถึงความพึงพอใจของนักลงทุนที่มีต่ออินโดนีเซีย ซึ่งอาจเป็นผลมาจากการมีทรัพยากรทางธรรมชาติเป็นจ านวนมากในประเทศ ซึ่งเป็นปัจจัยส าคัญต่ออุตสาหกรรมการผลิต การมีจ านวนแรงงานมากที่สุด ในอาเซียนและเป็นแรงงานที่มีค่าจ้างต่ า ผลิตภาพคุ้มค่ากับอัตราค่าจ้าง การมีอัตราการบริโภคภายในประเทศที่สูง และแนวโน้มความมั่นคงทาง การเมืองที่มีมากขึ้น จึงเป็นเรื่องปกติที่นักลงทุนจากทั่วโลก ต่างให้ความสนใจกับประเทศอินโดนีเซีย

INDONESIA’s

ATTRACTIVENESS • Abundant &

untapped resource

• Value for money

labor

• Largest domestic

consumption

• Political stability

ไทยให้ความสนใจทีจ่ะไปลงทุนในพมา่ ในขณะทีท่ั่วโลกก าลงัมอง อนิโดนเีซยี

4

Manufacturing

Wholesale & retail trade

Financial services

Transport & Communication

Mining

Agriculture Total FDI

2004 2005 2006 2007 2008 2009 2010

4.0

2.5

1.0

-0.5

INDONESIA’S QUARTERLY FDI INFLOWS BY INDUSTRY Source: DBS Group Research B

illio

n U

S D

olla

rs

“As several multinational

automobile

manufacturers begin to

heavily invest in

Indonesia, one must

question if Thailand can

truly call itself Detroit of

Asia or will the Thai

automobile industry will end up like Detroit.”

Within 2014, over $4.1 billion worth of investments will be made in Indonesia.

Posco, multinational steel making company will spend up to $3 billion on a steelmaking

project

Suzuki Motor Corp. will spend $779 million to build an engine plant and increase output in

Indonesia

Toyota Motor Corp. plans to spend $337 million to expand its production capacity

Caterpillar Inc. is to invest $150 million to build a new factory to produce mining trucks for

customers across Asia and in Indonesia Source: Wall Street Journal, 2011

Thailand must determined where it

stands within the manufactring value

chain and hold tight to its standing

as the manufacturer of part and

product requiring high precision.

อินโดนีเซียมีทรัพยากรธรรมชาติมากที่สุดในอาเซียน ส่งผลให้มีการขยายตัวในอุตสาหกรรมการผลิตมากเป็นอันดับหนึ่ง ดังนั้น หากนักลงทุนทั่วโลกย้ายฐานการผลิตไปที่ อินโดนีเซีย ไทยจ าเป็นต้องเร่งพัฒนาศักยภาพฝีมือแรงงานและทักษะในด้านการบริหารจัดการ เพ่ือรักษาจุดแข็งที่แตกต่างของแรงงาน

5

Reason to Invest 1:

ABUNDANT & UNTAPPED

Natural Resources

MYANMAR

Petroleum, Timber, Tin,

Antimony, Zinc, Copper,

Tungsten, Lead, Coal,

Marble, Limestone,

Precious stones, Natural

gas, Hydropower

THAILAND

Tin, Rubber, Natural gas,

Tungsten, Tantalum, Timber,

Lead, Fish, Gypsum, Lignite,

Fluorite, Hydropower

CAMBODIA

Oil and gas, Timber,

Gemstones, Iron ore,

Manganese, Phosphate,

Hydropower

LAOS

Timber,

Hydropower,

Gypsum, Tin,

Gold, Gemstones

MALAYSIA

Tin, Petroleum,

Timber, Copper, Iron

ore, Natural gas,

Tungsten, Bauxite

SINGAPORE

Fish, Deep-

water ports

INDONESIA

Petroleum, Tin, Natural gas, Nickel, Timber, Bauxite,

Copper, Fertile soils, Coal, Gold, Silver

VIETNAM

Coal, Manganese,

Bauxite, Chromate, Oil

and gas, Forest,

Hydropower

BRUNEI

Petroleum, Natural

gas, Timber

PHILIPPINES

Timber, Silver, Gold,

Salt, Copper

Source: Asia Competitiveness Institute

INDONESIA:

can last over

มี ก๊าซ ใช้ได้เกิน Natural Gas supply

ปี

years

can last over

มี ถา่นหนิ ใช้ได้เกนิ Coal supply

ปี

years

เพียง 10 ปี ปริมาณน ้ามันส ารอง ในประเทศอาเซียน เพิ่มขึ้นร้อยละ 50 ในขนะที่น ้ามันส ารองในตะวันออกกลาง

เพิ่มแค่ร้อยละ 14 Within 10 years ASEAN’s Oil

Reserves increased almost

50%, while the Middle East’s

reserves increase

by only 14%.

2010

1990

2010

1990

ASEA

N

Mid

dle

Ea

st

Proved Oil Reserves (Billion Barrels)

11.6

17.2

659.6

752.5

“Due to the region’s abundant

and untapped natural resources,

strong supporting infrastructures

and growing labor force, ASEAN’s

FDI inflows will definitely continue

to increase.”

อาเซียน คอื ฐานการผลิตใหม่ของโลก

Source: Siam Intelligence Unit

6

WORLD LEADING RUBBER EXPORTERS

Source: Thai Rubber Association

If the world continues to consume its natural

resources at its current rate, the origination of

these natral resources will find their supplies

diminishing. As result, investors will have to search

and seek for future supplies in other geographical

areas. ASEAN and its untapped natural resources

will undoubtedly be one of the world’s future

origination of the world’s natural resources. For

instance, Indonesia will be the potential hub for

natural gas as it is located within the Ring of Fire.

Among the being the source for natural gas,

ASEAN also hold various other high demand

natural resource that includes oil, hydropower,

rubber, tin and copper. With many abandant

resources, member countries will be able to set

the world’s prices and penetrate the industries

that requires these resources. For example, ASEAN,

being the world’s largest exporter of rubber, can

positioned itself as manufacturer of medical

equipments or automotive and electronic parts.

Moreover, ASEAN will be able to set the price for

the world’s rubber supplies.

Discovering

ASEAN’s

Chest of Natural

Resources

% of the world’s 74 อาเชยีนส่งออก รอ้ยละ ยางพาราโลก rubber exporters are

ASEAN member countries

มีศักยภาพที่จะผลิตไฟฟ้าพลังน้ า ไดห้ลายหมื่นเมกะวัตต ์

LAOS PDR &

MYANMAR

Over 10,000 mega watts of

hydropower potential

can be found in

LAOS Battery of Asia

INDONESIA Mineral Riched

MYANMAR

ASEAN’s Unopened

present

SINGAPORE Grooming its citizens into the best resources it has

to offer

แหล่งทรัพยากรเดิมก าลังจะหมดไปจากโลกในไม่ช้า !! ดังนั้น นักลงทุนจึงต้องแสวงหาแหล่งทรัพยากรใหม่ อาเซียนเป็นขุมทรัพย์ด้านทรัพยากรแหล่งใหญ่ของโลก อินโดนีเซียตั้งอยู่แนว Ring of firer ก าลังจะกลายเป็นศูนย์กลางก๊าซธรรมชาติ นอกจากนี้อาเซียนยังมีทรัพยากรอ่ืนๆ อีกมากมาย อาทิ ยางพารา ดีบุก สังกะสี การมีทรัพยากรธรรมชาติเป็นจ านวนมาก จะท าให้ อาเซียนกลายเป็นผู้น าในการก าหนดราคาของตลาดโลกได้ และเป็นแหล่งดึงดูดนักลงทุนที่จ าเป็นต้องใช้ทรัพยากรธรรมชาติเหล่านี้ในการผลิต หากอาเซียนจะเป็นผู้น าในการส่งออกยางพารา ก็ควรให้ความส าคัญต่อการส่งออกอุปกรณ์ทางการแพทย์ การผลิตรถยนต์ รวมทั้งเครื่องใช้ไฟฟ้าต่างๆ และในอนาคตราคายางพาราโลกอาจถูกก าหนดโดยอาเซียน

THAILAND – MYANMAR

10 จังหวัด คือ เชียงราย (Chiang Rai), แม่ฮ่องสอน (Mae Hong Son), เชียงใหม่ (Chiang Mai), ตาก (Tak), กาญจนบุรี (Kanchanaburi), ราชบุรี (Ratchaburi), เพชรบุรี (Phetchaburi), ประจวบคีรีขันธ์

(Prachuap Khiri Khan), ชุมพร (Chumporn) และระนอง (Ranong)

THAILAND – LAOS

11 จังหวัด คือ เชียงราย (Chiang Rai), พะเยา (Phayao), น่าน (Nan), อุตรดิตถ์

(Uttatadit), พิษณุโลก (Phitsanulok), เลย (Loei), หนองคาย (Nong Khai), นครพนม (Nakorn Phanom), อ านาจเจริญ (Amnat Charoen), มุกดาหาร (Mukdahan) และอุบลราชธานี (Ubon Ratchathani)

THAILAND – CAMBODIA

7 จังหวัด คือ อุบลราชธานี (Ubon Ratchathani),

ศรีสะเกษ (Sisaket), สุรินทร์ (Surin), บุรีรัมย์ (Buriram),

สระแก้ว (Sa Kaew), จันทบุรี (Chanthaburi) และตราด (Tart)

THAILAND – MALAYSIA

4 จังหวัด คือ สตูล (Satou), สงขลา (Songkhla), ยะลา (Yala) และ นราธิวาส

(Narathiwat)

Thailand

10 gateways 4 countries

การขนส่ง 39 เส้นทางสู่อาเซียน ความสะดวกและคล่องตัวในการเคลื่อนย้าย สนิคา้ บรกิาร

และ แรงงาน ของอาเซียน

Reason to Invest 2:

Supporting Infrastuctures

7

Philippines 0 gateways 0 countries

Vietnam 5 gateways 3 countries

Cambodia 3 gateways 3 countries

Laos 9 gateways 3 countries

Myanmar 5 gateways 3 countries

Malaysia 4 gateway 2 countries

การคมนาคมเป็นปัจจัยส าคัญที่สนับสนุนการเคลื่อนย้ายเงินทุน สินค้า บริการ และแรงงานในกลุ่มประเทศอาเซียน ไทยตั้งอยู่ ในจุดกึ่งกลางของอาเซียน และมีความคล่องตัวด้านการคมนาคมขนส่งด้วย 10 เส้นทางที่สามารถเช่ือมต่อไปยัง 4 ประเทศ ใกล้เคียง และมีพื้นที่ 30 จังหวัดที่เช่ือมต่อกับประเทศเพื่อนบ้านของไทย ด้านหนึ่งติดกับมาเลเซียซึ่งเป็นประเทศมีอัตราการเติบโตในอุตสาหกรรมบริการและเป็นช่องทางการเคลื่อนย้ายแรงงานทักษะระหว่างประเทศ ด้านหนึ่งเช่ือมต่อกับลาว พม่า เวียดนามและกัมพูชา ซึ่งเป็นกลุ่มประเทศที่มีการเคลื่อนย้ายไร้ทักษะเข้าสู่ประเทศไทยเป็นจ านวนมาก

Singapore 3 gateways 2 countries

Source: UNESCAP

39gateways

to ASEAN’s connectivity and freeflows of products, services and

labor.

Transportation and supporting infrastuctures is a crucial component to

ASEAN’s factors ofproduction freeflows. Thailand has a total of 10

gateways connecting it to 4 other countries. Its connectedness with

Myanmar, Laos and Cambodia allow constant flow of labor, while being

connected to Malaysia allows the freeflow of skilled labors in the service

sector. Thus providing Thailand with a strategic location, opening its door

to ASEAN and the rest of the world. On the other hand, due to Indonesia

and Philippines’s archipelagic nature, the countries do not have any

gateways linking it to other countries. However, mass amount of water

surrounding it, it could become ASEAN’s maritime logistic center.

8

Indonesia 0 gateways 0 countries

0.19

3.21

3.69

8.80

11.90

39.62

39.81

46.48

117.00

Brunei

Darussalam

Singapore

Lao People's

Democrati…

Cambodia

Malaysia

Thailand

Philippines

Viet Nam

Indonesia

Source: CIA World Factbook LABOR FORCE

อาเซียน มีประชากรวัยท างานกว่า 429 ล้านคน กว่า 270 ล้านคน ประกอบอาชีพอยู่ในอุตสาหกรรมต่างๆ ซึ่งมีจ านวนมากกว่ากลุ่มแรงงานในสหรัฐเกือบ 1 เท่าตัว (135 ล้านคน) ประเทศที่มีกลุ่มแรงงานมากที่สุดในอาเซียน คือ อินโดนีเซีย คิดเป็นร้อยละ 44 ของแรงงานทั้งหมดในอาเซียน

MALAYSIA

The Marathon Runners

Long-tern cost efficiency

THAILAND

The Creative Souls

High craftsmanship

0% 20% 40% 60% 80% 100%

United States

Japan

Vietnam

Thailand

Singapore

Philippines

Myanmar

Malaysia

Laos

Indonesia

Cambodia

Brunei

NO

N

ASEA

N

ASEA

N

0-14 15-64 65 & above

POPULATION DISTRIBUTION BY AGE GROUPS

CAMBODIA

The Investors’ Favorites

Low wages

CHINA

The Miracle Workers

High productivity

LAOS

The Rising Stars

Sky rocketing labor force

growth

Selecting the

Right Labor Force

ASEAN’s labor force consist of

429 million,

in which 270 million work

in the manufacturing

sector.

INDONESIA is current

ASEAN’s top provider of

working population.

INDONESIA

The Survivors

Value for money &

large labor force

ในปี 2558 กลุ่มประเทศอาเซียนจะประกอบไปด้วยประชากรกว่า 600 ล้านคน ร้อยละ 70 จะ เป็นกลุ่มคนวัยท างาน ที่มี อายุระหว่าง 15-64 ปี อย่างไรก็ตาม แต่ละประเทศมีแรงงานที่มีควานถนัดไม่เหมือนกัน ดังนั้น นักลงทุนจ าเป็นต้องเลือกประเทศ ที่สามารถตอบโจทย์วัตถุประสงค์ขององค์กรได้มากที่สุด

The Labor Force of ASEAN แรงงานของ

Reason to Invest 3:

By 2015, ASEAN will have a total

population of 600 million

individual, 70% of which will

become its working population.

Because member countries have

different areas of expertise,

investors must select a workforce

that best answer their

organizational goals.

Source: ILO 2010, The Conference Board and

Groningen Growth and Development Centre Total

Economy Database, National Wages and Productivity

Commission, IE Singapore

9

10

สิงคโปร ์ผลติภาพมากกวา่ไทย

5 เทา่ตวั

Lower wages Higher FDI inflows Higher employment

ประสิทธิภาพแรงงาน

21.27

9.67

9.42

9.05

3.75

2.67

2.23

2.03

1.11

Singapore

Thailand/Bangkok

Malaysia

Philippines/NCR

(Peso)

China/Beijing

Indonesia/Jakarta

Vietnam

Cambodia

Myanmar

DAILY WAGES IN US DOLLARS (2012)

Daily Wages in USD

Source: National Wages & Productivity

Commission, 2012

6.80

ASEAN Average

High

Low

ค่าจ้างแรงงานไทย 1 คน 300 บาท/วัน สามารถจ้างพม่าได้ 9 คน เวียดนามและกัมพูชาได้ 4 คน อินโดนีเซียได้ 3 คน และจ้างชาวจีนได้ 3 คน ในขณะที่ค่าจ้างแรงงานไทยมีความใกล้เคียงกับมาเลเซีย แต่ผลิตภาพในการท างานของแรงงานมาเลเซียมากกว่าไทยกว่า 2 เท่าตัว ค่าจ้างแรงงานสิงคโปร์แพงกว่าแรงงานไทยกว่า 2 เท่าตัวแต่ผลิตภาพมากกว่าไทยถึง 5 เท่าตัว และเมื่อเทียบกับแรงงานเวียดนาม แม้ว่าไทยจะแพงกว่าเวียดนามถึง 5 เท่า แต่ผลิตภาพของไทยนั้นดีกว่าเพียง 2 เท่าเท่านั้นเอง ถ้าพูดถึงความคุ้มค่ าทางการลงทุนธุรกิจ เราก็ แพ้เวียดนามเห็นๆ การที่จะลดค่าจ้างแรงงานให้ต่ าลงคงไม่มีทางเป็นไปได้ ไทยควรต้องสร้างความคุ้มค่า โดยการเพิ่มผลิตภาพในการท างานมากกว่า

ไทย มาเลเซีย สิงคโปร์

As a result of the increase in minimum wages to 300 baht

per day, Thailand has become the second most

expensive labor force, exceed it former predecessors

Philippines and Malaysia. Thais must now promote it core

competencies, such as their creativity and high

craftsmanship, rather than competing on wages alone to

attract investors.

11

แรงงานทักษะ ค่าจ้างสูง = กระจายตวั แรงงานไร้ทักษะ ค่าจ้างต่ า = กลบัถิ่นฐาน

การเปิดเสรีอาเซียนก่อให้เกิดการเคลื่อนย้ายฐานการผลิตและลงทุนไปสู่กลุ่มประเทศ CLMV เพิ่มมากขึ้น ส่งผลให้กลุ่มแรงงานในประเทศที่เคยออกไปค้าแรงงานในต่างประเทศ มีแนวโน้มจะ กลับถิ่นฐาน ของตนเองเพิ่มมากขึ้นตามทิศทางการลงทุนของอาเซียน

แนวโน้มแรงงาน

SINGAPORE MALAYSIA THAILAND

PHYSICIAN

NURSES

ENGINEERS

USD 3,281

USD 1,131

USD 1,466

USD 3,523

USD 1,237

USD 1,731

USD 937

USD 358

USD 756

ASEAN SKILLED LABOR AVERAGE

SALARIES COMPARISON

Source: World Salaries Org.

แนวโน้มกลุ่มแรงงานทักษะจะมีการ กระจายตัว มากขึ้น ไปยังกลุ่มประเทศที่มีค่าจ้างแรงงานที่สูงกว่าประเทศของตนเอง แรงงานทักษะไทยมีแนวโน้มจะเคลื่อนย้ายไปประเทศสิงคโปร์ มาเลเซียและฟิลิปปินส์ ในขณะที่แรงงานทักษะในประเทศที่มีค่าจ้างต่ ากว่าไทยก็มีแนวโน้มที่จะเคลื่อนย้ายมาท างานในประเทศไทยด้วยเช่นกัน

0%

20%

40%

60%

80%

100%

ASEAN GDP DISTRIBUTION BY SECTOR

Agriculture Industry Service

กัมพูชา ลาว พม่าและเวียดนาม มีแรงงานที่มีความหลากหลายและเป็ น แรงงานต้นทุนต่ า จึง เป็ นโอกาสของการลงทุนในกลุ่มธุรกิจต้นน้ าหรือกลุ่มธุรกิจต้นน้ าหรือกลุ่มธุรกิจที่ ใช้ประโยชน์โดยตรงจากทรัพยากรธรรมชาติมากขึ้น ในขณะที่มาเลเซีย อินโดนีเซียและไทย มีแรงงานทักษะมากกว่าจึงมีการลงทุนในกลุ่มธุรกิจกลางน้ าและกลุ่มอุตสาหกรรมสร้างสรรค์มากขึ้น

การเติบโตในอุตสาหกรรมภาคการเกษตรและอุตสาหกรรมการผลิตมีแนวโน้มเพิ่มสูงขึ้นอย่างต่ อ เ นื่ อ ง โ ดย เ ฉพ า ะ ป ร ะ เ ท ศ กัมพูชา ลาว พม่าและเวียดนาม ส่งผลให้แรงงานเหล่านั้นที่อยู่ ในประเทศไทย มีแนวโน้มที่จะเดินทางกลับประเทศตนเองมากขึ้น เพื่อไปประกอบอาชีพในอุตสาหกรรมต่ า งๆ ที่ ก า ลั ง เ ติ บ โ ตต ามทิ ศทางการลงทุน ในปร ะ เทศของตนเองมากขึ้น

แรงงานวิชาชีพหรือแรงงานทักษะจะกระจายตัวออกไปยังประเทศต่ างๆ ในอา เซี ยน ที่ มี ค่ า จ้ า งแรงงานที่ สู งกว่ าปร ะ เทศ ไทย สิงคโปร์เป็นประเทศที่มีแนวโน้มการกระจายตัวของแรงงานทักษะมากที่สุด เนื่องมาจากสิงคโปร์ เป็นประ เทศที่มี อัตราการเติบ โตในธุรกิจภาคบริการเพิ่มสูงขึ้นอย่างต่อเนื่อง ซึ่งสอดคล้องกับการเ ป็ น ป ร ะ เ ท ศที่ มี อั ต ร า ค่ า จ้ า งแรงงานที่สูงที่สุดในอาเซียน

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Lao

s

Mya

nm

ar

Ca

mb

od

ia

Vie

tna

m

Tha

ilan

d

Ind

on

esi

a

Ph

ilip

pin

es

Ma

laysi

a

Bru

ne

i

Sin

ga

po

re

ASEAN LABOR FORCE IN

AGRICULTURIAL SECTOR

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Bru

ne

i

Ma

laysi

a

Vie

tna

m

Sin

ga

po

re

Ca

mb

od

ia

Ph

ilip

pin

es

Tha

ilan

d

Ind

on

esi

a

Mya

nm

ar

Lao

s

ASEAN LABOR FORCE IN

INDUSTRIAL SECTOR

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Sin

ga

po

re

Ph

ilip

pin

es

Ma

laysi

a

Ind

on

esi

a

Tha

ilan

d

Bru

ne

i

Vie

tna

m

Ca

mb

od

ia

Mya

nm

ar

Lao

s

ASEAN LABOR FORCE IN

SERVICE SECTOR

What to do when Thailand

is Facing a Labor Imbalance... as it foreign lower wage labor goes back to their homeland & Thais skilled labor

are being drained to other better paid nations.

12

What Should Thailand Do

as It is in a

SANDWICH ECONOMY? How is Thailand able to compete with the rest of ASEAN and the world, when it is trapped in

its own doing that has prevented it from growing. Thailand is in a “sandwich economy”

where it is unable to move up or down. Due to its inefficient of capability Thailand is unable

to move upward to being a global citizen like Singapore. While Thailand cannot compete in

low markets, Laos, Cambodia an Myanmar have attracted investors by providing them with

low wages labor force. Indonesia, on the other hand, will soon take all as it holds abundant

and untapped natural resources, largest labor force, below ASEAN average wages cost,

more political stability and increasing domestic consumption. Thus ruling INDONESIA as the

world’s most attractive investment destination.

ประเทศไทยจะท าอย่างไร เมื่อเราต้องติดอยู่ในสภาพของการพัฒนาเศรษฐกิจท่ามกลางความพร้อมในด้านต่างๆ ของประเทศในกลุ่มอาเซียน การพิจารณาเลือกที่จะตัดสินใจจะแข่งขันในตลาดต้นทุนต่ าอาจจะไม่เหมาะสม เนื่องจากโครงสร้างของระบบการผลิตและการจ้างงานได้ถูกพัฒนาสูงขึ้นแล้ว ในขณะที่การเลือกที่จะก้าวไปสู่ตลาดของผลิตภัณฑ์ที่พึ่งพาวิทยาศาสตร์และเทคโนโลยีช้ันสูงก็คงเป็นไปได้ค่อนข้างยากในสภาวการณ์ปัจจุบัน เพราะเราเองยังมีอุปสรรคหลายประการ โดยเฉพาะในด้านโครงสร้างพื้นฐานด้านการพัฒนาและระบบกฎหมาย

ในขณะที่สิงคโปร์เป็นประเทศที่ก้าวเข้าสู่ Global Citizen ไปเรียบร้อยแล้ว ลาว กัมพูชา และพม่าก็ได้เข้าไปนั่งในใจของนักลงทุนด้วยค่าแรงที่ต่ ากว่าในขณะเดียวกันอินโดนีเซียถือได้ว่าเป็นดาวรุ่งดวงใหญ่ที่เพียบพร้อมต่อการลงทุน

ในปัจจัยส าคัญ อันเนื่องมาจากทรัพยากรธรรมชาติที่มากมาย ฐานแรงงานที่ใหญ่ที่สุด ค่าแรงที่ ต่ ากว่าอีกหลายประเทศในอาเซียน ความมั่นคงทางการเมืองที่มีมากขึ้น และมีอัตราการบริโภคภายในประเทศสูงสุดในอาเซียน ด้วยสาเหตุดังกล่าว “อินโดนีเซีย” จึงกลายเป็นประเทศที่น่าลงทุนมากที่สุดในอาเซียน

อย่างไรก็ตาม หากพิจารณาถึงความได้เปรียบของประเทศไทยจากการเป็นศูนย์กลางด้านการขนส่งสินค้าระหว่างประเทศในอาเซียนและการเป็นประตูสู่ตลาดโลก พร้อมทั้งศักยภาพทางด้านแรงงานที่มีอยู่ เป็นปัจจัยส าคัญที่น่าจะน าเข้ามาพิจารณาในการก าหนดกลยุทธ์ของประเทศไทย เพื่อสร้างศักยภาพในการตอบรับของการรวมตัวในเศรษฐกิจอาเซียน

13

Dr. Poomporn Thamsatitdej College of Innovation , Thammasat University [email protected] Dr. Karndee Leopairote Thammasat Business School [email protected] Ms. Wiyada Markthamai Research Specialist [email protected] Ms. Chanyawat Sangmuang Research Specialist [email protected] Ms. Tuangpat Visuddhidham Research Specialist [email protected] Ms. Wisuta Jaengprajak Research Specialist [email protected] Website: www.aseanintelligence.com Facebook: www.facebook.com/aseanintelligence Twitter: @ASEAN_team Copyright (c) 2012 ASEAN Business Intelligence All right reserved.

Contributors

14

![Rex mundi v1 05 [lemuria]](https://img.pdfslide.net/doc/110x75/568ca8a11a28ab186d9a1efa/rex-mundi-v1-05-lemuria.jpg)